Embed Size (px)

Citation preview

Introduction to Developers DiversifiedNovember 2006

2

Developers Diversified (NYSE: DDR)

Large and growing retail shopping center platform

Outstanding financial performance

Major landlord to nation’s leading retailers

Excellence in design, retail mix and tenant relations

The leading owner, developer and manager of market-dominant community shopping centers

3

4

Joe PadanilamSVP of

Acquisitions &Dispositions

Scott WolsteinCEO

David JacobsteinPresident & COO

Bill SchaferExecutive VP and

CFO

Joan AllgoodExecutive VP

CorporateTransactions &Governance

Richard BrownExecutive VP of

International

David WeissSVP and General

Counsel

Michelle DawsonVP of Investor

Relations

Daniel HurwitzSenior Executive

VP & CIO

TBDVP of NewBusiness

Development

Scott SchroederVP of Marketing &

CorporateCommunications

Robin Walker-GibbonsExecutive VP of Leasing

Ken SternVP of Peripheral

Development

Dan HermanSVP of

Development East

Stan HoffmanVP of

Development West

John SabatosVP of Construction

Dale JohnsonVP & Corp.Controller

Francine GlandtVP of Capital

Markets &Treasury

Craig SchultzVP of Tax

David FavoriteVP of PropertyManagement/Community

Centers

John KokinchakSVP of Property

Management

LorraineMcGlone

VP of InformationTechnology

Neal InfanteVP & Property

Controller

Tim BruceExecutive VP ofDevelopment

Nan ZieleniecSVP of Human

Resources

Marc HaysSVP of Leasing

Specialty Centers

Erik ChristopherVP of Development

Leasing

Bill ReadVP of Leasing

Southeast Region

Francis GonzalezVP of PropertyManagementPuerto Rico

Eddie SullivanVP of PropertyManagement

Mid Atlantic Region

Christa VesySVP and Chief

Accounting Officer

David DieterleSteven Dorsky

Anthony VodickaSVPs of Leasing

Management TeamDeep executive bench with broad industry expertise

5

Management Team Average tenure for EVPs and above is 12 years with Developers Diversified and 23 years in retail real estate

(1) Affiliated with pre-IPO entity. IPO in February 1993.

Scott A. Wolstein CEO & Chairman 25 25David M. Jacobstein Pres. & COO 7 21Daniel B. Hurwitz Sr. EVP & CIO 7 20Joan U. Allgood EVP-Corporate 19 24

Transactions & Governance Richard E. Brown EVP-International 7 26Timothy J. Bruce EVP-Development 4 20William H. Schafer EVP & CFO 14 22Robin R. Walker-Gibbons EVP-Leasing 11 25

Name TitleYears with Company

Years in Industry

(1)

(1)

(1)

Total Years 94 183

6

Developers Diversified - Post IRRETI MergerKey Facts

Total Market Cap $15.3B

Total Franchise Value $21.8B

Corporate Credit Ratings BBB/Baa2

Number of Retail Properties 809

GLA 162 msf

Number of States 45 plus Puerto Rico and Brazil

Development Pipeline $3.5B plus additional $1.5B under

preliminary pursuit

Long Term Avg. Leased Rate 96%

5 Year Annualized Total Return as of 3Q06 33%

Dividend Growth (2002-2006) 55%

Included in S&P 400

7

1965 Developers Diversified began as Developers Diversified Group (DDG) in 1965 when Bert L. Wolstein formed the Company to develop community shopping centers anchored by Kmart.

1977 DDG expanded its activities to include the development of community shopping centers anchored by JCPenney in the upper Midwest.

1981 The Company’s principals formed Diversified Equities Limited Partnership, which led DDG into an era of acquisition and equity capital formation.

1993 On February 2, 1993, Developers Diversified Realty Corporation began operating as a publicly traded Real Estate Investment Trust (REIT).

1995 Developers Diversified’s portfolio dramatically increased when it acquired a community shopping center portfolio previously owned by Homart Development.

1998 The portfolio received another boost In 1998 when the Company acquired three more community center portfolios, expanding its presence in Ohio, Utah and Missouri.

Developers Diversified Company History

GLA: 27 msf

Properties: 106

Employees: 133

GLA: 17 msf

Properties: 53

Employees: 75

GLA: 42 msf

Properties: 159

Employees: 230

8

2001 The Company announced the acquisition of 10 properties from Burnham Pacific (NYSE: BPP). Developers Diversified also acted as liquidation agent for the remainder of the BPP portfolio.

