Embed Size (px)

Citation preview

IRA Challenge

Learning Objectives

Determine whether common industry views on various IRA topics are trueDiscuss common misconceptions regarding IRA portability rules

2

To avoid the 50% excess accumulation penalty tax on a missed RMD, the RMD can be distributed

in the current year and corrected to reflect having been distributed in the prior year.

1

3

According to 2017 Publication 590-B, the deadline to receive the annual RMD is December 31. If the RMD for a given year is not received, a 50% excise tax on the amount not distributed may be due. The IRA owner may request a waiver of the 50% excise tax though Form 5329.

1To avoid the 50% excess accumulation penalty tax on a missed RMD, the RMD can be distributed in the current year and corrected to reflect having been distributed in the prior year.

Treas. Reg. 1.408-8, Q&A 1

4

After reviewing his quarterly statement, the IRA owner notifies his financial organization that he reported the

April 9 IRA contribution for the prior year. Without prior notification, the financial organization can correct Form

5498 to report the contribution for the prior year.

2

5

According to the 2017 Publication 590-A, contributions between January 1 and the tax return deadline should be allocated to either the current year or the prior year. Without direction, the financial organization can assume and report the contribution for the current year.

2After reviewing his quarterly statement, the IRA owner notifies his financial organization that he reported the April 9 IRA contribution for the prior year. Without prior notification, the financial organization can correct Form 5498 to report the contribution for the prior year.

6

SEP plan contributions made for the prior plan year are reported on the current year’s Form 5498.

3

7

According to the 2018 Instructions for Forms 1099-R and 5498, SEP plan contributions are reported for the year they are received.

3SEP plan contributions made for the prior plan year are reported on the current year’s Form 5498.

8

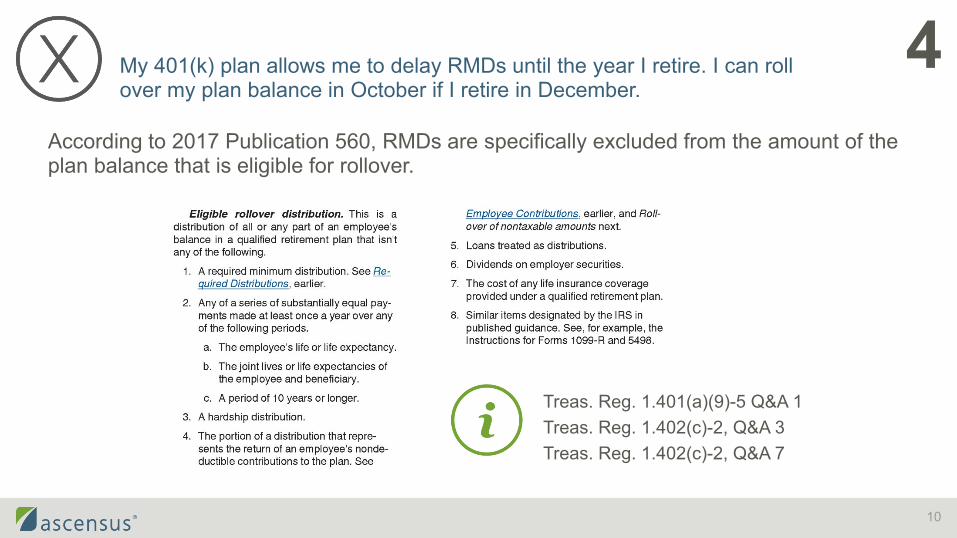

My 401(k) plan allows me to delay RMDs until the year I retire. I can roll over my planbalance in October if I retire in December.

4

9

According to 2017 Publication 560, RMDs are specifically excluded from the amount of the plan balance that is eligible for rollover.

4My 401(k) plan allows me to delay RMDs until the year I retire. I can roll over my plan balance in October if I retire in December.

Treas. Reg. 1.401(a)(9)-5 Q&A 1Treas. Reg. 1.402(c)-2, Q&A 3Treas. Reg. 1.402(c)-2, Q&A 7

10

IRA owners and beneficiaries of any age areeligible to make qualified charitable distributions.

5

11

According to 2017 Publication 590-B, IRA owners and beneficiaries who are age 70½ or older are eligible to make qualified charitable distributions.

