Embed Size (px)

Citation preview

INTERNATIONAL ISSUES

FILING TAXES FOR RESIDENT ALIENS, NON RESIDENT ALIENS AND ILLEGAL ALIENS

PRESENTER: Hortencia Torres, JD,EA, ABAGLOBAL TAX

920 W. Broad St.Falls Church, VA 22046

STATISTICS

PERMANENT RESIDENT STATUS PROCESSED 1820-2007 ALMOST TWO HUNDRED YEARS OF CONTINUING INMIGRATION

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,0001,800,0002,000,000

1820

1828

1836

1844

1852

1860

1868

1876

1884

1892

1900

1908

1916

1924

1932

1940

1948

1956

1964

1972

1980

1988

1996

2004

Year

Pers

ons

(Source: dhs.gov)

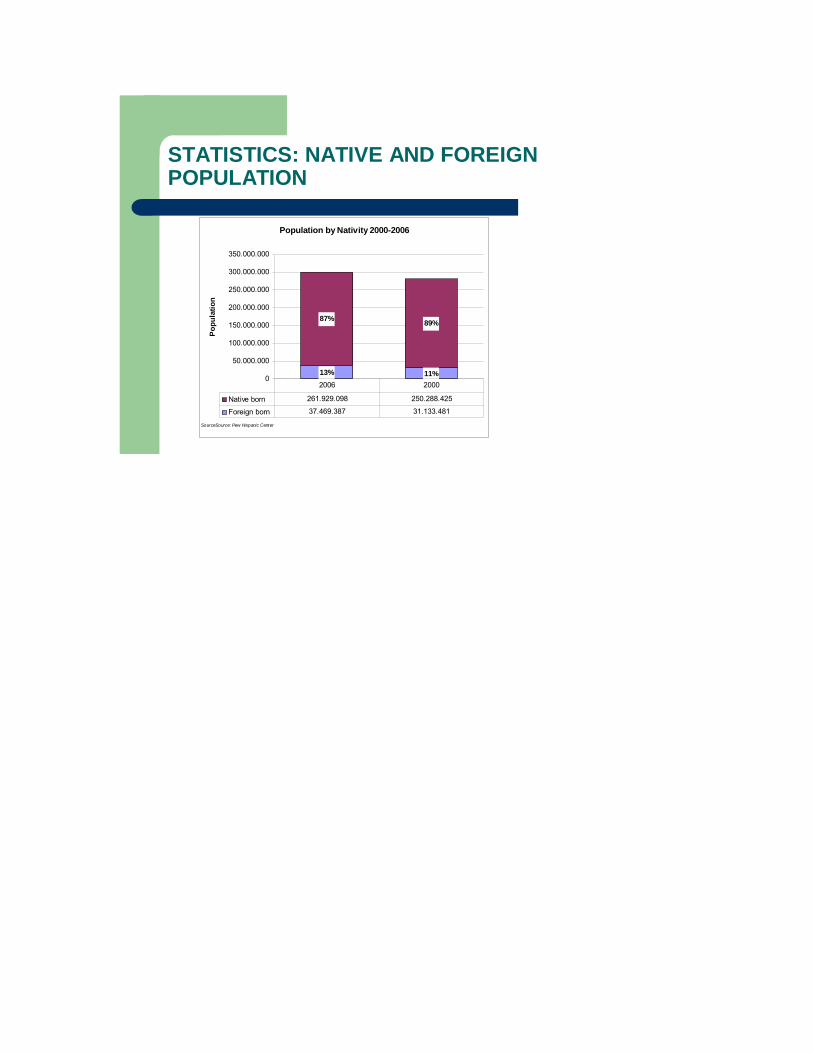

STATISTICS: NATIVE AND FOREIGN POPULATION

Population by Nativity 2000-2006

13% 11%

87% 89%

0

50.000.000

100.000.000

150.000.000

200.000.000

250.000.000