2002 Developers Diversified and joint venture partners KlaffRealty and Lubert Adler Funds were awarded designation rights to the Service Merchandise retail assets.

2003 In March 2003, Developers Diversified and JDN Realty (NYSE: JDN) merged, creating one of the largest open-air shopping center companies in the country.

2004 Developers Diversified acquired a portfolio of 107 shopping centers from Benderson Development, positioning it as the largest owner and operator of community shopping centers in the U.S. The Company was also added to the S&P 400 index of mid cap stocks.

2005 Developers Diversified celebrated its 40th anniversary. The Company acquired 15 shopping centers in Puerto Rico. Also, Developers Diversified and joint venture partner Macquarie DDR Trust acquired 37 Mervyns stores.

2006 Developers Diversified acquired a 50% interest in Sonae Sierra Brazil, a fully integrated retail real estate company based in Sao Paulo. Announced $6.2B acquisition of Inland Retail Real Estate Trust, $3.0B to be placed in new JV with TIAA-CREF.

Developers DiversifiedCompany History

GLA: 57 msf

Properties: 228

Employees: 353

GLA: 58 msf

Properties: 286

Employees: 368

GLA: 83 msf

Properties: 362

Employees: 461

GLA: 103 msf

Properties: 458

Employees: 551

GLA: 113 msf

Properties: 496

Employees: 574

GLA: 162 msf

Properties: 809

Employees: 649

9

Successful financing, execution and integration of large portfolio acquisitions is a core competency

$3

$5

$7

$9

$11

$13

$15

$17

$19

$21

$23

4Q02 4Q03 4Q04 4Q05 Post IRRETIMerger

280

360

440

520

600

680

760

840

Total Franchise ValueNumber of Properties

• 286 Assets • 58 MSF • $5.0B TFV

• 362 Assets • 83 MSF • $7.6B TFV

• 458 Assets • 103 MSF • $11.4B TFV

• 496 Assets • 113 MSF • $13.9B TFV

Tota

l Fra

nchi

se V

alue

($ B

illion

s)

Num

ber of Properties

Caribbean Property

Group

Mervyns

BendersonDevelopment

JDN Realty

• March 2003 • $1.0 Billion • 81 Properties 15MSF • 21 Developments

7MSF

• 809 Assets • 162 MSF • $21.8B TFV

Sonae Sierra Brazil

• May-Dec. 2004 • $2.3 Billion • 107 Properties • 18 MSF

• January 2005• $1.2 Billion• 15 Properties • 5 MSF

• September 2005 • $396 Million• 36 Properties • 3 MSF

• October 2006 • $150 Million• 9 Properties • 3 MSF

Inland RetailReal Estate Trust, Inc.

• 1Q07 • $6.2 Billion • 307 Properties • 44 MSF

10

Although we have sometimes moved against conventional wisdom, our investment strategy has paid off

Pursue market-dominant community centersConsumers’ preferred retail venueRetail format with strongest tenant demandStrongest combination of value and convenience

Pursue developmentGreatest opportunity to create valueIn-house expertise creates control and flexibility

Pursue joint venturesPreserves capital and enhances financial flexibilityCreates fee streams and promoted interestsGenerates higher ROE than on-balance sheet structures

11

Our community center portfolio quality leads our peer group, based on quality real estate and premier tenancy

Portfolio is comprised of many of the most successful community center assets in the U.S.

Strong asset demographics Nearly 80% of space is located in the top 50 U.S. metro markets

Top landlord to the nation’s most successful retailersHighest credit quality tenancy among shopping center REITs

12

Developers Diversified – Post IRRETI Merger Over 800 shopping centers comprising 162 msf, located in 45 states plus Puerto Rico and Brazil

Puerto Rico

15.7 msf9.7%

10.7 msf6.6%

17.6 msf10.9%

16.2 msf10.0%

10.5 msf6.5%

4.9 msfTotal GLA by State

More than 5.0 MSF+1.0 – 5.0 MSF Less than 1.0 MSF

Brazil

3.4 msf

13

RemarksPlanned opening stores in 2006 (Store Growth)Tenant

Plan to increase store count from 750 to 1,300

80 stores (11%)Bed Bath & Beyond

Will open 100 stores in 2007100 stores (12%)PETsMART

Will open 500 stores over the next 5 years80 stores (11%)Kohl’s

Will open 500 stores by 2010N/AHome Depot

Will open 150 stores in 2007150 stores (12%) Lowe’s

Will open 80 stores in 4Q06 through 2Q07 110 stores (8%)Target

Real estate committee approved 1,500 new locations; plan to remodel 1,800 existing stores

