Investor Presentation - s3.amazonaws.com€¦ · This presentation (and oral statements...

43

Investor Presentation February / March, 2018 NYSE: PWR

Investor Presentation - s3.amazonaws.com€¦ · This presentation (and oral statements regardingthe subject matter ... Recognized market leader in electric power and oil and gas

This presentation (and oral statements regarding the subject matter of this presentation) includes forward-looking statements intended to qualifyunder the ldquosafe harborrdquo from liability established by the Private Securities Litigation Reform Act of 1995 These forward-looking statements includeany statements reflecting Quantas expectations intentions strategies assumptions or beliefs about future events or performance or that do notsolely relate to historical or current facts Forward-looking statements involve certain risks uncertainties and assumptions that are difficult topredict or beyond Quantas control and actual results may differ materially from those expected implied or forecasted by our forward-lookingstatements due to inaccurate assumptions and known and unknown risk and uncertainties For additional information concerning some of therisks uncertainties and assumptions that could affect our forward-looking statements please refer to Quantarsquos Annual Report on Form 10-K for theyear ended December 31 2017 and its other documents filed with the Securities and Exchange Commission as well as the risks uncertainties andassumptions identified in this presentation Investors and analysts should not place undue reliance on Quantarsquos forward-looking statements whichare current only as of the date of this presentation Quanta does not undertake and expressly disclaims any obligation to update or revise anyforward-looking statements to reflect events or circumstances after the date of this presentation or otherwise and Quanta expressly disclaims anywritten or oral statements made by any third party regarding the subject matter of this presentation

Forward Looking Statement Disclaimer

Page 2

Page 3

Key Takeaways

Quanta is the leading construction-led infrastructure solutions provider in the markets we serve with unmatched scope and scale

Quanta continues to see opportunities to increase shareholder value through growth in revenues and EPS over a multi-year period

Quantarsquos corporate actions demonstrate confidence in our long-term growth prospects and a commitment to generating shareholder value

We will maintain a strong financial profile to support our strategic initiatives for near- and long-term profitable growth

Page 4

Leading Construction-Led Infrastructure Solutions Provider

Who is Quanta Services Committed to the health and safety of our employees customers and community

Recognized market leader in electric power and oil and gas pipeline construction in North America

Entrepreneurial business model and culture

Broad self-performing platform developed through organic growth and acquisitions

Strong scope and scale with deep customer relationships

Revenue as reported by type of work geography contract and project type based on revenues of $9466 million for the twelve months ended Dec 31 2017 Represents the midpoint of guidance range

Estimated Revenue by Geography

United States74

LATAM amp Other2

Canada21

Australia3

Page 6

Overview ndash Diverse and High Quality Customer Base

Top 10

36

9 No single customer accounted formore than 9 of revenues in 2017

The ten largest customers accountedfor approximately 36 of revenues in2017

Strong relationships with the majorityof US investor owned utilities and Canadian utilities ndash many going backfor decades

Quantarsquos Low Customer Concentration Is Unique Versus Peers

Page 7

Leading Construction-Led Infrastructure Solutions Provider

bull Grow the ldquobase businessrdquo and compliment with larger scale projects

bull Organic growth and strategic acquisitions

bull Pricing discipline and risk management

bull Focus on safe executionbull Cost managementbull Maintain financial strength

Time

Reve

nues

Coupled with Successful Implementation of Other Strategic Imperatives hellip

Larger Projects

For illustrative purposes

Page 10

Strategic Acquisitions ndash Criteria and Rationale

Acquisition Strategic Rationale

bull Seek well respected entrepreneurial leadership with extensive history of operational excellencebull Only interested in companies that bring strategic value to Quanta and provide opportunity for 1+1=3 growth

opportunity over time

bull Brings leadership position in new geographybull Enhances presence and capabilities in an existing

geographybull Brings or enhances customer relationshipsbull Brings leadership position in adjacent or new

marketbull Brings unique service or technology that Quanta

can leverage to further differentiate its turnkey solution offering

Typical Deal Terms

bull Target 4x-5x EBITDA multiplebull 40 of consideration in Quanta stock 60 of

consideration in cashbull Meaningful stock component for operational and

stakeholder alignment

bull Company leadership stays on to run the businessbull Non-compete agreementsbull Stock locked up for period of time

Acquisitions Have and Will Continue to Play A Strategic Role in Differentiating Quanta in the Marketplace and Positioning the Company for Profitable Long-Term Growth

Page 11

Differentiated Competitive Position ndash In the Sweet Spot

bull Quanta is the leading and largest construction-led infrastructure solutions provider in North America

bull Unmatched scope providing broader solutions to customersbull Unmatched scale as the largest employer of skilled workforce

in the industry ndash more than 33000 employeesbull Track record of safe executionbull Projects are getting larger and more complex customers

increasingly seeking cost certainty and performancebull Quanta has consistently been working on numerous large

projects simultaneously for the past + six yearsbull Significant revenues from strategic relationships recurring work

and an increasing amount of negotiated work

Quanta vs Specialty Contractors Quanta vs Traditional EampCs

bull Today our customers believe skilled construction labor is a finite resource and critical to overall project success where engineering and procurement are more commoditized

bull Quanta is construction-led and self-performs its projects ndashcontrols quality and execution

bull EampCs typically provide project management oversight and have limited self-perform construction capabilities

bull Quanta derives significant revenues from strategic relationships recurring work and an increasing amount of negotiated work

bull Price is often the primary driver of who wins EampC projects

Est Large Project Capability

Bubble Size = Avg Market Cap

0

20

40

60

80

100

Est

Self

Perf

orm

Cap

abili

ty

Bubble Size = Avg Market Cap

LargerSmallerLargerSmaller

Est

Self

Perf

orm

Cap

abili

ty

Est Large Project Capability

Page 12

Differentiated Competitive Position ndash In the Sweet Spotbull Quanta is construction-led and is uniquely

positioned to meet customer needs versus both specialty contractors and traditional engineering and construction companies

bull Customers understand that skilled labor is critical to project success

bull Projects are getting larger and more complex and customers are increasingly seeking comprehensive solutions

bull Demand for specialty construction resources is high and increasing but supply is limited

bull Quanta has the largest infrastructure specialty workforce in North America +33000 employees globally

bull Quanta has strategically invested in engineering and program management to provide true complete engineering procurement and construction (EPC) solutions

0

20

40

60

80

100

Est

Self

Perf

orm

Cap

abili

ty

Est Large Project Capability

Bubble Size = Avg Market Cap

LargerSmaller

Page 13

Electric Power Infrastructure Services Segment Overview

$5303$4937 $4850

$5600

107

75 8393

2014 2015 2016 2017

Revenue Op Margin

(2)

(1) Operating margin excludes a $1025 million charge to cost of services for long-term contract receivable in 2014 Refer to appendix for non-GAAP reconciliation(2) Excludes a $66 million property and equipment charge in 2015 and a $57 million asset impairment charge in 2016 Includes the impact of $661 million in 2015 and $548 million in 2016 of project losses Refer to appendix for non-GAAP reconciliation

Financial SnapshotFor the years ended Dec 31 ($ in millions)

$3395 $3308 $3369$4032

$6716 $6313 $6658$7359

2014 2015 2016 2017

12-Mth Backlog Total Backlog

(2)

(1)

Differentiatorsbull Largest TampD solutions provider in

North Americabull Reputation and Track Recordbull Unmatched Solutions Scope and

Scalebull Safety Recordbull Manpower and Equipment

Resourcesbull Northwest Lineman College (NLC)bull Lazy Q Training Facility amp other

industry leading training initiativesbull Energized Servicesbull EPC Capabilities Across All Offeringsbull Infrastructure Capital Solutions

Page 14

Power Grid Investment Drivers ndash Transmission amp Distribution

Market Drivers

bull An aging grid that requires repair upgrade and maintenancebull Utility spending continues to shift from generation to

transmission and distributionbull Favorable transmission regulation Energy Policy Act of lsquo05