300.000.000

350.000.000

SourceSource: Pew Hispanic Center

Pop

ulat

ion

Native born 261.929.098 250.288.425

Foreign born 37.469.387 31.133.481

2006 2000

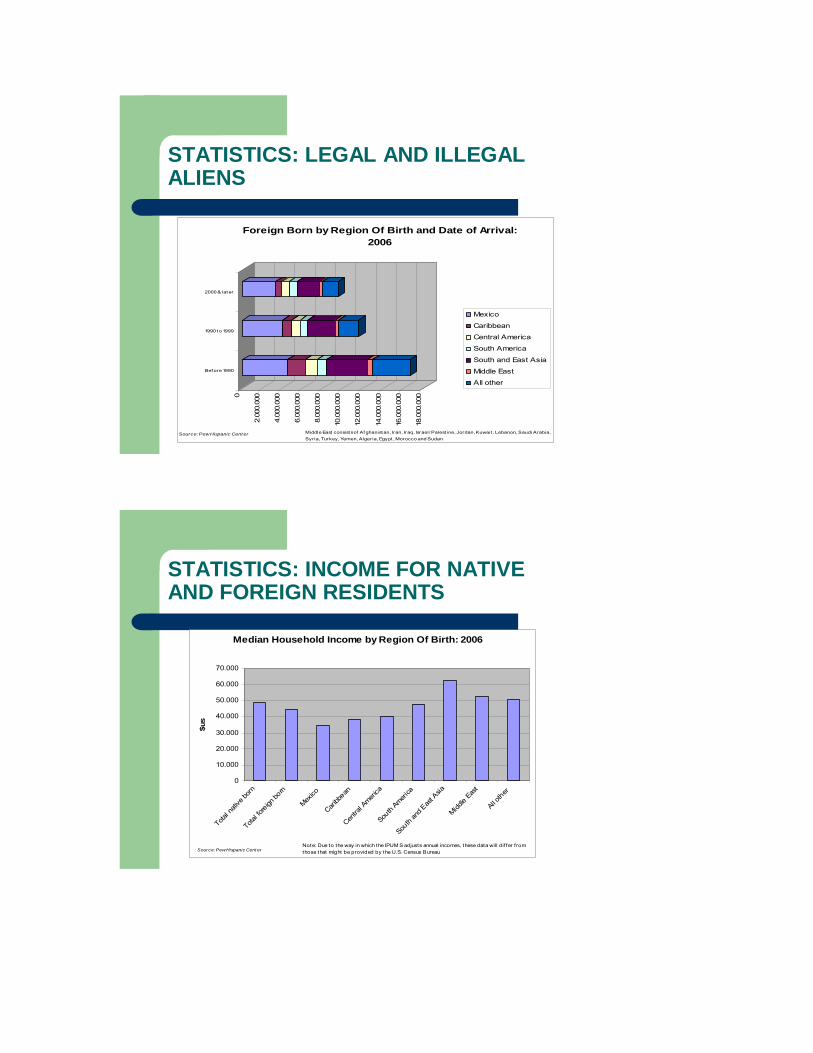

STATISTICS: LEGAL AND ILLEGAL ALIENS

0

2.00

0.00

0

4.00

0.00

0

6.00

0.00

0

8.00

0.00

0

10.0

00.0

00

12.0

00.0

00

14.0

00.0

00

16.0

00.0

00

18.0

00.0

00

Source: Pew Hispanic Cent er

Bef ore 1990

1990 t o 1999

2000 & lat er

Foreign Born by Region Of Birth and Date of Arrival: 2006

Mexico

Caribbean

Central America

South America

South and East Asia

Middle East

All other

Middle East consist s of Af ghanist an, Iran, Iraq, Israel/ Palest ine, Jordan, Kuwait , Lebanon, Saudi Arabia, Syria, Turkey, Yemen, Algeria, Egypt , Morocco and Sudan.

