Embed Size (px)

Citation preview

1

1

Investor PresentationJune 2015

2

Investment Summary

Canada’s largest pure-play office REIT

24.1 million sf of valuable, hard to replicate central business district and suburban office properties

CBD properties generate ~70 % of NOI

Proven track record of value creation by senior management

Strong tenant roster

Significant unrealized value-add/repositioning opportunities

Well diversified by geography, asset & tenant mix

Strong occupancy with staggered lease maturities and rental rate growth

A conservative and flexible balance sheet; 47.6% Debt to GBV

Investment grade credit rating

In our history, we’ve never had a better quality portfolio or a stronger balance sheet with embedded opportunities for growth and value creation.

3

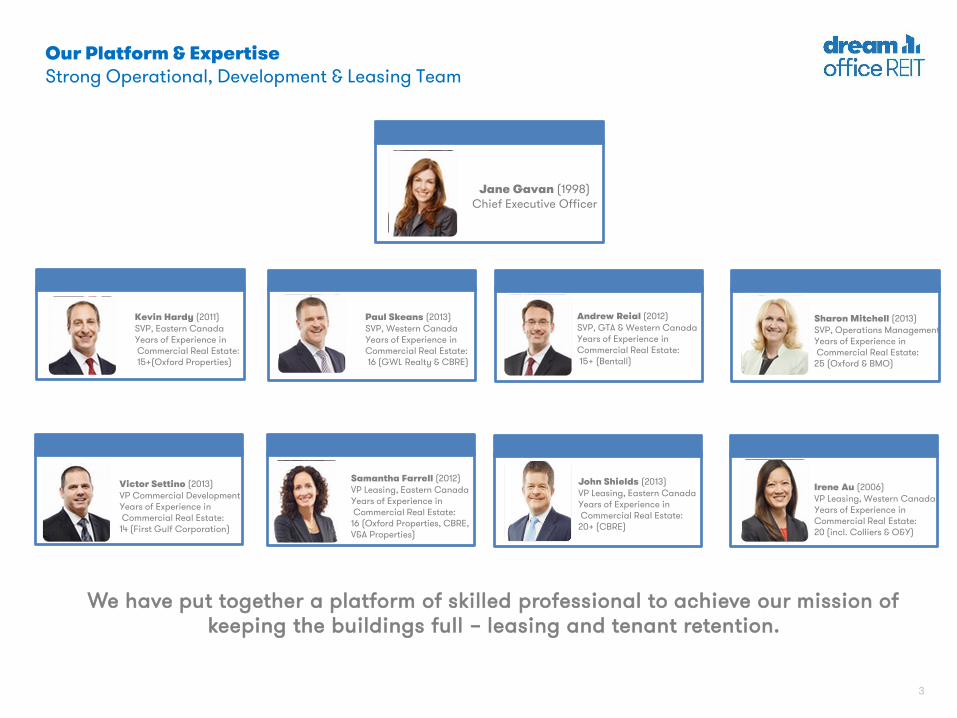

Kevin Hardy (2011)SVP, Eastern CanadaYears of Experience inCommercial Real Estate:15+(Oxford Properties)

Paul Skeans (2013)SVP, Western Canada Years of Experience in Commercial Real Estate:16 (GWL Realty & CBRE)

Victor Settino (2013)VP Commercial DevelopmentYears of Experience inCommercial Real Estate:

14 (First Gulf Corporation)

Sharon Mitchell (2013)SVP, Operations ManagementYears of Experience inCommercial Real Estate:

25 (Oxford & BMO)

Our Platform & ExpertiseStrong Operational, Development & Leasing Team

We have put together a platform of skilled professional to achieve our mission of keeping the buildings full – leasing and tenant retention.

Andrew Reial (2012)SVP, GTA & Western Canada Years of Experience in Commercial Real Estate:15+ (Bentall)

Samantha Farrell (2012)VP Leasing, Eastern CanadaYears of Experience inCommercial Real Estate:

16 (Oxford Properties, CBRE, V&A Properties)

John Shields (2013)VP Leasing, Eastern CanadaYears of Experience inCommercial Real Estate:

20+ (CBRE)

Irene Au (2006)VP Leasing, Western CanadaYears of Experience in Commercial Real Estate: 20 (incl. Colliers & O&Y)

Jane Gavan (1998)Chief Executive Officer

4

Our Platform & ExpertiseStrong Support from Dream

Dream’s platform benefits D.un:

Transaction & capital markets expertise Track record of development & value

creation Synergies realized across broad platform Asset management & development

capabilities

20 year history in real estate and renewable power developer, manager and investor

Completed ~$20 billion of real estate and alternative investment transactions

178 dedicated professionals in all disciplines

Extensive network of global JV partners and financial institution support

Dream has…

5

On April 2nd we completed the reorganization of the management structure of DREAM Office REIT.

As a result of the reorganization, the annual management fee, acquisition fee and capital expenditure fee payable to Dream Asset Management Corporation (“Dream”) have been eliminated. In consideration for the sale, Dream received 4.85 million exchangeable limited partnership units exchangeable for REIT units.

Dream will continue to provide strategic oversight on a cost recovery basis.

Dream Office continues to leverage the expertise of the acquisition and financing teams at Dream.

Reorganization of Management Structure

6

Proven Track Record of Growth & PerformanceResults of Our 6 Year Capital Allocation Strategy

Unit Price $12.60 (as at Dec 31, 2008) $ 25.52 (as at June 3 , 2015)

Market Capitalization $260 million $2.9 billion

1-Year Fwd Consensus AFFO Estimates $2.22 $2.40

AFFO Payout Ratio (on Consensus Estimates) 99% 93%

AFFO Multiple (on Consensus Estimates) 5.7x 10.6x

Annual Distribution / Implied Yield $2.20 / 17.5% $2.24 / 8.8%

Consensus NAV Estimate $25.90 $30.72

Total Assets $1.3 billion $7.0 billion

NOI by Segment: 90% Office / 10% Industrial 98% Office

CBD / Suburban / Other Exposure as a % of NOI 65% / 23% / 12% 71% / 27% / 2%

Downtown Toronto / Calgary as a % of NOI 13% Toronto / 39% Calgary 30% Toronto / 16% Calgary

Top 5 Assets (and % of NOI)Telus Tower (7%); AIR MILES Tower(7%); McFarlane Tower (6%); 840 7th

Avenue (5%); Station Tower (5%)

Scotia Plaza (10%); 700 De la Gauchètiere (5%); Adelaide Place (4%); IBM Corp. Park (3%); Telus Tower (3%);

Geographic Distribution of NOICalgary (47%); Toronto (13%); Vancouver (9%); NWT (6%); Regina (4%); Sask (3%); SW Ontario (1%); Industrial/Other (17%)

Greater Toronto Area (44%); Calgary (19%); Yellowknife/Saskatoon/Regina (8%);

Edmonton (8%); BC (5%); Montreal (5%); SW Ont. (4%); Ottawa (4%); QC/ Atlantic

Canada (2%); Other (1%)

Reported Debt to GBV / Term / Wtd. Average Int. Rate 66% / 5.5 years / 5.8% 47.6% / 4.1 years / 4.2%

We have transformed our asset profile over the last six years, improving the stability of our cash flow and the quality of our balance sheet.

