Embed Size (px)

Citation preview

Journal of Public Economics 46 (1991) 347-381. North-Holland

Investment and government intervention in credit markets when there is asymmetric information

Robert Innes*

University of California, Davis, CA 95616, USA and University of Arizona, Tucson, AZ 85721, USA

Received April 1989, revised version received April 1991

This paper models private firm investment choices and government credit policy in an entrepreneurial firm financial market wherein firm owners have better information about the quality of their return distributions than do external financiers. The analysis shows that, despite the absence of an informational advantage, the government can often increase social welfare by offering subsidized debt contracts. However, the paper also finds that some common credit subsidy policies, including loan guarantees and government backing of targeted lending institutions, yield constrained inefftc:ent outcomes in general.

1. Introduction

This paper examines a competitive capital market in which risk neutral entrepreneurs/borrowers have private information about the quality of their return distributions. Since entrepreneurs with low quality investment projects present prospective lenders with higher default risk than those with high quality projects, lenders are willing to offer high quality types better loan terms (i.e. a lower interest rate). These better loan terms give the low quality types an incentive to ‘masquerade’ as high quality. However, since the high quality entrepreneurs can make better use of any investment funds that they borrow, they can discourage low quality ‘masquerading’ by choosing to take out a sufficiently large loan. Alternatively, if the cost of this excessive investment is too high, the high quality types can bear the costs of sharing a contract with low quality entrepreneurs.

In deducing the properties of the informational equilibrium, the following

*I am indebted to two anonymous referees, Professor Atkinson, Larry Karp, Richard Sexton, T.W. Schultz, Stacey Schreft, Brian Wright, David Zilberman, Gordon Rausser and seminar participants at U.C. Berkeley, U.C. Davis, the University of Chicago, the University of Arizona, Montana State University and the 1989 Western Economic Association meetings for helpful remarks on earlier drafts.

0047-2727/91/$03.50 0 1991-Elsevier Science Publishers B.V. All rights reserved

348 R. Innes, Investment and government intervention

analysis identities inefficiencies and shows that, despite a lack of any informational advantage, government can often intervene to improve social welfare. This intervention takes a form that is frequently observed in practice, namely the offer of subsidized credit contracts. In essence, debt subsidies that are attractive only to low quality firms reduce the latter firms incentive to disguise themselves as high quality; the subsidies thereby permit sorting at efficient (perfect information) investment levels. Despite the potential for beneficial government intervention, other typical credit subsidy policies, including loan guarantees and government backing of targed lending institu- tions, are found to yield outcomes that are, in general, neither first best nor second best.

The importance of asymmetric information for both investment choices and the efficiency properties of credit market equilibria has been noted in several recent articles. The contributions that are most relevant to this analysis are the interesting papers by Mankiw (1986) and DeMeza and Webb (1987, 1988, 1989). ‘3’ These articles also analyze credit markets in which borrowers have private information about their investment projects’ return distributions. However, all of these papers identify inefficiencies in competi- tive equilibrium lending decisions that are of a very different nature than those found here.

DeMeza and Webb (DW) (1987), for example, find that credit taxes can correct an over-investment problem when borrowers have a common and fixed investment/loan size. In DW’s model, all quality types must be given the same loan terms, so that the low quality entrepreneurs face a high- quality-subsidized interest rate which is lower than they would face with perfect information. This implicit subsidy leads low quality entrepreneurs, who would not undertake their investment projects in a perfect information world, to borrow and invest. The resulting over-investment can be deterred by taxing the loan contract. While DW’s analysis is consistent with use of

‘Much of this literature springs from the work by Jaffee and Russell (1976) and Stiglitz and Weiss (1981) on equilibrium ‘credit rationing’ in markets with imperfect information. In addition to the papers cited above, two other strands of this credit rationing research have recently received considerable attention. First, a number of papers have examined the implications of costly collateral provision in credit market models with asymmetric information [e.g. Besanko and Thakor (1987), Bester (1985), and Chan and Kanatas (1985)]. In this research, provision of collateral can serve as a signaling device, but variable investment choices are not permitted. Second, several papers have focused on asymmetries in profit observation costs and their effects on both financial contract forms and investment levels [e.g., Diamond (1984), Williamson (1987), Bernanke and Gertler (1989). and Gale and Hellwig (l98S)]. In the latter research, investors can only observe ex post protits with a cost but, unlike here, there is no informational asymmetry concerning the entrepreneur’s ex ante profit distribution.

‘Milde and Riley (1988) also analyze the use of investment choices as signals of entrepreneurs’ quality types, coming to some conclusions on the attributes of the free-market equilibrium that are similar to those derived below. However, Milde and Riley (1988) do not permit pooling outcomes in their equilibrium and do not elaborate on either the efficiency properties of plausible equilibria or the effect of standard policy interventions in this environment. The latter subjects are emphasized here.

R. Innes, Investment and government intervention 349

debt (rather than equity) financial instruments, its logic depends on the inability of quality types to self-select by choice of investment size.

Mankiw (1986) also precludes self-selection by assuming that investment levels are fixed and common across borrowers. However, in contrast to DW, Mankiw reaches policy conclusions similar to those expressed here (i.e. that debt subsidies can be optimal). In his model, benefits of intervention result from a divergence between the bank’s return on a loan (which is truncated) and the social return on a loan (which is not); this divergence implies that banks are concerned with certain unknown risk parameters which the government is not, often leading banks to reject loans for socially desirable projects. This argument assumes that both the informational asymmetry and debt financing are immutable. Here, in contrast, the analysis endogenizes both information (by permitting investment signaling) and, implicitly, the form of the financial instrument (by constructing a model that has been shown to induce debt contract forms). Moreover, policy benefits are attribu- table to their effect on the screening process rather than to any inefliciency in banks’ acceptance or rejection of loan applications.

Finally, the latest DeMeza and Webb paper (1989) is most closely related to this analysis in that it permits entrepreneurs to choose their investment levels. Despite this similarity, the latter paper focuses on different issues than are examined here. In particular, DW (1989) consider: (1) how competitive pooling equilibria diverge from the most efficient pooling contract and (ii) the policy implications of this divergence. In comparing these pooling contracts, they find that ‘over-investment’ tends to persist, even in the absence of entry by inefficient low quality entrepreneurs. As in the earlier DW papers, the excessive investment can be deterred by an interest rate tax. However, given their focus on pooling outcomes, DW are not concerned with the govern- ment’s ability to foster self-selection, an ability which motivates all of the policy analysis and policy conclusions that are presented here. In essence, DW (1989) consider a different government ‘target’ (i.e. the best possible pooling contract) than is considered in this paper (i.e. contracts that are first or second best, allowing for self-selection). The sharp contrast between the policy conclusions derived here and those developed in DW (1989) illustrates the importance of this distinction.

In what follows there are two types of entrepreneurs, low and high quality, who face a set of competitive and risk neutral investors. Under perfect information, the high quality entrepreneurs invest more than the low quality types because of the high quality types’ superior ability to utilize the investment funds. Under asymmetric information the high and low quality entrepreneurs’ loan contracts that emerge in the competitive equilibrium are those that are most preferred by the high quality entrepreneurs, subject to three constraints: (i) the investors earn a non-negative expected profit on each distinct contract; (ii) contracts are incentive-compatible in that each

350 R. Innes, Investment and government intervention

quality type weakly prefers his contract to the other type’s contract; and (iii) low quality entrepreneurs obtain an expected payoff which is at least as high as that which they can obtain under perfect information. In essence, the low quality entrepreneurs must adhere to the high-quality-preferred contracts in order to conceal their type and thereby obtain any information rents that are available.

Two types of free-market equilibria are possible: pooling and separating. When there is pooling, high quality entrepreneurs face higher interest rates than under perfect information owing to the higher default risk of low quality borrowers. However, the high quality types can still make better use of investment funds than can low quality types. Therefore, in a pooling (single contract) equilibrium, the high quality entrepreneurs choose a con- tract that specifies less investment than they would undertake in a first-best/ perfect information world, but more investment than low quality types would undertake under perfect information. In a separating (two contract) equili- brium, low quality entrepreneurs invest at their first-best level and, in order to signal their type, high quality entrepreneurs typically invest more than under perfect information.

By offering a subsidized credit contract designed for low quality entrepre- neurs, the government can reduce the low quality types’ incentive to mimic the high quality types and thereby elicit a separating equilibrium with tirst- best investment choices by all borrowers. Thus, when the free-market equilibrium is pooling, this subsidized credit policy leads to a lower investment level for low quality entrepreneurs and a higher level for high quality entrepreneurs. When the market equilibrium is separating (and not first best), this policy leads to a lower investment level for high quality entrepreneurs. These results contradict a conventional view that government lending programs necessarily lead to excessive investment.

A uniform (lump-sum) government grant to entrepreneurs can also elicit contractual choices that are first or second best. By reducing the interquality disparity in default risk, government grants reduce the disparity in loan terms that are offered different quality types under perfect information, which in turn reduces the incentive for low quality entrepreneurs to masquerade as high quality types; the grants thereby permit high quality entrepreneurs to signal their type with investment choices that diverge less from their first-best level.

However, not all forms of credit subsidy policy can support outcomes that are efficient in a first- or second-best sense. Under perfect information, neither government grants nor the direct offers of the subsidized contract described above will alter entrepreneurs’ investment choices; hence, in this paper’s financial market, the only effect of these programs is to reduce the costs of asymmetric information. In contrast, both loan guarantees and

interest rate subsidies to targeted lending institutions yield entrepreneurs

R. lnnes, Investment and government intervention 351

improved perfect information loan terms on all investment levels, almost always leading low quality entrepreneurs to make an investment choice that is neither first nor second best.

Given the extensive government involvement in entrepreneurial credit markets, both in the United States and abroad, these observations are potentially of more than theoretical interest. In the United States, examples of this intervention include support of small businesses, via the Small Business Administration, and to farmers, via the Farmers Home Admini- stration (FmHA), the Farm Credit System (FCS), and the new ‘Farmer Mac’. Intervention has also taken all of the forms discussed here, including direct offers of credit (e.g. via the FmHA), loan guarantees (e.g. via ‘Farmer Mac’), grants (e.g. via the U.S. farm program), and interest rate subsidies (e.g. via implicit government backing of FCS securities). The following analysis sheds some light on the economic implications of these types of government programs in the presence of asymmetric information.

