Embed Size (px)

Citation preview

THE MANUFACTURING ECONOMIC UPDATE

Dr. Chad Moutray

Chief Economist National Association of Manufacturers

Revised July 24, 2014

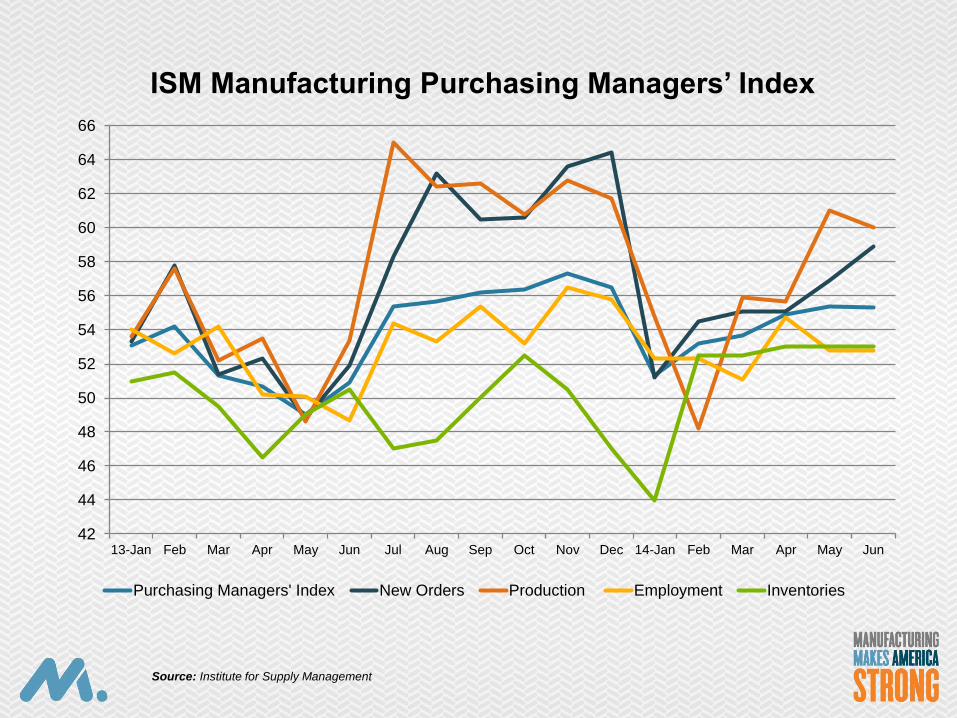

Manufacturing Output

42

44

46

48

50

52

54

56

58

60

62

64

66

13-Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 14-Jan Feb Mar Apr May Jun

ISM Manufacturing Purchasing Managers’ Index

Purchasing Managers' Index New Orders Production Employment Inventories

Source: Institute for Supply Management

-20

-15

-10

-5

0

5

10

15

20

25

30

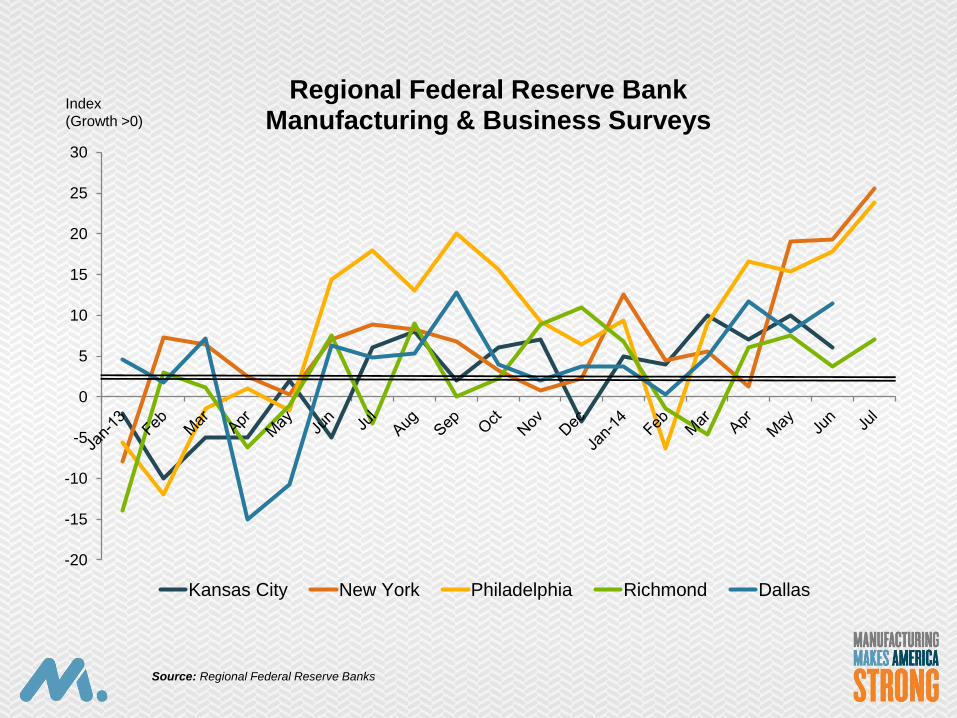

Regional Federal Reserve Bank Manufacturing & Business Surveys

Kansas City New York Philadelphia Richmond Dallas

Index

(Growth >0)

Source: Regional Federal Reserve Banks

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

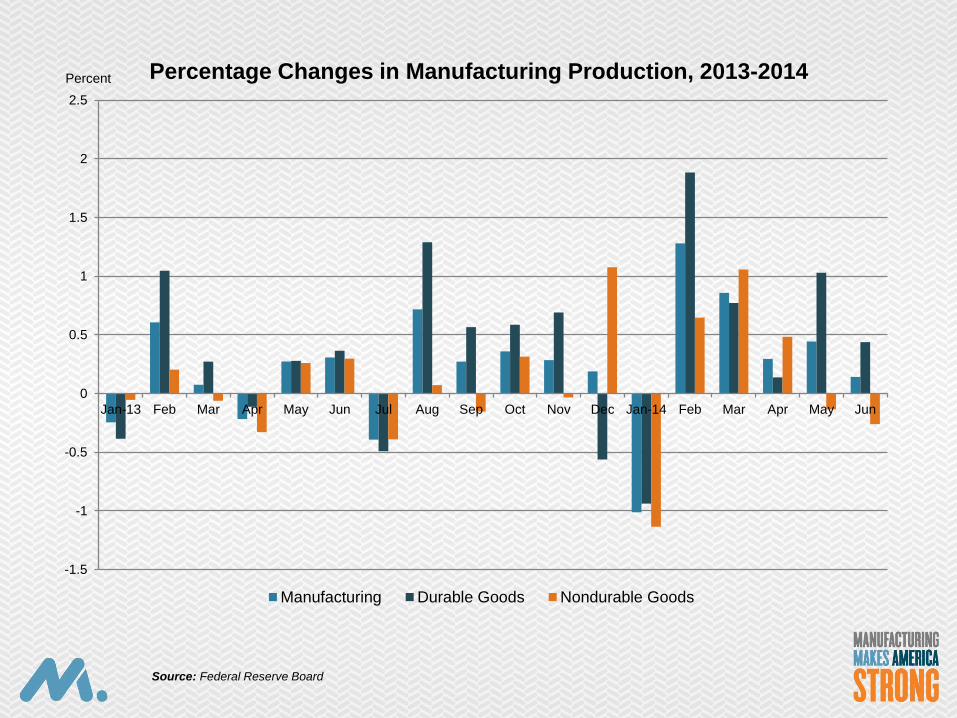

Jan-13 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan-14 Feb Mar Apr May Jun

