Embed Size (px)

Citation preview

Investment Opportunity Assessment for Timor-Leste

May 2005

This publication was produced by Nathan Associates Inc. for review by the United States Agency

for International Development.

Contents

Executive Summary v

1. Introduction 1

2. General and Economic Context 5

Economic Structure 5

Investment Trends 8

Foreign Investment 10

Business Environment Framework 12

3. Foreign Direct Investment Trends and Motives 15

Rise of China 15

Move to Services 16

Sources of FDI 17

FDI Motivations and Implications for Timor-Leste 18

4. Comparative and Competitive Advantages 23

5. Potential of Economic Sectors 29

Employment by Sector 29

GDP and Exports by Sector 30

Sector Investment Opportunities 31

Investment Impact by Location 35

Conclusion 36

6. Domestic and Foreign Direct Investment 39

International Experience with Linkages and Spillovers 40

II

Present and Potential Linkages and Spillovers in Timor-Leste 42

Conclusion 45

7. Investment Challenges 47

Regulatory Environment 47

Infrastructure, Utility Provision, and Zones 49

Public–private Dialogue and Business Associations 51

Trade Policy 52

Skill Development and Domestic Businesses 52

Investment Promotion and the IEPA 53

Regional Competitors 54

Investment Targets 55

8. Recommendations and Next Steps 57

9. Current Investment Opportunities 61

Agriculture, Agro-Industry, and Agribusiness 61

Livestock 63

Forestry 64

Fisheries and Aquaculture 64

Tourism 64

Light Manufacturing 66

Food Processing 67

Oil and Gas 67

Financial and Business Services 68

Other Services 69

Economic Infrastructure 69

Appendix A. Terms of Reference

Appendix B. Persons Interviewed

Appendix C. Investment Law Provisions

Appendix D. Investment Incentives in Selected Southeast Asian Countries

Appendix E. SWOT Analysis of Timor-Leste

III

ILLUSTRATIONS

Figures

Figure 2-1. Outstanding Credit of Commercial Banks to Private Enterprises 10 Figure 3-1. FDI Inflows, Developed and Developing Countries, 1990-2003 16

Tables

Table 2-1. GDP by Economic Sector, 2003 6 Table 2-2. Timor-Leste’s Top 10 Countries of Import, 2003 7 Table 2-3. Imports by Product Category, 2003 7 Table 2-4. Timor-Leste’s Top Seven Export Markets, 2003 8 Table 2-5. Trends in Public and Private Value Added and Investment, 2000-2003 9 Table 2-6. Number of Business Licenses Issued and Renewed 11 Table 3-1. Outflows of FDI from Select Countries 18 Table 3-2. Foreign Direct Investment Motives and Host-country Attributes 20 Table 5-1. Sectors and Possible Locations in Timor-Leste 36 Table 7-1. Countries Competing for FDI in the Southeast Asia and Pacific Regions 54

Exhibits

Exhibit 2-1. Laws and Incentives Creating a Favorable Investment Environment 13 Exhibit 4-1. Summary of Workshop Opinions on Timor-Leste’s Strengths, Weaknesses,

Opportunities, and Threats 24

Executive Summary How can Timor-Leste create new and sustainable employment and reduce poverty? The

young country has one of the highest poverty rates in the world—estimated at more than

40 percent. About 20 percent of the labor force is unemployed; and in urban areas, about 40 percent of young people are unemployed. Each year, another 15,000 people enter the

labor force. About two-thirds of the employed work in the agricultural sector and mainly

at a subsistence level. In urban areas, the Government of Timor-Leste is the major employer. Total foreign direct investment (FDI) in Timor-Leste is about $1.75 billion,

nearly all in the capital-intensive oil and gas sector and creating few jobs onshore.

In addition, Timor-Leste’s economy has been in transition since the country broke from Indonesia in 1999. GDP was $270.1 million that year, then rose steadily to peak at $380.7

million in 2002, largely because of a “dollar bubble” created by the presence of the United

Nations and a large military contingent. With the drastic reduction of that presence, GDP for 2003 fell 3 percent from the 2002 peak. The national budget estimates a further

decrease of 1 percent for 2004, though some believe the decrease to be as much as 3

percent. Timor-Leste is also an import economy with major trade imbalances. Trade data

for 2003 show that the paltry $7 in export earnings barely covered 3 percent of that year’s

imports of $230 million. Oil and gas revenues are expected to correct the trade balance by

2006—and to boost GDP in 2004-2005. Imports will likely dominate non-petroleum trade for some time and non-petroleum contribution to GDP is likely to remain negative until

2006, when new laws are expected to stimulate domestic investment and attract foreign

direct investment. Although the Sector Investment Program (SIP) estimates average economic growth of 1.7 percent between 2003–2007, performance so far suggests that non-

oil real growth is likely to be negative.

The Government of Timor-Leste clearly faces major challenges in generating sustainable employment. But no government can create the number of jobs required to meet labor

market demands without a vibrant private sector nourished by domestic and foreign

investment. To stimulate investment as the source of growth, the government needs to create an enabling environment for the private sector. The government has already taken

some pro-investment steps: passing investment laws with incentives linked to business

inputs and job creation; building the capacity of investment promotion agencies; and

adopting “one-stop-shop” investment licensing to simplify decision-making. Still,

VI

optimism regarding Timor-Leste’s investment opportunities is guarded because of

numerous constraints: poor economic infrastructure, low worker skills, low labor productivity, relatively high wages, small population, a small market, and stiff

competition from neighboring countries that are aggressively improving their business

environments.

To attract and retain more FDI, Timor-Leste must prepare itself to compete with its

neighbors. Here, the country enjoys some advantages that will enable it to position itself

favorably as an FDI destination: oil, gas, and mineral resources; arable land; natural beauty and rich cultural traditions; good investment incentives; and a simple, transparent

investment regime superior to competing countries. Because of its small internal market,

high production costs, and low labor productivity, Timor-Leste will have to produce for the export market. Competing in that market will be daunting. Timor-Leste must adopt a

strategy that takes into account its limitations as well as its strengths. The country lacks

sufficient comparative advantages to compete on price. Instead, a competitive advantage model based on strategic positioning of products in niche markets, a model successfully

adopted for the country’s organic coffee, is recommended.

Promoting, attracting, and realizing investment poses a broad agenda, especially for Timor-Leste, which needs to develop skills, policies, infrastructure, sector strategies,

business associations, and skills. Campaigns to attract foreign investment should target

high–potential markets in countries whose investors have already expressed strong interest in Timor-Leste: Australia, Malaysia, Singapore, Thailand, Macau, Hong Kong,

and Portugal. Synergies between foreign and domestic investors will multiply the benefits

of targeted investment promotion. Timor-Leste’s potential for linkages and spillovers,

especially in agribusiness and tourism, is substantial, and can be best realized through

sector development strategies. Once sector strategies are underway the government can

promote skill development. Institutions that combine business management and technical training are needed to supplement the Business Development Center program. Strong

business associations and public-private dialogue will be crucial. The IEPA and ADE can

foster a collaborative spirit to ensure that synergies between FDI and domestic investment occur. Branding strategies implemented with sector strategies and investments will have

significant spillover effects on domestic businesses. The success of these efforts will

depend on investments in economic infrastructure (public or private): power, communications, ICT.

In sum, we recommend that the Government of Timor-Leste, the IEPA, and private sector

leaders undertake the following steps to promote, attract, and realize investment in Timor-Leste:

• Develop strategic business plans

• Create sector strategies and working groups • Provide training in administrative procedures

• Pursue sector-driven private-sector training and capacity building, especially for

tourism and agribusiness

VII

• Improve the business environment

• Build transport and energy infrastructure • Improve telecommunications infrastructure and reduce communication costs

• Reduce air transport costs.

Though only three years old, Timor-Leste has a considerable stock of FDI (US$ 1.75 billion), making it the envy of many similar countries, some of which have been

promoting investment for decades. But this impressive stock is in non-renewable

resources, a sector characterized by capital-intensive equipment and low employment. To achieve sustainable development, Timor-Leste must invest the income from its non-

renewable resources in its people and infrastructure while promoting investment in other

sectors.

1. Introduction On May 20, 2002, Timor-Leste regained its independence after nearly a quarter-century under Indonesia occupation. During that time it was considered one of the poorest areas in Indonesia. In 1996, half of its population lived below the poverty line and infrastructure was lacking—paved roads serviced less than 16 percent of population centers and less than 15 percent had access to electricity.

