Embed Size (px)

Citation preview

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 1/32

PT Perusahaan Listrik Negara (Persero)

Investor Update Electricity for a Better Life

STRICTLY CONFIDENTIAL

As of 30 June 2010

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 2/32

TABLE OF CONTENTS

COMPANY OVERVIEW2

INVESTMENT STORY3

REGULATORY UPDATE4

FINANCIAL UPDATE5

1

APPENDIX6

PLN PROGRESS UPDATE1

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 3/32

PLN PROGRESS UPDATE

2

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 4/32

PLN Progress Update

3

From FY 2009 to FY 2010, EBITDA has increased from Rp 15tn to Rp 23tn while the

EBITDA margins increased from 9% to 16%

The EBITDA interest coverage has also increased to 3,9x in FY 2009 from 2.4x in FY2008

Improvements infinancial

performance

PLN keeps on improving its operations efficiency thereby reduce subsidy requirement

Notable improvements include improvement in energy mix and reduction in system losses

New ElectricityLaw

Continuedefficiency

improvement

Law No. 30 of 2009 on Electricity (“New Electricity Law”) issued in Sept 2009

Once implemented, other players will be permitted to participate in generation,

transmission, distribution and retail segments

However, PLN will retain first priority to be the electricity supplier for the public needs

New Law will potentially support PLN to achieve a more solid financial position

There have been a number of notable improvements and updates at PLN in the last few months

Acceleretedcapacity

development

Further significant progress has been made in the 10,000 MW Fast Track Program (FTP) I

From 35 original projects, 14 projects (5,500 MW) have achieved over 70% completion

ALL funding for generation projects and IDR portion for T/L projects have been signed

Three additional FTP I generation projects, totalled 430 MW, have found lenders

As proof of its continuing support for PLN, the government had increased the 5% margin in

the 2009 to 8% in 2010 as stipulated in the 2010 State Budget Law

GoI has approved a Rp 7.5 tn soft-loan to finance projects

GoI has approved 10% tariff increase, the first increase since 2003, making the sellingprice closer to its economical level, reducing subsidy burden.

More governmentsupport

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 5/32

COMPANY OVERVIEW

4

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 6/32

5

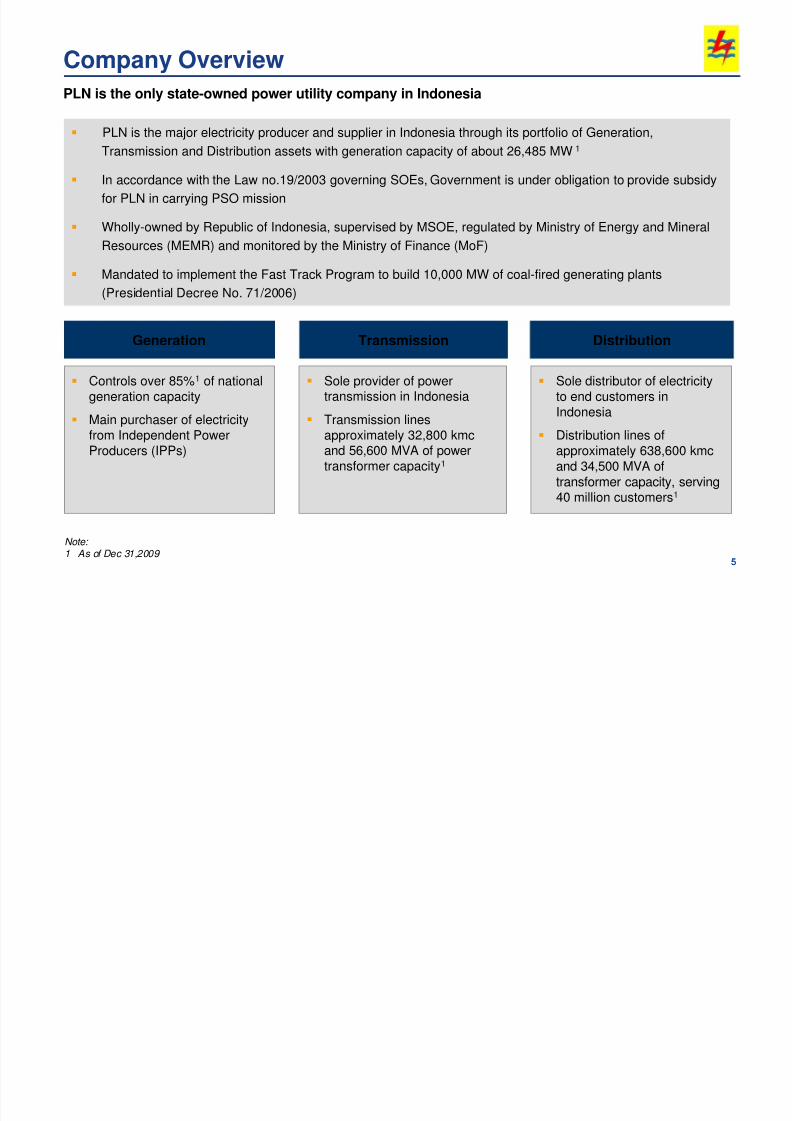

PLN is the major electricity producer and supplier in Indonesia through its portfolio of Generation,Transmission and Distribution assets with generation capacity of about 26,485 MW1

In accordance with the Law no.19/2003 governing SOEs, Government is under obligation to provide subsidy

for PLN in carrying PSO mission

Wholly-owned by Republic of Indonesia, supervised by MSOE, regulated by Ministry of Energy and Mineral

Resources (MEMR) and monitored by the Ministry of Finance (MoF)

Mandated to implement the Fast Track Program to build 10,000 MW of coal-fired generating plants(Presidential Decree No. 71/2006)

Company Overview

PLN is the only state-owned power utility company in Indonesia

5

Controls over 85%1 of nationalgeneration capacity

Main purchaser of electricityfrom Independent PowerProducers (IPPs)

Sole provider of powertransmission in Indonesia

Transmission linesapproximately 32,800 kmcand 56,600 MVA of powertransformer capacity1

Sole distributor of electricityto end customers in

Indonesia Distribution lines of

approximately 638,600 kmcand 34,500 MVA oftransformer capacity, serving40 million customers1

Generation Transmission Distribution

Note:

1 As of Dec 31,2009

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 7/32

6

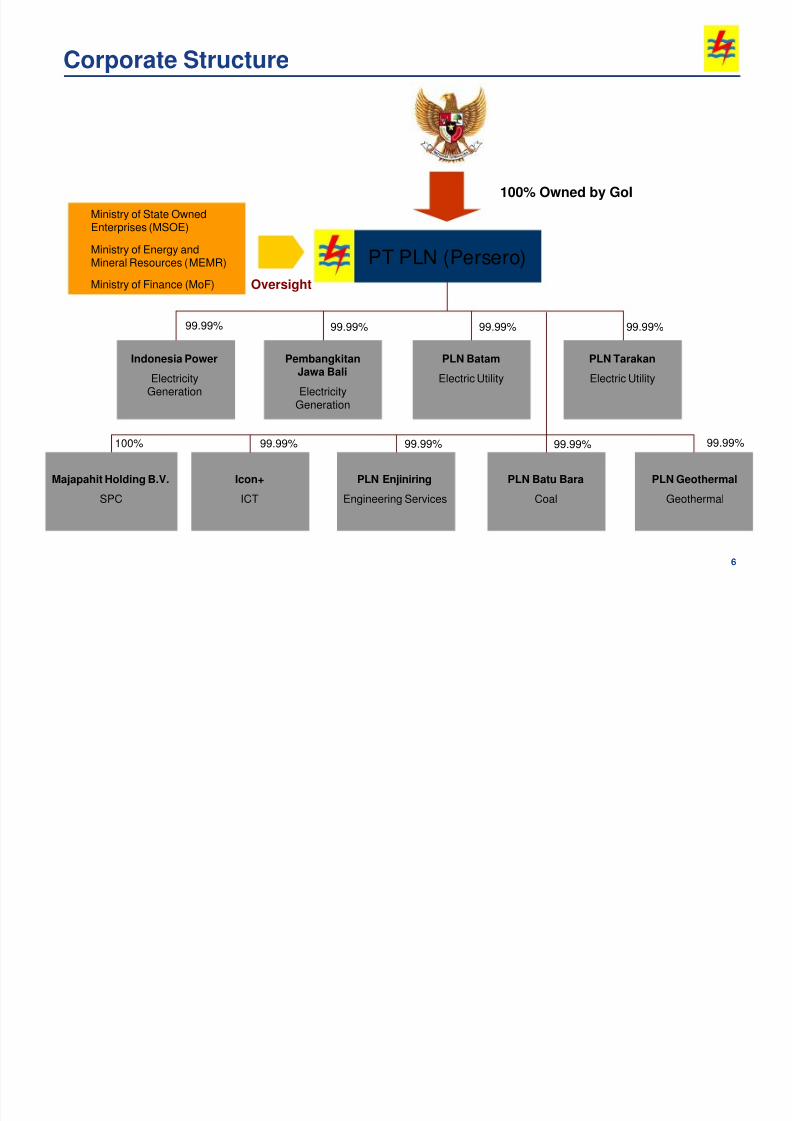

100% Owned by GoI

99.99% 99.99%

99.99%99.99% 99.99%

99.99% 99.99%

Indonesia Power

ElectricityGeneration

PT PLN (Persero)

99.99%

PLN Geothermal

Geothermal

Ministry of State OwnedEnterprises (MSOE)

Ministry of Energy andMineral Resources (MEMR)

Ministry of Finance (MoF) Oversight

Corporate Structure

100%

PLN Batu Bara

Coal

Majapahit Holding B.V.