340 stores (11%)Wal-Mart

We are the largest landlord to the nation’s most successful retailers

JC Penney N/A Will open 170 stores and renovate 250 others over the next 4 years

14

Wal-Mart / Sam’s Club 114 17.7 54 7.7 60 10.0 Target 64 8.4 10 1.3 54 7.1Lowe’s Home Imp. 43 5.4 23 2.8 20 2.6Home Depot 44 4.7 17 1.6 27 3.1 Kohl’s 41 3.5 37 3.2 4 0.3The TJX Companies 96 3.1 96 3.1 0 0.0Mervyns 40 3.1 39 3.0 1 0.1Kmart / Sears 27 2.8 25 2.4 2 0.4Publix 59 2.7 58 2.7 1 0.0Tops Markets 40 2.5 39 2.4 1 0.1Total Top 10 Tenants 53.9 30.1 23.7

Total Units

Total GLA (millions)

Owned Units

Owned GLA (millions)

UnownedUnits

Unowned GLA (millions)

Developers Diversified – Post IRRETI MergerLargest Tenants by Total GLA

15

Developers Diversified – Post IRRETI MergerLargest Tenants by Pro Rata Rents

Wal-Mart / Sam’s Club 54 $41.4 4.1%

Publix 58 21.9 2.1%

PETsMART 101 19.7 1.9%

The TJX Companies 96 18.5 1.8%

Tops Markets 39 17.0 1.7%

Mervyns 39 17.0 1.7%

Lowe’s Home Imp. 23 15.5 1.5%

Circuit City 42 15.2 1.5%

Kohl’s 37 14.5 1.4%

Bed Bath & Beyond 55 14.3 1.4%

Top Ten Tenants $194.9 19.1%Total Portfolio $1,021.4 100.0%

Owned Units

Total Base Rent ($m)

% ofTotal Rent

16

Base Rent: Total Portfolio & Inline Shops (< 20,000 sf)

Our portfolio is resistant to economic changes, store closings and tenant bankruptcies

$3.00

$6.00

$9.00

$12.00

$15.00

$18.00

19871991

19951999

2003

80%

85%

90%

95%

100%

19871991

19951999

2003

Percentage Leased

3Q06

3Q06

Total PortfolioInline Shops

17

$18.0$20.0

$14.6

$0.7

$6.2$4.8

$3.4$2.8

$1.6

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

$20.0

1999 2000 2001 2002 2003 2004 2005 2006 2007

Ancillary IncomePuerto Rico assets anticipated to contribute +$7.0M annually

Rev

enue

s ($

Mill

ions

)

(Estimated)Department Created

CompoundAnnualized

Growth Rate +50%

18

Total Market Capitalization

$0

$2

$4

$6

$8

$10

$12

$14

$16

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Has grown 25.5x, from $0.6 million at IPO to over $15 billion

Mar

ket C

apita

lizat

ion

(Bill

ions

)$15.3

Post IR

RETI

Merge

r

19

(1) Based on publicly disclosed earnings guidance.(2) Based on annualized 3Q06 dividend of $0.59 per share.

Earnings and Dividend Per Share GrowthFFO per share has grown by 4x and dividends have grown by 3x since IPO

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

FFO (diluted) / Share

Dividends / Share

$3.38 - $3.42 (1)

$2.36 (2)

20IPO

2/9

3

4Q93

4Q94

4Q95

4Q96

4Q97

4Q98

4Q99

4Q00

4Q01

4Q02

4Q03

4Q04

4Q05

Cur

rent

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

Stock PriceReaches 5xIPO Price

Sto

ck P

rice

Developers Diversified Stock Price(NYSE: DDR)

2x1 Stock Split

August 1998

$60.00

$65.00

21

Competitive Performance

22

Five Year Annualized Total Returnas of December 31, 2005

(1) Strip center peer group includes FRT, KIM, NXL, PNP, REG, WRI. HTG does not have a five year history.

37.0%

26.8%

20.0% 25.0% 30.0% 35.0% 40.0%

DevelopersDiversified

PeerGroup (1)

(1)

23

Five Year Annualized Dividend Growthas of December 31, 2005

8.5%

3.9%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

DevelopersDiversified

PeerGroup

24

Five Year Annualized FFO Growthas of December 31, 2005

8.0%

5.7%

4.0% 5.0% 6.0% 7.0% 8.0%

DevelopersDiversified

(1)Peer

Group

25

AFFO as a Percentage of FFO High tenant recovery of building maintenance costs, limited T.I.’s and a salaried, in-house leasing staff

AFFO as a % of FFO

94%

84%

75% 85% 95%

DevelopersDiversified

(1) Reflects adjustments for straight line rent and recurring capital expenditures. Developers Diversified’sfigures include amounts for joint ventures. Source: company reports.

