Embed Size (px)

Citation preview

KCA Deutag is a leading international

drilling and engineering company

working onshore and offshore with

a focus on safety, quality and

operational performance

Investor Presentation

SECOND QUARTER 2019

0

Disclaimer

1

The distribution of this presentation in certain jurisdictions may be restricted by law.Persons into whose possession this presentation comes are required to informthemselves about and to observe any such restrictions.

This presentation contains forward-looking statements concerning KCADeutag. These forward-looking statements are based on management’s currentexpectations, estimates and projections. They are subject to a number ofassumptions and involve known and unknown risks, uncertainties and other factorsthat may cause actual results and developments to differ materially from any futureresults and developments expressed or implied by such forward-lookingstatements. KCA Deutag has no obligation to periodically update or release anyrevisions to the forward-looking statements contained in this presentation to reflectevents or circumstances after the date of this presentation.

Agenda

2

Second Quarter Investor Presentation

1 Q2 Key Highlights

2 Operational Highlights

3 Business Update

4 Business Unit Financials

5 Group Results

6 Summary

Q2 Key Highlights

3

Q2 2019 revenue of $395.1m (Q2 2018: $292.8m) and EBITDA of $74.4m (Q2 2018: $50.3m)

Bentec successfully delivered the final 3 rigs for our customer in Ukraine

Operational integration of the former Dalma business now complete with synergies of $27.6m identified

and 89% of these already secured

4 Land Drilling awarded a number of new contracts in the Middle East, Russia, Europe and Africa

Contract backlog of $5.4bn (at 1 August 2019) across a blue chip customer base

Significant progress made on our technology initiative, Well of Innovation, with launch in September

Financial results noted above include results from the Dalma business which was acquired 30 April 2018

2018 results restated in compliance with IFRS 16

1

2

3

4

5

6

KCA Deutag Operations are Diversified Across Global Markets

London Bad Bentheim

Tyumen

Nizwa

St. Johns

Bergen

Dubai

Land Drilling Offshore Services RDS offices BentecRegional offices

Aberdeen (HQ)

North Sea

/Norway

18 Plat

Europe &

Caspian

7 Rigs

Caspian

7 Plat

Russia

17 Rigs

Middle

East

41 Rigs

Angola

2 Plat

Africa

11 Rigs

Brunei

1 Rig

Canada

1 Plat

Map shows position at 1 August 2019

(1) The % split of LTM EBITDA is calculated using total KCAD group Q2 2019 LTM Proforma EBITDA of $306m (after corporate

costs of $16m)

Russia

Sakhalin

3 Plat

PRESENCE IN KEY AREAS

131

60 5545

20

0

30

60

90

120

150

Europe North Africa Middle East North Sea Russia

Ye

ars

4

Geographical EBITDA Split(1)

Baku

Market Outlook By Business Unit

5

Business Units Outlook

Land Drilling

New contract awards and extensions in Middle East, Russia, Europe and Africa

Tendering has levelled out though remains steady

Pricing remains competitive

Utilisation levels steadily increasing

Bentec Tendering activity continues in a very competitive and difficult market

Offshore Services Activity remains steady with some reactivation discussions

RDS

New Greenfield and Brownfield tendering opportunities but very slow conversion rates

Greater investment in the industry required to provide meaningful uptick

Targeting diversification in the FPSO, Subsea, Wind and Decommissioning sectors

• Recent decline in oil price and continued volatility driven by concerns around a global

slowdown with continued uncertainty

• A very challenging landscape where our customers continue to maintain a low pricing