Percentage Changes in Manufacturing Production, 2013-2014

Manufacturing Durable Goods Nondurable Goods

Percent

Source: Federal Reserve Board

0

1

2

3

4

5

6

7

8

9

10

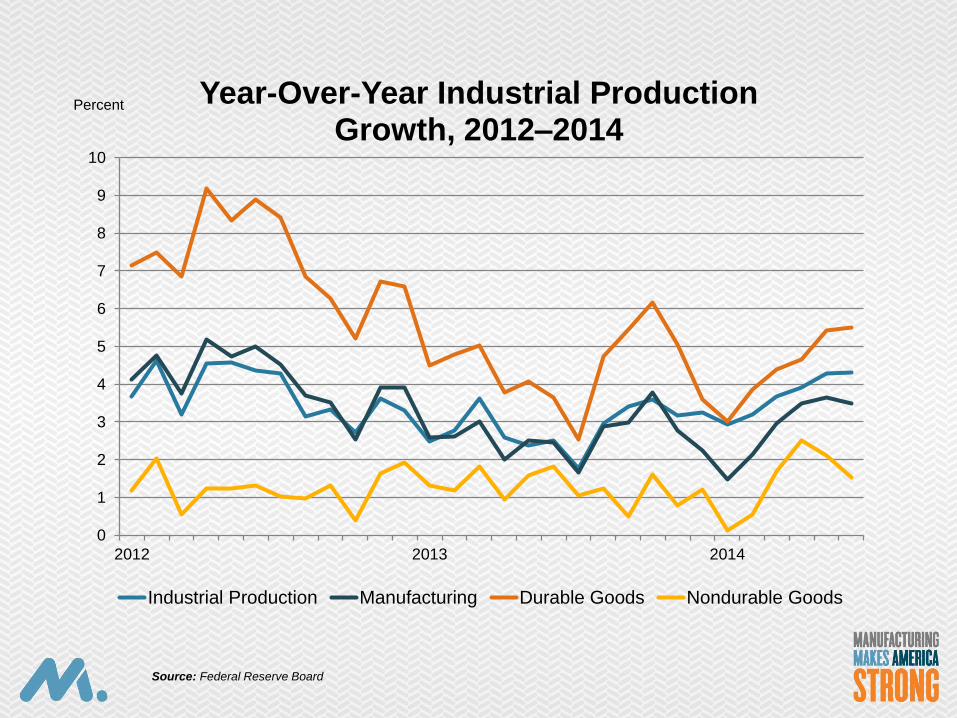

2012 2013 2014

Year-Over-Year Industrial Production Growth, 2012–2014

Industrial Production Manufacturing Durable Goods Nondurable Goods

Percent

Source: Federal Reserve Board

Economic Outlook

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

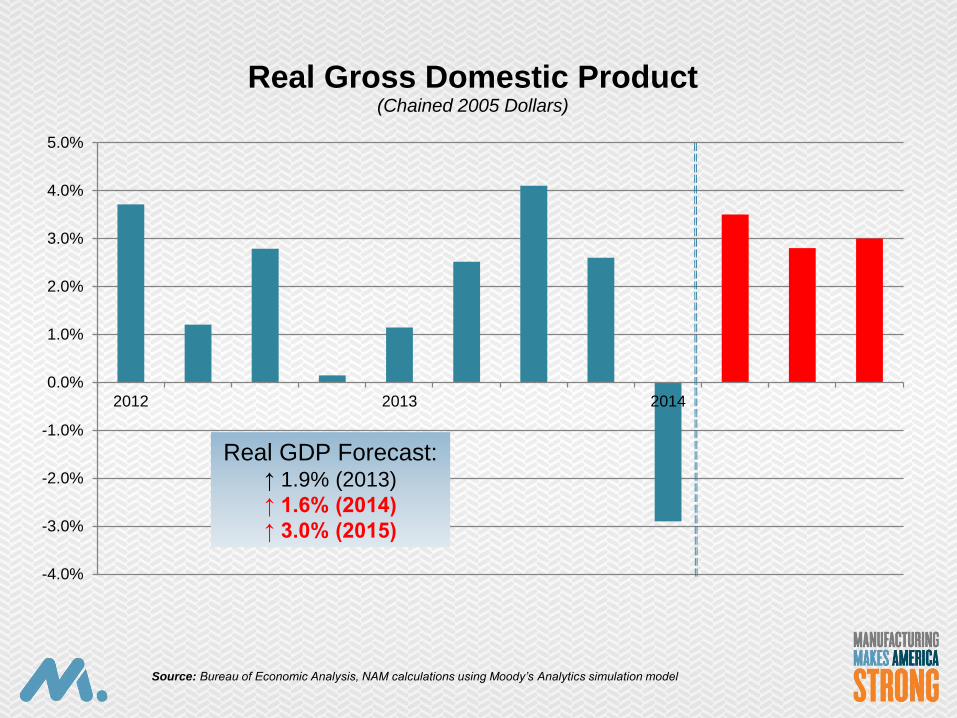

2012 2013 2014

Real Gross Domestic Product (Chained 2005 Dollars)

Real GDP Forecast: ↑ 1.9% (2013)

↑ 1.6% (2014)

↑ 3.0% (2015)

Source: Bureau of Economic Analysis, NAM calculations using Moody’s Analytics simulation model

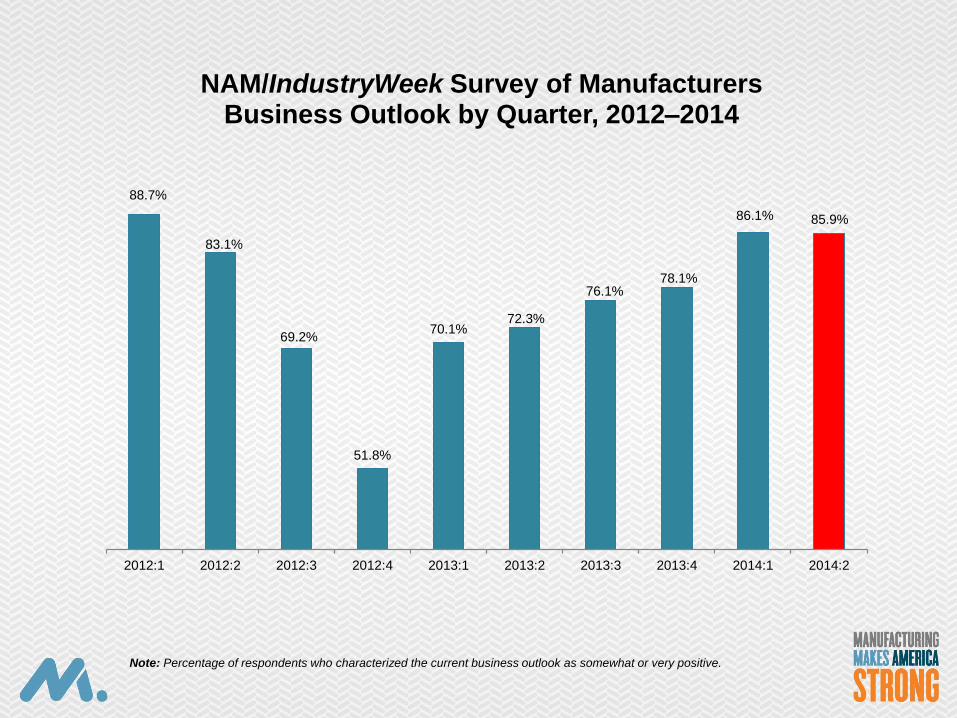

88.7%

83.1%

69.2%

51.8%

70.1% 72.3%

76.1% 78.1%

86.1% 85.9%

2012:1 2012:2 2012:3 2012:4 2013:1 2013:2 2013:3 2013:4 2014:1 2014:2

NAM/IndustryWeek Survey of Manufacturers Business Outlook by Quarter, 2012–2014

Note: Percentage of respondents who characterized the current business outlook as somewhat or very positive.

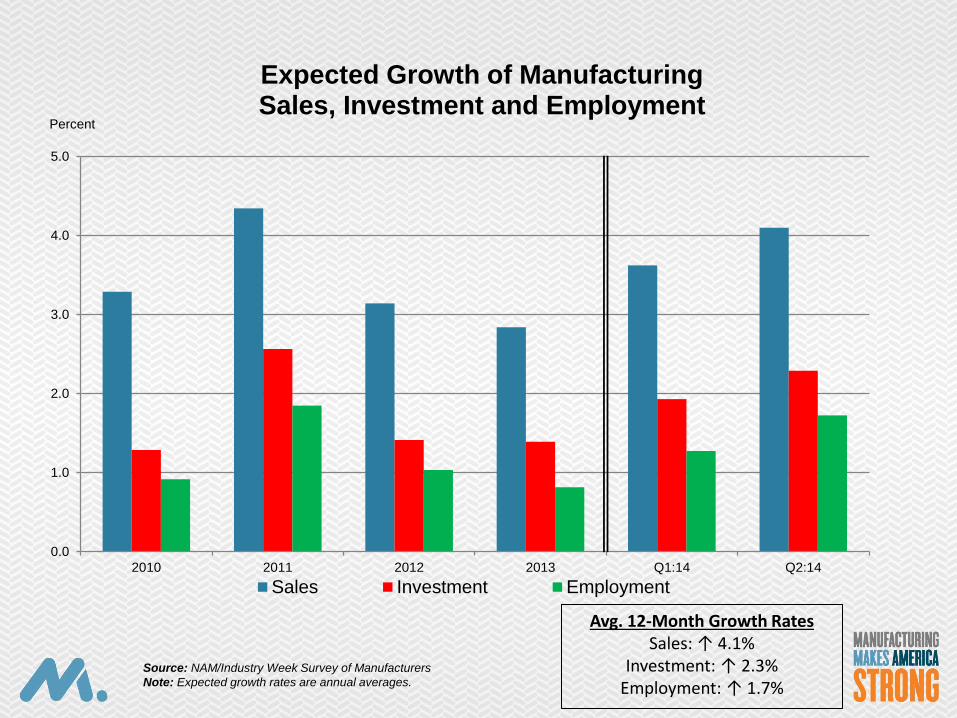

0.0

1.0

2.0

3.0

4.0

5.0

2010 2011 2012 2013 Q1:14 Q2:14

Expected Growth of Manufacturing Sales, Investment and Employment

Sales Investment Employment

Percent

Avg. 12-Month Growth Rates Sales: ↑ 4.1%

Investment: ↑ 2.3% Employment: ↑ 1.7%

Source: NAM/Industry Week Survey of Manufacturers

Note: Expected growth rates are annual averages.