NERC Reliability Standards possibly FERC Order 1000 over the long-term

bull More stringent reliability standards will require repairing lines and adding redundant capacity

bull Regional grid infrastructure is too congested to get lowest-cost power to consumers

bull Coal and nuclear generation retirements and switching to natural gas and renewable generation strains the grid

bull Existing and new renewable generation needs interconnection to the grid

bull Renewed distribution focus on reliability versus costsbull System hardening initiatives particularly in areas hard hit by

severe weather

bull Challenged economic conditions in Canada

bull Environmental and other regulatory scrutiny right of way acquisition permitting etc

bull Tepid load growthbull Economybull Energy efficiency initiatives

bull State renewable portfolio standards being evaluated in some states

bull Transmission ROE challenges due to low interest rate environment

bull Distribution returns lower than FERC transmission returnsbull Regulatory and consumer pressures on utilities against rising

power bills

Restraining Factors

$0$5

$10$15$20$25$30$35$40$45

Avg08-11

Avg12-15

16 17 18 19 20 21 22

2015 Est 2016 Est 2017 Est

Page 15

Power Grid Investment Drivers ndash Transmission amp Distribution

$0

$5

$10

$15

$20

$25

$30

$35

Avg08-11

Avg12-15

16 17 18 19 20 21 22

2015 Est 2016 Est 2017 Est

bull Utility spending continues to shift from generation to transmission and distribution

bull Transmission and distribution spending continues to reach all time highs and forecasts point towards sustained robust spending

bull Previously delayed larger transmission projects are expected to move forward over next several years

Source The C3 Group 2017

Est North American Transmission SpendingOut-year estimates tend tohave upward revision bias

Billi

ons

Billi

ons

Est North American Distribution CapExOut-year estimates tend tohave upward revision bias

bull Sub-transmission interconnection

bull Technology innovations will continue to grow A focus on upgrades to modernize the grid will overlap with spending needed to address aging infrastructure

bull Opportunity for industrial driven load growth and overall load growth asif economic growth increases

bull Northwest Lineman College (NLC) is a for profit nationally accredited and industry leading training program providing safety and certification training to pre-apprentices apprentices journey level lineworkers crew leaders substation technicians and system operators NLC was founded in 1993 NLC has four campuses across the US (Idaho California Florida and Texas)

Overview

bull Tight labor market for lineman and other skilled employees Recruiting training and maintaining people is critical for us and for our customers

bull NLCrsquos world class program should elevate and expedite Quantarsquos training and development efforts which will benefit our customers the industry and Quanta

bull Developing curricula for communications and natural gas distribution services Ability to develop other curricula for services Quanta provides

bull Complements Quantarsquos other initiatives underway to address workforce needs

bull Lazy Q Training Facilitybull Veteran Recruiting and Developmentbull Quanta-Sam Houston State University Partnership

Strategic Rationale

Page 17

Oil amp Gas Infrastructure Services Segment Overview

$2445 $2635 $2801

$3867

83

54 53 48

2014 2015 2016 2017Revenue Op Margin

(1) Excludes a $388 million expense associated with an arbitration decision Refer to appendix for non-GAAP reconciliation(2) Includes $73 million of project losses(3) Includes a $19 million charge to expense associated with a construction barge

Financial SnapshotFor the years ended Dec 31 ($ in millions)

$1825 $1901$2484 $2414$2521

$3074 $3092

$3819

2014 2015 2016 2017

12-Mth Backlog Total Backlog

(2)

(1)

Differentiatorsbull Largest Pipeline Solutions Provider

in North Americabull Reputation amp Track Recordbull Safe Project Executionbull Turnkey Solutionsbull EPC Capabilitiesbull Critical Path Industrial Servicesbull In-House Mechanized Weldingbull In-House Pigging Technologybull Pipe Logistics Managementbull Infrastructure Capital Solutions

(3)

Page 18

Oil amp Gas Infrastructure Investment Drivers

bull Production of shale natural gas oil and natural gas liquids has grown dramatically and is expected to remain at high levels forthe foreseeable future

bull Much of these resources are in areas that have not been traditional hydrocarbon fuel sources and do not have adequate infrastructure in place to gather store process and transport product

bull Canadian oil production lacks adequate takeaway pipeline infrastructurebull Economics of pipeline transportation is increasingly attractive versus rail in a lower oil price environmentbull Pipeline construction capacity is more limited in Canada versus the US and construction capacity constraints could be significant

bull It will take many years and significant energy infrastructure investment to harvest these resources

Shale Gas amp Tight Oil Plays Drive US Natural Gas Production

2000-2040 (trillion cubic feet)

Source EIA Annual Energy Outlook 2017

Tight Oil Drives US Oil Production2000-2040 (millions of barrels per day)

Source EIA Annual Energy Outlook 2017

Canadian Oil Sands amp Conventional Oil Production(Millions of barrels per day)

Source Canadian Assoc of Petroleum Producers

Page 19

Oil amp Gas Infrastructure Investment Drivers

bull Need for pipeline and related infrastructure driven by the significant increase in North American unconventional natural gas and oil production ndash not commodity prices

bull Takeaway pipelines have not been built fast enough to keep pace with hydrocarbon production ndash significant pipeline development needed

bull Large pipeline construction industry capacity is currently tight but could get significantly strained over the next several years

North American Pipeline ForecastProbability Weighted

bull Quanta is the largest pipeline construction company in North America

bull This positions Quanta to provide significant large diameter pipe construction capacity to the industry while remaining active in select shales

bull We are ready to assist our customers in meeting their development goals in what could be a resource challenged environment

In B

illio

ns

Quanta Is the Largest Pipeline Construction Company in North America

Stifel expects upward revisions to Tier 1 amp 2 projects in out years

x Tier 1 amp 2

x Tier 3 amp Potential

Page 20

Oil amp Gas Infrastructure Investment Drivers

Natural Gas Distribution amp Pipeline Integritybull US pipeline infrastructure is getting older and much of it was

installed before 1970bull Local Distribution Companies (LDCs) increasing spend on pipe

inspection and replacementbull Regulations push expanding inspection programs and

accelerating distribution pipeline replacement work bull Long timelines for some replacement plans (decades) will push

spend accelerationbull State regulators establishing cost recovery mechanisms to

accelerate replacement programs

Significant Inventory Remains for Replacement

Diversified and Expanding Solutions to Capture Midstream and Downstream Industry Spend

Downstream Industrial Services

Projected North American Downstream MaintenanceSpending 2017 ndash 2021 ~ $113 Billion

Refinery34

PetChem42

Gas Proc16

LNG8

Source Douglas-Westwood

bull Substantial installed base of industrial facilities operating in a highly corrosive environment

bull As plants age critical process unitsrsquo risk of failure increases significantly requiring consistent and recurring maintenance investment

bull Deferrals and other factors yield expectations for significant turnaround season over coming years ndash reversion to mean activity levels

bull Stronghold gives Quanta a significant presence in downstream services and a strong platform for growth

Page 21

Telecom Infrastructure Services Overview

To be an industry leading and true EPC contractor providing comprehensive communications infrastructure solutions to customers in the United States Canada and select markets in Latin America

Goal

Diverse Existing amp Target Customer BaseMarkets Served

Page 22

Telecom Infrastructure Investment Drivers

bull Telco gigabit fiber to the home deployment programs

bull Cable MSOs deploying DOCSIS 31

bull Upcoming - 5G wireless and fiber backhaul

bull Ongoing 4G wireless network optimization

bull Connect America Fund - rural fiber build-out

bull Federal government funded FirstNet - national wireless network for first responders

United States

bull Backbone and last mile fiber (behind relative to the US)

bull Telco gigabit fiber to the home deployment programs

bull Cable MSOs deploying DOCSIS 31

bull Upcoming - 5G wireless and fiber backhaul

bull Ongoing 4G wireless network optimization

bull Federal government infrastructure initiatives generally positive

Canada

bull Significantly behind North America in both wireline and wireless connectivity

bull However demand for connectivity media and data intensive services is strong

bull Fiber and backhaul networks significantly behind North America

bull Primarily 3G wireless some 4G wireless (country dependent)

bull Various governments have infrastructure expansion initiatives

bull Concession and P3 opportunities

bull Connectivity for quality of life social and commercial reasons

Latin America

Geographic Diversity Provides Exposure to Multiple Market Drivers

Page 23

Telecom Infrastructure Services Overview

Fiber Builds

Wireless Deployment

Make Ready Services

Civil Construction

Engineering Design

Material Management

EPC

Wireless Wireline

United States

Wireless Wireline

Canada

Wireless Wireline

Latin America

Quantarsquos Capabilities

= Current Service= In Development

Comprehensive Infrastructure Solutions Offered On A Turnkey Discrete Service or EPC Basis

bull Proven greenfield expansion model in Latin America ndash US should be less difficult

