Embed Size (px)

DESCRIPTION

Internship ReportFinancial Statement AnalysisFirst Security Islami Bank Ltd.by Moez Ansary

Citation preview

Financial Statements Analysis of an

Islami Bank in Bangladesh

A Study on First Security Islami

Bank Limited, Bangladesh

Internship Report

on

“Financial Statements Analysis of an Islami Bank in Bangladesh:

A Study on First Security Islami Bank Limited, Bangladesh”

Supervised By:

Mr. Iehit Sharma

Senior Lecturer

Department of Business Administration

Leading University, Sylhet

Submitted By:

Moez Al Azim Ansary

ID: 1101010183

Major in Accounting & Information Systems

BBA Program

27th Batch

Department of Business Administration

Leading University, Sylhet

Submitted To:

Department of Business Administration

For the partial fulfillment of the requirements for the

Degree of Bachelor of Business Administration (BBA)

Major in Accounting & Information Systems (AIS)

at

Leading University

Sylhet, Bangladesh

Date of Submission: February 28, 2015

:v.r6FrRgRFffi<rt<eft:ritd d,ii s.)t-l ulllr$y,. .. r[i rt nst sEcu RlrY ts LAM I BAN K trD.

FSIBL/AMBI2O|5I25

Date 05.01 .2015

To whom it may Concern

This is to certify that Mr. Moez Al Azim Ansary S/o Abdul Hannan Ansary of 68 Payra

Jhamarpar, Dargah Moholla, Sylhet, an intern from Leading University, Sylhet has

completed his internship program at our Branch with adequate dedication sincerity &responsibility. During the three months period Mr. Moez Al Azim Ansary rotatedhimself to various working desk at the branch and has learned many primary level and

useful practical banking functions.

We wish him every success in life.

2-al{Md. Sohrab Uddin MollaAsstt Vice President & Manager

AMBARKHANABRANCH: ;

MWenCornplex,Holding#&f0,641,WalrebsBSS,WestAmbarkhana,Sylhet-3100

; www.fsiblbd.com

iv

Letter of Transmittal

February 28, 2015

Mr. Iehit Sharma

Senior Lecturer

Department of Business Administration

Leading University, Sylhet

Subject: Submission of Internship Report

Dear Sir,

With the passage of time, I am now standing on the verge of Bachelors of

Business Administration program, hence am finalized with my Internship Report

named “Financial Statements Analysis of an Islami Bank in Bangladesh: A

Study on First Security Islami Bank Limited, Bangladesh”. Vividly enough, my

research comprises adequate endeavors. But no doubt, my contribution will be

best evaluated on your sharp scale of acceptance and remarks.

Consequently, I am transmitting my Internship Report to your very concern.

Hopefully you will discover my well-researched, informative and innovative

approach as a hallmark of exploration. Rather, in case of any further clarification

or elaboration as to my research work, I would welcome the opportunity to

consult with you to explore how my findings could best meet your needs.

Thanking you.

Yours Sincerely,

___________________________ Moez Al Azim Ansary

ID No: 1101010183

Major: Accounting & Information Systems

BBA Program (27th Batch)

Department of Business Administration

Leading University, Sylhet

v

Letter of Acceptance

February 28, 2015

This is to certify that Internship Report titled “Financial Statements Analysis

of an Islami Bank in Bangladesh: A Study on First Security Islami Bank

Limited, Bangladesh” is submitted in partial fulfillment of the requirements for

the award of the degree in Bachelor of Business Administration from Leading

University, Sylhet is a record of the analysis carried out by Moez Al Azim Ansary,

ID No-1101010183 under my active supervision and guidance as the partial

fulfillment for the award of BBA degree.

I wish his success in the future.

Supervisor

___________________________________

Mr. Iehit Sharma

Senior Lecturer

Department of Business Administration

Leading University, Sylhet

vi

Declaration

I, Moez Al Azim Ansary, a student of BBA program at Leading University, Sylhet,

solemnly affirm and hereby declare that the Internship report titled “Financial

Statements Analysis of an Islami Bank in Bangladesh: A Study on First

Security Islami Bank Limited, Bangladesh” submitted in partial fulfillment of

the requirements for completion of the degree in Bachelor of Business

Administration at Leading University, Sylhet.

I also declare that this report is prepared after completing my three months

Internship period in First Security Islami Bank Limited, Amborkhana Branch,

Sylhet. This is my original work and not submitted for the award of any other

Degree, Diploma Fellowship or other similar title or prizes. It is prepared under

the extensive supervision and guidance of Mr. Iehit Sharma, Senior Lecturer,

Department of Business Administration, Leading University, Sylhet.

Declared by

___________________________ Moez Al Azim Ansary

ID No: 1101010183

Major: Accounting & Information Systems

BBA Program (27th Batch)

Department of Business Administration

Leading University, Sylhet

vii

Acknowledgement

First, I would like to express my gratitude to almighty ALLAH to give me the

strength to complete the study within the stipulated time.

I deeply thank to my honorable internship supervisor Mr. Iehit Sharma, Senior

Lecturer, Department of Business Administration, Leading University for

assigning me the project and for all his kind support to accomplish it. His

valuable suggestions and guidance helped me a lot to prepare the report in a

well-organized manner. I would like to thank our whole Department of Business

Administration specially Head of the Department Dr. Tofayel Ahmed, for

facilitating me to do internship and preparing this report.

I also wish to thank and give the due respect to my family and friends for their

cordial support and help they offered throughout the process of performing the

whole report.

Finally, my heartfelt gratitude goes to Mr. Md. Sohrab Uddin Molla (Branch

Manager and AVP), Mr. Md. Maksud Ibn Mustafa (SPO and Operation Manager),

Mr. Salahuddin Shamim (Probationary Officer), Mr. Md. Ishtiaque Uddin

(Probationary Officer), Mr. Anwar Hossain Misba (Senior Cash Officer), Mr. Ariful

Islam Nayeem (Assistant Officer), Mrs. Rabea Binte Shiraj (Principal Officer) and

all the co-workers of First Security Islami Bank Limited, Amborkhana Branch,

Sylhet for their keenness in giving me training and valuable information, which

was very helpful to complete my internship report.

viii

Executive Summary

Banks are the most important financial institutions in modern economy. They

are an integral part of modern economic activities. In a developing country like

Bangladesh, the Islamic banking system as a whole has a vital role play in the

process of economic development. First Security Islami Bank Limited (FSIBL) has

started its journey on 29th August 1999 with the said principles in mind and

conduct banking system according to Shariah based policy. This report mainly

deals with the financial statements analysis of an Islami bank in Bangladesh: a

study on First Security Islami Bank Limited. The horizontal analysis, vertical

analysis and ratio analysis are essential technique for financial statements

analysis. Different users such as investors, management, bankers and creditors

use the financial statements analysis of a company for their decision making

purpose. In this report, the financial statements of First Security Islami Bank

Limited have been studied for five years from 2009 to 2013 and also different

types of financial ratios of the bank are calculated. The clear concept on bank,

Islamic banking and different types of financial analysis are given in the report.

The liquidity, profitability, financial position and the financial trend of First

Security Islami Bank Limited are the main focus of this report which have been

analyzed and used for comparing different years. By analyzing the financial

statements of the bank, it has been traced the financial strengths and weakness

of the bank. Finally some comments are shown regarding the changes of this

bank’s financial performance for the last five years. By analyzing the horizontal,

vertical and different ratios like liquidity ratios, efficiency ratios, profitability

ratios, solvency ratios and market prospect ratios, and cash flow analysis, it can

be said that FSIBL has been improving and doing well in the last five years except

in few years. So the bank should be concern about the types of financial analysis

especially the types of ratios. However, FSIBL’s overall earnings performance

was satisfactory, but it should be improved.