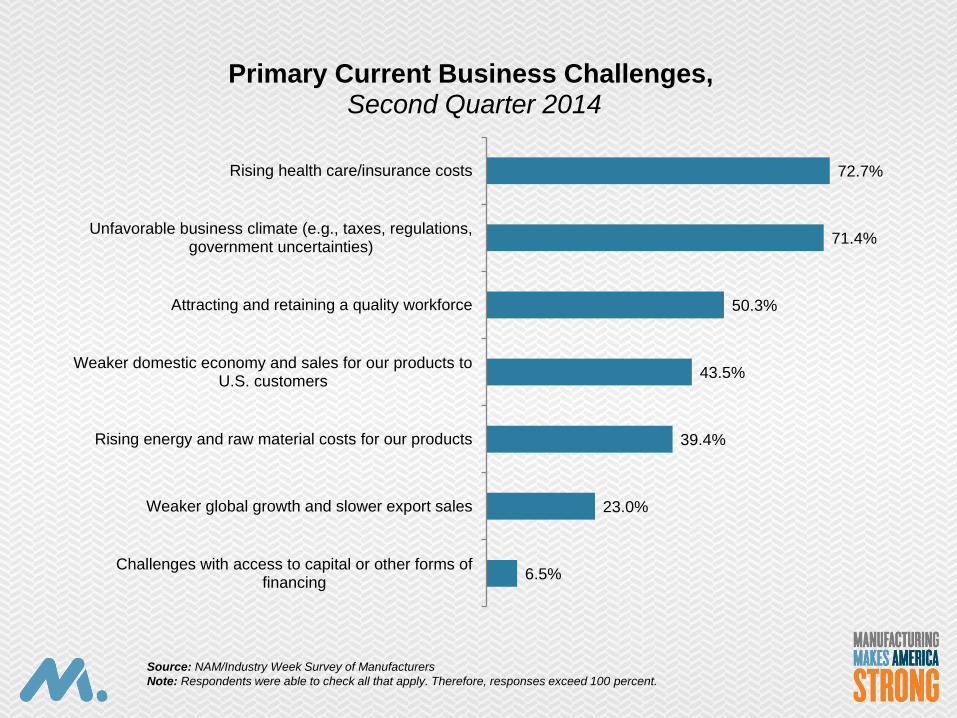

6.5%

23.0%

39.4%

43.5%

50.3%

71.4%

72.7%

Challenges with access to capital or other forms offinancing

Weaker global growth and slower export sales

Rising energy and raw material costs for our products

Weaker domestic economy and sales for our products toU.S. customers

Attracting and retaining a quality workforce

Unfavorable business climate (e.g., taxes, regulations,government uncertainties)

Rising health care/insurance costs

Primary Current Business Challenges, Second Quarter 2014

Source: NAM/Industry Week Survey of Manufacturers

Note: Respondents were able to check all that apply. Therefore, responses exceed 100 percent.

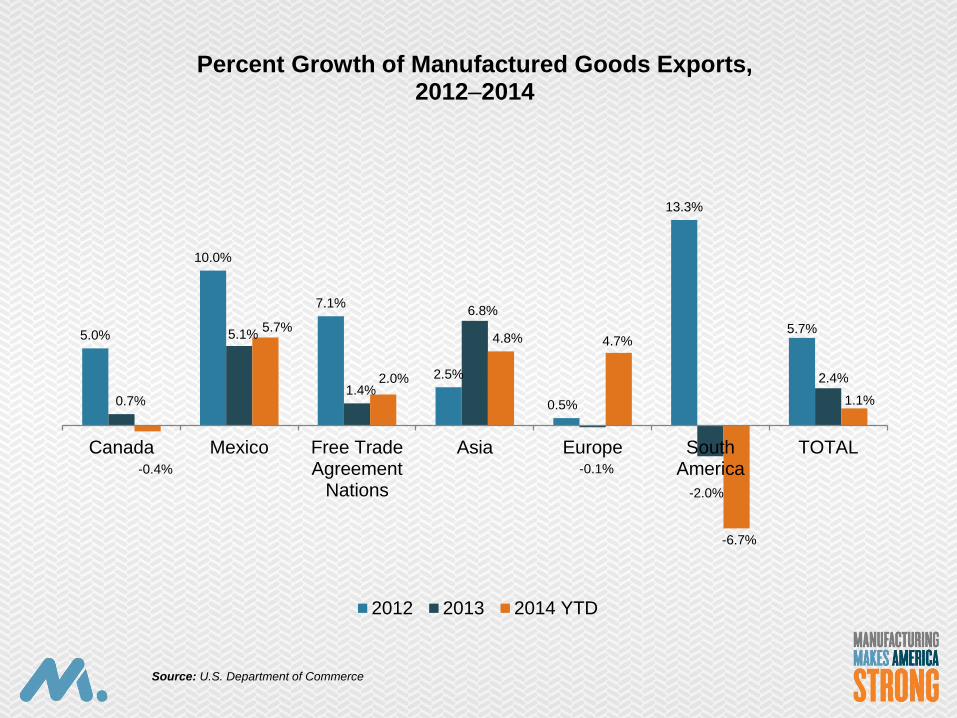

International Economic Update, including Exports

5.0%

10.0%

7.1%

2.5%

0.5%

13.3%

5.7%

0.7%

5.1%

1.4%

6.8%

-0.1%

-2.0%

2.4%

-0.4%

5.7%

2.0%

4.8% 4.7%

-6.7%

1.1%

Canada Mexico Free TradeAgreement

Nations

Asia Europe SouthAmerica

TOTAL

Percent Growth of Manufactured Goods Exports, 2012–2014

2012 2013 2014 YTD

Source: U.S. Department of Commerce

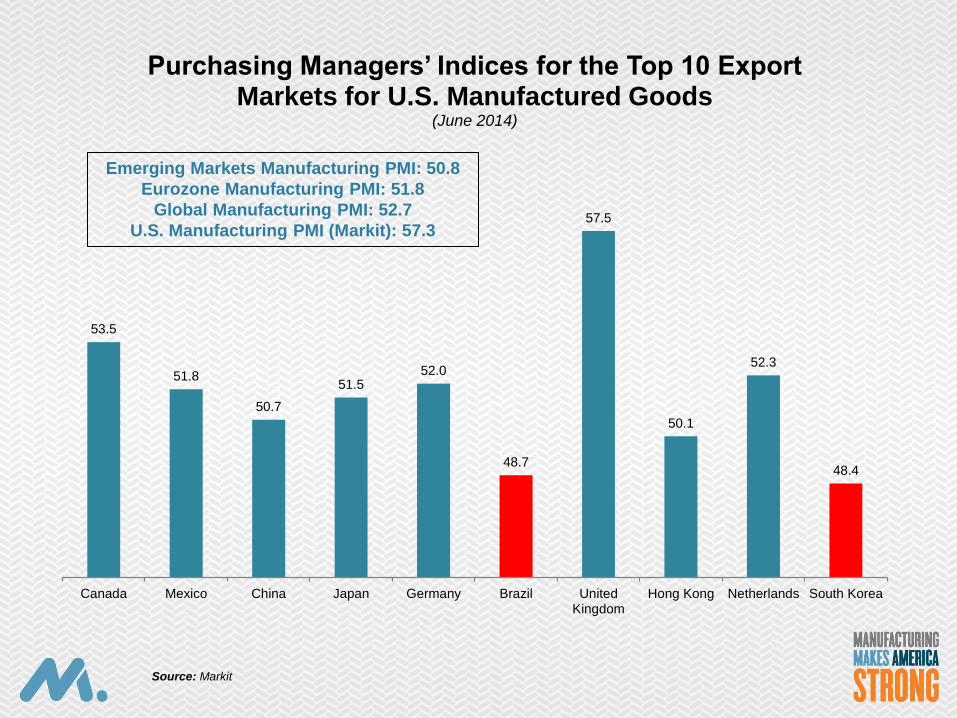

53.5

51.8

50.7

51.5 52.0

48.7

57.5

50.1

52.3

48.4

Canada Mexico China Japan Germany Brazil UnitedKingdom

Hong Kong Netherlands South Korea

Purchasing Managers’ Indices for the Top 10 Export Markets for U.S. Manufactured Goods

(June 2014)

Emerging Markets Manufacturing PMI: 50.8

Eurozone Manufacturing PMI: 51.8

Global Manufacturing PMI: 52.7

U.S. Manufacturing PMI (Markit): 57.3

Source: Markit

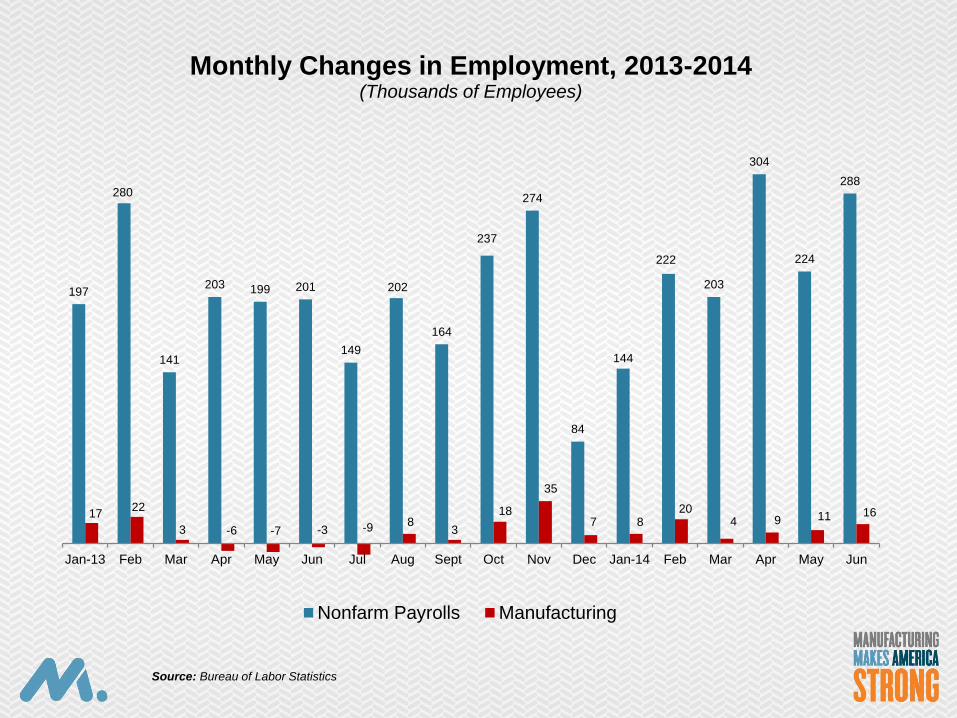

Manufacturing Employment

197

280

141

203 199 201

149

202

164

237

274

84

144

222

203

304

224

288

17 22

3 -6 -7 -3 -9 8 3

18

35

7 8 20

4 9 11 16

Jan-13 Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec Jan-14 Feb Mar Apr May Jun

