Embed Size (px)

Citation preview

0

Investor Briefing Acquisition and Capital Raising

March 2003

1

Disclaimero This presentation is not a recommendation, by ABN AMRO Morgans, Wilson HTM,

Caliburn Partnership or Flight Centre Limited, that you invest in the securities. You should conduct and rely on your own investigations. This offer is only made to persons that fall within one of the exclusions from the disclosure requirement contained in section 708 of the Corporations Act.

o To the maximum extent permitted by law: o no representation, warranty or undertaking, express or implied, is made and no

responsibility or liability is accepted, by Caliburn Partnership, ABN AMRO Morgans, Wilson HTM or Flight Centre Limited, as to the adequacy, accuracy, completeness and reasonableness of this presentation; and

o no responsibility for any errors or omissions from this presentation whether arising out of negligence or otherwise is accepted by Caliburn Partnership, ABN AMRO Morgans, Wilson HTM or Flight Centre Limited.

All $ Australian currency unless otherwise indicated Unless stated otherwise, an exchange rate of $A/£0.371 has been used

2

Agenda

1. Executive Summary

2. Transaction Overview

3. Strategic Rationale

4. Overview of Flight Centre

5. Proforma Financials

6. Capital Raising

7. Summary

Appendices

3

1. Executive Summary

o Flight Centre proposes to acquire Britannic, a leading UK corporate travel business

o Fixed acquisition price of £45.3 million (A$122 million) plus deferred profit share and performance payments*

o No additional debt from acquisition - £5.6** million (A$15 million) in cash on Britannic’s balance sheet

o EPS enhancing - 2002 proforma

* Refer Appendix A for details ** Based on £5.6 million cash on Britannic’s balance sheet as at 31 December 2002. In addition, Flight Centre will

assume any additional cash generated by Britannic between 1 January 2003 and completion

4

1. Executive Summary cont’d

o Capital raising to fund initial payment and preserve balance sheet flexibility

o A$79.6 million via a Non-Renounceable Entitlement Offer

o 1:20 at an Offer price of $18/share (11.3% discount to last price)

o Founders have taken up approximately 1.03 million shares (approximately A$18.5 million)

o All new shares will qualify for the fully franked interim dividend of 18.5 cents per share payable on 29 April 2003

o Balance of consideration (in later years) funded from free cash flow

5

2. Overview of Britannic

o Leading UK corporate travel agency

o Focused on medium to large corporate accounts

o Key clients include a number of major UK and multi-national corporations

o Provides innovative, end-to-end, travel management solutions

o Network of 24 offices and 40 locations throughout the UK

o Experienced management team led by Britannic founder Alan Spence

o Demonstrated track record of profitability and growth

6

2. Financial Track Record

o Britannic is a profitable company with a consistent track record

Year end Year end Year end(A$ million) Dec 2000 Dec 2001 Dec 2002

Revenue 421.8 440.9 432.7

EBIT 9.8 14.2 17.6

EBIT (% of revenue) 2.3% 3.2% 3.9%

Notes: 1. Assumes A$/£ exchange rate of 0.3578

Britannic’s Historical Financial Performance

o In the past two years, Britannic’s business model has moved away from commission based to fee based revenue resulting in increased profitability and decreased revenue

7

2. Acquisition Summary

o Fixed acquisition price of £45.3 million (A$122 million) plus deferred profit share and performance payments – see Appendix A

o 6.3x pro-forma historical (CY02) EBIT*

o Synergies and cost savings from the acquisition not factored in

o Acquisition is scheduled to complete in mid March 2003

o Alan Spence, the MD and CEO of Britannic, will enter into a service agreement to the end of 2007

* After factoring anticipated levels of performance payments (assuming 10% growth in earnings per annum), discounting the deferred payments (at 10%), and based on an exchange rate of A$/£0.371. The multiple does not factor in any additional cash generated by Britannic between 1 January 2003 and completion

8

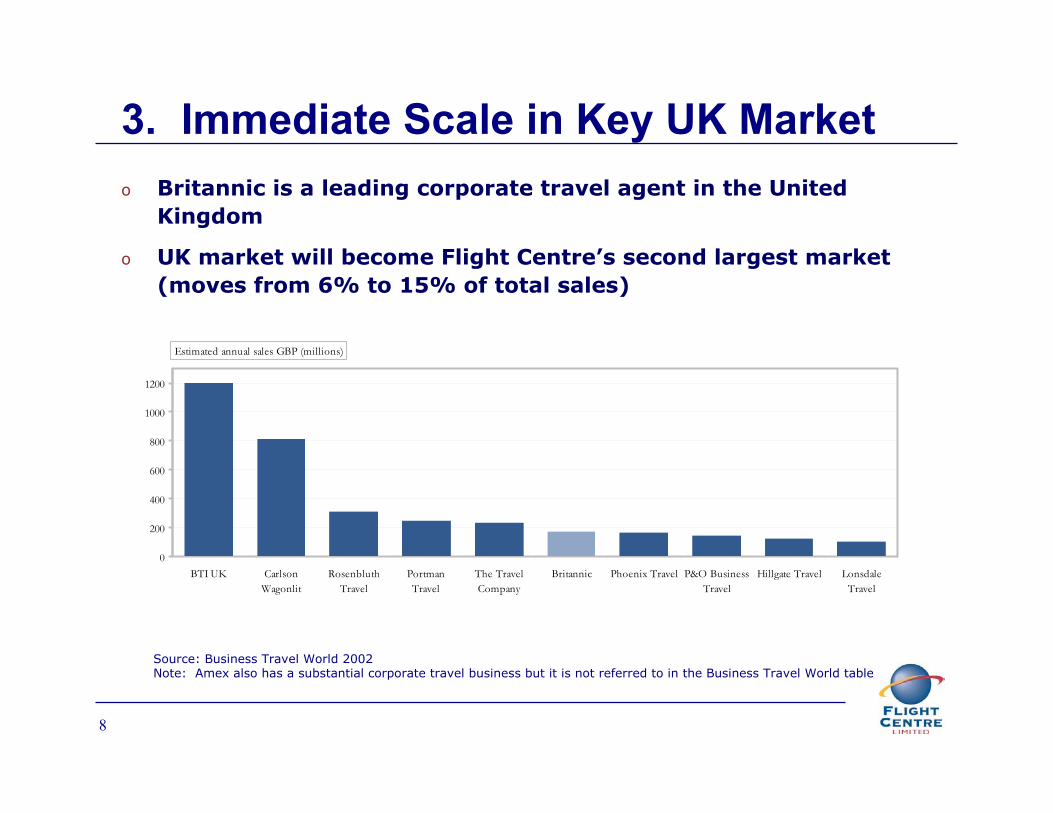

3. Immediate Scale in Key UK Marketo Britannic is a leading corporate travel agent in the United

Kingdom

o UK market will become Flight Centre’s second largest market (moves from 6% to 15% of total sales)

Source: Business Travel World 2002Note: Amex also has a substantial corporate travel business but it is not referred to in the Business Travel World table

0

200

400

600

800

1000

1200

BTI UK CarlsonWagonlit

RosenbluthTravel

PortmanTravel

The TravelCompany

Britannic Phoenix Travel P&O BusinessTravel

Hillgate Travel LonsdaleTravel

Estimated annual sales GBP (millions)

9

3. Developing a Global Platformo Further development of corporate travel platform, consistent

with recent Hong Kong and ITG corporate acquisitions

American International Travel (Med)

American International Travel (Med)Hong Kong

Britannic (Med to Large)Corporate TravellerUK

Corporate TravellerSouth Africa

Corporate TravellerUS/Canada

ITG (Large)SBT Business Travel

(Med)Corporate TravellerAust/NZ

Medium to Large Business Focus

Small to Medium Focus

o Increased exposure to strategic UK market – a key international corporate market

o Complements existing UK corporate business

o Premium corporate accounts

o Enhances capacity to provide global corporate offering

10

o Leading Australian travel retailer

o Rapidly expanding corporate travel operations

o In just 22 years, grown from single Sydney store to more than 1,000 shops and businesses

o Operations encompass Australia, New Zealand, UK, Canada, US, South Africa and Hong Kong

o ASX listed - market capitalisation of A$1.8 billion

o Since listing in 1995, Flight Centre has achieved average total shareholder returns (capital appreciation and dividends) of in excess of 50% per annum

o Five year CAGR in sales of ~25% and EBIT of ~34%

4. Overview of Flight Centre

11

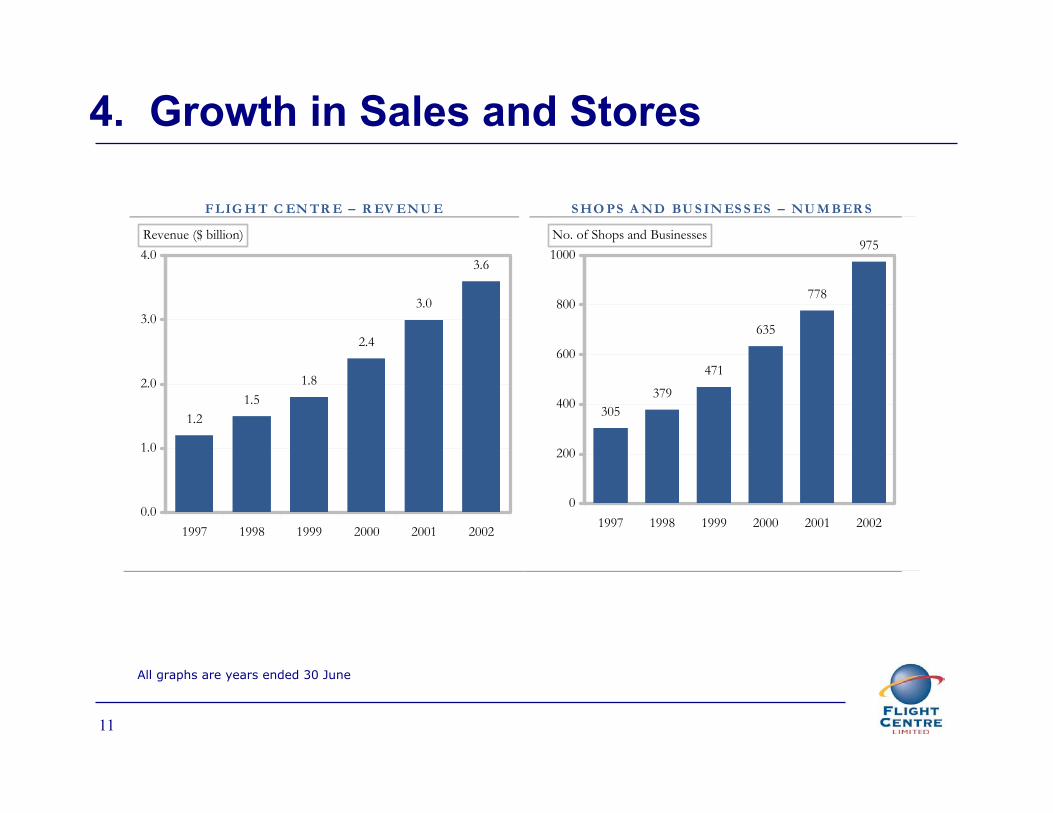

4. Growth in Sales and Stores

F LIG H T C EN TR E – R EV ENU E S HO PS A ND BU S IN ES S ES – NU M BER S

1.21.5

1.8

2.4

3.0

3.6

0.0

1.0

2.0

3.0

4.0

1997 1998 1999 2000 2001 2002

Revenue ($ billion)

305379

471

635

778

975

0

200

400

600

800

1000

1997 1998 1999 2000 2001 2002

No. of Shops and Businesses

All graphs are years ended 30 June

12

4. Growth in Profits

F LIG H T C EN TR E – EB I T F LIG H T C EN TR E – NPA T

21.427.8

44.0

61.566.9

91.1

0

20

40

60

80

100

1997 1998 1999 2000 2001 2002

EBIT ($ m)

14.918.3

27.9

40.3 42.9

62.0

0

20

40

60

80

1997 1998 1999 2000 2001 2002

NPAT ($ m)