7

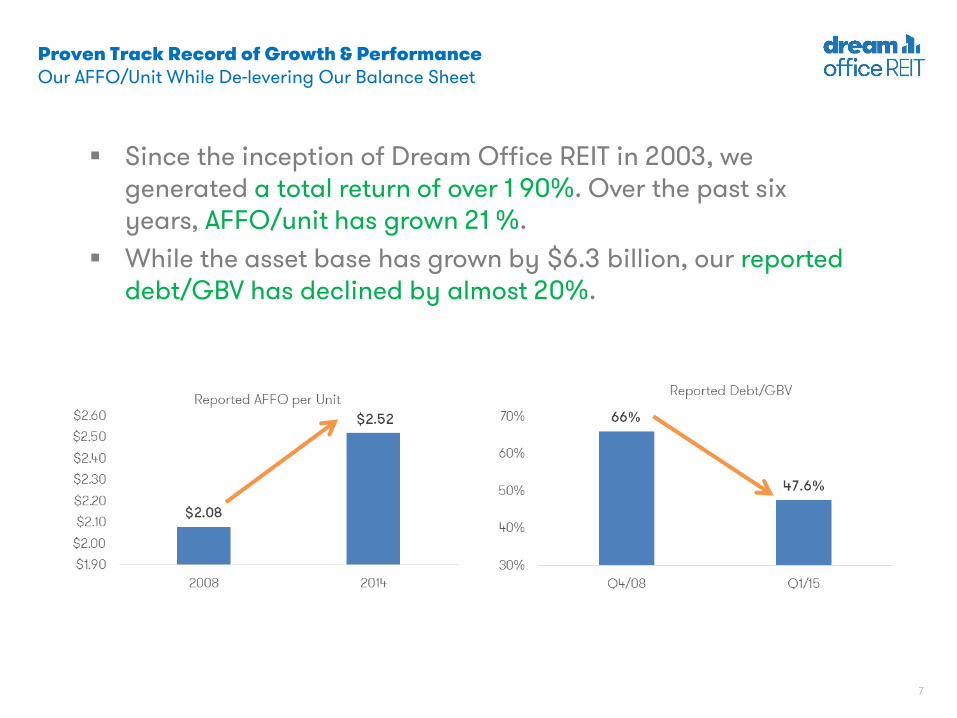

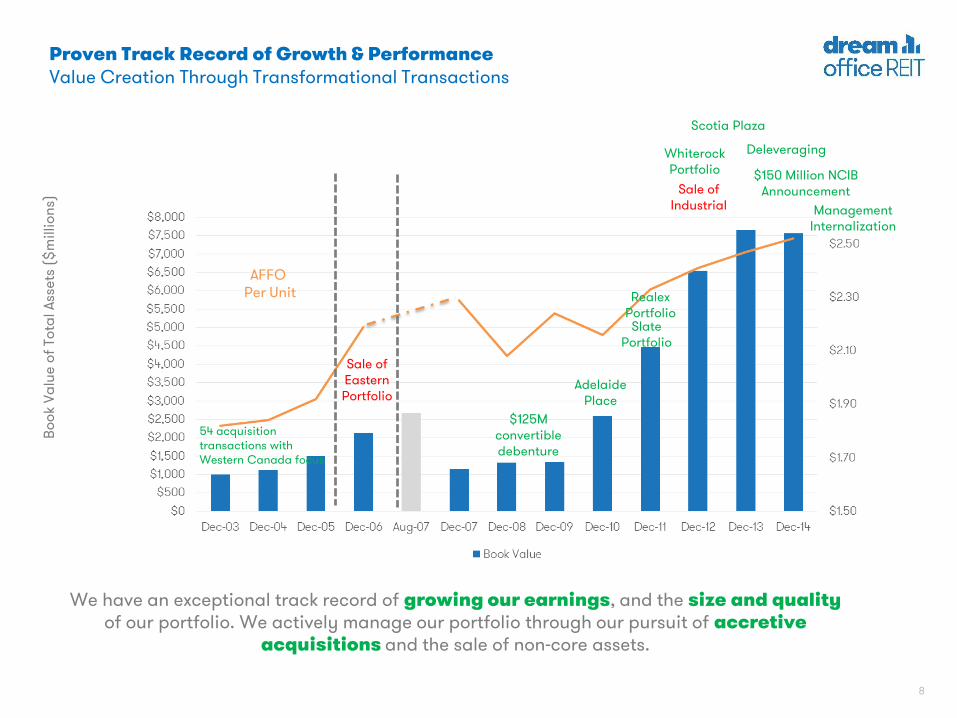

Since the inception of Dream Office REIT in 2003, we generated a total return of over 1 90%. Over the past six years, AFFO/unit has grown 21 %.

While the asset base has grown by $6.3 billion, our reported debt/GBV has declined by almost 20%.

Proven Track Record of Growth & PerformanceOur AFFO/Unit While De-levering Our Balance Sheet

8

Bo

ok

Va

lue

of

Tota

l Ass

ets

($

mil

lio

ns)

AFFO Per Unit

54 acquisition transactions with Western Canada focus

Sale ofEasternPortfolio

$125Mconvertible debenture

AdelaidePlace

SlatePortfolio

Sale ofIndustrial

Scotia Plaza

$150 Million NCIB Announcement

Proven Track Record of Growth & PerformanceValue Creation Through Transformational Transactions

WhiterockPortfolio

RealexPortfolio

We have an exceptional track record of growing our earnings, and the size and quality of our portfolio. We actively manage our portfolio through our pursuit of accretive

acquisitions and the sale of non-core assets.

Deleveraging

Management Internalization

9

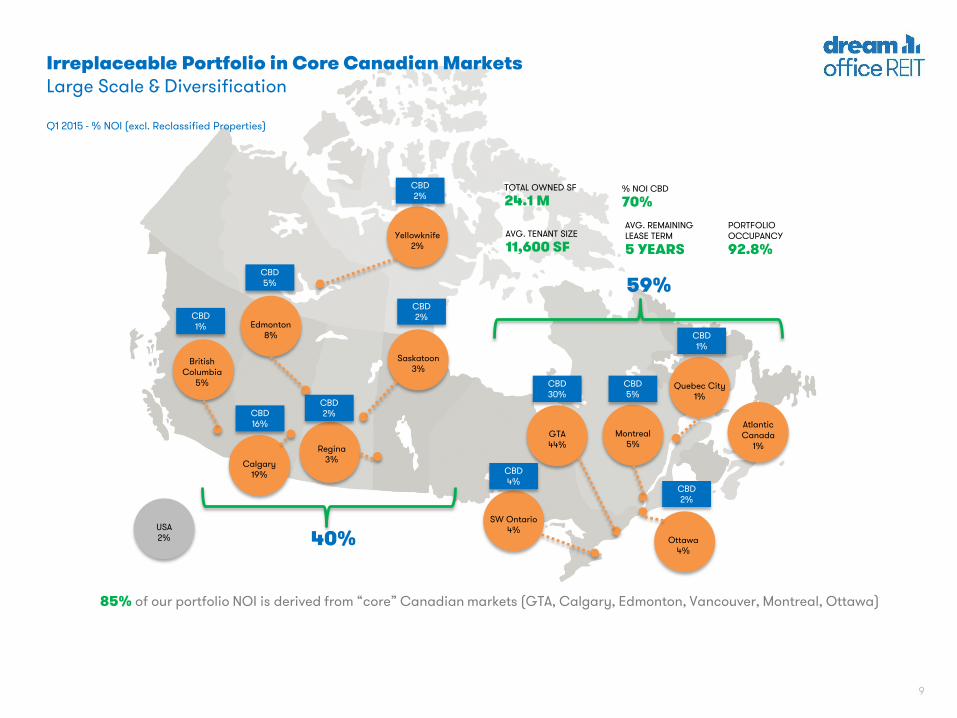

% NOI CBD

70%TOTAL OWNED SF

24.1 M

BritishColumbia

5%

Calgary19%

Yellowknife2%

Edmonton8%

Saskatoon3%

Regina3%

GTA44%

SW Ontario4%

Ottawa4%

Montreal5%

Quebec City1%

AtlanticCanada

1%

USA2%

CBD1%

CBD5%

CBD16%

CBD2%

CBD2%

CBD2%

CBD4%

CBD30%

CBD5%

CBD1%

CBD2%

40%

85% of our portfolio NOI is derived from “core” Canadian markets (GTA, Calgary, Edmonton, Vancouver, Montreal, Ottawa)

59%

AVG. TENANT SIZE

11,600 SF

AVG. REMAINING LEASE TERM

5 YEARS

PORTFOLIOOCCUPANCY

92.8%

Irreplaceable Portfolio in Core Canadian MarketsLarge Scale & Diversification

Q1 2015 - % NOI (excl. Reclassified Properties)

10

11,363

Scotia PlazaToronto (10%)

700 De la GauchetièreMontreal (5%)

Adelaide PlaceToronto (4%)

IBM Corporate ParkCalgary (3%)

Telus HouseCalgary (3%)

State Street Financial Ctr.Toronto (2%)

Enbridge PlaceEdmonton (2%)

Barclay Centre I & IICalgary (2%)

5001 Yonge StreetToronto (2%)

AIR MILES TowerToronto (2%)

655 Bay StreetToronto (1%)

HSBC Bank PlaceEdmonton (2%)

Station TowerSurrey (1%)

Irreplaceable PortfolioInstitutional Quality Assets

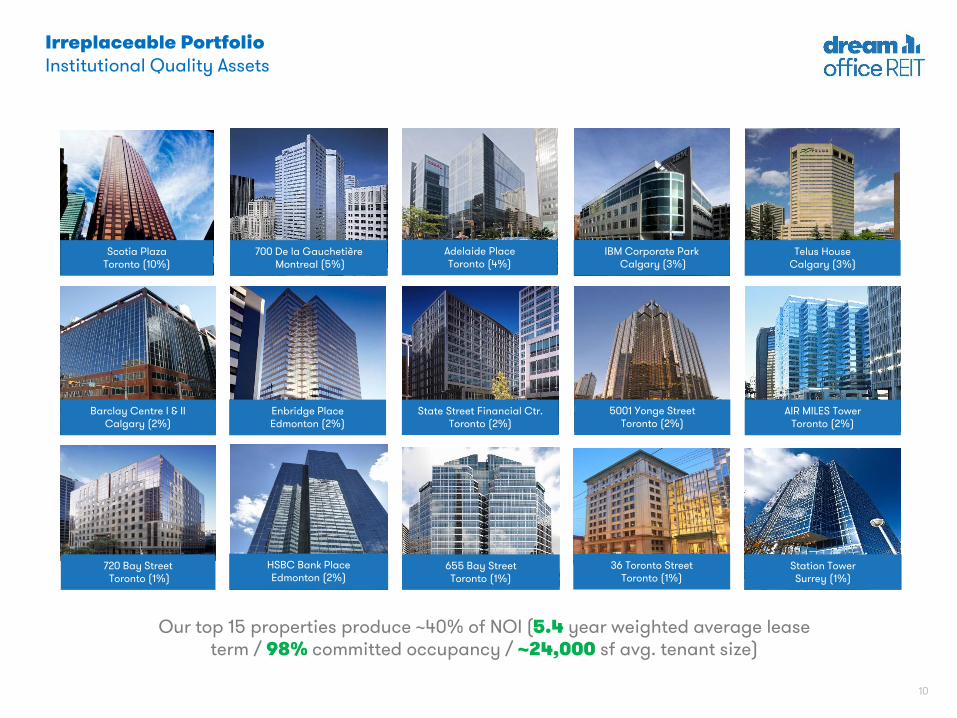

Our top 15 properties produce ~40% of NOI (5.4 year weighted average lease term / 98% committed occupancy / ~24,000 sf avg. tenant size)