environment coupled with ongoing local cost pressures

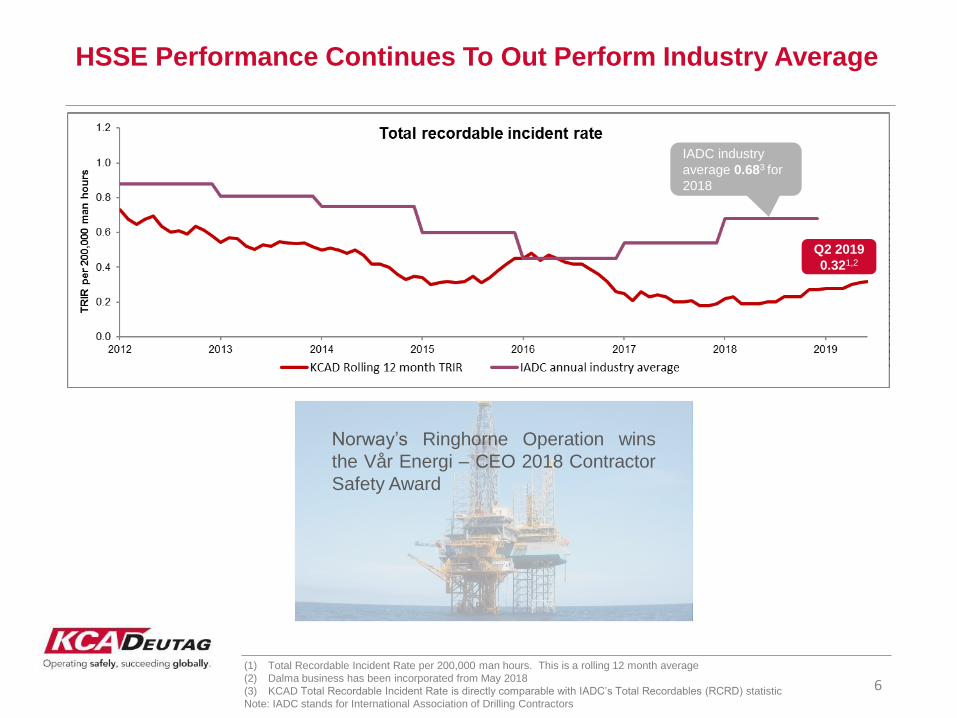

HSSE Performance Continues To Out Perform Industry Average

6

(1) Total Recordable Incident Rate per 200,000 man hours. This is a rolling 12 month average

(2) Dalma business has been incorporated from May 2018

(3) KCAD Total Recordable Incident Rate is directly comparable with IADC’s Total Recordables (RCRD) statistic

Note: IADC stands for International Association of Drilling Contractors

Q2 2019

0.321,2

IADC industry

average 0.683 for

2018

Norway’s Ringhorne Operation wins

the Vår Energi – CEO 2018 Contractor

Safety Award

A Well of Innovation

7

• Upcoming September 2019 launch of KCA Deutag’s “Well of Innovation” marketing campaign and our

exciting new +veDRILL technology brand

• Sitting underneath this, there are six product ranges. These address the main issues and challenges

that our customers face and that our technology can help them solve.