The paper is organized as follows. Section 2 describes the model in detail. Section 3 characterizes the free-market informational equilibrium in the entrepreneurial credit market. Section 4 analyzes the positive and welfare implications of the various policy measures mentioned above. Finally, section 5 presents some concluding observations. An appendix contains formal proofs of selected lemmas and propositions3

2. The model

2.1. Entrepreneurs

Consider a population of risk neutral entrepreneurs who are of two types: high quality (H) and low quality (L). The proportion of low (high) quality entrepreneurs in the population is g(L)(g(H) =( 1 -g(L))). Each entrepreneur knows his own quality, but others do not. Furthermore, each produces a stochastic end-of-period net worth (also called profit) n=n(q,A, e), where q

represents quality type, A denotes the initial asset value of the firm and 8 is a random variable. Assets, A, are financed by external funds equal to I dollars and a given amount, (A-Z), of the entrepreneur’s initial wealth. Without loss of generality, each member of the population is assumed to commit a common amount of his own funds to the firm so that I defines L4 Given I (and thus A) and q, 8 gives rise to probability density and distribution

30ther proofs are available from the author upon request. 40wing to the logic of Leland and Pyle (1977), it can be shown that entrepreneurs will invest

all of their wealth in the firm. Hence, this paper actually restricts its attention to a population of entrepreneurs with homogeneous wealth endowments.

352 R. Innes, Investment and government intervention

functions for z, f(z 14, I) and F(n 1 q,Z), respectively. The function f(.) is assumed to be continuously differentiable on [0, K(q, Z)], where K(.) >O whenever Z>O. In addition, higher quality (higher q) and higher investment levels produce ‘better’ net worth distributions in the sense of first-order stochastic dominance. Formally,

F,(z) < 0, F,(z) < 0 and F&d < 02 (1)

Vn E [O, K(q, Z)], where subscripts denote partial derivatives. The negative cross-partial derivative in (1) ensures that higher quality is associated with ‘better’ marginal investment returns.

Defining expected firm profit as

KM. 0

n,(z)-E{+,q)= { Q’(+iJ)d~~ 0

condition (1) implies that C:(Z) >0 and &T~(Z)/dq>O. It will also be assumed that tig( )<O, lim,,,%b(Z)= cc and lim,,, E;(Z) = 0. The latter constraints ensure positive and finite equilibrium investment levels for both quality types.

2.2. Financial contracts

A financial contract between an entrepreneur and investors prescribes the investment level, I, and the amount of money that the investors are to be paid at the end of the period. The latter amount will depend on the profit/ net worth that is available for payment, 71, implying an investor payoff function, R(n). For analytical purposes, some weak restrictions will be placed on the forms that these functions can take: R(n) must be non-decreasing.5 In addition, R(z) zn: (limited liability). Given these restrictions, it can be shown that any given contract, (Z,R(z)), earns an investor a higher expected profit when taken by a high quality entrepreneur than when taken by a low quality entrepreneur?

%ee Innes (1988) for a discussion of behavioral foundations for this monotonicity constraint. 6For convenience, eq. (2) implicitly assumes that R(n) is piecewise differentiable. This

assumption is not required for any of the resuults in this paper.

R. Innes, Investment and government intervention 353

KC,)

)Z,H}-E(R(n)IZ,L}=- i R'(n)(F(nIZ,H)-F(n:IZ,L)}dn>O.

(2)

2.3. Investors

The investors are assumed to be risk neutral and competitive in that they will offer any set of contracts that is expected to yield them a non-negative mean profit (i.e. an expected return no less than that on a risk-free bond, p). For simplicity, in what follows it is also assumed that investors prefer to sign a zero expected profit contract than to have no contract, while they prefer no contract to any negative expected profit contract.

In calculating their profit/return expectations, investors are cognizant of the choice problems that face entrepreneurs of different quality, the distribu- tion of qualities in the population, and the nature of the market game that they are playing (see subsections 2.4 and 2.6 below). Thus, if different entrepreneurs choose different financial contracts, investors will infer quality from this choice; otherwise, the quality of an applicant entrepreneur will be treated as a random variable with its known distribution.

For convenience, the investor’s opportunity cost of funds, p, is assumed to be invariant to changes in total entrepreneurial investment. Implications of relaxing this ‘small sector’ assumption will be noted when relevant.

2.4. The game

Following Hellwig (1987) and DeMeza and Webb (1989), a three-stage pure strategy game between the investors and entrepreneurs is posited. This game structure is chosen because it always has at least one Nash equilibrium [avoiding the non-existence problem identilied by Rothschild and Stiglitz (1976)], and also because it seems to accord with institutional conventions in capital markets for entrepreneurial firms. The three stages of the posited game are as follows:

Stage 1. Each investor announces a set of contract offers. Stage 2. Each entrepreneur applies for one contract out of the set of

Stage 1 investor offers. Stage 3. After observing the Stage 2 application choices of the population

of entrepreneurs, each investor decides whether to accept or reject each application that he has received.

Thus, each entrepreneur applies for one of the loan contracts on offer by competing banks; each bank then reviews each application that it has received (in light of all applications made) and decides which of these

354 R. Innes, Investment and government intervention

applications to fund.‘*s Given the sequential nature of this game, I will be concerned here with sequential Nash equilibria in the sense of Kreps and Wilson ( 1982).9

2.5. Nash equilibrium contracts under perfect information

Under perfect information, Bertrand-type competition between investors in Stage 1 permits each entrepreneur to obtain a contract that maximizes his net expected profit subject to the investor receiving a zero expected profit. Therefore, the perfect information investment levels of the quality 4 entrepre- neur, Z4*, solves

maxE{rr/I,q}-(l+p)I. I

A corresponding perfect information investor payoff function, R,*(Z), is any function such that the above functional form restrictions hold and

2.6. Equilibrium under asymmetric information

Under asymmetric information, there can be many sequential Nash equilibria to the three-stage game described above [see, for example, Hellwig (1987)]. Any of these equilibria yield signed contracts that have the following properties:

(El) Investors earn a non-negative mean profit on each distinct contract.

‘If one were to eliminate the third stage to the game above, implying that investors commit to sign any contracts that they offer, then the game would be analogous to that analyzed by Rothschild and Stightz (1976) and it would often have no Nash equilibrium. However, as a referee has pointed out, the first stage to this game is not essential to the existence or characterization of an equilibrium in this paper; nothing that follows would be altered in substance if Stage 1 were eliminated and each entrepreneur were simply to propose a single contract in Stage 2. The three-stage structure is retained here in order to be consistent with prior analyses.

‘The usual assumption is made here that, when a given stage of the game is reached, all agents have observed all actions taken in prior stages. A potential criticism of this assumption is that it requires each investor to observe the applications received by other investors. However, this paper’s characterization of an equilibrium extends quite directly to an analog of the above three-stage game in which investors take applications on a case-by-case basis, i.e. two or more investors play a separate loan contract game with each entrepreneur and do not observe all Stage 2 application choices as of Stage 3.

% a sequential equilibrium, the Nash requirement that each agent’s strategy be a best response to othe agents’ strategies is not only applied to the overall game, but to each and every information set in the game.

R. Innes, Investment and government intervention 355

(E2) Low quality entrepreneurs earn an expected payoff that is at least as high as their perfect information expected payoff, %E -E(n) I:, L) -

u+m.

The investor’s ability to reject applications in Stage 3 (and to infer entrepreneur’s Stage 2 application choices) ensures the (El) is satisfied for any signed contracts that emerge in a sequential equilibrium. Furthermore, (E2) must hold in a sequential equilibrium - and all entrepreneurs obtain signed contracts - because investors are always willing to offer (in Stage 1) and sign (in Stage 3) perfect information low quality contracts, earning a zero expected profit on any low quality applicants and a positive expected profit on any high quality applicants.

In this paper I restrict attention to sequential equilibria which have other properties that I believe to represent plausible restrictions on agents’ behavior both on and off the equilibrium path. The first of these properties is an incentive compatibility requirement for signed contracts that emerge in equilibrium:

(E3) Each (and every) entrepreneur weakly prefers the contract that he obtains to contracts obtained by other entrepreneurs.

With a finite set of entrepreneurs, perfect information contracts can emerge in a sequential equilibrium even when these contracts violate the incentive compatibility condition (E3). To see this, consider the Stage 2 choice problem of the low quality entrepreneur when perfect information contracts have been offered in Stage 1 and the low quality type prefers the high quality contract on offer. (A high quality entrepreneur never prefers a low quality perfect information contract to his own perfect information contract.) Given the posited equilibrium strategies (according to which each entrepreneur applies for his perfect information contract), if any low quality type were to apply for the high quality contract, investors would observe more appli- cations for the latter contract than would be possible if only high quality entrepreneurs had applied. Therefore, the low quality application for the high quality contract would lead investors to reject (in Stage 3) all applications for the now-unprofitable high quality contract. Deducing this investor response to his application for the high quality contract, the low quality entrepreneur would not deviate (at Stage 2) from the low quality contract on offer.”

There are two problems with this perfect information equilibrium. First, it requires each low quality entrepreneur to believe that his application choice affects market outcomes, a requirement that violates conventional notions of competitive/atomistic behavior. Second, this equilibrium requires entrepre-

“I am indebted to a referee for these observations.

356 R. Innes, Investment and government intervention

neurs to allocate themselves to distinct contracts without any mechanism that provides them with an economic incentive to do so. Why, a priori, should low quality entrepreneurs believe that they must settle for the ‘bad’ contract, while high quality types believe that they can obtain the ‘good’ contract? In fact, a continuum of equally plausible (and implausible) sequential equilibria give a ‘good’ contract to a mix of low and high quality entrepreneurs and give a ‘bad’ contract to the remaining mix of entrepre- neurs. Because of these problems with incentive-incompatible equilibria, I believe that (E3) is a natural restriction in this paper’s competitive model.

In addition to imposing (E3), I will restrict attention here to the sequential equilibria that are most preferred by high quality entrepreneurs among those that yield signed contracts that satisfy (El)-(E3). I believe [and Hellwig (1987) has argued] that these particular equilibria are the most plausible outcomes of the above game for the following reason. Among contracts satisfying (El)-(E3), any set that is not most preferred by high quality entrepreneurs is expected to be supplanted (in Stage 1) by competitive offers of the contracts that are most preferred by the high quality types; the latter contract offers will be expected to attract at least the high quality agents, yielding the associated investors signed contracts with a non-negative expected profit. This last statement implicitly imposes some restrictions on investors’ beliefs about which entrepreneurs would apply for the high-quality- preferred contracts, were they offered in Stage 1. In an expanded version of this paper, some plausible restrictions of these beliefs are formalized in a ‘Strong Intuitive Criterion’ [a somewhat stronger criterion than the Cho and Kreps (1987) ‘Intuitive Criterion’] and shown to restrict sequential equili- brium outcomes to high-quality-preferred contracts. A formal statement of my restriction to the latter equilibria follows.