36 Toronto StreetToronto (1%)

720 Bay StreetToronto (1%)

11

12

3

4

5

6

7

25

16

18

8

26

1320

9

12

10

17

14

22

2411

2123

19

15

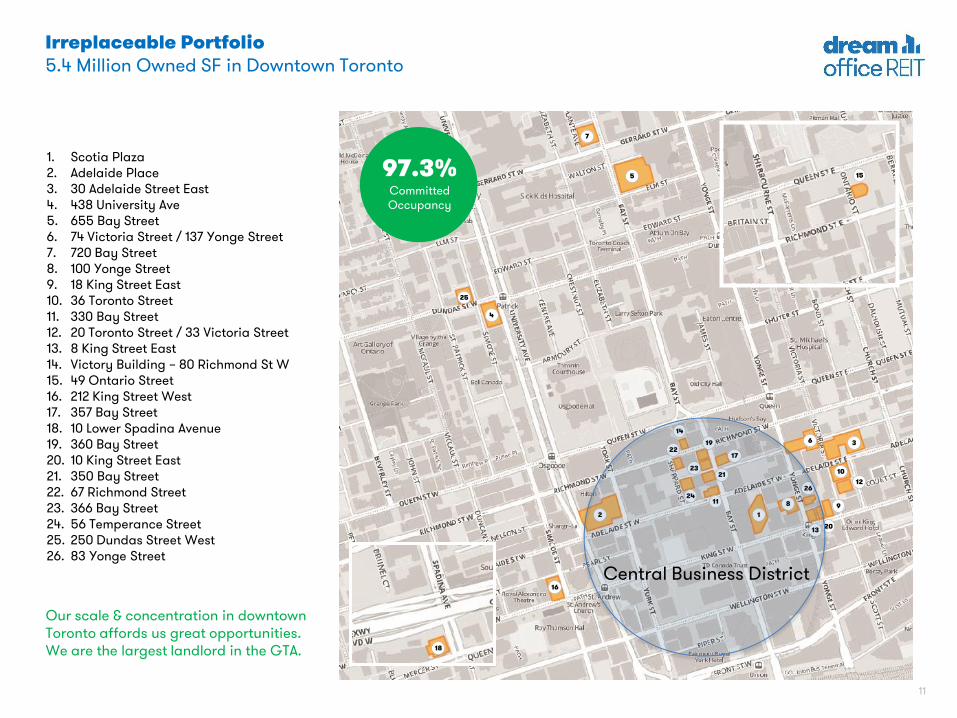

Our scale & concentration in downtown Toronto affords us great opportunities. We are the largest landlord in the GTA.

Irreplaceable Portfolio5.4 Million Owned SF in Downtown Toronto

1. Scotia Plaza2. Adelaide Place3. 30 Adelaide Street East4. 438 University Ave5. 655 Bay Street6. 74 Victoria Street / 137 Yonge Street7. 720 Bay Street8. 100 Yonge Street9. 18 King Street East10. 36 Toronto Street11. 330 Bay Street12. 20 Toronto Street / 33 Victoria Street13. 8 King Street East14. Victory Building – 80 Richmond St W15. 49 Ontario Street16. 212 King Street West17. 357 Bay Street18. 10 Lower Spadina Avenue19. 360 Bay Street20. 10 King Street East21. 350 Bay Street22. 67 Richmond Street23. 366 Bay Street24. 56 Temperance Street25. 250 Dundas Street West26. 83 Yonge Street

97.3% Committed Occupancy

Central Business District

12

Irreplaceable PortfolioPotential Benefits from Transit Proposals

ScarboroughPopulation: >600,000

*Source: StatsCan 2011 Consensus

North YorkPopulation: >650,000

MississaugaPopulation: >700,000

TorontoPopulation: >2,500,000

13

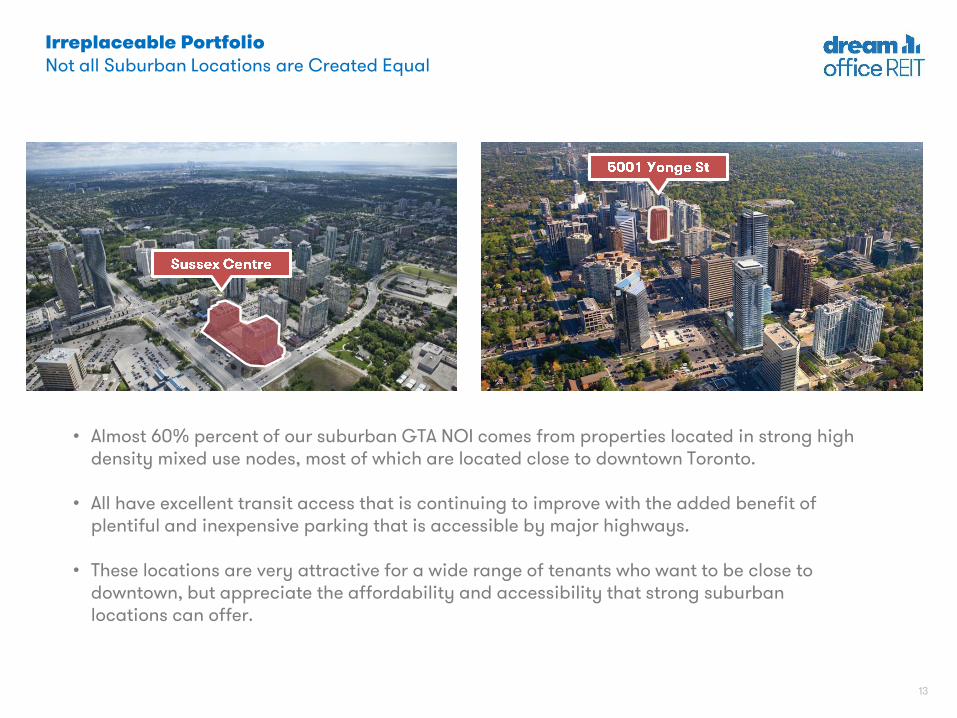

Suburb?

• Almost 60% percent of our suburban GTA NOI comes from properties located in strong high density mixed use nodes, most of which are located close to downtown Toronto.

• All have excellent transit access that is continuing to improve with the added benefit of plentiful and inexpensive parking that is accessible by major highways.

• These locations are very attractive for a wide range of tenants who want to be close to downtown, but appreciate the affordability and accessibility that strong suburban locations can offer.

Suburb?Irreplaceable PortfolioNot all Suburban Locations are Created Equal

14

• Our 427 corridor assets enjoy tremendous highway access to downtown, the airport and other key business locations in the GTA.

• This year, we introduced a shuttle bus that connects our buildings with subway and GO stations, something our competitors do not have the scale to implement.

15

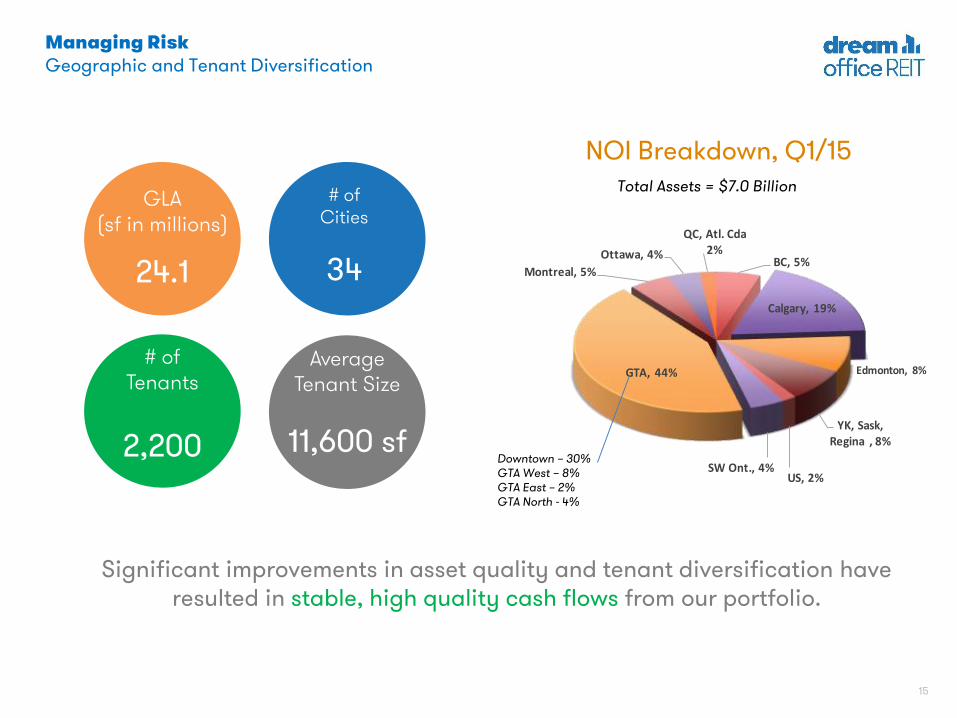

Managing RiskGeographic and Tenant Diversification

NOI Breakdown, Q1/15Total Assets = $7.0 Billion

BC, 5%

Calgary, 19%

Edmonton, 8%

YK, Sask, Regina , 8%

US, 2%SW Ont., 4%

GTA, 44%

Montreal, 5%

Ottawa, 4%

QC, Atl. Cda2%

Downtown – 30%GTA West – 8%GTA East – 2%GTA North - 4%

# of Tenants

2,200

GLA(sf in millions)

24.1

Average Tenant Size

11,600 sf

# of Cities

34

Significant improvements in asset quality and tenant diversification have resulted in stable, high quality cash flows from our portfolio.