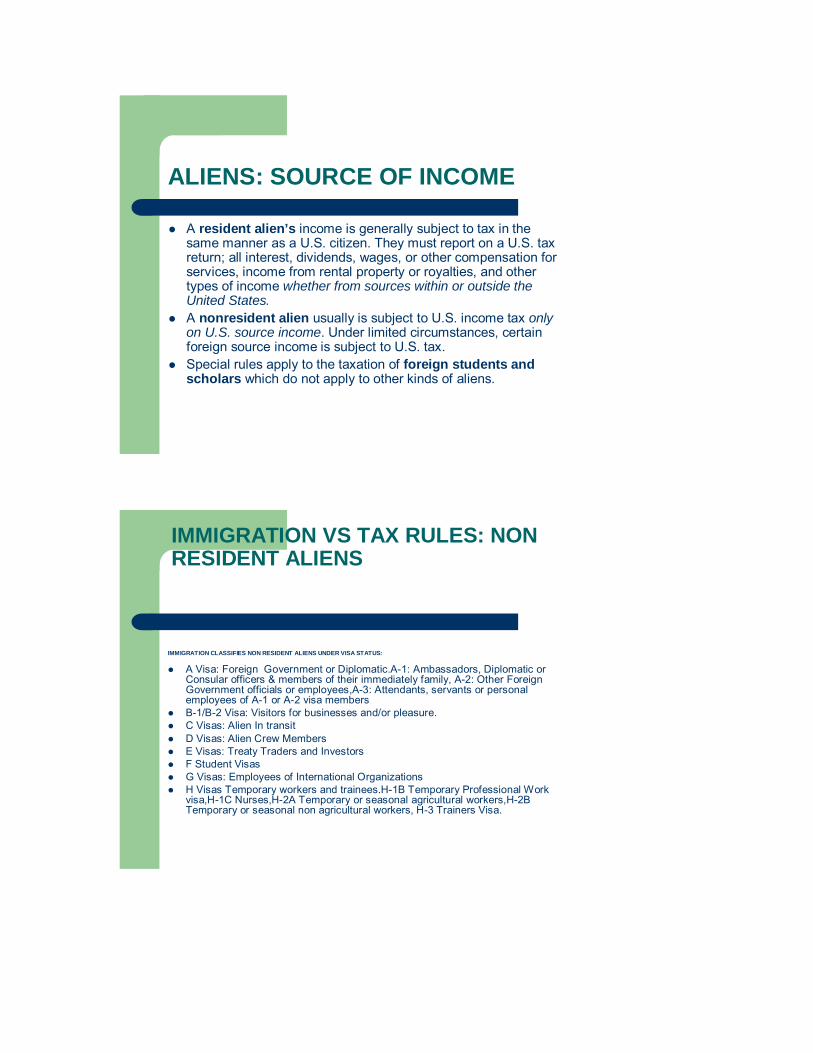

STATISTICS: INCOME FOR NATIVE AND FOREIGN RESIDENTS

Median Household Income by Region Of Birth: 2006

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

Total n

ative

born

Total fo

reign

born

Mexico

Caribb

ean

Centra

l Amer

ica

South

America

South

and E

ast A

sia

Middle

East

All oth

er

$us

Source: Pew Hispanic Cent erNote: Due to the way in which the IPUM S adjusts annual incomes, these data will dif fer f rom those that might be provided by the U.S. Census Bureau

ALIENS: SOURCE OF INCOME

A resident alien’s income is generally subject to tax in the same manner as a U.S. citizen. They must report on a U.S. tax return; all interest, dividends, wages, or other compensation for services, income from rental property or royalties, and other types of income whether from sources within or outside the United States.A nonresident alien usually is subject to U.S. income tax only on U.S. source income. Under limited circumstances, certain foreign source income is subject to U.S. tax.Special rules apply to the taxation of foreign students and scholars which do not apply to other kinds of aliens.