Leverage existing US field operations people equipment and property

bull Select strategic acquisitions may play a role but NOT a roll-up approach

Provide wireline and wireless services - heavier on wireline

bull Increasing convergence of wireless and wireline due fiber requirements of both

Project centric nimble approach versus MSA focused EPC services to differentiate

bull Less capital intensive with better margin opportunity

GOAL

STRATEGY

STRATEGY

STRATEGY

STRATEGY

To be the leading communications infrastructure solutions provider in the markets we serve

Page 25

Engineer Procure Construct (EPC) Is A Differentiatorbull Quanta has a long history in the EPC business and is increasingly performing select projects on an EPC basisbull Customersrsquo capital programs are at historic levels and growing Projects are getting larger and more complexbull Evolution of regulatory demands competition and alternative pricing models

bull Many customers have limited internal resources and expertise to manage these dynamics and are turning to Quanta for solutions

bull Project cost certainty becoming increasingly important

bull We are enhancing initiatives to ensure we have a scalable comprehensive enterprise-wide capability for EPC projects that is consistently executed across all segments and geographies

bull EPC projects are a meaningful contributor to our current backlog and provide significant opportunity for future growth

Integrated Services

Construction amp Installation

Assessment Planning amp

Development

Engineering amp Design

Procurement Operation and Maintenance

Page 26

What is Infrastructure Solutions

Infrastructure Solutions Represent Strategic Partnerships with Customers and Capital Partners

bull Public private partnerships (P3)bull Concessionsbull Build Own Operate or Transfer (BOOT)bull Build to Suit (BTS) arrangements

These solutions are a growth engine for each of our segments and geographies and a core component of our strategic imperative to deliver differentiated solutions to

our customers

Encompasses

Page 27

Infrastructure Solutions Drivers

bull Provide transparency to a project shape design constructability risk allocation and overall project structure

bull Manages risk that yields more informed EPC project decisions

bull Improves success rate of both winning the engagement and successful execution

bull Where appropriate we invest alongside our partners

bull Significant capital needs to fund substantial infrastructure needs

bull Utilization of concessions public private partnerships (P3) and private infrastructure partnerships to fund and attract high-quality entities for complex projects

bull Changes in regulation (such as FERC Order 1000)

bull New entrants together with high interest and availability of investor infrastructure investment capital

Quanta Is A True Partner

bull Quanta increasingly sought as a partner for our execution capabilities the need for price certainty and our financial strength

bull Projects are larger more complex greater scope Typically under lump-sum turnkey arrangements which create greater opportunities and risks for Quanta

bull Successful Infrastructure Solutions and project execution track record

Quanta Sought for Executionamp Track Record

Market Structure amp Projects Getting More Complex

A Combination of Drivers are Occurring that Create Demand and Opportunity for Our Infrastructure Solutions

Page 28

Fully Integrated Solutions Based Provider

Capitalbull Determine capital structurebull Source capitalbull Quanta minority direct

investmentbull First Infrastructure Capital

Advisors

PartnershipsPartner withbull Customersbull Equity Capital

(3) Negatively impacted by project losses of $734 million ($473 million net of tax) or $021 per diluted share primarily related to an individual power plant project

$7651

(4) Negatively impacted by project losses of $548 million ($334 million net of tax) or $024 per diluted share related to an individual power plant project

Strong Revenue and Earnings Per Share Recovery

$10000

$2445$2635

$2801

$3867

83

54 5348

2014 2015 2016 2017 2018 EstRevenue Op Margin

(4)

(5)(4)

(5)(6)

Page 31

Recent Financial Performance amp 2017 ExpectationsFor the Years Ended December 31

($ in millions)Electric Power

$5303

$4937 $4850

$5600

107

7583

93

2014 2015 2016 2017 2018 Est

Revenue Op Margin(1) Operating margin excludes a $1025 million charge to cost of services for long-term contract receivable in 2014 Refer to appendix for non-GAAP reconciliation(2) Excludes a $66 million property and equipment impairment charge Includes the impact of $661 million of project losses Refer to appendix for non-GAAP reconciliation(3) Excludes a $57 million asset impairment charge Includes the impact of $548 million of project losses Refer to appendix for non-GAAP reconciliation

(1)

(2)(3)

f Est $58 - $60 Billion

Est operating incomemargins of 925 to 98

Guidance Commentary($ in millions)

Oil amp Gas Infrastructure

(4) Excludes a $388 million expense associated with an arbitration decision Refer to appendix for non-GAAP reconciliation(5) Includes $73 million of project losses(6) Includes a $19 million charge to expense associated with a construction barge

Est revenue growth at high-end of approx 10 vs 2017

Positive Industry Trends amp Competitive Positioning Provide Opportunity for Backlog Growth

Page 33

Strong Balance Sheet to Support Growth Strategies

$191 $129 $112 $138

$920 $1036 $1153$729

123114 123115 123116 12312017

Cash Credit Facility (Unused)

($ in millions) 12312014 12312015 12312016 12312017

Cash and Equivalents $ 191 $ 129 $ 112 $ 138

Other Debt 12 15 10 4

Credit Facility 69 467 351 668

Total Debt 81 482 361 672

Total Equity 4526 3088 3343 3796

Total Capitalization $ 4607 $ 3570 $ 3704 $ 4468

($ in millions)Liquidity

$1111 $1165 $1265

$867

Liquidity includes cash and cash equivalents and availability under our revolving credit facility as described in our Form 10k

Page 34

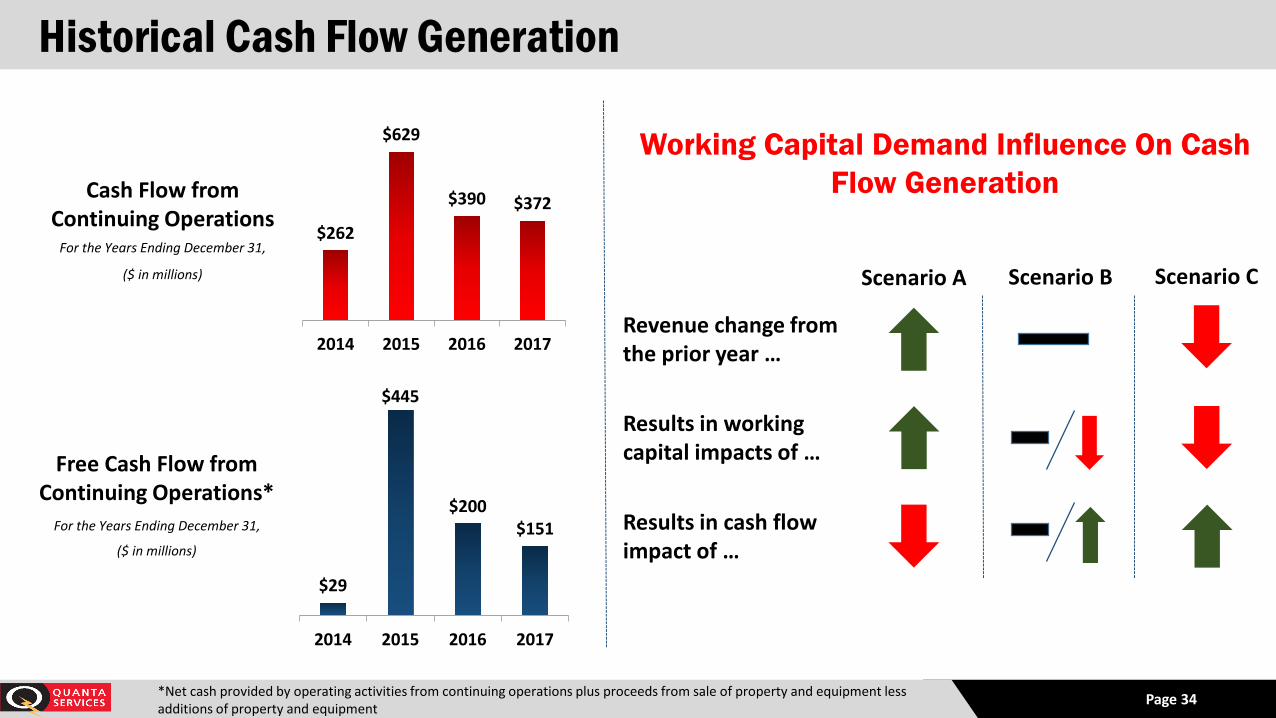

Historical Cash Flow Generation

$29

$445

$200$151

2014 2015 2016 2017

Cash Flow from Continuing Operations

$262

$629

$390 $372

2014 2015 2016 2017

Net cash provided by operating activities from continuing operations plus proceeds from sale of property and equipment less additions of property and equipment

