Embed Size (px)

Citation preview

Thomas Cook Group Corporate Strategy

Investor Day PresentationRoyal Opera House, London10 March 2010

Page 2

This presentation does not constitute an invitation or inducement to underwrite, subscribe for or otherwise acquire or dispose of (or engage in any other investment activity in relation to) any Thomas Cook Group plc (‘the Company’) shares or other securities.

This presentation contains certain forward-looking statements and forecasts (based on information known to the Company on the date shown) with respect to future matters, including strategies, initiatives and targets, the financial condition, results and operations of the Company. These statements and forecasts involve risks and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward-looking statements and forecasts, including factors that are outside of the Company’s control. This presentation does not constitute a commitment by the Company to proceed with a certain transaction or business practice in the future. Except as required by its legal or regulatory obligations, the Company does not undertake any obligation to update or revise publicly any forward-looking statement or forecast, whether as a result of new information, future events or otherwise. The reader should, however, consult any future disclosures that the Company may publish via the Regulatory News Service.

Past performance is no guide to future performance and persons needing advice should consult an independent financial adviser. Neither the Company nor anyone acting on its behalf makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this presentation. Neither the Company nor any person acting on its behalf shall have any liability whatsoever for loss, howsoever arising, directly or indirectly, from use of the

information contained within this presentation.

10 March 2010

Disclaimer and cautionary statement

Welcome and IntroductionManny Fontenla-Novoa, Group CEO

Page 4Page 4

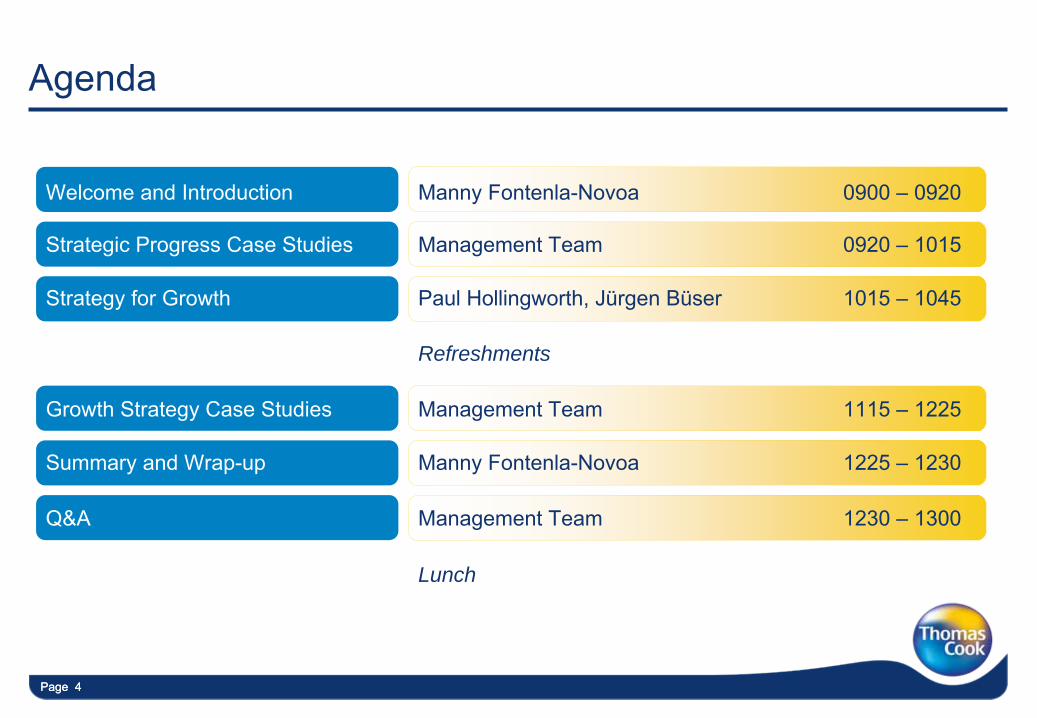

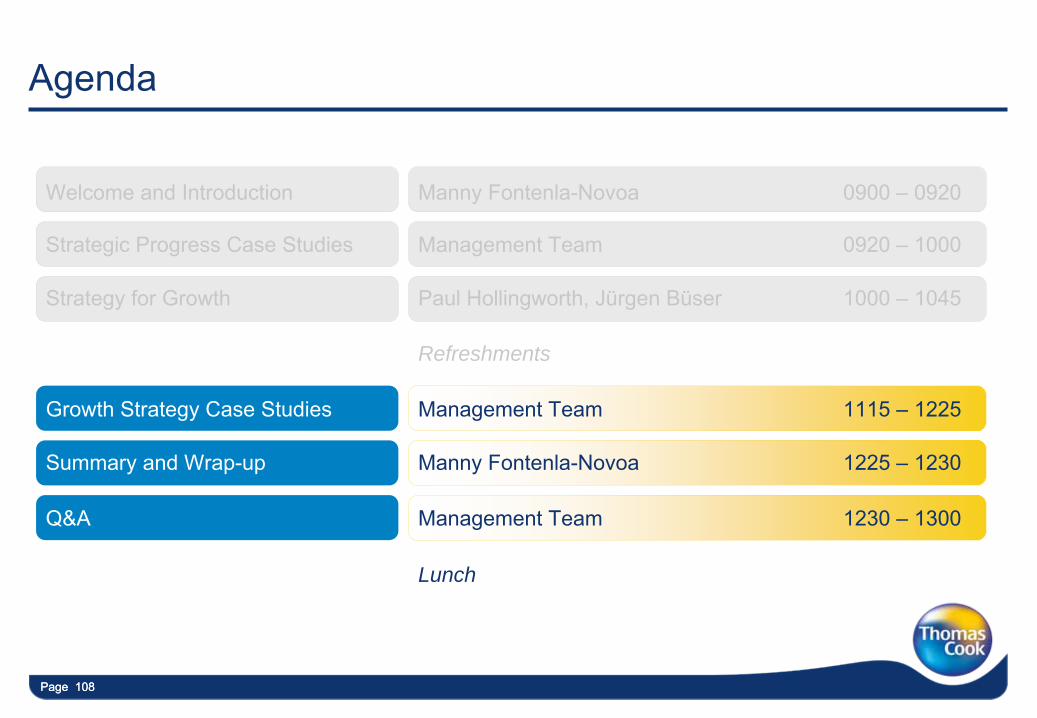

Agenda

Welcome and Introduction Manny Fontenla-Novoa 0900 –

0920

Strategic Progress Case Studies Management Team 0920 –

1015

Strategy for Growth Paul Hollingworth, Jürgen Büser 1015 –

1045

Refreshments

Growth Strategy Case Studies Management Team 1115 –

1225

Summary and Wrap-up Manny Fontenla-Novoa 1225 –

1230

Q&A Management Team 1230 –

1300

Lunch

Page 5Page 5

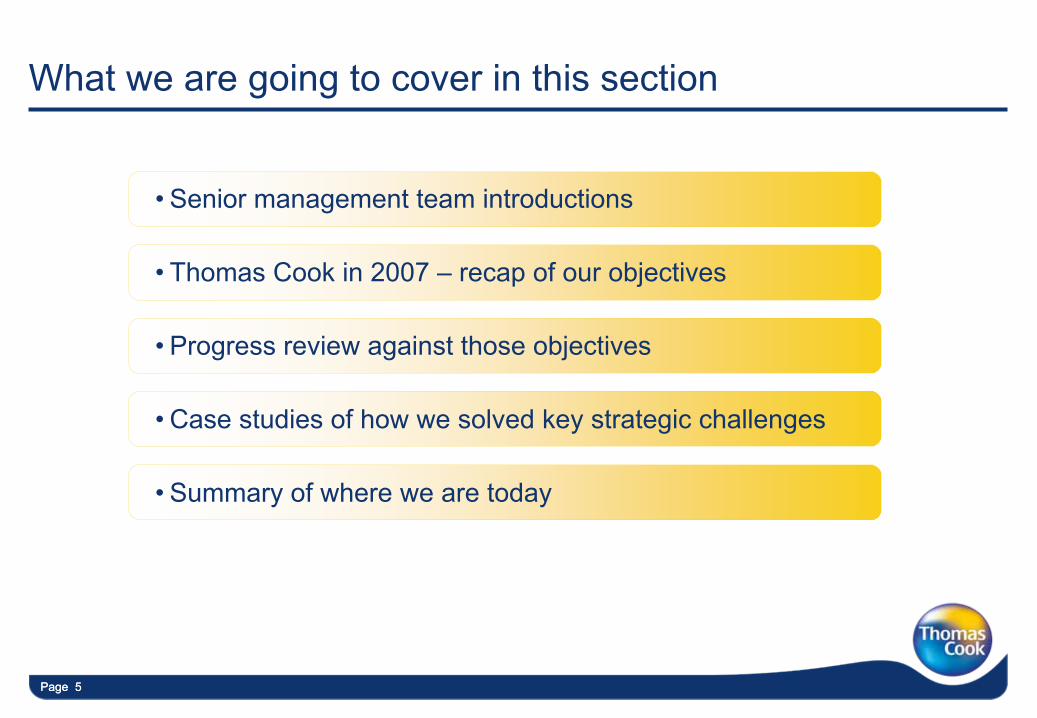

What we are going to cover in this section

•

Senior management team introductions

•

Thomas Cook in 2007 –

recap of our objectives

•

Progress review against those objectives

•

Case studies of how we solved key strategic challenges

•

Summary of where we are today

Page 6

Senior management team introductions

Page 7Page 7

Thomas Cook management team presenting today

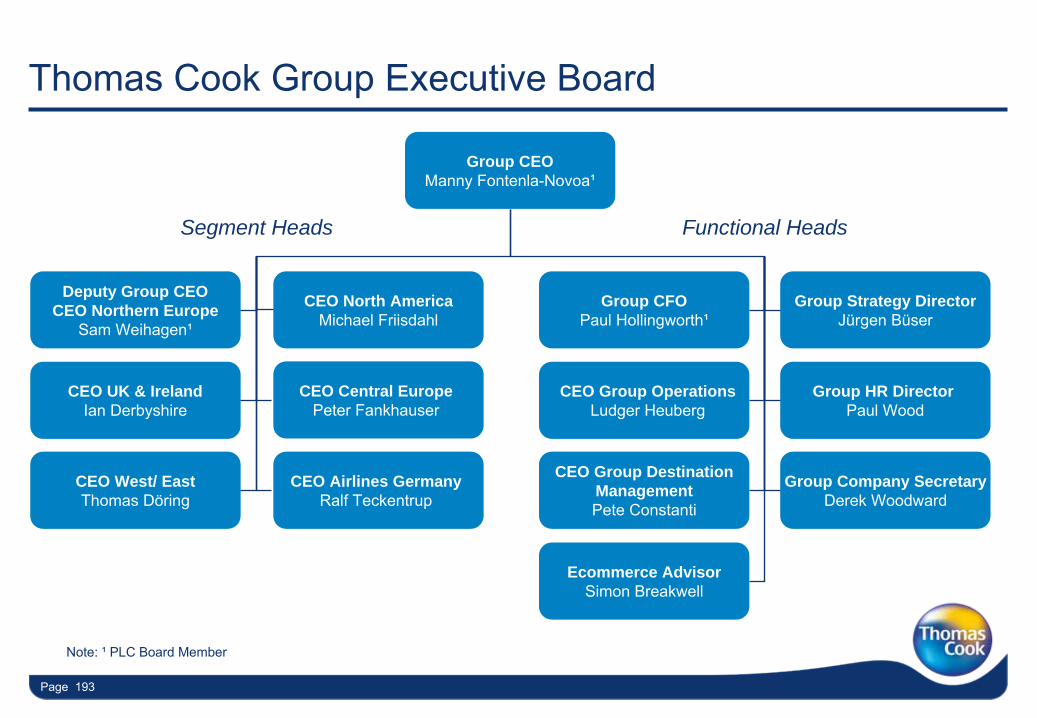

•

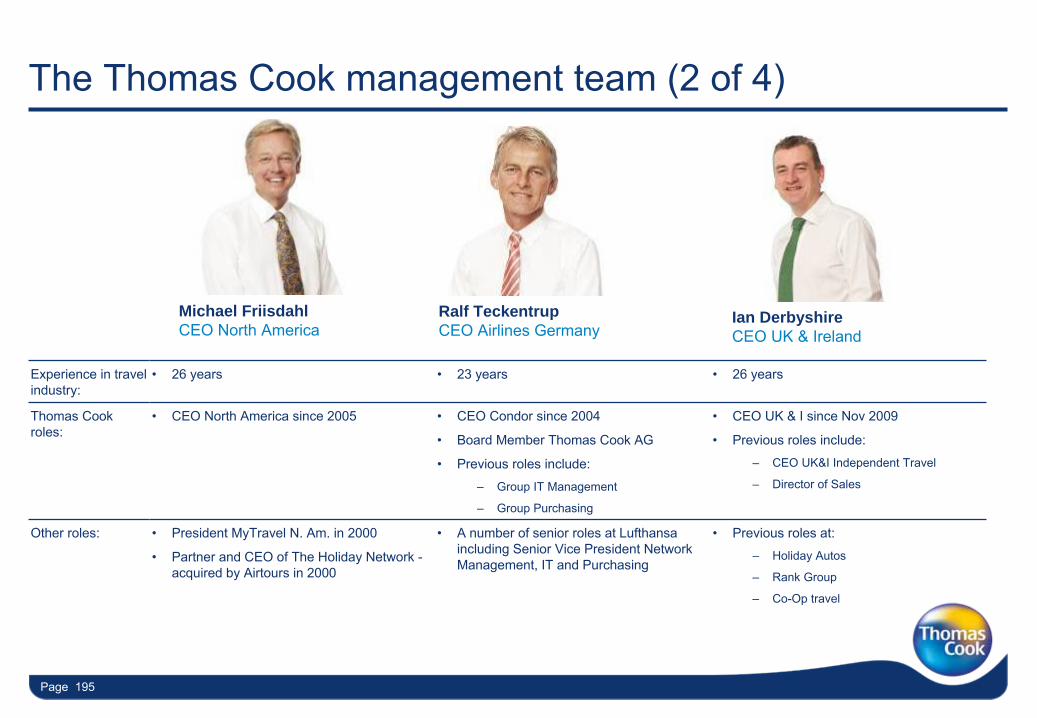

Sam Weihagen, CEO Northern Europe¹

•

Ian Derbyshire, CEO UK & Ireland

•

Thomas Döring, CEO West/ East

•

Peter Fankhauser, CEO Central Europe

•

Michael Friisdahl, CEO North America

•

Ralf Teckentrup, CEO Airlines Germany

•

Paul Hollingworth, Group CFO

•

Pete Constanti, CEO Group Destination Management

•

Jürgen Büser, Group Strategy Director

•

Simon Breakwell, Ecommerce Advisor

Segment Heads Functional Heads

Note: ¹

Also Deputy Group CEO

Page 8

Thomas Cook in 2007

Page 9Page 9

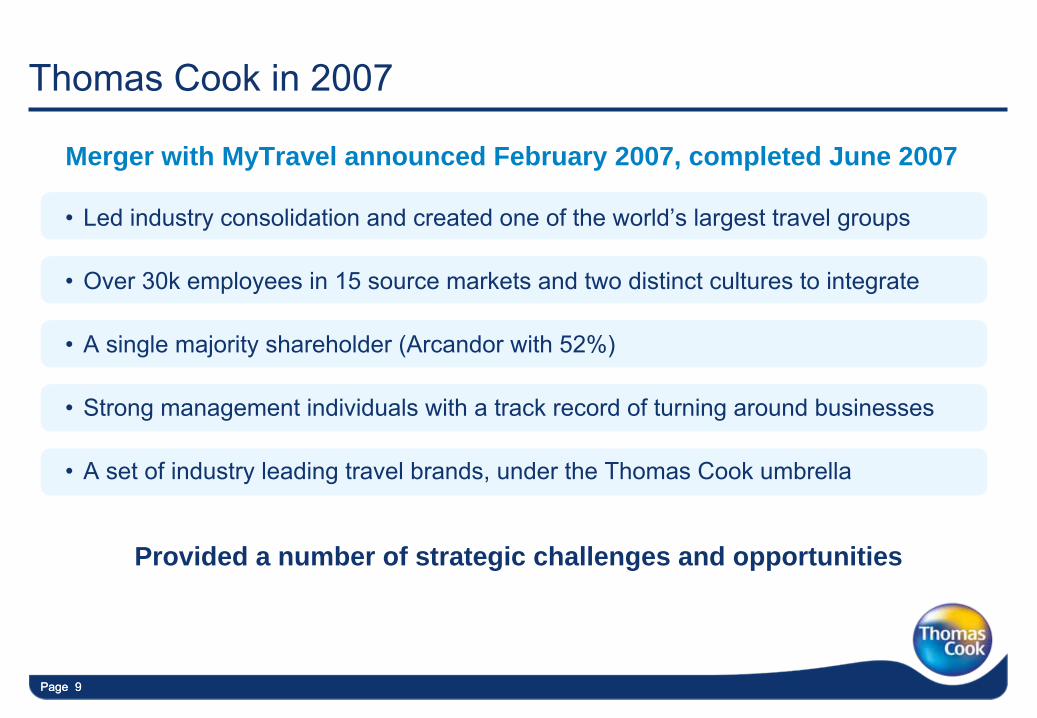

Thomas Cook in 2007

•

Led industry consolidation and created one of the world’s largest travel groups

•

Over 30k employees in 15 source markets and two distinct cultures to integrate

•

A single majority shareholder (Arcandor with 52%)

•

Strong management individuals with a track record of turning around businesses

•

A set of industry leading travel brands, under the Thomas Cook umbrella

Provided a number of strategic challenges and opportunities

Merger with MyTravel announced February 2007, completed June 2007

Page 10

We developed a strategy for long term growth

Strategic objectives

Strengthening our business and investing for growth

Financial rigourBrandsCustomer insightTechnology

Results orientated

Obsessed with customer service

United as one team Driving robust decisions

Pioneering our future

Values

ProductEnablers

Become a leading

independent travel provider

Become the leading

travel-related financial services provider

Capture growth and

value through M&A and

partnerships

Maximisevalue of

mainstream

Growth drivers

Vision

P R O U D

Note: Version shown is strategy as of FY09, this has not materially changed since 2007

Page 11Page 11

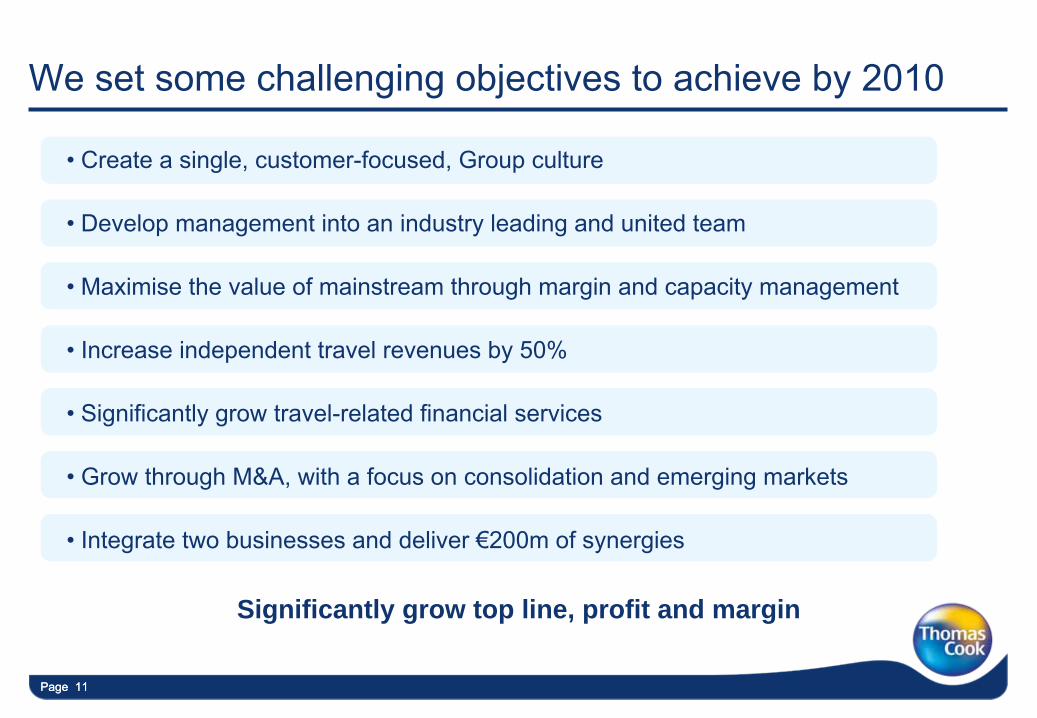

We set some challenging objectives to achieve by 2010

•

Create a single, customer-focused, Group culture

•

Develop management into an industry leading and united team

•

Maximise the value of mainstream through margin and capacity management

•

Increase independent travel revenues by 50%

•

Significantly grow travel-related financial services

•

Grow through M&A, with a focus on consolidation and emerging markets

•

Integrate two businesses and deliver €200m of synergies

Significantly grow top line, profit and margin

Page 12

Progress since the merger

Page 13Page 13

Since 2007 we’ve seen unprecedented market conditions

Page 13

Pound nears parity with the Euro

Economy at 60-year low, says Darling

Surge in last-minute foreign holidays

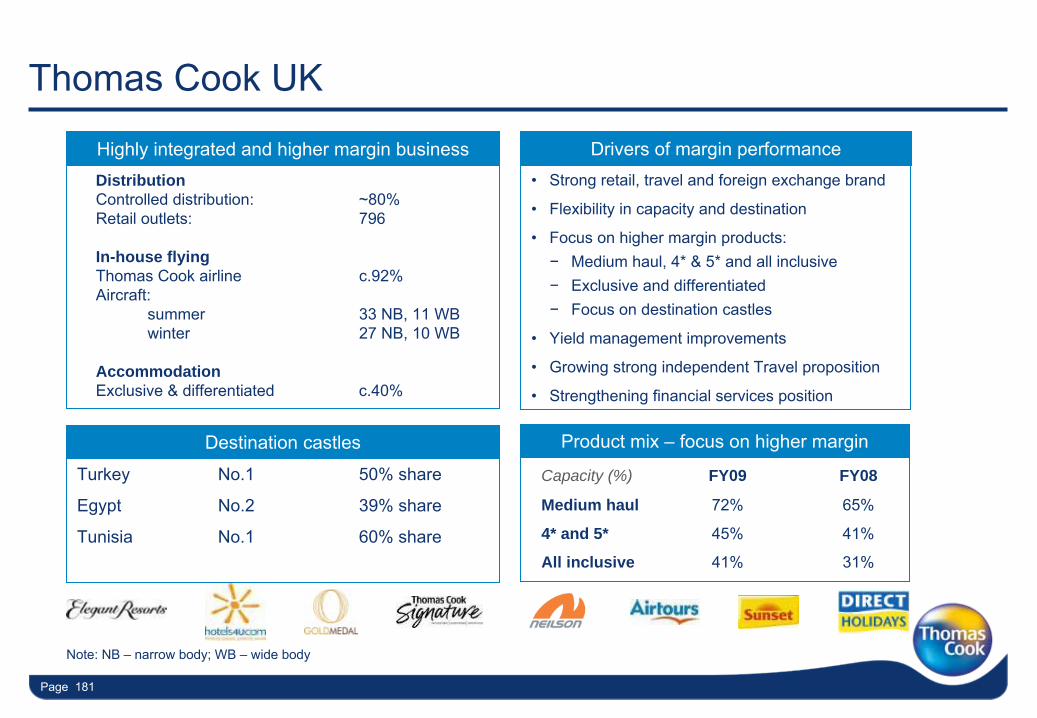

Oil rises past $140

Pound hits Eight-year low against dollar

Credit crisis fells Lehman Brothers Jobless highest level for 17 years

Despite this backdrop, we’ve made significant progress

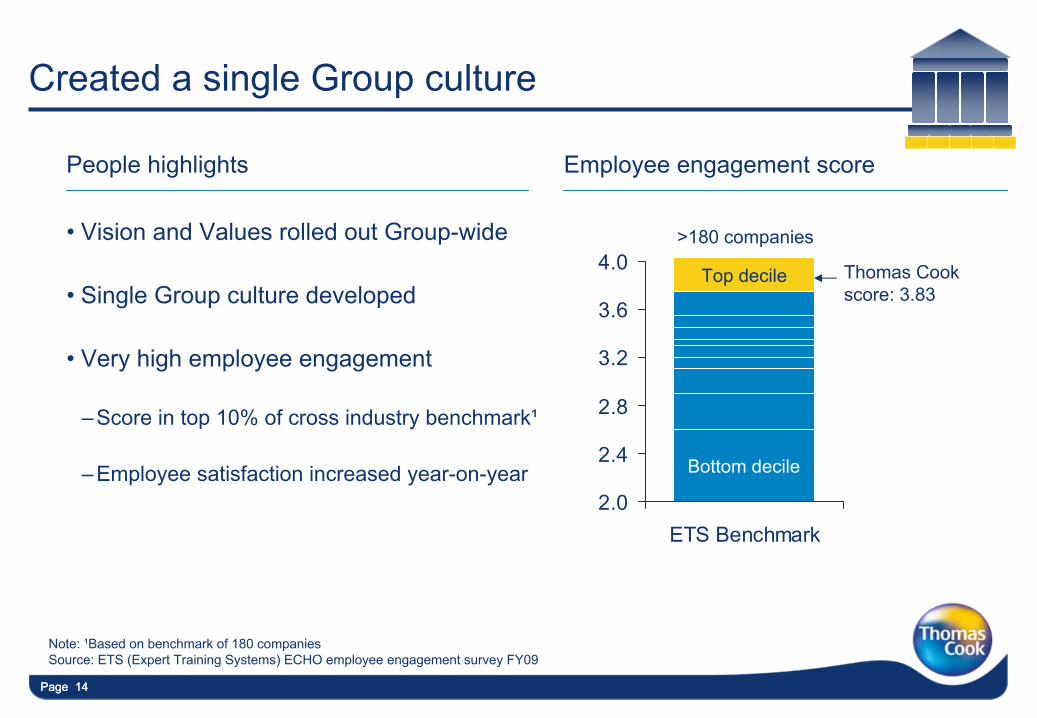

Page 14Page 14

Created a single Group culture

•

Vision and Values rolled out Group-wide

•

Single Group culture developed

•

Very high employee engagement

–Score in top 10% of cross industry benchmark¹

–Employee satisfaction increased year-on-year

Note: ¹Based on benchmark of 180 companiesSource: ETS (Expert Training Systems) ECHO employee engagement survey FY09

People highlights Employee engagement score

2.0

2.4

2.8

3.2

3.6

4.0

ETS Benchmark

Top decile

Bottom decile

Thomas Cook score: 3.83

>180 companies

Page 15Page 15

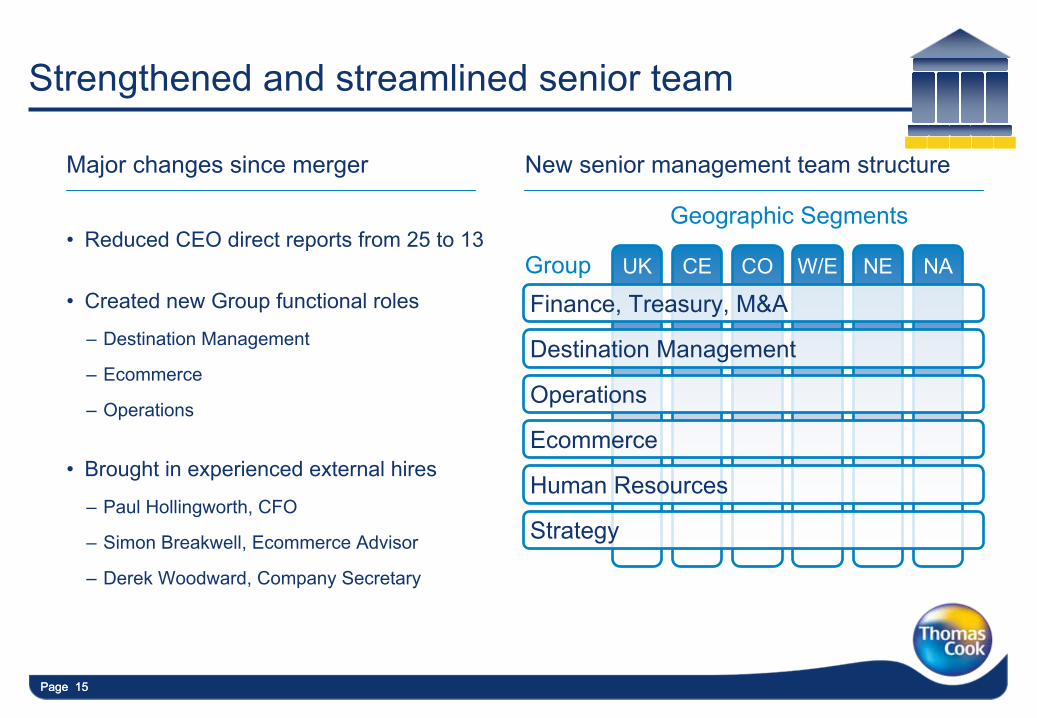

Strengthened and streamlined senior team

Major changes since merger New senior management team structure

•

Reduced CEO direct reports from 25 to 13

•

Created new Group functional roles

–

Destination Management

–

Ecommerce

–

Operations

•

Brought in experienced external hires

–

Paul Hollingworth, CFO

–

Simon Breakwell, Ecommerce Advisor

–

Derek Woodward, Company Secretary

Geographic Segments

UK CE CO W/E NE NA

Finance, Treasury, M&A

Destination Management

Operations

Ecommerce

Human Resources

Strategy

Group

Page 16Page 16

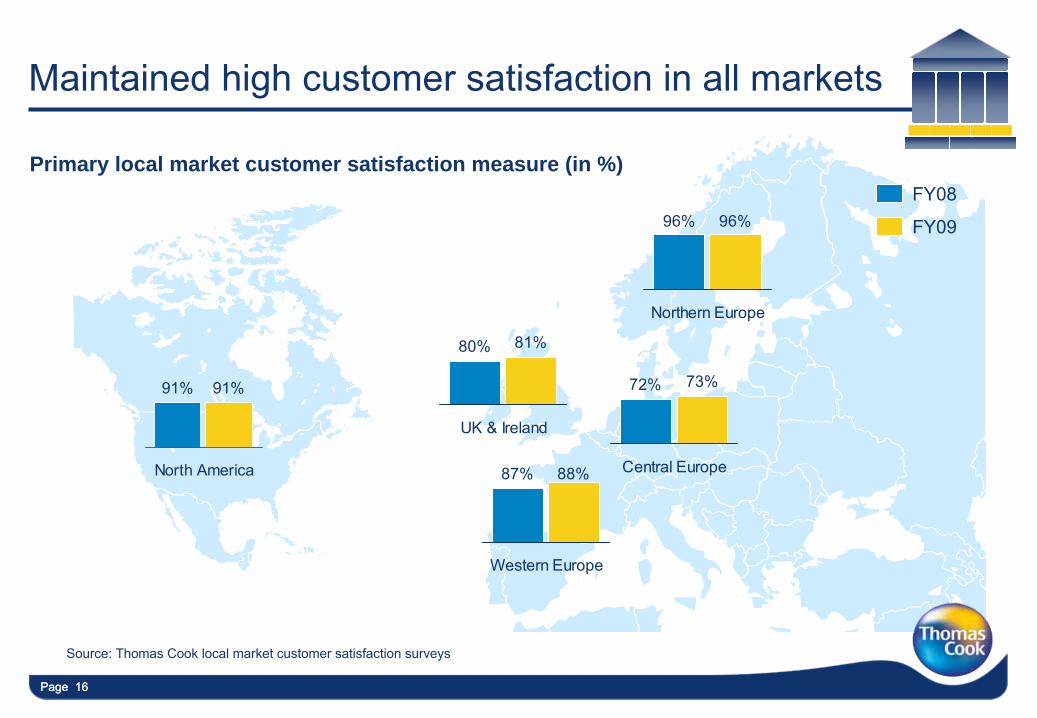

Maintained high customer satisfaction in all markets

Primary local market customer satisfaction measure (in %)

Source: Thomas Cook local market customer satisfaction surveys

FY08

FY09

91% 91%

North America 87% 88%

Western Europe

80% 81%

UK & Ireland

96% 96%

Northern Europe

72% 73%

Central Europe

Page 17

Received extensive trade and consumer recognition

Page 18

Enhanced our leading portfolio of travel brandsGlobal umbrella brand

Major local brands

Other local brands

Page 19Page 19

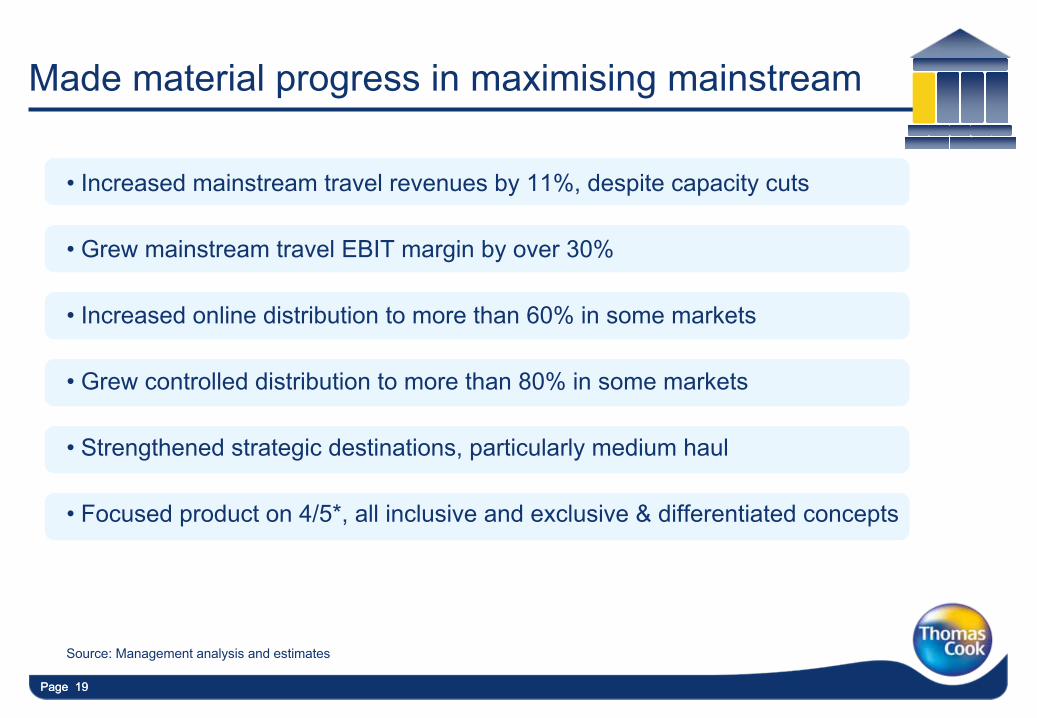

Made material progress in maximising mainstream

•

Increased mainstream travel revenues by 11%, despite capacity cuts

•

Grew mainstream travel EBIT margin by over 30%

•

Increased online distribution to more than 60% in some markets

•

Grew controlled distribution to more than 80% in some markets

•

Strengthened strategic destinations, particularly medium haul

•

Focused product on 4/5*, all inclusive and exclusive & differentiated concepts

Source: Management analysis and estimates

Page 20Page 20

Grew independent revenues by over 50%

•

Increased independent travel revenues by over 50%

•

Created one of the leading wholesale travel businesses–

Hotels4U, Gold Medal and TriWest deals strengthened position

•

Continued to be a leader in cruise retail

•

Built thomascook.com

into a top travel website with 3m users a month¹

•

Strengthened position in scheduled package market through acquisitions

Note: ¹Monthly unique users in the UKSource: Management analysis and estimates

Page 21Page 21

Extracted value from financial services

•

Acquired India’s largest travel and foreign exchange business–Thomas Cook India with over 50% foreign exchange market share¹

•

Entered airport Forex market in UK (winning last 2 tenders) and India

•

Increased UK foreign exchange market share by ~75% since 2008

•

Moved to a single Group-wide insurance underwriter

•

But, curtailed ambitions in credit card business due to market conditions

Note: ¹

Share of the regulated marketSource: Management estimates; YouGov

Page 22Page 22

M&A strengthened position & solved key challenges

Successfully completed and integrated 14 acquisitions:

•

£450m consideration, 5-7x EBITDA paid depending on profile

•

Bolstered mainstream and significantly enhanced independent

•

Addressed key markets such as France, Canada and the UK

•

Grew in emerging markets, reacquiring Thomas Cook India and Egypt

•

Created value with ROIC to exceed cost of capital overall

Page 23Page 23

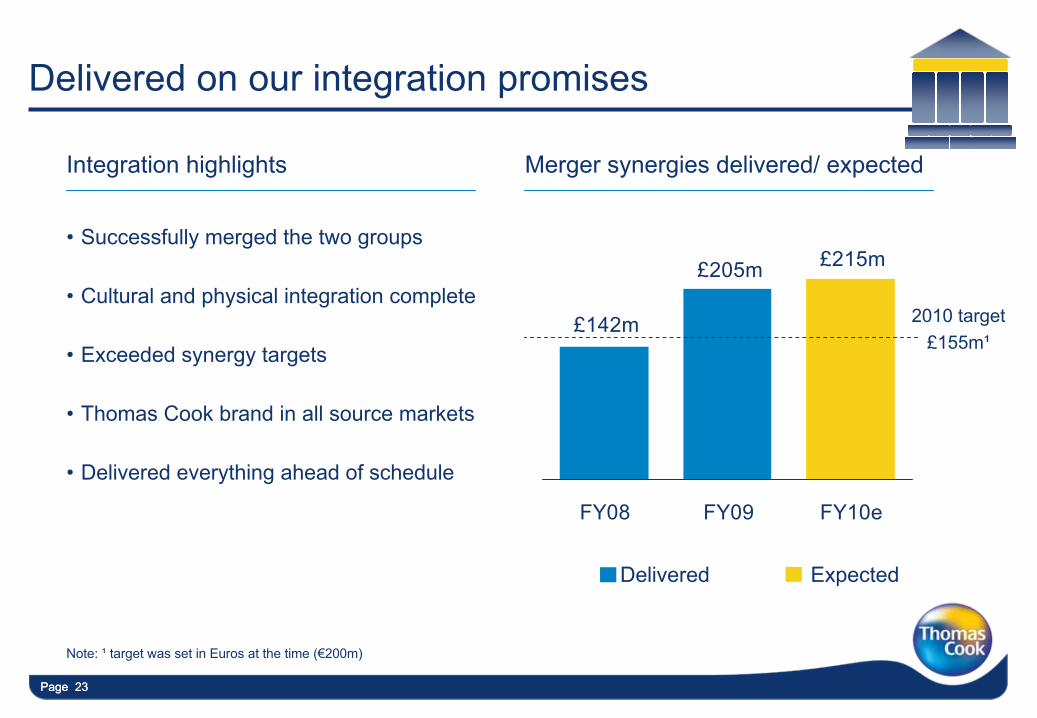

Delivered on our integration promises

•

Successfully merged the two groups

•

Cultural and physical integration complete

•

Exceeded synergy targets

•

Thomas Cook brand in all source markets

•

Delivered everything ahead of schedule

Note: ¹

target was set in Euros at the time (€200m)