Monthly Changes in Employment, 2013-2014 (Thousands of Employees)

Nonfarm Payrolls Manufacturing

Source: Bureau of Labor Statistics

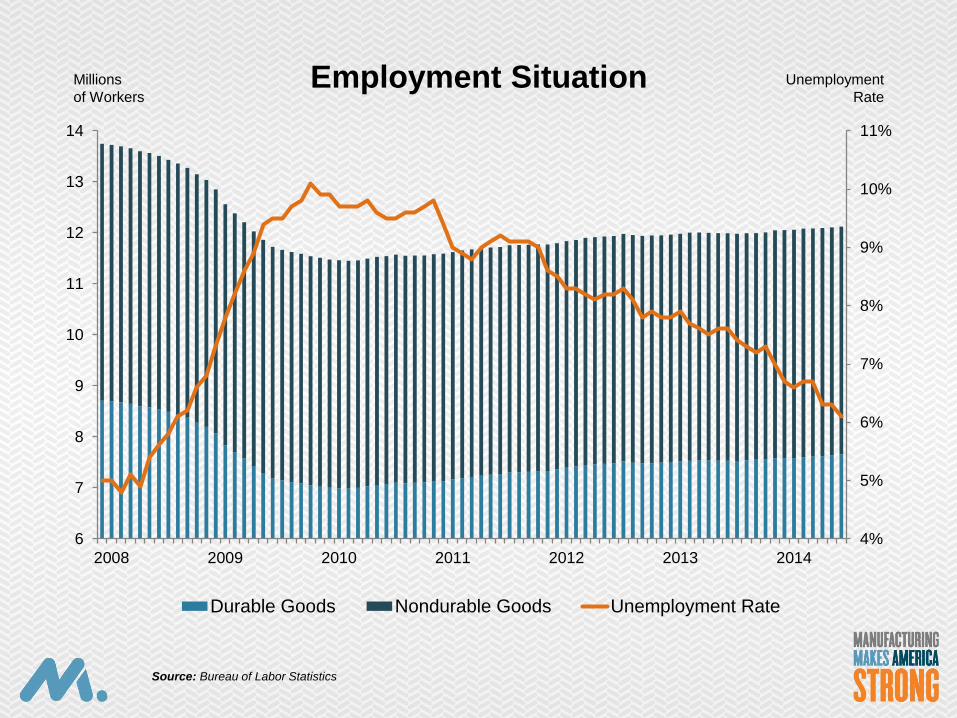

4%

5%

6%

7%

8%

9%

10%

11%

6

7

8

9

10

11

12

13

14

2008 2009 2010 2011 2012 2013 2014

Employment Situation

Durable Goods Nondurable Goods Unemployment Rate

Millions

of Workers

Unemployment

Rate

Source: Bureau of Labor Statistics

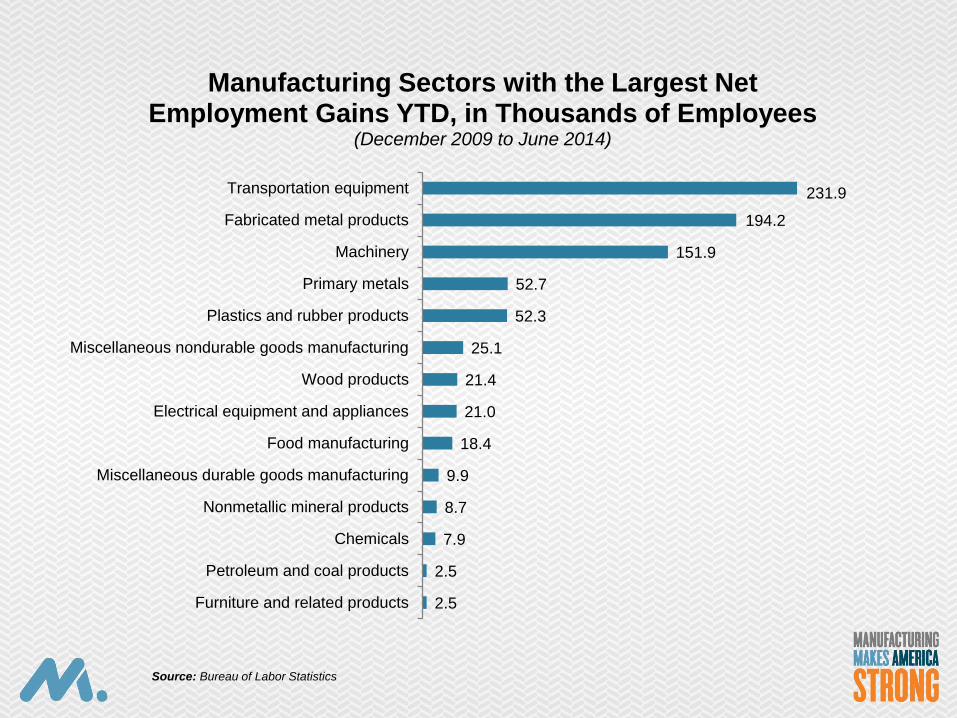

2.5

2.5

7.9

8.7

9.9

18.4

21.0

21.4

25.1

52.3

52.7

151.9

194.2

231.9

Furniture and related products

Petroleum and coal products

Chemicals

Nonmetallic mineral products

Miscellaneous durable goods manufacturing

Food manufacturing

Electrical equipment and appliances

Wood products

Miscellaneous nondurable goods manufacturing

Plastics and rubber products

Primary metals

Machinery

Fabricated metal products

Transportation equipment

Manufacturing Sectors with the Largest Net Employment Gains YTD, in Thousands of Employees

(December 2009 to June 2014)

Source: Bureau of Labor Statistics

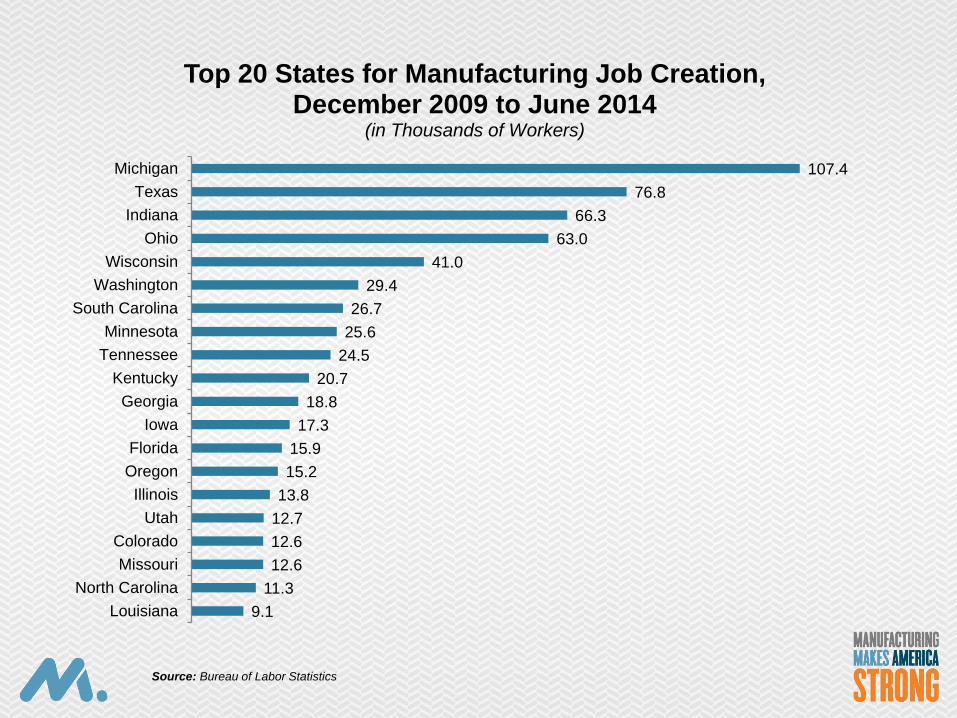

9.1

11.3

12.6

12.6

12.7

13.8

15.2

15.9

17.3

18.8

20.7

24.5

25.6

26.7

29.4

41.0

63.0

66.3

76.8

107.4

Louisiana

North Carolina

Missouri

Colorado

Utah

Illinois

Oregon

Florida

Iowa

Georgia

Kentucky

Tennessee

Minnesota

South Carolina

Washington

Wisconsin

Ohio

Indiana

Texas

Michigan

Top 20 States for Manufacturing Job Creation, December 2009 to June 2014

(in Thousands of Workers)