IMMIGRATION VS TAX RULES: NON RESIDENT ALIENS

IMMIGRATION CLASSIFIES NON RESIDENT ALIENS UNDER VISA STATUS:

A Visa: Foreign Government or Diplomatic.A-1: Ambassadors, Diplomatic or Consular officers & members of their immediately family, A-2: Other Foreign Government officials or employees,A-3: Attendants, servants or personal employees of A-1 or A-2 visa membersB-1/B-2 Visa: Visitors for businesses and/or pleasure.C Visas: Alien In transitD Visas: Alien Crew MembersE Visas: Treaty Traders and InvestorsF Student Visas G Visas: Employees of International OrganizationsH Visas Temporary workers and trainees.H-1B Temporary Professional Work visa,H-1C Nurses,H-2A Temporary or seasonal agricultural workers,H-2B Temporary or seasonal non agricultural workers, H-3 Trainers Visa.

IMMIGRATION VS TAX RULES: NON RESIDENT ALIENS

I Visa: Foreign CorrespondentsJ Visa: Exchange Visitor Visa (Au-Pair, Summer Camp Counselors & Staff, Post graduate students, Medical Students (Interns)K Visa: Fiancée of U.S. CitizenL Visa Intra company TransfersM Visa: Non-Academic or Vocational Studies into a program to study or train at a non-academic institution in the U.S. N Visa: Special Category Family MembersO Visas: Extraordinary abilities in science, arts, education, business, athletics or extraordinary achievements in Movie-TV field.P Visas: Specially defined entertainers and athletes Q Visas: Cultural Exchange VisitorsR Visa: Religious WorkersS Visas: Aliens assisting certain government investigations

RESIDENT ALIENS FOR TAX PURPOSES

Green Card Test.- You are a resident for tax purposes if you are a lawful permanent resident of the US at any time during 2007 and/or if you have been given the privilege of residing permanently in the US as an immigrant. You generally have this status if the USCIS has issued a “green card.” You continue to have resident status under this test unless the status is taken away from you or is administratively or judicially determined to have been abandoned. Substantial Present Test.-You will be considered a U.S. resident for tax purposes if you meet the substantial presence test for calendar year 2007. To meet this test, you must be physically present in the United States on at least:

– 31 days during 2007, and – 183 days during the 3-year period that includes 2007, 2006, and 2005, counting:

All the days you were present in 2007, and⅓ of the days you were present in 2006, and⅙ of the days you were present in 2005.

– Do not count any day you were present in the United States as an "exempt individual" or commute from Canada or Mexico to work in the United States on more than 75% of the workdays during your working period.

EXEMPT INDIVIDUAL: NON RESIDENT ALIENS FOR TAX PURPOSES

The term “exempt individual” does not refer to someone exempt from U.S. tax, but to anyone in the following categories.

– An individual temporarily present in the United States as a foreign government-related individual.

– A teacher or trainee temporarily present in the United States under a “J” or “Q” visa, who substantially complies with the requirements of the visa.

– A student temporarily present in the United States under an “F,” “J,” “M,” or “Q” visa, who substantially complies with the requirements of the visa.

– A professional athlete temporarily in the United States to compete in a charitable sports event.

OTHER RESIDENT ALIENS FOR TAX PURPOSES

Non resident Spouse treated as a resident.-You can claim an exemption for your spouse on a Married Filing Separate return if your spouse had no gross income for U.S. tax purposes and was not the dependent of another taxpayer You can claim this exemption even if your spouse has not been a resident alien for a full tax year or is an alien who has not come to the United States. Non resident Dependents treated as residents.- You can claim an exemption for each person who qualifies as a dependent according to the rules for U.S. citizens. The dependent must be a citizen or national of the United States or be a resident of the United States, Canada, or Mexico for some part of the calendar year in which your tax year begins

NON RESIDENT ALIENS FOR TAX PURPOSES

Even if you meet the substantial presence test, you can be treated as a nonresident alien if you are present in the United States for fewer than 183 days during the current calendar year, you maintain a tax home in a foreign country during the year, and you have a closerconnection to that country than to the United States. This does not apply if you have applied for status as a lawful permanent resident of the United States, or you have an application pending for adjustment of status.Sometimes, a tax treaty between the United States and another country will provide special rules for determining residency forpurposes of the treaty.An alien whose status changes during the year from resident to nonresident, or vice versa, generally has a dual status for that year, and is taxed on the income for the two periods under the provisions of the law that apply to each period.