5IRA owners and beneficiaries of any age are eligible to make qualified charitable distributions.

Notice 2007-7, Q&A 37

12

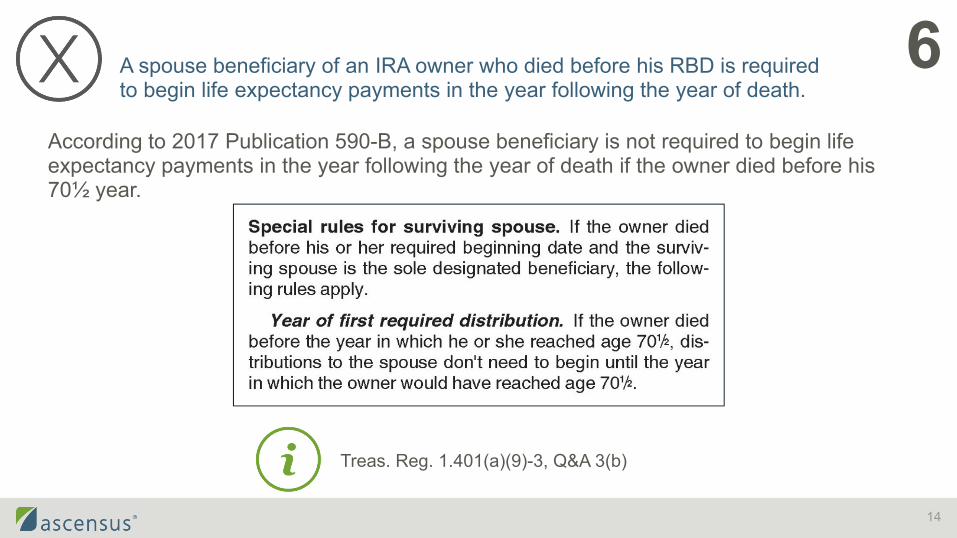

A spouse beneficiary of an IRA owner who died before his RBD is required to begin life expectancy payments in the year following the year of death.

6

13

According to 2017 Publication 590-B, a spouse beneficiary is not required to begin life expectancy payments in the year following the year of death if the owner died before his 70½ year.

6A spouse beneficiary of an IRA owner who died before his RBD is required to begin life expectancy payments in the year following the year of death.

Treas. Reg. 1.401(a)(9)-3, Q&A 3(b)

14

The one-per-12-month rule does not apply to rollovers from an

employer-sponsored retirement plan.

7

15

According to 2017 Publication 590-A, there is not a one-per-12-month rule on rollovers from an employer-sponsored retirement plan.

7The one-per-12-month rule does not apply to rollovers from an employer-sponsored retirement plan.

IRC Sec. 408(d)(3)(B) Announcement 2014-32

16

A Traditional IRA may be rolled over or transferred to a SIMPLE IRA, provided the SIMPLE IRA

has met the 2-year requirement.

8

17

Consolidated Appropriations Act of 2016

According to 2017 Publication 590-A and the SIMPLE IRA Withdrawal and Transfer Rules on irs.gov, a Traditional IRA may be rolled over or transferred to a SIMPLE IRA after satisfying the SIMPLE IRA 2-year waiting period (2 years from the date that the first contribution under the employer’s SIMPLE IRA plan was made to the SIMPLE IRA).

8A Traditional IRA may be rolled over or transferred to a SIMPLE IRA, provided the SIMPLE IRA has met the 2-year requirement.