(1)

PeerGroup

26

22.0%

17.0%

12.0% 16.0% 20.0% 24.0%

DevelopersDiversified

Five Year Annualized NAV Growthas of December 31, 2005

Source: Greenstreet Advisors, as reported by Forbes, SNL Financial, Realty Stock Review.

PeerGroup

27

23.7%

13.4%

10.0% 15.0% 20.0% 25.0%

DevelopersDiversified

Five Year Annualized Growth in Gross Book Value of Real Estate Assetsas of December 31, 2005

(1) Gross book value of consolidated and unconsolidated joint venture real estate assets. If gross figureswere not available, net book values were used.

(1)

PeerGroup

28

Development Expertise

29

Development has always been one of our core competencies

Our development pipeline is driven by tenant demand for new product

Mall-based retailers are migrating to open air format, where occupancy costs are significantly lowerTraditional community center tenants continue to grow their portfolios by 8% - 12% annually

Our national platform effectively sources and evaluates potential opportunities

In-house development team manages risk throughout development process

Our tenant relationships efficiently provide market intelligenceLeasing and development teams collaborate throughout development process

30

Developments Over the last five years alone, we have developed 39 projects across the U.S. representing a variety of retail formats

2005 $157.9 3,002,9872004 312.9 1,963,4202003 330.2 3,250,8922002 216.4 2,092,9622001 384.1 3,732,996

14,043,257Total

Year Substantially

Completed GLANet Project Cost

(Millions)

$1,401.5

31

Lifestyle and Hybrid Center Portfolio Growing demand driven by migration of tenants to open air format

1. Los Angeles (Pasadena), CA 556,9612. Denver (Littleton), CO 255,1843. Kansas City (Leawood), KS 490,0304. Chicago (Deer Park), IL 471,0845. San Antonio, TX - construction in progress 665,2296. Dallas (Allen), TX - construction in progress 429,8737. Detroit (Bloomfield Hills), MI - pipeline 602,1378. Guilford, CT - pipeline 154,9119. Southern Pines, NC - pipeline 635,700

4,261,109Total

Location GLA

(1)

(1) Acquired through joint venture.

Paseo Colorado - Pasadena, CA

Aspen Grove - Littleton, CA

Aspen Grove - Littleton, CA

Town Center Plaza - Leawood, KS

Town Center Plaza - Leawood, KS

Deer Park Town Center - Deer Park, IL

Village at Stone Oak - San Antonio, TX

39

Mixed Use Developments Land scarcity in key markets is creating increased focus on efficient land use

1. Los Angeles (Long Beach, CityPlace), CA Residential (complete) 2. Los Angeles (Long Beach, The Pike), CA Residential (complete), Hotel (pipeline)3. Miami, FL Residential (in progress)4. Raleigh (Apex), NC Office and Residential (pipeline)5. Seattle (Kirkland), WA Office, Residential, Hotel (pipeline)6. Columbus (Dublin), OH Office, Residential, Hotel (pipeline)7. Chicago (Deer Park), IL Office (pipeline)8. Southern Pines, NC Office and Residential (pipeline)9. Dallas (Allen), TX Office, Residential, Hotel (pipeline)10. Detroit (Bloomfield Hills), MI Office and Residential (pipeline)11. Pittsburgh (Mt. Nebo), PA Hotel (pipeline)12. Freehold, NJ Hotel (pipeline)13. Boise (Nampa), ID Hotel (pipeline)14. Kansas City (Merriam), KS Hotel (pipeline)

Location Uses (Status)

CityPlace - Long Beach, CA

The Pike at Rainbow Harbor - Long Beach, CA

The Shops at Midtown Miami - Miami, FL

The Shops at Midtown Miami - Miami, FL

Beaver Creek Commons - Apex, NC

Nampa Gateway Center - Nampa, ID

46

Urban Infill and Brownfield Developments Complex developments require expertise in entitlements and public assistance