Definition. A Wilson Allocation [from Wilson (1977)] is a set of two (possibly identical) contracts, (I,,&(X)} for q= L, H, that maximize the expected payoff of the high quality entrepreneurs (q= H) subject to contraints (El)-(E3):

max E+-RH(~ILH) (I,,R,l,q=L.H

s.t.

.@E{R(4 ILL) +(l -gVW{N4 (LH)1(1 +pV,

if (I,, RJ = (1, RI, q = L, H, @lb)

R. Innes, Investment and government intervention 357

(E3)

Assumption. An equilibrium to the three-stage game described in subsection 2.4 yields a Wilson Allocation.‘l

2.7. Debt contracts

For the setting described above, it has been shown elsewhere [Innes (1988)] that equilibrium financial contracts take a debt form, R&II) = min (rr, zq), where zq is a promised loan payment.” In essence, debt contracts maximize investor payoffs in low entrepreneurial profit states of nature. Since low quality types have probability weight concentrated in these states, high quality agents, by taking a debt contract, can minimize the low quality type’s incentive to masquerade and also reduce the cost of sharing a contract with their low quality counterparts. The incentive-compatibility constraint, (E3), and the investor return requirement (under pooling), (Elb), are thereby relaxed, permitting higher net expected profits for the high quality entrepreneur.

This debt-contracting result will be taken as given in the following analysis.

3. Competitive investment choices

Since the technological relationships between investment and net worth

“While a Wilson Allocation is a plausible outcome of the three-stage game posited here, another game structure has been shown to have plausible solutions with different contractual outcomes. This alternative formulation is as follows. In Stage 1, each entrepreneur announces an investment level. In Stage 2, each investor offers to each entrepreneur a payotf function, R(s), that will accompany the announced investment level. Finally, in Stage 3, each entrepreneur chooses one contract out of the Stage 2 offers that he has received. Owing to the logic of Cho and Kreps (1987) [see also Hellwig (1987) and Milde and Riley (1988)], Riley (1979) ‘reactive’ outcomes result from a strategically stable [Kohlberg and Mertens (1986)] equilibrium to the latter game. The central difference between Wilson and Riley allocations is as follows. Whenever possible, Riley outcomes elicit complete separation (i.e. all agents reveal their quality type by their contract choice). A Wilson allocation, in contrast, can contain ‘pooling’ contracts that are shared by different quality types, even when ‘separating’ allocations are possible. For the present setting, in fact, the two allocations diverge only when the Wilson allocation is pooling, in which case the Wilson allocation Pareto dominates Riley outcomes. In the interest of characterizing Pareto dominant pooling behavior, this paper adheres to a Wilson construction [as do DeMeza and Webb (1989)]. However, all of the results derived here have direct analogs in a ‘Riley game’ of the type described above, analogs that will be noted when relevant.

“This debt-contracting result actually requires a slightly stronger condition than F,(n)<0 everywhere, namely the monotone likelihood ratio property [Milgrom (1981)], a[&( .)/f( .)]j&z >O everywhere. Although the latter condition IS Implicitly assumed to hold here, tt IS not used in any of the derivations that follow.

358 R. Innes, Investment and government intervention

depend on an entrepreneur’s quality type, it is not surprising that the entrepreneur’s choice of investment can serve as a quality-sorting device under certain circumstances. The objective of this section is to shed some light on conditions under which such self-selection occurs, and on qualitative features of the investment-financial contract equilibrium. The next section focuses on the policy implications of this equilibrium.

To characterize the equilibrium contract structure, the following graphical concepts will be employed (see figs. 1-3 below): (i) entrepreneur indifference curves; (ii) investor offer curves; and (iii) investor iso-expected-proJt curves.

Letting z denote the promised loan payment on a debt contract, an entrepreneur’s indifference curve is a set of (z,I) contracts that yield a common net expected entrepreneurial profit (or utility) level. Since entrepre- neurs are always better off with a lower promised payment, z, given the investment level, I, lower indifference curves correspond to higher utility levels.

Similarly, an investor offer curve is a set of (z,I) contracts that yield investors an expected profit (net of the opportunity cost of funds) equal to zero. If the investor knows the quality of applicant entrepreneurs, his set of offers (the separating offer curve) will be different for different entrepreneurs. In particular, a higher quality type will be offered better terms, implying a lower offer curve. If the investor cannot infer the quality of applicants, his set of offers (the pooling offer curve) will lie somewhere between the separating offer curves.

More generally, .an investor iso-expected-profit curve is defined as any set of (z,I) contracts that yield a constant (zero or non-zero) investor expected profit on a given quality of entrepreneur. Since investors are always better off with a higher z (given I), higher iso-profit curves correspond to higher investor expected profits.

Formally, these curves are defined as follows:

Quality q indifference curve (IC,):

wl. I)

B&I, z) E J (X - z)f(~ 1 q, I) drc = B, constant.

Quality q separating offer curve (OC,):

R,(I,z)~ii,(Z)-B,(Z,z)-(1+p)l=0.

Pooling offer curue (OC,):

(3)

(4)

g(W,U, 4 + (1 -g(WW, 4 = 0. (5)

R. lnnes, Investment and government intervention 359

Quality q investor iso-expected-profit curve (If’,):

R&Z, z) = a,, constant. (6)

As is typical for self-selection models, a central feature of this analysis is the relationship that is assumed to hold between different quality types’ indifference mappings. The following relationship is assumed to hold here:

Assumption:

MRS,(I,z) =$ _ _ - ML 4 > - &,(I, 4 = e

&,,(I, 4 B,z(L 4 Br. dl _ = MRS,U,z). (7)

BW

In words, eq. (7) implies that high quality entrepreneurs have steeper indifference curves than low quality types. On an intuitive level this assumption is very plausible; it simply requires that high quality entrepre- neurs’ marginal investment returns are sufficiently large relative to those of low quality entrepreneurs that, in exchange for additional investment funds, the high quality agents can give up larger fixed payments and still preserve their net expected profit.

However, relationships other than (7) are possible even when the con- ditions in (1) hold. For instance, Milde and Riley (1988) construct an example in which marginal investment returns are invariant to quality.13 To preserve their expected payoffs in this case, entrepreneurs of different quality can give up exactly the same amount of expected profit in exchange for an extra dollar of investment. Since low quality types have higher default risk, the transfer of this common expected profit level is associated with a larger increase in the promised loan payment, z, for lower quality types. Therefore, steeper low quality indifference curves prevail.

Given the latter possibility, an expanded version of this paper investigates the implications of reversing the inequality in (7) for the results developed here. This extension is discussed in section 5 and is available in its complete form from the author.

Regardless of an entrepreneur’s quality type, the following relations ensure that indifference curves are everywhere upward-sloping:

K(q. I)

B,,V,z)= - j- J’,(+LW-O, (84

(8b)

“In my notation, this example is as follows: n(q, A, 0) = fi(A, 0) + q, with flA >O and be > 0.

360 R. Innes, Investment and government intervention

where (8a) results from integration by parts and eq. (1). Intuitively, higher investment levels, given z, increase an entrepreneur’s net expected payoff. Hence, to preserve the latter payoff, an increase in I must be accompanied by an increase in the debt obligation, z.

Analogous properties of the investor iso-expected-profit derived and are as follows.

Lemma 1. Investor iso-expected proJit curves are everywhere with slope

IPSg(l,z)=$ _ >(l +p), V(I,z)ER:,vq~H. R,

curves can be

upward-sloping,

(9)

In addition, the latter slopes decrease with quality: alPS,(I,z)/aq ~0.

Lemma 1 has the following interpretation. When investors commit an additional dollar of investment funds, the increase in the promised loan payment needed to preserve their expected profit is greater than (1 +p) dollars, owing to default risk. Furthermore, the required addition in pro- mised payment is higher for lower quality types because of the latter types’ higher default risk and inferior ability to generate profits from both total and marginal investment resources.

In a world of perfect information, this inferior ability of low quality entrepreneurs leads to the following property of investment choices:

Lemma 2. Perfect information investment choices, I$, are increasing in q.

