Embed Size (px)

Citation preview

Important disclosures and certifications are contained from page 16 of this report. www.danskeresearch.com

Investment Research

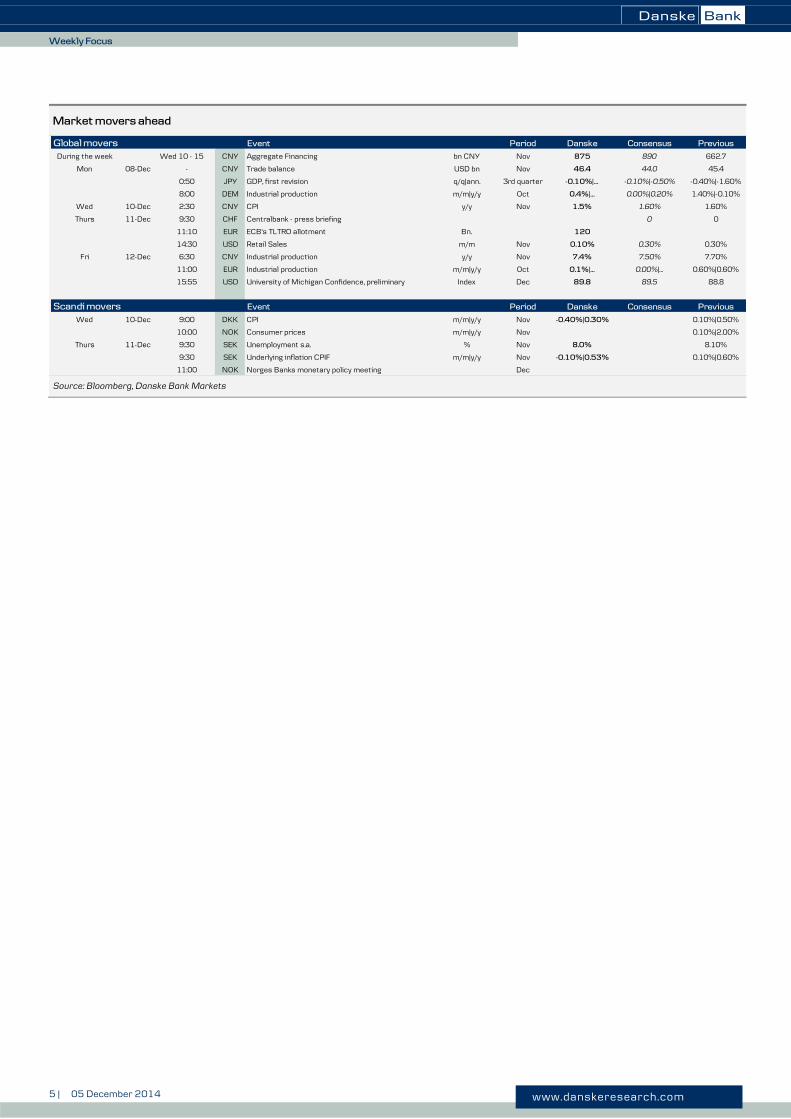

Market movers ahead

There are downside risks to the coming week’s US retail sales data and upside risks to

the preliminary December University of Michigan’s consumer sentiment index.

Furthermore, the Fed’s Labour Market Condition Index for November will be

released on Monday, which will provide important input for the FOMC meeting on

16-17 December.

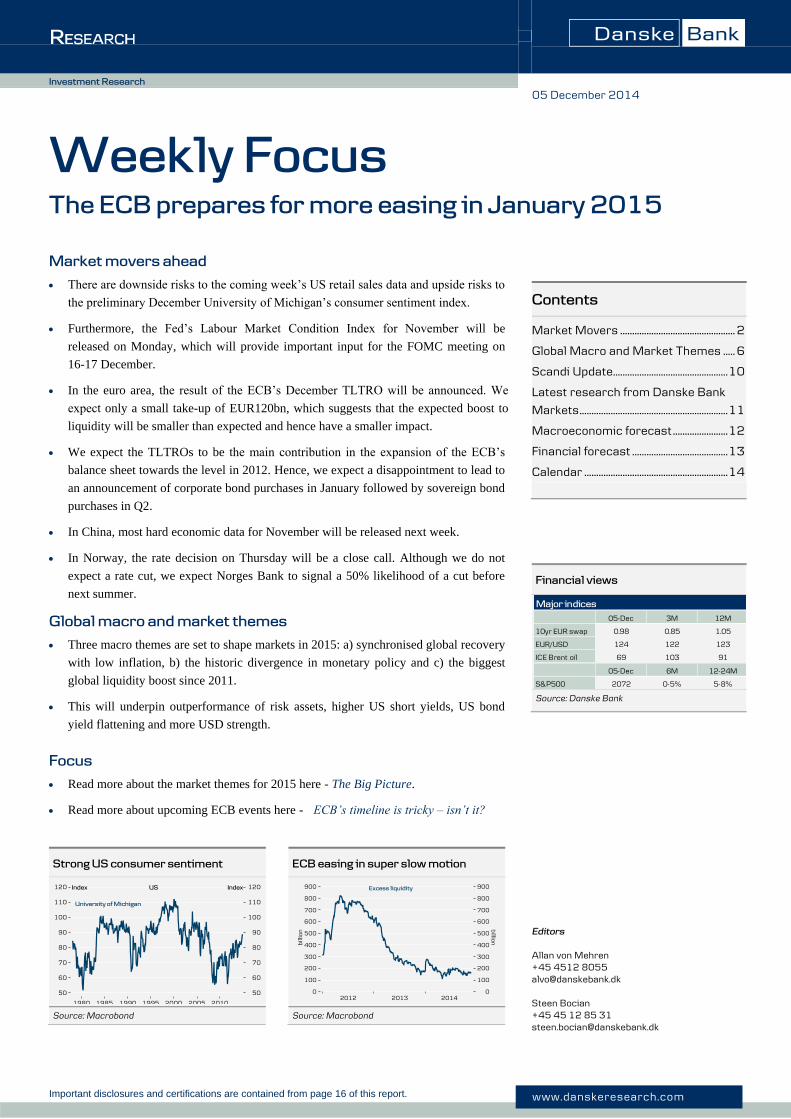

In the euro area, the result of the ECB’s December TLTRO will be announced. We expect only a small take-up of EUR120bn, which suggests that the expected boost to liquidity will be smaller than expected and hence have a smaller impact.

We expect the TLTROs to be the main contribution in the expansion of the ECB’s

balance sheet towards the level in 2012. Hence, we expect a disappointment to lead to

an announcement of corporate bond purchases in January followed by sovereign bond

purchases in Q2.

In China, most hard economic data for November will be released next week.

In Norway, the rate decision on Thursday will be a close call. Although we do not

expect a rate cut, we expect Norges Bank to signal a 50% likelihood of a cut before

next summer.

Global macro and market themes

Three macro themes are set to shape markets in 2015: a) synchronised global recovery

with low inflation, b) the historic divergence in monetary policy and c) the biggest

global liquidity boost since 2011.

This will underpin outperformance of risk assets, higher US short yields, US bond

yield flattening and more USD strength.

Focus

Read more about the market themes for 2015 here - The Big Picture.

Read more about upcoming ECB events here - ECB’s timeline is tricky – isn’t it?

05 December 2014

Editors

Allan von Mehren +45 4512 8055 [email protected]

Steen Bocian +45 45 12 85 31 [email protected]

Weekly Focus

The ECB prepares for more easing in January 2015

Contents

Market Movers ................................................ 2

Global Macro and Market Themes ..... 6

Scandi Update................................................ 10

Latest research from Danske Bank

Markets .............................................................. 11

Macroeconomic forecast ....................... 12

Financial forecast ........................................ 13

Calendar ............................................................ 14

Financial views

Source: Danske Bank

Strong US consumer sentiment ECB easing in super slow motion

Source: Macrobond Source: Macrobond

Major indices

05-Dec 3M 12M

10yr EUR swap 0.98 0.85 1.05

EUR/USD 124 122 123

ICE Brent oil 69 103 91

05-Dec 6M 12-24M

S&P500 2072 0-5% 5-8%

2 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Market Movers

Global

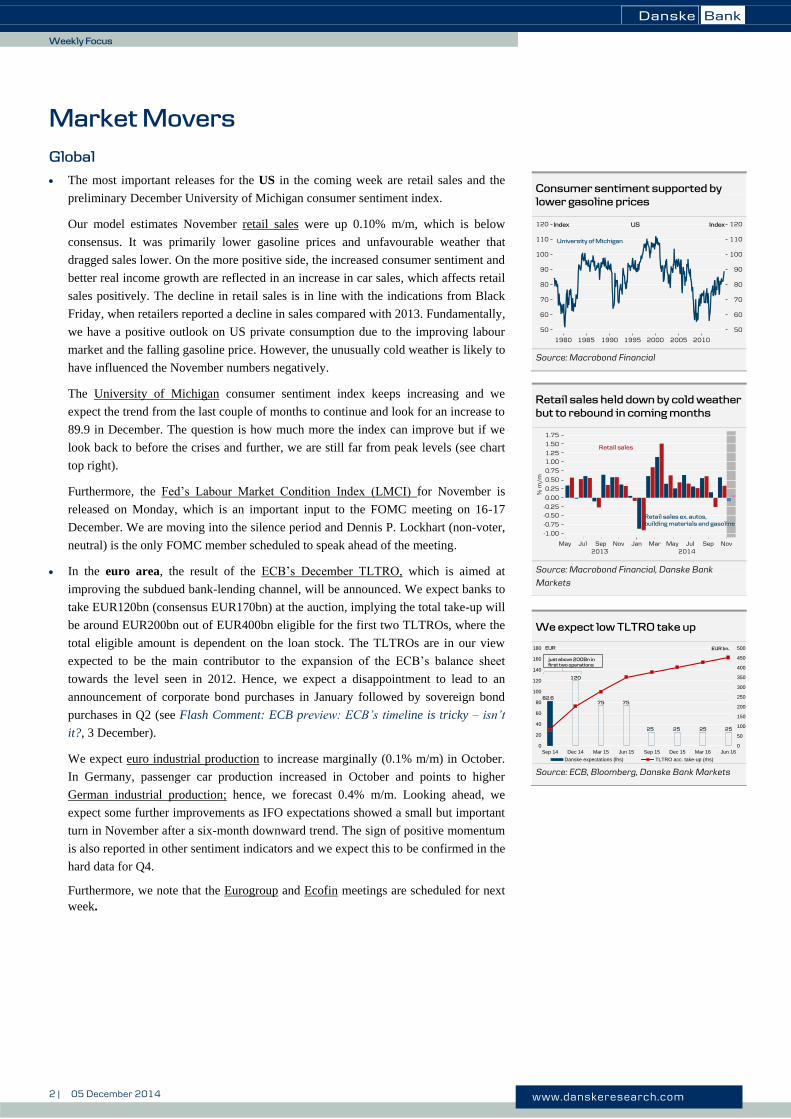

The most important releases for the US in the coming week are retail sales and the

preliminary December University of Michigan consumer sentiment index.