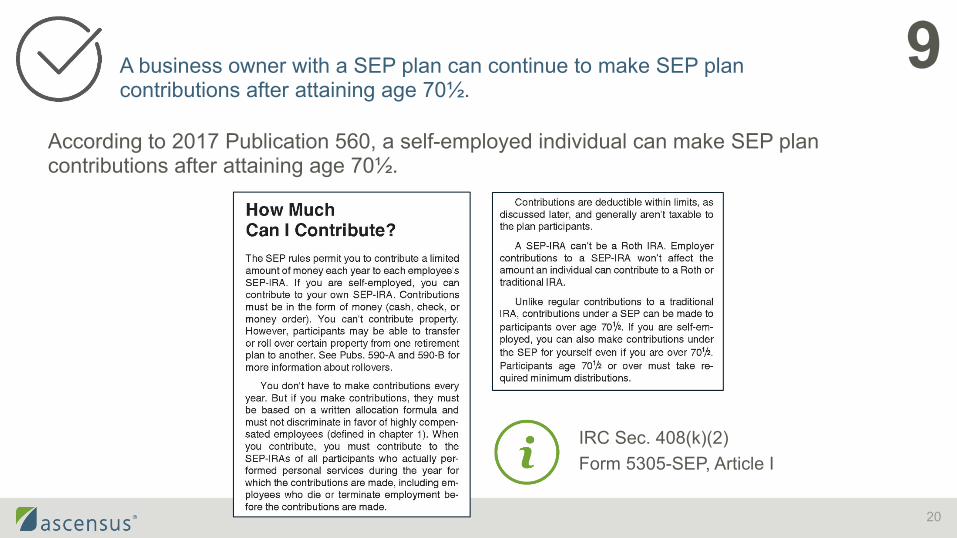

18

A business owner with a SEP plan can continue to make SEP plan contributions after attaining age 70½.

9

19

According to 2017 Publication 560, a self-employed individual can make SEP plan contributions after attaining age 70½.

9A business owner with a SEP plan can continue to make SEP plan contributions after attaining age 70½.

IRC Sec. 408(k)(2)Form 5305-SEP, Article I

20

Plan participants may directly roll over pretax assets to a Traditional IRA and

after-tax assets to a Roth IRA.

10

21

According to Notice 2014-54, plan participants may directly roll over pretax assets to a Traditional IRA and after-tax assets to a Roth IRA.

10Plan participants may directly roll over pretax assets to a Traditional IRA and after-tax assets to a Roth IRA.

Notice 2014-54 Disbursements of benefits from the plan to the recipient that are scheduled to be made at the same time (disregarding differences due to reasonable delays to facilitate plan administration) are treated as a single distribution without regard to whether the recipient has directed that the disbursements be made to a single destination or multiple destinations.

22

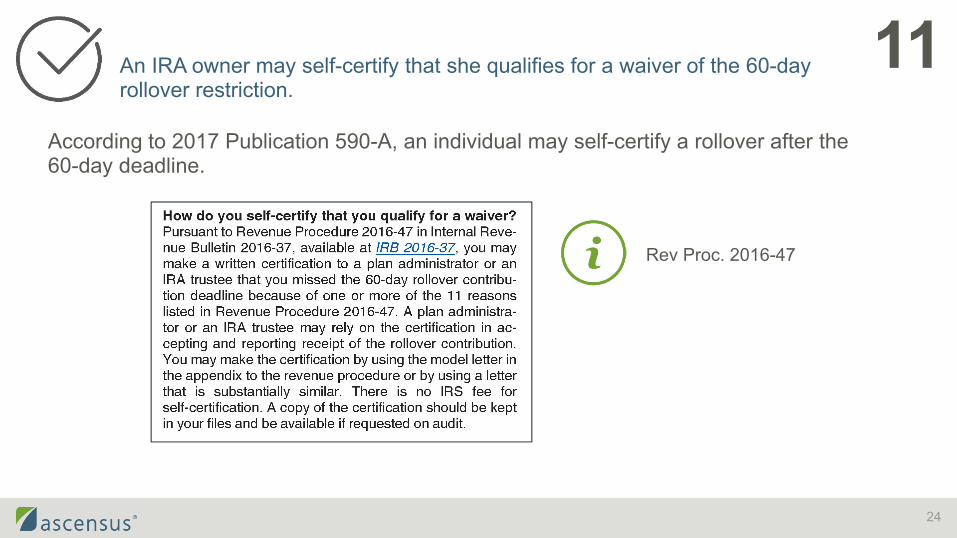

An IRA owner may self-certify that she qualifies for a waiver of the

60-day rollover restriction.

11

23

According to 2017 Publication 590-A, an individual may self-certify a rollover after the 60-day deadline.

11An IRA owner may self-certify that she qualifies for a waiver of the 60-day rollover restriction.