ix

Table of Contents

Chapter Title Page No. One Introduction 1-6

1.1

1.2

1.3

1.4

1.5

1.6

1.7

Origin of the Report

Significance of the Study

Objective of the Study

Scope of the Study

Methodology of the Study

Sources of Data

Limitation of the Study

2

2

3

3

4

5

6

Two Theoretical Overview 7-45

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

2.10

2.11

Bank

Functions of Bank

Islamic Banking

2.3.1: Principles of Islamic Banking

2.3.2: Riba or Interest

Difference between Riba and Profit

Difference between Conventional Banking and Islamic

Banking

Financial Statements

Components of Financial Statements

Components of Bank’s Financial Statements

Financial Statements Analysis

Techniques to Financial Statements Analysis

Literature Review

2.11.1: Classification of Assets and Liabilities

2.11.2: Limitations of Financial Statements

2.11.3: Building Blocks of Financial Statement

.................Analysis

2.11.4: Horizontal Analysis

2.11.5: Vertical Analysis

8

9

14

15

15

16

17

18

19

19

20

20

21

22

24

25

25

28

x

2.12

2.11.6: Ratio Analysis

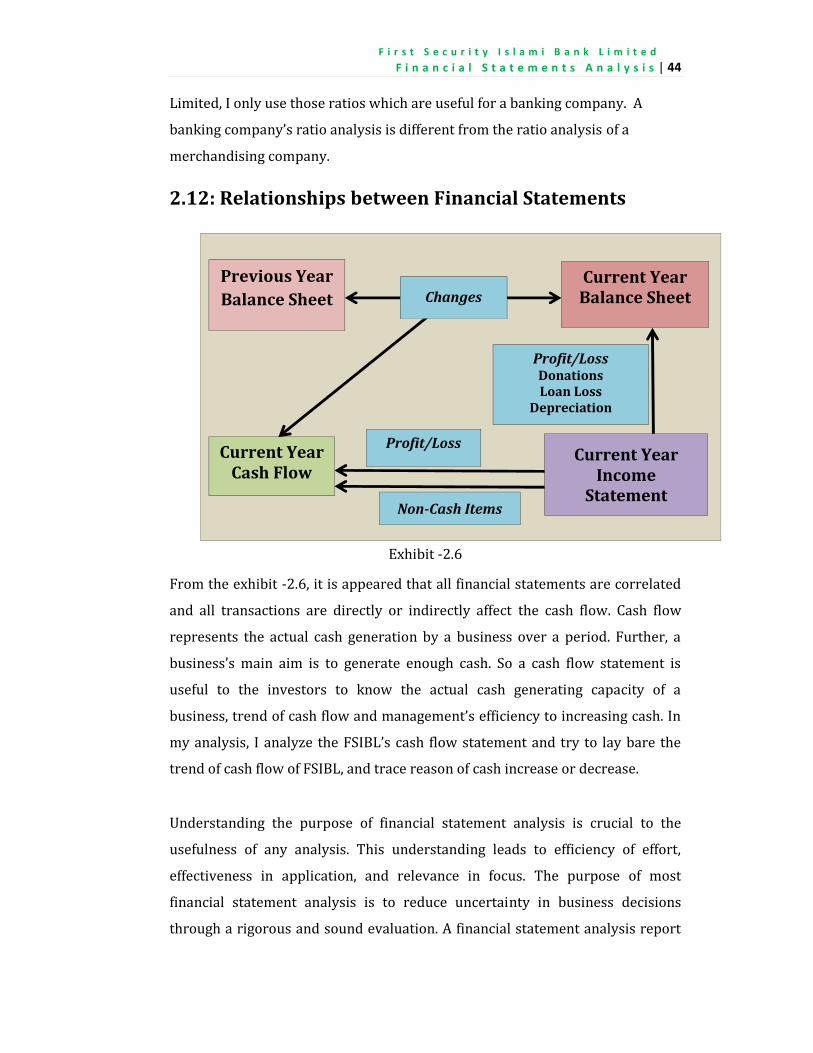

Relationships between Financial Statements

30

44

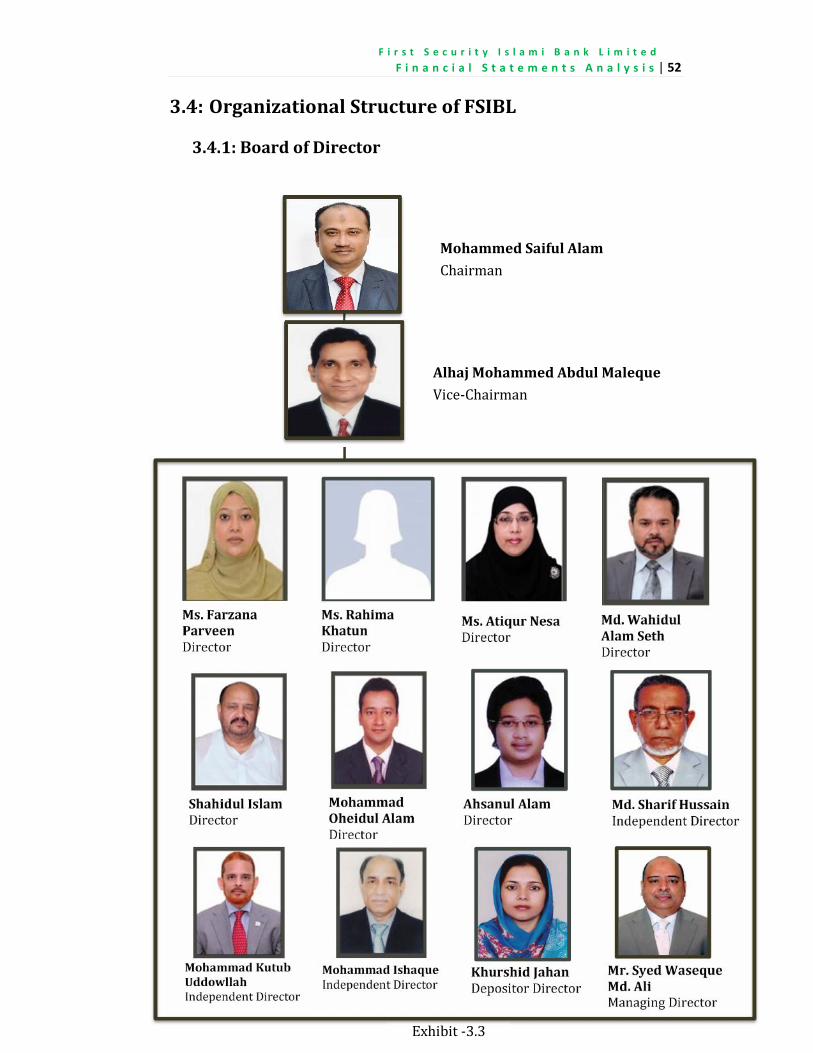

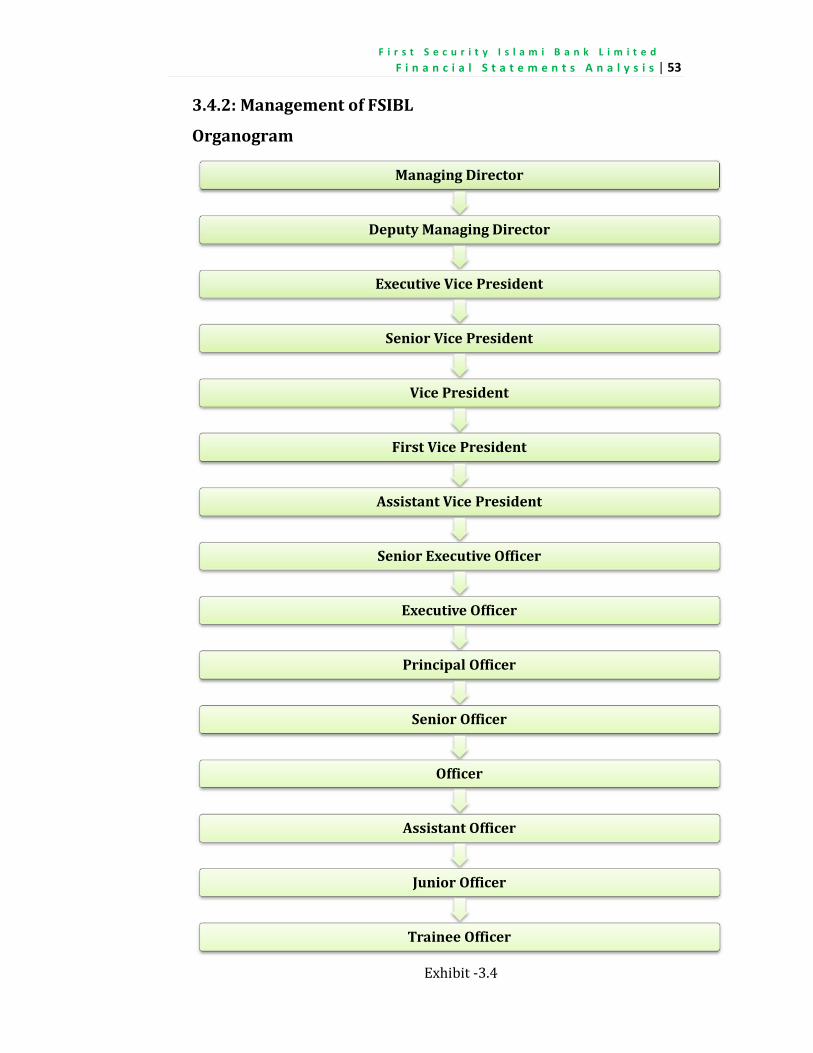

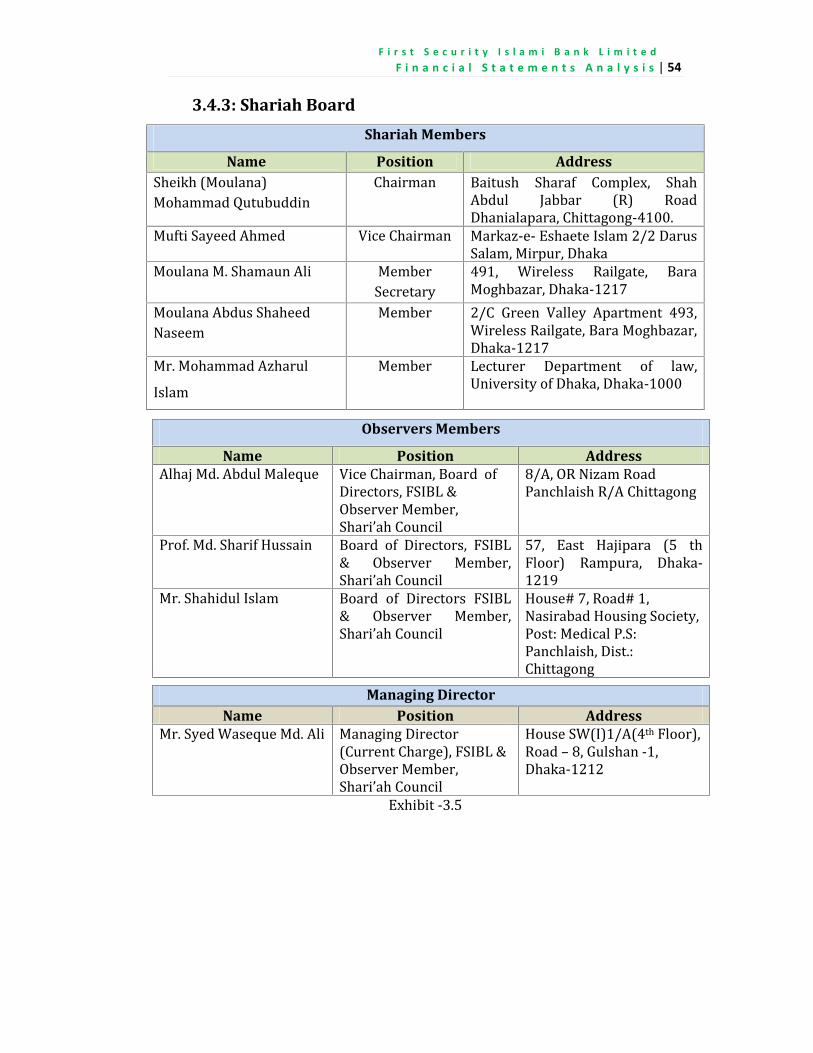

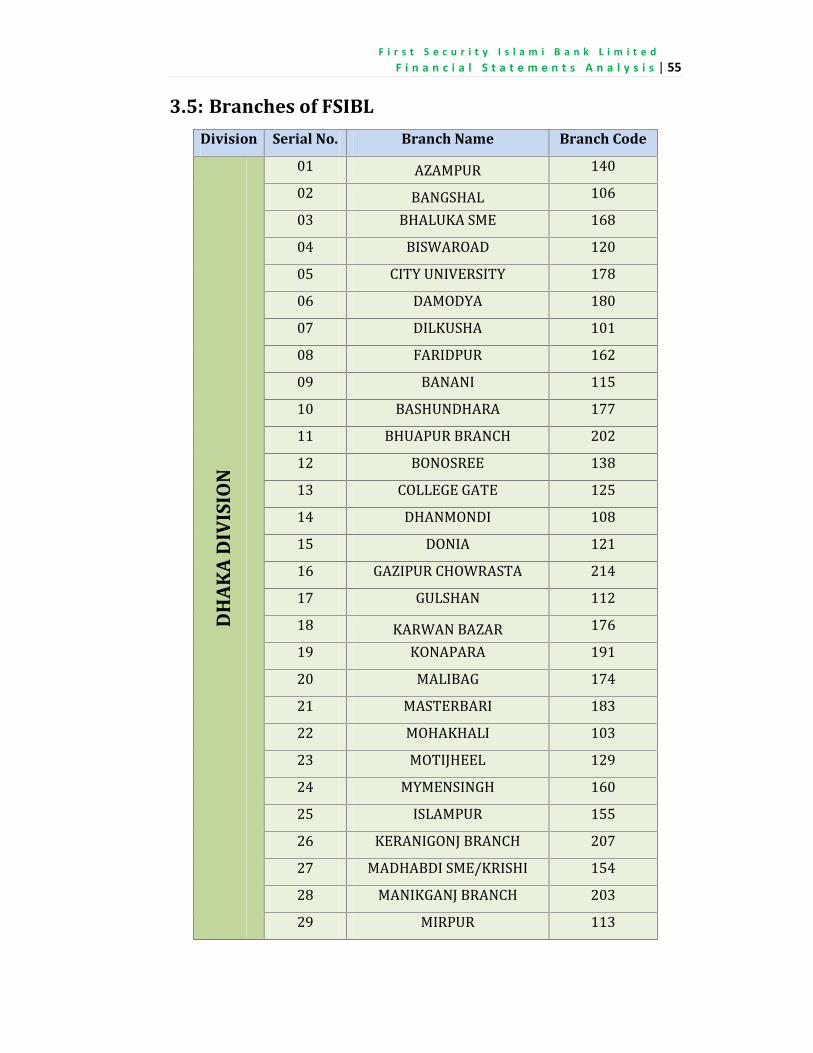

Three Organizational Overview 46-63

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

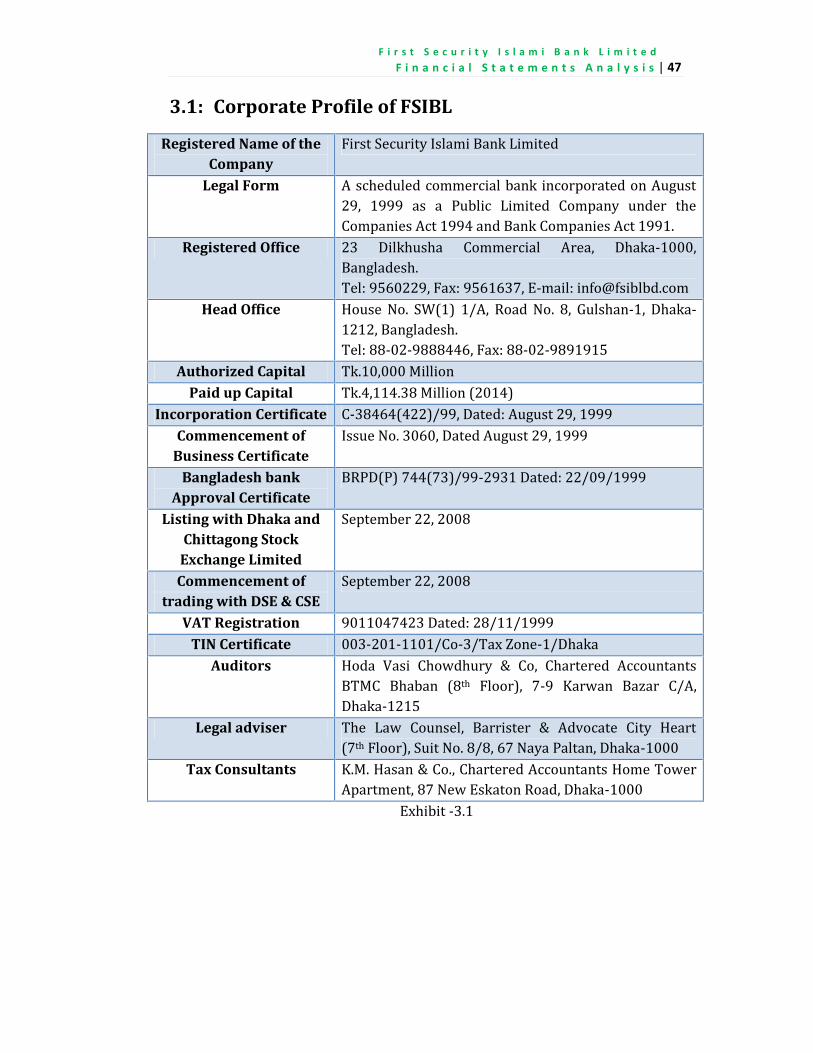

Corporate Profile of FSIBL

Historical Background of FSIBL

Vision, Mission, Objective and Strategies of FSIBL

Organizational Structure of FSIBL

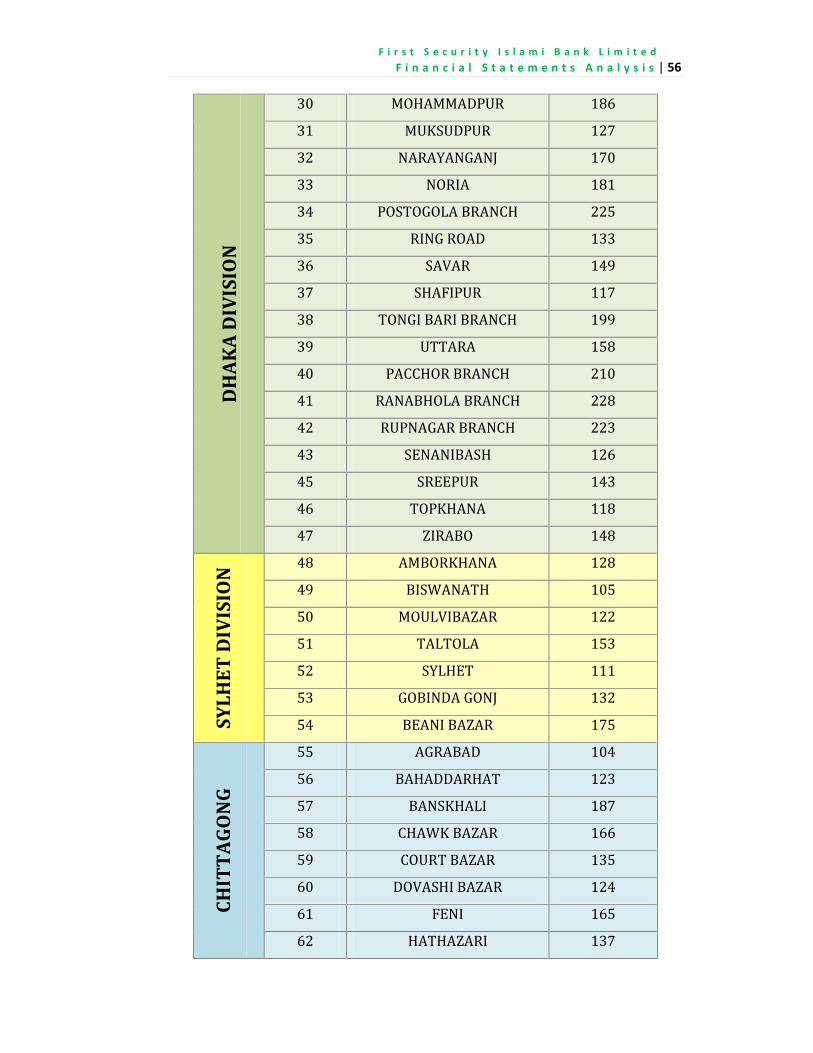

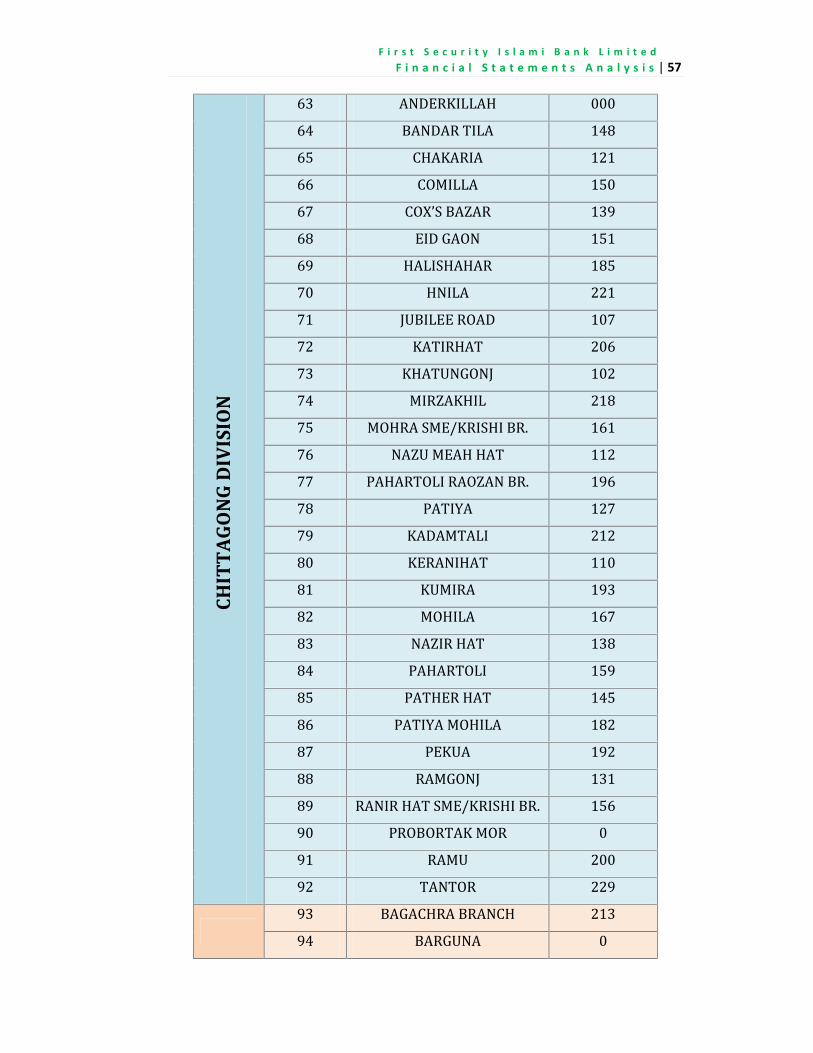

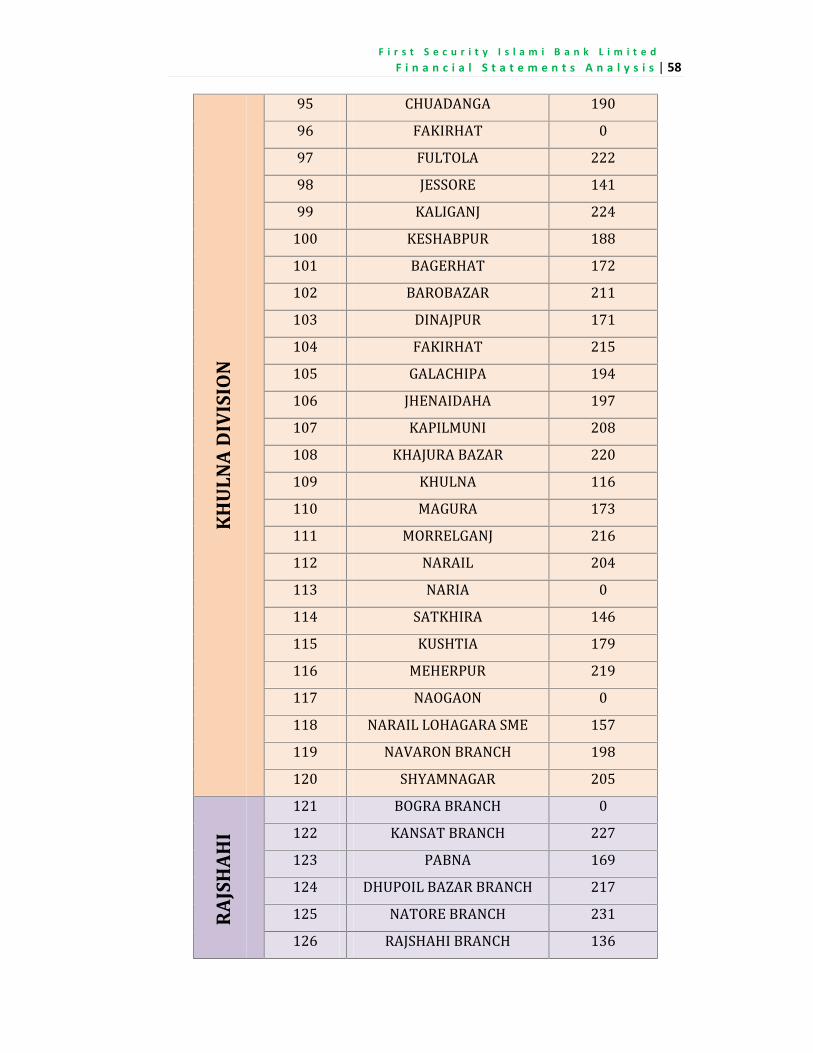

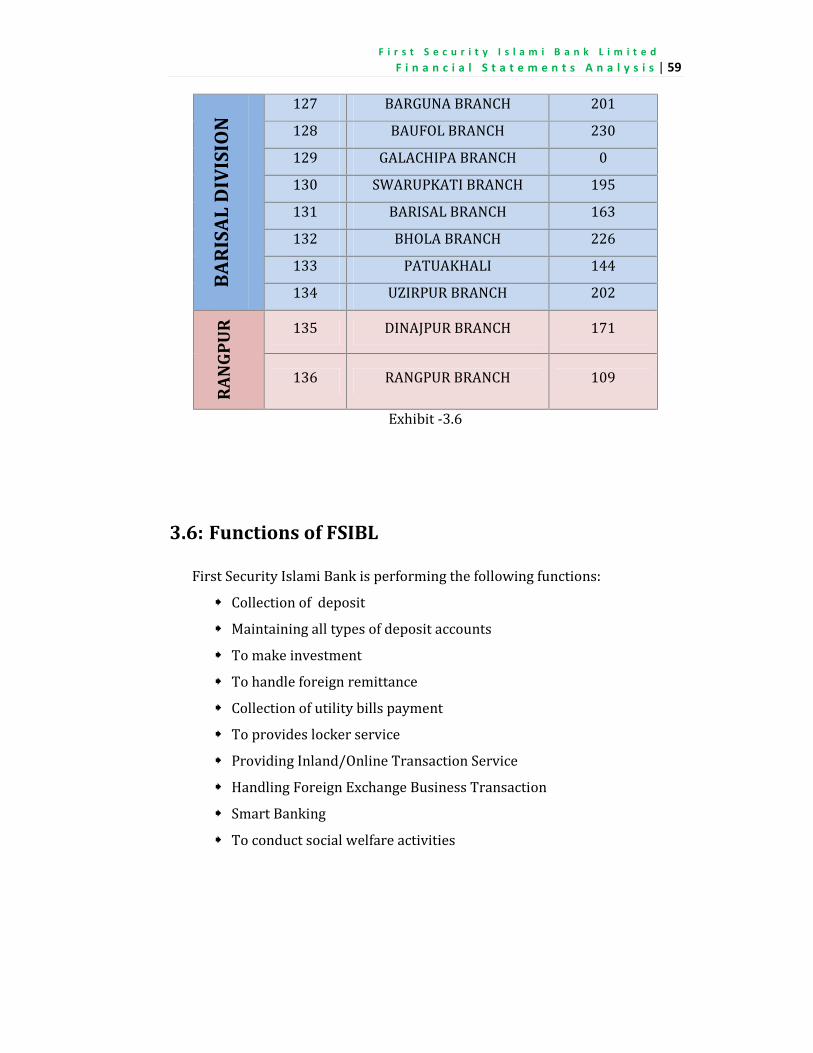

Branches of FSIBL

Functions of FSIBL

Features of FSIBL

Principal Products & Services of FSIBL

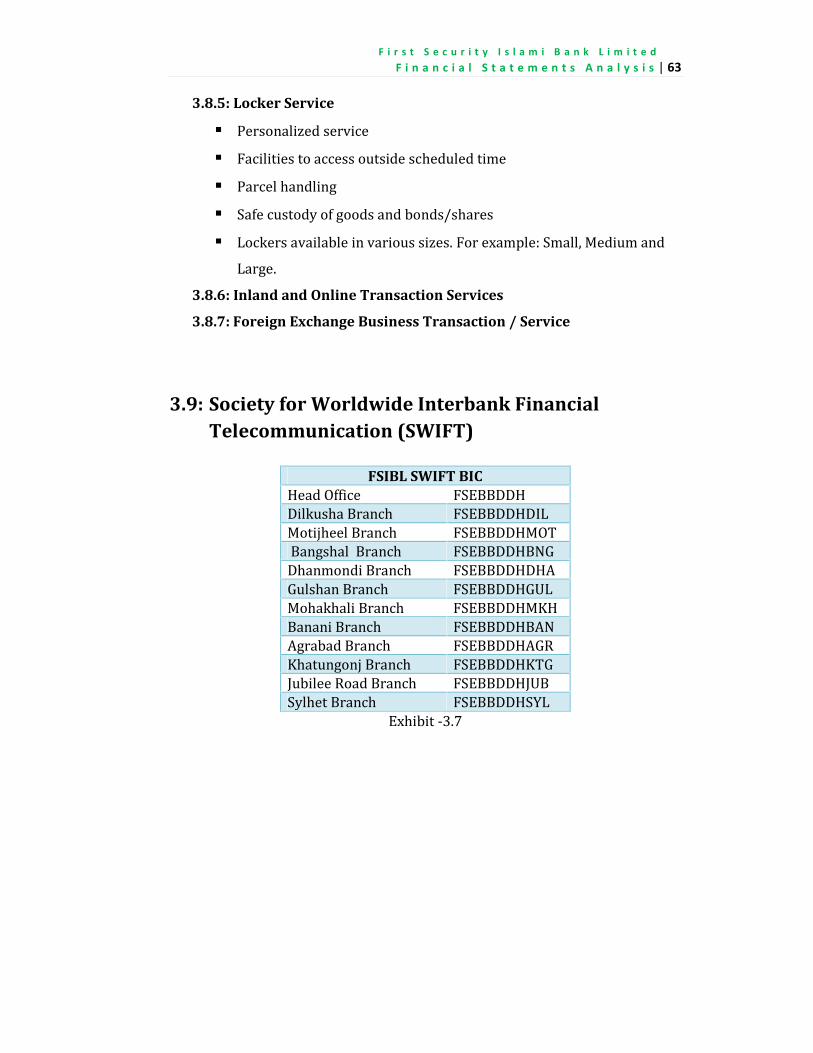

Society for Worldwide Interbank Financial

47

49

50

52

55

59

60

61

63

Four Core Part : Financial Statements Analysis of FSIBL 64-100

4.1

4.2

4.3

4.4

4.5

4.6

Introduction

Reconstruction of Financial Statements of FSIBL

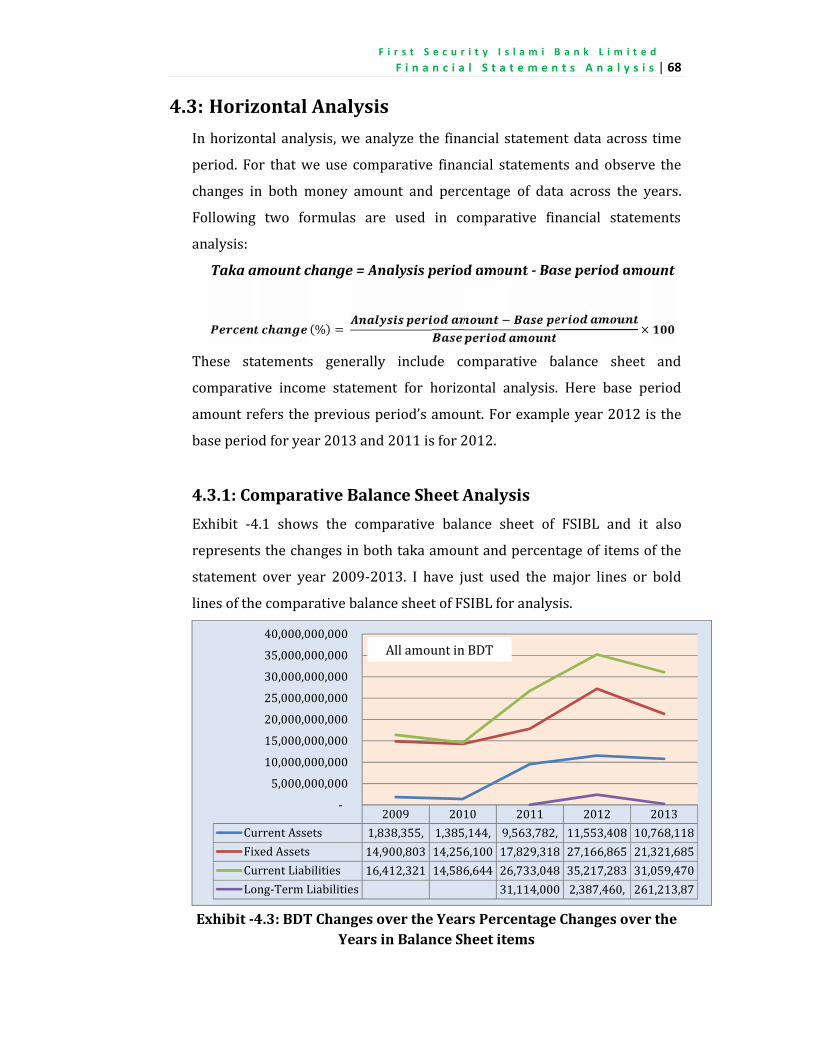

Horizontal Analysis

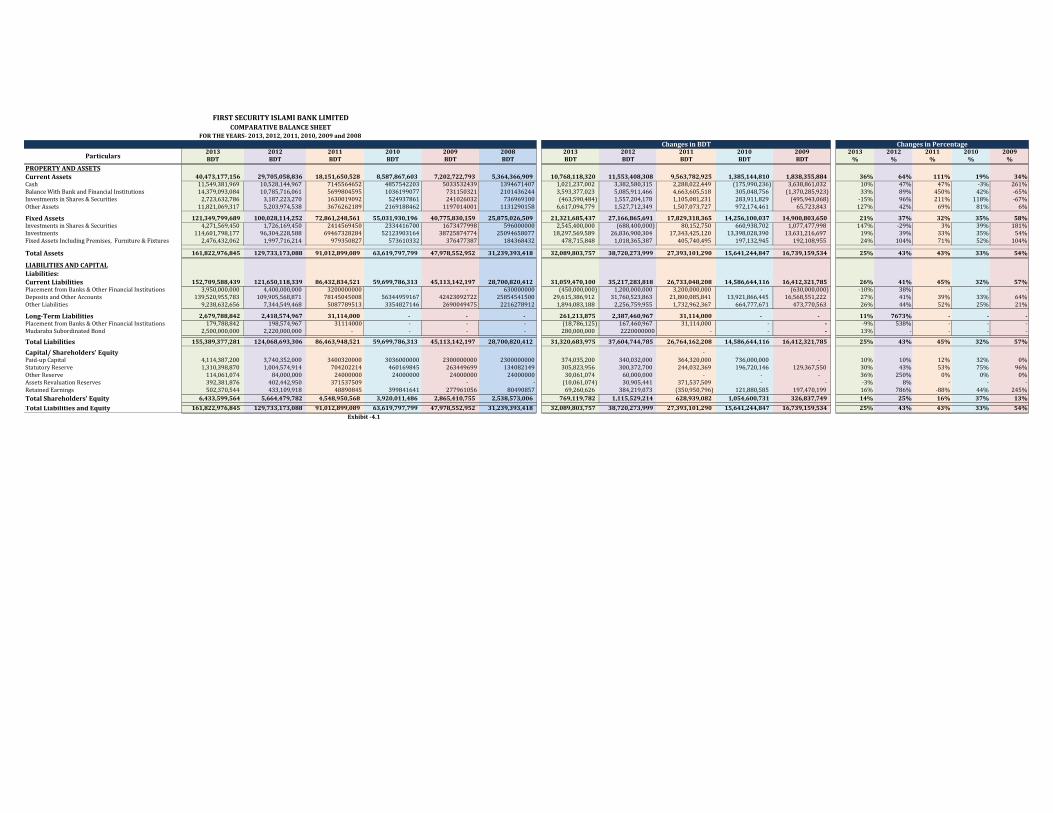

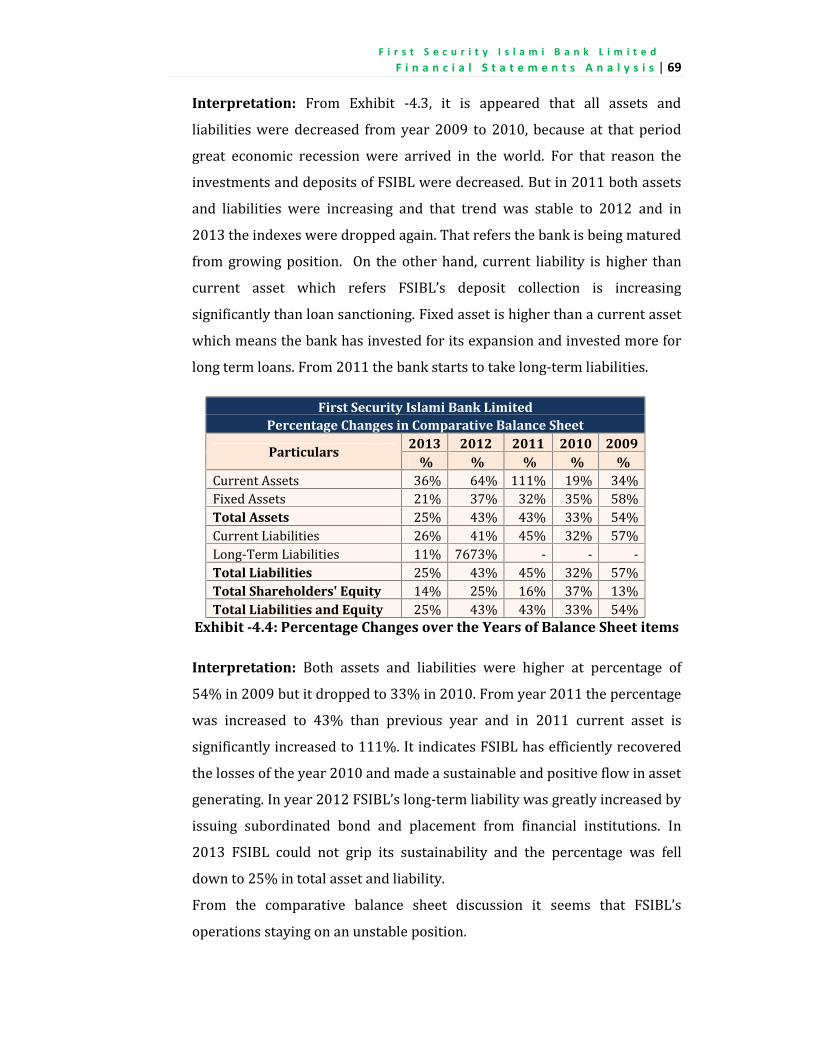

4.3.1: Comparative Balance Sheet Analysis

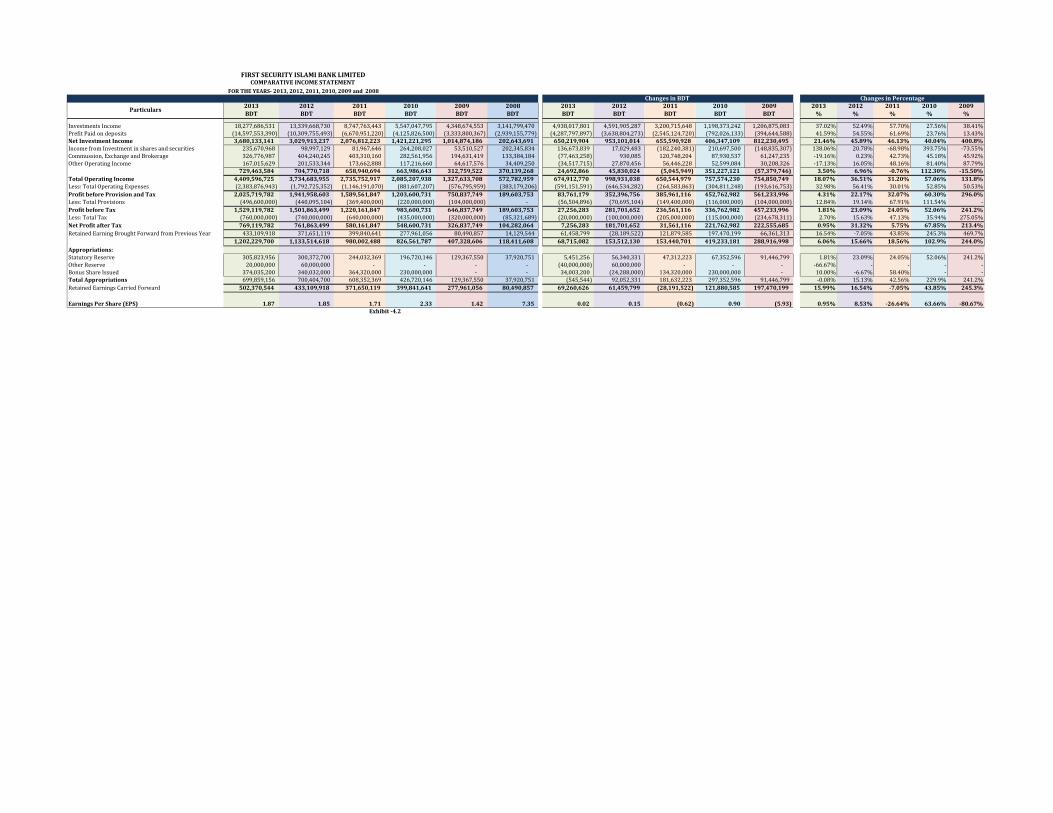

4.3.2: Comparative Income Statement Analysis

4.3.3: Trend Analysis

Vertical Analysis

4.4.1: Common-size Balance Sheets Analysis

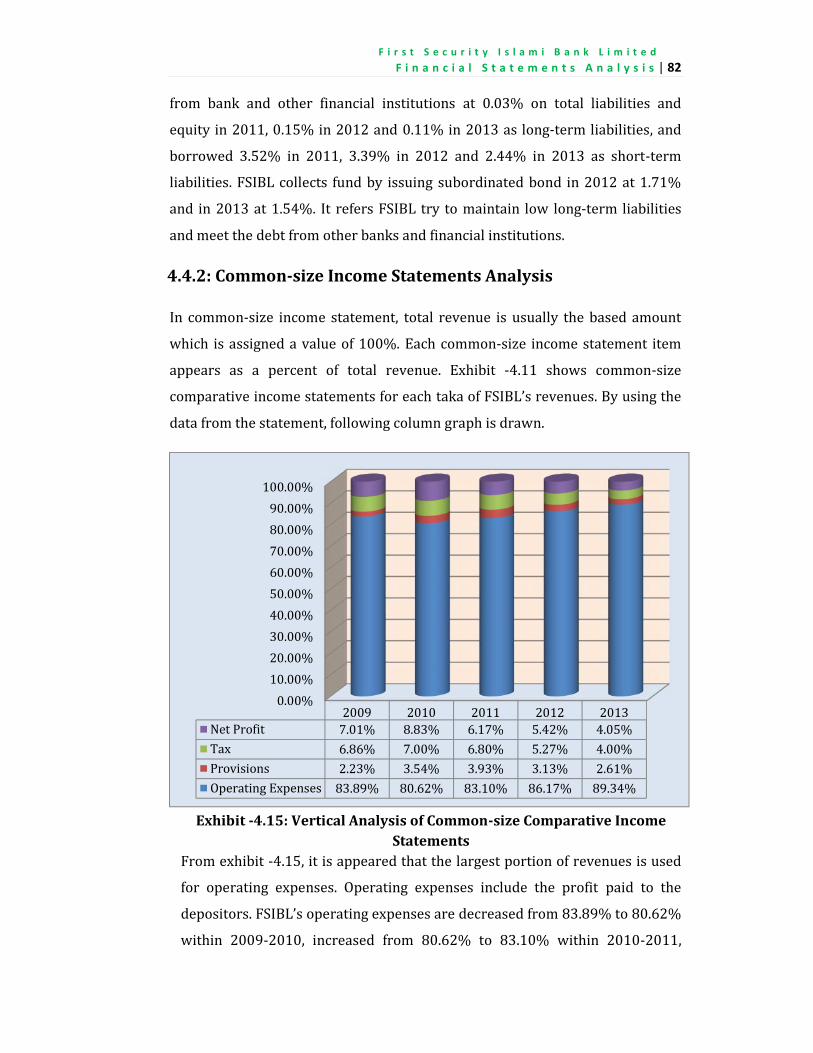

4.4.2: Common-size Income Statements Analysis

Ratio Analysis

4.5.1: Liquidity and Efficiency Ratio

4.5.2: Solvency Ratio

4.5.3: Profitability Ratio

4.5.4: Market Prospects Ratio

Analysis of Cash Flow Statement

65

65

68

68

70

73

76

79

82

83

83

89

93

96

98

Five Findings, Recommendation and Conclusion 101-106

5.1

5.2

5.3

Findings

Recommendations

Conclusion

102

105

106

xi

References

Appendix

107

109

1

Introduction

Chapter One

Introduction

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 2Financial statement analysis is the process of reviewing and analyzing acompany's financial statements to make better economic decisions. Thesestatements include the income statement, balance sheet, statement of cashflows, and statement of retained earnings. Financial statement analysis isrequired for evaluating risks, performance, financial health, and futureprospects of an organization. In this report, the financial statements of FirstSecurity Islami Bank Limited (FSIBL) are analyzed. FSIBL is one of the reputedbanks in Bangladesh. It conducts its banking activities according to IslamiShariah.1.1: Origin of the ReportThis report on “Financial Statements Analysis of an Islami Bank inBangladesh: A Study on First Security Islami Bank Limited, Bangladesh” hasbeen prepared as a partial requirement for the completion of the internshipprogram for the Bachelor of Business Administration (BBA) program ofLeading University, Sylhet. For internship purpose, I chose First SecurityIslami bank Ltd. (FSIBL), Ambarkhana Branch, Sylhet. The preparation ofthis report was supervised by Mr. Iehit Sharma, Senior Lecturer, LeadingUniversity, Sylhet.1.2: Significance of the StudyFirst Security Islami Bank Ltd. is one of the leading private banks inBangladesh. It provides highest benefits to its clients among the IslamiBanks in Bangladesh. There are few private banks those provide profits orinterest to their clients as high as FSIBL. FSIBL’s banking system is aiming toattain the goal of Islamic Economy through setting well designed IslamicMonitory System. Islam has clear-cut guidelines to avoid interest (Riba)regarding use of money. So, Islamic Banking System strongly follows theIslamic Shariah in its business. Islamic Shariah appreciates risk and profitsharing. As an Islami bank FSIBL has to take risk when doing banking