Our model estimates November retail sales were up 0.10% m/m, which is below

consensus. It was primarily lower gasoline prices and unfavourable weather that

dragged sales lower. On the more positive side, the increased consumer sentiment and

better real income growth are reflected in an increase in car sales, which affects retail

sales positively. The decline in retail sales is in line with the indications from Black

Friday, when retailers reported a decline in sales compared with 2013. Fundamentally,

we have a positive outlook on US private consumption due to the improving labour

market and the falling gasoline price. However, the unusually cold weather is likely to

have influenced the November numbers negatively.

The University of Michigan consumer sentiment index keeps increasing and we

expect the trend from the last couple of months to continue and look for an increase to

89.9 in December. The question is how much more the index can improve but if we

look back to before the crises and further, we are still far from peak levels (see chart

top right).

Furthermore, the Fed’s Labour Market Condition Index (LMCI) for November is

released on Monday, which is an important input to the FOMC meeting on 16-17

December. We are moving into the silence period and Dennis P. Lockhart (non-voter,

neutral) is the only FOMC member scheduled to speak ahead of the meeting.

In the euro area, the result of the ECB’s December TLTRO, which is aimed at

improving the subdued bank-lending channel, will be announced. We expect banks to

take EUR120bn (consensus EUR170bn) at the auction, implying the total take-up will

be around EUR200bn out of EUR400bn eligible for the first two TLTROs, where the

total eligible amount is dependent on the loan stock. The TLTROs are in our view

expected to be the main contributor to the expansion of the ECB’s balance sheet

towards the level seen in 2012. Hence, we expect a disappointment to lead to an

announcement of corporate bond purchases in January followed by sovereign bond

purchases in Q2 (see Flash Comment: ECB preview: ECB’s timeline is tricky – isn’t

it?, 3 December).

We expect euro industrial production to increase marginally (0.1% m/m) in October.

In Germany, passenger car production increased in October and points to higher

German industrial production; hence, we forecast 0.4% m/m. Looking ahead, we

expect some further improvements as IFO expectations showed a small but important

turn in November after a six-month downward trend. The sign of positive momentum

is also reported in other sentiment indicators and we expect this to be confirmed in the

hard data for Q4.

Furthermore, we note that the Eurogroup and Ecofin meetings are scheduled for next

week.

Consumer sentiment supported by

lower gasoline prices

Source: Macrobond Financial

Retail sales held down by cold weather

but to rebound in coming months

Source: Macrobond Financial, Danske Bank

Markets

We expect low TLTRO take up

Source: ECB, Bloomberg, Danske Bank Markets

0

50

100

150

200

250

300

350

400

450

500

0

20

40

60

80

100

120

140

160

180

Sep 14 Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16

Danske expectations (lhs) TLTRO acc. take-up (rhs)

EUR EUR bn.

just above 200Bn in

first two operations

82.6

120

75 75

25 25 25 25

3 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

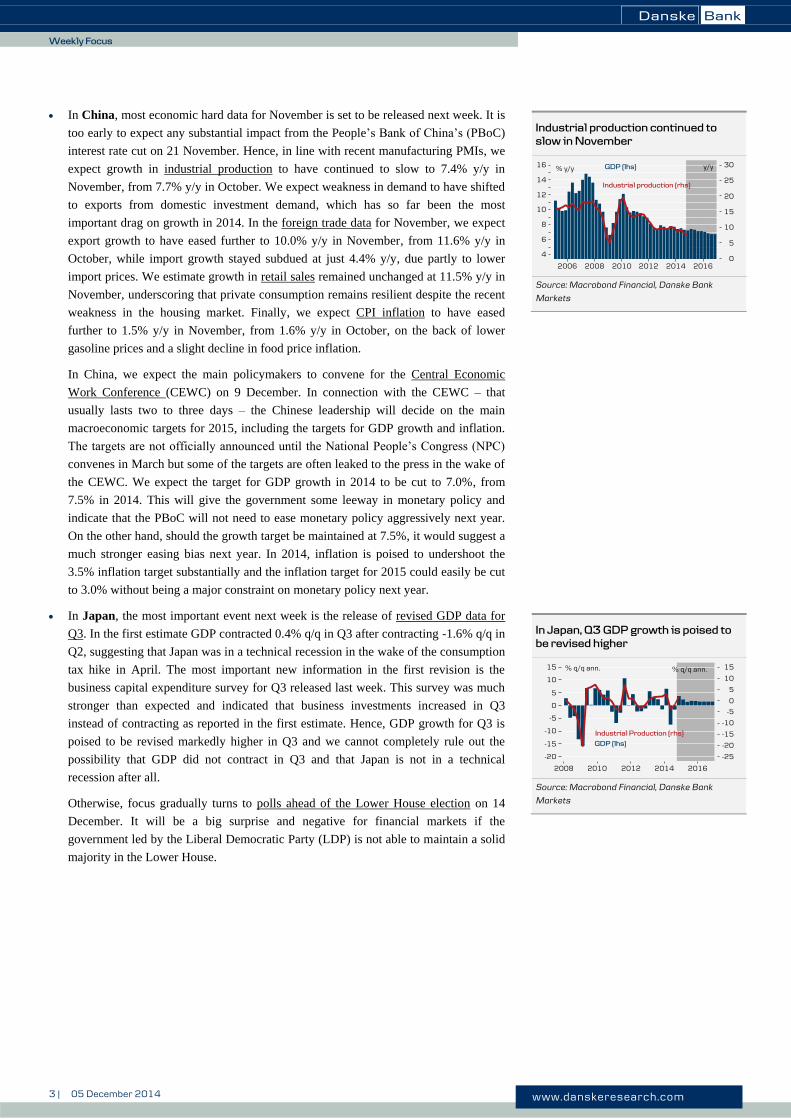

In China, most economic hard data for November is set to be released next week. It is

too early to expect any substantial impact from the People’s Bank of China’s (PBoC)

interest rate cut on 21 November. Hence, in line with recent manufacturing PMIs, we

expect growth in industrial production to have continued to slow to 7.4% y/y in

November, from 7.7% y/y in October. We expect weakness in demand to have shifted

to exports from domestic investment demand, which has so far been the most

important drag on growth in 2014. In the foreign trade data for November, we expect

export growth to have eased further to 10.0% y/y in November, from 11.6% y/y in

October, while import growth stayed subdued at just 4.4% y/y, due partly to lower

import prices. We estimate growth in retail sales remained unchanged at 11.5% y/y in

November, underscoring that private consumption remains resilient despite the recent

weakness in the housing market. Finally, we expect CPI inflation to have eased

further to 1.5% y/y in November, from 1.6% y/y in October, on the back of lower

gasoline prices and a slight decline in food price inflation.

In China, we expect the main policymakers to convene for the Central Economic

Work Conference (CEWC) on 9 December. In connection with the CEWC – that

usually lasts two to three days – the Chinese leadership will decide on the main

macroeconomic targets for 2015, including the targets for GDP growth and inflation.

The targets are not officially announced until the National People’s Congress (NPC)

convenes in March but some of the targets are often leaked to the press in the wake of

the CEWC. We expect the target for GDP growth in 2014 to be cut to 7.0%, from

7.5% in 2014. This will give the government some leeway in monetary policy and

indicate that the PBoC will not need to ease monetary policy aggressively next year.

On the other hand, should the growth target be maintained at 7.5%, it would suggest a

much stronger easing bias next year. In 2014, inflation is poised to undershoot the

3.5% inflation target substantially and the inflation target for 2015 could easily be cut

to 3.0% without being a major constraint on monetary policy next year.

In Japan, the most important event next week is the release of revised GDP data for

Q3. In the first estimate GDP contracted 0.4% q/q in Q3 after contracting -1.6% q/q in

Q2, suggesting that Japan was in a technical recession in the wake of the consumption

tax hike in April. The most important new information in the first revision is the

business capital expenditure survey for Q3 released last week. This survey was much

stronger than expected and indicated that business investments increased in Q3

instead of contracting as reported in the first estimate. Hence, GDP growth for Q3 is

poised to be revised markedly higher in Q3 and we cannot completely rule out the

possibility that GDP did not contract in Q3 and that Japan is not in a technical

recession after all.

Otherwise, focus gradually turns to polls ahead of the Lower House election on 14

December. It will be a big surprise and negative for financial markets if the

government led by the Liberal Democratic Party (LDP) is not able to maintain a solid

majority in the Lower House.

