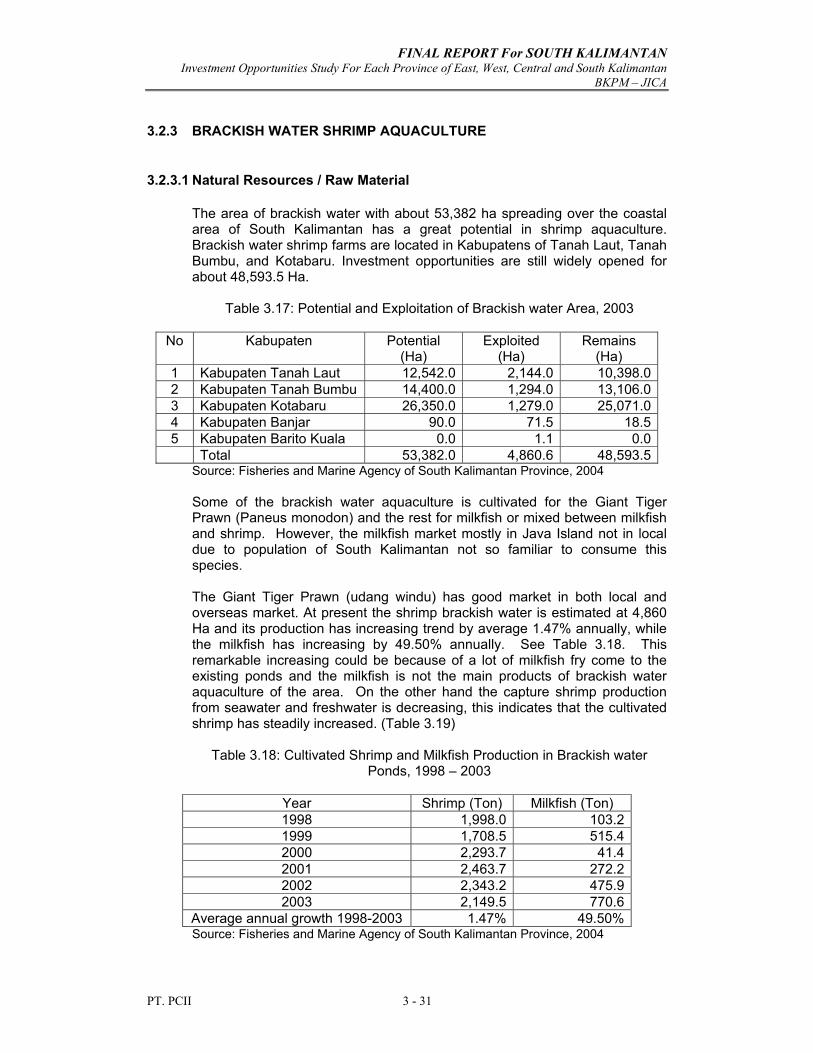

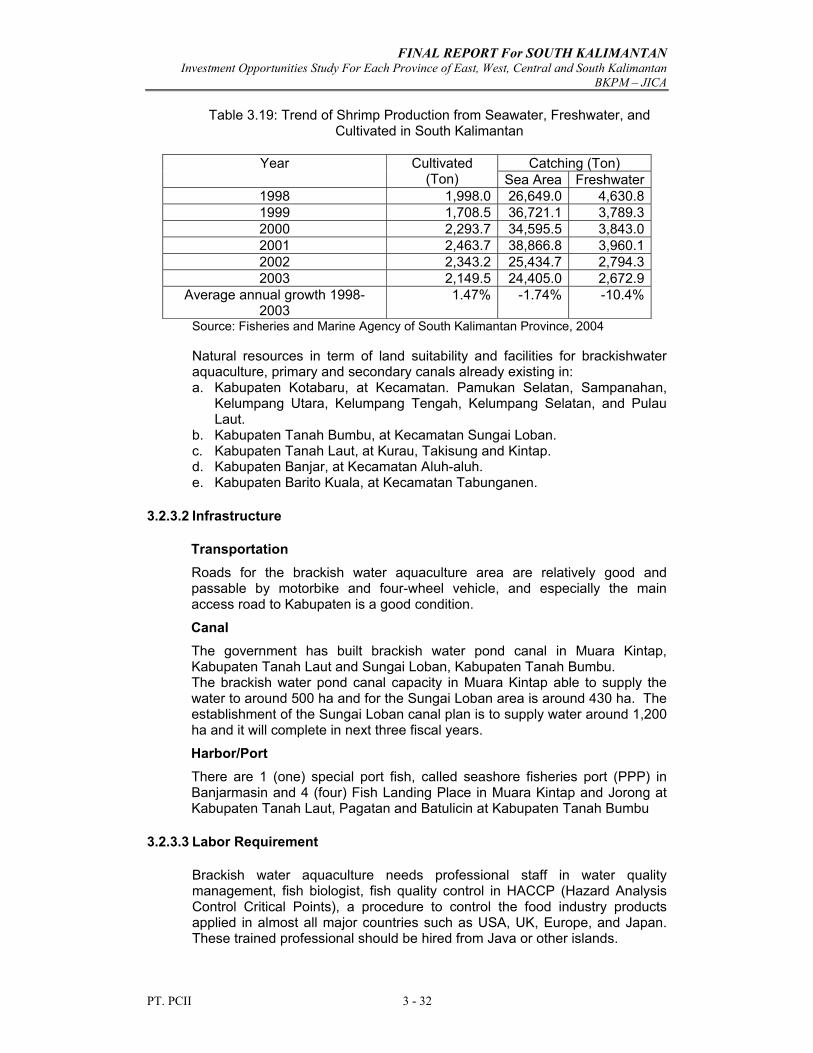

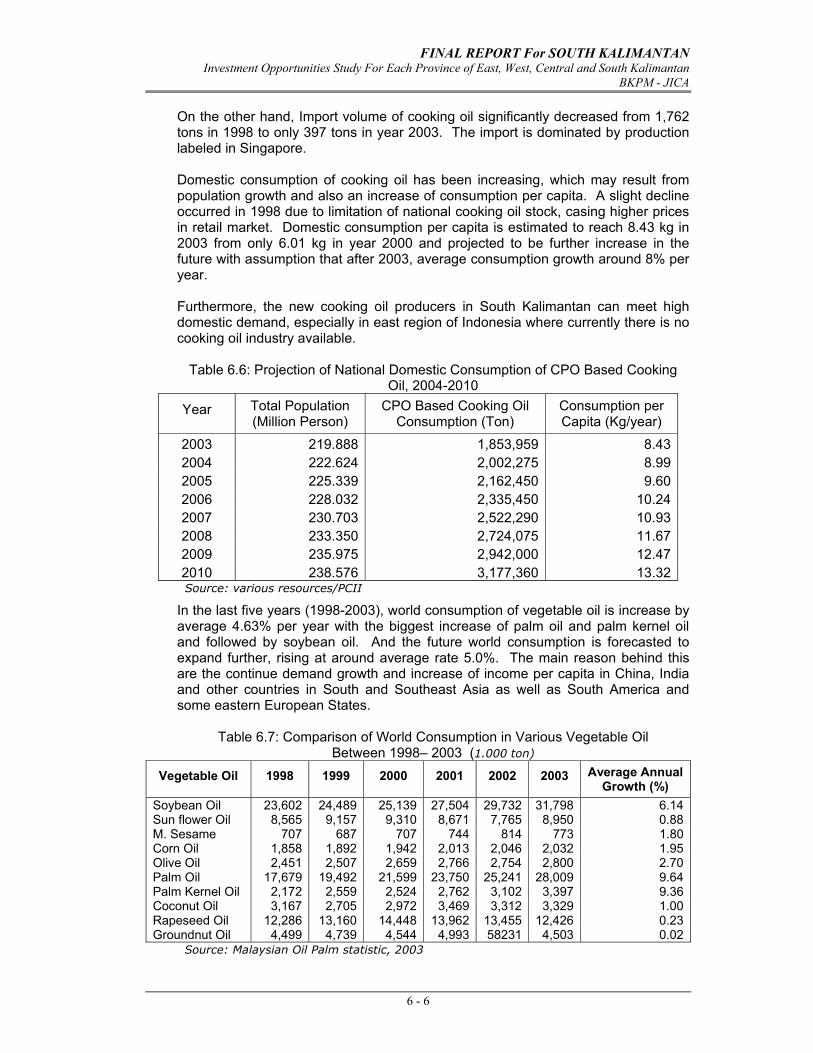

Embed Size (px)

Citation preview

M ARC H, 2 005E AST KAL IMA NTA N

INV EST MENT OP PORT UNIT IES STUD YF OR E ACH PRO VINC E OFEAS T, WE ST, C ENT RAL AND SOU TH K ALIM ANT AN

BKPM

INVESTMENT OPPORTUNITIES STUDYFOR EACH PROVINCE

OFEAST, WEST, CENTRAL AND SOUTH KALIMANTAN

INVESTMENT COORDINATING BOARD (BKPM)JAPAN INTERNATIONAL COOPERATION AGENCY

PT. PACIFIC CONSULINDO INTERNATIONAL INDONESIA(formerly PT.Mitrapacific Consulindo International)

FINAL REPORT SOUTH KALIMANTAN

March, 2005

i

TABLE OF CONTENTS

Page

I. OVERVIEW OF PROVINCIAL ECONOMY ...................................... 1 - 1

1.1. Geographical Conditions ......................................................... 1 - 1

1.2. GRDP and Growth Rate by Sector ......................................... 1 - 2

1.3. International Trade of Province ............................................... 1 - 5

1.4. Population Growth and Unemployment Rate .......................... 1 - 7

1.5. Land Price in Major Kabupaten/Kota ...................................... 1 - 9

1.6. Other Basic Economic and Industrial Indicators .................... 1 - 9

1.7. Investment Performance of PMA and PMDN ........................ 1 - 13

1.8. Industrial Map ......................................................................... 1 - 17

II. CURRENT SITUATION AND FUTURE PROSPECT OF INFRASTRUCTURE........................................................................... 2 - 1

2.1 Road ....................................................................................... 2 - 1

2.2 River ........................................................................................ 2 - 2

2.3 Harbor ...................................................................................... 2 - 6

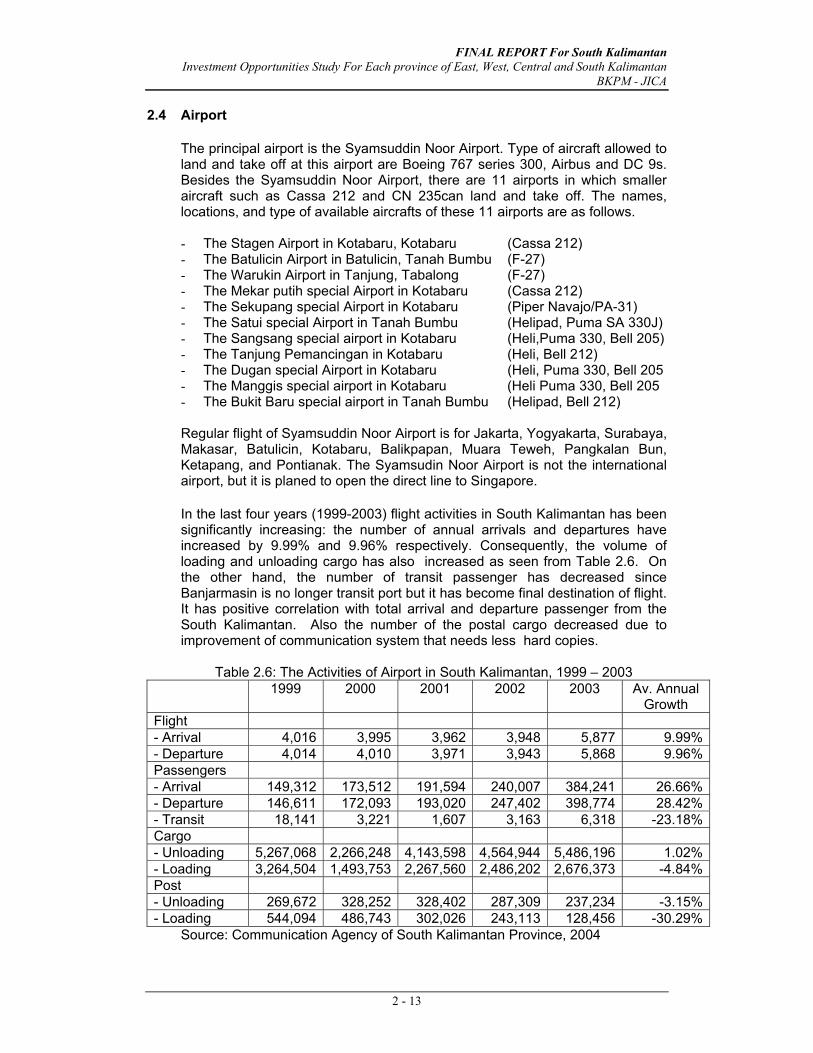

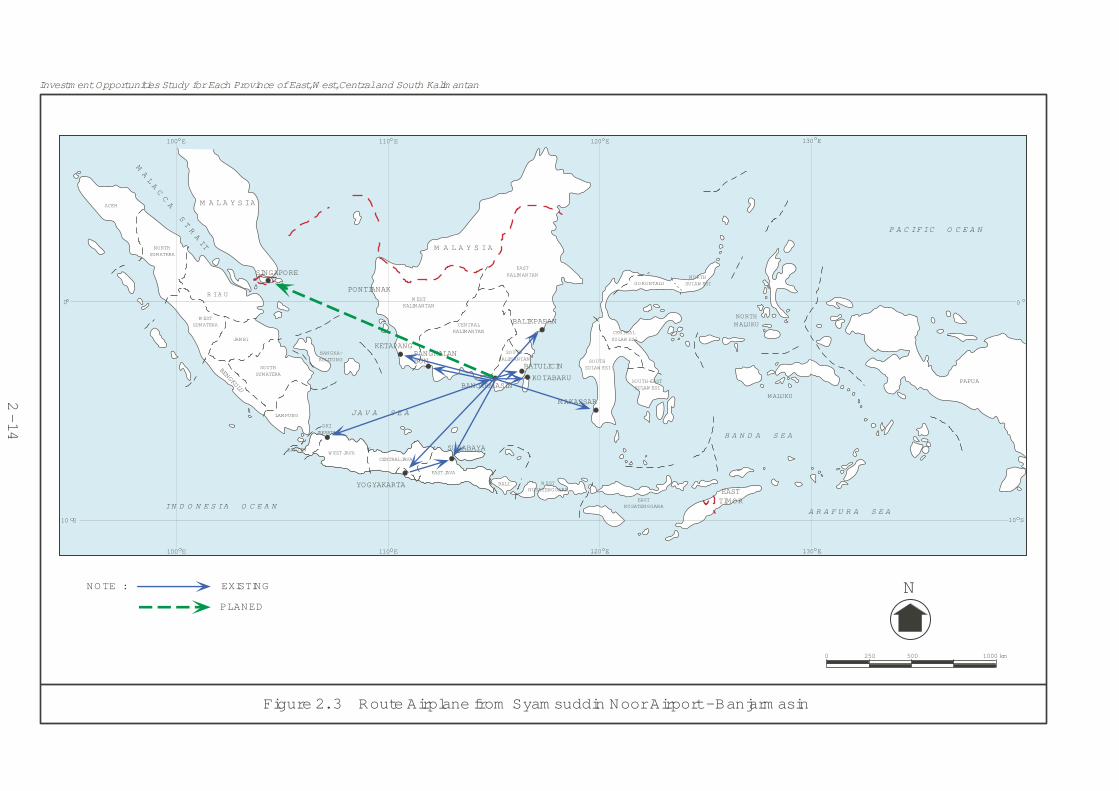

2.4. Airport ..................................................................................... 2 - 13

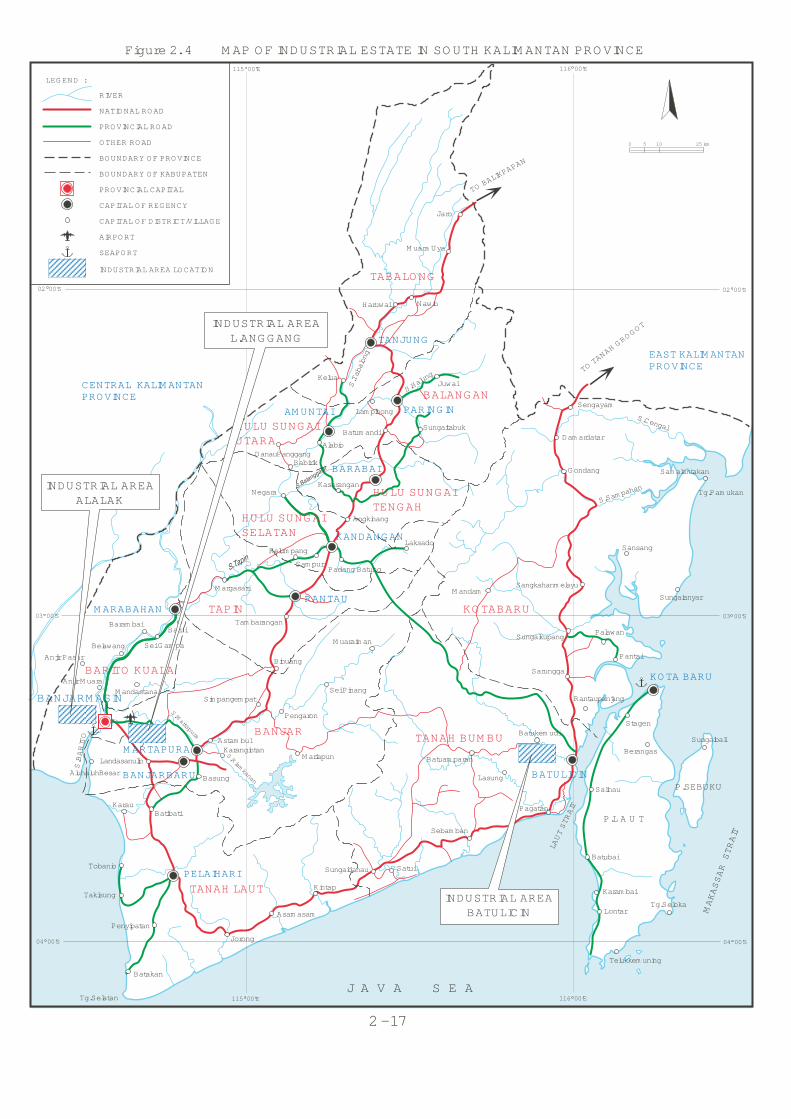

2.5. Industrial Estate ....................................................................... 2 - 15

2.6. Electricity ................................................................................. 2 - 15

2.7. Post and Telecommunication .................................................. 2 - 16

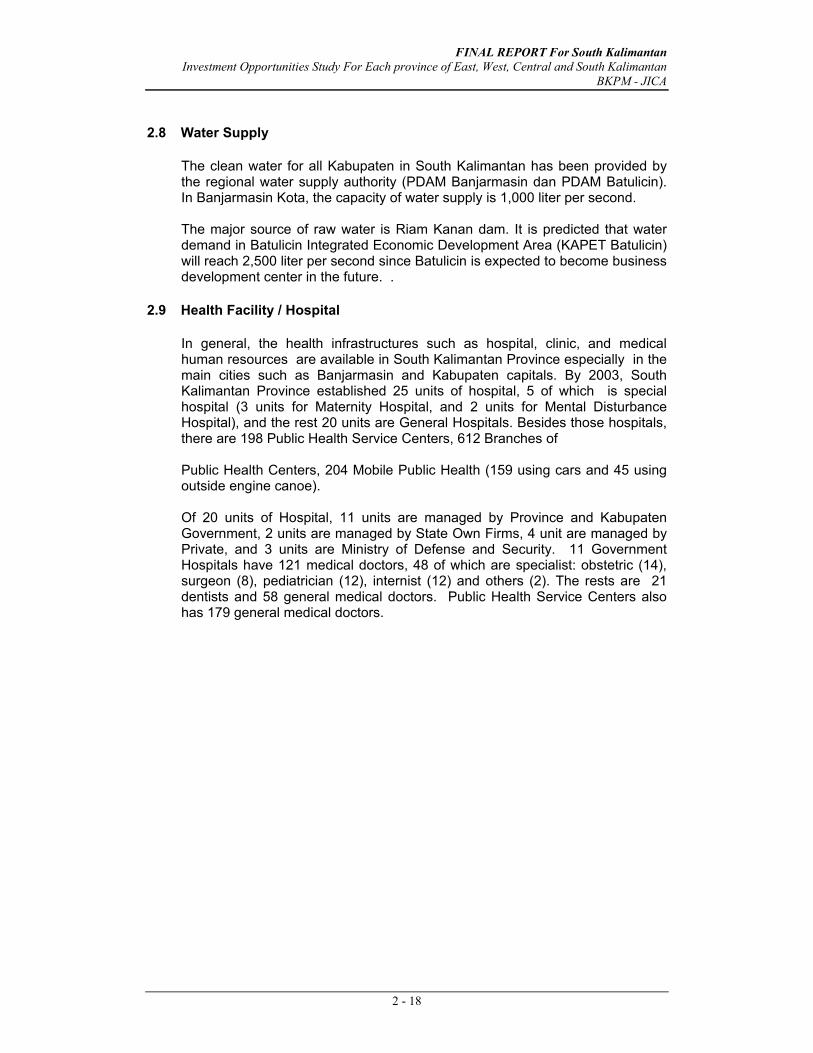

2.8. Water Supply ........................................................................... 2 - 18

2.9. Health Facility / Hospital .......................................................... 2 - 18

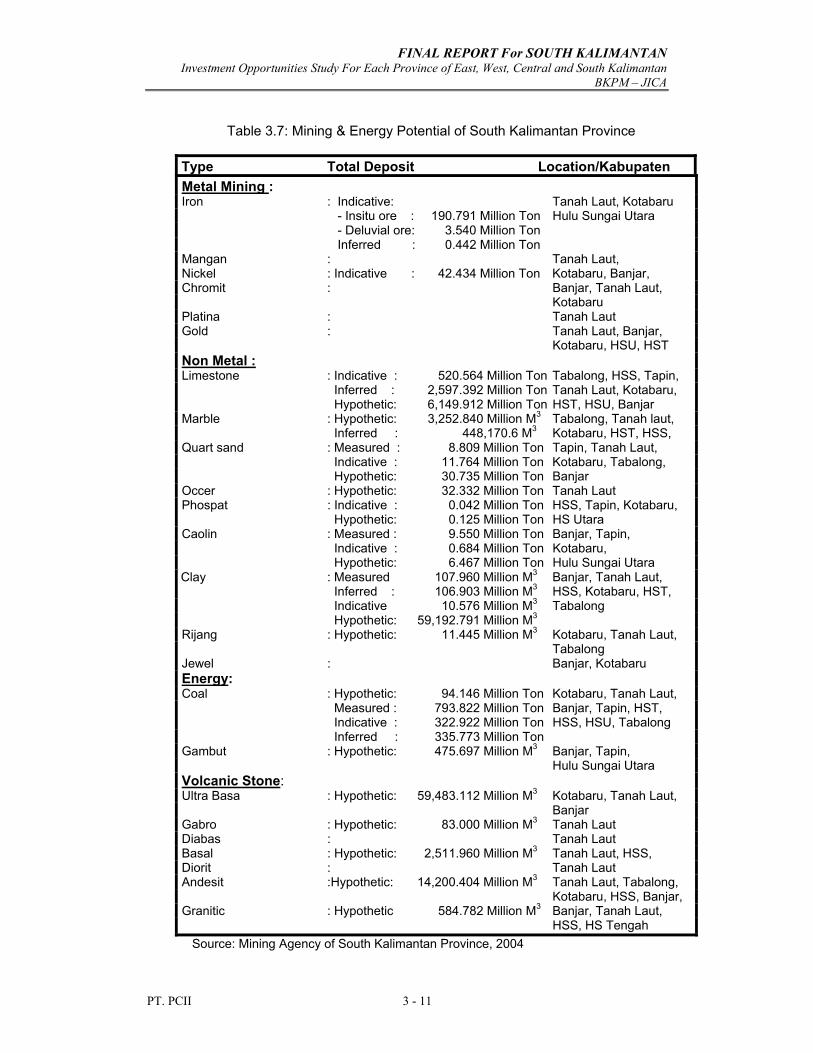

III. CURRENT SITUATION AND FUTURE PROSPECT OF MAJOR SECTORS........................................................................................... 3 - 1

3.1. Major Sector Analysis ............................................................. 3 - 1

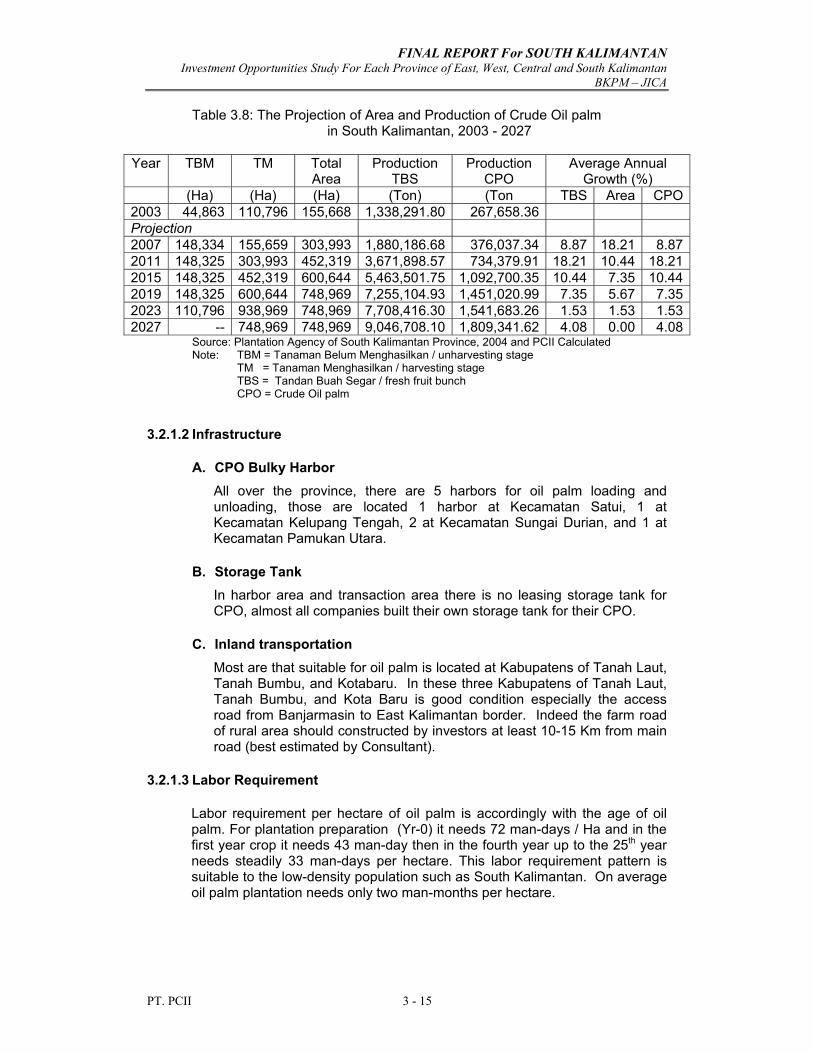

3.2. Commodity Analysis ............................................................... 3 - 14

ii

IV. CURRENT SITUATION AND FUTURE PROSPECT OF MAJOR STRATEGIC AREAS.......................................................................... 4 - 1

4.1. Major Strategic Areas by Leading Sectors ............................. 4 - 1

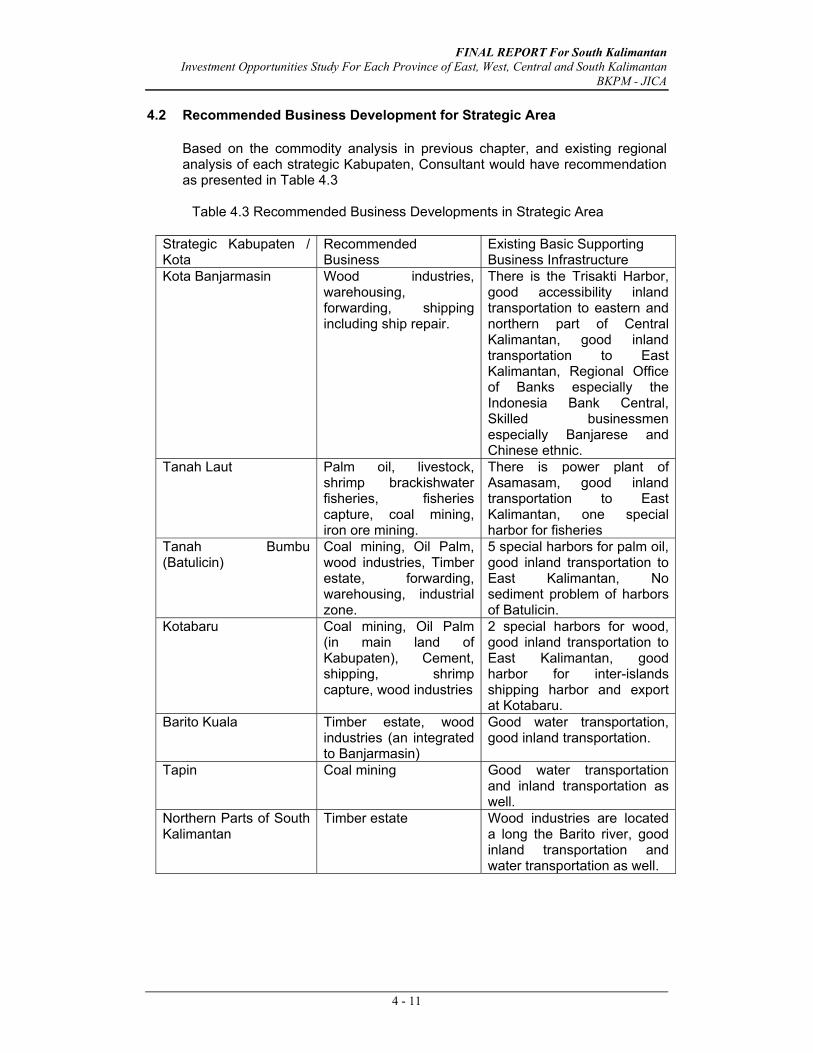

4.2. Recommended Business Development for Strategic Area .... 4 - 11

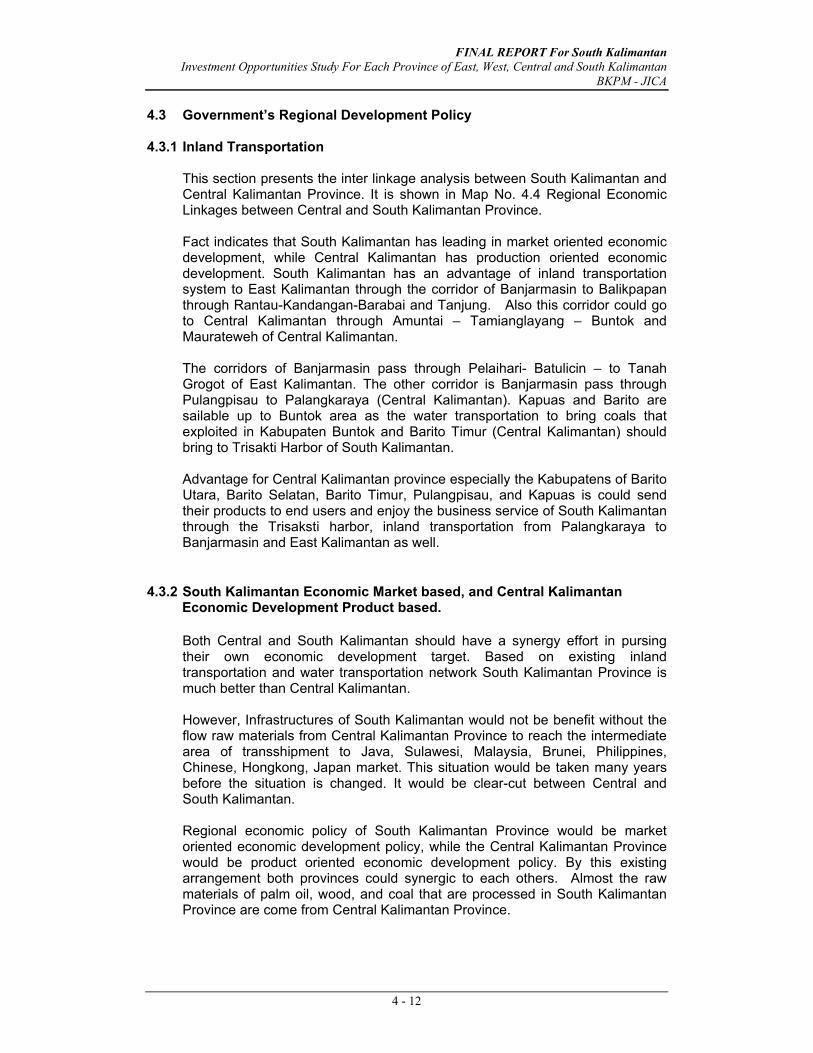

4.3. Government’s Regional Development Policy .......................... 4 - 12

4.4. Future Prospect of Major Strategic Area ................................ 4 - 15

4.5. Batulicin Industrial Development Bonded Zone / KAPET

Batulicin ................................................................................... 4 - 16