16

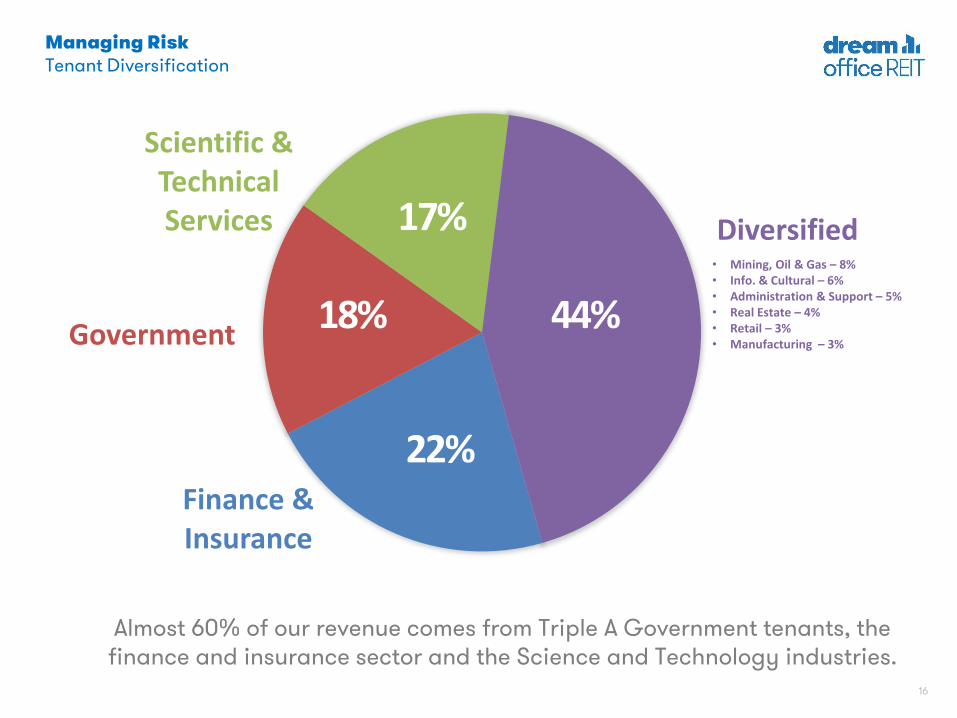

Managing RiskTenant Diversification

Almost 60% of our revenue comes from Triple A Government tenants, the finance and insurance sector and the Science and Technology industries.

Finance & Insurance

Government

Scientific & Technical Services Diversified

22%

18%

17%• Mining, Oil & Gas – 8%• Info. & Cultural – 6%• Administration & Support – 5%• Real Estate – 4%• Retail – 3%• Manufacturing – 3%

44%

17

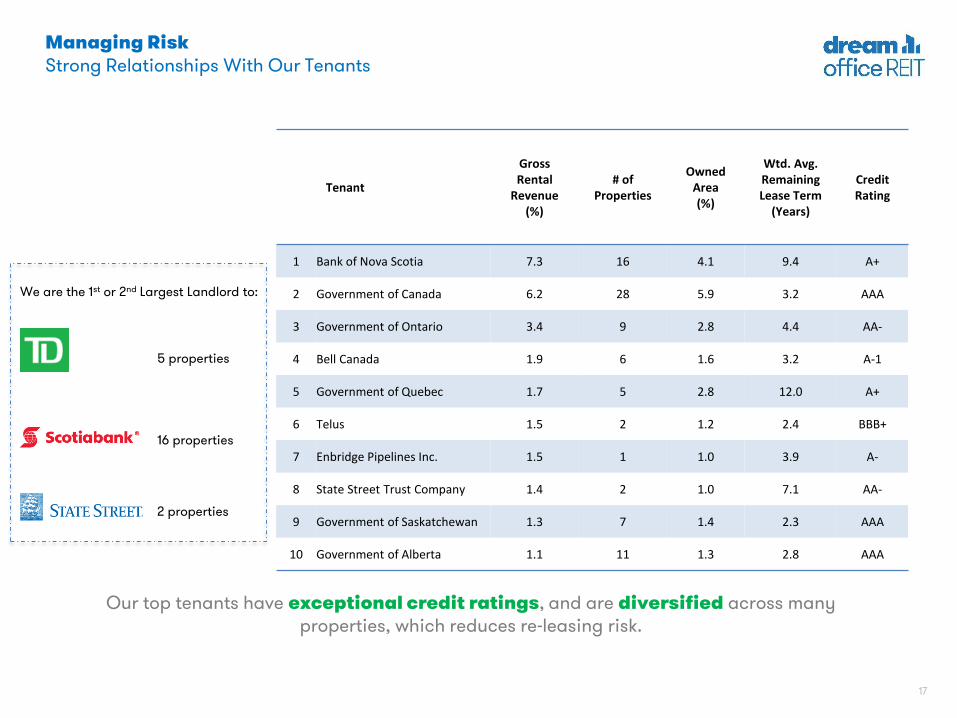

Tenant

Gross Rental

Revenue(%)

# of Properties

Owned Area(%)

Wtd. Avg. Remaining Lease Term

(Years)

CreditRating

1 Bank of Nova Scotia 7.3 16 4.1 9.4 A+

2 Government of Canada 6.2 28 5.9 3.2 AAA

3 Government of Ontario 3.4 9 2.8 4.4 AA-

4 Bell Canada 1.9 6 1.6 3.2 A-1

5 Government of Quebec 1.7 5 2.8 12.0 A+

6 Telus 1.5 2 1.2 2.4 BBB+

7 Enbridge Pipelines Inc. 1.5 1 1.0 3.9 A-

8 State Street Trust Company 1.4 2 1.0 7.1 AA-

9 Government of Saskatchewan 1.3 7 1.4 2.3 AAA

10 Government of Alberta 1.1 11 1.3 2.8 AAA

Managing RiskStrong Relationships With Our Tenants

Our top tenants have exceptional credit ratings, and are diversified across many properties, which reduces re-leasing risk.

We are the 1st or 2nd Largest Landlord to:

5 properties

16 properties

2 properties

18

-

2,000,000

4,000,000

6,000,000

8,000,000

1 0,000,000

1 2,000,000

2015 2016 2017 2018 2019 2020+

Expiries of tenants > 1 00k sf Expiries of tenants < 1 00k sf

*Market rents are estimates only and are based on current market rents with no allowance for increases in future years. Subject to changes in market conditions.

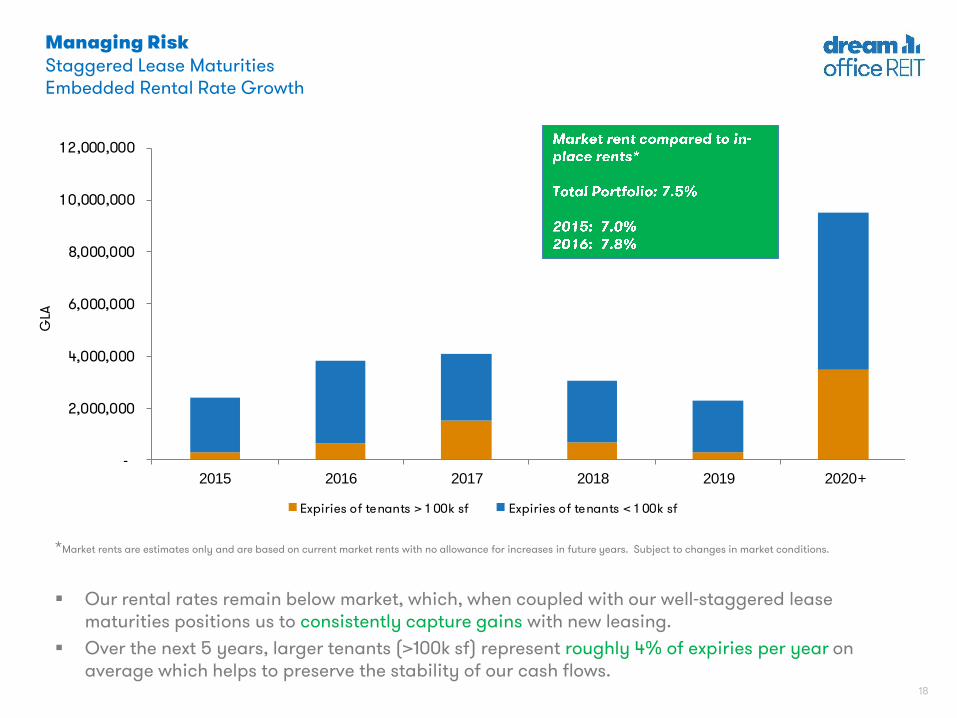

Managing RiskStaggered Lease MaturitiesEmbedded Rental Rate Growth

Our rental rates remain below market, which, when coupled with our well-staggered lease maturities positions us to consistently capture gains with new leasing.

Over the next 5 years, larger tenants (>100k sf) represent roughly 4% of expiries per year on average which helps to preserve the stability of our cash flows.