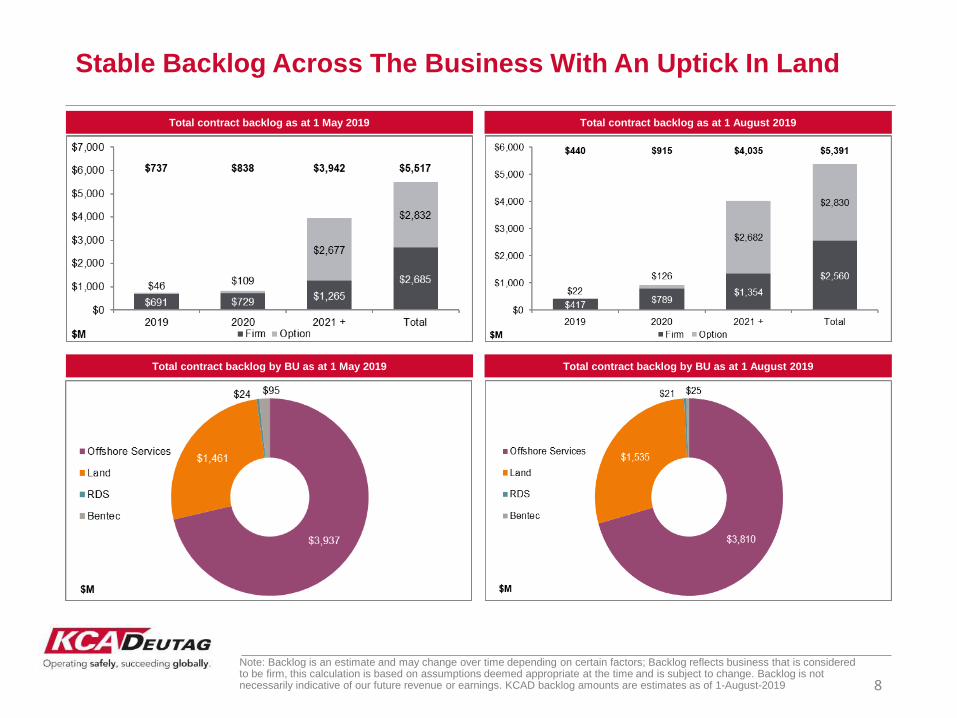

Stable Backlog Across The Business With An Uptick In Land

Note: Backlog is an estimate and may change over time depending on certain factors; Backlog reflects business that is considered to be firm, this calculation is based on assumptions deemed appropriate at the time and is subject to change. Backlog is not necessarily indicative of our future revenue or earnings. KCAD backlog amounts are estimates as of 1-August-2019 8

Total contract backlog as at 1 August 2019

Total contract backlog by BU as at 1 August 2019

Total contract backlog as at 1 May 2019

Total contract backlog by BU as at 1 May 2019

Long Term Offshore Services Contract Backlog(1)

9

(1) Contract and rig status shown as at 1 August 2019

Firm

Options

Not Disclosed

Contract Platform

Client Country Assets Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 end date status #

Exxon Canada Hebron Mar-46 Operating 1

Equinor (Statoil) Norway CAT J (2) May-36 Operating 2

Equinor (Statoil) Norway Oseberg's (4) & Kvitebjorn Oct-28 Operating / Stacked 3/2