Source: Bureau of Labor Statistics

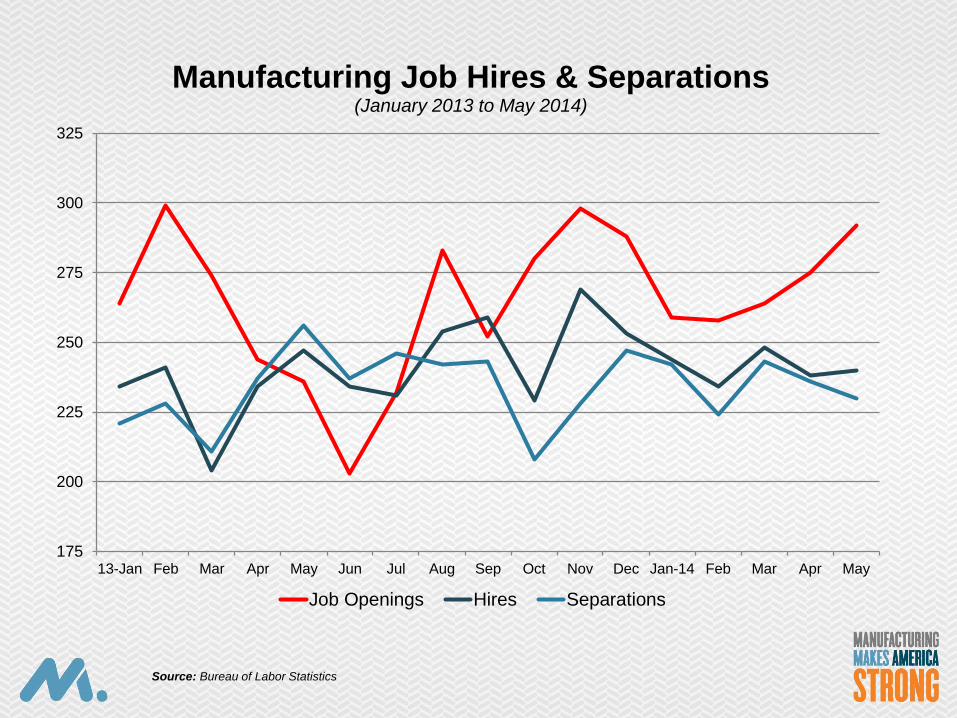

175

200

225

250

275

300

325

13-Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan-14 Feb Mar Apr May

Manufacturing Job Hires & Separations (January 2013 to May 2014)

Job Openings Hires Separations

Source: Bureau of Labor Statistics

Other Topics:

Consumer spending, housing and pricing pressures

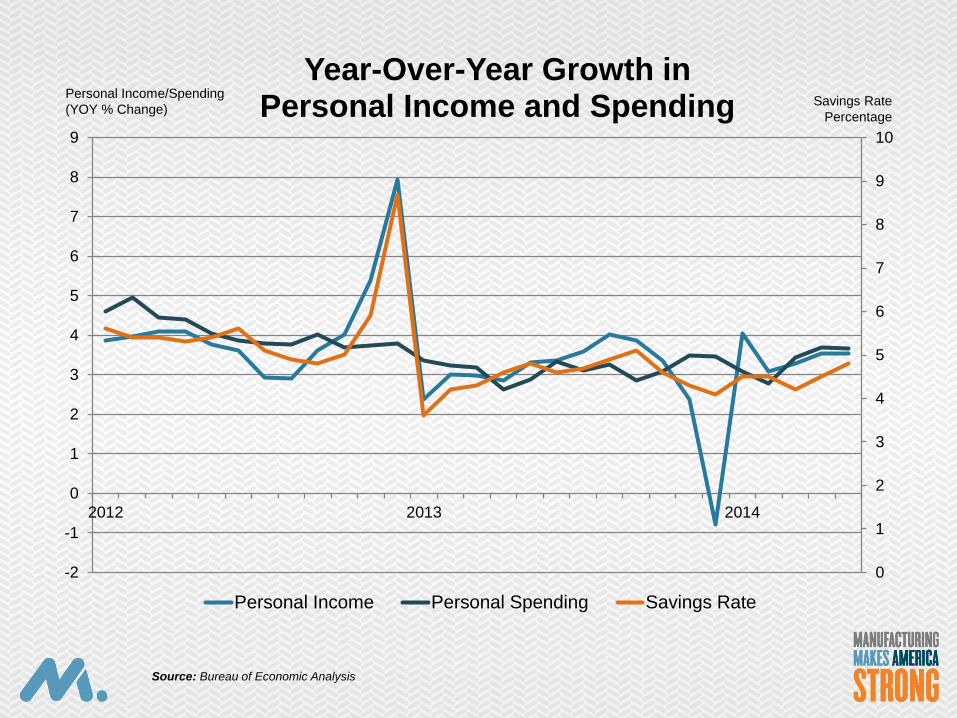

0

1

2

3

4

5

6

7

8

9

10

-2

-1

0

1

2

3

4

5

6

7

8

9

2012 2013 2014

Year-Over-Year Growth in Personal Income and Spending

Personal Income Personal Spending Savings Rate

Personal Income/Spending

(YOY % Change)

Source: Bureau of Economic Analysis

Savings Rate

Percentage

0%

1%

2%

3%

4%

5%

6%

7%

8%

2012 2013 2014

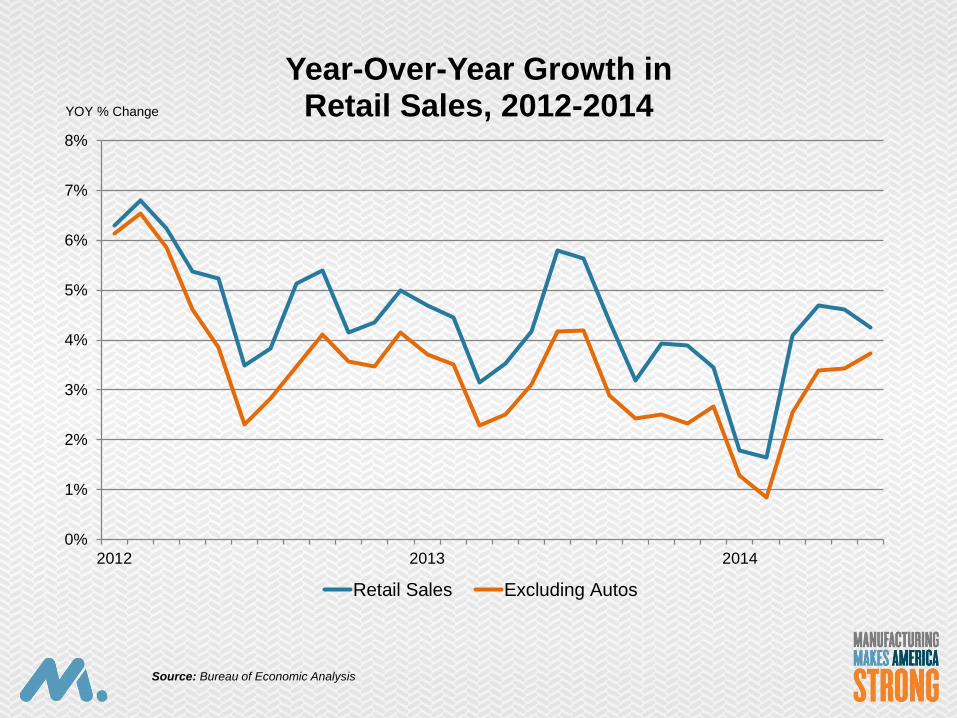

Year-Over-Year Growth in Retail Sales, 2012-2014

Retail Sales Excluding Autos

YOY % Change

Source: Bureau of Economic Analysis

70

75

80

85

90

95

100

105

110

20

30

40

50

60

70

80

90

100

110

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

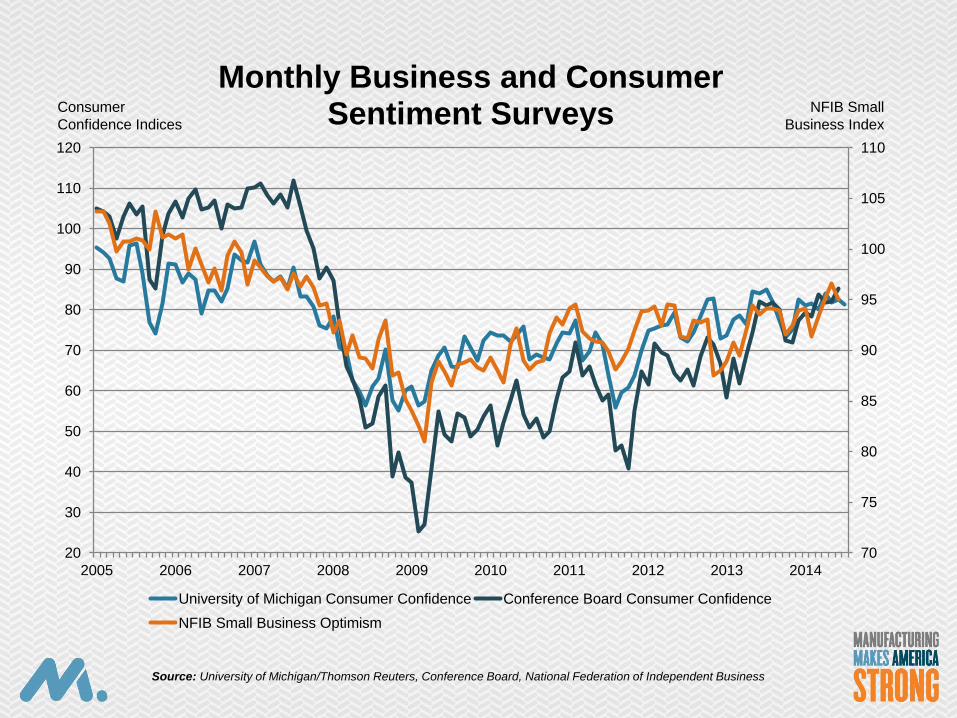

Monthly Business and Consumer Sentiment Surveys

University of Michigan Consumer Confidence Conference Board Consumer Confidence

NFIB Small Business Optimism

Consumer

Confidence Indices

NFIB Small

Business Index

Source: University of Michigan/Thomson Reuters, Conference Board, National Federation of Independent Business