Delivered

Integration highlights Merger synergies delivered/ expected

£215m£205m

£142m

FY08 FY09 FY10e

2010 target£155m¹

Expected

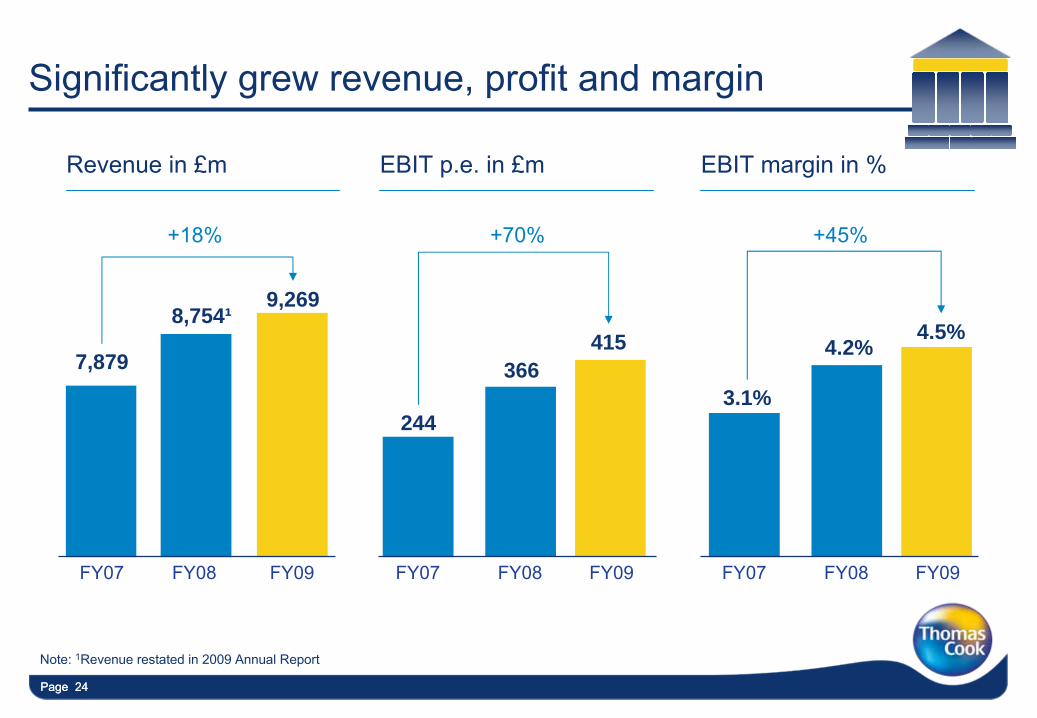

Page 24Page 24

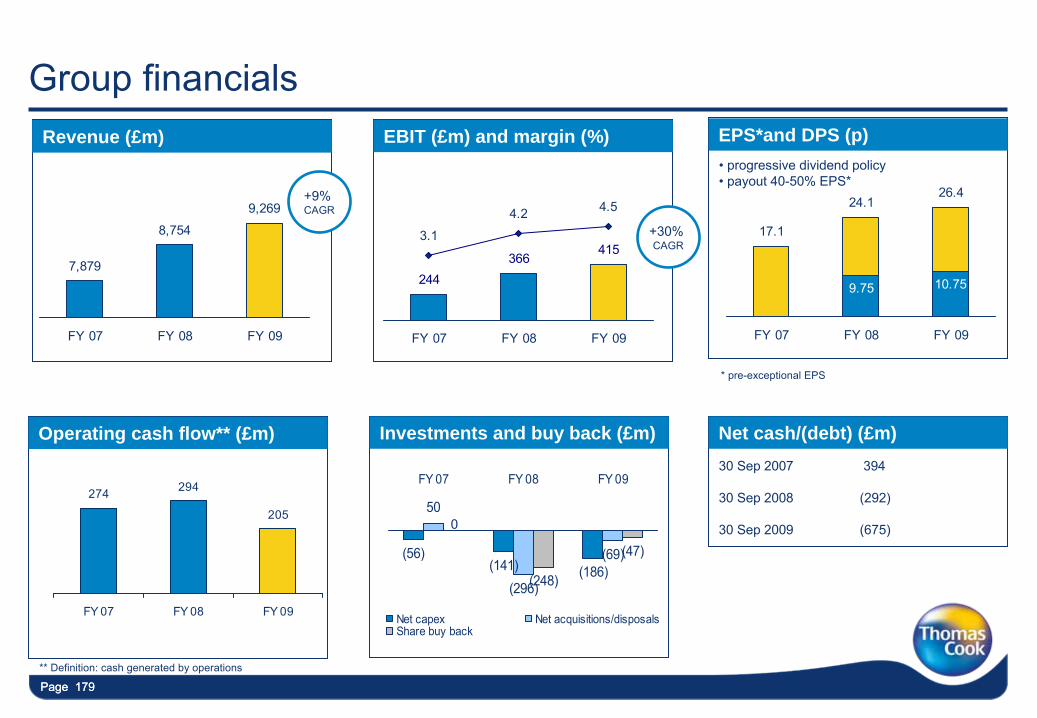

FY07 FY08

8,754¹

7,879 366

244

FY07 FY08

4.2%

3.1%

FY07 FY08FY09

9,269

FY09

4.5%

FY09

+70%+18% +45%

415

Revenue in £m EBIT p.e. in £m EBIT margin in %

Significantly grew revenue, profit and margin

Note: 1Revenue restated in 2009 Annual Report

Page 25Page 25

In summary, how did we do?

Significantly grow top line, profit and margin

•

Create a single, customer-focused, Group culture

•

Develop management into an industry leading and united team

•

Maximise the value of mainstream through margin and capacity management

•

Increase independent travel revenues by 50%

•

Significantly grow travel-related financial services

•

Grow through M&A, with a focus on consolidation and emerging markets

•

Integrate two businesses and deliver €200m of synergies

Strategic progress case studies

Page 27Page 27

Key strategic challenges we faced in 2007

Page 27

How to make profits in an unconsolidated and highly competitive market?Germany

How to defend market leading margins of 8-9%?Northern Europe

How to succeed in a market with no barriers to entry and huge overcapacity?North America

How to restructure a loss making business with a weak market position?France

Page 28Page 28

How to succeed in a Canadian market with no barriers to entry and huge overcapacity?

Michael Friisdahl –

CEO North America

Page 29Page 29

North America objectives

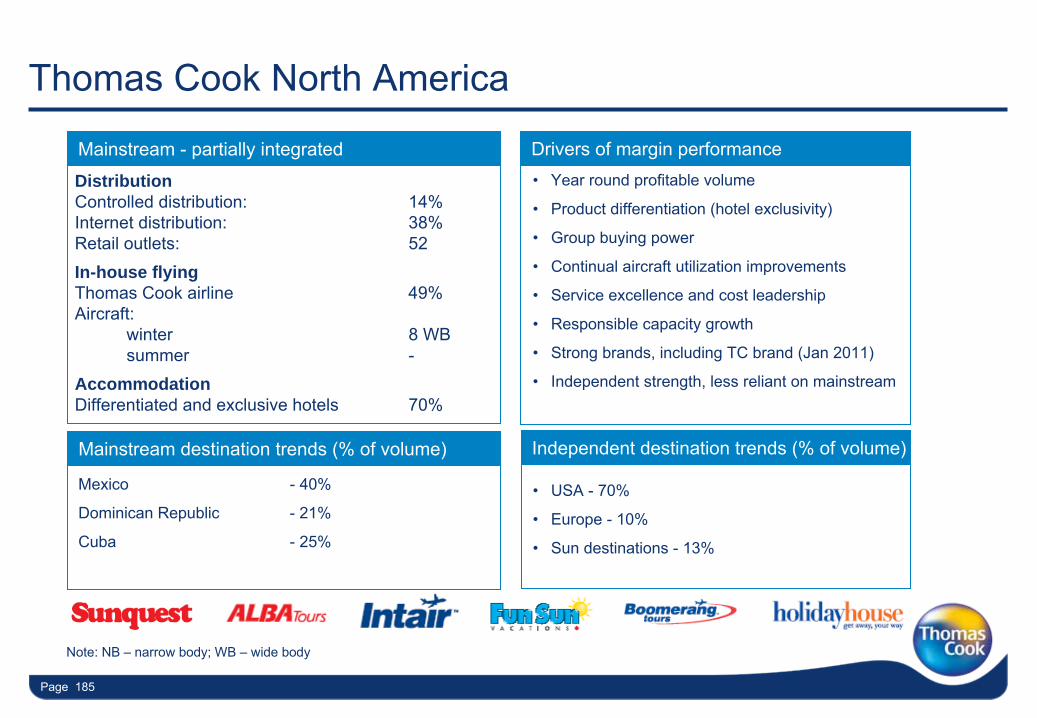

•

Strengthen leadership position in leisure travel market

•

Reduce risk stemming from mainstream overcapacity

•

Achieve 5% margin

Page 29

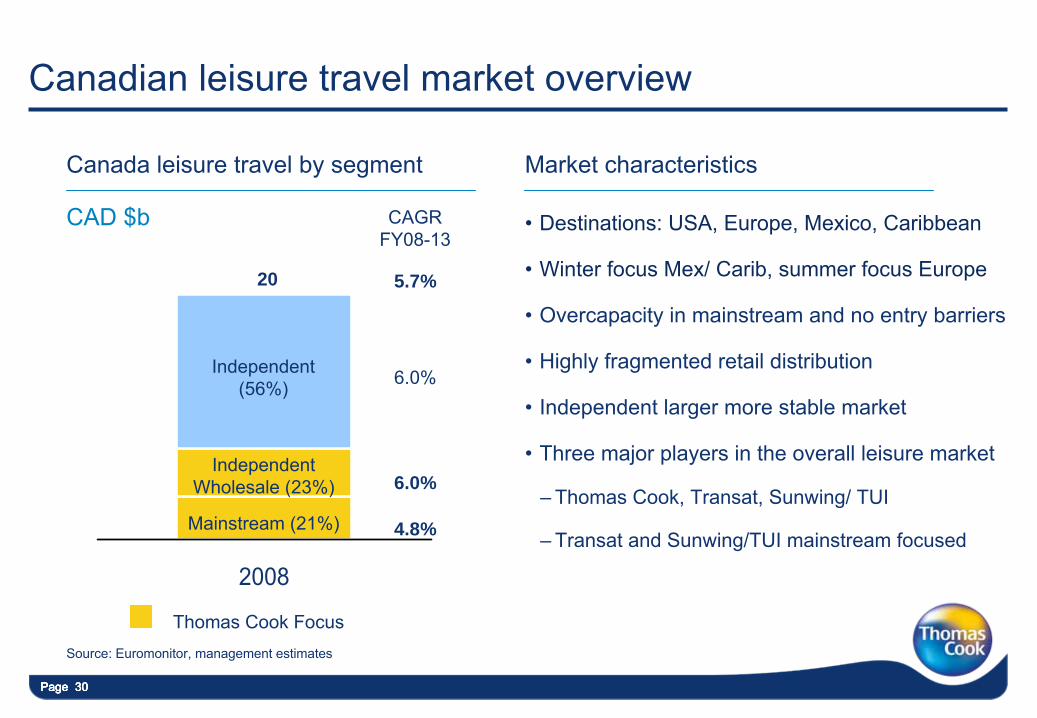

Page 30Page 30Page 30

Canadian leisure travel market overview

Page 30

2008

20

6.0%

4.8%

5.7%

Mainstream (21%)

Independent

(56%)

Source: Euromonitor, management estimates

Independent

Wholesale (23%) 6.0%

Thomas Cook Focus

CAGR

FY08-13

Canada leisure travel by segment Market characteristics

•

Destinations: USA, Europe, Mexico, Caribbean

•

Winter focus Mex/ Carib, summer focus Europe

•

Overcapacity in mainstream and no entry barriers

•

Highly fragmented retail distribution

•

Independent larger more stable market

•

Three major players in the overall leisure market

–

Thomas Cook, Transat, Sunwing/ TUI

–

Transat and Sunwing/TUI mainstream focused

CAD $b

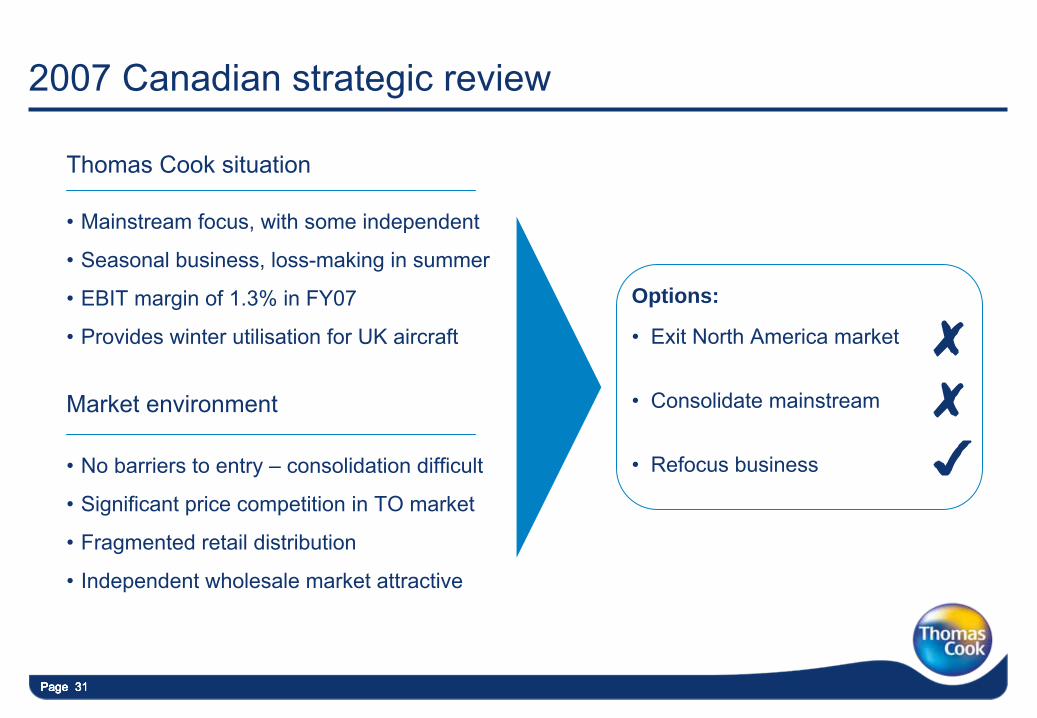

Page 31Page 31Page 31

2007 Canadian strategic review

Page 31

Market environment

•

No barriers to entry –

consolidation difficult

•

Significant price competition in TO market

•

Fragmented retail distribution

•

Independent wholesale market attractive

Thomas Cook situation

•

Mainstream focus, with some independent

•

Seasonal business, loss-making in summer

•

EBIT margin of 1.3% in FY07

•

Provides winter utilisation for UK aircraft •

Exit North America market

•

Consolidate mainstream

•

Refocus business

Options:

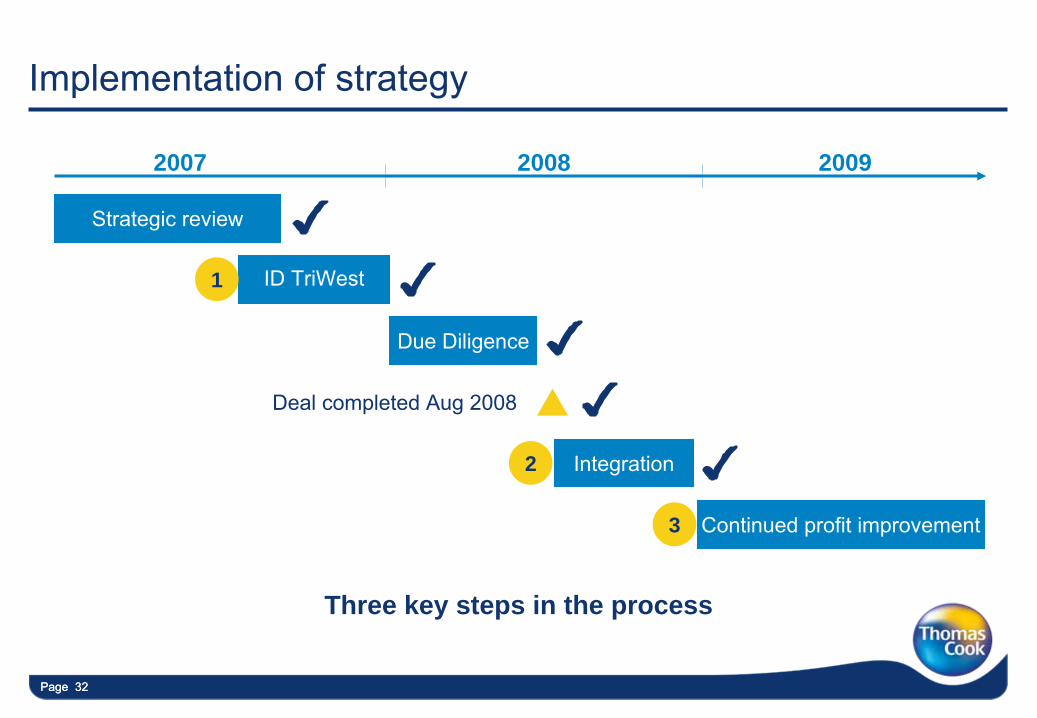

Page 32Page 32

Implementation of strategy

2007 2008 2009

Strategic review

ID TriWest

Continued profit improvement

Due Diligence

Integration

Deal completed Aug 2008

1

2

3

Three key steps in the process

Page 33Page 33Page 33Page 33Page 33

Target identified –

TriWest1

Note: ¹

Flexible Independent TravelSource: Management estimates

•

TriWest a leader in independent wholesale, with two main brands (Fun Sun, Intair)

•

FY07 revenues of CAD$172m, EBIT of CAD$13m,

total staff of 565 –

high synergy potential

•

Strength in markets where Thomas Cook had limited presence, especially Quebec

•

Company with year round profitability and a wider destination reach

FIT¹

Wholesaler Air Consolidator

•

Non-risk

•

Strength in Western Canada

•

Air, hotel, transfers, car, cruises, attractions

•

Flexible departure dates

•

Flexible duration

•

Largest Canadian air consolidator

•

National presence, strength in Quebec

•

Net rates, published fares

•

70 airline partners

•

Market leading web booking engine

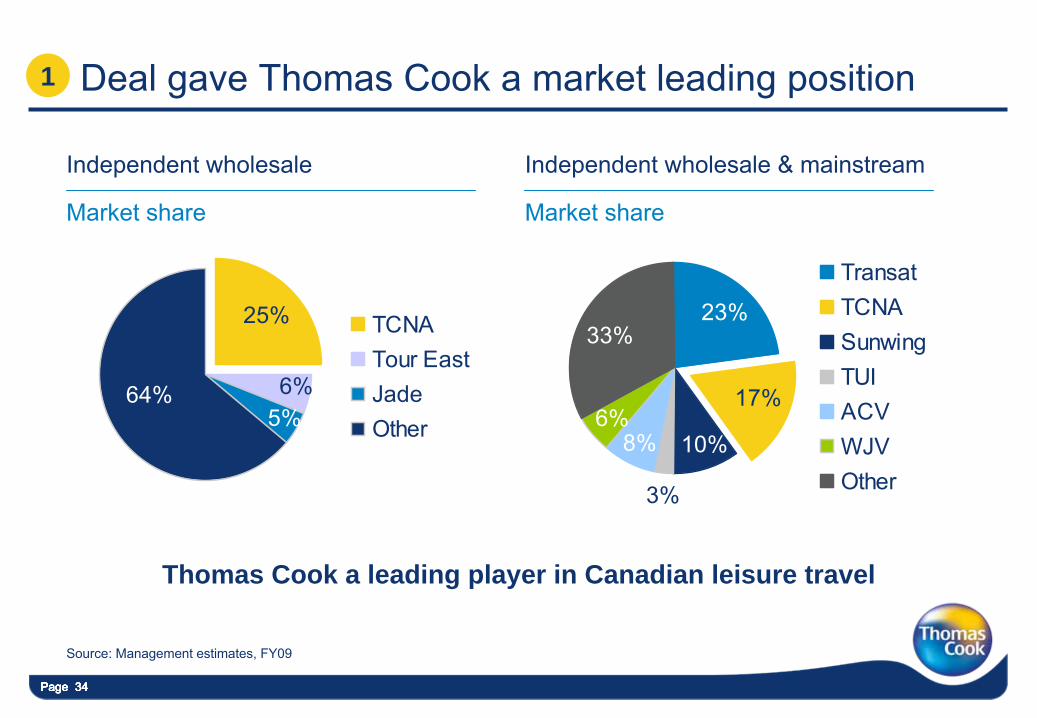

Page 34Page 34Page 34Page 34Page 34

Deal gave Thomas Cook a market leading position

Source: Management estimates, FY09

3%

23%

17%

10%8%6%

33%

TransatTCNASunwingTUIACVWJVOther

64%

25%

6%5%

TCNATour EastJadeOther

Independent wholesale Independent wholesale & mainstream

Thomas Cook a leading player in Canadian leisure travel

1

Market share Market share

Page 35Page 35Page 35Page 35Page 35

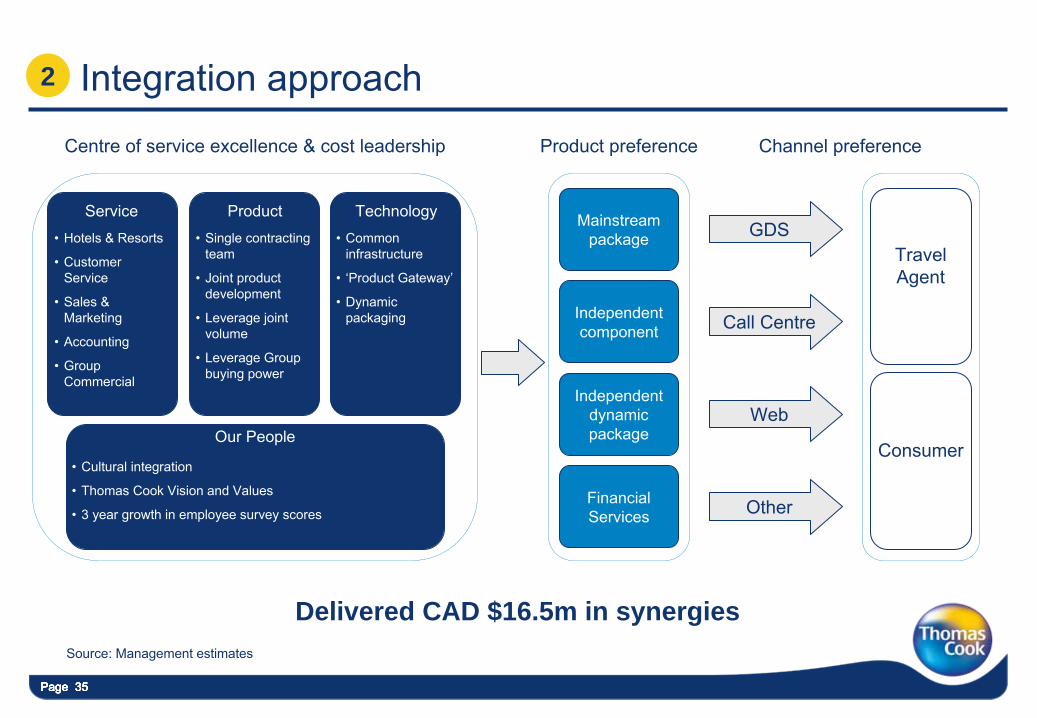

Integration approach2

Source: Management estimates

Mainstream

package

Independent

component

Independent

dynamic

package

FinancialServices

Web

GDS

Call Centre

Other

Our People

•

Hotels & Resorts

•

Customer Service

•

Sales & Marketing

•

Accounting

•

Group Commercial

•

Single contracting team

•

Joint product development

•

Leverage joint volume

•

Leverage Group buying power

•

Common infrastructure

•

‘Product Gateway’

•

Dynamic packaging

Service Product Technology

TravelAgent

Consumer

Centre of service excellence & cost leadership Channel preferenceProduct preference

Delivered CAD $16.5m in synergies

•

Cultural integration

•

Thomas Cook Vision and Values

•

3 year growth in employee survey scores

Page 36Page 36Page 36

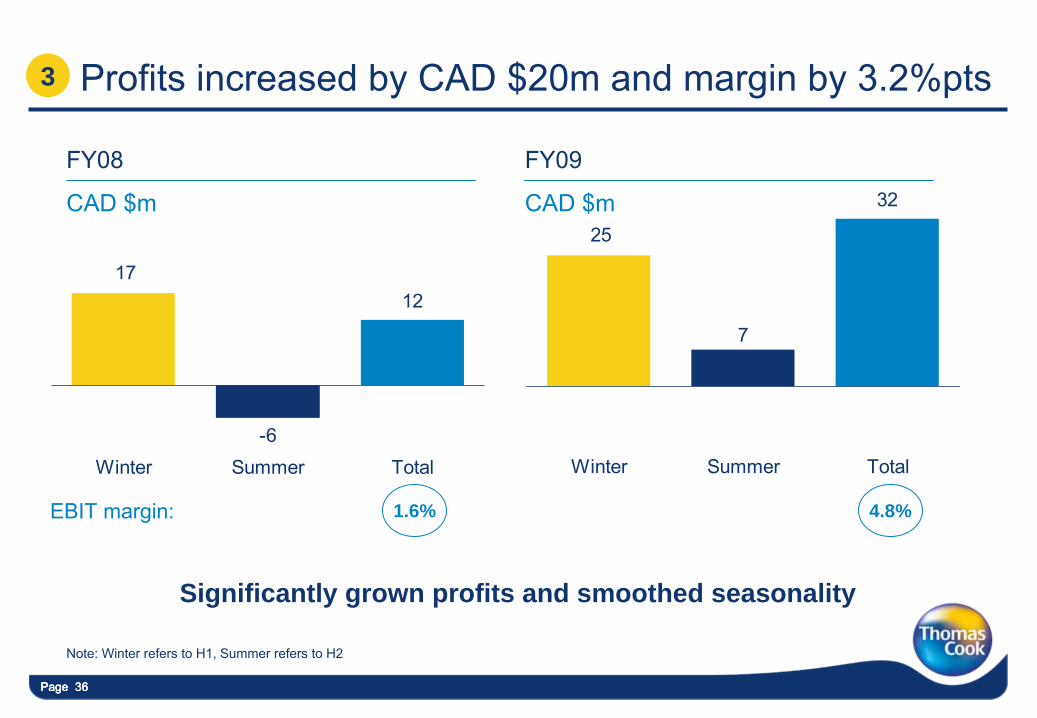

1217

-6Winter Summer Total

32

7

25

Winter Summer Total

Profits increased by CAD $20m and margin by 3.2%pts

FY08

CAD $m

1.6% 4.8%EBIT margin:

Note: Winter refers to H1, Summer refers to H2

Significantly grown profits and smoothed seasonality

3

FY09

CAD $m

Page 37Page 37Page 37Page 37

Future growth

•

Leverage the Thomas Cook brand to drive consumer awareness and revenue growth

•

Grow independent travel through Thomas Cook online strategy (including B2C)

•

Improve mainstream profitability through product exclusivity and

cost savings

•

Continue to develop and leverage service excellence and cost leadership

•

Grow Thomas Cook Financial Services

Maintain market leading margins

Page 38

How to restructure a loss making French business with a weak market position?

Thomas Döring –

CEO West/East Europe

Page 39

France objectives

Focus on mainstream travel:

•

Turnaround loss making French business

•

Create a platform for future profitable growth

Page 40Page 40

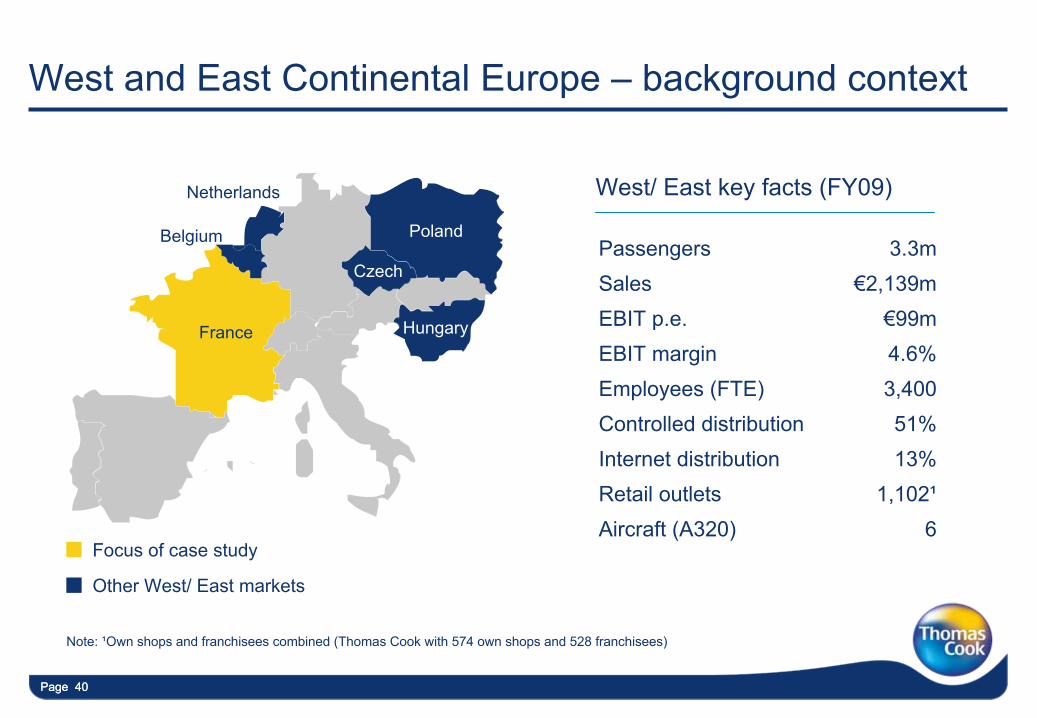

West and East Continental Europe –

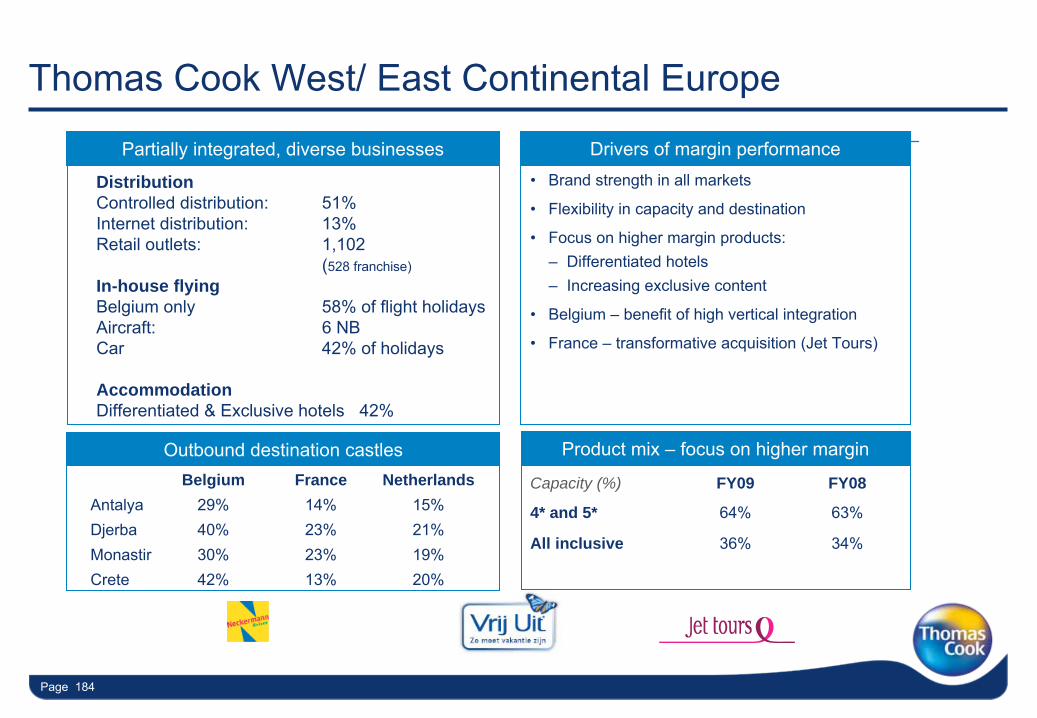

background context

Poland Belgium

Netherlands

France Hungary

Czech

Hungary

Other West/ East markets

Passengers 3.3mSales €2,139mEBIT p.e. €99mEBIT margin 4.6%Employees (FTE) 3,400Controlled distribution 51%Internet distribution 13%Retail outlets 1,102¹Aircraft (A320) 6

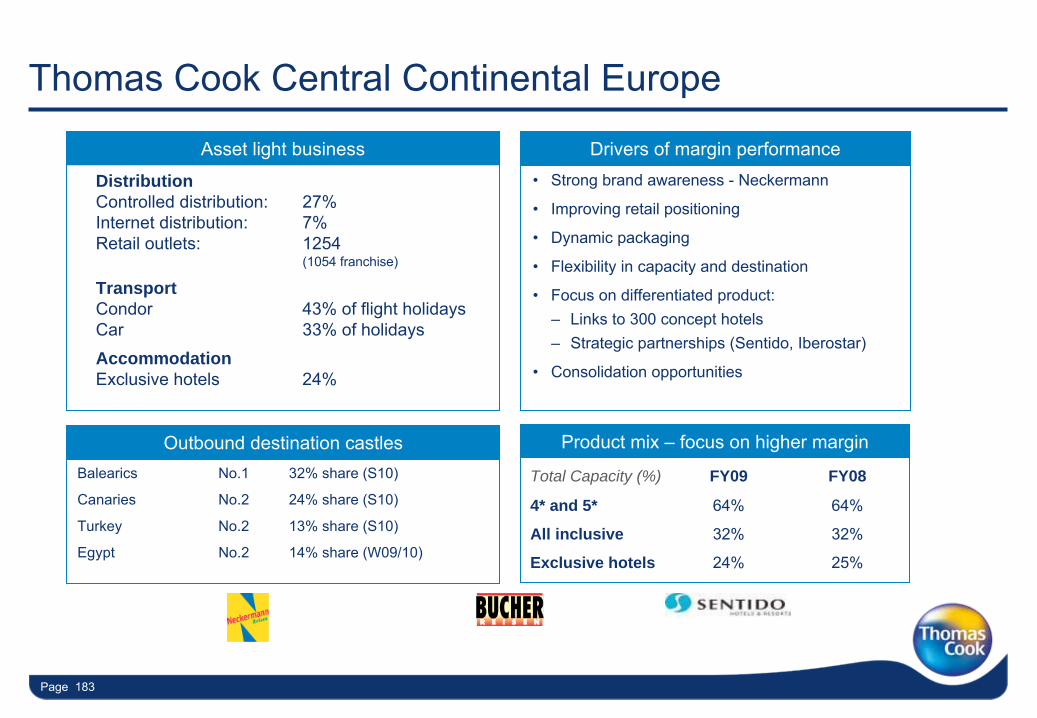

West/ East key facts (FY09)

Focus of case study

Note: ¹Own shops and franchisees combined (Thomas Cook with 574 own shops and 528 franchisees)

Page 41Page 4141

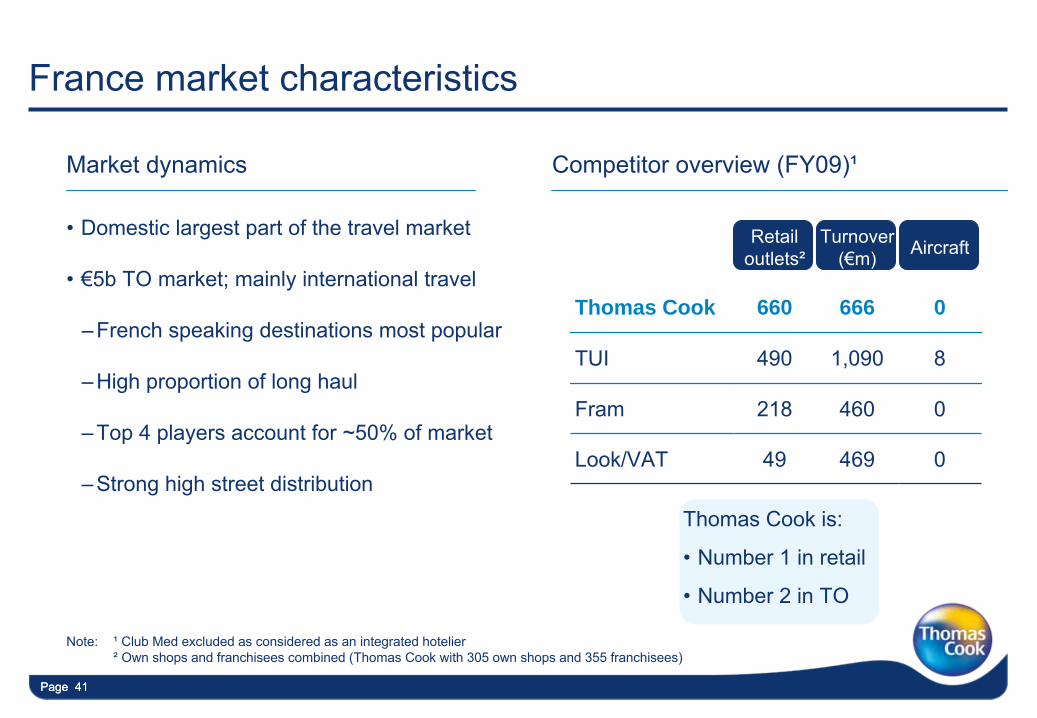

France market characteristics

•

Domestic largest part of the travel market

•

€5b TO market; mainly international travel

–French speaking destinations most popular

–High proportion of long haul

–Top 4 players account for ~50% of market

–Strong high street distribution

Note: ¹

Club Med excluded as considered as an integrated hotelier

²

Own shops and franchisees combined (Thomas Cook with 305 own shops and 355 franchisees)

Market dynamics

Retail outlets²

Turnover (€m) Aircraft

Thomas Cook 660 666 0

TUI 490 1,090 8

Fram 218 460 0

Look/VAT 49 469 0

Competitor overview (FY09)¹

Thomas Cook is:

•

Number 1 in retail

•

Number 2 in TO

Page 42Page 42

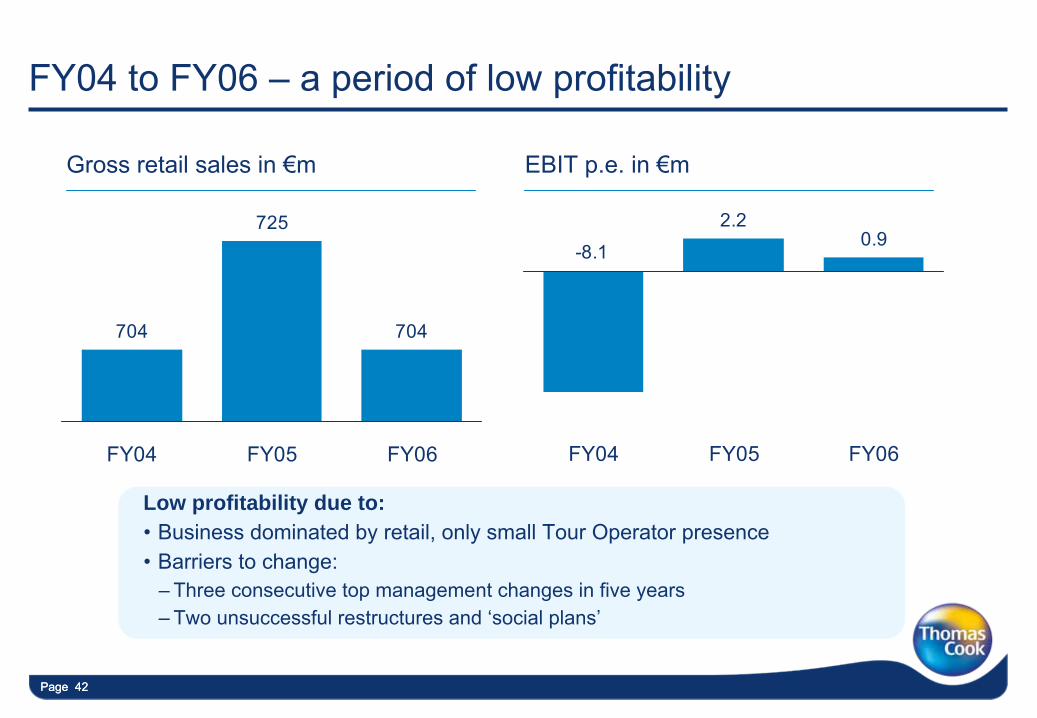

FY04 to FY06 –

a period of low profitability

704

725

704

FY04 FY05 FY06

Gross retail sales in €m EBIT p.e. in €m

2.20.9

-8.1

FY04 FY05 FY06

Low profitability due to:•

Business dominated by retail, only small Tour Operator presence•

Barriers to change: –

Three consecutive top management changes in five years–

Two unsuccessful restructures and ‘social plans’

Page 43

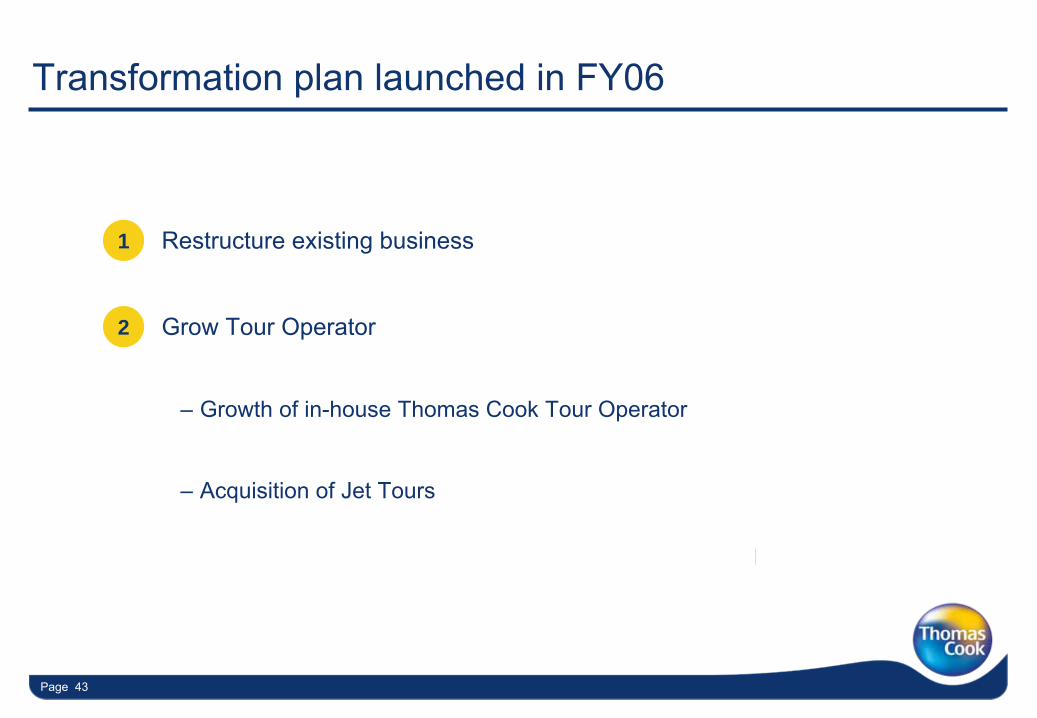

Transformation plan launched in FY06

•

Restructure existing business

•

Grow Tour Operator

–

Growth of in-house Thomas Cook Tour Operator

–

Acquisition of Jet Tours

1

2

Page 44Page 44

13.7

5.32.4

8.6

37.0

7.0

TO Retail IT Finance Other Total

Overhead cost reduction (€m)

Restructure existing business1

Restructuring FY06 –

FY09

•

Overhead costs reduced by 25%

–Tour operator and retail costs

–Merger synergies e.g. IT and Finance

–FTE’s reduced by >400

•

Retail efficiency

–14% increase in average sales per FTE

–In-house TO sales rose from 25% to 47%

Page 45Page 45

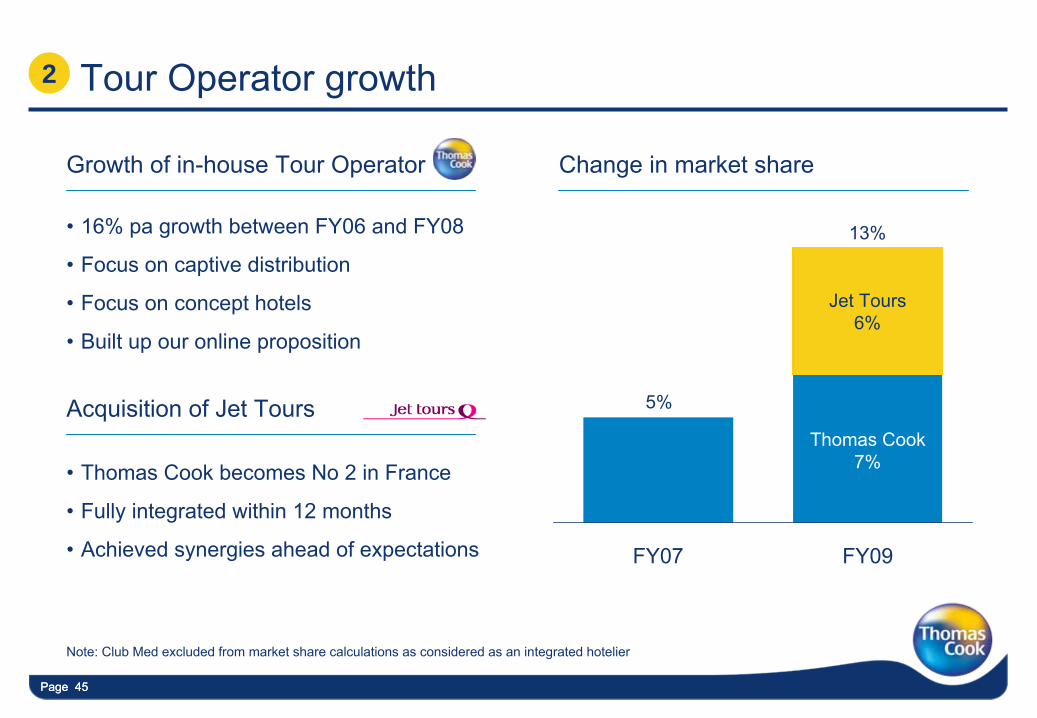

Growth of in-house Tour Operator

Tour Operator growth2

Change in market share

•

16% pa growth between FY06 and FY08

•

Focus on captive distribution

•

Focus on concept hotels

•

Built up our online proposition

Acquisition of Jet Tours

•

Thomas Cook becomes No 2 in France

•

Fully integrated within 12 months

•

Achieved synergies ahead of expectations

Note: Club Med excluded from market share calculations as considered as an integrated hotelier

5%

13%

FY07 FY09

Jet Tours6%

Thomas Cook7%

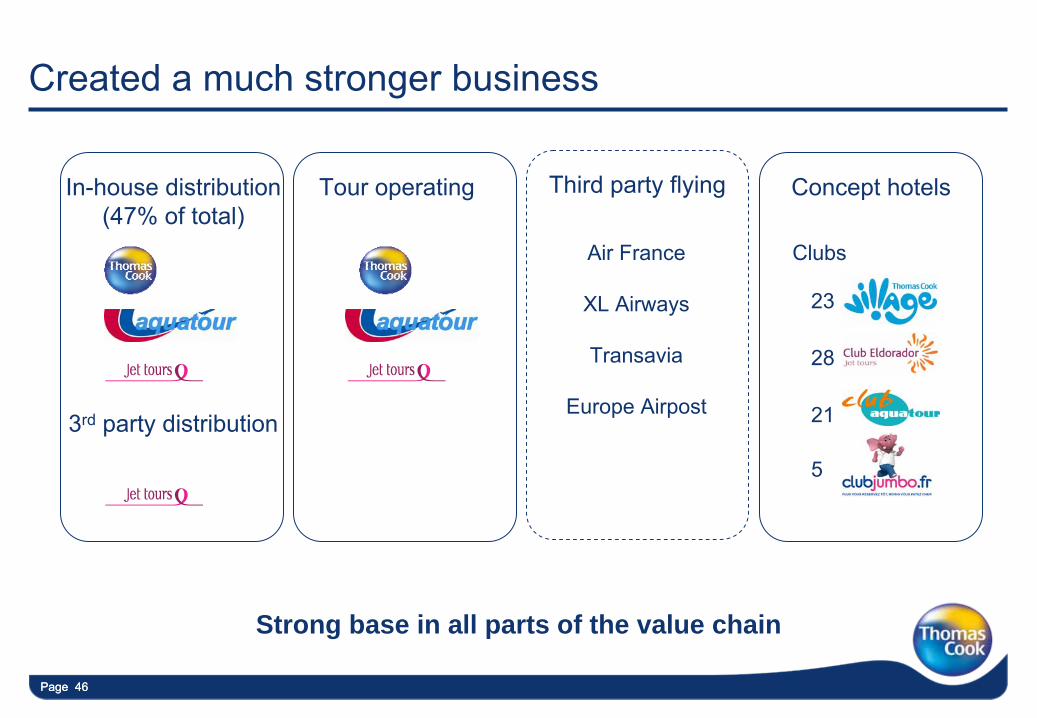

Page 46Page 4646

Created a much stronger business

3rd

party distribution

Third party flying

Clubs

In-house distribution(47% of total)

Tour operating Concept hotels

5

28

23

21

Air France

XL Airways

Transavia

Europe Airpost

Strong base in all parts of the value chain

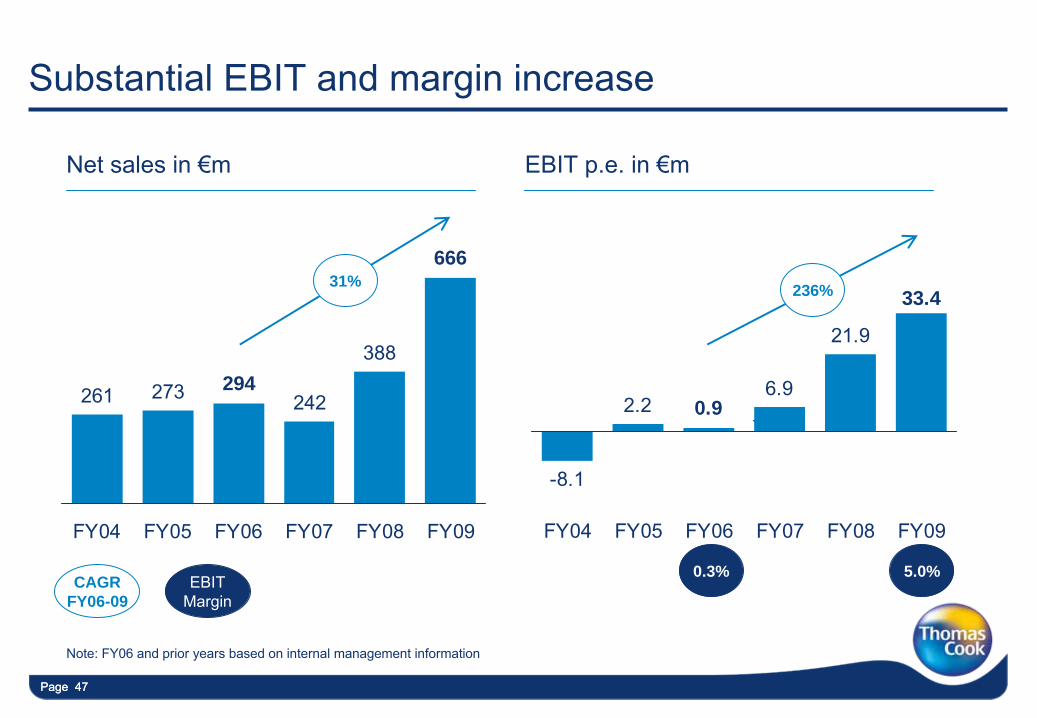

Page 47Page 47

Substantial EBIT and margin increase

261 273 242

388294

666

FY04 FY05 FY06 FY07 FY08 FY09

-8.1

2.26.9

21.9

33.4

0.9

FY04 FY05 FY06 FY07 FY08 FY09

`

0.3%

Net sales in €m EBIT p.e. in €m

31%

CAGR FY06-09

EBIT Margin

5.0%

Note: FY06 and prior years based on internal management information

236%

Page 48Page 48

Future growth

•

Growth of Thomas Cook online

•

Growth of Jet Tours by leveraging restructured third party distribution

•

Growth and margin through more and new club products e.g.

•

Maintain cost leadership and drive further efficiency improvements

Page 49

How to make profits in an unconsolidated and highly competitive German market?

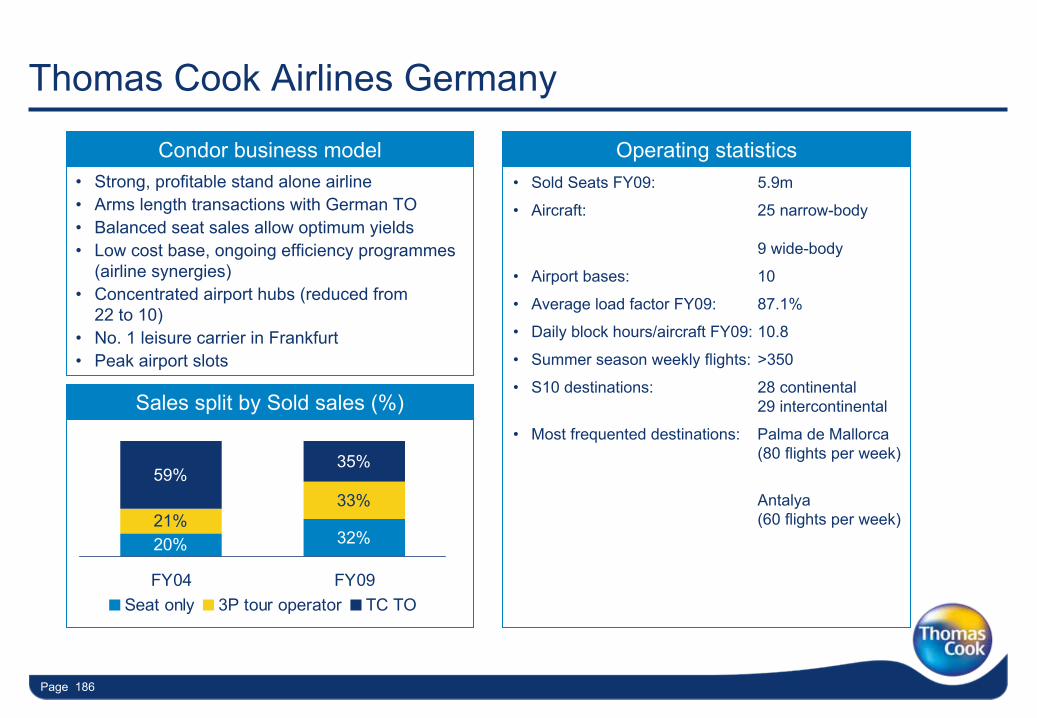

Peter Fankhauser –

CEO Central Europe

Page 50

Germany objectives

•

Turnaround a €160m loss making business

•

Become the most profitable German travel company

•

Create platform for future profitable growth

Page 51Page 51

Thomas Cook in Germany

Germany is Europe’s largest, but most fragmented, market

German travel market characteristics

•

Europe’s largest travel market; 50m pax

p.a.

•

Highly competitive and fragmented market

–

Full price transparency; high price competition

–

Capacity pressure from aggressive smaller carriers

–

Highly fragmented retail landscape

–

Retail brand

–

Up-market Tour Operator

A leading player, with 4 major brands

–

Value for money brand

–

Mass market Tour Operator

–

Last minute brand

–

Airline

Page 52Page 52

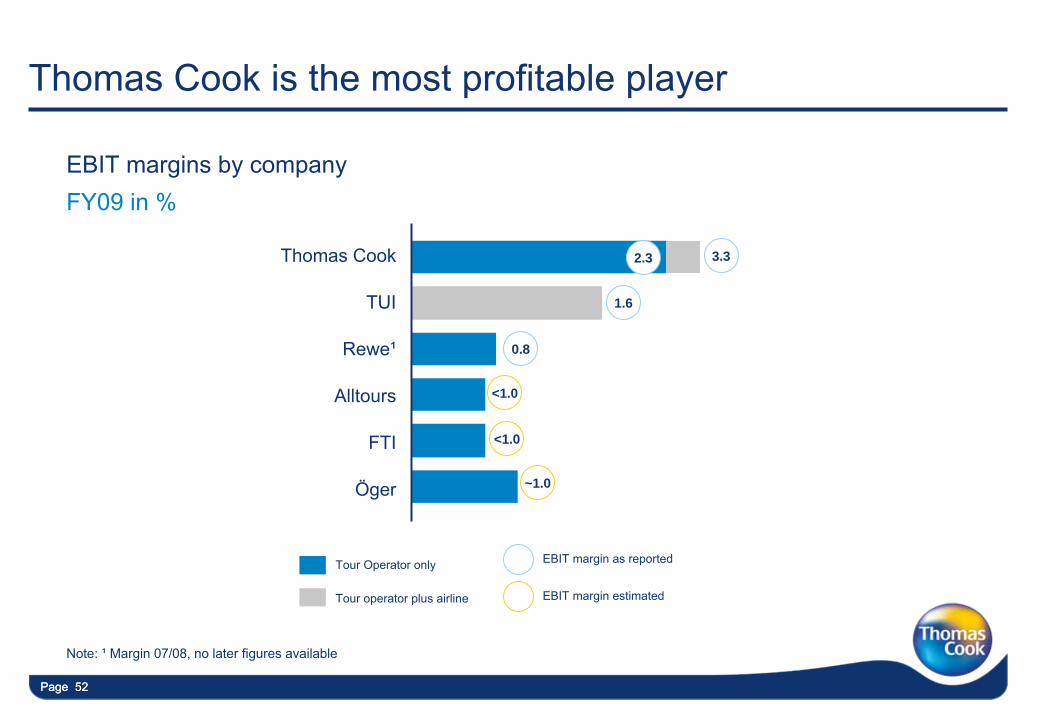

Thomas Cook is the most profitable player

EBIT margins by company FY09 in %

Thomas Cook

TUI

Alltours

Rewe¹

FTI

Öger

EBIT margin as reportedTour Operator only

Tour operator plus airline EBIT margin estimated

3.3

1.6

<1.0

<1.0

~1.0

0.8

2.3

Note: ¹

Margin 07/08, no later figures available

Page 53Page 53

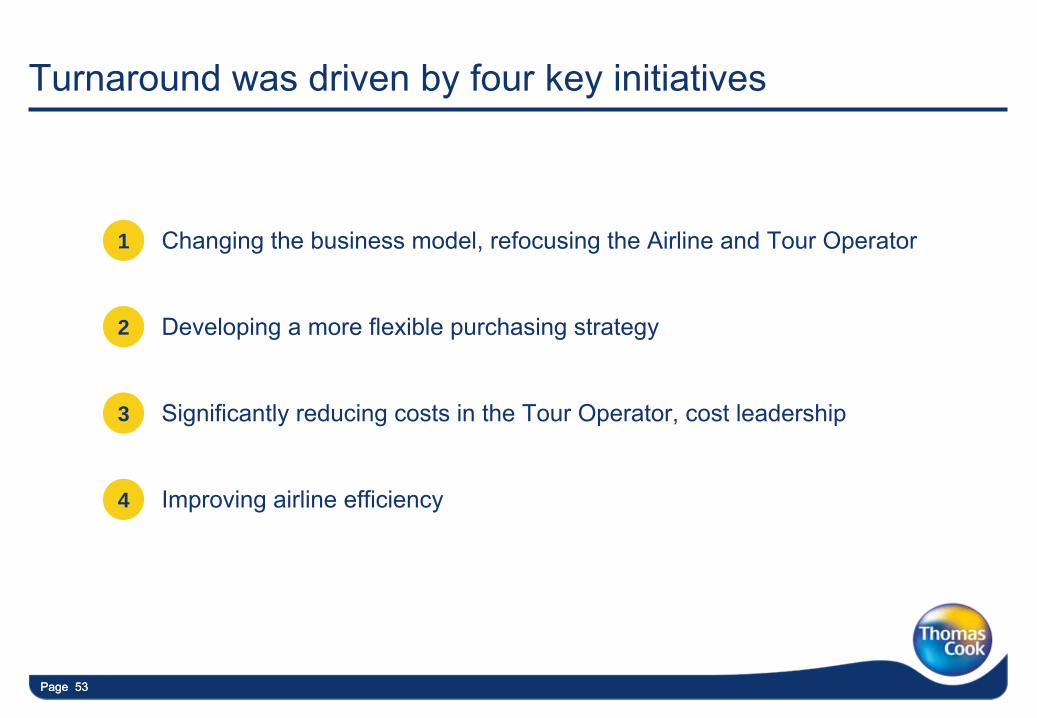

Turnaround was driven by four key initiatives

•

Changing the business model, refocusing the Airline and Tour Operator

•

Developing a more flexible purchasing strategy

•

Significantly reducing costs in the Tour Operator, cost leadership

•

Improving airline efficiency

1

2

3

4

Page 54Page 54

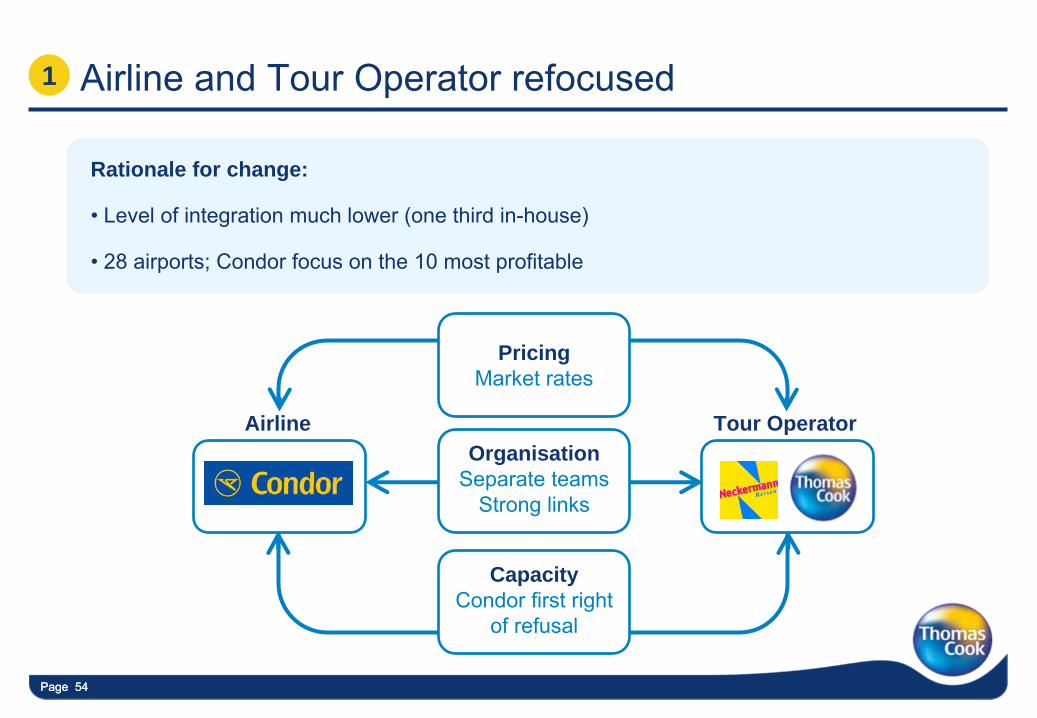

Rationale for change:

•

Level of integration much lower (one third in-house)

•

28 airports; Condor focus on the 10 most profitable

Airline and Tour Operator refocused1

Tour OperatorAirlineOrganisation

Separate teamsStrong links

PricingMarket rates

CapacityCondor first right

of refusal

Page 55Page 55

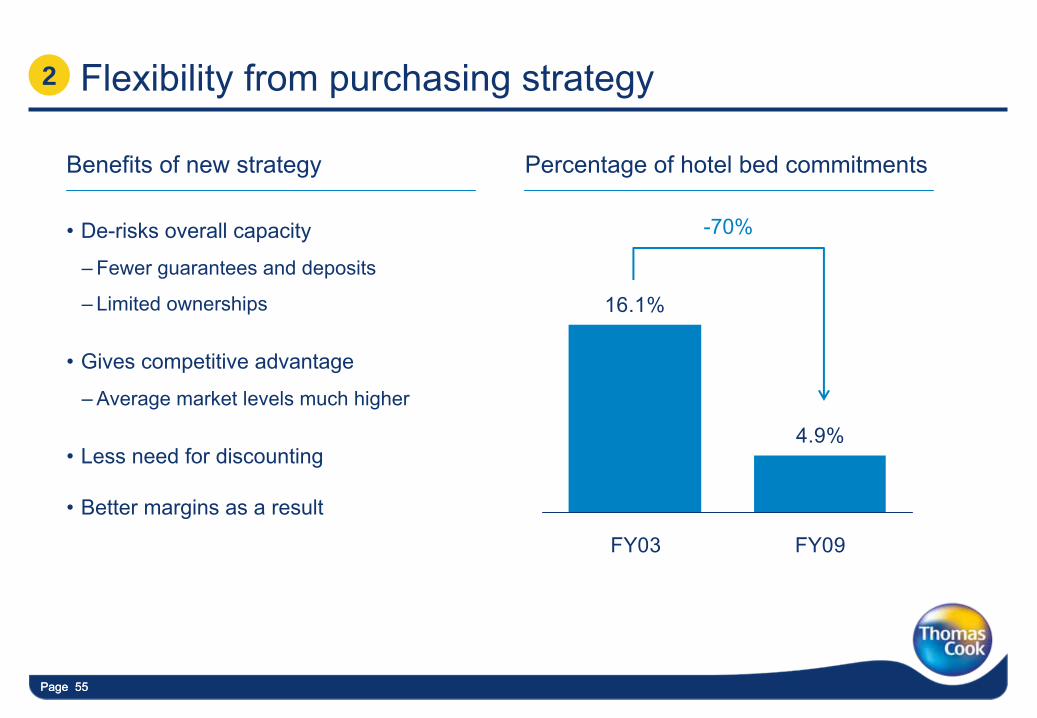

Flexibility from purchasing strategy

•

De-risks overall capacity

–

Fewer guarantees and deposits

–

Limited ownerships

•

Gives competitive advantage

–

Average market levels much higher

•

Less need for discounting

•

Better margins as a result

Benefits of new strategy Percentage of hotel bed commitments

16.1%

4.9%

FY03 FY09

-70%

2

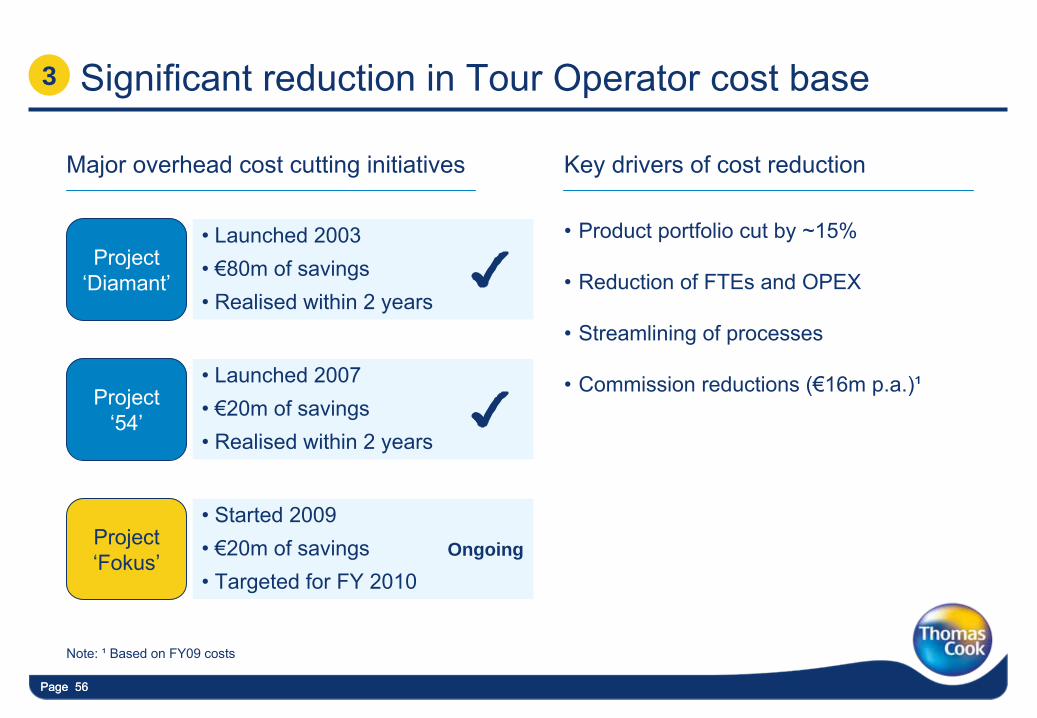

Page 56Page 56

•

Launched 2003 •

€80m of savings•

Realised within 2 years

•

Launched 2007 •

€20m of savings•

Realised within 2 years

•

Started 2009 •

€20m of savings•

Targeted for FY 2010

Significant reduction in Tour Operator cost base

•

Product portfolio cut by ~15%

•

Reduction of FTEs and OPEX

•

Streamlining of processes

•

Commission reductions (€16m p.a.)¹

Major overhead cost cutting initiatives

3

Project ‘Diamant’

Project ‘54’

Project ‘Fokus’

Ongoing

Key drivers of cost reduction

Note: ¹

Based on FY09 costs

Page 57Page 57

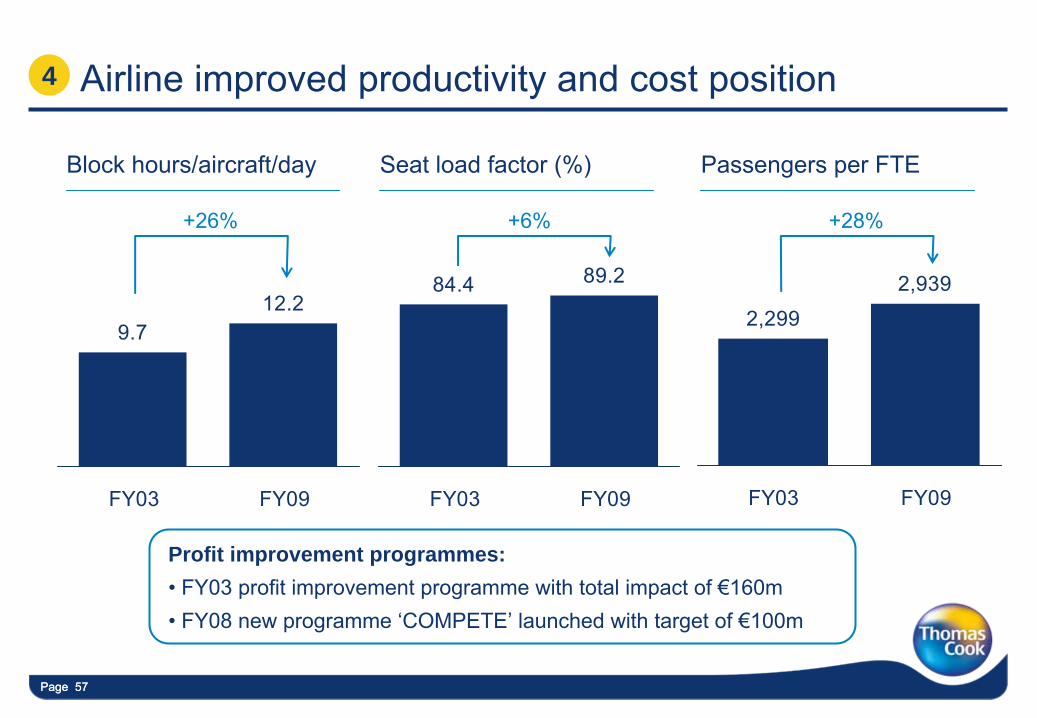

Airline improved productivity and cost position

Block hours/aircraft/day Seat load factor (%) Passengers per FTE

4

9.712.2

FY03 FY09

+26%

84.4 89.2

FY03 FY09

2,299

2,939

FY03 FY09

Profit improvement programmes:•

FY03 profit improvement programme with total impact of €160m•

FY08 new programme ‘COMPETE’

launched with target of €100m

+6% +28%

Page 58Page 58

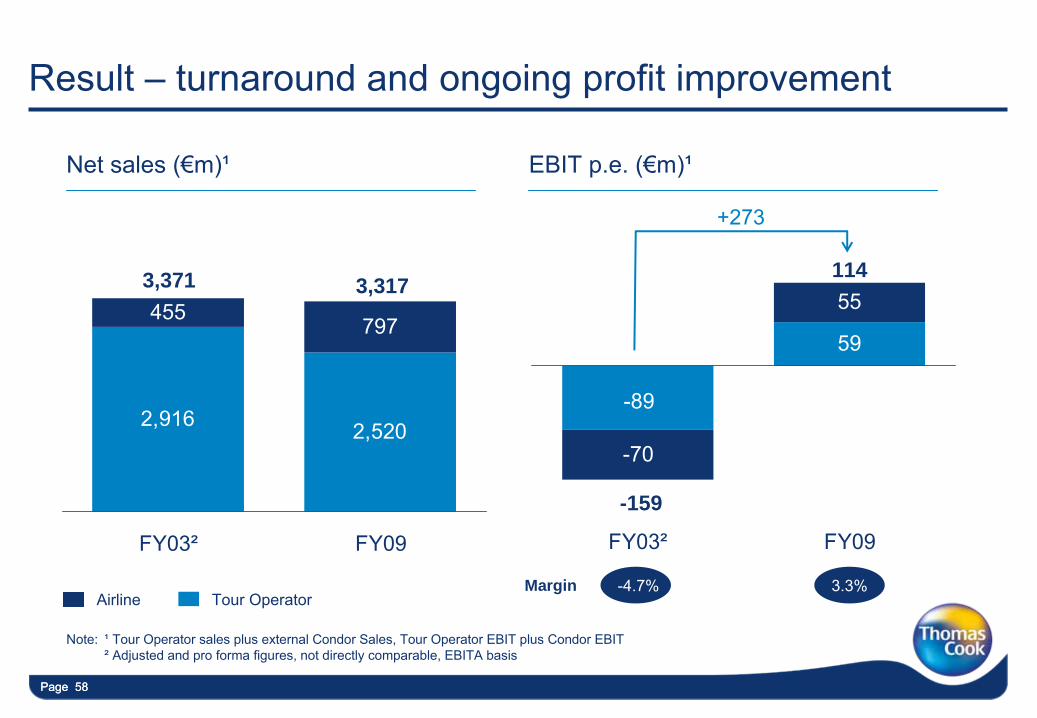

Result –

turnaround and ongoing profit improvement

2,916 2,520

455797

FY03² FY09

Net sales (€m)¹

3,371 3,317

Tour Operator

Note: ¹

Tour Operator sales plus external Condor Sales, Tour Operator EBIT plus Condor EBIT ²

Adjusted and pro forma figures, not directly comparable, EBITA basis

Airline

EBIT p.e. (€m)¹

59

-70

55

-89

FY03² FY09

-159

114

-4.7% 3.3%Margin

+273

Page 59Page 59

Future growth

•

Extend mainstream ‘live pricing’

model to drive growth

•

Expand online share, introduce ePackaging and grow OTA business

•

Extend exclusive and differentiated concepts like

•

Continue to drive cultural change through Group values

•

Centralise overseas purchasing and functions to reduce costs

•

Continue to look for opportunities to consolidate the market

Page 60

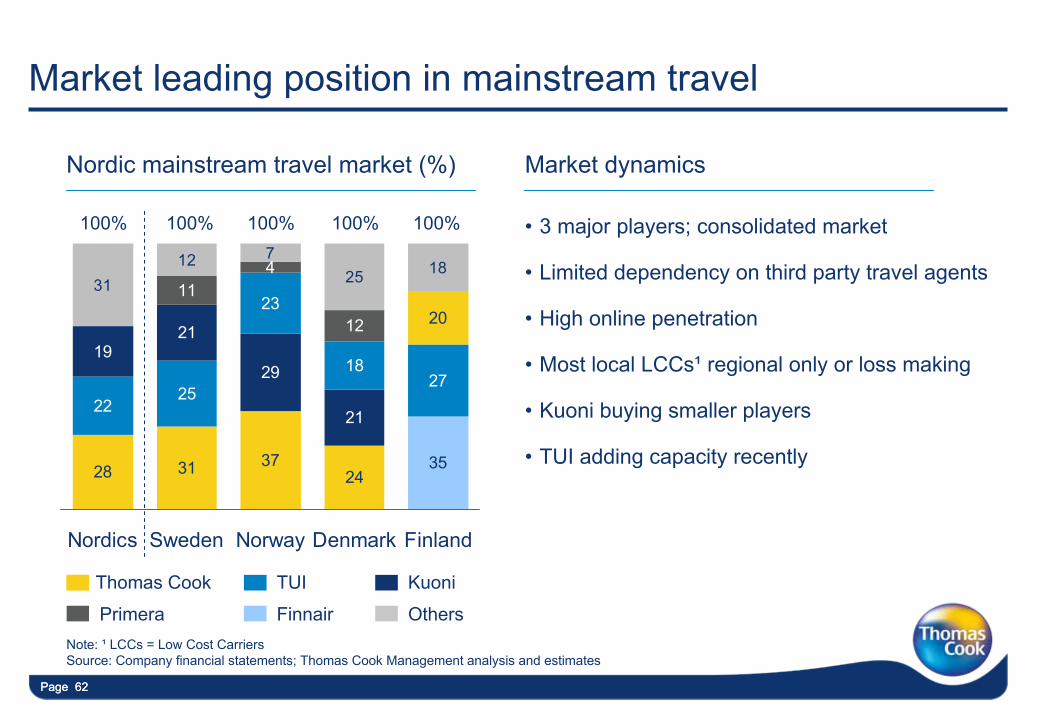

How to defend market leading margins of 8-9% in Nordic markets?