($ in millions)

For the Years Ending December 31

Working Capital Demand Influence On Cash Flow Generation

completed in April 2016bull Acquired 351 million shares at $2136 per share

bull $500 million for opportunistic repurchases through Feb 28 2017bull Acquired $450 million 192 million shares retired

Completed - $500 Million Share Repurchase Authorization (2015)bull Acquired approximately 174 million shares for total cost of $500

million

$2197

$1593

0

25

50

75

100

125

150

175

200

225

$0000

$500000

$1000000

$1500000

$2000000

$2500000

$3000000

2014 2018E

Net Income Required to Generate $001 In EPS

Avg Dil Shs Out

Earnings Power Improvement

$ in

Tho

usan

ds

Shares in Millions

Announced (May 2017) - New $300 Million Share Repurchase Authorization through June 30 2020bull Have acquired 14 million shares for $500 million as of Feb 22 2018

Reflects Confidence and Commitment to Generating Stockholder Value

Page 36

Opportunistic amp Disciplined Capital Allocation

Capital Deployment Preference(Amounts in millions)

bull Working Capitalbull Capital Expendituresbull Acquisitionsbull Investmentsbull Return of Capital

bull Generally in sync with preference however hellip

bull Financial strength provides the ability to be opportunistic

bull Flexible and strategic capital allocation is a competitive advantage

Capital Deployment Posture

2014 ndash 2017 Sources amp Uses of Cash

Sources

Cash Flow fromOperations

DivestitureProceeds

Borrowings

$3172

$1653

$842

$677

Uses

StockRepurchase

CAPEX amp OtherNet

Acquisitions Net

Other

$1750

$828

$805

$140$3523

52

27

21

50

24

23

3

Amounts reflect the retrospective application of a recent accounting pronouncement related to the classification of tax withholding payments for share-based compensation

Financial Strength Allows for Flexible and Strategic Capital Allocation ndash A Competitive Advantage

Page 37

Strong Foundation For Growth amp Improved Profitability

Multi-Year Growth Opportunities

Innovative Industry Leading Solutions

Scale amp Scope

Financial Strength

Safety amp Operational Excellence

Page 38

QuantaServicesIR

QuantaIR

Connect With Quanta Services Investor Relations

Corporate Office2800 Post Oak Blvd Suite 2600Houston TX 77056713-629-7600wwwquantaservicescom

Investor ContactKip Rupp CFAVice President ndash Investor Relations713-341-7260investorsquantaservicescom

Page 39

Reconciliation of Adjusted Net Income from Continuing Operations Attributable to Common Stock

2014 2015 2016 2017 2018 2018Reconciliation of adjusted net income from continuing operations attributable to common stockNet income from continuing operations attributable to common stock (GAAP as reported) 269224$ 120286$ 198725$ 314978$ 310000$ 374000$ Adjustments

Asset impairment charges - 58451 7964 58057 - -Severance and restructuring charges - - 6352 - - -Acquisition and integration costs 14754 7966 3053 10579 6600 6600 Impact of Tax Cut and Jobs Act - - - (70129) Tax benefits primarily related to entity restructuring and recapitalization efforts - - - (18224) Impact of income tax contingency releases (8099) - (20488) (7223) - -Change in fair value of contingent consideration liabilities - - - (5171) Impact of tax benefit from realization of previously unrecognized deferred tax asset - (4228) - - - -Impact of Alberta tax law change - 4982 - - - -Provision for long-term contract receivable 102460 - - - - -Arbitration expense 38848 - - - -Impact of sale of equity ownership in Howard Energy - - - - -Income tax impact of adjustments 55935 (16186) (3982) (23522) (1700) (1700)

Adjusted net income from continuing operations attributable to common stock before certain non-cash adjustments 361252 171271 191624 259345 314900 378900

Non-cash stock based compensation 37449 36939 41134 46448 50700 50700 Amortization of intangible assets 34257 34848 31685 32205 41300 41300 Income tax impact of non-cash adjustments (26453) (25817) (26183) (28877) (24100) (24100)

Adjusted net income from continuing operations attributable to common stock 406505$ 217241$ 238260$ 309121$ 382800$ 446800$ Weighted average sharesWeighted average shares outstanding for diluted earnings per share 219690 195120 157288 157155 159300 159300 Weighted average shares outstanding for adjusted diluted earnings per share 219690 195120 157288 157155 159300 159300 Diluted earnings per share from continuing operations attributable to common stock and adjusted diluted earnings per share from continuing operations attributable to common stockDiluted earnings per share from continuing operations attributable to common stock 122$ 062$ 126$ 200$ 195$ 235$ Adjusted diluted earnings per share from continuing operations attributable to common stock 185$ 111$ 151$ 197$ 240$ 280$

Estimated Guidance Range

For the Years Ended December 31

(in thousands except per share information)(Unaudited)

Recast of Adjusted Diluted

Page 40

Reconciliation of Electric Power and Oil amp Gas Infrastructure Services Segments Operating Income As Adjusted

Amounts in millions except percentagesOil amp Gas

Infrastructure12312014 12312015 12312016 12312014

Revenues 53027$ 49373$ 48505$ 24446$

Operating Income (as reported) 4630 3623 3957 1628

Addback Provisions for long term contract receivable 1025 - - - Arbitration expense - - - 388 Asset impairment charge - 66 57 -

Operating Income (as adjusted) 5655$ 3689$ 4014$ 2016$

Operating income margin (as reported) 87 73 82 67Operating income margin (as adjusted) 107 75 83 83

Electric Power

Sheet1

Page 41

Reconciliation of Free Cash Flow

2014 2015 2016 2017Net Cash Provided by Operating Activities of Continuing Operations 261649 628649 390187 372475 Less Net Capital ExpendituresAdditions of Property and Equipment (247216) (209968) (212555) (244651) Proceeds from Sale of Property and Equipment 14448 26178 21975 23348 Net Capital Expenditures (232768) (183790) (190580) (221303)

Free Cash Flow 28881 444859 199607 151172

Free Cash Flow from Cont Ops

Page 42

Forward Looking Statement DisclaimerThis presentation (and oral statements regarding the subject matter of this presentation) includes ldquoforward-looking statementsrdquo intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995 These statements reflect assumptions expectations projections intentions or beliefs about future events and use words such as anticipate estimate project forecast may will should could expect believe plan intend and other words of similar meaning You can identify these statements by the fact that they do not relate strictly to historical or current facts In particular these include but are not limited to statements relating to the following

bull Projected or estimated revenues net income earnings per share attributable to common stock backlog margins capital expenditures weighted average shares outstanding tax rates or other financial or operating resultsbull Our business or financial outlook growth trends or opportunities in particular marketsbull The potential benefits from acquisitions and investmentsbull The expected financial and operational performance of acquired businessesbull The future demand for and availability of labor resources in the industries we servebull Future capital allocation initiatives including the amount timing and strategy with respect to any future stock repurchasesbull Our ability to deliver increased value and return capital to stockholders bull The strategic use of our balance sheetbull The expected value of contracts or intended contracts with customersbull The scope services term and results of any projects awarded or expected to be awarded for services to be provided by usbull The anticipated commencement and completion dates for any projects awardedbull The development of larger electric transmission and oil and natural gas pipeline projects and the level of oil natural gas and natural gas liquids prices and their impact on our business or the demand for our services bull The impact of existing or potential legislation including the Tax Cuts and Jobs Act of 2017 bull Potential opportunities that may be indicated by bidding activity or discussions with customersbull The expected outcome of pending or threatened litigation bull Beliefs and assumptions about the collectability of receivablesbull The business plans or financial condition of our customersbull Our plans and strategies bull The current economic and regulatory conditions and trends in the industries we serve bull Possible recovery on pending or contemplated change orders or affirmative claims against customers or third parties and bull Other statements reflecting expectations intentions assumptions or beliefs about future events and other statements that do not relate strictly to historical or current facts