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 3business and share profit to its stakeholders and customers. So, to knowabout the ability of the bank to take risk and making profits, its financialstrength and performance should be understood. Therefore, the financialstatements of the bank should be analyzed for understanding the financialstrength and performance of the bank.1.3: Objective of the Study

General Objective:

To analyze the financial statements of First Security Islami Bank Ltd.with the key focus of its overall financial performance.Specific Objectives:

To know the current financial position of First Security Islami BankLtd. To know the five years financial performance of FSIBL by calculatingand analyzing different types of ratio. To know the financial trend of FSIBL focusing the five years’ financialperformance. To get the practical experience on banking activities. To give some recommendation for the development of First SecurityIslami Bank Ltd.

1.4: Scope of the StudyThis report is based on my observation and studies during my internshipperiod in First Security Islami Bank Limited, at Amborkhana Branch. Theprime focus was on financial statement analysis of First Security Islami BankLimited for giving some concepts about the financial position and financialperformance of the bank over at least five years. The scope of my study islimited to the First Security Islami Bank Limited. During the three monthsinternship program almost all sections I have been observed. However, inthis report the financial statements of FSIBL are analyzed from differentviewpoint including ratio analysis. This repost may help those people who

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 4want to know about the financial performance of First Security Islami BankLimited.1.5: Methodology of the StudySeveral types of research methods are used in studies depending on the fieldor research. As this research is on financial statement analysis, certainmethods were followed to fulfill the objectives of the report, making themaximum utilization of the scopes and to avoid the limitations as much aspossible to prepare the final outcome of the report. There are four types ofresearch methods were used to complete this report. These methods are -

Qualitative Method: Qualitative method is concerned with the quality orkind and describing meaning. In this report I have used qualitativeresearch method to provide a clear concept about my research topic andto maintain the standards of my research I have analyzed the financialstatements from different viewpoint. Quantitative Method: Quantitative research is based on the quantitativemeasurements of some characters. It is applicable to phenomena that canbe expressed in terms of quantities. I have used the quantitativeapproaches in this report for some statistical content analysis and todetermine the significance of findings. Analytical Method: In analytical research, the researcher has to use factsor information those already available, and analyze these to make acritical evaluation of the material. In this report, I have used analyticalmethod for ratio analysis and to evaluate the financial performance ofFSIBL. Descriptive Method: Descriptive research includes surveys and fact-finding enquiries of different kinds. The major purpose of descriptiveresearch is description of the state of affairs as it exists at present. In thisrepost, I have used the descriptive approach to explain the financialstatements, graphs, ratios, financial trend, financial performance andcurrent financial condition of FSIBL.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 5Financial statement analysis needs the combination of mathematicalequations, graphical presentation and explanation. So, I have used abovefour types of research methods to get proper and successful outcome frommy research.1.6: Sources of DataData have been collected from two sources such as primary sources of dataand secondary sources of data. Primary sources of data are those sourcesfrom which the researcher collects data directly by field work. Andsecondary sources of data are those sources which provide data that arealready collected by another researcher. From this point of view data aretwo types among them one is primary data and another is secondary data.The data directly collected by the researchers are called primary data. Thedata that has been already collected by another researcher or person forhis/her work purpose are called secondary data. I have collected the bothtypes of data from primary and secondary sources.

Primary Sources of Data:

Face to face conversation with the employees,senior officers, SPO and the Manager. Studying different relevant files like register books,statement of affairs, financial statements etc. Practical work at FSIBL during my internshipprogram to increase my knowledge.