SPC

Icon+

ICT

PLN Enjiniring

Engineering Services

PembangkitanJawa Bali

ElectricityGeneration

PLN Batam

Electric Utility

PLN Tarakan

Electric Utility

6

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 8/32

7

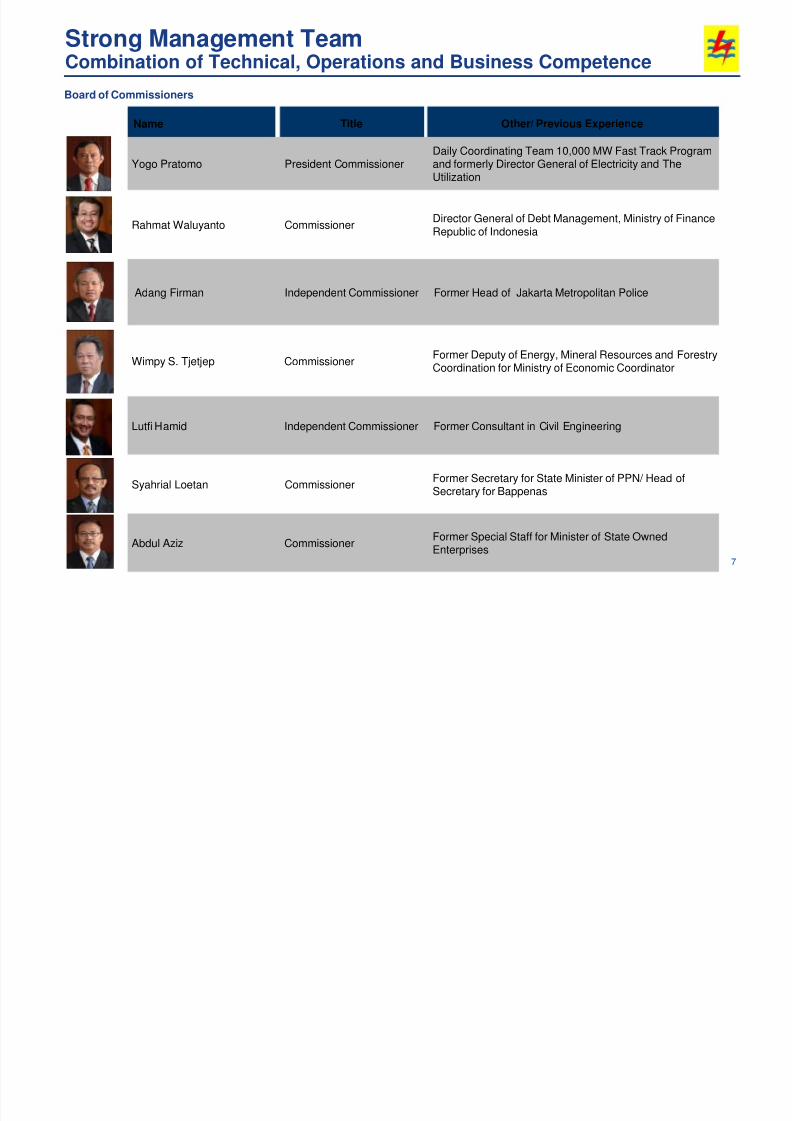

Strong Management TeamCombination of Technical, Operations and Business Competence

Name Title Other/ Previous Experience

Board of Commissioners

Yogo Pratomo President CommissionerDaily Coordinating Team 10,000 MW Fast Track Programand formerly Director General of Electricity and TheUtilization

Rahmat Waluyanto CommissionerDirector General of Debt Management, Ministry of FinanceRepublic of Indonesia

Adang Firman Independent Commissioner Former Head of Jakarta Metropolitan Police

Wimpy S. Tjetjep CommissionerFormer Deputy of Energy, Mineral Resources and ForestryCoordination for Ministry of Economic Coordinator

Lutfi Hamid Independent Commissioner Former Consultant in Civil Engineering

Syahrial Loetan CommissionerFormer Secretary for State Minister of PPN/ Head ofSecretary for Bappenas

Abdul Aziz CommissionerFormer Special Staff for Minister of State Owned

Enterprises

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 9/32

8

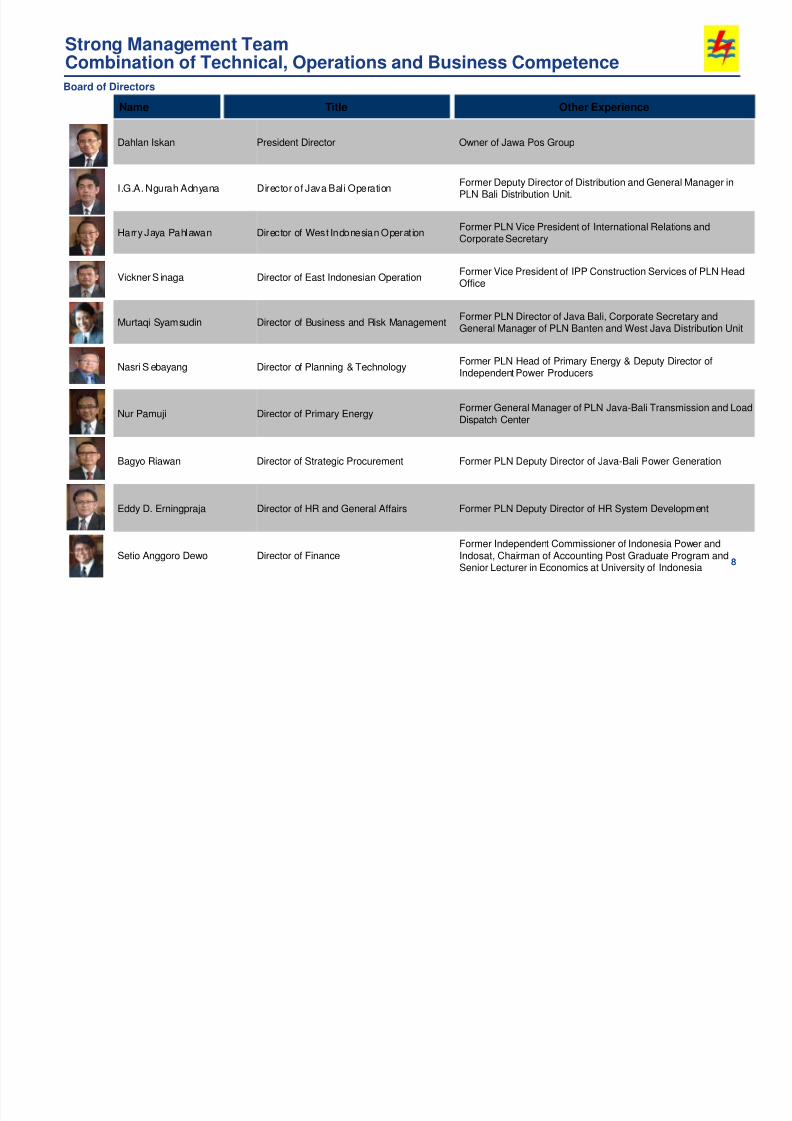

Strong Management TeamCombination of Technical, Operations and Business Competence

Dahlan Iskan President Director Owner of Jawa Pos Group

I.G.A. Ngurah Adnyana Director of Java Bali OperationFormer Deputy Director of Distribution and General Manager inPLN Bali Distribution Unit.

Harry Jaya Pahlawan Director of West Indonesian OperationFormer PLN Vice President of International Relations andCorporate Secretary

Vickner S inaga Director of East Indonesian OperationFormer Vice President of IPP Construction Services of PLN HeadOffice

Murtaqi Syamsudin Director of Business and Risk ManagementFormer PLN Director of Java Bali, Corporate Secretary andGeneral Manager of PLN Banten and West Java Distribution Unit

Nasri S ebayang Director of Planning & TechnologyFormer PLN Head of Primary Energy & Deputy Director ofIndependent Power Producers

Nur Pamuji Director of Primary EnergyFormer General Manager of PLN Java-Bali Transmission and LoadDispatch Center

Bagyo Riawan Director of Strategic Procurement Former PLN Deputy Director of Java-Bali Power Generation

Eddy D. Erningpraja Director of HR and General Affairs Former PLN Deputy Director of HR System Development

Setio Anggoro Dewo Director of Finance

Former Independent Commissioner of Indonesia Power and

Indosat, Chairman of Accounting Post Graduate Program andSenior Lecturer in Economics at University of Indonesia