Although our management believes that the expectations reflected in such forward-looking statements are reasonable it can give no assurance that such expectations will prove to be correct These forward-looking statements are not guarantees of future performance and involve or rely on a number of risks uncertainties and assumptions that are difficult to predict or beyond our control These forward-looking statements reflect our beliefs and assumptions based on information available to our management at the time the statements are made We caution you that actual outcomes and results may differ materially from what is expressed implied or forecasted by our forward-looking statements and that any or all of our forward-looking statements may turn out to be wrong Forward-looking statements can be affected by inaccurate assumptions and by known or unknown risks and uncertainties including the following

bull Market conditionsbull The effects of industry economic financial or political conditions outside our control including weakness in capital marketsbull Quarterly variations in our operating resultsbull Trends and growth opportunities in relevant marketsbull The cost of borrowing availability of credit and cash fluctuations in the price and volume of our common stock debt covenant compliance interest rate fluctuations and other factors affecting our financing and investing activitiesbull Delays reductions in scope or cancellations of anticipated pending or existing projects including as a result of weather regulatory or permitting issues environmental processes project performance issues claimed force majeure events protests or other

political activity or our customers capital constraintsbull The successful negotiation execution performance and completion of anticipated pending and existing contracts including the ability to obtain awards of projects on which we bid or are otherwise discussing with customersbull Our ability to retain key personnel and qualified employees

Page 43

Forward Looking Statement Disclaimerbull Our ability to attract or the potential shortage of skilled labor bull Our dependence on fixed price contracts and the potential to incur losses with respect to the contractsbull Estimates relating to our use of percentage-of-completion accountingbull Adverse weatherbull Our ability to generate internal growthbull Competition in our business including our ability to effectively compete for new projects and market sharebull The effect of natural gas natural gas liquids and oil prices on our operations and growth opportunities and on

our customersrsquo capital programs and demand for our servicesbull The future development of natural resourcesbull The failure of existing or potential legislative actions to result in demand for our servicesbull Liabilities associated with multiemployer pension plans including underfunding of liabilities and termination

or withdrawal liabilitiesbull Unexpected costs or liabilities that may arise from pending or threatened litigation indemnity obligations or

other claims asserted against us including liabilities for claims that are not covered by third-party insurancebull The outcome of pending or threatened litigationbull Risks relating to the potential unavailability or cancellation of third party insurance the exclusion of coverage

for certain losses and potential increases in premiums for coverage deemed beneficial to usbull Cancellation provisions within our contracts and the risk that contracts expire and are not renewed or are

replaced on less favorable termsbull Loss of customers with whom we have long-standing or significant relationshipsbull The potential that participation in joint ventures or similar structures exposes us to liability andor harm to

our reputation for acts or omissions by our partnersbull Our inability or failure to comply with the terms of our contracts which may result in additional costs

unexcused delays warranty claims failure to meet performance guarantees damages or contract terminations

bull The inability or refusal of our customers to pay for services including the failure to collect outstanding receivables

bull The failure to recover on payment claims against project owners or third party contractors or to obtain adequate compensation for customer-requested change orders

bull The failure of our customers to comply with regulatory requirements applicable to their projects which may result in project delays and cancellations

bull Budgetary or other constraints that may reduce or eliminate tax incentives or government funding for projects which may result in project delays or cancellations

bull Estimates and assumptions in determining our financial results and backlogbull Our ability to realize our backlogbull Risks associated with operating in international markets including instability of foreign governments

currency fluctuations tax and investment strategies as well as compliance with foreign legal systems and cultural practices the US Foreign Corrupt Practices Act and other applicable anti-bribery and anti-corruption laws

bull Our ability to successfully identify complete integrate and realize synergies from acquisitions

bull The potential adverse impact resulting from uncertainty surrounding investments and acquisitions including the ability to retain key personnel from an acquired business and the potential increase in risks already existing in our operations

bull The adverse impact of impairments of goodwill receivables property equipment and other intangible assets or investments

bull Our growth outpacing our decentralized management and infrastructurebull Requirements relating to governmental regulation and changes theretobull Inability to enforce our intellectual property rights or the obsolescence of such rightsbull Risks related to the implementation of new information technology solutionsbull The impact of our unionized workforce on our operations including labor stoppages or interruptions due to

strikes or lockoutsbull Potential liabilities and other adverse effects arising from occupational health and safety mattersbull Our dependence on suppliers subcontractors equipment manufacturers and other third party contractorsbull Fluctuations of prices of certain materials used in our businessbull The ability to access sufficient funding to finance desired growth and operationsbull Our ability to obtain performance bondsbull Potential exposure to environmental liabilitiesbull Our ability to continue to meet certain regulatory requirements applicable to us and our subsidiariesbull Rapid technological and other structural changes that could reduce the demand for our servicesbull New or changed tax laws treaties or regulationsbull Increased healthcare costs arising from healthcare reform legislation or other governmental actionbull Regulatory changes that result in increased labor costsbull Significant fluctuations in foreign currency exchange rates andbull The other risks and uncertainties described elsewhere herein and in our Annual Report on Form 10-K for the

year ended December 31 2017 filed with the SEC and as may be detailed from time to time in our other public filings with the SEC (available through our website at wwwquantaservicescom or the SECrdquos Electronic Data Gathering and Analysis Retrieval System (EDGAR) at wwwsecgov)

All of our forward-looking statements whether written or oral are expressly qualified by these cautionary statements and any other cautionary statements that may accompany such forward-looking statements or that are otherwise included in this presentation Should one or more of these risks materialize or should underlying assumptions prove incorrect actual results may vary materially from those expressed or implied in any forward-looking statements Investors are cautioned not to place undue reliance on these forward-looking statements which are current only as of this date We do not undertake and expressly disclaim any obligation to update or revise any forward-looking statements to reflect events or circumstances after the date of this presentation or otherwise and we expressly disclaim any written or oral statements made by any third party regarding the subject matter of this presentation

Slide Number 1

Slide Number 2

Slide Number 3

Slide Number 4

Slide Number 5

Slide Number 6

Slide Number 7

Slide Number 8

Slide Number 9

Slide Number 10

Slide Number 11

Slide Number 12

Slide Number 13

Slide Number 14

Slide Number 15

Slide Number 16

Slide Number 17

Slide Number 18

Slide Number 19

Slide Number 20

Slide Number 21

Slide Number 22

Slide Number 23

Slide Number 24

Slide Number 25

Slide Number 26

Slide Number 27

Slide Number 28

Slide Number 29

Slide Number 30

Slide Number 31

Slide Number 32

Slide Number 33

Slide Number 34

Slide Number 35

Slide Number 36

Slide Number 37

Slide Number 38

Slide Number 39

Slide Number 40

Slide Number 41

Slide Number 42

Slide Number 43

Free Cash Flow From Continuing Operations

Source

2014

2015

2016

2017

(Support Cash Flow Statement)

Net Cash Provided by Operating Activities of Continuing Operations

261649

628649

390187

372475

(Support Cash Flow Statement)

Less Net Capital Expenditures

(Support Cash Flow Statement)

Additions of Property and Equipment

(247216)

(209968)

(212555)

(244651)

(Support Cash Flow Statement)

Proceeds from Sale of Property and Equipment

14448

26178

21975

23348

(Recalculation)