Rev Proc. 2016-47

24

A sole spouse beneficiary delayed distributions until her deceased spouse (the original IRA owner) would have

reached age 70½ and failed to satisfy her first life expectancy payment. The spouse beneficiary is subject

to a 50% penalty tax on the amount she should have taken as the beneficiary.

12

25

According to 2017 Publication 590-B, a spouse beneficiary is not subject to a 50% penalty tax because, by failing to take the payment, the IRA is deemed to be treated as her own.

12A sole spouse beneficiary delayed distributions until her deceased spouse (the original IRA owner) would have reached age 70½ and failed to satisfy her first life expectancy payment. The spouse beneficiary is subject to a 50% penalty tax on the amount she should have taken as the beneficiary.

Treas. Reg. 1.408-8, Q&A 5(b)(1)

26

Following a 2018 or later conversion froma SEP or SIMPLE IRA to a Roth IRA,

the IRA owner may choose to recharacterize the conversion amount

back to a SEP or SIMPLE IRA.

13

27

According to the IRA FAQS – Recharacterization of IRA Contributions on irs.gov, an individual may not recharacterize a 2018 or later SEP or SIMPLE IRA contribution that has been converted.

13Following a 2018 or later conversion from a SEP or SIMPLE IRA to a Roth IRA, the IRA owner may choose to recharacterize the conversion amount back to a SEP or SIMPLE IRA.

The Tax Cuts and Jobs Act of 2017 (Public Law 115-97)

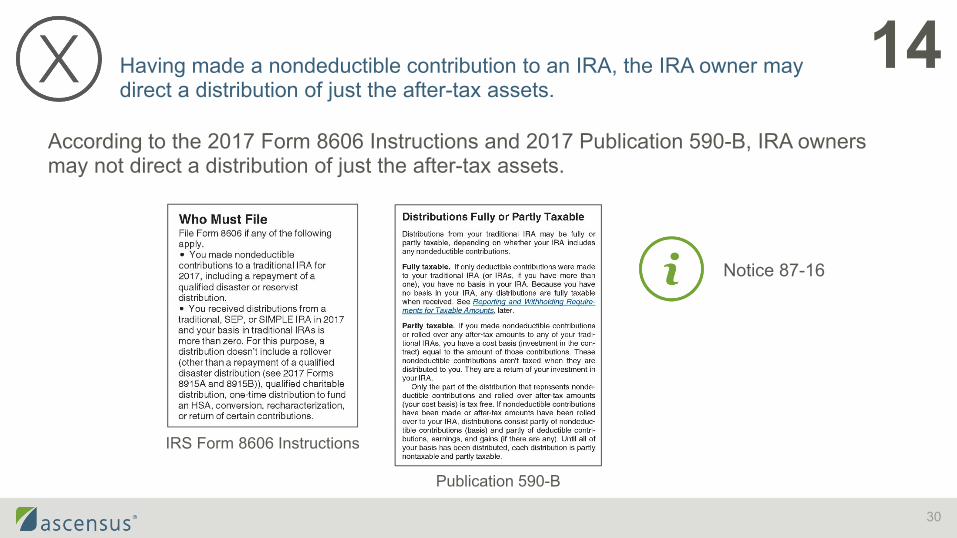

28

Having made a nondeductible contributionto an IRA, the IRA owner may direct

a distribution of just the after-tax assets.

14

29

According to the 2017 Form 8606 Instructions and 2017 Publication 590-B, IRA owners may not direct a distribution of just the after-tax assets.

14Having made a nondeductible contribution to an IRA, the IRA owner may direct a distribution of just the after-tax assets.

Publication 590-B

IRS Form 8606 Instructions

Notice 87-16

30

A 45-year-old taxpayer has MAGI in excess of the allowable limit for 2018. She can still put $5,500 into her

Roth IRA this year by making a 2018 Traditional IRA contribution and then converting that amount.

15

31

According to 2017 Publication 590-A, MAGI restrictions apply to Roth IRA contributions but not Roth IRA conversions. Taxpayers who make contributions to Traditional IRAs in order to do a subsequent conversion of that contribution commonly refer to this loophole in the tax code as the “backdoor Roth IRA”.