8

10

12

14

16

18

20

22

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

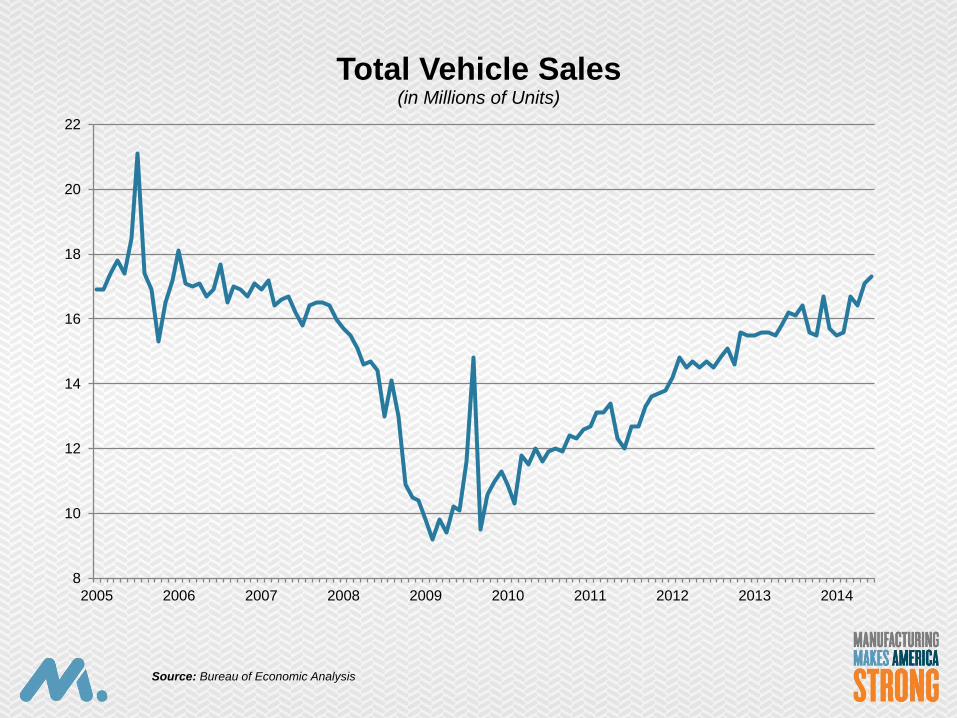

Total Vehicle Sales (in Millions of Units)

Source: Bureau of Economic Analysis

0

10

20

30

40

50

60

70

80

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

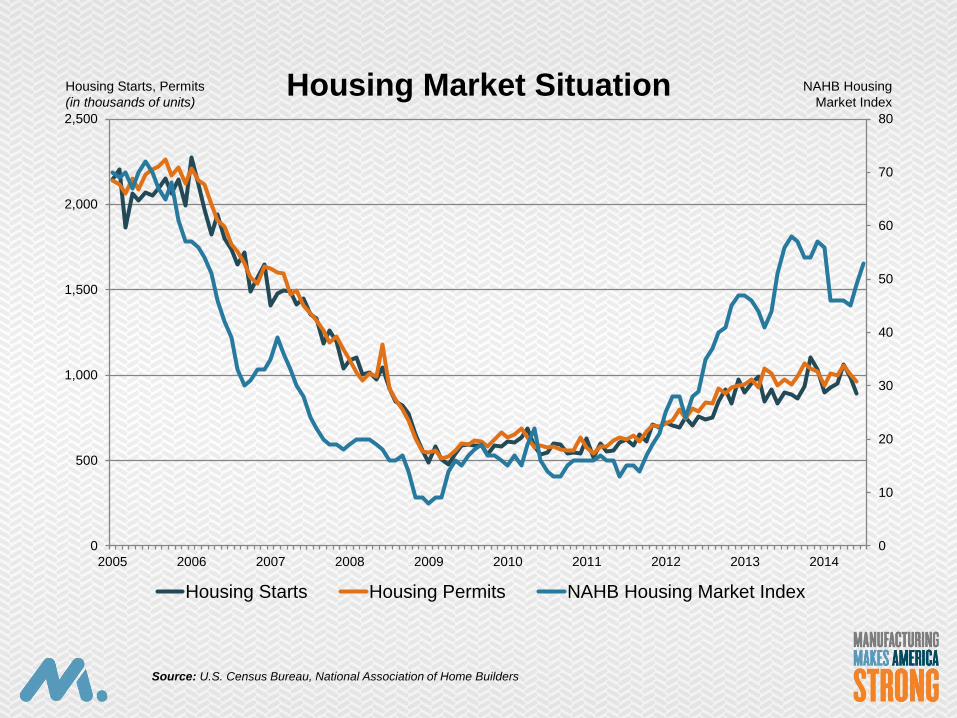

Housing Market Situation

Housing Starts Housing Permits NAHB Housing Market Index

NAHB Housing

Market Index

Housing Starts, Permits

(in thousands of units)