AIOC Azerbaijan Azeris, SD, DWG, Cop & Chirag Apr-26 Operating 7

Vår Energi Norway Ringhorne Dec-25 Operating 1

Enquest UK Thistle, Heather & Magnus Dec-25 Operating / Stacked 1/2

CNOOC UK Scott Feb-25 Operating 1

Exxon Angola Kizomba (2) Jan-24 Stacked 2

Total UK Alwyn / Dunbar May-23 Operating / Stacked 1/1

Chrysaor (COP) UK Britannia Nov-22 Stacked 1

Equinor (Statoil) Norway Pipe pool management Nov-22 Active mgmt. contract

CNR UK Ninian's (2) Tiffany Nov-21 Operating / Stacked 1/2

SEIC Russia LA, PA & PB May-21 Operating 3

2019 2020 2021

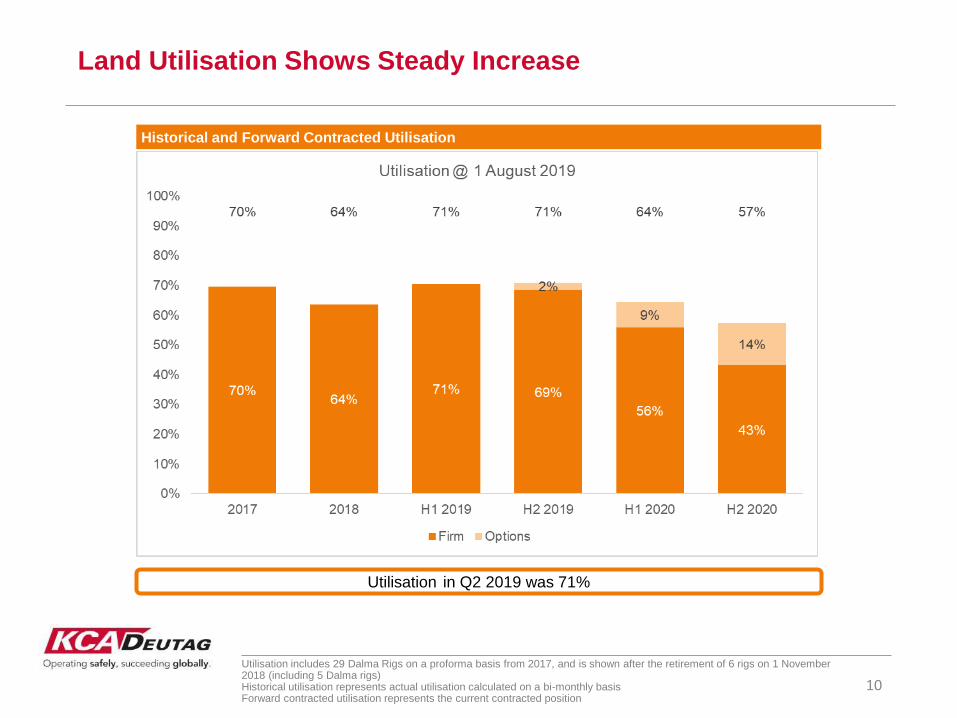

Utilisation includes 29 Dalma Rigs on a proforma basis from 2017, and is shown after the retirement of 6 rigs on 1 November 2018 (including 5 Dalma rigs)Historical utilisation represents actual utilisation calculated on a bi-monthly basisForward contracted utilisation represents the current contracted position

Land Utilisation Shows Steady Increase

10

Historical and Forward Contracted Utilisation

Utilisation in Q2 2019 was 71%

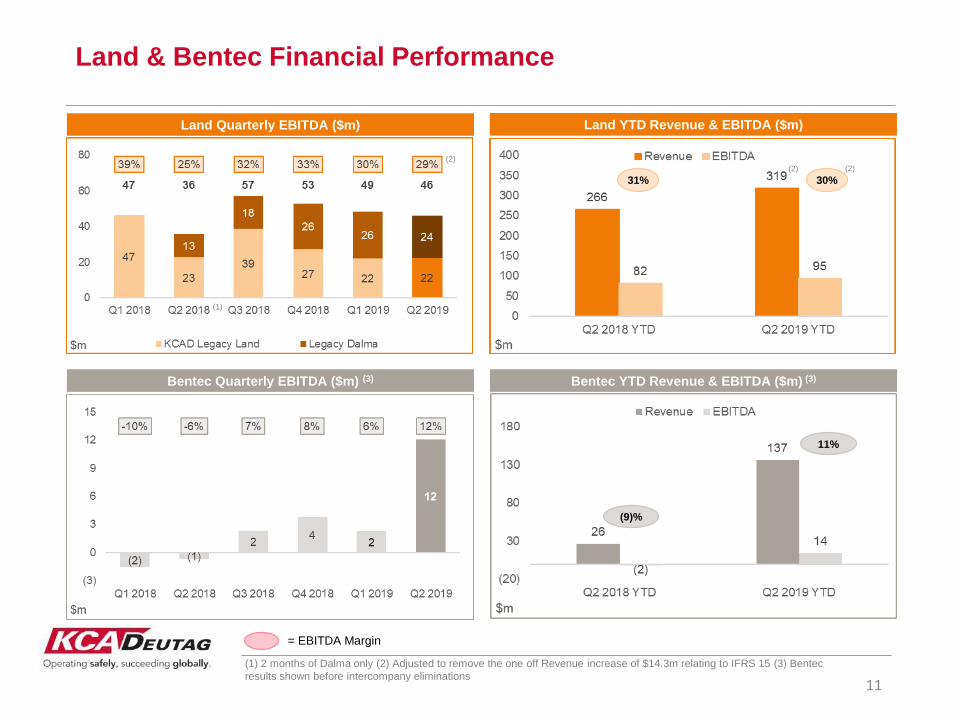

(1) 2 months of Dalma only (2) Adjusted to remove the one off Revenue increase of $14.3m relating to IFRS 15 (3) Bentec

results shown before intercompany eliminations11

Land & Bentec Financial Performance

Land Quarterly EBITDA ($m)