15A 45-year-old taxpayer has MAGI in excess of the allowable limit for 2018. She can still put $5,500 into her Roth IRA this year by making a 2018 Traditional IRA contribution and then converting that amount.

32

If a 2017 contribution is recharacterized or removed as an excess in 2018, the reporting

is done on a 2017 Form 1099-R.

16

33

According to 2018 Form 1099-R, recharacterizations are reported in the year of the distribution. 2018 Instructions for Forms 1099-R and 5498 includes the reporting code used to report a prior-year recharacterization.

16If a 2017 contribution is recharacterized or removed as an excess in 2018, the reporting is done on a 2017 Form 1099-R.

34

IRS Form 1099-R

Instructions for Forms 1099-R and 5498

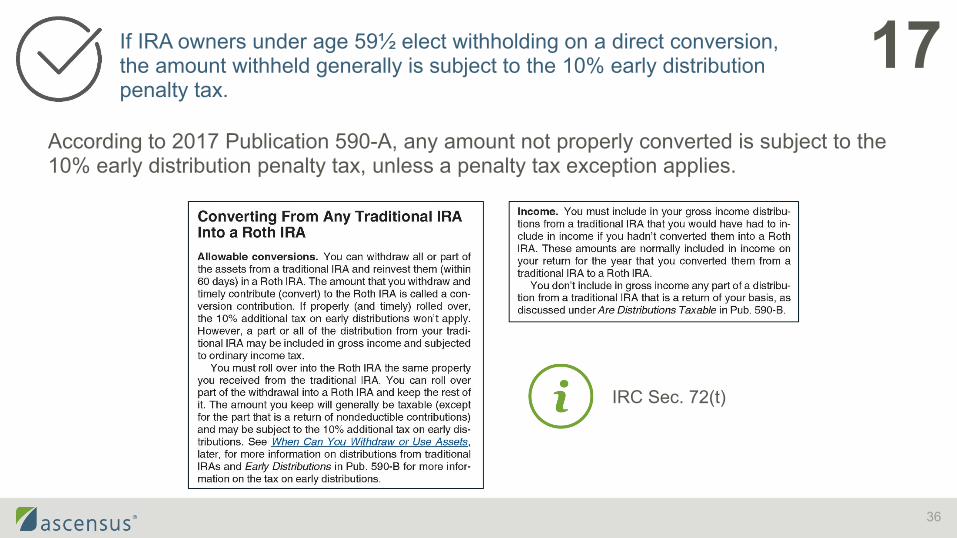

If IRA owners under age 59½ elect withholding on a direct conversion, the

amount withheld generally is subject to the 10% early distribution penalty tax.

17

35

According to 2017 Publication 590-A, any amount not properly converted is subject to the 10% early distribution penalty tax, unless a penalty tax exception applies.

17If IRA owners under age 59½ elect withholding on a direct conversion, the amount withheld generally is subject to the 10% early distribution penalty tax.

IRC Sec. 72(t)

36

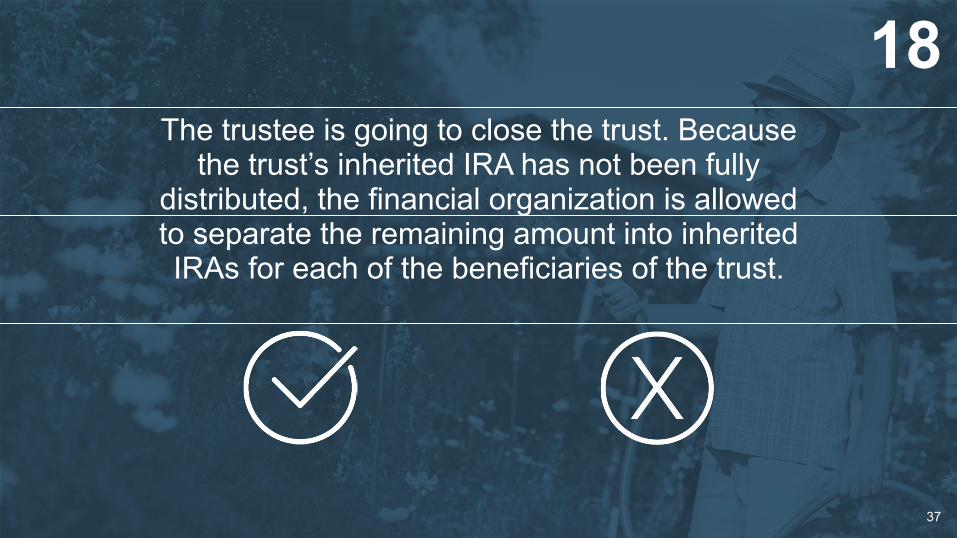

The trustee is going to close the trust. Because the trust’s inherited IRA has not been fully

distributed, the financial organization is allowed to separate the remaining amount into inherited IRAs for each of the beneficiaries of the trust.

18

37

According to 2017 Publication 590-B, separate accounting rules cannot be used by beneficiaries of a trust.

18The trustee is going to close the trust. Because the trust’s inherited IRA has not been fully distributed, the financial organization is allowed to separate the remaining amount into inherited IRAs for each of the beneficiaries of the trust.

Treas. Reg. 1.401(a)(9)-4, Q&A 5(c)

38

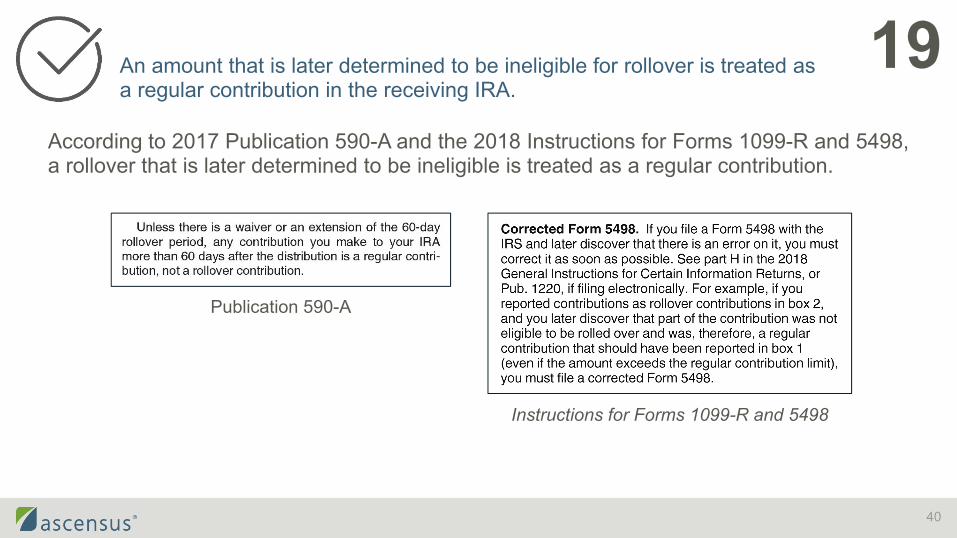

An amount that is later determined to be ineligible for rollover is treated as a regular

contribution in the receiving IRA.

19

39

According to 2017 Publication 590-A and the 2018 Instructions for Forms 1099-R and 5498, a rollover that is later determined to be ineligible is treated as a regular contribution.

19An amount that is later determined to be ineligible for rollover is treated as a regular contribution in the receiving IRA.

Publication 590-A

Instructions for Forms 1099-R and 5498

40

Any year of death RMD that the IRA owner did not satisfy before her death must be

removed by the IRA owner’s estate.

20

41

According to 2017 Publication 590-B, any year of death RMD is the responsibility of the beneficiaries.

20Any year of death RMD that the IRA owner did not satisfy before her death must be removed by the IRA owner’s estate.

Treas. Reg. 1.401(a)(9)-5, Q&A 4(a)

42

Questions?

Thank you for attending

We Appreciate Your OpinionPlease complete the electronic course survey for this course located on the Ascend 2018 mobile app. Still need to download the app? Paper versions of the survey are located at the Business Center.

IRA Challenge

We help over 8 million Americanssave for life’s biggest moments. Education. Healthcare. Retirement.

Ascensus® and the Ascensus logo are registered trademarks of Ascensus, LLC.Copyright ©2018 Ascensus, LLC. All Rights Reserved.

Ascensus provides administrative and recordkeeping servicesand is not a broker-dealer or an investment advisor.