SSN VS ITIN

Taxpayer Identification Number.- Is an identification number used by the Internal Revenue Service (IRS) in the administration of tax laws. It is issued either by the Social Security Administration (Ex: SSN) or by the IRS (Ex: ITIN). Social Security Number (SSN).- A Social Security number (SSN) is issued by the Social Security Administration. You must submit evidence of your identity, age, and U.S. citizenship or lawful alien status. Individual Taxpayer Identification Number (ITIN).- Are issued by the IRS, is a tax processing number only available forcertain nonresident and resident aliens, their spouses, and dependents who cannot get a Social Security Number (SSN). It is a 9-digit number, beginning with the number "9", formatted like an SSN (NNN-NN-NNNN).

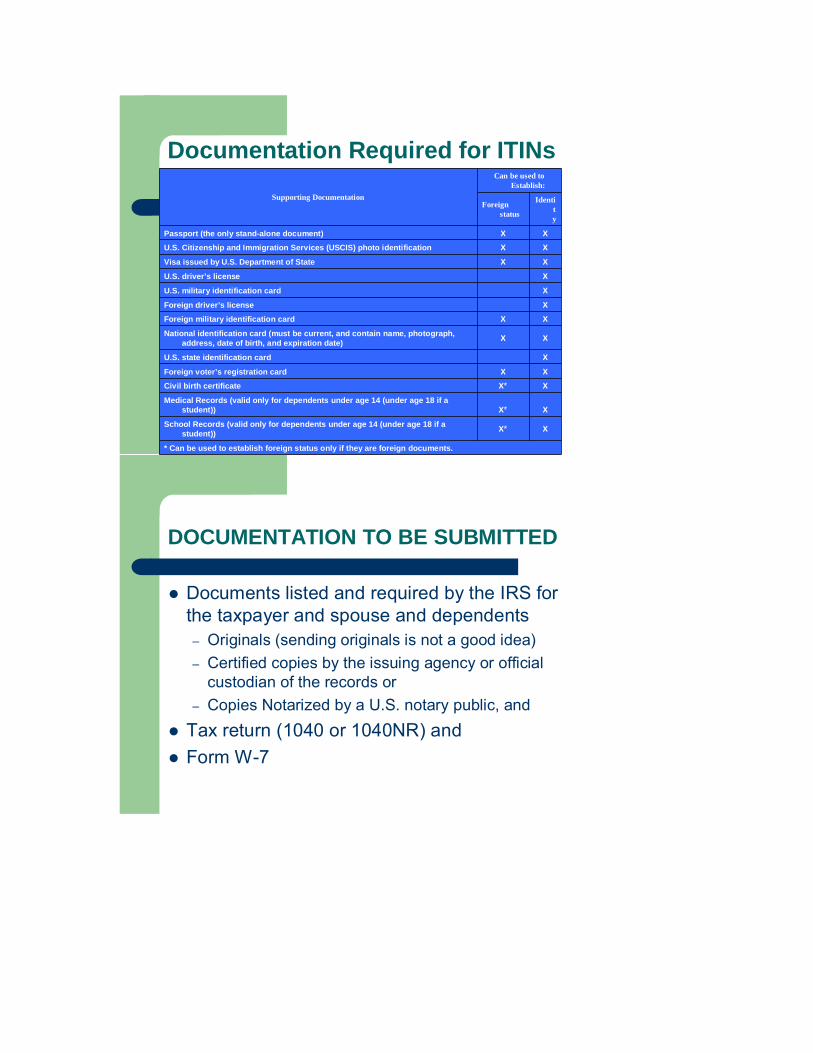

Supporting Documentation

Can be used to Establish:

Foreign status

Identity

Passport (the only stand-alone document) X X

U.S. Citizenship and Immigration Services (USCIS) photo identification X X

Visa issued by U.S. Department of State X X

U.S. driver’s license X

U.S. military identification card X

Foreign driver’s license X

Foreign military identification card X X

National identification card (must be current, and contain name, photograph, address, date of birth, and expiration date) X X

U.S. state identification card X

Foreign voter’s registration card X X

Civil birth certificate X* X

Medical Records (valid only for dependents under age 14 (under age 18 if a student)) X* X

School Records (valid only for dependents under age 14 (under age 18 if a student)) X* X

* Can be used to establish foreign status only if they are foreign documents.