Still one of the poorest countries in the world, Timor-Leste now has bright prospects. The Government of the Democratic Republic of Timor-Leste recognizes, however, that the lack of a solid legal and regulatory framework for business development and the lack of domestic capital, technology, managerial expertise, and general know-how in the private sector are hindering economic development. Thus, to create jobs and combat poverty it has made attracting foreign direct investment (FDI) a priority. In this regard, it considers developing and implementing a business-friendly regulatory environment essential. While the government has planned and taken many steps to support private sector development, legislation to regulate the business environment and each sector is still needed so private investors have a predictable environment in which to make investment decisions.

In addition to instituting measures to create a framework for private sector development,

the government needs to better understand the country’s general and sector-specific investment opportunities, as well what obscures these opportunities. This Investment

Opportunity Assessment (IOA) examines investment opportunities and challenges facing

Timor-Leste and provides guidance on how government, institutions, and the private sector can build on newly passed legislation to attract domestic and foreign investment

into key economic sectors. It examines the country’s investment climate, comparative and

competitive advantages, and the prospects and constraints of key economic sectors. It

draws on (1) the experience of Nathan Associates’ Resident Investment Advisor (RIA)

gained over the past 20 months in Timor-Leste, (2) a workshop and SWOT (strengths,

weaknesses, opportunities, and threats) analysis, and (3) fieldwork involving the workshop and SWOT analysis. The few existing studies or recommendations on

investment opportunities and challenges in Timor-Leste were also considered, though

most of these focus on the functional business environment:

2

• Feasibility and market studies on a few niche agricultural products by IFC and others,

as well as a more recent recommendations for IFC in Timor-Leste;

• A small and medium industry strategy that focuses on the investment framework

(prepared for AUSAID);

• A detailed study by the World Tourism Organization on the potential of the tourism sector; and

• Sectoral investment programs (SIPs), including one for private sector development, that

focus on public investment and reform needs (prepared by the government and donor organizations).

Other than what is available from individual entrepreneurs or projects, statistical and

sector-level information is scant.1 A team of three Nathan Associates experts and two Timorese staff from the Investment Division of the Ministry of Development and

Environment (MDE) carried out fieldwork, including a workshop from April 4-22, 2005.

The team gathered information from various sources, including existing literature and documentation, face-to-face interviews, observation of business operations and potential

investment locations, and the workshop. The team interviewed domestic entrepreneurs,

foreign investors, technical advisors, government officials, and many others. Their

opinions are reflected in this report, but without attribution.

Sponsored by the MDE and financed with USAID resources under Nathan Associates’

Investment Advisory Services Project, the one-day workshop was a core activity. More than 50 representatives from government, business, and local civil society and

international organizations participated enthusiastically in the workshop and its working

groups. The workshop was the first of its kind in Timor-Leste to address investment opportunities and constraints for the country as a whole. It also provided a means for

gathering opinions on strengths, weaknesses, opportunities, and threats in six key sectors:

fisheries and aquaculture, tourism, light manufacture, oil and gas upstream and downstream services, and financial and business support services.

Section 2 of this assessment provides information on the state of the private sector and

investment in Timor-Leste, including investment trends and the business environment. Section 3 sets Timor-Leste in the context of global FDI trends and summarizes the

motivations for foreign investment. Section 4 examines the country’s comparative and

competitive advantages; Section 5 the potential of key economic sectors and the implications of that potential by region. Section 6 examines the relationship between domestic investment and FDI in Timor-Leste; and Section 7 describes challenges for investment promotion—creating a favorable investment environment, competing in the region, and targeting investment sources. In Section 8 we offer recommendations and next steps for realizing Timor-Leste’s investment opportunities. As a type of guide

1 Indeed, in due course, statistical capabilities and the tracking of investment-related information and benchmarking in Timor-Leste need to be improved. USAID and the Government of Timor Leste are expecting to collaborate on this issue as part of MCA Threshold activities.

3

for the IEPA, this assessment stresses the role desired for the new agency where

appropriate. Terms of Reference for this assessment are provided in Appendix A, and persons interviewed are listed in Appendix B.

2. General and Economic Context With a population of 924,6002 and occupying 15,007 square kilometers at the tail end of

Southeast Asia, between Indonesia and Australia, Timor-Leste is the region’s newest and

second smallest country.3 It occupies more than half of the Timor Island, primarily the eastern half, with the exception of the enclave of Oecusse-Ambeno in Indonesia’s

southernmost province of West Timor. From the perspective of investment opportunity,

Timor-Leste is well positioned. It stands to soon become a part of ASEAN4 and its proximity to Australia provides ready access to a robust market.

Economic Structure

Timor-Leste has a very small economy; in 2003 GDP was $341 million and annual per

capita income was $369—a national average of barely more than $1 per person per day on

a 365 day basis! Logically, the estimated poverty rate is also one of the highest in the world, affecting more than 40 percent of the population.5 In addition, Timor-Leste is

principally an import economy: total imports in 2003 were $230 million and merchandise

imports were about $143 million. Measured against a paltry $7 million in exports for the same year, 6 export receipts covered only 3 percent and 4 percent of total imports and

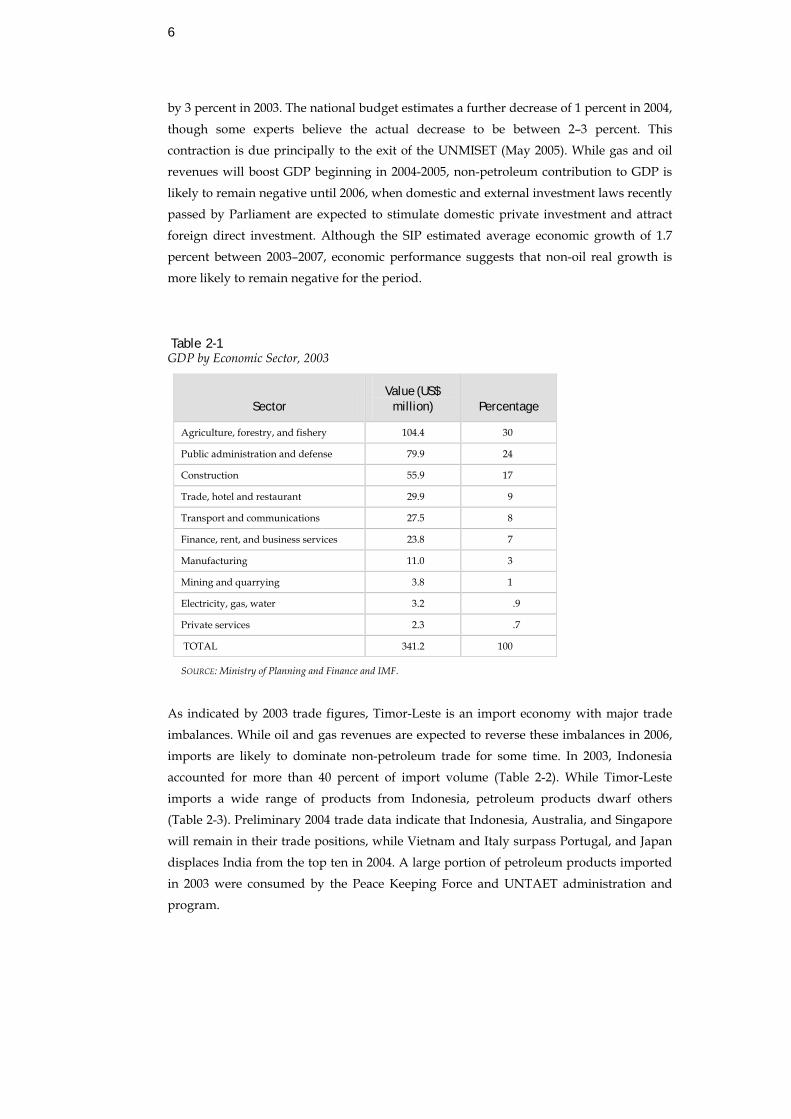

merchandise imports, respectively, in 2003. Table 2-1 presents GDP distribution by sector.