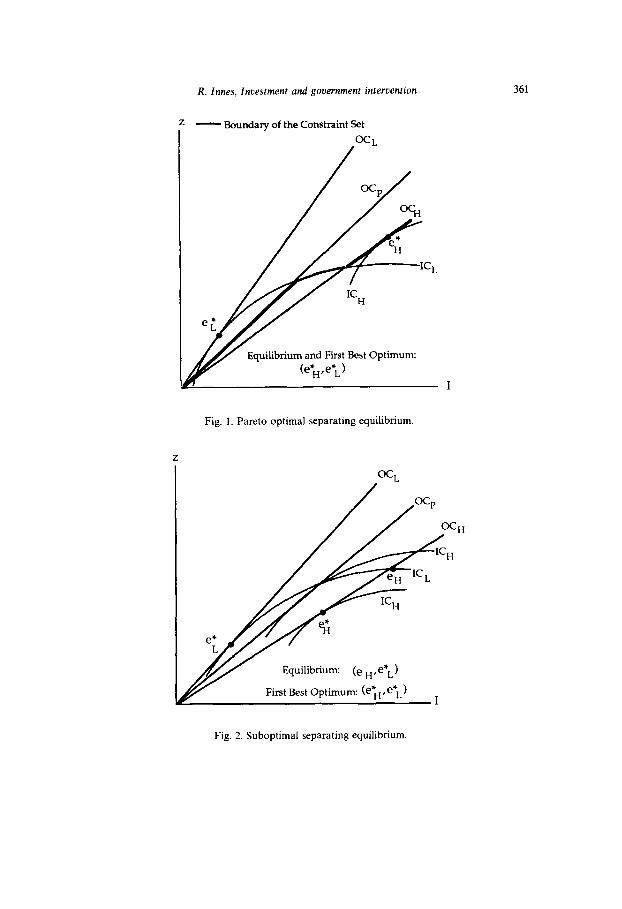

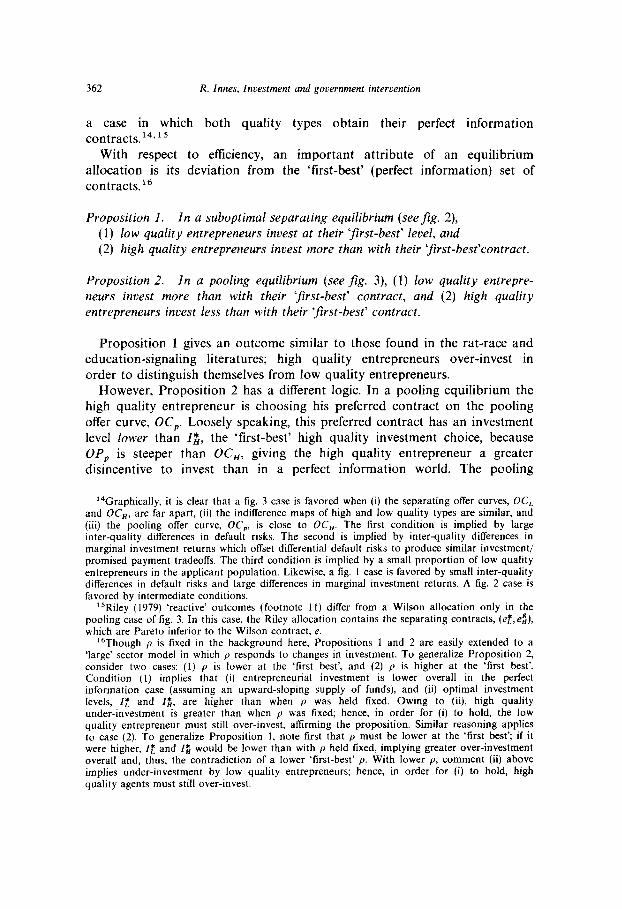

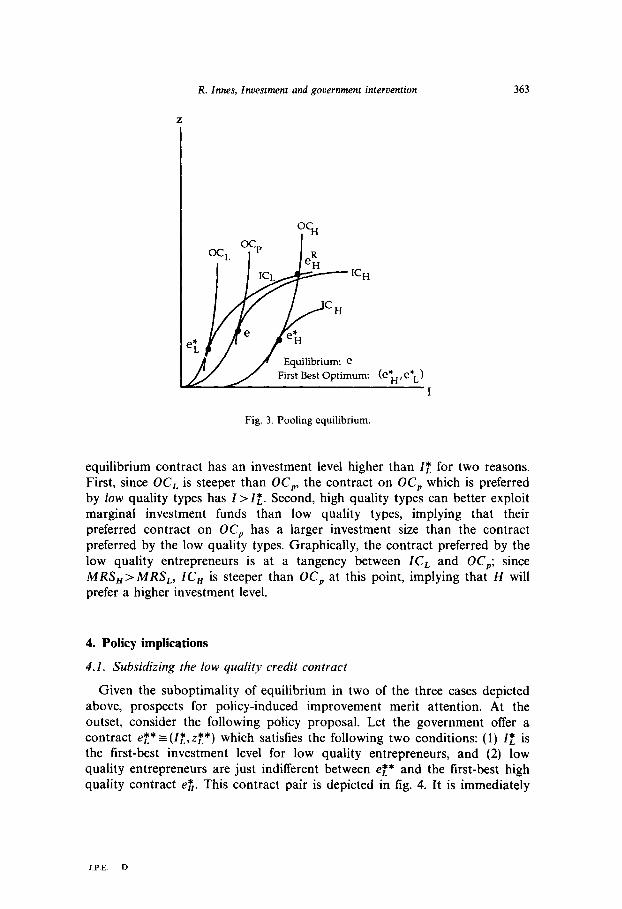

For a world of asymmetric information, fig. 1 illustrates the set of high quality contracts that satisfy the feasibility constraints (El)-(E3) (recalling the characterization of equilibrium in section 2). Since contracts below IC, are preferred by the low quality type to his own perfect information (tirst- best) contract, any high quality contract in this region must be on or above OC,. In contrast, a high quality contract above ZC, does not attract low quality entrepreneurs and, hence, must only be on or above OC,. By the definition of a Wilson Allocation in section 2, the equilibrium high quality contract will be the point on the boundary of the constraint set which is on the lowest high quality indifference curve and, thus, is most preferred by this type of entrepreneur. If this point is on OC,, the contract will be pooling (as in fig. 3). Otherwise, the contract will be separating (as in figs. 1 and 2). Fig. 2 depicts the case of a ‘suboptimal’ separating equilibrium in which the low quality incentive compatibility constraint is strictly binding in that the high quality type prefers an infeasible point on OC,,es. In contrast, fig. 1 depicts

R. Innes, Investment and government intervention

- Boundary of the Constraint Set

/// Equilibrium and First Best Optimum:

Fig. 1. Pareto optimal separating equilibrium.

Z

First Best Optimum: (e*H,e*L) I

Equilibrium: (e H,e*L)

361

Fig. 2. Suboptimal separating equilibrium.

362 R. Innes, Znoestment and government intervention

a case in which both quality types obtain their perfect information contracts.i4’i5

With respect to efliciency, an important attribute of an equilibrium allocation is its deviation from the ‘first-best’ (perfect information) set of contracts.16

Proposition 1. In a suboptimal separating equilibrium (see fig. 2), (1) low quality entrepreneurs invest at their ‘first-best’ level, and (2) high quality entrepreneurs invest more than with their tfirst-best’contract.

Proposition 2. In a pooling equilibrium (see fig. 3), (1) low quality entrepre- neurs invest more than with their ‘first-best’ contract, and (2) high quality entrepreneurs invest less than with their tfirst-best’ contract.

Proposition 1 gives an outcome similar to those found in the rat-race and education-signaling literatures; high quality entrepreneurs over-invest in order to distinguish themselves from low quality entrepreneurs.

However, Proposition 2 has a different logic. In a pooling equilibrium the high quality entrepreneur is choosing his preferred contract on the pooling offer curve, OC,. Loosely speaking, this preferred contract has an investment level lower than I& the ‘first-best’ high quality investment choice, because OP, is steeper than OC,, g iving the high quality entrepreneur a greater disincentive to invest than in a perfect information world. The pooling

“Graphically, it is clear that a fig. 3 case is favored when (i) the separating offer curves, OC,_ and OC,, are far apart, (ii) the indifference maps of high and low quality types are similar, and (iii) the pooling offer curve, OC,, is close to OC,. The first condition is implied by large inter-quality differences in default risks. The second is implied by inter-quality differences in marginal investment returns which offset differential default risks to produce similar investment/ promised payment tradeoffs. The third condition is implied by a small proportion of low quality entrepreneurs in the applicant population. Likewise, a fig. 1 case is favored by small inter-quality differences in default risks and large differences in marginal investment returns. A fig. 2 case is favored by intermediate conditions.

r5Riley (1979) ‘reactive’ outcomes (footnote 11) differ from a Wilson allocation only in the pooling case of fig. 3. In this case, the Riley allocation contains the separating contracts, (et,e$), which are Pareto inferior to the Wilson contract, e.

16Though p is fixed in the background here, Propositions 1 and 2 are easily extended to a ‘large’ sector model in which p responds to changes in investment. To generalize Proposition 2, consider two cases: (1) p is lower at the ‘first best’, and (2) p is higher at the ‘first best’. Condition (1) implies that (i) entrepreneurial investment is lower overall in the perfect information case (assuming an upward-sloping supply of funds), and (ii) optimal investment levels, Zy and Zb, are higher than when p was held fixed. Owing to (ii), high quality under-investment is greater than when p was fixed; hence, in order for (i) to hold, the low quality entrepreneur must still over-invest, affirming the proposition. Similar reasoning applies to case (2). To generalize Proposition 1, note first that p must be lower at the ‘first best’; if it were higher, Zt and Z$, would be lower than with p held fixed, implying greater over-investment overall and, thus, the contradiction of a lower ‘first-best’ p. With lower p, comment (ii) above implies under-investment by low quality entrepreneurs; hence, in order for (i) to hold, high quality agents must still over-invest.

R. Innes, Investment and government intervention 363

Z

First Best Optimum: (e*,,e*,,) I

Fig. 3. Pooling equilibrium.

equilibrium contract has an investment level higher than 12 for two reasons. First, since OC, is steeper than OC,, the contract on OC, which is preferred by low quality types has I > 12. Second, high quality types can better exploit marginal investment funds than low quality types, implying that their preferred contract on OC, has a larger investment size than the contract preferred by the low quality types. Graphically, the contract preferred by the low quality entrepreneurs is at a tangency between ICL and OC,; since MRS,> MRS,, IC, is steeper than OC, at this point, implying that H will prefer a higher investment level.

4. Policy implications

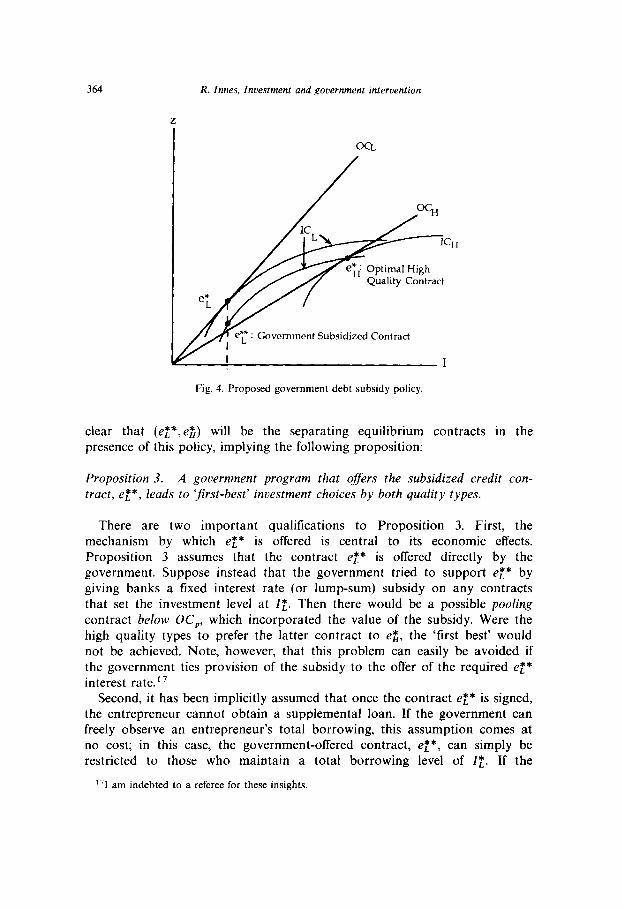

4.1. Subsidizing the low quality credit contract

Given the suboptimality of equilibrium in two of the three cases depicted above, prospects for policy-induced improvement merit attention. At the outset, consider the following policy proposal. Let the government offer a contract eE* =(I:, zE*) which satisfies the following two conditions: (1) 1: is the first-best investment level for low quality entrepreneurs, and (2) low quality entrepreneurs are just indifferent between eC* and the first-best high quality contract et. This contract pair is depicted in fig. 4. It is immediately

J.P.E. D

364 R. Innes, Investment and government intervention

Fig. 4. Proposed government debt subsidy policy.

clear that (eZ*, f e ) will be the separating equilibrium contracts in the presence of this policy, implying the following proposition:

Proposition 3. A government program that offers the subsidized credit con- tract, ez*, leads to ‘jirst-best’ investment choices by both quality types.