Secondary Sources of Data:

Annual Reports including financial reports of FSIBL. Website of FSIBL. Journals and prospectus of FSIBL. Different books, magazines and journals related tothe finance and banking. Different websites and blogs.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 6

1.7: Limitation of the StudyI did my best and there has no dearth of sincerity on my part to make thereport. But there are some limitations which I have faced while reaching theobjectives of this report, because it is very difficult to analyze the financialstatements over five years of a Bank. Some of these following limitations areapparent in this study: The time limit of the internship is only 3 months which is very shortperiod of time to learn about whole banking activities. As annual reports need 3-4 months to be published after end of theperiod, I cannot collect the recent annual financial report (2014) ofFSIBL. As final financial statements are prepared in head office, it becomesdifficult to understand the elements of the statements from branchoffice. When I have prepared the classified financial statement fromunclassified one then I faced problem to replacement of the items ofthe statement, because the duration of all items are not properlymentioned. There were lack of proper secondary information about FirstSecurity Islami Bank Limited and its products. Annual reports,policy guidelines, website and other related documents do not coverfull and sufficient information. As the bank officials are so much busy that it was difficult for themto co-operate with me, which is also a constraint for this report.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 7

Chapter Two

Theoretical Overview

2

Theoretical Overview

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 8

2.1: BankBank is a financial institution that collects money from people as depositcommitting to pay interest or profit at a fixed or probable percentage rateto the depositors for their deposited money and lends or invests it to thebusinesses requiring interest or profit as return at a fixed or probablepercentage rate which is higher than the rate at which it pays interest orprofit to the depositors against the loan or investment and gains profitfrom the difference between the interest or profit against loan orinvestment and interest or profit against deposits. In broadly, anyfinancial institution that receives, collects, transfers, pays, exchanges,lends, invests or safeguards money for its customers is called bank.Generally we indicate the commercial bank when using the term “Bank”.Commercial banks are those institutions which conduct the businesspurely on profit motive. Commercial banks receive surplus money fromthe people who are not using it and lend to those who need it forproductive purpose.A commercial bank is a dealer in short and medium-term credit. Itborrows money from a group of people at a lower rate of interest andlends to the other group of people at some higher rate of interest. Thedifference between the two rates of interest is the profit of the bank.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 9

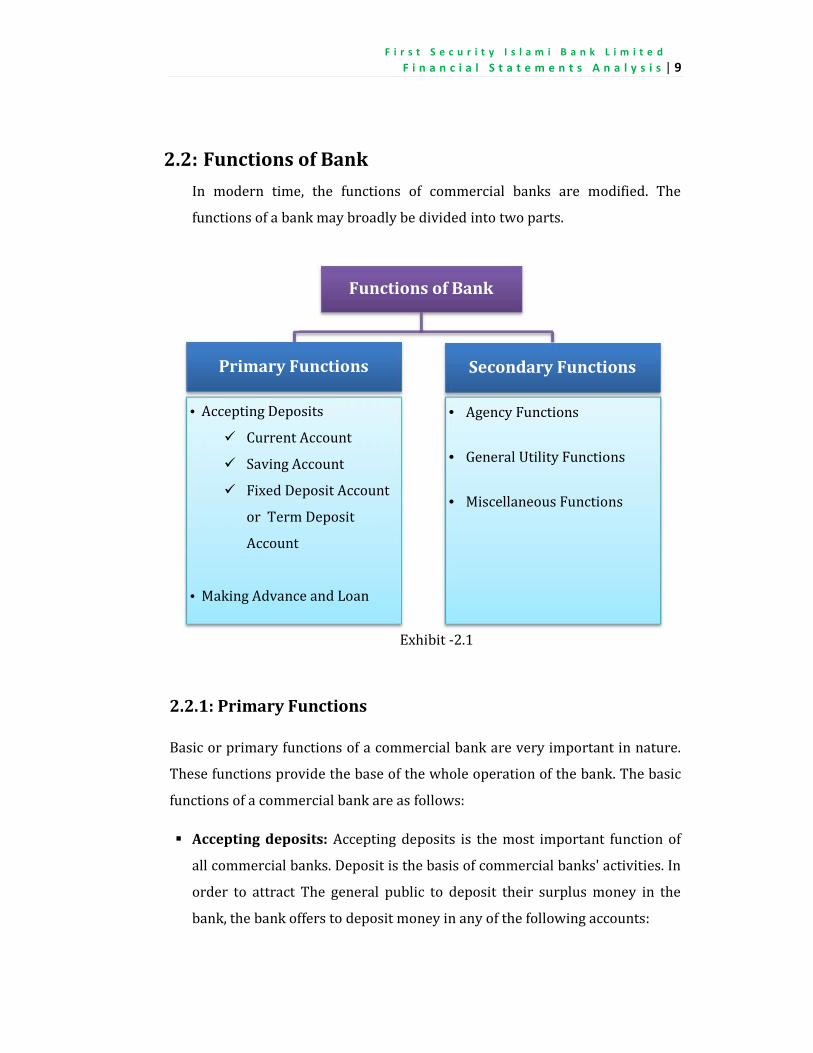

2.2: Functions of BankIn modern time, the functions of commercial banks are modified. Thefunctions of a bank may broadly be divided into two parts.

Exhibit -2.12.2.1: Primary FunctionsBasic or primary functions of a commercial bank are very important in nature.These functions provide the base of the whole operation of the bank. The basicfunctions of a commercial bank are as follows: Accepting deposits: Accepting deposits is the most important function ofall commercial banks. Deposit is the basis of commercial banks' activities. Inorder to attract The general public to deposit their surplus money in thebank, the bank offers to deposit money in any of the following accounts:

Functions of Bank

Secondary FunctionsPrimary Functions

Accepting Deposits Current Account Saving Account Fixed Deposit Accountor Term DepositAccount

Making Advance and Loan

Agency Functions General Utility Functions Miscellaneous Functions

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 10

Current Account: Current or demand account is one where theamount can be withdrawn at any time by the depositor. Such depositaccounts are generally maintained by businessmen or organizations.They can be drawn upon by a cheque without any restriction. Banksdo not pay any interest on these accounts. Rather, banks imposeservice charges for running these accounts. Saving Account: Saving account is suitable for non-trading and smallincome earners. Saving account helps in mobilization of the saving oflow income people. The commercial banks pay interest on this typeof deposits. But, the interest rate is very poor. Fixed Deposit Account or Term Deposit Account: Fixed depositaccount is the account in which amounts are deposited for a certainfixed period of time. The deposits cannot be withdrawn before theexpiry of this fixed period. The longer the period of deposits, thehigher is the rate of profit or interest. Deposit Scheme Account: These types of deposit accounts are newlyadded by the commercial banks in the banking systems forencouraging the fixed-income and low-income people to deposit. Inthis system people have to pay monthly installment at a fixed amountfor a certain period of time to his/her deposit account, and aftermaturity date he/she will get a large sum of money including theprincipal and profit.

Making Advance and Loan: The deposits received by banks are notallowed to remain idle. So, after keeping certain cash reserves, thebalance is given to needy borrowers and interest is charged from them,which is the main source of income for the banks. Different types ofloans and advances made by Commercial banks are: Overdraft: Overdraft is a short-term loan granted by commercialbanks to their account holders. Under this type of loan, thecustomers are allowed to draw more than what they have intheir current account up to a certain limit. The excess amountoverdrawn is called overdraft.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 11

Cash Credit: Cash credit refers to a loan given to the borroweragainst his current assets like shares, stocks, bonds, etc. A creditlimit is sanctioned and the amount is credited in his account. Theborrower may withdraw any amount within his credit limit andinterest is charged on the amount actually withdrawn. Demand Loans: Demand loans refer to those loans which can berecalled on demand by the bank at any time. The entire sum ofdemand loan is credited to the account and interest is payable onthe entire sum. Loans: Commercial banks grant loans for short and medium-term to individuals and traders against the security of movableand immovable property. The amount of loan is credited to theborrower's account. Interest is charged on the entire loansanctioned.

2.2.2: Secondary FunctionsThe secondary functions of commercial bank can be classified in threeheads. They are described below: Agency Functions: The banks render important services as agent onbehalf of their customers in return for a small commission. When banksact as agent, law of agency applies. The agency functions or services ofbank are as follows: Collection of Cheques: Commercial banks collect the cheques, billsof exchange, etc. on behalf of their customers. Banks collect local andoutstation cheques and bills of exchange through clearing housefacilities provided by the central bank. Collection of Income: The commercial banks collect dividends,interest on investment, pension and rent of property due to thecustomers. When any income is collected by the bank, a creditvoucher is sent to the customer for information. Payment of Expenses: The banks make payment of insurancepremiums, rent, trade subscription, school fee and other obligation of

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 12the customers. When any expense is paid by the bank, a debit voucheris sent to the customer for information. Dealer in Securities: The banks carry out purchase and sale ofsecurities on behalf of their customers. Banks do it well because theyare aware of the market conditions. Acts as Trustee: The banks act as trustee to manage trust propertyas per instructions of property owners. Banks are required to followthe terms and conditions of trust deed. Acts as Agent: Commercial bank sometimes acts as an agent on behalfof its customers at home or abroad in dealing with other banks orfinancial institutions. Obeys Standing Instructions: Sometimes, customer may order hisbank to do something on his behalf regarding the conduct of hisaccount. This written order is called standing instruction. The bankbeing the agent of its customer obeys the standing instructions. Acts as Tax Consultant: Commercial bank acts as tax consultant to itsclient. The commercial bank prepares general sales tax return, incometax return, etc. Tiles the same with tax authorities. Collection of Utility Bills: Commercial banks provide facilities for thecollection of utility bills from general public on behalf of governmentbodies. This facilitates the public to pay utility bills in time.

General Utility Functions: Commercial bank performs different utilityfunctions for their customers. When bank performs utility functions, itdoes not act as an agent of the customers. The general utility functionsare as follows: Provides Lockers Facilities: Commercial banks provide lockersfacilities to its customers for safe custody of Jewelery, shares,securities and other valuables. This has minimized the risk of losingdue to theft.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 13

Issue of Travelers Cheque: Commercial banks preserve the wills oftheir customers as trustees and execute them after their death asexecutors. ATM Facilities: An ATM is also known as cash point. The banksnowadays provide ATM facilities through issuing debit card and creditcard. The customers can withdraw money easily and quickly 24 hoursa day. Foreign Exchange: Commercial banks deal in foreign exchange. Thisenables the individuals and businessmen to obtain foreign currency inexchange of their home currency. For dealing in foreign exchange,commercial banks have to obtain permission from the central bank. Transfer of Money: Commercial banks provide facilities for thetransfer of money to any place within and outside the country. Thefunds are transferred by means of draft, telephonic transfer,electronic transfer etc. Finance Foreign Trade: A commercial bank finances foreign trade byaccepting foreign bills of exchange. Bank also issues letter of credit onbehalf of its customers to facilitate foreign trade. Trade Information: Commercial banks collect and provide tradeinformation and tender advice to its customers about financialmatters. Issuing Credit Cards: Banks issue credit cards to their trustworthyand valued customers. This facilitates the customers to pay for theirnecessities of life.

Miscellaneous Functions: Commercial banks perform the followingmiscellaneous functions: Zakat Collection: Commercial banks collect Zakat from their accountholders and deposit the same into Central Zakat Fund, according toZakat and Usher ordinance - 1980. Hajj Services: The commercial banks provide free Hajj sendees to theintending pilgrims. Banks receive Hajj applications. Banks also

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 14facilitate to form Hajj groups. Banks make necessary arrangements forthe training of intending pilgrims. Qarz-e-Hasna: The commercial banks provide Qarz-e-Hasna todeserving patients for medical treatment and to students for higherstudies within the country and abroad. The Qarz-e-Hasna is refund Alein easy installments.

2.3: Islamic BankingIslamic banking has been defined in a number of ways. The definition ofIslamic bank, as approved by the General Secretariat of the OIC, is stated inthe following manner. "An Islamic bank is a financial institution whosestatus, rules and procedures expressly state its commitment to theprinciple of Islamic Shariah and to the banning of the receipt and paymentof interest on any of its operations"(Ali & Sarkar 1995, pp.20-25). Ajaz A.Khan viewing the concept from the perspective of an Islamic economy andthe prospective role to be played by an Islamic bank therein opines:“Islamic banking is banking or banking activity that is consistent with theprinciples of sharia and its practical application through the developmentof Islamic economics. As such, a more correct term for 'Islamic banking' is'Sharia compliant finance.”It appears from the above definitions that Islamic banking is systems offinancial intermediation that avoids receipt and payment of interest in itstransactions and conducts its operations in a way that helps achieve theobjectives of an Islamic economy. Alternatively, this is a banking systemwhose operation is based on Islamic principles of transactions of whichprofit and loss sharing (PLS) is a major feature, ensuring justice and equityin the economy. That is why Islamic banks are often known as PLS-banks.In single sentence Islamic Bank can be defined as a financial intermediarythat conducts its banking activities according to Islamic Shariah byavoiding receipt and payment of interest/riba in its transactions andconducts its activities based on profit or loss sharing motive for achievingthe objectives of Islamic economy.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 15

2.3.1: Principles of Islamic Banking:Islamic Banking has some exclusive principles by which it can bedistinguished from conventional banking. The core principles of Islamicbanking are stated below: Prohibition of Interest: Interest is strictly prohibited in Islam. Because,Interest is fixed and predetermined benefit accepted by the lender forlending his money and given by the borrower for borrowing money.Islamic Shariah prohibits all benefits in transactions. Interest is calledRiba in Islam. Partnership Business: Islamic banks invest money to the businessorganization as partner and they look after business for ensuring theproper use of fund. Profit and Loss Sharing: It is the basic principle of Islamic banking.Islamic banking system conducts the business activities based on profitand loss sharing. As bank works as partner it accepts the losses if anyloss occurred in business and participates in profits when profits gain. Invest in Shariah approved Heads: Islamic Banking system isconcerned in use of fund. It only invests into Halal businesses that meanShariah approved business heads. Shariah Board: In every Islamic bank, there have a special governingcommittee that governing the whole activities of the bank is calledShariah Board. This board ensures that the investment is made to theHalal business and activities are conducted according to Islamic Shariah.2.3.2: Riba or Interest:The word used by the Quran concerning 'interest' is Riba. The literalmeanings of Riba are money increase, increase of anything or increment ofanything from its original amount. However, all increases are notconsidered as Riba in Islam. Money may increase in business activities aswell. This increase is not at all considered as Riba. Islam prohibits onlythose increases that are charged on the loan with a prefixed rate.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

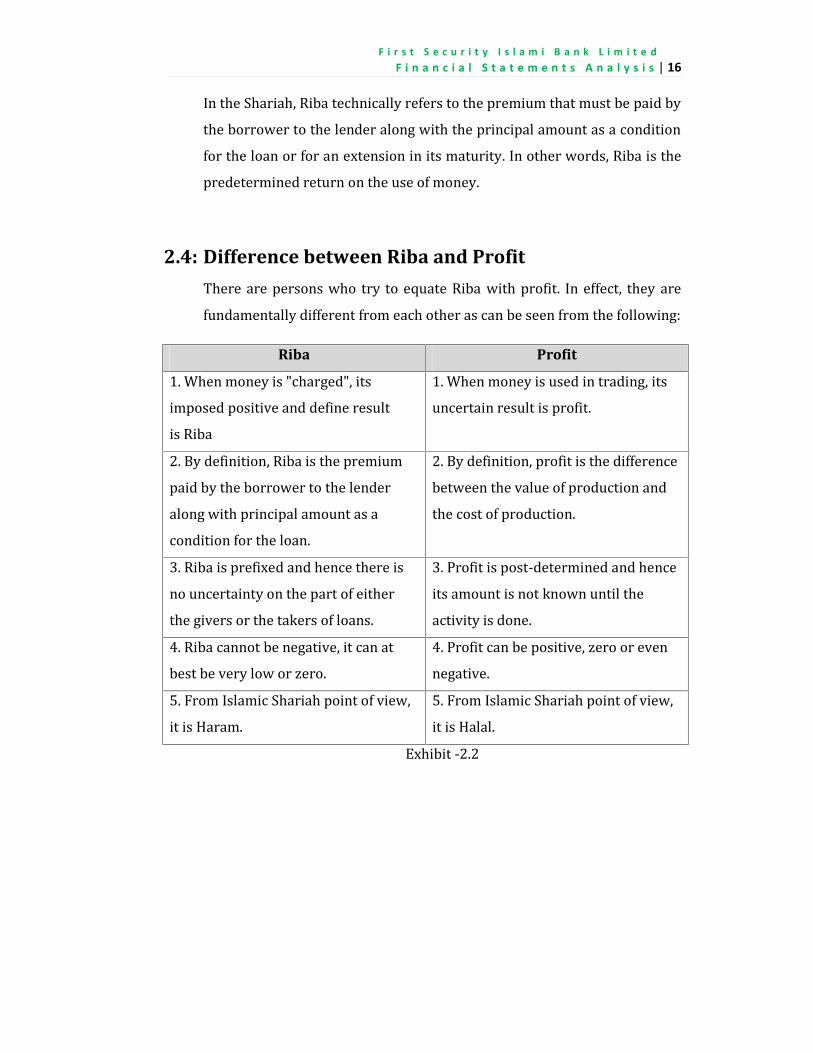

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 16In the Shariah, Riba technically refers to the premium that must be paid bythe borrower to the lender along with the principal amount as a conditionfor the loan or for an extension in its maturity. In other words, Riba is thepredetermined return on the use of money.2.4: Difference between Riba and ProfitThere are persons who try to equate Riba with profit. In effect, they arefundamentally different from each other as can be seen from the following:

Riba Profit1. When money is "charged", itsimposed positive and define resultis Riba1. When money is used in trading, itsuncertain result is profit.

2. By definition, Riba is the premiumpaid by the borrower to the lenderalong with principal amount as acondition for the loan.2. By definition, profit is the differencebetween the value of production andthe cost of production.

3. Riba is prefixed and hence there isno uncertainty on the part of eitherthe givers or the takers of loans.3. Profit is post-determined and henceits amount is not known until theactivity is done.4. Riba cannot be negative, it can atbest be very low or zero. 4. Profit can be positive, zero or evennegative.5. From Islamic Shariah point of view,it is Haram. 5. From Islamic Shariah point of view,it is Halal.Exhibit -2.2

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 17

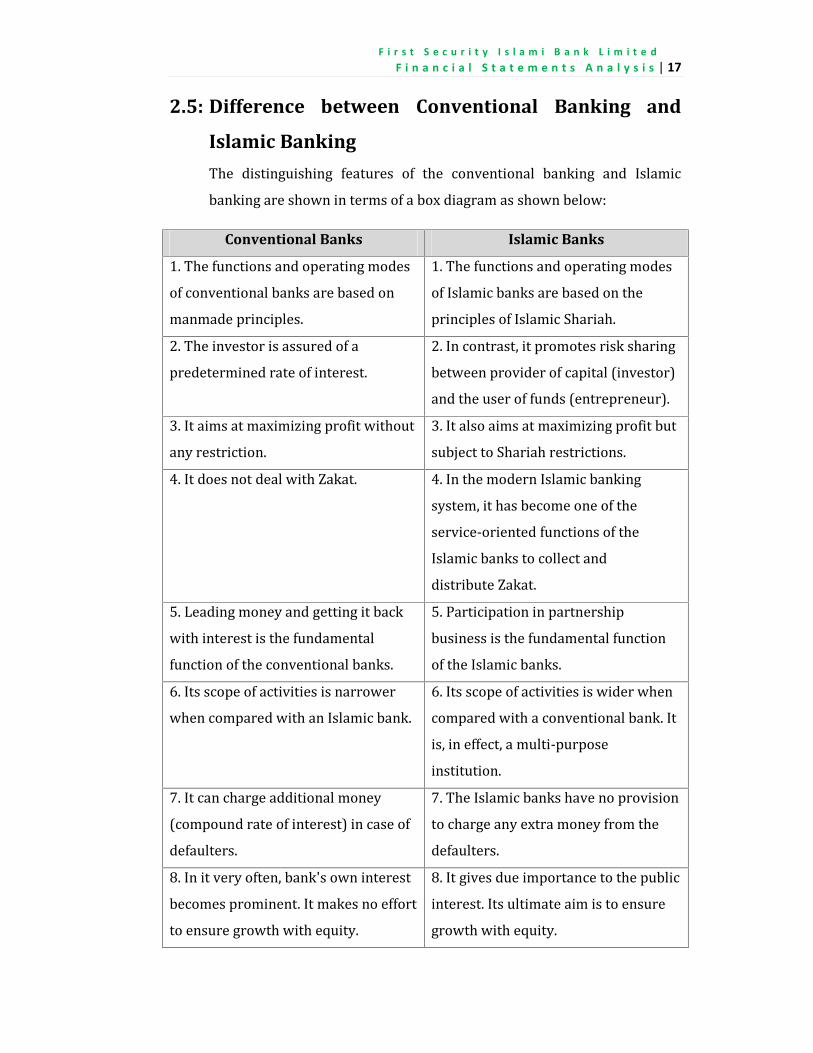

2.5: Difference between Conventional Banking and

Islamic BankingThe distinguishing features of the conventional banking and Islamicbanking are shown in terms of a box diagram as shown below:Conventional Banks Islamic Banks1. The functions and operating modesof conventional banks are based onmanmade principles.