Bentec Quarterly EBITDA ($m) (3)

= EBITDA Margin

Land YTD Revenue & EBITDA ($m)

Bentec YTD Revenue & EBITDA ($m) (3)

31% 30%

(9)%

(1)

11%

(2)

(2)(2)

12

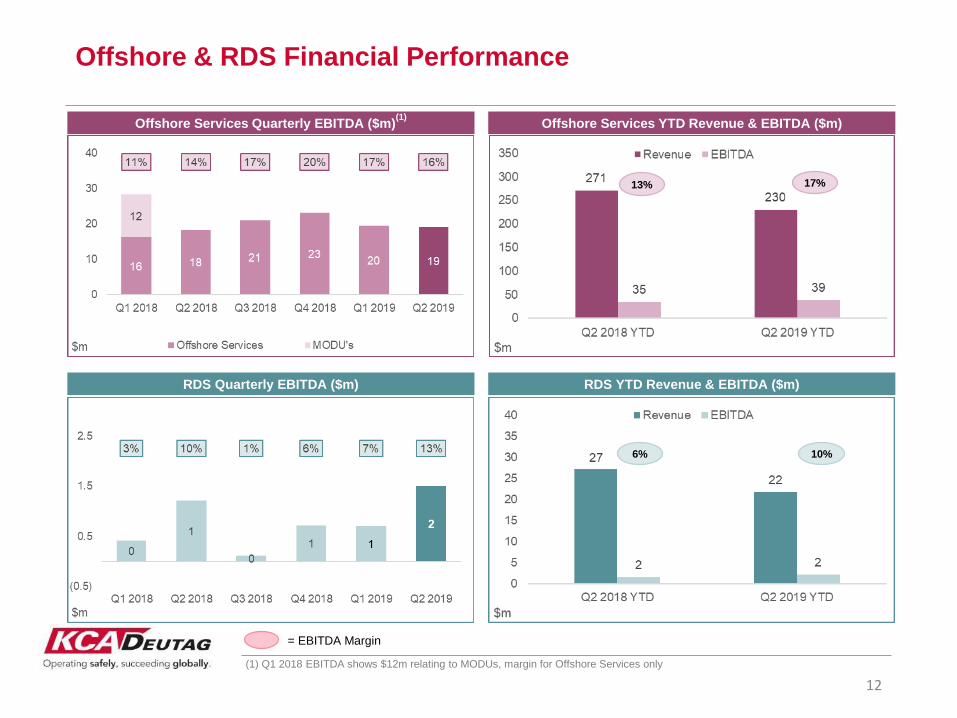

Offshore & RDS Financial Performance

Offshore Services Quarterly EBITDA ($m)(1)

RDS Quarterly EBITDA ($m)

(1) Q1 2018 EBITDA shows $12m relating to MODUs, margin for Offshore Services only

Offshore Services YTD Revenue & EBITDA ($m)

RDS YTD Revenue & EBITDA ($m)