1. Los Angeles (Long Beach - CityPlace), CA 295,3092. Los Angeles (Long Beach - The Pike), CA 215,9123. Boston (Everett), MA 639,8074. Miami, FL - construction in progress 634,2115. Horseheads, NY - construction in progress 699,1636. Seabrook, NH - pipeline 398,8057. Ukiah, CA - pipeline 665,3998. Boston (Norwood), MA - pipeline 95,242

Location GLA

3,643,848Total

47

International/Offshore Investments

48

Puerto Rico PortfolioOffshore experience has been highly successful

Portfolio Overview$1.2 billion acquisition (Jan. 2005)15 operating retail assets (4.9 MSF)3 of the 10 largest shopping centers and 13 of the 50largest shopping centers in Puerto Rico

Profitable component of overall portfolio (based on proportionateshare ownership of JV assets)

14% of Total Revenues 15% of Net Asset Value8% of Total GLA

49

Brazil Portfolio

Portfolio Overview$150 million acquisitionNine shopping malls (3.4 msf) and property management companySecond largest retail portfolio in Brazil66% of investment concentrated in the largest shopping mall under one roof in South AmericaIntent to double investment through development and third party acquisitions over the next three years

Retail Market OverviewFavorable economic, demographic and consumer trends Highly fragmented retail real estate ownershipSignificant cap rate compression anticipated as market evolves

50% joint venture interest in Sonae Sierra Brazil, a fully integrated retail real estate company based in Sao Paulo

50

Joint Venture Relationships

51

Joint ventures have been an integral component of our investment strategy

Macquarie DDR Trust (Australian Listed Property Trust)Invests in stabilized community shopping centers locatedin major U.S. metro areas Infinite life

Coventry Real Estate Fund II Sources diverse, high-yield value-add investments $1.3B fund3 year capital commitment period, 5 year life thereafter

52

$745

$1,500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

IPO Nov. 2003 12/31/04 12/31/05

Por

tfolio

Val

ue ($

mill

ions

)

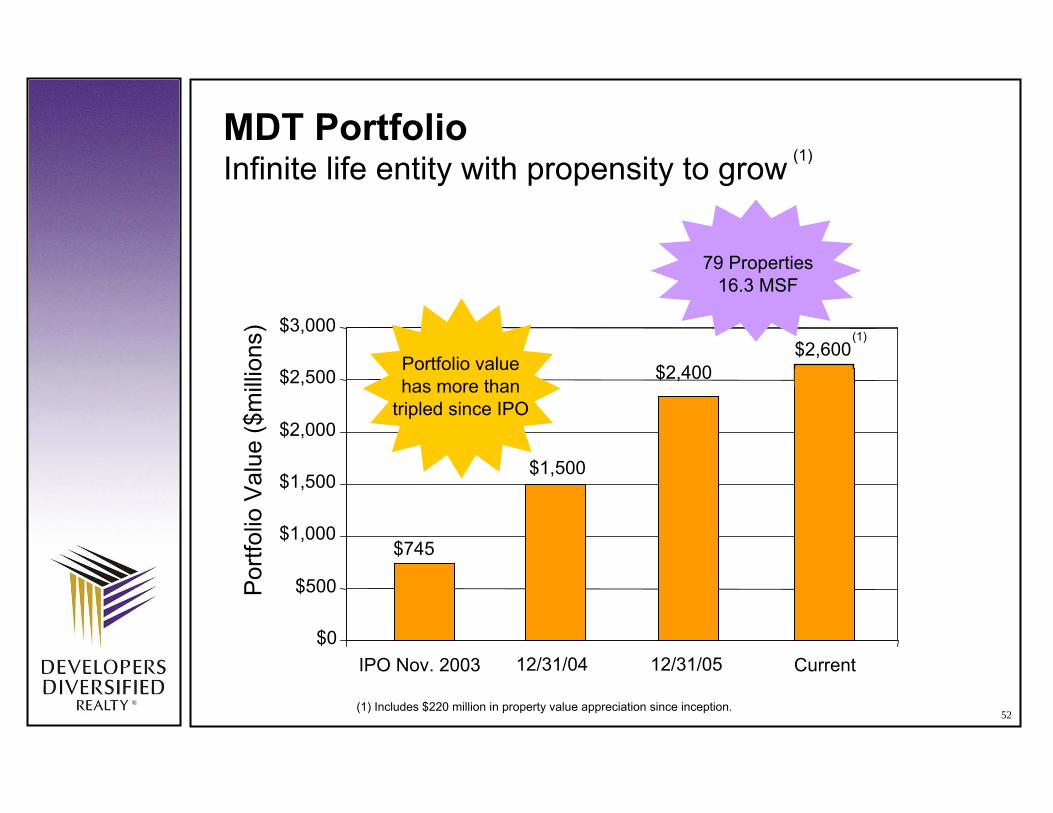

(1) Includes $220 million in property value appreciation since inception.