Sam Weihagen –

CEO Northern Europe

Page 61

Northern Europe objectives

•

Defend industry leading margins in mainstream

•

Strengthen market leading position

•

Create platform for future growth

Page 62Page 62

•

3 major players; consolidated market

•

Limited dependency on third party travel agents

•

High online penetration

•

Most local LCCs¹

regional only or loss making

•

Kuoni

buying smaller players

•

TUI adding capacity recently

Market leading position in mainstream travel

Nordic mainstream travel market (%) Market dynamics

Thomas Cook TUI Kuoni

Primera Finnair Others

3524

373128

2725

22

20

21

29

2119

18

2312

411

1825712

31

FinlandDenmarkNorwaySwedenNordics

100% 100% 100% 100% 100%

Note: ¹

LCCs = Low Cost Carriers

Source: Company financial statements; Thomas Cook Management analysis and estimates

Page 63Page 63

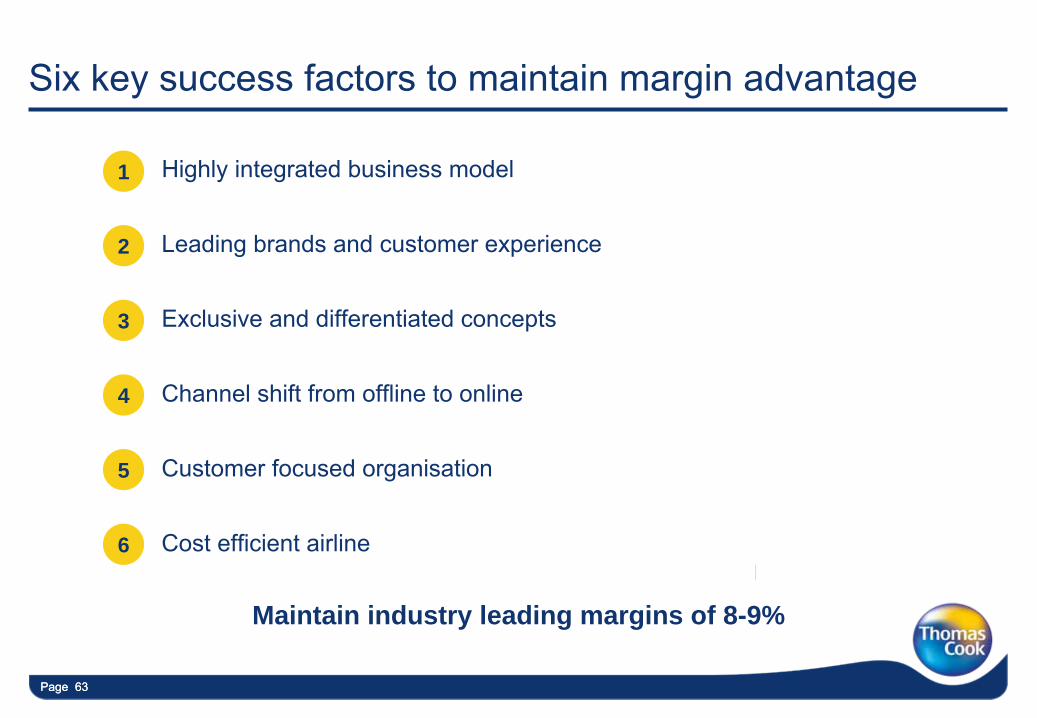

Six key success factors to maintain margin advantage

•

Highly integrated business model

•

Leading brands and customer experience

•

Exclusive and differentiated concepts

•

Channel shift from offline to online

•

Customer focused organisation

•

Cost efficient airline

1

2

3

4

5

Maintain industry leading margins of 8-9%

6

Page 64Page 64

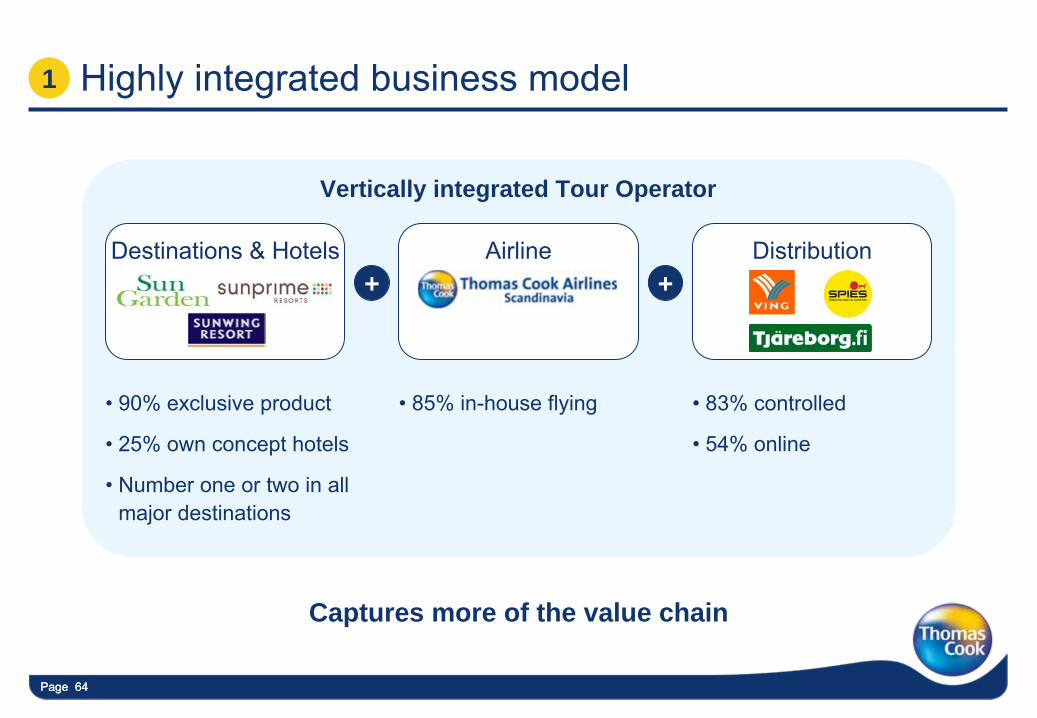

Highly integrated business model1

Destinations & Hotels Airline Distribution+ +

Vertically integrated Tour Operator

•

90% exclusive product

•

25% own concept hotels

•

Number one or two in all major destinations

•

85% in-house flying •

83% controlled

•

54% online

Captures more of the value chain

Page 65Page 65

Market leading brands and customer experience

•

Ving

–

biggest travel brand in Sweden and Norway

•

Spies –

biggest travel brand in Denmark

•

Tjäreborg

–

highly trusted brand in Finland

•

Ving.se

voted the best travel website in Sweden¹

•

Positive customer feedback year after year

•

Over 96% customer satisfaction

•

96% customers recommend us to friends

•

Loyalty driven by exclusive hotel concepts

Market leading brands Differentiated customer experience

2

Page 65

Note: ¹

also voted best overall website in Sweden

Page 66

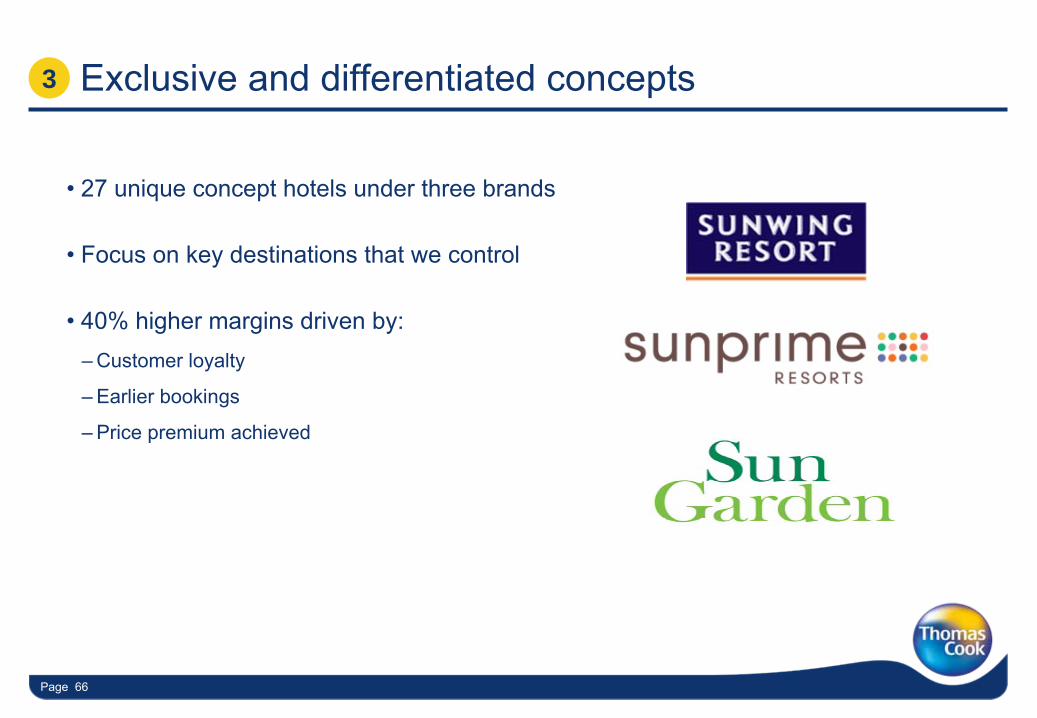

Exclusive and differentiated concepts

•

27 unique concept hotels under three brands

•

Focus on key destinations that we control

•

40% higher margins driven by:–

Customer loyalty

–

Earlier bookings

–

Price premium achieved

- 66 -

3

Page 67Page 67

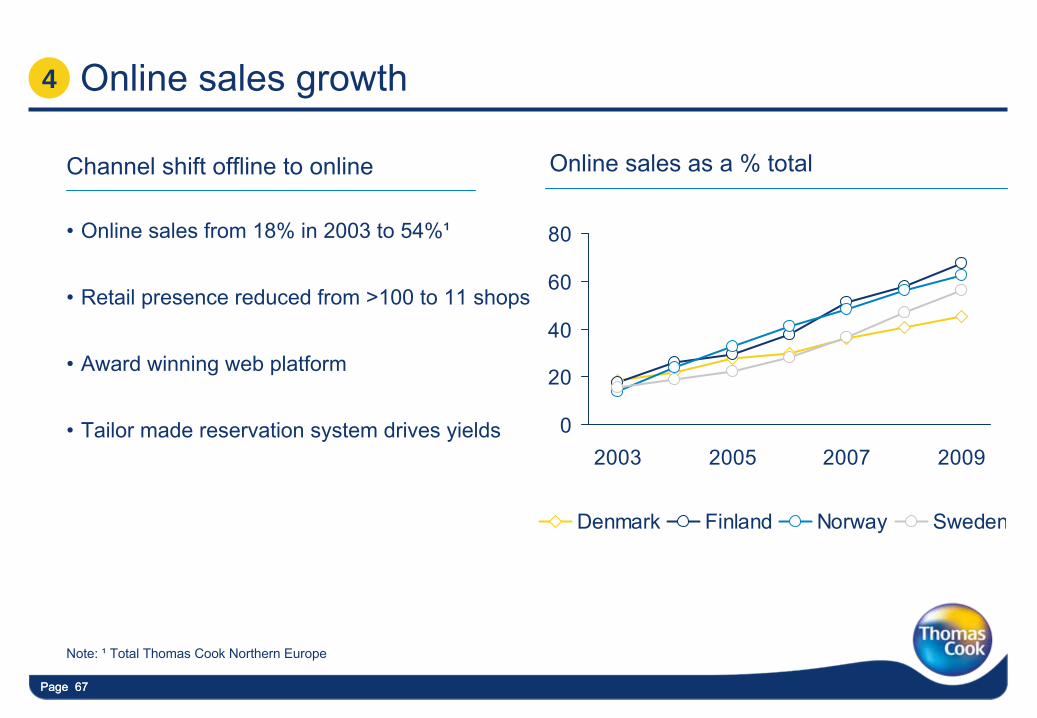

Online sales growth

•

Online sales from 18% in 2003 to 54%¹

•

Retail presence reduced from >100 to 11 shops

•

Award winning web platform

•

Tailor made reservation system drives yields

Channel shift offline to online

4

Online sales as a % total

0

20

40

60

80

2003 2005 2007 2009

Denmark Finland Norway Sweden

Note: ¹

Total Thomas Cook Northern Europe

Page 68Page 68

New customer friendly website 4

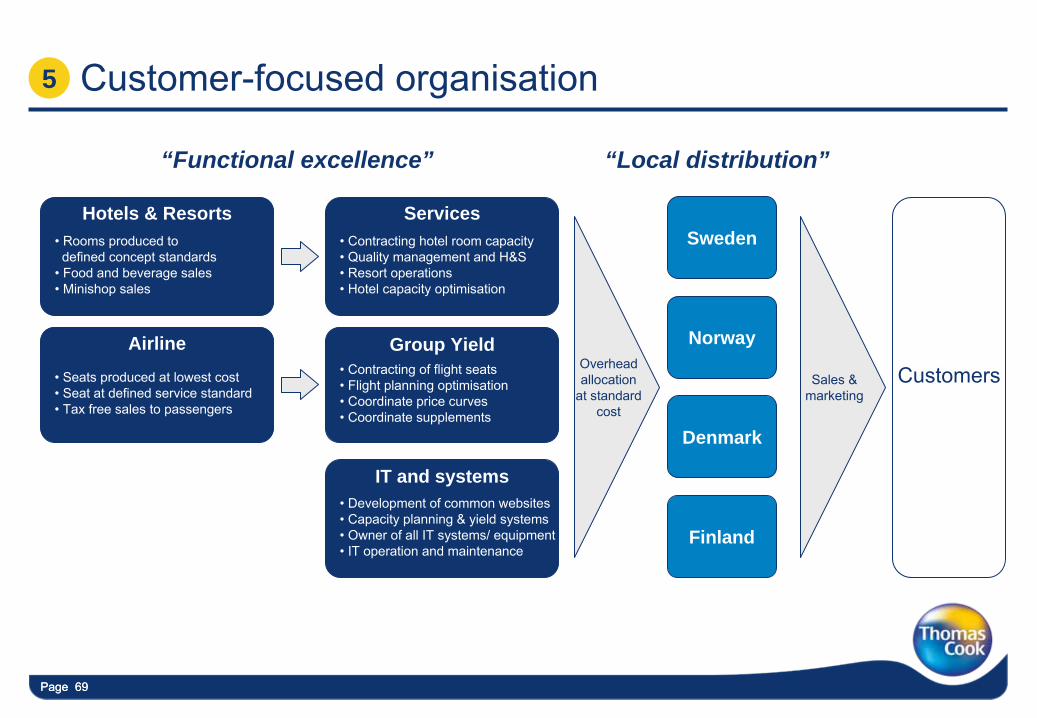

Page 69Page 69

“Functional excellence” “Local distribution”

Customers• Seats produced at lowest cost• Seat at defined service standard• Tax free sales to passengers

•

Rooms produced to defined concept standards

• Food and beverage sales• Minishop

sales

Sweden

Norway

Denmark

Finland

Overhead allocation

at standard cost

Sales & marketing

• Development of common websites• Capacity planning & yield systems• Owner of all IT systems/ equipment• IT operation and maintenance

• Contracting of flight seats• Flight planning optimisation• Coordinate price curves• Coordinate supplements

• Contracting hotel room capacity• Quality management and H&S• Resort operations• Hotel capacity optimisation

Services

Group Yield

IT and systems

Hotels & Resorts

Airline

5 Customer-focused organisation

Page 70

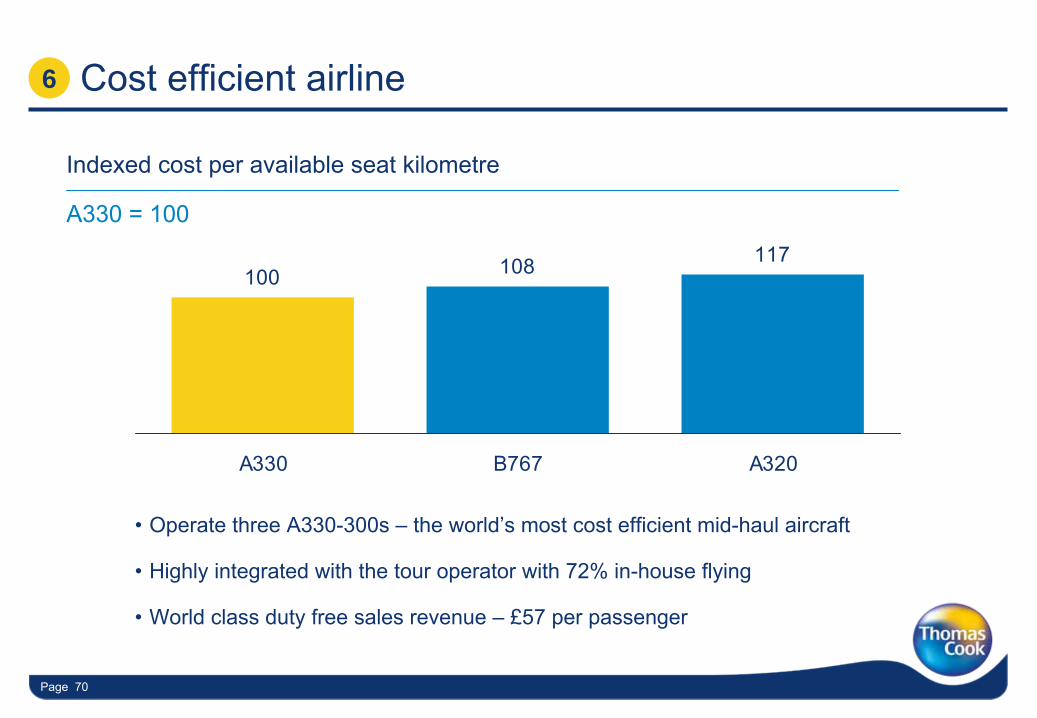

Cost efficient airline

- 70 -

6

•

Operate three A330-300s –

the world’s most cost efficient mid-haul aircraft

•

Highly integrated with the tour operator with 72% in-house flying

•

World class duty free sales revenue –

£57 per passenger

100 108 117

A330 B767 A320

A330 = 100

Indexed cost per available seat kilometre

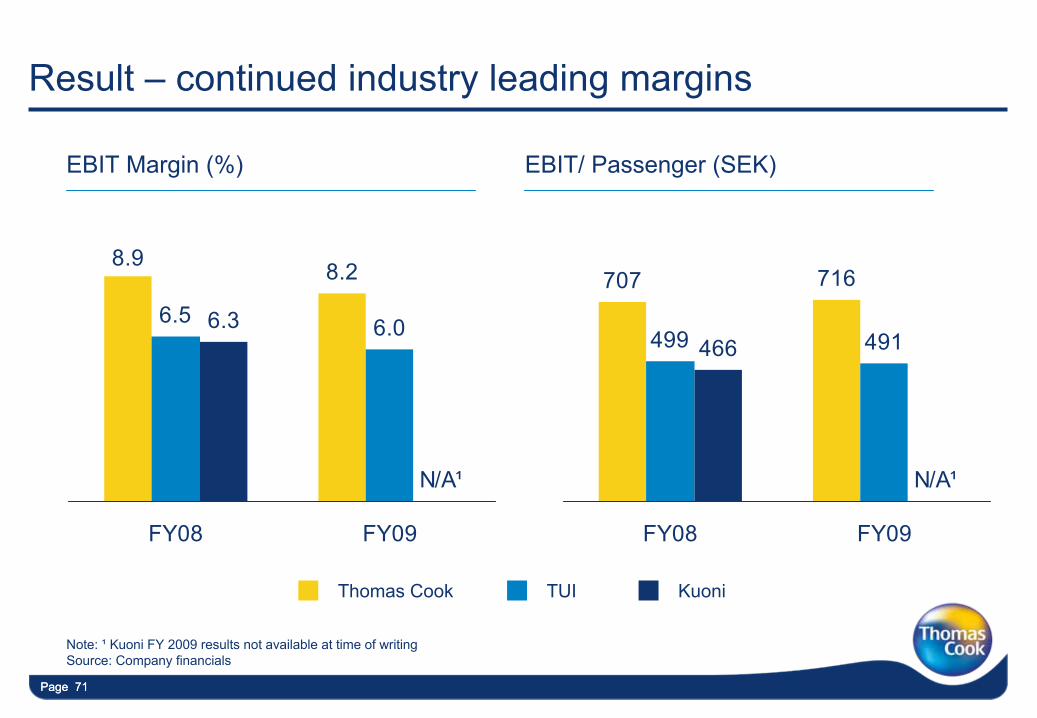

Page 71Page 71

8.9 8.2

6.5 6.06.3

N/A¹

FY08 FY09

Result –

continued industry leading margins

EBIT Margin (%) EBIT/ Passenger (SEK)

Note: ¹

Kuoni

FY 2009 results not available at time of writing

Source: Company financials

707 716

499 491466

N/A¹

FY08 FY09

Thomas Cook TUI Kuoni

Page 72

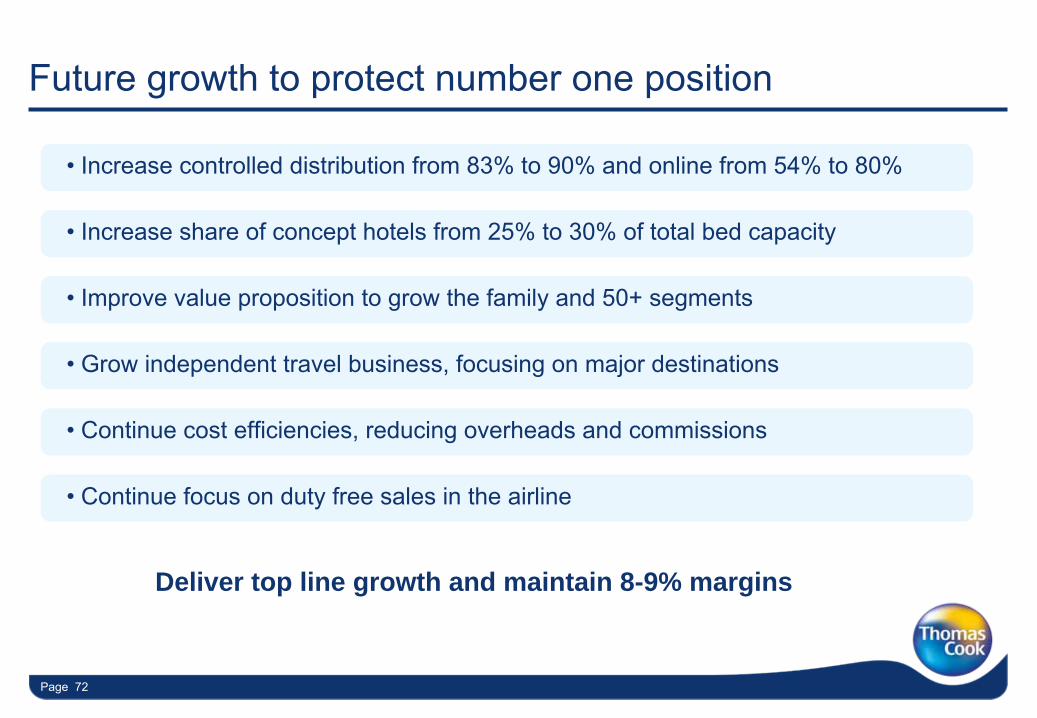

Future growth to protect number one position

•

Increase controlled distribution from 83% to 90% and online from

54% to 80%

•

Increase share of concept hotels from 25% to 30% of total bed capacity

•

Improve value proposition to grow the family and 50+ segments

•

Grow independent travel business, focusing on major destinations

•

Continue cost efficiencies, reducing overheads and commissions

•

Continue focus on duty free sales in the airline

Deliver top line growth and maintain 8-9% margins

Page 73

Summary

Manny Fontenla-Novoa –

Group CEO

Page 74Page 74

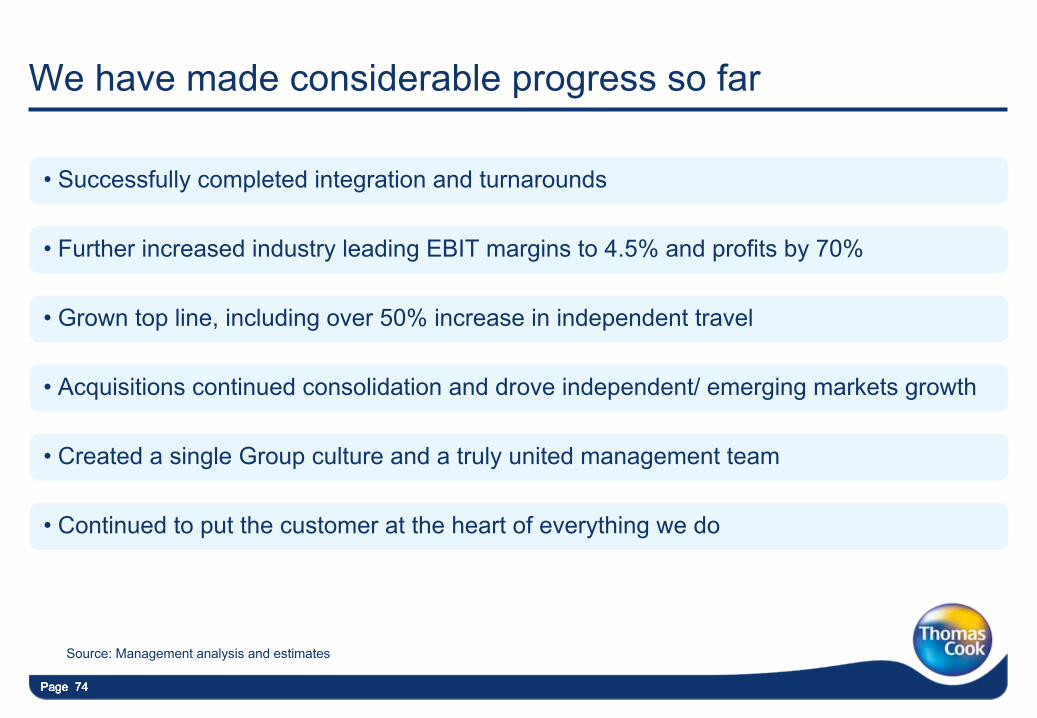

We have made considerable progress so far

Page 74

•

Successfully completed integration and turnarounds

•

Further increased industry leading EBIT margins to 4.5% and profits by 70%

•

Grown top line, including over 50% increase in independent travel

•

Acquisitions continued consolidation and drove independent/ emerging markets growth

•

Created a single Group culture and a truly united management team

•

Continued to put the customer at the heart of everything we do

Source: Management analysis and estimates

Page 75Page 75

We have the strategy, structure, people, brands, scale and ambition to

significantly grow top and bottom lines

Strategy for Growth

Page 77Page 77

What we will cover in this section

•

Key trends in our market place

•

Our strategy for growing top and bottom line

•

Case studies of major strategic initiatives

•

Summary of our medium term growth potential

Page 77

Page 78

Key trends in our market place

Jürgen Büser –

Group Strategy

Director

Page 79Page 79

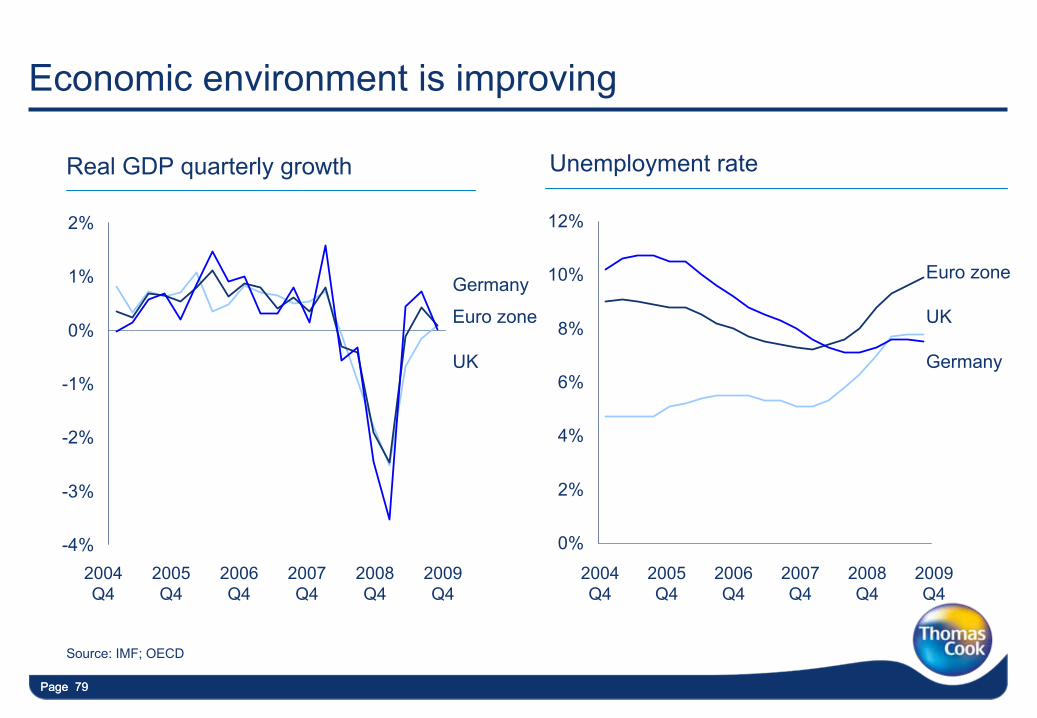

Economic environment is improving

Source: IMF; OECD

Real GDP quarterly growth Unemployment rate

2004 Q4

2005 Q4

2006 Q4

2007 Q4

2008 Q4

2009 Q4

Euro zone

-4%

-3%

-2%

-1%

0%

1%

2%

UK

2004 Q4

2005 Q4

2006 Q4

2007 Q4

2008 Q4

2009 Q4

0%

2%

4%

6%

8%

10%

12%

UK

Euro zone

Germany

Germany

Page 80

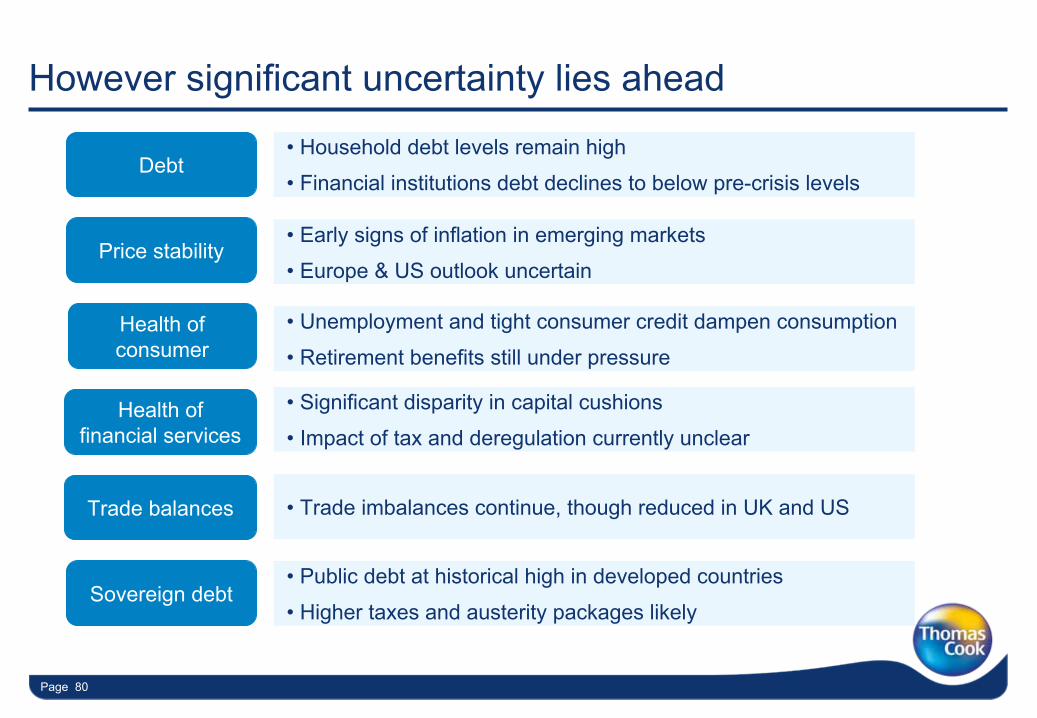

However significant uncertainty lies ahead

Debt

Price stability• Early signs of inflation in emerging markets

• Europe & US outlook uncertain

Health of consumer

• Unemployment and tight consumer credit dampen consumption

• Retirement benefits still under pressure

Health of financial services

• Significant disparity in capital cushions

• Impact of tax and deregulation currently unclear

Trade balances • Trade imbalances continue, though reduced in UK and US

Sovereign debt• Public debt at historical high in developed countries

• Higher taxes and austerity packages likely

• Household debt levels remain high

• Financial institutions debt declines to below pre-crisis levels

Page 81

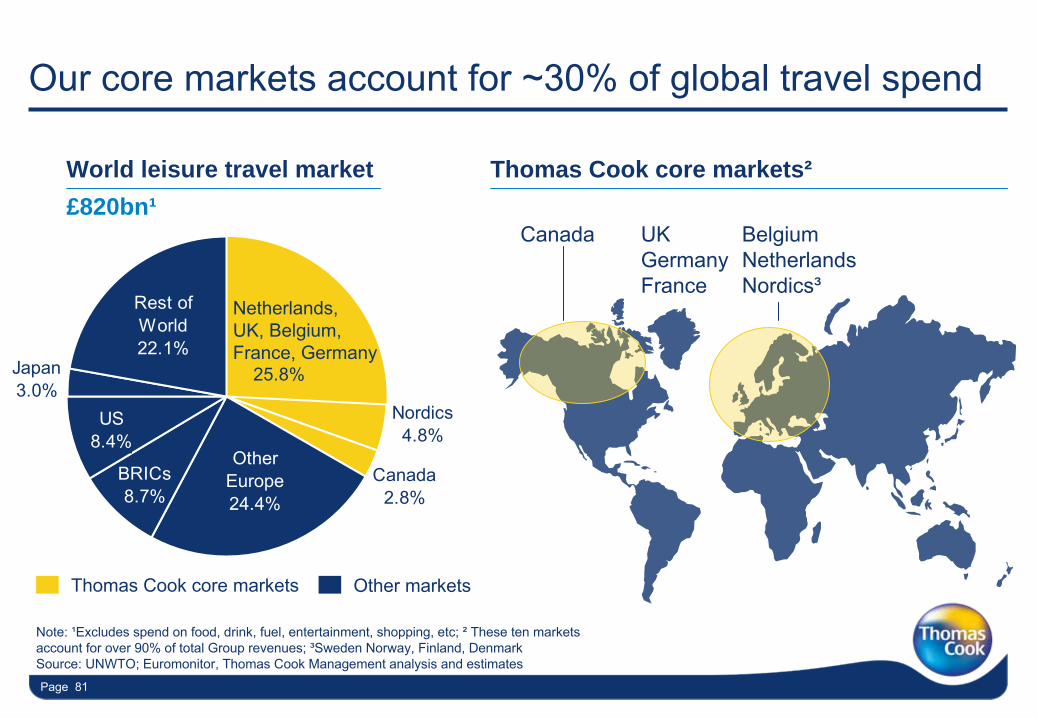

Our core markets account for ~30% of global travel spend

Leisure

CorporateCorporate

Leisure

Leisure

Corporate

Canada UKGermanyFrance

BelgiumNetherlandsNordics³

Note: ¹Excludes spend on food, drink, fuel, entertainment, shopping, etc; ²

These ten markets account for over 90% of total Group revenues; ³Sweden Norway, Finland, DenmarkSource: UNWTO; Euromonitor, Thomas Cook Management analysis and estimates

Thomas Cook core markets²

Japan3.0%

25.8%

Other Europe24.4%

Rest of World22.1%

US8.4%

BRICs8.7%

Canada2.8%

Nordics4.8%

World leisure travel market £820bn¹

Netherlands, UK, Belgium, France, Germany

Thomas Cook core markets Other markets

Page 82Page 82

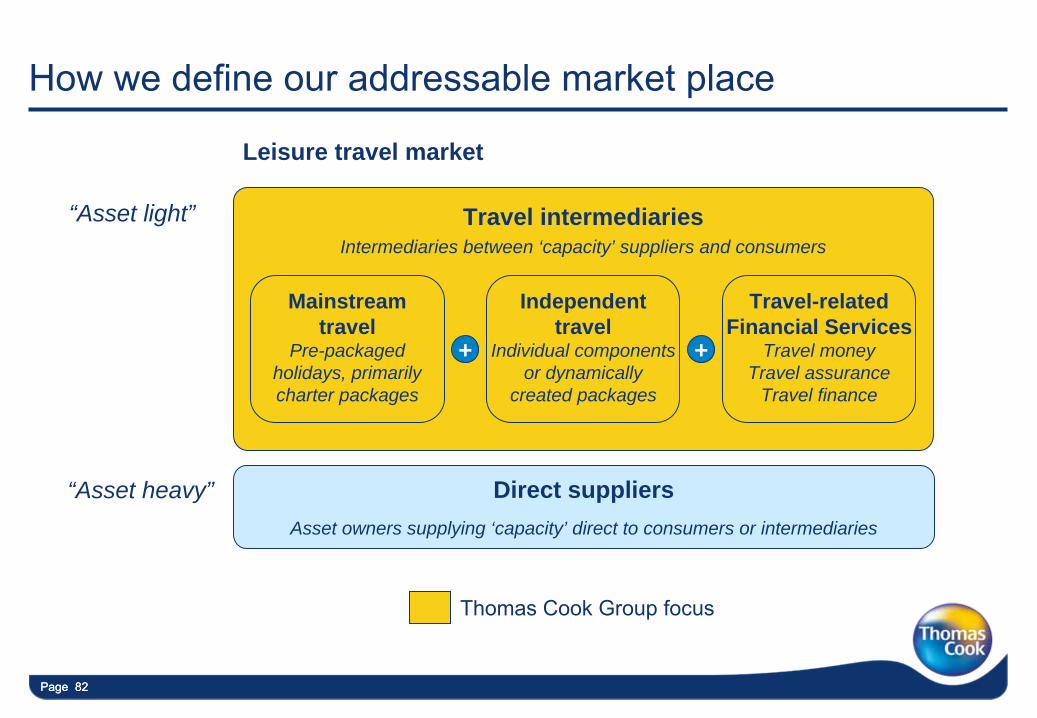

How we define our addressable market place

Thomas Cook Group focus

Travel intermediaries Intermediaries between ‘capacity’ suppliers and consumers

Direct suppliersAsset owners supplying ‘capacity’ direct to consumers or intermediaries