13% 17%

6% 10%

= EBITDA Margin

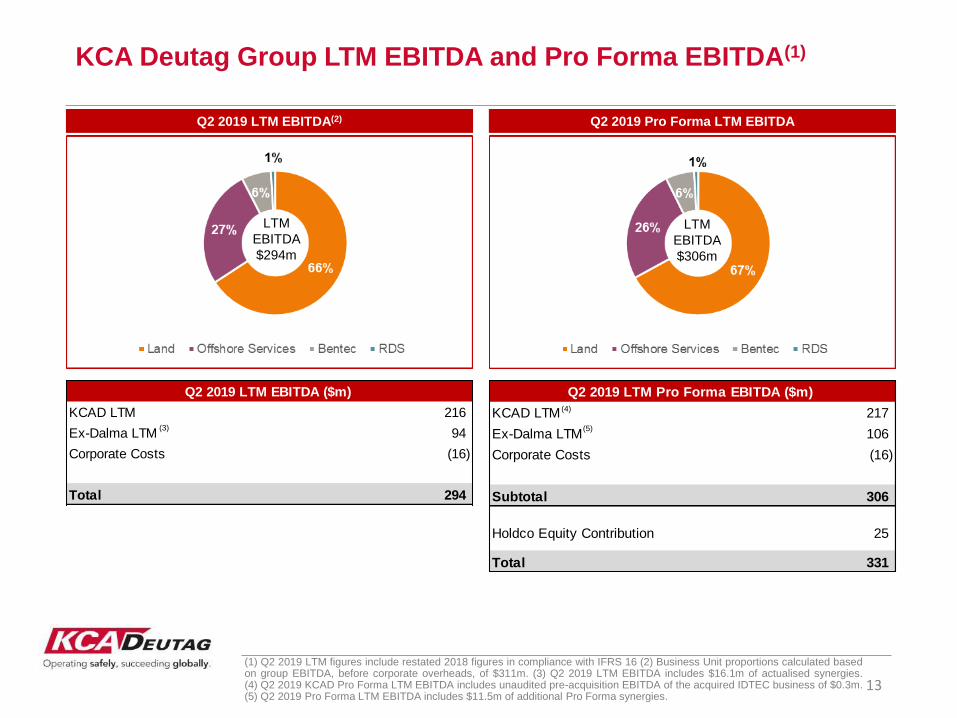

KCAD LTM 216

Ex-Dalma LTM 94

Corporate Costs (16)

Total 294

Q2 2019 LTM EBITDA ($m)

KCAD LTM 217

Ex-Dalma LTM 106

Corporate Costs (16)

Subtotal 306

Holdco Equity Contribution 25

Total 331

Q2 2019 LTM Pro Forma EBITDA ($m)

KCA Deutag Group LTM EBITDA and Pro Forma EBITDA(1)

13

Q2 2019 LTM EBITDA(2)

LTM

EBITDA

$294m

Q2 2019 Pro Forma LTM EBITDA

LTM

EBITDA

$306m

(1) Q2 2019 LTM figures include restated 2018 figures in compliance with IFRS 16 (2) Business Unit proportions calculated basedon group EBITDA, before corporate overheads, of $311m. (3) Q2 2019 LTM EBITDA includes $16.1m of actualised synergies.(4) Q2 2019 KCAD Pro Forma LTM EBITDA includes unaudited pre-acquisition EBITDA of the acquired IDTEC business of $0.3m.(5) Q2 2019 Pro Forma LTM EBITDA includes $11.5m of additional Pro Forma synergies.

(3)

(4)

(5)

Q2 2019 Q1 2019 Q2 2018 2019 YTD 2018 YTD

$'m $'m $'m $'m $'m

Cash generated from operations 102.1 26.0 14.9 128.1 80.5

Tax paid (6.4) (12.5) (9.7) (18.9) (17.8)

Cash flow from operating activities 95.7 13.5 5.2 109.2 62.7

Capital expenditure (13.0) (18.2) (12.4) (31.2) (21.8)

Acquisition of Holdco rig 0.0 (25.0) 0.0 (25.0) 0.0

Proceeds from sale of Fixed Assets 0.0 0.1 (0.1) 0.1 0.7

Interest received 6.5 6.6 5.7 13.1 11.7

Dalma acquistion 0.0 0.0 (440.2) 0.0 (440.2)