V. CONTRAINTS IN INVESTMENT CLIMATE ...................................... 5 - 1

5.1. Infrastructure Issues ............................................................... 5 - 1

5.2. Land Related Issues ................................................................ 5 - 2

5.3. Lack of Government’s Facility/Support .................................... 5 - 4

5.4. Labor Cost ............................................................................... 5 - 5

5.5. Land Price in Major Kabupaten/Kota ....................................... 5 - 6

5.6. Government ‘s Efforts............................................................... 5 - 6

5.7. Proposal ................................................................................... 5 - 6

VI. PROPOSAL OF PROSPECTIVE PROJECTS .................................. 6 - 1

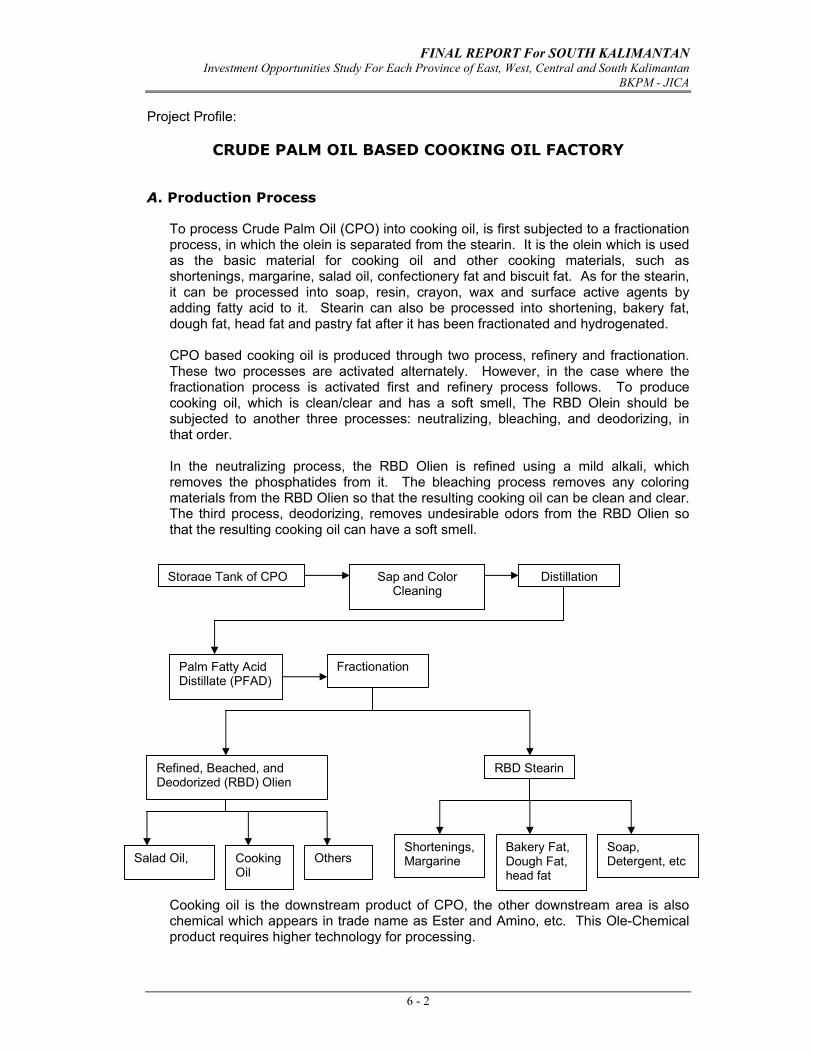

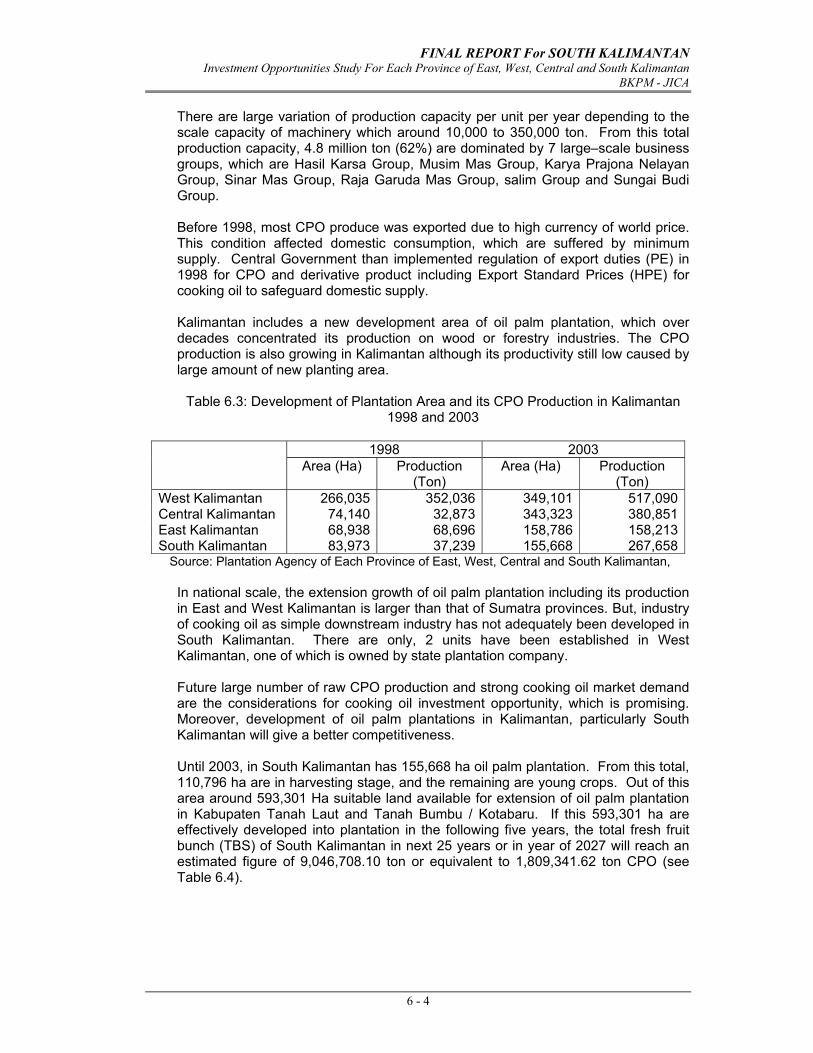

Crude Palm Oil Based Cooking Oil Factory ....................................... 6 - 2

A. Production Process ............................................................ 6 - 2

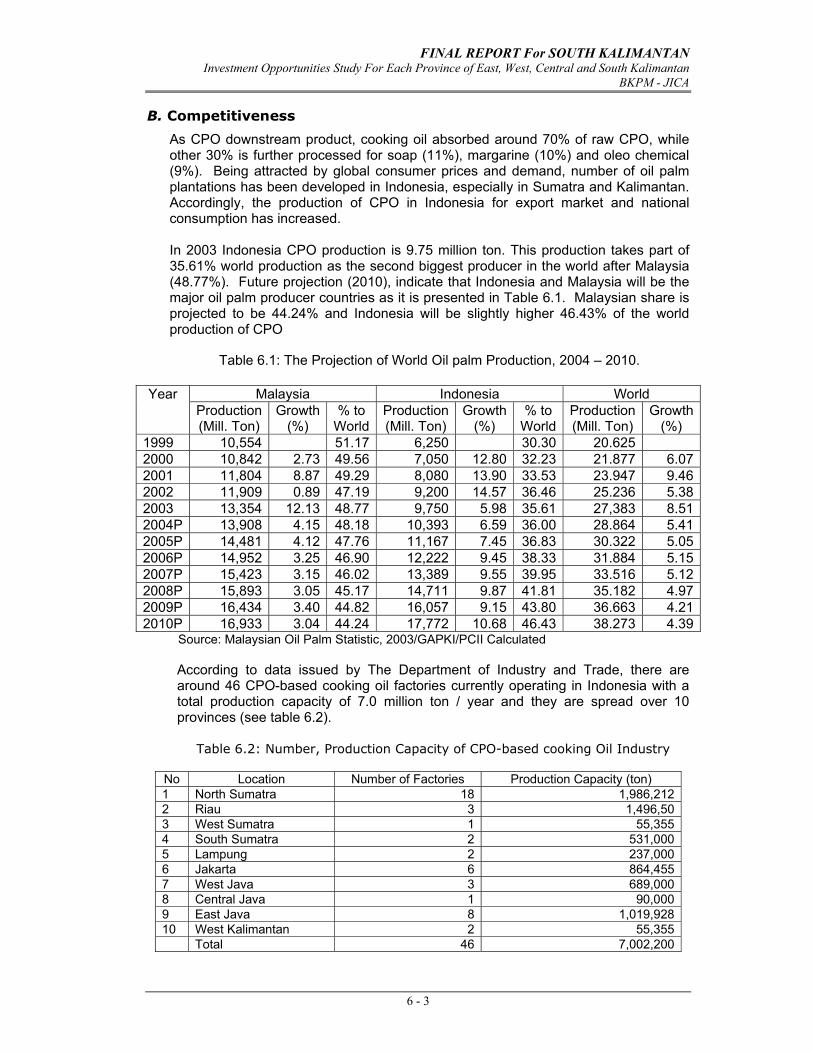

B. Competitiveness ................................................................. 6 - 3

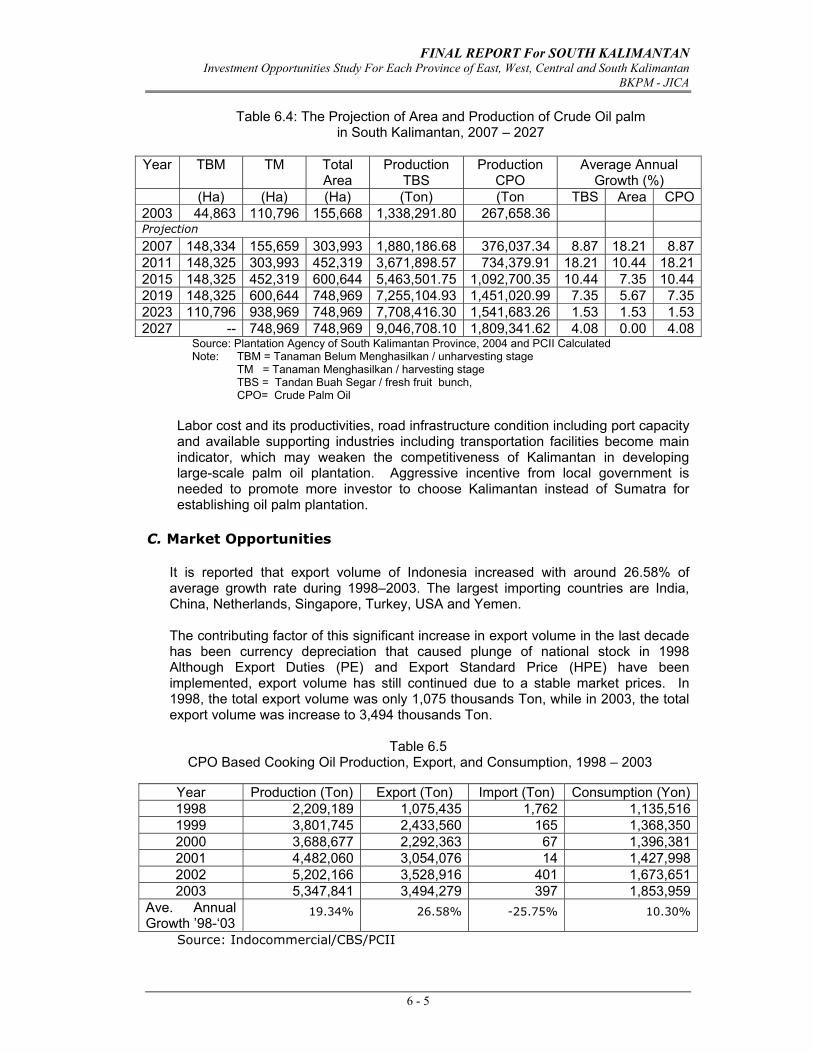

C. Market Opportunities .......................................................... 6 - 5

D. Potential Location ............................................................... 6 - 7

E. Infrastructure and Business Support Facilities................... 6 - 7

F. Proposed Business Scale................................................... 6 - 8

H. Cost of Factor ..................................................................... 6 - 8

Rubber Nursery, Replanting and Trading Business ........................... 6 - 10

A. Production Process ............................................................ 6 - 10

B. Competitiveness ................................................................. 6 - 10

C. Market Opportunities .......................................................... 6 - 11

D. Potential Location ............................................................... 6 - 12

E. Infrastructure and Business Support Facilities................... 6 - 12

F. Proposed Business Scale................................................... 6 - 12

iii

G. Cost of Factors ................................................................... 6 - 12

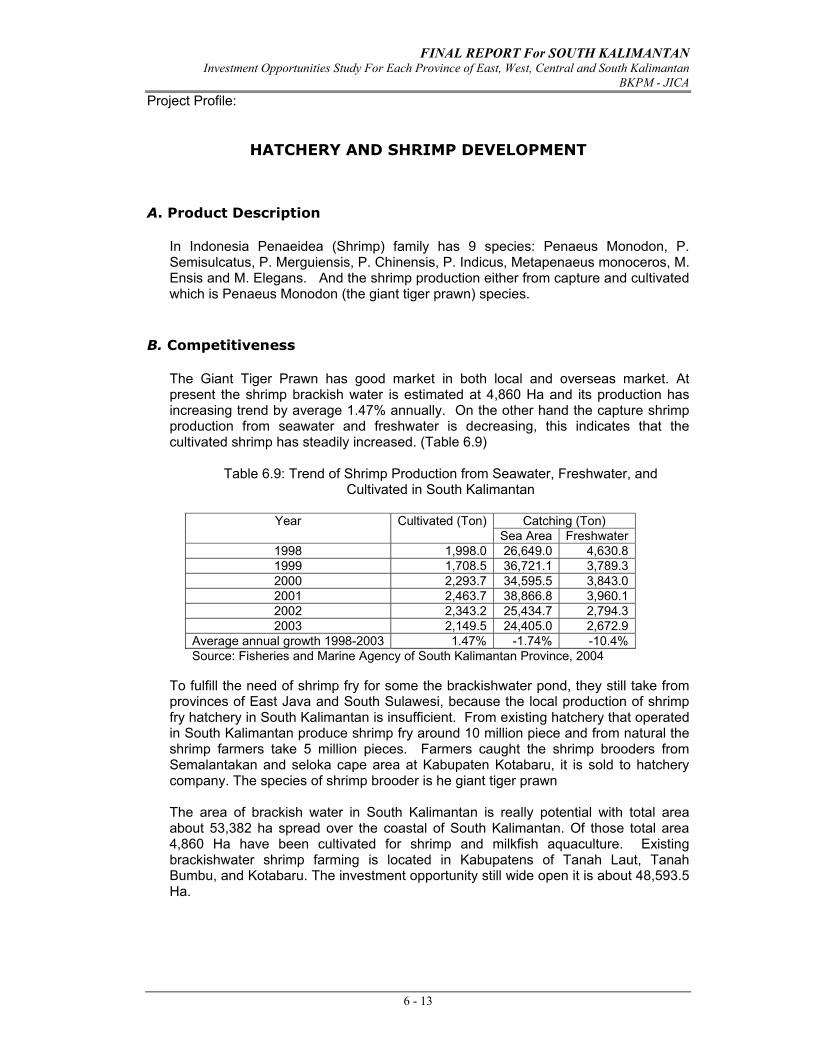

Hatchery and Shrimp Development.................................................... 6 - 13

A. Production Description ....................................................... 6 - 13

B. Competitiveness ................................................................. 6 - 13

C. Market Opportunities .......................................................... 6 - 14

D. Potential Location ............................................................... 6 - 15

E. Infrastructure and Business Support Facilities................... 6 - 15

F. Proposed Business Scale................................................... 6 - 16

G. Cost of Factors ................................................................... 6 - 16

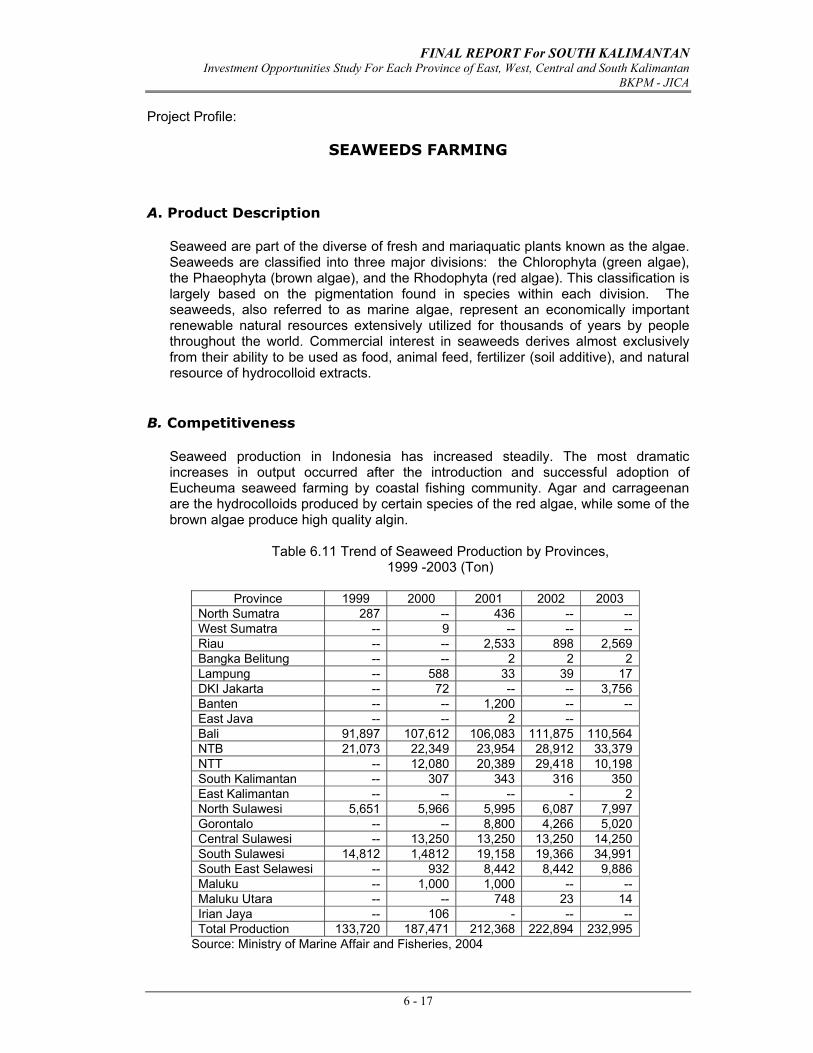

Seaweeds Farming ............................................................................. 6 - 17

A. Production Description ....................................................... 6 - 17

B. Competitiveness ................................................................. 6 - 17

C. Market Opportunities .......................................................... 6 - 18

D. Potential Location ............................................................... 6 - 19

E. Infrastructure and Business Support Facilities................... 6 - 20

F. Proposed Business Scale................................................... 6 - 20

G. Cost of Factors ................................................................... 6 - 20

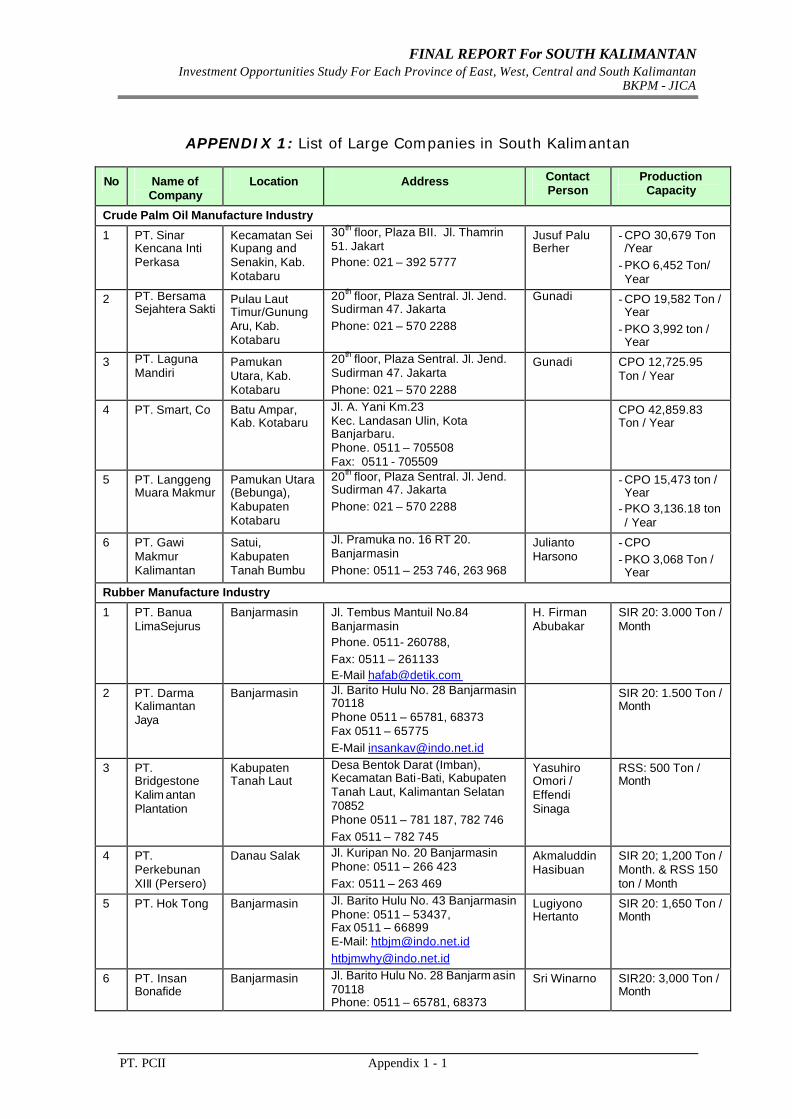

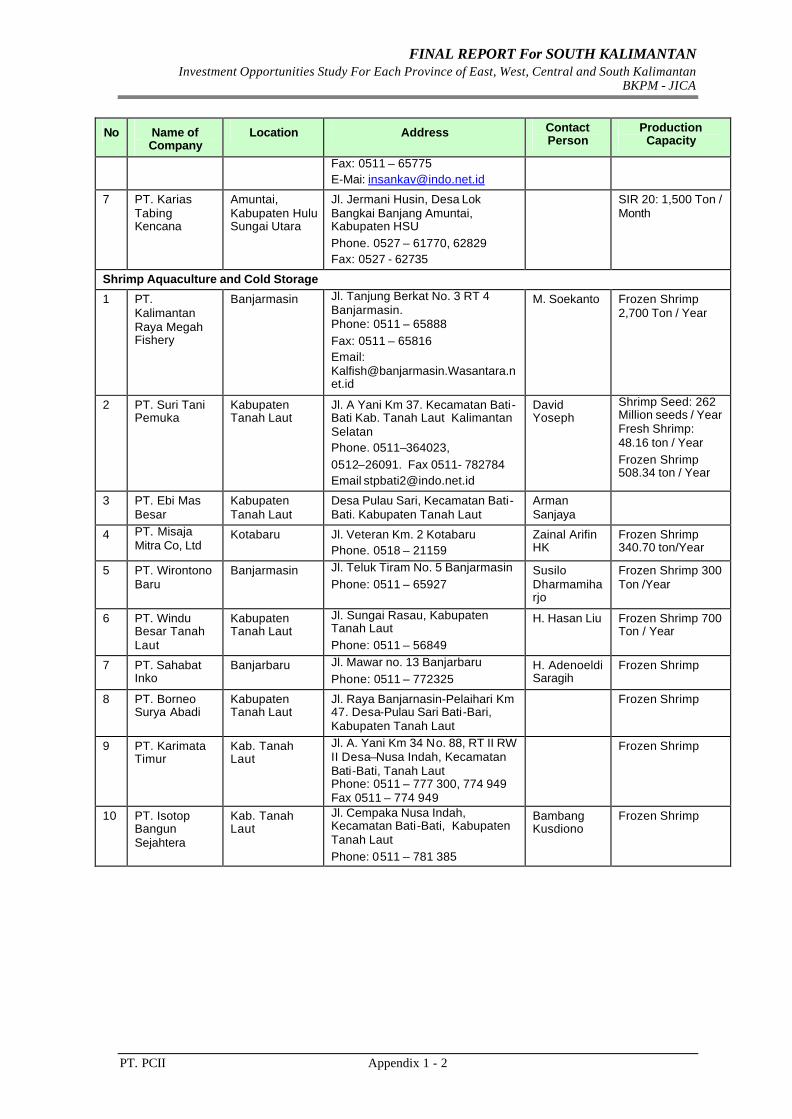

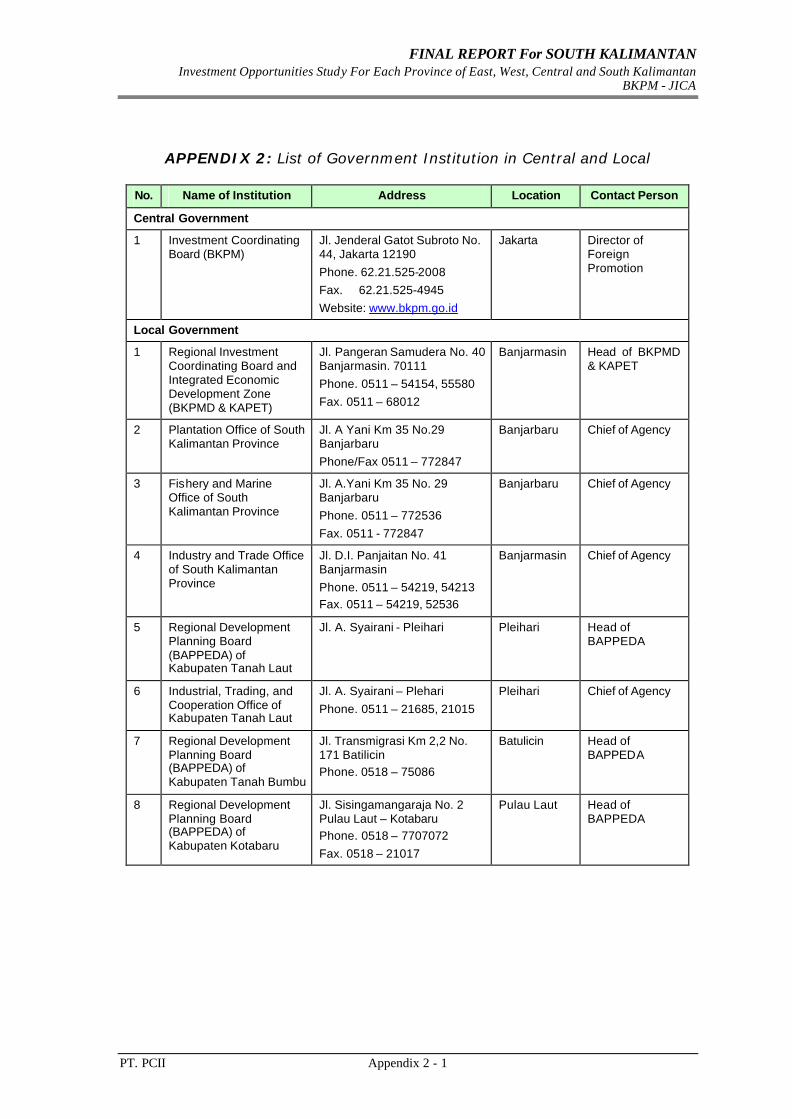

APPENDIX

List of Local Business and Contact Point

iv

LIST OF TABLES

Page Table 1-1. The Area of Kabupaten/Kota by Altitude Class (Ha), 2002 ... 1 - 1 Table 1-2. The Area of Kabupaten/Kota by Slope Class (Ha), 2002 ....... 1 - 1 Table 1-3. Total GRDP at Constant 1993 Prices by Kalimantan Provinces,

1999 – 2003 (Mill. Rupiah) ...................................................... 1 - 2

Table 1-4. GRDP per Capita at Constant 1993 Prices by Kalimantan

Provinces, 1999 – 2003 (Mill. Rupiah) .................................... 1 - 3

Table 1-5. The Percentage Growth and Structure of South Kalimantan

Provinces at 1993 Constant Prices by Economic sector, ....... 1 - 4

Table 1-6. Export – Import of South Kalimantan, 1993 – 2003 ................ 1 - 5

Table 1-7. Percentage of Export Value by Commodity of South -

Kalimantan, 1993 - 2003 (%) .................................................. 1 - 6

Table 1-8. Total and Average Growth Population in South Kalimantan ... 1 - 7

Table 1-9. Employment of more than 10 years old by Sector, 2003 ....... 1 - 8

Table 1-10 Rupiah and Foreign Currency Credit by Bank Group ............ 1 - 11

Table 1-11 Rupiah and Foreign Currency Credit by Purpose ................... 1 - 11

Table 1-12 Bank Credit Development by Economic Sector ...................... 1 - 12

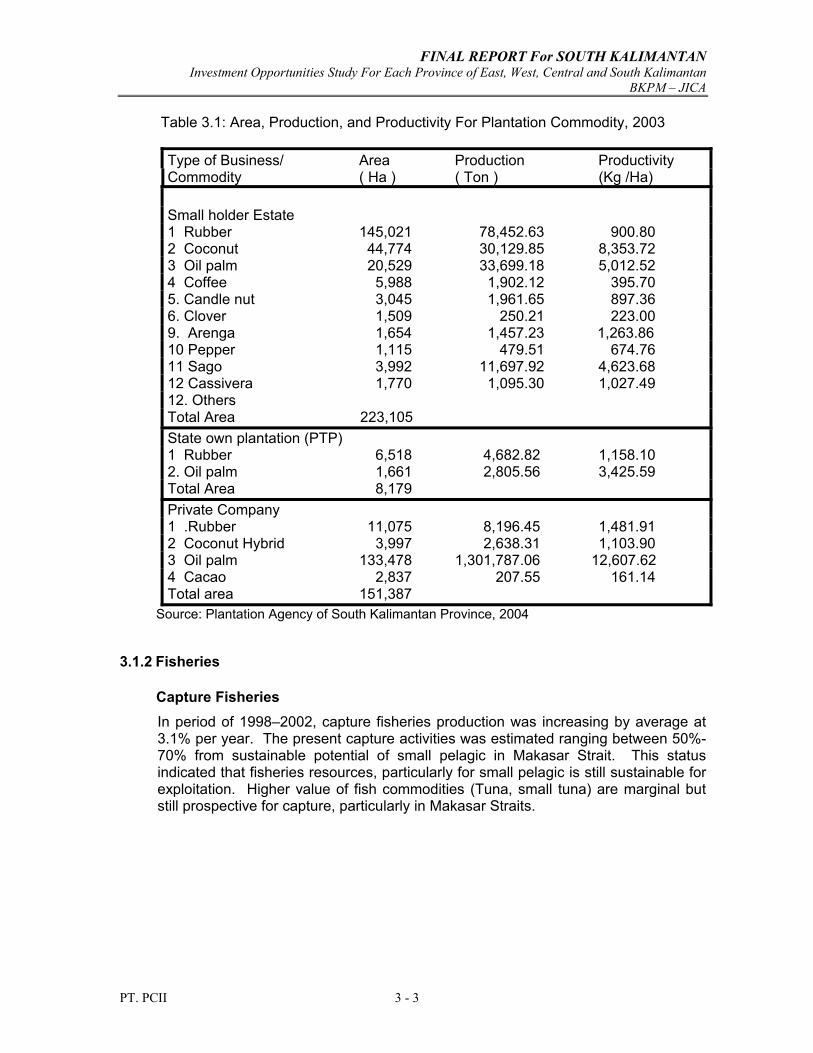

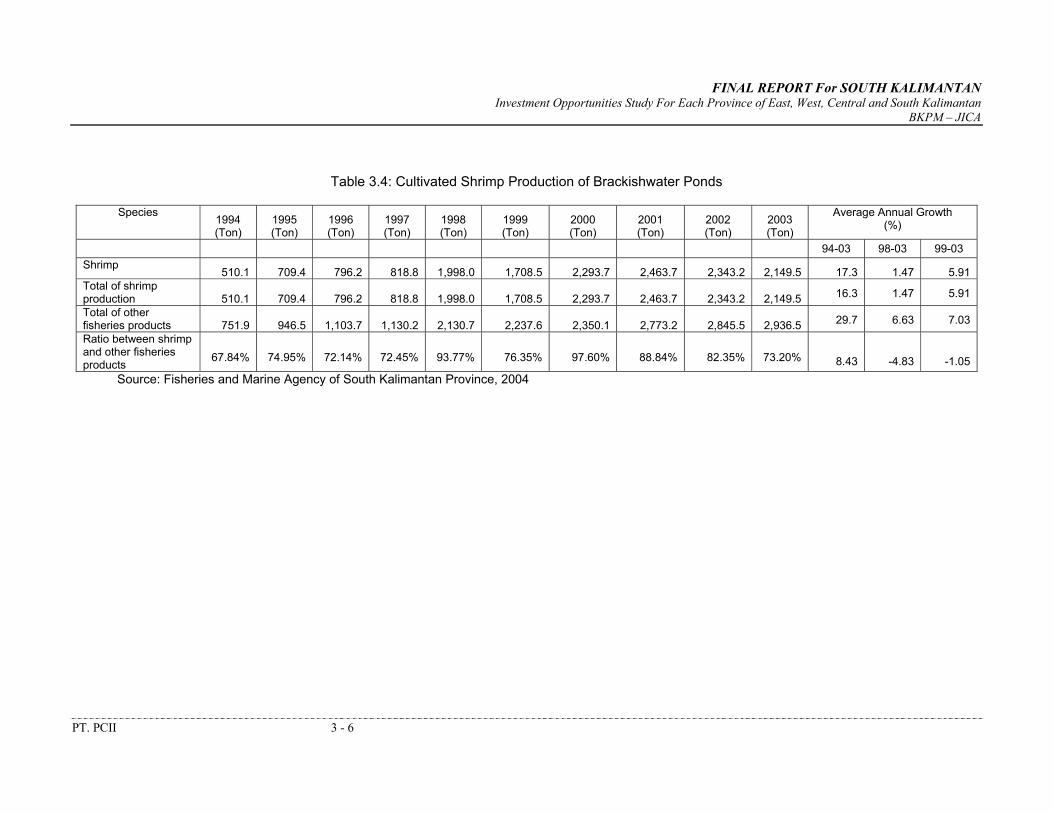

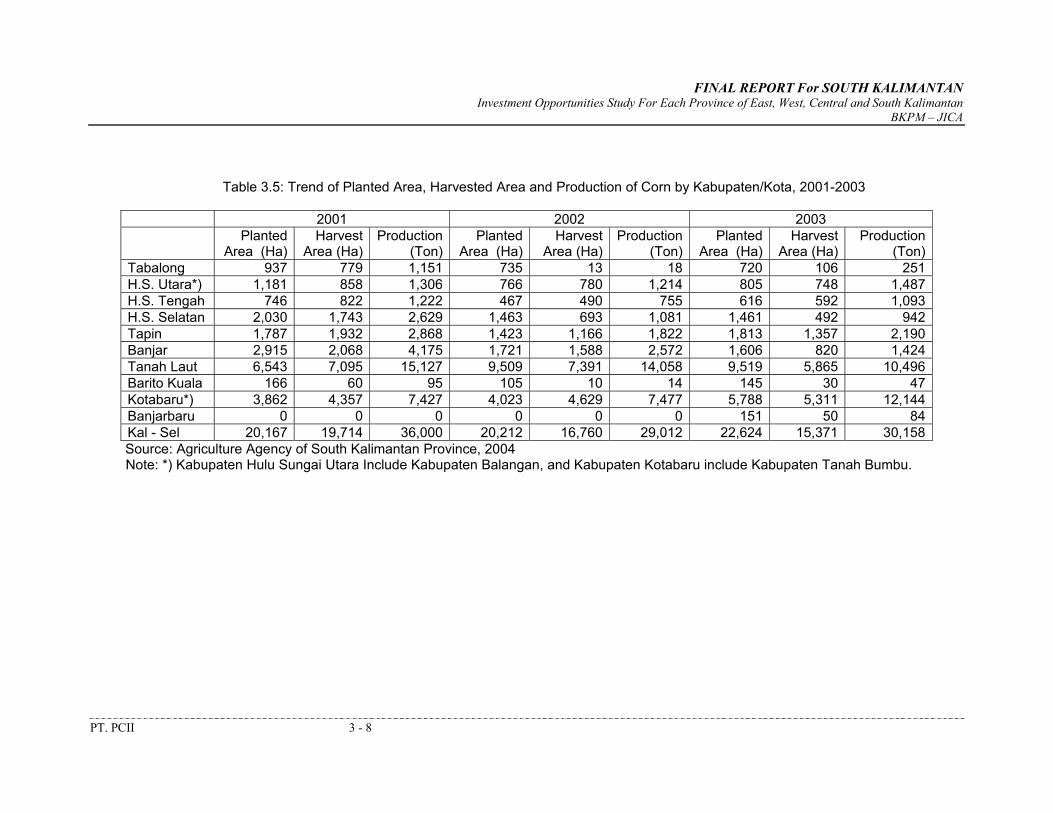

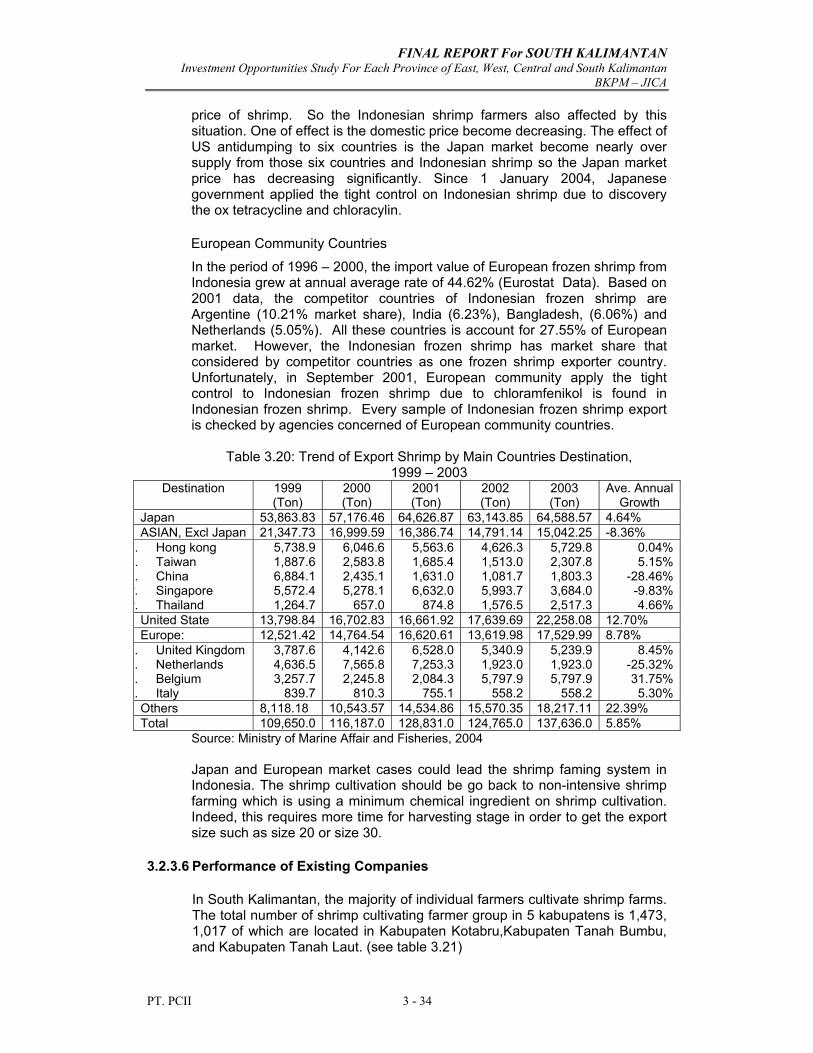

Table 2-1. Road Condition, South Kalimantan, 2004 .............................. 2 - 1 Table 2-2. River and Canal in South Kalimantan Province ...................... 2 - 3 Table 2-3. Special Ports in South Kalimantan, 2004 ............................... 2 - 7 Table 2-4. Profile of Selected Main Harbor in South Kalimantan ............ 2 - 8 Table 2-5. Recapitulation of Cargo and Passenger Flow In South Kalimantan Harbors ................................................................ 2 - 10 Table 2-6. The Activities of Airport in South Kalimantan, ........................ 2 - 13 Table 3-1. Area, Production & Productivity for Plantation Commodity, ... 3 - 3 Table 3-2. Capture Shrimp Production of Sea Area ................................ 3 - 5 Table 3-3. Capture Shrimp Production of Fresh Area............................... 3 - 5 Table 3-4. Cultivated Shrimp Production of Brackish Ponds .................... 3 - 6 Table 3-5. Trend of Planted area, Harvested Area and Production of Corn