Net Capital Expenditures

(232768)

(183790)

(190580)

(221303)

(Recalculation)

Free Cash Flow

28881

444859

199607

151172

Adjusted Operating Income Margin

$ in millions

Support for slide 23

Amounts in millions except percentages

Electric Power

Oil amp Gas Infrastructure

123114

123115

123116

123114

Revenues

$ 53027

$ 49373

$ 48505

$ 24446

Operating Income (as reported)

4630

3623

3957

1628

Addback

Provisions for long term contract receivable

1025

-0

-0

-0

Arbitration expense

-0

-0

-0

388

Asset impairment charge

-0

66

57

-0

Operating Income (as adjusted)

$ 5655

$ 3689

$ 4014

$ 2016

Operating income margin (as reported)

87

73

82

67

Operating income margin (as adjusted)

107

75

83

83

Quanta Services Inc and Subsidiaries

Reconciliation of Non-GAAP Financial Measures

Adjusted Diluted Earnings Per Share from Continuing Operations

For the Years Ended December 31

(in thousands except per share information)

(Unaudited)

Estimated Guidance Range

2013

2014

2015

2016

2017

2018

2018

Reconciliation of adjusted net income from continuing operations attributable to common stock

Net income from continuing operations attributable to common stock (GAAP as reported)

$ 372057

$ 269224

$ 120286

$ 198725

$ 314978

$ 310000

$ 374000

Adjustments

Asset impairment charges

-

-

58451

7964

58057

-

-

Severance and restructuring charges

-

-

-

6352

- 0

-

-

Acquisition and integration costs

8145

14754

7966

3053

10579

6600

6600

Impact of Tax Cut and Jobs Act

- 0

- 0

- 0

(70129)

Tax benefits primarily related to entity restructuring and recapitalization efforts

- 0

- 0

- 0

(18224)

Impact of income tax contingency releases

(9935)

(8099)

- 0

(20488)

(7223)

-

-

Change in fair value of contingent consideration liabilities

- 0

- 0

- 0

(5171)

Impact of tax benefit from realization of previously unrecognized deferred tax asset

-

-

(4228)

-

- 0

-

-

Impact of Alberta tax law change

-

-

4982

-

- 0

-

-

Provision for long-term contract receivable

-

102460

-

-

- 0

-

-

Arbitration expense

-

38848

-

-

-

-

Impact of sale of equity ownership in Howard Energy

(112744)

-

-

-

-

-

Income tax impact of adjustments

39836

55935

(16186)

(3982)

(23522)

(1700)

(1700)

Adjusted net income from continuing operations attributable to common stock before certain non-cash adjustments

297359

361252

171271

191624

259345

314900

378900

Non-cash stock based compensation

34381

37449

36939

41134

46448

50700

50700

Amortization of intangible assets

25865

34257

34848

31685

32205

41300

41300

Income tax impact of non-cash adjustments

(22715)

(26453)

(25817)

(26183)

(28877)

(24100)

(24100)

Adjusted net income from continuing operations attributable to common stock

$ 334890

$ 406505

$ 217241

$ 238260

$ 309121

$ 382800

$ 446800

Weighted average shares

Weighted average shares outstanding for diluted earnings per share

214978

219690

195120

157288

157155

159300

159300

Weighted average shares outstanding for adjusted diluted earnings per share

214978

219690

195120

157288

157155

159300

159300

Diluted earnings per share from continuing operations attributable to common stock and adjusted diluted earnings per share from continuing operations attributable to common stock

Diluted earnings per share from continuing operations attributable to common stock

$ 173

$ 122

$ 062

$ 126

$ 200

$ 195

$ 235

Adjusted diluted earnings per share from continuing operations attributable to common stock

$ 156

$ 185

$ 111

$ 151

$ 197

$ 240

$ 280

2017 Forecast

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

US IOU

17599783395

17375430450

17116821481

17473265629

19719353886

18593206538

21049378470

23210018195

24651006483

28003750000

29530700000

30481300000

30509750000

31231850000

31138000000

Co-ops

3679033739

3613552751

2806195753

3044502916

2639012201

3360515403

3050612075

2834000972

3277074511

3309845256

3342943708

3376373145

3410136877

3444238245

3478680628

MuniGovt Owned

2525145025

2693819865

2624788344

2608815562

2682098477

2938725525

3183015391

3330273309

3454862656

3664198000

3769427295

3778921940

3483677493

3817389338

3817389338

Canadian

3324942988

3202431553

3726264949

4213182949

4228837570

4323705834

4106960884

3465854177

3159852215

3254697600

3381315300

3453964800

3380277450

3406223700

3406223700

Total NA 2017 Market

27128905147

26885234619

26274070528

27339767056

29269302134

29216153300

31389966819

32840146653

34542795864

38232490856

40024386303

41090559885

40783841819

41899701283

41840293665

From August 2015 Report

North American Electric Distribution Spending

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

US IOUs

$175

$173

$171

$174

$197

$186

$210

$226

$244

$244

$247

$249

$250

US Co-ops

$27

$29

$27

$29

$35

$41

$34

$39

$40

$40

$41

$42

$42

US Muni

$25

$26

$26

$28

$28

$29

$29

$30

$31

$31

$32

$32

$33

Total US

$226

$227

$224

$231

$260

$256

$273

$295

$314

$316

$320

$323

$325

Canada

$33

$33

$34

$39

$38

$39

$39

$38

$41

$41

$42

$43

$43

Total

$260

$261

$259

$269

$298

$294

$312

$333

$354

$357

$362

$365

$368

15 vs 16

$00

$01

$02

$04

($01)

($04)

$06

$04

$08

$21

$19

$28

$26

From August 2016 Report

North American Electric Distribution Spending

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

US IOUs

$176

$174

$171

$175

$197

$186

$210

$232

$258

$270

$271

$281

$281

US Co-ops

$27

$29

$27

$29

$31

$33

$38

$39

$40

$41

$41

$42

$43

US Muni

$25

$26

$26

$28

$28

$29

$29

$30

$31

$31

$32

$33

$33

Total US

$228

$229

$224

$232

$256

$248

$277

$301

$329

$342

$344

$356

$357

Canada

$32

$32

$37

$41

$41

$42

$41

$36

$33

$36

$37

$37

$37

Total

$260

$261

$261

$273

$297

$290

$318

$337

$362

$378

$381

$393

$394

From September 2017 Report

North American Electric Distribution Spending

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

US IOUs

$176

$174

$171

$175

$197

$186

$210

$232

$247

$280

$295

$305

$305

$312

$311

US Co-ops

$37

$36

$28

$30

$26

$34

$31

$28

$33

$33

$33

$34

$34

$34

$35

US Muni

$25

$27

$26

$26

$27

$29

$32

$33

$35

$37

$38

$38

$35

$38

$38

Total US

$238

$237

$225

$231

$250

$249

$273

$294

$314

$350

$366

$376

$374

$385

$384

Canada

$33

$32

$37

$42

$42

$43

$41

$35

$32

$33

$34

$35

$34

$34

$34

Total

$271

$269

$263

$273

$293

$292

$314

$328

$345

$382

$400

$411

$408

$419

$418

2015 vs 2016 vs 2017

2015 Est

2016 Est

2017 Est

Avg 08-11

$262

$264

$269

Avg 12-15

$309

$311

$307

16

$354

$362

$345

17

$357

$378

$382

18

$362

$381

$400

19

$365

$393

$411

20

$368

$394

$408

21

$419

22

$418

2017

This presentation (and oral statements regarding the subject matter of this presentation) includes forward-looking statements intended to qualifyunder the ldquosafe harborrdquo from liability established by the Private Securities Litigation Reform Act of 1995 These forward-looking statements includeany statements reflecting Quantas expectations intentions strategies assumptions or beliefs about future events or performance or that do notsolely relate to historical or current facts Forward-looking statements involve certain risks uncertainties and assumptions that are difficult topredict or beyond Quantas control and actual results may differ materially from those expected implied or forecasted by our forward-lookingstatements due to inaccurate assumptions and known and unknown risk and uncertainties For additional information concerning some of therisks uncertainties and assumptions that could affect our forward-looking statements please refer to Quantarsquos Annual Report on Form 10-K for theyear ended December 31 2017 and its other documents filed with the Securities and Exchange Commission as well as the risks uncertainties andassumptions identified in this presentation Investors and analysts should not place undue reliance on Quantarsquos forward-looking statements whichare current only as of the date of this presentation Quanta does not undertake and expressly disclaims any obligation to update or revise anyforward-looking statements to reflect events or circumstances after the date of this presentation or otherwise and Quanta expressly disclaims anywritten or oral statements made by any third party regarding the subject matter of this presentation