GLA

19

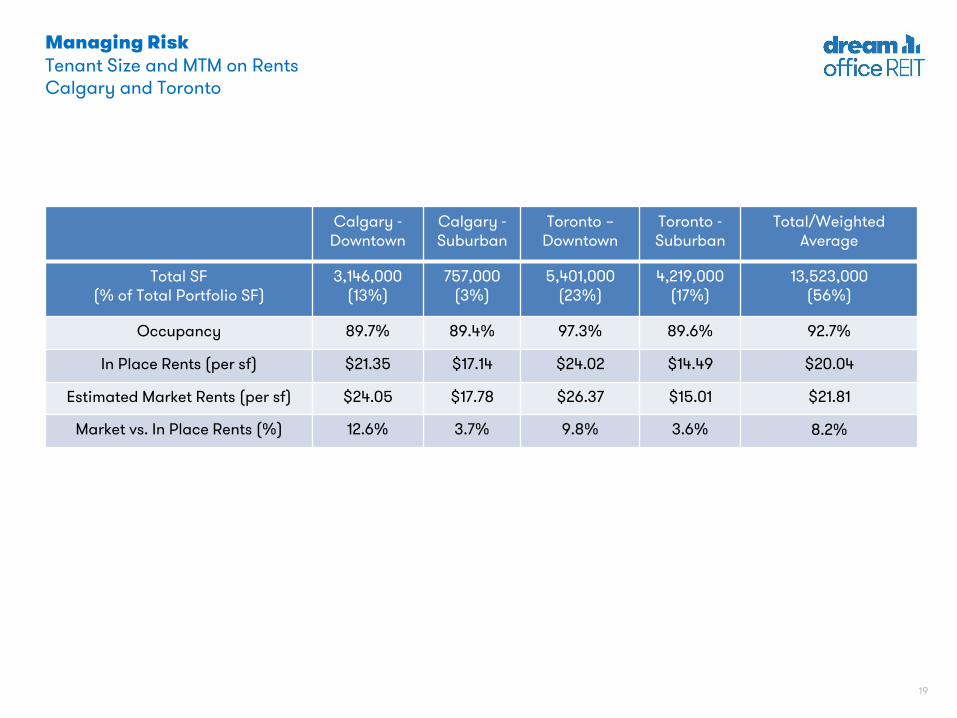

Managing RiskTenant Size and MTM on RentsCalgary and Toronto

6,000 SF

4,200 SF

7,400 SF

3,800 SF

13,000 SF

5,800 SF

6,300 SF

9,400 SF

7,200 SF

AverageTenant

Size

Calgary -Downtown

Calgary -Suburban

Toronto –Downtown

Toronto -Suburban

Total/Weighted Average

Total SF (% of Total Portfolio SF)

3,146,000 (13%)

757,000 (3%)

5,401,000 (23%)

4,219,000 (17%)

13,523,000(56%)

Occupancy 89.7% 89.4% 97.3% 89.6% 92.7%

In Place Rents (per sf) $21.35 $17.14 $24.02 $14.49 $20.04

Estimated Market Rents (per sf) $24.05 $17.78 $26.37 $15.01 $21.81

Market vs. In Place Rents (%) 12.6% 3.7% 9.8% 3.6% 8.2%

20

86%

88%

90%

92%

94%

96%

98%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q1/15

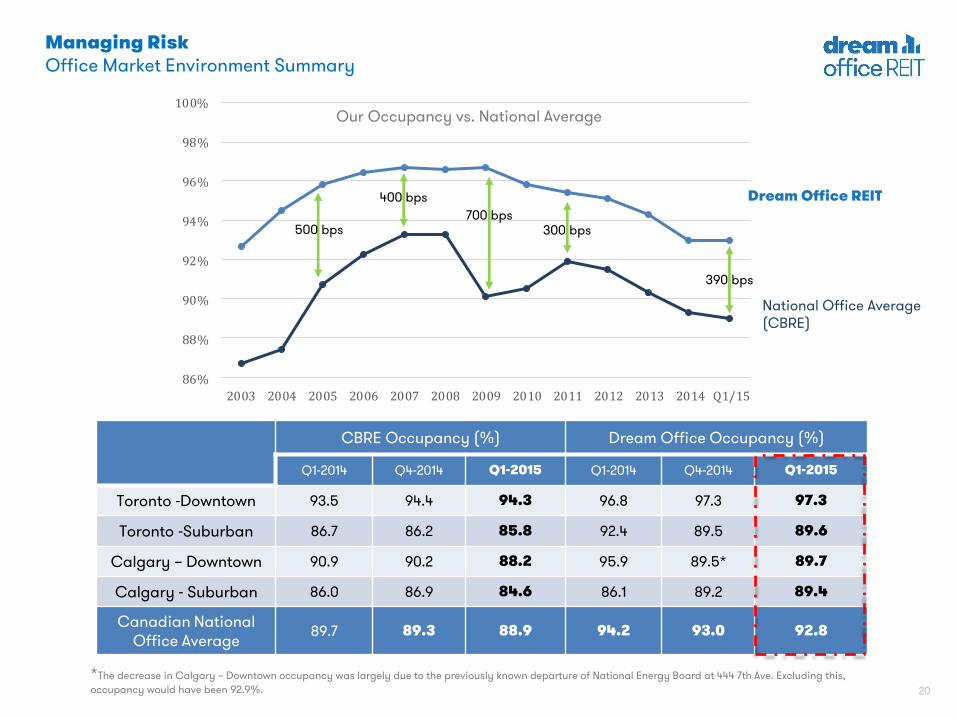

Managing RiskOffice Market Environment Summary

Net Absorption1.4 M sq. ft.

Development Pipeline

22.3 M sq. ft.

CBRE Occupancy (%) Dream Office Occupancy (%)

Q1-2014 Q4-2014 Q1-2015 Q1-2014 Q4-2014 Q1-2015

Toronto -Downtown 93.5 94.4 94.3 96.8 97.3 97.3

Toronto -Suburban 86.7 86.2 85.8 92.4 89.5 89.6

Calgary – Downtown 90.9 90.2 88.2 95.9 89.5* 89.7

Calgary - Suburban 86.0 86.9 84.6 86.1 89.2 89.4

Canadian National Office Average

89.7 89.3 88.9 94.2 93.0 92.8

Our Occupancy vs. National Average

700 bps

390 bps

300 bps500 bps

Dream Office REIT400 bps

National Office Average(CBRE)

*The decrease in Calgary – Downtown occupancy was largely due to the previously known departure of National Energy Board at 444 7th Ave. Excluding this,

occupancy would have been 92.9%.

21

0

200

400

600

800

1,000

1,200

1,400

1,600

2015 2016 2017 2018 2019 2020+

Calgary Downtown Calgary Suburban Edmonton Downtown Edmonton Suburban

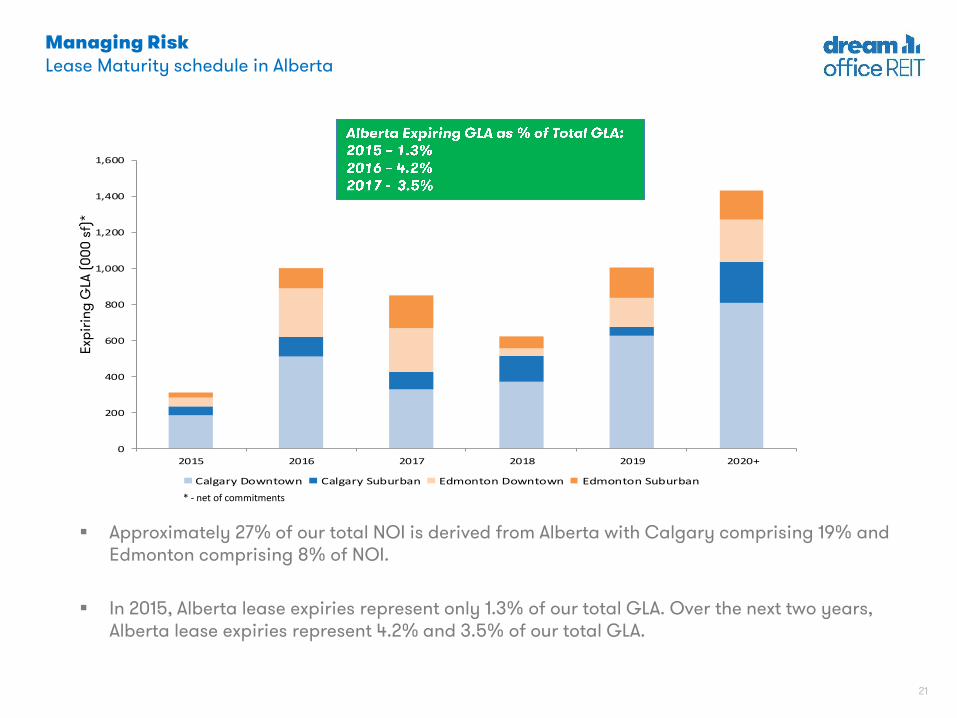

Managing RiskLease Maturity schedule in Alberta

Approximately 27% of our total NOI is derived from Alberta with Calgary comprising 19% and Edmonton comprising 8% of NOI.

In 2015, Alberta lease expiries represent only 1.3% of our total GLA. Over the next two years, Alberta lease expiries represent 4.2% and 3.5% of our total GLA.