Industrial production continued to

slow in November

Source: Macrobond Financial, Danske Bank

Markets

In Japan, Q3 GDP growth is poised to

be revised higher

Source: Macrobond Financial, Danske Bank

Markets

4 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Scandi

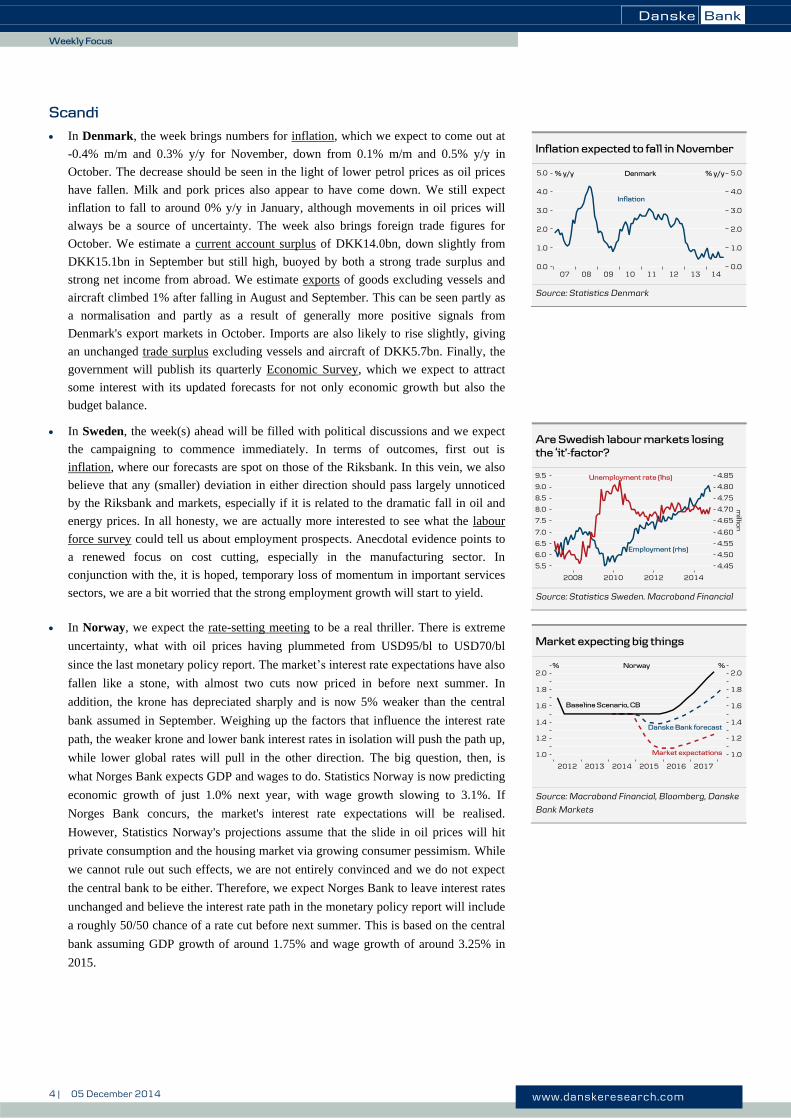

In Denmark, the week brings numbers for inflation, which we expect to come out at

-0.4% m/m and 0.3% y/y for November, down from 0.1% m/m and 0.5% y/y in

October. The decrease should be seen in the light of lower petrol prices as oil prices

have fallen. Milk and pork prices also appear to have come down. We still expect

inflation to fall to around 0% y/y in January, although movements in oil prices will

always be a source of uncertainty. The week also brings foreign trade figures for

October. We estimate a current account surplus of DKK14.0bn, down slightly from

DKK15.1bn in September but still high, buoyed by both a strong trade surplus and

strong net income from abroad. We estimate exports of goods excluding vessels and

aircraft climbed 1% after falling in August and September. This can be seen partly as

a normalisation and partly as a result of generally more positive signals from

Denmark's export markets in October. Imports are also likely to rise slightly, giving

an unchanged trade surplus excluding vessels and aircraft of DKK5.7bn. Finally, the

government will publish its quarterly Economic Survey, which we expect to attract

some interest with its updated forecasts for not only economic growth but also the

budget balance.

In Sweden, the week(s) ahead will be filled with political discussions and we expect

the campaigning to commence immediately. In terms of outcomes, first out is

inflation, where our forecasts are spot on those of the Riksbank. In this vein, we also

believe that any (smaller) deviation in either direction should pass largely unnoticed

by the Riksbank and markets, especially if it is related to the dramatic fall in oil and

energy prices. In all honesty, we are actually more interested to see what the labour

force survey could tell us about employment prospects. Anecdotal evidence points to

a renewed focus on cost cutting, especially in the manufacturing sector. In

conjunction with the, it is hoped, temporary loss of momentum in important services

sectors, we are a bit worried that the strong employment growth will start to yield.

In Norway, we expect the rate-setting meeting to be a real thriller. There is extreme

uncertainty, what with oil prices having plummeted from USD95/bl to USD70/bl

since the last monetary policy report. The market’s interest rate expectations have also

fallen like a stone, with almost two cuts now priced in before next summer. In

addition, the krone has depreciated sharply and is now 5% weaker than the central

bank assumed in September. Weighing up the factors that influence the interest rate

path, the weaker krone and lower bank interest rates in isolation will push the path up,

while lower global rates will pull in the other direction. The big question, then, is

what Norges Bank expects GDP and wages to do. Statistics Norway is now predicting

economic growth of just 1.0% next year, with wage growth slowing to 3.1%. If

Norges Bank concurs, the market's interest rate expectations will be realised.

However, Statistics Norway's projections assume that the slide in oil prices will hit

private consumption and the housing market via growing consumer pessimism. While

we cannot rule out such effects, we are not entirely convinced and we do not expect

the central bank to be either. Therefore, we expect Norges Bank to leave interest rates

unchanged and believe the interest rate path in the monetary policy report will include

a roughly 50/50 chance of a rate cut before next summer. This is based on the central

bank assuming GDP growth of around 1.75% and wage growth of around 3.25% in

2015.

Inflation expected to fall in November

Source: Statistics Denmark

Are Swedish labour markets losing

the ‘it’-factor?

Source: Statistics Sweden. Macrobond Financial

Market expecting big things

Source: Macrobond Financial, Bloomberg, Danske

Bank Markets

5 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Market movers ahead

Source: Bloomberg, Danske Bank Markets

Global movers Event Period Danske Consensus Previous

During the week Wed 10 - 15 CNY Aggregate Financing bn CNY Nov 875 890 662.7

Mon 08-Dec - CNY Trade balance USD bn Nov 46.4 44.0 45.4

0:50 JPY GDP, first revision q/q|ann. 3rd quarter -0.10%|… -0.10%|-0.50% -0.40%|-1.60%

8:00 DEM Industrial production m/m|y/y Oct 0.4%|… 0.00%|0.20% 1.40%|-0.10%

Wed 10-Dec 2:30 CNY CPI y/y Nov 1.5% 1.60% 1.60%

Thurs 11-Dec 9:30 CHF Centralbank - press briefing 0 0

11:10 EUR ECB's TLTRO allotment Bn. 120

14:30 USD Retail Sales m/m Nov 0.10% 0.30% 0.30%

Fri 12-Dec 6:30 CNY Industrial production y/y Nov 7.4% 7.50% 7.70%

11:00 EUR Industrial production m/m|y/y Oct 0.1%|… 0.00%|… 0.60%|0.60%

15:55 USD University of Michigan Confidence, preliminary Index Dec 89.8 89.5 88.8

Scandi movers Event Period Danske Consensus Previous

Wed 10-Dec 9:00 DKK CPI m/m|y/y Nov -0.40%|0.30% 0.10%|0.50%

10:00 NOK Consumer prices m/m|y/y Nov 0.10%|2.00%

Thurs 11-Dec 9:30 SEK Unemployment s.a. % Nov 8.0% 8.10%

9:30 SEK Underlying inflation CPIF m/m|y/y Nov -0.10%|0.53% 0.10%|0.60%

11:00 NOK Norges Banks monetary policy meeting Dec

6 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Global Macro and Market Themes

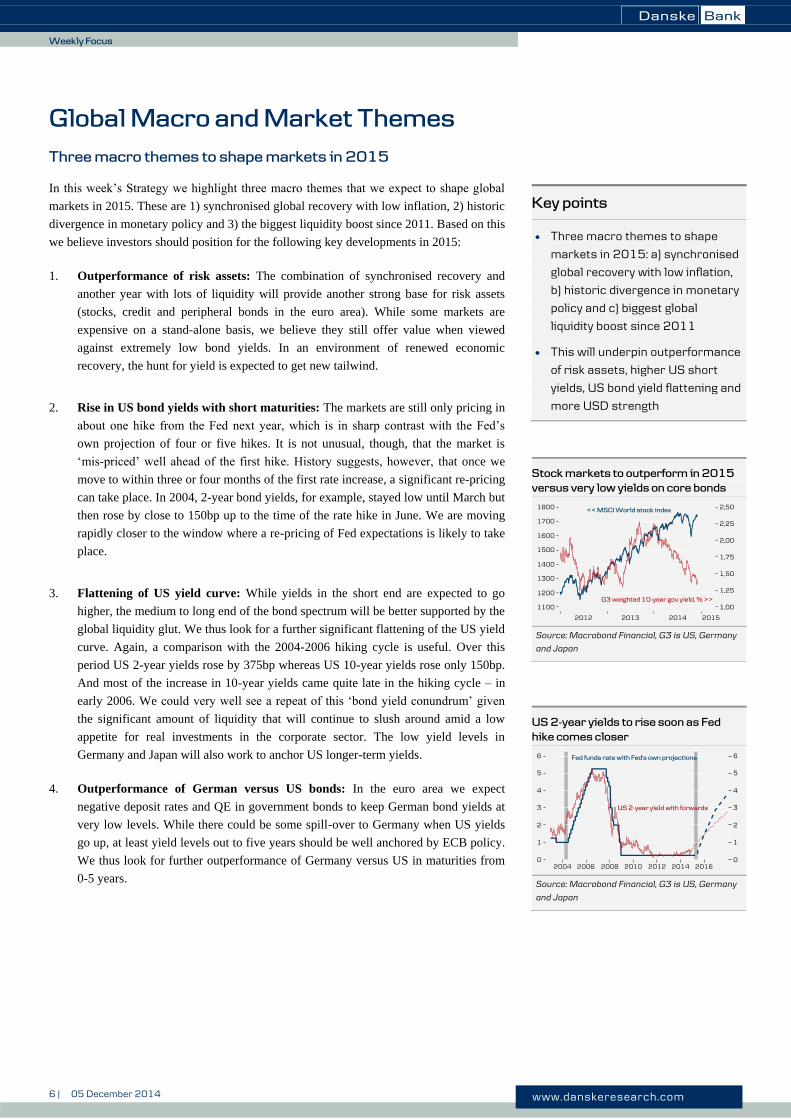

Three macro themes to shape markets in 2015

In this week’s Strategy we highlight three macro themes that we expect to shape global

markets in 2015. These are 1) synchronised global recovery with low inflation, 2) historic

divergence in monetary policy and 3) the biggest liquidity boost since 2011. Based on this

we believe investors should position for the following key developments in 2015:

1. Outperformance of risk assets: The combination of synchronised recovery and

another year with lots of liquidity will provide another strong base for risk assets

(stocks, credit and peripheral bonds in the euro area). While some markets are

expensive on a stand-alone basis, we believe they still offer value when viewed

against extremely low bond yields. In an environment of renewed economic

recovery, the hunt for yield is expected to get new tailwind.

2. Rise in US bond yields with short maturities: The markets are still only pricing in

about one hike from the Fed next year, which is in sharp contrast with the Fed’s

own projection of four or five hikes. It is not unusual, though, that the market is

‘mis-priced’ well ahead of the first hike. History suggests, however, that once we

move to within three or four months of the first rate increase, a significant re-pricing

can take place. In 2004, 2-year bond yields, for example, stayed low until March but

then rose by close to 150bp up to the time of the rate hike in June. We are moving

rapidly closer to the window where a re-pricing of Fed expectations is likely to take

place.

3. Flattening of US yield curve: While yields in the short end are expected to go

higher, the medium to long end of the bond spectrum will be better supported by the

global liquidity glut. We thus look for a further significant flattening of the US yield

curve. Again, a comparison with the 2004-2006 hiking cycle is useful. Over this

period US 2-year yields rose by 375bp whereas US 10-year yields rose only 150bp.

And most of the increase in 10-year yields came quite late in the hiking cycle – in

early 2006. We could very well see a repeat of this ‘bond yield conundrum’ given

the significant amount of liquidity that will continue to slush around amid a low

appetite for real investments in the corporate sector. The low yield levels in

Germany and Japan will also work to anchor US longer-term yields.

4. Outperformance of German versus US bonds: In the euro area we expect

negative deposit rates and QE in government bonds to keep German bond yields at

very low levels. While there could be some spill-over to Germany when US yields

go up, at least yield levels out to five years should be well anchored by ECB policy.

We thus look for further outperformance of Germany versus US in maturities from

0-5 years.

Key points

Three macro themes to shape

markets in 2015: a) synchronised

global recovery with low inflation,

b) historic divergence in monetary

policy and c) biggest global

liquidity boost since 2011

This will underpin outperformance

of risk assets, higher US short

yields, US bond yield flattening and

more USD strength

Stock markets to outperform in 2015

versus very low yields on core bonds

Source: Macrobond Financial, G3 is US, Germany

and Japan

US 2-year yields to rise soon as Fed

hike comes closer

Source: Macrobond Financial, G3 is US, Germany

and Japan

7 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

5. Lower EUR/USD and higher USD/JPY: The strong divergence of monetary

policy will lead to more USD strength. As the Fed hikes and ECB eases further and

Bank of Japan keeps pumping significant amounts of money out, we should see a

further decline in EUR/USD and a higher USD/JPY in the first half of the year.

Over the summer we expect to see a peak in USD strength as Fed hikes will be

priced by then, but for the coming six months, a re-pricing of Fed policy is expected

to underpin more appreciation of the USD.

These are the main trends we believe investors should position for. Below we give a little

more colour on the macro themes behind these financial expectations.

Macro theme #1: Synchronised recovery with low inflation

Following a year of very divergent growth across regions we expect to see a synchronised

recovery among the big regions during H1 2015, see also The Big Picture: Synchronised

recovery in H1 15, 1 December 2014.

In the US, the underlying economic momentum is improving underneath the current

slight moderation. The job market is strong, wealth increases have been significant and

recently a sharp decline in oil prices has been giving a strong boost to consumers. On top

of this, the fiscal drag has eased markedly and profit growth is robust. The main

headwind currently is a stronger USD but this is not enough to stop the US economy. The

US is probably heading for its strongest year since 2005, with growth just above 3%.

In the euro area, we believe the cycle is bottoming and look for gradual

improvement in growth and business surveys over the coming quarters. We see

evidence that the Ukraine crisis has been the main culprit behind this year’s slowdown.

The effects of this shock are expected to gradually fade. At the same time, new tailwinds

will gradually kick in: a sharp weakening of the euro, the big decline in oil prices and

significant easing of both monetary and fiscal policy. The EU investment plan could give

a lift to GDP of approximately 0.3-0.4% over the coming years according to the EU

Commission. Easing lending standards should also start to support credit availability next

year.

The last major engine in the world economy, China, is also expected to see some

improvement. Growth has slowed over the past quarters but the People’s Bank of China

has shown a determination to lift growth by cutting rates and, with inflation clearly below

the target, we believe it can ease enough to get growth back on the 7½% growth path that

the government is targeting.

Finally, Japan is recovering from the sharp slowdown following the VAT hike in

April. Industrial production and retail sales have already recovered and we expect

continued moderate improvement over the coming year.

While growth is picking up, inflation is bound to go lower in coming quarters. The

sharp decline in oil prices will push inflation down in the short term and there is a not

insignificant likelihood that we will see the first negative print in the euro area since the

aftermath of the financial crisis in 2009. While the decline in oil prices is positive for

growth, it will make the ECB’s job harder as the risk of inflation getting stuck far below

their ‘close to 2%’ inflation target is going up.

G3 growth to recover, PMI’s to move

higher in H1

Source: Macrobond Financial

Euro area bottoming

Source: Macrobond Financial

Euro inflation balancing around zero in

coming months

Source: Macrobond Financial

More USD strength expected in 2015

Source: Macrobond Financial

8 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Macro theme #2: Historic divergence in monetary policy

2015 will likely be a historic year from a monetary policy point of view. The Fed is

well on track to reach ‘lift-off’ on rates in June while the ECB will need to grab for

more tools to get the desired easing of monetary policy. The usual pattern of the ECB

raising rates around 6-9 months after the Fed is not going to happen this time. Instead the

two central banks will be moving in opposite directions over the coming one or two years.

The Fed is projecting that it will raise rates by 250bp over the next two years, whereas the

ECB in the same period will keep rates unchanged and aim for an increase in the balance

sheet of EUR1trn.

The difference was also highlighted this week with differing central bank communication

across the Atlantic. ECB president Mario Draghi focused on the inflation impact of

the lower oil prices and said that the ECB would evaluate whether further stimulus

measures are needed in early Q1. We look for the ECB to introduce purchases of

corporate bonds in January and sovereign bonds in Q2, Flash Comment: Euro – Draghi

hinted at more easing in January, 4 December 2014.

On the other hand vice chairman of the Fed Bill Dudley (dove, voter) on Tuesday

emphasised the positive effects on growth of the lower oil prices and played down the

risk of sustained lower inflation. He also expressed more confidence that US growth

would finally be able to sustain a stronger performance in contrast to previous years

where hopes of growth breaking out were subsequently dashed. He also repeated that he

agrees with the general expectation of lift-off in mid-2015.

The difference between the Fed and ECB makes sense from an economic point of

view: In the US the output gap is about to close over the next one to two years whereas

the euro area still has a very high output gap, probably around 4-5%. Inflation is on track

to reach the Fed’s 2% goal over the next 1-1½ years, whereas euro area inflation may go

into negative territory in the coming months.

Japan is really a special case, experimenting with a much more aggressive style of

economic policy. It is the only country where the output gap is pretty much closed and

inflation around 1% is between the level of the US and the euro area. Yet Bank of Japan

is the central bank adding the most stimulus, with net asset purchases corresponding to

16% of GDP.

Macro theme #3: The biggest liquidity boost since 2011

With massive asset purchases from Bank of Japan and new measures from the ECB

during 2015, this will be another year of massive liquidity boost to the financial system.

In fact it is likely to be the biggest increase since 2011, although it depends on how fast

the ECB moves to reach its soft target of increasing the balance sheet by EUR1trn. But if

the ECB manages to increase the balance sheet in 2015 by a little over half of that, we

could get a global liquidity boost of USD1.5trn, since the Bank of Japan is scheduled to

increase the balance sheet by what corresponds to USD700bn.

This time it’s different

Source: Macrobond Financial

Solid outlook for US growth – 2015 to

be strongest year since 2005

Source: Macrobond Financial

Global liquidity to get big boost in 2015

Source: Macrobond Financial

9 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

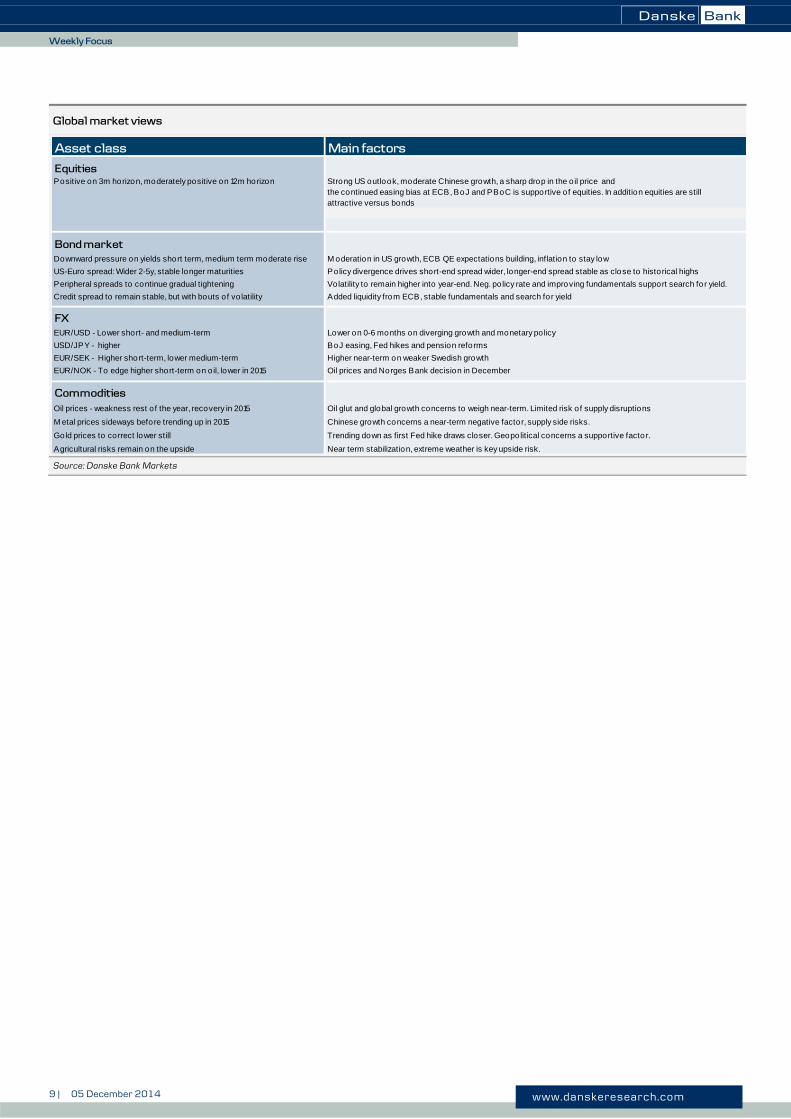

Global market views

Source: Danske Bank Markets

Asset class Main factors

Equities

Positive on 3m horizon, moderately positive on 12m horizon Strong US outlook, moderate Chinese growth, a sharp drop in the o il price and

the continued easing bias at ECB, BoJ and PBoC is supportive of equities. In addition equities are still

attractive versus bonds

Bond market

Downward pressure on yields short term, medium term moderate rise M oderation in US growth, ECB QE expectations building, inflation to stay low

US-Euro spread: Wider 2-5y, stable longer maturities Policy divergence drives short-end spread wider, longer-end spread stable as close to historical highs

Peripheral spreads to continue gradual tightening Volatility to remain higher into year-end. Neg. policy rate and improving fundamentals support search for yield.

Credit spread to remain stable, but with bouts of vo latility Added liquidity from ECB, stable fundamentals and search for yield

FX

EUR/USD - Lower short- and medium-term Lower on 0-6 months on diverging growth and monetary policy

USD/JPY - higher BoJ easing, Fed hikes and pension reforms

EUR/SEK - Higher short-term, lower medium-term Higher near-term on weaker Swedish growth

EUR/NOK - To edge higher short-term on o il, lower in 2015 Oil prices and Norges Bank decision in December

Commodities

Oil prices - weakness rest of the year, recovery in 2015 Oil glut and global growth concerns to weigh near-term. Limited risk of supply disruptions

M etal prices sideways before trending up in 2015 Chinese growth concerns a near-term negative factor, supply side risks.

Gold prices to correct lower still Trending down as first Fed hike draws closer. Geopolitical concerns a supportive factor.

Agricultural risks remain on the upside Near term stabilization, extreme weather is key upside risk.

10 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Scandi Update

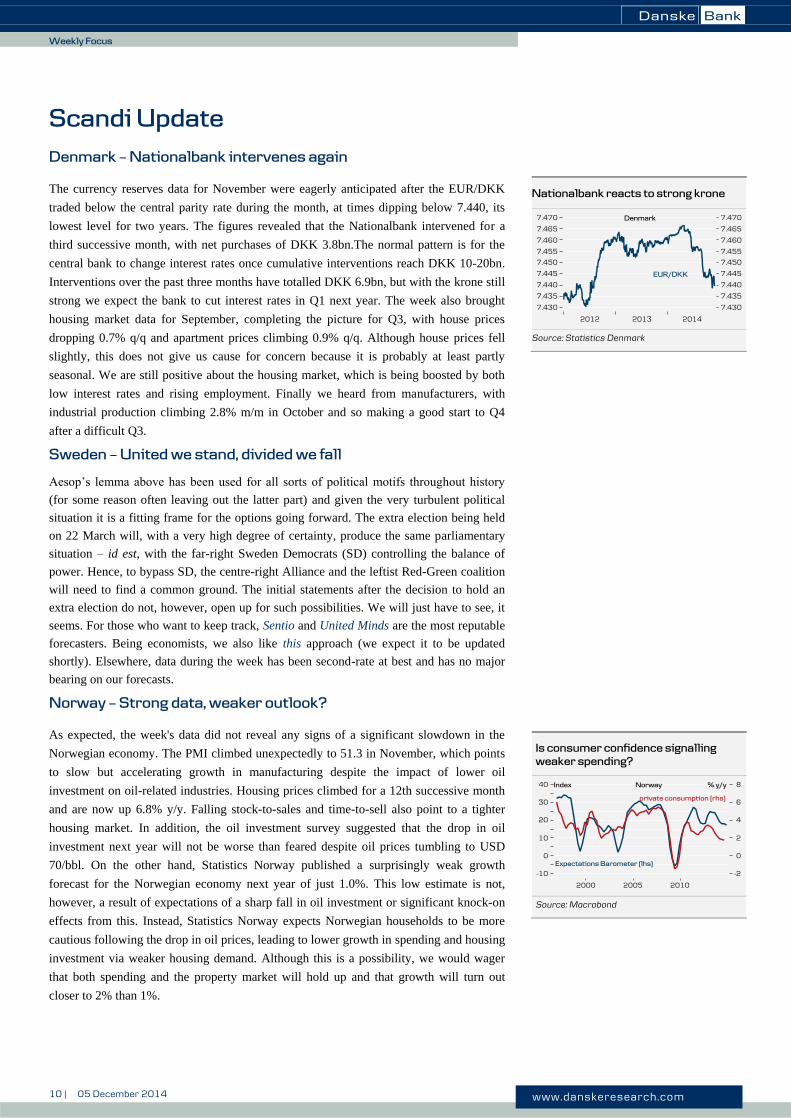

Denmark – Nationalbank intervenes again

The currency reserves data for November were eagerly anticipated after the EUR/DKK

traded below the central parity rate during the month, at times dipping below 7.440, its

lowest level for two years. The figures revealed that the Nationalbank intervened for a

third successive month, with net purchases of DKK 3.8bn.The normal pattern is for the

central bank to change interest rates once cumulative interventions reach DKK 10-20bn.

Interventions over the past three months have totalled DKK 6.9bn, but with the krone still

strong we expect the bank to cut interest rates in Q1 next year. The week also brought

housing market data for September, completing the picture for Q3, with house prices

dropping 0.7% q/q and apartment prices climbing 0.9% q/q. Although house prices fell

slightly, this does not give us cause for concern because it is probably at least partly

seasonal. We are still positive about the housing market, which is being boosted by both

low interest rates and rising employment. Finally we heard from manufacturers, with

industrial production climbing 2.8% m/m in October and so making a good start to Q4

after a difficult Q3.

Sweden – United we stand, divided we fall

Aesop’s lemma above has been used for all sorts of political motifs throughout history

(for some reason often leaving out the latter part) and given the very turbulent political

situation it is a fitting frame for the options going forward. The extra election being held

on 22 March will, with a very high degree of certainty, produce the same parliamentary

situation – id est, with the far-right Sweden Democrats (SD) controlling the balance of

power. Hence, to bypass SD, the centre-right Alliance and the leftist Red-Green coalition

will need to find a common ground. The initial statements after the decision to hold an

extra election do not, however, open up for such possibilities. We will just have to see, it

seems. For those who want to keep track, Sentio and United Minds are the most reputable

forecasters. Being economists, we also like this approach (we expect it to be updated

shortly). Elsewhere, data during the week has been second-rate at best and has no major

bearing on our forecasts.

Norway – Strong data, weaker outlook?

As expected, the week's data did not reveal any signs of a significant slowdown in the

Norwegian economy. The PMI climbed unexpectedly to 51.3 in November, which points

to slow but accelerating growth in manufacturing despite the impact of lower oil

investment on oil-related industries. Housing prices climbed for a 12th successive month

and are now up 6.8% y/y. Falling stock-to-sales and time-to-sell also point to a tighter

housing market. In addition, the oil investment survey suggested that the drop in oil

investment next year will not be worse than feared despite oil prices tumbling to USD

70/bbl. On the other hand, Statistics Norway published a surprisingly weak growth

forecast for the Norwegian economy next year of just 1.0%. This low estimate is not,

however, a result of expectations of a sharp fall in oil investment or significant knock-on

effects from this. Instead, Statistics Norway expects Norwegian households to be more

cautious following the drop in oil prices, leading to lower growth in spending and housing

investment via weaker housing demand. Although this is a possibility, we would wager

that both spending and the property market will hold up and that growth will turn out

closer to 2% than 1%.

Nationalbank reacts to strong krone

Source: Statistics Denmark

Is consumer confidence signalling

weaker spending?

Source: Macrobond

11 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Latest research from Danske Bank Markets

4/12 Flash Comment: Euro - Draghi hinted at more easing in January

Draghi had a dovish stance during the ECB's press conference, but from a market

perspective sweet talk was not enough.

3/12 Flash Comment - Higher euro retail sales in October, we look for further

improvements

Euro area retail sales increased 0.4% m/m in October after declining 1.2% m/m in

September. In yearly terms they were up 1.4% in October and have increased at around

that level since April.

3/12 Flash Comment - Sweden: Government crisis

The right-wing party Sweden Democrats announced that it will support the former

alliance government’s alternative budget bill, which effectively means that the present

government’s budget bill will be rejected.

3/12 Monitor - US Labour Market: improvement to continue

We expect nonfarm payrolls to gain 240,000 in November, which is a little above

consensus of 228,000. We expect the unemployment rate to be flat at 5.8% (same as

consensus).

1/12 Flash Comment US: ISM manufacturing remains too high

The US ISM manufacturing index surprised once again in November.

1/12 Flash Comment China: NBS manufacturing PMI declines more than expected in

November

China's official manufacturing PMI in November declined to 50.3 (consensus: 50.5,

DBM: 50.6) from 50.8 in October.

1/12 The Big Picture: Synchronous global recovery in H1 15

The Big Picture presents our view of the global economy and outlook for US, euro area,

Japan and China.

12 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

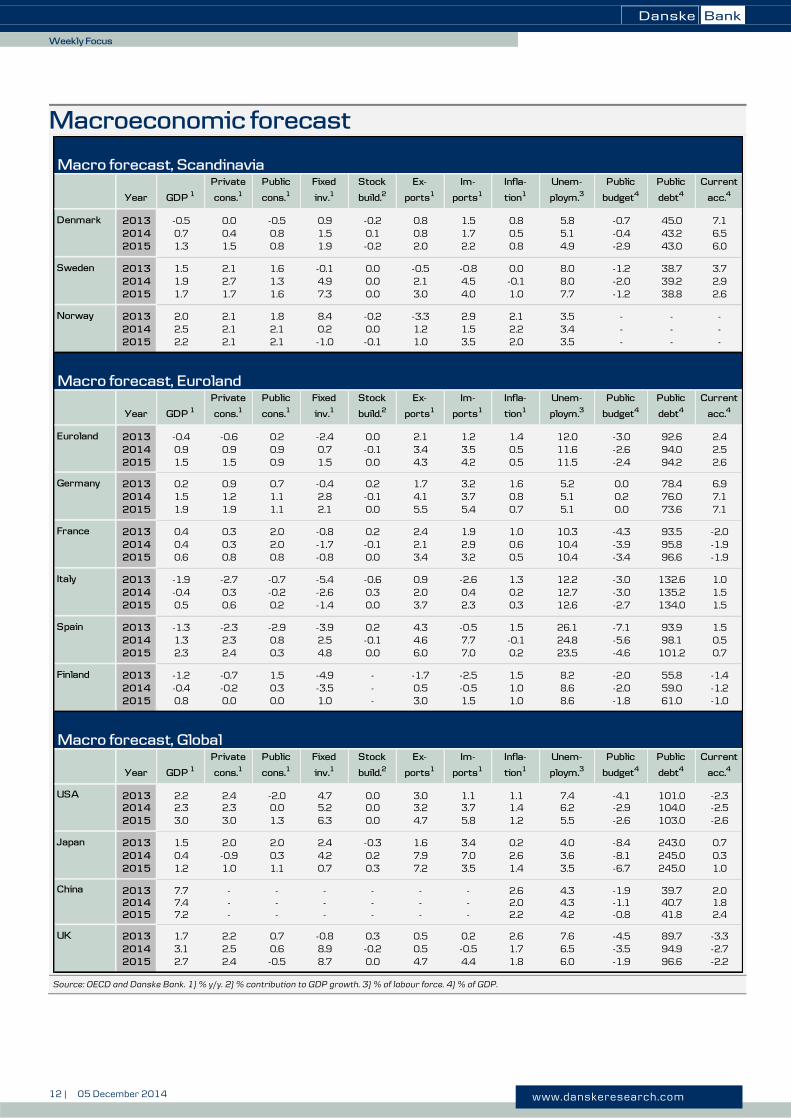

Macroeconomic forecast

Source: OECD and Danske Bank. 1) % y/y. 2) % contribution to GDP growth. 3) % of labour force. 4) % of GDP.

Macro forecast, Scandinavia

Denmark 2013 -0.5 0.0 -0.5 0.9 -0.2 0.8 1.5 0.8 5.8 -0.7 45.0 7.12014 0.7 0.4 0.8 1.5 0.1 0.8 1.7 0.5 5.1 -0.4 43.2 6.52015 1.3 1.5 0.8 1.9 -0.2 2.0 2.2 0.8 4.9 -2.9 43.0 6.0

Sweden 2013 1.5 2.1 1.6 -0.1 0.0 -0.5 -0.8 0.0 8.0 -1.2 38.7 3.72014 1.9 2.7 1.3 4.9 0.0 2.1 4.5 -0.1 8.0 -2.0 39.2 2.92015 1.7 1.7 1.6 7.3 0.0 3.0 4.0 1.0 7.7 -1.2 38.8 2.6

Norway 2013 2.0 2.1 1.8 8.4 -0.2 -3.3 2.9 2.1 3.5 - - -2014 2.5 2.1 2.1 0.2 0.0 1.2 1.5 2.2 3.4 - - -2015 2.2 2.1 2.1 -1.0 -0.1 1.0 3.5 2.0 3.5 - - -

Macro forecast, Euroland

Euroland 2013 -0.4 -0.6 0.2 -2.4 0.0 2.1 1.2 1.4 12.0 -3.0 92.6 2.42014 0.9 0.9 0.9 0.7 -0.1 3.4 3.5 0.5 11.6 -2.6 94.0 2.52015 1.5 1.5 0.9 1.5 0.0 4.3 4.2 0.5 11.5 -2.4 94.2 2.6

Germany 2013 0.2 0.9 0.7 -0.4 0.2 1.7 3.2 1.6 5.2 0.0 78.4 6.92014 1.5 1.2 1.1 2.8 -0.1 4.1 3.7 0.8 5.1 0.2 76.0 7.12015 1.9 1.9 1.1 2.1 0.0 5.5 5.4 0.7 5.1 0.0 73.6 7.1

France 2013 0.4 0.3 2.0 -0.8 0.2 2.4 1.9 1.0 10.3 -4.3 93.5 -2.02014 0.4 0.3 2.0 -1.7 -0.1 2.1 2.9 0.6 10.4 -3.9 95.8 -1.92015 0.6 0.8 0.8 -0.8 0.0 3.4 3.2 0.5 10.4 -3.4 96.6 -1.9

Italy 2013 -1.9 -2.7 -0.7 -5.4 -0.6 0.9 -2.6 1.3 12.2 -3.0 132.6 1.02014 -0.4 0.3 -0.2 -2.6 0.3 2.0 0.4 0.2 12.7 -3.0 135.2 1.52015 0.5 0.6 0.2 -1.4 0.0 3.7 2.3 0.3 12.6 -2.7 134.0 1.5

Spain 2013 -1.3 -2.3 -2.9 -3.9 0.2 4.3 -0.5 1.5 26.1 -7.1 93.9 1.52014 1.3 2.3 0.8 2.5 -0.1 4.6 7.7 -0.1 24.8 -5.6 98.1 0.52015 2.3 2.4 0.3 4.8 0.0 6.0 7.0 0.2 23.5 -4.6 101.2 0.7

Finland 2013 -1.2 -0.7 1.5 -4.9 - -1.7 -2.5 1.5 8.2 -2.0 55.8 -1.42014 -0.4 -0.2 0.3 -3.5 - 0.5 -0.5 1.0 8.6 -2.0 59.0 -1.22015 0.8 0.0 0.0 1.0 - 3.0 1.5 1.0 8.6 -1.8 61.0 -1.0

Macro forecast, Global

USA 2013 2.2 2.4 -2.0 4.7 0.0 3.0 1.1 1.1 7.4 -4.1 101.0 -2.32014 2.3 2.3 0.0 5.2 0.0 3.2 3.7 1.4 6.2 -2.9 104.0 -2.52015 3.0 3.0 1.3 6.3 0.0 4.7 5.8 1.2 5.5 -2.6 103.0 -2.6

Japan 2013 1.5 2.0 2.0 2.4 -0.3 1.6 3.4 0.2 4.0 -8.4 243.0 0.72014 0.4 -0.9 0.3 4.2 0.2 7.9 7.0 2.6 3.6 -8.1 245.0 0.32015 1.2 1.0 1.1 0.7 0.3 7.2 3.5 1.4 3.5 -6.7 245.0 1.0

China 2013 7.7 - - - - - - 2.6 4.3 -1.9 39.7 2.02014 7.4 - - - - - - 2.0 4.3 -1.1 40.7 1.82015 7.2 - - - - - - 2.2 4.2 -0.8 41.8 2.4

UK 2013 1.7 2.2 0.7 -0.8 0.3 0.5 0.2 2.6 7.6 -4.5 89.7 -3.32014 3.1 2.5 0.6 8.9 -0.2 0.5 -0.5 1.7 6.5 -3.5 94.9 -2.72015 2.7 2.4 -0.5 8.7 0.0 4.7 4.4 1.8 6.0 -1.9 96.6 -2.2

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Current

acc.4

Im-

ports1

Public

debt4

Public

budget4

Ex-

ports1

Infla-

tion1

Unem-

ploym.3

Ex-

ports1

Im-

ports1

Infla-

tion1

Unem-

ploym.3

Public

budget4

Current

acc.4

Public

debt4

Unem-

ploym.3

Public

budget4

Public

debt4

Year

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Current

acc.4

GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Ex-

ports1

Im-

ports1

Infla-

tion1

13 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

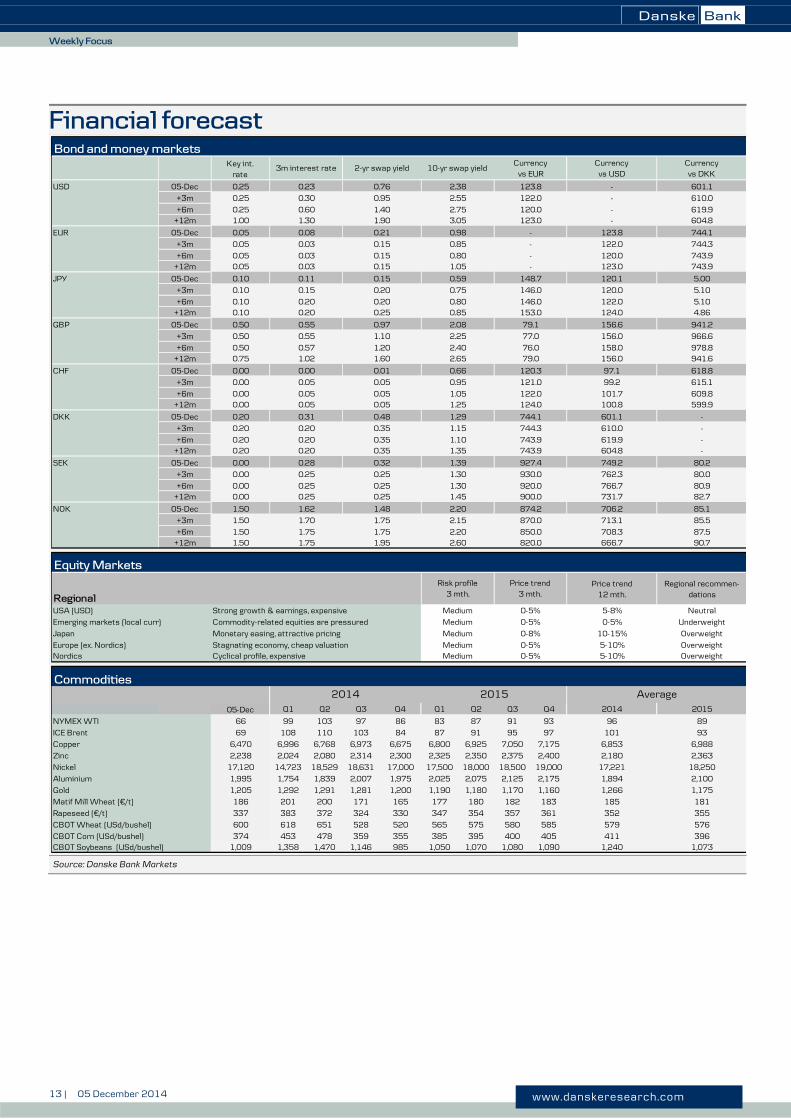

Financial forecast

Source: Danske Bank Markets

Bond and money markets

Currencyvs USD

Currencyvs DKK

USD 05-Dec - 601.1

+3m - 610.0

+6m - 619.9+12m - 604.8

EUR 05-Dec 123.8 744.1

+3m 122.0 744.3

+6m 120.0 743.9+12m 123.0 743.9

JPY 05-Dec 120.1 5.00

+3m 120.0 5.10

+6m 122.0 5.10+12m 124.0 4.86

GBP 05-Dec 156.6 941.2

+3m 156.0 966.6

+6m 158.0 978.8+12m 156.0 941.6

CHF 05-Dec 97.1 618.8

+3m 99.2 615.1

+6m 101.7 609.8+12m 100.8 599.9

DKK 05-Dec 601.1 -

+3m 610.0 -

+6m 619.9 -+12m 604.8 -

SEK 05-Dec 749.2 80.2

+3m 762.3 80.0

+6m 766.7 80.9+12m 731.7 82.7

NOK 05-Dec 706.2 85.1

+3m 713.1 85.5

+6m 708.3 87.5+12m 666.7 90.7

Equity Markets

Regional

Price trend12 mth.

Regional recommen-dations

USA (USD) Strong growth & earnings, expensive 5-8% Neutral

Emerging markets (local curr) Commodity-related equities are pressured 0-5% Underweight

Japan Monetary easing, attractive pricing 10-15% Overweight

Europe (ex. Nordics) Stagnating economy, cheap valuation 5-10% OverweightNordics Cyclical profile, expensive 5-10% Overweight

Commodities

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2014 2015

NYMEX WTI 99 103 97 86 83 87 91 93 96 89

ICE Brent 108 110 103 84 87 91 95 97 101 93

Copper 6,996 6,768 6,973 6,675 6,800 6,925 7,050 7,175 6,853 6,988

Zinc 2,024 2,080 2,314 2,300 2,325 2,350 2,375 2,400 2,180 2,363

Nickel 14,723 18,529 18,631 17,000 17,500 18,000 18,500 19,000 17,221 18,250

Aluminium 1,754 1,839 2,007 1,975 2,025 2,075 2,125 2,175 1,894 2,100

Gold 1,292 1,291 1,281 1,200 1,190 1,180 1,170 1,160 1,266 1,175

Matif Mill Wheat (€/t) 201 200 171 165 177 180 182 183 185 181

Rapeseed (€/t) 383 372 324 330 347 354 357 361 352 355

CBOT Wheat (USd/bushel) 618 651 528 520 565 575 580 585 579 576

CBOT Corn (USd/bushel) 453 478 359 355 385 395 400 405 411 396CBOT Soybeans (USd/bushel) 1,358 1,470 1,146 985 1,050 1,070 1,080 1,090 1,240 1,073

337

Average

Key int.rate

0.25

0.25

0.251.00

1.50

0.00

0.05

0.05

0.100.10

0.50

10-yr swap yield

0.28

0.20

0.200.20

3m interest rate

1.75

0.05

0.10

0.50

0.00

0.20

0.03

0.55

0.571.02

0.000.00

0.05

0.50

0.25

0.00

0.10

0.31

0.05

0.75

0.050.05

0.20

0.20

0.20

0.25

0.25

1.50

0.00

0.000.00

1.50

1.50

1.70

1.75

0.23

0.08

0.11

0.55

0.00

0.30

0.601.30

0.03

0.03

0.20

0.15

0.20

1.75

1.75

0.25

1.95

0.25

1.481.62

0.35

0.350.35

0.05

0.050.05

0.32

0.25

1.401.90

1.10

1.201.60

0.20

0.200.25

123.8

-

-

--

148.7

744.3

743.9743.9

927.4

874.2

820.0

930.0

850.0

920.0900.0

870.0

120.3

744.1

77.0

79.0

121.0

122.0124.0

122.0

120.0123.0

146.0

146.0153.0

Currencyvs EUR

2-yr swap yield

Risk profile3 mth.

Price trend3 mth.

2.55

2.38

2.75

0.76

0.21

0.15

0.97

0.01

0.48

0.15

0.150.15

0.95

79.1

3.05

76.0

374

05-Dec

66

17,120

6,470

2,238

1,205

186

69

1,995

20152014

0.85

0.801.05

0.75

0.800.85

2.08

2.25

0.59

Medium 0-5%

1,009

600

0.98

1.301.45

2.20

2.15

2.20

2.402.65

0.66

0.95

1.051.25

2.60

1.101.35

1.15

1.39

1.30

1.29

Medium

Medium

Medium 0-8%

Medium 0-5%

0-5%

0-5%

14 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

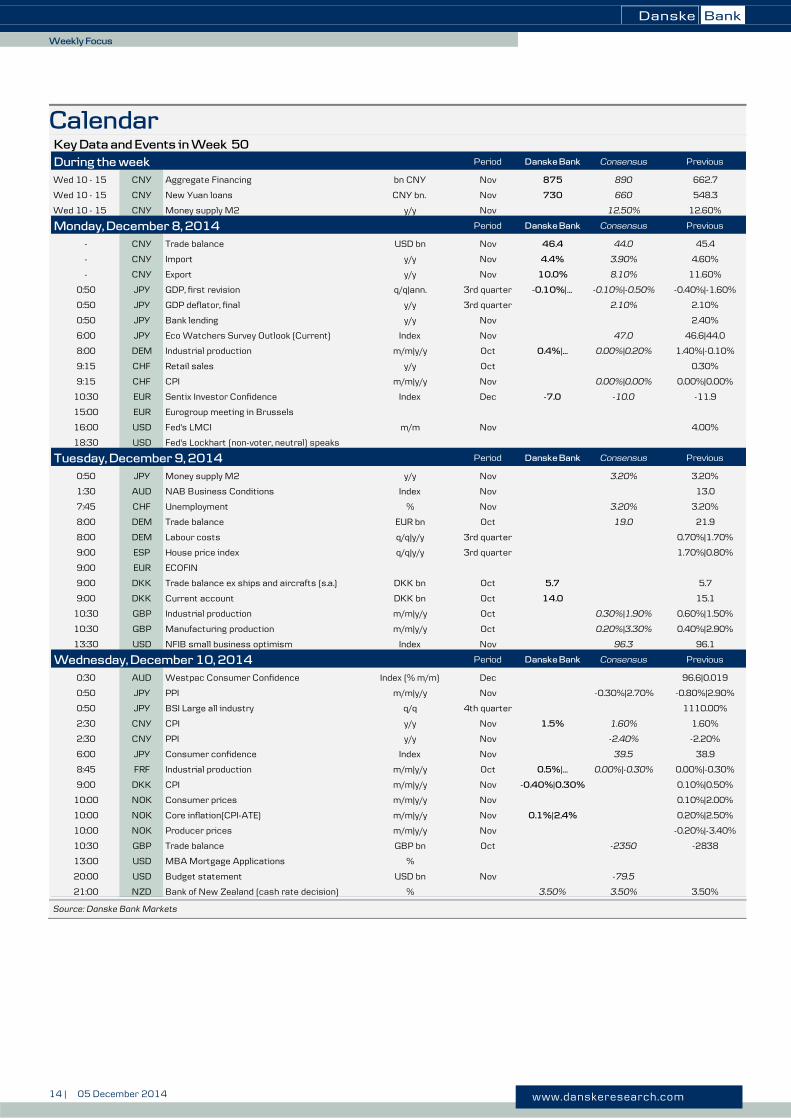

Calendar

Source: Danske Bank Markets

Key Data and Events in Week 50

During the week Period Danske Bank Consensus Previous

Wed 10 - 15 CNY Aggregate Financing bn CNY Nov 875 890 662.7

Wed 10 - 15 CNY New Yuan loans CNY bn. Nov 730 660 548.3

Wed 10 - 15 CNY Money supply M2 y/y Nov 12.50% 12.60%

Monday, December 8, 2014 Period Danske Bank Consensus Previous

- CNY Trade balance USD bn Nov 46.4 44.0 45.4

- CNY Import y/y Nov 4.4% 3.90% 4.60%

- CNY Export y/y Nov 10.0% 8.10% 11.60%

0:50 JPY GDP, first revision q/q|ann. 3rd quarter -0.10%|… -0.10%|-0.50% -0.40%|-1.60%

0:50 JPY GDP deflator, final y/y 3rd quarter 2.10% 2.10%

0:50 JPY Bank lending y/y Nov 2.40%

6:00 JPY Eco Watchers Survey Outlook (Current) Index Nov 47.0 46.6|44.0

8:00 DEM Industrial production m/m|y/y Oct 0.4%|… 0.00%|0.20% 1.40%|-0.10%

9:15 CHF Retail sales y/y Oct 0.30%

9:15 CHF CPI m/m|y/y Nov 0.00%|0.00% 0.00%|0.00%

10:30 EUR Sentix Investor Confidence Index Dec -7.0 -10.0 -11.9

15:00 EUR Eurogroup meeting in Brussels

16:00 USD Fed's LMCI m/m Nov 4.00%

18:30 USD Fed's Lockhart (non-voter, neutral) speaks

Tuesday, December 9, 2014 Period Danske Bank Consensus Previous

0:50 JPY Money supply M2 y/y Nov 3.20% 3.20%

1:30 AUD NAB Business Conditions Index Nov 13.0

7:45 CHF Unemployment % Nov 3.20% 3.20%

8:00 DEM Trade balance EUR bn Oct 19.0 21.9

8:00 DEM Labour costs q/q|y/y 3rd quarter 0.70%|1.70%

9:00 ESP House price index q/q|y/y 3rd quarter 1.70%|0.80%

9:00 EUR ECOFIN

9:00 DKK Trade balance ex ships and aircrafts (s.a.) DKK bn Oct 5.7 5.7

9:00 DKK Current account DKK bn Oct 14.0 15.1

10:30 GBP Industrial production m/m|y/y Oct 0.30%|1.90% 0.60%|1.50%

10:30 GBP Manufacturing production m/m|y/y Oct 0.20%|3.30% 0.40%|2.90%

13:30 USD NFIB small business optimism Index Nov 96.3 96.1

Wednesday, December 10, 2014 Period Danske Bank Consensus Previous

0:30 AUD Westpac Consumer Confidence Index (% m/m) Dec 96.6|0.019

0:50 JPY PPI m/m|y/y Nov -0.30%|2.70% -0.80%|2.90%

0:50 JPY BSI Large all industry q/q 4th quarter 1110.00%

2:30 CNY CPI y/y Nov 1.5% 1.60% 1.60%

2:30 CNY PPI y/y Nov -2.40% -2.20%

6:00 JPY Consumer confidence Index Nov 39.5 38.9

8:45 FRF Industrial production m/m|y/y Oct 0.5%|… 0.00%|-0.30% 0.00%|-0.30%

9:00 DKK CPI m/m|y/y Nov -0.40%|0.30% 0.10%|0.50%

10:00 NOK Consumer prices m/m|y/y Nov 0.10%|2.00%

10:00 NOK Core inflation(CPI-ATE) m/m|y/y Nov 0.1%|2.4% 0.20%|2.50%

10:00 NOK Producer prices m/m|y/y Nov -0.20%|-3.40%

10:30 GBP Trade balance GBP bn Oct -2350 -2838

13:00 USD MBA Mortgage Applications %

20:00 USD Budget statement USD bn Nov -79.5

21:00 NZD Bank of New Zealand (cash rate decision) % 3.50% 3.50% 3.50%

15 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

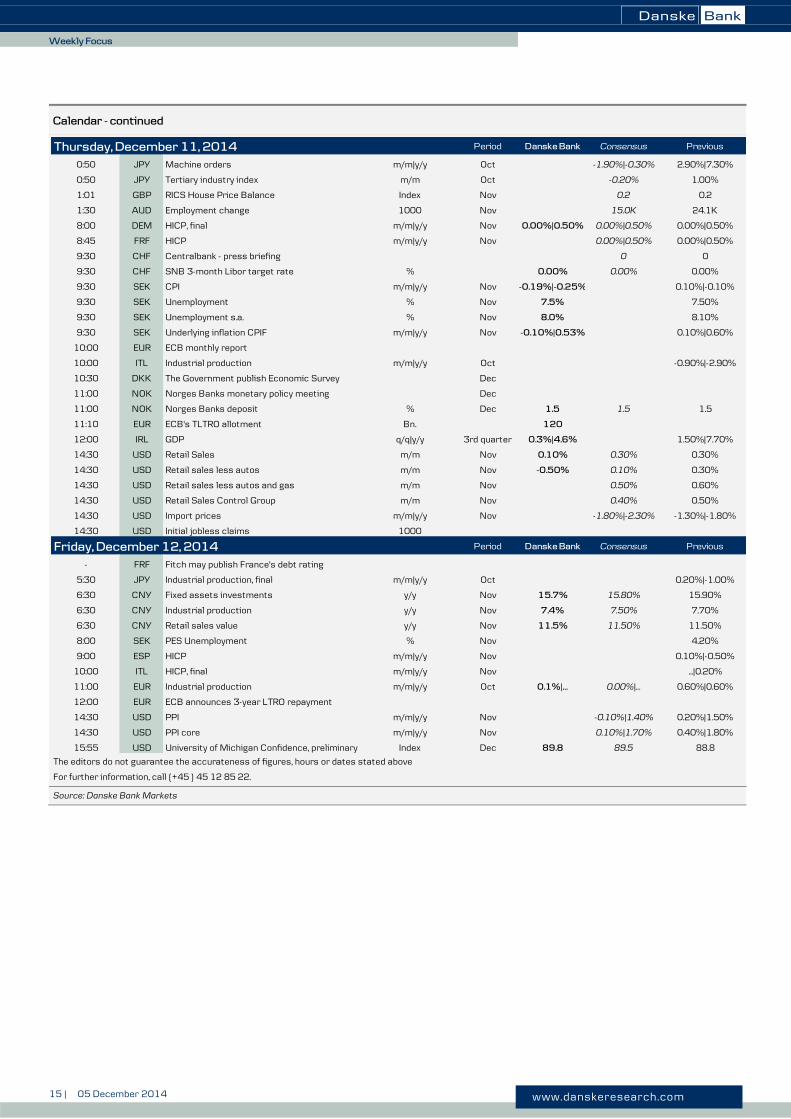

Calendar - continued

Source: Danske Bank Markets

Thursday, December 11, 2014 Period Danske Bank Consensus Previous

0:50 JPY Machine orders m/m|y/y Oct -1.90%|-0.30% 2.90%|7.30%

0:50 JPY Tertiary industry index m/m Oct -0.20% 1.00%

1:01 GBP RICS House Price Balance Index Nov 0.2 0.2

1:30 AUD Employment change 1000 Nov 15.0K 24.1K

8:00 DEM HICP, final m/m|y/y Nov 0.00%|0.50% 0.00%|0.50% 0.00%|0.50%

8:45 FRF HICP m/m|y/y Nov 0.00%|0.50% 0.00%|0.50%

9:30 CHF Centralbank - press briefing 0 0

9:30 CHF SNB 3-month Libor target rate % 0.00% 0.00% 0.00%

9:30 SEK CPI m/m|y/y Nov -0.19%|-0.25% 0.10%|-0.10%

9:30 SEK Unemployment % Nov 7.5% 7.50%

9:30 SEK Unemployment s.a. % Nov 8.0% 8.10%

9:30 SEK Underlying inflation CPIF m/m|y/y Nov -0.10%|0.53% 0.10%|0.60%

10:00 EUR ECB monthly report

10:00 ITL Industrial production m/m|y/y Oct -0.90%|-2.90%

10:30 DKK The Government publish Economic Survey Dec

11:00 NOK Norges Banks monetary policy meeting Dec

11:00 NOK Norges Banks deposit % Dec 1.5 1.5 1.5

11:10 EUR ECB's TLTRO allotment Bn. 120

12:00 IRL GDP q/q|y/y 3rd quarter 0.3%|4.6% 1.50%|7.70%

14:30 USD Retail Sales m/m Nov 0.10% 0.30% 0.30%

14:30 USD Retail sales less autos m/m Nov -0.50% 0.10% 0.30%

14:30 USD Retail sales less autos and gas m/m Nov 0.50% 0.60%

14:30 USD Retail Sales Control Group m/m Nov 0.40% 0.50%

14:30 USD Import prices m/m|y/y Nov -1.80%|-2.30% -1.30%|-1.80%

14:30 USD Initial jobless claims 1000

Friday, December 12, 2014 Period Danske Bank Consensus Previous

- FRF Fitch may publish France's debt rating

5:30 JPY Industrial production, final m/m|y/y Oct 0.20%|-1.00%

6:30 CNY Fixed assets investments y/y Nov 15.7% 15.80% 15.90%

6:30 CNY Industrial production y/y Nov 7.4% 7.50% 7.70%

6:30 CNY Retail sales value y/y Nov 11.5% 11.50% 11.50%

8:00 SEK PES Unemployment % Nov 4.20%

9:00 ESP HICP m/m|y/y Nov 0.10%|-0.50%

10:00 ITL HICP, final m/m|y/y Nov ...|0.20%

11:00 EUR Industrial production m/m|y/y Oct 0.1%|… 0.00%|… 0.60%|0.60%

12:00 EUR ECB announces 3-year LTRO repayment

14:30 USD PPI m/m|y/y Nov -0.10%|1.40% 0.20%|1.50%

14:30 USD PPI core m/m|y/y Nov 0.10%|1.70% 0.40%|1.80%

15:55 USD University of Michigan Confidence, preliminary Index Dec 89.8 89.5 88.8

The editors do not guarantee the accurateness of figures, hours or dates stated above

For further information, call (+45 ) 45 12 85 22.

16 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Disclosure This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The authors of the research report are Allan von Mehren, Chief Analyst and Steen Bocian, Chief

Economist.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in this

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis

of relevant assumptions, are stated throughout the text.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change and Danske Bank does not

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

17 | 05 December 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.

Disclaimer related to distribution in the United States

This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer

and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S.

Securities and Exchange Commission. The research report is intended for distribution in the United States solely

to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this

research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence

of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are

not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements

of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial

Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-

U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be

registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and

auditing standards of the U.S. Securities and Exchange Commission.