8

Board of Directors

Name Title Other Experience

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 10/32

INVESTMENT STORY

9

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 11/32

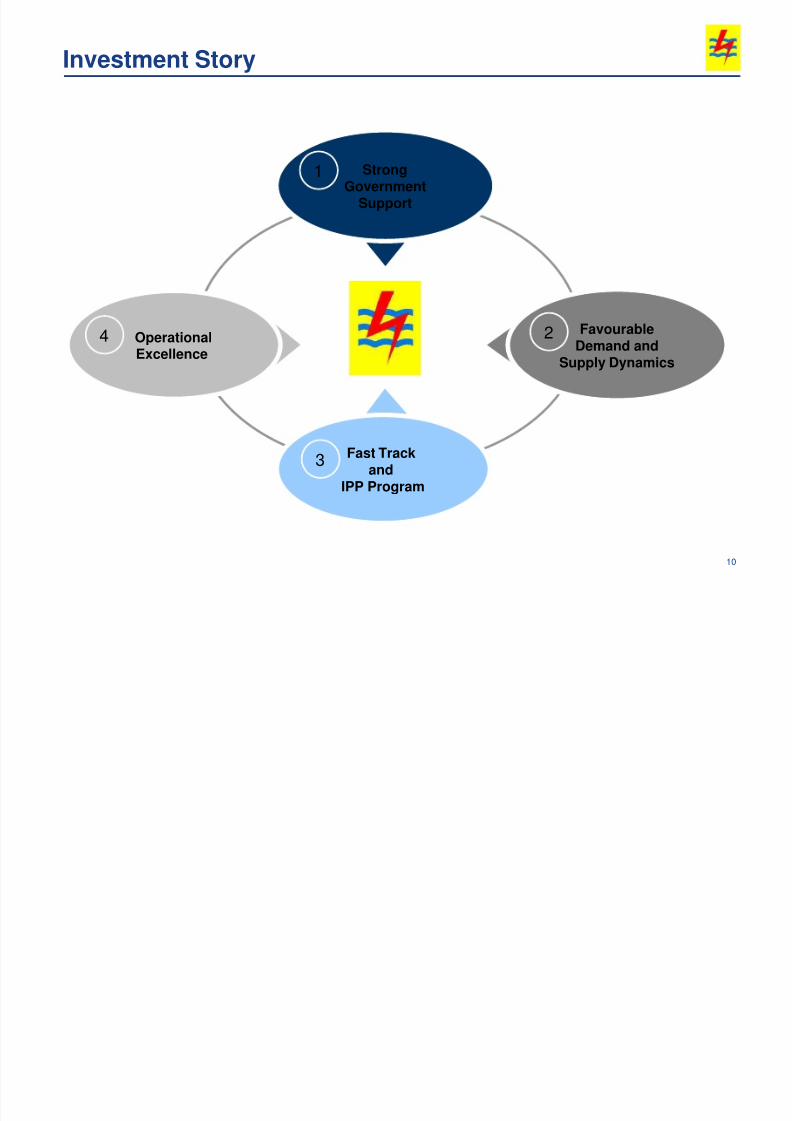

Investment Story

StrongGovernment

Support

FavourableDemand and

Supply Dynamics

1

2

Fast Trackand

IPP Program

3

OperationalExcellence

4

10

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 12/32

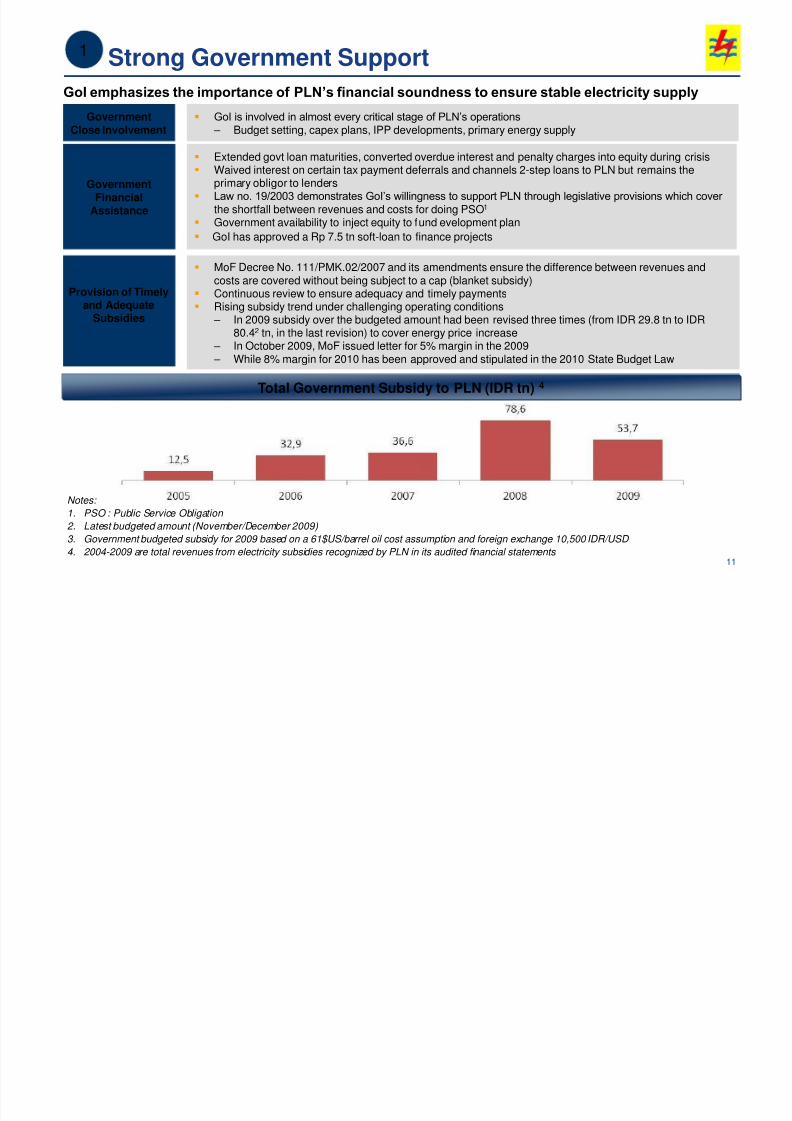

MoF Decree No. 111/PMK.02/2007 and its amendments ensure the difference between revenues and

costs are covered without being subject to a cap (blanket subsidy) Continuous review to ensure adequacy and timely payments Rising subsidy trend under challenging operating conditions

– In 2009 subsidy over the budgeted amount had been revised three times (from IDR 29.8 tn to IDR80.42 tn, in the last revision) to cover energy price increase

– In October 2009, MoF issued letter for 5% margin in the 2009 – While 8% margin for 2010 has been approved and stipulated in the 2010 State Budget Law

GoI emphasizes the importance of PLN’s financial soundness to ensure stable electricity supply

Notes:

1. PSO : Public Service Obligation

2. Latest budgeted amount (November/December 2009)

3. Government budgeted subsidy for 2009 based on a 61$US/barrel oil cost assumption and foreign exchange 10,500 IDR/USD

4. 2004-2009 are total revenues from electricity subsidies recognized by PLN in its audited financial statements

Total Government Subsidy to PLN (IDR tn) 4

Strong Government Support

Extended govt loan maturities, converted overdue interest and penalty charges into equity during crisis Waived interest on certain tax payment deferrals and channels 2-step loans to PLN but remains the

primary obligor to lenders Law no. 19/2003 demonstrates GoI’s willingness to support PLN through legislative provisions which cover

the shortfall between revenues and costs for doing PSO1

Government availability to inject equity to fund evelopment plan

GoI has approved a Rp 7.5 tn soft-loan to finance projects

GovernmentFinancial

Assistance

GoI is involved in almost every critical stage of PLN’s operations

– Budget setting, capex plans, IPP developments, primary energy supplyGovernment

Close Involvement

Provision of Timelyand Adequate

Subsidies

11

1

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 13/32

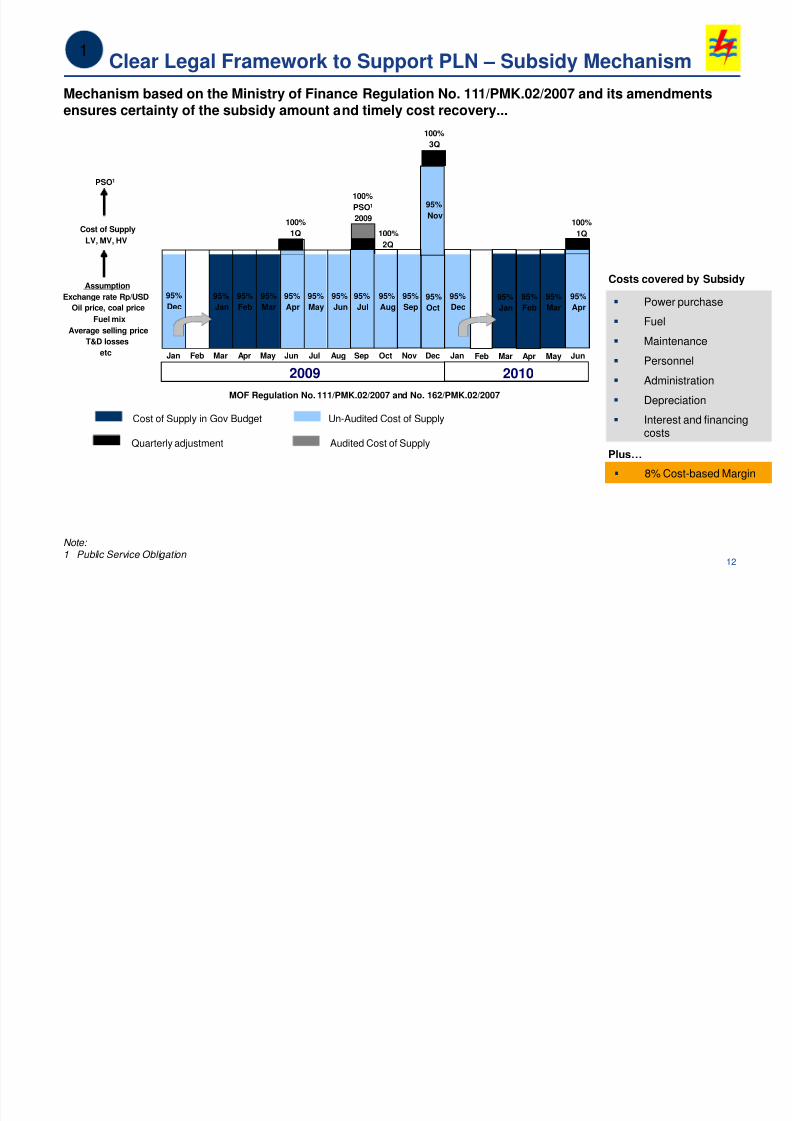

Clear Legal Framework to Support PLN – Subsidy Mechanism

Mechanism based on the Ministry of Finance Regulation No. 111/PMK.02/2007 and its amendmentsensures certainty of the subsidy amount and timely cost recovery...

Costs covered by Subsidy

Power purchase

Fuel

Maintenance

Personnel

Administration

Depreciation

Interest and financingcosts

1

Note:

1 Public Service Obligation 12

Cost of Supply in Gov Budget Un-Audited Cost of Supply

Audited Cost of Supply

MOF Regulation No. 111/PMK.02/2007 and No. 162/PMK.02/2007

95%

Dec

95%

Dec

95%

Jan

95%

Feb

95%

Mar

95%

Apr

95%

May

95%

Jun

95%

Jul

95%

Aug

95%

Sep

95%

Oct

2009

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Assumption

Exchange rate Rp/USD

Oil price, coal price

Fuel mix

Average selling price

T&D losses

etc

Cost of Supply

LV, MV, HV

PSO1

Jan

100%

1Q 100%

2Q

100%

3Q

100%

PSO1

2009

95%

Nov

2010

95%

Jan

95%

Feb

Feb Mar Apr

95%

Jan

95%

Jan

95%

Oct

95%

Jul

95%

Mar

May

Quarterly adjustment

95%

Apr

Jun

100%

1Q

8% Cost-based Margin

Plus…

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 14/32

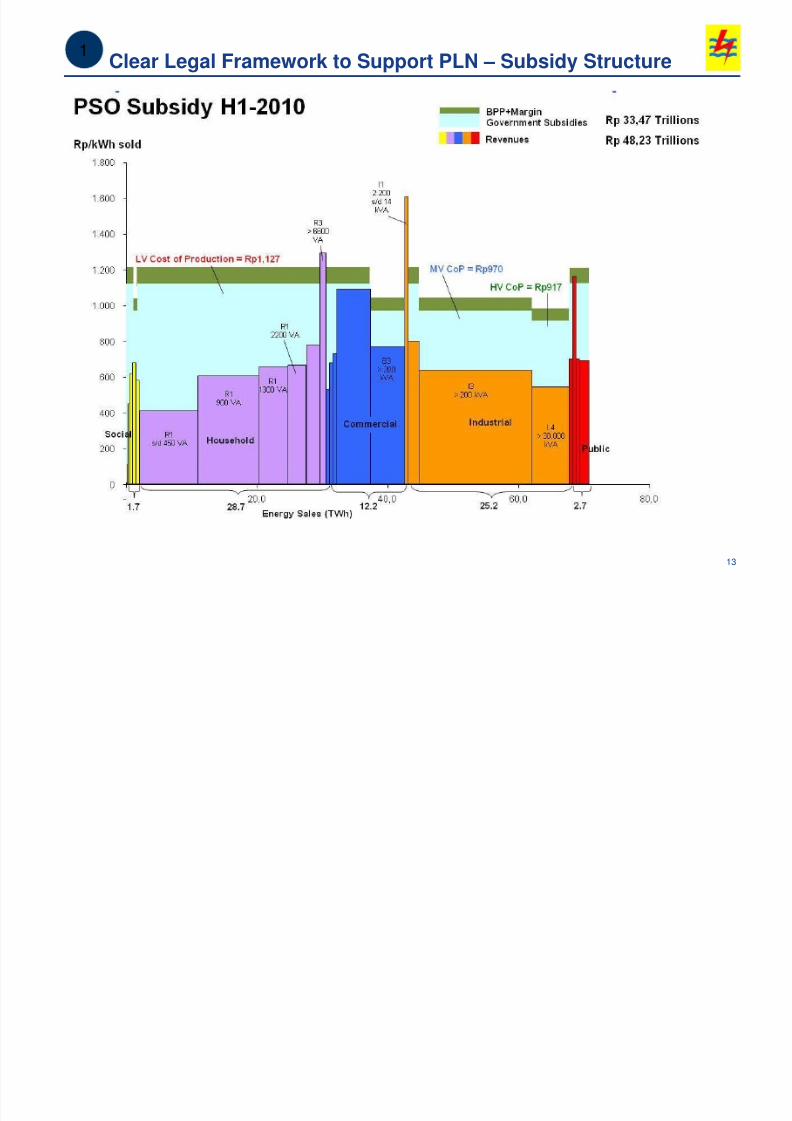

Clear Legal Framework to Support PLN – Subsidy Structure1

13

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 15/32

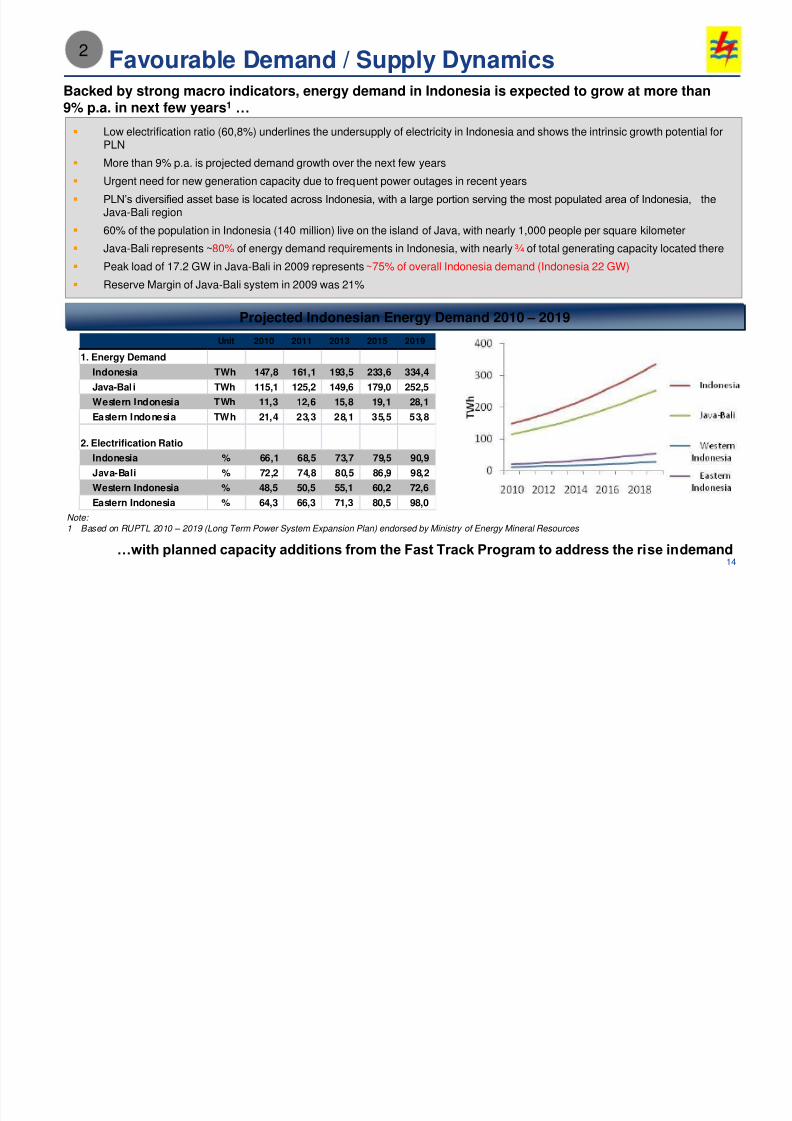

Favourable Demand / Supply DynamicsBacked by strong macro indicators, energy demand in Indonesia is expected to grow at more than9% p.a. in next few years1 …

…with planned capacity additions from the Fast Track Program to address the rise in demand

2

Projected Indonesian Energy Demand 2010 – 2019

Low electrification ratio (60,8%) underlines the undersupply of electricity in Indonesia and shows the intrinsic growth potential forPLN

More than 9% p.a. is projected demand growth over the next few years

Urgent need for new generation capacity due to frequent power outages in recent years

PLN’s diversified asset base is located across Indonesia, with a large portion serving the most populated area of Indonesia, theJava-Bali region

60% of the population in Indonesia (140 million) live on the island of Java, with nearly 1,000 people per square kilometer

Java-Bali represents ~80% of energy demand requirements in Indonesia, with nearly ¾ of total generating capacity located there

Peak load of 17.2 GW in Java-Bali in 2009 represents ~75% of overall Indonesia demand (Indonesia 22 GW)

Reserve Margin of Java-Bali system in 2009 was 21%

14

Note: 1 Based on RUPTL 2010 – 2019 (Long Term Power System Expansion Plan) endorsed by Ministry of Energy Mineral Resources

Unit 2010 2011 2013 2015 2019

1. Energy Demand

Indonesia TWh 147,8 161,1 193,5 233,6 334,4

Java-Bal i TWh 115,1 125,2 149,6 179,0 252,5

Western Indonesia TWh 11,3 12,6 15,8 19,1 28,1

Eastern Indonesia TWh 21,4 23,3 28,1 35,5 53,8

2. Electrification Ratio

Indonesia % 66,1 68,5 73,7 79,5 90,9

Java-Bali % 72,2 74,8 80,5 86,9 98,2

Western Indonesia % 48,5 50,5 55,1 60,2 72,6

Eastern Indonesia % 64,3 66,3 71,3 80,5 98,0

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 16/32

15

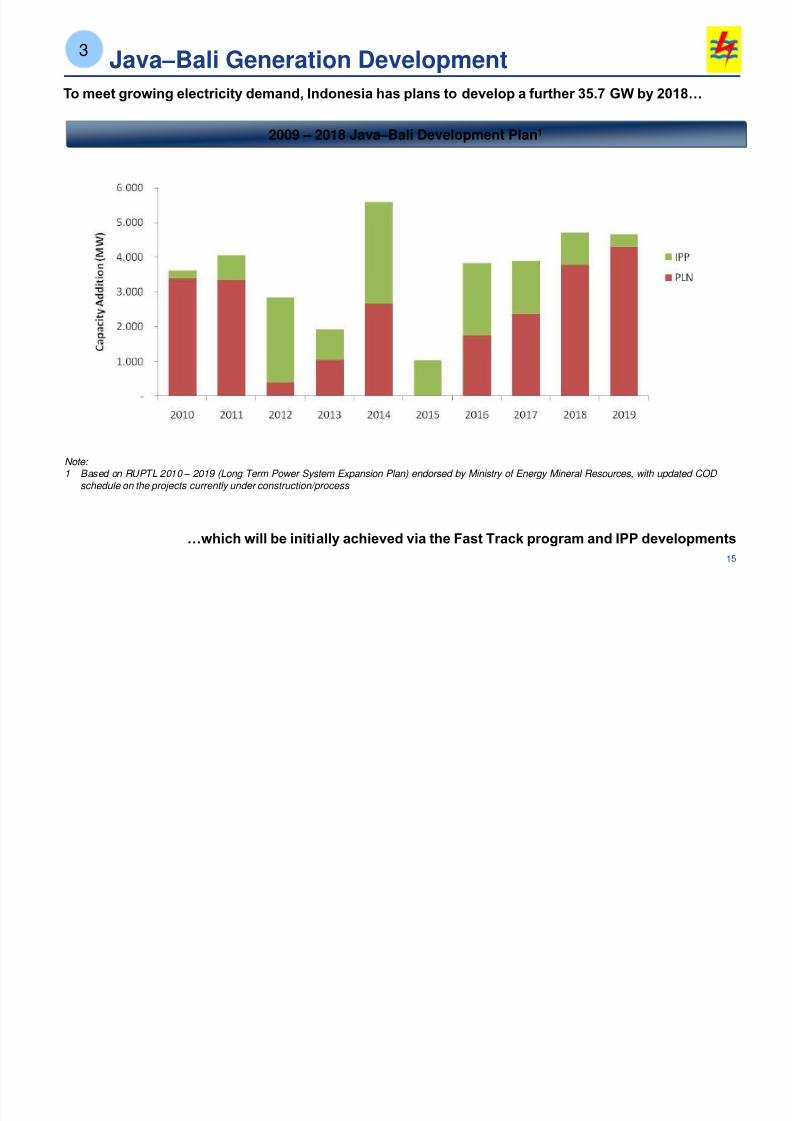

Java –Bali Generation Development

To meet growing electricity demand, Indonesia has plans to develop a further 35.7 GW by 2018…

3

2009 – 2018 Java –Bali Development Plan1

Note: 1 Based on RUPTL 2010 – 2019 (Long Term Power System Expansion Plan) endorsed by Ministry of Energy Mineral Resources, with updated COD

schedule on the projects currently under construction/process

…which will be initially achieved via the Fast Track program and IPP developments

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 17/32

Shortage of electricity in Indonesia

Abundance of coal in Indonesia Electricity generation with coal is much cheaper than with oil fuel

Long term strategy to replace oil fuel generation with coal fuel generation to lower fuel costs

Key Drivers

Overview ofFast TrackProgram

Formalised through Presidential Regulation no. 71/2006 in which PLN was mandated by GoIto build coal-fired power plants throughout Indonesia

To reduce subsidy burden for the GoI, to reduce PLN’s costs and to meet rising domestic

electricity demand

A Committee is set up through Presidential Regulation No. 72/2006, whose membersinclude Coordinating Minister of Economics, MOF, MSOE, MEMR and BAPPENAS

Develop 10 coal-fired power plants in Java-Bali and 26 coal-fired power plants outside Java-Bali totaling of approx. 9.5 GW; of which 25% will be completed by 2010 and another 50%by 2011

Once completed, significantly reduce oil fuel as a proportion of total fuel from 35.2%1 in 2008to below 10%1 in 2012

ProgramDescription

15% equity funding from PLN already committed

85% bank financing guaranteed by the GOI already committedFinancing

Fast Track Program – Overview3

16

Note: 1 Excludes IPPs and it is expressed in terms of percentage of total kilowatt hours generated by each fuel source

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 18/32

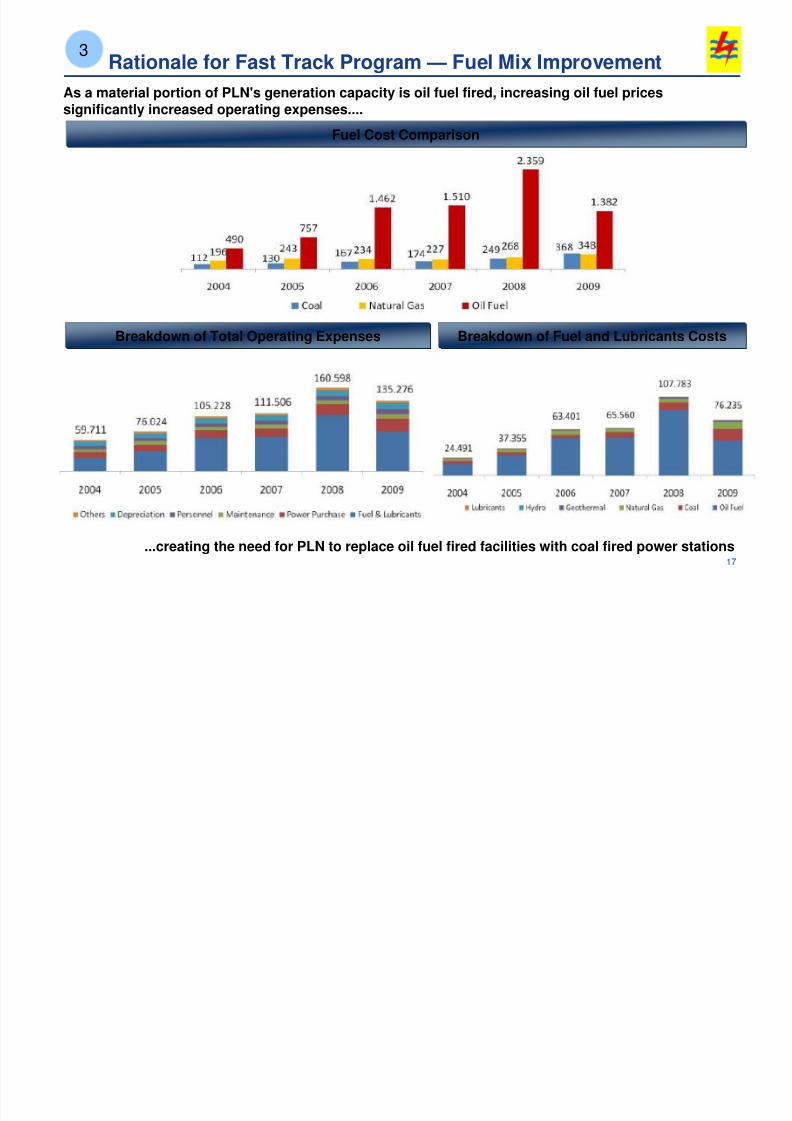

Breakdown of Fuel and Lubricants CostsBreakdown of Total Operating Expenses

As a material portion of PLN's generation capacity is oil fuel fired, increasing oil fuel pricessignificantly increased operating expenses....

...creating the need for PLN to replace oil fuel fired facilities with coal fired power stations

Rationale for Fast Track Program — Fuel Mix Improvement3

Fuel Cost Comparison

17

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 19/32

Fast Track Program in Progress Overview

Project progress varies; Four projects, equivalent to 2.5 GW, have achieved more than 90%progress; another ten (3 GW) have progressed more than 70%.

- Two units (Labuan – 600 MW) had achieved COD, another 1.7 GW from various projects

will follow by end of 2010- The remainder will be largely completed by 2011

ProjectConstruction

34 EPCContracts

signed; Twoare in Process

34 EPC contracts signed including 10 locations in Java-Bali (7.5GW) and 24 locationsoutside Java-Bali (2.0GW); Another two, Kaltim & Riau are to be signed latest by October

Total capacity of approximately 9.92 GW if all 36 locations are built

More than half of coal requirements have been secured by long term coal supply contracts(20 years)

Most of the remaining balance is under contract finalization process while the rest of thebalance will be tendered out

Coal Supply

Transmission is being developed in parallel with the substation construction

Total investment estimate is USD 2.2 billion

FTP I-related substation construction has achieved 36% progress

Transmissionsystem

18

3

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 20/32

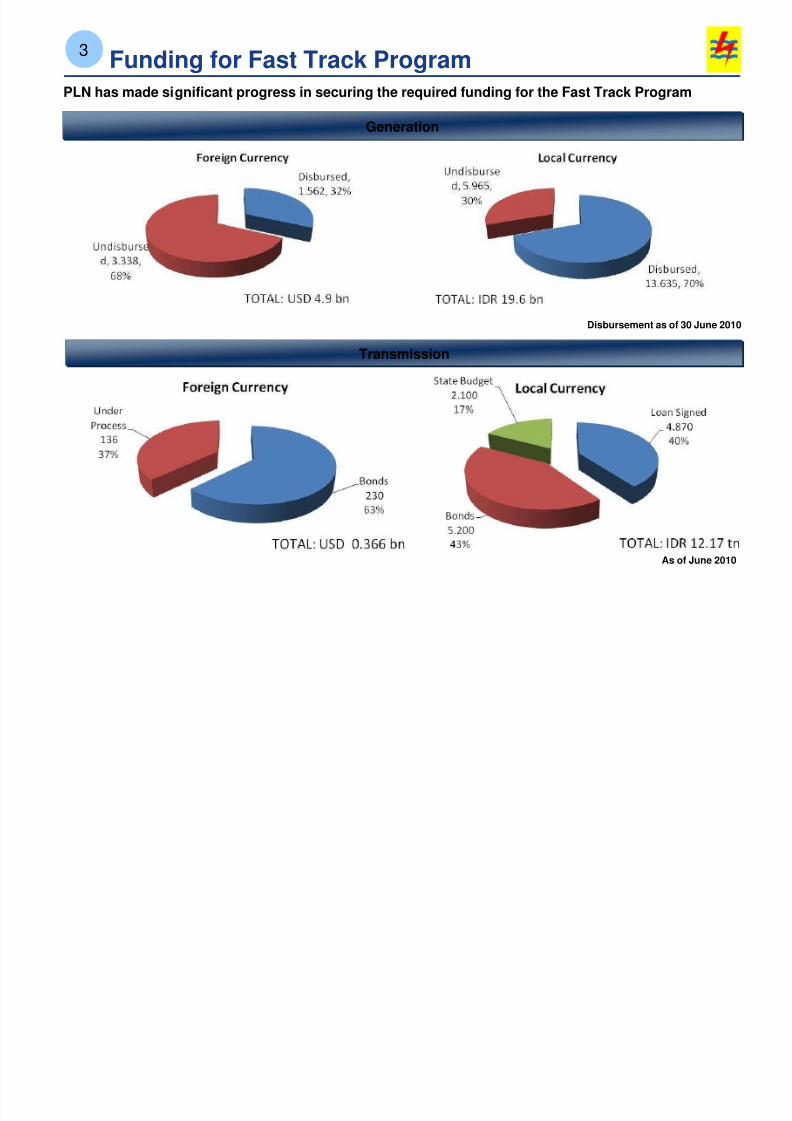

Funding for Fast Track Program

PLN has made significant progress in securing the required funding for the Fast Track Program

Transmission

Generation

3

Disbursement as of 30 June 2010

As of June 2010

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 21/32

Coal

68%

Geothermal

15%

Gas

16%

Oil

1%

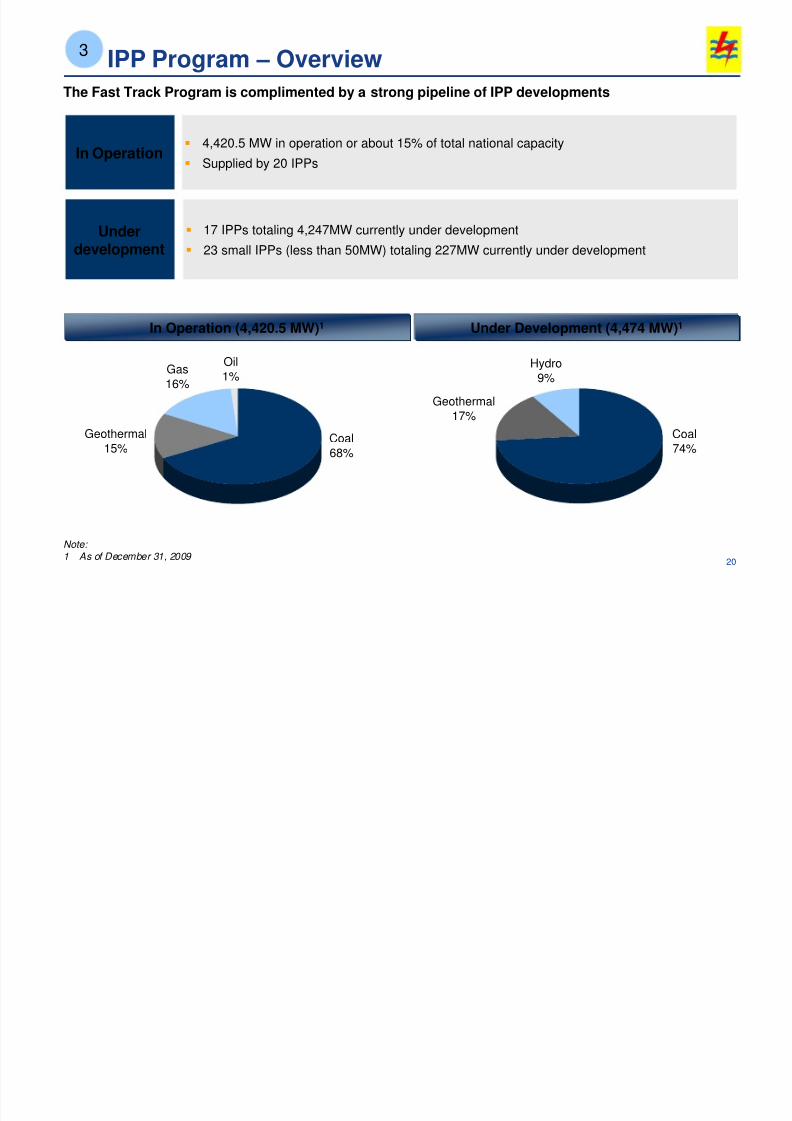

17 IPPs totaling 4,247MW currently under development

23 small IPPs (less than 50MW) totaling 227MW currently under development

Underdevelopment

In Operation 4,420.5 MW in operation or about 15% of total national capacity

Supplied by 20 IPPs

IPP Program – Overview3

20

Under Development (4,474 MW)1In Operation (4,420.5 MW)1

Coal

74%

Geothermal

17%

Hydro

9%

Note:

1 As of December 31, 2009

The Fast Track Program is complimented by a strong pipeline of IPP developments

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 22/32

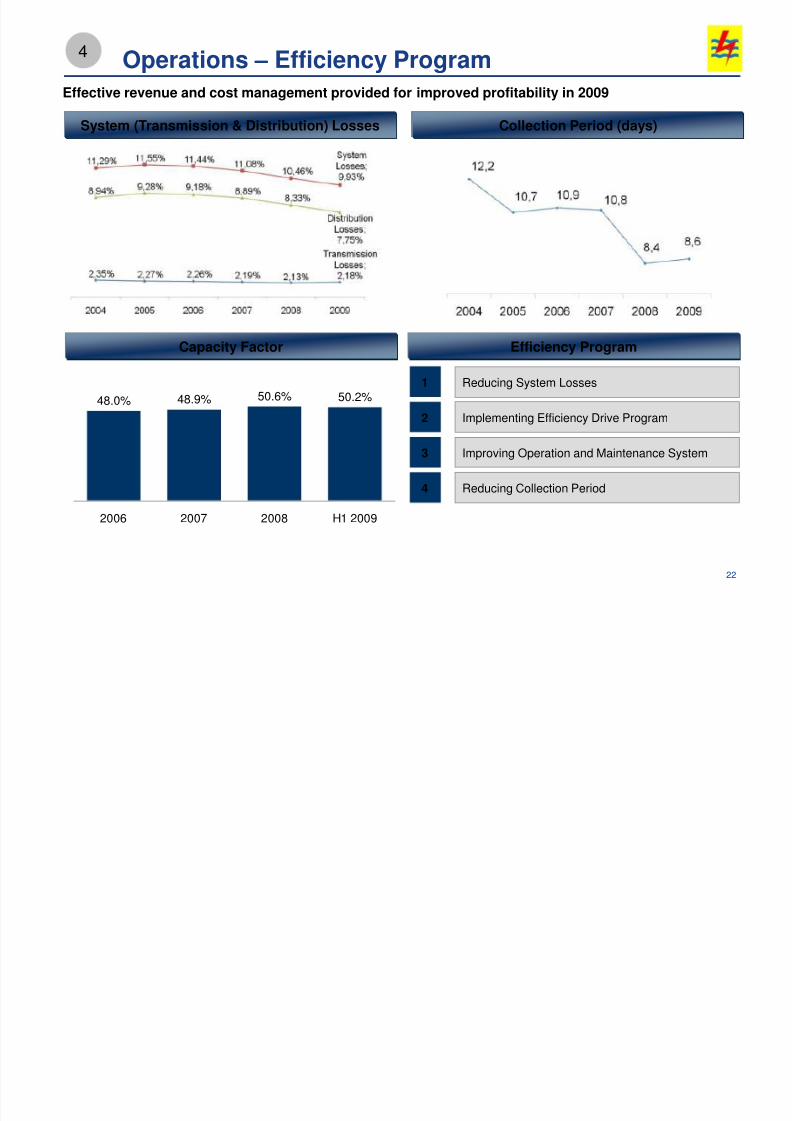

48.0% 48.9% 50.6% 50.2%

2006 2007 2008 H1 2009

Operations – Efficiency Program

System (Transmission & Distribution) Losses Collection Period (days)

Reducing System Losses1

Implementing Efficiency Drive Program2

Improving Operation and Maintenance System3

4 Reducing Collection Period

Efficiency ProgramCapacity Factor

22

4

Effective revenue and cost management provided for improved profitability in 2009

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 23/32

REGULATORY UPDATE

24

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 24/32

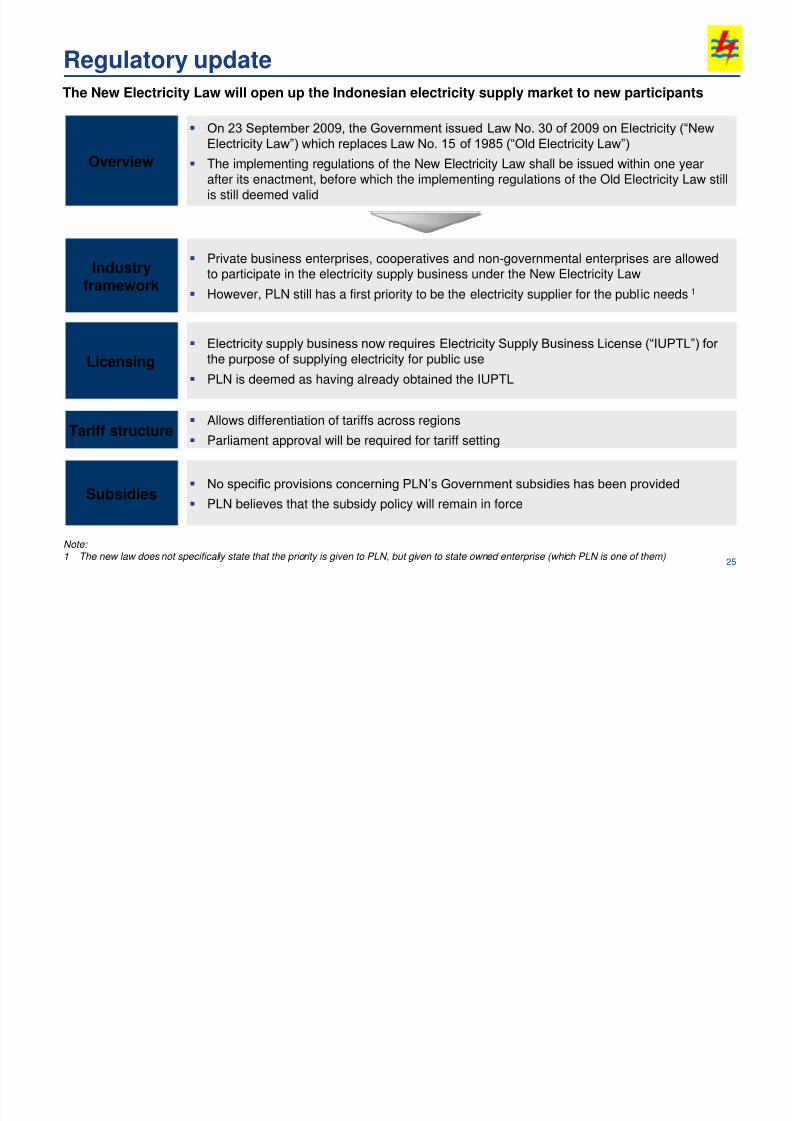

Regulatory update

Private business enterprises, cooperatives and non-governmental enterprises are allowed

to participate in the electricity supply business under the New Electricity Law However, PLN still has a first priority to be the electricity supplier for the public needs1

Industry

framework

Overview

On 23 September 2009, the Government issued Law No. 30 of 2009 on Electricity (“New

Electricity Law”) which replaces Law No. 15 of 1985 (“Old Electricity Law”)

The implementing regulations of the New Electricity Law shall be issued within one yearafter its enactment, before which the implementing regulations of the Old Electricity Law stillis still deemed valid

Allows differentiation of tariffs across regions

Parliament approval will be required for tariff settingTariff structure

No specific provisions concerning PLN’s Government subsidies has been provided

PLN believes that the subsidy policy will remain in forceSubsidies

Electricity supply business now requires Electricity Supply Business License (“IUPTL”) for

the purpose of supplying electricity for public use

PLN is deemed as having already obtained the IUPTL

Licensing

25

The New Electricity Law will open up the Indonesian electricity supply market to new participants

Note:

1 The new law does not specifically state that the priority is given to PLN, but given to state owned enterprise (which PLN is one of them)

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 25/32

FINANCIAL UPDATE

26

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 26/32

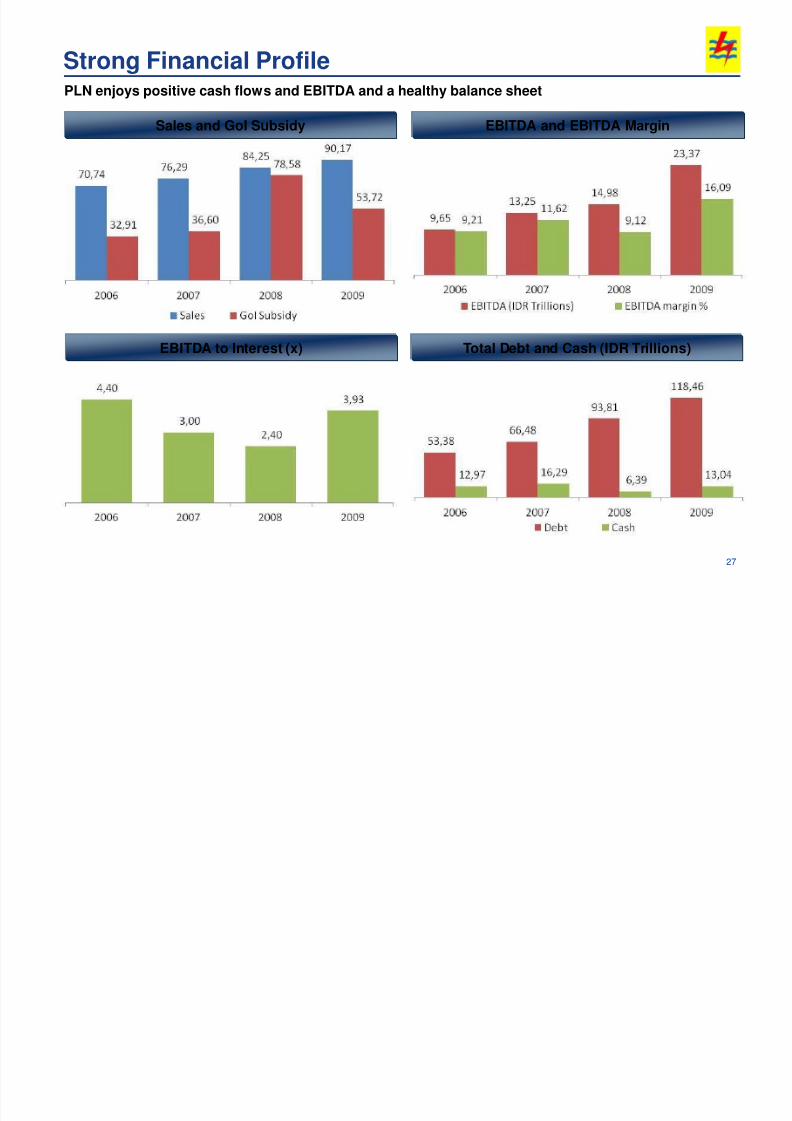

Strong Financial Profile

EBITDA and EBITDA Margin

EBITDA to Interest (x)

Sales and GoI Subsidy

Total Debt and Cash (IDR Trillions)

PLN enjoys positive cash flows and EBITDA and a healthy balance sheet

27

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 27/32

THANK YOU

28

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 28/32

APPENDIX

29

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 29/32

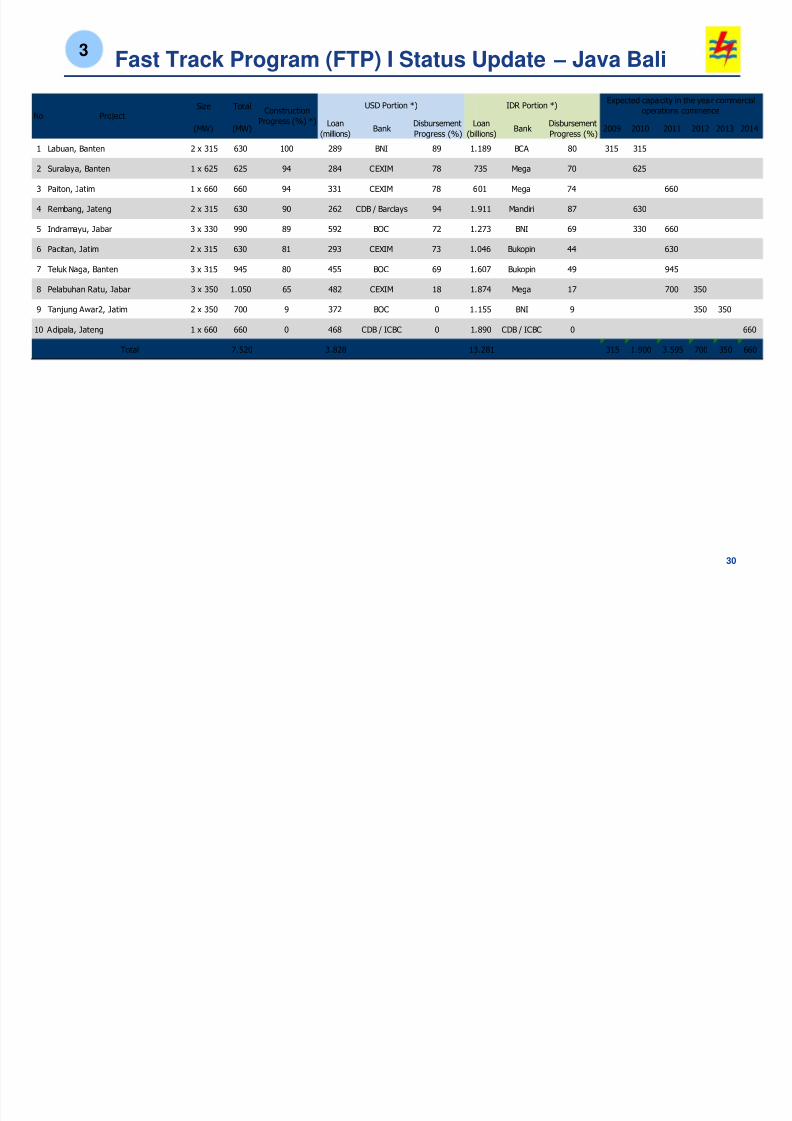

Fast Track Program (FTP) I Status Update – Java Bali3

30

Size Total

(MW) (MW)Loan

(millions)Bank

Disbursement

Progress (%)

Loan

(billions)Bank

Disbursement

Progress (%)2009 2010 2011 2012 2013 2014

1 Labuan, Banten 2 x 315 630 100 289 BNI 89 1.189 BCA 80 315 315

2 Suralaya, Banten 1 x 625 625 94 284 CEXIM 78 735 Mega 70 625

3 Paiton, Jatim 1 x 660 660 94 331 CEXIM 78 601 Mega 74 660

4 Rembang, Jateng 2 x 315 630 90 262 CDB / Barclays 94 1.911 Mandiri 87 630

5 Indramayu, Jabar 3 x 330 990 89 592 BOC 72 1.273 BNI 69 330 660

6 Pacitan, Jatim 2 x 315 630 81 293 CEXIM 73 1.046 Bukopin 44 630

7 Teluk Naga, Banten 3 x 315 945 80 455 BOC 69 1.607 Bukopin 49 945

8 Pelabuhan Ratu, Jabar 3 x 350 1.050 65 482 CEXIM 18 1.874 Mega 17 700 350

9 Tanjung Awar2, Jatim 2 x 350 700 9 372 BOC 0 1.155 BNI 9 350 350

10 Adipala, Jateng 1 x 660 660 0 468 CDB / ICBC 0 1.890 CDB / ICBC 0 660

7.520 3.828 13.281 315 1.900 3.595 700 350 660Total

No ProjectConstruction

Progress (%) *)

Expected capacity in the year commercial

operations commenceUSD Portion *) IDR Portion *)

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 30/32

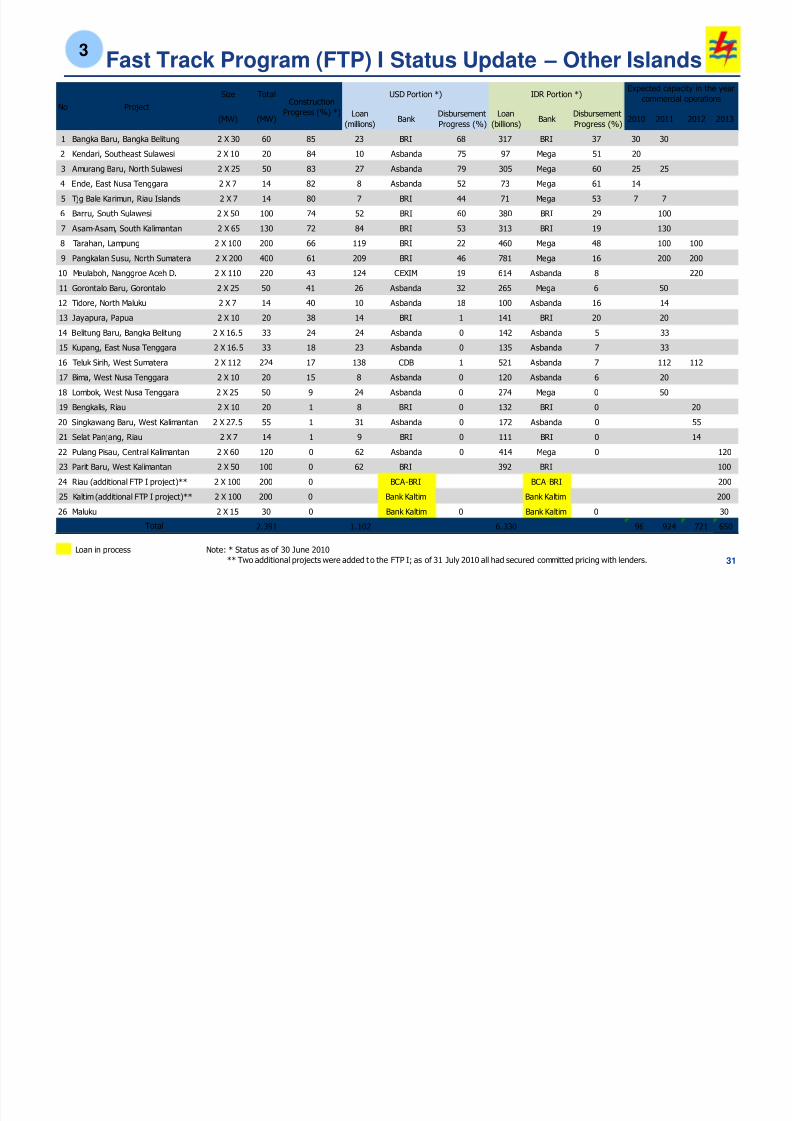

Fast Track Program (FTP) I Status Update – Other Islands3

31

Size Total

(MW) (MW)Loan

(millions)Bank

Disbursement

Progress (%)

Loan

(billions)Bank

Disbursement

Progress (%)2010 2011 2012 2013

1 Bangka Baru, Bangka Belitung 2 X 30 60 85 23 BRI 68 317 BRI 37 30 302 Kendari, Southeast Sulawesi 2 X 10 20 84 10 Asbanda 75 97 Mega 51 20

3 Amurang Baru, North Sulawesi 2 X 25 50 83 27 Asbanda 79 305 Mega 60 25 25

4 Ende, East Nusa Tenggara 2 X 7 14 82 8 Asbanda 52 73 Mega 61 14

5 Tjg Bale Karimun, Riau Islands 2 X 7 14 80 7 BRI 44 71 Mega 53 7 7

6 Barru, South Sulawesi 2 X 50 100 74 52 BRI 60 380 BRI 29 100

7 Asam-Asam, South Kalimantan 2 X 65 130 72 84 BRI 53 313 BRI 19 130

8 Tarahan, Lampung 2 X 100 200 66 119 BRI 22 460 Mega 48 100 100

9 Pangkalan Susu, North Sumatera 2 X 200 400 61 209 BRI 46 781 Mega 16 200 200

10 Meulaboh, Nanggroe Aceh D. 2 X 110 220 43 124 CEXIM 19 614 Asbanda 8 220

11 Gorontalo Baru, Gorontalo 2 X 25 50 41 26 Asbanda 32 265 Mega 6 50

12 Tidore, North Maluku 2 X 7 14 40 10 Asbanda 18 100 Asbanda 16 14

13 Jayapura, Papua 2 X 10 20 38 14 BRI 1 141 BRI 20 20

14 Belitung Baru, Bangka Belitung 2 X 16.5 33 24 24 Asbanda 0 142 Asbanda 5 33

15 Kupang, East Nusa Tenggara 2 X 16.5 33 18 23 Asbanda 0 135 Asbanda 7 33

16 Teluk Sirih, West Sumatera 2 X 112 224 17 138 CDB 1 521 Asbanda 7 112 112

17 Bima, West Nusa Tenggara 2 X 10 20 15 8 Asbanda 0 120 Asbanda 6 20

18 Lombok, West Nusa Tenggara 2 X 25 50 9 24 Asbanda 0 274 Mega 0 50

19 Bengkalis, Riau 2 X 10 20 1 8 BRI 0 132 BRI 0 20

20 Singkawang Baru, West Kalimantan 2 X 27.5 55 1 31 Asbanda 0 172 Asbanda 0 55

21 Selat Panjang, Riau 2 X 7 14 1 9 BRI 0 111 BRI 0 14

22 Pulang Pisau, Central Kalimantan 2 X 60 120 0 62 Asbanda 0 414 Mega 0 120

23 Parit Baru, West Kalimantan 2 X 50 100 0 62 BRI 392 BRI 100

24 Riau (additional FTP I project)** 2 X 100 200 0 BCA-BRI BCA-BRI 200

25 Kaltim (additional FTP I project)** 2 X 100 200 0 Bank Kaltim Bank Kaltim 200

26 Maluku 2 X 15 30 0 Bank Kaltim 0 Bank Kaltim 0 30

2.391 1.102 6.330 96 924 721 650

Loan in process Note: * Status as of 30 June 2010

** Two additional projects were added to the FTP I; as of 31 July 2010 all had secured committed pricing with lenders.

Total

Expected capacity in the year

commercial operationsNo Project

Construction

Progress (%) *)

USD Portion *) IDR Portion *)

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 31/32

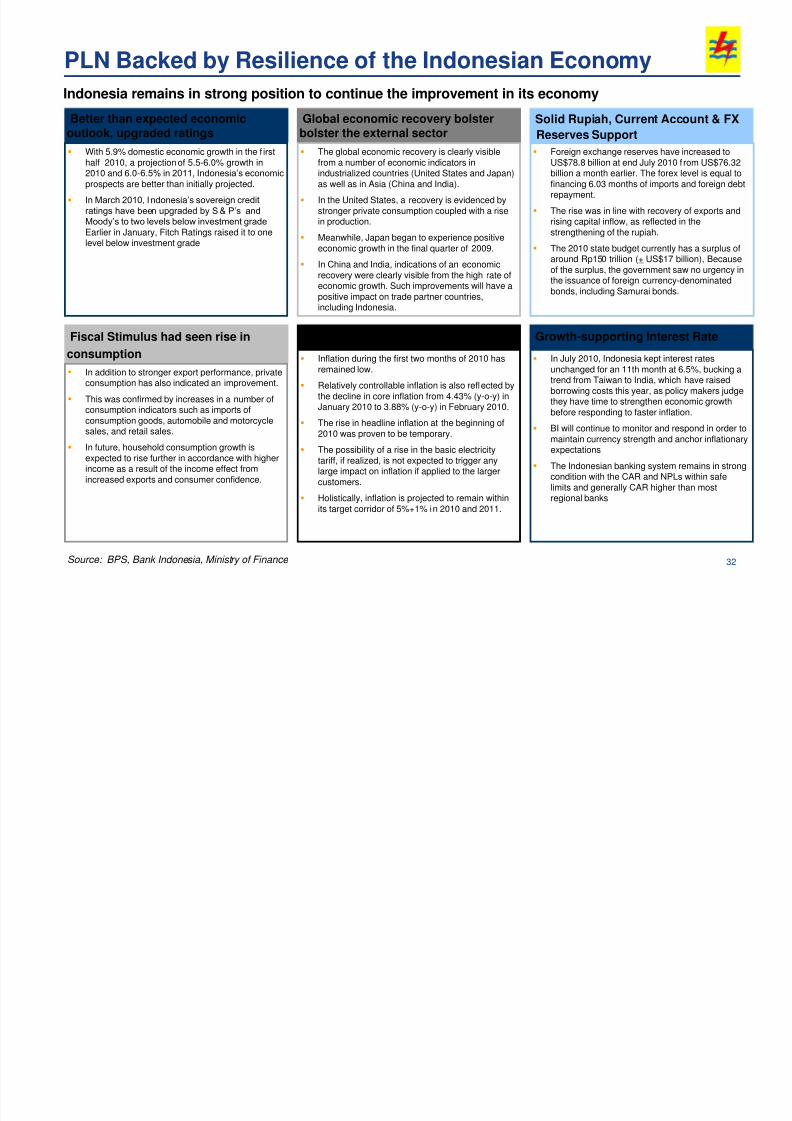

Indonesia remains in strong position to continue the improvement in its economy

Better than expected economicoutlook, upgraded ratings

With 5.9% domestic economic growth in the f irsthalf 2010, a projection of 5.5-6.0% growth in2010 and 6.0-6.5% in 2011, Indonesia’s economic

prospects are better than initially projected.

In March 2010, Indonesia’s sovereign credit

ratings have been upgraded by S & P’s andMoody’s to two levels below investment grade

Earlier in January, Fitch Ratings raised it to onelevel below investment grade

Global economic recovery bolsterbolster the external sector

The global economic recovery is clearly visiblefrom a number of economic indicators inindustrialized countries (United States and Japan)as well as in Asia (China and India).

In the United States, a recovery is evidenced bystronger private consumption coupled with a risein production.

Meanwhile, Japan began to experience positiveeconomic growth in the final quarter of 2009.

In China and India, indications of an economicrecovery were clearly visible from the high rate ofeconomic growth. Such improvements will have apositive impact on trade partner countries,including Indonesia.

Solid Rupiah, Current Account & FX

Reserves Support

Foreign exchange reserves have increased toUS$78.8 billion at end July 2010 f rom US$76.32billion a month earlier. The forex level is equal tofinancing 6.03 months of imports and foreign debtrepayment.

The rise was in line with recovery of exports andrising capital inflow, as reflected in thestrengthening of the rupiah.

The 2010 state budget currently has a surplus ofaround Rp150 trillion (+ US$17 billion), Becauseof the surplus, the government saw no urgency in

the issuance of foreign currency-denominatedbonds, including Samurai bonds.

Fiscal Stimulus had seen rise in

consumption

In addition to stronger export performance, privateconsumption has also indicated an improvement.

This was confirmed by increases in a number ofconsumption indicators such as imports of

consumption goods, automobile and motorcyclesales, and retail sales.

In future, household consumption growth isexpected to rise further in accordance with higherincome as a result of the income effect fromincreased exports and consumer confidence.

Source: BPS, Bank Indonesia, Ministry of Finance

Controllable Inflation

Inflation during the first two months of 2010 hasremained low.

Relatively controllable inflation is also reflected bythe decline in core inflation from 4.43% (y-o-y) inJanuary 2010 to 3.88% (y-o-y) in February 2010.

The rise in headline inflation at the beginning of2010 was proven to be temporary.

The possibility of a rise in the basic electricitytariff, if realized, is not expected to trigger anylarge impact on inflation if applied to the largercustomers.

Holistically, inflation is projected to remain withinits target corridor of 5%+1% in 2010 and 2011.

Growth-supporting Interest Rate

In July 2010, Indonesia kept interest ratesunchanged for an 11th month at 6.5%, bucking atrend from Taiwan to India, which have raisedborrowing costs this year, as policy makers judgethey have time to strengthen economic growthbefore responding to faster inflation.

BI will continue to monitor and respond in order tomaintain currency strength and anchor inflationaryexpectations

The Indonesian banking system remains in strongcondition with the CAR and NPLs within safelimits and generally CAR higher than mostregional banks

PLN Backed by Resilience of the Indonesian Economy

32

8/7/2019 Investor Update Untuk Meeting Juli 2010

http://slidepdf.com/reader/full/investor-update-untuk-meeting-juli-2010 32/32

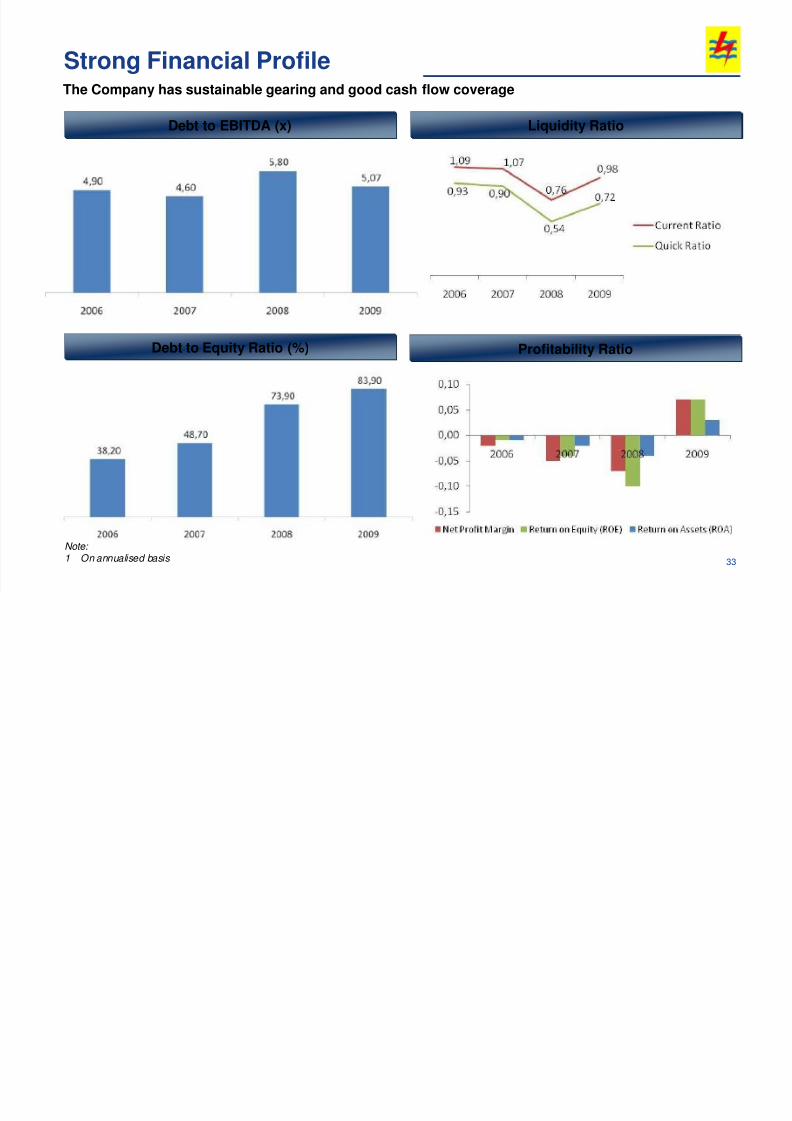

Strong Financial Profile

Debt to EBITDA (x)

Debt to Equity Ratio (%)

Liquidity Ratio

Profitability Ratio

The Company has sustainable gearing and good cash flow coverage

33

Note:

1 On annualised basis

![Juli everbs [recuperado]](https://img.pdfslide.us/doc/110x75/54b87dbc4a7959ce2d8b458b/juli-everbs-recuperado.jpg)