All graphs are years ended 30 June

13

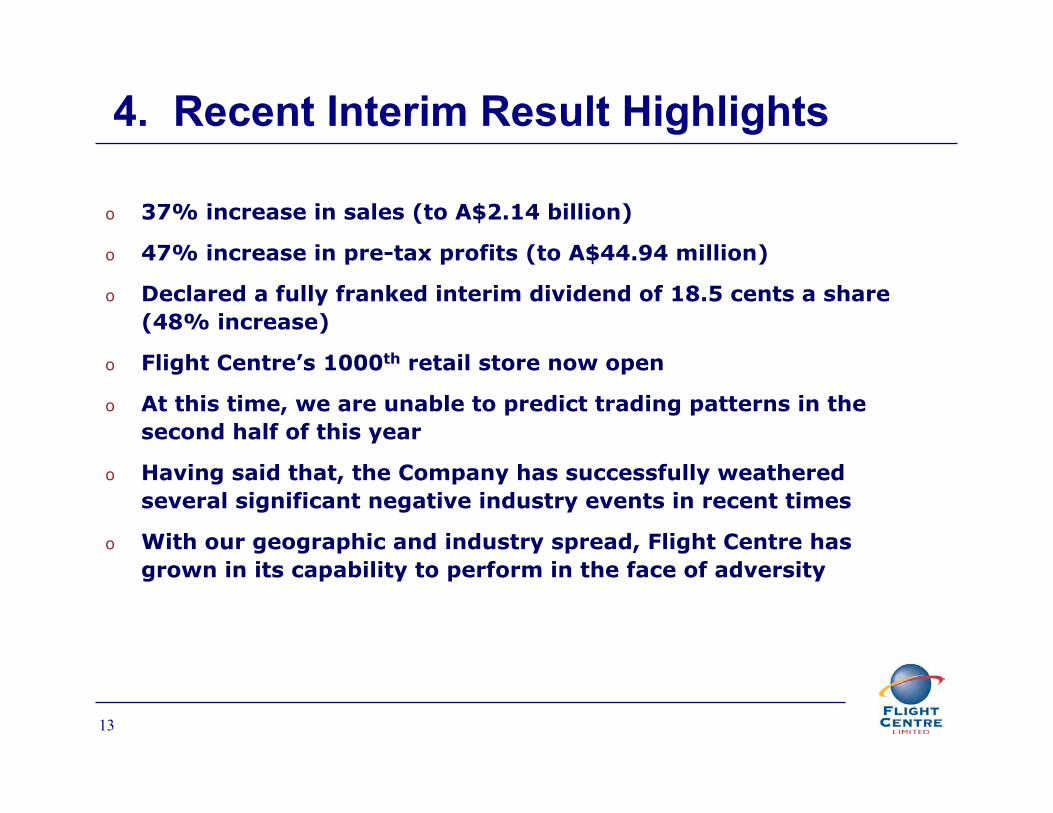

o 37% increase in sales (to A$2.14 billion)

o 47% increase in pre-tax profits (to A$44.94 million)

o Declared a fully franked interim dividend of 18.5 cents a share (48% increase)

o Flight Centre’s 1000th retail store now open

o At this time, we are unable to predict trading patterns in the second half of this year

o Having said that, the Company has successfully weathered several significant negative industry events in recent times

o With our geographic and industry spread, Flight Centre has grown in its capability to perform in the face of adversity

4. Recent Interim Result Highlights

14

5. Proforma Financialso The acquisition enhances EPS on a historic pro-forma basis

o + 3% post goodwill

o + 9% pre goodwill

o Synergies and cost savings have not been factored in

o No additional debt from acquisition

o Flight Centre will assume £5.6* million (A$15 million) in cash

o Goodwill on acquisition of A$100 million

* Based on £5.6 million cash on Britannic’s balance sheet as at 31 December 2002. In addition, Flight Centre will assume any additional cash generated by Britannic between 1 January and completion

15

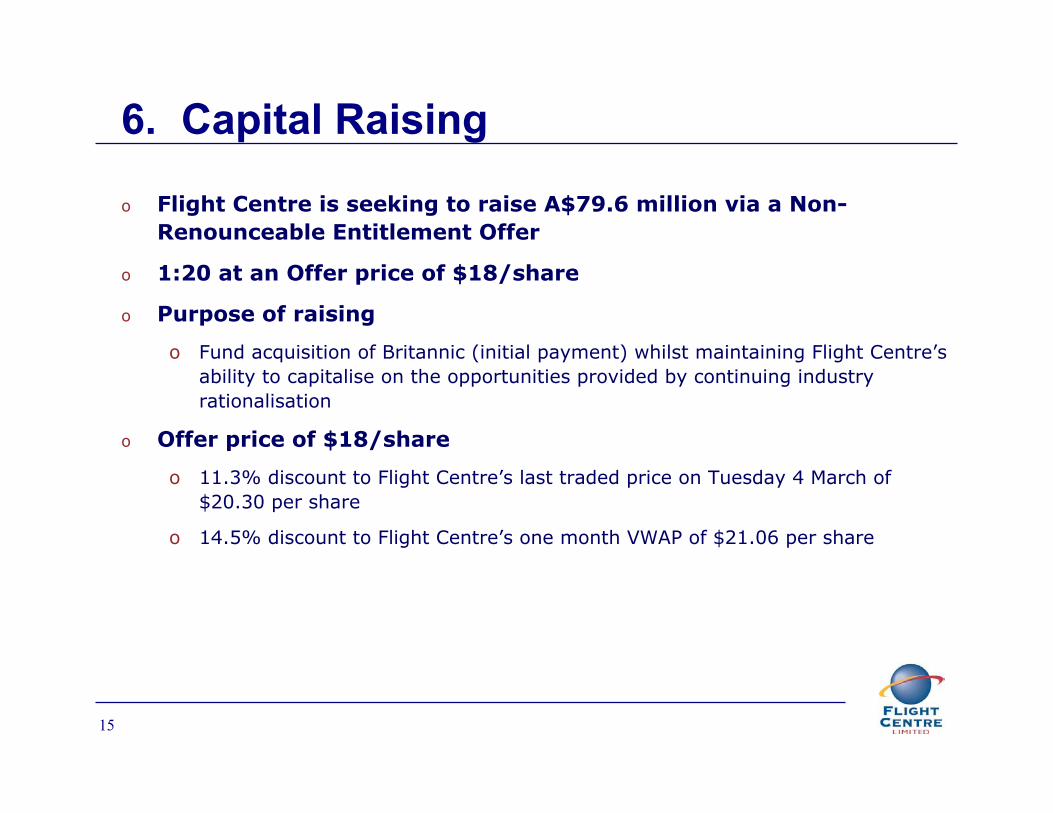

6. Capital Raising

o Flight Centre is seeking to raise A$79.6 million via a Non-Renounceable Entitlement Offer

o 1:20 at an Offer price of $18/share

o Purpose of raising

o Fund acquisition of Britannic (initial payment) whilst maintaining Flight Centre’s ability to capitalise on the opportunities provided by continuing industry rationalisation

o Offer price of $18/share

o 11.3% discount to Flight Centre’s last traded price on Tuesday 4 March of $20.30 per share

o 14.5% discount to Flight Centre’s one month VWAP of $21.06 per share

16

6. Capital Raising cont’d

o Institutional Entitlement Offer

o Accelerated entitlement issue for Founders and Significant Institutional shareholders

o Founders have committed to take up 1.03 million shares (approximately $18.5m)

o Remaining Founder entitlements are to be placed with institutions

o Retail Entitlement Offer

o Remaining institutional shareholders and retail shareholders

o Standard Rights Issue Timetable

o All shares issued under the Offer will qualify for the fully franked interim dividend of 18.5 cents per share payable on 29 April 2003

o It is proposed that the Retail Entitlement Offer is underwritten by ABN AMRO Morgans and Wilson HTM

17

6. Key Dates

Dividend record dateTues 22 April

Settlement of Institutional OfferTues 11 March

Announcement of Combined Offer and Acquisition

Fri 7 March

Record dateWed 19 March

Institutional Offer closesThurs 6 March

Trading halt (48 hours) and Investor Roadshow

Wed 5 March – Thurs 6 March

18

7. Summary

o Sensible acquisition and good strategic fit

o Strengthens Flight Centre’s growing corporate business

o Provides scale in strategic UK market

o Experienced management team, with MD incentivised to remain with the business

o EPS enhancing - 2002

o Synergies / cost savings (not factored in)

o Opportunity to purchase new shares in Flight Centre at a 11.3% discount to the last trading price

o All new shares will qualify for the fully franked interim dividend of 18.5 cents per share payable on 29 April 2003

19

Questions

20

Contact Details

Messrs Ron Malek / Matthew StubbsCaliburn PartnershipPh: 02 9229 1410

Mr Shane FlynnChief Executive OfficerFlight Centre LimitedPh: 0439 710 023

Mr Graham TurnerManaging DirectorFlight Centre LimitedPh: 0412 741 867

Mr Norman C. FussellChairmanFlight Centre LimitedPh: 0419 772 063

Messrs Simon Keyser/David GrothWilson HTMPh: 07 3212 1310 or 02 8247 6622

Messrs Tim Crommelin/Anthony KirkABN AMRO MorgansPh: 07 3334 4888

Mr Jim SturgessChief Financial OfficerFlight Centre LimitedPh: 0402 890 654

21

Appendices

22

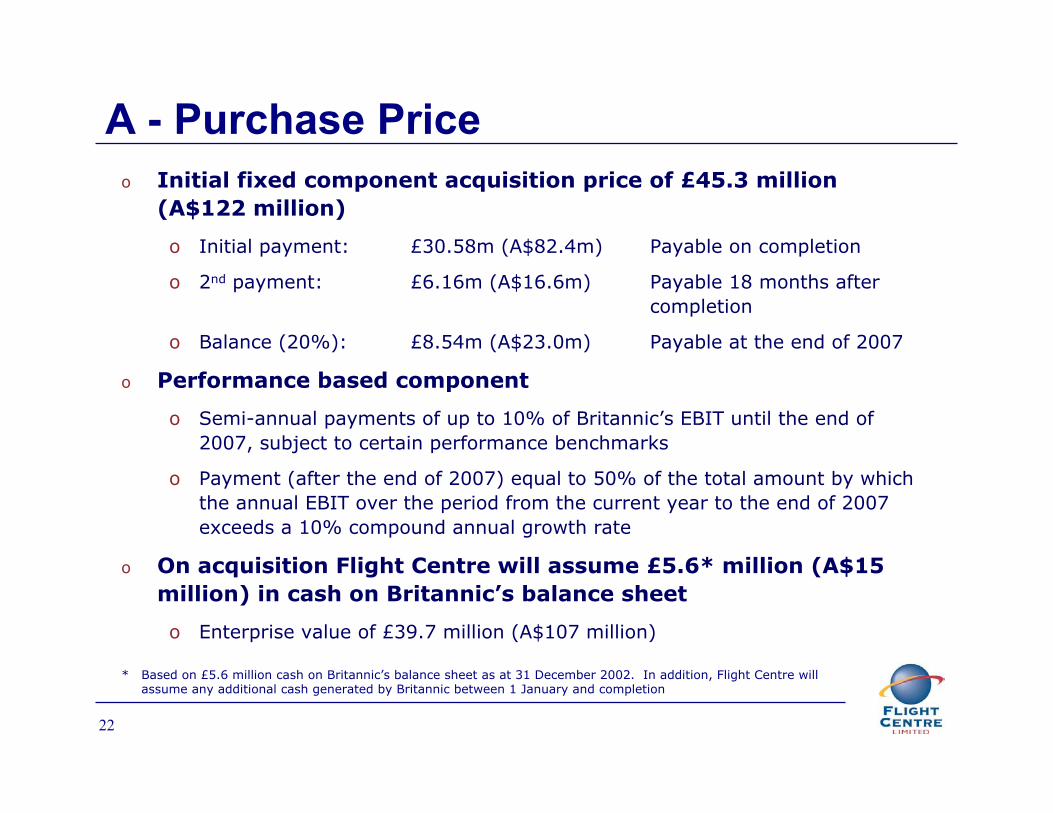

A - Purchase Priceo Initial fixed component acquisition price of £45.3 million

(A$122 million)

o Initial payment: £30.58m (A$82.4m) Payable on completion

o 2nd payment: £6.16m (A$16.6m) Payable 18 months after completion

o Balance (20%): £8.54m (A$23.0m) Payable at the end of 2007

o Performance based component

o Semi-annual payments of up to 10% of Britannic’s EBIT until the end of 2007, subject to certain performance benchmarks

o Payment (after the end of 2007) equal to 50% of the total amount by which the annual EBIT over the period from the current year to the end of 2007 exceeds a 10% compound annual growth rate

o On acquisition Flight Centre will assume £5.6* million (A$15 million) in cash on Britannic’s balance sheet

o Enterprise value of £39.7 million (A$107 million)

* Based on £5.6 million cash on Britannic’s balance sheet as at 31 December 2002. In addition, Flight Centre will assume any additional cash generated by Britannic between 1 January and completion