Mainstream travel

Pre-packaged holidays, primarily charter packages

Independent travel

Individual components or dynamically

created packages

Travel-related Financial Services

Travel money Travel assurance

Travel finance

+ +

“Asset light”

“Asset heavy”

Leisure travel market

Page 83Page 83

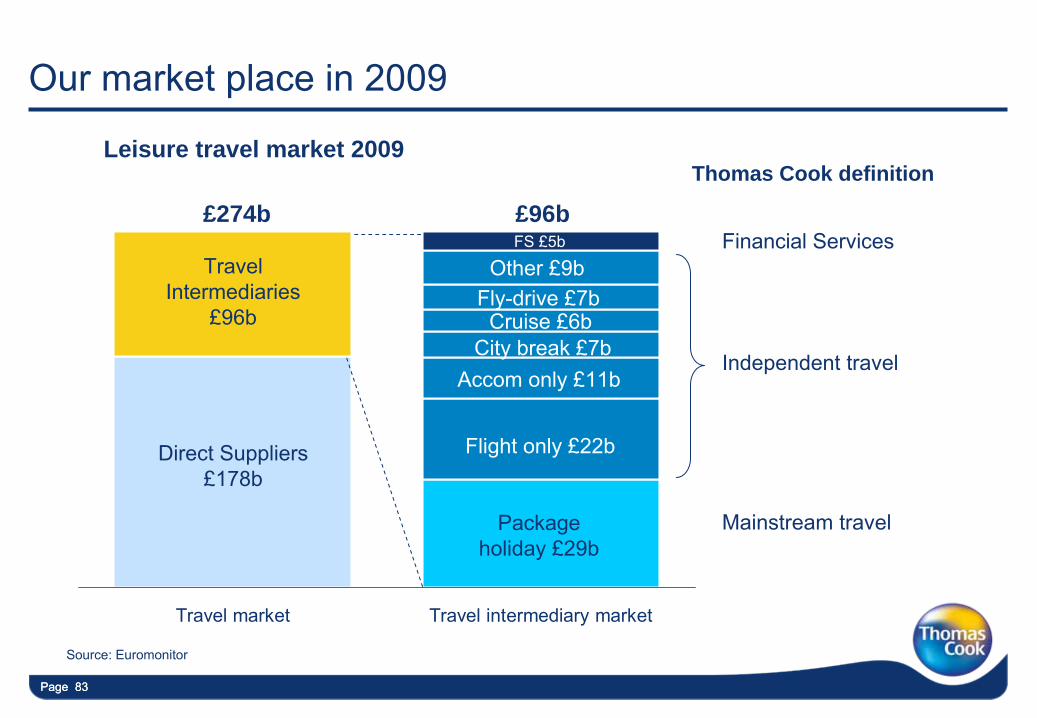

Leisure travel market 2009

Our market place in 2009

Travel market Travel intermediary market

Mainstream travel

Independent travel

Financial Services£274b £96b

Source: Euromonitor

Thomas Cook definition

Travel

Intermediaries£96b

Direct Suppliers£178b

Other £9bFly-drive £7b

City break £7bAccom

only £11b

Flight only £22b

Cruise £6b

Package holiday £29b

FS £5b

Page 84

Key trends affecting our market place

Major travel markets continue to grow faster than the general economy

Intermediaries continue to capture around a third of total expenditure

Mainstream travel market will continue to be large and to grow in value terms

Independent travel to drive majority of the growth in the intermediary market

Online growth will be faster than offline; growth in both mainstream and independent

Thomas Cook key destinations will continue to grow fast

Consumers will continue to drive change in the industry

1

2

3

4

5

7

6

Page 85

50

100

150

200

250

300

350

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08

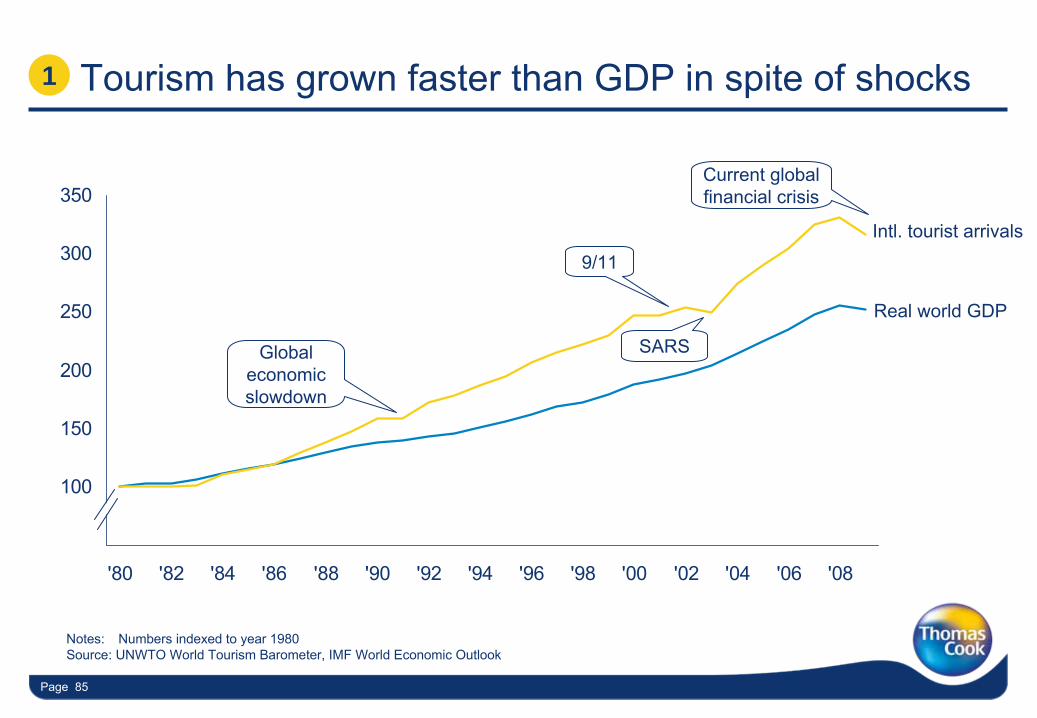

Tourism has grown faster than GDP in spite of shocks

Notes:

Numbers indexed to year 1980Source: UNWTO World Tourism Barometer, IMF World Economic Outlook

Real world GDP

Intl. tourist arrivals

9/11

SARSGlobal economic slowdown

Current global financial crisis

1

Page 86

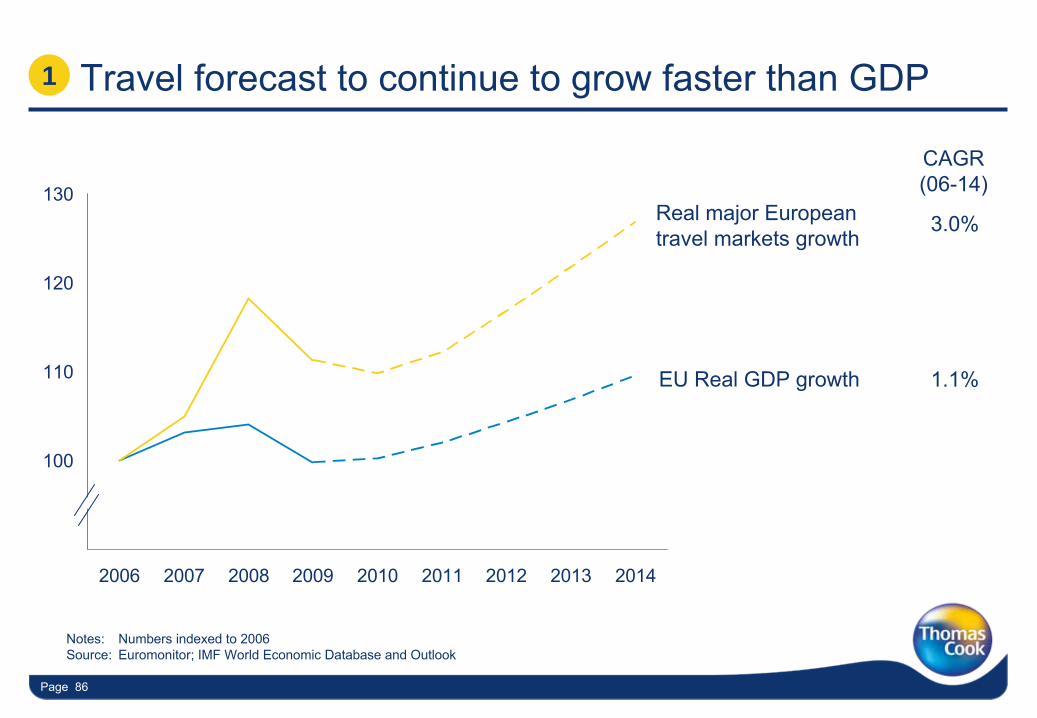

Travel forecast to continue to grow faster than GDP

Notes:

Numbers indexed to 2006Source: Euromonitor; IMF World Economic Database and Outlook

Real major European travel markets growth

EU Real GDP growth

CAGR

(06-14)

3.0%

1.1%

90

100

110

120

130

2006 2007 2008 2009 2010 2011 2012 2013 2014

1

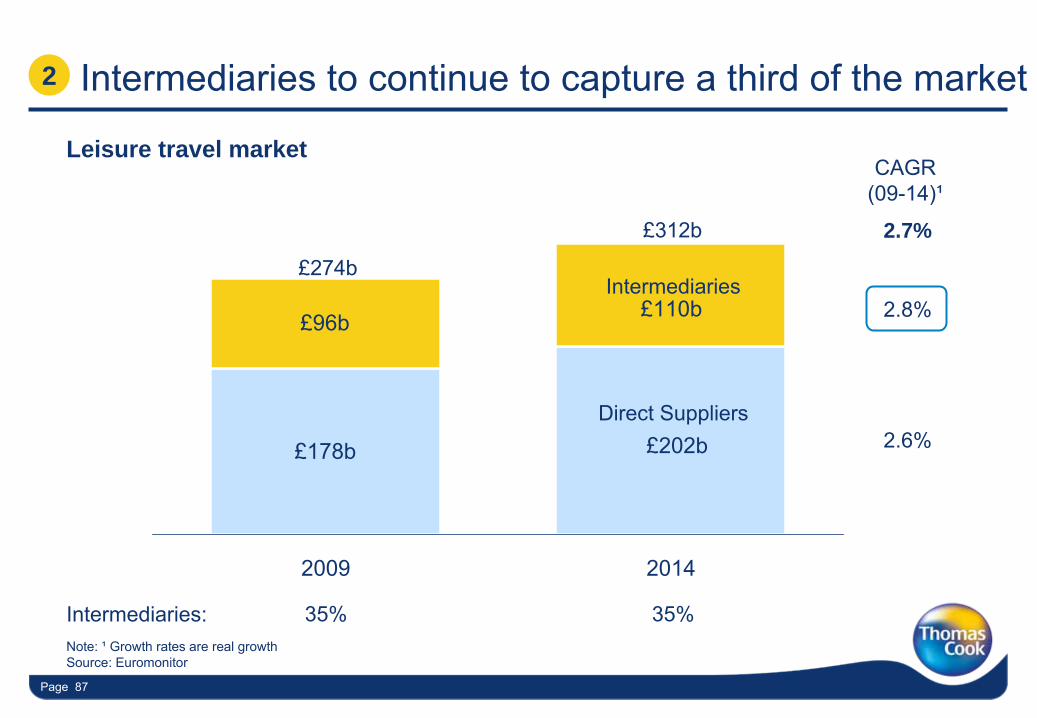

Page 87

£202b£178b

£110b£96b

2009 2014

CAGR(09-14)¹

£274b

Note: ¹

Growth rates are real growthSource: Euromonitor

£312b

2.6%

2.8%

2.7%

Intermediaries: 35% 35%

2

Intermediaries

Direct Suppliers

Intermediaries to continue to capture a third of the market

Leisure travel market

Page 88

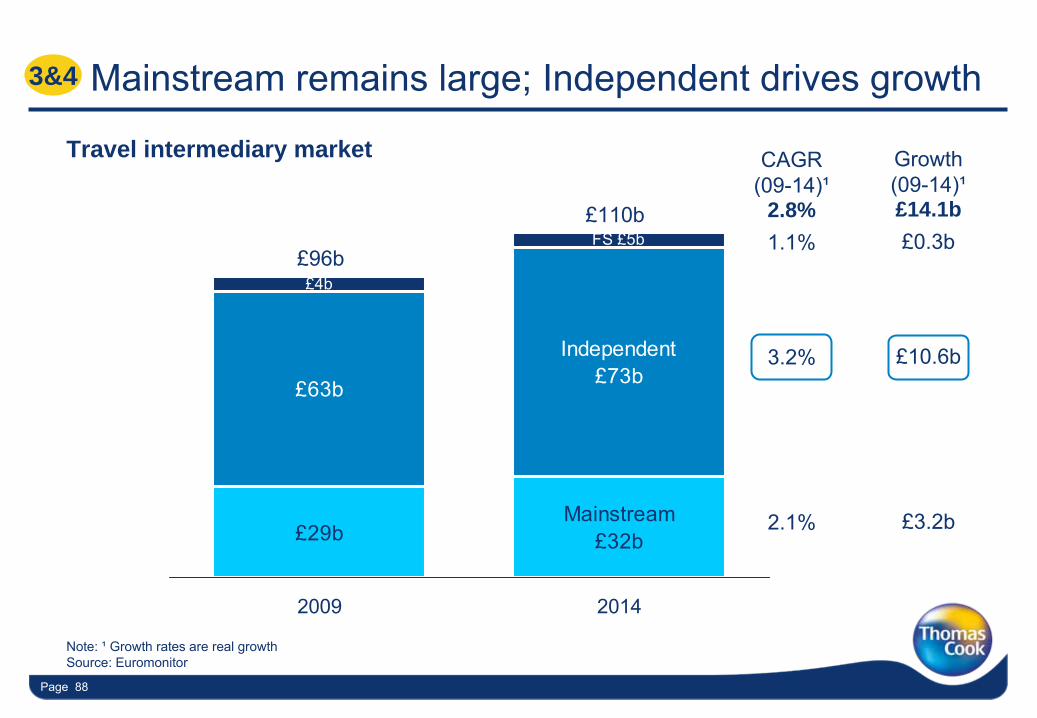

Mainstream £32b

Independent £73b

FS £5b

£29b

£63b

£4b

2009 2014

CAGR(09-14)¹

3.2%

£96b

Travel intermediary market

£110b

2.1%

2.8%1.1%

Growth(09-14)¹

£10.6b

£3.2b

£14.1b£0.3b

3&4 Mainstream remains large; Independent drives growth

Note: ¹

Growth rates are real growthSource: Euromonitor

Page 89

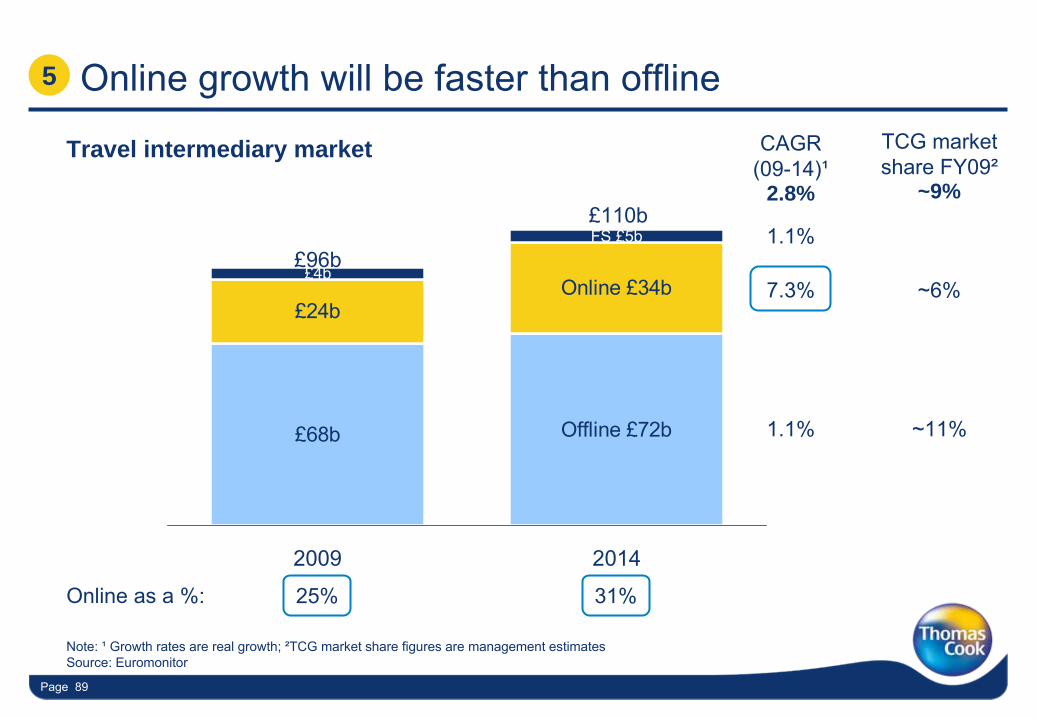

Online growth will be faster than offline

Offline £72b

Online £34b

FS £5b

£68b

£24b

£4b

2009 2014

7.3%

Online as a %: 25% 31%

£96b

£110b

1.1%

2.8%

1.1%

TCG market share FY09²

~6%

~11%

5

~9%

CAGR(09-14)¹

Travel intermediary market

Note: ¹

Growth rates are real growth; ²TCG market share figures are management estimatesSource: Euromonitor

Page 90

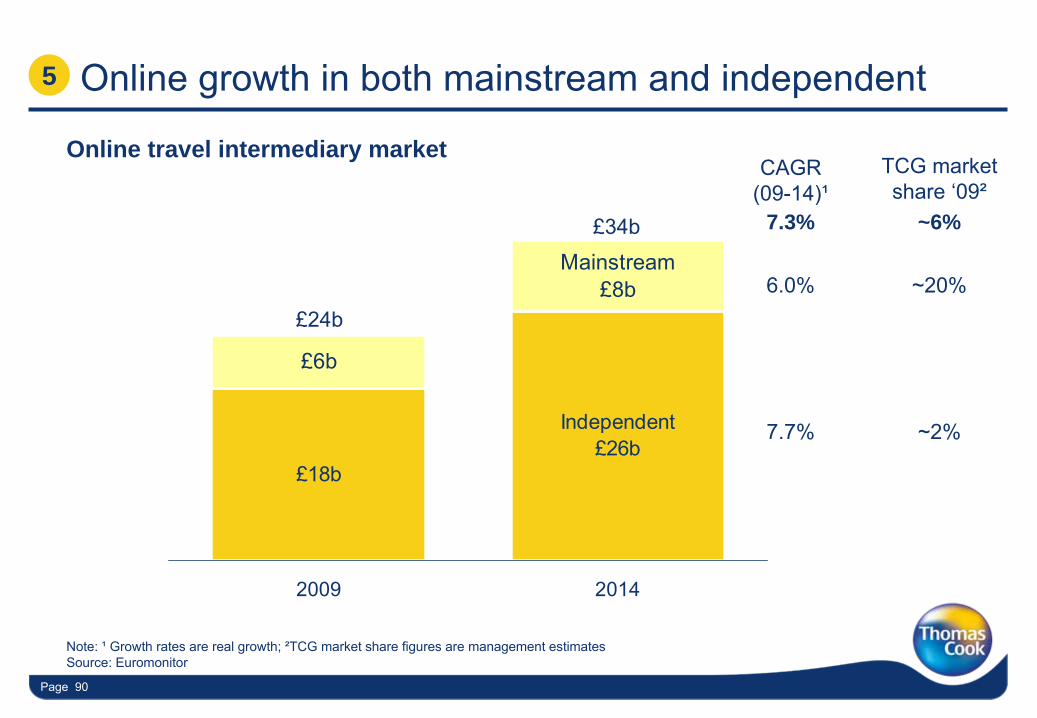

Online growth in both mainstream and independent

Independent £26b

Mainstream £8b

£18b

£6b

2009 2014

6.0%£24b

£34b

7.7%

7.3%

~20%

~2%

5

~6%

TCG market share ‘09²

CAGR(09-14)¹

Online travel intermediary market

Note: ¹

Growth rates are real growth; ²TCG market share figures are management estimatesSource: Euromonitor

Page 91

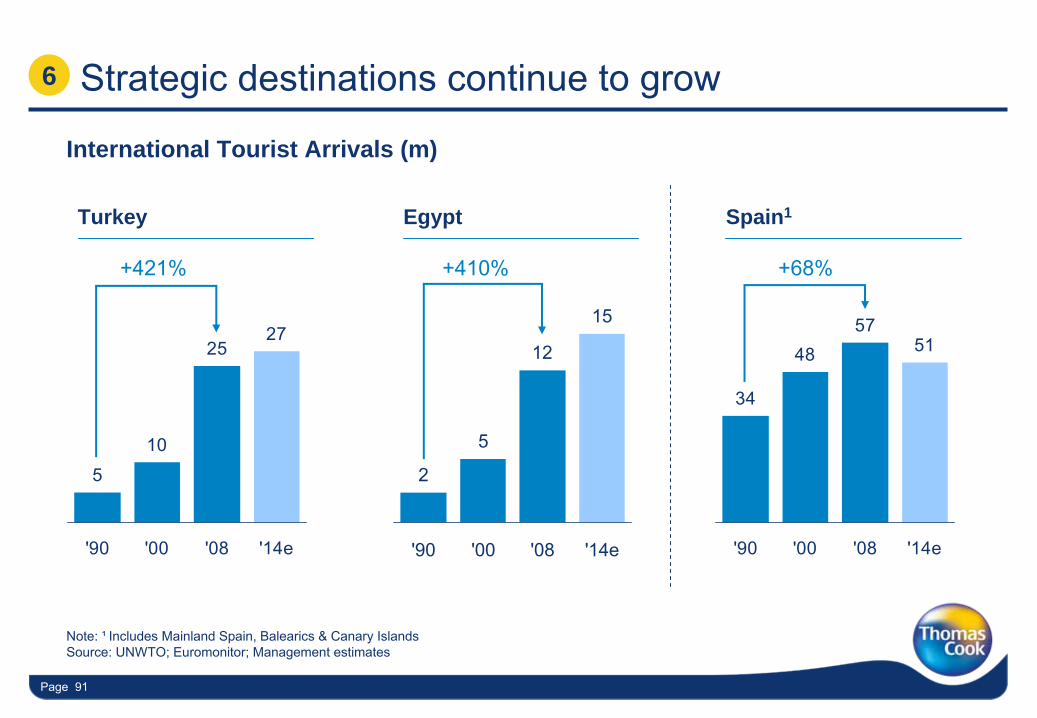

5

10

2527

'90 '00 '08 '14e

2

5

12

15

'90 '00 '08 '14e

Turkey Egypt

+421% +410%

Strategic destinations continue to grow

Note: ¹

Includes Mainland Spain, Balearics & Canary IslandsSource: UNWTO; Euromonitor; Management estimates

6

International Tourist Arrivals (m)

34

4857

51

'90 '00 '08 '14e

Spain1

+68%

Page 92

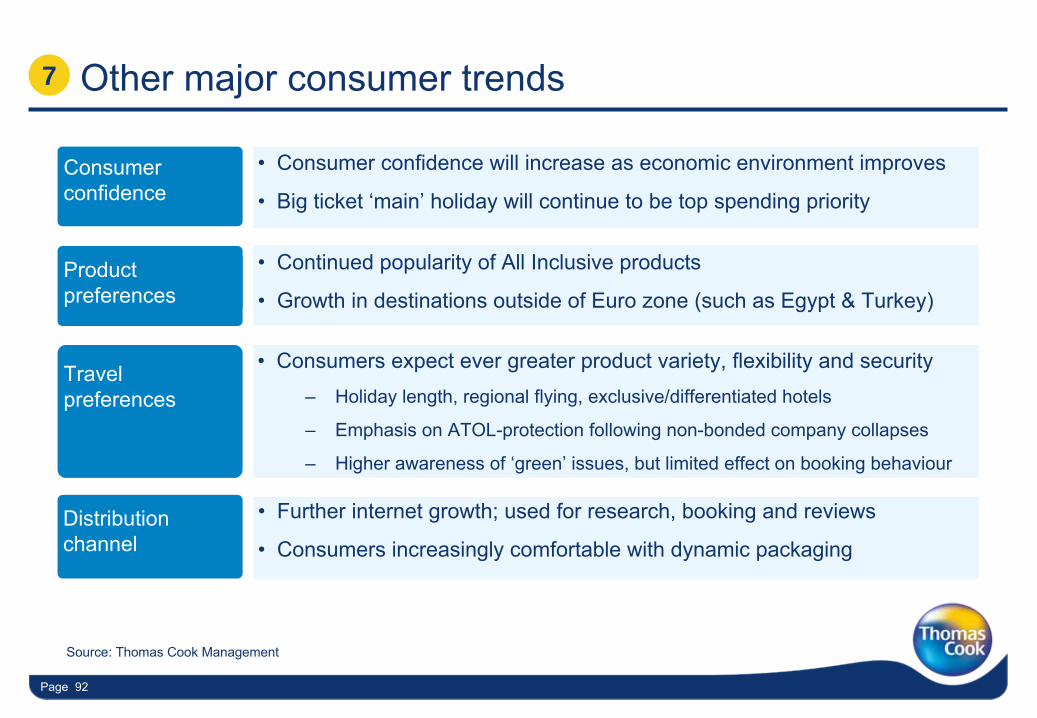

Other major consumer trends7

•

Further internet growth; used for research, booking and reviews

•

Consumers increasingly comfortable with dynamic packagingDistribution

channel

•

Consumers expect ever greater product variety, flexibility and security–

Holiday length, regional flying, exclusive/differentiated hotels

–

Emphasis on ATOL-protection following non-bonded company collapses

–

Higher awareness of ‘green’

issues, but limited effect on booking behaviour

Travel preferences

•

Consumer confidence will increase as economic environment improves

•

Big ticket ‘main’

holiday will continue to be top spending priorityConsumer confidence

•

Continued popularity of All Inclusive products

•

Growth in destinations outside of Euro zone (such as Egypt & Turkey)Product preferences

Source: Thomas Cook Management

Page 93

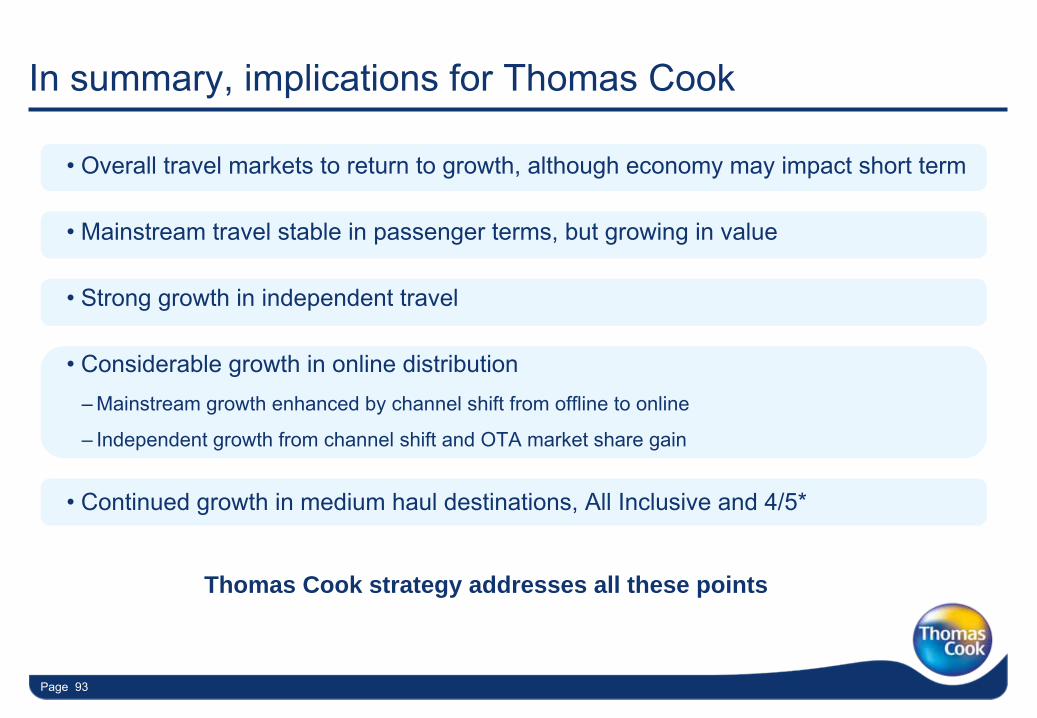

In summary, implications for Thomas Cook

•

Overall travel markets to return to growth, although economy may

impact short term

•

Mainstream travel stable in passenger terms, but growing in value

•

Strong growth in independent travel

•

Considerable growth in online distribution–

Mainstream growth enhanced by channel shift from offline to online

–

Independent growth from channel shift and OTA market share gain

•

Continued growth in medium haul destinations, All Inclusive and 4/5*

Thomas Cook strategy addresses all these points

Page 94

Medium Term Growth Strategy

Paul Hollingworth –

Group CFO

Page 95Page 95

Observations

•

Operations –

large complex business focused on the customer

•

People –

wealth and depth of experience

•

Finance –

renewed focus on cash management

•

Corporate –

fairly new to public company life

•

Open to change –

ambitious change programme; sign of greater organisational maturity

Lots of energy, lots to do, lots of opportunity

Page 96

Our strategy continues to serve us well

Strategic objectives

Strengthening our business and investing for growth

Financial rigourBrandsCustomer insightTechnology

Results orientated

Obsessed with customer service

United as one team Driving robust decisions

Pioneering our future

Values

ProductEnablers

Become a leading

independent travel provider

Become the leading

travel-related financial services provider

Capture growth and

value through M&A and

partnerships

Maximisevalue of

mainstream

Growth drivers

Vision

P R O U D

Page 97

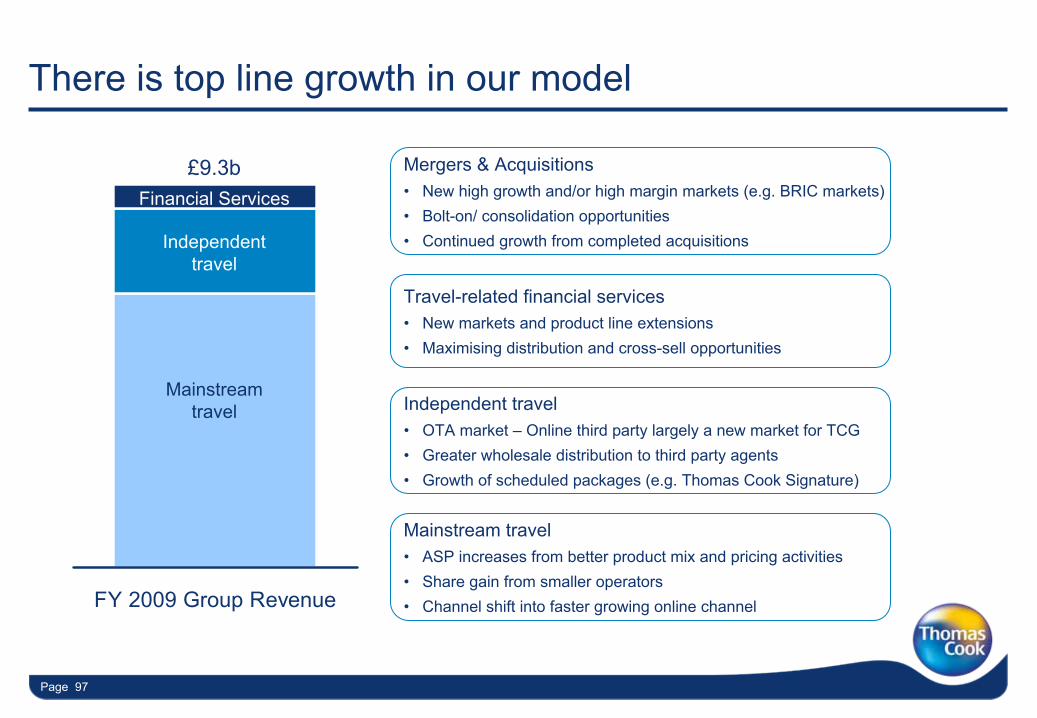

There is top line growth in our model

FY 2009 Group Revenue

£9.3b

Mainstream

travel

Independent

travel

Financial Services

Mergers & Acquisitions•

New high growth and/or high margin markets (e.g. BRIC markets)•

Bolt-on/ consolidation opportunities•

Continued growth from completed acquisitions

Travel-related financial services•

New markets and product line extensions•

Maximising distribution and cross-sell opportunities

Independent travel•

OTA market –

Online third party largely a new market for TCG•

Greater wholesale distribution to third party agents•

Growth of scheduled packages (e.g. Thomas Cook Signature)

Mainstream travel•

ASP increases from better product mix and pricing activities•

Share gain from smaller operators•

Channel shift into faster growing online channel

Page 98

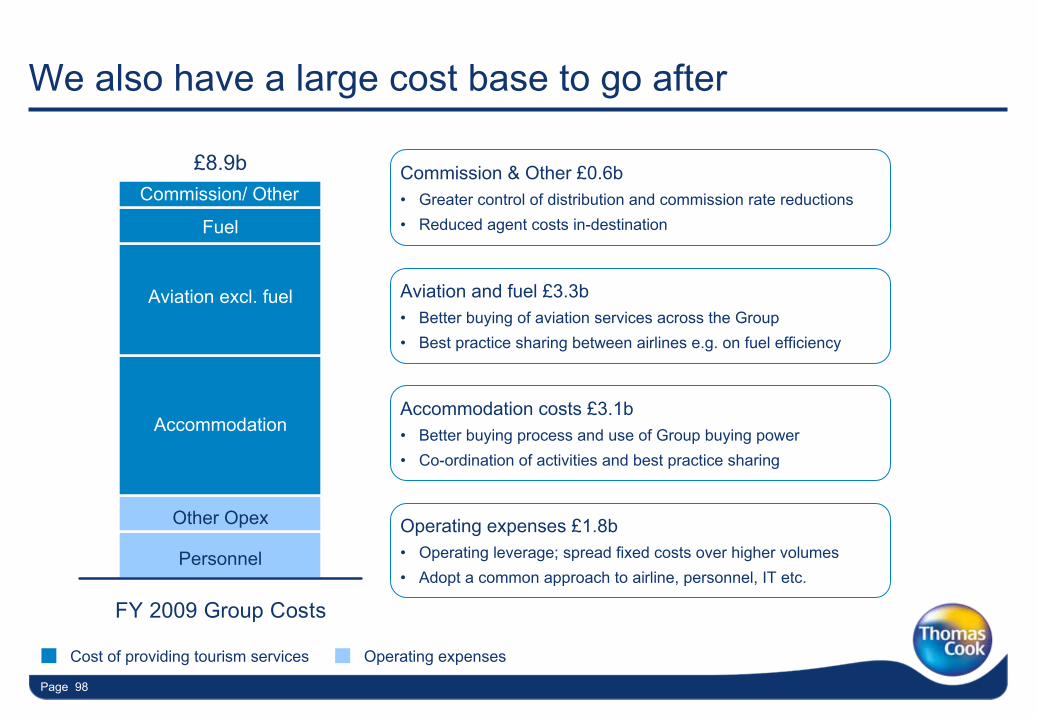

We also have a large cost base to go after

Cost of providing tourism services Operating expenses

FY 2009 Group Costs

£8.9b

Other Opex

Accommodation

Personnel

Aviation excl. fuel

Fuel

Commission/ OtherCommission & Other £0.6b•

Greater control of distribution and commission rate reductions•

Reduced agent costs in-destination

Aviation and fuel £3.3b•

Better buying of aviation services across the Group•

Best practice sharing between airlines e.g. on fuel efficiency

Accommodation costs £3.1b•

Better buying process and use of Group buying power•

Co-ordination of activities and best practice sharing

Operating expenses £1.8b•

Operating leverage; spread fixed costs over higher volumes•

Adopt a common approach to airline, personnel, IT etc.