Timor-Leste’s economy has been in transition since 1999 and has fluctuated with political events. According to Ministry of Plan and Finance and IMF data, GDP was $270.1 million

in 1999, the year Timor-Leste broke from Indonesia and the economy was plundered by

social strife. GDP then rose steadily, peaking at $380.7 million in 2002, the year of the rebirth of the Democratic Republic of Timor-Leste. This four-year rise in GDP was due

principally to the “dollar bubble” created by the presence of the UN and a military

contingent. With the drastic reduction of that presence in 2003 and 2004, GDP decreased

2 2004 National Census. 3 Only Brunei is smaller, with a land area of about 5,200 sq. kilometers and a population of 372,000. 4 The Timorese Minister of Foreign Affaires and Cooperation recently announced that Timor-Leste intends

to join ASEAN. 5 UN Human Development Report. 6 Coffee was the principal export commodity in 2003 and the United States was its principal market where

it is sold as organic coffee.

6

by 3 percent in 2003. The national budget estimates a further decrease of 1 percent in 2004,

though some experts believe the actual decrease to be between 2–3 percent. This contraction is due principally to the exit of the UNMISET (May 2005). While gas and oil

revenues will boost GDP beginning in 2004-2005, non-petroleum contribution to GDP is

likely to remain negative until 2006, when domestic and external investment laws recently passed by Parliament are expected to stimulate domestic private investment and attract

foreign direct investment. Although the SIP estimated average economic growth of 1.7

percent between 2003–2007, economic performance suggests that non-oil real growth is more likely to remain negative for the period.

Table 2-1 GDP by Economic Sector, 2003

Sector Value (US$

million) Percentage

Agriculture, forestry, and fishery 104.4 30

Public administration and defense 79.9 24

Construction 55.9 17

Trade, hotel and restaurant 29.9 9

Transport and communications 27.5 8

Finance, rent, and business services 23.8 7

Manufacturing 11.0 3

Mining and quarrying 3.8 1

Electricity, gas, water 3.2 .9

Private services 2.3 .7

TOTAL 341.2 100

SOURCE: Ministry of Planning and Finance and IMF.

As indicated by 2003 trade figures, Timor-Leste is an import economy with major trade

imbalances. While oil and gas revenues are expected to reverse these imbalances in 2006, imports are likely to dominate non-petroleum trade for some time. In 2003, Indonesia

accounted for more than 40 percent of import volume (Table 2-2). While Timor-Leste

imports a wide range of products from Indonesia, petroleum products dwarf others (Table 2-3). Preliminary 2004 trade data indicate that Indonesia, Australia, and Singapore

will remain in their trade positions, while Vietnam and Italy surpass Portugal, and Japan

displaces India from the top ten in 2004. A large portion of petroleum products imported

in 2003 were consumed by the Peace Keeping Force and UNTAET administration and

program.

7

Table 2-2 Timor-Leste’s Top 10 Countries of Import, 2003

Country Value (US$

million) Percentage

Indonesia 83 41

Australia 23 11

Singapore 13 6

Portugal 10 5

Thailand .95 0.5

China .92 0.5

Vietnam .68 0.3

Italy .61 0.3

India .38 0.2

Denmark .33 0.2

SOURCE: RDTL Department of Statistics.

Table 2-3 Imports by Product Category, 2003

Product Category Value (US$

million) Percentage

Petroleum products 64 32

Food and beverages 20 10

Capital goods 14 7

Construction materials 12 6

Vehicles and spares 12 6

Others 81 40

TOTAL 203 100

Source: RDTL Department of Statistics. As shown in Table 2-4, Timor-Leste’s exports in 2003 were very limited—earning barely

$7 million. Coffee was the primary export and the United States was the principal market.

Indonesia was the second-largest export market, but exports were valued at less than $1 million. Exports to Australia, the third-largest market, were valued at little more than half

a million dollars. Exports to the remaining top four countries were negligible, when

combined, accounting for less than the Australian market.

Timor-Leste’s economy remains primarily rural, based largely on agricultural production. The main products are coffee and a few other cash and food crops, such as rice and maize. Under occupation, the main export crops were coffee, some spices (such as cloves), vanilla, and candlenut.

8

Table 2-4 Timor-Leste’s Top Seven Export Markets, 2003

Country Value (US$

million) Percentage

United States 2.85 41

Indonesia .91 13

Australia .54 8

Singapore .16 2

Germany .14 2

Norway .07 1

Portugal .07 1

Source: RDTL Department of Statistics.

Investment Trends

The Sector Investment Program (SIP) presents GDP and investment figures from 2000-

2003 by public and private sector shares (Table 2-5). While indicating a mixture of public and private economic activity, data also indicate that private-sector activities dominate

and are increasing even though non-oil GDP has been declining: private-sector activity

accounted for about two-thirds of GDP in 2003. Agriculture continues to contribute the most to GDP, about 30 percent. The agriculture sector employs more than three-quarters

of the labor force but is characterized by low productivity because of the subsistence

nature of the sector activity.

From the perspective of gross fixed investment, data in Table 2-5 indicate that investment

in Timor-Leste fluctuated in a pattern similar to GDP fluctuation during 2000-2003. From

a base of $118.8 million in 2000, gross investment peaked at $145.4 million in 2001 and then declined steadily to $105 million in 2003. As can be expected in a post-conflict period,

public investment far outstripped private investment. Concomitantly, because of recent

contraction in non-oil sectors, private investment share of the GDP in 2003 declined to 4.4 percent of GDP from a high of 9.5 percent in 2000 and 2001.

Why so much fluctuation? During the early period of transition, donor-funded

expenditures on reconstruction and rehabilitation relied on private suppliers of goods and services. Private activity grew rapidly and helped restore the supply of goods and

services. As reconstruction slowed in 2002, and UN staff began to leave, private-sector

growth slowed. This slowing is expected to continue through 2005, as the UNMISET program concludes in May 2005 and the economy bottoms out in the second half of this

calendar year. This negative trend may be countered in 2005 by higher-than-expected

revenue from the petroleum sector and investment attracted by new domestic and

external investment laws.

9

Table 2-5 Trends in Public and Private Value Added and Investment, 2000-2003

Amount Growth 2000-2003

(% p.a.)

Indicator 2000 2001 2002 2003 Nominal Real

Non-oil GDP

Private sector

Agriculture 81.5 84.7 91.2 97.4 6.1 4.7

Private non-farm 98.2 111.5 110.7 114.7 5.3 2.6

Subtotal 179.7 196.2 201.9 212.1 5.8 3.3

Public sector 136.5 171.7 141.4 123.6 (3.3) (3.5)

Total 316.2 367.9 343.3 335.7 2.0 0.7

Oil and gas 77.5 44.3 41.5 52.7 (12.1) (12.5)

Total GDP 393.7 412.2 384.8 388.4 (0.5) (1.7)

Gross fixed investment 118.8 145.4 118.9 105.0

% of GDP

Private sector 9.5 9.1 5.7 4.4

Public sector 20.7 26.2 25.2 22.6

Total 30.2 35.3 30.9 27.0

Memo item

Private sector output 65.3 58.3 63.3 68.2

Note: Public and private investment are estimated independent of SIP data.

SOURCE: National Statistics Office, January 2005.

While the overall economy showed signs of contraction in the past year or two, the financial sector did not. As can be seen from Figure 2-1, the supply of domestic credit has

expanded, with credit extended by commercial banks to private and enterprises

increasing considerably since June of last year, mainly because of a change in credit policy and a lowering of interest rates by the largest commercial lender in Timor-Leste.7 In

January–October 2004, credit outstanding nearly trebled from $29 million to $76 million.

According to BPA data, the main credit sectors as of June 2004 were construction; trade and finance; and industry, transport, and communication. This credit supply appears to

be a response to credit demand caused by strong growth in domestic construction driven

by government contracts and by the housing market. Some expansion has been associated with a reported increase in demand for working capital in the trade sector, given its

importance to private business activity. A lowering of interest rates from 15+ percent to

an average of 11–12 percent and premium customers taking out loans with rates as low as 8-9 percent contributed to the sharp rise in credit demand in the latter half of 2004.

7 According to data published in local newspapers, Caixa Geral de Depositos, a wholly-owned Portuguese Government bank known locally as BNU, is the major lender in Timor-Leste,.

10

Figure 2-1 Outstanding Credit of Commercial Banks to Private Enterprises

75,78771,17975,67470,699

51,779

28,949

16,49211,0147,897

0

10

20

30

40

50

60

70

80

Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Aug-04 * Sep-04 * Oct-04 *

Mill

ion

USD

SOURCE: Bank and Payments Authority of Timor-Leste, Economic Bulletin. Another indicator of investment trends is the number of business registrations or

“licenses” (Table 2-6). By the end of 2004, about 10,700 licenses had been issued—two-

thirds to individually-owned businesses8 and one-third to companies. Only 37 percent of licenses for individual business were legally valid, while 56 percent of licenses issued to

companies were legally valid.9 Licensing has declined because of lack of access to credit

and because many licenses were obtained simply to bid on government contracts. The latter supposition was corroborated by a study conducted in mid-2003. Of the 200-plus

licensed businesses examined, about 40 percent either no longer existed or had never

opened.10 In 2004, the number of new licenses issued grew considerably, suggesting a correlation with the sharp rise in credit supply from commercial banks during the second

half of the year (Figure 2-1).