Source: U.S. Census Bureau, National Association of Home Builders

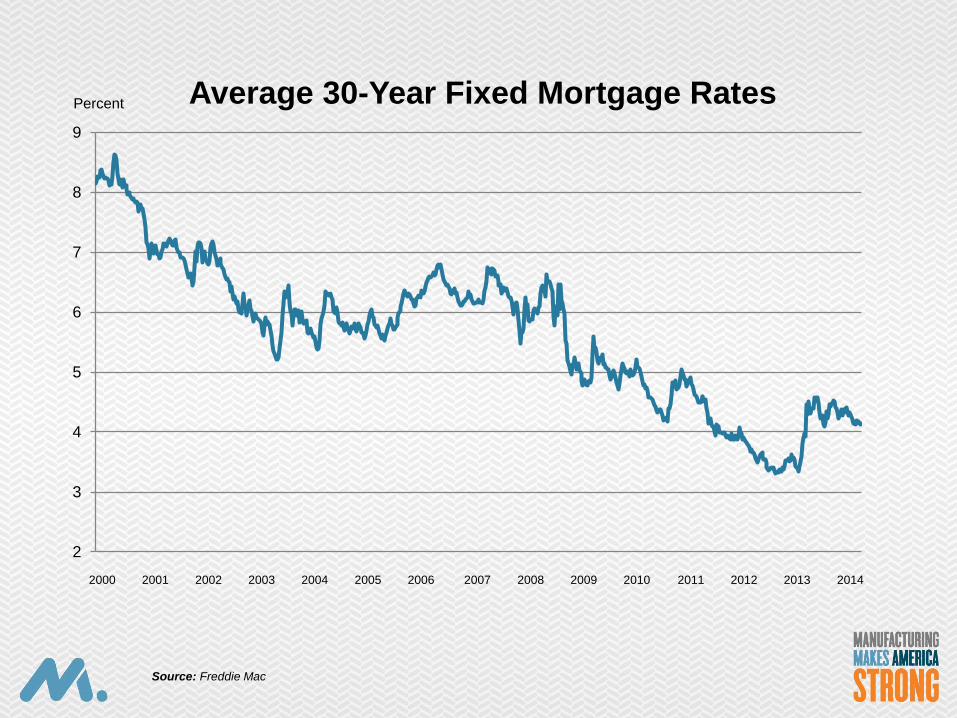

2

3

4

5

6

7

8

9

Average 30-Year Fixed Mortgage Rates

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Percent

Source: Freddie Mac

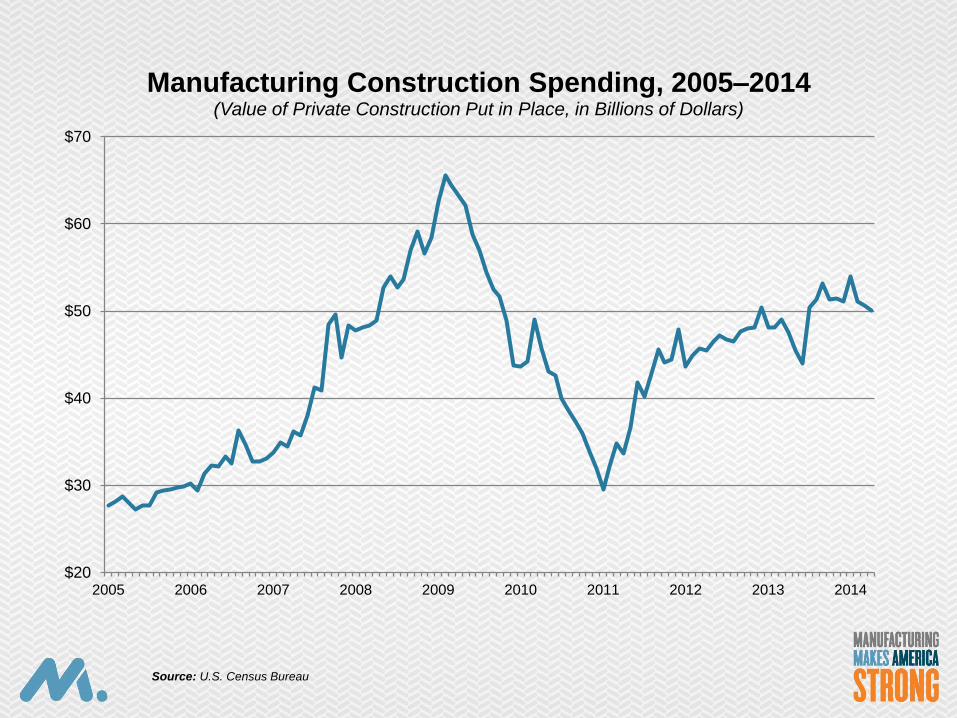

$20

$30

$40

$50

$60

$70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Manufacturing Construction Spending, 2005–2014 (Value of Private Construction Put in Place, in Billions of Dollars)

Source: U.S. Census Bureau

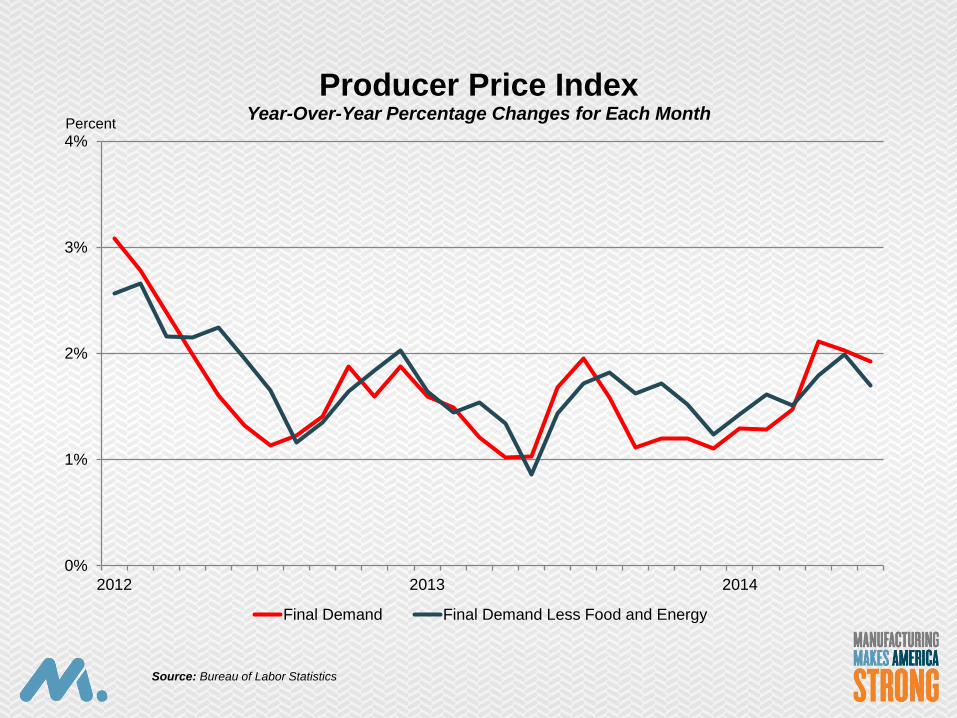

0%

1%

2%

3%

4%

2012 2013 2014

Producer Price Index Year-Over-Year Percentage Changes for Each Month

Final Demand Final Demand Less Food and Energy

Percent

Source: Bureau of Labor Statistics

Increased Investments in U.S. Manufacturing

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

45%

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fixed Direct Investment in Manufacturing, 1997–2013

Manufacturing FDI Percentage of Manufacturing as a Percent of Total FDI

Manufacturing FDI (in Billions of Dollars)

Manufacturing FDI (Percentage of Total FDI from All Industries)

Source: Bureau of Economic Analysis

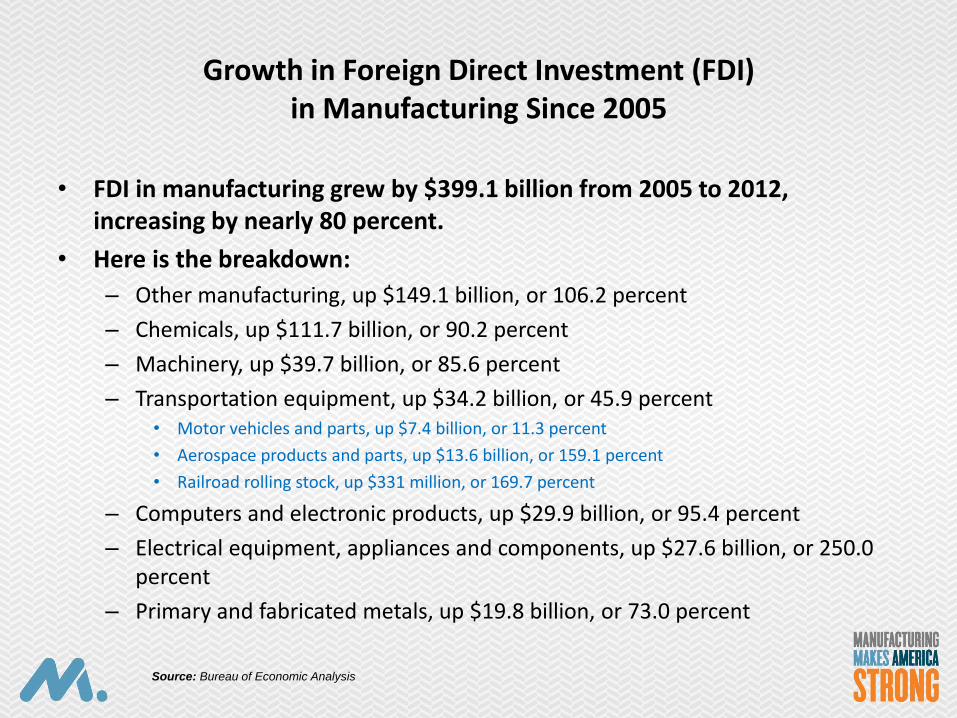

Growth in Foreign Direct Investment (FDI) in Manufacturing Since 2005

• FDI in manufacturing grew by $399.1 billion from 2005 to 2012, increasing by nearly 80 percent.

• Here is the breakdown:

– Other manufacturing, up $149.1 billion, or 106.2 percent

– Chemicals, up $111.7 billion, or 90.2 percent

– Machinery, up $39.7 billion, or 85.6 percent

– Transportation equipment, up $34.2 billion, or 45.9 percent • Motor vehicles and parts, up $7.4 billion, or 11.3 percent

• Aerospace products and parts, up $13.6 billion, or 159.1 percent

• Railroad rolling stock, up $331 million, or 169.7 percent

– Computers and electronic products, up $29.9 billion, or 95.4 percent

– Electrical equipment, appliances and components, up $27.6 billion, or 250.0 percent

– Primary and fabricated metals, up $19.8 billion, or 73.0 percent

Source: Bureau of Economic Analysis

$0

$100

$200

$300

$400

$500

$600

$700

$800

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

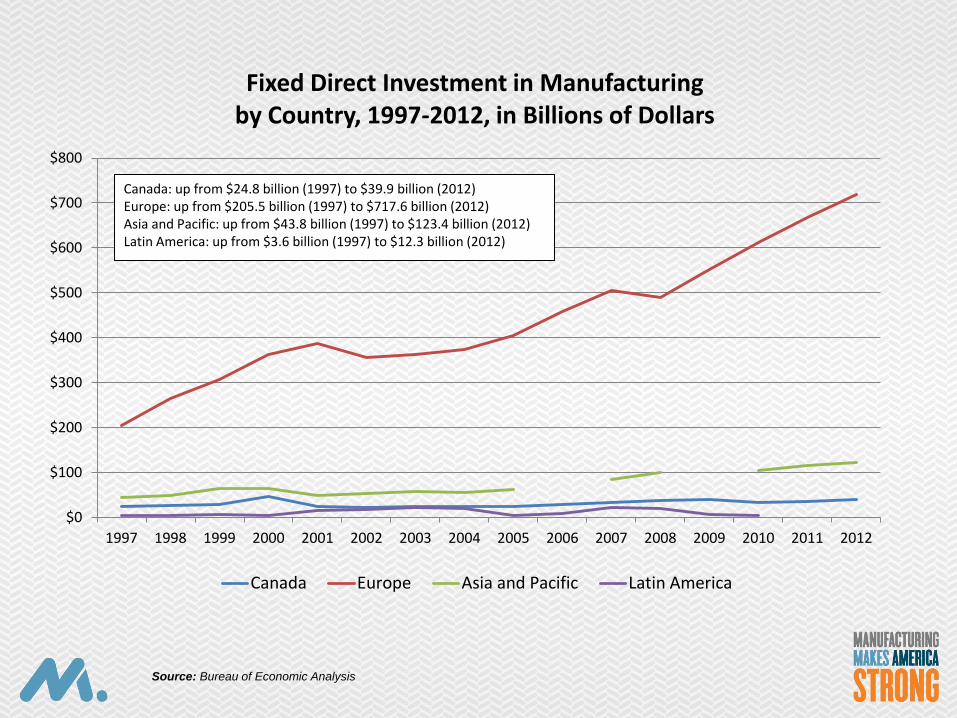

Fixed Direct Investment in Manufacturing by Country, 1997-2012, in Billions of Dollars