Page 99

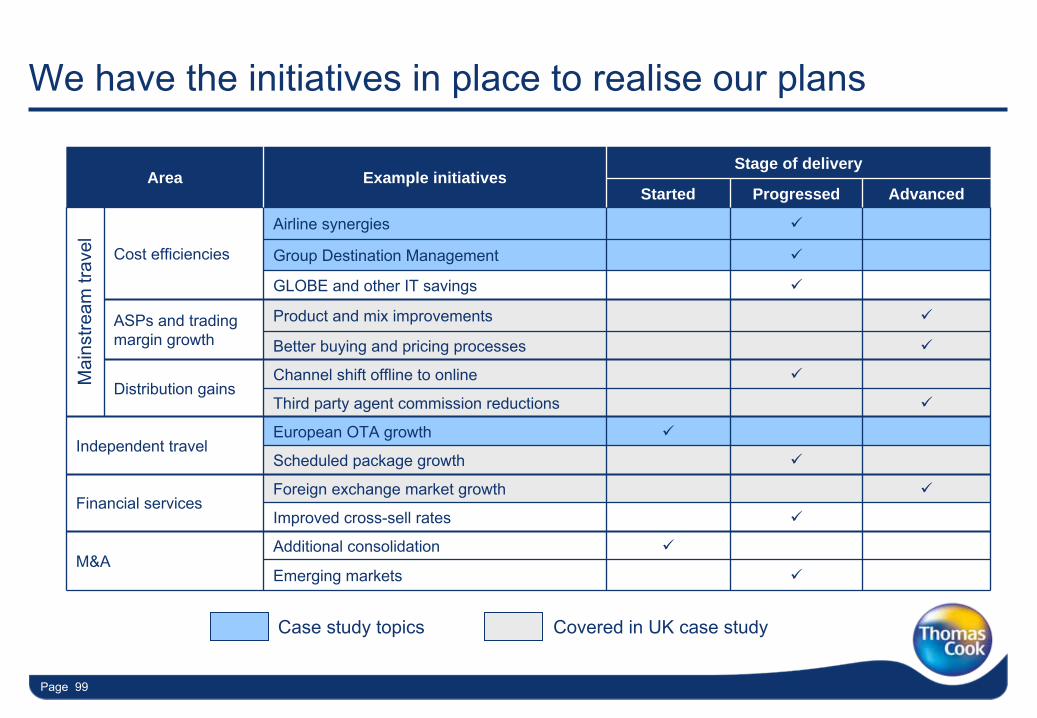

We have the initiatives in place to realise our plans

Area Example initiativesStage of delivery

Started Progressed Advanced

Cost efficiencies

Airline synergies

Group Destination Management

GLOBE and other IT savings

ASPs and trading margin growth

Product and mix improvements

Better buying and pricing processes

Distribution gainsChannel shift offline to online

Third party agent commission reductions

Independent travelEuropean OTA growth

Scheduled package growth

Financial servicesForeign exchange market growth

Improved cross-sell rates

M&AAdditional consolidation

Emerging markets

Case study topics

Mai

nstre

am tr

avel

Covered in UK case study

Page 100

Medium term margin growth potential

+ + +

Total 100-150 bps

+ + + + +

= = = = =

110-130 bps 130-150 bps 10-20 bps N/A ~(150) bps

Mainstream travel

Independent travel

Financial services M&A Margin pressure

Cost efficiencies European OTA growth Forex growth Market

developmentNew acquisitions

Distribution gains Improved cross-

sell ratesWholesale growth

ASP and trading margin growth

New product launches Execution riskScheduled

package growthDisposals of

non-core assets

Note: Basis points improvement applies to total Group medium term revenue

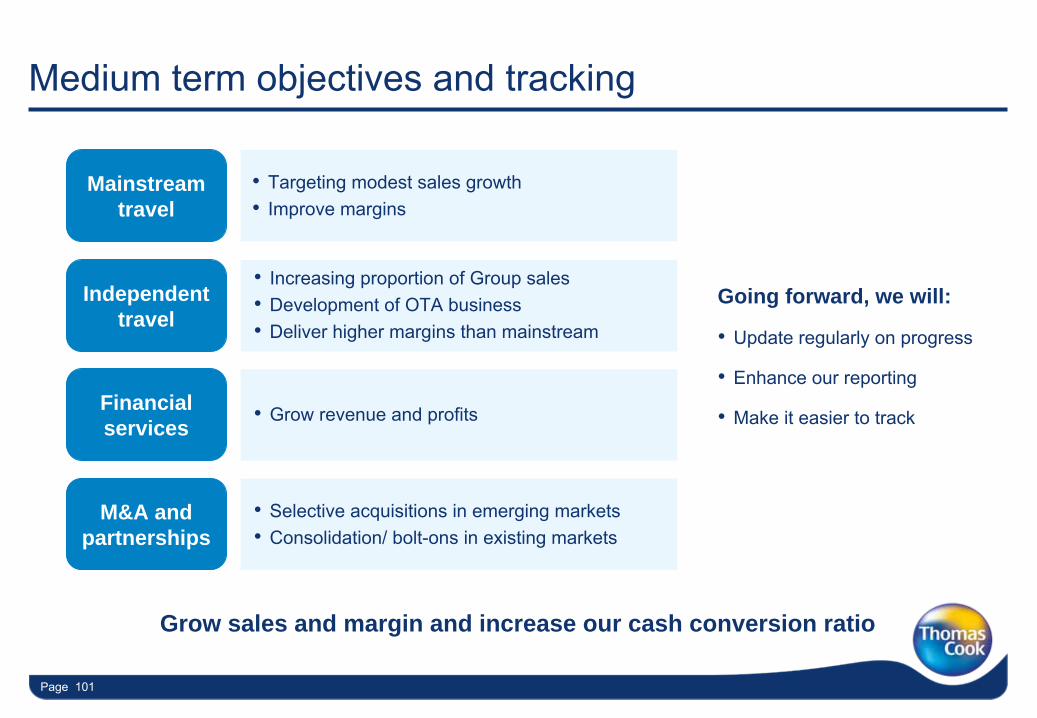

Page 101

•

Increasing proportion of Group sales•

Development of OTA business

•

Deliver higher margins than mainstream

Mainstream travel

M&A and partnerships

Independent travel

Financial services

•

Targeting modest sales growth•

Improve margins

•

Selective acquisitions in emerging markets•

Consolidation/ bolt-ons

in existing markets

•

Grow revenue and profits

Going forward, we will:

•

Update regularly on progress

•

Enhance our reporting

•

Make it easier to track

Grow sales and margin and increase our cash conversion ratio

Medium term objectives and tracking

Page 102Page 102

M&A continues to be part of our strategy

•

Capture growth and value

–

Maximise value in current business

–

New initiatives in existing markets

–

Entry in other emerging markets

Page 103Page 103

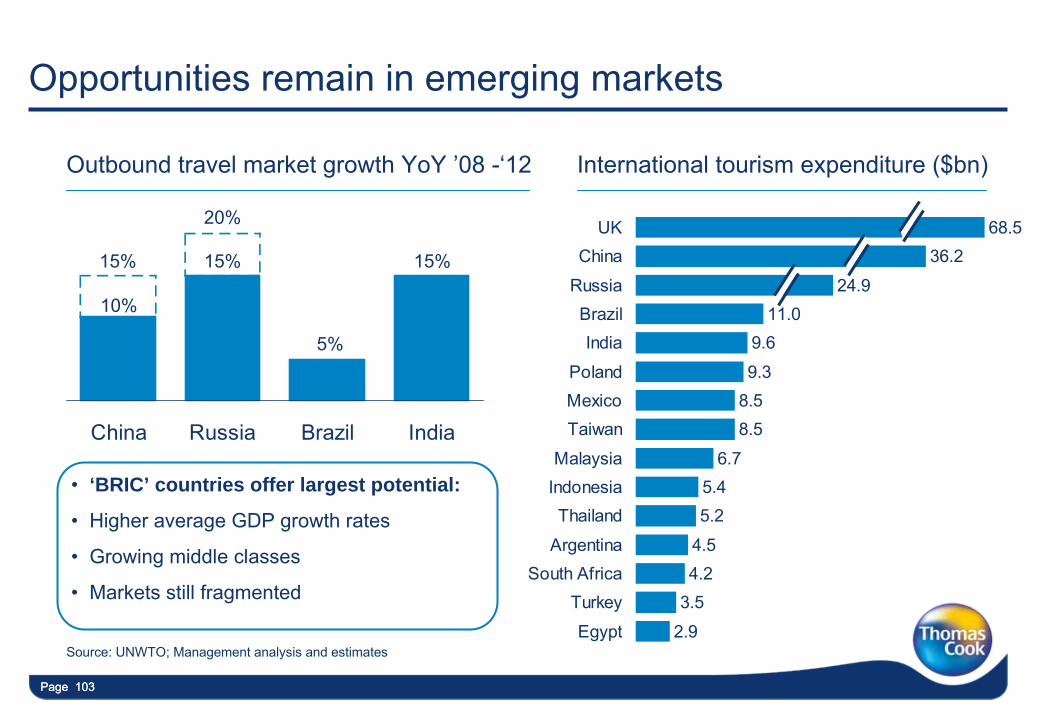

China Russia Brazil India

Opportunities remain in emerging markets

Outbound travel market growth YoY

’08 -‘12 International tourism expenditure ($bn)

2.9

3.54.24.5

5.25.4

6.7

8.58.59.3

9.611.0

68.536.2

24.9

Egypt

TurkeySouth Africa

Argentina

ThailandIndonesiaMalaysia

TaiwanMexicoPoland

IndiaBrazil

Russia

ChinaUK

10%

15% 15%

20%

5%

15%

•

‘BRIC’ countries offer largest potential:

•

Higher average GDP growth rates

•

Growing middle classes

•

Markets still fragmented

Source: UNWTO; Management analysis and estimates

Page 104Page 104

Russia opportunity

•

Fastest growing BRIC travel market

•

20m passengers p.a. (international and domestic)

•

Only 5% of population travels abroad for leisure

•

Similar product to W. European mainstream

–

Beach, especially Turkey and Egypt

Sources: Russian Federal Tourism Agency, expert estimates

Market overview

•

Leading Tour Operator with strong distribution

–

Multi-destination Tour Operator

–

Retail focus on Moscow and key regions

–

Leveraging core destinations

•

Leverage existing expertise

–

Brand

–

Bed banks

–

Strong positions in key destinations

Our vision in Russia

Source: UNWTO; Management analysis and estimates

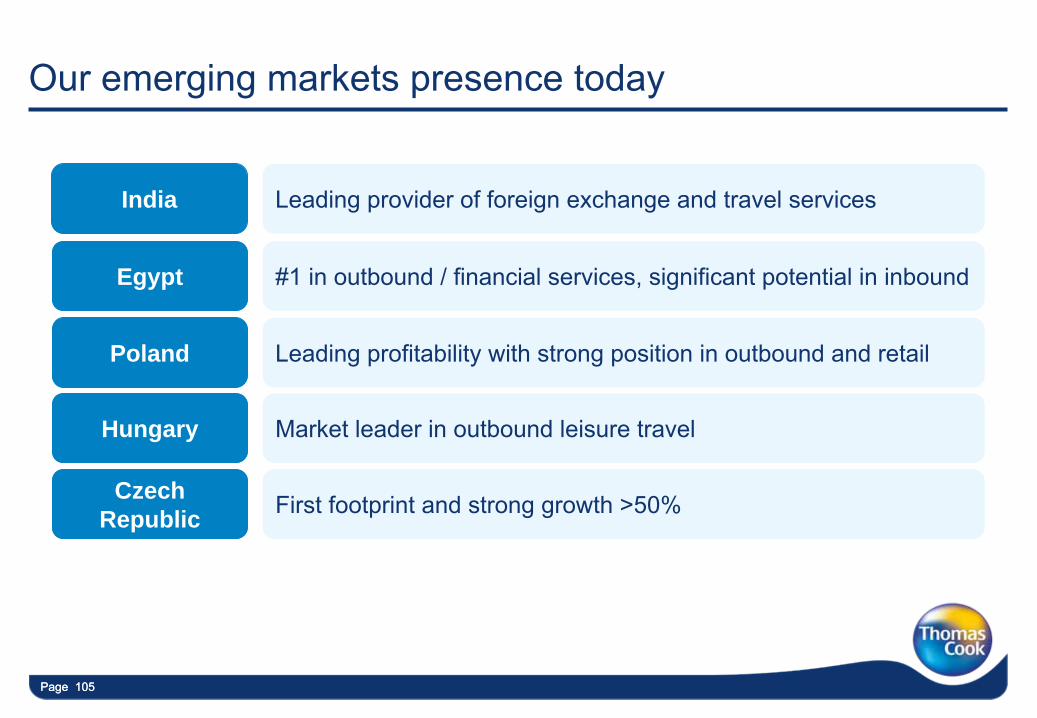

Page 105Page 105

Leading provider of foreign exchange and travel services

#1 in outbound / financial services, significant potential in inbound

Leading profitability with strong position in outbound and retail

Market leader in outbound leisure travel

First footprint and strong growth >50%

Our emerging markets presence today

India

Egypt

Poland

Hungary

Czech Republic

Page 106Page 106

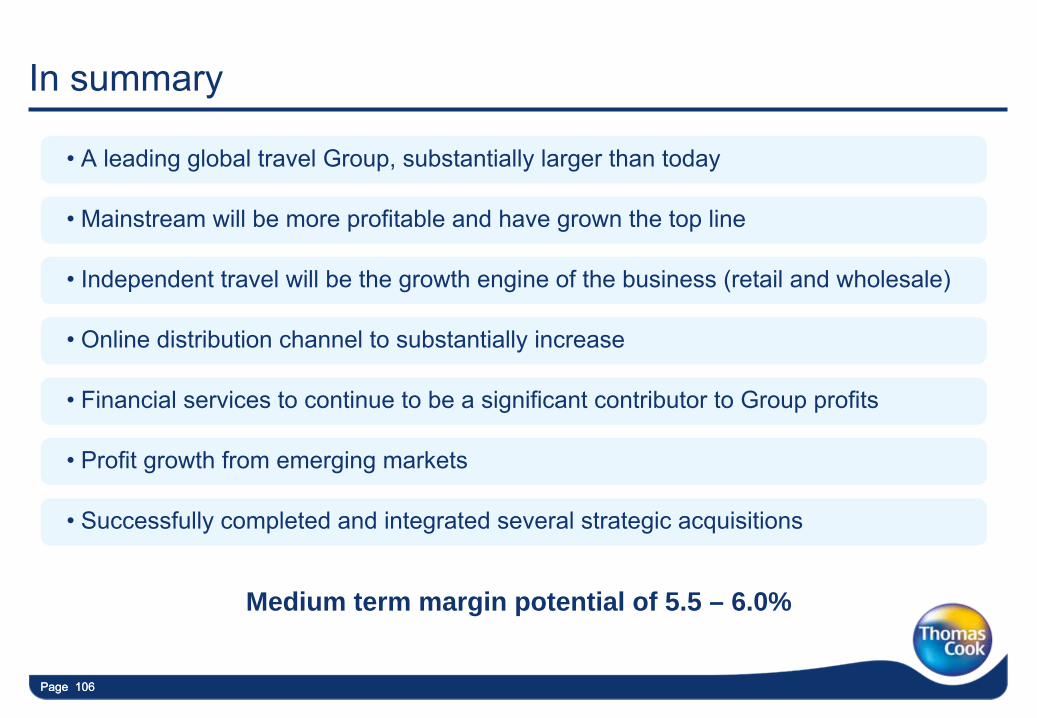

In summary

•

A leading global travel Group, substantially larger than today

•

Mainstream will be more profitable and have grown the top line

•

Independent travel will be the growth engine of the business (retail and wholesale)

•

Online distribution channel to substantially increase

•

Financial services to continue to be a significant contributor to Group profits

•

Profit growth from emerging markets

•

Successfully completed and integrated several strategic acquisitions

Medium term margin potential of 5.5 – 6.0%

Page 107

Refreshments

Page 108Page 108

Agenda

Welcome and Introduction Manny Fontenla-Novoa 0900 –

0920

Strategic Progress Case Studies Management Team 0920 –

1000

Strategy for Growth Paul Hollingworth, Jürgen Büser 1000 –

1045

Refreshments

Growth Strategy Case Studies Management Team 1115 –

1225

Summary and Wrap-up Manny Fontenla-Novoa 1225 –

1230

Q&A Management Team 1230 –

1300

Lunch

Growth strategy case studies

Page 110Page 110

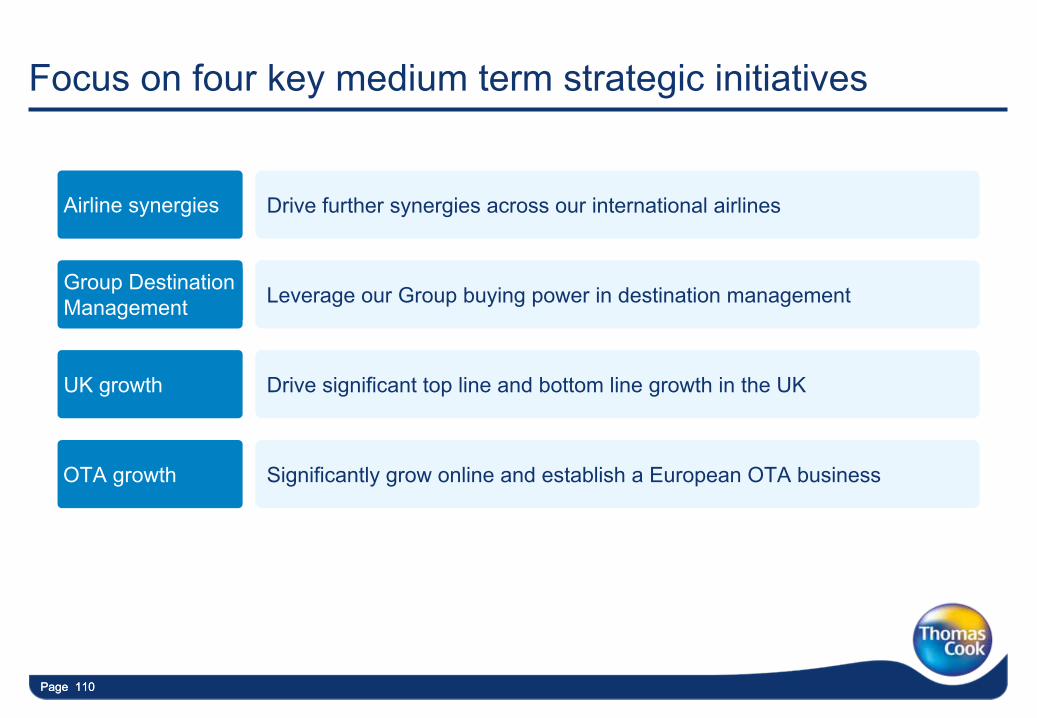

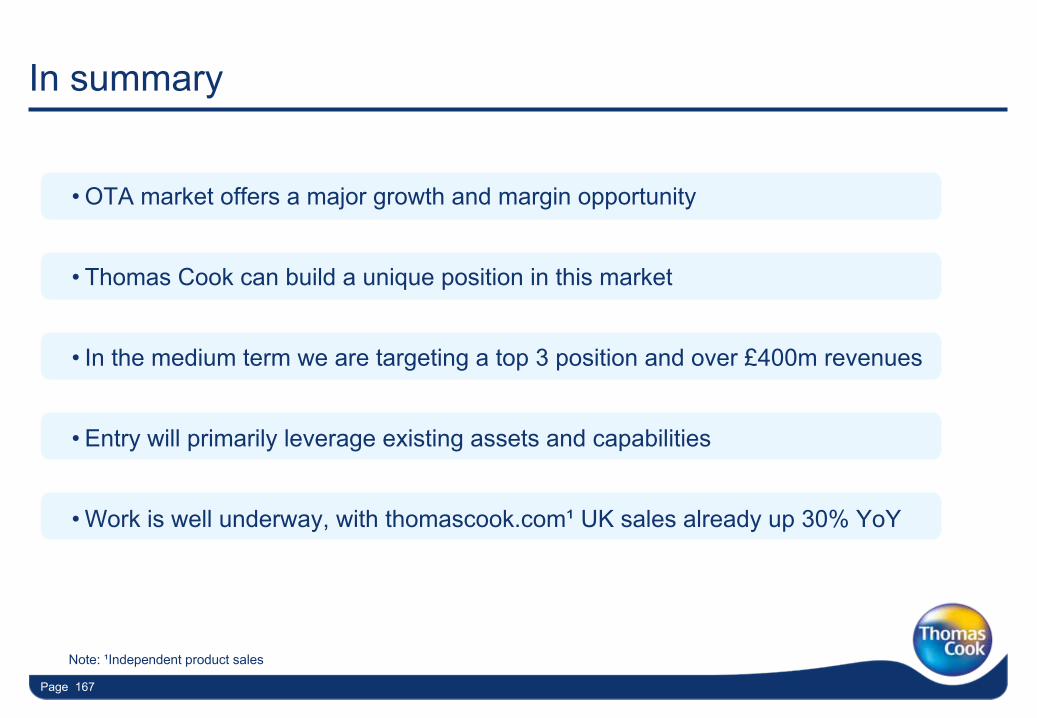

Significantly grow online and establish a European OTA businessOTA growth

Focus on four key medium term strategic initiatives

Drive significant top line and bottom line growth in the UKUK growth

Drive further synergies across our international airlinesAirline synergies

Leverage our Group buying power in destination managementGroup Destination Management

Page 111

Drive further synergies across our international airlines

Ralf Teckentrup –

CEO Airlines Germany

Page 112

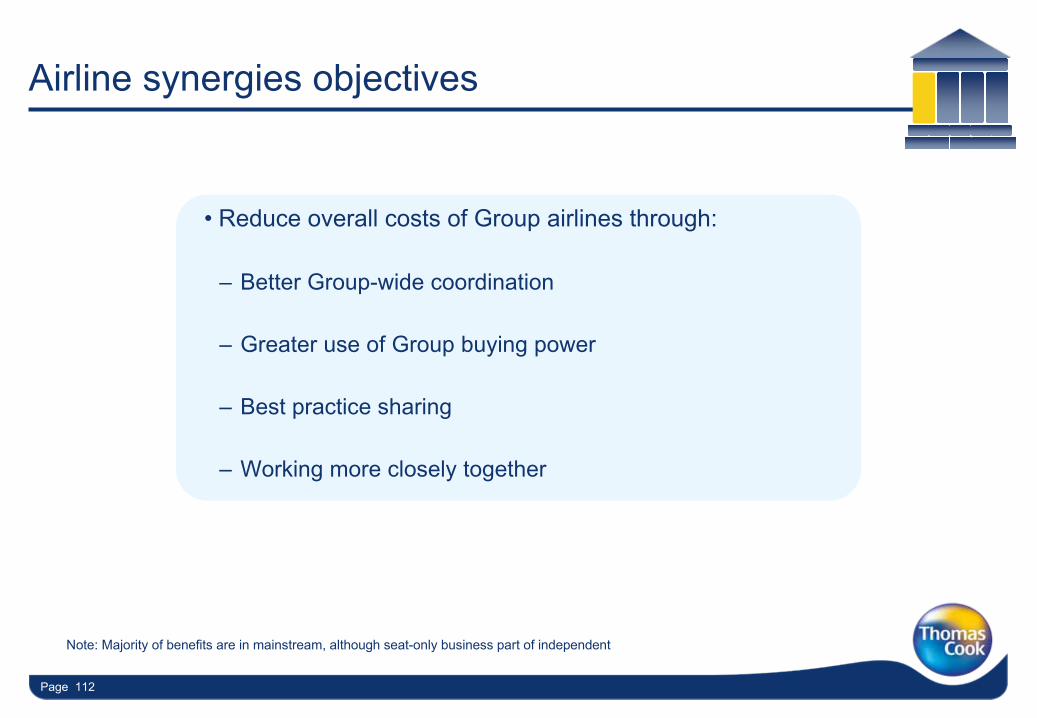

Airline synergies objectives

Note: Majority of benefits are in mainstream, although seat-only business part of independent

•

Reduce overall costs of Group airlines through:

– Better Group-wide coordination

– Greater use of Group buying power

– Best practice sharing

– Working more closely together

Page 113Page 113

Thomas Cook Group today operates 94 aircraft

No. of aircraft (summer season)

Northern Europe

UK & IrelandGermany

Belgium

Canada6-8 1-2

Seasonal optimisation of aircraft

•

94 aircraft

•

>17m passengers

•

>6,200 employees

•

Cost base of £2.3b11

3443

6

x

Page 114Page 114

•

UK merger of Thomas Cook and MyTravel airlines in 2007/2008

•

Condor merger talks with Air Berlin in FY08; TUIfly/ Germanwings

in H2’08

•

Regular efficiency and cost cutting programmes, but priority within each airline

•

High-level contact across Group airlines, however limited coordination

•

Transfer of aircraft between UK, Canada & Scandinavia (seasonal optimisation)

•

Synergies realised case-by-case in an opportunistic way

Historically limited cross-Group airline cooperation

Within individual

Thomas Cook

airlines

Cross-Group cooperation/

synergies

Management focus up until 2008

Opportunity to benefit from greater cooperation between airlines

Page 115Page 115

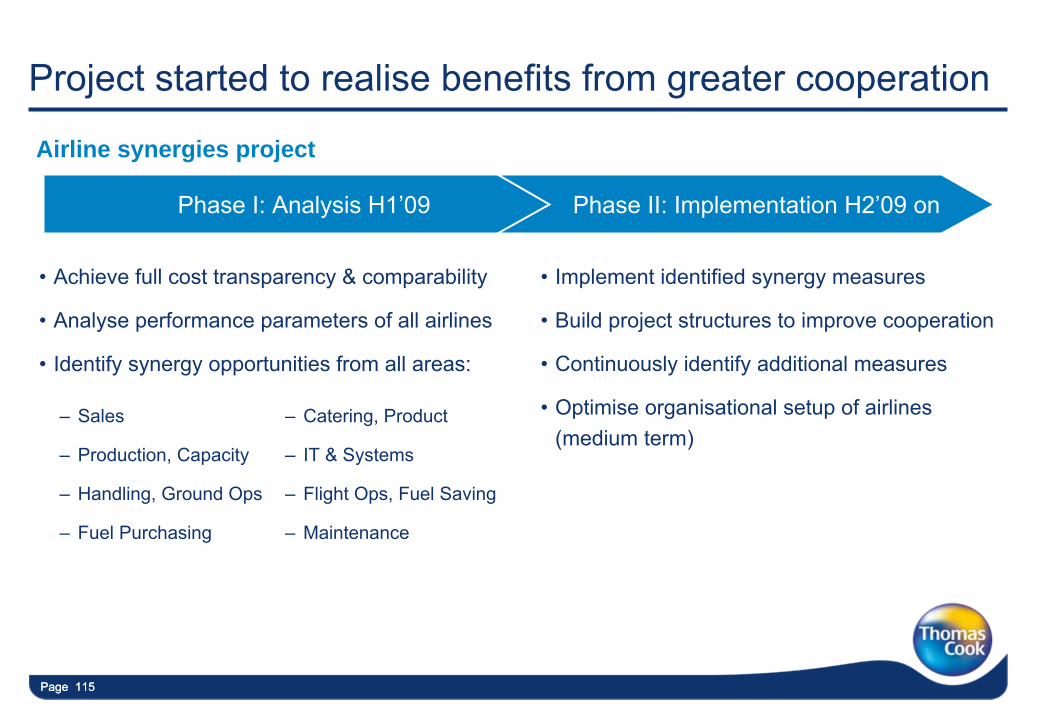

Project started to realise benefits from greater cooperation

•

Implement identified synergy measures

•

Build project structures to improve cooperation

•

Continuously identify additional measures

•

Optimise organisational setup of airlines (medium term)

•

Achieve full cost transparency & comparability

•

Analyse performance parameters of all airlines

•

Identify synergy opportunities from all areas:

–

Sales

–

Production, Capacity

–

Handling, Ground Ops

–

Fuel Purchasing

–

Catering, Product

–

IT & Systems

–

Flight Ops, Fuel Saving

–

Maintenance

Phase I: Analysis H1’09 Phase II: Implementation H2’09 on

Airline synergies project

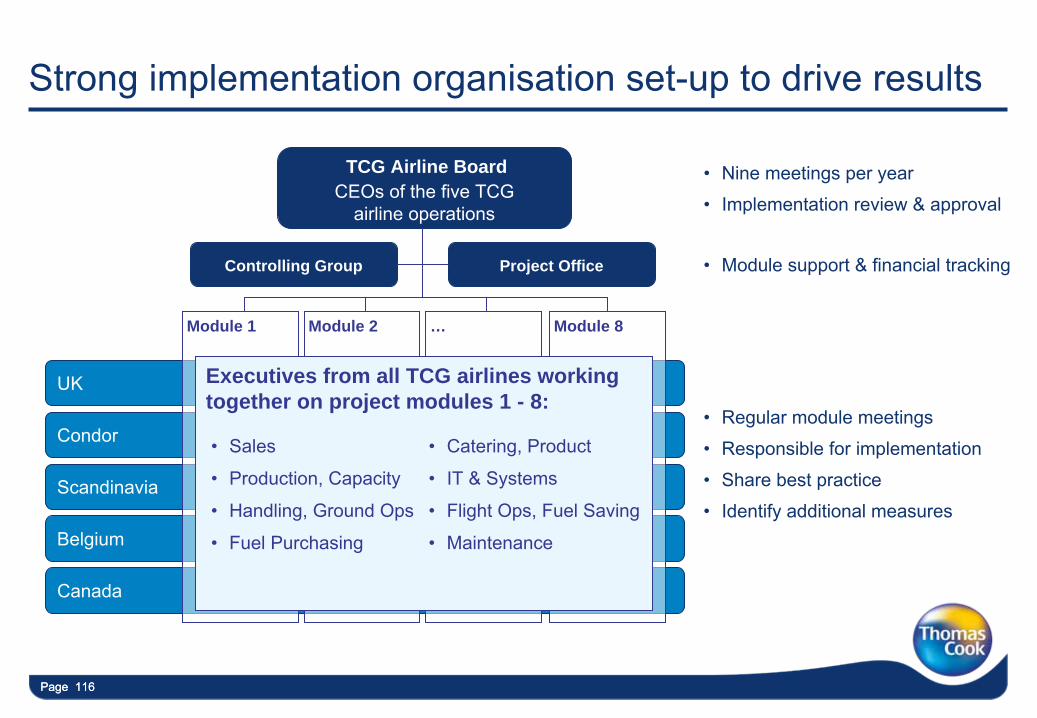

Page 116Page 116

UK

Condor

Scandinavia

Belgium

Canada

Project OfficeControlling Group

Module 1 Module 2 … Module 8

Executives from all TCG airlines working together on project modules 1 - 8:

TCG Airline Board

•

Sales

•

Production, Capacity

•

Handling, Ground Ops

•

Fuel Purchasing

•

Catering, Product

•

IT & Systems

•

Flight Ops, Fuel Saving

•

Maintenance

•

Nine meetings per year

•

Implementation review & approval

•

Module support & financial tracking

•

Regular module meetings

•

Responsible for implementation

•

Share best practice

•

Identify additional measures

CEOs

of the five TCG airline operations

Strong implementation organisation set-up to drive results

Page 117Page 117

UK 15 43%

Condor 16 45%

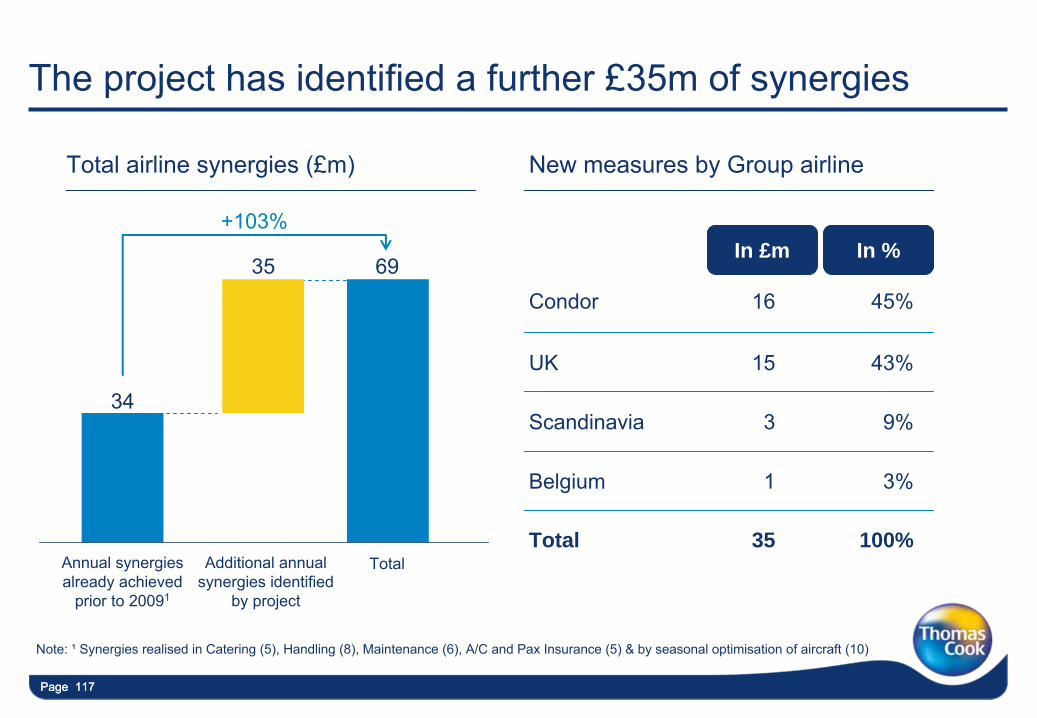

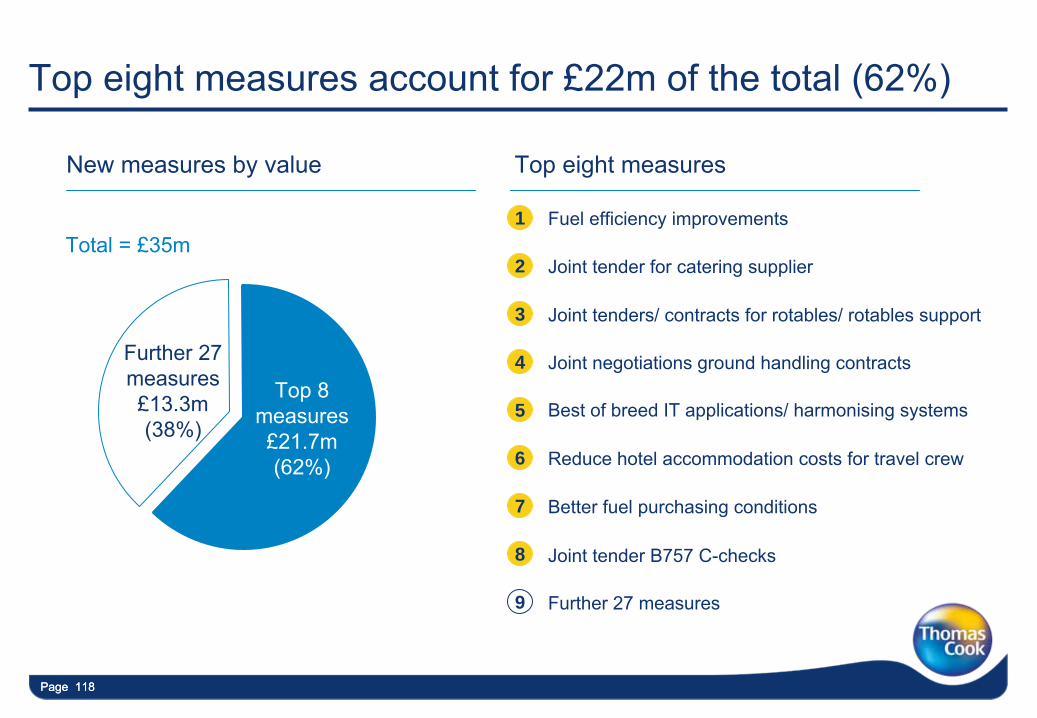

The project has identified a further £35m of synergies

34

Annual synergies already achieved

prior to 20091

35

Additional annual synergies identified

by project

69

Total

+103%

Note: ¹

Synergies realised in Catering (5), Handling (8), Maintenance (6), A/C and Pax

Insurance (5) & by seasonal optimisation of aircraft (10)

Scandinavia

Belgium

3

1

35

9%

3%

Total airline synergies (£m) New measures by Group airline

Total

In £m

100%

In %

Page 118Page 118

New measures by value

Top eight measures account for £22m of the total (62%)

Top 8measures£21.7m(62%)

Further 27measures£13.3m(38%)

Total = £35mFuel efficiency improvements

Joint tender for catering supplier

Reduce hotel accommodation costs for travel crew

Joint tenders/ contracts for rotables/ rotables

support

Joint tender B757 C-checks

Better fuel purchasing conditions

Best of breed IT applications/ harmonising systems

Joint negotiations ground handling contracts

Further 27 measures

1

2

3

4

5

6

7

8

9

Top eight measures

Page 119Page 119

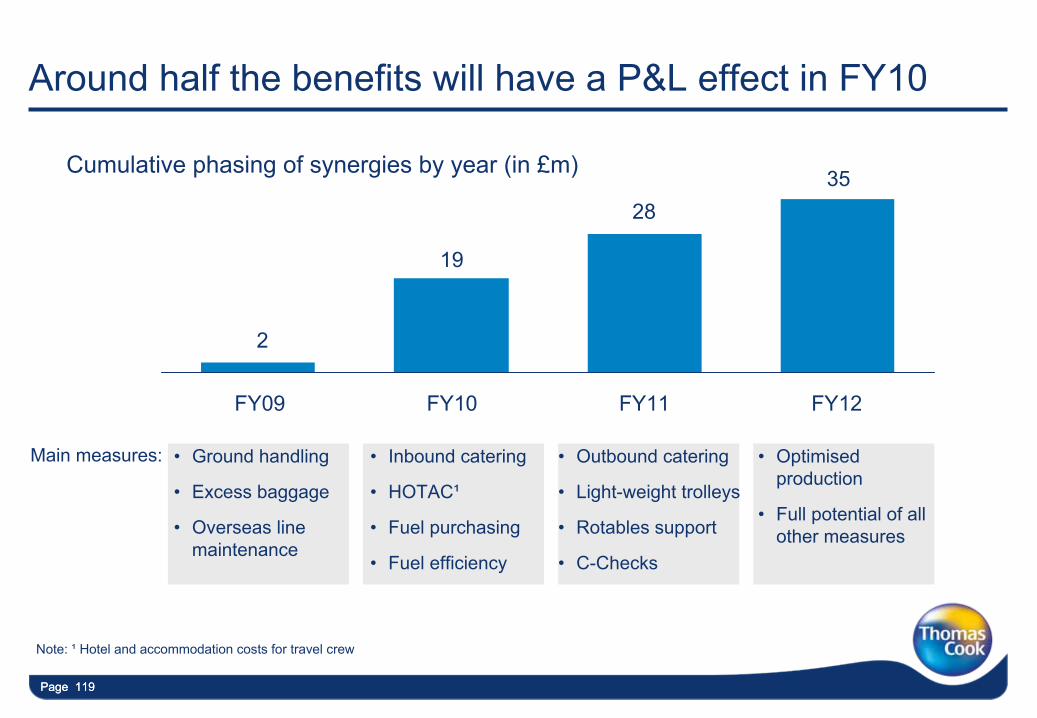

Around half the benefits will have a P&L effect in FY10

2

FY09

19

FY10

28

FY11

35

FY12

•

Inbound catering

•

HOTAC¹

•

Fuel purchasing

•

Fuel efficiency

•

Outbound catering

•

Light-weight trolleys

•

Rotables

support

•

C-Checks

•

Optimised production

•

Full potential of all other measures

•

Ground handling

•

Excess baggage

•

Overseas line maintenance

Main measures:

Cumulative phasing of synergies by year (in £m)

Note: ¹

Hotel and accommodation costs for travel crew

Page 120Page 120

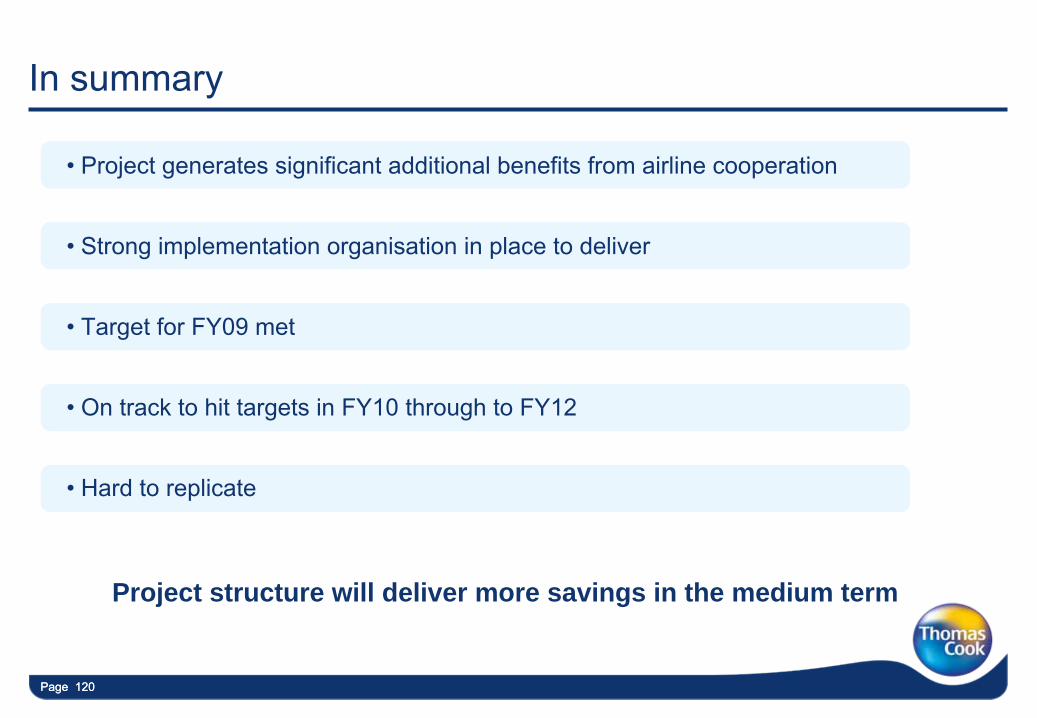

In summary

•

Project generates significant additional benefits from airline cooperation

•

Strong implementation organisation in place to deliver

•

Target for FY09 met

•

On track to hit targets in FY10 through to FY12

•

Hard to replicate

Project structure will deliver more savings in the medium term

Page 121

Leverage our Group buying power in destination management

Pete Constanti –

CEO Group Destination

Management

Page 122

Group destination management objectives

•

Unlock value through greater Group coordination

•

Reduce accommodation costs

•

Reduce other destination-related overheads

•

Protect and enhance product portfolio

Page 123

Introduction to destination management

Historically destination management performed by local markets

Source market

passengers

Content / data•

Photos & descriptions•

Local area info.•

Hotel allotments & rates•

Other information

Content / data•

Photos & descriptions•

Local area info.•

Hotel allotments & rates•

Other information

DestinationIncoming agents•

Owned or third party agents•

Handling, transfers etc.Customer Service•

Customer facing teams/ reps•

Management of teamsAccommodation•

Hotel rooms and bed rates•

Overseas purchasing

DestinationIncoming agents•

Owned or third party agents•

Handling, transfers etc.Customer Service•

Customer facing teams/ reps•

Management of teamsAccommodation•

Hotel rooms and bed rates•

Overseas purchasing

Page 124Page 124

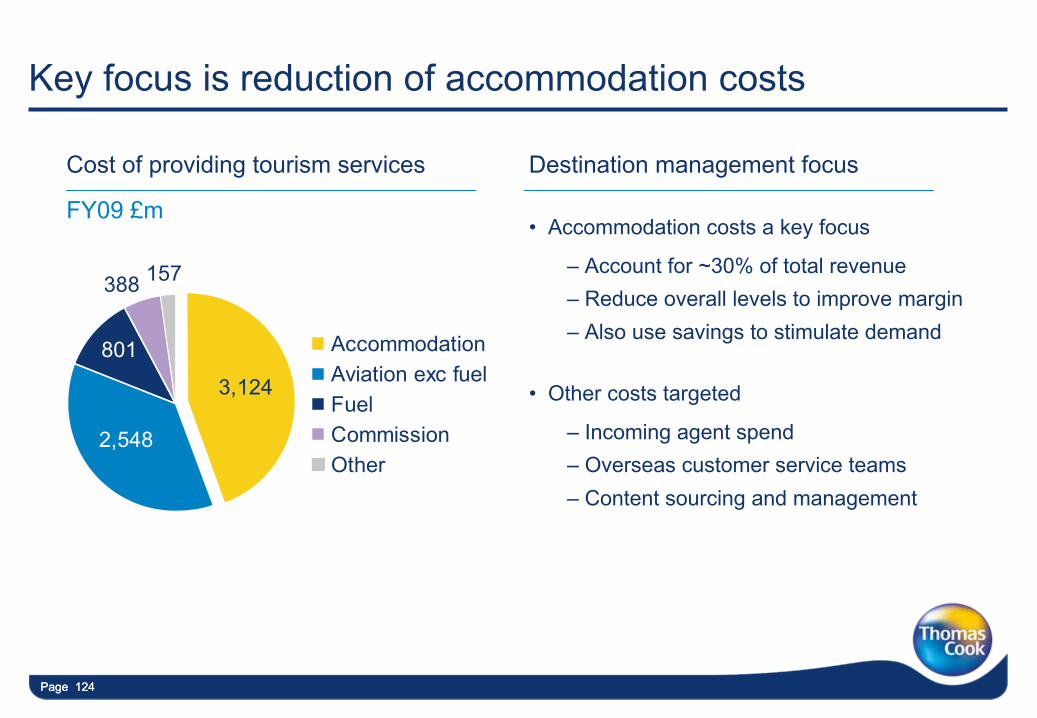

Key focus is reduction of accommodation costs

2,548

801

3,124

388 157

AccommodationAviation exc fuelFuelCommissionOther

FY09 £m

Cost of providing tourism services Destination management focus

•

Accommodation costs a key focus

–

Account for ~30% of total revenue–

Reduce overall levels to improve margin–

Also use savings to stimulate demand

•

Other costs targeted

–

Incoming agent spend–

Overseas customer service teams–

Content sourcing and management

Page 125

Also opportunities to support top line growth

Higher average prices

•

More exclusivity agreements and access to higher margin product

•

Defence of strategic destinations and key hotels

•

Group approach to extending breadth of product range

Increased in-destination

revenue

•

Best practice sharing on in-destination revenue generation

•

Increased sales of tours, tickets, excursions, etc.

Better conversion

rates

•

Better quality content in the right place at the right time

•

Improved conversion rates from enhanced content management

Page 126

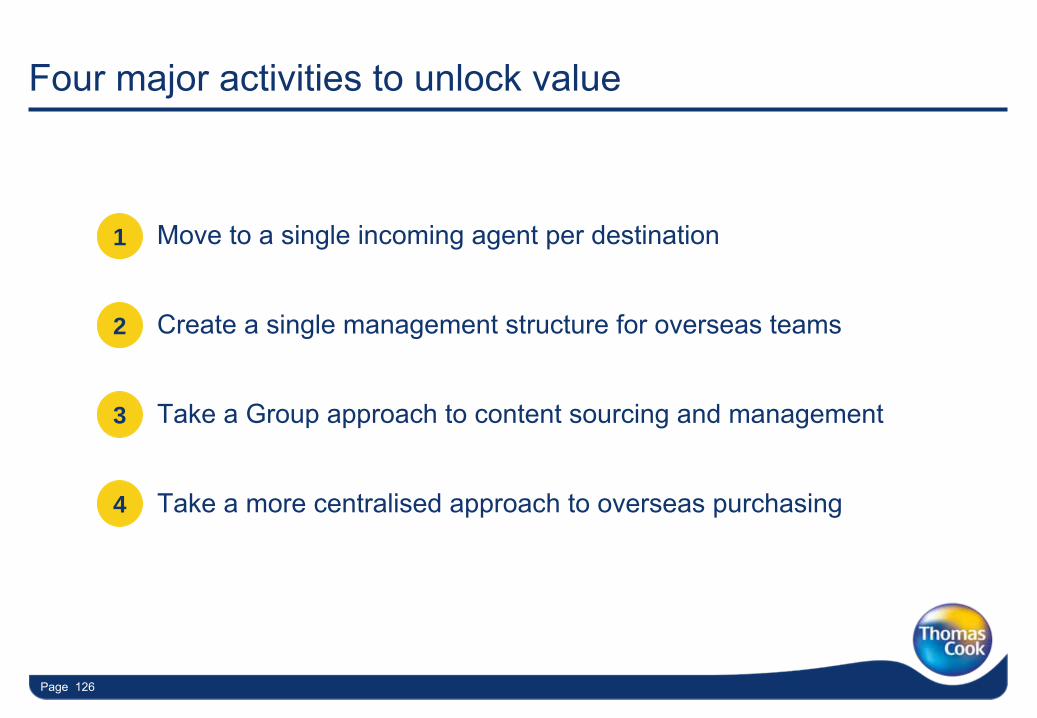

Four major activities to unlock value

•

Move to a single incoming agent per destination

•

Create a single management structure for overseas teams

•

Take a Group approach to content sourcing and management

•

Take a more centralised approach to overseas purchasing

1

2

3

4

Page 127

A new approach to activities in-destination

Targeting savings of approximately £10m p.a.

Incoming agents

•

Move to a single handling agent in each major gateway/ destination

•

Manage centrally to get best rates and protect & enhance product

range

1

Overseas customer service & sales

•

Create a single management structure for overseas teams

•

Strengthen service proposition and share best practices

2

Content and data

management

•

Develop a Group-wide approach to content sourcing and management

•

Remove duplication of activities and improve overall content quality

3

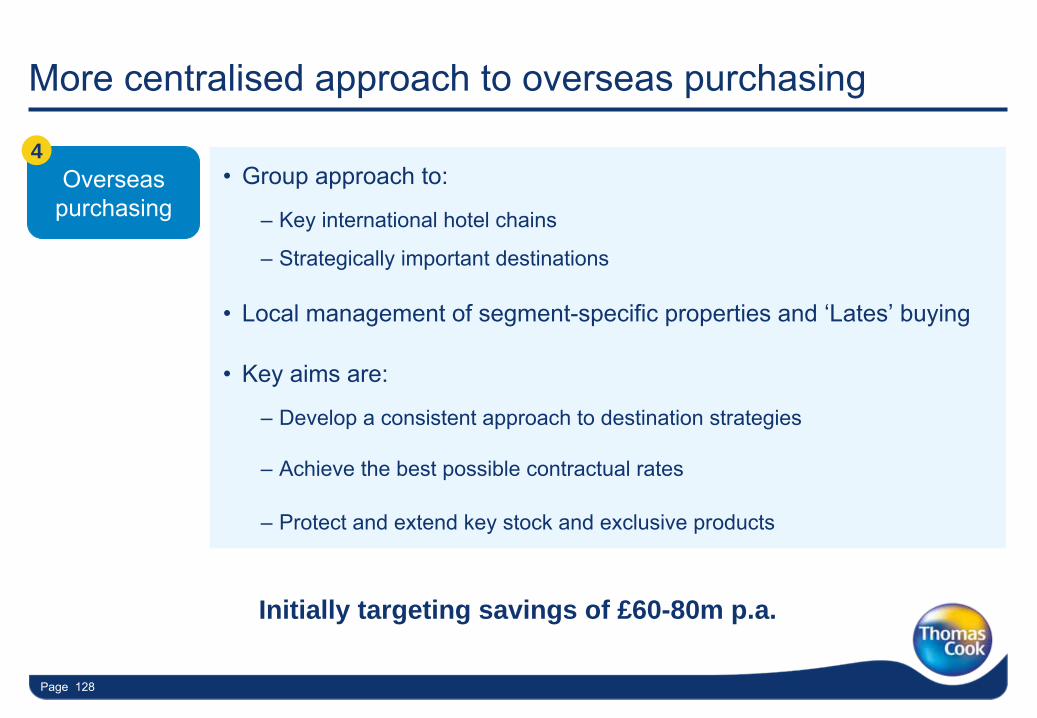

Page 128

•

Group approach to:

–

Key international hotel chains

–

Strategically important destinations

•

Local management of segment-specific properties and ‘Lates’

buying

•

Key aims are:

–

Develop a consistent approach to destination strategies

–

Achieve the best possible contractual rates

–

Protect and extend key stock and exclusive products

Overseas purchasing

4

More centralised approach to overseas purchasing

Initially targeting savings of £60-80m p.a.

Page 129Page 129

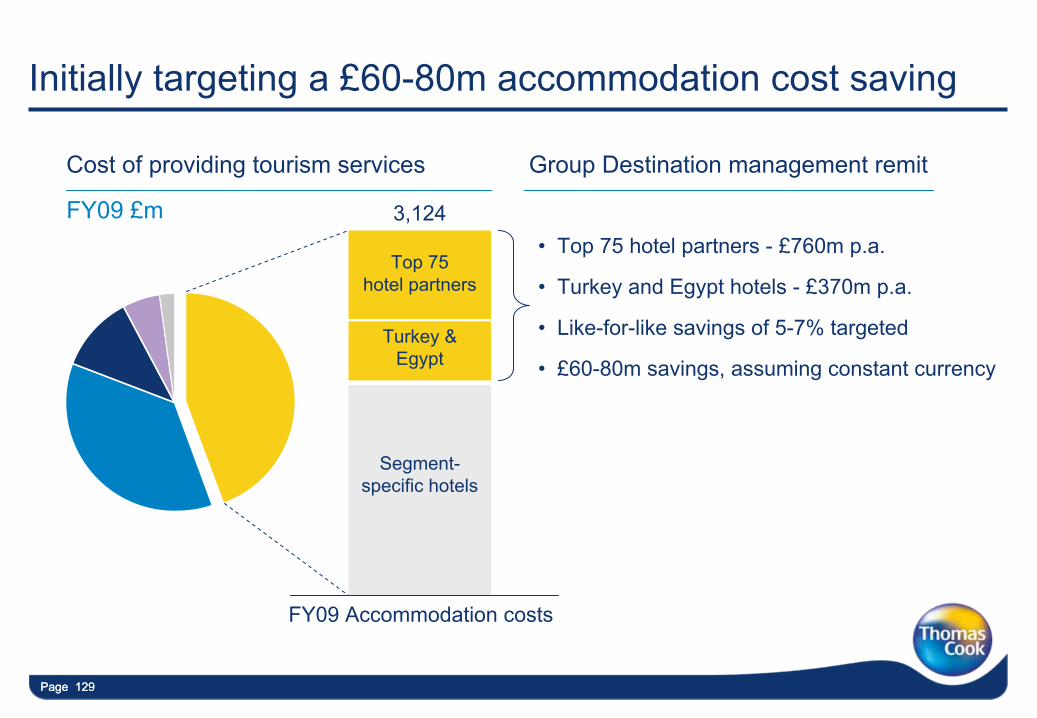

Initially targeting a £60-80m accommodation cost saving

Turkey & Egypt

Top 75

hotel partners

Segment-

specific hotels

3,124

FY09 Accommodation costs

•

Top 75 hotel partners -

£760m p.a.

•

Turkey and Egypt hotels -

£370m p.a.

•

Like-for-like savings of 5-7% targeted

•

£60-80m savings, assuming constant currency

FY09 £m

Cost of providing tourism services Group Destination management remit

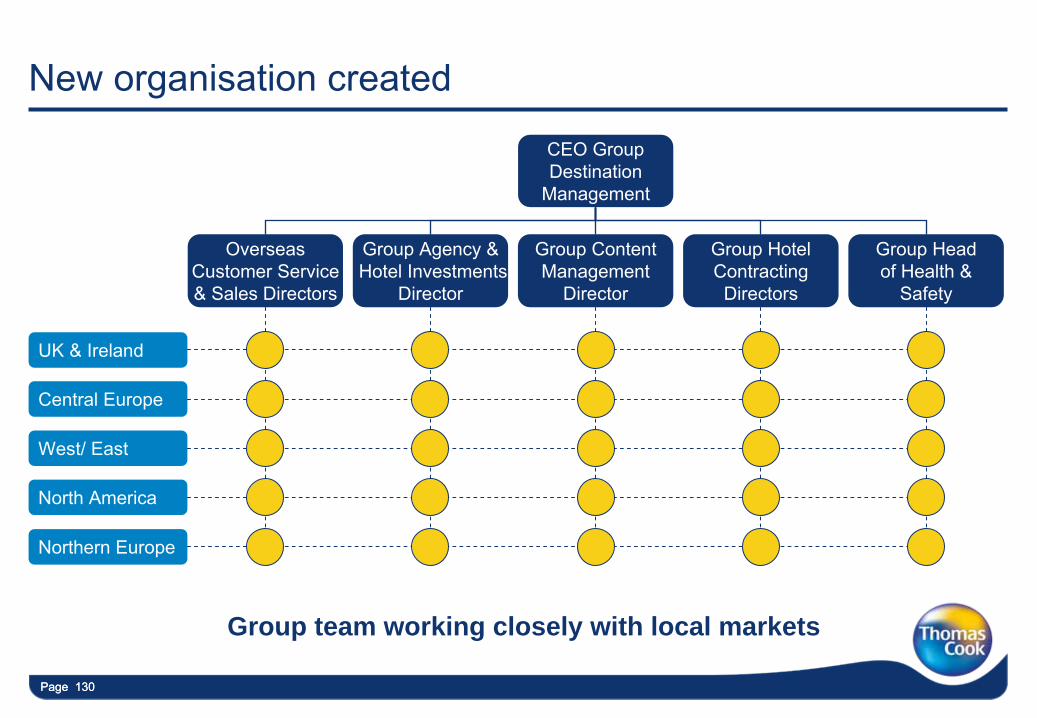

Page 130

Northern Europe

North America

UK & Ireland

Central Europe

West/ East

Page 130

New organisation created

Group team working closely with local markets

CEO Group

Destination

Management

Overseas

Customer Service

& Sales Directors

Group Agency &

Hotel Investments

Director

Group Content

Management

Director

Group Hotel Contracting

Directors

Group Head

of Health &

Safety

Page 131

In summary

•

A significant change to the way we do business

•

Group hotel purchasing organisation for biggest hotel chains and

strategic destinations

•

Customer service organisation under a single management structure

•

Single agent per gateway in major destinations

•

Single content management system and process

•

Group destination management working closely with the segments

Leveraging our position through a world class approach

Page 132

Drive significant top line and bottom line growth in the UK & Ireland

Ian Derbyshire –

CEO UK & Ireland

Page 133

UK & Ireland objectives

•

Significantly grow top line & target industry leading margins

•

Continue mainstream product focus & margin improvement

•

Significantly grow independent travel online and offline

•

Continue to build financial services business

Page 134Page 134

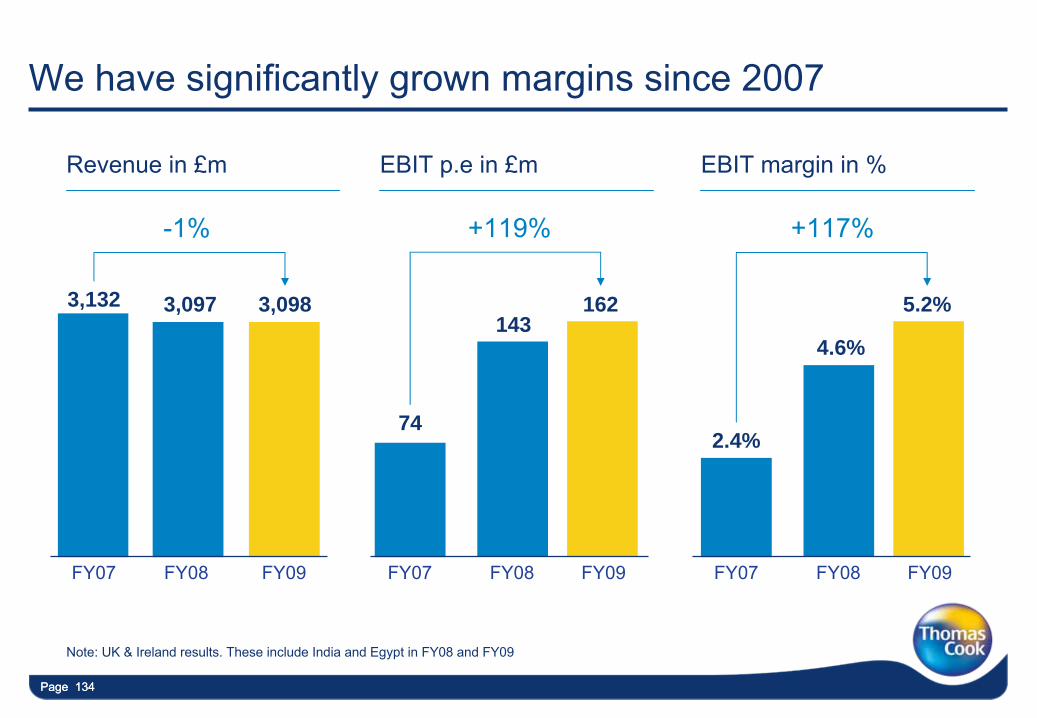

Note: UK & Ireland results. These include India and Egypt in FY08 and FY09

FY07 FY08

3,0973,132143

74

FY07 FY08

4.6%

2.4%

FY07 FY08FY09

3,098

FY09

5.2%

FY09

+119%-1% +117%

162

We have significantly grown margins since 2007

Revenue in £m EBIT p.e in £m EBIT margin in %

Page 135Page 135

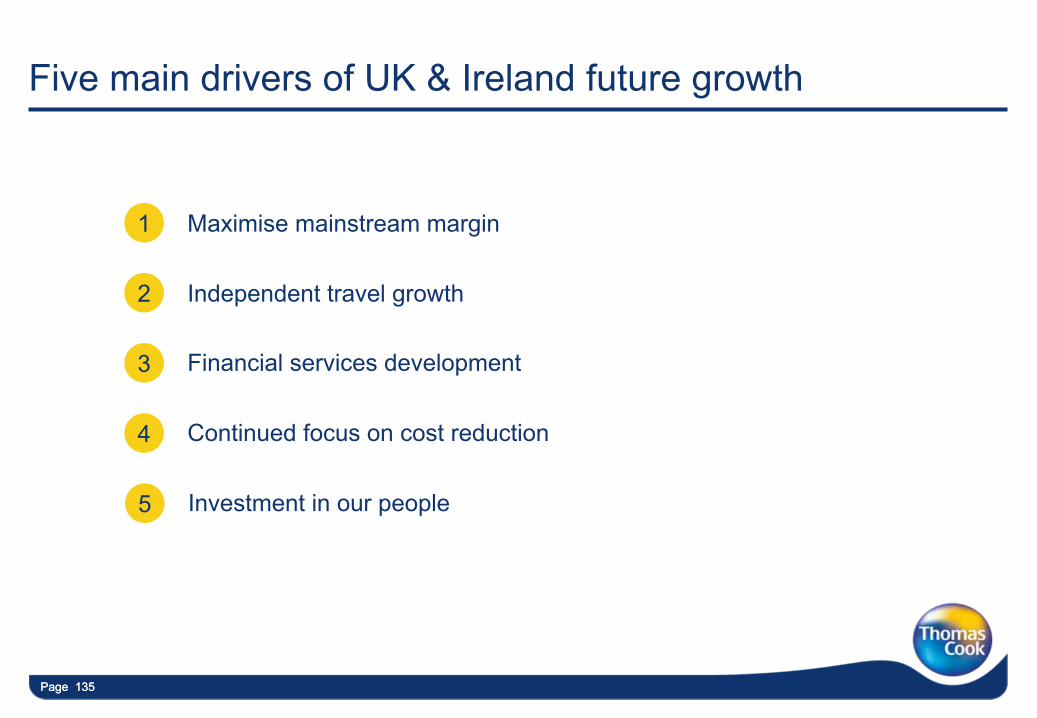

Maximise mainstream margin1

Independent travel growth2

Financial services development 3

Continued focus on cost reduction4

Five main drivers of UK & Ireland future growth

Investment in our people5

Page 136Page 136

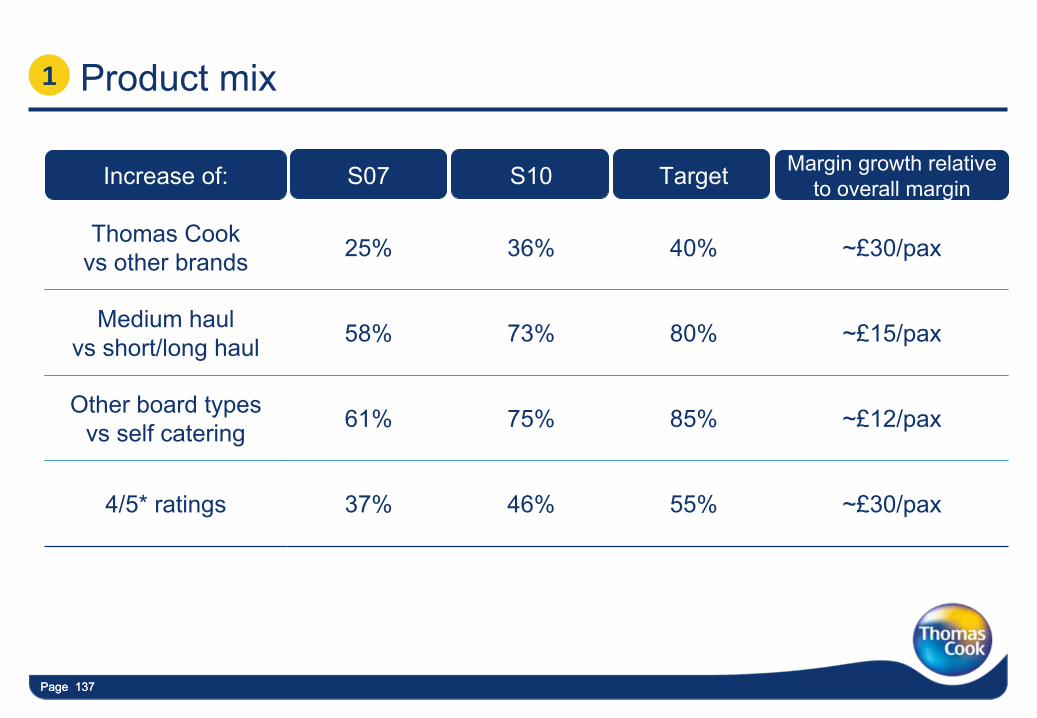

•

Continuing the strategy we started in 2007, improving product mix

•

Growth of differentiated and exclusive product

•

Protect and grow strategic destinations

•

Automated yield management

•

Leverage our vertically integrated model

Maximise mainstream margin1

Main drivers of mainstream margin growth

Page 137Page 137

Increase of: S07 S10 Target Margin growth relative

to overall margin

Thomas Cook vs

other brands 25% 36% 40% ~£30/pax

Medium haul vs

short/long haul 58% 73% 80% ~£15/pax

Other board types vs

self catering 61% 75% 85% ~£12/pax

4/5* ratings 37% 46% 55% ~£30/pax

Product mix1

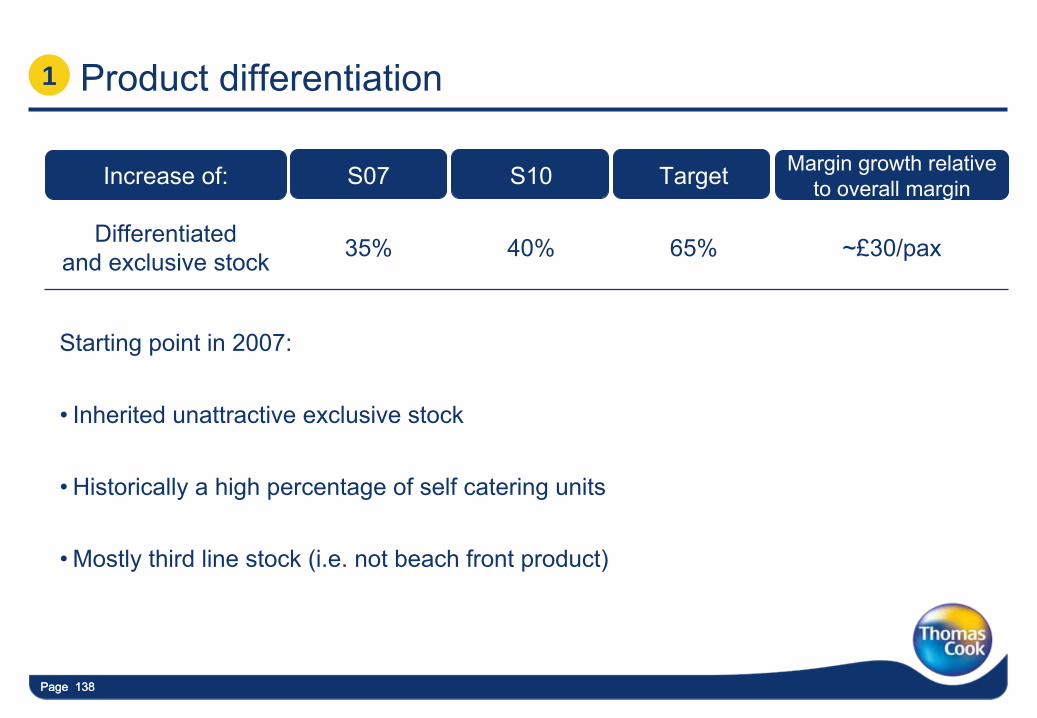

Page 138Page 138

Increase of: S07 S10 Target Margin growth relative

to overall margin

Differentiatedand exclusive stock 35% 40% 65% ~£30/pax

Product differentiation1

Starting point in 2007:

•

Inherited unattractive exclusive stock

•

Historically a high percentage of self catering units

•

Mostly third line stock (i.e. not beach front product)

Page 139Page 139

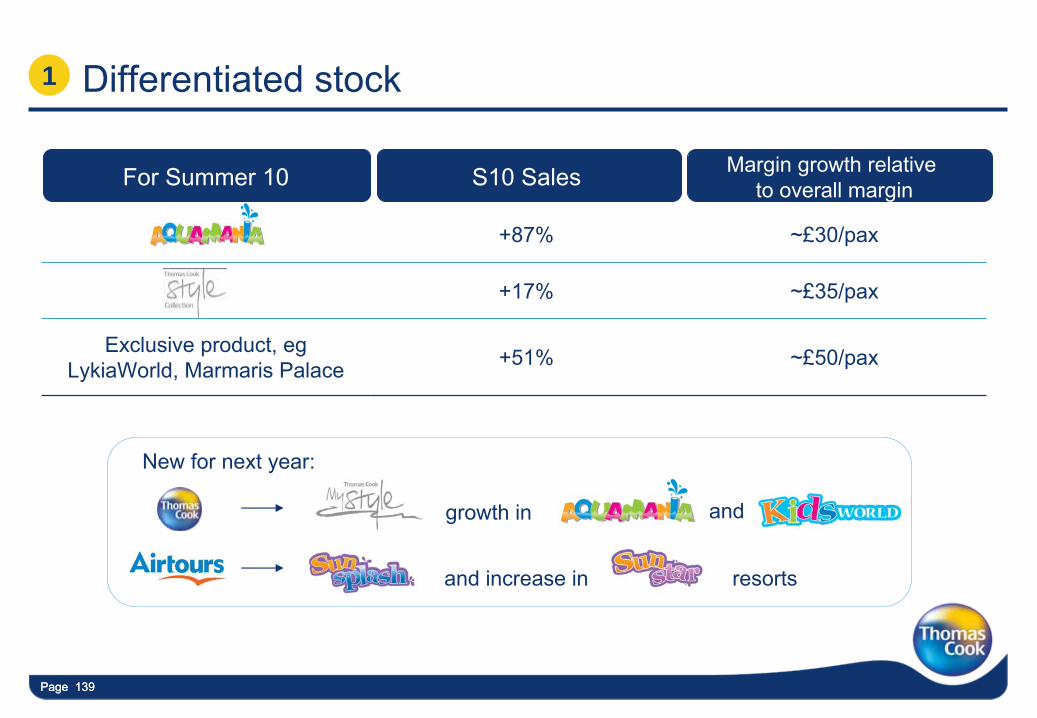

Differentiated stock

For Summer 10 S10 Sales Margin growth relative to overall margin

+87% ~£30/pax

+17% ~£35/pax

Exclusive product, egLykiaWorld, Marmaris

Palace +51% ~£50/pax

New for next year:

growth in

and increase in resorts

and

1

Page 140Page 140

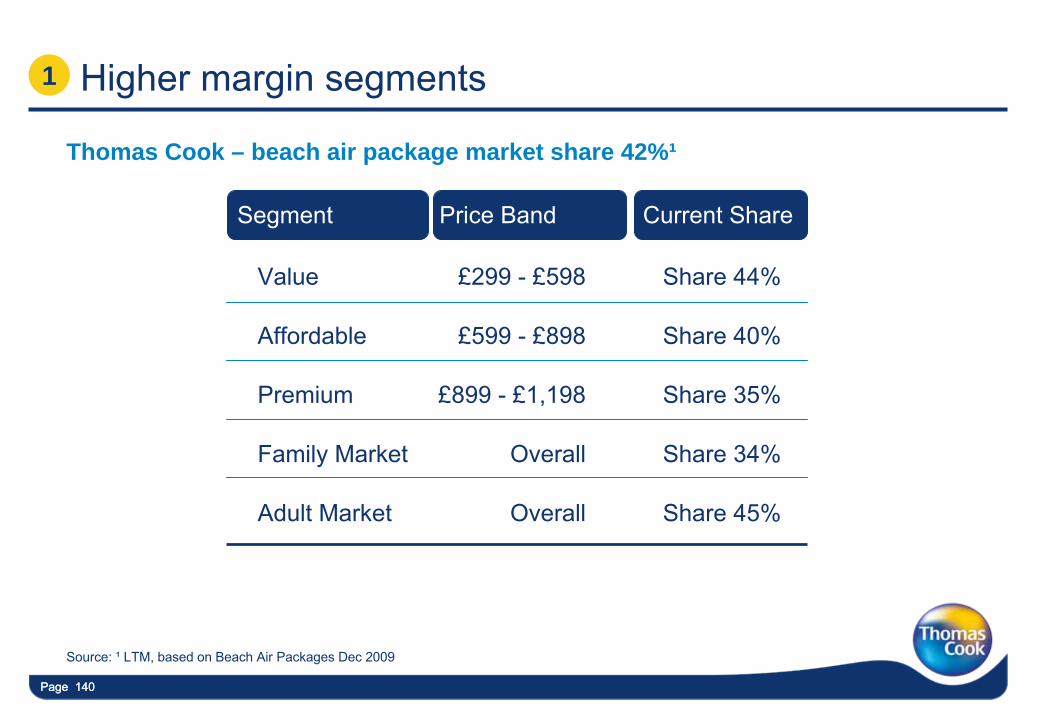

Higher margin segments

Thomas Cook – beach air package market share 42%¹

Value £299 -

£598

Affordable £599 -

£898

Premium £899 -

£1,198

Family Market Overall

Adult Market Overall

Source: ¹

LTM, based on Beach Air Packages Dec 2009

Share 44%

Share 40%

Share 35%

Share 34%

Share 45%

Segment Price Band Current Share

1

Page 141Page 141

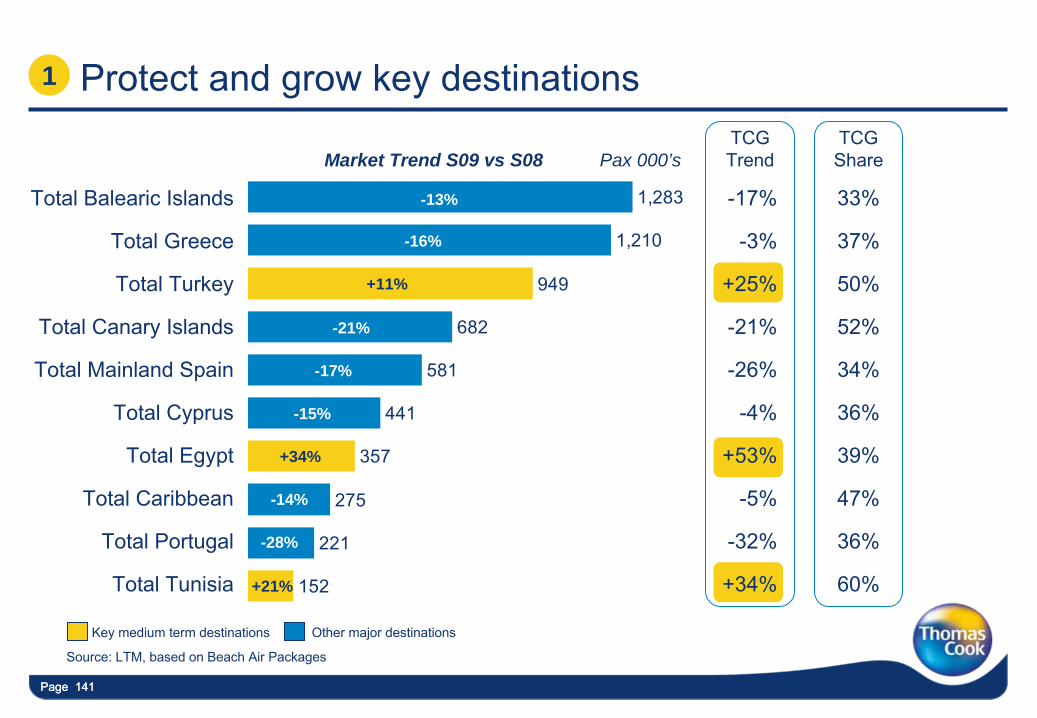

Protect and grow key destinations

152

221

275

357

441

581

682

949

1,210

1,283Total Balearic Islands

Total Greece

Total Turkey

Total Canary Islands

Total Mainland Spain

Total Cyprus

Total Egypt

Total Caribbean

Total Portugal

Total Tunisia

Source: LTM, based on Beach Air Packages

-17%

-3%

+25%

-21%

-26%

-4%

+53%

-5%

-32%

+34%

33%

37%

50%

52%

34%

36%

39%

47%

36%

60%

TCG Trend

TCG ShareMarket Trend S09 vs S08 Pax 000’s

-13%

-16%

+11%

-21%

-17%

-15%

+34%

-14%

-28%

+21%

1

Key medium term destinations Other major destinations

Page 142Page 142Page 142

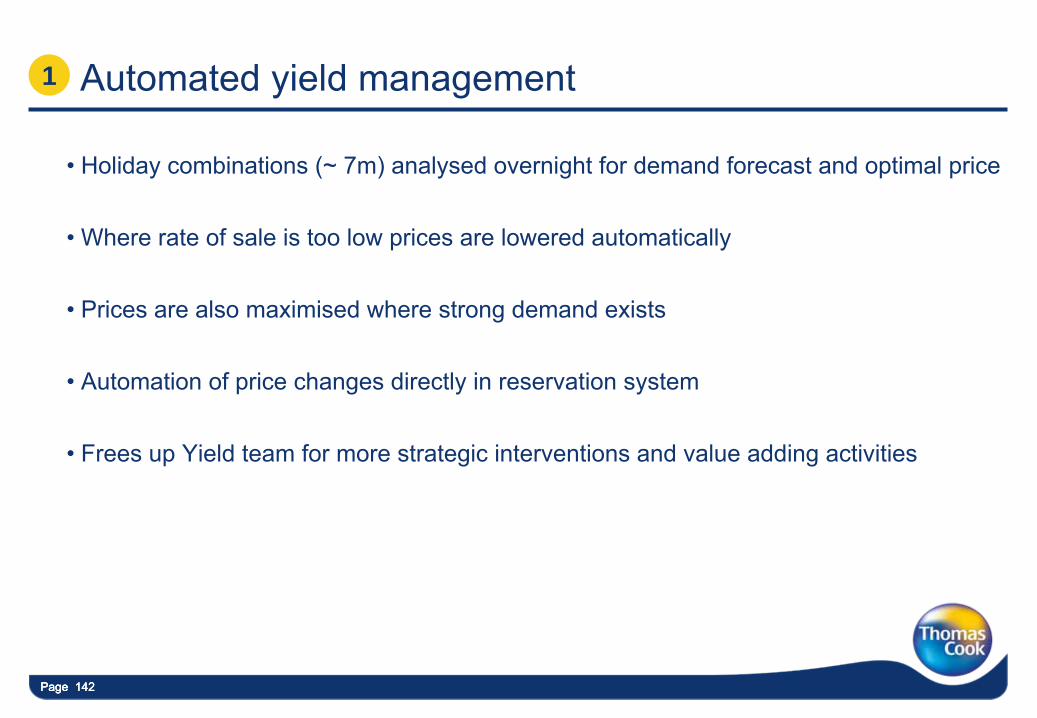

Automated yield management

•

Holiday combinations (~ 7m) analysed overnight for demand forecast and optimal price

•

Where rate of sale is too low prices are lowered automatically

•

Prices are also maximised where strong demand exists

•

Automation of price changes directly in reservation system

•

Frees up Yield team for more strategic interventions and value adding activities

1

Page 143Page 143

Board Basis S07 S10 Target

In-house distribution 65% 77% 85%

Retail productivity £38k / FTE £42k / FTE £50k / FTE

In-house flying ~75% ~90% 85-90%

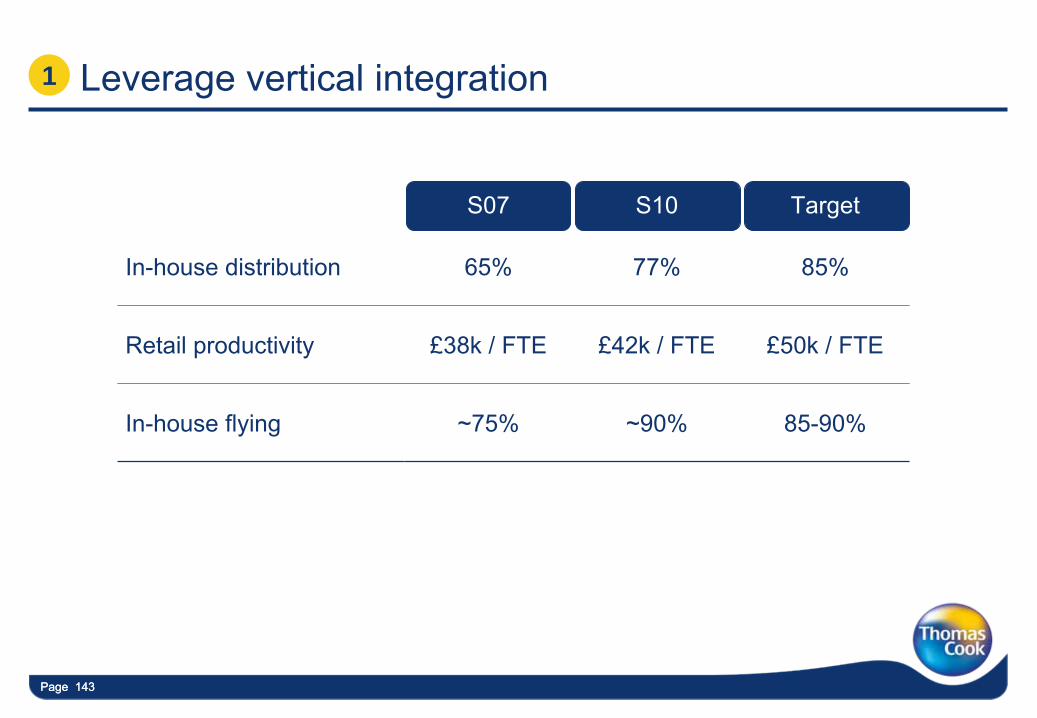

Leverage vertical integration1

Page 144Page 144

Independent travel platform -

Wholesale2

• Number 1 B2B bed bank in the UK

• Significantly grow B2C through OTAB2B bed banks

• A leading scheduled flight consolidator

• Continue to grow volumes and offering

Scheduled flight

consolidator

Brands and products in place to drive significant growth

Page 145Page 145

Independent travel platform –

B2C 2

•

Leading provider of sports-related product

•

Exclusive Olympics 2012 sponsorship

•

We are the largest TO in teaching people to sail

•

Market leader in activity beach clubs

Specialist businesses

•

Strengthened portfolio with Gold Medal acquisition

•

Growth into new product areas

•

Elegant Resorts acquisition -

# 1 luxury long haul TO

Scheduled packages

Brands and products in place to drive significant growth

Page 146Page 146

Independent travel passenger growth

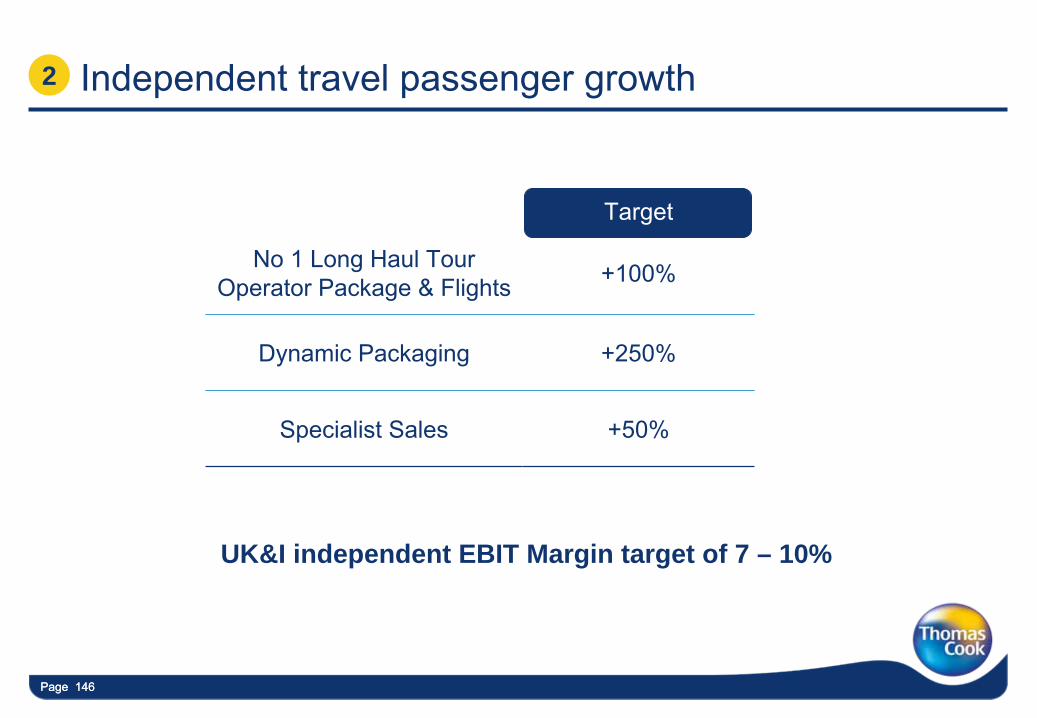

Board Basis Target

No 1 Long Haul TourOperator Package & Flights +100%

Dynamic Packaging +250%

Specialist Sales +50%

2

UK&I independent EBIT Margin target of 7 – 10%

Page 147Page 147

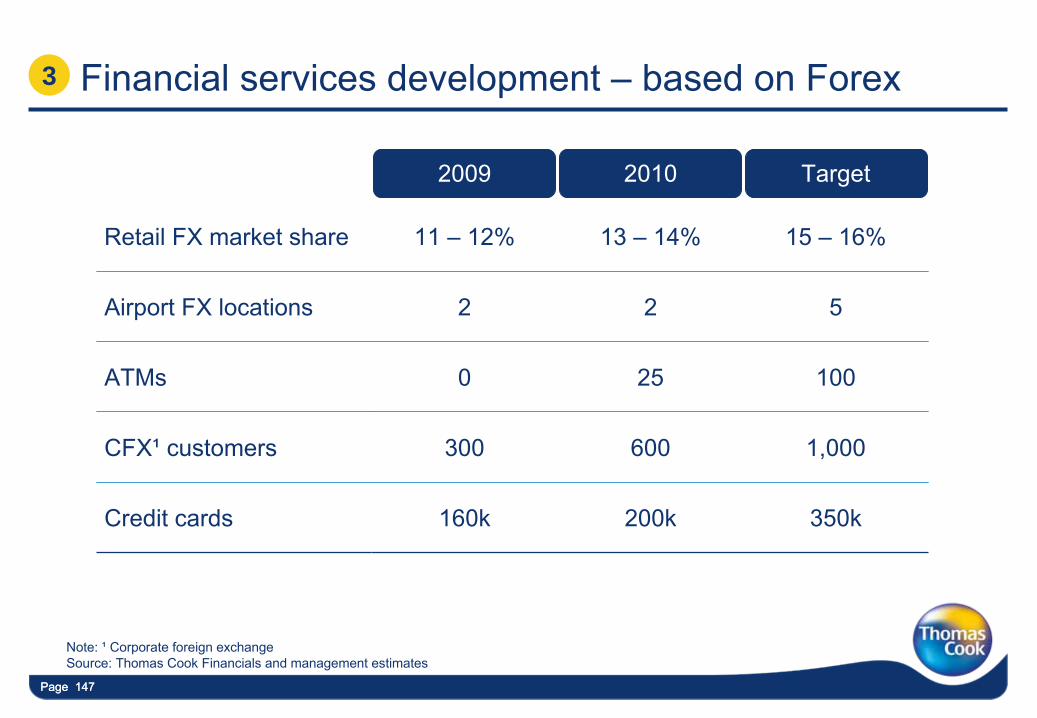

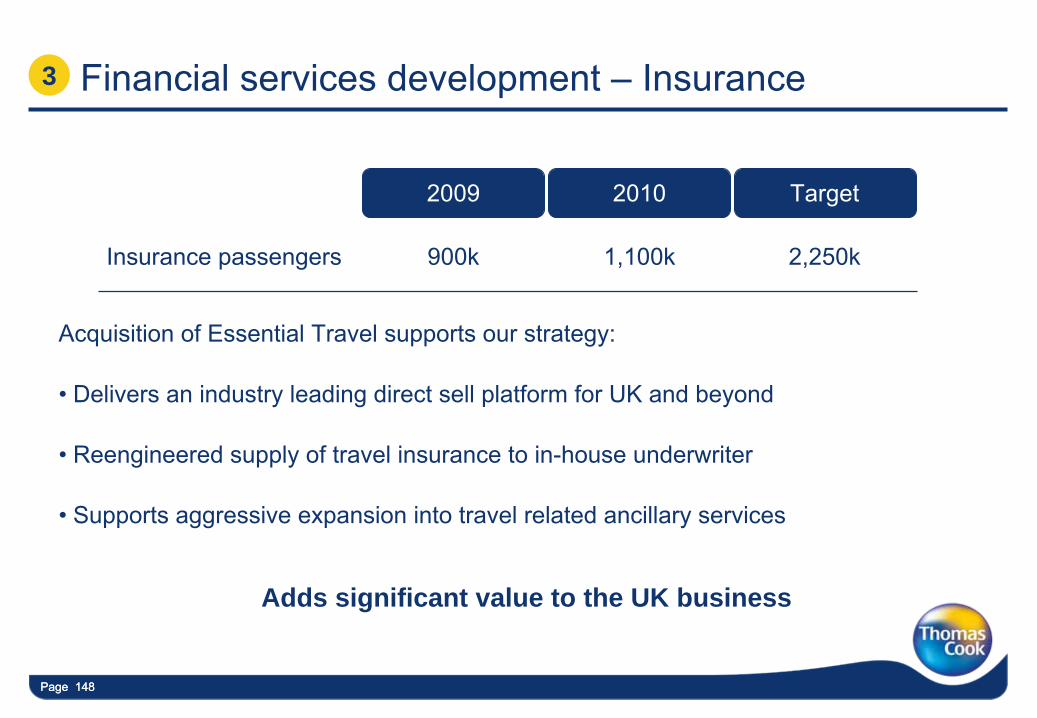

Financial services development –

based on Forex

2009 2010 Target

Retail FX market share 11 –

12% 13 –

14% 15 –

16%

Airport FX locations 2 2 5

ATMs 0 25 100

CFX¹

customers 300 600 1,000

Credit cards 160k 200k 350k

Note: ¹

Corporate foreign exchange Source: Thomas Cook Financials and management estimates

3

Page 148Page 148

Financial services development –

Insurance

2009 2010 Target

Insurance passengers 900k 1,100k 2,250k

Acquisition of Essential Travel supports our strategy:

•

Delivers an industry leading direct sell platform for UK and beyond

•

Reengineered supply of travel insurance to in-house underwriter

•

Supports aggressive expansion into travel related ancillary services

3

Adds significant value to the UK business

Page 149Page 149

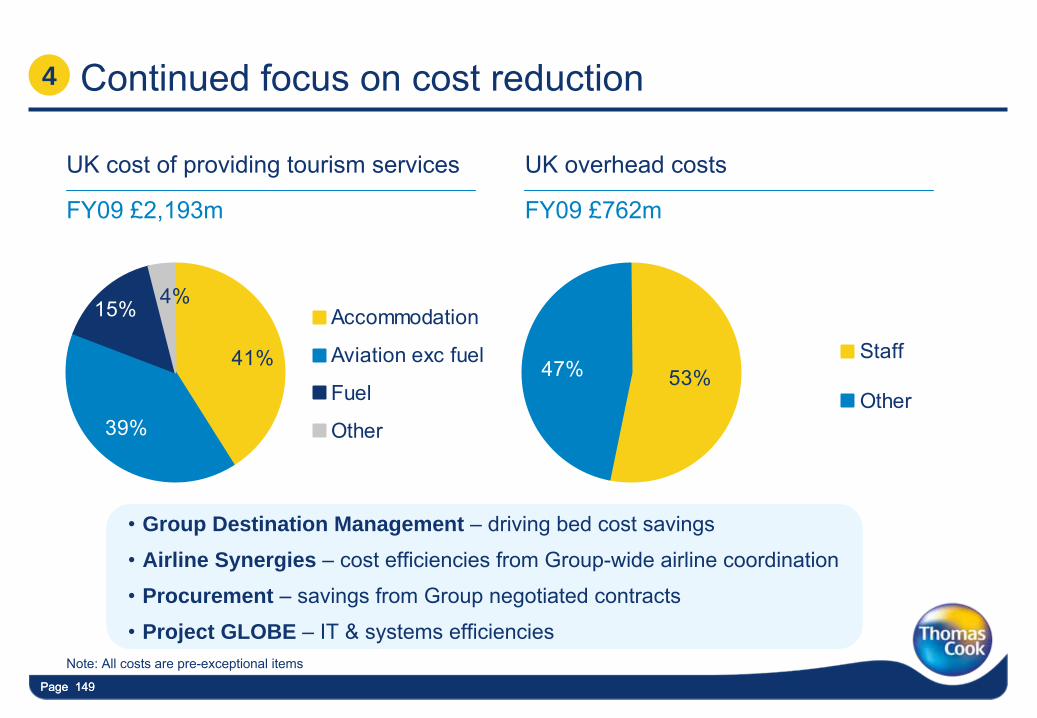

Continued focus on cost reduction

4%

39%

15%

41%

Accommodation

Aviation exc fuel

Fuel

Other

4

UK cost of providing tourism services UK overhead costs

FY09 £2,193m FY09 £762m

47% 53%Staff

Other

•

Group Destination Management –

driving bed cost savings

•

Airline Synergies –

cost efficiencies from Group-wide airline coordination

•

Procurement –

savings from Group negotiated contracts

•

Project GLOBE –

IT & systems efficienciesNote: All costs are pre-exceptional items

Page 150Page 150

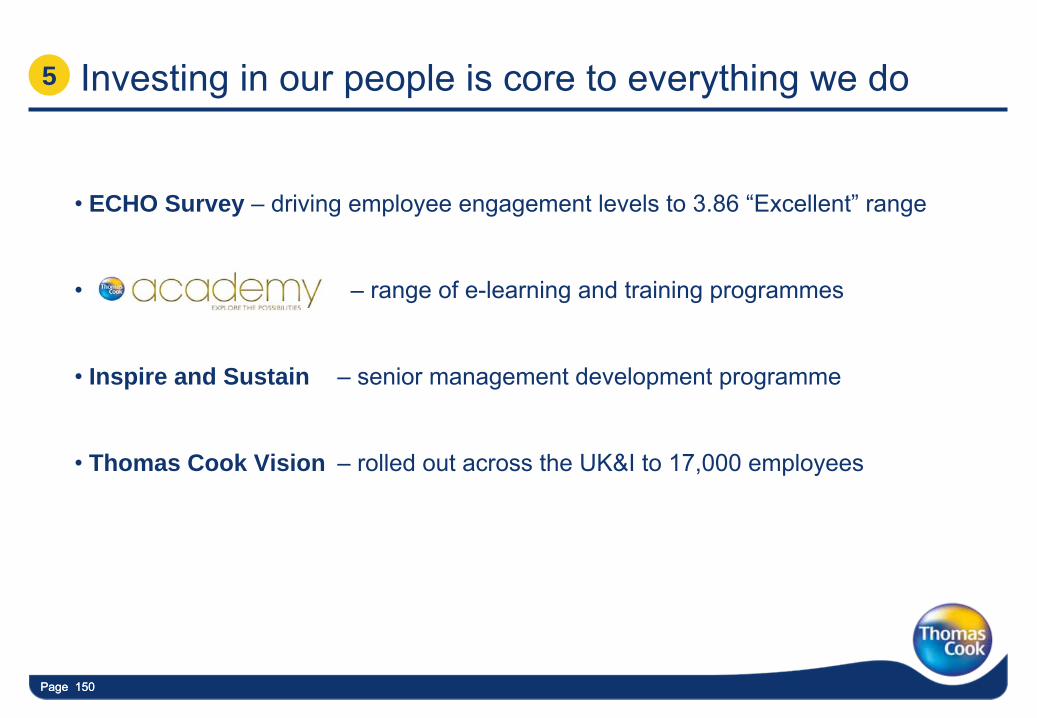

Investing in our people is core to everything we do

•

ECHO Survey –

driving employee engagement levels to 3.86 “Excellent”

range

•

–

range of e-learning and training programmes

•

Inspire and Sustain –

senior management development programme

•

Thomas Cook Vision –

rolled out across the UK&I to 17,000 employees

5

Page 151Page 151Page 151

In summary

•

We will continue to drive benefits from original mainstream strategy set in 2007

•

We will increase margin performance by securing differentiated &

exclusive product

•

Significant volume growth will continue in independent travel

•

Redefining of our financial services proposition will drive growth

Create the UK’s leading travel business

Page 152

Significantly grow online and establish a European OTA business

Simon Breakwell –

Ecommerce Advisor

Page 153

European OTA objectives

•

Thomas Cook online to become a top 3 European OTA

•

Targeting £3-3.5b incremental gross sales

•

Significant profit to come from OTA growth

Page 154

•

Online sale of in-house product as part of multi-channel offer

•

Mainly a European dynamic with TCG/ TUI as market leaders

•

Suppliers of travel components such as airlines, hotels, car hire etc.

•

Major channel for airlines, hotels still reliant on agents

•

Act as middleman, mainly B2B although some B2C brands

•

Bed banks, flight consolidators, etc.

Note: ¹

Packages created online by the user from various travel components (e.g. Flight + hotel + car hire bundle)

OTAs

also starting to sell traditional mainstream packages

Online Travel Agents (OTAs)

•

Online sale of third party components and ePackages¹

•

Expedia/ Priceline European market leaders

Lines beginning to blur between different players

Tour Operators

Suppliers Direct

Wholesalers

Four main types of player in the online travel market

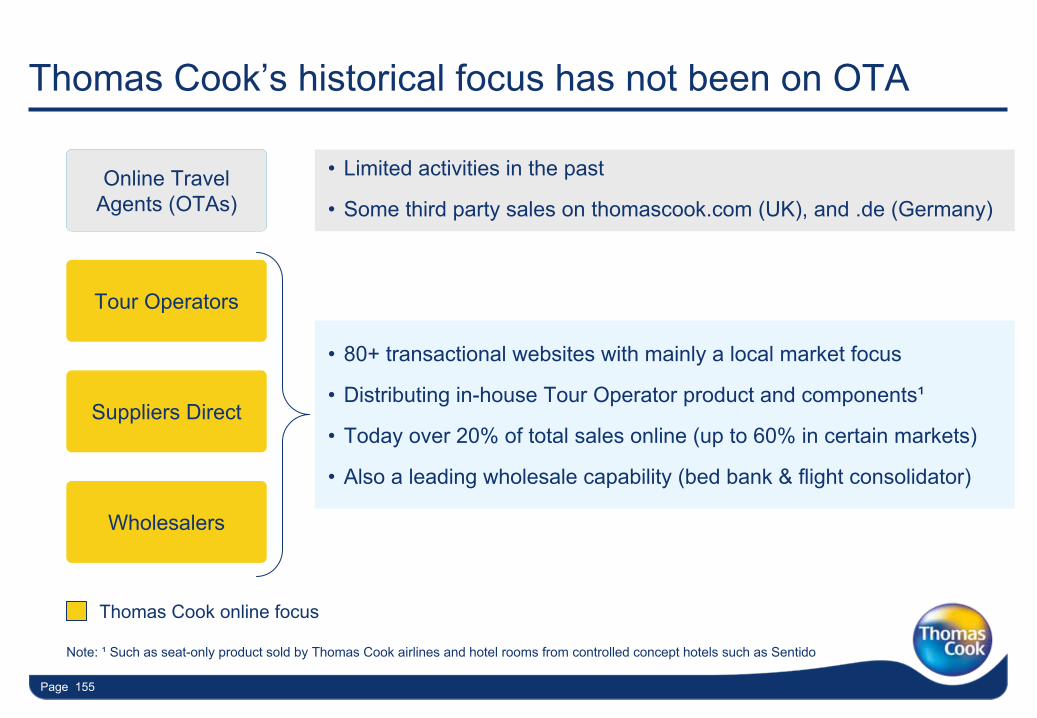

Page 155

Online Travel Agents

•

80+ transactional websites with mainly a local market focus

•

Distributing in-house Tour Operator product and components¹

•

Today over 20% of total sales online (up to 60% in certain markets)

•

Also a leading wholesale capability (bed bank & flight consolidator)

•

Limited activities in the past

•

Some third party sales on thomascook.com

(UK), and .de (Germany)Online Travel

Agents (OTAs)

Tour Operators

Suppliers Direct

Wholesalers

Note: ¹

Such as seat-only product sold by Thomas Cook airlines and hotel rooms from controlled concept hotels such as Sentido

Thomas Cook online focus

Thomas Cook’s historical focus has not been on OTA

Page 156

•

Expand into European OTA market with Thomas Cook branded sites

•

Retail sites selling in-house product & acting as agent for third partiesOnline Travel

Agents (OTAs)

Strategy going forwards

•

Maintain online growth and channel shift of TO and Direct product

•

Local sites for major brands (Ving, Neckermann, Airtours, Condor etc.)

Tour Operators

Suppliers Direct

Wholesalers•

Build & strengthen wholesale capability

•

Third party agent platforms, bed bank and flight consolidator

Major focus is European OTA market entry

Page 157Page 157

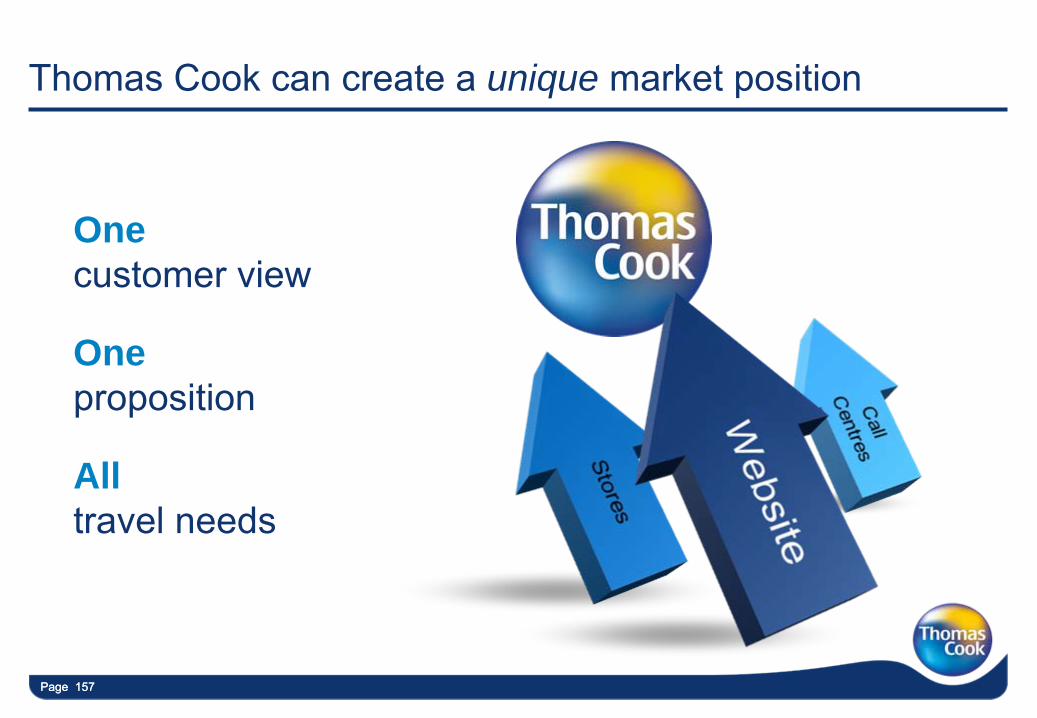

Thomas Cook can create a unique market position

One customer view

One proposition

All travel needs

Page 158Page 158

The OTA market is a major opportunity for Thomas Cook

• European OTA market is large and growing fast

• Barriers to entry are still relatively low

• OTA model offers a route into new source markets

• Significant online platform to build from

• Leverages existing Thomas Cook capabilities

• Thomas Cook can create a unique market position

1

2

3

4

6

Targeting £3-3.5b of incremental gross sales in medium term

5

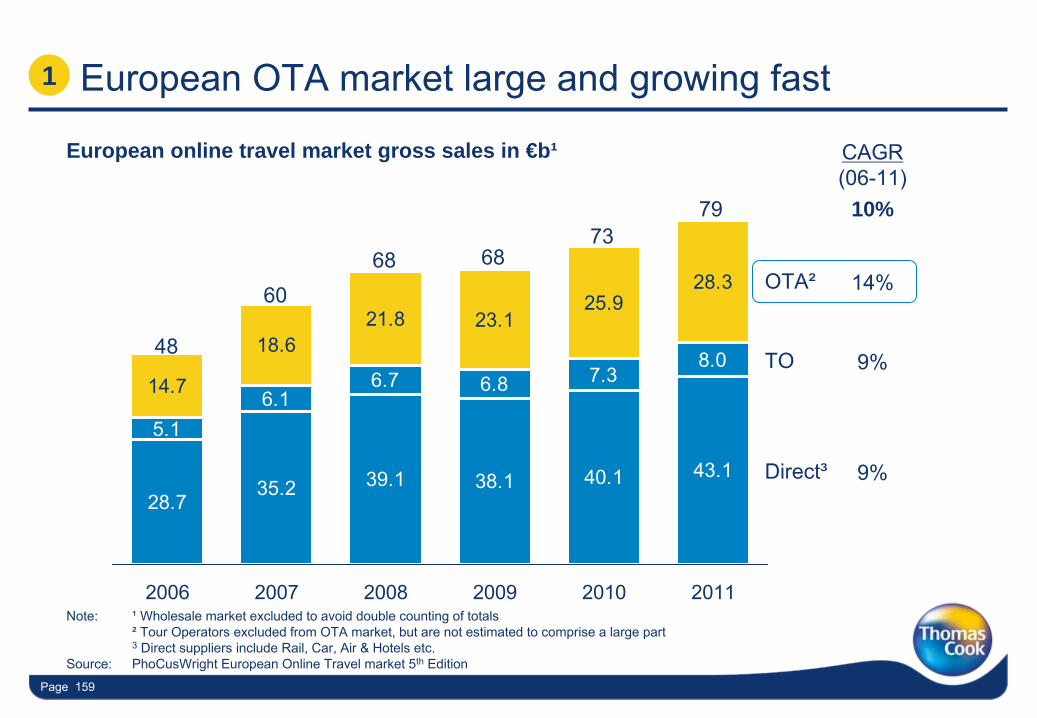

Page 159

28.735.2 39.1 38.1 40.1 43.1

5.16.1

6.7 6.8 7.38.0

14.7

18.621.8 23.1

25.928.3

2006 2007 2008 2009 2010 2011

79

European OTA market large and growing fast

European online travel market gross sales in €b¹

Note:

¹

Wholesale market excluded to avoid double counting of totals²

Tour Operators excluded from OTA market, but are not estimated to comprise a large part3

Direct suppliers include Rail, Car, Air & Hotels etc.Source: PhoCusWright

European Online Travel market 5th

Edition

CAGR(06-11)

9%

6873

6860

48

OTA²

Direct³

TO

9%

14%

10%

1

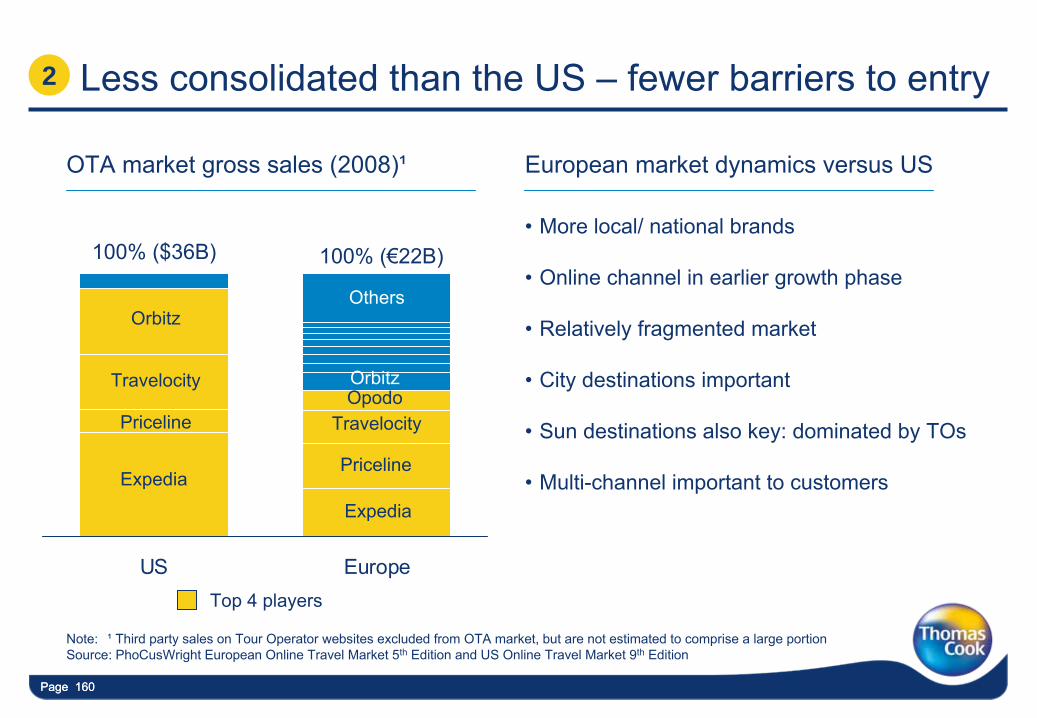

Page 160Page 160

•

More local/ national brands

•

Online channel in earlier growth phase

•

Relatively fragmented market

•

City destinations important

•

Sun destinations also key: dominated by TOs

•

Multi-channel important to customers

Less consolidated than the US –

fewer barriers to entry

OTA market gross sales (2008)¹ European market dynamics versus US

2

Note:

¹

Third party sales on Tour Operator websites excluded from OTA market, but are not estimated to comprise a large portionSource: PhoCusWright

European Online Travel Market 5th

Edition and US Online Travel Market 9th

Edition

US Europe

100% (€22B)

Expedia

Priceline

TravelocityOpodo

100% ($36B)

Expedia

Priceline

Travelocity

Orbitz

Top 4 players

Orbitz

Others

Page 161Page 161

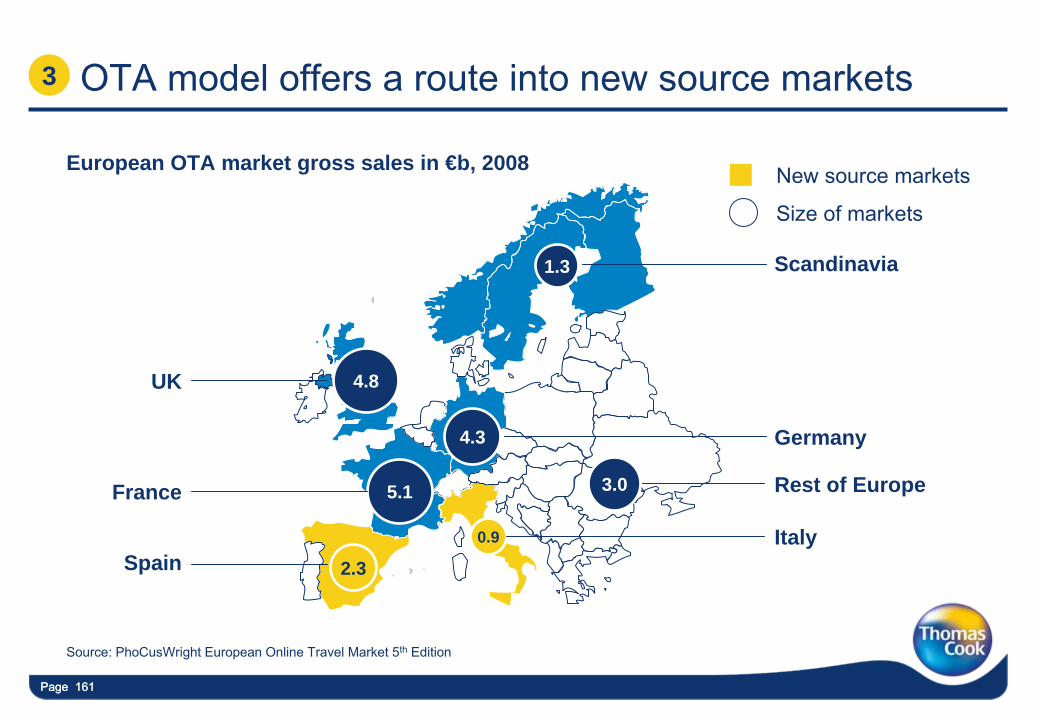

OTA model offers a route into new source markets

Source: PhoCusWright

European Online Travel Market 5th

Edition

3

1.3 Scandinavia

4.3 Germany

0.9

3.0 Rest of Europe

Italy2.3Spain

5.1France

4.8UK

New source markets

Size of markets

European OTA market gross sales in €b, 2008

Page 162

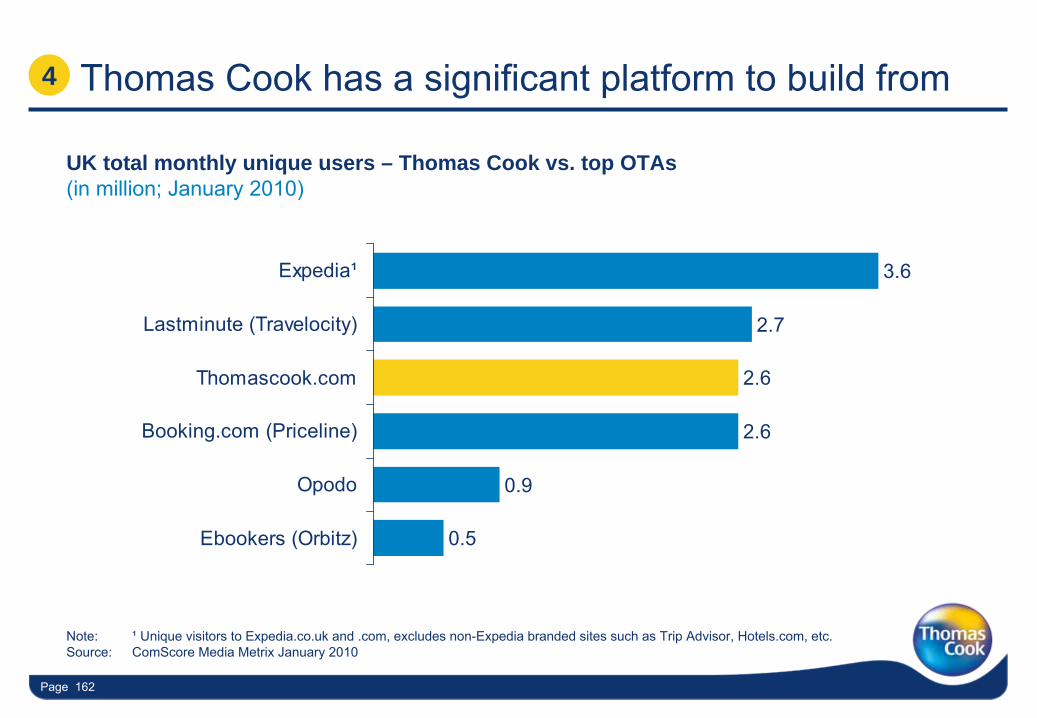

Thomas Cook has a significant platform to build from

UK total monthly unique users – Thomas Cook vs. top OTAs (in million; January 2010)

Note:

¹