Embed Size (px)

DESCRIPTION

Introduction to Financial Management FIN 102 – Week 4a. Dr. Andrew L. H. Parkes “A practical and hands on course on the valuation and financial management of corporations”. The Time Value of Money Continued. Annuities Ordinary vs. Annuities Due Future Value Present Value Payments - PowerPoint PPT Presentation

Citation preview

Introduction to Financial Introduction to Financial ManagementManagementFIN 102 – Week 4aFIN 102 – Week 4a

Dr. Andrew L. H. ParkesDr. Andrew L. H. Parkes““A practical and hands on course on the valuation A practical and hands on course on the valuation

and financial management of corporations”and financial management of corporations”

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

22

The Time Value of MoneyThe Time Value of MoneyContinuedContinued

AnnuitiesAnnuities Ordinary vs. Annuities Ordinary vs. Annuities

DueDue Future ValueFuture ValuePresent ValuePresent ValuePaymentsPayments

Amortizing a LoanAmortizing a LoanAnnuities are often used for

retirement and called a nest egg.

Two Basic Topics:

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

33

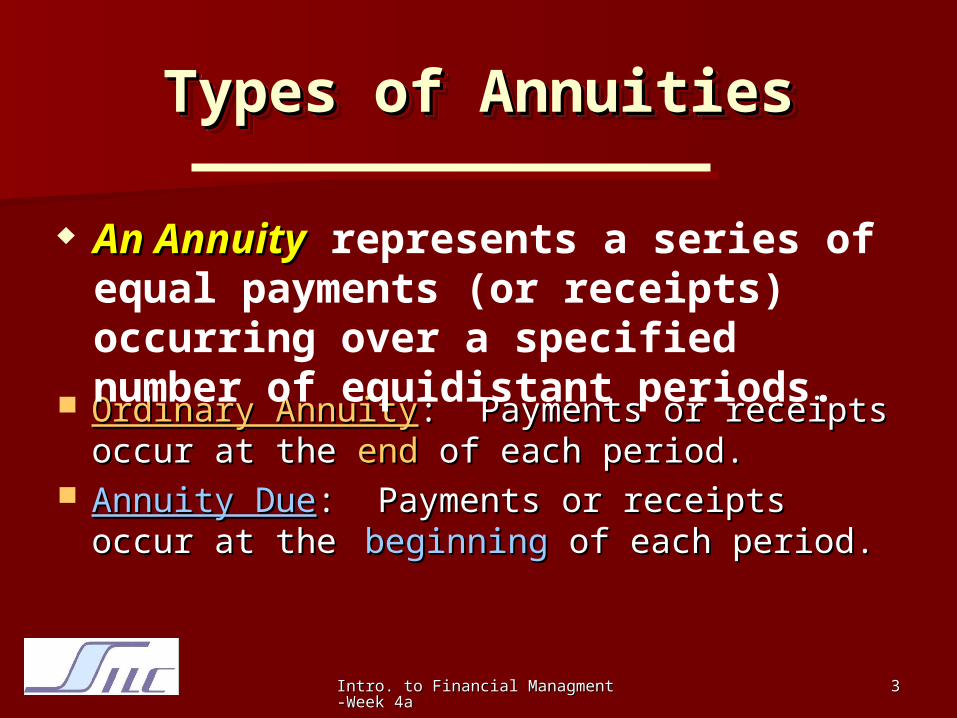

Types of AnnuitiesTypes of AnnuitiesTypes of AnnuitiesTypes of Annuities

Ordinary AnnuityOrdinary Annuity: Payments or receipts : Payments or receipts occur at the occur at the endend of each period. of each period.

Annuity DueAnnuity Due: Payments or receipts occur at : Payments or receipts occur at the the beginningbeginning of each period. of each period.

An AnnuityAn Annuity represents a series of equal payments (or receipts) occurring over a specified number of equidistant periods.

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

44

Examples of AnnuitiesExamples of Annuities

Student Loan PaymentsStudent Loan Payments Car Loan PaymentsCar Loan Payments Insurance PremiumsInsurance Premiums Mortgage PaymentsMortgage Payments Retirement SavingsRetirement Savings

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

55

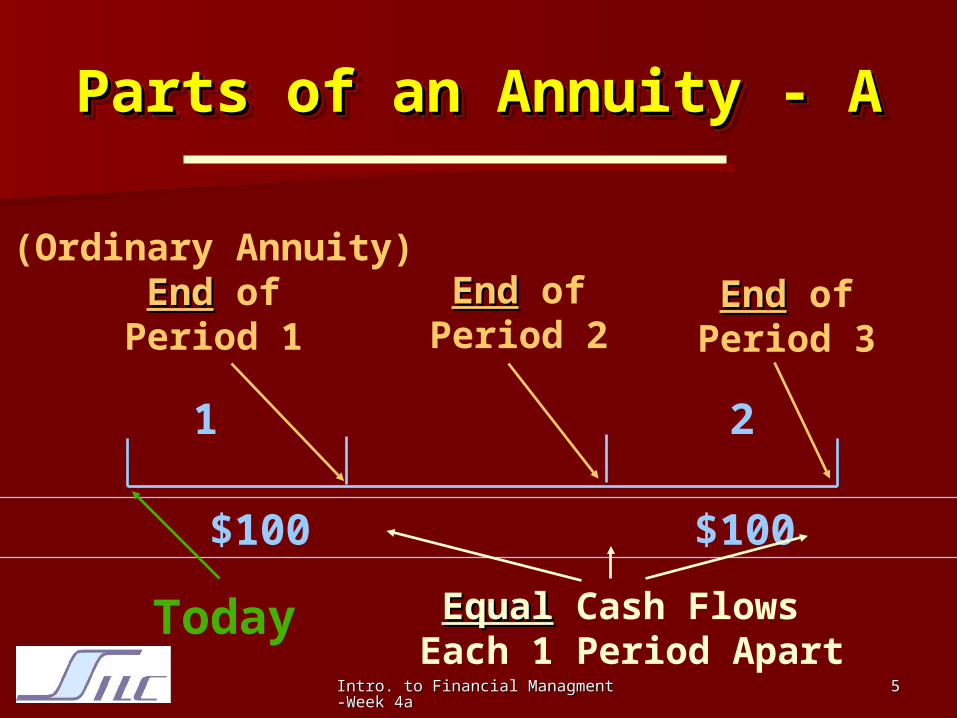

Parts of an Annuity - AParts of an Annuity - AParts of an Annuity - AParts of an Annuity - A

0 1 2 3

$100 $100 $100

(Ordinary Annuity)EndEnd of

Period 1EndEnd of

Period 2

Today EqualEqual Cash Flows Each 1 Period Apart

EndEnd ofPeriod 3

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

66

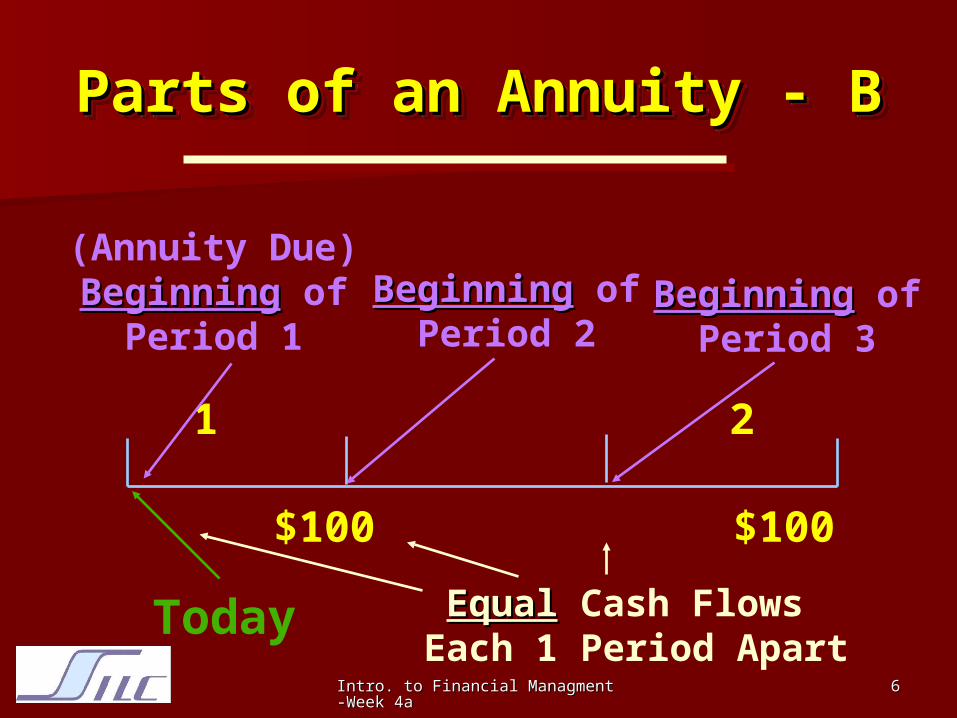

Parts of an Annuity - BParts of an Annuity - BParts of an Annuity - BParts of an Annuity - B

0 1 2 3

$100 $100 $100

(Annuity Due)BeginningBeginning of

Period 1BeginningBeginning of

Period 2

Today EqualEqual Cash Flows Each 1 Period Apart

BeginningBeginning ofPeriod 3

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

77

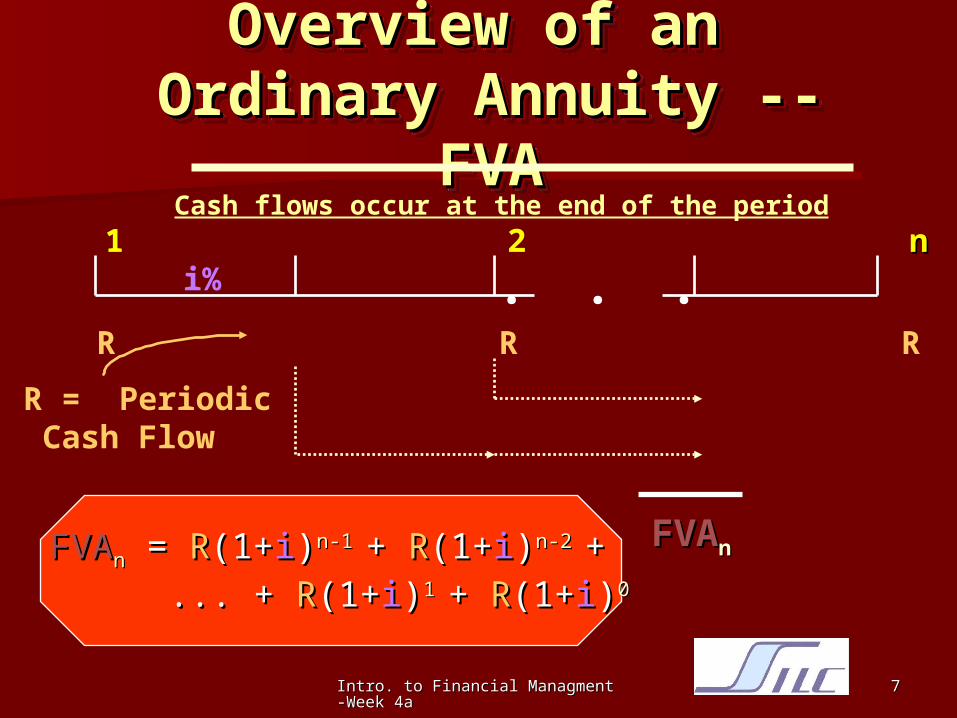

FVAFVAnn = = RR(1+(1+ii))n-1 n-1 + + RR(1+(1+ii))n-2 n-2 + + ... + ... + RR(1+(1+ii))11 + + RR(1+(1+ii))00

Overview of an Overview of an Ordinary Annuity -- Ordinary Annuity --

FVAFVA

Overview of an Overview of an Ordinary Annuity -- Ordinary Annuity --

FVAFVA

R R R

0 1 2 n n n+1

FVAFVAnn

R = Periodic Cash Flow

Cash flows occur at the end of the period

i% . . .

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

88

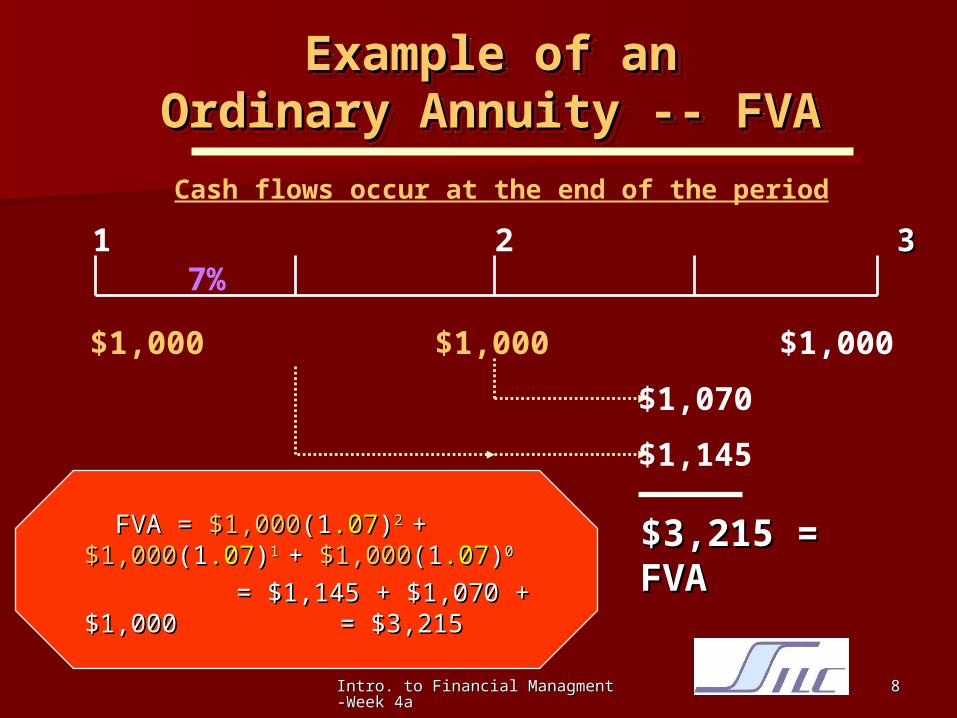

FVA = FVA = $1,000$1,000(1(1.07.07))2 2 + + $1,000$1,000(1(1.07.07))1 1 + + $1,000$1,000(1(1.07.07))00

= $1,145 + $1,070 + $1,000 = $1,145 + $1,070 + $1,000 = $3,215= $3,215

Example of anExample of anOrdinary Annuity -- FVAOrdinary Annuity -- FVA

Example of anExample of anOrdinary Annuity -- FVAOrdinary Annuity -- FVA

$1,000 $1,000 $1,000

0 1 2 3 3 4

$3,215 = FVA$3,215 = FVA

7%

$1,070

$1,145

Cash flows occur at the end of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

99

Ordinary annuitiesOrdinary annuities

Henry saves $600 each half year and Henry saves $600 each half year and invests it at 13% (convertible semi invests it at 13% (convertible semi annually) How much money has annually) How much money has Henry got after 10 years?Henry got after 10 years?

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1010

The answerThe answer Time Line:Time Line: After a half year Henry puts in After a half year Henry puts in

his first $600his first $600 and so forth every half year and so forth every half year Starting today the first $600 will stay in the Starting today the first $600 will stay in the

account 9.5 years … account 9.5 years … on the time line!on the time line! The The secondsecond amount of $600 for 9 years. amount of $600 for 9 years. The The thirdthird amount 8.5 years etc. amount 8.5 years etc. The The lastlast amount of $600 will have no time to amount of $600 will have no time to

gather any interest gather any interest Let us use EXCEL!! – see the Let us use EXCEL!! – see the FunctionFunction key key

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1111

FVADFVADnn = = RR(1+(1+ii))n n + + RR(1+(1+ii))n-1 n-1 + + ... + ... + RR(1+(1+ii))22 + +

RR(1+(1+ii))1 1 = FVA= FVAn n (1+(1+ii))

Overview View of anOverview View of anAnnuity DueAnnuity Due

Overview View of anOverview View of anAnnuity DueAnnuity Due

R R R R R

0 1 2 3 n-1 n-1 n

FVADFVADnn

i% . . .

Cash flows occur at the beginning of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1212

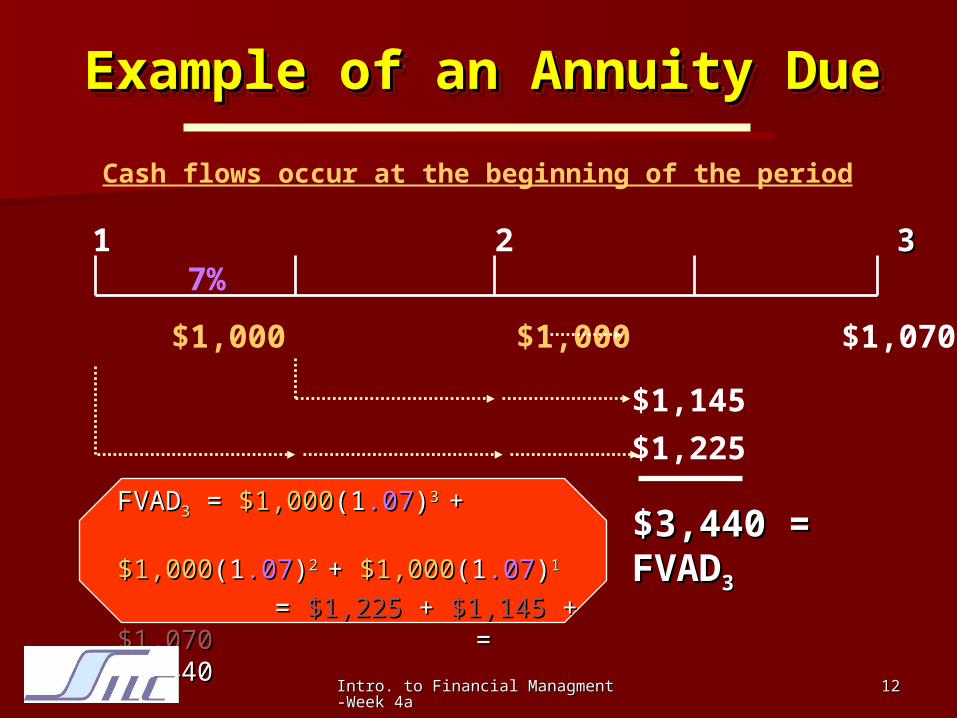

FVADFVAD33 = = $1,000$1,000(1(1.07.07))3 3 + + $1,000$1,000(1(1.07.07))2 2 + +

$1,000$1,000(1(1.07.07))11

= = $1,225$1,225 ++ $1,145$1,145 ++ $1,070$1,070 == $3,440$3,440

Example of an Annuity DueExample of an Annuity DueExample of an Annuity DueExample of an Annuity Due

$1,000 $1,000 $1,000 $1,070

0 1 2 3 3 4

$3,440 = FVAD$3,440 = FVAD33

7%

$1,225

$1,145

Cash flows occur at the beginning of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1313

Ordinary versus Annuities Ordinary versus Annuities DueDue

There is one extra There is one extra interest period that interest period that accrues.accrues.

So we multiply the So we multiply the ordinary annuity by ordinary annuity by (1+i).(1+i).

THAT IS ALL! THAT IS ALL!

Traders on the floor of the New York Stock Exchange watch the news of a bigger-than-

expected rate cut from the Federal Reserve.

Spencer Platt / Getty Images

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1414

The Power of Compound The Power of Compound InterestInterest

A 20-year-old student wants to start A 20-year-old student wants to start saving for retirement.saving for retirement. She plans to She plans to save save $3$3 a day. Every day, she puts a day. Every day, she puts $3 in her drawer. At the end of the $3 in her drawer. At the end of the year, she invests the accumulated year, she invests the accumulated savings savings ($1,095)($1,095) in an online stock in an online stock account. The stock account has an account. The stock account has an expected annual return of expected annual return of 12%12%..

How muchHow much money will she have money will she have when she is 65 years old? – when she is 65 years old? – Set up Set up the problem!the problem!

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1515

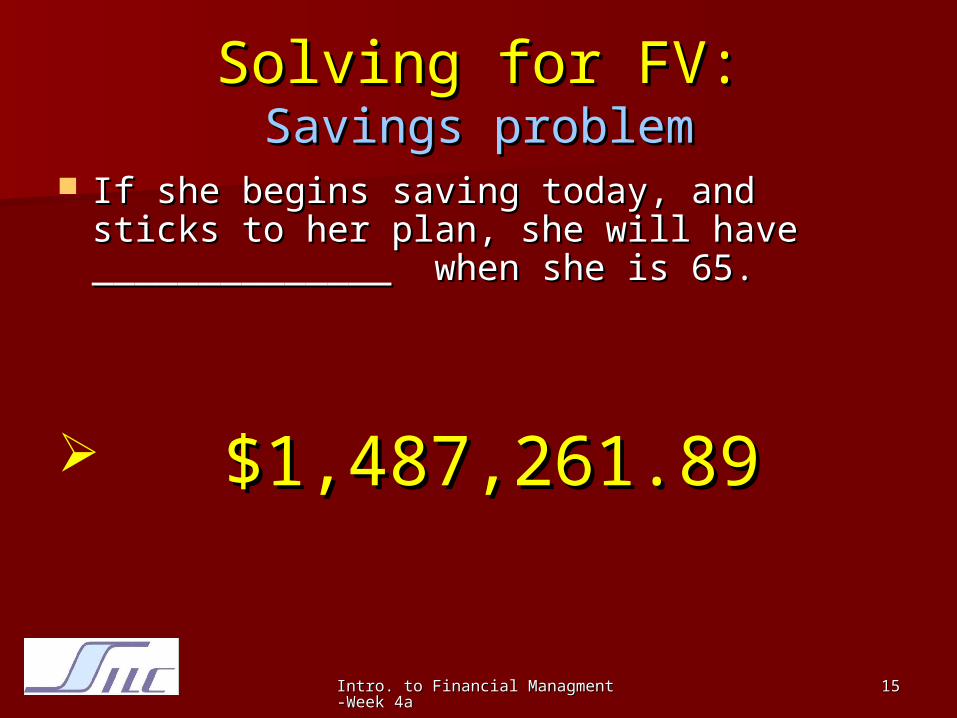

Solving for FV:Solving for FV:Savings problemSavings problem

If she begins saving today, and sticks If she begins saving today, and sticks to her plan, she will have to her plan, she will have ______________ when she is 65.______________ when she is 65.

$1,487,261.89$1,487,261.89

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1616

Solving for FV:Solving for FV:Savings problem, if you wait until Savings problem, if you wait until

you are 40 years old to startyou are 40 years old to start If a 40-year-old investor begins saving today If a 40-year-old investor begins saving today

_____________at age 65. This is $1.3 million _____________at age 65. This is $1.3 million less than if starting at age 20.less than if starting at age 20.

$146,000.59$146,000.59 Lesson: It pays to start saving early.Lesson: It pays to start saving early.

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1717

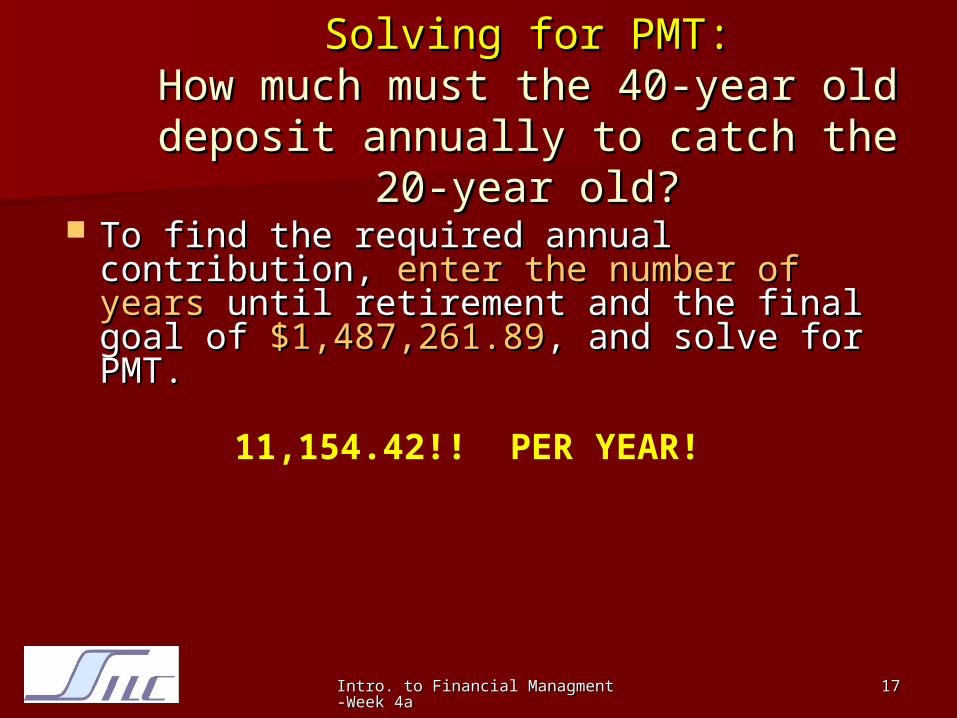

Solving for PMT:Solving for PMT:How much must the 40-year old How much must the 40-year old deposit annually to catch the 20-deposit annually to catch the 20-

year old?year old? To find the required annual contribution, To find the required annual contribution,

enter the number of yearsenter the number of years until until retirement and the final goal of retirement and the final goal of $1,487,261.89$1,487,261.89, and solve for PMT., and solve for PMT.

11,154.42!! PER YEAR!

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1818

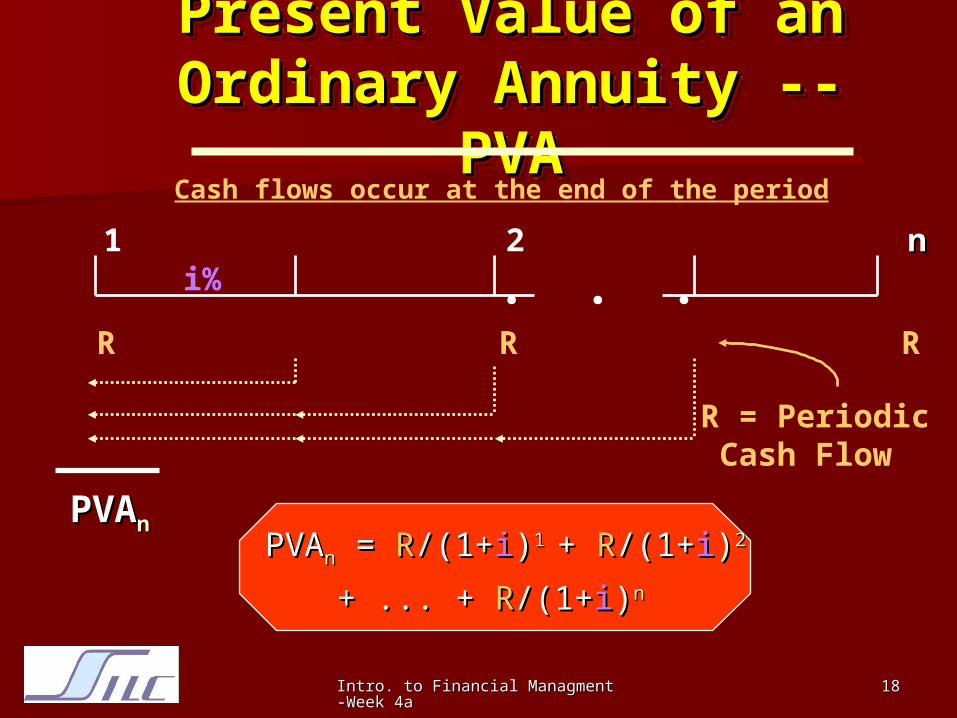

PVAPVAnn = = RR/(1+/(1+ii))1 1 + + RR/(1+/(1+ii))2 2

+ ... + + ... + RR/(1+/(1+ii))nn

Present Value of anPresent Value of anOrdinary Annuity -- Ordinary Annuity --

PVAPVA

Present Value of anPresent Value of anOrdinary Annuity -- Ordinary Annuity --

PVAPVA

R R R

0 1 2 n n n+1

PVAPVAnn

R = Periodic Cash Flow

i% . . .

Cash flows occur at the end of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

1919

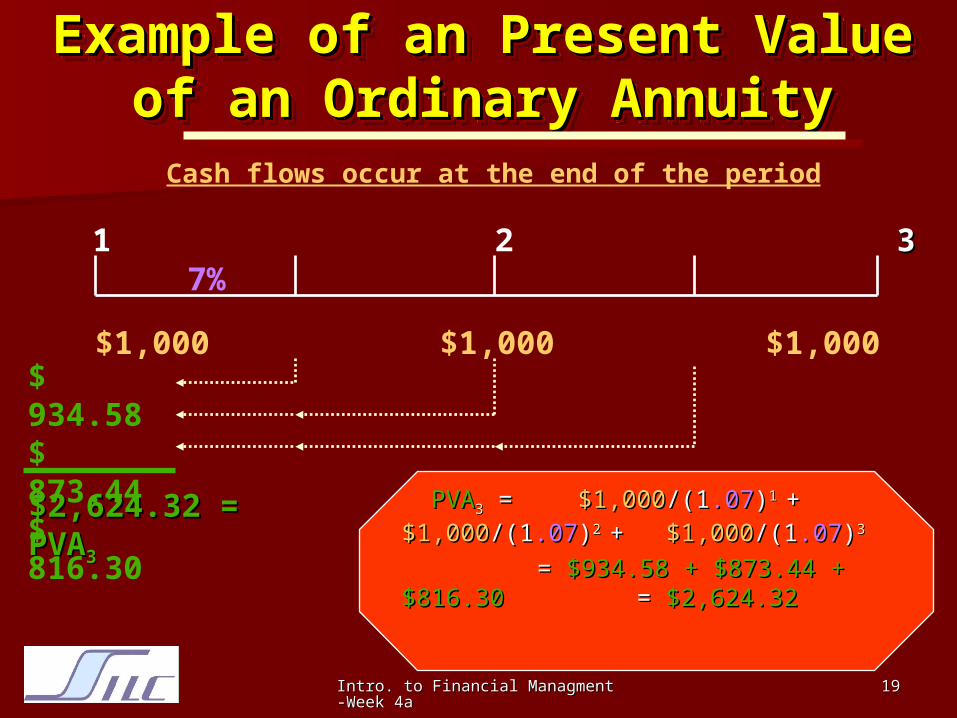

PVAPVA33 = = $1,000$1,000/(1/(1.07.07))1 1 + + $1,000$1,000/(1/(1.07.07))2 2 + + $1,000$1,000/(1/(1.07.07))33

== $934.58 + $873.44 + $816.30 $934.58 + $873.44 + $816.30 == $2,624.32 $2,624.32

Example of an Present Value Example of an Present Value of an Ordinary Annuityof an Ordinary Annuity

Example of an Present Value Example of an Present Value of an Ordinary Annuityof an Ordinary Annuity

$1,000 $1,000 $1,000

0 1 2 33 4

$2,624.32 = PVA$2,624.32 = PVA33

7%

$ 934.58$ 873.44 $ 816.30

Cash flows occur at the end of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2020

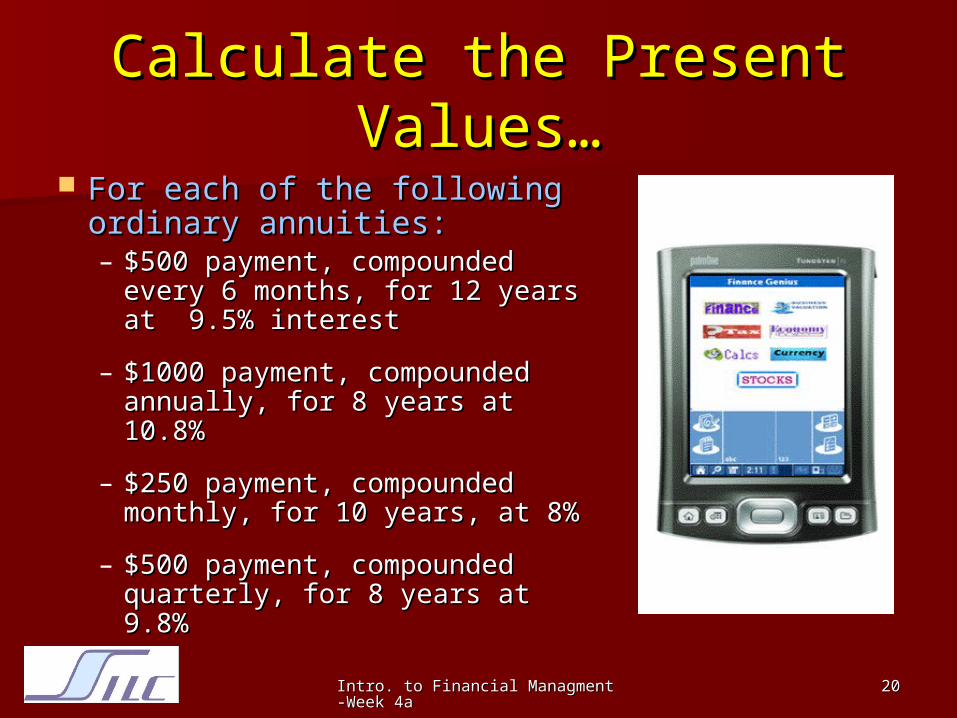

Calculate the Present Calculate the Present Values…Values…

For each of the following For each of the following ordinary annuities:ordinary annuities:– $500 payment, compounded $500 payment, compounded

every 6 months, for 12 years every 6 months, for 12 years at 9.5% interest at 9.5% interest

– $1000 payment, $1000 payment, compounded annually, for 8 compounded annually, for 8 years at 10.8%years at 10.8%

– $250 payment, compounded $250 payment, compounded monthly, for 10 years, at 8%monthly, for 10 years, at 8%

– $500 payment, compounded $500 payment, compounded quarterly, for 8 years at 9.8%quarterly, for 8 years at 9.8%

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2121

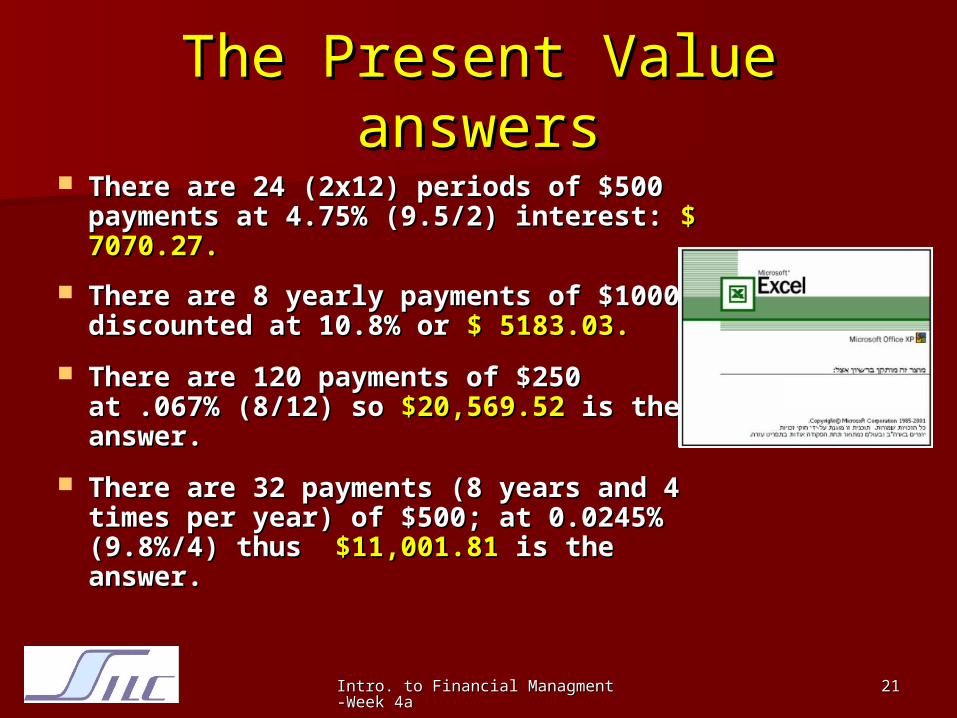

The Present Value answersThe Present Value answers There are 24 (2x12) periods of $500 payments There are 24 (2x12) periods of $500 payments

at 4.75% (9.5/2) interest: at 4.75% (9.5/2) interest: $ 7070.27.$ 7070.27.

There are 8 yearly payments of $1000 There are 8 yearly payments of $1000 discounted at 10.8% or discounted at 10.8% or $ 5183.03.$ 5183.03.

There are 120 payments of $250 at .067% There are 120 payments of $250 at .067% (8/12) so (8/12) so $20,569.52$20,569.52 is the answer. is the answer.

There are 32 payments (8 years and 4 times There are 32 payments (8 years and 4 times per year) of $500; at 0.0245% (9.8%/4) thus per year) of $500; at 0.0245% (9.8%/4) thus $11,001.81$11,001.81 is the answer. is the answer.

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2222

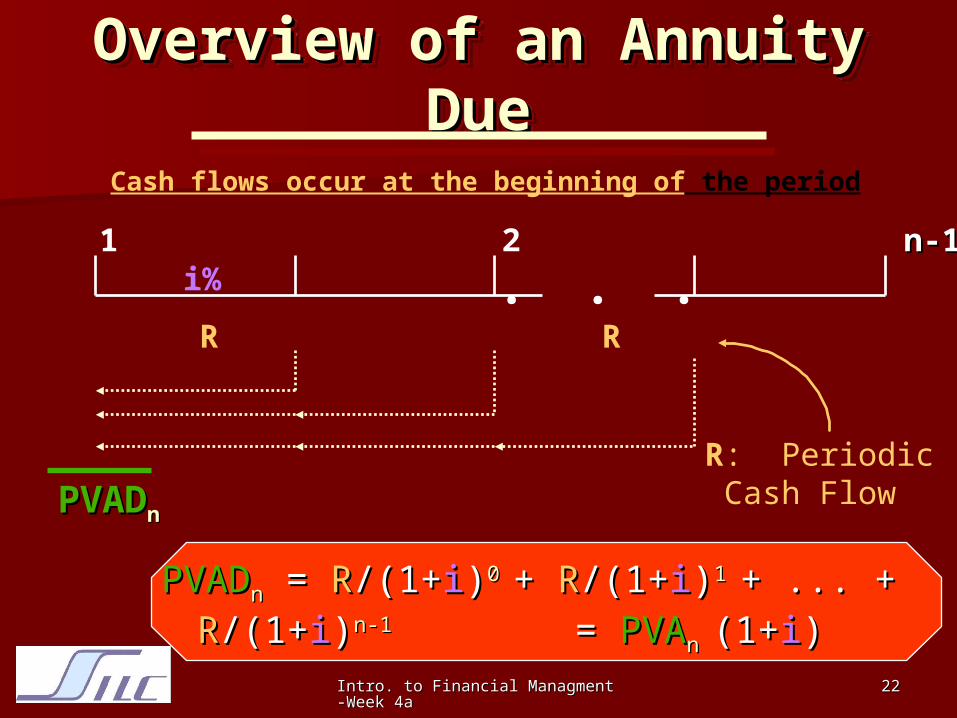

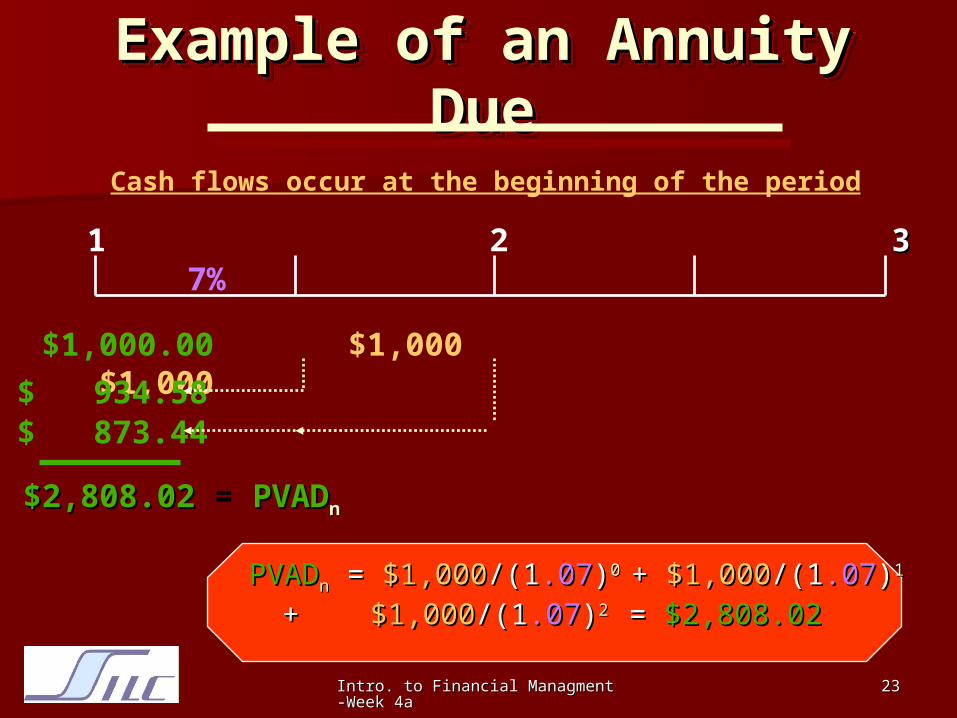

PVADPVADnn = = RR/(1+/(1+ii))0 0 + + RR/(1+/(1+ii))1 1 + ... + + ... + RR/(1+/(1+ii))n-1n-1 = = PVAPVAn n (1+(1+ii))

Overview of an Annuity Overview of an Annuity DueDue

Overview of an Annuity Overview of an Annuity DueDue

R R R R

0 1 2 n-1 n-1 n

PVADPVADnn

R: Periodic Cash Flow

i% . . .

Cash flows occur at the beginning of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2323

PVADPVADnn = = $1,000$1,000/(1/(1.07.07))0 0 + + $1,000$1,000/(1/(1.07.07))1 1 + + $1,000$1,000/(1/(1.07.07))2 2 = = $2,808.02$2,808.02

Example of an Annuity Example of an Annuity DueDue

Example of an Annuity Example of an Annuity DueDue

$1,000.00 $1,000 $1,000

0 1 2 3 3 4

$2,808.02 $2,808.02 = PVADPVADnn

7%

$ 934.58$ 873.44

Cash flows occur at the beginning of the period

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2424

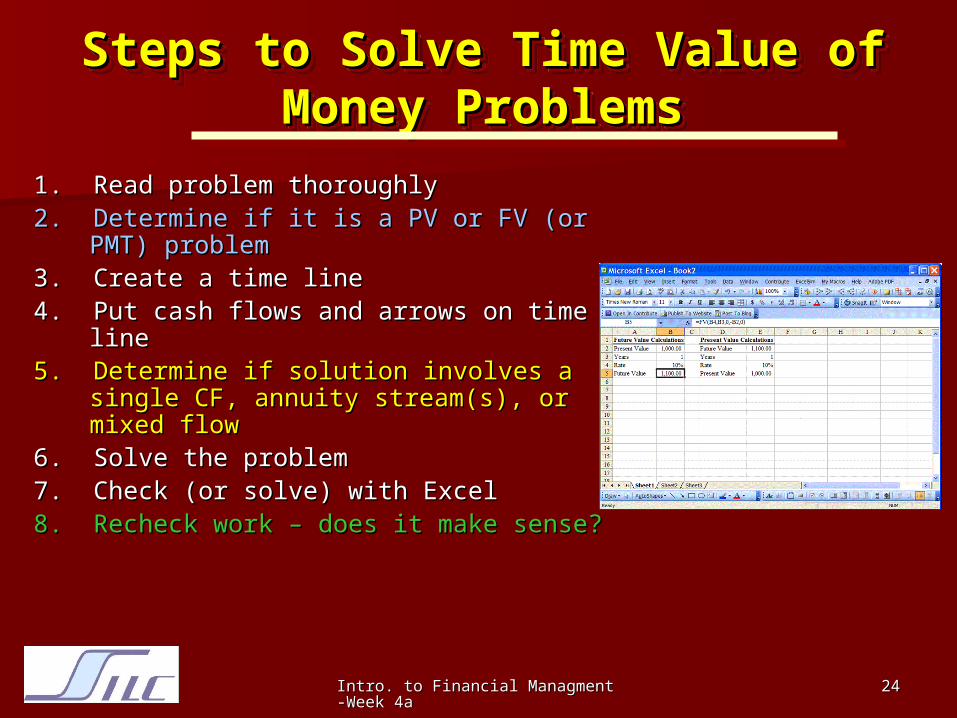

1. Read problem thoroughly1. Read problem thoroughly2. Determine if it is a PV or FV (or PMT) 2. Determine if it is a PV or FV (or PMT)

problemproblem3. Create a time line3. Create a time line4. Put cash flows and arrows on time 4. Put cash flows and arrows on time

lineline5. Determine if solution involves a single 5. Determine if solution involves a single

CF, annuity stream(s), or mixed flowCF, annuity stream(s), or mixed flow6. Solve the problem6. Solve the problem7. Check (or solve) with Excel7. Check (or solve) with Excel8. Recheck work – does it make sense?8. Recheck work – does it make sense?

Steps to Solve Time Value of Steps to Solve Time Value of Money ProblemsMoney Problems

Steps to Solve Time Value of Steps to Solve Time Value of Money ProblemsMoney Problems

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2525

Used CarUsed Car

A used car sells for $10,000 in cash A used car sells for $10,000 in cash OR:OR:

$2000 deposit plus 6 instalments of $2000 deposit plus 6 instalments of $1400 per month for 6 months $1400 per month for 6 months

What is the implied interest in the What is the implied interest in the instalment plan?instalment plan?

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2626

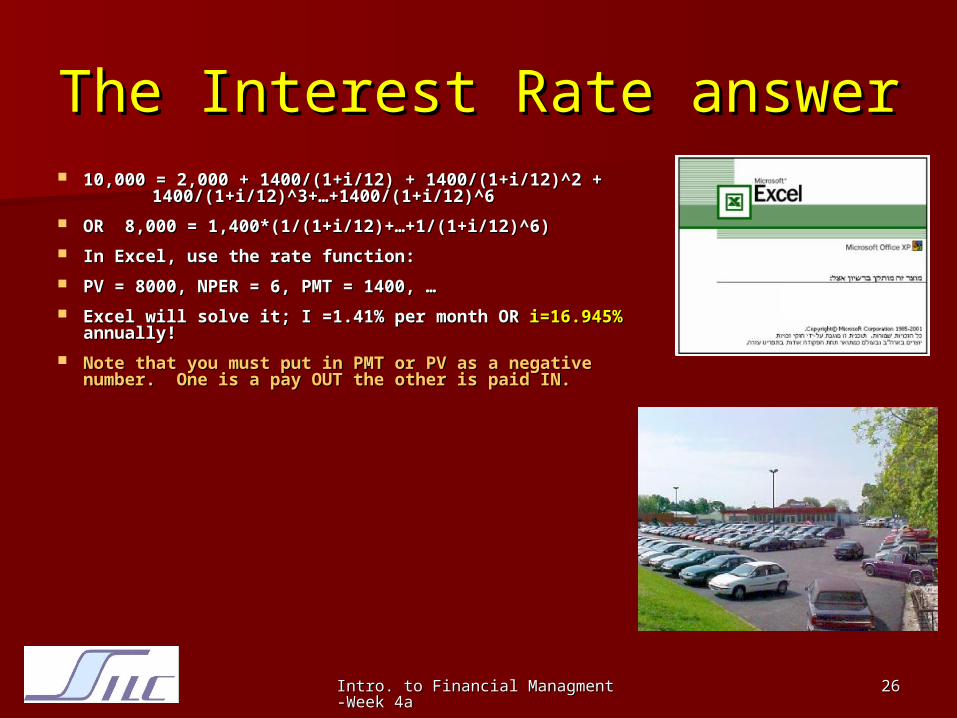

The Interest Rate answerThe Interest Rate answer 10,000 = 2,000 + 1400/(1+i/12) + 1400/(1+i/12)^2 + 10,000 = 2,000 + 1400/(1+i/12) + 1400/(1+i/12)^2 +

1400/(1+i/12)^3+…+1400/(1+i/12)^61400/(1+i/12)^3+…+1400/(1+i/12)^6

OR 8,000 = 1,400*(1/(1+i/12)+…+1/(1+i/12)^6)OR 8,000 = 1,400*(1/(1+i/12)+…+1/(1+i/12)^6)

In Excel, use the rate function:In Excel, use the rate function:

PV = 8000, NPER = 6, PMT = 1400, …PV = 8000, NPER = 6, PMT = 1400, …

Excel will solve it; I =1.41% per month OR Excel will solve it; I =1.41% per month OR i=16.945%i=16.945% annually! annually!

Note that you must put in PMT or PV as a negative number. One Note that you must put in PMT or PV as a negative number. One is a pay OUT the other is paid IN.is a pay OUT the other is paid IN.

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2727

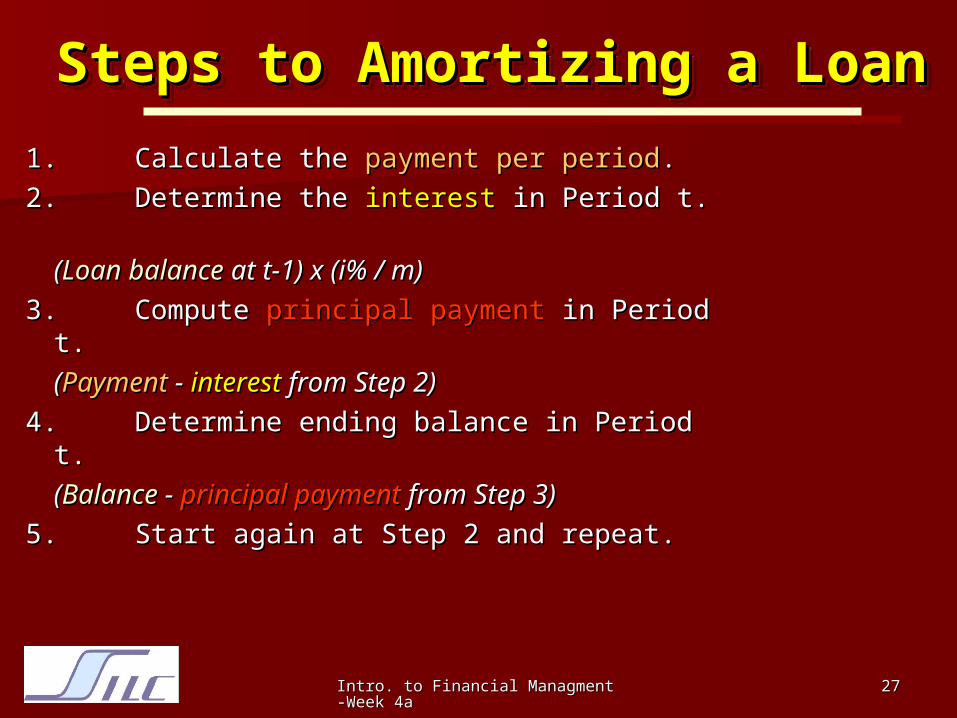

1.1.Calculate the Calculate the payment per periodpayment per period..

2.2.Determine the Determine the interestinterest in Period t. in Period t.

((Loan balance Loan balance at t-1) x (i% / m)at t-1) x (i% / m)

3.3.ComputeCompute principal payment principal payment in Period t.in Period t.

((PaymentPayment - - interest interest from Step 2)from Step 2)

4.4.Determine ending balance in Period t.Determine ending balance in Period t.

((BalanceBalance - - principal payment principal payment from Step 3)from Step 3)

5.5.Start again at Step 2 and repeat.Start again at Step 2 and repeat.

Steps to Amortizing a LoanSteps to Amortizing a LoanSteps to Amortizing a LoanSteps to Amortizing a Loan

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2828

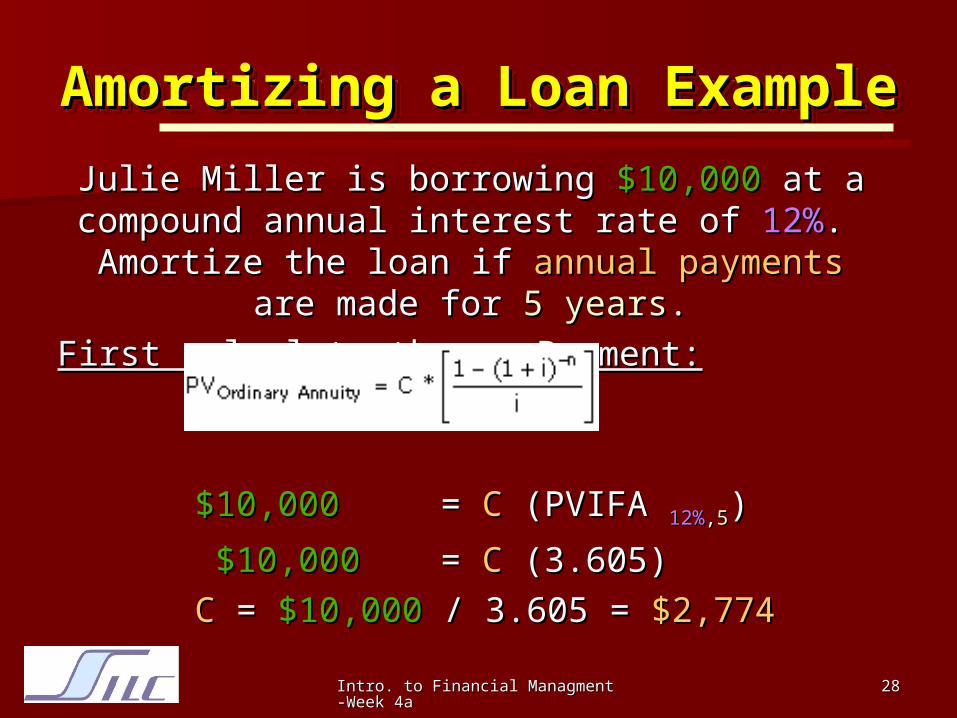

Julie Miller is borrowing Julie Miller is borrowing $10,000 $10,000 at a at a compound annual interest rate of compound annual interest rate of 12%12%. .

Amortize the loan if Amortize the loan if annual payments annual payments are are made for made for 5 years5 years..

First calculate theFirst calculate the Payment:Payment:

$10,000 $10,000 = = CC (PVIFA (PVIFA 12%12%,,55))

$10,000$10,000 = = CC (3.605) (3.605)

CC = = $10,000$10,000 / 3.605 = / 3.605 = $2,774$2,774

Amortizing a Loan ExampleAmortizing a Loan ExampleAmortizing a Loan ExampleAmortizing a Loan Example

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

2929

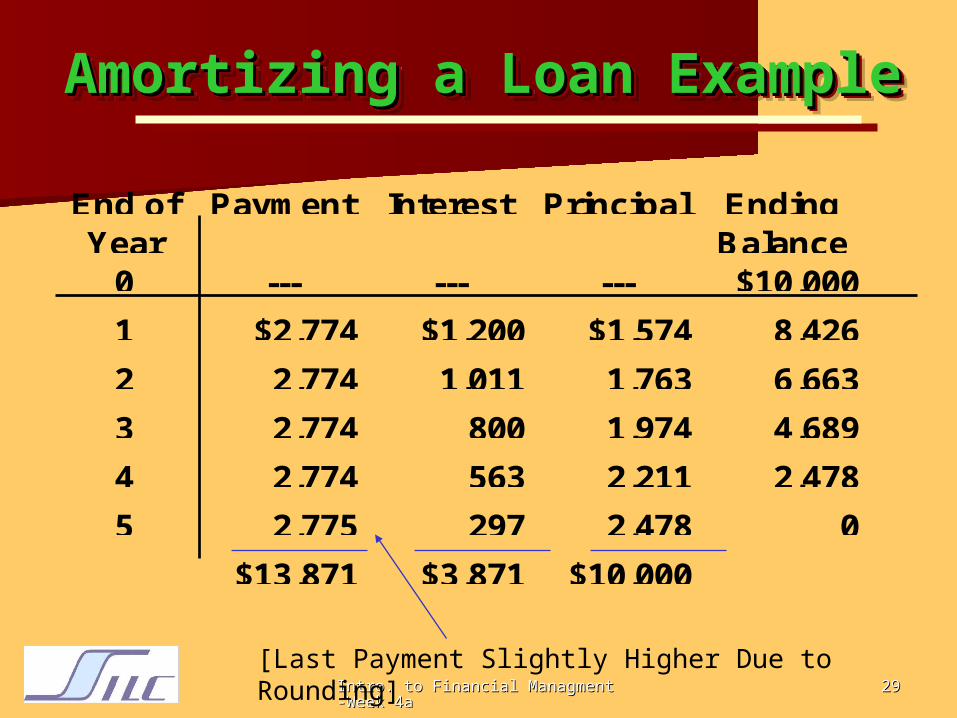

Amortizing a Loan ExampleAmortizing a Loan ExampleAmortizing a Loan ExampleAmortizing a Loan Example

End ofYear

Payment Interest Principal EndingBalance

0 --- --- --- $10,000

1 $2,774 $1,200 $1,574 8,426

2 2,774 1,011 1,763 6,663

3 2,774 800 1,974 4,689

4 2,774 563 2,211 2,478

5 2,775 297 2,478 0

$13,871 $3,871 $10,000

[Last Payment Slightly Higher Due to Rounding]

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

3030

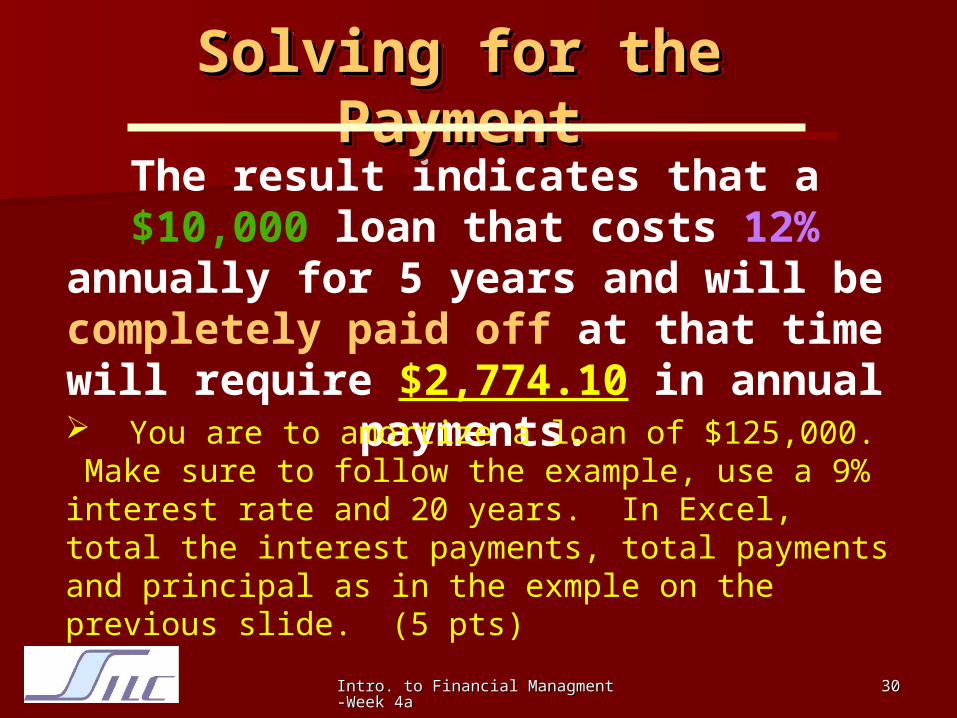

The result indicates that a $10,000 loan that costs 12% annually for 5 years and will be

completely paid off at that time will require $2,774.10 in annual payments.

Solving for the Solving for the PaymentPayment

Solving for the Solving for the PaymentPayment

You are to amortize a loan of $125,000. Make sure to follow the example, use a 9% interest rate and 20 years. In Excel, total the interest payments, total payments and principal as in the exmple on the previous slide. (5 pts)

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

3131

Homework AssignmentHomework Assignment Chose a company from the Value Line documents (See Chose a company from the Value Line documents (See

my website, this is a Dow Jones 30 company).my website, this is a Dow Jones 30 company).

Read the Value Line document and take a look at the Read the Value Line document and take a look at the financials.financials.

Now calculate Free Cash Flow (FCF) = (NOPAT + Now calculate Free Cash Flow (FCF) = (NOPAT + depreciation +/- change in Working Capital - Capital depreciation +/- change in Working Capital - Capital Spending)Spending)

Do this for all the years available on the Value Line Do this for all the years available on the Value Line document.document.

Assume that the Cost of Capital (WACC%)=10%Assume that the Cost of Capital (WACC%)=10%

Forecast the FCF for FY 2006 etc. years (assume an Forecast the FCF for FY 2006 etc. years (assume an endless stream of FCF’s)endless stream of FCF’s)

Now calculate the Present Value and use the WACC% Now calculate the Present Value and use the WACC% as discount factor (i)as discount factor (i)

The present value you have calculated is an estimate The present value you have calculated is an estimate for the value of the company you have chosenfor the value of the company you have chosen

Do it in Excel…and save time… Have fun!Do it in Excel…and save time… Have fun!

Intro. to Financial Managment-WeeIntro. to Financial Managment-Week 4ak 4a

3232

These are calculation These are calculation techniques you need to techniques you need to

master…master… We will use them in the near We will use them in the near

future to calculate the future to calculate the present values of future cash present values of future cash flows of companiesflows of companies

Next week we will discuss Next week we will discuss

Risk and Return (Chapter 5)Risk and Return (Chapter 5) We want to be aligned in the same direction…

![PIANO CONCERTO IN F 2nd Movement for Clarinets · 102 102 102 102 102 102 102 102 102 102 102 10 44 [Title]](https://img.pdfslide.us/doc/110x75/5e3946b540eed0696e2e90d2/piano-concerto-in-f-2nd-movement-for-clarinets-102-102-102-102-102-102-102-102-102.jpg)