Other (0.1) 0.4 0.0 0.3 0.0

Cash flow from investing activities (6.6) (36.1) (447.0) (42.7) (449.6)

Interest paid (83.8) (18.8) (62.8) (102.6) (76.7)

Foreign exchange 0.6 0.2 (3.5) 0.8 (7.9)

Dividend paid to minority shareholders (0.2) (0.3) 0.0 (0.5) (0.3)

Lease payments (3.6) (5.8) (5.5) (9.4) (9.6)

2.1 (47.3) (513.6) (45.2) (481.4)

(19.3) (5.4) 432.1 (24.7) 426.8

Increase in loan from parent company 0.0 25.0 0.0 25.0 0.0

Net cash flow (17.2) (27.7) (81.5) (44.9) (54.6)

Net Cash flow before debt

drawdown/(repayment)

Drawdown/(repayment) of debt and debt

redemption/issuance costs

Cash Flow and Working Capital

14

9

9

(1) 2018 results restated in compliance with IFRS 16 (2) Denotes the effect of foreign exchange rate changes on

cash and bank overdrafts (3) Deltas denote quarterly working capital movement

(2)

Free Cash Flow (1) Working Capital (3)

Amount Utilised Coupon Maturity Facility Rating Leverage

Revolver Cash ($215m) 168 L+400 Mar-22 Caa1/B- 0.51x

Senior Secured Term Loan 411 L+675 Feb-23 Caa1/B- 1.24x

Oman Term Loan 24 L+400 Dec-20 - 0.07x

Total Bank Debt 603 1.82x

Senior Secured Notes 2021 375 7.250% May-21 Caa1/B- 1.13x

Senior Secured Notes 2022 535 9.875% Apr-22 Caa1/B- 1.62x

Senior Secured Notes 2023 400 9.625% Apr-23 Caa1/B- 1.21x

Total Institutional Debt 1,913 5.78x

Other debt 6

Gross Debt 1,920 5.80x

Cash 147 0.44x

Net Debt 1,773 5.36x

Finance lease liabilites 59 0.18x

Net Debt per balance sheet 1,832 5.54x

Capital Structure

15

Net leverage as at 30 June 2019

(1) PF LTM EBITDA adjusted for unaudited LTM EBITDA of the acquired IDTEC business of $0.3m and synergies of the acquired

Dalma businesses of $11.5m. (2) Q1 & Q2 2019 LTM EBITDA includes the second $25m Holdco equity contribution, as defined in the

Amended Credit Agreement. (3) In addition to the $215m Revolver Cash facility, we also have $115m of guarantee facilities

Net Debt Evolution

306

(1)

(3)

(2)

(3)

295

2525

(2)

Closing Remarks

16

• Bentec successfully delivered the final 3 rigs for our customer in Ukraine

• Land Drilling awarded a number of new contracts in the Middle East, Russia, Europe and Africa

• Q2 2019 revenue of $395.1m and EBITDA of $74.4m

• Contract backlog of $5.4bn (at 1 August 2019) across a blue chip customer base

• Significant progress made on our technology initiative, Well of Innovation, with launch in

September

• Operational integration of the forma Dalma business now complete with synergies of $27.6m

identified and 89% of these already secured

Integration of Dalma Energy LLC

18

Target synergies ($28m EBITDA & $3m capex)

EBITDA synergies by type

Integration plan complete

• Expectation of run rate EBITDA synergies increased slightly

from $27.4m (Q1 2019) to $27.6m (Q2 2019)

• Synergy target more than double original estimate of c.$11m

• Capex synergies increased from $2m to $3m

• Monthly run rate achievement in June 2019 of $2.0m, being

89%1 of total savings identified

• Close to full run rate synergy realisation

• Small additional supply chain synergies identified in both

Oman and Saudi Arabia(1)

(1) Run rate synergy achievement based on 30 June 2019 actual achievement