Exp

irin

g G

LA (

00

0 s

f)*

* - net of commitments

22

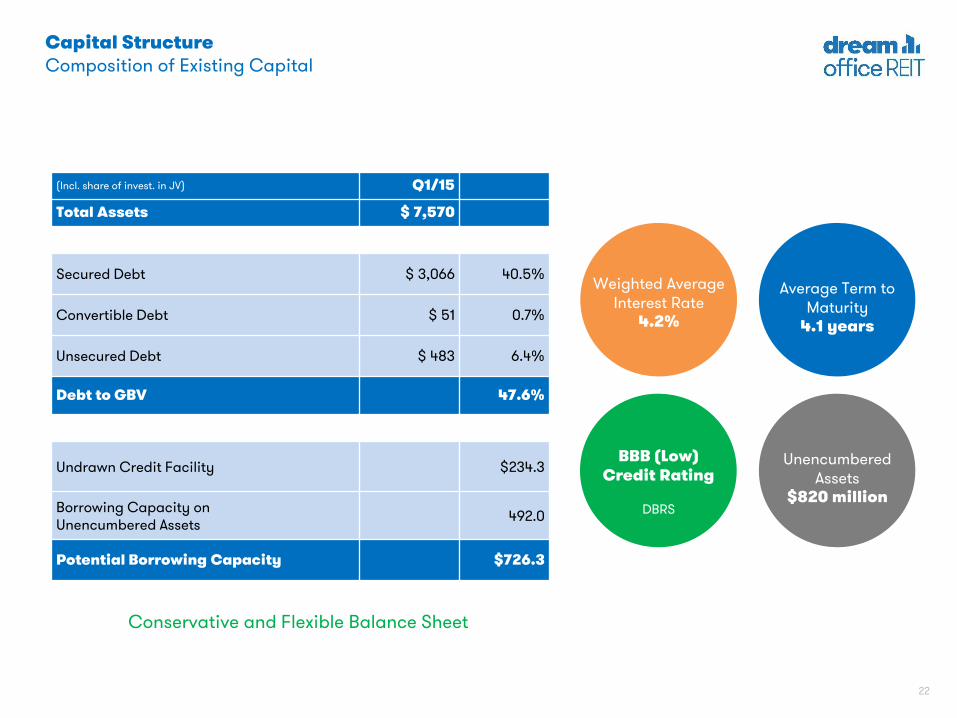

BBB (Low)Credit Rating

DBRS

(Incl. share of invest. in JV) Q1/15

Total Assets $ 7,570

Secured Debt $ 3,066 40.5%

Convertible Debt $ 51 0.7%

Unsecured Debt $ 483 6.4%

Debt to GBV 47.6%

Undrawn Credit Facility $234.3

Borrowing Capacity on Unencumbered Assets

492.0

Potential Borrowing Capacity $726.3

Weighted Average Interest Rate

4.2%

Average Term to Maturity

4.1 years

Capital StructureComposition of Existing Capital

Conservative and Flexible Balance Sheet

Unencumbered Assets

$820 million

23

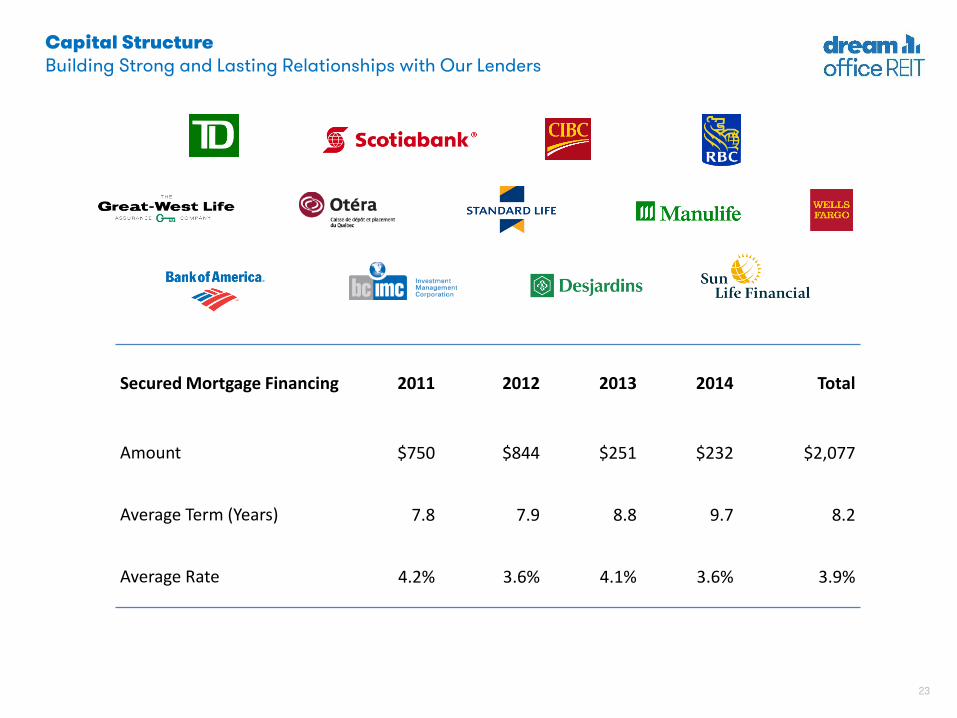

Capital StructureBuilding Strong and Lasting Relationships with Our Lenders

Secured Mortgage Financing 2011 2012 2013 2014 Total

Amount $750 $844 $251 $232 $2,077

Average Term (Years) 7.8 7.9 8.8 9.7 8.2

Average Rate 4.2% 3.6% 4.1% 3.6% 3.9%

24

4.0%

4.4%4.5%

3.9%

3.3%

4.3%

5.2%

4.2%

4.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

0

100

200

300

400

500

600

700

2015 2016 2017 2018 2019 2020 2021 2022 2023+

Unsecured Secured Weighted Average Face Rate

Tota

l De

bt

Ma

turi

tie

s ($

mil

lio

ns)

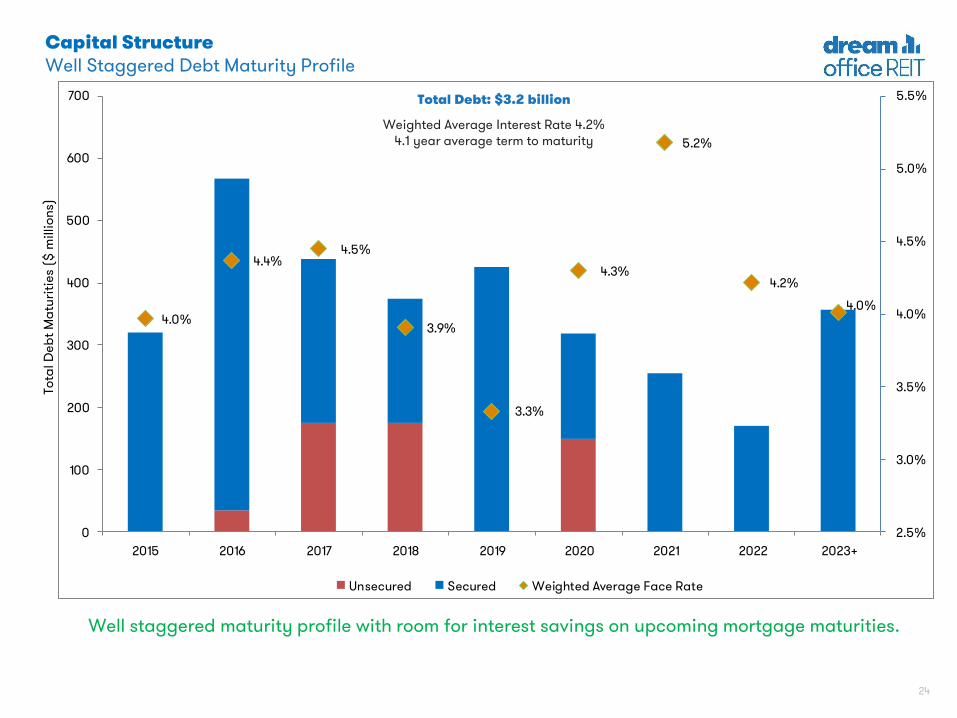

Weighted Average Interest Rate 4.2%4.1 year average term to maturity

Capital StructureWell Staggered Debt Maturity Profile

Well staggered maturity profile with room for interest savings on upcoming mortgage maturities.

Total Debt: $3.2 billion

25

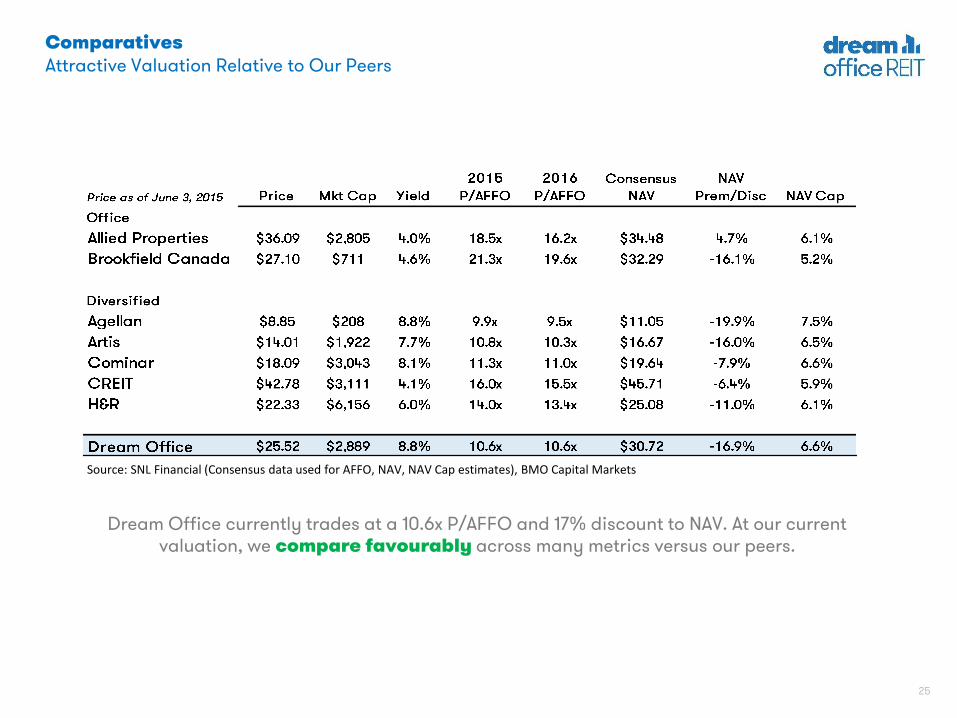

ComparativesAttractive Valuation Relative to Our Peers

Dream Office currently trades at a 10.6x P/AFFO and 17% discount to NAV. At our current valuation, we compare favourably across many metrics versus our peers.