There are two important qualifications to Proposition 3. First, the mechanism by which eE* is offered is central to its economic effects. Proposition 3 assumes that the contract ez* is offered directly by the government. Suppose instead that the government tried to support et* by giving banks a fixed interest rate (or lump-sum) subsidy on any contracts that set the investment level at 1:. Then there would be a possible pooling contract below OC,, which incorporated the value of the subsidy. Were the high quality types to prefer the latter contract to e$, the ‘first best’ would not be achieved. Note, however, that this problem can easily be avoided if the government ties provision of the subsidy to the offer of the required ez* interest rate.i7

Second, it has been implicitly assumed that once the contract eE* is signed, the entrepreneur cannot obtain a supplemental loan. If the government can freely observe an entrepreneur’s total borrowing, this assumption comes at no cost; in this case, the government-offered contract, er*, can simply be restricted to those who maintain a total borrowing level of 1:. If the

I’1 am indebted to a referee for these insights.

R. Innes, Investment and government intervention 365

government cannot monitor total borrowings and eE* is below OC,, then high quality entrepreneurs will also want to take the subsidized contract and, most likely, supplement it with additional borrowing.” In this case, a ‘first best’ will not be achieved. l9 Note, however, that this problem can also be avoided if the government itself offers both eZ* and e& and levies large taxes on any private contracts.

Abstracting from these issues, Propositions l-3 imply that the govern- ment’s offer of the subsidized contract, eZ*, will lead to a lower (and first-best) low quality investment level and a higher (first-best) high quality investment level if the original no-intervention equilibrium is of the pooling (fig. 3) variety. If the no-intervention equilibrium is of the separating (fig. 2) type, the subsidy policy will lead to a lower (first-best) high quality investment level. The latter qualitative implications extend naturally to a market with Q> 2 quality types. For example, in a fully separating equili- brium, the offer of a subsidized credit contract to the lowest quality entrepreneur will permit less over-investment by all other quality types.

However, the sense in which the foregoing subsidy policy is ‘optimal’ remains a bit murky. Clearly, the policy achieves ‘efficient’ investment choices

Fqg(t& cls”-“sf, $;;’ aggregate expected net firm profits [i.e.

are maximized. The latter attribute could be called ex-post o’ptimality, with optimality implicitly based on a willingness to pay (or potential compensation) criterion. The importance of the label ‘ex post’ is evident from the observation that the subsidized debt contract, et*, must be financed by ‘expected taxes’ on some agents. If the welfare criterion for policy evaluation is the Hicks compensation standard, then the appropriate question to ask is: Can a compensation/tax program be constructed such that, with the policy and compensation, all agents are at least as well off as before and some agent is strictly better off? If the answer is yes, the policy is ex ante welfare improving.

Unfortunately, it is not a priori evident that the subsidized debt program satisfies the latter criterion. For example, suppose that a large proportion of the entrepreneurial population is low quality and that high quality entrepre- neurs’ gains from the policy (without taxes) are not very large. Since taxes on high quality agents are constrained by the requirement that the entrepre- neurs’ pre-policy utilities be preserved, they cannot be very high. Moreover, taxes on low quality agents are constrained to be incentive compatible; that is, they cannot be so high that low quality agents would prefer to

‘*If eZ* is above OC,,, then OC, will give the high quality entrepreneurs better loan terms than are possible with et* and supplemental borrowing. Therefore in this case, the high quality types will not take eZ*.

“In fact, it can be shown that the equilibrium in this case will either be pooling (with the same qualitative properties as given in Proposition 2) or separating (with high quality over-investment).

366 R. Innes, Investment and government intervention

Pre-policy equilibrium: e

First-best optimum: ($, et)

Post-policy contracts with maxima1 taxes: (eH eL 1

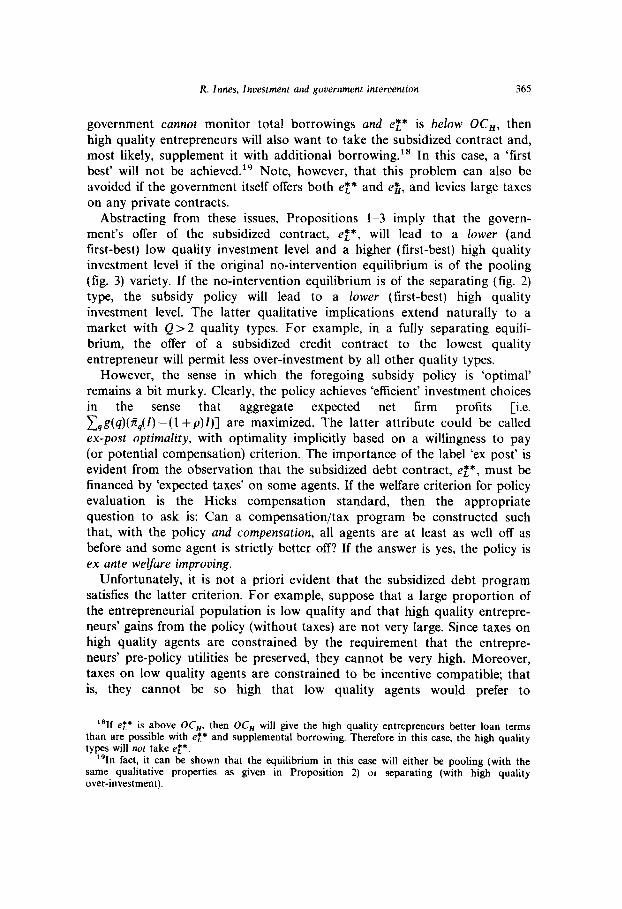

Fig. 5. Debt subsidy and taxation in a pooling equilibrium.

masquerade as high quality. Thus, with a high proportion of low quality types and an associated high program cost, utility-preserving and incentive- compatible taxes will not be able to finance the debt subsidy policy. While leading to a Pareto optimum ex post, the policy will not be ex ante welfare improving.

To investigate the prospective conflict between ex ante and ex post welfare criteria further, note that, owing to the reasoning given in subsection 2.7, optimal taxes will take the form of additional promised payments.” In other words, an entrepreneur will simply face a higher z with taxes than without and the ‘ex ante’ welfare question posed here boils down to a question of whether government can find a set of incentive-compatible debt contracts which Pareto dominates the competitive equilibrium.

To address this question for the fig. 3 (pooling) case, consider the two points on the high and low quality indifference curves, through e (the equilibrium), at the respective first-best investment optima (see fig. 5). Owing to Proposition 2 [and eq. (7)], these contracts are incentive feasible; that is, neither quality prefers the other’s contract to his or her own. Moreover, with

‘OBoth optimal financial contracts and optimal taxes are designed to foster screening. Since debt-type payoff functions minimize the low quality entrepreneurs’ incentive to masquerade, optimal tax/ftnancial contracts take this form.

R. Innes, Investment and government intervention 367

Z

Pre-policy equilibrium: (eH, e: )

First-best optimum: ($, e*L)

Post-policy contracts with maximal taxes: (a, ed

Fig. 6. Debt subsidy and taxation in a separating equilibrium.

these contracts, both entrepreneurs receive the same expected profit as at e, but total expected profit has risen. Thus, expected tax revenues are greater than program costs and the debt subsidy policy is ex ante optimal.

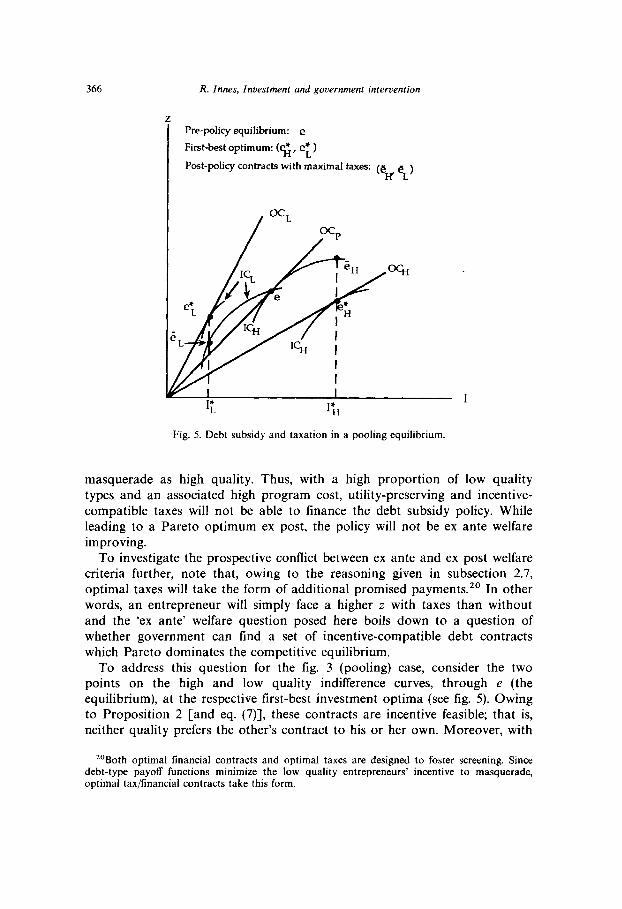

For the fig. 2 case (separating), note that higher quality taxes (or, equivalently, higher z) will permit higher low quality taxes by relaxing the incentive-compatibility constraint. Thus, to evaluate the ex ante optimality of the proposed debt subsidy policy, the first step is to maximize the post-policy high quality z subject to utility preservation; this maximal z will be denoted ZH (see fig. 6). The second step is to find the associated maximal low quality z, ZL, consistent with the self-selection constraint. Now let P~=(I$,Z~) and Cr,-(IZ‘ZJ denote the post-policy contracts with maximal (utility-preserving and incentive-compatible) taxes and let et ~(12,~:) and eg=(Zg,zz) repre- sent the perfect information contracts. Then under the proposed subsidy policy the net expected transfer from government to a low quality entrepre- neur will be (BL(~J--BB,(e~)) and the tax on each high quality entrepreneur will be (Bde$)-B,(ZH)). The necessary and suffkient condition for ex ante optimality of the proposed policy can thus be stated as follows:

368 R. Innes, Investment and government intervention

In the circumstances described earlier [i.e. high g(L) and a low gain to high quality entrepreneurs from moving to the first-best contract], (10) will be violated, confirming the above intuition.