Documentation Required for ITINs

DOCUMENTATION TO BE SUBMITTED

Documents listed and required by the IRS for the taxpayer and spouse and dependents – Originals (sending originals is not a good idea)– Certified copies by the issuing agency or official

custodian of the records or– Copies Notarized by a U.S. notary public, and

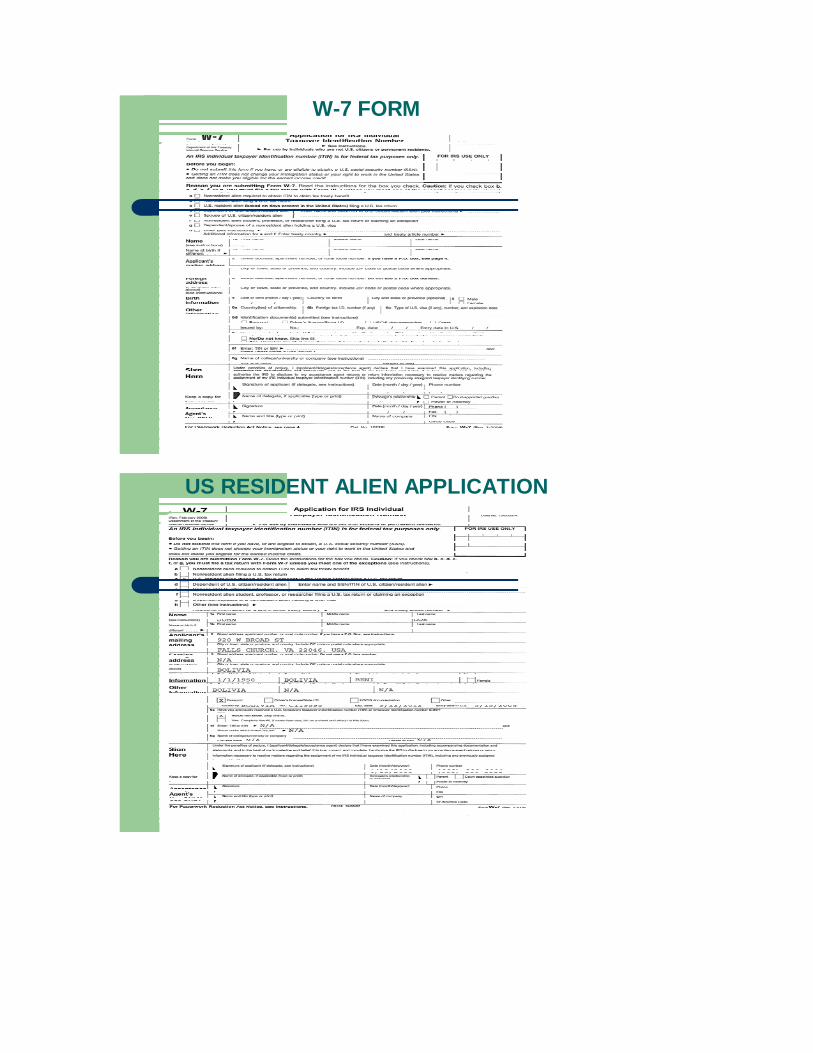

Tax return (1040 or 1040NR) andForm W-7

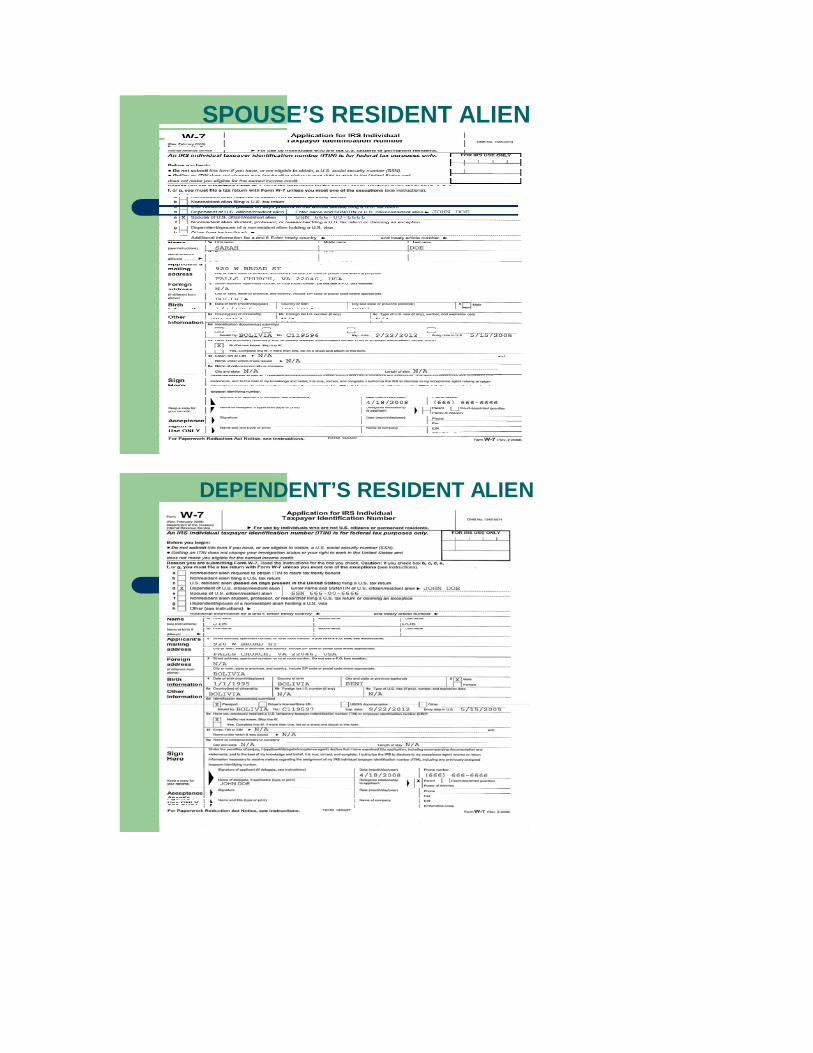

W-7 FORM

US RESIDENT ALIEN APPLICATION

SPOUSE’S RESIDENT ALIEN

DEPENDENT’S RESIDENT ALIEN

MISCELLANEOUS

Remember the USCIS have poverty guidelines that are important to share with taxpayers who earns wages in cash if they are planning to change their immigrant legal status in the future.The taxpayer’s spouse of an resident or non resident alien could be included as an exemption regardless if she or he is living out of the country.If a resident aliens are physically present in a foreign country or countries for at least 330 full days during any period of 12 consecutive months, may qualify for the foreign earned income exclusion. The exclusion is $85,700 in 2007. In addition, may be able to exclude or deduct certain foreign housing amounts.

MISCELLANEOUS

Employees of foreign persons, organizations, or offices. Income for personal services performed in the United States as a nonresident alien is not considered to be from U.S. sources and is tax exempt if you meet all three of the following conditions.

– You perform personal services as an employee of or under a contract with a nonresident alien individual, foreign partnership, or foreign corporation, not engaged in a trade or business in the United States; or you work for an office or place of business maintained in a foreign country or possession of the United States by a U.S. corporation, a U.S. partnership, or a U.S. citizen or resident.

– You perform these services while you are a nonresident alien temporarily present in the United States for a period or periods of not more than a total of 90 days during the tax year.

– Your pay for these services is not more than $3,000.

NEED HELP ?

Call GLOBAL TAX Customer Service at 703-533-3636 (not toll free)Mon-Fri. 10:00 am – 7:00 pm ESTCheck www.myglobaltax.comwww.irs.gov