Source: SNL Financial (Consensus data used for AFFO, NAV, NAV Cap estimates), BMO Capital Markets

26

Current Capital InitiativesCreating Value for our Unitholders

Active NCIB: We have repurchased $58 million of REIT units (or 2.2million units) to date and we plan to repurchase approximately $150million. We expect the program to be AFFO accretive on a steady-statebasis

Proactively investing in our buildings: For 2015, we plan to invest$75 million in building improvements, our largest annual investmentin our history

Active Disposition Pipeline: We are targeting $300 million in non-core property dispositions for the year, including a $150 millionportfolio in Eastern Canada, which we have recently brought to market.Net proceeds will be used to fund our NCIB program

We will continue to seek creative methods to close the value gap between the trading value of our units and their fair value.

1

2

3

27

At current valuation, with our current portfolio, management team and strategy, we believe we are a very compelling investment.

The Current Opportunity

Dream Office REIT is currently generating a 8.8% cash yield and an 8%+ AFFOyield (on consensus estimates)

We are conservatively financed in our view with our current debt to gross book

value ratio of approximately 47.6% We own a collection of assets that are hard to replicate, with our portfolio quality at

its best in our history We believe that our ability to meet tenants’ needs in our portfolio, our relationships

and our contracts with tenants will help us outperform whatever benchmarks may beapplicable

Furthermore, we believe that with our scale and dedicated management team, wewill continue to generate increased and new sources of income

28

Appendix: Value Creation

29

Case Study

Suburban Modernization

Sussex Centre

Value CreationRepositioning Scotia Plaza

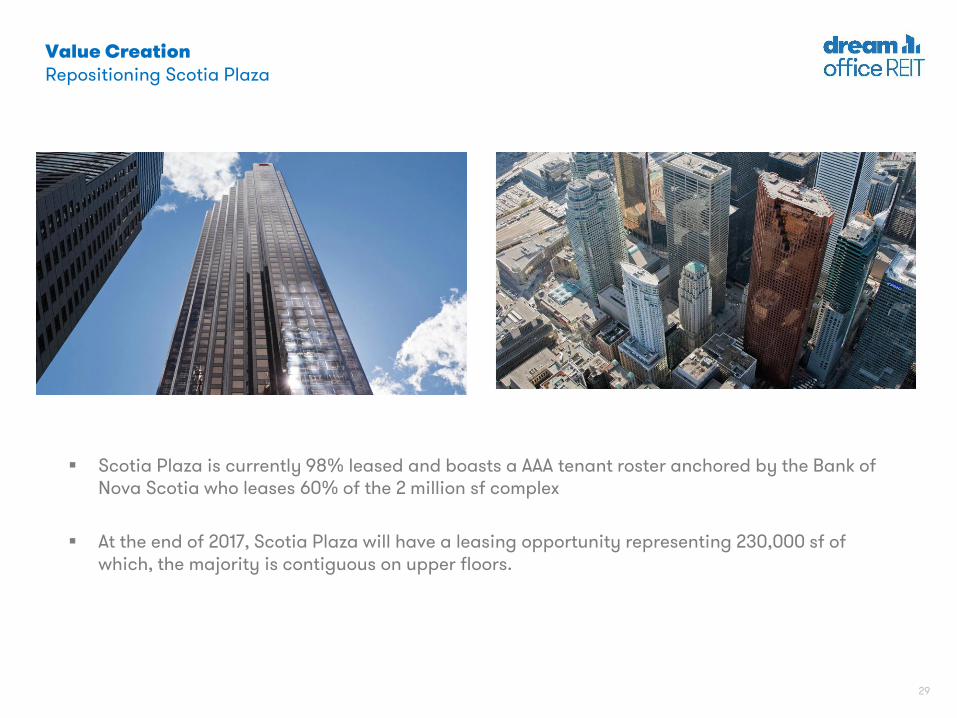

Scotia Plaza is currently 98% leased and boasts a AAA tenant roster anchored by the Bank of Nova Scotia who leases 60% of the 2 million sf complex

At the end of 2017, Scotia Plaza will have a leasing opportunity representing 230,000 sf of which, the majority is contiguous on upper floors.

30

Case Study

Suburban Modernization

Sussex Centre

Value CreationRepositioning Scotia Plaza

We are rebranding Scotia Plaza with a three year capital plan that includes an $80M investment into state of the art systems, sustainability and common areas all targeted towards a superior tenant experience.

The first major capital project to kick off at Scotia Plaza is one directly linked to the needs of our tenant. We have commenced what will be the largest elevator modernization project in North America and have partnered with Schindler, a global leader in elevator technology.

Scotia Plaza will benefit from the same state of the art technology used in WTC4, Rockefeller Centre and The ICC Building in Hong Kong.

Over the next three years, we are revitalizing the main lobby, PATH, food-court and exterior forecourts on the King and Adelaide Street entrances.

31

Case Study

Suburban Modernization

Sussex Centre

Value CreationRepositioning Scotia Plaza

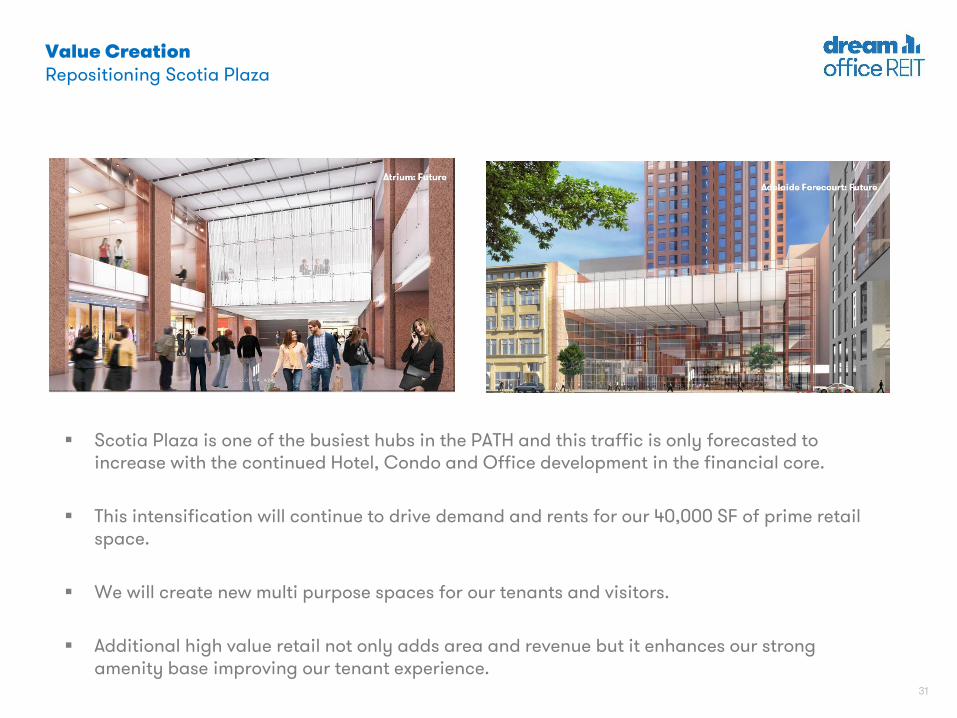

Scotia Plaza is one of the busiest hubs in the PATH and this traffic is only forecasted to increase with the continued Hotel, Condo and Office development in the financial core.

This intensification will continue to drive demand and rents for our 40,000 SF of prime retail space.

We will create new multi purpose spaces for our tenants and visitors.

Additional high value retail not only adds area and revenue but it enhances our strong amenity base improving our tenant experience.

32

Case Study

Suburban Modernization

Sussex Centre

Value CreationSuburban Modernization – Sussex Centre

Mississauga City Centre is home to four million square feet of office space as well as Square One, one of Canada’s largest shopping centres.

Sussex Centre is a key element of the City Centre and is surrounded by the highest residential density in Mississauga, Canada’s 6th largest city.