Nevertheless, there is a wide variety of circumstances under which either a pooling equilibrium emerges or (10) will be satisfied. In these circumstances the debt subsidy policy proposed here, complimented by compensating taxes, will lead to Pareto improvements.21

The scope for Pareto improvement begs the following question: If govern- ment can make everyone better off, why are private agents unable to do so? The answer derives from an important attribute of the competitive process described in section 2. Specifically, each and every contract must earn investors non-negative expected profits in equilibrium. This outcome of competition, while intuitively compelling, places a constraint on private agents’ contract choices which the government can relax. In particular, government can support cross-subsidized contracts, one of which earns negative expected profits and the other of which earns positive expected profits. For example, consider the cross-subsidized contracts (pH,CL) in fig. 5. One policy that would support these contracts is a direct government offer of (c?~,E~), accompanied by a large tax on any offers by private investors. Hence, while government has neither an informational advantage over private investors nor an ability to offer any payoff function form unavailable to private agents, it is not constrained by the dictates of competition.

4.2. Optima&y properties of other interventions

Some government credit market interventions take a form analogous to that described above, namely the direct offer of a subsidized credit contract (i.e. ez*). However, other typical interventions do not take this form. The remainder of this section seeks to characterize the optimality properties of these other interventions, namely loan guarantees, grants to entrepreneurs and subsidies to targeted lending institutions. This investigation focuses primarily on ‘ex post’ efficiency in that it is concerned with Pareto improvement from the equilibrium which a particular intervention elicits. If no such improvement is possible, the equilibrium is said to be constrained efficient. The following feature of constrained efficient allocations will provide a useful benchmark for this inquiry.

‘llt is assumed here that rr(q,A,@) does not depend on equilibrium investment choices of other quality types and other indicator (e.g. wealth) classes. If a set of debt subsidy policies affects a whole sector and the sector is large in either an input or an output market, the policy will affect the prolit relation. Nevertheless, one can think of the curves in figs. l-4 as those associated with equilibrium net worth relations in a perfect information economy. The policy proposed in fig. 4 then leads to a &t-best outcome, implying ex post optimality. Unfortunately, the question of ex ante optimality in this more general setting is not so easily resolved and must be left to future research.

R. Innes, Investment and government intervention 369

Lemma 3. Any constrained efficient allocation entails separation. Further- more, any constrained eflcient allocation with the following property sets low quality investment at its first-best level: the high quality entrepreneur strictly prefers his own contract to the low quality contract.

Fom arguments analogous to those made above (see fig. 5) Pareto improvements are possible from any pooling contract, implying the first part of Lemma 3. The second part of the lemma can be established by finding a Pareto dominant alternative to any separating set of contracts with a non- first-best low quality investment level and a slack high quality selection constraint. This alternative can be found by replacing the low quality contract with another that is on the same low quality indifference curve and closer to I:; the latter contract preserves incentive compatibility and the low quality entrepreneur’s profits while increasing the payoff to investors.

It should be pointed out that given the definition of a Wilson Allocation, the ‘slack high quality selection constraint’ condition in Lemma 3 will be satisfied in any of the pre- or post-intervention equilibria of interest here.

4.2.1. Loan guarantees A government loan guarantee program provides investors with an assur-

ance that the government will make up any difference between a given guaranteed loan payment and an entrepreneur’s actual loan payment. For example, suppose the government offers to guarantee loans of size no greater than L*. Then, if an entrepreneur borrowers 15 L*, the bank offering this loan is guaranteed a payment of (1 +p)l. On the other hand, if an entrepreneur borrows I > L*, the unguaranteed portion of the loan, Z-L*, is junior (in order of payment) to the guaranteed portion of the loan. Therefore the government will give the bank any positive difference between the guaranteed loan payment, (1 +p)L*, and the entrepreneur’s profits, rr. The bank will thereby receive the guaranteed amount, (1 + p)L*, whenever the entrepreneur’s profits are less than this amount; otherwise, the bank will simply receive the entrepreneur’s payment, min (rr, z).

In what follows it will be assumed that provision of a government loan guarantee is not contingent on an entrepreneur’s choice of investment. This assumption comes at no cost in generality if the government cannot freely observe the entrepreneur’s investment choice.22 Without this restriction the government could do the following: (i) make the loan guarantee available only to entrepreneurs who set I =I:, and (ii) set L* < Zz in such a way that

“However, the government must be able to restrict an entrepreneur to one guaranteed loan. Otherwise it could not enforce any maximum on the guaranteed loan size.

370 R. Innes, Investment and government intervention

banks are willing to offer low quality entrepreneur’s the contract et* (see fig. 4). The latter policy is equivalent to that analyzed in subsection 4.1 above.

Given this assumption, a guaranteed loan size of L* elicits separating investor offer curves that satisfy the following equation (after integration by parts):

OC,( L*): z=(l +p)Z, VIILL*,

z-S;,+,,,.F(~lZ,q)d7C=(l+P)Z, VZ>L*. (11)

While the loan guarantee program changes investors’ offer curves, it does not change entrepreneurs’ indifference curves. Under the program, the government simply absorbs some of the default cost implicit in entrepreneurs’ investment choices, leading, in general, to inefficient distortions in investment choice incentives.

To characterize these distortions, I will focus first on entrepreneurs’ perfect information investment levels with a loan guarantee policy. Defining Zz as the first best investment for a quality q entrepreneur and Z&L*) as the quality q perfect information investment choice with a guaranteed loan size of L*, the following lemma can be derived:

Lemma 4. (a) L* < Z,*oZ,( L*) < 1:; (b) L* > Z,*oZ,(L*) > 1;; (c) L*=Z,*oZ,(L*)=Z,*.

To gain an intuitive appreciation for Lemma 4, consider the move from the separating offer curve without government intervention, OC,(O), to that with a loan guarantee program, OC,(L*). For Z<L*, the slope of the new offer curve, OC,(L*), is (1 +p), which is less than the slope of the original curve, OC,(O), owing to Lemma 1. However, for I> L*, the loan guarantee offer curve is steeper. Loosely speaking, this relationship is attributable to the following observation. Without a loan guarantee program, marginal entrepre- neurial investment at Z = L* gives the investor the benefit of reducing the risk of default on the original (pre-marginal-investment) loan; with a loan guarantee program, this investor benefit is absent, implying that a greater increase in promised payment is necessary to yield the investor his required return. The same reasoning applies to marginal investment costs when Z is larger than L*.

Since OC,(L*) is flatter than OCJO) for Z < L*, the loan guarantee program gives the entrepreneur a greater incentive to raise Z in this region [implying

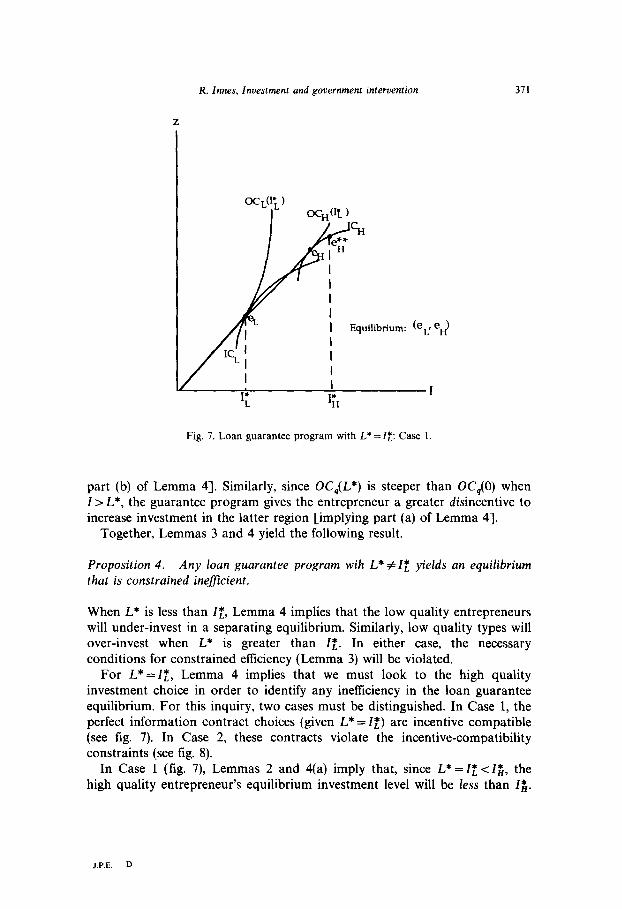

R. Innes, Investment and government intervention 371

Z

e*+ P $I

IH I I I I 1 Equilibrium: (eLJ eH)

I

Fig. 7. Loan guarantee program with L* = 1:: Case 1.

part (b) of Lemma 41. Similarly, since OC,(L*) is steeper than OC,(O) when I> L*, the guarantee program gives the entrepreneur a greater disincentive to increase investment in the latter region [implying part (a) of Lemma 41.

Together, Lemmas 3 and 4 yield the following result.

Proposition 4. Any loan guarantee program wih L* # 1: yields an equilibrium that is constrained inefjcient.

When L* is less than I:, Lemma 4 implies that the low quality entrepreneurs will under-invest in a separating equilibrium. Similarly, low quality types will over-invest when L* is greater than 12. In either case, the necessary conditions for constrained efficiency (Lemma 3) will be violated.

For L* =I;, Lemma 4 implies that we must look to the high quality investment choice in order to identify any inefficiency in the loan guarantee equilibrium. For this inquiry, two cases must be distinguished. In Case 1, the perfect information contract choices (given L* = 12) are incentive compatible (see fig. 7). In Case 2, these contracts violate the incentive-compatibility constraints (see fig. 8).

In Case 1 (fig. 7), Lemmas 2 and 4(a) imply that, since L* = ZE <I$, the high quality entrepreneur’s equilibrium investment level will be less than Zb.

J.P.E.- D

372 R. Innes, Investment and government intervention

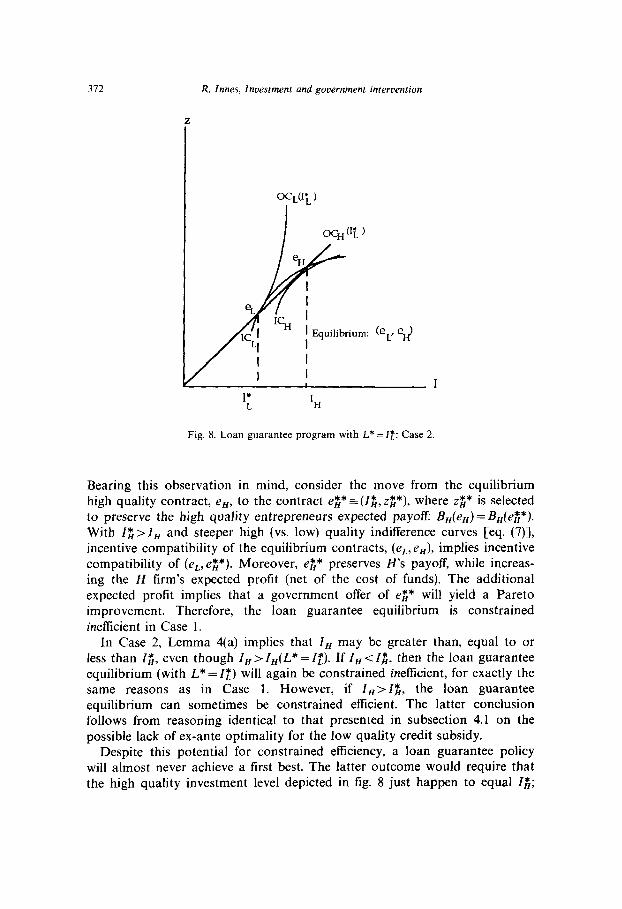

Fig. 8. Loan guarantee program with L* = 12: Case 2.

Bearing this observation in mind, consider the move from the equilibrium high quality contract, eH, to the contract e;C* =(Zg, zg*), where z$* is selected to preserve the high quality entrepreneurs expected payoff: B,(e,) = B,(e$*). With lg>Z, and steeper high (vs. low) quality indifference curves [eq. (7)], incentive compatibility of the equilibrium contracts, (e,, e,), implies incentive compatibility of (e,,eP). Moreover, ez* p reserves H’s payoff, while increas- ing the H firm’s expected profit (net of the cost of funds). The additional expected profit implies that a government offer of e$* will yield a Pareto improvement. Therefore, the loan guarantee equilibrium is constrained inefficient in Case 1.

In Case 2, Lemma 4(a) implies that I, may be greater than, equal to or less than Zs, even though I, > Z,,(L* = Zz). If I, < I$, then the loan guarantee equilibrium (with L*=Iz) will again be constrained inefficient, for exactly the same reasons as in Case 1. However, if I,> Zg, the loan guarantee equilibrium can sometimes be constrained efficient. The latter conclusion follows from reasoning identical to that presented in subsection 4.1 on the possible lack of ex-ante optimality for the low quality credit subsidy.

Despite this potential for constrained efficiency, a loan guarantee policy will almost never achieve a first best. The latter outcome would require that the high quality investment level depicted in fig. 8 just happen to equal I$;

R. Innes, Investment and government intervention 313

this condition is not only unlikely to hold, but is also sensitive to the slightest change in the technological specification.

In summary, loan guarantees yield constrained inefficiency whenever L* # 1: and in a wide spectrum of cases otherwise. In addition, a ‘first-best’ equilibrium can almost never be produced by any intervention of this kind.

4.2.2. Government grants to entrepreneurs

Instead of providing investors with a guarantee on entrepreneurial loans, government can offer entrepreneurs a grant of K dollars payable at the end of the period. Added into firm profits, the grant would be available to pay investors, thereby reducing default risk. It is easy to see that the effects of such a grant are very different from those of a loan guarantee program. First, a grant does not alter entrepreneurs’ perfect information investment choices, regardless of the level at which K is set; with a grant and perfect information, a quality 4 entrepreneur will choose his investment to maximize n,(Z)- (1 +p)Z +K, yielding a choice, I,*, which is invariant to K.

Second, by reducing disparity in the loan terms that investors are willing to offer different quality types, a government grant reduces low quality types’ incentive to masquerade and can, therefore, lead to first-best outcomes. For example, if K were set as high as (1 + p)Zz, the separating offer curves facing high and low quality entrepreneurs would be identical for all I SZg; in this case, there would be no incentive for adverse selection and a first-best equilibrium would emerge.

More generally, define K* as the minimum government grant that leads entrepreneurs to choose their first-best investment levels in equilibrium. Then the following proposition holds.

Proposition 5. K* exists and is less than (1 +p)Zg. Furthermore, for

KE [O,K*), increases in K reduce the investment level that high quality entrepreneurs must undertake in order to signal their type.

Thus, grants to entrepreneurs can push the market closer to a first best and, if sufficiently large, will achieve a first-best outcome.

4.2.3. Investment subsidies

Another common form of government credit market intervention is a backing of targeted lending institutions by the state treasury. For example, the U.S. Farm Credit system has at least the implicit support of the U.S. government, permitting it to issue bonds at an interest rate only very slightly above Treasury security yields. Effectively, this support lowers the oppor-

374 R. Innes, Investment and government intervention

tunity cost of funds to the lender, p.23 The following proposition describes an important implication of this type of policy measure.

Proposition 6. Any government subsidy of the opportunity cost of funds, p, yields an equilibrium that is constrained inefficient.

As with loan guarantees, investment subsidies uniformly improve the loan terms available to entrepreneurs without altering their indifference mappings. Unlike loan guarantees, investment subsidies also uniformly reduce the entrepreneurs’ cost of marginal investment. As a result, low quality over- investment is inevitable with this type of intervention, implying (with Lemma 3) constrained inefficiency.

Despite this constrained inefliciency result, DeMeza and Webb (1989) show that an investment tax can sometimes have a desirable optimality property. In particular, when the competitive equilibrium is pooling, some tax on p will increase aggregate expected profits (net of the opportunity cost of funds). This interesting result is attributable to the ‘over-investment’ mentioned in the Introduction, namely a competitive level of borrowing that exceeds the level which, given pooling behavior, is most efficient. The results here, in contrast, reflect the government’s ability to support separating equilibria that Pareto dominate the best possible pooling allocation.

4.3. Financing government interventions

In the above discussion of alternative policy regimes, it has mostly been assumed that the government takes a loss on its interventions. If these interventions must instead be financed by a parallel tax program, the choice of tax mechanism will affect contractual outcomes. However, the simplest possible tax regime turns out to have no effect on equilibrium contract choices, implying that a balanced government budget constraint alters none of the foregoing results. This regime is as follows: a constant proportional tax on entrepreneurs’ net profits (after they have received any government grant and made their required loan payment). Such a tax alters neither indifference curves nor offer curves, thereby preserving the pre-tax equilibrium.

5. Summary and conclusion

In a credit market characterized by asymmetrically informed entrepreneur/ borrowers and lenders, this paper has analyzed entrepreneurs’ investment choices and the effects of standard government interventions, including the

Z31t is assumed here that targeted lenders pass the targeted subsidies on to borrowing entrepreneurs. The cooperative structure of the U.S. Farm Credit System will elicit this ‘competitive’ behavior, as will the availability of the subsidies to more than one lender.

R. Innes, Investment and government intervention 375

direct offer of subsidized credit contracts, loan guarantees, grants to entrepre- neurs, and subsidies to targeted lending institutions.

In contrast to some similar research on over- and under-investment in credit markets [e.g. DeMeza and Webb (1987, 1988) and Mankiw (1986)], this analysis permits entrepreneurs to choose their loan size and to signal their quality type by this choice. As a result, the nature of any deviation from a ‘first-best’ (perfect information) outcome is fundamentally different here than in ‘fixed investment’ models. There, inefficiency can be attributed to either banks’ rejection of some good loan applications (e.g. Mankiw) or their acceptance of some bad ones (e.g. DeMeza and Webb). Here, it is not the loan applications that are ‘good’ or ‘bad’ per se, but rather the investment choices that are ‘too high’ or ‘too low’ relative to what they would be with perfect information. For example, high quality entrepreneurs often over- invest (relative to a first best) in order to signal their type. Alternatively, if the cost of this over-investment is too high, a pooling equilibrium will emerge in which high quality types under-invest (because of higher ‘pooled’ interest rates) and low quality types over-invest (in order to conceal their

type). In principle, government intervention can improve matters here; by

subsidizing the low quality entrepreneurs, the latter agent’s incentive to mimic high quality types can be reduced, thereby permitting self-selection with first-best invstment choices. However, the foregoing analysis shows that some typical forms of government credit subsidization, though promoting self-selection, tend to distort investment choice incentives in inefficient ways. Loan guarantees, for example, increase entrepreneurs’ incentive to borrow and invest when the investment level is less than the guaranteed loan size; at higher investment levels, guarantees decrease the incentive to borrow and invest. As a result, it is almost always impossible to find a guaranteed loan size that will support a first-best choice by all quality types; and, in most cases, it is even impossible for a loan guarantee program to support a ‘second-best’ (constrained efficient) outcome. Similar problems arise with subsidies to targeted lending institutions, but not with either grants to entrepreneurs or the government offer of a specific subsidized credit contract that is designed to attract low quality borrowers.

Arguably the strongest assumption made in this analysis is that of a positive relationship between quality and an entrepreneur’s ‘willingness to pay’ (in terms of promised loan payment) for marginal investment funds. To determine the importance of this assumption, it is reversed in an expanded version of this paper. Not surprisingly, this reversal can lead to fundamental changes in the equilibrium, such as high quality agents’ signaling by under- investment [see Milde and Riley (1988)]. However, the spirit of the above policy conclusions is found to persist in this altered environment. For example, the offer of subsidized credit contracts can still reduce low quality

376 R. Innes, Investment and government intervention

entrepreneurs’ incentive to masquerade, permitting either screening at efficient investment choices or the emergence of an efficient pooling equili- brium. Likewise, grants still reduce adverse selection incentives and thereby promote optimal investment behavior. Loan guarantees and subsidies to targeted lenders also retain their distortionary attributes in the altered setting, generally (though not always) precluding ‘first-’ or ‘second-best’ outcomes.

