Embed Size (px)

Citation preview

6

the behaviour of investors as well as the value of investment projects. In previous papers

(McDonald and Siegel, 1986; Cortazar and Schwartz, 1997; Yeo and Qiu, 2003; Kjӕrland, 2007)

it was proved that timing flexibility and optionality add a significant value to the investment

project.

In our study we use the real options framework provided by Dixit and Pindyck (1994).

The real options methodology described in Dixit and Pindyck (1994) has been broadly used in

energy related studies. However, regarding gas storage markets, the real options analysis has

been mainly applied for modelling gas prices, optimizing injection and withdrawal schedules

(Thompson et al., 2003; Boogert and Jong, 2006; Holland, 2007). In our paper we attempt to

contribute to filling the niche of real options applications in gas storage research and, instead of

optimizing the storage schedule, we optimize the investment timing of storage projects. Hence,

the main question of this paper is: what is the optimal timing of investments in gas storage in

partially or totally depleted gas fields under uncertainty? Furthermore, we also aim to determine

how optionality affects the value of the storage project and the impact of various parameters –

such as volatility, investment costs and gas price spread - on investment timing. In order to

answer these questions, we will build a model based on the real options approach and perform a

sensitivity analysis to the results found.

In this paper we try to address these questions by looking at the investment opportunity

through the perspective of a private company which has a right to invest in underground gas

storage. We will analyze two different cases of this investment problem. In the first case the

company can invest in a completely depleted gas field. In the second case the company holds a

right to invest in a partially depleted gas field, which still has a sufficient amount of gas that

could be used as cushion gas in the storage project. Hence in the second case the company has

two options – either to deplete the field first and start storage later on, or to keep the gas in the

field and start storage without buying cushion gas. The goal of the analysis is to derive the

trigger gas prices for investing in each option. Besides determining the trigger gas prices, we will

also obtain the values of the option and the net payoffs of storage projects. Moreover, after

deriving the analytical results of the model, we will estimate the numerical trigger prices and the

values of the options in the numerical case. This numerical case will be applied to the Dutch gas

market.

7

In our study various data sources are used such as Bloomberg, reports and observations

from previous research. However, the access to European gas price data is very restricted. As a

consequence, regarding gas prices, we mainly use historical data on US gas prices.

The remainder of this paper is organized as follows: in chapter 2 we will provide a

literature review about previous research on gas storage and real options applications in energy

related studies. In chapter 3 an overview of the gas market will be given. We will look at the

historical and projected gas market aspects such as gas demand, gas supply, gas production and

gas price. In chapter 4 we will discuss three main types of underground gas storage facilities and

storage costs. The real options methodology will be provided in chapter 5. In chapter 6 we will

apply this methodology on valuing investment opportunities in gas storage. In chapter 7 we will

present a numerical case. We will give conclusions in chapter 8.

8

2. Literature Review

2.1. Previous research on gas storage

The changing patterns in the gas market bring challenges to the whole world, as well as

to separate regions and countries. Due to the depletion of gas fields and rising energy demand,

the need for gas storage is increasing significantly. A lot of attention has been paid to the scarcity

of natural gas resources, changes in gas production and consumption levels. However, there has

been less focus on the essential part of the gas market – seasonal flexibility. There are several

articles and reports analyzing gas storage, seasonal flexibility and its challenges.

The need of seasonal flexibility was already discussed in early papers. Welch et al.

(1971) emphasize the problem of meeting seasonal peak demands of natural gas. The authors

mention five ways to face this problem; one of those is gas storage. However, due to the very

limited gas storage capacity, other measures were analyzed in the paper. In another work Caton

(1982) also points out the importance of gas supply and storage planning. In a recent paper of

CIEP (2006) the role of seasonal gas storage is identified as the crucial tool for offsetting the

increasing European demand for seasonal gas flexibility.

There are a few papers focusing on gas demand and its factors. In one of them Levary

and Dean (1980) construct a model which provides the optimal amount of stored natural gas

every year. In the paper it is concluded, that in order to get a good estimate of gas demand,

weather forecasts have to be updated and future gas storage demand recalculated after every

period. The authors derive the optimal strategy for purchasing seasonal gas which precisely

covers the swing supply. In the paper it is also proved that planned seasonal gas storage brings

economic efficiency as the gas price for consumers (compared to the price with gas shortage) is

reduced. Furthermore, Lyness (1984) stresses the impact of seasonal changes in temperature on

demand. He summarizes the paper stating that mathematical methods used for forecasting gas

demand are only useful in the short term, whereas in the long term they become unreliable due to

high uncertainty about the environment. It is also concluded that interaction between forecasting

gas demand and planning gas storage is increasing significantly in the long term.

Concerning future expectations of gas storage capacities, Höffler and Kübler (2007)

estimate that, besides existing forecasted stored gas capacity, there will be additional demand of

9

storage between 10 (without strategic storage) and 29 billion m3 (with strategic storage of

imported gas from non-European countries) until 2030 in North-Western Europe. In another

article, Joode and Özdemir (2010) expand the Höffler and Kübler (2007) analysis by

incorporating other sources of seasonal flexibility provisions such as imports via pipeline, LNG

imports and gas production. They build a dynamic gas market model (GASTALE) and use it for

estimating demand for gas storage in North-Western countries2 until 2030. The authors

determine that additional storage capacity demand will be between 13 billion m3 (in the low gas

demand scenario) and 20 billion m3 (in the reference gas demand scenario) in targeted countries

until 2030.

The most typical gas storage facilities are salt caverns, aquifers, or depleted gas fields. In

CIEP (2006) depleted gas fields are mentioned as the preferred seasonal storage facility.

Furthermore, in EBN report (2010) it is presented that small Dutch gas fields are expected to be

depleted in 20-30 years. Together with additional available storage facilities, this implies that

there will be a great potential for converting depleted gas fields into storage reservoirs.

2.2. Main obstacles for investment in seasonal storage

Despite gas storage necessity, increasing demand and availability of storage facilities,

investors are reluctant to invest in gas storage projects. Several papers (CIEP, 2006; Höffler and

Kübler, 2007) indicate that market liberalization has led to higher investment risks due to

increased uncertainties over market share and future regulatory regime. Furthermore, in CIEP

(2006) it is emphasized that long project building time and gas spot market volatility increase the

uncertainty over future revenues. Besides, in this paper it is also pointed out that future demand

of gas storage is not certain either. In a number of papers (Caton, 1984; CIEP, 2006; Codognet

and Glachant, 2006; Höffler and Kübler, 2007) it is stressed that storage projects require very

high investment costs. Since large storage volumes are needed for balancing seasonal

fluctuations, it means that gas storage facilities have to be sufficiently big, which implies high

sunk costs. An important obstacle for investment in gas storage is also the necessity of transport

2 J.de Joode and Ö. Özdemir use the concept of Northwestern countries for Belgium, Denmark, France,

Germany, Luxembourg, Ireland, The Netherlands, UK, while Höffler and Kübler add Switzerland, but do not include Luxembourg and Ireland.

10

capacity (CIEP, 2006). Höffler and Kübler (2007) state that competition-favorable conditions for

integrating storage and transport systems are needed, as well as unbundling of storage providers

from transport providers.

In Codognet and Glachant (2006) it is stated that at around 50-80 percent of total sunk

costs comprises of expenses used for buying cushion gas which is required for maintaining the

pressure in the field. Consequently, high volatility of gas prices and long development time

increase the uncertainty over investments costs. Moreover, in the same article the uncertainty

over future revenues from gas storage projects (which depend on the summer-winter gas price

spread) is stressed.

The common conclusion in these papers is that the uncertainties related to storage market

regulation, demand and gas price make investors reluctant to invest in very costly storage

projects. Hence, under-investment in gas storage occurs.

2.3. Real options applications in energy related studies

The essential real options theory is provided by Dixit and Pindyck (1994). The real

options framework from their book is often used in scientific articles in various fields, including

the energy area. Real option valuation takes into account the irreversibility of investment,

uncertainties in cash flows and timing flexibility (Dixit and Pindyck, 1994).

One of the earliest articles that study the importance of investment timing is written by

McDonald and Siegel (1986). They derive the optimal investment rule and the formula for

estimating the value of an investment option. McDonald and Siegel (1986) prove that optionality

adds value to the investment project. According to them, it is optimal to wait and invest when

benefits are twice higher than the investment costs.

Also the importance of investment timing flexibility is stressed in several articles

(Cortazar and Schwartz, 1997; Yeo and Qiu, 2003; Kjӕrland, 2007). Kjӕrland (2007) uses the

real options framework provided by Dixit and Pindyck (1994) to evaluate investment

opportunities in hydropower in Norway. The author also determines the trigger price for starting

investment. Moreover, in the article Kjӕrland (2007) summarizes that the results of his analysis

are supported by real investment behaviour in the Norwegian hydropower industry. Hence, the

usage of real options valuation proves to be more reliable than previous methods.

11

In recent articles the real options approach has also been used to evaluate investments in

renewable energy and R&D projects (Martínez-Ceseña and Mutale, 2011; Siddiqui and Fleten,

2010; Lee and Shih, 2010; Siddiqui et al., 2007). Siddiqui and Fleten (2010) apply the real

options methodology for valuing and comparing two alternative energy projects. The authors

stochastically define two uncertainties - electricity price and operating cost. In another paper Fan

and Zhu (2010) expand the analysis and develop a model based on real options for valuing

overseas oil-resource investment decisions under oil price, exchange rate and investment

environment uncertainties3. In the paper they determine the option value index (OVI) which can

be used for comparison of oil-investment conditions in different countries.

However, real options applications in gas storage market are still limited. In the previous

papers attention was mostly paid to modeling gas prices stochastically (including mean-reversion

process), optimizing injection and withdrawal schedules using Monte-Carlo simulations

(Thompson et al., 2003; Boogert and Jong, 2006; Holland, 2007). In addition, the storage

schedule valuation is expanded in Felix et al. (2009), where the authors apply real options

analysis for valuing gas storage while taking limited gas market liquidity into account. They

determine that illiquidity decreases gas storage value as well as injection and withdrawal

amounts.

Real options connect the theory with uncertain market and business environments as well

as managerial flexibility. Hence, real options analysis has been acknowledged as a useful tool for

making decisions in investment behaviour, optimal production and other actions. It is expected

that, despite their complexity, real options applications will increase significantly.

3 The authors measure the investment environment parameter using the World Bank “Ease of Doing Business Index”.

12

3. Gas Market Overview

The recognition of the need for seasonal flexibility was already discussed in chapter 2.

However, the knowledge of gas market and its historical and projected trends are very important

for realizing the necessity of seasonal gas storage. In this chapter we will look at the actual

situation in the gas market and present the natural gas demand, gas production, trade and storage.

Furthermore, we will also take a look at the gas price’s trends and its characteristics, as the gas

price is a very important gas market feature which also affects the investments in gas storage.

3.1. Natural Gas Demand

The importance of natural gas supply is increasing significantly as natural gas share in

meeting world energy demand is rising every year. According to the World Energy Outlook

2010 (WEO) projections, world gas demand is going to increase drastically across all three

different scenarios4, at least for the projection period (until 2035).

Figure 1. World primary natural gas demand by scenarios (Source: WEO 2010)

4 There are three different scenarios in the World Energy Outlook 2010: The New Policies Scenario (It is

newly presented in WEO 2010. The main feature of this scenario is that policy commitments and plans that were announced by the governments are taken into account); The Current Policies Scenario (In this scenario it is assumed that no actions are taken since 2010 and there is no change in policies); The 450

Scenario (This is climate change mitigation scenario in which 2°C of global warming and 450 ppm concentration of CO2-eq are taken as one of the main goals).

13

In figure 1 different natural gas demand growth scenarios are presented. It is shown that

demand grows fastest under the Current Policies Scenario with a 55 percent increase from 2008

until 2035. In case of the New Policies Scenario, when announced policies, actions and

commitments are taken into account, slightly smaller gas demand growth is determined (44

percent during 2008-2035). The smallest - 15 percent - demand growth until 2035 is predicted

under the 450 Scenario. Moreover, according to the 450 Scenario there is also a small drop in gas

demand after 2025 which occurs due to the implementation of renewable energy policies and

increase in usage of nuclear power (World Energy Outlook 2010).

According to IEA data presented in the WEO 2010, the annual primary natural gas

demand growth in OECD countries under the New Policies Scenario is estimated to be 0.5

percent, whereas in non-OECD countries growth in demand is significantly higher and accounts

for 2 percent annually. Increase in demand is slower in OECD countries due to smaller

(compared to non-OECD countries) economic growth and higher energy use efficiency (WEO

2010). Furthermore, the annual gas demand increase is projected to be 0.4 percent in the EU. For

comparison it should be mentioned that natural gas demand growth in the whole world is 1.4

percent annually.

Regarding sector trends, more than a third of natural gas (39 percent in 2008) is used in

the power sector. This share is expected to reach 41 percent in 2035. Moreover, almost half of

the natural gas demand increase during 2008-2035 is caused by the power sector. Other

important sectors using a significant share of gas are the building and industry sectors (WEO

2010).

To sum it up, the world demand for natural gas is expected to increase by 15-55 percent

in upcoming 25 years. In order to see how this growing demand could be met, we will analyze

other important aspects of the gas market such as gas production, imports and exports, gas

storage. It will be presented in the next section.

3.2. Natural gas production, trade and storage

There is still a large amount of natural gas resources in the world, which would be

sufficient enough for satisfying the increasing future demand (CIEP, 2006). However, most of

the largest natural gas resources are located in regions where demand is not the highest. This

14

implies the need for gas transportation and supply to other regions. Moreover, in natural gas

markets, uncertainties over resource exploration and development remain, bringing insecurities

for the future (WEO 2010). It is also very important to stress that only at around 10 percent of

world gas resources are found in OECD countries. According to the IEA projections under the

New Policies Scenario, natural gas production in the whole world will increase by 1.3 percent

annually during the 2008-2035 period, while in the European Union it will decrease by 3.1

percent annually. This fall in production is influenced by depletion of gas fields in the North Sea

region. In addition, the largest increase in gas production is projected in non-OECD countries

(1.9 percent annually during 2008-2035).

Currently 25 percent of primary natural gas demand is imported by OECD countries and

almost half of Europe’s primary gas demand is met by imports. According to the WEO (2010),

Europe’s dependency on gas supply from outside the region will increase drastically by more

than 20 percent and will be equal to 67 percent in 2035 (under the New Policies Scenario).

Taking European Union countries separately, this dependency becomes even worse – from 60

percent in 2008 to 84 percent in 2035.

Figure 2. Swing Supply in North-Western countries 1995-2004.

(Source: F.Höffler and M. Kübler, 2007)

Having in mind Europe’s reliance on natural gas imports from other regions, it is

important to analyze how seasonal fluctuations in gas demand are covered. Figure 2 represents

historical data on how seasonal gas imbalances were met during 1995-2004 in North-Western

15

countries. Three different ways of covering demand are shown: production, imports and storage.

At the beginning of the period gas production was the main source for gas swing supply (52

percent). However, it started to decrease gradually and in 2004 it covered only 39 percent of

swing demand. It can be observed that the gas storage share in mitigating the imbalances had

increased from approximately 30 percent in 1995 to 40 percent in 2004.

It is clear that declining production in North-Western Countries and their growing

dependency on suppliers from outside the region lead to necessity of sufficient gas storage

capacity for securing gas supply. Moreover, the large supply routes bring even more insecurity

due to long transportation distance, transportation costs, extended delivery time and political and

regulatory issues. The recent conflict between Russia and Ukraine in 2006 has increased the

awareness of gas storage importance. During this incident Russia stopped exporting gas through

Ukraine, thus affecting a number of countries that were dependent on those gas imports.

Furthermore, seasonal gas storage not only secures the gas supply, but also helps to avoid

high fluctuations in gas prices. In case of spot priced markets, shortages in gas supply would lead

to very high and volatile gas prices. On the other hand, if gas prices are set according to

indexation to oil prices, supply shortage would result in cutting down gas supplies to some of the

consumers (CIEP, 2006). Thus the lack of storage capacity could bring damages to industrial and

residential gas consumers as well as to the countries’ economy, thereby affecting the whole

society.

Figure 3. Planned or being constructed storage capacities in Europe.

(Source: Natural Gas Market Review 2009)

16

Gas storage has already been acknowledged as a crucial and essential part of the gas

value chain (CIEP, 2006; Höffler and Kübler, 2007; Natural Gas Market Review 2009).

Furthermore, it was estimated that until 2030 the gap in gas capacity and demand will be

between 10 to 30 billion cubic meters in North-western Countries (Höffler and Kübler, 2007).

As stated before, the main reasons for under-investment in gas storage are related to uncertainties

regarding the regulatory regime and the demand context. This problem is also presented in figure

3. It can be seen that there are plenty of storage projects planned, however due to uncertainties it

is not definite yet when they will be implemented.

Regarding the recent gas storage situation, it should be mentioned that in 2009 there was

82 billion cubic meters of installed operating working storage capacity in Europe. More than 65

percent of stored gas was placed in depleted gas or oil fields, 20 percent in salt aquifers and 12

percent in salt caverns.

Having in mind the growing geographical difference between gas production and demand

locations, the required gas storage capacity in Europe is expected to increase significantly. In the

following section we will analyze the gas market of the Netherlands which have a considerable

position in Europe’s gas market. However, it appears that for remaining this position in the

future, more storage capacity is required.

3.3. The gas market in the Netherlands

After the discovery of the Groningen gas field in the early 1960s, the Netherlands became

a gas producing country and started to play a very important role in the international gas market.

The Netherlands has been using the “small fields’ policy” which was introduced in order to

increase production from small fields as well as to encourage development and exploration of it,

leaving the large Groningen field mainly for provision of swing supply. Even with the “small

fields’ policy” the Netherlands has maintained an important position as a large producer and

exporter in Europe. It should be noted that more than a third of total European Union gas

production was produced in the Netherlands in 2007 (Foreest, 2010). In addition, 54 percent of

primary gas production in the Netherlands in 2008, which in total accounted for 85.7 billion

cubic meters, was from the Groningen field, the rest came from small fields (Natural Gas Market

Review 2009).

17

According to CBS data, in 2009 total natural gas consumption in the Netherlands was

46.3 billion cubic meters. The energy consumption by final consumers (except power plants) has

recently slightly decreased due to increasing energy efficiency. It is also expected that this

decline could have been influenced by the current financial crisis. However, natural gas demand

in the power generation sector is increasing. In 2009 electricity power plants used 9 billion cubic

meters of natural gas, which accounts for 20 percent of total gas consumption in the Netherlands

(CBS Statline).

Gas exports from the Netherlands are increasing gradually every year. In 2009 the

Netherlands’ natural gas exports were 52.7 billion cubic meters. On the other hand, gas imports

to the Netherlands have also increased significantly from 1999. In 2009 imports were equal to a

bit more than a half of natural gas exports (CBS statline). Large gas exports from the

Netherlands are essential for meeting seasonal gas demand swings in North-Western countries.

Figure 4. Natural gas historic production and forecasts in the Netherlands.

(Source: EBN, 2010)

The Netherlands can be seen as a “matured gas country” as many fields have already

been discovered and explored. It is shown in figure 4 that gas production starts declining in the

following years, especially from small fields. This implies that the Netherlands will change from

a gas exporting country into a net gas importer. However, depleted gas fields provide the country

18

with great gas storage potential. In addition, there are also considerations for turning the

Netherlands into the gas transportation hub for North-Western countries (the so called “The

Dutch gas roundabout”).

Consequently, The Netherlands have to increase the usage of underground gas storage in

order to maintain the position of covering seasonal swing gas demand in North-Western

countries. According to Gasunie (2007), in 2007 the Netherlands had 5 billion cubic meters of

stored gas, which was 11 percent of all consumed gas in the country. In North-Western Europe

stored gas volume was estimated to be 14 percent of total consumption. Taking into account

decreasing gas production, rising demand and increasing dependency on imports, it is clear that

for securing gas supply a significantly higher amount of storing capacity is required.

3.4. The gas price

The gas price is very important as it influences many economic sectors and activities. On

the other hand, the gas price is sensitive to other factors itself. Basically, the main gas price

drivers are gas demand and oil prices due to the remaining tight gas and oil price linkage (WEO

2009). Historically gas prices have been constantly increasing (figure 5), with a significant

increase from 2000. The recent economic recession had an impact on gas demand which led to a

drop in gas prices in 2009. According to gas price projections by IEA (2009), the gas price is

expected to rise modestly after 2010.5 The slower increase in the future gas price is influenced by

LNG imports (gas-to-gas competition), improvements in technology, lower exploration costs and

new developments which provide additional supply (WEO 2009).

The gas price plays an essential role in making gas storage investment decisions as it

influences the costs for buying cushion gas. Moreover, gas price volatility brings high

uncertainty over costs and future cash flows. Using the Henry Hub Spot index on US data6, it

was calculated that historical annual gas price volatility was approximately 74 percent (excluding

the highest price peaks) during 1991-2010. Due to high volatility investors prefer to postpone

their investments.

5 According to the newest Eurostat data, the gas price for industrial consumers in EU-27 has already increased by 10 percent from the first half of 2009 to the second half of 2010. 6In this paper mainly US data on gas prices is used, as access to European gas price data is very limited.

19

Figure 5. Historical gas prices. (Based on HHUB index (1991-2010))

Regarding gas storage value, the main revenues can be estimated as a difference between

gas prices in summer and winter seasons.7 Besides, usually gas storage sales are based on future

contracts. Using EIA data on monthly natural gas futures contracts, this paper determined that

between 1994-2010 the average seasonal gas price spread was 0.45 $/MMbtu which equals to

0.015 €/m3.8 Market conditions, storage supply and demand and variations in prices of gas

futures contracts have a significant influence on seasonal gas price spread.

The gas price and seasonal gas price spread play are essential for making decisions about

the investments in gas storage projects. The gas price directly affects the investment costs as

buying cushion gas is one of the main expenditures. Furthermore, the profit from gas storage

project comes in the form of a seasonal gas price spread. Later, in chapter 6, we will provide a

stochastical gas price expression and evaluate investment timing in respect to the gas price. In

the next chapter we will explain the characteristics of underground gas storage reservoirs - such

as cushion gas and working gas –, and provide the functions of different types of storage

facilities.

7 Traditionally seasonal gas storage combines seven months of gas injection (from April until October) and five months of withdrawal period (from November until March, which are peak-heating winter months). Other storage facilities with more than one gas storage cycle per year have different injection and withdrawal periods. In this paper one storage cycle per year is assumed. 8 For conversion it is taken that 1 MMBtu (million Btu) is equal to 27.7536 cubic meters; $/€=0.6944 (31

May 2011).

0

2

4

6

8

10

12

14

16

18

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

gas

pri

ce, d

ol/

MM

btu

20

4. Underground gas storage

Since it is clear that the need for seasonal flexibility is increasing, now it is important to

analyze the types of the main underground gas storage facilities and its characteristics. As every

underground gas storage reservoir has different geological and engineering conditions, their

suitability for storage and usage differ (FERC, 2004). In the following section, the main

measures and purposes of an underground gas storage reservoir are provided. We already

mentioned cushion gas and other gas field’s features in the previous chapters; here we will give

the explanations of it. Next, we will discuss the differences in three main types of underground

gas storage reservoirs and storage costs.

4.1. The main characteristics and functions of an underground gas storage facility

There are several measures that describe an underground gas storage reservoir. The

maximum amount of natural gas that can be placed in an underground gas storage facility is

called the total storage capacity. Total stored gas comprises base (cushion) gas and working gas.

Cushion gas is the volume of gas that is used as a permanent inventory in a storage facility. The

purpose of cushion gas is to maintain the pressure and deliverability rate in the facility. The

amount of gas in the reservoir that is above the level of cushion gas is called working gas. In the

storage project working gas is injected and withdrawn. This is the gas that is being operated.

The measure of deliverability presents the amount of gas that can be withdrawn

(delivered) from a storage site during one day. Contrary, the injection rate indicates the amount

of gas that can be injected in a storage facility within one day. Deliverability and injection rates

depend directly on the amount of total gas in the facility as it influences the pressure. When the

amount of stored gas in the site is increasing, the deliverability rate enhances, whereas injection

rate decreases.

All of the measures mentioned above are not fixed. Injection and withdrawal rates change

with the amount of gas in the storage facility. Besides, the volume of cushion gas, working gas

and total storage capacity can be influenced by changes in equipment and operational

parameters.

21

There are two main functions of an underground gas storage facility - it can be used for

covering either peak-day or seasonal gas demand swings. The storage facilities that provide with

peak-day supply need to have high deliverability rates. They are used when the difference in

daily demand is large or the gas price is very high. In case of seasonal storage, gas is typically

injected during the summer period and withdrawn in winter. Thus seasonal storage provides a

stable supply of gas during the winter period. High gas demand in winter is mainly the

consequence of heating during the cold season.

4.2. Three types of underground gas storage facilities

There are three main types of underground gas storage facilities: salt caverns, aquifers

and depleted gas/oil fields. Gas storage reservoirs differ in their geological characteristics which

lead to different usage purposes and development costs.

Salt caverns are created by performing a solution mining procedure - fresh water is

pumped into the salt dome and salt water is drained from it. The fact that this type of facility is

man-made, enables investors to determine the capacity of the reservoir which is bounded by the

size of the salt dome and other geological conditions. In comparison to other underground

storage facility types, a salt cavern has very high development costs per m3 of working gas. On

the other hand, the storage capacity of salt caverns is significantly smaller than other reservoirs,

thus development costs of a single cavern are much lower compared to the investment in a

depleted gas field or an aquifer. In addition, only 20-30 percent of total storage capacity in a salt

cavern is cushion gas, and the rest is working gas volume. Moreover, as salt caverns are

relatively small and have significantly high deliverability and injection rates, working gas can be

recycled (filled and emptied) even 10-12 times per year (FERC, 2004). Due to these

characteristics, salt caverns are mostly used for short peak-day demands.

Another storage type is an aquifer. This is an underground formation of water-bearing

permeable rocks that is suitable for storage. Aquifers have high development costs. Besides, the

required amount of cushion gas in this type of facility varies from 60 to 80 percent of total gas

capacity (FERC, 2004). However, aquifers achieve high deliverability rates and working gas can

be cycled once or more per year. High geological risks and large expenditures result in low use

of aquifers as underground storage facilities.

22

The most common underground gas storage reservoir is a depleted gas or oil field. A

depleted field that was used for gas or oil production can be used for underground gas storage.

Converting a depleted field into a gas storage facility bears a few important advantages. Firstly,

the characteristics of the field that was used before are well known. Moreover, since the reservoir

held original gas before, it proves that the facility is secure for storing the gas. In addition,

previous usage usually implies that there is an existing pipeline infrastructure nearby (IEA).

However, depleted gas fields have high development costs for converting them into storage

reservoirs. Furthermore, 50-60 percent of cushion gas is required for maintaining the pressure. In

comparison to salt caverns, depleted gas fields’ deliverability rates are lower: working gas can be

cycled usually once per year. Even though this storage facility is typically used for seasonal gas

storage, some of it can also be used for peak-day demands.

In this paper depleted gas fields are taken as an underground gas storage facility. These

reservoirs usually have a sufficient size and required deliverability characteristics for seasonal

gas storage. Furthermore, the availability of this type of facilities is increasing due to gas field

depletion.

4.3. Storage costs

Development costs of an underground gas storage facility vary a lot as these are

influenced by the type of storage facility and its performance characteristics. In addition, as gas

storage projects tend to have a very long lead time - from 5 to 10 years (Codognet and Glachant,

2006) – the costs of capital also become significant. However, for simplicity reasons the time to

build a storage facility is not taken into account in this paper. The main focus is on development

costs and tariffs.

One of the biggest elements of development costs is the expenditure on cushion gas. It

was already mentioned before that more than half of stored gas capacity has to be used as

cushion gas. In addition, not all cushion gas can be extracted at the end of the storage project life,

which implies investors’ losses. Furthermore, during the storage project life operational costs are

borne. These costs are related to activities such as gas injection and withdrawal and performance

of compressor facilities.

23

However, very little information is available regarding actual gas storage costs. Table 1

presents the investment costs in an underground gas storage facility provided by ENECO in

2000. The investment costs in Europe and USA differ significantly. This may be the result of

differences in geological and technical characteristics.

Table 1. Investment costs in developing underground gas storage facility

(capacity 100 million cubic meters) in 2000. (Source: UNECE)

Type of UGS

facility

Investment costs per working

gas volume, €/ m3

Europe USA

Aquifer 0.24-0.42 0.10

Depleted field 0.24-0.42 0.09

Salt cavern 0.49-0.70 0.21

In another source, CIEP (2006), it is given that typical storage costs (tariffs) vary from

0.05 to 0.15 €/m3 of stored gas volume. Furthermore, in the paper the required investment in

developing storage reservoirs is estimated. In respect of the given volume of working gas in each

type of the reservoir, investment costs in a depleted gas field is determined to be 0.28 €/m3, in an

aquifer – 0.32 €/m3 and in a salt cavern – 0.80 €/m3. If typical working gas capacity of a depleted

gas field is 2,500 million m3, then the required investment costs are €700 million. Whereas for a

salt cavern, which has much lower working gas capacity – typically 50 million m3 –, investment

costs are €40 million. In addition, investment in a storage facility also implies that expenditures

for building a pipeline infrastructure are needed. Transport costs depend on the transportation

distance, transport capacity and the existence of pipeline infrastructure. Typically, transport costs

per 100 km differ between 0.002-0.008 €/m3/year (CIEP, 2006).

Storage costs play an important role as they have an impact on making investment

decisions. However, as it was shown above, storage costs differ significantly and are not certain.

This brings more uncertainty over gas storage projects and worsens the problem of under-

investment.

24

5. Real Options Methodology

After discussing the practical issues of underground gas storage facilities and analyzing

the actual market conditions of investments in gas storage, we turn to the analytical part of this

paper. In this chapter we will present the real options methodology - mathematical background,

valuation method and its advantages.

We have chosen this method for valuing investments opportunities in gas storage for

several reasons. Firstly, traditional investment valuation methods which use discounted cash

flow analysis - such as NPV - are incomplete as they fail to incorporate managerial flexibility

and innovations into the analysis (Yeo and Qiu, 2003). In real life investments are made in

volatile markets with high uncertainties, thus static valuations tend to misevaluate the

investments. In contrast to NPV, real options acknowledge the actual possibilities that investors

hold – to choose to postpone investment until new information arrives or the conditions become

more favourable, or to abandon the project in case of negative changes in the investment related

environment (IBM, 2002). This means that real options analysis includes timing flexibility which

adds value to the investment project as well as affects the investment decision making process.

Moreover, not only the possibility to delay the investment but also the irreversibility of the

investment is taken into account in real options analysis.

The theory of real options is an extension of financial options. A financial call option

provides the owner with the right – but not the obligation – to buy a security at a particular pre-

determined exercise price on a specific maturity date . Likewise, a real option can be defined

as the investors’ right – without the obligation – to invest in real (tangible) assets (Martínez-

Ceseña and Mutale, 2011). Investors acquire the assets by paying an exercise price, which in

case of real options is the capital costs required for developing the investment project. The value

of both – financial and real – options can be influenced by various factors such as expiration

times, assets or stocks’ value, volatilities and risk-free rates. However, financial and real options

also have important dissimilarities, for instance different length of expiration and tradability

(Yeo and Qiu, 2003).

In real option analysis, uncertainties (for example in gas prices and costs) can be

modelled stochastically. This is essential for determining the value of the investment project.

Stochastic processes and valuation method used in this paper are presented in the next section.

25

5.1. Real options framework

In this paper the real options framework from Dixit and Pindyck (1994) is used. The

authors also provide with mathematical background that is necessary for performing real options

valuation. The basics of it are presented in this section.

5.1.1. Stochastic processes

A variable which evolves through time with some sort of randomness is called a

stochastic process. The stochastic processes can be continuous-time (in the sense that variables

change continuously over time) and discrete-time (when variables can vary only at discrete

moments in time). In this paper continuous-time processes are used.

A Wiener process, which also can be named as a Brownian motion, is a continuous-time

stochastic process. A Wiener process holds three essential features:

It is a Markov process, which implies that the probability distribution for future

values is only dependent on the current state of the value. Past values are

irrelevant for forecasting the future changes of the process.

Its increments are independent, which means that changes in the process in the

next time interval do not depend on the previous changes.

Changes in the process are normally distributed.

Mathematically a Wiener process is expressed as follows:

, (5.1)

where is the increment of a Wiener process; is a random variable with normal distribution,

zero mean and standard deviation of one; is an infinitesimally small time period.

A Wiener process can be used for building more complex processes. One of its

generalizations is the geometric Brownian motion (GBM) with drift. Geometric Brownian

motion takes into account proportional changes in variable and can be described

mathematically as

, (5.2)

where is the change in over an infinitesimally small interval of time, is the drift

parameter, is the variance parameter, is the increment of a Wiener process.

26

Geometric Brownian motion has both properties – a drift rate and a “noise” term

(expressed by a standard Weiner process). The drift rate can also be named as a growth rate as it

shows the trend of the variable. Geometric Brownian motion is often used for modelling

economic and financial variables such as stock prices, energy prices and interest rates (Dixit and

Pindyck, 1994).

5.1.2. Ito’s Lemma

The stochastic processes presented above are continuous in time, however, not

differentiable. In order to determine the differentials of the functions of geometric Brownian

motion, Ito’s lemma is used.

Ito’s Lemma can be seen as a Taylor series expansion. To begin with, assume that

follows the geometric Brownian motion (described in equation (5.2)) and the function

can be once differentiable in and more than twice in . The total differential of is

expressed as:

. (5.3)

However, in ordinary calculus higher-order terms in equation (5.3) disappear. It can be

shown by expanding the third term from the equation:

. (5.4)

Note that . Thus the expression of now becomes:

. (5.5)

The first and second terms from equation (5.5) can be eliminated because terms

and approaches zero value faster than when it becomes infinitesimally small. The

term becomes:

. (5.6)

27

Regarding the fourth term in equation (5.3), all terms in the expression of will

be raised to the power higher than 1 and as a result vanish faster than . The same counts for all

other higher order terms, for instance . Fence, all higher order terms in equation (5.3) can

be eliminated. Thus Ito’s Lemma is expressed as

. (5.7)

Ito’s Lemma will be used in the next chapter for valuing the options to investment in

storage projects. In the next section the valuation method is presented.

5.1.3. Real options valuation method

In this paper the contingent claims method is applied for valuing investment

opportunities. This analysis, which is strongly connected to financial economics, is used to

evaluate an investment project that is characterized by the flows of benefits and costs under

particular uncertainties. In addition, a company’s right to invest in a project that brings flows of

profit can be seen as an asset. Following the important assumption that markets have a sufficient

variety of traded assets, the contingent claims analysis provides the rules for evaluating the

investment opportunity – an asset – which the company holds. The techniques presented in this

section will be applied and illustrated in concrete cases in the following chapters.

To begin with, assume that investors have a right to invest in a project which value

is dependent on the project output price . This variable follows the geometric Brownian

motion9:

, (5.8)

where is the drift parameter, is the variance parameter, is the increment of a Wiener

process.

Suppose that stochastic fluctuations in output price can be spanned by assets in

financial markets. Thus an investor can build a portfolio of traded assets that precisely replicate

the risk and the return of the investment project. 9 An important assumption in contingent claims analysis is that the underlying uncertainties can be mainly modelled by an Ito’s process, which special case is the geometric Brownian motion.

28

In this analysis the investor’s portfolio is constructed by holding a long position in the

project (which is aimed to be valued) and having a short position in units of the project output

. Next, is determined to make the portfolio riskless. Since the portfolio is free from risk, it

also earns the risk-free rate of return. Using these properties, the differential equation is derived

which can be solved by applying boundary conditions. Once the value of the investment

opportunity is known, the optimal investment timing and other conditions can be determined.

Now assume that is the function of and follows the geometric Brownian motion

with the same parameters and :

. (5.9)

Following contingent claims method, the replicating portfolio is built which price is .

This portfolio is perfectly correlated with and its price follows the stochastic process described

as:

, (5.10)

where is the drift rate, is the variance parameter, is the increment of a Wiener process.

The parameters and differ from the ones presented in equation (5.9). As spans the

stochastic fluctuations in , it is the increment of a Wiener process - - that is the same in both

equations (5.9 and 5.10).

Investors will hold this portfolio of assets only if they receive a total expected rate of

return . This is the risk-adjusted expected discount rate of return, which according to the capital

asset pricing model (CAPM) can be described as

, (5.11)

where is the risk-free rate, is the market price of risk, and indicates the correlation

between returns on a particular asset and the market portfolio .

We assume that the return from the portfolio comes only from capital gains as portfolio

does not pay dividend. It follows that, in order make investors willing to hold the portfolio,

return from portfolio has to be equal to . Thus the price of the portfolio can be described as:

. (5.12)

29

It is important to note, that - the growth rate of the value of the project - has to be

smaller than risk-adjusted discount rate . Otherwise the value would be unbounded as

with choosing higher the integral of equation (5.9) could be made indefinitely large. In other

words, this would imply that the growth rate of the value of the project would be expected to be

higher than the discount rate. As a consequence, waiting for longer would always be a better

choice and investment would not be implemented.

Regarding total return from the portfolio, a part of it arises from the expected capital

gain .10 As another part of the return comes in the form of some sort of dividend:

. (5.13)

As by assumption the output of the project is a commodity that can be stored,

characterizes the convenience yield from storage.11 To be more precise, represents the flow of

benefits (such as the capability to keep the production steady and prevent the stock shortage) that

investors get due to holding a commodity. For example, imagine that the company owns

storehouses of wheat. A natural disaster such as a drought occurs and damages large fields of

wheat. These circumstances lead to a shortage of wheat in the market and consequently a

significant increase in its prices. It is clear that the company which is holding the wheat in

storehouses now can get great benefits from it.

The use of contingent claims analysis gives a few more advantages. Firstly, the ability to

span stochastic changes in variables with the existing assets in the market means that there is no

need to take into account investors’ or firms’ risk preferences and discount rates. In this analysis

these are market’s beliefs and preferences that play a role (Smith and McCardle, 1999). Another

advantage of contingent claims valuation is that variables which follow a stochastic process do

not need to be forecasted (Kjӕrland, 2007).

In the following chapter we will analyze and value the options to invest in gas storage

projects. For this purpose we will use the real options methodology and framework which was

provided in this chapter. Furthermore, we will also present the approximations and assumptions

used in our analysis.

10

Parameter is expressed as the growth rate in the geometric Brownian motion. 11 Note that in this paper convenience yield and the risk-free rate of return are assumed to be exogenous parameters.

30

6. Valuing Investment in Gas Storage Project

It was shown in chapter 3 that the gap in seasonal gas storage capacity is increasing.

Furthermore, many gas storage projects have been delayed. In the section where storage costs

were discussed, it was mentioned that the expenditure for buying cushion gas accounts for the

largest share of the investment costs12. In addition, these costs for cushion gas are very uncertain

as they depend on the volatile gas price. An important feature of investments in gas storage

projects is irreversibility as sunk costs cannot be recovered. Besides, timing flexibility plays an

essential role as investors could change their investment decision according to new information

on gas price changes and market conditions.

Real options valuation is suitable for analyzing investment problems that bear the

characteristics mentioned above. A company’s right to invest in a gas storage project can be seen

as a real option, with the possibility to wait and delay the investment. The uncertain gas price can

be modelled as a stochastic variable which follows the geometric Brownian motion.

Furthermore, as the output of the storage project is natural gas, the assumption of tradability in

the markets (discussed in chapter 5) clearly holds.

We use real option analysis in this paper in order to value the investment in gas storage

and to determine the optimal timing of it. We describe this investment problem in two different

cases. Firstly, we assume that the gas field is completely depleted. This implies that, for

converting a gas field into a storage facility, additional costs are borne for buying cushion gas. In

this case we aim to estimate the trigger gas price at which it is optimal to invest in gas

storage and buy cushion gas. Furthermore, in the second case it is assumed that there is still

enough gas left in the field for using it as cushion gas and converting the field into gas storage.

The goal in this case is to determine two types of gas prices:

the price at which it is optimal to deplete the field completely and

afterwards, when the gas price drops to the level , to switch to gas storage;

12

According Codognet and Glachant (2006), the costs for buying cushion gas are estimated to be 50-80 percent of total investment costs.

31

the price at which it is optimal to immediately13 convert the gas field into a

storage facility.

There are several important assumptions made in our analysis. Firstly, the storage project

lasts for an infinitively long period. Besides, there is no leading time in developing the storage

project and there is no depreciation of it. As it was already mentioned, the gas field that could be

used for the storage project is either completely depleted, or contains a particular amount of gas

that would be sufficient for leaving it as cushion gas for the storage project. It is also assumed

that in case of not completely depleted gas field, all gas in place could be extracted and sold.

Furthermore, the characteristics of the gas field’s capacity do not change during the operational

period which means that deliverability and injection rates and working gas capacity remain

constant. Hence, there is a particular known amount of working gas that is stored and extracted

every year. The profit depends on the gas price spread, which is taken as a constant.

Furthermore, operational costs are included in the gas price spreads. In addition, transportation

costs of natural gas are excluded from our analysis. We assume that the existing pipeline

infrastructure can be used and transportation costs account only for a small share of gas storage

costs.

The analysis is based on the contingent claims method. In both cases we will firstly

determine the value of the investment. Secondly, we will determine the value of the option to

invest. The boundary conditions will be used for obtaining the solutions.

6.1. Valuing investment in completely depleted gas fields

6.1.1. The value and costs of the investment project

Now we analyze the case when the investment can be done in a completely depleted gas

field. To begin with, assume the company has a right to invest in a gas storage facility. As the

field is completely empty, this means that besides basic investment , which is needed for

13

Note that in this analysis we use the term “immediate” in the sense that the gas field will not be depleted before converting it into a storage facility. “Immediate storage” does not imply start of gas storage right away after getting the right to invest, but instead indicates that no other actions are taken before storage.

32

procedures such as changing equipment and installations, an additional investment for buying

cushion gas is required. The basic investment is taken as a constant. Additional investment is

a function of the gas price , which changes according to the geometric Brownian motion:

, (6.1)

where is the drift coefficient, is the proportional variance coefficient and is the increment

of a standard Wiener process.

As accounts for the price of all bought cushion gas and can be expressed by

multiplying gas price and the amount of gas that is needed for making it as cushion gas, it

also follows the geometric Brownian motion and has the same drift and variance coefficients:

. (6.2)

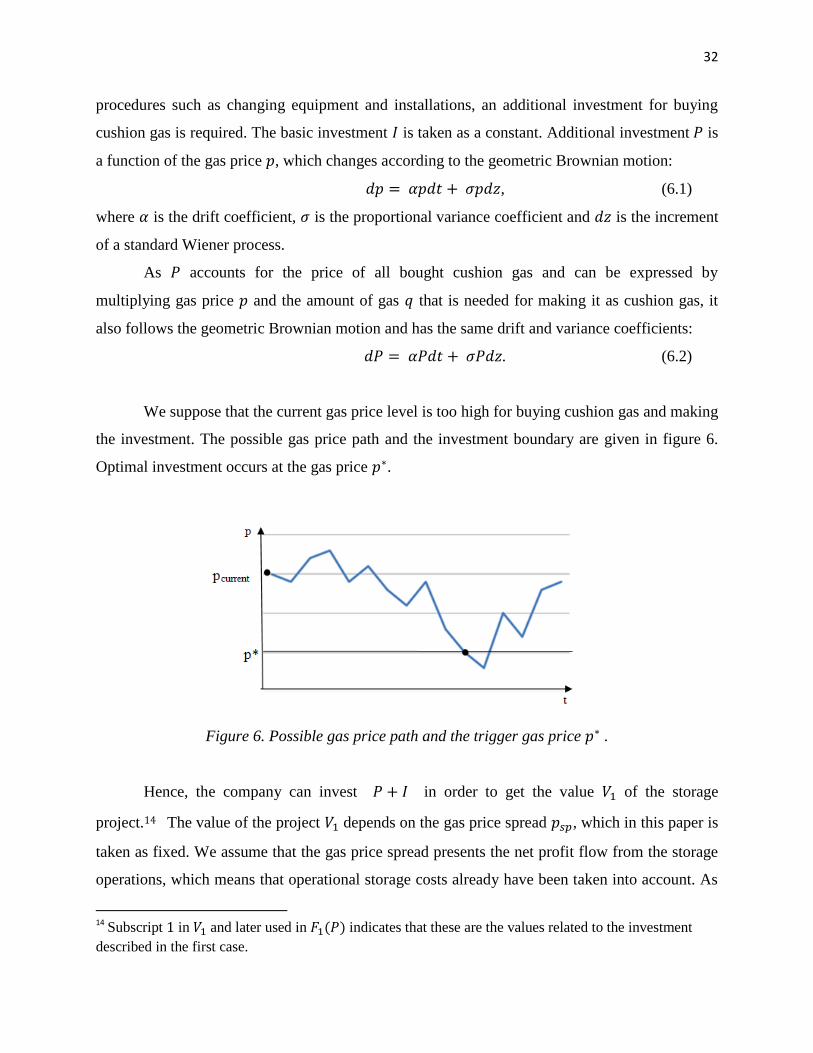

We suppose that the current gas price level is too high for buying cushion gas and making

the investment. The possible gas price path and the investment boundary are given in figure 6.

Optimal investment occurs at the gas price .

Figure 6. Possible gas price path and the trigger gas price .

Hence, the company can invest in order to get the value of the storage

project.14 The value of the project depends on the gas price spread , which in this paper is

taken as fixed. We assume that the gas price spread presents the net profit flow from the storage

operations, which means that operational storage costs already have been taken into account. As

14

Subscript in and later used in indicates that these are the values related to the investment described in the first case.

33

by assumption the project is infinitively lived, the value of the project can be calculated as a

perpetuity:

, (6.3)

where is the risk-free rate, is the amount of gas stored and sold per year, is the gas price

spread.

According to the real options theory, it is not optimal to make an investment if the future

cash flows (in this case it is ) ) are smaller than the value of an option to invest

. One of the conditions to determine the optimal timing is that the net payoffs from the

project have to be equal to the value of the option to invest. Note that the company, while

investing, is giving up the value of the option . Thus it is crucial for our analysis to

determine the value of the option to invest. This step will follow in the next subsection.

6.1.2. The value of the option

In order to determine the value of this investment option, we follow the steps of

contingent claims analysis which was discussed in the previous chapter 5.

To begin with, note that the value of an option to invest bears the uncertainty as it

depends on the gas price and is the function of the expenditure . It is assumed that the

uncertainty over future values can be replicated by existing assets in the economy. Hence,

a risk-free portfolio is built. A company holds a long position in the option to invest and a short

position in units of . During a short time interval dt, the company has to pay dividend

for holding the short position. Note that the option does not have a profit flow. Thus the capital

gain from the portfolio is

, (6.4)

where is the costs for buying the short position. Next, has to be determined.

Value can be obtained by applying Ito’s Lemma:

. (6.5)

After substitution of , equation (6.5) becomes

. (6.6)

34

As ,15 it follows that

. (6.7)

. (6.8)

Note that there is one term exposed to risk in the last equation - . Besides, in

our analysis the values of the options are dependent on the variable and not explicitly on time.

Thus we can eliminate the term from the equations as it is equal to zero.

The return on capital after substitution and terms collection is derived as:

. (6.9)

It can be seen now, that in order to make the portfolio free of risk, has to be chosen

equal to . Then the terms in dz disappear and portfolio becomes riskless. After substituting

into equation (6.9), we get that the capital gain from holding the portfolio is

. (6.10)

Total return from portfolio - which is capital gain minus dividend paid for the short

position - becomes

. (6.11)

As , and total return of portfolio is equal to the riskless return, it follows

that

; (6.12)

. (6.13)

Equation (6.13) is a second order linear differential equation, dependent on the variable

and its first and second order derivatives. For the solution of this homogeneous equation,

15

It was already explained while describing Ito’s Lemma. See subsection “Ito’s Lemma”.

35

function can be tried. After substituting this solution in to equation (6.13) and collecting

the terms, we get the characteristic equation

. (6.14)

Solving this equation, and are obtained:

; (6.15)

. (6.16)

In addition, , . This follows from the properties of the characteristic

equation (6.14).16

Now the general solution of the equation (6.13) can be obtained. It is the sum of two

independent solutions and

:

, (6.17)

where and are the constants to be determined.

Regarding the general solution, some economic considerations have to be taken into

account. When the costs for buying cushion gas are very high, the value of the option to invest is

becoming worthless. Thus when is approaching infinity, should become zero. However,

the term is also going to infinity when increases. Thus the term is set to zero in

equation (6.17). Now the solution is

. (6.18)

To obtain the values of , and , we use the following boundary conditions: 16

The characteristic equation has the shape of an upward-pointing parabola (see Appendix A for the graph of the characteristic equation). Moreover, and . Thus one root is larger than 1, and another one is negative.

36

. (6.19)

. (6.20)

The considerations of optimal investment provide conditions (6.19) and (6.20). can be

called the free boundary at which it is optimal to make an investment. Thus the first condition

(6.19) says that after investment the company gets a net payoff , which is equal to

the value of an option to invest at an optimal . This is called the “value-matching” condition.

The second condition (6.20) is the “smooth-pasting” condition, which means that the slopes of

the two functions (option value and net payoff) have to match the boundary .

It follows that

; (6.21)

. (6.22)

After solving the system of these equations, we get:

; (6.23)

. (6.24)

Here are the costs for buying all cushion gas needed. So the optimal costs for buying

one m3 of gas - which is the price of gas - at which investment should be made are:

(6.25)

where is the amount of cushion gas needed to buy.

It can be seen from equation (6.23) that the price for buying all cushion gas depends on

the parameter and on the difference between the project value and the basic investment costs.

If the value of the project increases (keeping other parameters constant), then the company is

willing to spend more on buying cushion gas. The parameter itself is a function of the risk-

37

free rate, convenience yield and volatility.17 Furthermore, if we express the project value from

equation (6.23), we get that

(6.26)

As , it follows that the value of the project has to exceed the costs ( )

in order to start the investment. This is contrary to the NPV rule which states that investment

should be done when the value is equal to the investment costs. The results imply that, according

to the real options approach, the company would demand higher return from its investment

because of the uncertainty and investments’ irreversibility.

In this section we have determined the optimal investment timing and the trigger gas

price at which investment in gas storage project should be implemented. The estimated optimal

gas price depends on a number of parameters such as the convenience yield, risk-free rate, gas

price volatility, value of the project and investment costs. The impact of the parameters on the

trigger price will be examined in the next chapter, where a numerical example will be provided.

In the next section another case of the investment in a gas storage project is analyzed.

6.2. The timing of two opportunities: gas field depletion and conversion into gas

storage

In this section we analyze the case where a company can make an investment in a

partially depleted gas field in order to convert it into a storage facility. It is assumed that the field

still holds a particular amount of gas that would be sufficient enough for using it as a required

volume of cushion gas. The company can choose between two options:

to convert the field immediately into a storage facility – option 1;

to deplete the field completely and then wait until the price drops sufficiently to

reinvest and start a storage project – option 2.

The choice between those two options depends on the gas price. If the gas price is high

( ), then it is profitable first to deplete the field and to sell the gas; and afterwards, when the

gas price drops to the gas price level (which was already determined in the previous analysis), 17 See equation (6.16).

38

to start storage. The company would convert the gas field immediately into a storage facility if

the gas price is at the low level . In our analysis we assume that the high trigger price

is always higher than the low trigger price . Hence the gap in between the two trigger gas

prices stands for a waiting period.

Assume that the current gas price is between the low and high gas prices. The possible

gas price paths and investment boundaries are illustrated in figure 7. The gas price path

favourable for the investment in option 1 is shown in figure 7(a). If the gas price firstly reaches

the boundary , then the company invests in gas storage. The possible gas price path when

investment in option 2 occurs is illustrated in figure 7(b). Note that we assume that is smaller

than . Thus in 7(b) it can be seen that after depleting the field and selling the gas at ,

the gas price has to drop to the lower level in order to start gas storage.

(a) (b)

Figure 7(a-b). Gas price paths and the trigger gas prices , and .

In the following subsections we will value these options and derive the high gas price –

the trigger price for investment in option 2 -, and the low gas price – the trigger price for

investment in option 1. As before, firstly the values of the projects are determined. Further,

starting with the options’ value expressions and using solving conditions, we obtain the

solutions.

6.2.1. The value and costs of the investment projects

In this case both investment projects require basic investment costs and have the same

profit flow from storing gas. However, the analyzed two investment opportunities differ in their

39

total costs and profits structure. The differences in the values of the projects are discussed in this

subsection.

Firstly, if the company is starting a gas storage project immediately, there is no need to

buy cushion gas as the required amount of it is left in the gas field. Thus, the company faces only

investment costs . Similarly to the previous analysis, these basic investment costs are taken as

fixed. The profit flow from this project is coming from the storage operations and depends on the

gas price spread . The gas price spread is taken as fixed, thus value of the infinitively lived

storage project can be obtained again as a perpetuity:

,18 (6.27)

where is the risk-free rate of return, is the amount of gas stored and sold per year, is the

gas price spread.

On the other hand, if the company firstly depletes the field and afterwards makes use of it

as a storage facility, it has higher investment costs. The company not only has to cover basic

investment costs , but also the costs for buying cushion gas. It was mentioned before, that

expenses for cushion gas depend on the gas price, which follows geometric Brownian motion.19

Furthermore, while implementing this option the company gets a profit from depleting the field

and selling the gas that was still left in the field. In addition, there are fixed production costs

for extracting the rest of the gas from the field. Thus the net payoff of this option is equal to the

profit from selling gas, less production costs and plus the value of the storage project that could

be implemented after gas field depletion, when the gas price drops sufficiently low.

Understanding the costs and profit flows of every investment project is important for

building the right solving conditions and therefore determining the value of the option. These

values of the options and solving conditions are presented and solved in the next subsection.

6.2.2. The value of the options

In this case the company holds an option – either to start gas storage immediately or to

deplete the field first – which has the value described as a function . At two different price 18

Subscript in and later used in indicates that these are the values related to the investment described in the second case. 19

See equation (6.2).

40

levels – the low price and the high price - the value of this option differs. This means that

investing in one of the two projects, the company gives up either the option value (at the

low price ) or (at the high price ).

The values of these options are derived by following the steps of the contingent claims

approach, using the same hedging argument as in the previous analysis. We get the following

expression for the value of the option to convert a gas field into a storage reservoir without

depleting it20:

, (6.28)

where and are the constants to be determined.

Similarly, the value of the option to deplete the field when the gas price is high and

afterwards to switch to gas storage is

. (6.29)

When the company invests in option 1, it gets a net payoff equal to ( ). Thus the

value matching condition for the value of this option becomes

. (6.30)

In addition, the smooth-pasting condition is

(6.31)

The way of solving the system of equations (6.30) and (6.31) is provided in Appendix B.

After solving it we get:

; (6.32)

. (6.33)

20

This is the value of the option that is implemented when the gas price is low, .

41

When the gas price is high, the company depletes the field first and gets the profit

from selling the gas. Besides, while depleting the field, the company also faces production costs

. After producing the gas, the company holds an empty field. The value of the option to invest

in storage when the field is completely depleted was already determined in the previous section

(see equation 6.18). As a reminder, it is equal to

. (6.34)

Hence, regarding option 2, for the value-matching condition we equate the value of the

option (equation 6.29) to the net payoff that the company would get after depleting the field:

. (6.35)

The smooth-pasting condition becomes

(6.36)

The solution of the system of equations (6.35) and (6.36) is given in Appendix C. Solving

it gives that

; (6.37)

. (6.38)

As the value for cannot be estimated directly, we determine the ratio

instead. The

following equations are obtained using equations (6.32), (6.33), (6.37) and (6.38):

–

; (6.39)

. (6.40)

42

It follows that

–

. (6.41)

Even though cannot be derived analytically, we can obtain a numerical solution of .

Then can also be calculated as:

. (6.42)

Similarly to the previous analysis, the trigger high and low gas prices depend on several

parameters. In the following chapter, together with the results from the first case, we will analyze

how the changes in particular parameters affect the values of those trigger prices. As an example,

we will take the Dutch gas market and assign the real values of the parameters. Numerical gas

prices that are necessary for implementing investments in gas storage will be estimated.

43

7. Numerical Case

Even though we use real options methodology to solve a practical investment problem,

the solutions derived in chapter 6 may appear too abstract. In this chapter we will use a

numerical case to illustrate the results of the real option analysis and provide realistic outcomes.

The numerical case will be applied for the Dutch21 gas market. We will firstly provide the actual

values of the parameters and then estimate the trigger gas prices. However, one should be aware

that these numerical values are not certain and change according economic and technical

conditions. Hence, we will perform a sensitivity analysis and examine the effect of particular

parameters on the trigger gas prices and other important outcomes.

7.1. Actual values of the parameters

There were a number of parameters used in the analysis. The main parameters are

associated with the gas price, discount rates, costs and capacity characteristics of the gas field.

In the analysis the main modelled uncertainty is the gas price which follows a geometric

Brownian motion.22 We estimated that the compound annual growth rate of the gas price (taken

as the Henry Hub Index HHUB23) during the period of 1990-2010 is 2.5 percent per year.24 Thus,

= 0.025. Excluding the gas price peaks from the same historical gas price data, it was

calculated that annual gas price volatility is 70 percent, ergo = 0.7. Furthermore, it was already

mentioned in chapter 3 that the historical seasonal gas price spread was 0.015 €/m3 during 1994-

2004. However, in order to make storage projects more financially feasible, we will use the

higher gas price spread ( = 0.03 €/m3) as one of the basic parameters. The value 0.015 €/m3

will be used later in the sensitivity analysis. 21

Although we want to estimate actual values of the investment in gas storage in The Netherlands, some data (such as data on historical gas price) is taken from US markets. This is due to a very limited access to European data. 22

To remind the reader, we express the gas price as , where is the drift coefficient, is the proportional variance coefficient and is the increment of a standard Wiener process. 23

The Source: Bloomberg. 24 The compound annual growth rate is calculated as follows:

.

44

Another important group of the parameters is the discount rates. The risk-free rate is

determined as the average of the last 10 years historical The Netherlands Government bond (10

year) yield and is equal to 4.2 percent. 25 Moreover, the value of convenience yield from gas

storage was already estimated in several articles (Wei and Zhu, 2006; Khan, Khokher, Simin,

2005). The estimates of convenience yield vary from 2.5 percent to 4 percent. In this paper we

take the average of these estimates – which is 3.25 percent – as the value of the convenience

yield. Consequently, we derive the risk-adjusted expected rate of return, which is expressed as

. Hence, = 0.058.

Concerning gas field characteristics, a medium sized gas storage facility is chosen. The

total gas field storage capacity is assumed to be 5 billion m3. Besides, we assume that 60 percent of

the gas field’s storage capacity is cushion gas. This implies that working gas capacity is 2 billion m3

and the rest, 3 billion m3 is cushion gas. In respect to the gas field capacity, we estimated the

average development costs to be €660 million26. The expenses for cushion gas depend on the gas

price and are derived in the analysis. Furthermore, the average gas production costs in the

Netherlands are taken as 0.02 €/m3 (Lochner and Bothe, 2009).

Since we have already assigned the actual values to the parameters, now we can obtain

the values of the investment projects and estimate the trigger gas prices. This follows in the next

section.

7.2. Results

In this section we will present the numerical results obtained while performing a real