Foreign Investment

While no systematic means for collecting data on foreign direct investment in Timor-Leste

yet exists (the soon-to-be established External Investment and Export Promotion Agency is to devise a means), total FDI is estimated to be slightly under $1.75 billion.11 Most is

concentrated in the gas and oil sector, with more than $1.65 billion already invested

offshore. Onshore FDI is estimated to be close to $100 million.

8 An individual business license costs $10 and a company license costs $100. Licenses issued in 2000 and 2001 were valid for two years, and since 2002 valid for one year.

9 The number of legally licensed businesses in operation in 2004 was 4,572 (2,760 individual business and 1,812 companies). Although numbers represent a significant improvement over 2003, they indicate that approximately 6,200 individual businesses and companies had not renewed registration at end of 2004.

10 ARD Report on Research Findings on Lease of Government Properties, October 18, 2003. 11 Data based on informal survey conducted for this assessment.

11

Table 2-6 Number of Business Licenses Issued and Renewed

Indicator 2000 2001 2002 2003 2004

L I C E N S E S I S S U E D

Self-owned 3,370 1,106 768 282 2,016

Company 376 337 696 926 894

Total 3,746 1,443 1,464 1,208 2,910

T O T A L L I C E N S E S I S S U E D

Self-owned 3,370 4,476 5,244 5,526 7,542

Company 376 713 1,409 2,335 3,229

Total 3,746 5,189 6,653 7,861 10,771

L I C E N S E S R E Q U I R I N G S E L F - R E N E W A L

Self-owned 0 0 3,370 5,244 5,526

Company 0 0 376 1,409 2,335

Total 0 0 3,746 6,653 7,861

L I C E N S E S R E N E W E D

Self-owned 0 0 95 96 744

Company 0 0 162 586 918

Total 0 0 257 682 1,662

P E R C E N T O F L I C E N S E S R E N E W E D

Self-owned 0 0 2.8 1.8 13.5

Company 0 0 43.1 41.6 39.3

Total 0 0 6.9 10.3 21.1

SOURCE: Department of Trade, SSCI, January 2005.

The top 10 investor countries in all economic sectors are

1. United States 6. Indonesia 2. Japan 7. Thailand

3. Italy 8. Singapore

4. Australia 9. Malaysia 5. Portugal 10. China

The top four countries together have invested about $1.65 billion in the Bayu-Undan gas

field in the Timor Sea. This gas field alone in the Joint Petroleum Development Area (JPDA), co-administered with Australia, is expected to net more than $4 billion in

royalties, taxes, and profit revenues for Timor-Leste in the next 20 years. Depending on

negotiations between Timor-Leste and Australia on an even larger gas field, the Greater Sunrise—whose estimated proceeds are expected to be net three to four times that of

Bayu-Undan with revenue streams over a 30- to 40-year period—Timor-Leste’s share may

be at least equal to or substantially larger than that received from Bayu-Undan. The

ranking of investor countries may change soon if the negotiations over the Greater Sunrise

gas field are successfully concluded, as reported in the press.

12

Ensuring a prosperous future depends only in part in managing proceeds from

hydrocarbon endowments. The greater challenge for sustainable development lies in promoting investment in the non-oil and mineral resource sectors. Timor-Leste must use

income generated from non-renewable resources for capital investments in human

resource and infrastructure.

Business Environment Framework

The Government of Timor-Leste is working to improve the enabling environment to build

a strong foundation for sustained private-sector-led growth that stimulates domestic investment and attracts FDI. So far, the government has adopted a private investment

policy and passed related laws and decrees. Legislation that supports private sector

development includes the Land and Property Law, the Commercial Companies Law, the Domestic Investment Law, the External Investment Law, the notary decree-law, and the

fisheries decree-law. Other laws, such as the insurance law and the private lease law, are

now in Parliament; the registration decree-law, the decree regulating business registration procedures, and the bankruptcy decree-law are being drafted. Other legislation for a

regulatory framework includes the association law, the chamber of commerce law, export

promotion law, environment decree-laws, intellectual property law, competition law, accounting systems decree-law, social security law, and legislation required to regulate

economic sectors (e.g., manufacturing, domestic and internal trade, tourism,

environment). The creation of an effective private sector framework means that this legislation needs to be adopted and regulations passed to set up or strengthen

implementing departments and services. This will be coupled with an investment

promotion program

In recently passing investment laws, and with regulations expected to be adopted by the

end of May 2005, the government has taken major steps to create the right legislative and

regulatory framework for investment. The rights and guarantees of these laws contribute to a sound and predictable investment environment (Exhibit 2-1). In addition, domestic

and foreign investment will be stimulated by robust investment incentives tied to job

creation, and the work of the newly created investment promotion agencies. Effective promotion and expeditious investment licensing will be essential to fostering an

environment that accelerates job creation and reduces poverty.

13

Exhibit 2-1 Laws and Incentives Creating a Favorable Investment Environment

On May 2, 2005, the National Parliament passed

the Domestic Investment Law and the External

Investment Law.12 Domestic investors had

expressed desire for a separate domestic law a

little over one year ago. The foreign investment

law had been in the works since 2000. The two

laws are mirror images in their guarantees,

incentives, and post-entry treatment. The External

Investment Law, which imposes a higher

minimum investment threshold, covers origin of

invested capital, the right of foreign investors to

repatriate profit and capital, and the right of

foreign investors to pursue conflict resolution

abroad under ICSID13 rules. Otherwise, the two

laws treat all investors equally. In creating a

separate domestic law, the government

demonstrated goodwill in listening to domestic

investors, and domestic investors are very

satisfied

with their own role in the development of the

country’s private investment regime. The specific

provisions of the domestic and external

investment laws are provided in Appendix C.

Timor-Leste’s investment incentive program was

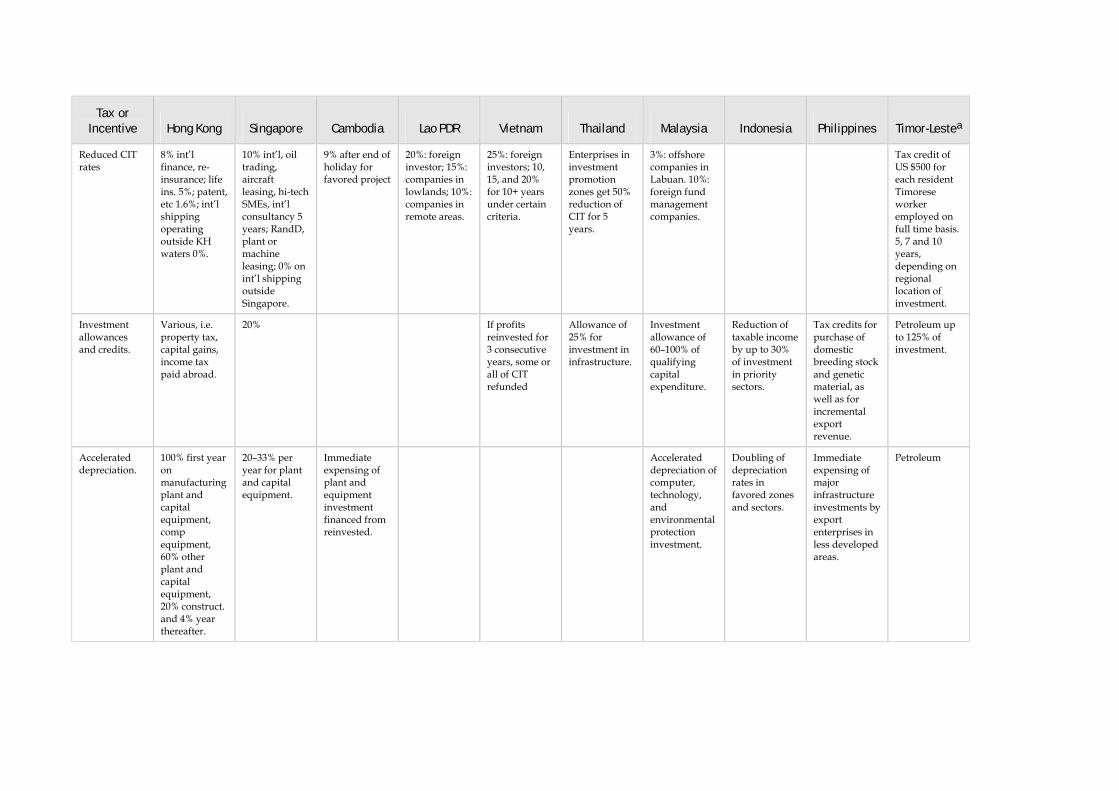

based on analysis of competition in Southeast

Asia, a region known for aggressive FDI

promotion and success in attracting and retaining

foreign investors. Appendix D presents the

incentive package offered by competing countries

and those offered by Timor-Leste. While Timor-

Leste’s package lacks aggressive incentives, such

as corporate “tax holiday,” it does offer a

corporate profit tax credit system linked to the

creation of direct full-time employment. The

choice of this option is based on the country’s

desire to combat unemployment and ultimately

reduce poverty.

12 Timor-Leste uses the concept of “external investment” to denote similar FDI treatment accorded its emigrant population abroad who invest under the same conditions as foreign citizens. Conflict resolution options available to foreign citizens are not naturally accorded to emigrant Timorese citizens. An emigrant is defined as someone who has lived continuously abroad or at least five years prior to submitting an external investment application.

13 ICSID - International Center for Settlement of Investment Disputes. As Timor-Leste is a member of the World Bank it is automatically a party to the ICSID Convention.

3. Foreign Direct Investment Trends and Motives

Global inflows of FDI grew from $209 billion in 1990 to almost $1.4 trillion in 2000; inflows to developing countries rose from $26 billion in 1990 to $188 billion in 1999, an

increase of nearly 630 percent (Figure 3-1). Though global flows have declined since 2000

to $560 billion in 2003, inflows to developing countries declined less. In fact, several low-income countries, including Timor-Leste and several Asian countries, enjoyed an increase.

In 2003, developing country FDI inflow amounted to $146 billion, or roughly 26 percent of

the global U.S. dollar value. China alone received $54 billion.14

Regionally, economic growth and an improved business environment are contributing to

a 27 percent increase in FDI in Southeast Asia. The United Nations Conference on Trade

and Development (UNCTAD) reports that inflows grew from $15 billion in 2002 to $19 billion in 2003. On the basis of surveys of multinational

corporations and the economic rebound in most of the

developed world, UNCTAD predicts that FDI inflow will increase in the mid-2000s.

Four Factors in FDI Surge of 1990s

Rise of China

The rising popularity of China and, to a lesser extent, India, and the shift in FDI from manufacturing to

services, are the two main trends in FDI of the last two

decades. China is attractive because it has more than 1.3 billion consumers and highly productive labor. It

has also embarked on a selective but wide range of

business environment reforms and increased its

integration into global commercial diplomacy by joining the WTO. India’s inward FDI in

1. Extensive investment in privatization of state-owned assets, particularly in Latin America and Eastern Europe.

2. Acquisitions of distressed banks after the 1997 Asian Financial Crisis.

3. A wave of international corporate cross-border mergers and acquisitions—many between developed and developing countries—outside the financial sector.

4. The growing attraction of China as an investment destination.

14 China’s figures are sometimes controversial because of “round tripping” : mainland firms recycle investment finance through Hong Kong as “new” investment to take advantage of incentives open only to foreign investors.

16

2003 was about $4.3 billion and its prominent companies, such as Tata Consulting and

Infosys Tech Ltd., are active outward investors in Asia.

Figure 3-1 FDI Inflows, Developed and Developing Countries, 1990-2003

0

200

400

600

800

1,000

1,200

1,400

1,600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

US$ billions

Total World

Developed Countries

Developing Countries

Note: Developed countries are high-income countries according to World Bank classification (2003 per capita GNI above US$ 9,385). Developing countries are low and middle-income countries according to World Bank classifications (2003 per capita GNI is US$ 9,385 or below). Regional groupings are according to World Bank definitions. Based on these criteria, certain countries considered “developing” by UNCTAD are considered high income by the World Bank, and are excluded from the definition of “developing countries” in these figures.

SOURCE: UNCTAD, World Investment Report 2004 data on FDI inflows; World Bank, World Development Report 2005 for country classifications.

Move to Services

FDI in services grew substantially in the second half of the 1990s, faster than investment in natural resources or manufacturing. Growth is in the “old” services—utilities, finance,

insurance, and retail and wholesale distribution—and in the “new” services of business

support and other services enabled by telecommunications and information technology. In developing countries as a whole, services represent more than half of inward FDI, with

flows concentrated at the upper-middle income economies. But in China, the Pacific and

in Africa, inward FDI stock15 is still concentrated in manufacturing and the primary sector even though the share of total FDI stock increased in Asia from 43 percent in 1995

to 50 percent in 2002. Competition among Malaysia, Singapore, and Thailand for high

value-added services has increased.

Global growth in service sector FDI is associated with

15 FDI Stock is the total value of all foreign owned assets in a country at a given point in time.

17

• Increased liberalization of regulation and loosening of foreign ownership in the

services sector in many countries -- including signatories to the WTO GATS and TRIM;

• Privatizations in the former Soviet Union and Eastern bloc countries as well as in Latin

America and Africa;

• IT sector development and growth, which itself has enabled services to be traded internationally; and

• Efficiency-driven contracting of business services that used to be performed in-house

in corporations (e.g. call centers and financial service back office operations).

As Timor-Leste formalizes the legal and policy framework governing all forms of

investment, including FDI, it must bear in mind the nature and recent trends in FDI

Sources of FDI

FDI originates from companies domiciled in the United States, France, the United

Kingdom, Belgium, the Netherlands, and Japan. Other important sources of investment are Asia, Singapore, Taiwan, Hong Kong, and mainland China. And regional blocs, such

as the EU and ASEAN, are emerging as sources of FDI among member countries.

Though developed countries will probably continue to provide most global FDI, companies in developing countries increased investment in other developing countries in

the 1990s. This “South-South” FDI peaked in 2000, when it accounted for about one-third

of flows to developing countries, up from 17 percent in 1995. Though these flows diminished in the early part of 2000s, as did global FDI, they remain important for Timor-

Leste. Investors from Asia, particularly ASEAN countries, can complement investment

from other regions and could be better equipped to tolerate the risks and challenges of

investment in Timor-Leste. Malaysia, Thailand, and Singapore, are increasingly active in

the region (e.g., Singaporean and Malaysian investors are active in telecommunications

and leisure/hospitality). Malaysia’s state-owned oil and gas company, Petronas, has investments in Vietnam, Cambodia, and Lao People’s Democratic Republic.

In addition to ASEAN countries, whose investors have expressed interest in Timor-Leste,

the country can count on investments from Australia and Portugal, which are already investing in Timor-Leste, even under adverse economic conditions and a less than ideal

regulatory environment. Australian business interests first came to provide goods and

services required by the Australian contingent in post-conflict Timor-Leste. Portuguese investors also came for similar reasons but have chosen to remain in strategic sectors, such

as commercial banking, telecommunications, and power. As a former colonial power,

Portugal’s investment interest in Timor-Leste will probably be long-term and is likely to

continue and expand to other areas, such as the financial sector (i.e., insurance, risk

capital) and infrastructure management.

18

Table 3-1 summarizes the FDI outflows from countries in the region that could be

important to Timor-Leste. The amounts include the activity of smaller, less-capitalized investors, a group that could be particularly important for targeted investment

promotion. Like domestic investors, these foreign investors would have concerns about

the business environment, complex or unclear business regulations, incentives, and red tape.

Table 3-1 Outflows of FDI from Select Countries

Country 2002/2003 Value of FDI (US$ millions)

Australia 7576.04/15107.6

China (Hong Kong) 17463.19/3769.4

China (Macao) 61.6/24.1

Malaysia 1904/1369.5

Philippines 59/158

Portugal 3288.63/95.5

Singapore 3699.4/5536.2

Thailand 106/557.2

SOURCE: Nathan Associates based on UNCTAD data.

As with overall FDI flows and in the OECD countries in particular, outflows fell more

dramatically in Portugal and Australia than in developing countries, such as Thailand

where figures indicate a rebound. Portuguese outward FDI is concentrated in Brazil and Spain. In 2000, Brazil was host to 47 percent of Portuguese foreign investment. FDI from

Portugal is concentrated in telecommunications, electricity, financial services, and retail.

Investments are also mainly through holding companies. As the Government of Timor-Leste devises policies and determines regulatory priorities, investment opportunities of

the “old” or conventional service sector should be remembered.

FDI Motivations and Implications for Timor-Leste

Competition for global FDI is stiff. As a new nation emerging from conflict, Timor-Leste

gained FDI in the building and construction, trade and distribution, banking and finance,

and telecommunications sectors. As they seek to attract more FDI to complement domestic investment and boost development, decision makers and other stakeholders in

Timor-Leste need to appreciate the motives for global and regional foreign investment.

FDI is first and foremost a business transaction; investors seek the highest possible return on investments within calculated risk margins. While often calculated with sophisticated

capital pay-off techniques that demonstrate how investments can be maximized, the basic

19

concept is simple and predicated on a bottom-lines principle: the greater the risk the

higher the return expected.

Investors have four basic reasons for undertaking foreign direct investment. They seek

• Resources, such as mineral and petroleum resources, fisheries, forestry, agricultural and

other natural assets, or cheap and highly productive labor; or

• Markets of new customers and clients that can be served best through local production

rather than exporting, and to take advantage of access offered by trade agreements; or

• Efficiency that lowers the cost of production within global production networks; or

• Strategic assets or alliances that complement and promote corporate strategic

objectives.

The decision to investigate a location and to eventually locate there is determined by the enterprise’s corporate strategy, competitive structure of its industry, and host-country

attributes (Table 3-2). Every investment tends to be unique and it is helpful to think in

terms of FDI project types. Factors predicated on corporate structure are push factors; those based on host-country attributes are pull factors. Competitive pressures faced by

enterprises in their existing locations push them to look overseas, and the way an investor

perceives the attractiveness of a country pulls in the particular type of project.

In addition to considering profits and the reduction of unique operating costs, investors

take into account incentives that governments confer on investors. The two most

important in developing countries are financial and tax incentives and guarantees on investment provided by the state or by the state’s status as a signatory to an

internationally recognized agreement. Governments usually determine incentives by

assessing the likely benefits of a particular type of FDI project. Timor-Leste is formalizing its policy and legal framework governing all kinds of investment, including foreign

investment.

Multilateral and bilateral trade and investment agreements have provisions that address investors’ concerns about non-commercial risks. The World Trade Organization and its

rulings are widely known, but investors from countries targeted by Timor-Leste could be

interested in bilateral investment treaties (BITs). Evidence of BITs’ direct stimulation of FDI is inconclusive, but large investors in developed countries find them reassuring. The

number of BITs globally has skyrocketed from 385 at the end of 1995 to about 2,000.

20

Table 3-2 Foreign Direct Investment Motives and Host-country Attributes

Motives for Investment Host -country Attributes

Resources or assets Raw materials/primary commodities

Markets Market size and per capita income

Market growth potential

Access to regional and third-country markets

Country-specific consumer preferences

Proximity to strategic clients/customers

Structure of markets (concentration, price structure)

Efficiency Low-cost unskilled labor

Skilled labor

Other input costs (e.g., transport and communications to/from host economy) and costs of intermediate products

Membership of a regional integration agreement conducive regional corporate networks

Strategic Assets Created assets based on technology or innovation (e.g., brand names) including assets

Created assets embodied in individuals, firms, industry clusters (e.g., R&D capabilities)

Physical infrastructure (ports, roads, power, telecommunications)

SOURCE: Nathan Associates, based on UNCTAD, World Investment Report 2003.

What do these motives imply for Timor-Leste?

Natural resource seeking FDI. Total FDI in Timor-Leste is estimated to be about $1.75 billion, with the Bayu-Undan gas field taking up $1.65 billion. Onshore investment is

estimated to be $80 to $100 million, of which $22 million have been invested in the

telecommunications sector. Success in attracting natural resource-seeking FDI, particularly in extractive industries, tends to bring about “Dutch disease”—the real

appreciation of a country’s currency due to a sudden inflow of capital usually caused by

the export of natural resource. Capturing additional export value within Timor-Leste will

entail attracting more investors into agro-processing. For these investors, concerns include

profit margins and the price of the particular commodity in the world market; availability

and cost of labor; quality certification; and adequate road and sea transportation. Timor-Leste can probably satisfy conditions for land availability and raw materials.

Market seeking FDI. Current and past export data indicates potential for market-seeking

FDI in the agricultural/agribusiness sector (coffee, coconut, vanilla, palm oil, and candlenut) as well as in fisheries. Location attributes of market-seeking FDI include

market size and access, and the near- and medium-term potential for economic growth.

Timor-Leste’s market is small and purchasing power is low. With the reduction and ultimate end of UNMISET activities in May 2005, purchasing power will be even lower.

In other parts of the world, small and regional investors, whether because mandated by

the state or in pursuit of commercial success, have been motivated to undertake joint

21

ventures with domestic firms on investment projects that initially focus on import

substitution, then gradually increase export share over time. Should Timor-Leste join ASEAN, the potential for gaining market-seeking FDI could improve considerably.

AFTA-CER16 envisages closer trade and investment between ASEAN and Australia and

New Zealand. Timor-Leste’s potential for having a large market through membership in the Community of Portuguese Language Countries (CPLP) is constrained because the

CPLP functions as a political organization17 and is not geographically contiguous. Small

economies, such as Timor-Leste haves served as trampoline for investors from quota-constrained countries and have exploited the privileged market access that attaches to

being a developing country. But marketing a country as an export platform is no longer

much of a comparative advantage. Doing so was most effective in the textiles and apparel industry but international agreements, WTO accession, and the end of global import

quotas on textiles and apparel have eroded the value of such market access.

Efficiency seeking FDI. The shift in global FDI to from manufacturing to services has intensified efficiency-seeking FDI. Manufacturing processes are now disaggregated in

complex networks. This efficiency-seeking FDI desires cheap labor and adequate

productivity, with production carried out by foreign affiliates in an extensive network organized by the parent company.18 Affiliates deliver the best cost-productivity

characteristic for the intermediate product, which is then exported to its next location in

the value chain for the next stage of processing. For smaller investors, such networks are less extensive, but the focus on reducing costs is still the primary motive. Frequently, the

decision to produce overseas is driven by rising costs in a parent company’s home

country or current location. For Timor-Leste, implications and concerns center on the high unit cost of labor relative to neighbors—though the real wage may be comparable.19

Strategic asset seeking FDI. This type of investment grew in the 1990s with the wave of

cross-border mergers and acquisitions and extensive privatizations in Eastern Europe and Central Asia. Investors seeking strategic assets want intangible as well tangible assets:

technology, brands, or trademarks. Though this form of FDI is increasing in South-South

investment, it is still largely an activity of developed countries. Timor-Leste is a very young with no widely known brands.

At present, Timor-Leste has only natural resources to offer potential foreign investors. The

country has attracted FDI in the gas and oil sector, but investment in other resource-based sectors such as agribusiness and fisheries has yet to materialize. The only agribusiness

commodity in which Timor-Leste seems to have a competitive advantage is coffee

exported to the United States as organically certified. Experts believe that demand in the international niche market for organic coffee is still high; however much more needs to

16 AFTA-CER is ASEAN Free Trade Area-Closer Economic Relations 17 In July 2003 Foreign Minister Jose Ramos Horta called for more focus for CPLP on economic, trade and

business cooperation. 18 Parent company is the multinational corporation based in the home country. 19 See Background Document, Timor-Leste Development Partners Meeting, June 2003, pg 6.

22

done to renew and improve the coffee stock, and to expand production. Likewise, organic

coffee branding needs to be strengthened and broadened.20

The government and private investors have signed several letters of intent with regard to

palm oil production and processing, modified cassava starch processing, and fisheries

catching and processing. Though promising to employ thousands, no investment has materialized, in part because a lack of a sea port in the southern part of the country. And

according to some experts, the more productive variety of palm oil envisaged for the

proposed venture requires a higher rainfall than Timor-Leste has, making high-quality cultivation difficult without irrigation. A recent study by the World Bank examining palm

oil, shiitake mushroom, and vanilla production in Timor-Leste underscored the lack of

local experience and expertise. The emergence of an industry based on these commodities will be impossible without strategic partnership or lead investment from experienced

foreign producers.21 Hence, to tap its natural resource potential, Timor-Leste must seek

foreign expertise, capital, technology, and markets to launch and sustain investment.

20 Starbucks recently launched a project to market Timor-Leste coffee in Washington D.C. and Australia under the country brand.

21 World Bank financed niche market studies of palm oil, vanilla and shiitake mushroom under the ARP II Project.

4. Comparative and Competitive Advantages The concept of comparative advantage is expressed by the dictum: “Nations should export goods and services that they can produce at lower costs then other nations, and

import goods and services that they cannot produce at lower costs.“ Comparative

advantage is based on a production model: lower production cost equals greater advantage. It also comprises resource endowments and natural conditions that form a

basis for building comparative advantage and, eventually, competitive advantage.

Competitive advantage is achieved on the basis of price or of product differentiation,

which are usually mutually exclusive. Consumers are willing to pay a higher price for

quality and unique products and services and unlikely to believe that lower priced

products or services are of the same quality.

The Investment Opportunity Workshop held April 13, 2005 was the second workshop of

USAID’s Resident Investment Advisor (RIA) program. The first built consensus on the

value of private investment to Timor-Leste. In the intervening period, the government approved foreign and domestic investment laws and established the Investment and

Export Promotion Agency (IEPA). The second workshop solicited the opinions of private

and public sector representatives on the country’s comparative and competitive advantages by using strengths, weaknesses, opportunities, and threats (SWOT) analysis in

a plenary session and in sector working groups (Exhibit 4-1). In articulating strengths and

opportunities through public-private sector dialogue, the workshop helped counter the many studies that have focused exclusively on bad news and challenges for Timor-Leste,

and built the enthusiasm necessary as the IEPA begins promoting investment in

partnership with government and business.

Recall that comparative advantages are natural or consolidated characteristics that

support private sector development and attract investment, while competitive advantages

are attributes created for the same purpose. As shown in Exhibit 4-1, many perceived strengths may not be as well established or as accurate as workshop participants assume.

Some opportunities, such as “heritage, tradition and diaspora” are also to be seen as

comparative advantages. And some apparent contradictions exist; for example, climate was noted as a strength and a threat.

24

Exhibit 4-1 Summary of Workshop Opinions on Timor-Leste’s Strengths, Weaknesses, Opportunities, and Threats

STRENGTHS

• Natural resources

• International goodwill from donors

• Strong leadership/vision in government

• Stable macro political-economy

• Public-private dialogue on development

• Sound national petroleum management plan

• Low labor costs

• Climate for specific agro-production

• Rich culture, political history, personalities

WEAKNESSES

• Inadequate infrastructure

• Enduring negative aspects or legacy

• Unavailable/unreliable economic data

• Small domestic market and income levels

• Centralization of government services

• High labor costs compared to competitors

• Unavailability of skilled labor

• Commercial legal framework unclear

• Multiple spoken languages

• High government taxes (excise etc)

• High transportation costs

• Wide trade imbalance

• Lack of recreation and social amenities for

investors

• Weak financial sector (intermediation)

• High interest rates

OPPORTUNITIES

• Heritage, tradition and diaspora/CPLP

• New Nation -- Assimilate best practices

• New Nation -- branding opportunities/niche

• Trade agreements and market access

• Differentiating T-L from neighbors

• Converting weaknesses into opportunities

• Investment in infrastructure development

• Great potential in tourism

• New investment laws may open

opportunities

THREATS

• Natural disasters and unfavorable climate

• Established regional brands (e.g., Bali)

• Lack of urgent attention to weaknesses

• Stiff economic competition from neighbors

• Cost of doing business

• Lack of attention to equitable growth

• Unfair competition from foreign investment

• Lack of consultation on future regulation

• High visa costs

SOURCE: Investment Opportunity Workshop Plenary Session edited by Nathan Associates.

Natural Resources. Timor-Leste’s most significant strength or comparative advantage is

its natural resources: offshore (and some onshore) oil and gas resources natural beauty that supports tourism, and fertile, underused land that can support the expansion of agro-

industry. The country’s climate and lack of pollution are also supportive of tourism and

agriculture, including branding as an organic producer. Timor-Leste’s economic growth will depend on careful management and exploitation of these resources (see Section 5).

Culture. Timor-Leste’s “rich culture, political history and [charismatic, strong]

personalities” are also a comparative advantage. A new, previously downtrodden nation, it boasts two Nobel Peace Prize winners and a rich culture dominated by Catholicism,

unique in Southeast Asia. These advantages need to be developed and branded to achieve

their full potential.

Labor Costs. Workshop participants saw low labor costs as a strength. Indeed, notional

minimum wage levels are about $85 per month. But given the high-cost dollar economy—

25

largely the result of the extended presence of an international organization--wage levels

are subject to upward pressure. And when adjusted for productivity, wage levels are far less attractive or viable for domestic or foreign businesses. One potential textile and

garment investor from Thailand observed that Timor-Leste has extremely limited

experience in light manufacturing sectors, and that productivity in greater Bangkok is probably three times higher. Because wages in Timor-Leste are unlikely to be lowered,

boosting competitiveness will require improving skills, negotiating better (preferential)

market access, and increasing logistical (infrastructure) and administrative efficiency.

Leadership and Vision. The government has shown strong leadership and vision,

characterized by the personal involvement of the Prime Minister. It has passed investment

legislation and established an investment agency. Even though these achievements have taken far longer than originally envisaged, the consultative process has created a shared

vision and strong foundation for future investment promotion (e.g., witness the nearly

unanimous approval of foreign and domestic investment laws in Parliament in April 2005). These achievements, however, merely signal that Timor-Leste is joining the

competition for foreign investment. Vision and leadership must be sustained as the

country engages and responds to foreign and domestic business henceforth. Leadership and vision is a competitive advantage.

Stability, Dialogue, and Petroleum Management. Workshop participants saw “stable

macro political-economy,” “public-private dialogue on development,” and a “sound national petroleum management plan” as strengths. Though well founded, these

strengths must not be taken for granted. Macroeconomic stability, for example, has been

achieved with considerable foreign aid and budgetary support, and many potential investors will see the next elections as a test of stability. Public-private dialogue on

development, especially investment, has been nurtured, but the real test lies in

implementation. Regular dialogue, particularly in key sectors and on the business environment will be crucial, and potential investors will be watching how government

reacts when disputes arise, as they inevitably will. And though strong, Timor-Leste’s plan

for managing royalties and revenues from oil and gas production will face many of the same challenges faced by other countries with similar plans.

Timor-Leste also has many opportunities or potential competitive advantages:

• Ability to leapfrog other nations or stages of development by assimilating best practices in administrative procedures or by introducing the latest technology. Timor-Leste

already depends on mobile telephony rather than fixed-line communication, but now

has the opportunity to exploit the potential of Internet communication. (Timor-Leste is in a position to invest in a simple but advanced Internet infrastructure whether through

cables or wireless systems that has spillover effects for the entire economy, from

agriculture to tourism and government.)

• Exploitation of natural resources to enhance competitiveness. The most direct example

is the plan to install hydroelectric generation capacity that could meet Timor-Leste’s

needs three times over. With negligible marginal cost, this energy could help electrify

26

large areas of the country and provide uninterrupted and reasonably priced power to

emerging industry. Typical charges of more than 20c/kwH constrain business growth and burden poor households that are on the power grid.

• Ability to build infrastructure, including hydropower plant, using financing options not

open to many poor nations. Eventually, these options will include revenue and royalties from oil and gas operations, but in the interim concessional loans (e.g., IDA loans) and

Millennium Challenge Corporation grants are possibilities. In a small country like

Timor-Leste, such funding would have widespread benefits. Workshop participants saw private investment in infrastructure as a possibility but this demand is likely to be

insufficient, whether in roads or electricity, to make this a near-term option.

• Ability to pursue niche market opportunities that would be inconsequential for large countries but would create jobs and have other good economic effects in a small

country.

• Abundant and fertile agricultural land with potential for organic branding, a lead established by the coffee cooperative. Café Cooperativa Timor exports more than 60

percent of Timor-Leste’s coffee—and coffee represents about 90 percent of non-service,

non-oil/gas exports by value.

• Starting from an artificially low point in some agricultural and forestry products.

Timor-Leste was once a major exporter of sandalwood and teak, principally to

Indonesia, but many forests and plantations were exhausted before independence with no attempt at reforestation. Forestry could be restored given government attention and

time.

• Poor country status and partner country goodwill that could lead to preferential trade arrangements.

Most of these are real or natural advantages. But advantages are also created. Consider

positive investment incentives created through preferential tax treatment and more streamlined investment processing. Thus, Timor-Leste has inherited and created

comparative advantages that will enable it to position itself more favorably as an FDI

destination.

Because of its relatively small market, high production costs, and low labor productivity,

Timor-Leste will have to produce for the export market. Competing with regional

neighbors who have comparative advantages in cost and productivity will be difficult. Timor-Leste in fact lacks sufficient comparative advantage to compete on price, the most

common approach, especially in Asia.22 It must therefore compete on the basis of product

differentiation and enter niche markets, as it has done successfully with organic coffee. To

22 Asian economies typically enter markets by producing low-price, low-quality products. Even Japan and South Korea used the price model to gain market entry. They then improve product quality in response to consumer demand, and by competing with countries that enter the market later and sell at lower prices. The automobile and electronic industries exemplify this pattern that drives innovation. Research on this model has focused on products and firms but the model true for countries as well.

27

the extent possible, differentiation should be the principal strategy of investment

promotion.

To realize Timor-Leste’s significant comparative and potential competitive advantages,

the government must maintain economic and political stability, continue working with

the private sector and civil society toward a common vision of economic development, and nurture vibrant businesses, whether domestic or foreign.

Some actions, such as improving infrastructure, will require significant financial resources

or foregoing revenues (e.g., fiscal incentives to match regional competitors). Other actions are equally important but require fewer resources: raising skill levels, improving the

efficiency and transparency of the business environment, and increasing public-private

dialogue. Finally, the new IEPA will play a central role in mediating between government and the private sector, in listening to businesses and communicating their concerns to

government, and in identifying new business areas and opportunities for government

support through public policy and investment.

5. Potential of Economic Sectors In Timor-Leste, identifying and promoting subsector investment opportunities must go

hand in hand with improving the business environment, facilitating public-private

dialogue, and devising a sector strategy. This is partly because of the concentrated pattern of activity in some sectors that have a record of competitive production, and the disparate

pattern in other sectors, and partly because of investment decisions that must be made to

boost basic skills and improve infrastructure. Consider, for example, the coffee subsector of agriculture. Coffee represented roughly $7million of Timor-Leste’s $8 million of non-

petroleum exports in 2004. Café Cooperativa Timor (CCT) was responsible for about 80

percent by value. CCT has 300 full-time and 3,000 seasonal employees. Almost 18,000 farming families are CCT affiliates. Even if non-CCT producers (40 percent of volume)

have a proportional impact on full-time employment, the aggregate contribution of this

major export industry on non-seasonal employment is limited. Thus, diversification and encouragement of derivative industries will be crucial.

Employment by Sector

Timor-Leste needs to create new employment in and beyond agriculture. About 15,000

individuals join the country’s workforce each year, many with aspirations beyond

agriculture now that Dili’s 18 institutions of higher education institutions are beginning to produce graduates. Absorbing 15,000 new workers each year poses a modest challenge for

most countries, but a major challenge for Timor-Leste.

Employment statistics in Timor-Leste are unreliable, and the treatment of part-time or seasonal agricultural workers is unclear. In a population of roughly 900,000 the workforce

is estimated at 270,000, with about 220,000 in the farm sector and 50,000 in other sectors

(manufacturing, agroprocessing, services, tourism). Government employs about 17,000. There is pressure to increase government employment, but major problems are lack of

skills and underemployment, and the government intends to remain lean and efficient.

Labor demographics and estimated employment figures by major sector groups are as

follows:

• Farm sector—220,000 (2001 est. from PSD SIP)

• Non-farm sector—50,000 (2001 est. from PSD SIP)

30

⎯ Tourism—1,300 (WTO investigations)

⎯ Government—17,000 (GOTL, Draft Budget Paper, April 2005) ⎯ Non-farm private sector (incl. NGOs)—33,000

Further breakdown of non-farm employment is difficult to come by, but these figures

along with anecdotal evidence have several important implications:

• Employment in more efficient agriculture and expanded agribusiness niches will be

crucial.

• Manufacturing employment, including from petroleum sector spillover, from a low base, especially with relatively low skill levels, cannot be relied on.

• Substantial net expansion of government employment should not be expected.

• Expansion of service sector employment, especially tourism, will be very important. Tourism can boost employment countrywide, especially for women, and services

export receipts. Tourism resources are a major comparative advantage of Timor-Leste.

Trading sector services employment will continue to be important, acting as a non-rural employment buffer for many, but the domestic consumption market will remain small

(and probably shrink), and the sector adds little value.

GDP and Exports by Sector

A breakdown of economic activity by GDP contribution in 2003 (Table 2-1) confirms the

importance of agriculture, forestry, and fisheries. The future contributions of other sectors will vary considerably. Construction, for example, contributed 24 percent to GDP in 2003,

reflecting donor financing for reconstruction. The sector’s future contribution will depend

on the government’s public investment decisions, which will be a function of the economic infrastructure development strategy and of emerging sector strategies.

The trade, hotel, and restaurant sector has been depending on and serving a large

international community. When the UN presence declines substantially beginning in May 2005 this demand will need to be replaced by growth in a proper tourism and hospitality

industry. Some pockets of activity and growth exist (e.g., diving) but the sector

desperately needs a vision and strategy, and the government is working with the World Tourism Organization to devise one.

The contribution of the transport and communications sector is due in large part to the

performance of Timor Telecom, which has a monopoly on fixed and mobile phone services until 2019. The performance of this sector notwithstanding, the braking effect of

this monopoly and high service costs on the rest of the economy will soon be acute.

Manufacturing contributes only 3 percent to GDP, and as the country moves out of reconstruction the sector’s future direction, other than possibly expanding to include

agro- and fish processing, remains unclear. The government expects mining and

31

quarrying (e.g., of precious metals) to contribute more to GDP; activity in this sector will

pick up once the relevant legislation is in place.

Manufactured exports are heavily concentrated in processed green bean coffee, while

tourism has some impact on services. According to the World Tourism Organization,

tourism’s contribution to GDP in 2003 was only about 0.5 percent or under $2 million, although it contributes to value-added in other sectors.

Sector Investment Opportunities

As expressed in the Private Sector Development SIP, the government believes that

significant opportunities for private investment exist in construction, agribusiness,

forestry and fisheries, petroleum and minerals, manufacturing and services, infrastructure, finance, and tourism. Each sector has its investment dynamics, but several

represent derived demand or opportunities as already discussed. Private investment

growth in Timor-Leste will be led by the agribusiness group and tourism in the near term (the petroleum sector in particular has its own dynamic), and by manufacturing and

services to some degree.

Identifying specific opportunities in promising sectors has been limited and often contradictory in conclusions. The World Bank has conducted some feasibility and market

studies for niche agricultural products such as vanilla, palm oil and shiitake mushrooms;

and CCT has been investigating vanilla, candlenut oil, fast-growing teak, and other products. A detailed IFC report on coffee, candlenuts, coconut oil and vanilla, and

tourism is forthcoming. Some feasibility studies for infrastructure projects, such as

industrial zones and electric power generation, have also been prepared. The World

Tourism Organization and SETAI have taken first steps for a master tourism plan. The

nature of tourism development in Timor-Leste is evidenced by the 2004 tourism

promotion budget of $10,000.

STRATEGIC PLANNING

Even with new investment laws and incentives in place, Timor-Leste will have to move

carefully in promoting investment in sectors. Promotion needs to be treated holistically

(e.g., improving the general business environment) and stress constructive engagement between public and private sectors and integrated approaches to development. Alongside

traditional promotion, especially of sectors such as tourism or coffee, the IEPA will need

to advise the government on workforce skills, domestic private-sector capacity, and public policy and public investment decisions (especially in infrastructure).

Because small-scale entrepreneurial initiatives can have a big impact in Timor-Leste, the

government—through the new IEPA or domestic SME agency—needs to work with entrepreneurs to identify and develop niches on an ongoing basis. For example, even

32

though prospects for coconut oil exports by one entrepreneur may not have been

identified through an investment agency strategy, the agency and government still need to systematically support the growth of such niche products. For industries with clear

potential but a limited record, the investment agencies need to facilitate dialogue between

government and business to ensure that opportunities are identified and acted on, and that training, capacity building, and policy and infrastructure needs are met.

WORKSHOP OPINIONS AND INTERVIEWS

The Investment Opportunity Workshop articulated expectations for six sectors, and

interviews provided additional suggestions on how to promote development in some sectors. Workshop participants produced SWOT matrices covering the following areas