1. The functions and operating modesof Islamic banks are based on theprinciples of Islamic Shariah.2. The investor is assured of apredetermined rate of interest. 2. In contrast, it promotes risk sharingbetween provider of capital (investor)and the user of funds (entrepreneur).3. It aims at maximizing profit withoutany restriction. 3. It also aims at maximizing profit butsubject to Shariah restrictions.4. It does not deal with Zakat. 4. In the modern Islamic bankingsystem, it has become one of theservice-oriented functions of theIslamic banks to collect anddistribute Zakat.5. Leading money and getting it backwith interest is the fundamentalfunction of the conventional banks.5. Participation in partnershipbusiness is the fundamental functionof the Islamic banks.6. Its scope of activities is narrowerwhen compared with an Islamic bank. 6. Its scope of activities is wider whencompared with a conventional bank. Itis, in effect, a multi-purposeinstitution.7. It can charge additional money(compound rate of interest) in case ofdefaulters.7. The Islamic banks have no provisionto charge any extra money from thedefaulters.8. In it very often, bank's own interestbecomes prominent. It makes no effortto ensure growth with equity.8. It gives due importance to the publicinterest. Its ultimate aim is to ensuregrowth with equity.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 189. For interest-based commercialbanks, borrowing from the moneymarket is relatively easier.9. For the Islamic banks, it iscomparatively difficult to borrowmoney from the money market.10. Since income from the advances isfixed, it gives little importance todeveloping expertise in projectappraisal and evaluations.10. Since it shares profit and loss, theIslamic banks pay greater attention todeveloping project appraisal andevaluations.11. The conventional banks givegreater emphasis on credit-worthiness of the clients.11. The Islamic banks, on the otherhand, give greater emphasis on theviability of the projects.12. The status of a conventional bank,in relation to its clients, is that ofcreditor and debtors.12. The status of Islamic bank inrelation to its clients is that ofpartners, investors and trader.13. A conventional bank has toguarantee all its deposits. 13. Strictly speaking, and Islamic bankcannot do that.Exhibit -2.3

2.6: Financial StatementsFinancial Statements are the summary of the financial activities of a firmor an organization. AIS Board define the financial statement, “A financialstatement (or financial report) is a formal record of the financial activitiesof a business, person, or other entity. Relevant financial information ispresented in a structured manner and in a form easy to understand.”It appears from the above definitions that financial statements are therecords that outline the financial activities of a business, an individual orany other entity. Financial statements are intended to present the financialinformation of the entity in question as clearly and concisely as possiblefor both the entity and for readers. Financial statements for businessesusually include: income statements, balance sheet, statements of changesin equity and cash flows, as well as other possible statements.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 19

2.7: Components of Financial StatementsAccording to International Accounting Standards (IAS) a complete set offinancial statements includes the flowing components. Statement of Financial Position / Balance Sheet Income Statement / Statement of Profit and Loss Account Statement of Cash Flow Statement of Changes in Equity Notes to these statements

2.8: Components of Bank’s Financial StatementsSince a bank is a financial institution, its financial statements are differentfrom other organization. Bank’s Financial Statements include an additionalcomponent which is called Liquidity Statement. The basic components ofbank’s financial statements are given below. Balance Sheet Statement of Profit and Loss Account / Income Statement Cash Flow Statement Statement of Changes in Equity Liquidity Statement Notes to these statements2.8.1:Balance Sheet: Balance sheet is a financial statement thatsummarizes a company's assets, liabilities and shareholders' equityat a specific point in time of a business' calendar year. These threebalance sheet segments give investors an idea as to what thecompany owns and owes, as well as the amount invested by theshareholders.2.8.2:Statement of Profit and Loss Account / Income Statement:Income statement is a financial report that shows an entity's resultsof financial performance over a specific time period. The timeperiod usually covers for a month, quarter, half year or year.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 20

2.8.3:Cash Flow Statement: A cash flow statement is the financialstatement that measures the cash generated or used by a companyin a given period.2.8.4:Statement of Changes in Equity: Statement of changes in equityis a financial statement that presents a summary of the changes inshareholders’ equity accounts in a company over an accountingperiod. It reconciles the opening balances of equity accounts withthe closing balances.2.8.5:Liquidity Statement: Liquidity Statement is a financial statementthat shows a company’s remaining liquid assets to meet the shortterm obligations over a certain period of time. Liquid assetsmainly cover cash and cash equivalent assets. Liquidity statementis necessary for banking companies and other financialinstitutions.2.8.6:Notes: Notes are not core financial statement, but they arenecessary understand other financial statements. Notes are thedetails of summary statements like balance sheet, incomestatement. Notes present process of calculation and particularsincluded of significant items in core financial statements.

2.9: Financial Statements AnalysisFinancial Statements Analysis is the process of reviewing and evaluating acompany's financial statements (such as the balance sheet or profit and lossaccount statement), thereby gaining an understanding of the financial healthof the company and enabling to make more effective policies.2.10: Techniques to Financial Statements AnalysisFinancial statement analysis is an evaluative method of determining thepast, current and projected performance of a company. Several techniquesare commonly used as part of financial statement analysis. Widely used aresated below.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 21

Horizontal Analysis: It compares the financial data of two or moreyears in both money and percentage form. Vertical Analysis: In vertical analysis each category of accounts onthe balance sheet is shown as a percentage of the total account. Ratio Analysis: Ratio analysis is a fundamental means of examiningthe health of a company by studying the relationships of key financialvariables. It calculates statistical relationships between data.A bank’s financial statements are always different from general companies. So,banks’ financial statements analysis is critical. Among the stated techniques theratio analysis is mostly used for analysis of any organization’s financialstatements.

2.11: Literature ReviewFinancial statement analysis applies analytical tools to general-purposefinancial statements and related data for making business decisions. Itinvolves transforming accounting data into more useful information.Financial statement analysis reduces our reliance on hunches, guesses, andinformation as well as our uncertainty in decision making. It does not lessenthe need for expert judgment; instead, it provides us an effective andsystematic basis for making business decisions.It is a standard practice for businesses to present financial statements thatadhere to generally accepted accounting principles (GAAP), to maintaincontinuity of information and presentation across international borders. Aswell, financial statements are often audited by government agencies,accountants, firms, etc. to ensure accuracy and for tax, financing or investingpurposes. Financial statements are integral to ensuring accurate and honestaccounting for businesses and individuals alike. So, some basic requirementmust be fulfilled by a person when he/she prepares financial statements.Balance sheet, income statement, statement of cash flow, statement ofequity and liquidity statement are the core financial statements of a bankingcompany. When one goes to analysis the financial statements he/she first

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 22concentrate to the balance sheet. Because balance sheet is required forevery type of financial analysis including ratio analysis. The balance sheetdepicts the assets and the liabilities at a stated point of time, for example31st December. The figures of the assets and liabilities are given in thebalance sheet from the basis of financial appraisal and duration. In fact,there are two stages in the evaluation of balance sheet: The analysis of balance sheet, refers examination of individual itemsof assets and liabilities and their classification into well-definedcategories, and Interpretation of the balance sheet through the Ratio Analysis.

2.11.1: Classification of Assets and LiabilitiesThe first step in the analysis of balance sheet is the scrutiny andexamination of different items of assets and liabilities and they are classifiedinto various categories. Assets:In the Balance sheet the assets are divided into three majorcategories in general when organizations prepare the balance sheets.These are as follows:

Current Assets Fixed/Long-Term Assets Other Assets

Current Assets: Current assets are those assets, which changestheir form in a short period and are exchanged for cash. In otherwords, current assets are meant to be liquidated for cash in the nearfuture. Generally the duration of these assets is within one year. Fixed/Long-Term Assets: The assets which are not consumed orsold during the normal course of business and they are used forcarrying on the business, such as land, building, machinery,furniture and fixtures etc. are fixed assets. Other Assets: Other assets are a grouping of accounts that are listedas a separate line item in the assets section of the balance sheet and

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 23which contain minor assets that do not naturally fit into any of themain asset categories. “These assets do not represent any property;rather they represent certain deferred revenue expenses or losseswhich are being written-off over the years” (S. A. Ali & R. A.Howlader, pp.345). But, some of the writers include the other assetsinto fixed assets, some writers include them into current assets andsome of the writers include the other assets into both fixed assetsand current assets according to their duration and type.It appears from the above definitions that other assets are themiscellaneous assets that cannot be classified as current assets orfixed assets. Examples of other assets include deferred tax assets,bond issue costs, advances to officers, prepaid pension costs, andlong-term prepayments. But, other assets can be included into majorcategories, if we have proper information or notes about their timeduration. Most of the case other assets include negligible accounts,so it can be included in current assets. In the case of FSIBL, thenotes about other assets indicate that it should be included incurrent assets when I have prepared the classified balance sheetaccording maturity for the purpose of ratio analysis. Liabilities:In the Balance sheet the liabilities are broadly divided into twocategories when organizations prepare the balance sheets. These areas follows:

Current Liabilities Long-Term Liabilities

Current Liabilities: Current liabilities are the obligations thoseare payable within one accounting year. Common examples areaccounts payable, wages payable, bank loan payable, interestpayable and tax payable. For a banking company placement fromBanks and other Financial Institutions, all deposit accounts, billspayable, current portion of ling-term liabilities and otherliabilities are elements of current liabilities.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 24

Long-Term Liabilities: Long-term liabilities are the obligationsthat a company expects to pay after one accounting year.Liabilities in this category include subordinated bonds, bondspayable, and mortgages payable, loan payable, long-term notespayable, lease liabilities, pension liabilities and other long-termliabilities.For the need of my research work I have prepared a comparative balancesheet by classifying items of the balance sheets according to their durationand character. Comparative Balance Sheets consist of balance sheetamounts from two or more balance sheet dates arranged side by side. Itsusefulness is often improved by showing each item’s money amountchange and percentage change to highlight large changes.Analysis of comparative financial statements begins by focusing on itemsthat shows large dollar and percent changes. We then try to identify thereason for these changes and, if possible, determine whether they arefavorable or unfavorable. We also follow up on items with small changeswhen we expected the changes to be large.2.11.2: Limitations of Financial StatementsThough Balance Sheet and Profit and Loss Account of a company areimportant sources for the analysis, the financial data contained therein havecertain limitations. The financial data depict the state of affairs or theoperating results in numerical terms. Sometimes wrong or illogicalconclusion may be derived from them if attention is not given to otherfactors that are not evident from the financial statements. For example, theproduction of a manufacturing company may fall due to labor strike or non-availability of raw materials due to transport bottlenecks, but it should notbe interpreted as decline in the efficiency or profitability of the concern. It is,therefore, essential that the investor should look beyond the financial dataand make future enquiries regarding the causes for any variation orabnormal trend noted in analyzing the data. Besides, the financial

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 25statements represent the performance of the business concern. Anymeaningful analysis of these statements will depend upon the projections ofthe future trend. Past events are just guides as to what may reasonably beexpected to occur in future.2.11.3: Building Blocks of Financial Statement AnalysisFinancial statements analysis focuses on one or more elements of acompany’s financial condition or performance. Our analysis emphasizes fourareas of inquiry with varying degrees of importance. These four areas aredescribed and illustrated in this chapter and considered the building blocksof financial statements analysis: Liquidity and Efficiency: It refers the ability of a company to meetshort-term obligations and to efficiently generate revenues. Solvency: It refers the ability to generate future revenue and meetlong-term obligations by a company. Profitability: It is the ability to provide financial rewards sufficientto attract and retain financing. Market prospects: It refers a company’s ability to generate positivemarket expectation.

2.11.4: Horizontal AnalysisAnalysis of any single financial number is of limited value. Instead, much offinancial statement analysis involves identifying and describing relationsbetween numbers, groups of numbers and changes in those numbers.Horizontal analysis refers to examination of financial statement data acrosstime. The term “horizontal analyses” arises from the left-to-right movementof our eyes as we review comparative statements across time.2.11.4.1: Comparative StatementsComparing amounts for two of more successive periods often helps inanalyzing financial statements. Comparative financial statements facilitatethis comparison by showing financial amount in side-by-side columns on a

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 26single statement, called comparative format. By using comparative financialstatements financial changes can be expressed in both dollar amount andpercentage. Computation of Dollar Change and Percent Change: Computingfinancial statements over time periods generally two-to-five years is oftendone by analyzing changes in line items. A change analysis usuallyincludes analyzing absolute dollar amount changes and percent changes.Both analyses are relevant because dollar changes can yield largepercentage changes inconsistent their importance. Dollar amount isnecessary to retain a proper perspective and to assess the importance ofchanges. The computation of dollar change for a financial statement itemas follows:

Dollar change = Analysis period amount - Base period amountAnalysis period is the point or period of time for the financial statementsunder analysis, and base period is the point or period of time for financialstatements used for comparison purposes. The prior year is commonlyused as a base period. We compute percent change by dividing the dollarchange by the base period amount and then multiplying this quantity by100 as follows: (%) = − ×We can always compute a dollar change, but we must be aware of a fewrules in working with percent changes. These rules are as follows: When a negative amount appears in the base period and a positiveamount appears in the analysis period then we cannot compute ameaningful percent change. When a positive amount appears in the base period and a negativeamount appears in the analysis period then we cannot compute ameaningful percent change. When no value is in the base period then no percent is computable. When an item has a value in the base period and zero in theanalysis period, the decrease is 100 percent.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 27

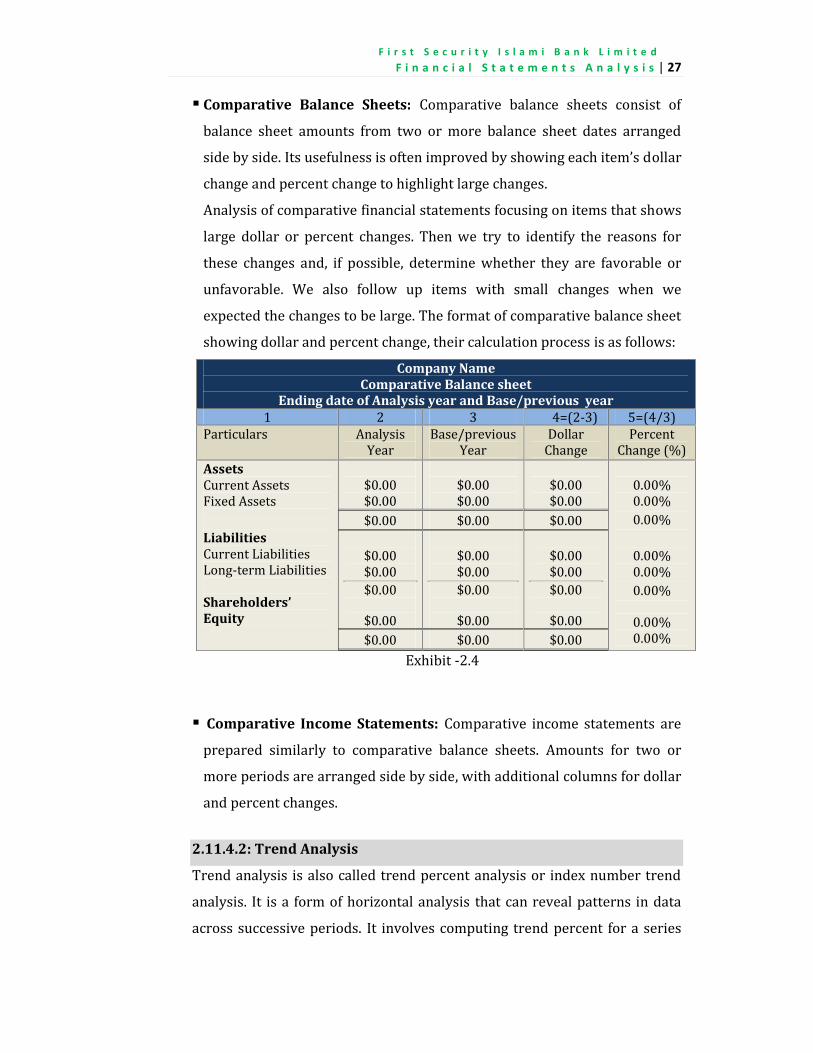

Comparative Balance Sheets: Comparative balance sheets consist ofbalance sheet amounts from two or more balance sheet dates arrangedside by side. Its usefulness is often improved by showing each item’s dollarchange and percent change to highlight large changes.Analysis of comparative financial statements focusing on items that showslarge dollar or percent changes. Then we try to identify the reasons forthese changes and, if possible, determine whether they are favorable orunfavorable. We also follow up items with small changes when weexpected the changes to be large. The format of comparative balance sheetshowing dollar and percent change, their calculation process is as follows:Company Name

Comparative Balance sheetEnding date of Analysis year and Base/previous year1 2 3 4=(2-3) 5=(4/3)Particulars AnalysisYear Base/previousYear DollarChange PercentChange (%)

AssetsCurrent AssetsFixed AssetsLiabilitiesCurrent LiabilitiesLong-term LiabilitiesShareholders’Equity

$0.00$0.00$0.00$0.00$0.00$0.00$0.00$0.00

$0.00$0.00$0.00$0.00$0.00$0.00$0.00$0.00

$0.00$0.00$0.00$0.00$0.00$0.00$0.00$0.00

0.00%0.00%0.00%0.00%0.00%0.00%0.00%0.00%Exhibit -2.4 Comparative Income Statements: Comparative income statements areprepared similarly to comparative balance sheets. Amounts for two ormore periods are arranged side by side, with additional columns for dollarand percent changes.2.11.4.2: Trend AnalysisTrend analysis is also called trend percent analysis or index number trendanalysis. It is a form of horizontal analysis that can reveal patterns in dataacross successive periods. It involves computing trend percent for a series

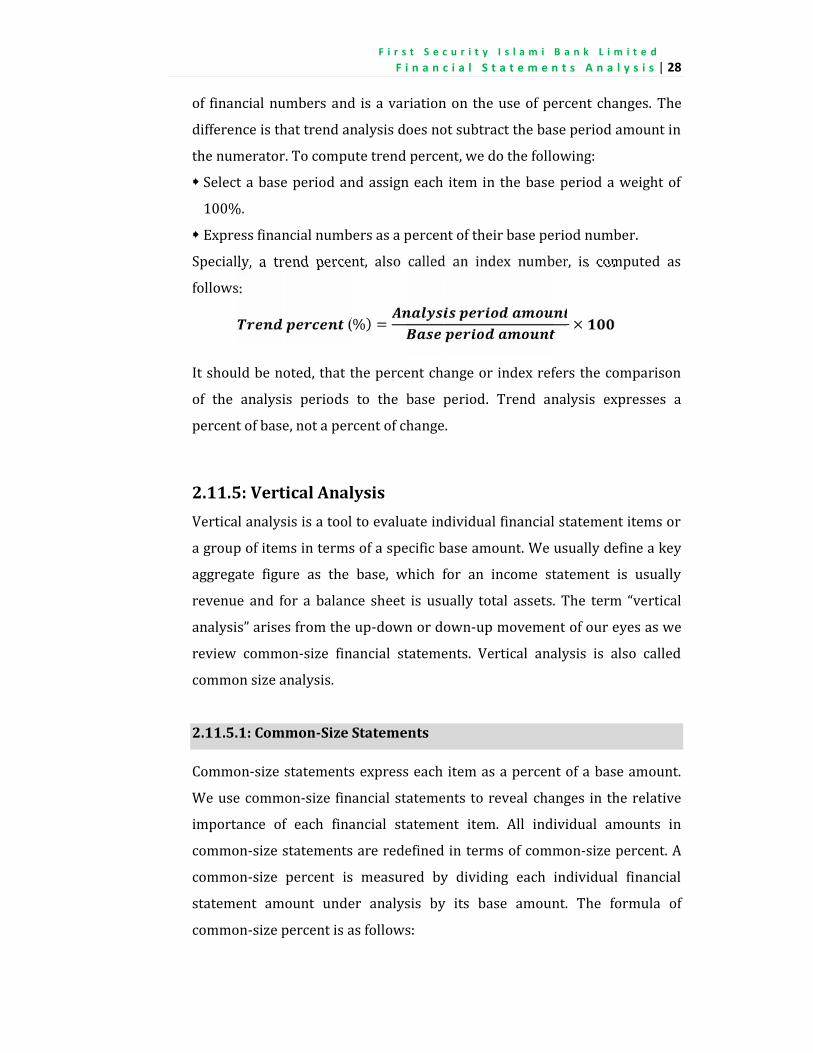

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 28of financial numbers and is a variation on the use of percent changes. Thedifference is that trend analysis does not subtract the base period amount inthe numerator. To compute trend percent, we do the following: Select a base period and assign each item in the base period a weight of100%. Express financial numbers as a percent of their base period number.Specially, a trend percent, also called an index number, is computed asfollows: (%) = ×It should be noted, that the percent change or index refers the comparisonof the analysis periods to the base period. Trend analysis expresses apercent of base, not a percent of change.2.11.5: Vertical AnalysisVertical analysis is a tool to evaluate individual financial statement items ora group of items in terms of a specific base amount. We usually define a keyaggregate figure as the base, which for an income statement is usuallyrevenue and for a balance sheet is usually total assets. The term “verticalanalysis” arises from the up-down or down-up movement of our eyes as wereview common-size financial statements. Vertical analysis is also calledcommon size analysis.2.11.5.1: Common-Size StatementsCommon-size statements express each item as a percent of a base amount.We use common-size financial statements to reveal changes in the relativeimportance of each financial statement item. All individual amounts incommon-size statements are redefined in terms of common-size percent. Acommon-size percent is measured by dividing each individual financialstatement amount under analysis by its base amount. The formula ofcommon-size percent is as follows:

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

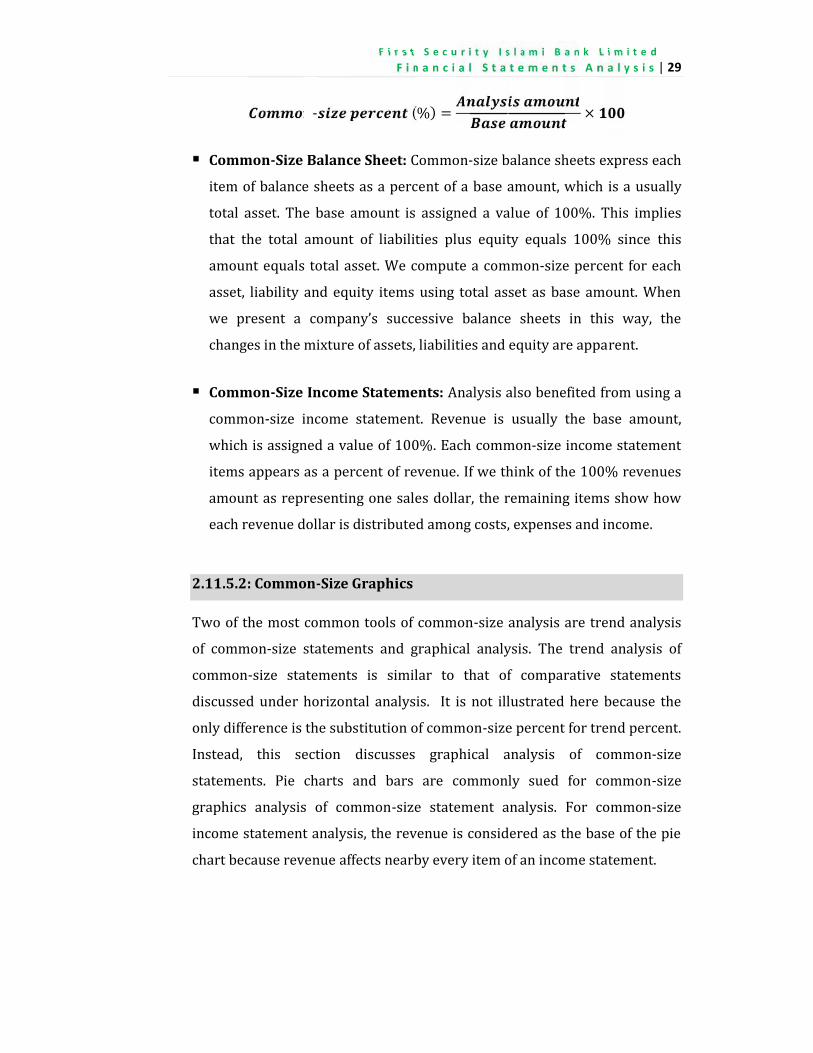

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 29

- (%) = × Common-Size Balance Sheet: Common-size balance sheets express eachitem of balance sheets as a percent of a base amount, which is a usuallytotal asset. The base amount is assigned a value of 100%. This impliesthat the total amount of liabilities plus equity equals 100% since thisamount equals total asset. We compute a common-size percent for eachasset, liability and equity items using total asset as base amount. Whenwe present a company’s successive balance sheets in this way, thechanges in the mixture of assets, liabilities and equity are apparent. Common-Size Income Statements: Analysis also benefited from using acommon-size income statement. Revenue is usually the base amount,which is assigned a value of 100%. Each common-size income statementitems appears as a percent of revenue. If we think of the 100% revenuesamount as representing one sales dollar, the remaining items show howeach revenue dollar is distributed among costs, expenses and income.2.11.5.2: Common-Size GraphicsTwo of the most common tools of common-size analysis are trend analysisof common-size statements and graphical analysis. The trend analysis ofcommon-size statements is similar to that of comparative statementsdiscussed under horizontal analysis. It is not illustrated here because theonly difference is the substitution of common-size percent for trend percent.Instead, this section discusses graphical analysis of common-sizestatements. Pie charts and bars are commonly sued for common-sizegraphics analysis of common-size statement analysis. For common-sizeincome statement analysis, the revenue is considered as the base of the piechart because revenue affects nearby every item of an income statement.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 30

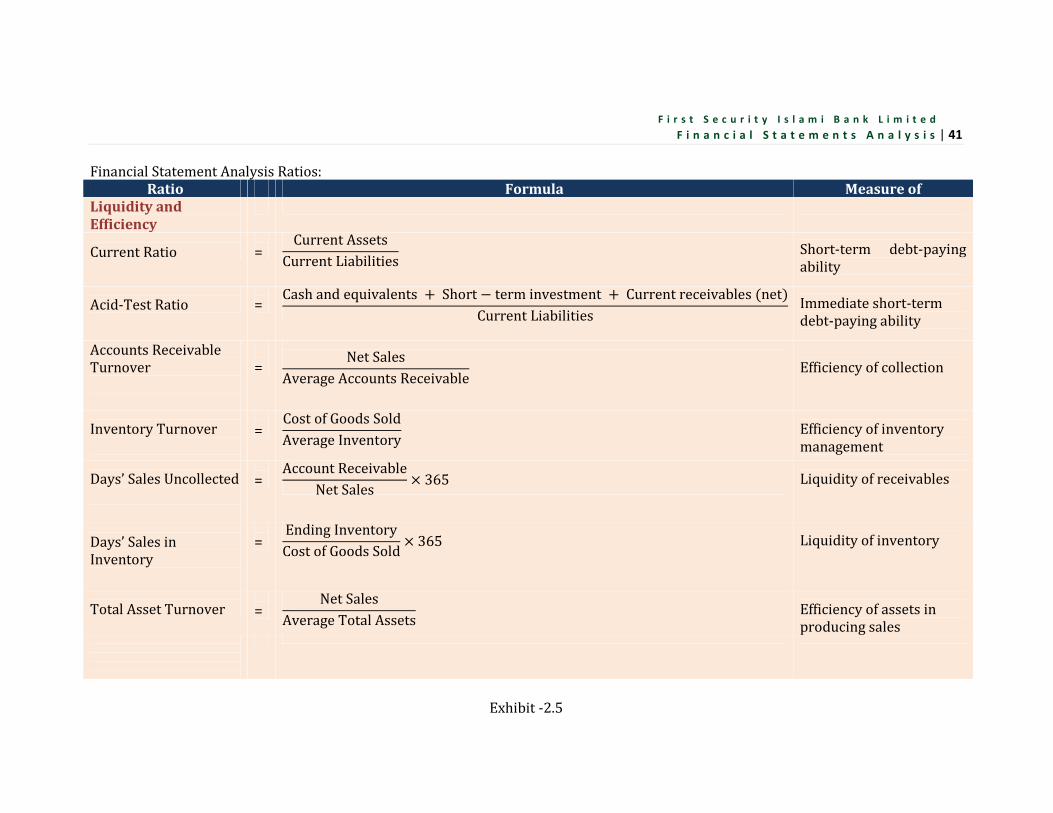

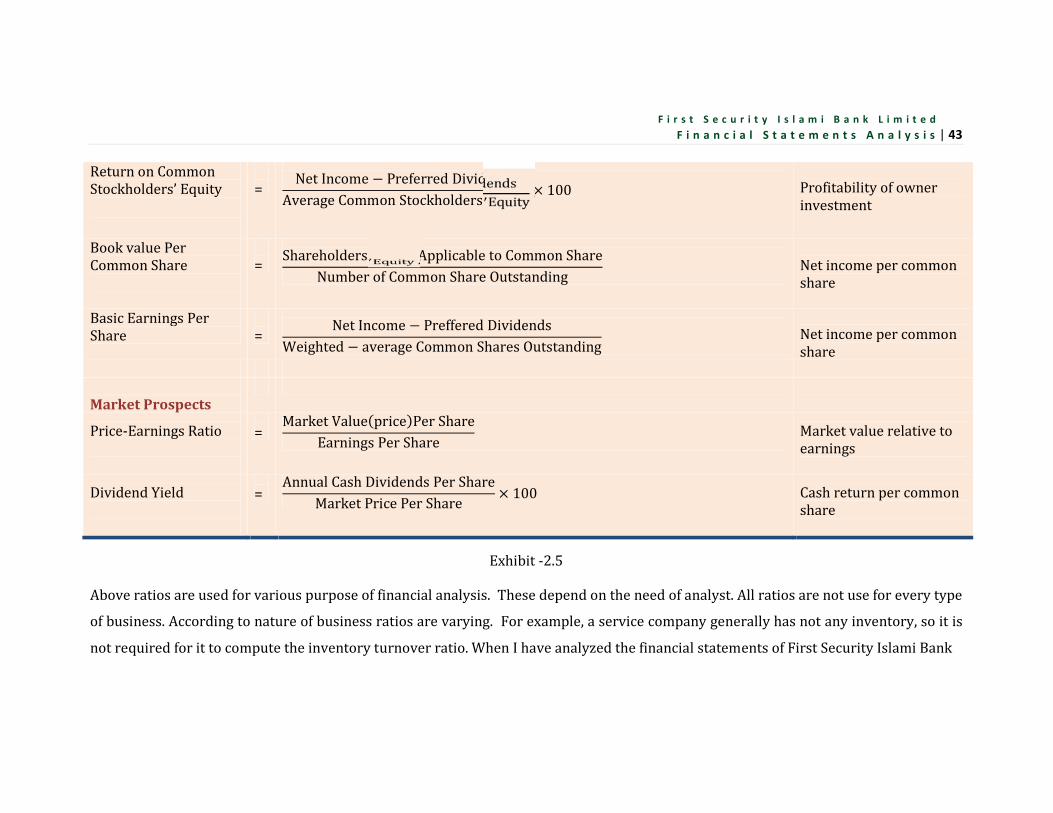

2.11.6: Ratio AnalysisRatios are among the more widely used tools of financial statement analysisbecause they provide clues to and symptoms of underlying conditions. Aratio can help us uncover conditions and trends difficult to detect byinspecting individual components making up the ratio. Ratios, like otheranalysis tools, are usually future oriented. They are often adjusted for theirprobable future trend and magnitude, and their usefulness depends on theskillful interpretation. A ratio expresses a mathematical relation betweentwo quantities. It can be expressed as a percent, rate, or proportion.Computation of ratio is a simple arithmetic operation, but its interpretationis not. To be meaningful, a ratio must refer to an economically importantrelation.In this section an important set of financial ratios and its applications aredescribed. The selected ratios are organized into the four building blocks offinancial statement analysis. These are as follows:(i) Liquidity and Efficiency Ratios(ii) Solvency Ratios(iii) Profitability Ratios(iv)Market Prospects Ratios

2.11.6.1: Liquidity and Efficiency RatiosLiquidity refers to the availability of resources of a company to meet short-term cash requirements. It is affected by the timing of cash inflows andoutflows along with prospects for future performance. Analysis of liquidityis aimed at a company’s funding requirements.Efficiency refers to how productive a company in using its assets. Efficiencyis usually measured relative to how much revenue is generated from acertain level of assets.Both liquidity and efficiency are important and complementary. If acompany fails to meet its current obligations, its continued existence isdoubtful. From this view point, all other measures of analysis are insecondary importance. Although accounting measurements assume thecompany’s continued existence, our analysis must always assess the validity

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

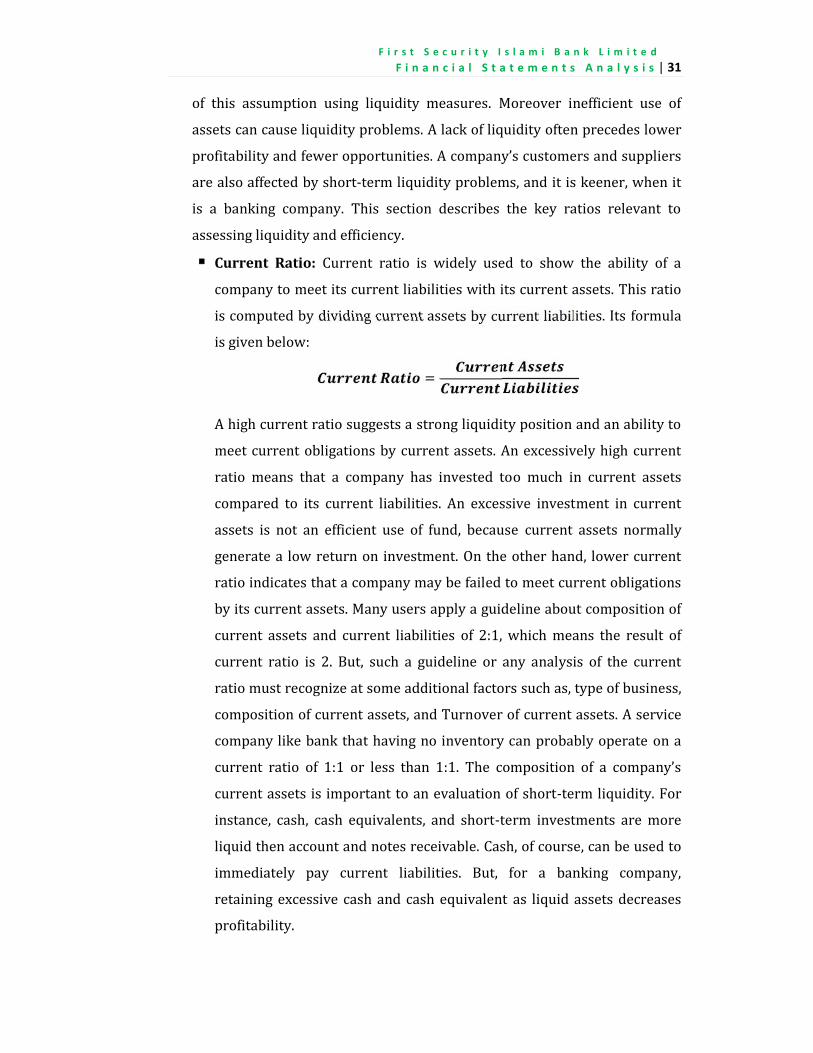

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 31of this assumption using liquidity measures. Moreover inefficient use ofassets can cause liquidity problems. A lack of liquidity often precedes lowerprofitability and fewer opportunities. A company’s customers and suppliersare also affected by short-term liquidity problems, and it is keener, when itis a banking company. This section describes the key ratios relevant toassessing liquidity and efficiency. Current Ratio: Current ratio is widely used to show the ability of acompany to meet its current liabilities with its current assets. This ratiois computed by dividing current assets by current liabilities. Its formulais given below: =

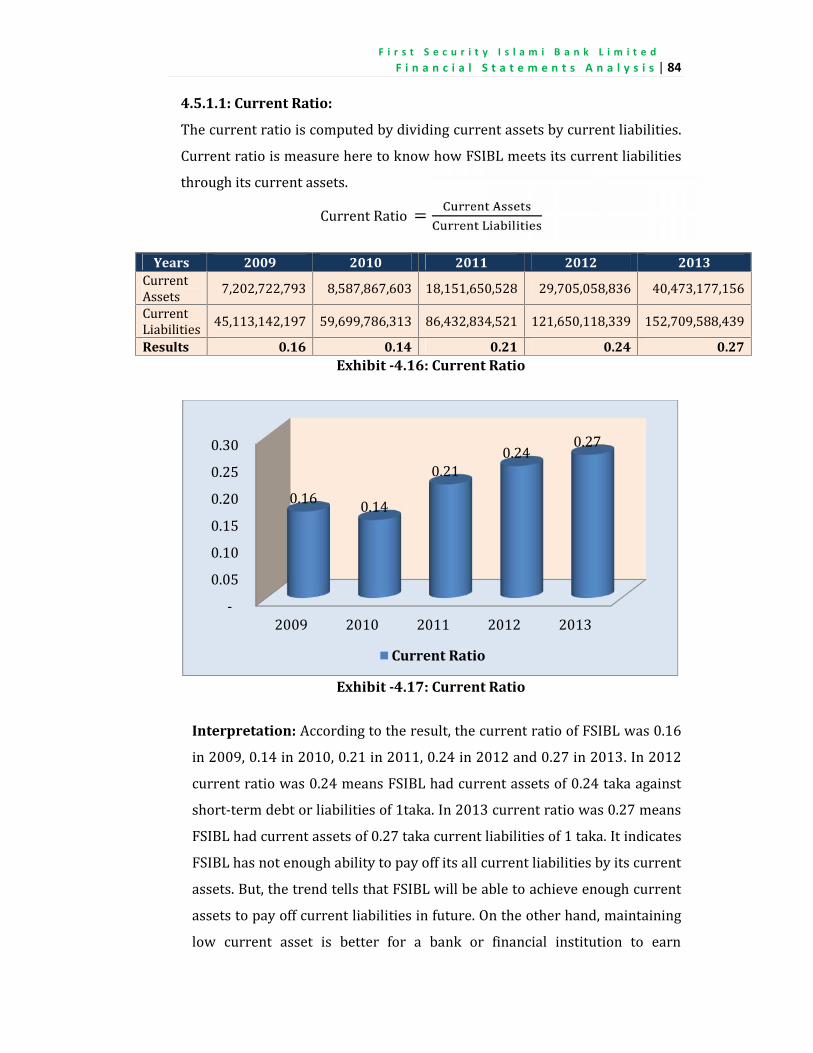

A high current ratio suggests a strong liquidity position and an ability tomeet current obligations by current assets. An excessively high currentratio means that a company has invested too much in current assetscompared to its current liabilities. An excessive investment in currentassets is not an efficient use of fund, because current assets normallygenerate a low return on investment. On the other hand, lower currentratio indicates that a company may be failed to meet current obligationsby its current assets. Many users apply a guideline about composition ofcurrent assets and current liabilities of 2:1, which means the result ofcurrent ratio is 2. But, such a guideline or any analysis of the currentratio must recognize at some additional factors such as, type of business,composition of current assets, and Turnover of current assets. A servicecompany like bank that having no inventory can probably operate on acurrent ratio of 1:1 or less than 1:1. The composition of a company’scurrent assets is important to an evaluation of short-term liquidity. Forinstance, cash, cash equivalents, and short-term investments are moreliquid then account and notes receivable. Cash, of course, can be used toimmediately pay current liabilities. But, for a banking company,retaining excessive cash and cash equivalent as liquid assets decreasesprofitability.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

