Embed Size (px)

Citation preview

SolvedScanner Appendix

IPCC Gr. I(Solution of May - 2015 )

Paper - 3A : Cost Accounting

Chapter - 1: Basic Concepts

2015 - May [5] (a)

Sunk Cost: Sunk costs are historical costs incurred in the past are knownas Sunk Costs. They play no role in decision making during the currentperiod. Sunk Costs are independent of any event that may occur in thefuture. e.g. in case of a decision related to the replacement of a machine, thewritten down value of the existing machine is a sunk cost and therefore, notconsidered.

Opportunity Cost: This cost refers to the value of sacrifice made or benefitof opportunity foregone in accepting an alternative course of action. Eg. the opportunity cost of going to college is the money you would haveearned if you worked instead, on the one hand, you lose four years of salarywhile getting your degree, on other hand, you hope to earn more during yourcareer, thanks to your education to offset the lost wages.

2015 - May [7] (a)

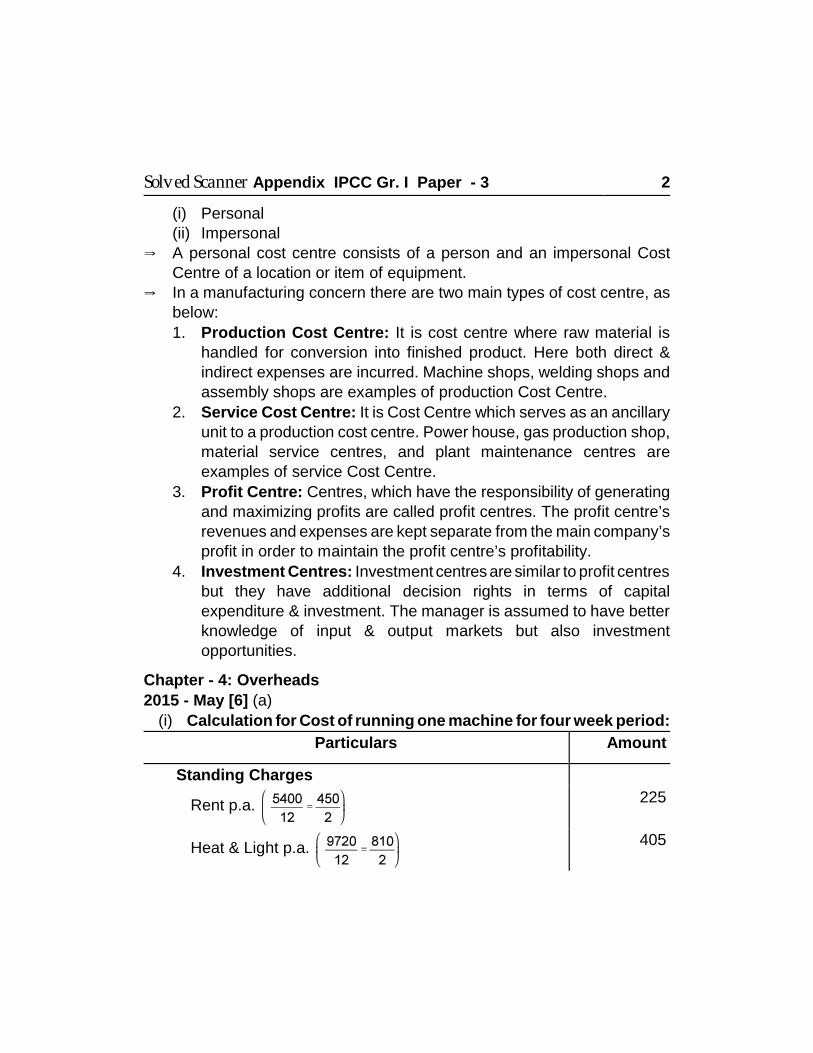

Cost Centre: Y It is defined as a location, person, or an item of equipment (or group of

these) for which cost may be ascertained and used for the purpose ofcost control. It is a part of an organization that does not produce directprofits and adds to the cost of running a company. Eg. R&D, marketing departments, help desk and customer services.

Cost Centre are of two types:

1

Solved Scanner Appendix IPCC Gr. I Paper - 3 2

(i) Personal(ii) Impersonal

Y A personal cost centre consists of a person and an impersonal CostCentre of a location or item of equipment.

Y In a manufacturing concern there are two main types of cost centre, asbelow:

1. Production Cost Centre: It is cost centre where raw material ishandled for conversion into finished product. Here both direct &indirect expenses are incurred. Machine shops, welding shops andassembly shops are examples of production Cost Centre.

2. Service Cost Centre: It is Cost Centre which serves as an ancillaryunit to a production cost centre. Power house, gas production shop,material service centres, and plant maintenance centres areexamples of service Cost Centre.

3. Profit Centre: Centres, which have the responsibility of generatingand maximizing profits are called profit centres. The profit centre’srevenues and expenses are kept separate from the main company’sprofit in order to maintain the profit centre’s profitability.

4. Investment Centres: Investment centres are similar to profit centresbut they have additional decision rights in terms of capitalexpenditure & investment. The manager is assumed to have betterknowledge of input & output markets but also investmentopportunities.

Chapter - 4: Overheads

2015 - May [6] (a)

(i) Calculation for Cost of running one machine for four week period:

Particulars Amount

Standing Charges

Rent p.a. 225

Heat & Light p.a. 405

Solved Scanner Appendix IPCC Gr. I Paper - 3 3

Foreman’s Salary 540

Depreciation 217

Running Charges

Maintenances & Repair (60 × 4) 240

Consumable Stores (75 × 4) 300

Power = (20 × 48 × 0.8) 768

Total cost for running one machine for four week 2695

(ii) Calculation for Machine Hour Rate: 20 units per hour so in 48 hoursthere is 960 units & 80 paise per units is paid .So = 20 × 0.8 = 16

Machine hour rate = ` 16

Chapter - 5: Integrated & Non-Integrated Accounts2015 - May [7] (b) Benefits of Integrated Accounting: Y Since there is one set of accounts, thus there is one figure of profit.

Hence, the question of reconciliation of cost profit and financial profitdoes not arise.

Y Efforts in duplicate recording of entries and to maintain separate set ofbooks are saved. Thus, there is saving of time & labour.

Y The operation of the system is facilitated with the use of mechanizedaccounting.

Y Costing data are available from books of original entry and hence, noday is caused in obtaining information.

Y Combination of two sets of books and centralization of accountingfunction results in economy.

Y Complete analysis of cost and sales is kept. Y Complete details of all receipts and payments in cash are kept.

Y Complete details of all assets and liabilities are kept and this systemdoes not use notional account to represent impersonal accounts.

Solved Scanner Appendix IPCC Gr. I Paper - 3 4

Y Since financial books are subject to a rigorous accuracy, checkingintegrated accounts ensures similar checks for cost account.

Chapter - 8: Contract Costing

2015 - May [5] (b) Escalation Clause: This clause is often provided incontracts to cover any likely changes in the prize or utilization of materialsand labour. Thus, a contractor is entitled to suitably enhance the contractprice the cost raises beyond a given percentage. The object of this clause isto safeguard the interest of the contractor against unfavorable changes incost. The escalation clause is of particular importance where prices ofmaterial and labour are anticipated to increase or where quantity of materialand labour time cannot be accurately estimated.

Chapter - 9: Operating Costing

2015 - May [3] (a)

(i) Calculation for Operating Cost Per Annum:

Particulars Amount `

Standing ChargesInsuranceGarage Rent (2,400 × 4)Road TaxSalary of staff (7,200 × 12)Tyres & Tubes (3,600 × 4)Depreciation

Maintenance ChargesRepairs (4,800 × 4)

Running Charges

Diesel

Oil Sundries

15,6009,6005,000

86,40014,40068,000

19,200

4,68,000

39,600

Total (+) Passenger Tax @ 22%

7,25,8001,59,676

Solved Scanner Appendix IPCC Gr. I Paper - 3 5

Total Operating Cost ` 8,85,476

(ii) Calculation for Cost Per Passenger Kilometer:

Particulars Amount (`)

Total Operating Cost ÷ Total Passenger Km.

8,85,47639,60,000

Cost Per Passenger Km. ` 0.2236

(iii) Calculation for One Way Fare per Passenger:

Particulars Amount (`)

Total Cost P.a.% Profit (25% of total takings) (7,25,800 × 25%)

8,85,4761,81,450

Total 10,66,926

÷ One way (2)One way total

÷ Passenger Km. =

25,33,463

19,80,000

Per Passenger fare for one way ` 0.2694

*Working Note:1. Calculation for passenger kilometer and total km.-

= [30 km × 10 round trip × 2 × 25 working days]Total = 15,000 km. × 12 months Km. = 1,80,000 km. Per annum

Total Passenger km. = 15,000 × 12 × 22 = 39,60,000 Passenger km.

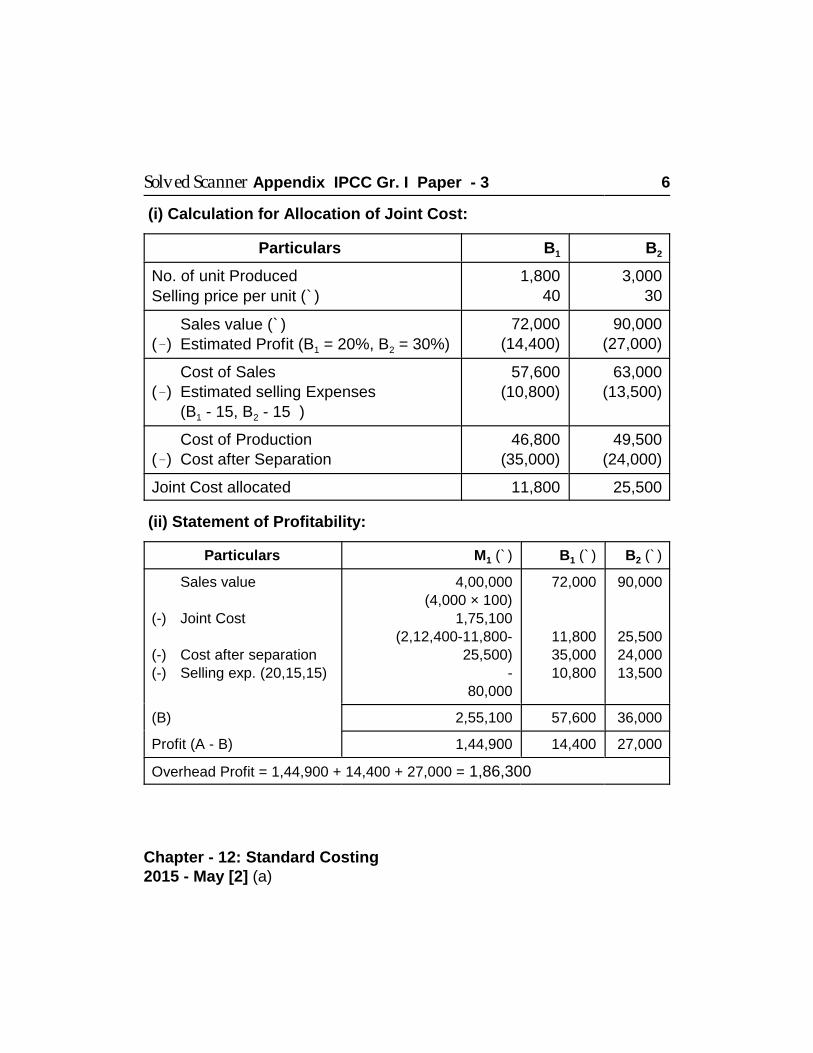

Chapter - 11: Joint Products & By Products

2015 - May [4] (a)

Solved Scanner Appendix IPCC Gr. I Paper - 3 6

(i) Calculation for Allocation of Joint Cost:

Particulars B1 B2

No. of unit Produced

Selling price per unit (`)

1,80040

3,00030

Sales value (`)(&) Estimated Profit (B1 = 20%, B2 = 30%)

72,000(14,400)

90,000(27,000)

Cost of Sales (&) Estimated selling Expenses

(B1 - 15, B2 - 15 )

57,600(10,800)

63,000(13,500)

Cost of Production(&) Cost after Separation

46,800(35,000)

49,500(24,000)

Joint Cost allocated 11,800 25,500

(ii) Statement of Profitability:

Particulars M1 (`) B1 (`) B2 (`)

Sales value

(-) Joint Cost

(-) Cost after separation(-) Selling exp. (20,15,15)

4,00,000(4,000 × 100)

1,75,100(2,12,400-11,800-

25,500)-

80,000

72,000

11,80035,00010,800

90,000

25,50024,00013,500

(B) 2,55,100 57,600 36,000

Profit (A - B) 1,44,900 14,400 27,000

Overhead Profit = 1,44,900 + 14,400 + 27,000 = 1,86,300

Chapter - 12: Standard Costing2015 - May [2] (a)

Solved Scanner Appendix IPCC Gr. I Paper - 3 7

(i) Variable overhead efficiency variance:Variable overhead

efficiency variance = × Standard rate

Standard rate per hour =

4 =

Budgeted hours = 60,000 hoursVariable overhead

efficiency variance = (60,000 - 74,000) × 4= (-14,000) × 4= 56,000 Adverse

(ii) Variable overhead expenditure variance:Variable overheadexpenditure variance = (Standard rate - Actual rate) × Actual hours

= × 74,000

= (4 - 3.14) × 74,000= 63,500 Favourable

(iii) Fixed overhead efficiency variance:Fixed overhead

efficiency variance = × Recovery rate

= (60,000 - 74,000) × 20= 2,80,000 Adverse

(iv) Fixed overhead capacity variance:Fixed overhead

capacity variance = × Recovery rate

= (74,000 - 60,000) × 20= 14,000 × 20= 2,80,000 Favourable

Chapter - 13: Marginal Costing

2015 - May [1] {C} (a)

Solved Scanner Appendix IPCC Gr. I Paper - 3 8

(i) Calculation for variable cost per unit:

Particulars 2013 2014 Difference

Sale units 80,000 1,20,000 40,000

Sale value @ ` 40 32,00,000 48,00,000 16,00,000

total cost ` 34,40,000 45,60,000 11,20,000

Variable cost per unit ` = ` 28

Fixed cost = 45,60,000 - 1,20,000 × 28

= ` 12,00,000

or

= 34,40,000 - 80,000 × 28

= ` 12,00,000

Variable cost per unit = ` 28

(ii) Calculation of PV Ratio:

PV Ratio = × 100

Sales = 32,00,000

V.C. =

(28 × 80,000) = (22,40,000)

Contribution = 9,60,000

PV Ratio = × 100

PV Ratio = 30%

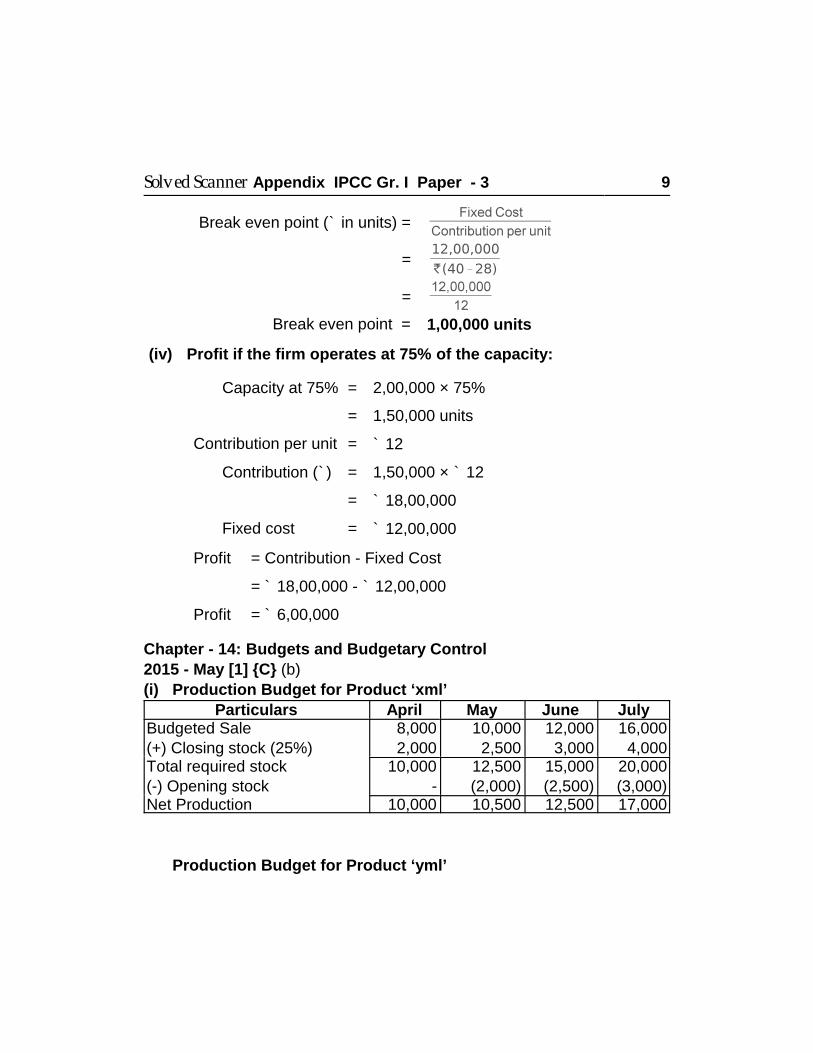

(iii) Calculation for Break even points (in units):

Solved Scanner Appendix IPCC Gr. I Paper - 3 9

Break even point (` in units) =

=

=

Break even point = 1,00,000 units

(iv) Profit if the firm operates at 75% of the capacity:

Capacity at 75% = 2,00,000 × 75%

= 1,50,000 units

Contribution per unit = ` 12

Contribution (`) = 1,50,000 × ` 12

= ` 18,00,000

Fixed cost = ` 12,00,000

Profit = Contribution - Fixed Cost

= ` 18,00,000 - ` 12,00,000

Profit = ` 6,00,000

Chapter - 14: Budgets and Budgetary Control

2015 - May [1] {C} (b)

(i) Production Budget for Product ‘xml’

Particulars April May June JulyBudgeted Sale(+) Closing stock (25%)

8,0002,000

10,0002,500

12,0003,000

16,0004,000

Total required stock(-) Opening stock

10,000-

12,500(2,000)

15,000(2,500)

20,000(3,000)

Net Production 10,000 10,500 12,500 17,000

Production Budget for Product ‘yml’

Solved Scanner Appendix IPCC Gr. I Paper - 3 10

Particulars April May June July

Budgeted Sale(+) Closing stock (25%)

6,0001,500

8,0002,000

9,0002,250

14,0003,500

Total required stock(-) Opening stock

7,500-

10,000(1,500)

11,250(2,000)

17,500(2,250)

Net Production 7,500 8,500 9,250 15,250

(ii) Production Cost Budget (for first quarter)(a) For Product ‘xml’

Particulars April May June July

Direct Material 22,00,000(220×10,000)

23,10,000(220×10,500)

27,50,000(220×12,500)

37,40,000(220×17,000)

Direct Labour 13,00,000(130×10,000)

13,65,000(130×10,500)

16,25,000(130×12,500)

22,10,000(130×17,000)

Manufacturing Exp. 20,000 21,000 25,000 34,000

Total Production Cost 35,20,000 23,31,000 27,75,000 37,74,000

(b) For product ‘yml’

Particulars April May June July

Direct Material 21,00,000(280×7,500)

23,80,000(280×8,500)

25,90,000(280×9,250)

42,70,000(280×15,250)

Direct Labour 9,00,000(120×7,500)

10,20,000(120×8,500)

11,10,000(120×9,250)

18,30,000(120×15,250)

Manufacturing Exp. 25,000 28,333 30,833 50,833

Total Production Cost 30,25,000 34,28,333 37,30,833 61,50,833

Solved Scanner Appendix IPCC Gr. I Paper - 3 11

Paper - 3B : Financial Management

Chapter - 1: Scope and Objectives of Financial Management

2015 - May [7] (d)

Conflicts in Profit Versus Wealth Maximization:

C In favour of Wealth Maximization Y Wealth Maximization helps to achieve a higher growth rate. Y It helps to attain a large market share. Y It gains leadership in the market in terms of products & technology. Y It promotes employee welfare. Y It helps to increase customer satisfaction.

C In against of Wealth Maximization Y It is prescriptive idea. Y it is not necessarily socially desirable. Y There is some controversy as to whether the objective is to

maximize stakeholders wealth or the wealth of the firm whichincludes other financial claims holders such as debenture holders,preference shareholders etc.

Y The objective of wealth maximization may also difficulties whenownership and management are separated as is the case in most ofthe large corporate form of organizations.

Chapter - 2: Time Value of Money

2015 - May [7] (e)

Present Value:Y The present value of a sum of money to be received at a future date is

determined by discounting the future value at the interest rate that themoney could earn over the period. This process is known as discounting.

PO = or PO = Fun (1 + i)-n

Where, Fun = Future value n years hence i = Rate of interest per annum n = Number of years for which discounting is done.

Perpetuity:

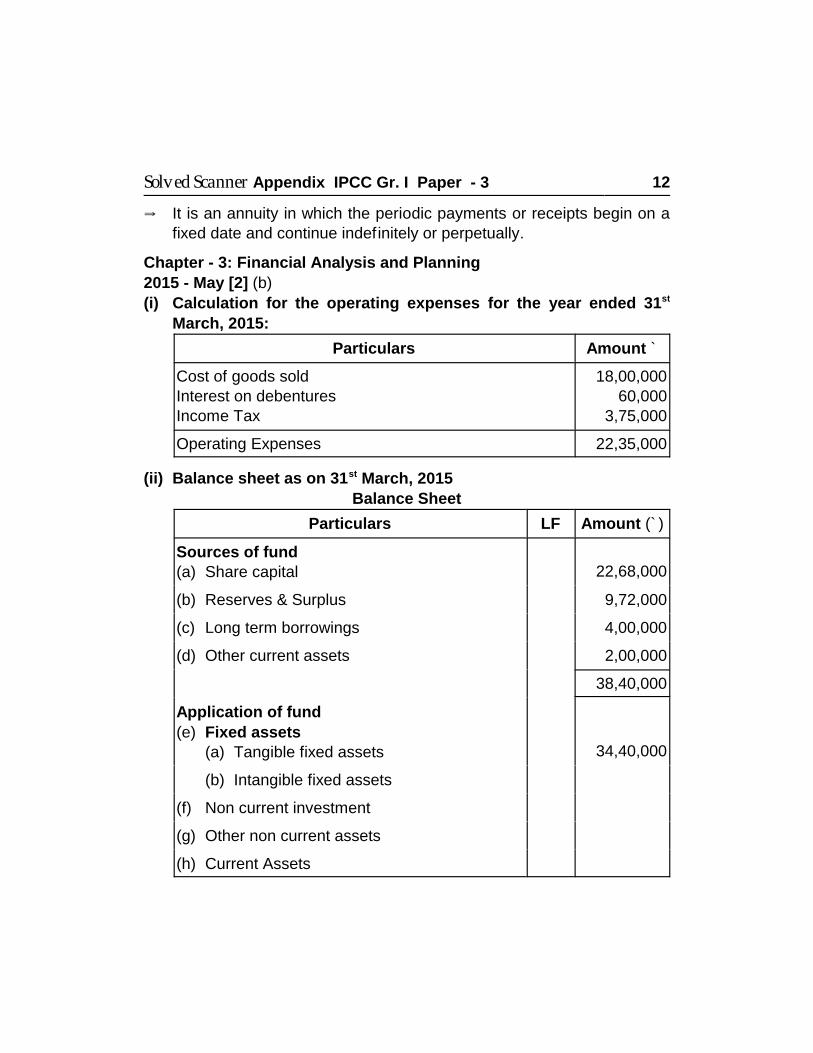

Solved Scanner Appendix IPCC Gr. I Paper - 3 12

Y It is an annuity in which the periodic payments or receipts begin on afixed date and continue indefinitely or perpetually.

Chapter - 3: Financial Analysis and Planning

2015 - May [2] (b)

(i) Calculation for the operating expenses for the year ended 31st

March, 2015:

Particulars Amount `

Cost of goods soldInterest on debenturesIncome Tax

18,00,00060,000

3,75,000

Operating Expenses 22,35,000

(ii) Balance sheet as on 31st March, 2015

Balance Sheet

Particulars LF Amount (`)

Sources of fund(a) Share capital 22,68,000

(b) Reserves & Surplus 9,72,000

(c) Long term borrowings 4,00,000

(d) Other current assets 2,00,000

38,40,000

Application of fund

(e) Fixed assets(a) Tangible fixed assets 34,40,000

(b) Intangible fixed assets

(f) Non current investment

(g) Other non current assets

(h) Current Assets

Solved Scanner Appendix IPCC Gr. I Paper - 3 13

(a) Trade receivables(b) Inventories(c) Cash & Cash Equivalents

2,00,0001,50,000

50,000

38,40,000

Working Notes:1. Calculation of NP:

NP = × 100

6.25 = × 100

NP = 60 lakhs × 6.25%

NP = ` 3,75,0002. Calculation for Profit Before Tax:

Profit After Tax = 3,75,000(+) Income Tax (50%) = 3,75,000

Profit Before Tax = 7,50,0003. Calculation for Profit Before Interest & Tax:

Profit Before Tax = 7,50,000(+) Interest = 60,000

Profit Before Interest & Tax = 8,10,0004. Calculation for Average Inventory:

Inventory Turnover Ratio =

12 =

Closing stock =

Closing stock = 1,50,000

5. Calculation for Cash & Bank Balance:

Solved Scanner Appendix IPCC Gr. I Paper - 3 14

Current Ratio =

2 =

4,00,000 = 3,50,000 + Cash & Bank

Cash & Bank = ` 50,0006. Calculation for debentures:

Debentures × 15% = Interest on debentures

Debentures =

15% debentures = ` 4,00,0007. Calculation of Net worth:

Profit Before Interest & Tax = Net worth × Return on net worth8,10,000 = Net worth × 25%

Net worth =

Net worth = ` 32,40,0008. Calculation for Share Capital & Reserve:

Net worth = Share Capital + Reserve

Share Capital = 32,40,000 ×

= 22,68,000Reserves = 32,40,000 - 22,68,000

Reserves = ` 9,72,000

Chapter - 4: Financing Decisions-Cost of Capital & Capital Structure

2015 - May [4] (b)

(i) Calculation for Post Tax Average Cost of Addition Debt:Total additional finance = 30 lakhs

(-) Retained earnings = (6 lakhs)Outsiders = 24 lakhsDebt @ 30% = 7.2 lakhs

(-) before (30,000) = (3.0 lakhs)

Solved Scanner Appendix IPCC Gr. I Paper - 3 15

Post debt = 4.2 lakhsCost @ 14% = 0.588 lakhs

(ii) Calculation for Cost of Retained Earnings & Cost of Equity:Cost of retained earnings (kr) = K (I - Tp)

= 0.10 (1 - 0.2)= 0.10 (0.8)= 8%

Cost of Equity (Ke) =

=

=

= 10.11%

* Calculation for dividend:70% of earning = 6,00,000 × 70%

= 4,20,000

(iii) Calculation for WACC:

Particulars Amount Cost Proportion WACC

Equity 16,80,000 10.11% 0.7 7.077

Debt 7,20,000 14% 0.3 4.2

Retained

earnings 6,00,000 8% - 8%

Solved Scanner Appendix IPCC Gr. I Paper - 3 16

Chapter - 5: Business Risk, Financial Risk & Leverage

2015 - May [1] {C} (d)

(i) Degree of operating leverage:

Degree of operating leverage =

P = = 0.926 times

Q = = 1.28 times

R = = 1.57 times

S = = 1.90 times

(ii) Degree of combined leverage:

Degree of combined leverage =

P = = 1.11 times

Q = = 0.96 times

R = = 0.91 times

S = = 1.096 times

Chapter - 6: Types of Financing

2015 - May [5] (c) Sale and Lease Back: Under this type of lease, theowner of an asset sells the asset to a party (the buyer), who in turn leasesback the same asset to the owner in consideration of a lease rentals. Underthis agreement, the asset is not physically exchanged but it all happen inrecords only. The main advantage of this method is that the lessee cansatisfy himself completely regarding the quality of an asset and afterpossession of the asset convert the sale into a lease agreement.

Solved Scanner Appendix IPCC Gr. I Paper - 3 17

Chapter - 8: Capital Budgeting and Investment Decisions

2015 - May [3] (b)

(i) Calculation for Cost of Project:Cost of project at 15% Internal rate of return, the sum of total cash inflows= Cost of the Project i.e. initial cash outlay.

Annual cash inflow = ` 60,000Useful life = 4 yearsConsiderating discounting factor @ 15%, cummulative cash inflow for4 years is 2.855

Hence, total cash flow for 5 years for the project = ` 60,000 × 2.855

Cost of Project = ` 1,71,300

(ii) Calculation for Payback Period:

Pay-back Period =

=

Pay-back Period = 2.855 years.

(iii) Calculation for Cost of Capital:

Profitability Index =

1.064 =

Sum of discounted cash inflows = ` 1,82,263.2

Hence, Cumulative discount factor for four years = = 3.038

From the discount factor table, at discount rate of 12% the cumulativediscount factor for 5 years is 3.038

Y Hence, Cost of Capital is 12%.

(iv) Calculation for Net Present value (NPV):NPV = Sum of Present values of cash inflows - Cost of Project = 182263.2 - 171300

NPV = ` 10963.2

Solved Scanner Appendix IPCC Gr. I Paper - 3 18

Chapter - 9: Meaning, Concept & Policies of Working Capital

2015 - May [6] (b)

(i) Calculation for Operating Cycle Period:Operating Cycle = RM Period + WIP Period + FG Period + DebtorCollection Period - Creditor Collection period= 50 days + 18 days + 22 days + 45 days - 55 daysOperating Cycle = 80 days.

(ii) No. of Operating Cycle in a year:One operating cycle is for 80 days. So

No. of Operating Cycle in a year = 4.5 times.

(iii) Calculation for Amount of working capital required for company

on cash cost basis:Annual operating cost = 21 lakhs

depreciation = ` 2,10,000Cash operating cost = Annual Cost - Depreciation

= ` 21 Lakhs - 2,10,000Cash operating cost = 18,90,000

=

= 4,20,000

Working Capital Required = ` 4,20,000

(iv) Reduction in working capital:

=

=

Working Capital = ` 6,56,250

Solved Scanner Appendix IPCC Gr. I Paper - 3 19

Chapter - 10: Treasury & Cash Management

2015 - May [5] (d) Miller-Orr Cash Management model: According to thismodel, the net cash flow is completely stochastic. When changes in cashbalance occur randomly the application of control theory serves a usefulpurpose. The miller-orr model is one of such control limit models. This modelis designed to determine the time & size of transfers between an investmentaccount and cash account. In this model, limits are set for cash balances. These limits may consists ofh as upper limit, z as the return point and zero as lower limit. When cashbalance reaches the upper limit the transfer of cash equal to h, is investedin marketable securities account. When it touches the lower limit, a transferfrom marketable securities account to cash account is made.During the period when cash balance says between h and o i.e. high and lowlimits of cash balance are set up on the basis of fixed cost associated withthe securities transaction, the opportunity cost of holding cash and degreeof likely fluctuations in cash balance. This limits satisfy the demands for cashat the lower possible total costs.

Theory: This model operates as under:(a) Cash outflows are not uniform during the year.(b) Upper and lower limits can be fixed for cash balances, as outflows do

not exceed a certain limit on any day. These limits are determined basedon fixed transaction costs, interest foregone on marketable securitiesand degree of likely fluctuations in cash balances.

(c) When cash balance reaches the upper limit, Surplus cash is invested inmarketable securities, to bring down the cash balance to the averagelimit or return point.

(d) When cash balance touches the lower limit, investments are disposedoff so that cash balances goes upto the average limit or return point.

(e) During the period when cash balance stays between high & low limits,there are no transactions between cash & marketable securities.

Formula: R =

Solved Scanner Appendix IPCC Gr. I Paper - 3 20

Chapter - 12: Management of Receivables

2015 - May [1] {C} (c)

| Debtors = 2,40,000 ×

Debtors = ` 30,000 × 10% = 3,000| Cost of Sales = 80% i.e. 2,40,000 × 80% = 1,92,000

Sales = 2,40,000(-) Cost = (1,92,000)

Profit = 48,000(-) Tax = (14,400)

Profit after tax = 33,600| Rate of return = 33,600 × 40% = 13,440| The firm should accept the offer because the benefit for acceptance is

better than ignorance.

Chapter - 13: Financing of Working Capital

2015 - May [7] (c) Differentiate between Factoring & Bill discounting.

Factoring: Factoring refers to the giving the bill to other as a security thatmoney is payable on due date. The organization can get finance by factoringbill from the parties.

Bill discounting: Y Bill discounting refers to the bill given to the bank & bank than gives the

finance of that bill. Y This is used where there is urgent need of funds.

Shuchita Prakashan (P) Ltd.25/19, L.I.C. Colony, Tagore Town,

Allahabad - 211002Visit us : www.shuchita.com

�

Solved Scanner Appendix IPCC Gr. I Paper - 3 21

FOR NOTES

Solved Scanner Appendix IPCC Gr. I Paper - 3 22

FOR NOTES

Solved Scanner Appendix IPCC Gr. I Paper - 3 23

FOR NOTES

Solved Scanner Appendix IPCC Gr. I Paper - 3 24

FOR NOTES