In essence, the policy implications derived here are motivated by a desire to promote inexpensive signaling without distorting investment choice incen- tives; these considerations do not depend, fundamentally, on the direction of inter-quality differences in marginal investment returns.

In closing, an important limitation of the analysis merits comment. Throughout, this paper has examined a closed market in which the only quality types present are those that can invest some funds profitably. In some settings (such as those with sufficiently high costs of entry for ‘lemons’), such a specification is plausible in both the short and long run.24 However, it is easy to think of settings in which ‘lemons’ respond to favorable pooling equilibria or government support programs by eventually entering the market. The latter phenomenon would imply a dual objective of government policy, namely to promote inexpensive self-selection and simultaneously discourage the entry of inefficient entrepreneurs. One can envision cases in which both objectives would be served by some of the policy interventions suggested above. For example, suppose a lemon-ridden pooling equilibrium emerges in an unfettered competitive market with three quality types (lemon, low, and high). Then the government’s offer of the utility-preserving contracts shown in fig. 5 (i.e. 2, and ZH) would not only have the desirable effects described in section 4; it would also reduce or eliminate investment by lemons. However, one can also envision cases in which government subsidies designed to reduce low quality entrepreneurs’ adverse selection incentives have the unfortunate side-effect of eliciting lemons’ participation in the market. It is hoped that future research will formally investigate these issues, characterizing the tradeoffs created by the possibility of entry and analyzing their effect on both the investment choice process and government’s policy

environment.

Appendix

Proof of Proposition 2. Define qualities between H and L by the parameter UE [O, l] such that

f(n 11, q(4) = af(n ) 1, L) + (1 - 4.0~ ) 1, W,

Z4Agriculture is arguably a sector that satisfies this condition.

R. Innes, Investment and government intervention 371

where q(0) = L, q( 1) =H, and q’(o) >O. Now note that from the investor’s point of view, the pooling case is equivalent to having an applicant with quality q(g(L)). Thus, a pooling equilibrium must be the high quality entrepreneur’s preferred contract on OC,(,(,,,. To characterize this equili- brium, consider the following high quality maximization problem:

max B,(Z, z,(Z)), where z,(Z): (z, I) E OC,. (‘4.1) I

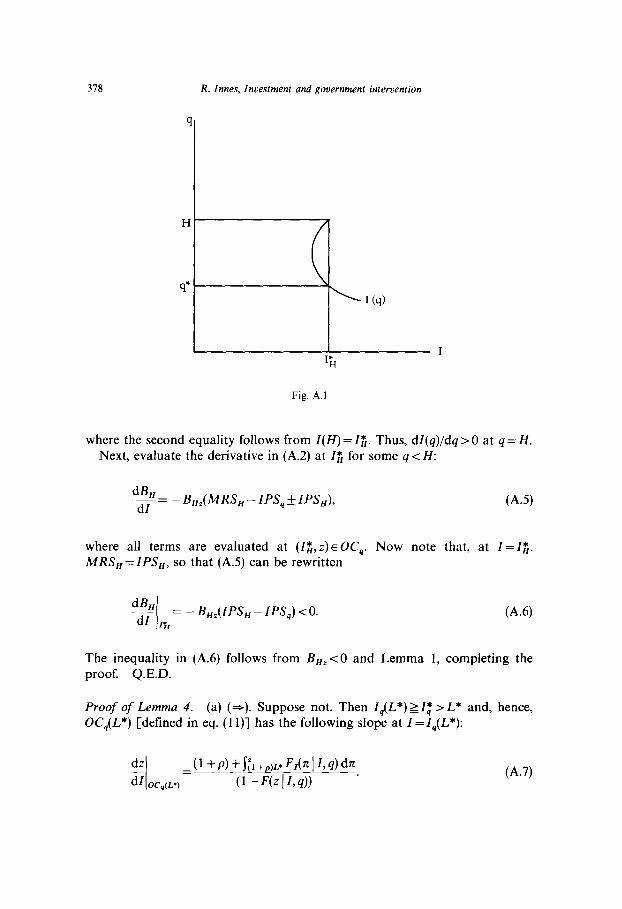

The solution to (A.l) will be denoted Z(q), which solves

d&A.) ---=~,,(~)+~,,(~)~zPS,( )= -&(.) dl

(A.3

evaluating all terms at (I, z,(Z)). To establish property (l), evaluate the right-hand side of (A.2) at 15 Zz. At

any such point, 71;--( 1 + p) 20 and, owing to Lemma 2, ?& -( 1+ p) > 0, implying 5; - (1 + p) > 0. Thus, given B,, = - (1 - F(z ( I, q)) < 0 and eq. (7), d&(.)/dZ > 0 when Z 5 Zt, implying that Z(q) > 12.

The derivation of property (2) proceeds in two steps. First, using (A.2) dZ(q)/dq will be expressed and shown to be positive at q=H. The latter positive sign implies that the solution to (A.l), Z(q), decreases when moving from q = H to q = H--E. Given continuity of Z(q), it also implies that, in order for Z(q) 2Z$ for some q < H, there must be a q* < H such that Z(q*) = Zj!, (see fig. A.l). But the second part of the proof shows that Z(q) # Zg for any q < H, implying that Z(q) < Z;“I, Vq < H. In particular, Z(q(g(L))) < If, the desired result.

To begin, differentiation of (A.2) yields:

!w=s!!c~. __f__~ 4 aMRS ( ) alps ( ) dq W4d) aZ aZ 1

(A.3)

where k(Z(q)) >O from the second-order condition for (A.l). To sign (A.3) at q = H, recall that B,, < 0 and, from Lemma 1, dZPS,( .)/iYq ~0. Expanding the remaining term at q = H,

(A.4)

378 R. Innes, Investment and government intervention

Fig. A.1

where the second equality follows from Z(H) =I;. Thus, dZ(q)/dq>O at q=H.

Next, evaluate the derivative in (A.2) at II: for some q < H:

dS,_ dl

- - B,,(MRS, - IPS, f ZPS,,), (A.9

where all terms are evaluated at (Zg,z) E OC,. Now note that, at Z=Zs. MRS,=ZPS,, so that (A.5) can be rewritten

dB, dz rh

= - B,,(ZPS, - ZPS,) < 0. (A-6)

The inequality in (A.6) follows from B,,<O and Lemma 1, completing the proof. Q.E.D.

Proof of Lemma 4. (a) (a). Suppose not. Then Z,(L*)zZr > L* and, hence, OC,(L*) [defined in eq. (1 l)] has the following slope at Z=Z,(L*):

dz

ii = (I+ P) + j;~ +p)~* F,(n 11, d dn

O&&L*) u-Fbp4d) . (A.7)

R. Innes, Investment and government intervention 319

Given (A.7), Z,(L*) must satisfy the following first-order condition for the q-type entrepreneur’s investment choice [defining z(Z): (I, z(Z)) E OC,(L*)]:

(1 +px* =[qz)-(l+p)]+ j F,(n:Ikq)d~=O.

0 64.8)

But if Z 2 Zz, then r?;(Z) s( 1+ p) and (A.8) will be violated, a contradiction. (b) (a). Suppose not. Then Z,(L*)zZ,“< L* and OC,(L*) has a slope of

(1 +p) at Z =I&!,*). Thus, the investment choice first-order condition is as follows:

dB,(Z, z(Z))

dZ =(l-F(z(z,q)){MRS,(Z,z)-(1+P)~=O~

Rewriting the derivative in (A.9):

dS’$;r(z)) = ( 1 - F(z 1 I, q)) { MRS,(Z, z)

=(7?;(z)-(1+p)}+(1-F(z

(A.9)

‘(z,q))~{zPsq(z,z)-(l+P)~‘o~

(A.lO)

where the inequality follows from Z,(L*) SZt and Lemma 1. Since (A.lO) contradicts (A.9), the supposition must be false.

(c) (3). If Z,(L*) >I:, then the foregoing arguments imply that (A.8), the relevant first-order condition, is violated, Likewise, if Z,(L*)<Z:, then the relevant first-order condition, (A.9), is violated.

(e) Suppose Z,(L*) < Z:+L* < Zz, violating (a)(-=). Then, for some (L*, I$): Z,(L*) < Zr, L* 2 Z:. But the latter inequality implies (from (b)(a) and (c)(a)) that Z,(L*) IZ:, a contradition. Symmetric contradictions prove Lemma 4 (b)(G) and (c)(t). Q.E.D.

Proof of Proposition 5. The first statement is obvious from the discussion in subsection 4.2.2. To prove the second statement, note that, given a grant of K E (0, K*), the high quality contract required for self-selection is character- ized by the following incentive-compatibility [(E.2)] and investor return requirement [(E. l)] conditions:

380 R. Innes, Investment and government intervention

f&(1:)-(1 +p)Z;+ K =B,(Z,,z,- K), (A.1 la)

K+71H(Z8)-BBH(ZH,~N-K)-(l +p)Z,=O. (A.llb)

Totally differentiating (A.1 1) with respect to Z,,z, and K, using Cramer’s Rule and simplifying, we obtain:

d’g =~.{g,,(Z,,z,--K)--B,,(z,,z,--K)) dK IAl

=~.(F(z,,-KI~,,,H)-F(z,-K~I,,L)J,

where

(A(~B,Z(.).B,,(.).(CMRS,(.)-MRS,(.)l

(A.12)

+ C(fwH) -Cl +P))lbfz(~)l~>

with all terms evaluated at (Z,,z, - K). The following relations imply (A( >O: (i) II& ) < 0; (ii) MRS, > MRS, from eq. (7); and (iii) by the construction of K*, I, > I;, implying &(Z,) - (1 + p) < 0. [If I, were less than or equal to Zz, then K (which is less than K*) would yield a first best equilibrium, contradicting the definition of K*.] Thus, since F,() <0 from eq. (l), dZ,/dK in (A.12) is negative. Q.E.D.

Proof of Proposition 6. Owing to Lemma 3 and the characterization of the equilibrium in subsection 2.6, it is sufficient to show that the perfect information low quality investment choice is greater than I:, the first-best level, when p is subsidized. This conclusion follows from differentiation of the perfect information first-order condition, ii; - (1 + p) = 0:

!!!L_ l <()

dp Iri(Z,) . (A.13)

Since a subsidy reduces p, the inequality in (A.13) completes the proof. Q.E.D.

References