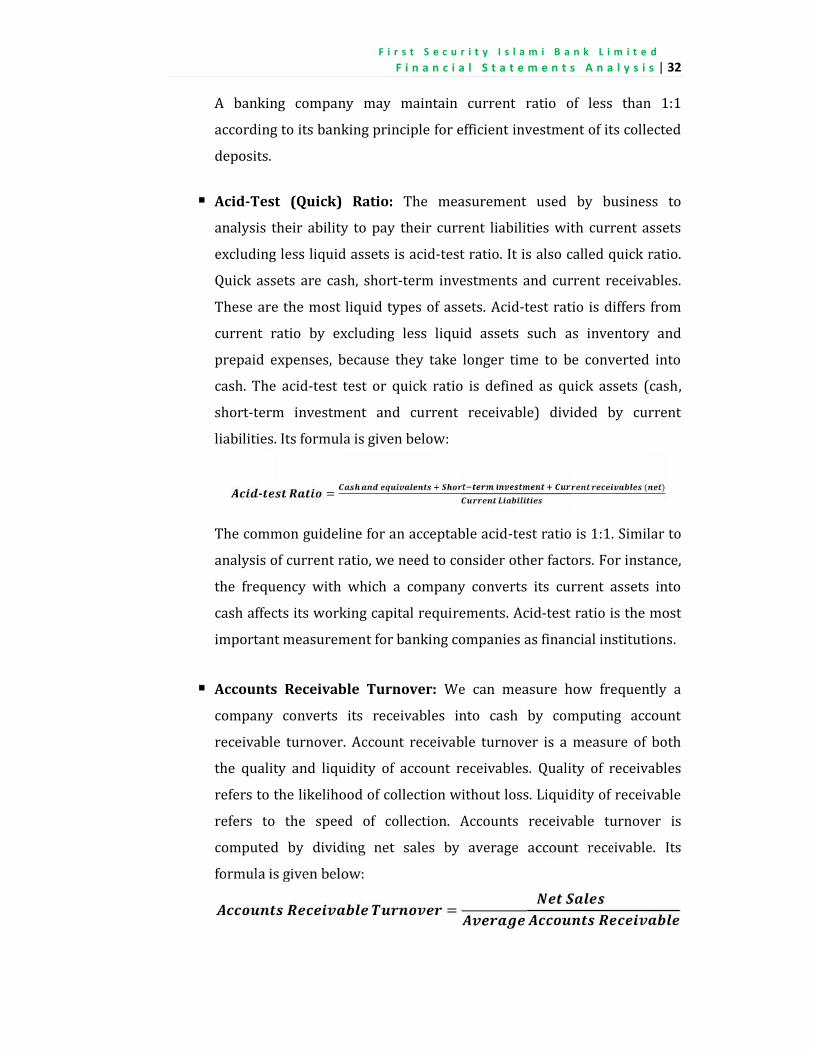

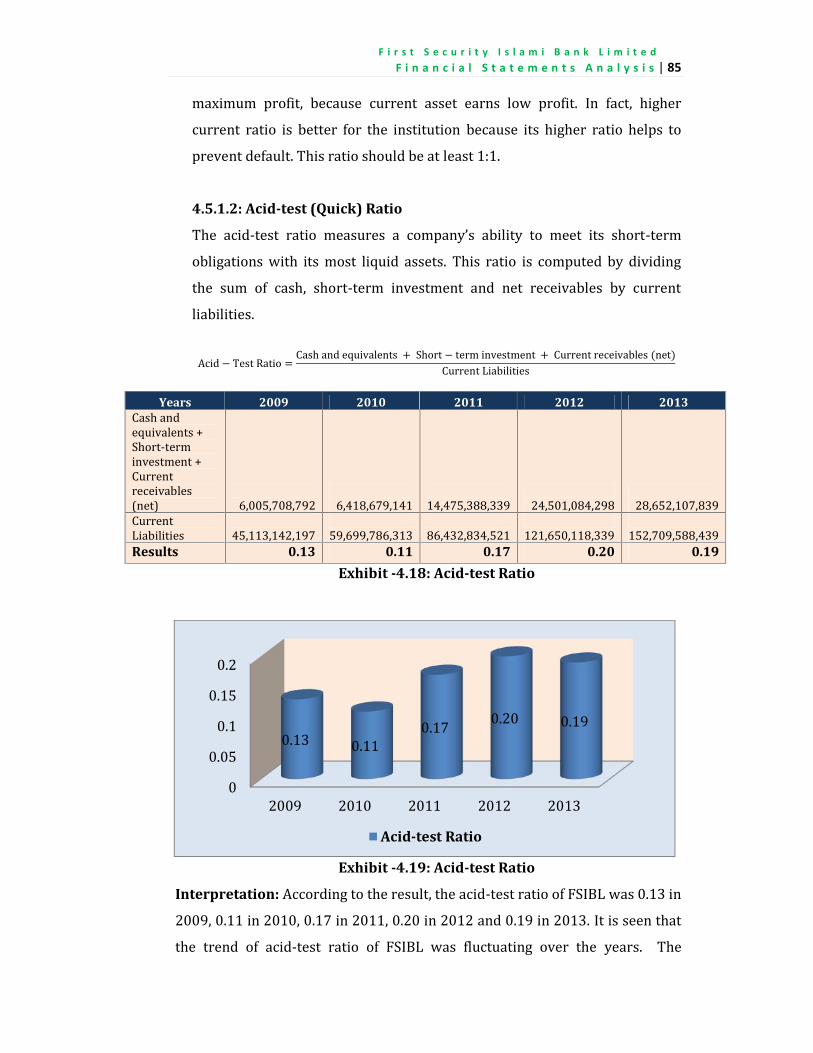

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 32A banking company may maintain current ratio of less than 1:1according to its banking principle for efficient investment of its collecteddeposits. Acid-Test (Quick) Ratio: The measurement used by business toanalysis their ability to pay their current liabilities with current assetsexcluding less liquid assets is acid-test ratio. It is also called quick ratio.Quick assets are cash, short-term investments and current receivables.These are the most liquid types of assets. Acid-test ratio is differs fromcurrent ratio by excluding less liquid assets such as inventory andprepaid expenses, because they take longer time to be converted intocash. The acid-test test or quick ratio is defined as quick assets (cash,short-term investment and current receivable) divided by currentliabilities. Its formula is given below:

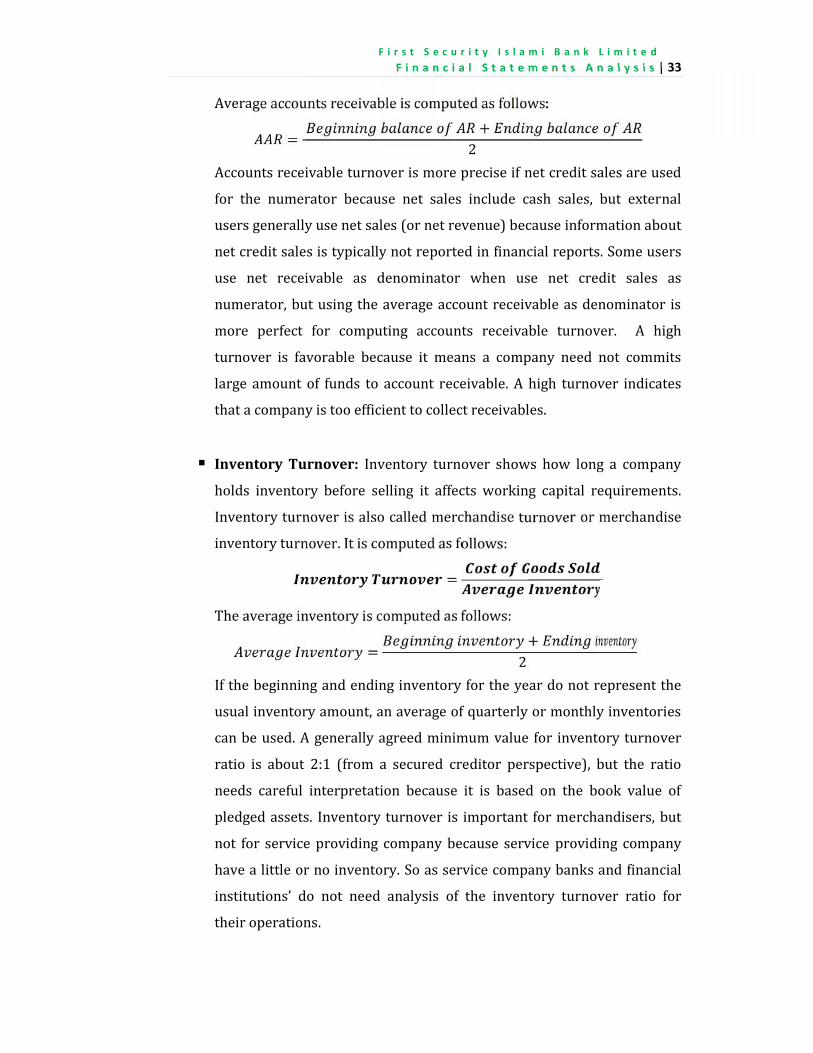

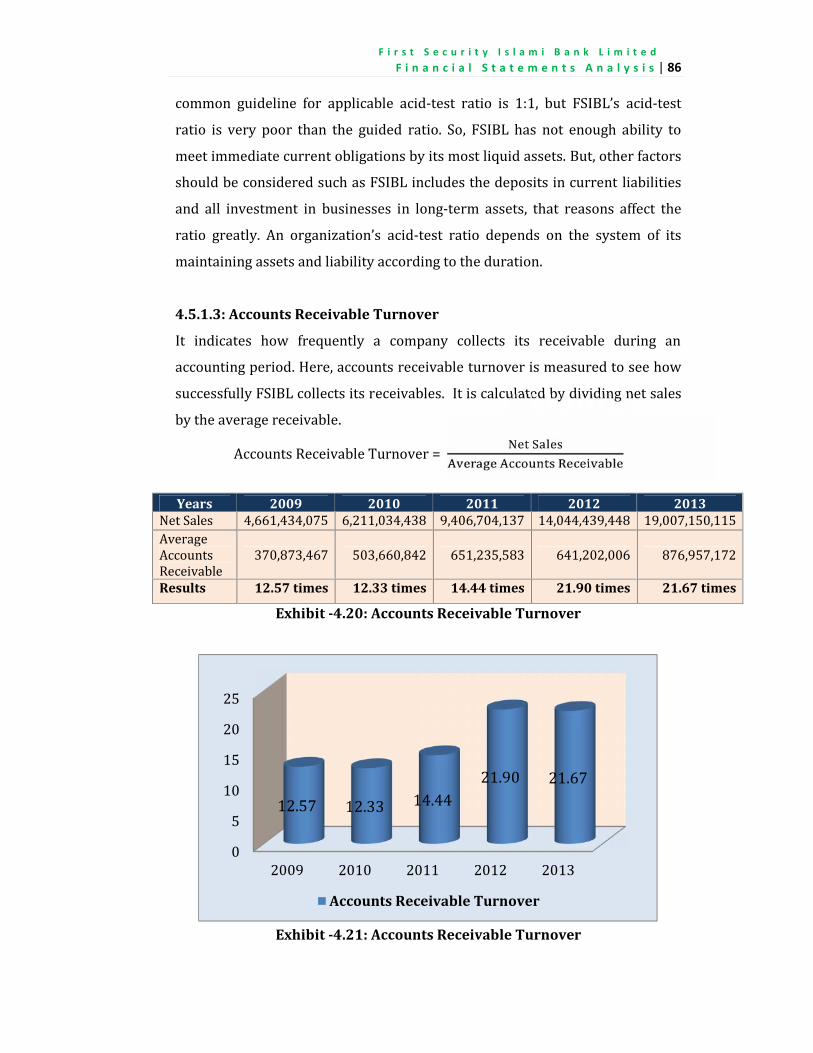

- = ( )The common guideline for an acceptable acid-test ratio is 1:1. Similar toanalysis of current ratio, we need to consider other factors. For instance,the frequency with which a company converts its current assets intocash affects its working capital requirements. Acid-test ratio is the mostimportant measurement for banking companies as financial institutions. Accounts Receivable Turnover: We can measure how frequently acompany converts its receivables into cash by computing accountreceivable turnover. Account receivable turnover is a measure of boththe quality and liquidity of account receivables. Quality of receivablesrefers to the likelihood of collection without loss. Liquidity of receivablerefers to the speed of collection. Accounts receivable turnover iscomputed by dividing net sales by average account receivable. Itsformula is given below: =

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 33Average accounts receivable is computed as follows:= +2Accounts receivable turnover is more precise if net credit sales are usedfor the numerator because net sales include cash sales, but externalusers generally use net sales (or net revenue) because information aboutnet credit sales is typically not reported in financial reports. Some usersuse net receivable as denominator when use net credit sales asnumerator, but using the average account receivable as denominator ismore perfect for computing accounts receivable turnover. A highturnover is favorable because it means a company need not commitslarge amount of funds to account receivable. A high turnover indicatesthat a company is too efficient to collect receivables. Inventory Turnover: Inventory turnover shows how long a companyholds inventory before selling it affects working capital requirements.Inventory turnover is also called merchandise turnover or merchandiseinventory turnover. It is computed as follows:=The average inventory is computed as follows:= +2If the beginning and ending inventory for the year do not represent theusual inventory amount, an average of quarterly or monthly inventoriescan be used. A generally agreed minimum value for inventory turnoverratio is about 2:1 (from a secured creditor perspective), but the rationeeds careful interpretation because it is based on the book value ofpledged assets. Inventory turnover is important for merchandisers, butnot for service providing company because service providing companyhave a little or no inventory. So as service company banks and financialinstitutions’ do not need analysis of the inventory turnover ratio fortheir operations.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

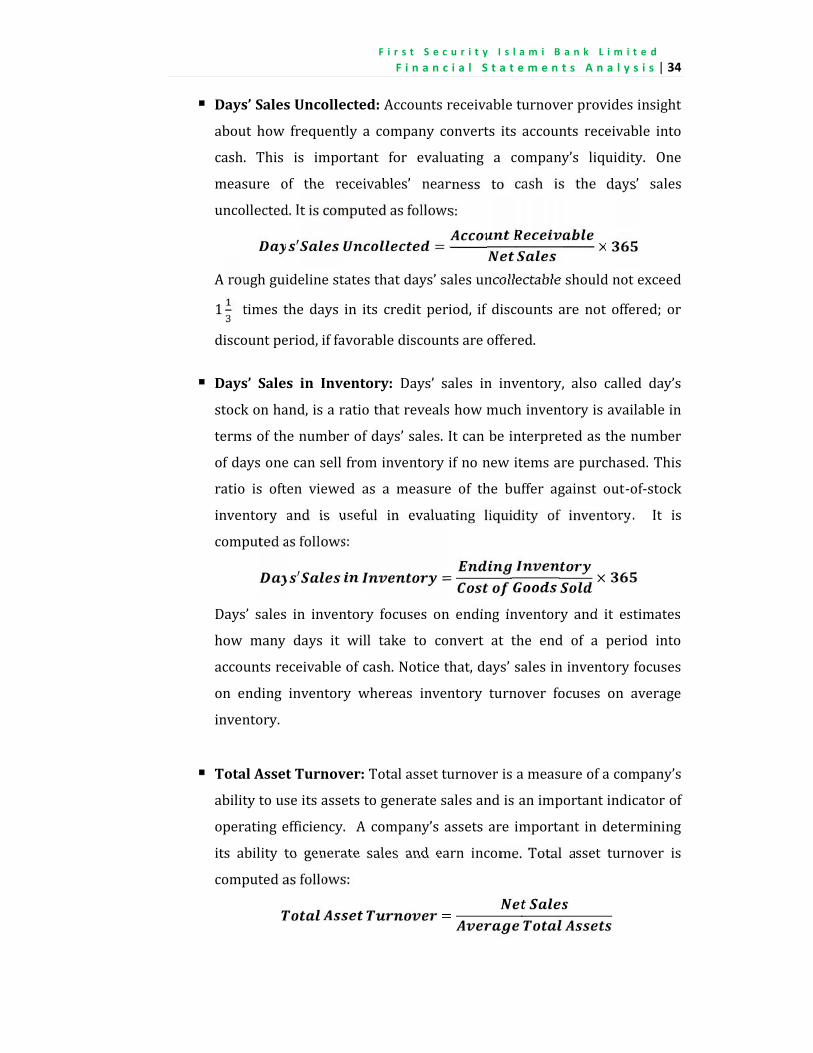

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 34

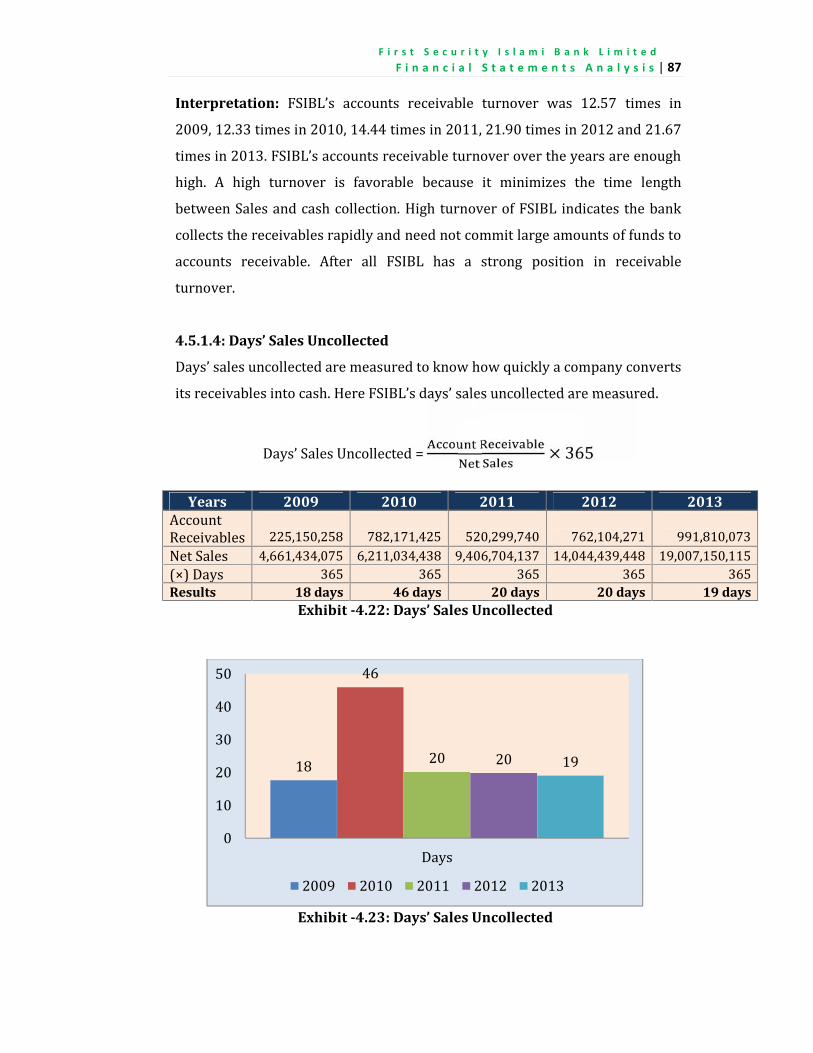

Days’ Sales Uncollected: Accounts receivable turnover provides insightabout how frequently a company converts its accounts receivable intocash. This is important for evaluating a company’s liquidity. Onemeasure of the receivables’ nearness to cash is the days’ salesuncollected. It is computed as follows:= ×A rough guideline states that days’ sales uncollectable should not exceed1 times the days in its credit period, if discounts are not offered; ordiscount period, if favorable discounts are offered. Days’ Sales in Inventory: Days’ sales in inventory, also called day’sstock on hand, is a ratio that reveals how much inventory is available interms of the number of days’ sales. It can be interpreted as the numberof days one can sell from inventory if no new items are purchased. Thisratio is often viewed as a measure of the buffer against out-of-stockinventory and is useful in evaluating liquidity of inventory. It iscomputed as follows: = ×Days’ sales in inventory focuses on ending inventory and it estimateshow many days it will take to convert at the end of a period intoaccounts receivable of cash. Notice that, days’ sales in inventory focuseson ending inventory whereas inventory turnover focuses on averageinventory. Total Asset Turnover: Total asset turnover is a measure of a company’sability to use its assets to generate sales and is an important indicator ofoperating efficiency. A company’s assets are important in determiningits ability to generate sales and earn income. Total asset turnover iscomputed as follows: =