Forward Looking Statement Disclaimer

Page 2

Page 3

Key Takeaways

Quanta is the leading construction-led infrastructure solutions provider in the markets we serve with unmatched scope and scale

Quanta continues to see opportunities to increase shareholder value through growth in revenues and EPS over a multi-year period

Quantarsquos corporate actions demonstrate confidence in our long-term growth prospects and a commitment to generating shareholder value

We will maintain a strong financial profile to support our strategic initiatives for near- and long-term profitable growth

Page 4

Leading Construction-Led Infrastructure Solutions Provider

Who is Quanta Services Committed to the health and safety of our employees customers and community

Recognized market leader in electric power and oil and gas pipeline construction in North America

Entrepreneurial business model and culture

Broad self-performing platform developed through organic growth and acquisitions

Strong scope and scale with deep customer relationships

Revenue as reported by type of work geography contract and project type based on revenues of $9466 million for the twelve months ended Dec 31 2017 Represents the midpoint of guidance range

Estimated Revenue by Geography

United States74

LATAM amp Other2

Canada21

Australia3

Page 6

Overview ndash Diverse and High Quality Customer Base

Top 10

36

9 No single customer accounted formore than 9 of revenues in 2017

The ten largest customers accountedfor approximately 36 of revenues in2017

Strong relationships with the majorityof US investor owned utilities and Canadian utilities ndash many going backfor decades

Quantarsquos Low Customer Concentration Is Unique Versus Peers

Page 7

Leading Construction-Led Infrastructure Solutions Provider

bull Grow the ldquobase businessrdquo and compliment with larger scale projects

bull Organic growth and strategic acquisitions

bull Pricing discipline and risk management

bull Focus on safe executionbull Cost managementbull Maintain financial strength

Time

Reve

nues

Coupled with Successful Implementation of Other Strategic Imperatives hellip

Larger Projects

For illustrative purposes

Page 10

Strategic Acquisitions ndash Criteria and Rationale

Acquisition Strategic Rationale

bull Seek well respected entrepreneurial leadership with extensive history of operational excellencebull Only interested in companies that bring strategic value to Quanta and provide opportunity for 1+1=3 growth

opportunity over time

bull Brings leadership position in new geographybull Enhances presence and capabilities in an existing

geographybull Brings or enhances customer relationshipsbull Brings leadership position in adjacent or new

marketbull Brings unique service or technology that Quanta

can leverage to further differentiate its turnkey solution offering

Typical Deal Terms

bull Target 4x-5x EBITDA multiplebull 40 of consideration in Quanta stock 60 of

consideration in cashbull Meaningful stock component for operational and

stakeholder alignment

bull Company leadership stays on to run the businessbull Non-compete agreementsbull Stock locked up for period of time

Acquisitions Have and Will Continue to Play A Strategic Role in Differentiating Quanta in the Marketplace and Positioning the Company for Profitable Long-Term Growth

Page 11

Differentiated Competitive Position ndash In the Sweet Spot

bull Quanta is the leading and largest construction-led infrastructure solutions provider in North America

bull Unmatched scope providing broader solutions to customersbull Unmatched scale as the largest employer of skilled workforce

in the industry ndash more than 33000 employeesbull Track record of safe executionbull Projects are getting larger and more complex customers

increasingly seeking cost certainty and performancebull Quanta has consistently been working on numerous large

projects simultaneously for the past + six yearsbull Significant revenues from strategic relationships recurring work

and an increasing amount of negotiated work

Quanta vs Specialty Contractors Quanta vs Traditional EampCs

bull Today our customers believe skilled construction labor is a finite resource and critical to overall project success where engineering and procurement are more commoditized

bull Quanta is construction-led and self-performs its projects ndashcontrols quality and execution

bull EampCs typically provide project management oversight and have limited self-perform construction capabilities

bull Quanta derives significant revenues from strategic relationships recurring work and an increasing amount of negotiated work

bull Price is often the primary driver of who wins EampC projects

Est Large Project Capability

Bubble Size = Avg Market Cap

0

20

40

60

80

100

Est

Self

Perf

orm

Cap

abili

ty

Bubble Size = Avg Market Cap

LargerSmallerLargerSmaller

Est

Self

Perf

orm

Cap

abili

ty

Est Large Project Capability

Page 12

Differentiated Competitive Position ndash In the Sweet Spotbull Quanta is construction-led and is uniquely

positioned to meet customer needs versus both specialty contractors and traditional engineering and construction companies

bull Customers understand that skilled labor is critical to project success

bull Projects are getting larger and more complex and customers are increasingly seeking comprehensive solutions

bull Demand for specialty construction resources is high and increasing but supply is limited

bull Quanta has the largest infrastructure specialty workforce in North America +33000 employees globally

bull Quanta has strategically invested in engineering and program management to provide true complete engineering procurement and construction (EPC) solutions

0

20

40

60

80

100

Est

Self

Perf

orm

Cap

abili

ty

Est Large Project Capability

Bubble Size = Avg Market Cap

LargerSmaller

Page 13

Electric Power Infrastructure Services Segment Overview

$5303$4937 $4850

$5600

107

75 8393

2014 2015 2016 2017

Revenue Op Margin

(2)

(1) Operating margin excludes a $1025 million charge to cost of services for long-term contract receivable in 2014 Refer to appendix for non-GAAP reconciliation(2) Excludes a $66 million property and equipment charge in 2015 and a $57 million asset impairment charge in 2016 Includes the impact of $661 million in 2015 and $548 million in 2016 of project losses Refer to appendix for non-GAAP reconciliation

Financial SnapshotFor the years ended Dec 31 ($ in millions)

$3395 $3308 $3369$4032

$6716 $6313 $6658$7359

2014 2015 2016 2017

12-Mth Backlog Total Backlog

(2)

(1)

Differentiatorsbull Largest TampD solutions provider in

North Americabull Reputation and Track Recordbull Unmatched Solutions Scope and

Scalebull Safety Recordbull Manpower and Equipment

Resourcesbull Northwest Lineman College (NLC)bull Lazy Q Training Facility amp other

industry leading training initiativesbull Energized Servicesbull EPC Capabilities Across All Offeringsbull Infrastructure Capital Solutions

Page 14

Power Grid Investment Drivers ndash Transmission amp Distribution

Market Drivers

bull An aging grid that requires repair upgrade and maintenancebull Utility spending continues to shift from generation to

transmission and distributionbull Favorable transmission regulation Energy Policy Act of lsquo05

NERC Reliability Standards possibly FERC Order 1000 over the long-term

bull More stringent reliability standards will require repairing lines and adding redundant capacity

bull Regional grid infrastructure is too congested to get lowest-cost power to consumers

bull Coal and nuclear generation retirements and switching to natural gas and renewable generation strains the grid

bull Existing and new renewable generation needs interconnection to the grid

bull Renewed distribution focus on reliability versus costsbull System hardening initiatives particularly in areas hard hit by

severe weather

bull Challenged economic conditions in Canada

bull Environmental and other regulatory scrutiny right of way acquisition permitting etc

bull Tepid load growthbull Economybull Energy efficiency initiatives

bull State renewable portfolio standards being evaluated in some states

bull Transmission ROE challenges due to low interest rate environment

bull Distribution returns lower than FERC transmission returnsbull Regulatory and consumer pressures on utilities against rising

power bills

Restraining Factors

$0$5

$10$15$20$25$30$35$40$45

Avg08-11

Avg12-15

16 17 18 19 20 21 22

2015 Est 2016 Est 2017 Est

Page 15

Power Grid Investment Drivers ndash Transmission amp Distribution

$0

$5

$10

$15

$20

$25

$30

$35

Avg08-11

Avg12-15

16 17 18 19 20 21 22

2015 Est 2016 Est 2017 Est

bull Utility spending continues to shift from generation to transmission and distribution

bull Transmission and distribution spending continues to reach all time highs and forecasts point towards sustained robust spending

bull Previously delayed larger transmission projects are expected to move forward over next several years

Source The C3 Group 2017

Est North American Transmission SpendingOut-year estimates tend tohave upward revision bias

Billi

ons

Billi

ons

Est North American Distribution CapExOut-year estimates tend tohave upward revision bias

bull Sub-transmission interconnection

bull Technology innovations will continue to grow A focus on upgrades to modernize the grid will overlap with spending needed to address aging infrastructure

bull Opportunity for industrial driven load growth and overall load growth asif economic growth increases

bull Northwest Lineman College (NLC) is a for profit nationally accredited and industry leading training program providing safety and certification training to pre-apprentices apprentices journey level lineworkers crew leaders substation technicians and system operators NLC was founded in 1993 NLC has four campuses across the US (Idaho California Florida and Texas)

Overview

bull Tight labor market for lineman and other skilled employees Recruiting training and maintaining people is critical for us and for our customers

bull NLCrsquos world class program should elevate and expedite Quantarsquos training and development efforts which will benefit our customers the industry and Quanta

bull Developing curricula for communications and natural gas distribution services Ability to develop other curricula for services Quanta provides

bull Complements Quantarsquos other initiatives underway to address workforce needs

bull Lazy Q Training Facilitybull Veteran Recruiting and Developmentbull Quanta-Sam Houston State University Partnership

Strategic Rationale

Page 17

Oil amp Gas Infrastructure Services Segment Overview

$2445 $2635 $2801

$3867

83

54 53 48

2014 2015 2016 2017Revenue Op Margin

(1) Excludes a $388 million expense associated with an arbitration decision Refer to appendix for non-GAAP reconciliation(2) Includes $73 million of project losses(3) Includes a $19 million charge to expense associated with a construction barge

Financial SnapshotFor the years ended Dec 31 ($ in millions)

$1825 $1901$2484 $2414$2521

$3074 $3092

$3819

2014 2015 2016 2017

12-Mth Backlog Total Backlog

(2)

(1)

Differentiatorsbull Largest Pipeline Solutions Provider

in North Americabull Reputation amp Track Recordbull Safe Project Executionbull Turnkey Solutionsbull EPC Capabilitiesbull Critical Path Industrial Servicesbull In-House Mechanized Weldingbull In-House Pigging Technologybull Pipe Logistics Managementbull Infrastructure Capital Solutions

(3)

Page 18

Oil amp Gas Infrastructure Investment Drivers

bull Production of shale natural gas oil and natural gas liquids has grown dramatically and is expected to remain at high levels forthe foreseeable future

bull Much of these resources are in areas that have not been traditional hydrocarbon fuel sources and do not have adequate infrastructure in place to gather store process and transport product

bull Canadian oil production lacks adequate takeaway pipeline infrastructurebull Economics of pipeline transportation is increasingly attractive versus rail in a lower oil price environmentbull Pipeline construction capacity is more limited in Canada versus the US and construction capacity constraints could be significant

bull It will take many years and significant energy infrastructure investment to harvest these resources

Shale Gas amp Tight Oil Plays Drive US Natural Gas Production

2000-2040 (trillion cubic feet)

Source EIA Annual Energy Outlook 2017

Tight Oil Drives US Oil Production2000-2040 (millions of barrels per day)

Source EIA Annual Energy Outlook 2017

Canadian Oil Sands amp Conventional Oil Production(Millions of barrels per day)

Source Canadian Assoc of Petroleum Producers

Page 19

Oil amp Gas Infrastructure Investment Drivers

bull Need for pipeline and related infrastructure driven by the significant increase in North American unconventional natural gas and oil production ndash not commodity prices

bull Takeaway pipelines have not been built fast enough to keep pace with hydrocarbon production ndash significant pipeline development needed

bull Large pipeline construction industry capacity is currently tight but could get significantly strained over the next several years

North American Pipeline ForecastProbability Weighted

bull Quanta is the largest pipeline construction company in North America

bull This positions Quanta to provide significant large diameter pipe construction capacity to the industry while remaining active in select shales

bull We are ready to assist our customers in meeting their development goals in what could be a resource challenged environment

In B

illio

ns

Quanta Is the Largest Pipeline Construction Company in North America

Stifel expects upward revisions to Tier 1 amp 2 projects in out years

x Tier 1 amp 2

x Tier 3 amp Potential

Page 20

Oil amp Gas Infrastructure Investment Drivers

Natural Gas Distribution amp Pipeline Integritybull US pipeline infrastructure is getting older and much of it was

installed before 1970bull Local Distribution Companies (LDCs) increasing spend on pipe

inspection and replacementbull Regulations push expanding inspection programs and

accelerating distribution pipeline replacement work bull Long timelines for some replacement plans (decades) will push

spend accelerationbull State regulators establishing cost recovery mechanisms to

accelerate replacement programs

Significant Inventory Remains for Replacement

Diversified and Expanding Solutions to Capture Midstream and Downstream Industry Spend

Downstream Industrial Services

Projected North American Downstream MaintenanceSpending 2017 ndash 2021 ~ $113 Billion

Refinery34

PetChem42

Gas Proc16

LNG8

Source Douglas-Westwood

bull Substantial installed base of industrial facilities operating in a highly corrosive environment

bull As plants age critical process unitsrsquo risk of failure increases significantly requiring consistent and recurring maintenance investment

bull Deferrals and other factors yield expectations for significant turnaround season over coming years ndash reversion to mean activity levels

bull Stronghold gives Quanta a significant presence in downstream services and a strong platform for growth

Page 21

Telecom Infrastructure Services Overview

To be an industry leading and true EPC contractor providing comprehensive communications infrastructure solutions to customers in the United States Canada and select markets in Latin America

Goal

Diverse Existing amp Target Customer BaseMarkets Served

Page 22

Telecom Infrastructure Investment Drivers

bull Telco gigabit fiber to the home deployment programs

bull Cable MSOs deploying DOCSIS 31

bull Upcoming - 5G wireless and fiber backhaul

bull Ongoing 4G wireless network optimization

bull Connect America Fund - rural fiber build-out

bull Federal government funded FirstNet - national wireless network for first responders

United States

bull Backbone and last mile fiber (behind relative to the US)

bull Telco gigabit fiber to the home deployment programs

bull Cable MSOs deploying DOCSIS 31

bull Upcoming - 5G wireless and fiber backhaul

bull Ongoing 4G wireless network optimization

bull Federal government infrastructure initiatives generally positive

Canada

bull Significantly behind North America in both wireline and wireless connectivity

bull However demand for connectivity media and data intensive services is strong

bull Fiber and backhaul networks significantly behind North America

bull Primarily 3G wireless some 4G wireless (country dependent)

bull Various governments have infrastructure expansion initiatives

bull Concession and P3 opportunities

bull Connectivity for quality of life social and commercial reasons

Latin America

Geographic Diversity Provides Exposure to Multiple Market Drivers

Page 23

Telecom Infrastructure Services Overview

Fiber Builds

Wireless Deployment

Make Ready Services

Civil Construction

Engineering Design

Material Management

EPC

Wireless Wireline

United States

Wireless Wireline

Canada

Wireless Wireline

Latin America

Quantarsquos Capabilities

= Current Service= In Development

Comprehensive Infrastructure Solutions Offered On A Turnkey Discrete Service or EPC Basis

bull Proven greenfield expansion model in Latin America ndash US should be less difficult

Leverage existing US field operations people equipment and property

bull Select strategic acquisitions may play a role but NOT a roll-up approach

Provide wireline and wireless services - heavier on wireline

bull Increasing convergence of wireless and wireline due fiber requirements of both

Project centric nimble approach versus MSA focused EPC services to differentiate

bull Less capital intensive with better margin opportunity

GOAL

STRATEGY

STRATEGY

STRATEGY

STRATEGY