33

Case Study

Suburban Modernization

Sussex Centre

Value CreationSuburban Modernization – Sussex Centre

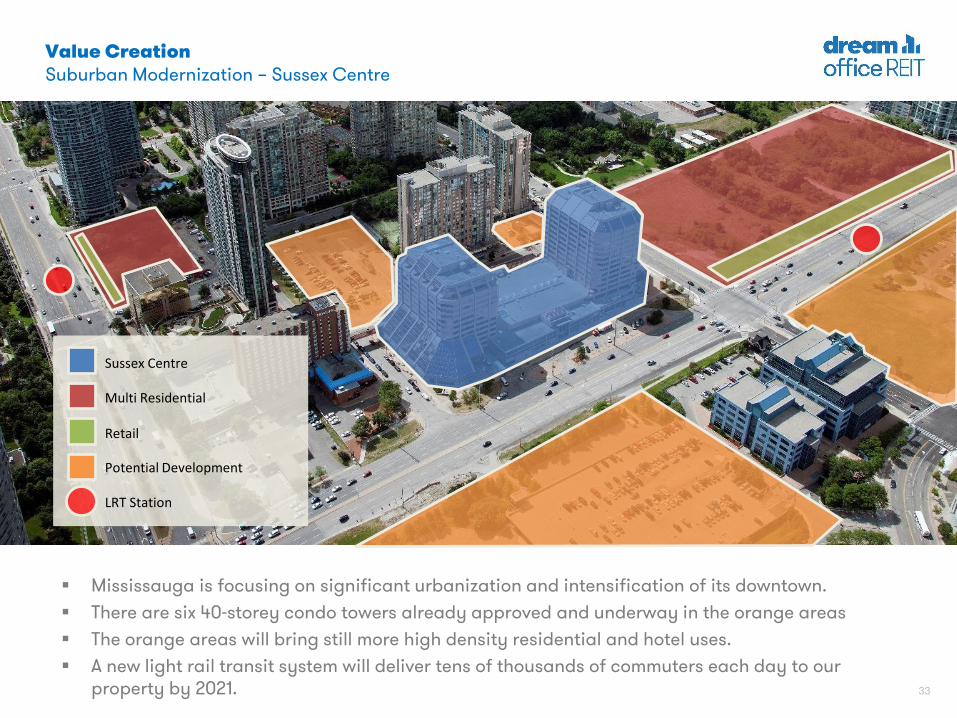

Mississauga is focusing on significant urbanization and intensification of its downtown.

There are six 40-storey condo towers already approved and underway in the orange areas

The orange areas will bring still more high density residential and hotel uses.

A new light rail transit system will deliver tens of thousands of commuters each day to our property by 2021.

Multi Residential

Retail

LRT Station

Potential Development

Sussex Centre

34

To complement these changes and bring in new tenants, we invested in LEED Gold certification for Sussex Centre.

We are upgrading tenant floors, taking advantage of underutilized space to create new amenities that will complement the changing way our tenants work, including shared board rooms, new lobby furniture and WIFI to create collaborative, casual work places.

After achieving LEED Gold in January 2014, occupancy improved from 75.5% to 84.8%. We expect to achieve 90% occupancy in 2016 and to drive stabilized occupancy to 95% or greater in 2017 following the remaining upgrades.

Value CreationSuburban Modernization – Sussex Centre

35

Our 1 million SF of retail space generates $24.5 million of NOI or 5.5% of our total NOI. As retail tenants seek more urban exposure, this presents an opportunity to:

• Grow existing rents

• Re-lease existing retail to best uses

• Re-purpose office and storage space to retail in CBD

• Add retail pads to suburban sites

Value CreationRetail Successes & Opportunities

36

Opportunities to Re-Purpose CBD space

Scotia PlazaCreation on 3,000 to 5,000 sf of new high value retail premises

8 King EastGround Floor and Lower Level Retail

357 Bay StreetGround & 2nd Floor Retail

700 De la GauchetièrePursuing new fitness centre in 10,000 sf of lower level storage

Value CreationCBD Retail Opportunities

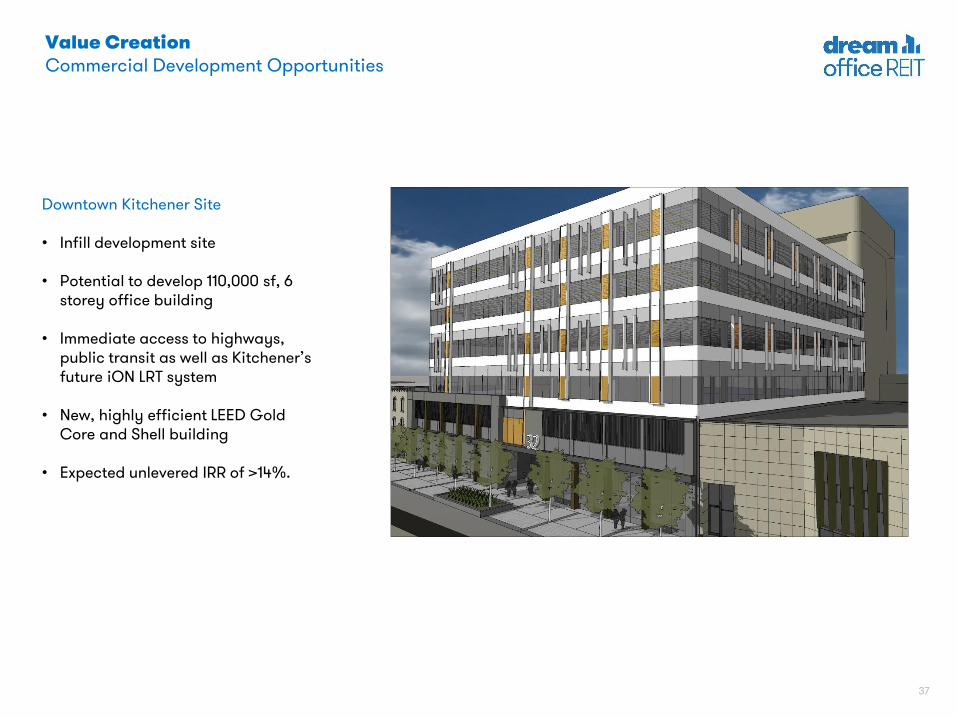

37

Downtown Kitchener Site

• Infill development site

• Potential to develop 110,000 sf, 6 storey office building

• Immediate access to highways, public transit as well as Kitchener’s future iON LRT system

• New, highly efficient LEED Gold Core and Shell building

• Expected unlevered IRR of >14%.

Value CreationCommercial Development Opportunities

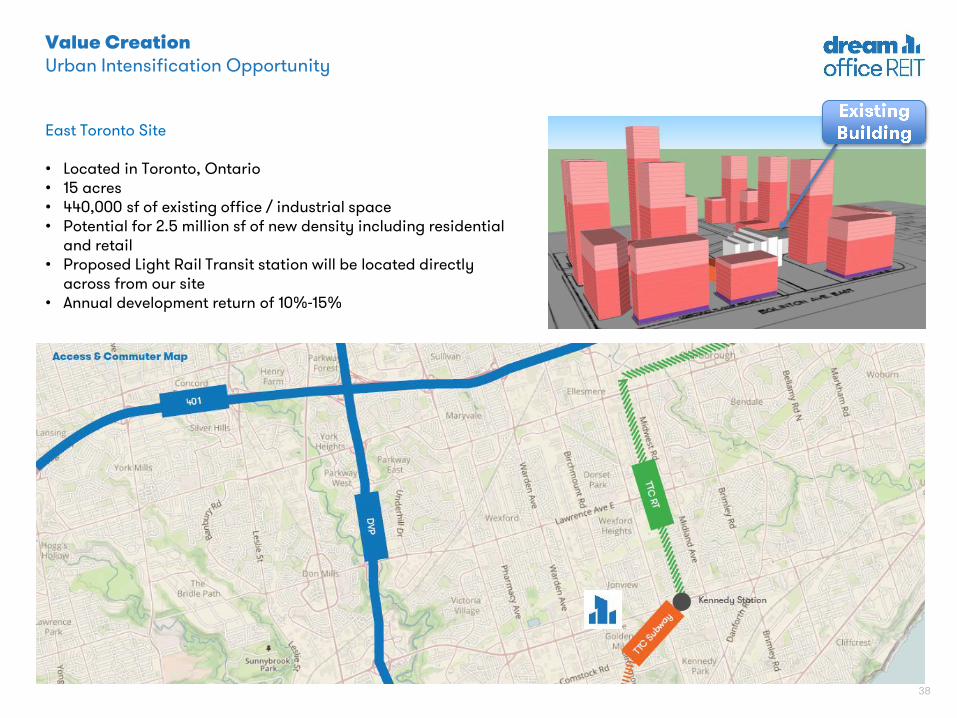

38

Value CreationUrban Intensification Opportunity

East Toronto Site

• Located in Toronto, Ontario• 15 acres• 440,000 sf of existing office / industrial space• Potential for 2.5 million sf of new density including residential

and retail• Proposed Light Rail Transit station will be located directly

across from our site• Annual development return of 10%-15%

39

40

Forward Looking Information

This slide presentation contains forward looking information within the meaning of

applicable securities legislation. Forward looking information is based on a number of

assumptions and is subject to a number of risks and uncertainties, many of which are

beyond Dream Office REIT's control, that could cause actual results to differ materially

from those that are disclosed in or implied by such forward looking information. These

risks and uncertainties include, but are not limited to, general and local economic and

business conditions; the financial condition of tenants; our ability to refinance maturing

debt; leasing risks, including those associated with the ability to lease vacant space. All

forward looking information in this presentation speaks as of June 3, 2015. Dream

Office REIT does not undertake to update any such forward looking information whether

as a result of new information, future events or otherwise. Additional information about

these assumptions and risks and uncertainties is disclosed in filings with securities

regulators filed on SEDAR (www.sedar.com).

![[Perforce] Perforce the Plentiful Platform](https://img.pdfslide.us/doc/110x75/5484017e5806b5bd588b45b9/perforce-perforce-the-plentiful-platform.jpg)