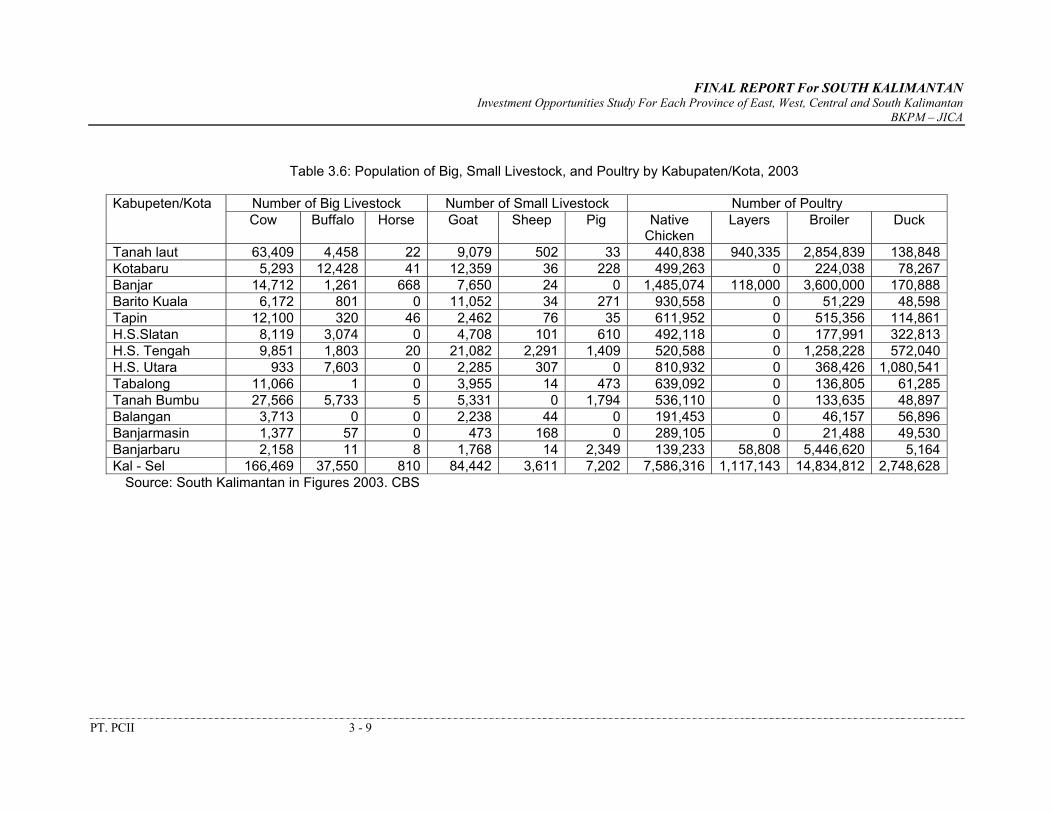

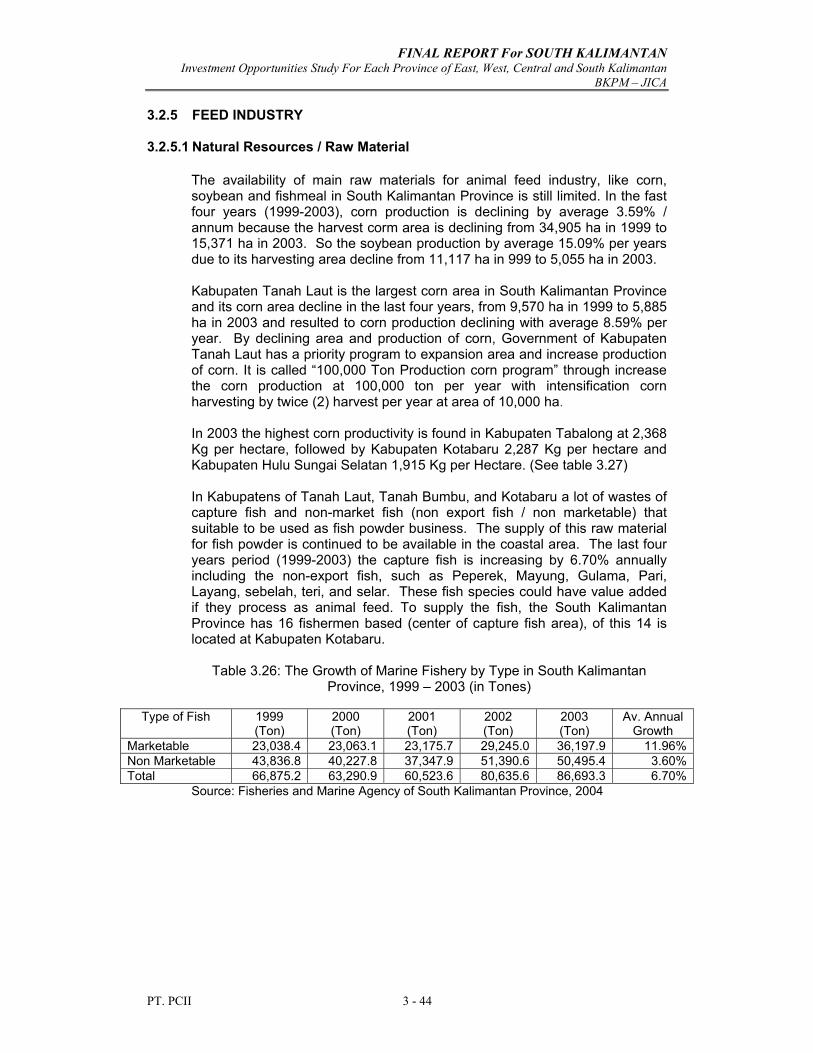

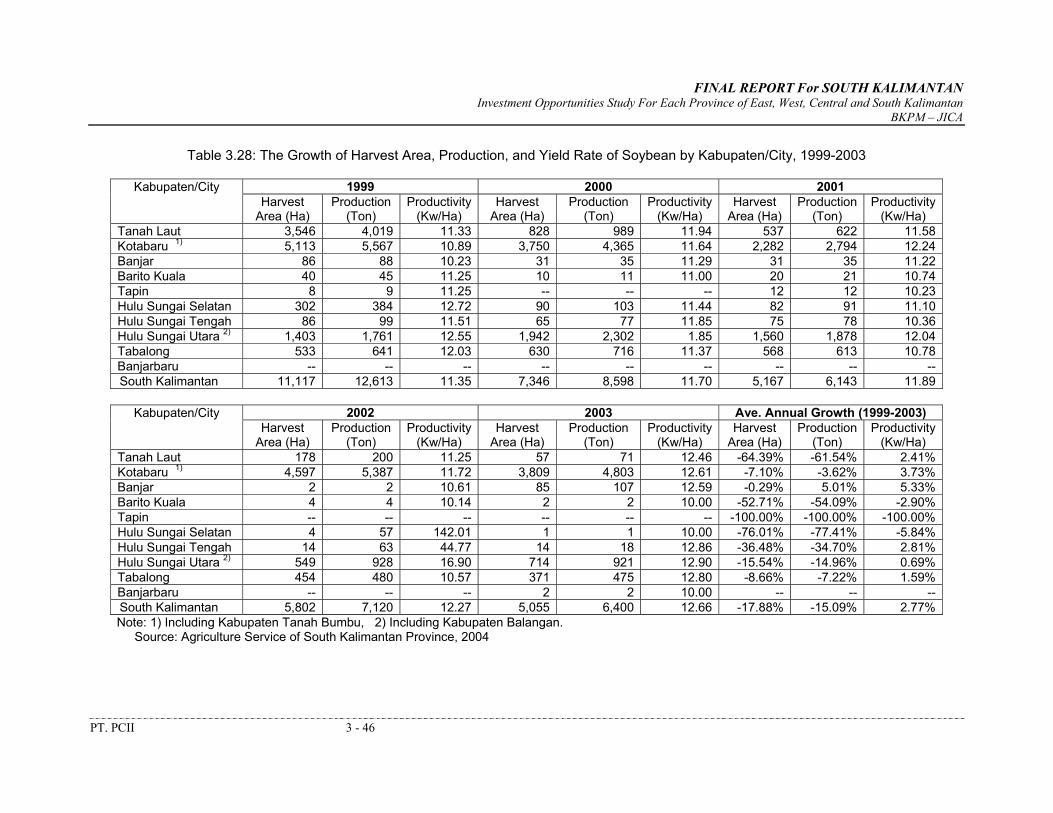

by Kabupaten/Kota, 2001 - 2003 ............................................. 3 - 8 Table 3-6. Population of Big, Small Ruminant & Poultry, 2003 ............... 3 - 9

v

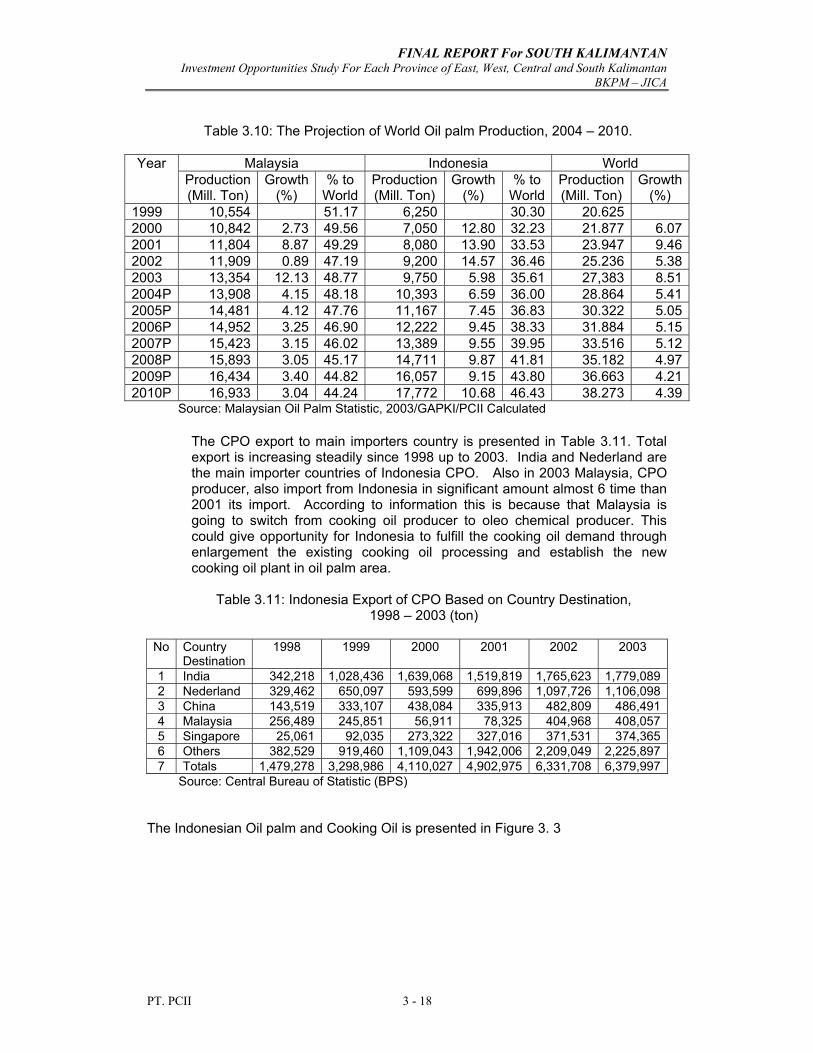

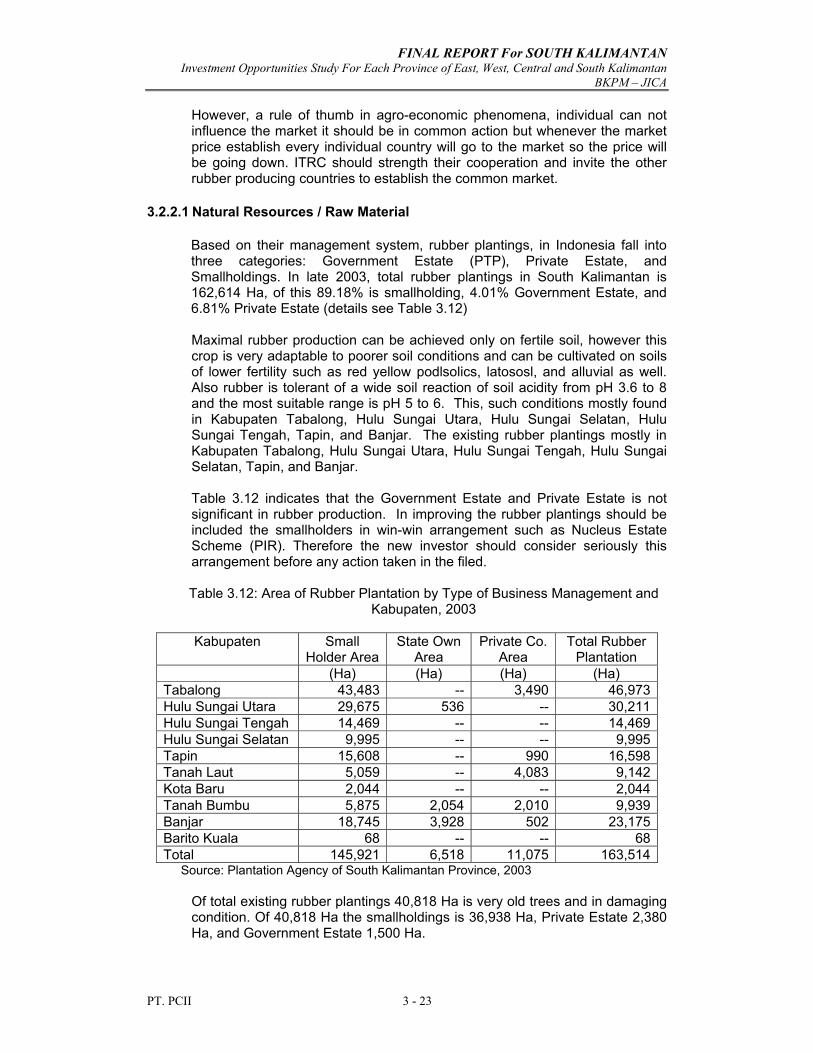

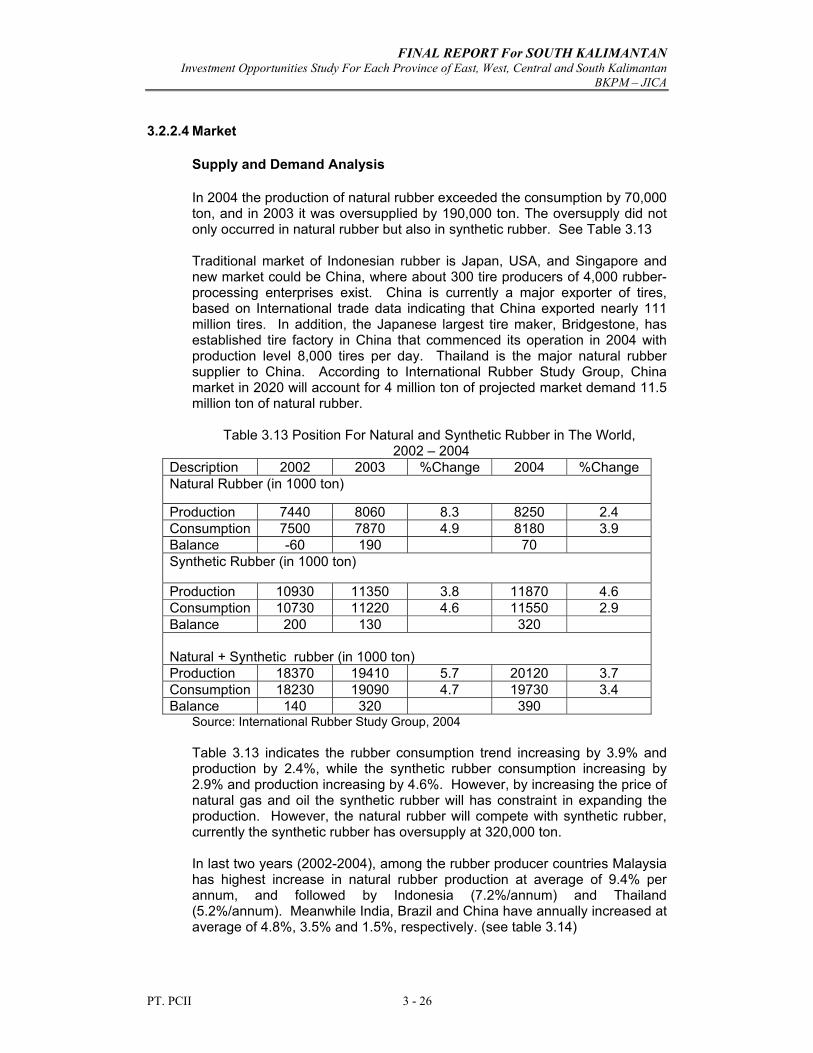

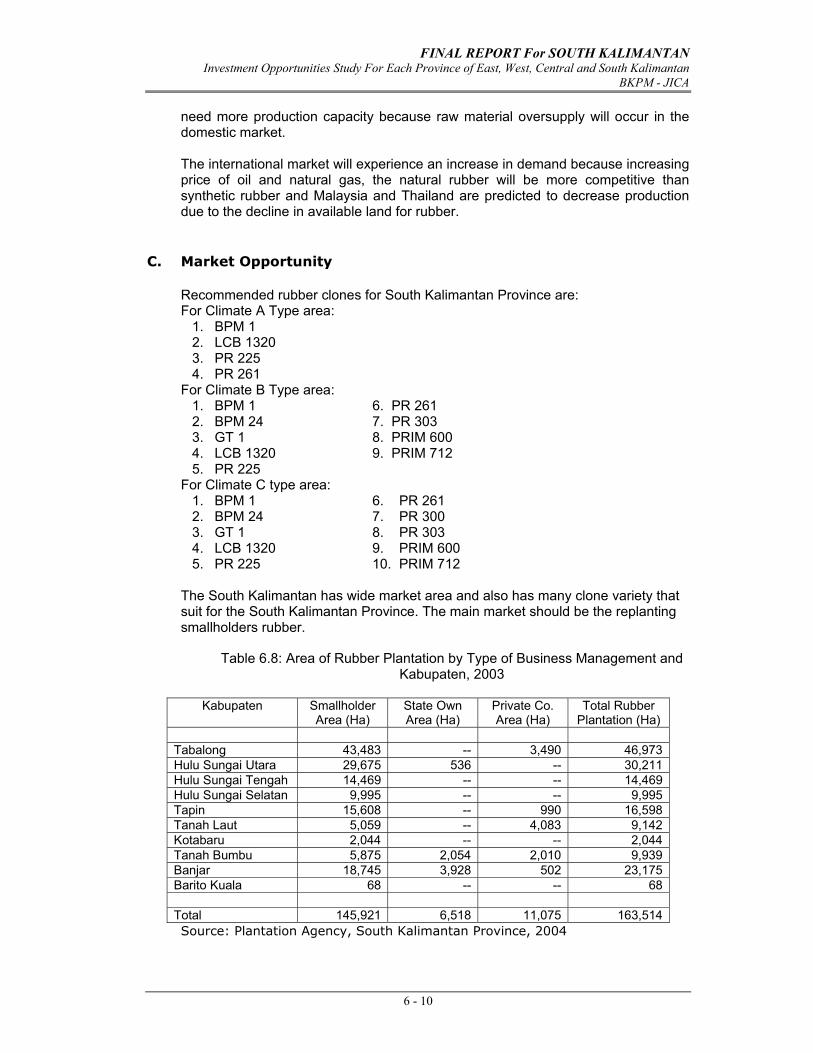

Table 3-7. Mining & Energy Potential of South Kalimantan Province....... 3 - 11 Table 3-8. The Projection of Area & Production CPO, 2003-2027 ........... 3 - 15 Table 3-9. World Vegetable Oil Consumption, 2003................................. 3 - 17 Table 3-10. The Projection of World Oil Palm Production, 2004–2010 ...... 3 - 18 Table 3-11. Indonesia Export CPO Based on Country Destination ........... 3 - 18 Table 3-12. Area of Rubber Plantation by Type of Business Management

and Kabupaten, 2003 .............................................................. 3 - 23 Table 3-13. Position for Natural and Synthetic Rubber in The World ......... 3 - 26 Table 3-14. The Trend of Natural Rubber Production................................. 3 - 27 Table 3-15. Natural Rubber Consumption by Major Countries .................. 3 - 28 Table 3-16. Rubber Factory in South Kalimantan, 2004............................. 3 - 29 Table 3-17. Potential and Exploitation of Brackish Water Area, 2003........3 - 31 Table 3-18. Cultivated Shrimp & Milkfish Production in BrackishWater .....3 - 31 Table 3-19. Trend of Shrimp Production from Seawater, Freshwater

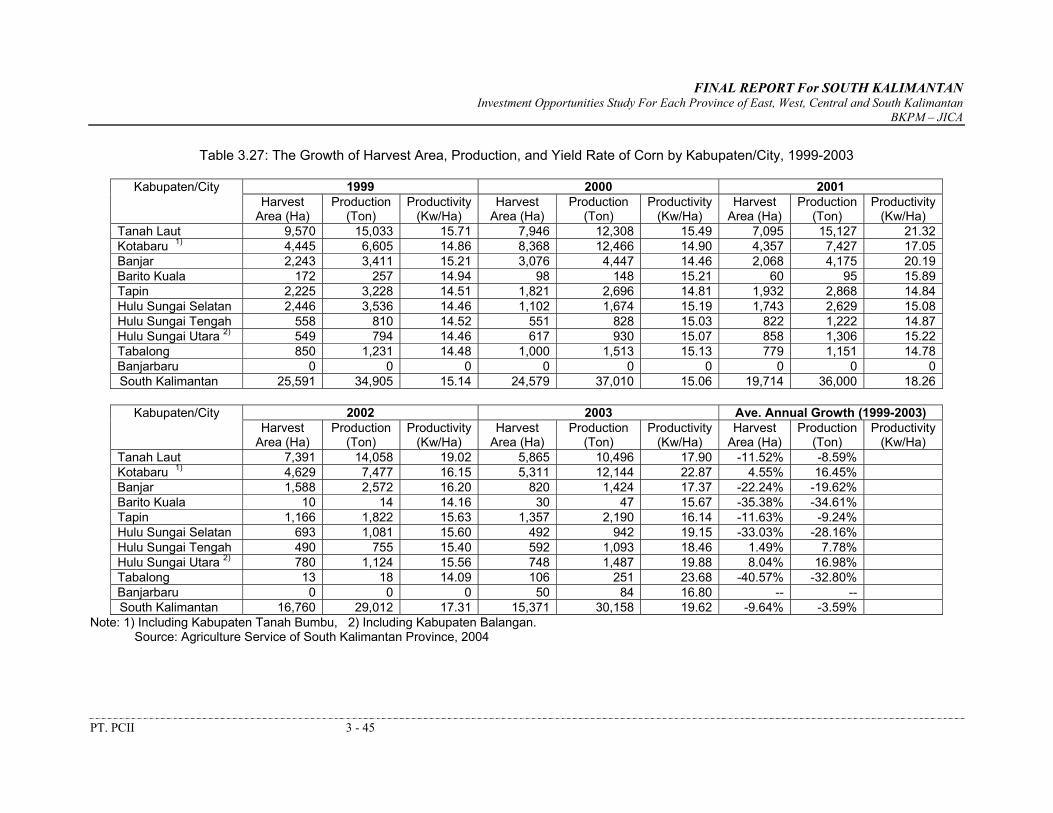

And Cultivated in South Kalimantan ........................................3 - 32 Table 3-20. Trend of Export Shrimp by Main Countries Destination ..........3 - 34 Table 3-21. Number of Fisheries Group by Category of Pond Area..........3 - 35 Table 3-22. Number of Fisheries Group by Type of Brackish Water ..........3 - 35 Table 3-23. Trend of Seaweed Production by Provinces ...........................3 - 37 Table 3-24. Cultivated Seaweed Area by Main Province, 2003 .................3 - 38 Table 3-25. Trend of Seaweed Export by Main Countries Destination.......3 - 40 Table 3-26. The Growth of Marine Fishery by Type in South Kalimantan..3 - 44 Table 3-27. The Growth of Harvest area, Production and Yield Rate of Corn

by Kabupaten/City, 1999 - 2003 ..............................................3 - 45 Table 3-28. The Growth of Harvest area, Production and Yield Rate of

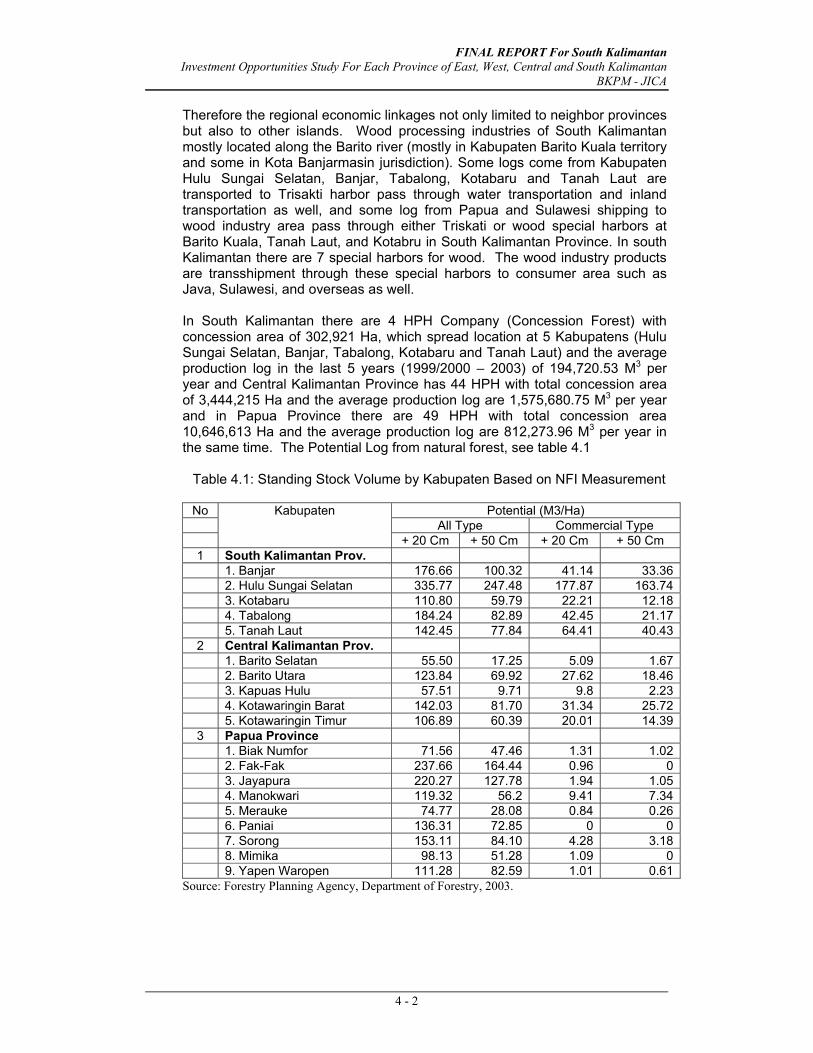

Soybean by Kabupaten/City, 1999 - 2003...............................3 - 46 Table 3-29. Reserve of Industrial Minerals in South Kalimantan................3 - 49 Table 3-30. Domestic Consumption of Cement in Indonesia .....................3 - 51 Table 3-31. Export of Indonesia Cement Industry ......................................3 - 52 Table 4-1. Standing Stock Volume by Kabupaten Based on NFI

Measurement ...........................................................................4 - 2 Table 4-2. List of HTI Management Right (HPHTI) ..................................4 - 4 Table 4-3. Recommended Business Development for Strategic Area .....4 - 11 Table 6-1. The Projection of World Oil Palm Production ..........................6 - 3 Table 6-2. Number, Production Capacity of Cooking Oil Industry ...........6 - 3

vi

Table 6-3. Development of Plantation area and Its CPO Production ......6 - 4 Table 6-4. The Projection of Area and Production of Crude Oil Palm .....6 - 5 Table 6-5. CPO Based Cooking Oil Production, Export, Import, and

Consumption, 1998 – 2003 .....................................................6 - 5 Table 6-6. Projection of Domestic Consumption of CPO Based

Cooking Oil ..............................................................................6 - 6 Table 6-7. Comparison of World Consumption in Various Vegetable Oil............................................................................6 - 6 Table 6-8. Area of Rubber Plantation by Type of Business Management and Kabupaten, 2003 ........................................6 - 10 Table 6-9. Trend of Shrimp Production from Seawater, Freshwater

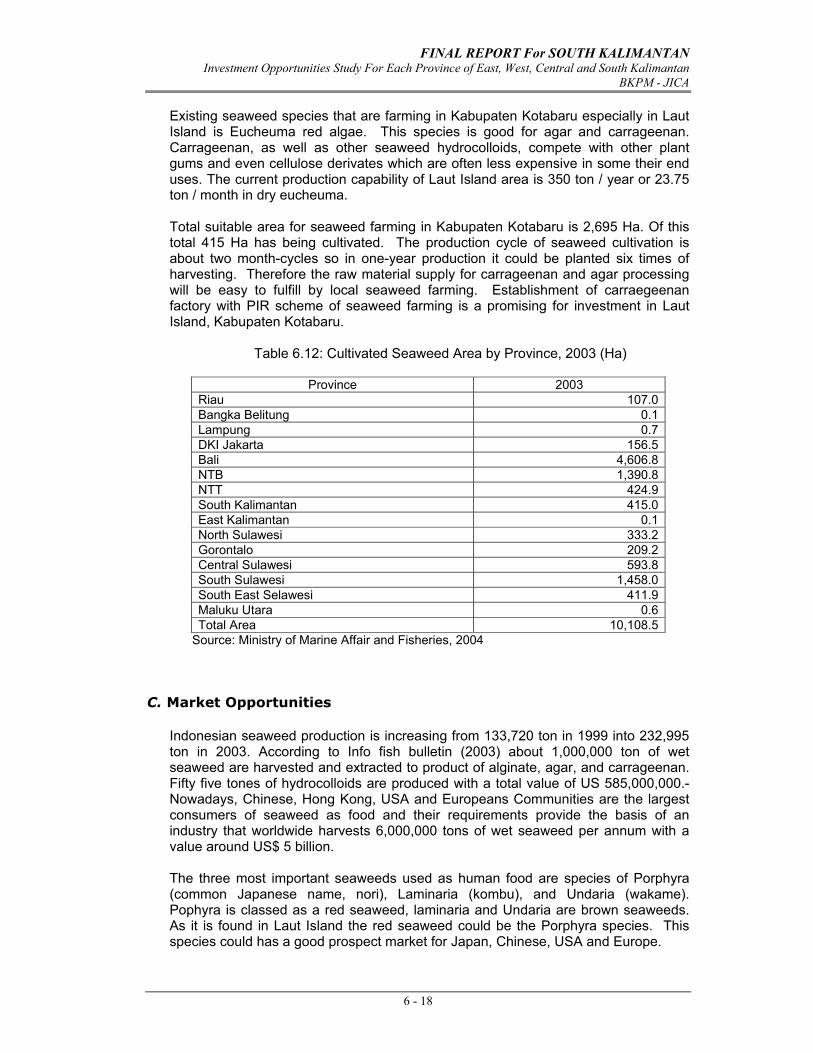

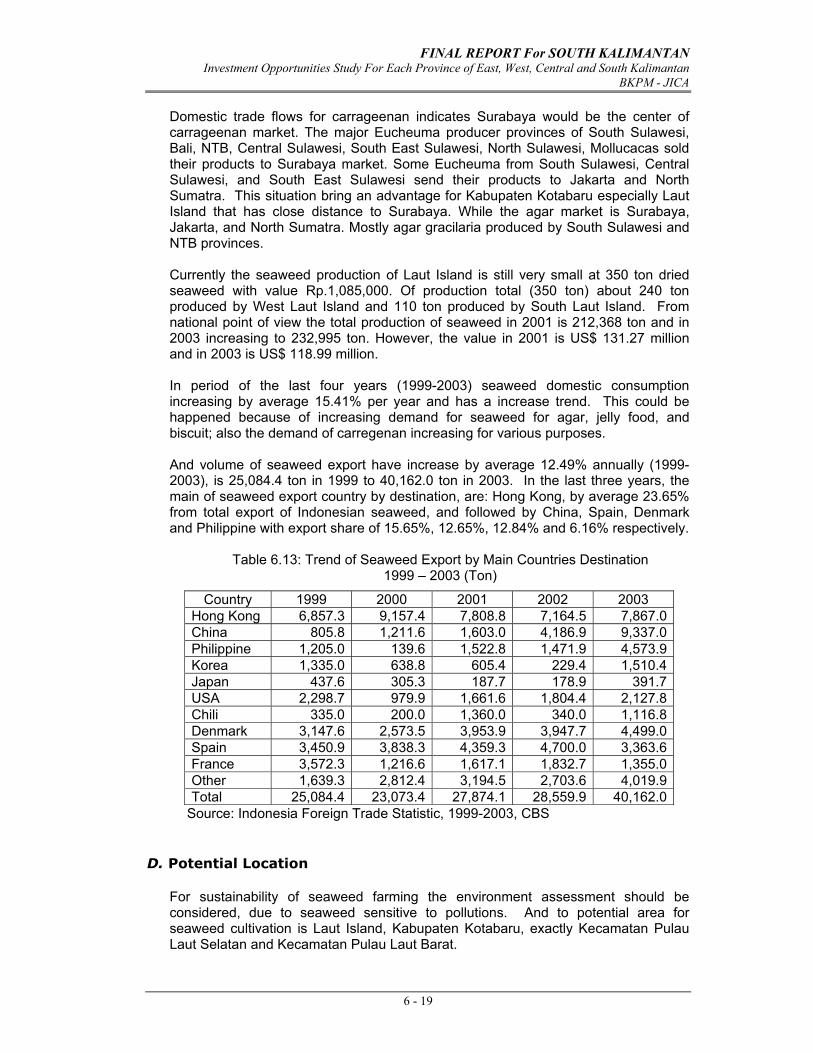

and Cultivated in South Kalimantan.........................................6 - 13 Table 6-10. Trend of Export Shrimp by Main Countries Destination ..........6 - 14 Table 6-11. Trend of Seaweed Production by Provinces ...........................6 - 17 Table 6-12. Cultivated Seaweed area by Province ....................................6 - 18 Table 6-13. Trend of Seaweed Export by Main Countries Destination.......6 - 19

vii

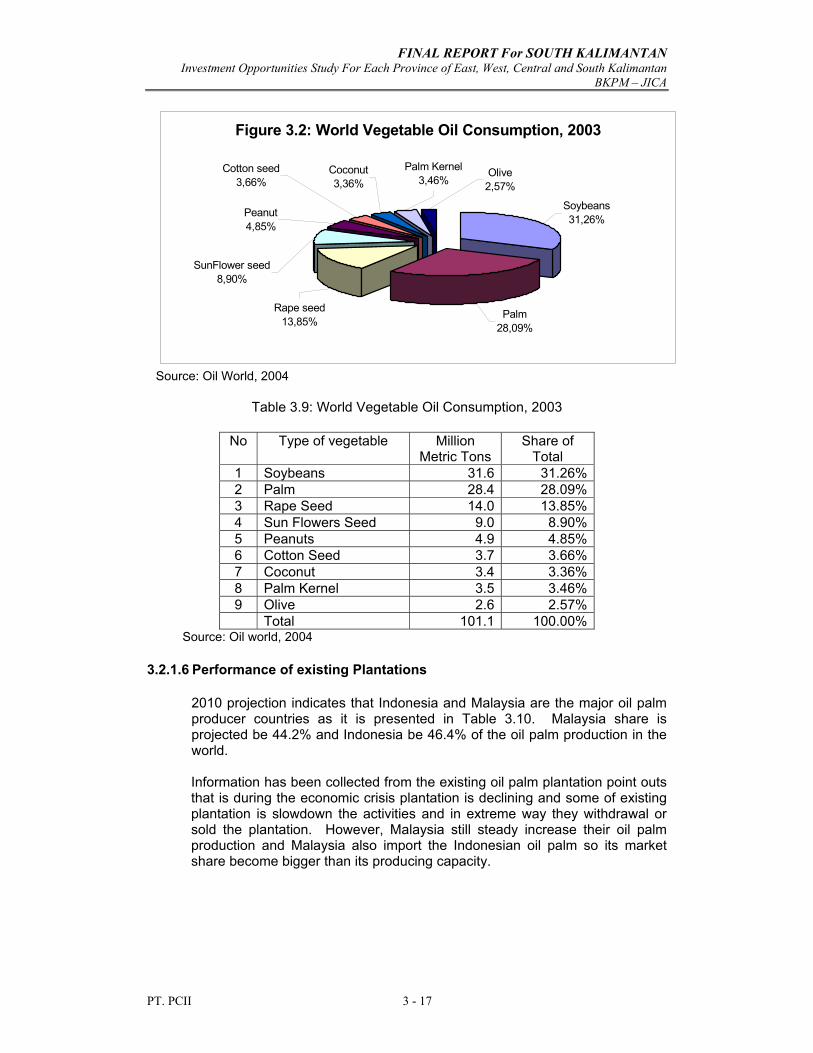

LIST OF FIGURES

Page Figure 1.1. Share of GRDP by Economic sector, 2003 ............................. 1 - 4 Figure 1.2. The Composition of Employment in South Kalimantan ........... 1 - 8 Figure 1.3. Number of Domestic & Foreign Investment Project Approved

by BKPM/BKPMD, 1993 - August 2004 ................................. 1- 13

Figure 1.4. The Growth of PMDN Projects in South Kalimantan, ............. 1- 13

Figure 1.5. The Growth of (PMDN Value in South Kalimantan, ............... 1 - 14

Figure 1.6. Percentage of PMDN Planned Projects by Sector .................. 1 - 14

Figure 1.7. Cumulative PMDN Plan & Realization of Investment Value ... 1 - 15

Figure 1.8. The Growth Foreign Direct Investment (PMA) Project in

South Kalimantan, 1993 - August 2004 .................................. 1 - 15

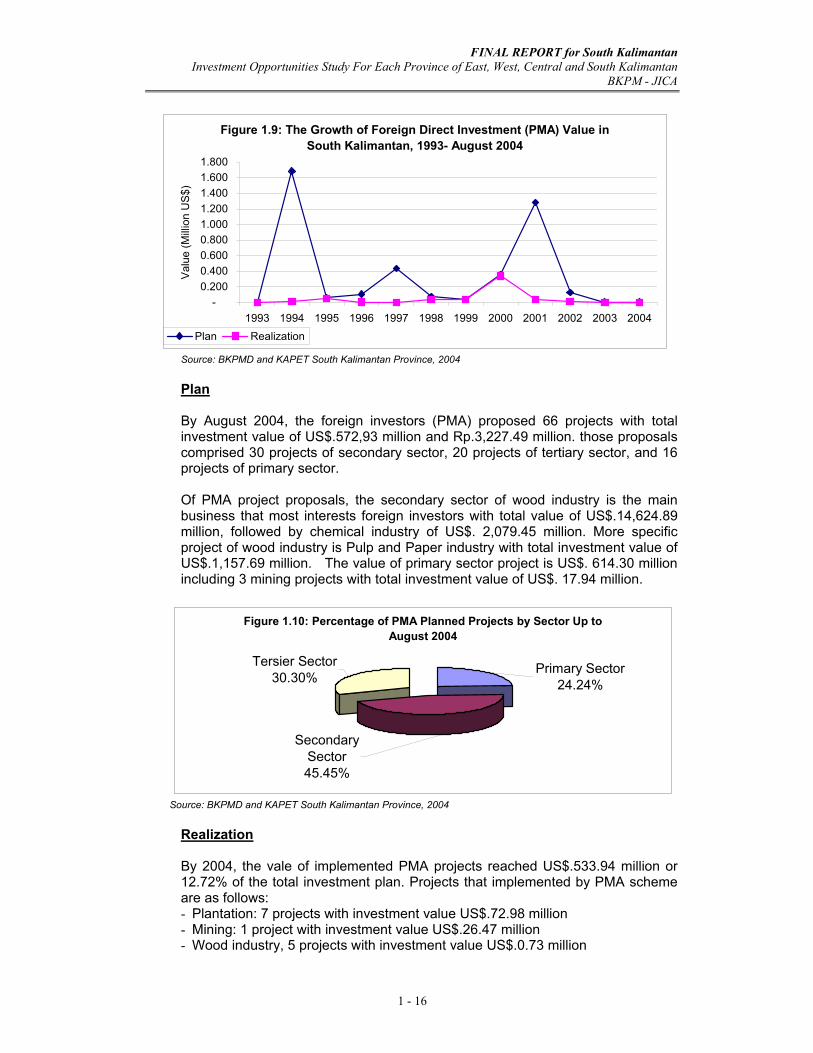

Figure 1.9. The Growth of PMA Value in South Kalimantan, ................... 1 - 16

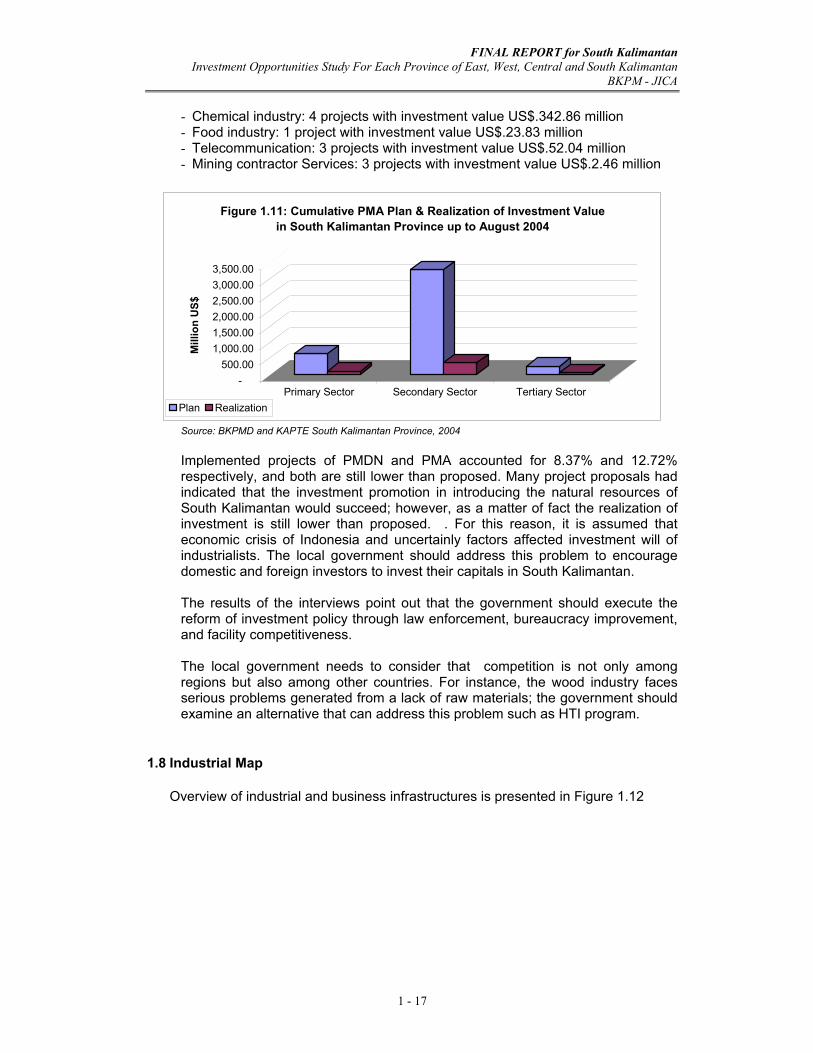

Figure 1.10. Percentage of PMA Planned Projects by Sector .................... 1 - 16

Figure 1.11. Cumulative PMA Plan & Realization of Investment Value ..... 1 - 17

Figure 1.12. Industrial Map .......................................................................... 1 - 18

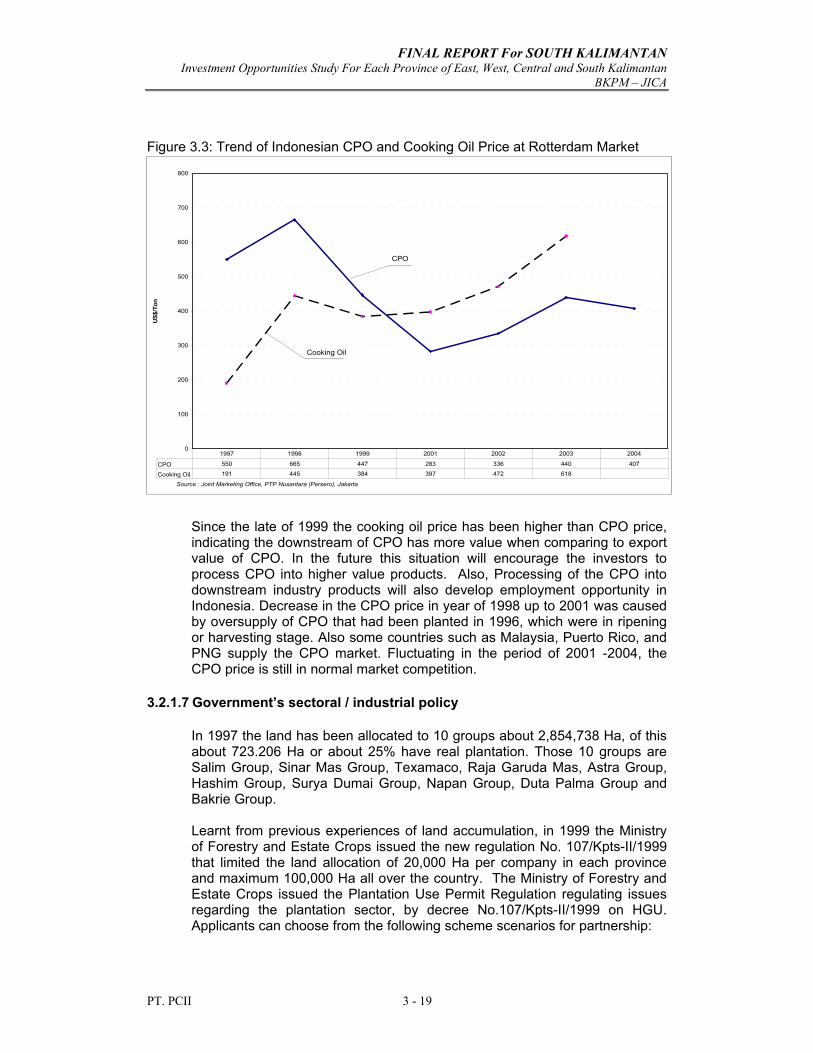

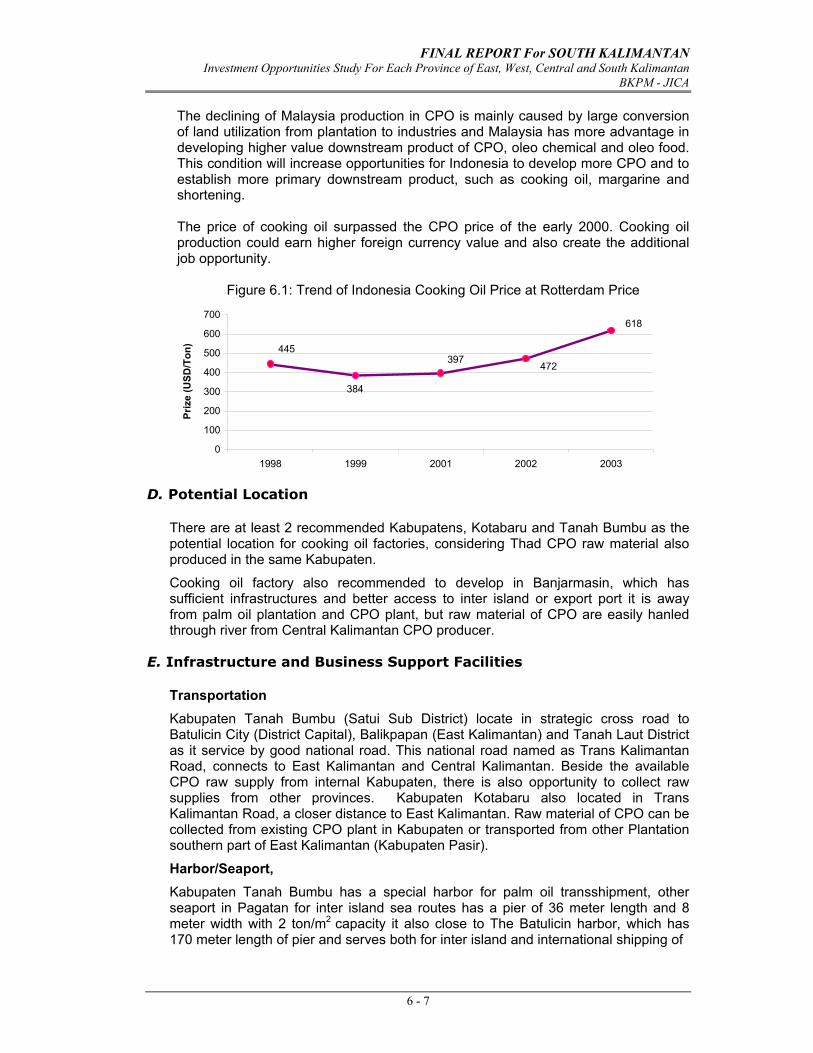

Figure 2.1. Map of National & Province Road Network ............................ 2 - 4 Figure 2.2. Map of River Network and Harbors in South Kalimantan ....... 2 - 5 Figure Batulicin Port Situatuin, 2004................................................... 2 - 11 Figure 2.3. Route Airplane From Syamsuddin Noor Airport ..................... 2 - 14 Figure 2.4. Map of Industrial Estate in South Kalimantan.......................... 2 - 17 Figure 3.1. Map of Main Natural Resources & Industrial Loaction ............ 3 - 13 Figure 3.2. World Vegetable Oil Consumption, 2003................................. 3 - 17 Figure 3.3. Trend of Indonesia CPO and Cooking Oil Price at Rotterdam

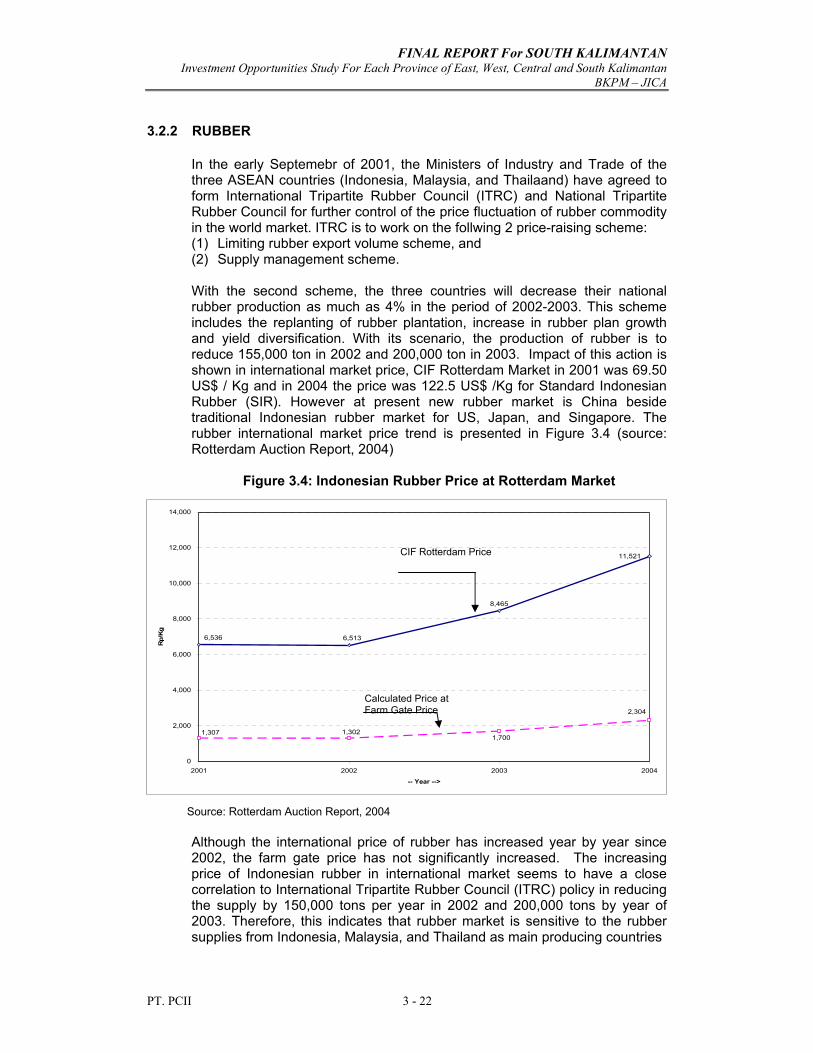

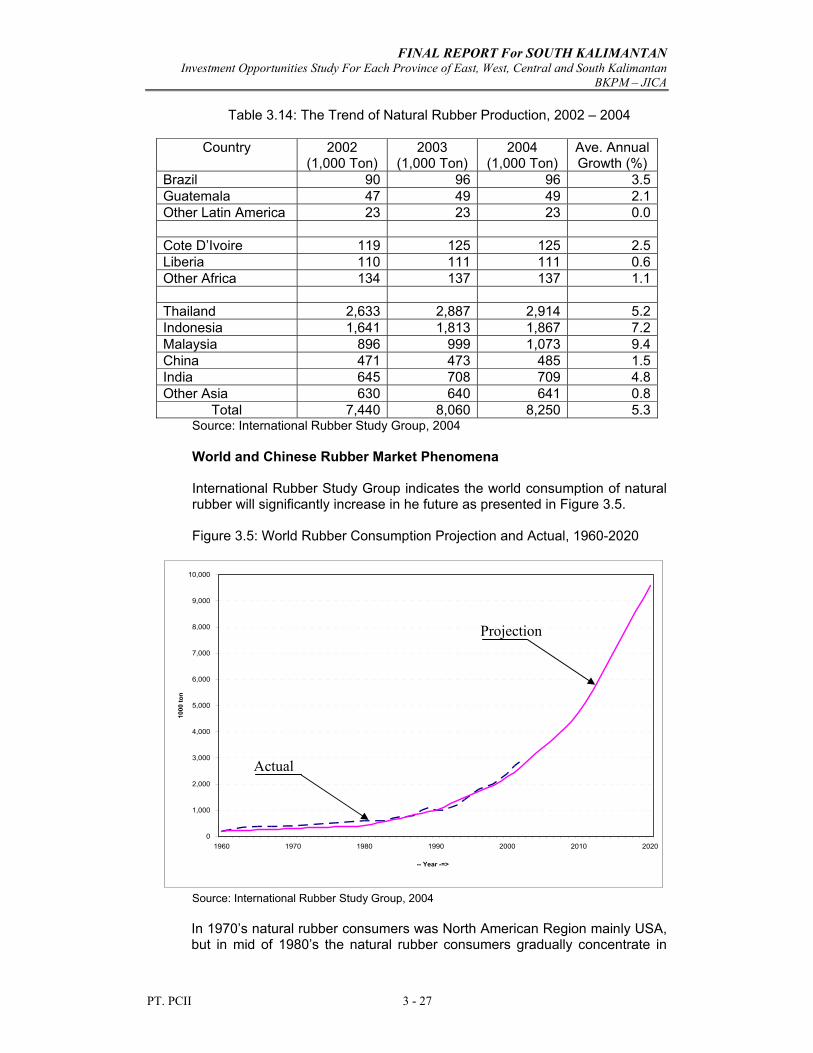

Market ...................................................................................... 3 - 19 Figure 3-4. Indonesian Rubber Price at Rotterdam Market .........................3 - 22

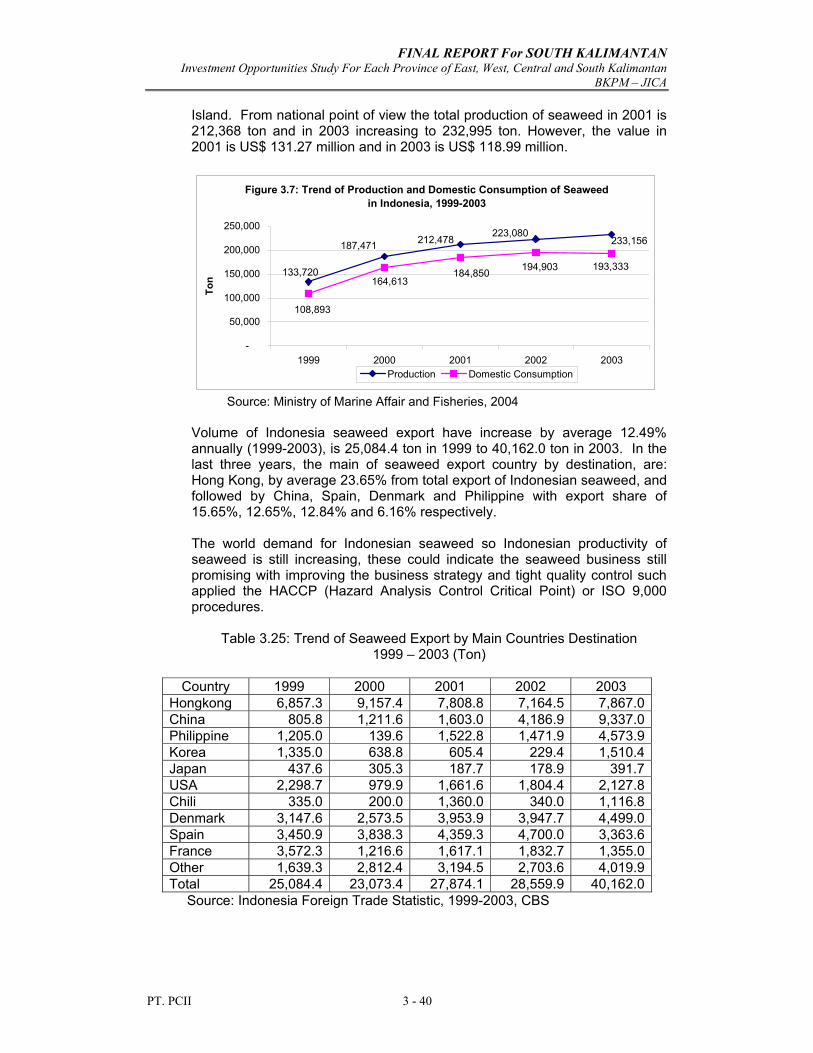

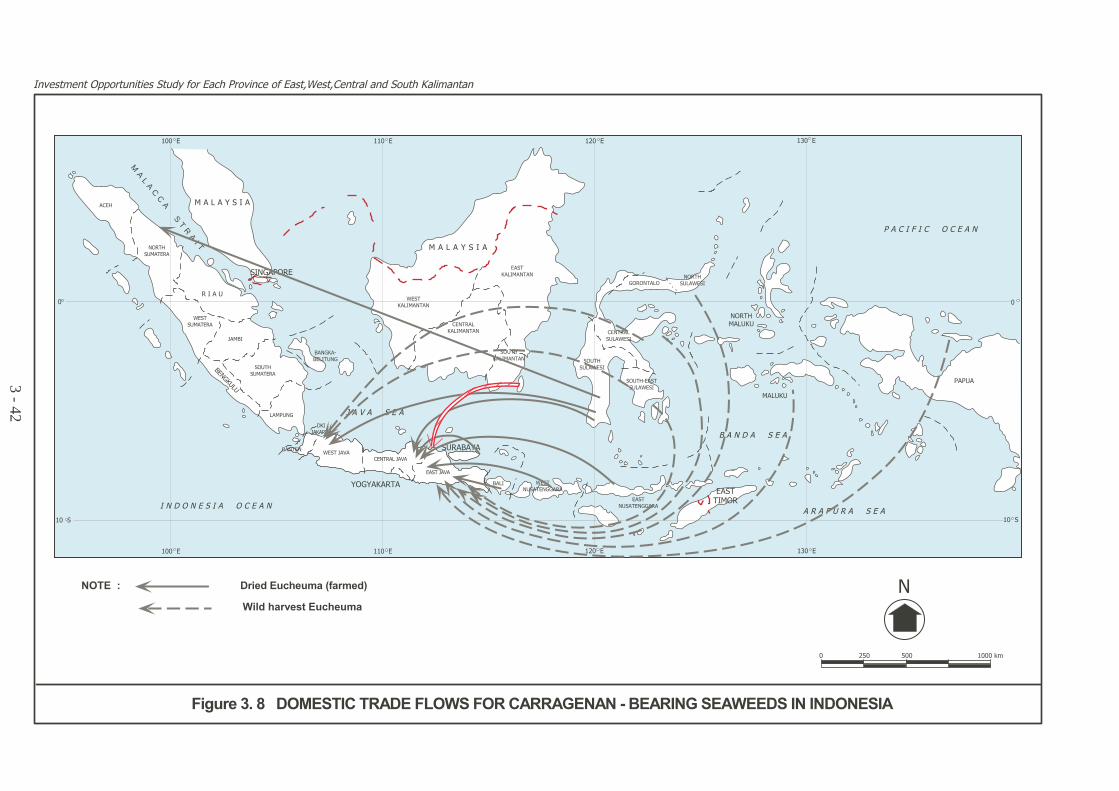

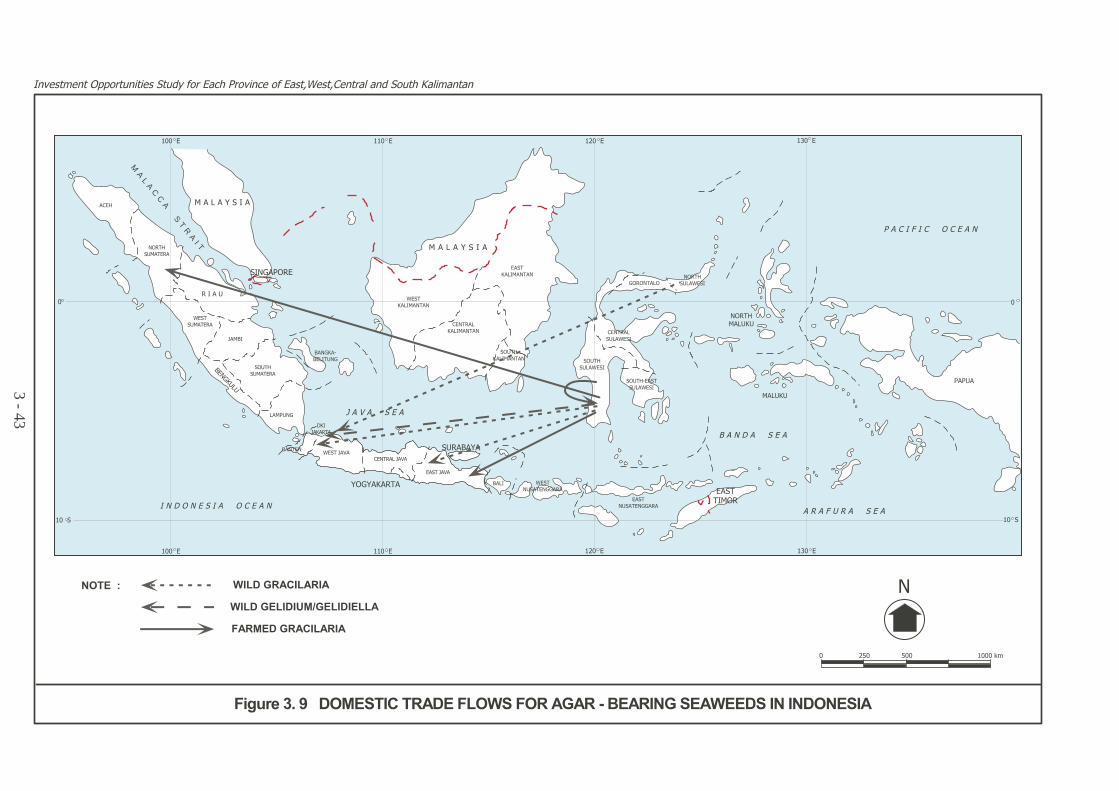

Figure 3-5. World Rubber Consumption Projection and Actual ...................3 - 27 Figure 3-6. China Natural Rubber Imports by Selected Countries Origin ..3 - 29 Figure 3-7. Trend of Production & Domestic Consumption of Seaweed in Indonesia ......................................................................................3 - 40 Figure 3-8. Domestic Trade Flows For Carragenan – Bearing Seaweeds

in Indonesia......................................................................................3 - 42

viii

Figure 3-9. Domestic Trade Flows For Agar – Bearing Seaweeds in

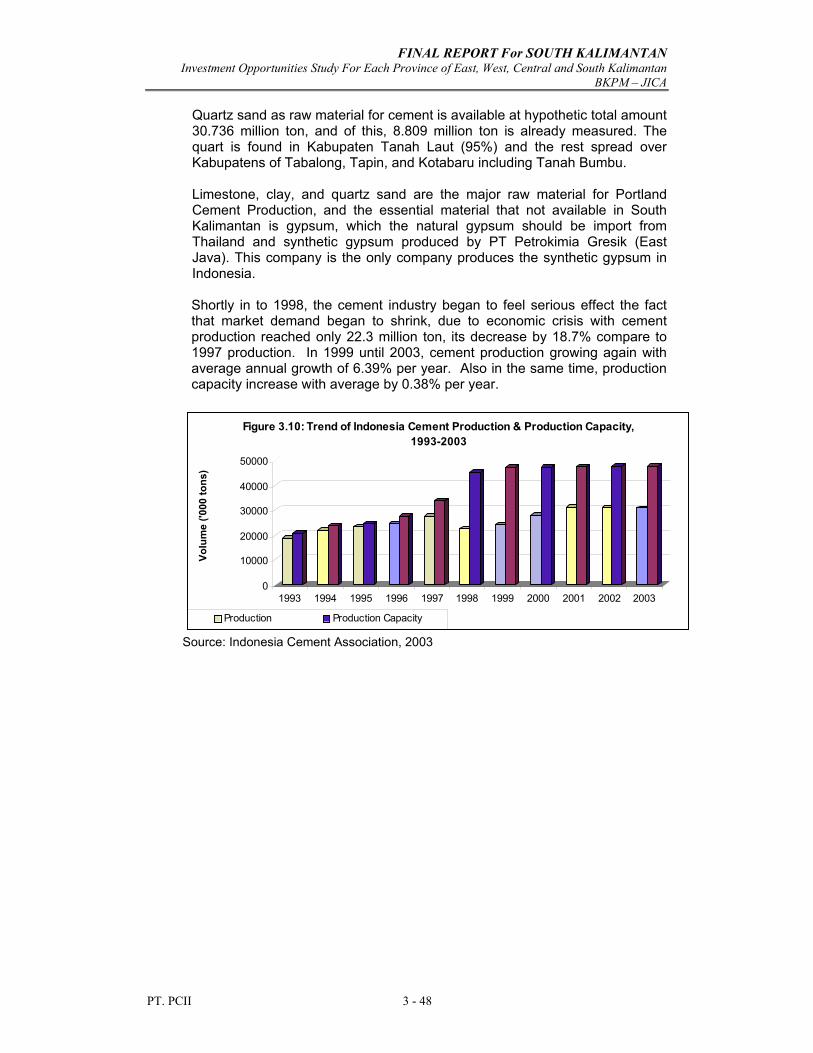

in Indonesia......................................................................................3 - 43 Figure 3-10. Trend of Indonesia Cement Production & Production Capacity

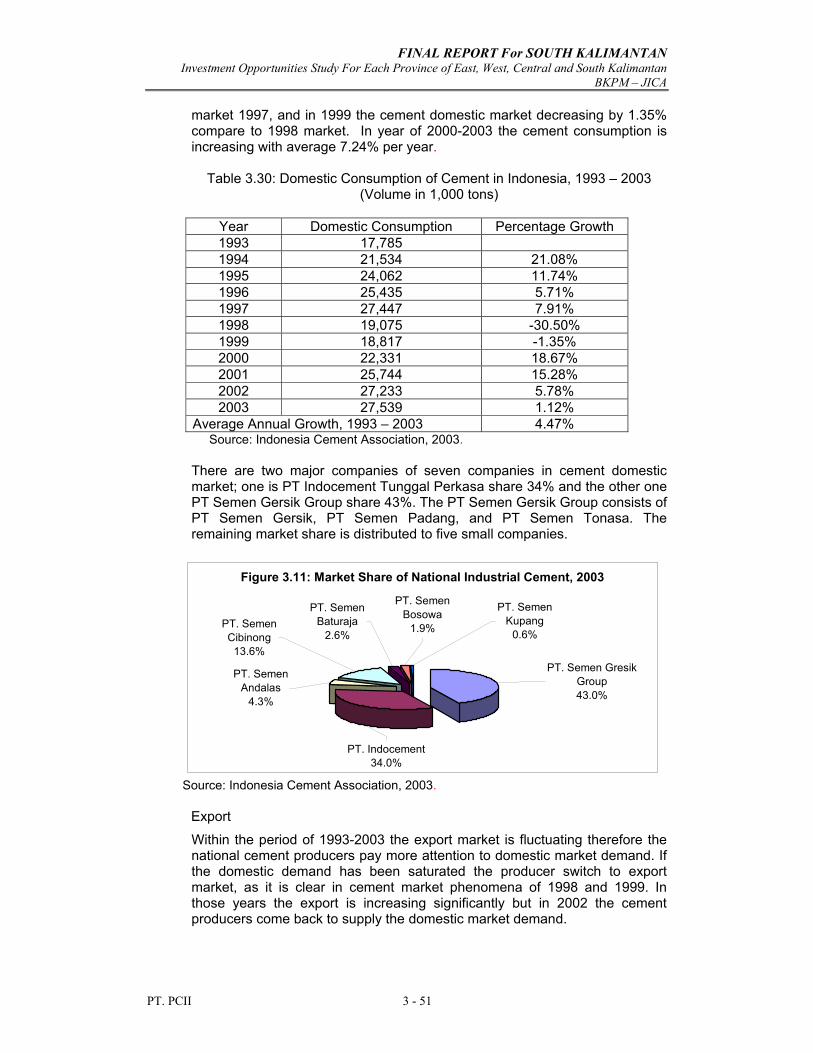

............................................................................................................3 - 48 Figure 3-11. Market Share of National Industrial Cement, 2003.................. 3 - 51 Figure 4-1. Map of Banjarmasin City and Surrounding .................................4 - 6 Figure 4-2. Map of Kabupaten Tanah Laut ....................................................4 - 7 Figure 4-3. Map of Kabupaten Tanah Bumbu and Kotabaru .......................4 - 10 Figure 4-4. Regional Eonomic Linkages Between Central Kalimantan And South Kalimantan ...................................................................4 - 13 Figure 6-1. Trend of Indonesia Cooking Oil Price at Rotterdam .................6 - 7

OVERVIEW OF PROVINCIAL ECONOMY

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 1

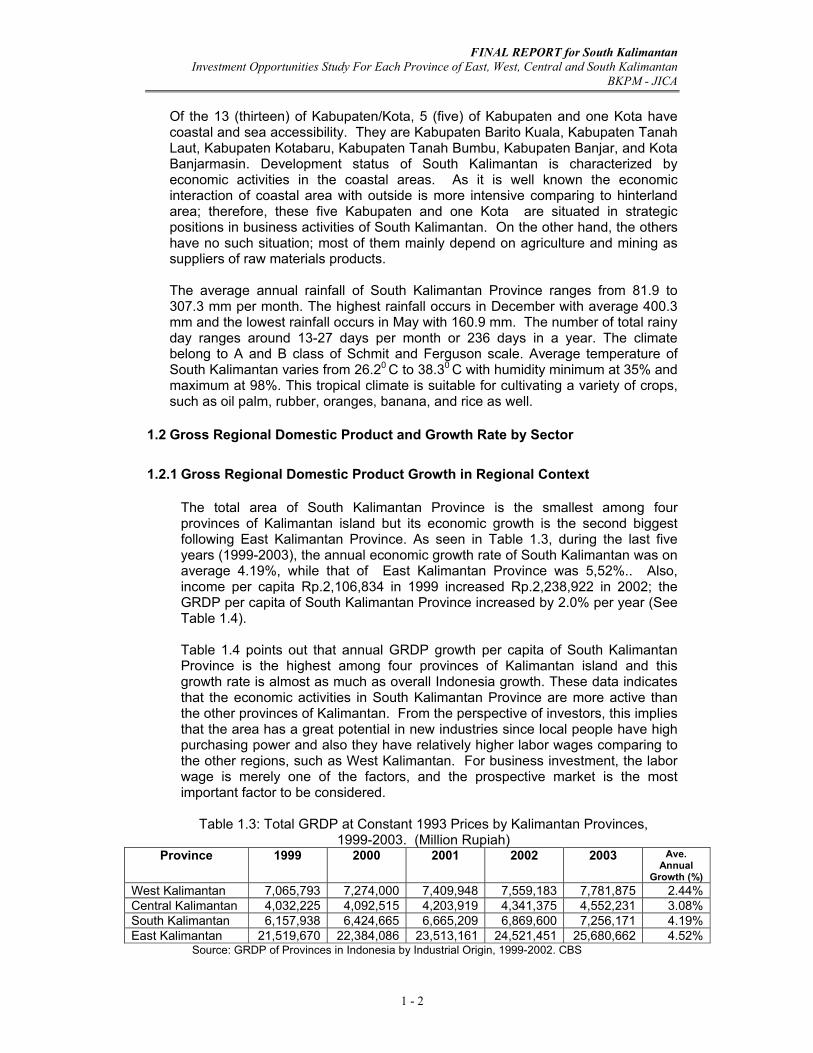

CHAPTER 1

OVERVIEW OF PROVINCIAL ECONOMY

1.1 Geographical Conditions

Geomorphology of South Kalimantan consists of alluvium and sandy soil formation. Dominant altitude of area is at 25-100 meter above sea level (see Table 1.1) and smaller area lies in hilly and mountainous system. The landform is classified into 4 slope classes category which are: 40.05% of area situated at 0-2% slope (flat lowland area), 31.87% of area belong to >2-15% slope (flat upland area), 19.02% of area belong to >15-40% slope (undulating area), and 6.16% of area belong to >40% slope (hilly and mountainous system) (see Table 1.2).

Table 1.1 The Area of Kabupaten/Kota by Altitude Class (Ha), 2002

Altitude Class Kabupaten/Kota

0-7 m >7-25 m >25-100 m >100-500 m 500-1000 m >1000 m Total

Tanah Laut 58,231 142,133 125,386 17,750 13,661 15,769 372,930 Kotabaru 86,618 300,535 667,931 320,388 67,064 6,433 1,448,969 Tanah Bumbu*) Banjar 123,277 16,754 81,037 187,289 43,735 15,176 467,268 Barito Kuala 237,622 0 0 0 0 0 237,622 Tapin 146,455 30,292 14,776 23,351 2,621 0 217,495 Hulu Sungai Selatan 105,198 18,254 16,590 27,546 11,226 1,680 180,494 Hulu Sungai Tengah 17,593 34,995 40,321 38,958 12,521 2,812 147,200 Hulu Sungai Utara 92,500 36,682 72,084 58,882 16,952 0 277,100 Balangan*) Tabalong 7,062 11,688 148,812 82,227 107,223 2,923 359,995 Banjarmasin 7.267 0 0 0 0 0 7.267 Banjarbaru 13,410 14,682 7,530 1,090 0 0 36,712 South Kalimantan 895,233 606,015 1,174,467 757,531 275,003 44,793 3.753.052

Source: South Kalimantan in Figure 2002. *) Kabupaten resulted from the development

Table 1.2: The Area of Kabupaten/Kota by Slope Class (Ha), 2002 Slope Class (%) Kabupaten/Kota

0-2 % >2-15 % >15-40 % >40 % Total

Tanah Laut 290,147 43,060 26,833 12,890 372,930 Kotabaru 154,211 877,315 331,297 86,146 1,448,969 Tanah Bumbu*) Banjar 196,282 114,234 121,550 25,202 467,268 Barito Kuala 237,622 0 0 0 237,622 Tapin 180,376 12,510 18,719 5,890 217,495 Hulu Sungai Selatan 128,376 20,737 19,090 12,610 180,494 Hulu Sungai Tengah 75,281 10,268 49,914 11,737 147,200 Hulu Sungai Utara 218,968 18,961 9,201 29,970 277,100 Balangan*) Tabalong 93,727 92,910 126,608 46,750 359,995 Banjarmasin 7,267 0 0 0 7,267 Banjarbaru 33,692 2,370 910 0 36,712 South Kalimantan 1,615,630 1,192,545 713,682 231,195 3.753.052

Source: South Kalimantan in Figure 2002. *) Kabupaten resulted from the development

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 2

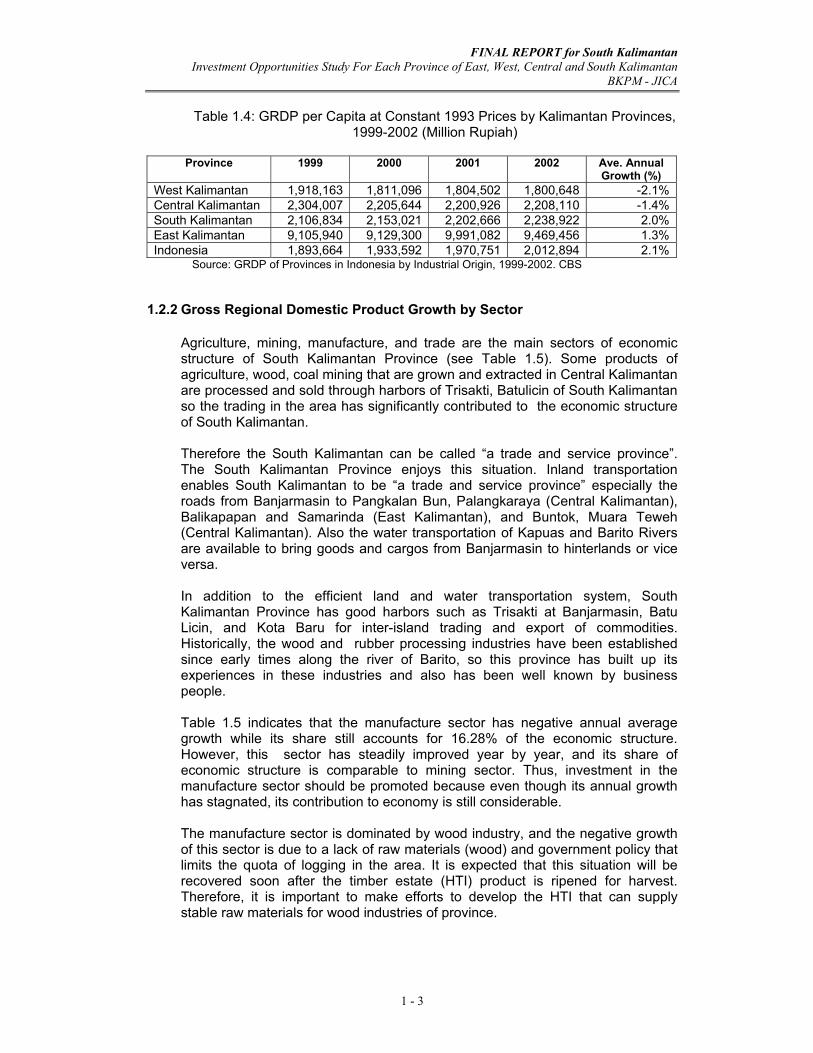

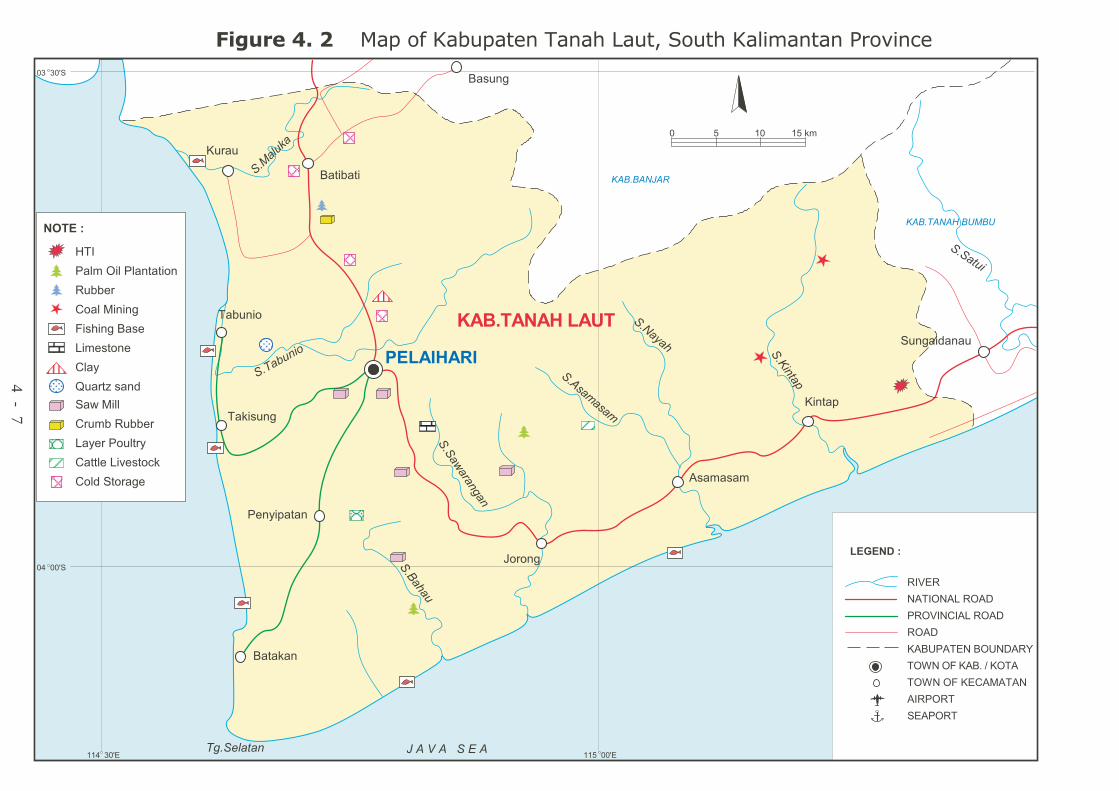

Of the 13 (thirteen) of Kabupaten/Kota, 5 (five) of Kabupaten and one Kota have coastal and sea accessibility. They are Kabupaten Barito Kuala, Kabupaten Tanah Laut, Kabupaten Kotabaru, Kabupaten Tanah Bumbu, Kabupaten Banjar, and Kota Banjarmasin. Development status of South Kalimantan is characterized by economic activities in the coastal areas. As it is well known the economic interaction of coastal area with outside is more intensive comparing to hinterland area; therefore, these five Kabupaten and one Kota are situated in strategic positions in business activities of South Kalimantan. On the other hand, the others have no such situation; most of them mainly depend on agriculture and mining as suppliers of raw materials products. The average annual rainfall of South Kalimantan Province ranges from 81.9 to 307.3 mm per month. The highest rainfall occurs in December with average 400.3 mm and the lowest rainfall occurs in May with 160.9 mm. The number of total rainy day ranges around 13-27 days per month or 236 days in a year. The climate belong to A and B class of Schmit and Ferguson scale. Average temperature of South Kalimantan varies from 26.20 C to 38.30 C with humidity minimum at 35% and maximum at 98%. This tropical climate is suitable for cultivating a variety of crops, such as oil palm, rubber, oranges, banana, and rice as well.

1.2 Gross Regional Domestic Product and Growth Rate by Sector 1.2.1 Gross Regional Domestic Product Growth in Regional Context

The total area of South Kalimantan Province is the smallest among four provinces of Kalimantan island but its economic growth is the second biggest following East Kalimantan Province. As seen in Table 1.3, during the last five years (1999-2003), the annual economic growth rate of South Kalimantan was on average 4.19%, while that of East Kalimantan Province was 5,52%.. Also, income per capita Rp.2,106,834 in 1999 increased Rp.2,238,922 in 2002; the GRDP per capita of South Kalimantan Province increased by 2.0% per year (See Table 1.4). Table 1.4 points out that annual GRDP growth per capita of South Kalimantan Province is the highest among four provinces of Kalimantan island and this growth rate is almost as much as overall Indonesia growth. These data indicates that the economic activities in South Kalimantan Province are more active than the other provinces of Kalimantan. From the perspective of investors, this implies that the area has a great potential in new industries since local people have high purchasing power and also they have relatively higher labor wages comparing to the other regions, such as West Kalimantan. For business investment, the labor wage is merely one of the factors, and the prospective market is the most important factor to be considered.

Table 1.3: Total GRDP at Constant 1993 Prices by Kalimantan Provinces,

1999-2003. (Million Rupiah) Province 1999 2000 2001 2002 2003 Ave.

Annual Growth (%)

West Kalimantan 7,065,793 7,274,000 7,409,948 7,559,183 7,781,875 2.44%Central Kalimantan 4,032,225 4,092,515 4,203,919 4,341,375 4,552,231 3.08%South Kalimantan 6,157,938 6,424,665 6,665,209 6,869,600 7,256,171 4.19%East Kalimantan 21,519,670 22,384,086 23,513,161 24,521,451 25,680,662 4.52%

Source: GRDP of Provinces in Indonesia by Industrial Origin, 1999-2002. CBS

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 3

Table 1.4: GRDP per Capita at Constant 1993 Prices by Kalimantan Provinces,

1999-2002 (Million Rupiah)

Province 1999 2000 2001 2002 Ave. Annual Growth (%)

West Kalimantan 1,918,163 1,811,096 1,804,502 1,800,648 -2.1%Central Kalimantan 2,304,007 2,205,644 2,200,926 2,208,110 -1.4%South Kalimantan 2,106,834 2,153,021 2,202,666 2,238,922 2.0%East Kalimantan 9,105,940 9,129,300 9,991,082 9,469,456 1.3%Indonesia 1,893,664 1,933,592 1,970,751 2,012,894 2.1%

Source: GRDP of Provinces in Indonesia by Industrial Origin, 1999-2002. CBS

1.2.2 Gross Regional Domestic Product Growth by Sector

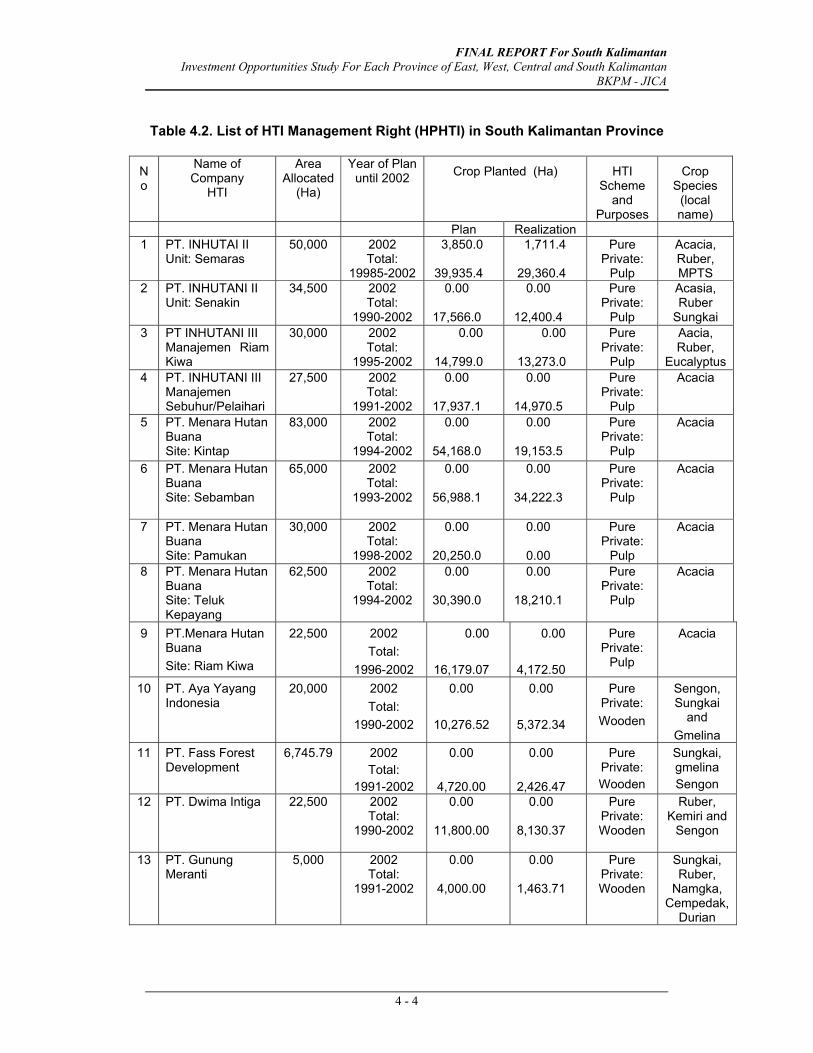

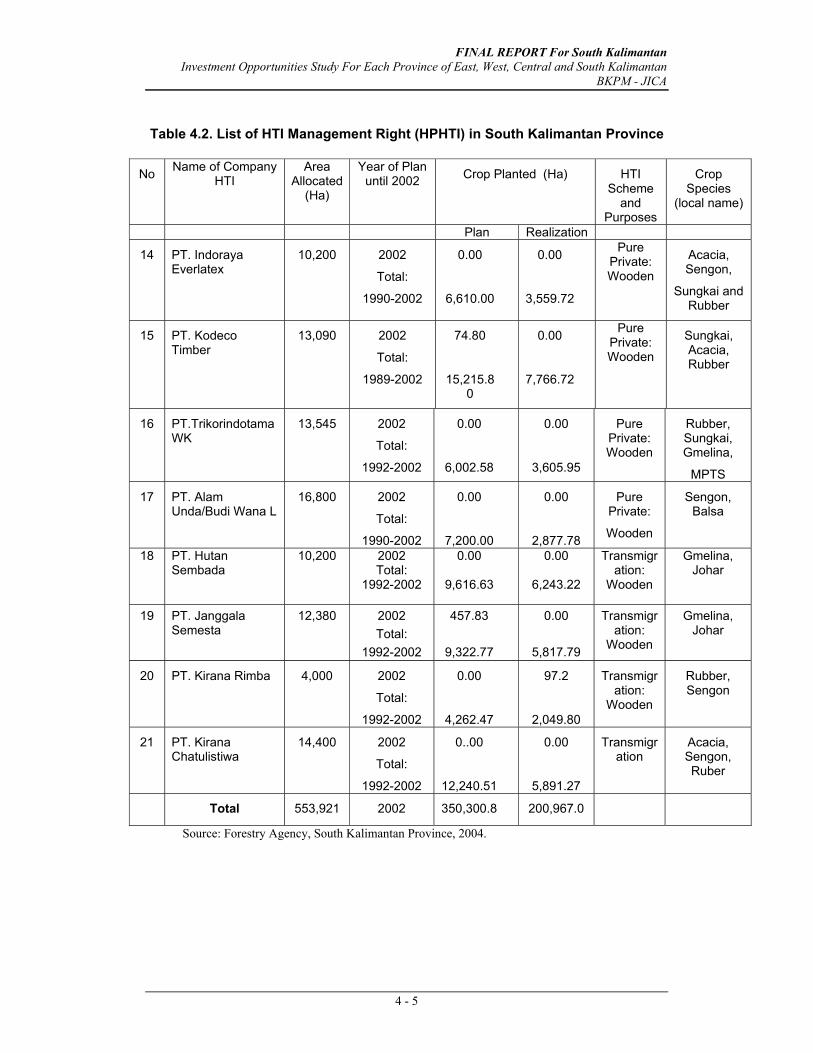

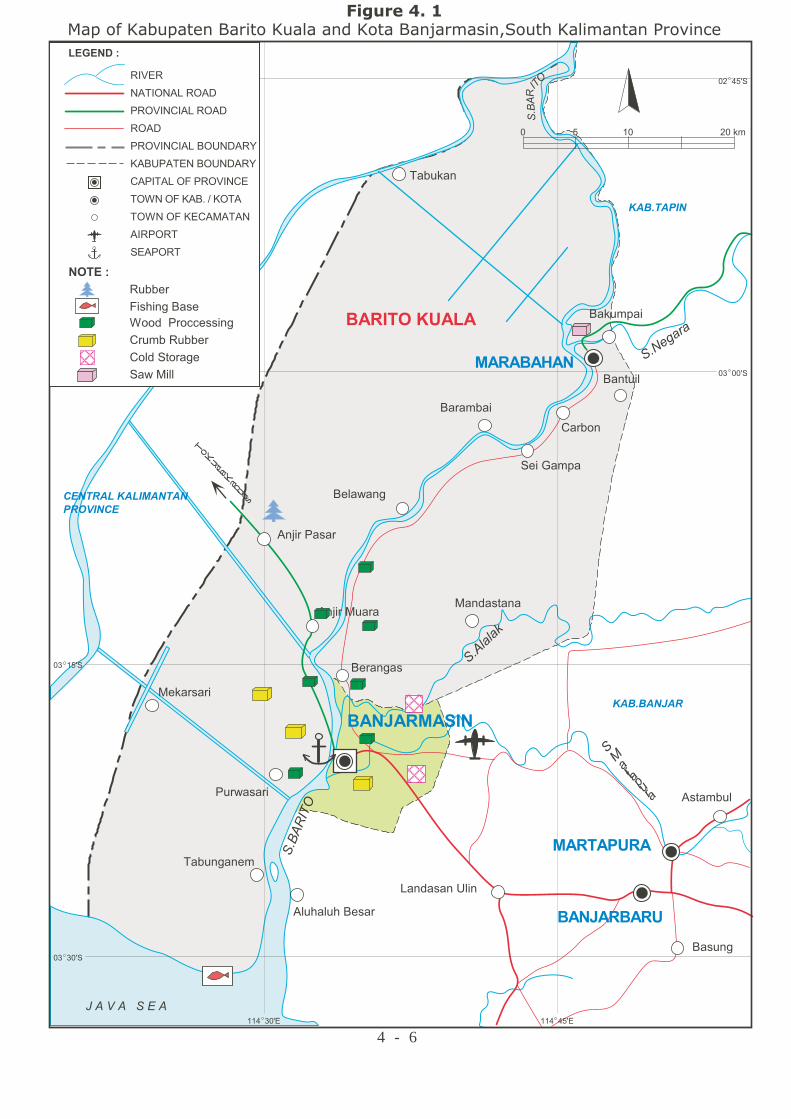

Agriculture, mining, manufacture, and trade are the main sectors of economic structure of South Kalimantan Province (see Table 1.5). Some products of agriculture, wood, coal mining that are grown and extracted in Central Kalimantan are processed and sold through harbors of Trisakti, Batulicin of South Kalimantan so the trading in the area has significantly contributed to the economic structure of South Kalimantan. Therefore the South Kalimantan can be called “a trade and service province”. The South Kalimantan Province enjoys this situation. Inland transportation enables South Kalimantan to be “a trade and service province” especially the roads from Banjarmasin to Pangkalan Bun, Palangkaraya (Central Kalimantan), Balikapapan and Samarinda (East Kalimantan), and Buntok, Muara Teweh (Central Kalimantan). Also the water transportation of Kapuas and Barito Rivers are available to bring goods and cargos from Banjarmasin to hinterlands or vice versa. In addition to the efficient land and water transportation system, South Kalimantan Province has good harbors such as Trisakti at Banjarmasin, Batu Licin, and Kota Baru for inter-island trading and export of commodities. Historically, the wood and rubber processing industries have been established since early times along the river of Barito, so this province has built up its experiences in these industries and also has been well known by business people. Table 1.5 indicates that the manufacture sector has negative annual average growth while its share still accounts for 16.28% of the economic structure. However, this sector has steadily improved year by year, and its share of economic structure is comparable to mining sector. Thus, investment in the manufacture sector should be promoted because even though its annual growth has stagnated, its contribution to economy is still considerable. The manufacture sector is dominated by wood industry, and the negative growth of this sector is due to a lack of raw materials (wood) and government policy that limits the quota of logging in the area. It is expected that this situation will be recovered soon after the timber estate (HTI) product is ripened for harvest. Therefore, it is important to make efforts to develop the HTI that can supply stable raw materials for wood industries of province.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 4

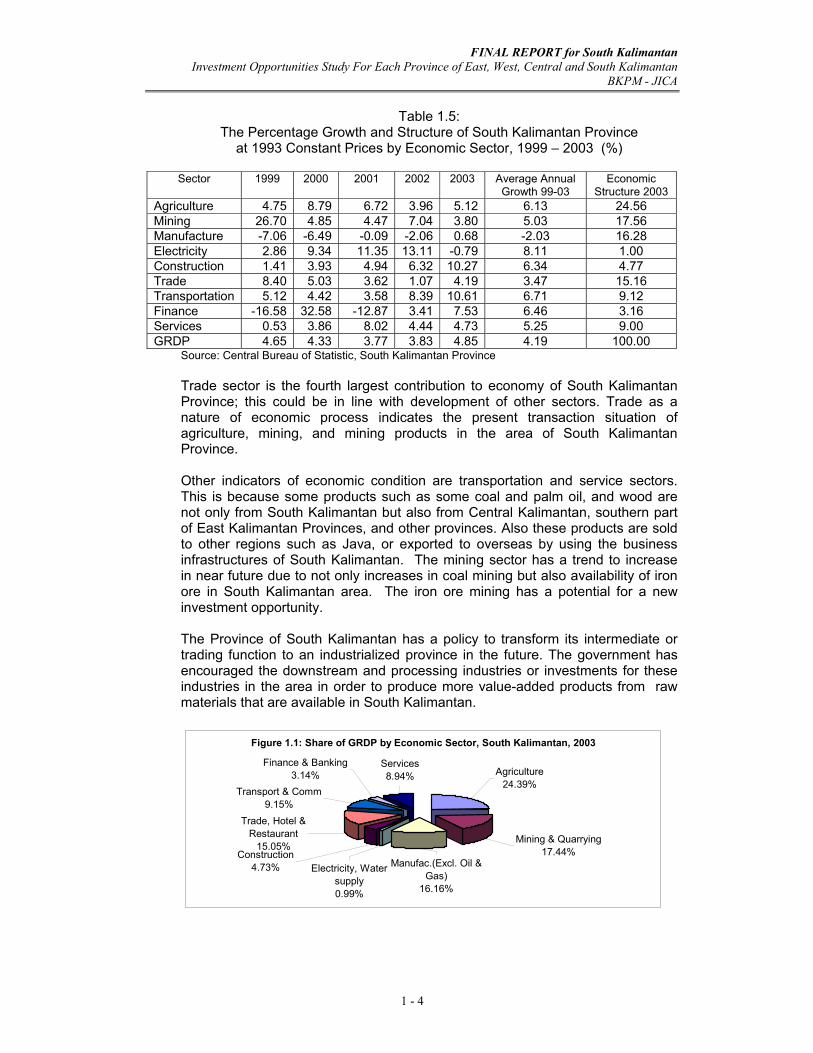

Table 1.5:

The Percentage Growth and Structure of South Kalimantan Province at 1993 Constant Prices by Economic Sector, 1999 – 2003 (%)

Sector 1999 2000 2001 2002 2003 Average Annual

Growth 99-03 Economic

Structure 2003 Agriculture 4.75 8.79 6.72 3.96 5.12 6.13 24.56 Mining 26.70 4.85 4.47 7.04 3.80 5.03 17.56 Manufacture -7.06 -6.49 -0.09 -2.06 0.68 -2.03 16.28 Electricity 2.86 9.34 11.35 13.11 -0.79 8.11 1.00 Construction 1.41 3.93 4.94 6.32 10.27 6.34 4.77 Trade 8.40 5.03 3.62 1.07 4.19 3.47 15.16 Transportation 5.12 4.42 3.58 8.39 10.61 6.71 9.12 Finance -16.58 32.58 -12.87 3.41 7.53 6.46 3.16 Services 0.53 3.86 8.02 4.44 4.73 5.25 9.00 GRDP 4.65 4.33 3.77 3.83 4.85 4.19 100.00

Source: Central Bureau of Statistic, South Kalimantan Province Trade sector is the fourth largest contribution to economy of South Kalimantan Province; this could be in line with development of other sectors. Trade as a nature of economic process indicates the present transaction situation of agriculture, mining, and mining products in the area of South Kalimantan Province. Other indicators of economic condition are transportation and service sectors. This is because some products such as some coal and palm oil, and wood are not only from South Kalimantan but also from Central Kalimantan, southern part of East Kalimantan Provinces, and other provinces. Also these products are sold to other regions such as Java, or exported to overseas by using the business infrastructures of South Kalimantan. The mining sector has a trend to increase in near future due to not only increases in coal mining but also availability of iron ore in South Kalimantan area. The iron ore mining has a potential for a new investment opportunity. The Province of South Kalimantan has a policy to transform its intermediate or trading function to an industrialized province in the future. The government has encouraged the downstream and processing industries or investments for these industries in the area in order to produce more value-added products from raw materials that are available in South Kalimantan.

Figure 1.1: Share of GRDP by Economic Sector, South Kalimantan, 2003

Transport & Comm9.15%

Finance & Banking3.14%

Services8.94%

Trade, Hotel & Restaurant

15.05%Construction

4.73% Electricity, Water supply0.99%

Manufac.(Excl. Oil & Gas)

16.16%

Mining & Quarrying17.44%

Agriculture24.39%

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 5

Agriculture sector has an inclining trend to share of GRDP mostly supported by fisheries, plantation, and food crops. Among those, the palm oil is the most promising source of GRDP growth. Besides palm oil, rubber crop also has significantly contributed to GRDP. Most of rubber plantations are operated by smallholders with or without Nucleus Estate Smallholders (PIR) Scheme; therefore, it is not promising for new private companies without PIR scheme because it is predicted that the social problems will arise. But oil palm, livestock, and fisheries especially brackishwater are still promising for new companies.

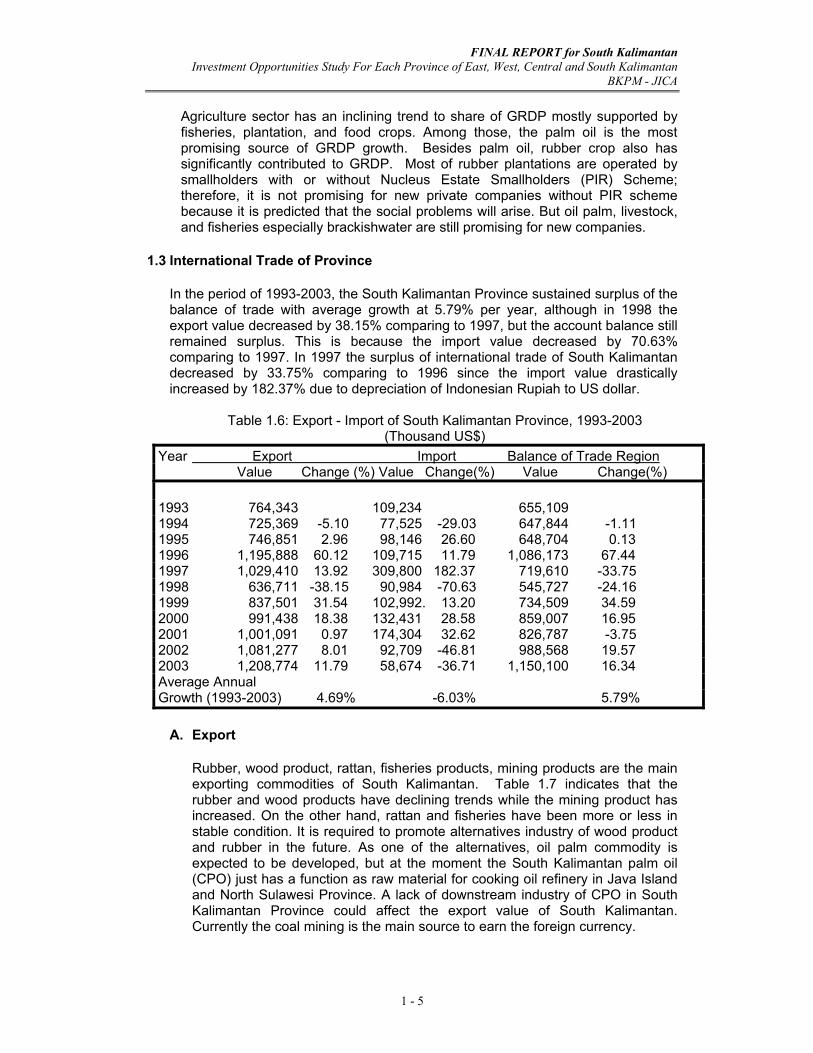

1.3 International Trade of Province

In the period of 1993-2003, the South Kalimantan Province sustained surplus of the balance of trade with average growth at 5.79% per year, although in 1998 the export value decreased by 38.15% comparing to 1997, but the account balance still remained surplus. This is because the import value decreased by 70.63% comparing to 1997. In 1997 the surplus of international trade of South Kalimantan decreased by 33.75% comparing to 1996 since the import value drastically increased by 182.37% due to depreciation of Indonesian Rupiah to US dollar.

Table 1.6: Export - Import of South Kalimantan Province, 1993-2003

(Thousand US$) Year Export Import Balance of Trade Region

Value Change (%) Value Change(%) Value Change(%) 1993 764,343 109,234 655,109 1994 725,369 -5.10 77,525 -29.03 647,844 -1.11 1995 746,851 2.96 98,146 26.60 648,704 0.13 1996 1,195,888 60.12 109,715 11.79 1,086,173 67.44 1997 1,029,410 13.92 309,800 182.37 719,610 -33.75 1998 636,711 -38.15 90,984 -70.63 545,727 -24.16 1999 837,501 31.54 102,992. 13.20 734,509 34.59 2000 991,438 18.38 132,431 28.58 859,007 16.95 2001 1,001,091 0.97 174,304 32.62 826,787 -3.75 2002 1,081,277 8.01 92,709 -46.81 988,568 19.57 2003 1,208,774 11.79 58,674 -36.71 1,150,100 16.34 Average Annual Growth (1993-2003) 4.69% -6.03% 5.79%

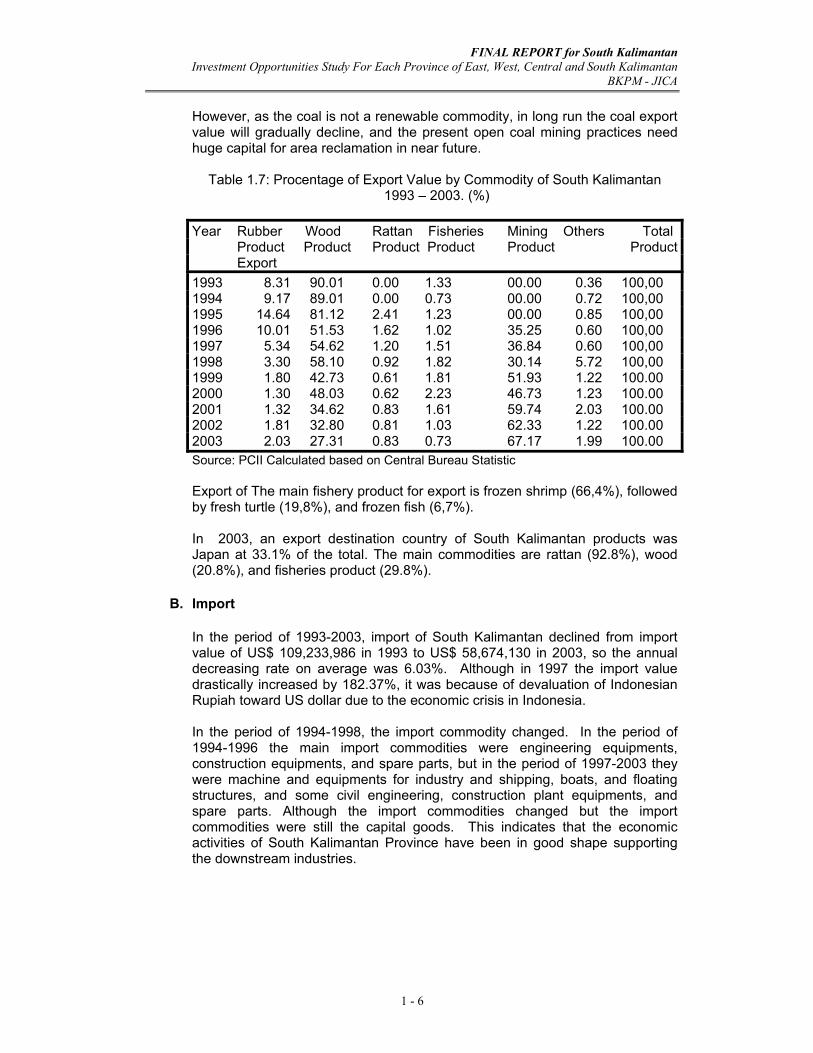

A. Export

Rubber, wood product, rattan, fisheries products, mining products are the main exporting commodities of South Kalimantan. Table 1.7 indicates that the rubber and wood products have declining trends while the mining product has increased. On the other hand, rattan and fisheries have been more or less in stable condition. It is required to promote alternatives industry of wood product and rubber in the future. As one of the alternatives, oil palm commodity is expected to be developed, but at the moment the South Kalimantan palm oil (CPO) just has a function as raw material for cooking oil refinery in Java Island and North Sulawesi Province. A lack of downstream industry of CPO in South Kalimantan Province could affect the export value of South Kalimantan. Currently the coal mining is the main source to earn the foreign currency.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 6

However, as the coal is not a renewable commodity, in long run the coal export value will gradually decline, and the present open coal mining practices need huge capital for area reclamation in near future.

Table 1.7: Procentage of Export Value by Commodity of South Kalimantan

1993 – 2003. (%)

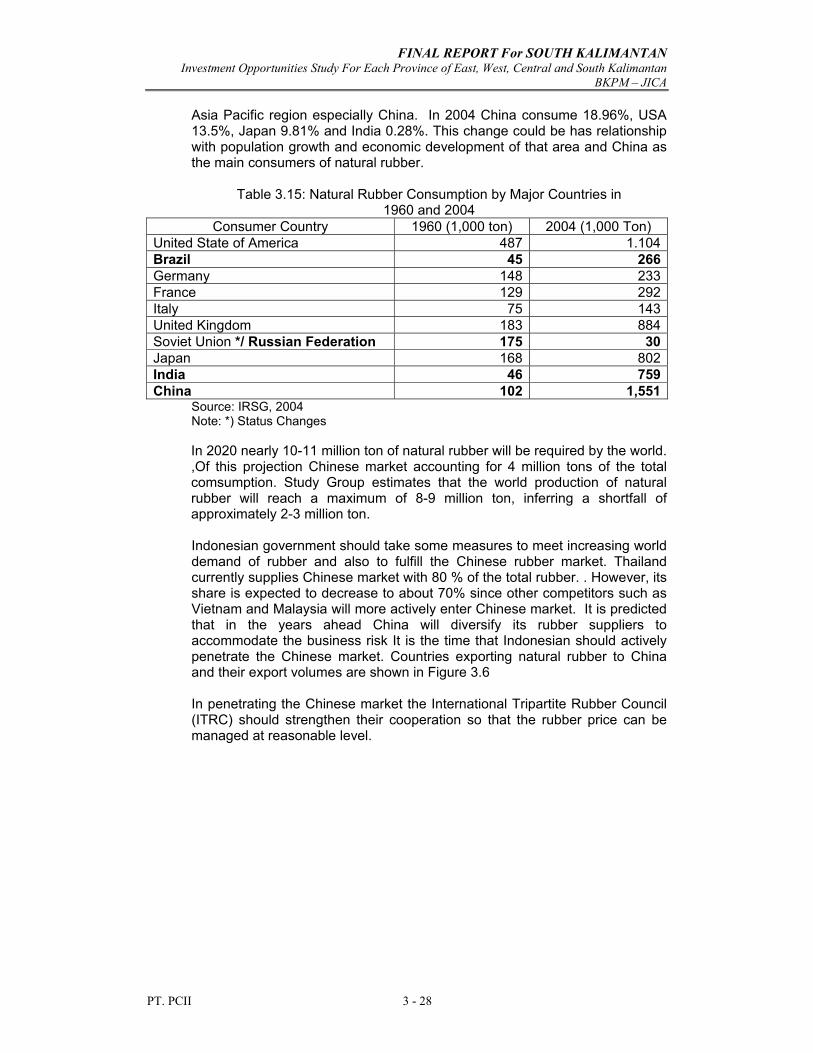

Year Rubber Wood Rattan Fisheries Mining Others Total Product Product Product Product Product Product Export 1993 8.31 90.01 0.00 1.33 00.00 0.36 100,00 1994 9.17 89.01 0.00 0.73 00.00 0.72 100,00 1995 14.64 81.12 2.41 1.23 00.00 0.85 100,00 1996 10.01 51.53 1.62 1.02 35.25 0.60 100,00 1997 5.34 54.62 1.20 1.51 36.84 0.60 100,00 1998 3.30 58.10 0.92 1.82 30.14 5.72 100,00 1999 1.80 42.73 0.61 1.81 51.93 1.22 100.00 2000 1.30 48.03 0.62 2.23 46.73 1.23 100.00 2001 1.32 34.62 0.83 1.61 59.74 2.03 100.00 2002 1.81 32.80 0.81 1.03 62.33 1.22 100.00 2003 2.03 27.31 0.83 0.73 67.17 1.99 100.00 Source: PCII Calculated based on Central Bureau Statistic Export of The main fishery product for export is frozen shrimp (66,4%), followed by fresh turtle (19,8%), and frozen fish (6,7%). In 2003, an export destination country of South Kalimantan products was Japan at 33.1% of the total. The main commodities are rattan (92.8%), wood (20.8%), and fisheries product (29.8%).

B. Import

In the period of 1993-2003, import of South Kalimantan declined from import value of US$ 109,233,986 in 1993 to US$ 58,674,130 in 2003, so the annual decreasing rate on average was 6.03%. Although in 1997 the import value drastically increased by 182.37%, it was because of devaluation of Indonesian Rupiah toward US dollar due to the economic crisis in Indonesia. In the period of 1994-1998, the import commodity changed. In the period of 1994-1996 the main import commodities were engineering equipments, construction equipments, and spare parts, but in the period of 1997-2003 they were machine and equipments for industry and shipping, boats, and floating structures, and some civil engineering, construction plant equipments, and spare parts. Although the import commodities changed but the import commodities were still the capital goods. This indicates that the economic activities of South Kalimantan Province have been in good shape supporting the downstream industries.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 7

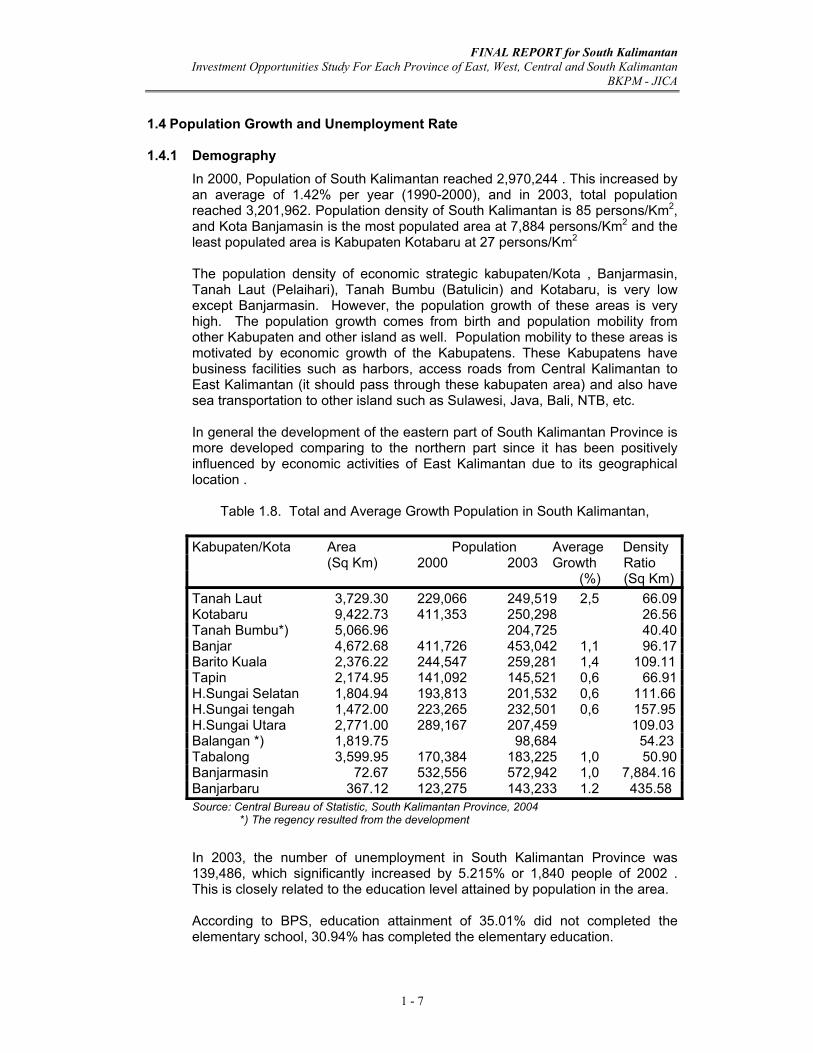

1.4 Population Growth and Unemployment Rate 1.4.1 Demography

In 2000, Population of South Kalimantan reached 2,970,244 . This increased by an average of 1.42% per year (1990-2000), and in 2003, total population reached 3,201,962. Population density of South Kalimantan is 85 persons/Km2, and Kota Banjamasin is the most populated area at 7,884 persons/Km2 and the least populated area is Kabupaten Kotabaru at 27 persons/Km2 The population density of economic strategic kabupaten/Kota , Banjarmasin, Tanah Laut (Pelaihari), Tanah Bumbu (Batulicin) and Kotabaru, is very low except Banjarmasin. However, the population growth of these areas is very high. The population growth comes from birth and population mobility from other Kabupaten and other island as well. Population mobility to these areas is motivated by economic growth of the Kabupatens. These Kabupatens have business facilities such as harbors, access roads from Central Kalimantan to East Kalimantan (it should pass through these kabupaten area) and also have sea transportation to other island such as Sulawesi, Java, Bali, NTB, etc. In general the development of the eastern part of South Kalimantan Province is more developed comparing to the northern part since it has been positively influenced by economic activities of East Kalimantan due to its geographical location .

Table 1.8. Total and Average Growth Population in South Kalimantan,

Kabupaten/Kota Area Population Average Density (Sq Km) 2000 2003 Growth Ratio (%) (Sq Km) Tanah Laut 3,729.30 229,066 249,519 2,5 66.09 Kotabaru 9,422.73 411,353 250,298 26.56 Tanah Bumbu*) 5,066.96 204,725 40.40 Banjar 4,672.68 411,726 453,042 1,1 96.17 Barito Kuala 2,376.22 244,547 259,281 1,4 109.11 Tapin 2,174.95 141,092 145,521 0,6 66.91 H.Sungai Selatan 1,804.94 193,813 201,532 0,6 111.66 H.Sungai tengah 1,472.00 223,265 232,501 0,6 157.95 H.Sungai Utara 2,771.00 289,167 207,459 109.03 Balangan *) 1,819.75 98,684 54.23 Tabalong 3,599.95 170,384 183,225 1,0 50.90 Banjarmasin 72.67 532,556 572,942 1,0 7,884.16 Banjarbaru 367.12 123,275 143,233 1.2 435.58

Source: Central Bureau of Statistic, South Kalimantan Province, 2004 *) The regency resulted from the development

In 2003, the number of unemployment in South Kalimantan Province was 139,486, which significantly increased by 5.215% or 1,840 people of 2002 . This is closely related to the education level attained by population in the area.

According to BPS, education attainment of 35.01% did not completed the elementary school, 30.94% has completed the elementary education.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 8

For investment with high technology, the investors should have special effort to have training programs or recruit the labor from other region such as from Java or other islands. However, recruitment of labor from Java could local emotional of indigenous people of area. For Banjarmasin area, 45.4% of labor force have university graduate, so Kabupaten Banjar about 22.7% of labor force have university graduate level.

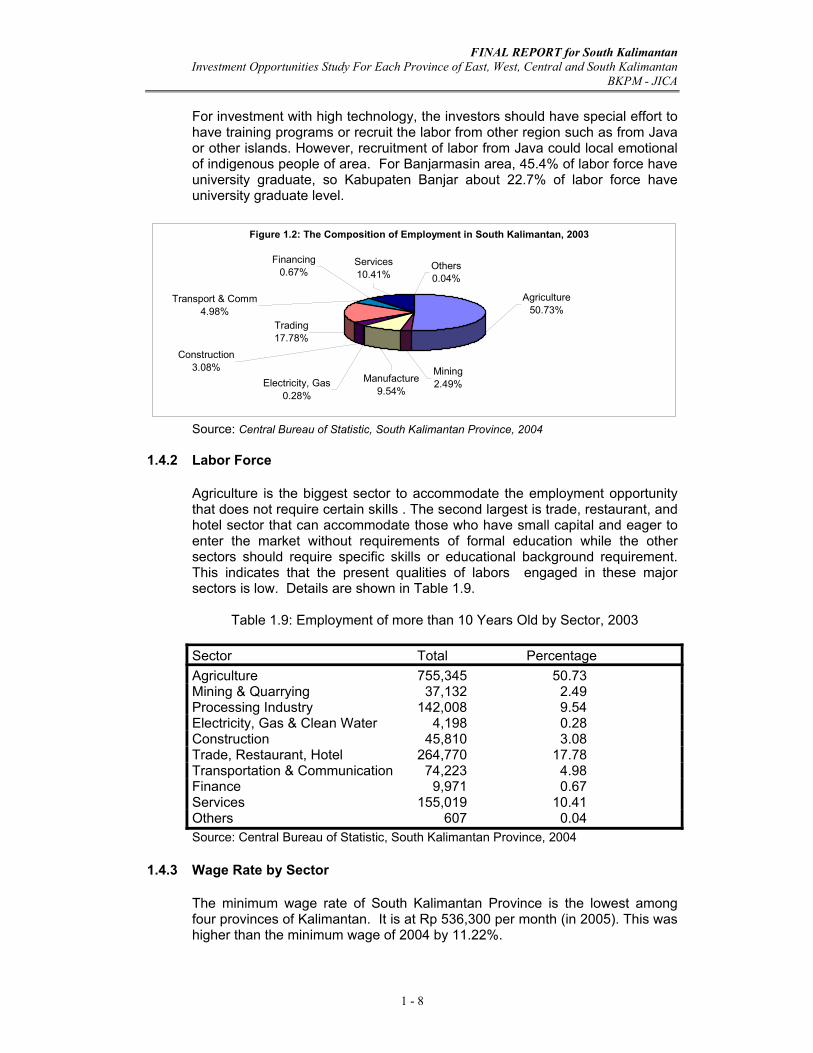

Figure 1.2: The Composition of Employment in South Kalimantan, 2003

Agriculture50.73%

Mining2.49%Electricity, Gas

0.28%

Manufacture9.54%

Construction3.08%

Trading17.78%

Transport & Comm4.98%

Financing0.67%

Services10.41%

Others0.04%

Source: Central Bureau of Statistic, South Kalimantan Province, 2004

1.4.2 Labor Force

Agriculture is the biggest sector to accommodate the employment opportunity that does not require certain skills . The second largest is trade, restaurant, and hotel sector that can accommodate those who have small capital and eager to enter the market without requirements of formal education while the other sectors should require specific skills or educational background requirement. This indicates that the present qualities of labors engaged in these major sectors is low. Details are shown in Table 1.9.

Table 1.9: Employment of more than 10 Years Old by Sector, 2003

Sector Total Percentage Agriculture 755,345 50.73 Mining & Quarrying 37,132 2.49 Processing Industry 142,008 9.54 Electricity, Gas & Clean Water 4,198 0.28 Construction 45,810 3.08 Trade, Restaurant, Hotel 264,770 17.78 Transportation & Communication 74,223 4.98 Finance 9,971 0.67 Services 155,019 10.41 Others 607 0.04 Source: Central Bureau of Statistic, South Kalimantan Province, 2004

1.4.3 Wage Rate by Sector

The minimum wage rate of South Kalimantan Province is the lowest among four provinces of Kalimantan. It is at Rp 536,300 per month (in 2005). This was higher than the minimum wage of 2004 by 11.22%.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 9

In addition to the general basis of minimum wage, the Governor of South Kalimantan has issued the minimum wage by sector basis through its decree No.059/2004. Sectoral minimum wages per month are as follows: Bank sector :Rp.550,000 per month Cement and Coal / oil sector :Rp.545,000 per month Livestock, Food industry, “jamu” industry/Home Industry, spare-part, repair and Maintenance :less than Rp.545,000/

month. Daily wages based on working day greatly depend upon the season and place. In this study, they are estimated as follow: 1. Semiskilled for construction works :Rp.50,000 per day 2. Semiskilled for agriculture works :Rp.35,000 per day 3. Semiskilled for operators :Rp.40,000 per day 4 Skilled artisan (Gold / jewelry smith etc) :Rp.80,000 per day

1.5 Land Price in Major Kabupaten/Kota

Land market price of South Kalimantan significantly varies depending upon the locations and utilization plans. For instance in Banjarmasin city the land price at commercial area is Rp.4,500,000 – Rp.5,500,000 per m2. Indeed the land price in rural area is lower than that of Banjarmasin. Cost of HGU needed for plantation development is about Rp.100,000 per hectare consisting of two types of administrative cost (legal charge) and land acquisition cost that greatly depends upon the NJOP value (land property tax value). The land price of Kabupaten Tanah Laut (Pelaihari), Tanah Bumbu (Batulicin), and Kotabaru is much lower than that of Banjarmasin. It is estimated at about 15-25% of Banjarmasin land price.

1.6 Other Basic Economic and Industrial Indicators

South Kalimantan province has various natural resources and business infrastructures such as Bank. Currently in South Kalimantan 30 bank institutions are in operation, composed of 14 general banks and 26 BPRs (community credit bank). 4 of the 14 general banks are owned by Government, 1 is BPD (province development bank), and 9 are owned by national private companies that has 194 offices and 67 Bank Rakyat Indonesia (BRI) Unit. The number of ATM reached 117 units by June of 2004.

In quarter II – 2004, the total asset of banking system was Rp.7.62 trillion or increasing by 5.83% compared to previous period increasing by 0.6%. The community funds collected by banking system was Rp.6.86 trillion that increased by 6.18% compared to last period. This implies that communities came to recognize an improvement of the banking system and trust it. .The increase were from 10.93% clearing account (Giro) and 7.43% saving, while time deposit decreased by 32.35%. The decreases in the time deposit implies that real sector is under improving, it could be short-term investment such as trading. However, it is too early to have a conclusion of long-term investment improvement. Table 1.10 presents (quarter II-2004) the current credit portfolio (Rp.4.14) trillion increased by 12.03% compared to the last period. The incremental credit portfolio is allocated for sectors of mining, electricity, agriculture, and processing industry. This credit portfolio consists of ones issued by government own general, of this total 78.04% in Rupiah currency credit and 99.87% in foreign currency.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 10

This indicates that the Government owned banks are still dominant in providing capital for South Kalimantan. Based on credit purpose, 21.13% is for investment, 50.91% is for working capital, and 27.96% is for consumption. According to Bank Indonesia Banjarmasin, the Loan to Deposit Ratio (LDR) based on project sites is 93.92% while it is 86.79% based on bank location. This is because business credit from Banks located outside of South Kalimantan have allocated the credit portfolio for projects operating in South Kalimantan. Most cases are found in Kabupaten Kotabaru Table 1.12 indicates that almost all sectors have annual growth in credit with more than two digits except manufacture and mining sector. It is assumed that the mining sector has been under production stage so no credit has been required. On the other hadn, manufacture sector, which is dominated by wood industry, has decreased due to insufficient log supply. However, in the last four years the credit portfolio for manicuring sector tends to increase with average 32.29% of the total credit followed by other sector (23.10%) and trading sector, hotel and restaurant (21.39%). It is said that since ancient times Banjar ethnic has been involved in business trading not only in domestic but also overseas especially to Middle East. A number of artisan products of Martapura have been sent to Saudi Arabia and its surrounding countries. Gold, jewel, and diamond made by Banjares are well known in Middle East. Capitals for artisan businesses are established by their own family business system; however, after the independence period they try to get acquaintance to the formal bank system. The essential is that they have a long experience in managing the family business, probably since the Dutch colonial period. This is an advantage of South Kalimantan that other three provinces do not have. Currently they probably lack technology to catch up the consumer’s demand. As basic economic factors of business, South Kalimantan has huge natural resources (coal, iron ore, diamond etc), skills in family business management, out of date technology especially in designing of products, and market in middle-east countries. Also in the 80’s, South Kalimantan experienced rubber and wood production boomso a number of rubber and wood industries were established along the Barito River

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 11

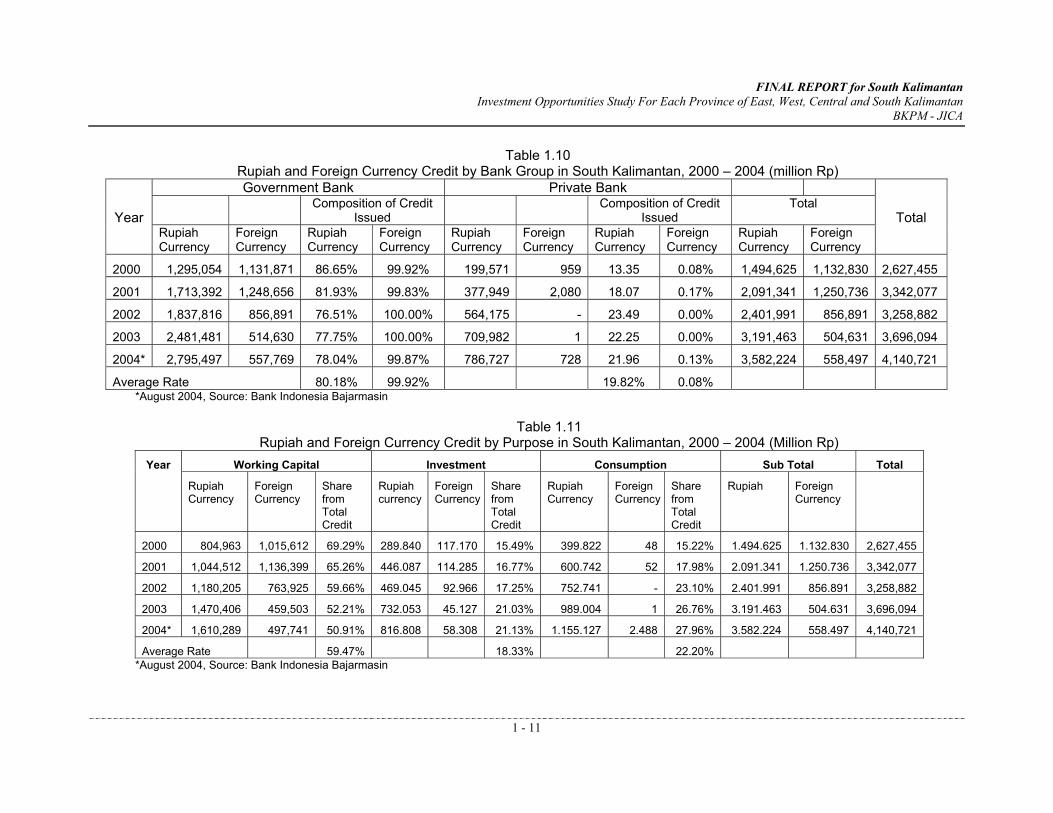

Table 1.10 Rupiah and Foreign Currency Credit by Bank Group in South Kalimantan, 2000 – 2004 (million Rp) Government Bank Private Bank

Composition of Credit Issued

Composition of Credit Issued

Total Year

Rupiah Currency

Foreign Currency

Rupiah Currency

Foreign Currency

Rupiah Currency

Foreign Currency

Rupiah Currency

Foreign Currency

Rupiah Currency

Foreign Currency

Total

2000 1,295,054 1,131,871 86.65% 99.92% 199,571 959 13.35 0.08% 1,494,625 1,132,830 2,627,455

2001 1,713,392 1,248,656 81.93% 99.83% 377,949 2,080 18.07 0.17% 2,091,341 1,250,736 3,342,077

2002 1,837,816 856,891 76.51% 100.00% 564,175 - 23.49 0.00% 2,401,991 856,891 3,258,882

2003 2,481,481 514,630 77.75% 100.00% 709,982 1 22.25 0.00% 3,191,463 504,631 3,696,094

2004* 2,795,497 557,769 78.04% 99.87% 786,727 728 21.96 0.13% 3,582,224 558,497 4,140,721

Average Rate 80.18% 99.92% 19.82% 0.08% *August 2004, Source: Bank Indonesia Bajarmasin

Table 1.11

Rupiah and Foreign Currency Credit by Purpose in South Kalimantan, 2000 – 2004 (Million Rp) Working Capital Investment Consumption Sub Total Total Year

Rupiah Currency

Foreign Currency

Share from Total Credit

Rupiah currency

Foreign Currency

Share from Total Credit

Rupiah Currency

Foreign Currency

Share from Total Credit

Rupiah Foreign Currency

2000 804,963 1,015,612 69.29% 289.840 117.170 15.49% 399.822 48 15.22% 1.494.625 1.132.830 2,627,455

2001 1,044,512 1,136,399 65.26% 446.087 114.285 16.77% 600.742 52 17.98% 2.091.341 1.250.736 3,342,077

2002 1,180,205 763,925 59.66% 469.045 92.966 17.25% 752.741 - 23.10% 2.401.991 856.891 3,258,882

2003 1,470,406 459,503 52.21% 732.053 45.127 21.03% 989.004 1 26.76% 3.191.463 504.631 3,696,094

2004* 1,610,289 497,741 50.91% 816.808 58.308 21.13% 1.155.127 2.488 27.96% 3.582.224 558.497 4,140,721

Average Rate 59.47% 18.33% 22.20% *August 2004, Source: Bank Indonesia Bajarmasin

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 12

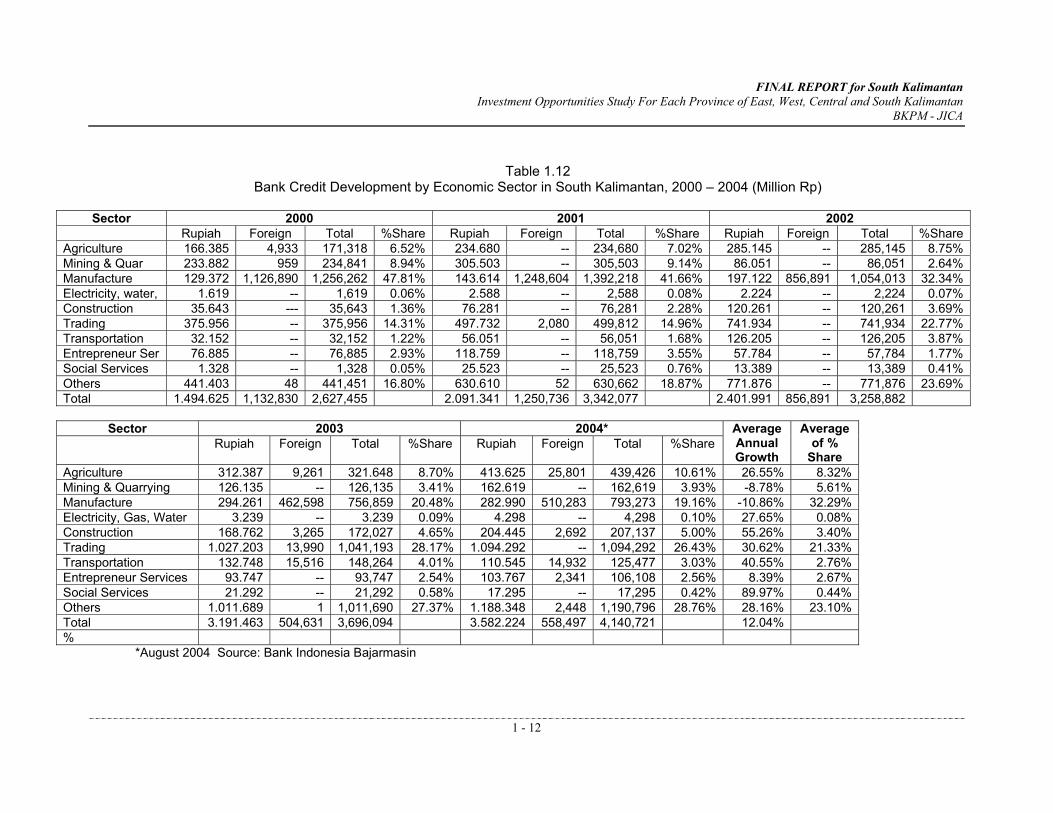

Table 1.12

Bank Credit Development by Economic Sector in South Kalimantan, 2000 – 2004 (Million Rp)

Sector 2000 2001 2002 Rupiah Foreign Total %Share Rupiah Foreign Total %Share Rupiah Foreign Total %Share

Agriculture 166.385 4,933 171,318 6.52% 234.680 -- 234,680 7.02% 285.145 -- 285,145 8.75%Mining & Quar 233.882 959 234,841 8.94% 305.503 -- 305,503 9.14% 86.051 -- 86,051 2.64%Manufacture 129.372 1,126,890 1,256,262 47.81% 143.614 1,248,604 1,392,218 41.66% 197.122 856,891 1,054,013 32.34%Electricity, water, 1.619 -- 1,619 0.06% 2.588 -- 2,588 0.08% 2.224 -- 2,224 0.07%Construction 35.643 --- 35,643 1.36% 76.281 -- 76,281 2.28% 120.261 -- 120,261 3.69%Trading 375.956 -- 375,956 14.31% 497.732 2,080 499,812 14.96% 741.934 -- 741,934 22.77%Transportation 32.152 -- 32,152 1.22% 56.051 -- 56,051 1.68% 126.205 -- 126,205 3.87%Entrepreneur Ser 76.885 -- 76,885 2.93% 118.759 -- 118,759 3.55% 57.784 -- 57,784 1.77%Social Services 1.328 -- 1,328 0.05% 25.523 -- 25,523 0.76% 13.389 -- 13,389 0.41%Others 441.403 48 441,451 16.80% 630.610 52 630,662 18.87% 771.876 -- 771,876 23.69%Total 1.494.625 1,132,830 2,627,455 2.091.341 1,250,736 3,342,077 2.401.991 856,891 3,258,882

Sector 2003 2004*

Rupiah Foreign Total %Share Rupiah Foreign Total %Share Average Annual Growth

Average of %

Share Agriculture 312.387 9,261 321.648 8.70% 413.625 25,801 439,426 10.61% 26.55% 8.32%Mining & Quarrying 126.135 -- 126,135 3.41% 162.619 -- 162,619 3.93% -8.78% 5.61%Manufacture 294.261 462,598 756,859 20.48% 282.990 510,283 793,273 19.16% -10.86% 32.29%Electricity, Gas, Water 3.239 -- 3.239 0.09% 4.298 -- 4,298 0.10% 27.65% 0.08%Construction 168.762 3,265 172,027 4.65% 204.445 2,692 207,137 5.00% 55.26% 3.40%Trading 1.027.203 13,990 1,041,193 28.17% 1.094.292 -- 1,094,292 26.43% 30.62% 21.33%Transportation 132.748 15,516 148,264 4.01% 110.545 14,932 125,477 3.03% 40.55% 2.76%Entrepreneur Services 93.747 -- 93,747 2.54% 103.767 2,341 106,108 2.56% 8.39% 2.67%Social Services 21.292 -- 21,292 0.58% 17.295 -- 17,295 0.42% 89.97% 0.44%Others 1.011.689 1 1,011,690 27.37% 1.188.348 2,448 1,190,796 28.76% 28.16% 23.10%Total 3.191.463 504,631 3,696,094 3.582.224 558,497 4,140,721 12.04%%

*August 2004 Source: Bank Indonesia Bajarmasin

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 13

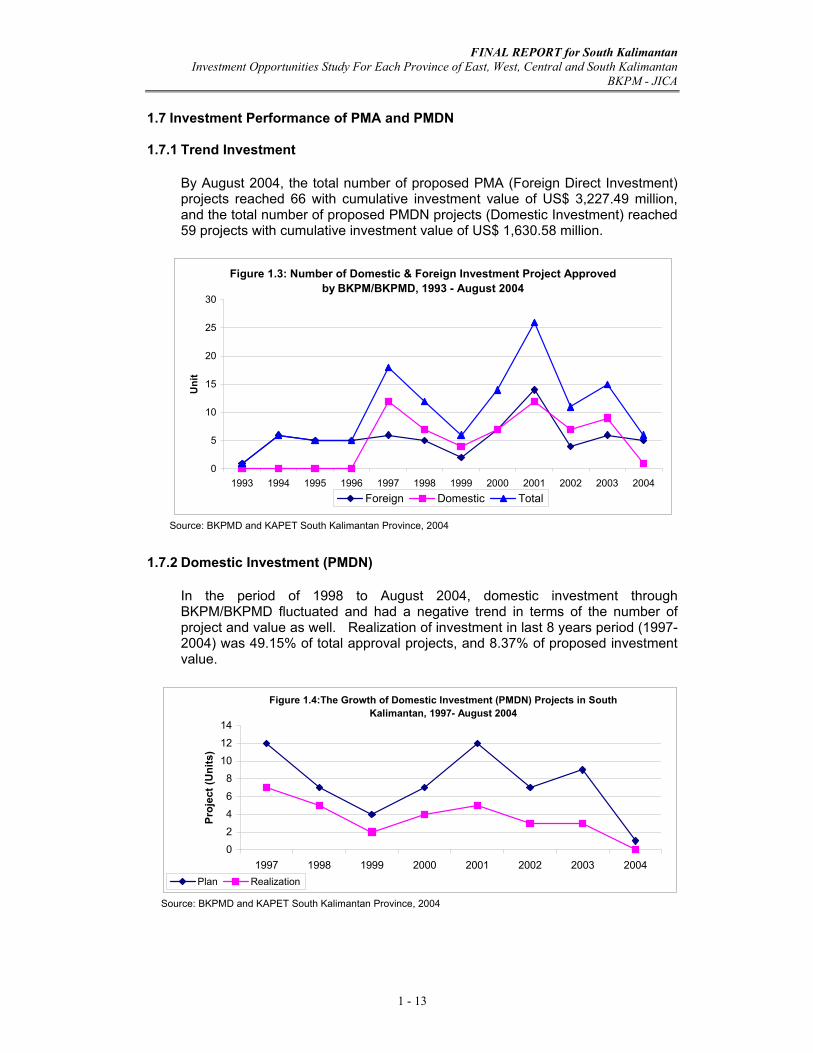

1.7 Investment Performance of PMA and PMDN 1.7.1 Trend Investment

By August 2004, the total number of proposed PMA (Foreign Direct Investment) projects reached 66 with cumulative investment value of US$ 3,227.49 million, and the total number of proposed PMDN projects (Domestic Investment) reached 59 projects with cumulative investment value of US$ 1,630.58 million.

Figure 1.3: Number of Domestic & Foreign Investment Project Approved by BKPM/BKPMD, 1993 - August 2004

0

5

10

15

20

25

30

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Uni

t

Foreign Domestic Total

Source: BKPMD and KAPET South Kalimantan Province, 2004 1.7.2 Domestic Investment (PMDN)

In the period of 1998 to August 2004, domestic investment through BKPM/BKPMD fluctuated and had a negative trend in terms of the number of project and value as well. Realization of investment in last 8 years period (1997-2004) was 49.15% of total approval projects, and 8.37% of proposed investment value.

Figure 1.4:The Growth of Domestic Investment (PMDN) Projects in South Kalimantan, 1997- August 2004

0246

8101214

1997 1998 1999 2000 2001 2002 2003 2004

Proj

ect (

Uni

ts)

Plan Realization

Source: BKPMD and KAPET South Kalimantan Province, 2004

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 14

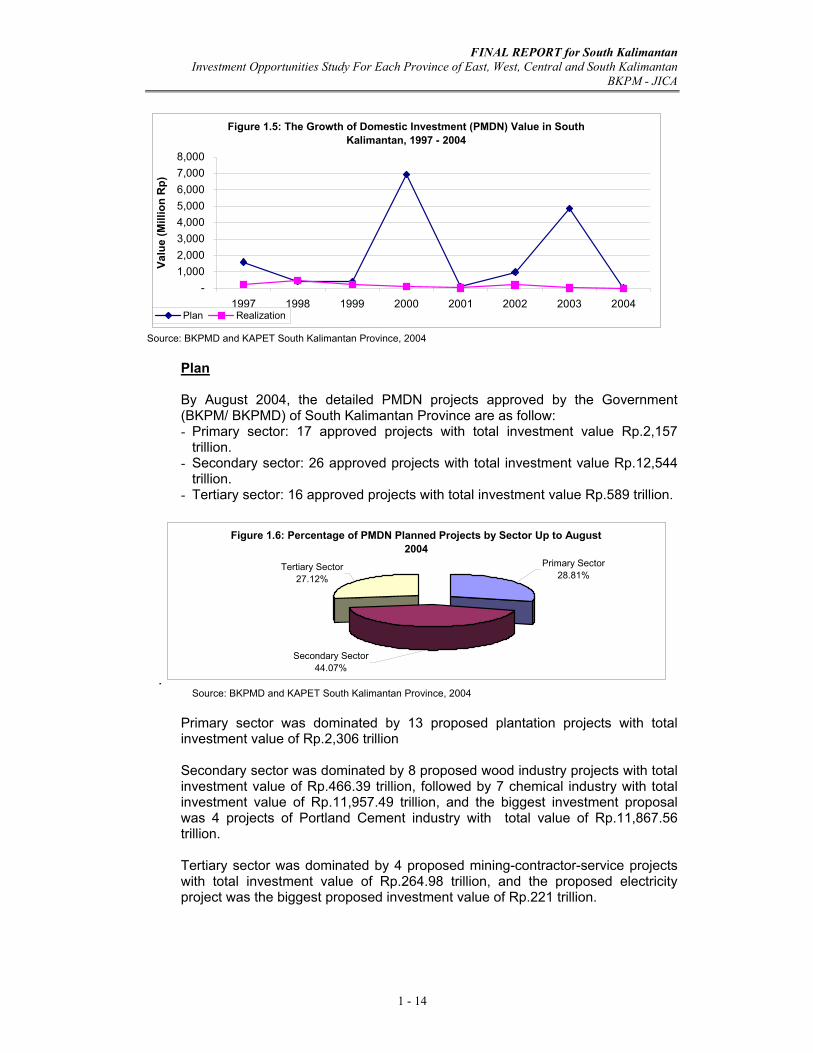

Figure 1.5: The Growth of Domestic Investment (PMDN) Value in South Kalimantan, 1997 - 2004

-1,0002,0003,0004,0005,0006,0007,0008,000

1997 1998 1999 2000 2001 2002 2003 2004

Valu

e (M

illio

n R

p)

Plan Realization

Source: BKPMD and KAPET South Kalimantan Province, 2004

Plan

By August 2004, the detailed PMDN projects approved by the Government (BKPM/ BKPMD) of South Kalimantan Province are as follow: - Primary sector: 17 approved projects with total investment value Rp.2,157

trillion. - Secondary sector: 26 approved projects with total investment value Rp.12,544

trillion. - Tertiary sector: 16 approved projects with total investment value Rp.589 trillion.

.

Figure 1.6: Percentage of PMDN Planned Projects by Sector Up to August 2004

Primary Sector28.81%

Secondary Sector44.07%

Tertiary Sector27.12%

Source: BKPMD and KAPET South Kalimantan Province, 2004

Primary sector was dominated by 13 proposed plantation projects with total investment value of Rp.2,306 trillion Secondary sector was dominated by 8 proposed wood industry projects with total investment value of Rp.466.39 trillion, followed by 7 chemical industry with total investment value of Rp.11,957.49 trillion, and the biggest investment proposal was 4 projects of Portland Cement industry with total value of Rp.11,867.56 trillion. Tertiary sector was dominated by 4 proposed mining-contractor-service projects with total investment value of Rp.264.98 trillion, and the proposed electricity project was the biggest proposed investment value of Rp.221 trillion.

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 15

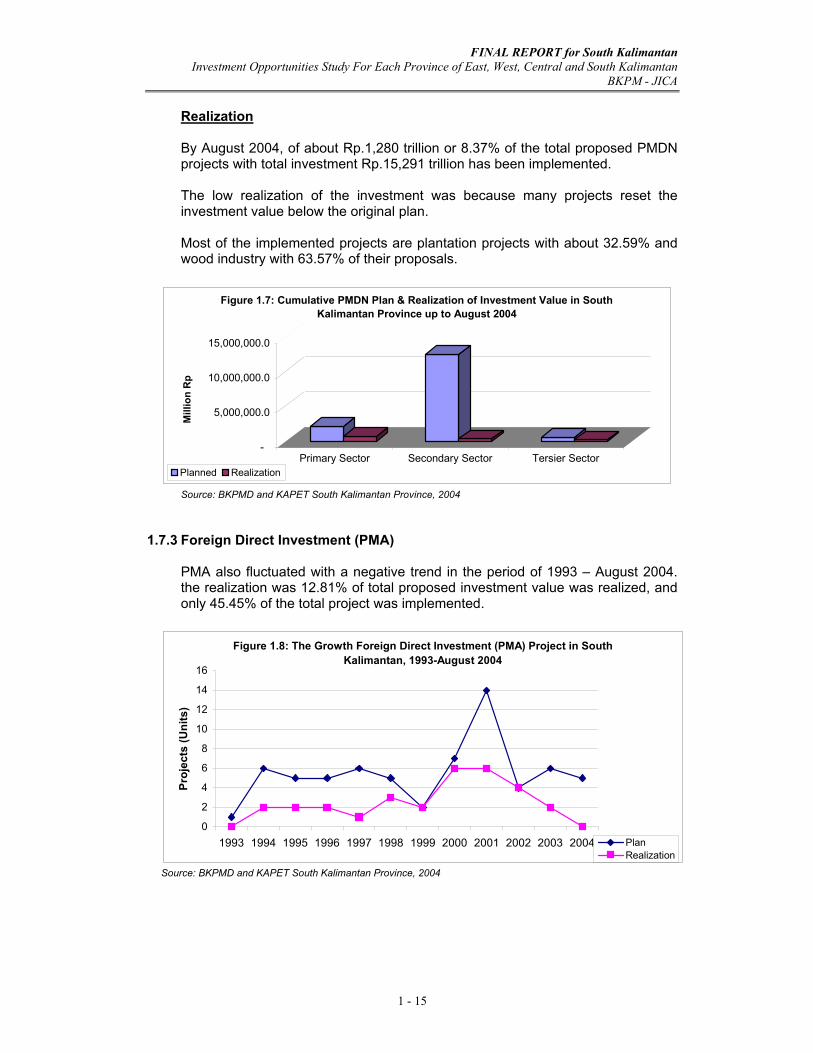

Realization By August 2004, of about Rp.1,280 trillion or 8.37% of the total proposed PMDN projects with total investment Rp.15,291 trillion has been implemented. The low realization of the investment was because many projects reset the investment value below the original plan. Most of the implemented projects are plantation projects with about 32.59% and wood industry with 63.57% of their proposals.

-

5,000,000.0

10,000,000.0

15,000,000.0

Mill

ion

Rp

Primary Sector Secondary Sector Tersier Sector

Figure 1.7: Cumulative PMDN Plan & Realization of Investment Value in South Kalimantan Province up to August 2004

Planned Realization

Source: BKPMD and KAPET South Kalimantan Province, 2004

1.7.3 Foreign Direct Investment (PMA)

PMA also fluctuated with a negative trend in the period of 1993 – August 2004. the realization was 12.81% of total proposed investment value was realized, and only 45.45% of the total project was implemented.

Figure 1.8: The Growth Foreign Direct Investment (PMA) Project in South Kalimantan, 1993-August 2004

0

2

4

6

8

10

12

14

16

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Proj

ects

(Uni

ts)

PlanRealization

Source: BKPMD and KAPET South Kalimantan Province, 2004

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 16

Figure 1.9: The Growth of Foreign Direct Investment (PMA) Value in South Kalimantan, 1993- August 2004

-0.2000.4000.6000.8001.0001.2001.4001.6001.800

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Val

ue (M

illio

n U

S$)

Plan Realization

Source: BKPMD and KAPET South Kalimantan Province, 2004 Plan By August 2004, the foreign investors (PMA) proposed 66 projects with total investment value of US$.572,93 million and Rp.3,227.49 million. those proposals comprised 30 projects of secondary sector, 20 projects of tertiary sector, and 16 projects of primary sector. Of PMA project proposals, the secondary sector of wood industry is the main business that most interests foreign investors with total value of US$.14,624.89 million, followed by chemical industry of US$. 2,079.45 million. More specific project of wood industry is Pulp and Paper industry with total investment value of US$.1,157.69 million. The value of primary sector project is US$. 614.30 million including 3 mining projects with total investment value of US$. 17.94 million.

Figure 1.10: Percentage of PMA Planned Projects by Sector Up to August 2004

Tersier Sector30.30%

Secondary Sector45.45%

Primary Sector24.24%

Source: BKPMD and KAPET South Kalimantan Province, 2004

Realization By 2004, the vale of implemented PMA projects reached US$.533.94 million or 12.72% of the total investment plan. Projects that implemented by PMA scheme are as follows: - Plantation: 7 projects with investment value US$.72.98 million - Mining: 1 project with investment value US$.26.47 million - Wood industry, 5 projects with investment value US$.0.73 million

FINAL REPORT for South Kalimantan Investment Opportunities Study For Each Province of East, West, Central and South Kalimantan

BKPM - JICA

1 - 17

- Chemical industry: 4 projects with investment value US$.342.86 million - Food industry: 1 project with investment value US$.23.83 million - Telecommunication: 3 projects with investment value US$.52.04 million - Mining contractor Services: 3 projects with investment value US$.2.46 million

-500.00

1,000.001,500.002,000.002,500.003,000.003,500.00

Mill

ion

US$

Primary Sector Secondary Sector Tertiary Sector

Figure 1.11: Cumulative PMA Plan & Realization of Investment Value in South Kalimantan Province up to August 2004

Plan Realization

Source: BKPMD and KAPTE South Kalimantan Province, 2004 Implemented projects of PMDN and PMA accounted for 8.37% and 12.72% respectively, and both are still lower than proposed. Many project proposals had indicated that the investment promotion in introducing the natural resources of South Kalimantan would succeed; however, as a matter of fact the realization of investment is still lower than proposed. . For this reason, it is assumed that economic crisis of Indonesia and uncertainly factors affected investment will of industrialists. The local government should address this problem to encourage domestic and foreign investors to invest their capitals in South Kalimantan. The results of the interviews point out that the government should execute the reform of investment policy through law enforcement, bureaucracy improvement, and facility competitiveness. The local government needs to consider that competition is not only among regions but also among other countries. For instance, the wood industry faces serious problems generated from a lack of raw materials; the government should examine an alternative that can address this problem such as HTI program.

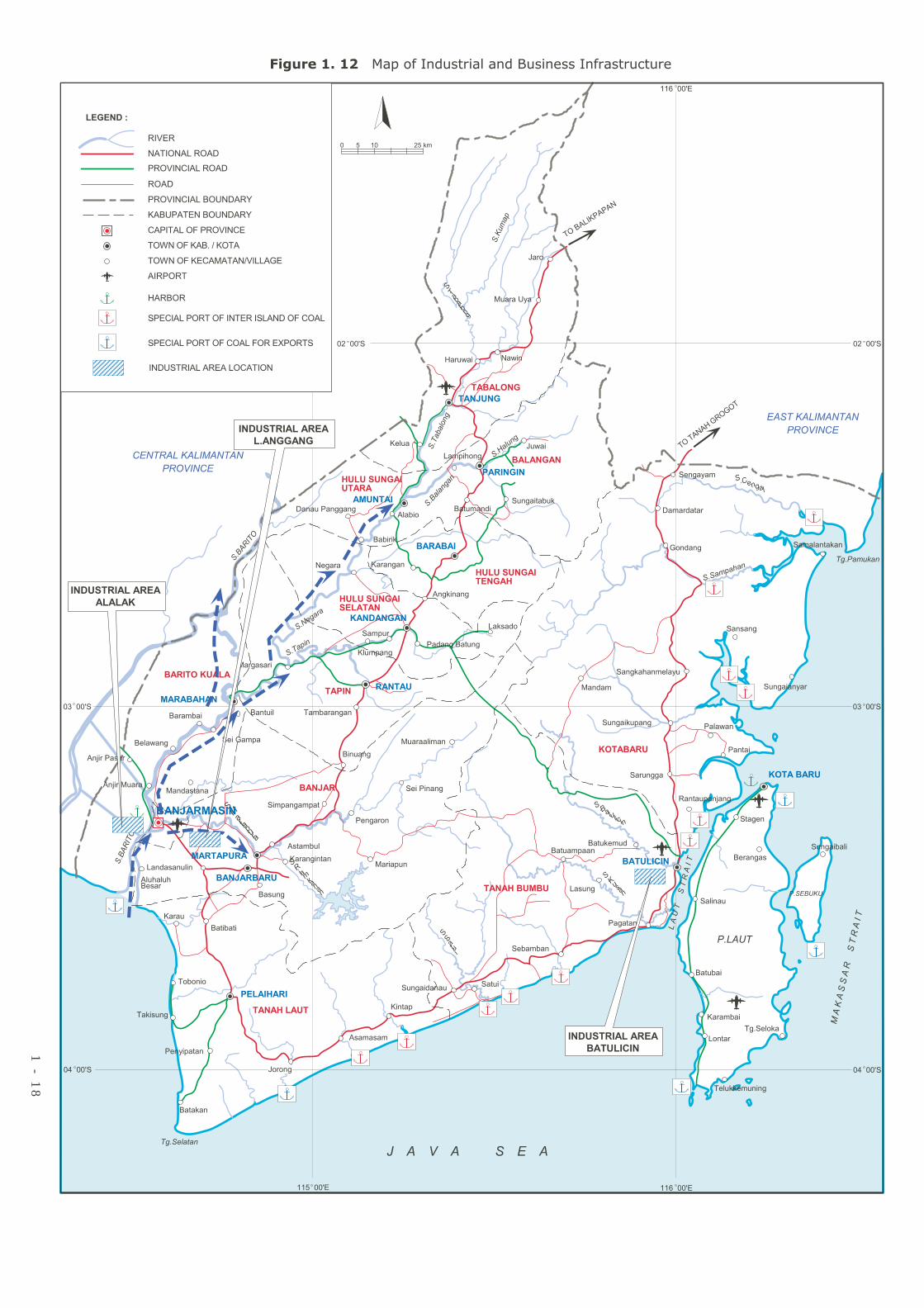

1.8 Industrial Map

Overview of industrial and business infrastructures is presented in Figure 1.12

��������� ���������

�������

���������

������

�������

������

�������

���� ����

�������

��������

�����

�������������

����

�������������������

������������������

�������������������

������������� �����

������������!���� �����"�

�������

����������������

�� ����

�������������

�� ����

� � �� � �� � �� � � � � � � � � � � � ��

��� ����

����������

�����

����

���

�������

� ���

����������

�����

����������

��

��� ��

��������

������

����

�������

������

�����

�����������

������

�����������������������������

���� ��!��

��"�����

���� ��!��

������

������

���

�����

������

���

����

����

������

� ����

�������

�#$%&%'(

�')*+�!,%+%

�')*+��%-%+

!%'.%-/%'%

�%+% 0%*

#*�"% 1%

�%'/,*$ �% 0%+%'(%'

!%+(%-%+*

�$, 1%'(

�#(%+%

�%'%,��%'((%'(

�%0*+*�

�*',%'(

* 1%'(% 1%/

�#'(%+2'

�-/% 0,$

�%+%'(*'/%'

�%/*0%/*

�%-,'(

32+2'(

�-% %-%

�#'4*1%/%'

�%/%�%'

�%'.%-%',$*'

�%+%,

�$,5%$,5�#-%+

6%+,&%*

�#$,%

�$%0*2

�*'/%1

,'(%*.%'%,

#*��*'%'(

!,%+%%$* %'

% 1,+

�'(�*'%'(

�%.%'(��%/,'(

�%+%'(%'

�%�-%.2

�%/, %'.*

�%&*'

!,%+%��4%

3%+2

�2'/%+

�(�#$2�%

�%(%/%'

�#+%'(%-

,'(%*�,1%'(

�%'/%*

�%�*-,'(

�202'*2

3,&%*

�% 1*52'(

,'(%*/%0,�

#0% 0%'

%/,*

�#$,��# ,'*'(

�%+% 0%*

�%/,0%*

�%/,% 1%%'

�%-,'(

%$*'%,

�%/,�# ,.

�%'/%,1%')%'(

�%$%&%'

%+,'((%

!%'.%

%'(�%5%' #$%4,

"2'.%'(

�% %+.%/%+

#'(%4%

/%(#'

,'(%*0%$*

,'(%*%'4%+

%'-%'(

% %$%'/%�%'

����������

�����##

����������

!%+*%1,'

����#�

��������

�����

�������6�"

��"��

�����

���������������

��������

���������

�����

������

6�����

����������������������������������

�������������������������7����

������

�������

��������$��

��������

����������

��#��������

���%��

�����������������������

������������������������ ������������������ ��� �� �

1 - 1

8

����������

��������

����������

���

����������

�������

CURRENT SITUATION AND FUTURE PROSPECT OF INFRASTRUCTURE

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 1

CHAPTER 2

CURRENT SITUATION AND FUTURE PROSPECT OF INFRASTRUCTURE

2.1 Road

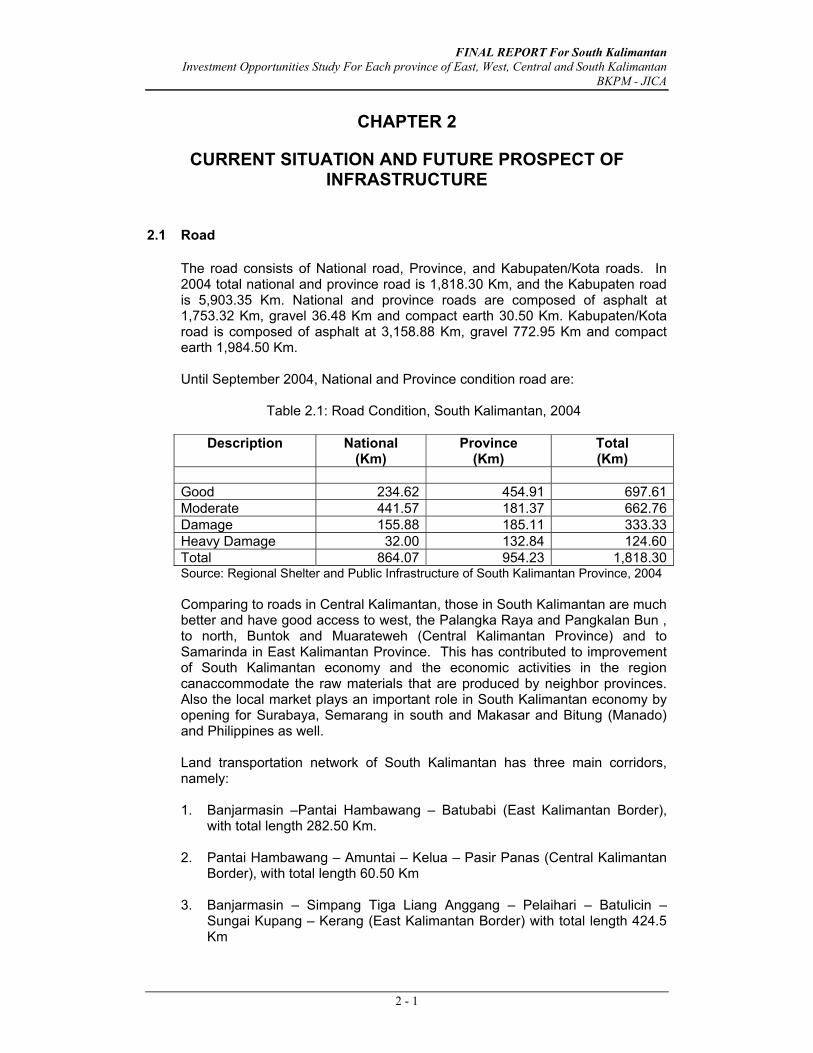

The road consists of National road, Province, and Kabupaten/Kota roads. In 2004 total national and province road is 1,818.30 Km, and the Kabupaten road is 5,903.35 Km. National and province roads are composed of asphalt at 1,753.32 Km, gravel 36.48 Km and compact earth 30.50 Km. Kabupaten/Kota road is composed of asphalt at 3,158.88 Km, gravel 772.95 Km and compact earth 1,984.50 Km. Until September 2004, National and Province condition road are:

Table 2.1: Road Condition, South Kalimantan, 2004

Description National (Km)

Province (Km)

Total (Km)

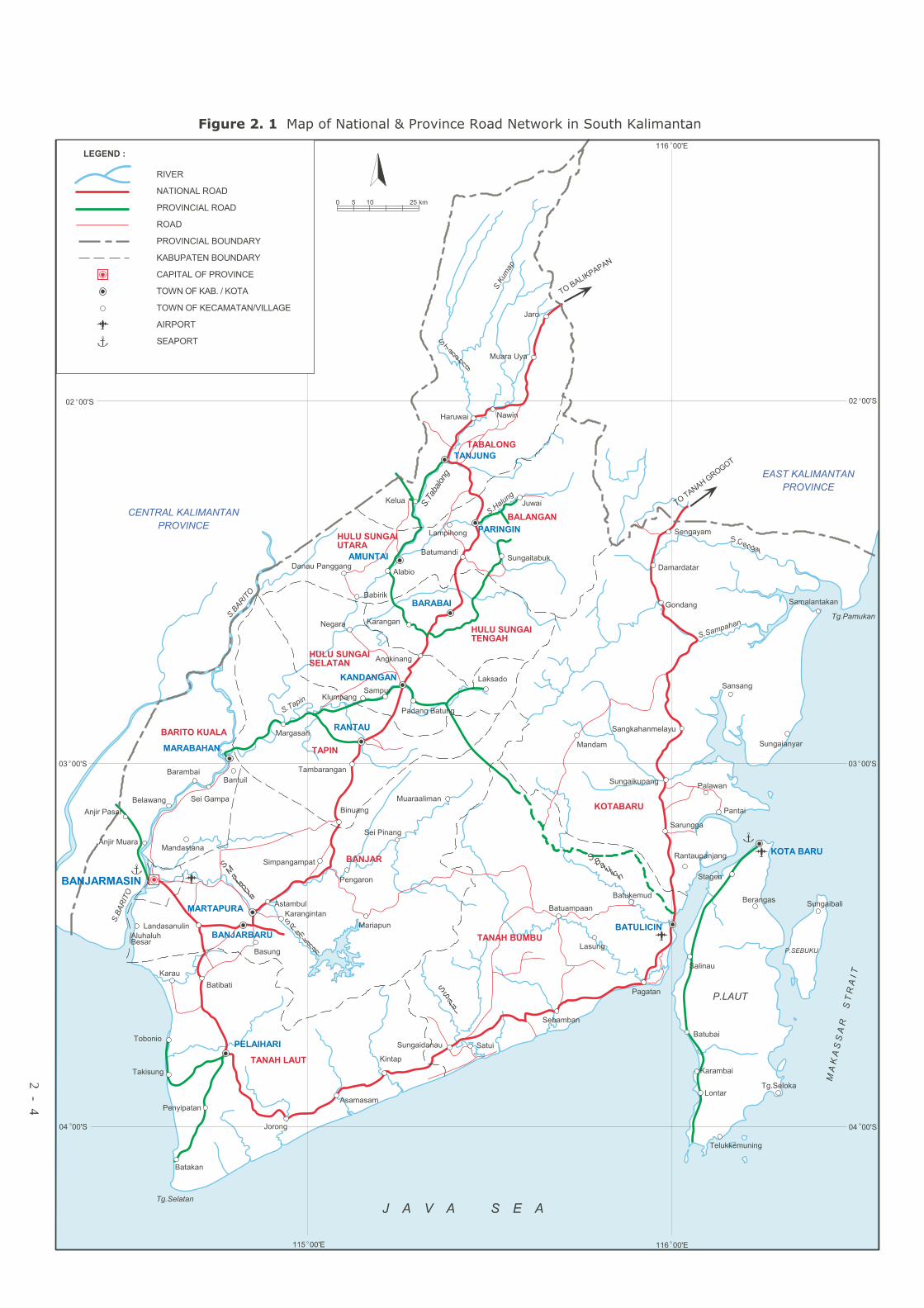

Good 234.62 454.91 697.61Moderate 441.57 181.37 662.76Damage 155.88 185.11 333.33Heavy Damage 32.00 132.84 124.60Total 864.07 954.23 1,818.30Source: Regional Shelter and Public Infrastructure of South Kalimantan Province, 2004 Comparing to roads in Central Kalimantan, those in South Kalimantan are much better and have good access to west, the Palangka Raya and Pangkalan Bun , to north, Buntok and Muarateweh (Central Kalimantan Province) and to Samarinda in East Kalimantan Province. This has contributed to improvement of South Kalimantan economy and the economic activities in the region canaccommodate the raw materials that are produced by neighbor provinces. Also the local market plays an important role in South Kalimantan economy by opening for Surabaya, Semarang in south and Makasar and Bitung (Manado) and Philippines as well. Land transportation network of South Kalimantan has three main corridors, namely:

1. Banjarmasin –Pantai Hambawang – Batubabi (East Kalimantan Border),

with total length 282.50 Km. 2. Pantai Hambawang – Amuntai – Kelua – Pasir Panas (Central Kalimantan

Border), with total length 60.50 Km

3. Banjarmasin – Simpang Tiga Liang Anggang – Pelaihari – Batulicin – Sungai Kupang – Kerang (East Kalimantan Border) with total length 424.5 Km

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 2

Besides those three corridors, also there are ring roads: 1. Ring road of Liang Anggang – Trisakti, with length 22 Km

2. Connecting road of Kandangan – Lumpangi – Batulicin, with total length

175.8 Km. Currently the segment of Kandangan – Lumpangi is asphalt while not all part of segment of Lumpangi – Batulicin (135.55 Km) is asphalt yet. South Kalimantan Provincial Government would asphalt this segment in the three fiscal year (2005, 2006 and 2007). The road that connects Banua Lima area (Kabupaten of Tapin, Hulu Sungai Selatan, Hulu Sungai Tengah, Hulu Sungai Utara, Tabalong) and Batulicin will be constructed and then products from northern part of South Kalimantan can be transported to Central Kalimantan as well are not necessary pass through Banjarmasin any longer it can pass through directly to Batulicin harbor

These access roads could create a favorable condition for investment in this area.

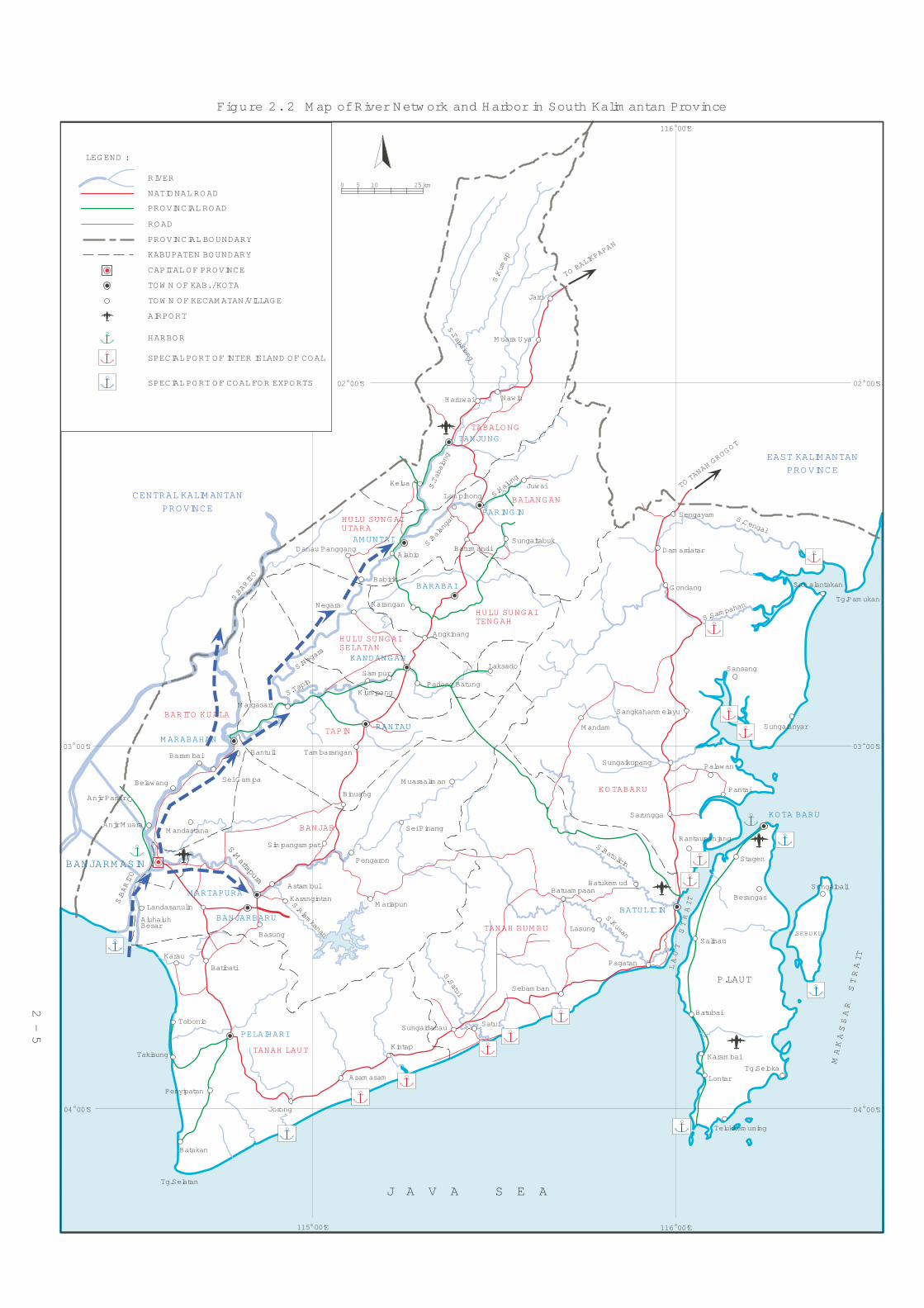

2.2 River

Water transportation through rivers is the common transportation mode to access Central Kalimantan and remote areas in South Kalimantan Province. Almost all Kabupaten/Kota have access to water transportation mode; however, at present a number of community use the land transportation mode due to availability of good road condition There are 10 important rivers, 3 canal (anjir) link the Barito River and Kapuas River and 13 harbors function as transshipment of land surface transportation mode. Canal that connects the Barito and Kapuas is the main line for coal transportation from Kabupaten Barito Selatan of Central Kalimantan to Batulicin and Trisakti harbors of South Kalimantan. Barito river is the biggest river in South Kalimantan, which can be cruised by ship with up to 3,500 tons of DWT capacity from the river mouth to Trisakti port in rainy season. From Trisakti harbor to Marabahan is sailed by smaller ship with 3,000 tons of DWT capacity. Negara river that connects Marabahan to Margasari can be cruised by ship with 2,000 ton DWT and the segment between Margasaro and Negara town can be cruised by smaller ship of 1,500 ton DWT. Martapura river that connects Martapura and Bajarmasin can be cruised by small ship with 500 ton DWT. Balangan river that connects Negara town and Amuntai can be cruised by ship with 500 ton DWT. All these cruises are possible in rainy reason with sufficient water depth. The river depth frequently fluctuates, which is mainly affected by rainfall. On average the rainy season is about 7 months so the water transportation is reliable for about 7 months per year and for the rest of the year inland transportation should be utilized.

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 3

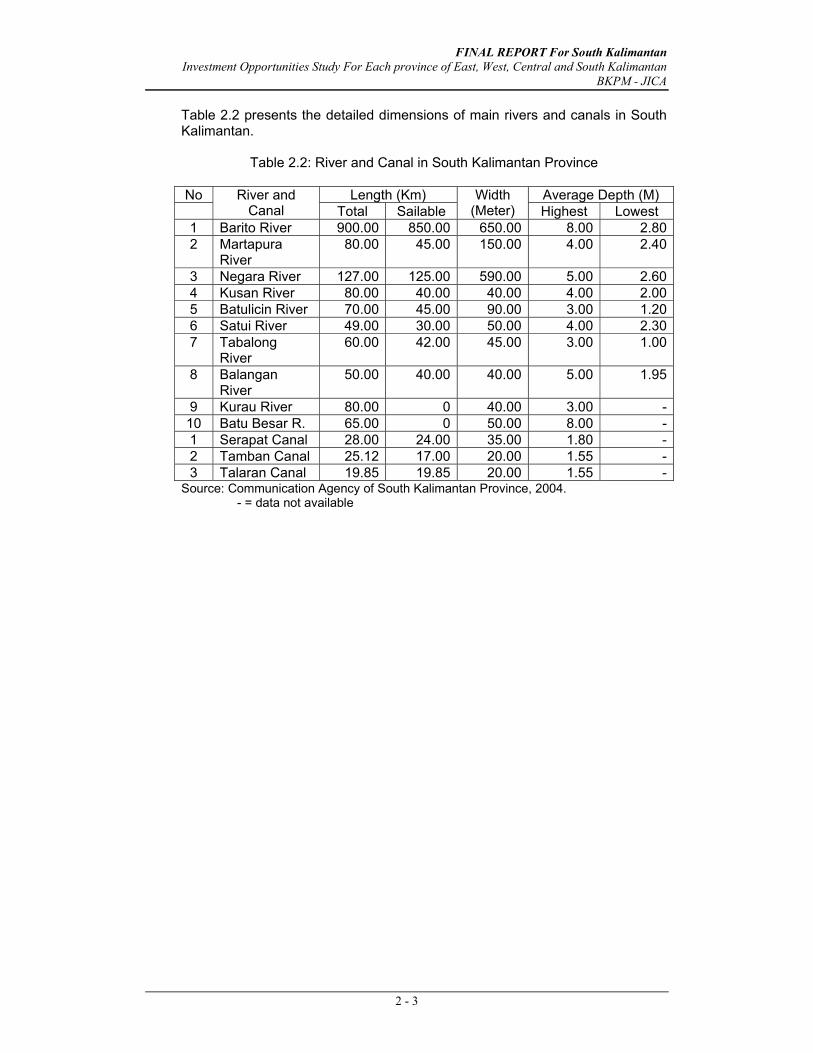

Table 2.2 presents the detailed dimensions of main rivers and canals in South Kalimantan.

Table 2.2: River and Canal in South Kalimantan Province

No Length (Km) Average Depth (M)

River and Canal Total Sailable

Width (Meter) Highest Lowest

1 Barito River 900.00 850.00 650.00 8.00 2.802 Martapura

River 80.00 45.00 150.00 4.00 2.40

3 Negara River 127.00 125.00 590.00 5.00 2.604 Kusan River 80.00 40.00 40.00 4.00 2.005 Batulicin River 70.00 45.00 90.00 3.00 1.206 Satui River 49.00 30.00 50.00 4.00 2.307 Tabalong

River 60.00 42.00 45.00 3.00 1.00

8 Balangan River

50.00 40.00 40.00 5.00 1.95

9 Kurau River 80.00 0 40.00 3.00 -10 Batu Besar R. 65.00 0 50.00 8.00 -1 Serapat Canal 28.00 24.00 35.00 1.80 -2 Tamban Canal 25.12 17.00 20.00 1.55 -3 Talaran Canal 19.85 19.85 20.00 1.55 -

Source: Communication Agency of South Kalimantan Province, 2004. - = data not available

��������� ���������

�������

���������

������

�������

������

�������

���� ����

�������

��������

�����

�������������

����

�������������������

������������������

�������������������

������������� �����

������������!���� �����"�

�������

������

����������������

�� ����

�������������

�� ����

� � �� � �� � �� � � � � � � � � � � � ��

��� ����

����������

�����

����

���

�������

� ���

����������

�����

����������

��

��� ��

��������

������

����

�������

������

�����

�����������

������

�����������������������������

���� ��!��

��"�����

���� ��!��

������

������

���

�����

������

���

����

����

������

� ����

�������

�#$%&%'(

�')*+�!,%+%

�')*+��%-%+

!%'.%-/%'%

�%+% 0%*

#*�"% 1%

�%'/,*$

�% 0%+%'(%'

!%+(%-%+*

�$, 1%'(

�#(%+%

�%'%,��%'((%'(

�%0*+*�

�*',%'(

* 1%'(% 1%/

�#'(%+2'

�-/% 0,$

�%+%'(*'/%'

�%/*0%/*

�%-,'(

32+2'(

�-% %-% �#'4*1%/%'

�%/%�%'

�%'.%-%',$*'

�%+%,

�$,5%$,5�#-%+

6%+,&%*

�#$,%

�$%0*2

�*'/%1

,'(%*.%'%,

#*��*'%'(

!,%+%%$* %'

% 1,+

�'(�*'%'(

�%.%'(��%/,'(

�%+%'(%'

�%�-%.2

�%/, %'.*

�%&*'

!,%+%��4%

3%+2

�2'/%+�(�#$2�%

�%(%/%'

�#+%'(%-

,'(%*�,1%'(

�%'/%*

�%�*-,'(

�202'*2

3,&%*

�% 1*52'(

,'(%*/%0,�

#0% 0%'

%/,*

�#$,��# ,'*'(

�%+% 0%*

�%/,0%*

�%/,% 1%%'

�%-,'(

%$*'%,

�%/,�# ,.

�%'/%,1%')%'(

�%$%&%'

%+,'((%

!%'.%

%'(�%5%' #$%4,

"2'.%'(

�% %+.%/%+

#'(%4%

/%(#'

,'(%*0%$*

,'(%*%'4%+

%'-%'(

% %$%'/%�%'

����������

�����##

����������

!%+*%1,'

����#�

��������

�����

�������6�"

��"��

�����

���������������

��������

���������

�����

������

������

�������

��������$��

��������������������������� ���������������������������������

2 - 4

115 00’E 116 00’E

02 00’S

116 00’E

04 00’S

03 00’S

04 00’S

03 00’S

25 km1050

02 00’S

LEG END :

RIVER

NATIONAL ROAD

ROAD

PROVINCIAL BOUNDARY

KABUPATEN BOUNDARY

CAPITAL OF PROVINCE

TOW N OF KAB. / KOTA

TOW N OF KECAM ATAN/VILLAGE

AIRPORT

CENTRAL KALIM ANTAN

PROVINCE

EAST KALIM ANTAN

PROVINCE

J A V A S E A

BARITO KUALA

HULU SUNG AISELATAN

TAPIN

BANJAR

TANAH LAUT

KOTABARU

HULU SUNG AITENG AH

HULU SUNG AIUTARA

TABALO NG

S.Cengal

S.Sam pa

han

S.Tapin

S.Riamkanan

S.Martapura

S.BARITO

M A K A S S A R S T R A I T

S.Tabalong

S.Halung

S.Tabalong

S.Kum

ap

TANJUNG

BARABAI

AM UNTAI

KANDANG AN

RANTAU

M ARABAHAN

M ARTAPURA

PELAIHARI

KOTA BARU

BANJARM ASIN

Belawang

Anjir M uara

Anjir Pasar

M andastana

Baram bai

Sei G am pa

Bantuil Tam barangan

M argasari

Klum pang

Negara

Danau Panggang

Babirik

Binuang

Sim pangam pat

Pengaron

Astam bul

Karangintan

Batibati

Basung

Jorong

Asam asam

Penyipatan

Batakan

Landasanulin

Karau

AluhaluhBesar

Haruwai

Kelua

Alabio

Kintap

Sungaidanau

Sei Pinang

M uaraalim an

Sam pur

Angkinang

Padang Batung

Karangan

Laksado

Batum andi

Nawin

M uara Uya

Jaro

Lontar

Tg.Seloka

Pagatan

Berangas

Sungaikupang

Pantai

Takisung

Tobonio

JuwaiLam pihong

Sungaitabuk

Sebam ban

Satui

Telukkem uning

Karam bai

Batubai

Batuam paan

Lasung

Salinau

Batukem ud

Rantaupanjang

Palawan

Sarungga

M andam

Sangkahanm elayu

Gondang

Dam ardatar

Sengayam

Stagen

Sungaibali

Sungaianyar

Sansang

Sam alantakan

Tg.Pam ukan

P.SEBUKU

Tg.Selatan

M ariapun

P.LAUT

TO BA

LIKPAPAN

TO TA

NAH GROG

OT

BANJARBARU

PROVINCIAL ROAD

BATULICIN

TANAH BUM BU

BALANG AN

PARING IN

HARBOR

SPECIAL PORT OF INTER ISLAND OF COAL

SPECIAL PORT OF COAL FOR EXPORTS

S.BARITO

S.Satui

S.Batulicin

S.Negara

S.Balangan

LAUT STRAIT

S.Kusan

Figure 2. 2 M ap of River Netw ork and Harbor in South Kalim antan Province

2 - 5

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 6

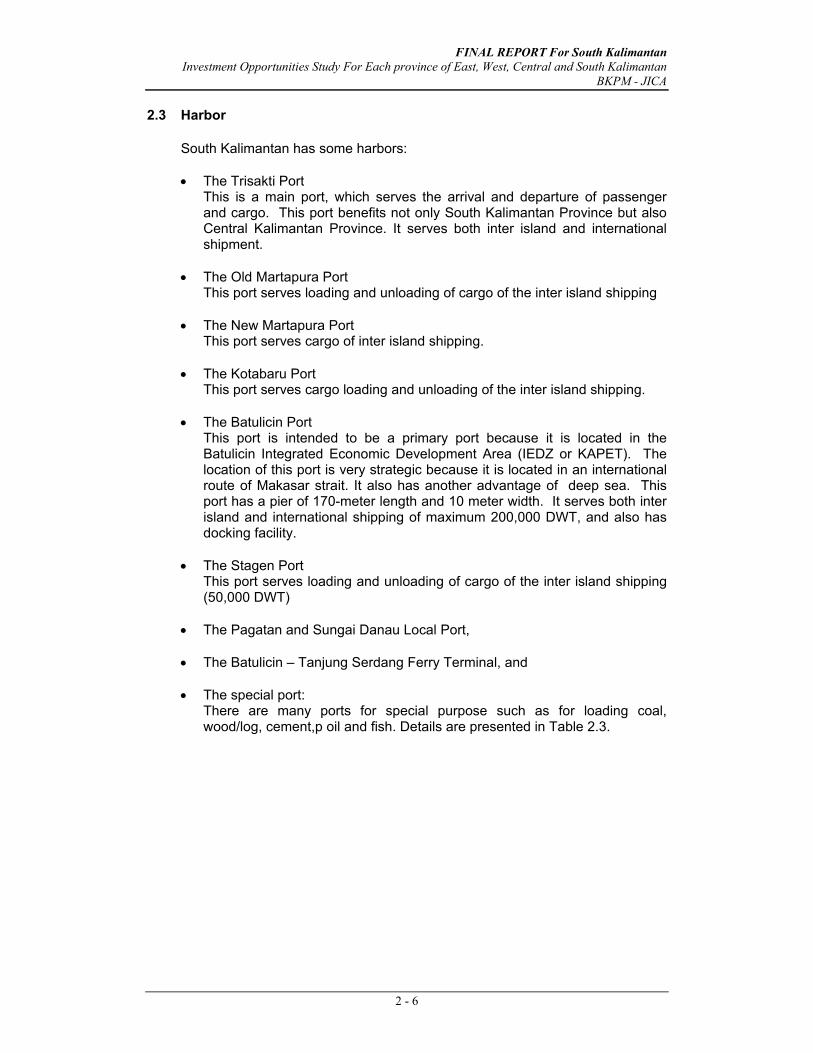

2.3 Harbor

South Kalimantan has some harbors: • The Trisakti Port

This is a main port, which serves the arrival and departure of passenger and cargo. This port benefits not only South Kalimantan Province but also Central Kalimantan Province. It serves both inter island and international shipment.

• The Old Martapura Port This port serves loading and unloading of cargo of the inter island shipping

• The New Martapura Port This port serves cargo of inter island shipping.

• The Kotabaru Port This port serves cargo loading and unloading of the inter island shipping.

• The Batulicin Port This port is intended to be a primary port because it is located in the Batulicin Integrated Economic Development Area (IEDZ or KAPET). The location of this port is very strategic because it is located in an international route of Makasar strait. It also has another advantage of deep sea. This port has a pier of 170-meter length and 10 meter width. It serves both inter island and international shipping of maximum 200,000 DWT, and also has docking facility.

• The Stagen Port This port serves loading and unloading of cargo of the inter island shipping (50,000 DWT)

• The Pagatan and Sungai Danau Local Port, • The Batulicin – Tanjung Serdang Ferry Terminal, and

• The special port:

There are many ports for special purpose such as for loading coal, wood/log, cement,p oil and fish. Details are presented in Table 2.3.

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 7

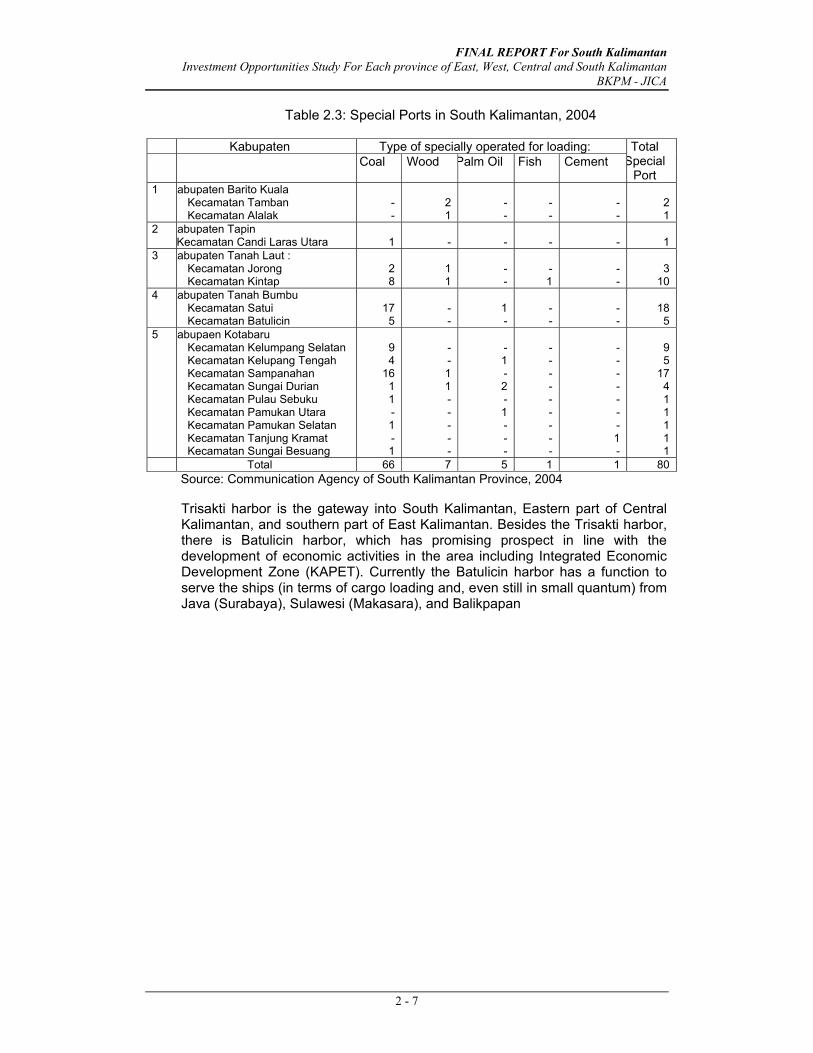

Table 2.3: Special Ports in South Kalimantan, 2004

Kabupaten Type of specially operated for loading:

Coal Wood Palm Oil Fish Cement Total

Special Port

1 Kabupaten Barito Kuala Kecamatan Tamban Kecamatan Alalak

- -

2 1

- -

- -

- -

2 1

2 Kabupaten Tapin Kecamatan Candi Laras Utara

1

-

-

-

-

1

3 Kabupaten Tanah Laut : Kecamatan Jorong Kecamatan Kintap

2 8

1 1

- -

- 1

- -

3

10 4 Kabupaten Tanah Bumbu

Kecamatan Satui Kecamatan Batulicin

17 5

- -

1 -

- -

- -

18 5

5 Kabupaen Kotabaru Kecamatan Kelumpang Selatan Kecamatan Kelupang Tengah Kecamatan Sampanahan Kecamatan Sungai Durian Kecamatan Pulau Sebuku Kecamatan Pamukan Utara Kecamatan Pamukan Selatan Kecamatan Tanjung Kramat Kecamatan Sungai Besuang

9 4

16 1 1 - 1 - 1

- - 1 1 - - - - -

- 1 - 2 - 1 - - -

- - - - - - - - -

- - - - - - - 1 -

9 5

17 4 1 1 1 1 1

Total 66 7 5 1 1 80 Source: Communication Agency of South Kalimantan Province, 2004 Trisakti harbor is the gateway into South Kalimantan, Eastern part of Central Kalimantan, and southern part of East Kalimantan. Besides the Trisakti harbor, there is Batulicin harbor, which has promising prospect in line with the development of economic activities in the area including Integrated Economic Development Zone (KAPET). Currently the Batulicin harbor has a function to serve the ships (in terms of cargo loading and, even still in small quantum) from Java (Surabaya), Sulawesi (Makasara), and Balikpapan

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 8

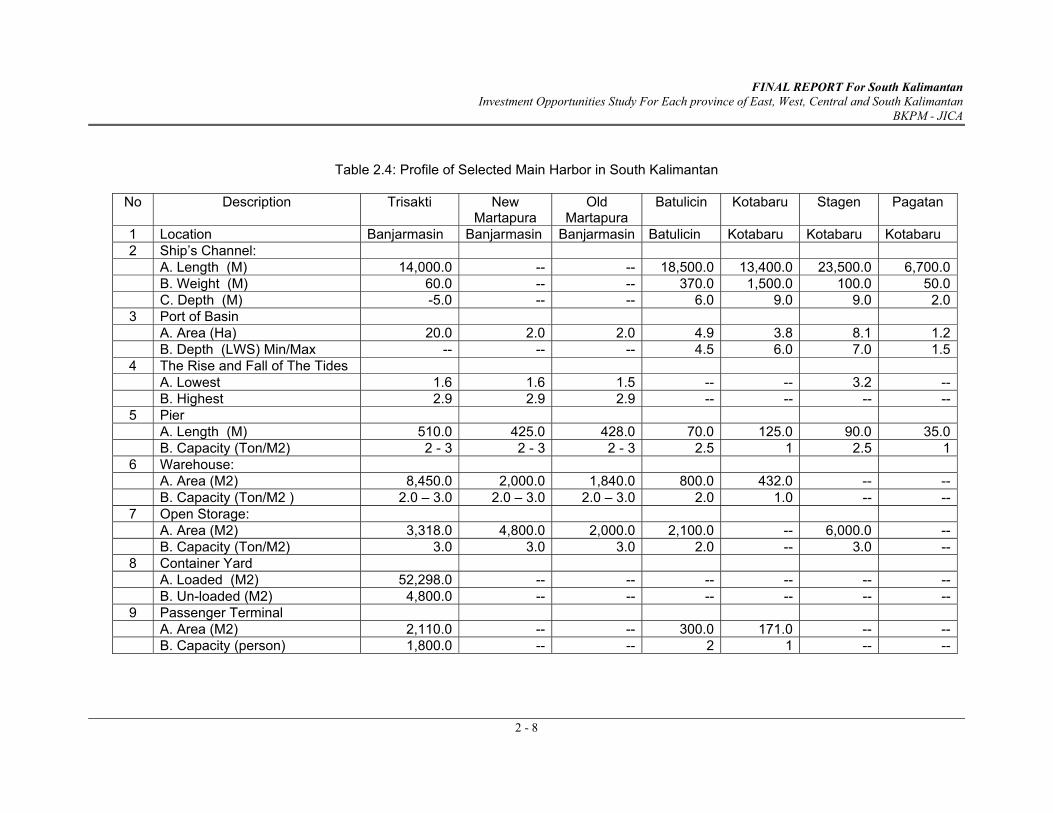

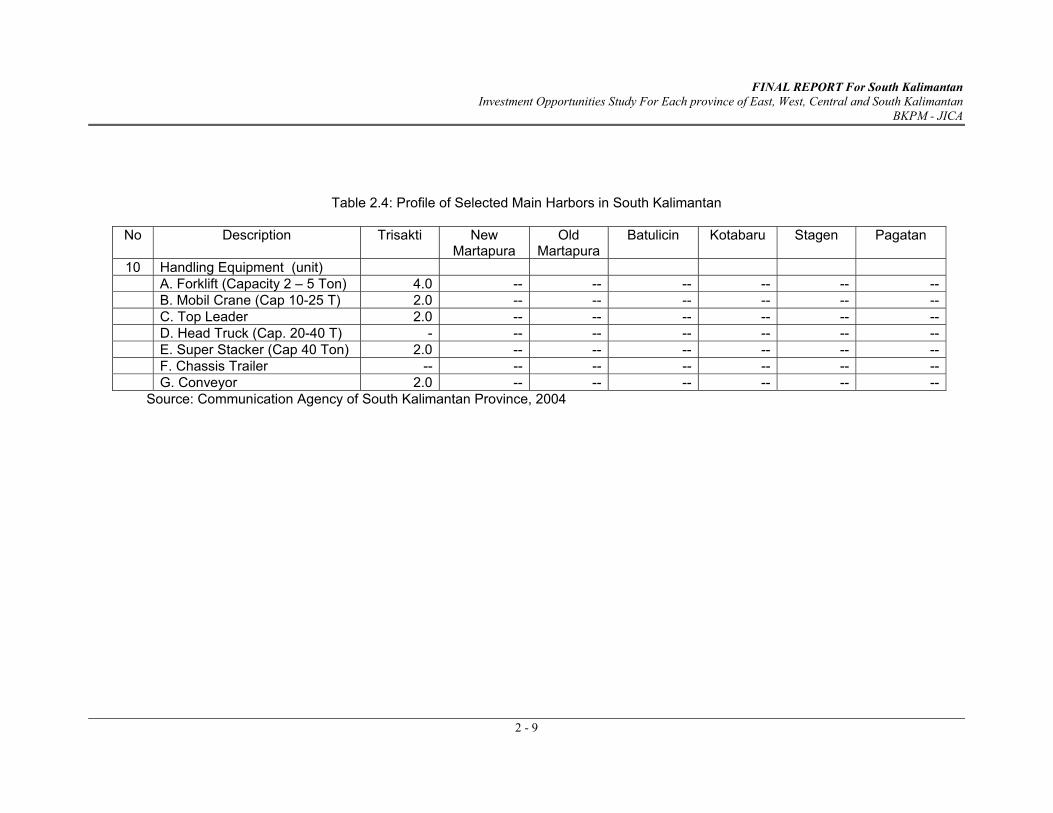

Table 2.4: Profile of Selected Main Harbor in South Kalimantan

No Description Trisakti New

Martapura Old

Martapura Batulicin Kotabaru Stagen Pagatan

1 Location Banjarmasin Banjarmasin Banjarmasin Batulicin Kotabaru Kotabaru Kotabaru 2 Ship’s Channel: A. Length (M) 14,000.0 -- -- 18,500.0 13,400.0 23,500.0 6,700.0 B. Weight (M) 60.0 -- -- 370.0 1,500.0 100.0 50.0 C. Depth (M) -5.0 -- -- 6.0 9.0 9.0 2.0

3 Port of Basin A. Area (Ha) 20.0 2.0 2.0 4.9 3.8 8.1 1.2 B. Depth (LWS) Min/Max -- -- -- 4.5 6.0 7.0 1.5

4 The Rise and Fall of The Tides A. Lowest 1.6 1.6 1.5 -- -- 3.2 -- B. Highest 2.9 2.9 2.9 -- -- -- --

5 Pier A. Length (M) 510.0 425.0 428.0 70.0 125.0 90.0 35.0

B. Capacity (Ton/M2) 2 - 3 2 - 3 2 - 3 2.5 1 2.5 16 Warehouse: A. Area (M2) 8,450.0 2,000.0 1,840.0 800.0 432.0 -- -- B. Capacity (Ton/M2 ) 2.0 – 3.0 2.0 – 3.0 2.0 – 3.0 2.0 1.0 -- --

7 Open Storage: A. Area (M2) 3,318.0 4,800.0 2,000.0 2,100.0 -- 6,000.0 -- B. Capacity (Ton/M2) 3.0 3.0 3.0 2.0 -- 3.0 --

8 Container Yard A. Loaded (M2) 52,298.0 -- -- -- -- -- -- B. Un-loaded (M2) 4,800.0 -- -- -- -- -- --

9 Passenger Terminal A. Area (M2) 2,110.0 -- -- 300.0 171.0 -- -- B. Capacity (person) 1,800.0 -- -- 2 1 -- --

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 9

Table 2.4: Profile of Selected Main Harbors in South Kalimantan

No Description Trisakti New Martapura

Old Martapura

Batulicin Kotabaru Stagen Pagatan

10 Handling Equipment (unit) A. Forklift (Capacity 2 – 5 Ton) 4.0 -- -- -- -- -- -- B. Mobil Crane (Cap 10-25 T) 2.0 -- -- -- -- -- -- C. Top Leader 2.0 -- -- -- -- -- -- D. Head Truck (Cap. 20-40 T) - -- -- -- -- -- -- E. Super Stacker (Cap 40 Ton) 2.0 -- -- -- -- -- -- F. Chassis Trailer -- -- -- -- -- -- -- G. Conveyor 2.0 -- -- -- -- -- --

Source: Communication Agency of South Kalimantan Province, 2004

FINAL REPORT For South Kalimantan Investment Opportunities Study For Each province of East, West, Central and South Kalimantan

BKPM - JICA

2 - 10

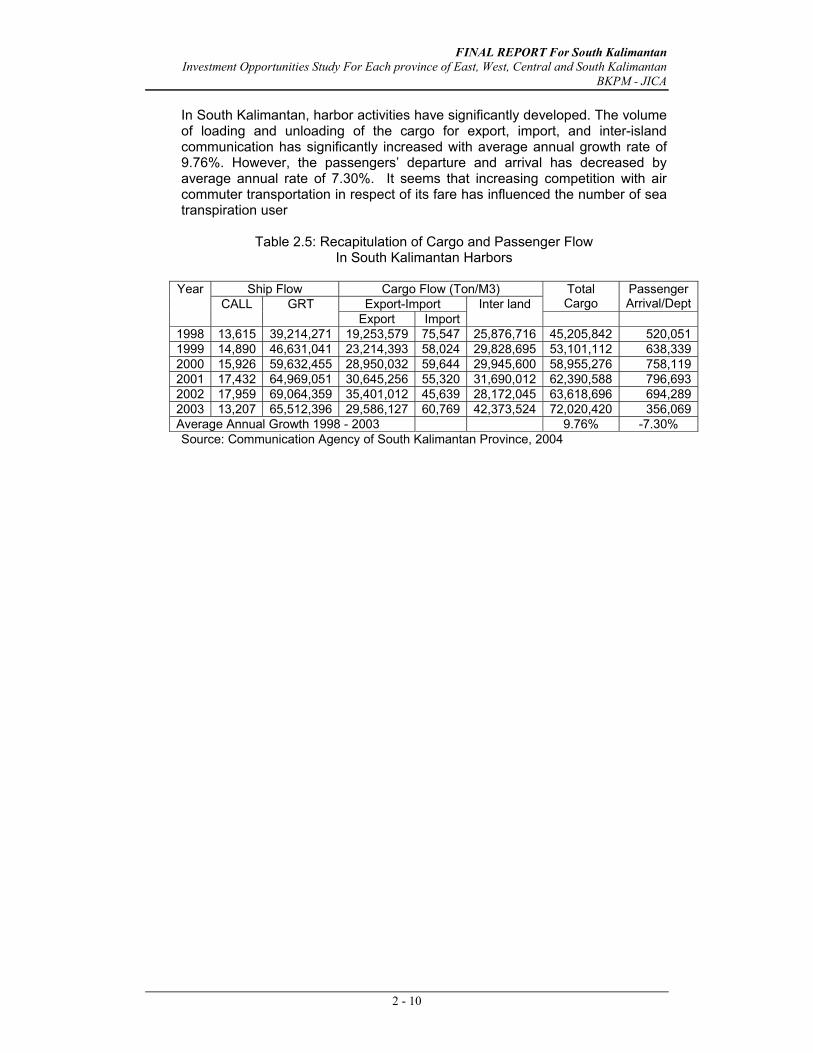

In South Kalimantan, harbor activities have significantly developed. The volume of loading and unloading of the cargo for export, import, and inter-island communication has significantly increased with average annual growth rate of 9.76%. However, the passengers’ departure and arrival has decreased by average annual rate of 7.30%. It seems that increasing competition with air commuter transportation in respect of its fare has influenced the number of sea transpiration user

Table 2.5: Recapitulation of Cargo and Passenger Flow In South Kalimantan Harbors