Portfolio value has more than

tripled since IPO

79 Properties16.3 MSF

$2,400

MDT PortfolioInfinite life entity with propensity to grow

Current

(1) $2,600

(1)

53

Our Coventry Fund II investments aggregate $1.3Bin anticipated project costs and over 8.4 MSF

TOTAL

535353

$1,2758,435,000

200$2,748,000Re-positioningNationwide10. Service Merchandise

270$730,000Development JVBloomfield Hills, MI

$

$

$

$

$

$

$

$

$

130420,000Development JVDallas, TX9. Watters Creek

39220,000Asset Re-positioningBenton Harbor, MI8. Fairplain Plaza

2201,300,000Mall Re-positioningCincinnati, OH7. Tri-County Mall

35308,000Development JVKansas City, MO6. Merriam Village

96737,000Mall Re-positioningAnaheim, CA5. Buena Park Downtown

40230,000Development JVSan Antonio, TX4. Westover Marketplace

85715,000Mall Re-developmentPhoenix, AZ3. Phoenix Spectrum

80290,000Mall Re-developmentSeattle, WA2. Totem Lakes Malls

66737,000Mall Re-developmentKansas City, MO1. Ward Parkway

Anticipated Project Cost ($Millions)SFInvestment TypeLocationAsset

11. Bloomfield Park

14$PendingPending12. Pending

54

Kuwait Financial Centre (80%)

$ 27.5Paradise Village; Phoenix, AZ

Churchill Family Trust (33%)

$ 202.413 grocery-anchored centers

$ 167.47 centers in CA, FL, IN, OH and VA

Kuwait Financial Centre (80%)

$ 6.61 MO centerSansone Group (50%)

$ 25.51 OH centerState Teachers Retirement Board of Ohio (50%)

$ 25.91 OH centerCasto Properties (20.55%)

$ 21.01 OH centerCasto Properties (50%)

$ 266.26 centers in AZ, MN, OR and TXDRA Advisors (50%)

$ 130.412 grocery-anchored centersPrudential Real Estate Investors (90%)

$ 33.9Shops at Techridge; Austin, TXPrudential Real Estate Investors (74.25%)

Coventry Real Estate Partners (1%)

$ 121.03 centers in CA and WA Prudential Real Estate Investors (79%)

Coventry Real Estate Partners (1%)

$ 84.0 Deer Park Town Center; Deer Park, IL

Prudential Real Estate Investors (74.25%)

Coventry Real Estate Partners (1%)

UndepreciatedBook Value

(in millions)AssetsPartner & Ownership %

Other Joint Ventures

$ 71.1

$ 224.5

$ 240.0

$ 7.1

$ 49.9

$ 54.0

$ 59.9

$ 398.0

$ 145.6

$ 62.0

$ 160.0

$ 140.0

158.55%

10.92%

43.37%

6.82%

95.69%

108.49%

185.24%

49.51%

11.66%

82.98%

32.23%

66.67%

FMV (in millions)

TOTALS $ 1,111.80 $ 1,612.10 45.00%

% Change(1)

(1) Fair market value is based on market-based cap rates.

56

We have strengthened our competitive position through a series of strategic acquisitions

$3

$5

$7

$9

$11

$13

$15

$17

$19

$21

$23

4Q02 4Q03 4Q04 4Q05 Post IRRETIMerger

280

360

440

520

600

680

760

840

Total Franchise ValueNumber of Properties

• 286 Assets • 58 MSF • $5.0B TFV

• 362 Assets • 83 MSF • $7.6B TFV

• 458 Assets • 103 MSF • $11.4B TFV

• 496 Assets • 113 MSF • $13.9B TFV

Tota

l Fra

nchi

se V

alue

($ B

illion

s)

Num

ber of Properties

BendersonDevelopment

Caribbean Property Group

JDN Realty

• 809 Assets • 162 MSF • $21.8B TFV

• March 2003 • $1.0 Billion • 81 Properties, 15 MSF • 21 Development

Properties, 7 MSF

• May-December 2004 • $2.3 Billion • 107 Properties • 18 MSF

• January 2005• $1.2 Billion• 15 Properties • 5 MSF

Inland Retail 1Q07

• $6.2 Billion • 307 Properties • 43.6 MSF