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 35

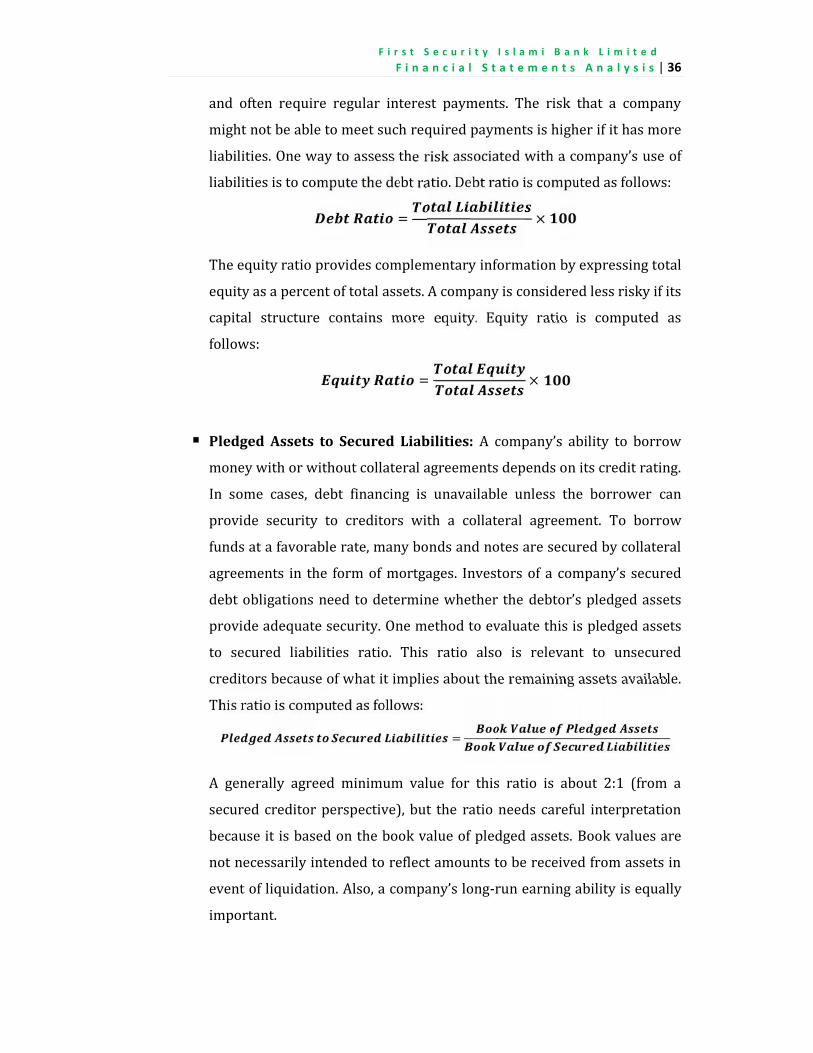

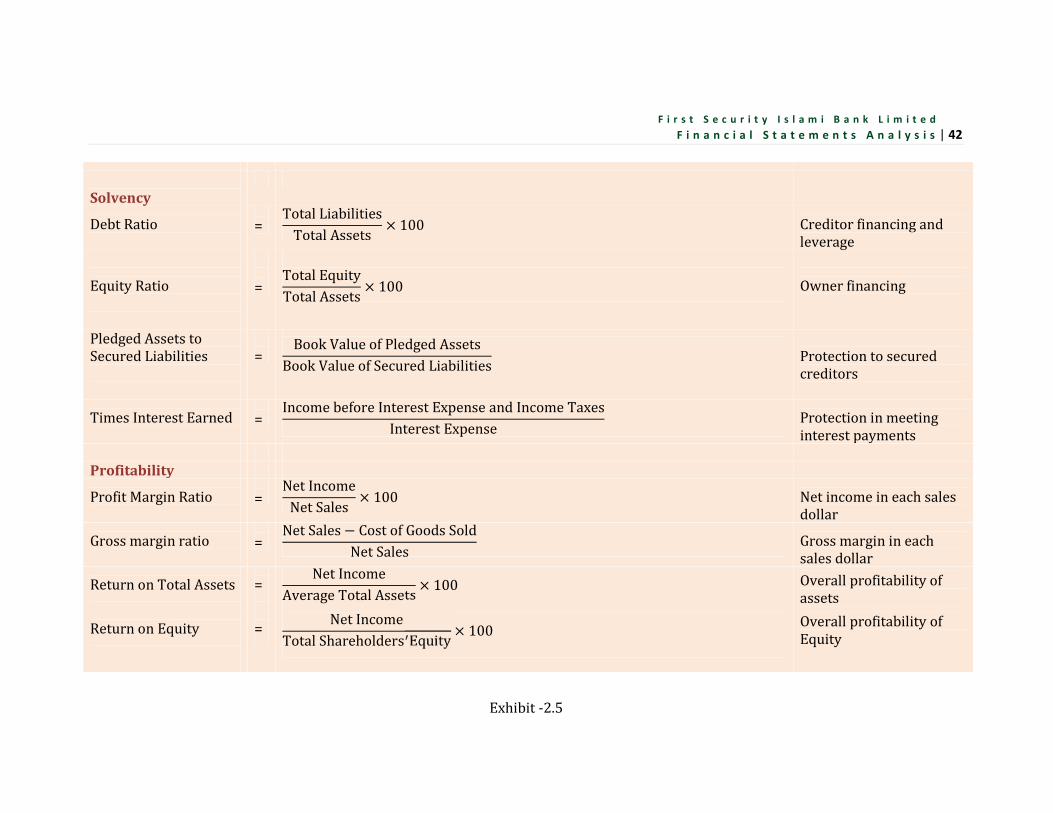

Average total assets is computed as follows:= +2Companies desire higher total asset turnover from their operations.Interpreting the total asset turnover also requires an understanding ofthe company’s operations. Some operations are capital intensive,meaning that a relatively large amount is invested in assets to generatesales. This suggests a relatively lower total asset turnover. Othercompanies’ having labor intensive operations, meaning that generatesales more by the efforts of people than using assets.2.11.6.2: Solvency RatiosSolvency refers to a company’s long-run financial viability and its ability tocover long-term obligations. All of a company’s business activities likefinancing, investing and operating activities affect its solvency. Analysis ofsolvency is long term and uses less precise but more encompassingmeasures than liquidity. One of the most important components of solvencyanalysis is the composition of a company’s capital structure. Capitalstructure refers to a company’s financing sources. It ranges from relativelypermanent equity financing to riskier or more temporary short-termfinancing. This analysis focuses on a company’s ability to meet itsobligations and provide security to its creditors over long run. Indicators ofthis ability include debt and equity ratios, the relation between pledgedassets and secured liabilities, and the company’s capacity to earn sufficientincome to pay fixed interest charges. Debt and Equity Ratios: One element of solvency analysis is to assessthe portion of a company’s assets contributed by creditors and theportion contributed by its owners is called debt and equity ratio. Acompany that finances a relatively large portion of its assets withliabilities is said to have a high degree of financial leverage. Higherfinancial leverage involves greater risk because liabilities must be repaid

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 36and often require regular interest payments. The risk that a companymight not be able to meet such required payments is higher if it has moreliabilities. One way to assess the risk associated with a company’s use ofliabilities is to compute the debt ratio. Debt ratio is computed as follows:= ×The equity ratio provides complementary information by expressing totalequity as a percent of total assets. A company is considered less risky if itscapital structure contains more equity. Equity ratio is computed asfollows: = × Pledged Assets to Secured Liabilities: A company’s ability to borrowmoney with or without collateral agreements depends on its credit rating.In some cases, debt financing is unavailable unless the borrower canprovide security to creditors with a collateral agreement. To borrowfunds at a favorable rate, many bonds and notes are secured by collateralagreements in the form of mortgages. Investors of a company’s secureddebt obligations need to determine whether the debtor’s pledged assetsprovide adequate security. One method to evaluate this is pledged assetsto secured liabilities ratio. This ratio also is relevant to unsecuredcreditors because of what it implies about the remaining assets available.This ratio is computed as follows: =

A generally agreed minimum value for this ratio is about 2:1 (from asecured creditor perspective), but the ratio needs careful interpretationbecause it is based on the book value of pledged assets. Book values arenot necessarily intended to reflect amounts to be received from assets inevent of liquidation. Also, a company’s long-run earning ability is equallyimportant.

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 37

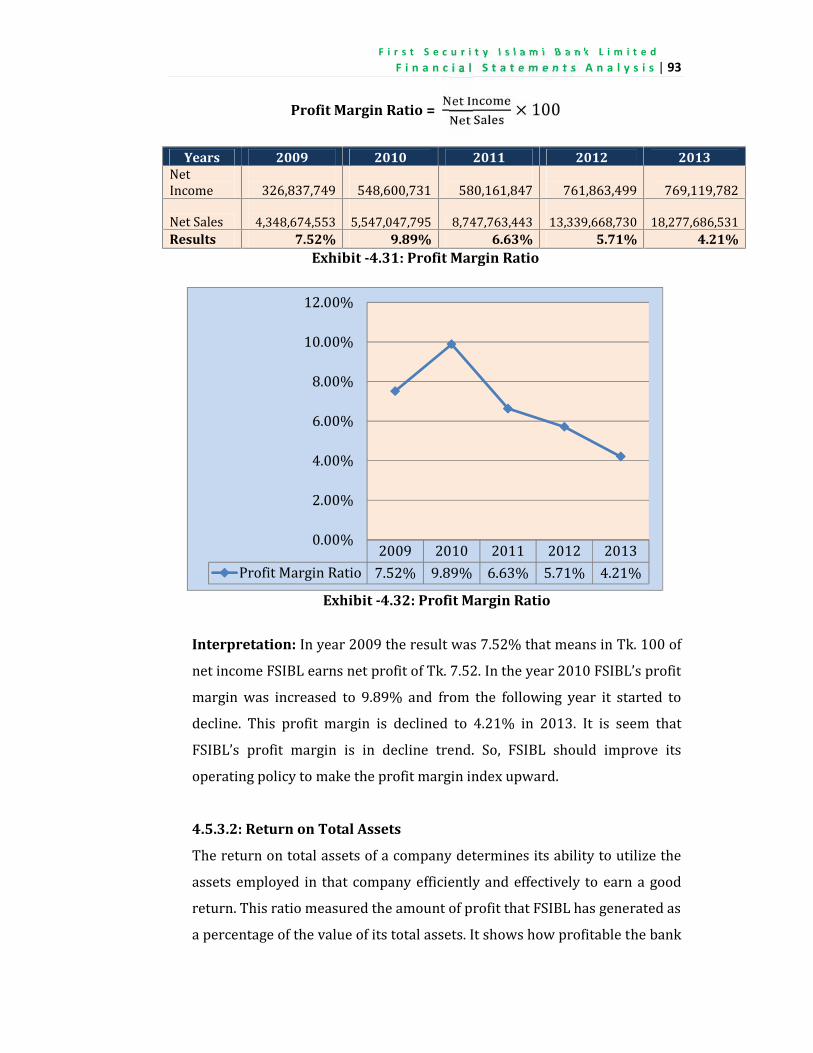

Times Interest Earned: The amount of income before deductions forinterest expense and income taxes is the amount available to pay interestexpense. A company incurs expenses on many of its current and long-term liabilities. Interest expense is often viewed as a fixed expensebecause the amount of these liabilities is likely to remain in one form oranother for a substantial period of time. This means that the amount ofinterest is unlikely to vary due to change in sales or other operatingactivities. While fixed expenses can be advantageous when a company isgrowing, they create risk. This risk stems from the possibility that acompany might be unable to pay fixed expenses if sales decline. Onemethod that measures a company’s ability to pay interest expenses istimes interest earned ratio. This ratio is computed as follows:=The larger this ratio, the less risky is the company for creditors. Oneguideline says that the creditors are reasonably safe if the company earnsits fixed interest expense two or more times each year.2.11.6.3: Profitability RatiosWe are especially interested in a company’s ability to use its assetsefficiently to produce profits and positive cash flows. Profitability refers to acompany’s ability to generate an adequate return on invested capital. Returnis judged by assessing earnings relative to the level and source of financing.Profitability is also relevant to solvency. This section describes keyprofitability measures and their importance to financial statement analysis. Profit Margin: A useful measure of a company’s operating results is theratio of its net income to net sales. This ratio is called profit margin. Itreflects a company’s ability to earn net income from sales. Profit margin iscomputed as follows: = ×100

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

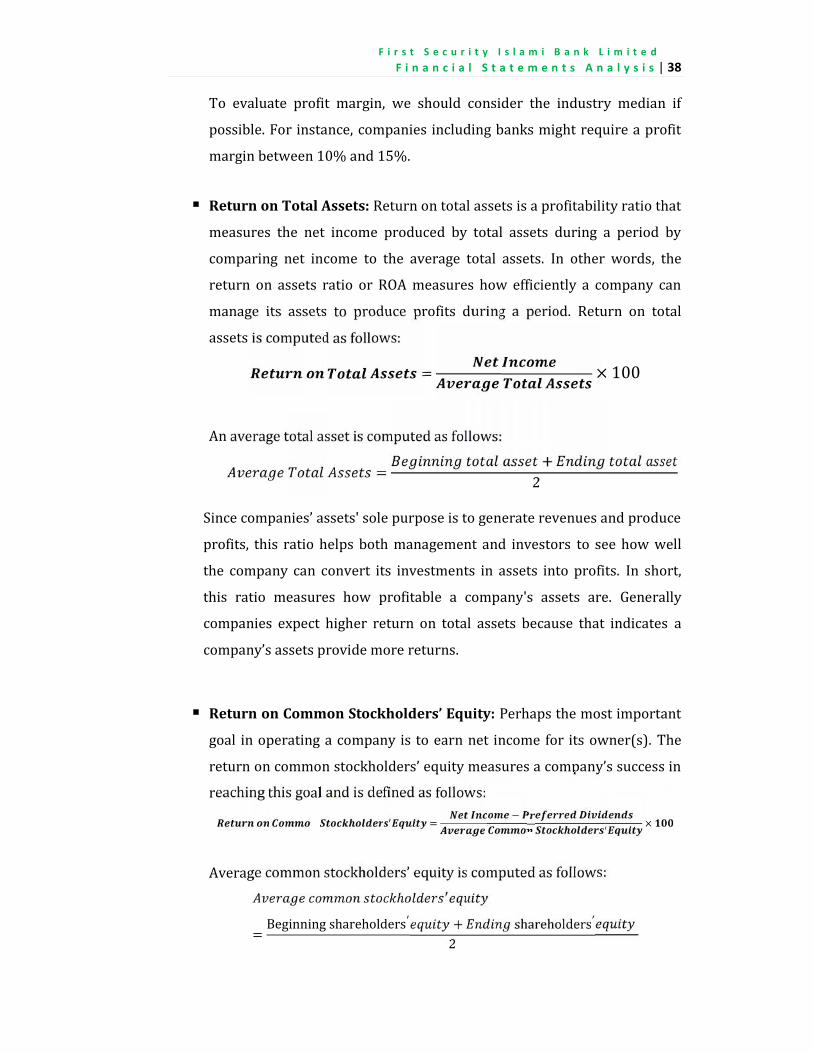

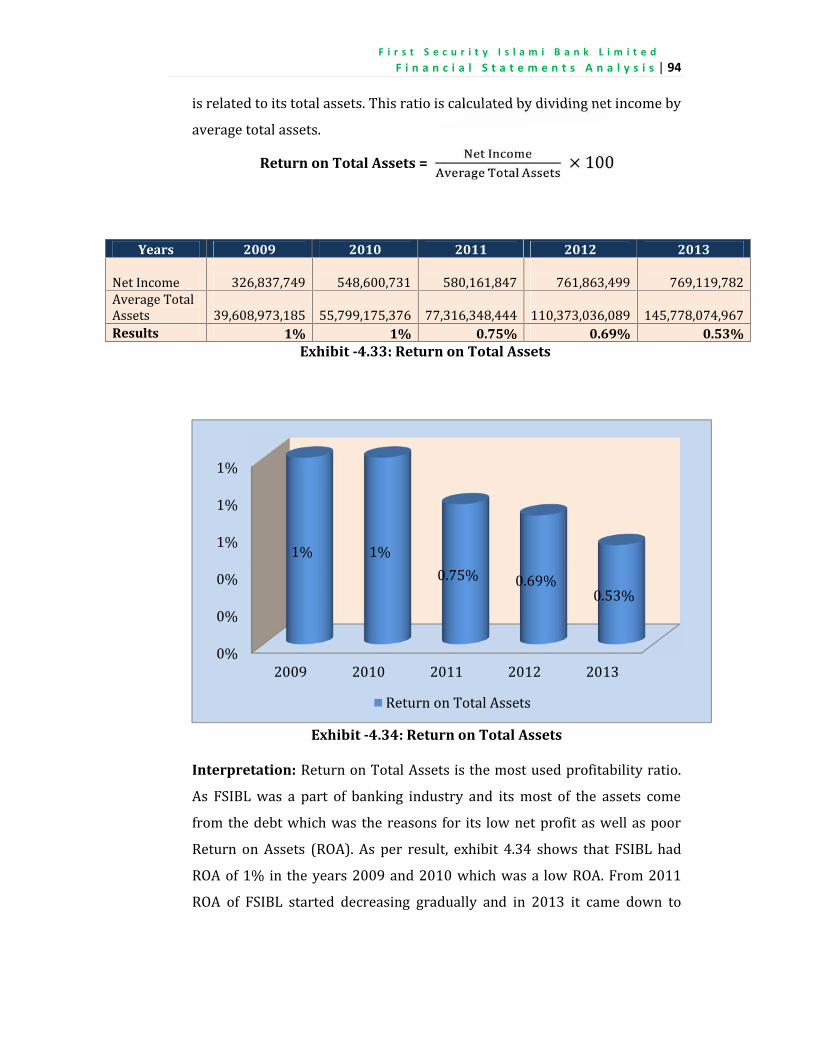

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 38To evaluate profit margin, we should consider the industry median ifpossible. For instance, companies including banks might require a profitmargin between 10% and 15%. Return on Total Assets: Return on total assets is a profitability ratio thatmeasures the net income produced by total assets during a period bycomparing net income to the average total assets. In other words, thereturn on assets ratio or ROA measures how efficiently a company canmanage its assets to produce profits during a period. Return on totalassets is computed as follows: = × 100

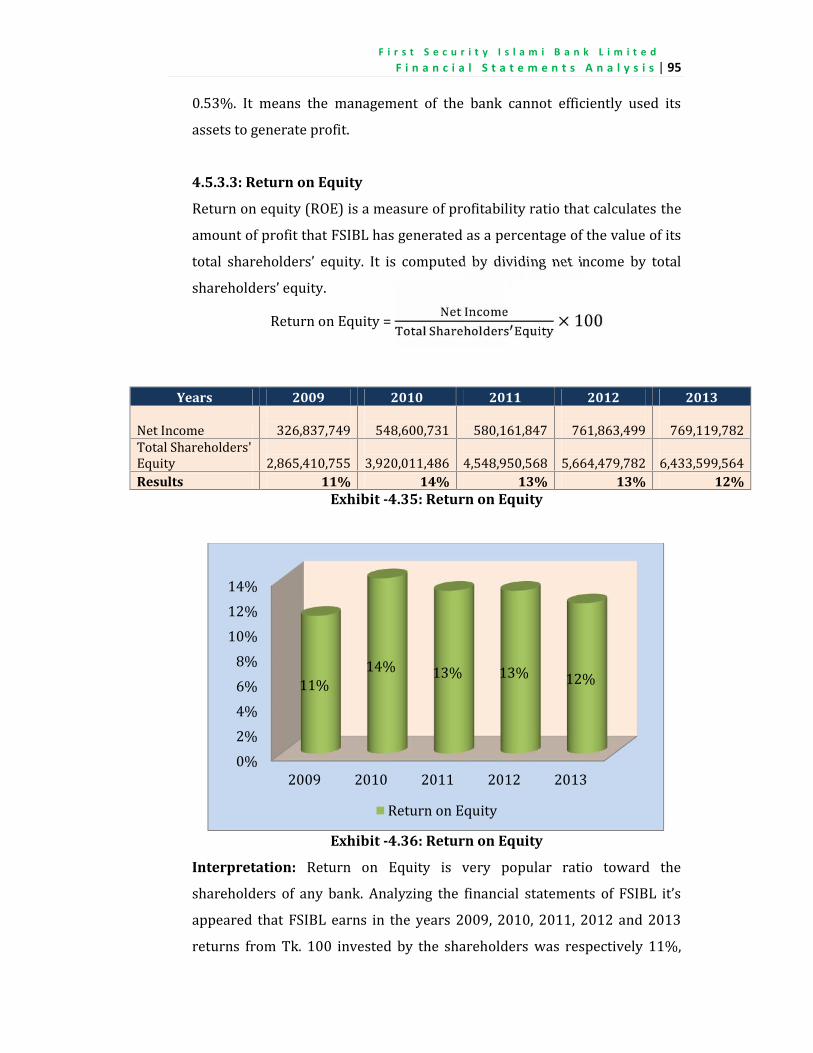

An average total asset is computed as follows:= +2Since companies’ assets' sole purpose is to generate revenues and produceprofits, this ratio helps both management and investors to see how wellthe company can convert its investments in assets into profits. In short,this ratio measures how profitable a company's assets are. Generallycompanies expect higher return on total assets because that indicates acompany’s assets provide more returns. Return on Common Stockholders’ Equity: Perhaps the most importantgoal in operating a company is to earn net income for its owner(s). Thereturn on common stockholders’ equity measures a company’s success inreaching this goal and is defined as follows:= − ×

Average common stockholders’ equity is computed as follows:ℎ= Beginning shareholders′ + shareholders′2

F i r s t S e c u r i t y I s l a m i B a n k L i m i t e d . . .

F i n a n c i a l S t a t e m e n t s A n a l y s i s | 39The denominator in this computation is the book value of common equityincluding any minority interest. In the numerator, the dividends oncumulative preferred stock are subtracted whether they are declared orare in arrears. If preferred stock is noncumulative, its dividends aresubtracted only if declared.2.11.6.4: Market Prospects RatiosMarket measures are useful for analyzing corporations with publicly tradedstock. These market measures use stock price, which reflects the market’s(public’s) expectations for the company. This includes expectations of bothcompany’s return and risk as market perceives it. Price-Earnings Ratio: A stock’s market value is determined by itsexpected future cash flows. A comparison of a company’s EPS and itsmarket value per share reveals information about market expectations.This comparison is traditionally made using a price-earnings ratio. Price-earnings ratio can be viewed as an indicator of the market’s expectedgrowth and risk for a stock. Some analysts interpret this ratio as whatprice the market is willing to pay for a company’s current earningsstream. Price-earnings ratios can differ across companies that havesimilar earnings because of either higher or lower expectations of futureearnings. A high level of expected risk suggests a low PE ratio. A highgrowth rate suggests a high PE ratio. The price-earnings ratio is definedas follows: