Embed Size (px)

Citation preview

Q3, 2018

INVESTOR PRESENTATION

2

Classification: General Business Use

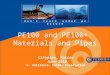

SABIC AT A GLANCE

50Countries of operations

Top 3 Largest global

chemical companies1

100+Countries of sales

USD BnTotal Assets9mYTD 2018

89USD Bn

Annual SalesFY 2017

40USD Bn

Net Income FY 2017

5USD Bn

Market Capitalization4

101

A+/A1Highest standalone

credit rating3

Top 3 Chemical Brand

Value2

MostProfitable global

chemical company5

Product Application Centers

Technology and Corporate Research and Innovation Centers

Production, Distribution, Storage Facilities and Logistical Hubs

International Subsidiaries and Sales Offices

Manufacturing and Compounding Companies

Global Headquarters

Source: 1 Forbes 2018, 2 Brand Finance 2018. Notes: 3 By all three ratings agencies, 4 As of 30 October 2018, 5 ICIS 100 Chemical companies 2018, All figures are rounded to the nearest billion. SAR/USD Rate: 0.2666.

3

Classification: General Business Use

0

10

20

30

40

50

60

70

80

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

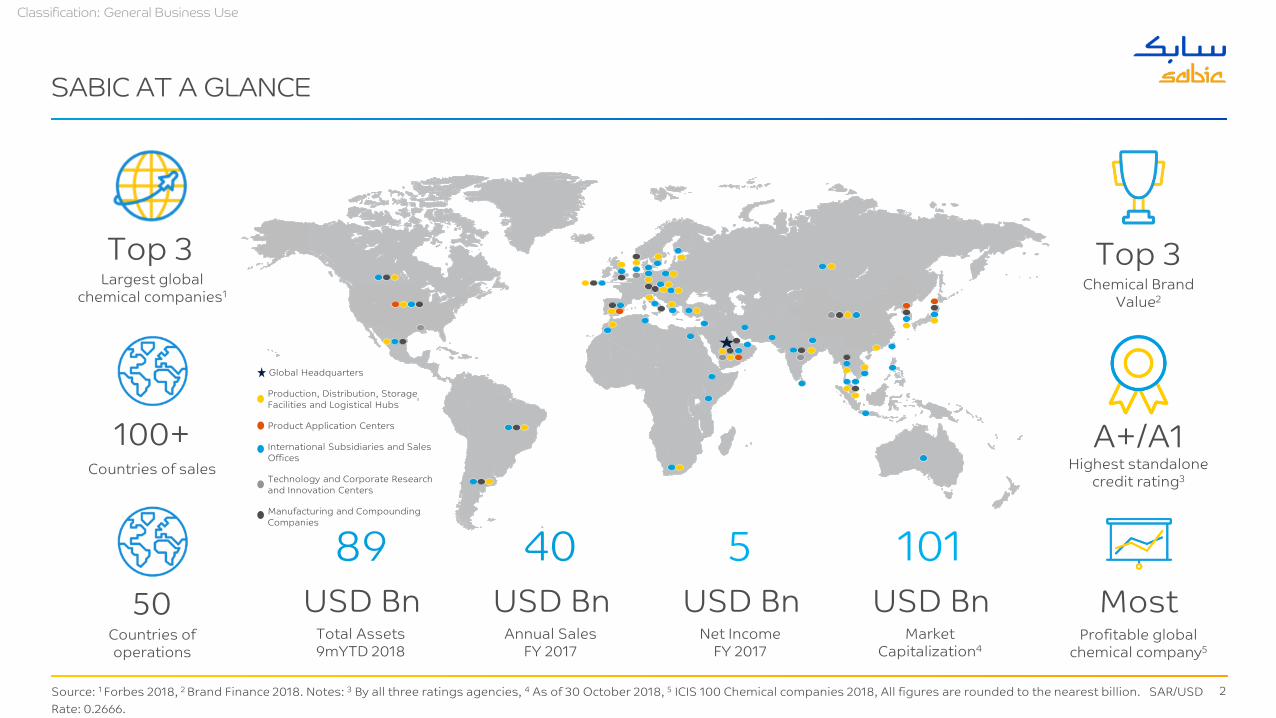

SABIC’S GROWTH SINCE ITS INCEPTION

In addition to SABIC’s organic growth, we have successfully acquired and integrated several businesses since establishment

MORE THAN 40 YEARS OF ORGANIC AND INORGANIC GROWTH

1984Gas

1985Sadaf, Yanpet,

Petrokemya, Kemya, Sharq and Ibn Sina

2002DSM Petrochemicals

2006Huntsman

Petrochemicals

2007GE Plastics

2010Yansab and Sharq

2011 / 2012Saudi Kayan

2017Ibn Sina POM

2018SAMAC

1983Hadeed,

Al-Bayroniand Ar-Razi

MM

T

740

2000 2017

SALES USD Billion

CAGR 10.7%

4

Classification: General Business Use

SABIC’S 2025 STRATEGY - WORLD LEADER IN CHEMICALS

TO BE THE PREFERRED WORLD LEADER IN CHEMICALS

by delivering Chemistry that MattersTM

More global…more integrated…more differentiated…ambitious growth

FINANCIALWorld class financial

performance• Grow revenues faster than

global GDP• Leading EBITDA margin in our

industry

MARKETAdapt to / differentiate

in markets• Closer to products with high

value add• Growth driven by

differentiated offerings and innovative solutions

FEEDSTOCKIncrease flexibility &

competitiveness• Access to diversified, global

competitive feedstock around the world

• Energy & feedstock optimization

TECHNOLOGYCreating

a competitive edge• Best in class productivity and

efficiency• Leadership in select

technologies

OUR VISION:

SUSTAINABILITY ORGANIZATION & CULTURE GLOBALIZATION

KEY HIGHLIGHTS

INVESTOR PRESENTATION

6

Classification: General Business Use

KEY HIGHLIGHTS

1. Market Leader in Multiple Products and Segments

2. Diversified Global Footprint

3. Cost Leadership and Operational Excellence

4. Strategic, Strong and Stable Alliances

5. Robust Financial Profile, Dividend and Stock Performance

7

Classification: General Business Use

1. MARKET LEADER IN MULTIPLE PRODUCTS AND SEGMENTS

1 Source: Global Market Share excluding Partners vs 2017 consumption from BI. 3Ps&E: PVC/ PET/ PS & Elastomers

PETROCHEMICALS AGRI-NUTRIENTS SPECIALTIES

TRANSPORTATIONMEDICAL DEVICES PACKAGING CLEAN ENERGYCONSTRUCTION

A global leading fertilizer producer;with over 7 MMT produced in 2017

► No 1 exporter of Granular Urea1

• Key products include urea, ammonia, phosphate and specialised products

• Represents circa 10% of SABIC’s total production by volume

• Sustainable projects to turn greenhouse gases to fertilizer

Global offerings of innovative solutions for various industries; • Broad portfolio including specialty compounds,

film and sheet, and a range of branded products such as NORYL™, ULTEM™, EXTEM™, and LNP™products

• 9,000 people employed• Over 10,000 customers• Portfolio of approximately 40,000 products

AGRI-NUTRIENTSELECTRICAL &ELECTRONICS

SABIC’s largest operating unit;One of the world’s largest global petrochemicals companies► No 1 producer of MTBE 1

► No 1 producer of glycols 1

► No 2 producer of Methanol and Polycarbonate 1

► No 3 producer of Polyethylene and Polypropylene 1

Manufactures a wide range of chemicals, plastics and other materials in Middle East, Europe, Americas and Asia

8

Classification: General Business Use

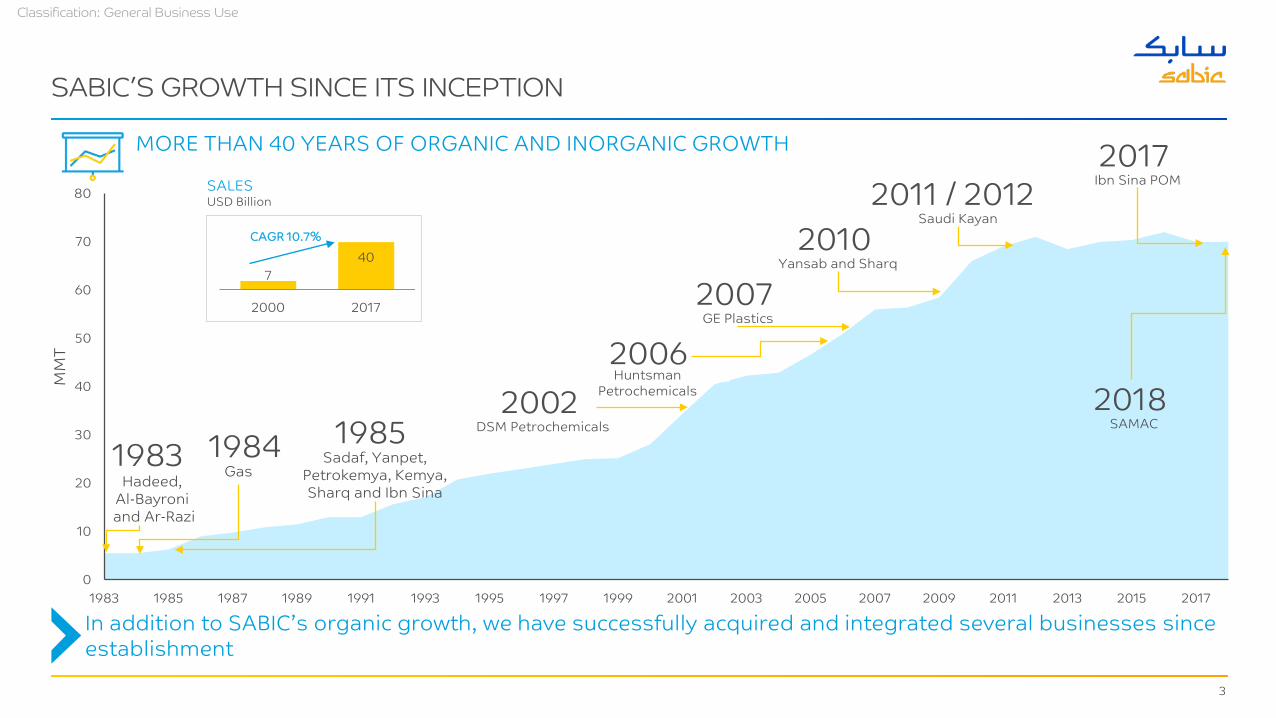

2. DIVERSIFIED GLOBAL FOOTPRINT

Source: SABIC’s Consolidated Financial Statement and Independent Auditor’ Report for FY 2017, Note 34. Notes: All figures as of FY 2017, PPE = Property, Plant and Equipment, 14% of Sales are from other locations. 1 Key growth areas outside of KSA

Globally, SABIC has presence in all the key demand centres and has close proximity to future growth markets Balanced sales across geographies

Product Application Centers

Technology and Corporate Research and Innovation Centers

Production, Distribution, Storage Facilities and Logistical Hubs

International Subsidiaries and Sales Offices

Manufacturing and Compounding Companies

Global Headquarters

2 Manufacturing Companies8 Compounding Companies1 Cracker

S P

25 Manufacturing Companies11 Crackers

A PSH Hadeed

P Petrochemicals

A Agri-Nutrients

S Specialties

Key Growth Areas1

1%

S8 Manufacturing Companies8 Compounding Companies

PS

8% 4%

P

9%

5 Manufacturing Companies 9 Compounding Companies3 Crackers

24%

15%

86%

39%

Sales

PPE

H

9

Classification: General Business Use

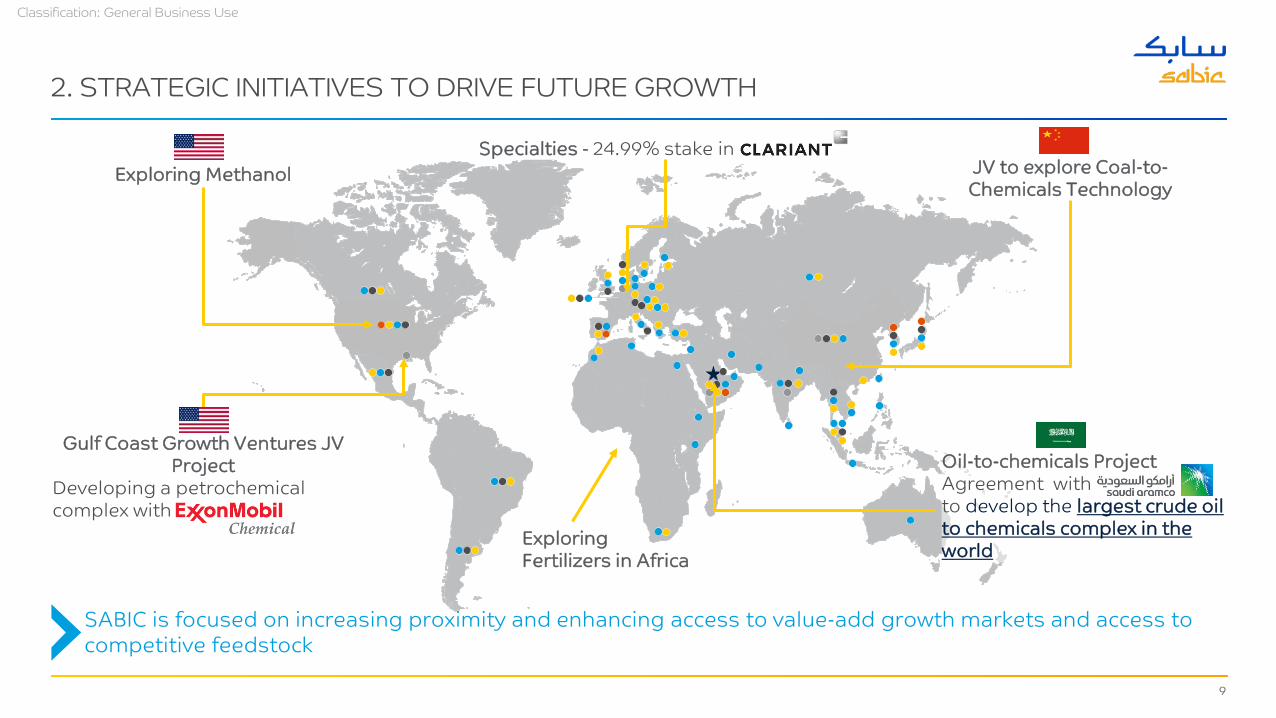

2. STRATEGIC INITIATIVES TO DRIVE FUTURE GROWTH

Oil-to-chemicals Project Agreement with Saudi Aramco to develop the largest crude oil to chemicals complex in the world

Exploring MethanolSpecialties - 24.99% stake in Clariant AG

JV to explore Coal-to-Chemicals Technology

Gulf Coast Growth Ventures JV Project

Developing a petrochemical complex with ExxonMobil Chemical Exploring

Fertilizers in Africa

SABIC is focused on increasing proximity and enhancing access to value-add growth markets and access to competitive feedstock

10

Classification: General Business Use

3. WORLD CLASS OPERATIONAL EXCELLENCE AND SUSTAINABLE PROGRESS

Source: 1 Gartner’s 2018 “Top 25 Supply-Chain Benchmarking”. Notes: 2 Changes in performance compared to 2010, 3 Environment, Health, Safety and Security (EHSS) rate is a severity-weighted rate that captures all EHSS incident types.

BUILDING SUSTAINABLE VALUE (FINANCIALLY AND NON-FINANCIALLY)

GREENHOUSE-GAS INTENSITY REDUCTION 2

9.3%

ENERGY-INTENSITY REDUCTION 2

7.6%

WATER INTENSITY REDUCTION 2

8.8%

MATERIAL-LOSS INTENSITY REDUCTION 2

35.2%

TOTAL CO2UTILIZATION in 2017 (MILLION METRIC TONS)

3.5mmt

FLARING REDUCTION 2

43%

EHSS RATE REDUCTION 2, 3

21%

STRONG FOCUS ON OPERATIONAL EXCELLENCE

• Maintain cost efficiency via global network of operations and assets with drive to be a first quartile producer

• Feedstock diversification, value chain integration and accessing competitive feedstocks globally

• Streamline operations by reducing the number of its SBUs from six to three – The metals SBU was integrated with the operating company Hadeed in 2017

• Top 3 - SABIC was ranked one of the top three companies for supply-chain excellence in the chemicals industry1

• Integration across supply chain network, logistics infrastructure, and business intelligence, delivering more than 28 mntonnes of product to nearly 20,000 destinations in more than 130 countries annually

• CO2 Purification plant capturing and purifying up to 500,000 Metric Tons of CO2 from the production of ethylene glycol every year

• Optimization and anti-coking technology saving 65,000 tonnes of feedstock

• Received UN’s first Clean Development Mechanism greenhouse-gas reduction credit in KSA

Operational Excellence Supply Chain Excellence Technology Improvements

REDUCTION IN RECORDABLE INCIDENT RATE 2

14%

11

Classification: General Business Use

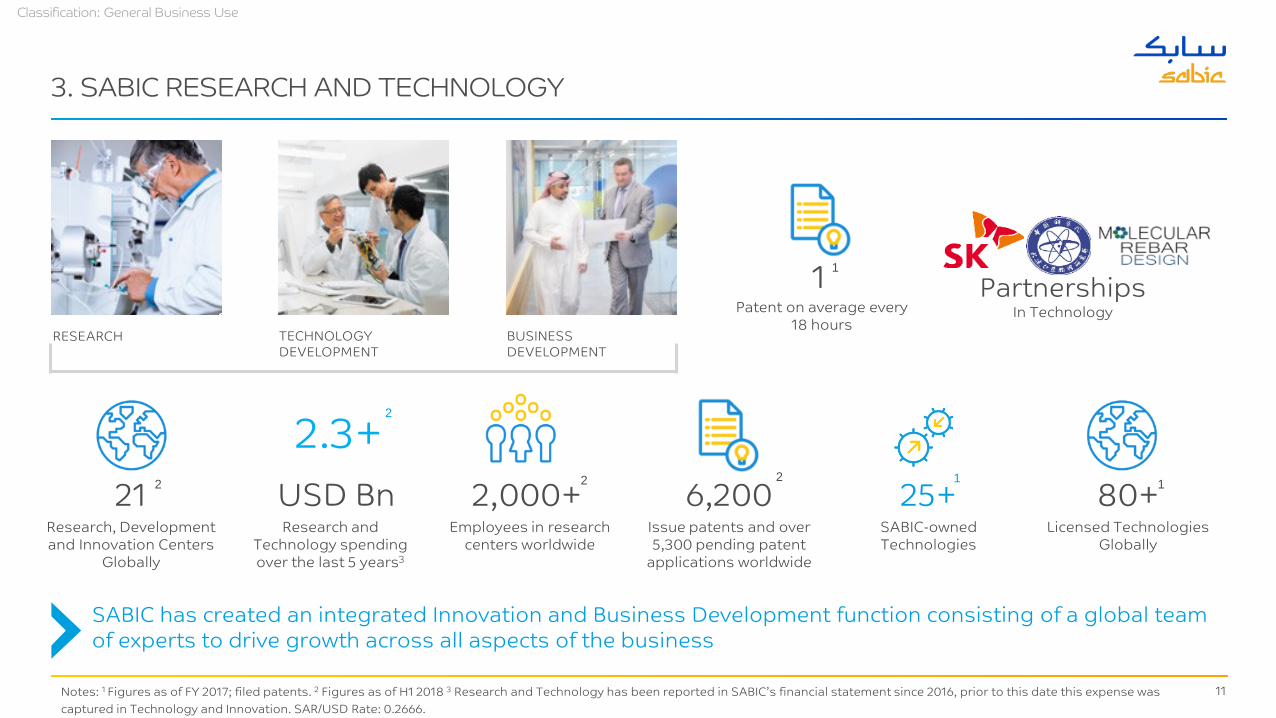

3. SABIC RESEARCH AND TECHNOLOGY

SABIC has created an integrated Innovation and Business Development function consisting of a global team of experts to drive growth across all aspects of the business

Notes: 1 Figures as of FY 2017; filed patents. 2 Figures as of H1 2018 3 Research and Technology has been reported in SABIC’s financial statement since 2016, prior to this date this expense was captured in Technology and Innovation. SAR/USD Rate: 0.2666.

PartnershipsIn Technology

RESEARCH TECHNOLOGY DEVELOPMENT

BUSINESS DEVELOPMENT

21Research, Development and Innovation Centers

Globally

1 Patent on average every

18 hours

USD BnResearch and

Technology spending over the last 5 years3

2,000+Employees in research

centers worldwide

6,200Issue patents and over 5,300 pending patent

applications worldwide

25+SABIC-owned Technologies

80+ Licensed Technologies

Globally

2.3+2 2 2 1

2

1

1

12

Classification: General Business Use

4. PARTNERSHIPS, THE CORNERSTONE OF SABIC’S BUSINESS GROWTH MODEL

PARTNERSHIP WITH BEST IN CLASS GLOBAL COMPANIES1

Notes: 1 Percentages represent direct SABIC’s ownership in the respective joint ventures.

Scientific Design50%

Kemya, Yanpet & GCGV

50%Cos-Mar

50%Ibn Zahr

80%

Ibn Sina50%

SAMAC50%

Chemtank75%

Sharq50%

SSTPC

50%

SSNC50%

PARTNERSHIP WITH UNIVERSITIES FOR R&D► SABIC values innovation, ingenuity and collaboration as core drivers of its business ► SABIC promotes these values through strategic agreements with premier global

research institutions ► To support our research, we have five key geographies with innovation hubs:

the Middle East, the USA, Europe, South Asia and North Asia

17 Global Universities

5 Technology

and Innovation

Hubs

11 Saudi Universities

SABIC has pioneered a culture of partnerships in its manufacturing and R&D activities

13

Classification: General Business Use

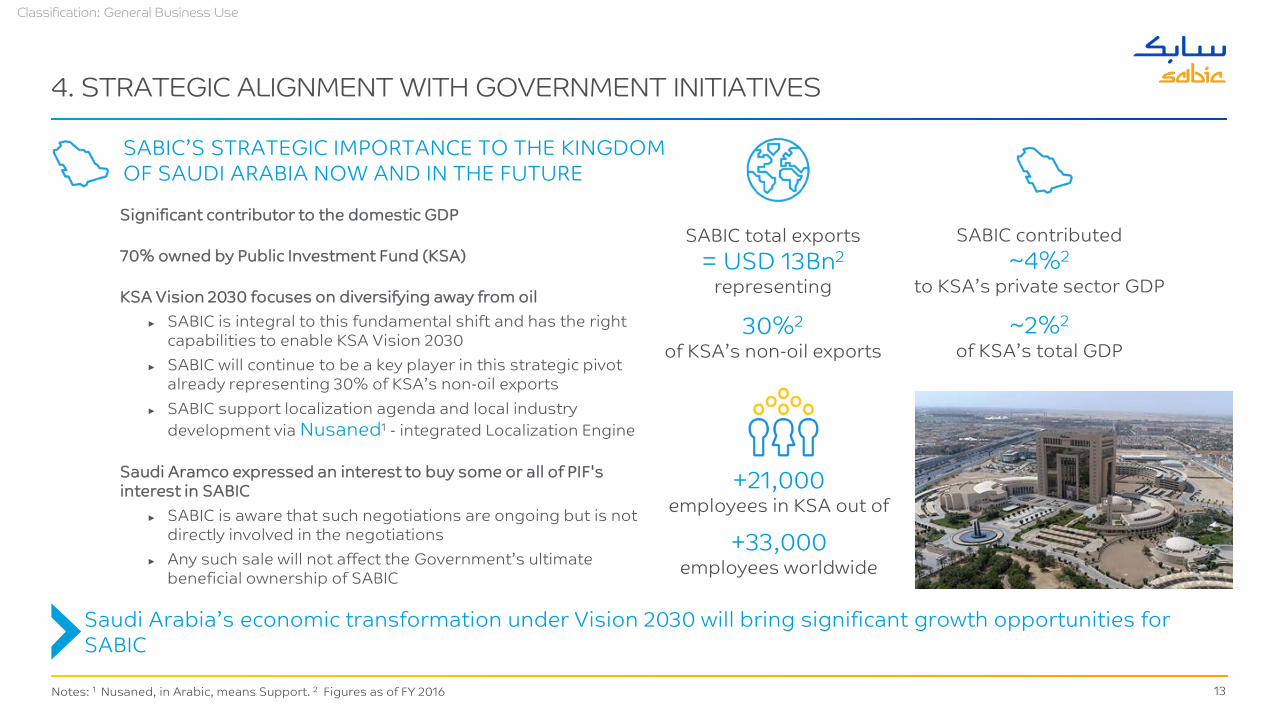

4. STRATEGIC ALIGNMENT WITH GOVERNMENT INITIATIVES

Significant contributor to the domestic GDP

70% owned by Public Investment Fund (KSA)

KSA Vision 2030 focuses on diversifying away from oil ► SABIC is integral to this fundamental shift and has the right

capabilities to enable KSA Vision 2030► SABIC will continue to be a key player in this strategic pivot

already representing 30% of KSA’s non-oil exports► SABIC support localization agenda and local industry

development via Nusaned1 - integrated Localization Engine

Saudi Aramco expressed an interest to buy some or all of PIF's interest in SABIC

► SABIC is aware that such negotiations are ongoing but is not directly involved in the negotiations

► Any such sale will not affect the Government’s ultimate beneficial ownership of SABIC

SABIC total exports= USD 13Bn2

representing

30%2

of KSA’s non-oil exports

SABIC contributed~4%2

to KSA’s private sector GDP

~2%2

of KSA’s total GDP

SABIC’S STRATEGIC IMPORTANCE TO THE KINGDOM OF SAUDI ARABIA NOW AND IN THE FUTURE

+21,000employees in KSA out of

+33,000employees worldwide

Notes: 1 Nusaned, in Arabic, means Support. 2 Figures as of FY 2016

Saudi Arabia’s economic transformation under Vision 2030 will bring significant growth opportunities for SABIC

14

Classification: General Business Use

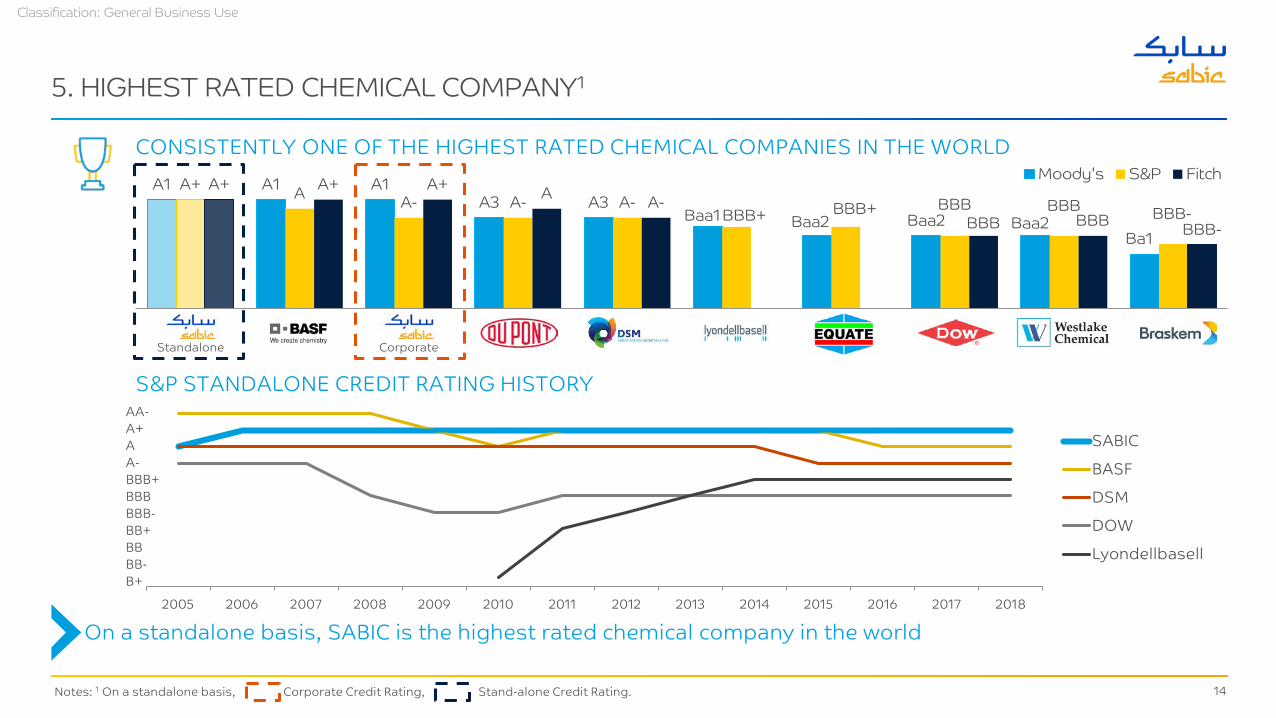

5. HIGHEST RATED CHEMICAL COMPANY1

A1 A1 A1A3 A3

Baa1 Baa2 Baa2 Baa2Ba1

A+ A A- A- A-BBB+ BBB+ BBB BBB BBB-

A+ A+ A+ A A-BBB BBB BBB-

SABIC SABIC DSM Equate Westlake

Moody's S&P FitchCONSISTENTLY ONE OF THE HIGHEST RATED CHEMICAL COMPANIES IN THE WORLD

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

SABIC

BASF

DSM

DOW

Lyondellbasell

AA-A+AA-BBB+BBBBBB-BB+BBBB-B+

S&P STANDALONE CREDIT RATING HISTORY

Notes: 1 On a standalone basis, Corporate Credit Rating, Stand-alone Credit Rating.

Standalone Corporate

On a standalone basis, SABIC is the highest rated chemical company in the world

15

Classification: General Business Use

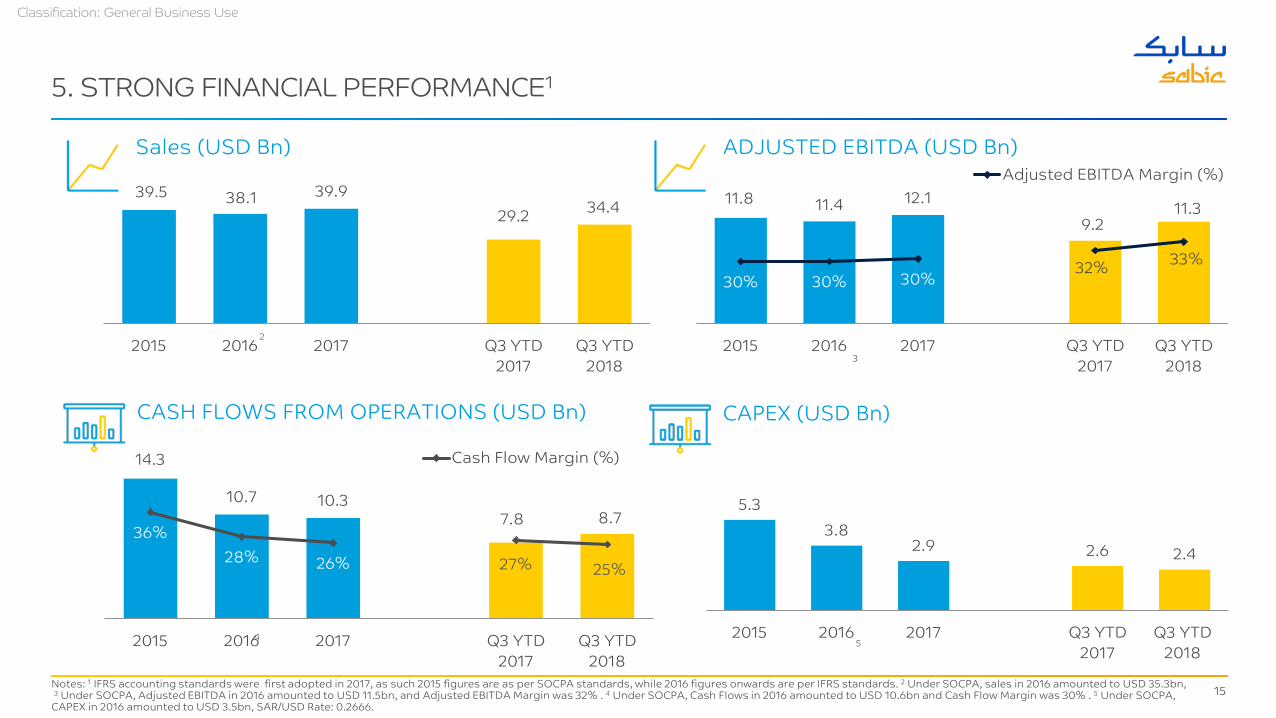

5. STRONG FINANCIAL PERFORMANCE1

Notes: 1 IFRS accounting standards were first adopted in 2017, as such 2015 figures are as per SOCPA standards, while 2016 figures onwards are per IFRS standards. 2 Under SOCPA, sales in 2016 amounted to USD 35.3bn,3 Under SOCPA, Adjusted EBITDA in 2016 amounted to USD 11.5bn, and Adjusted EBITDA Margin was 32% . 4 Under SOCPA, Cash Flows in 2016 amounted to USD 10.6bn and Cash Flow Margin was 30% . 5 Under SOCPA,

CAPEX in 2016 amounted to USD 3.5bn, SAR/USD Rate: 0.2666.

39.5 38.1 39.929.2 34.4

2015 2016 2017 Q3 YTD2017

Q3 YTD2018

Sales (USD Bn) ADJUSTED EBITDA (USD Bn)

11.8 11.4 12.19.2

11.3

30% 30% 30%32% 33%

2015 2016 2017 Q3 YTD2017

Q3 YTD2018

Adjusted EBITDA Margin (%)

14.3

10.7 10.37.8 8.7

36%28% 26% 27% 25%

0%

10%

20%

30%

40%

50%

60%

2015 2016 2017 Q3 YTD2017

Q3 YTD2018

Cash Flow Margin (%)

CASH FLOWS FROM OPERATIONS (USD Bn) CAPEX (USD Bn)

5.33.8

2.9 2.6 2.4

2015 2016 2017 Q3 YTD2017

Q3 YTD2018

2

3

45

16

Classification: General Business Use

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 2018

Crude Oil, Brent

Polyethylene (RHS)

EBITDA Margin (%)

Net Income Margin (%)

30%

28%

30% 30% 30%

13% 12%

13%16% 17%

33%

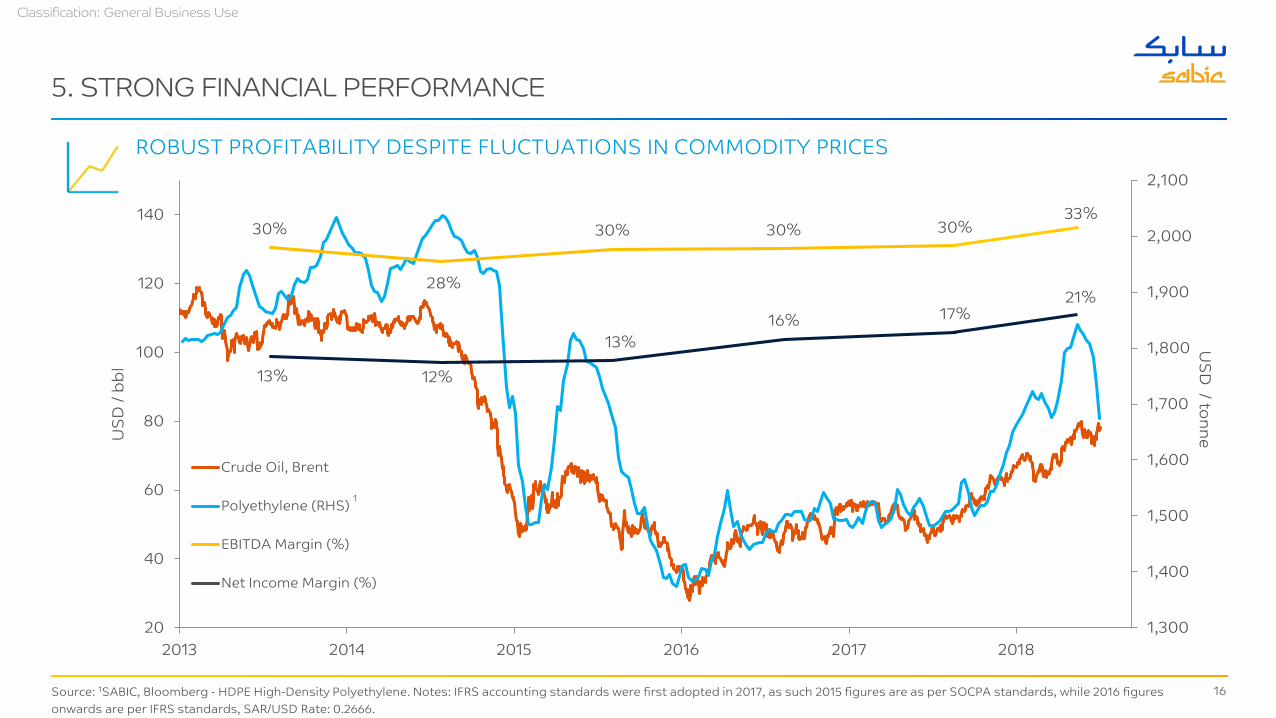

5. STRONG FINANCIAL PERFORMANCE

Source: 1SABIC, Bloomberg - HDPE High-Density Polyethylene. Notes: IFRS accounting standards were first adopted in 2017, as such 2015 figures are as per SOCPA standards, while 2016 figures onwards are per IFRS standards, SAR/USD Rate: 0.2666.

ROBUST PROFITABILITY DESPITE FLUCTUATIONS IN COMMODITY PRICESU

SD /

bbl

USD

/ tonne

1

21%

17

Classification: General Business Use

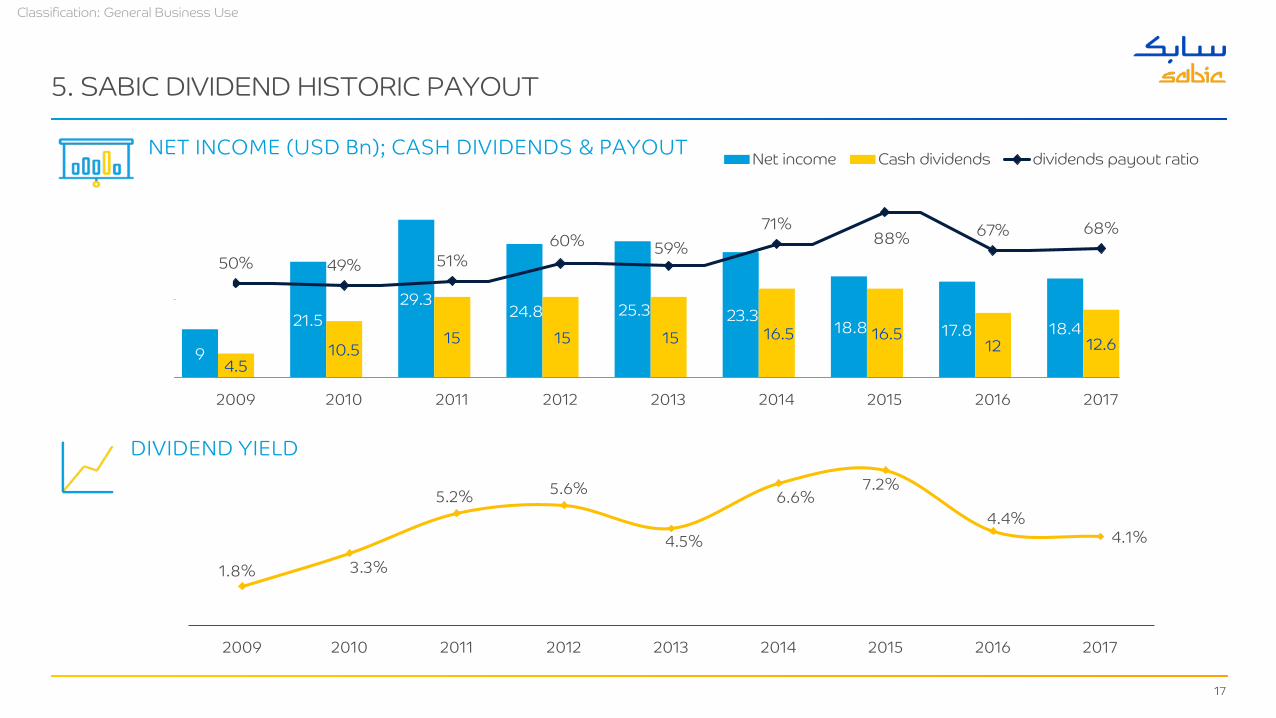

5. SABIC DIVIDEND HISTORIC PAYOUT

22

9

21.529.3

24.8 25.3 23.3 18.8 17.8 18.4

94.5

10.515 15 15 16.5 16.5

12 12.6

5

41%50% 49% 51%

60% 59%71%

88% 67% 68%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net income Cash dividends dividends payout ratio

1.8% 3.3%

5.2% 5.6%

4.5%

6.6%7.2%

4.4%4.1%

2009 2010 2011 2012 2013 2014 2015 2016 2017

DIVIDEND YIELD

NET INCOME (USD Bn); CASH DIVIDENDS & PAYOUT

18

Classification: General Business Use

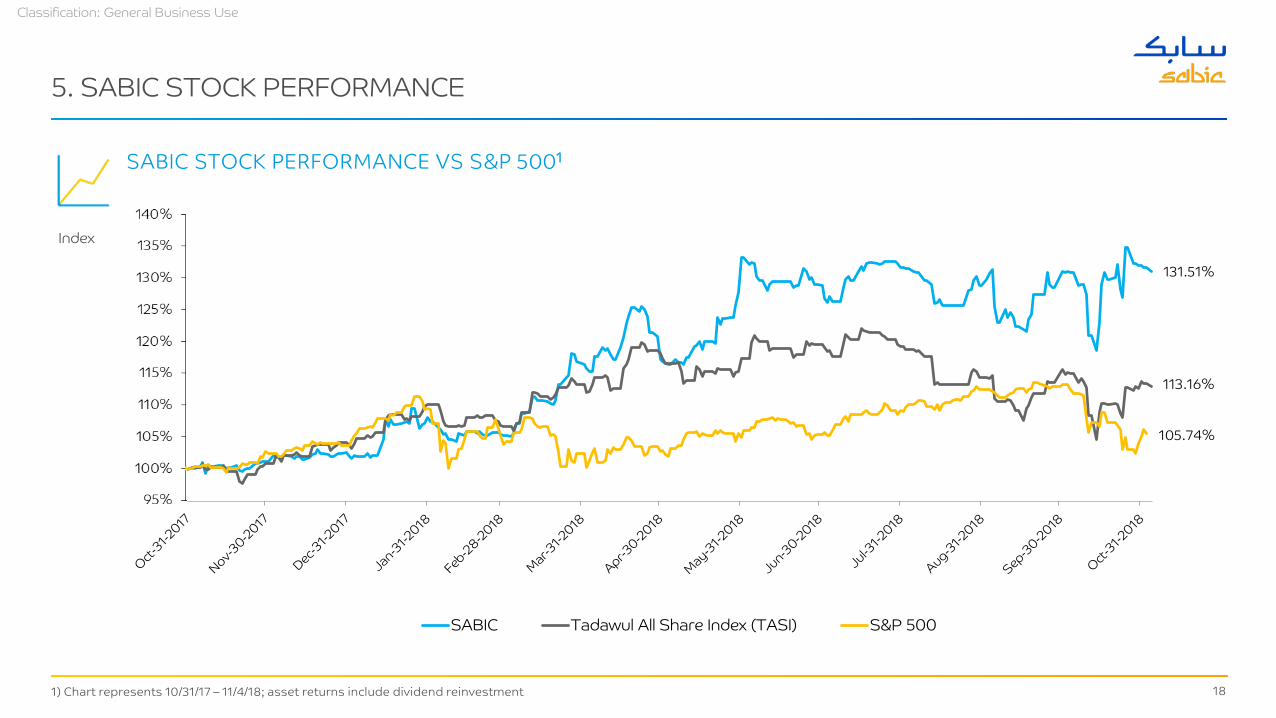

5. SABIC STOCK PERFORMANCE

1) Chart represents 10/31/17 – 11/4/18; asset returns include dividend reinvestment

SABIC STOCK PERFORMANCE VS S&P 5001

131.51%

105.74%

Index

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

SABIC Tadawul All Share Index (TASI) S&P 500

113.16%

19

Classification: General Business Use

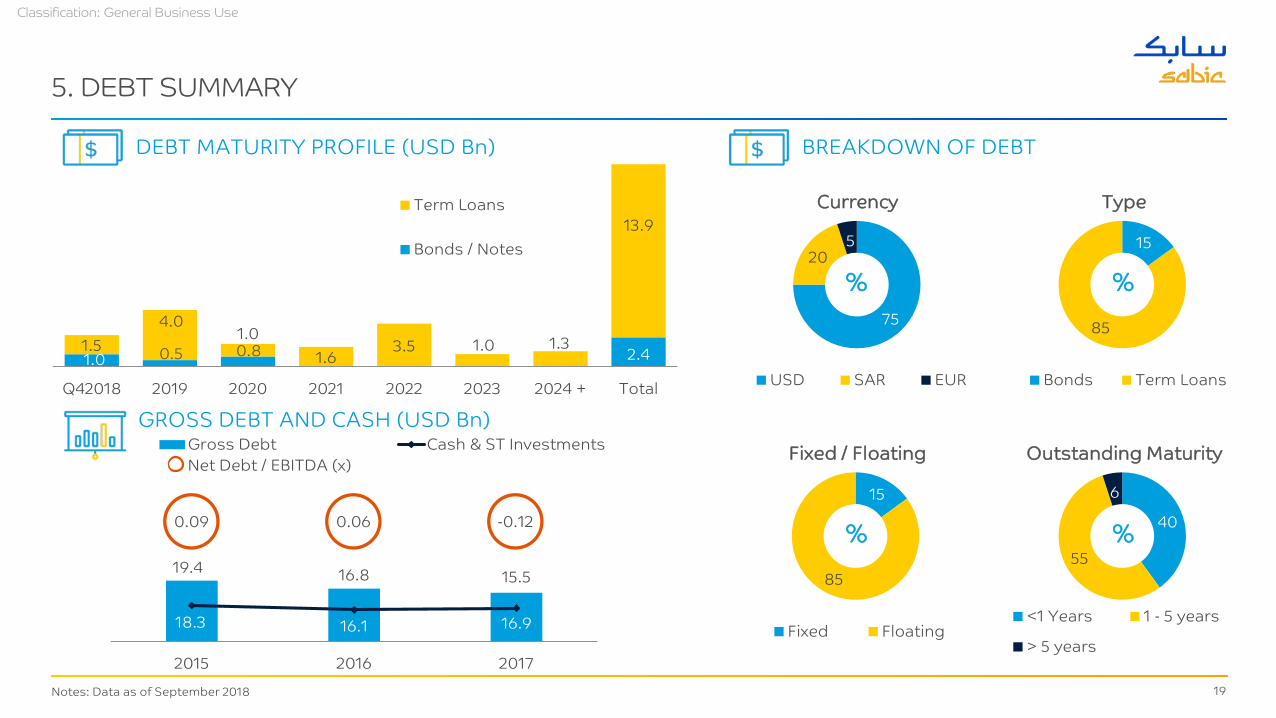

19.4 16.8 15.5

18.3 16.1 16.90.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2015 2016 2017

Gross Debt Cash & ST InvestmentsNet Debt / EBITDA (x)

5. DEBT SUMMARY

Type

15

85

Bonds Term Loans

%

Currency

75

205

USD SAR EUR

%

Fixed / Floating

15

85

Fixed Floating

%

Outstanding Maturity

40

55

6

<1 Years 1 - 5 years

> 5 years

%

DEBT MATURITY PROFILE (USD Bn)

Notes: Data as of September 2018

BREAKDOWN OF DEBT

GROSS DEBT AND CASH (USD Bn)

0.09 0.06 -0.12

1.0 0.5 0.8 2.41.54.0

1.01.6

3.5 1.0 1.3

13.9

Q42018 2019 2020 2021 2022 2023 2024 + Total

Term Loans

Bonds / Notes

20

Classification: General Business Use

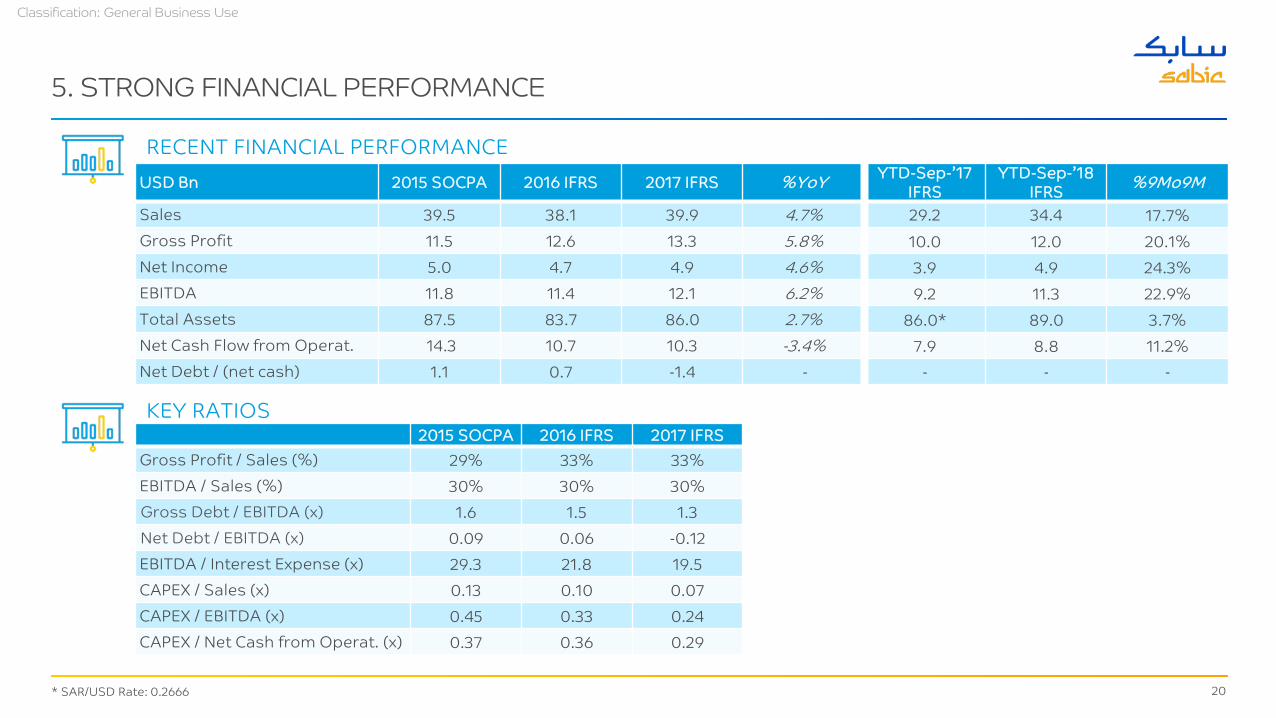

5. STRONG FINANCIAL PERFORMANCE

USD Bn 2015 SOCPA 2016 IFRS 2017 IFRS %YoY YTD-Sep-’17IFRS

YTD-Sep-’18IFRS %9Mo9M

Sales 39.5 38.1 39.9 4.7% 29.2 34.4 17.7%Gross Profit 11.5 12.6 13.3 5.8% 10.0 12.0 20.1%Net Income 5.0 4.7 4.9 4.6% 3.9 4.9 24.3%EBITDA 11.8 11.4 12.1 6.2% 9.2 11.3 22.9%Total Assets 87.5 83.7 86.0 2.7% 86.0* 89.0 3.7%Net Cash Flow from Operat. 14.3 10.7 10.3 -3.4% 7.9 8.8 11.2%Net Debt / (net cash) 1.1 0.7 -1.4 - - - -

* SAR/USD Rate: 0.2666

2015 SOCPA 2016 IFRS 2017 IFRSGross Profit / Sales (%) 29% 33% 33%EBITDA / Sales (%) 30% 30% 30%Gross Debt / EBITDA (x) 1.6 1.5 1.3Net Debt / EBITDA (x) 0.09 0.06 -0.12EBITDA / Interest Expense (x) 29.3 21.8 19.5CAPEX / Sales (x) 0.13 0.10 0.07CAPEX / EBITDA (x) 0.45 0.33 0.24CAPEX / Net Cash from Operat. (x) 0.37 0.36 0.29

RECENT FINANCIAL PERFORMANCE

KEY RATIOS

21

Classification: General Business Use

KEY HIGHLIGHTS

1. Market Leader in Multiple Products and Segments

2. Diversified Global Footprint

3. Cost Leadership and Operational Excellence

4. Strategic, Strong and Stable Alliances

5. Robust Financial Profile, Dividend and Stock Performance

THANK YOU