23

B - Proforma Financial Performance

1 2 MON THS TO 31 DECE MB ER 2 00 2

( A$ MI L L I ON) FL IGHT CEN TRE BRI TAN N IC

PRO FORMA ADJUST MEN T S CONSOLIDATE D

Revenue 4,173.1 432.7 0.0 4,605.8

EBIT 103.9 17.6 (5.0) 116.5

Profit after tax 72.2 12.9 (7.2) 77.9

Basic EPS before amortisation of goodwill 86.1 93.8

- accretion/(dilution) 9% Basic EPS 82.5 84.8 - accretion/dilution 3%

Weighted average number of Shares used as the denominator in calculating basic EPS (million) 87.57 91.96

24

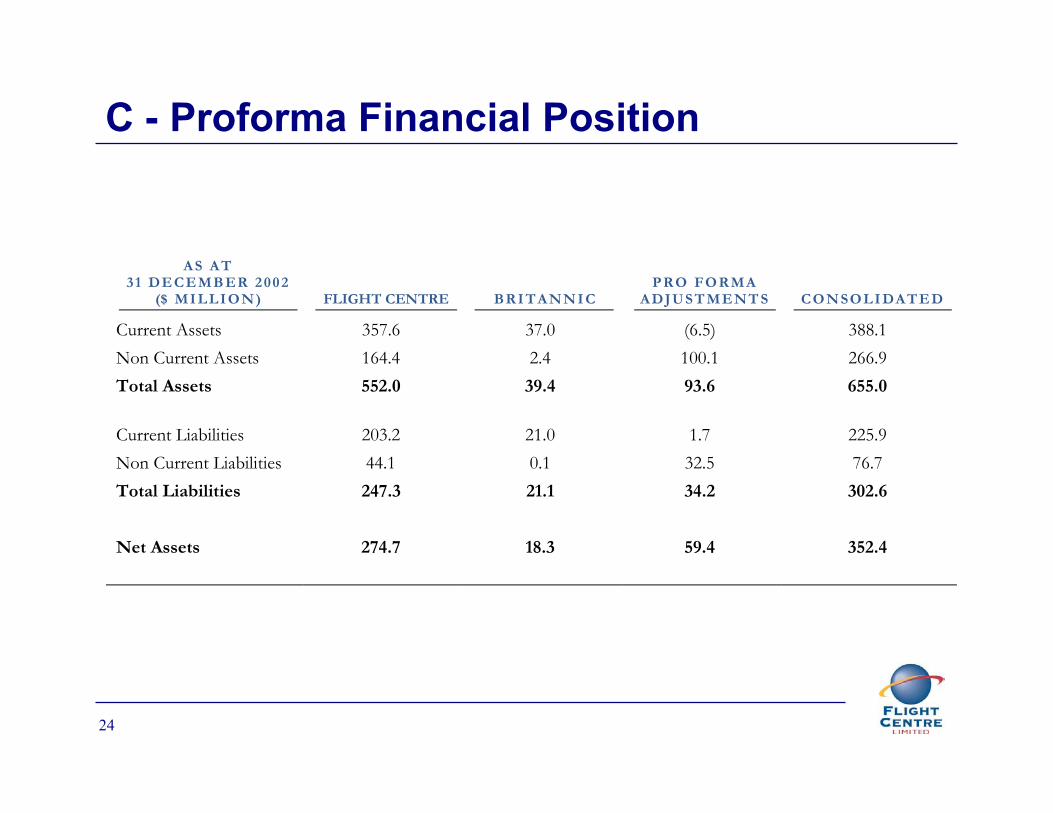

C - Proforma Financial Position

AS AT 31 DE CE MB ER 2 00 2

($ MI LLI ON ) FLIGHT CENTRE BRI TANN I C PRO FORMA

ADJUST MENT S CON SOLI DATE D

Current Assets 357.6 37.0 (6.5) 388.1 Non Current Assets 164.4 2.4 100.1 266.9 Total Assets 552.0 39.4 93.6 655.0 Current Liabilities 203.2 21.0 1.7 225.9 Non Current Liabilities 44.1 0.1 32.5 76.7 Total Liabilities 247.3 21.1 34.2 302.6

Net Assets 274.7 18.3 59.4 352.4