Canada Europe Asia and Pacific Latin America

Canada: up from $24.8 billion (1997) to $39.9 billion (2012) Europe: up from $205.5 billion (1997) to $717.6 billion (2012) Asia and Pacific: up from $43.8 billion (1997) to $123.4 billion (2012) Latin America: up from $3.6 billion (1997) to $12.3 billion (2012)

Source: Bureau of Economic Analysis

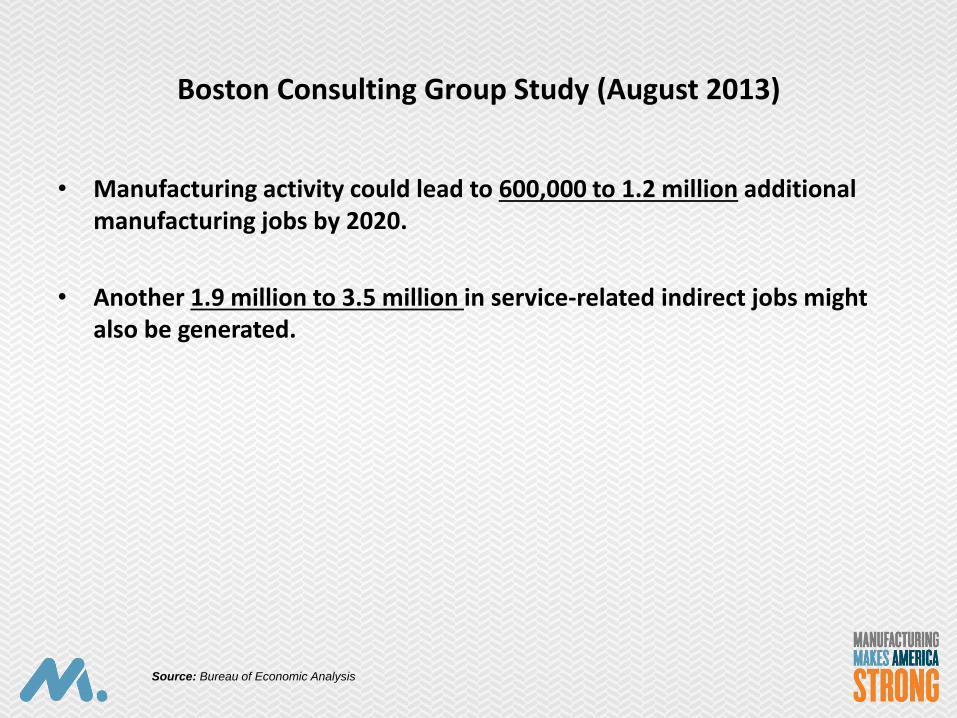

Boston Consulting Group Study (August 2013)

• Manufacturing activity could lead to 600,000 to 1.2 million additional manufacturing jobs by 2020.

• Another 1.9 million to 3.5 million in service-related indirect jobs might also be generated.

Source: Bureau of Economic Analysis

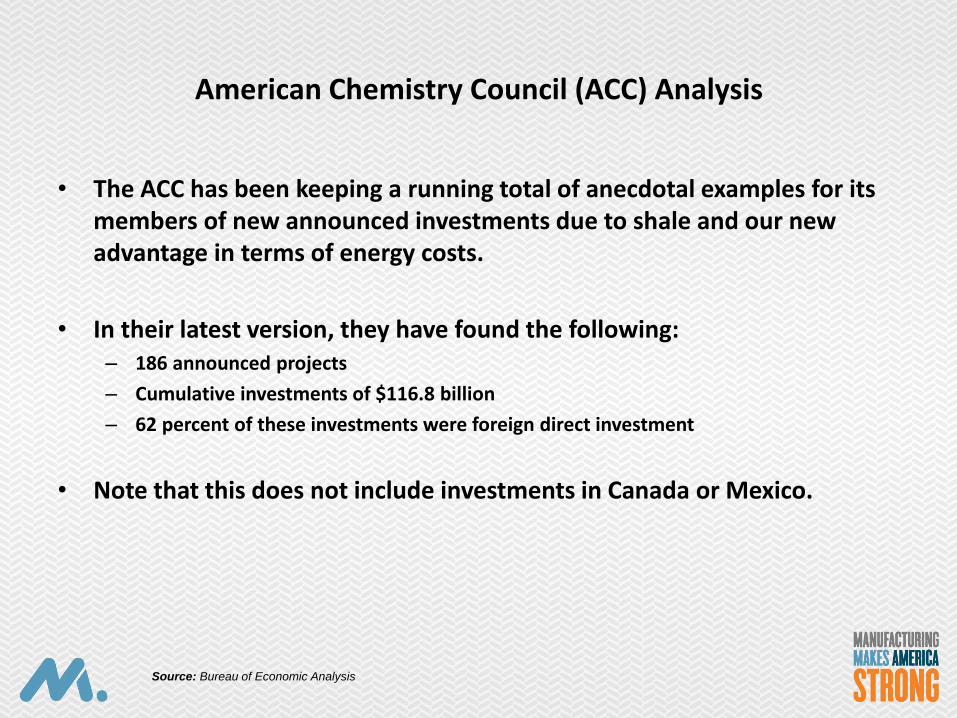

American Chemistry Council (ACC) Analysis

• The ACC has been keeping a running total of anecdotal examples for its members of new announced investments due to shale and our new advantage in terms of energy costs.

• In their latest version, they have found the following: – 186 announced projects

– Cumulative investments of $116.8 billion

– 62 percent of these investments were foreign direct investment

• Note that this does not include investments in Canada or Mexico.

Source: Bureau of Economic Analysis

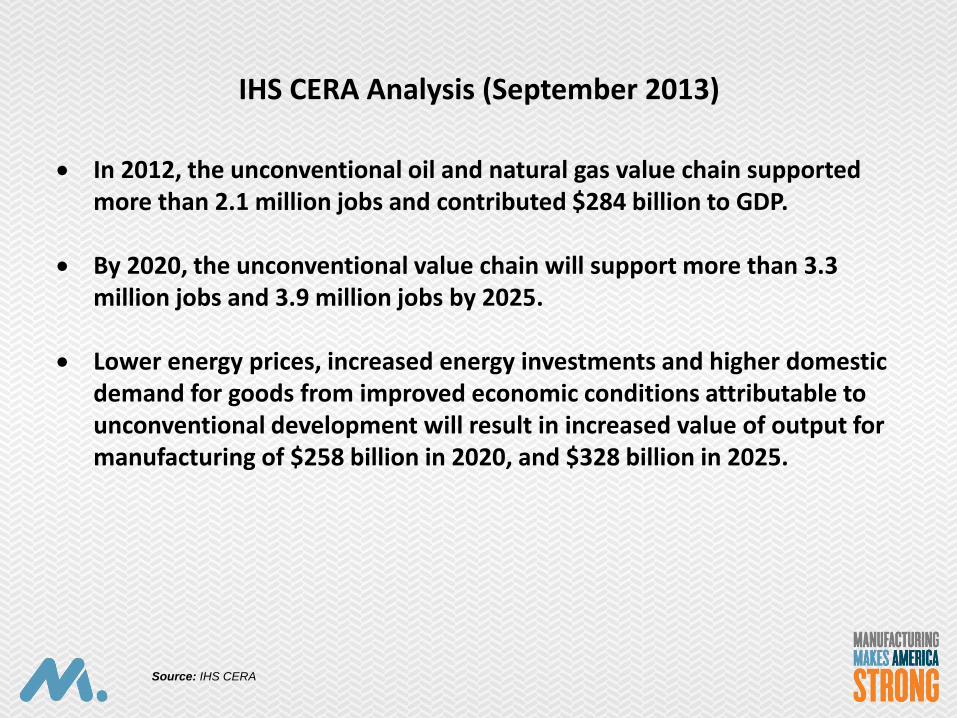

IHS CERA Analysis (September 2013)

In 2012, the unconventional oil and natural gas value chain supported more than 2.1 million jobs and contributed $284 billion to GDP.

By 2020, the unconventional value chain will support more than 3.3 million jobs and 3.9 million jobs by 2025.

Lower energy prices, increased energy investments and higher domestic

demand for goods from improved economic conditions attributable to unconventional development will result in increased value of output for manufacturing of $258 billion in 2020, and $328 billion in 2025.

Source: IHS CERA

100

120

140

160

180

200

220

240

260

280

300

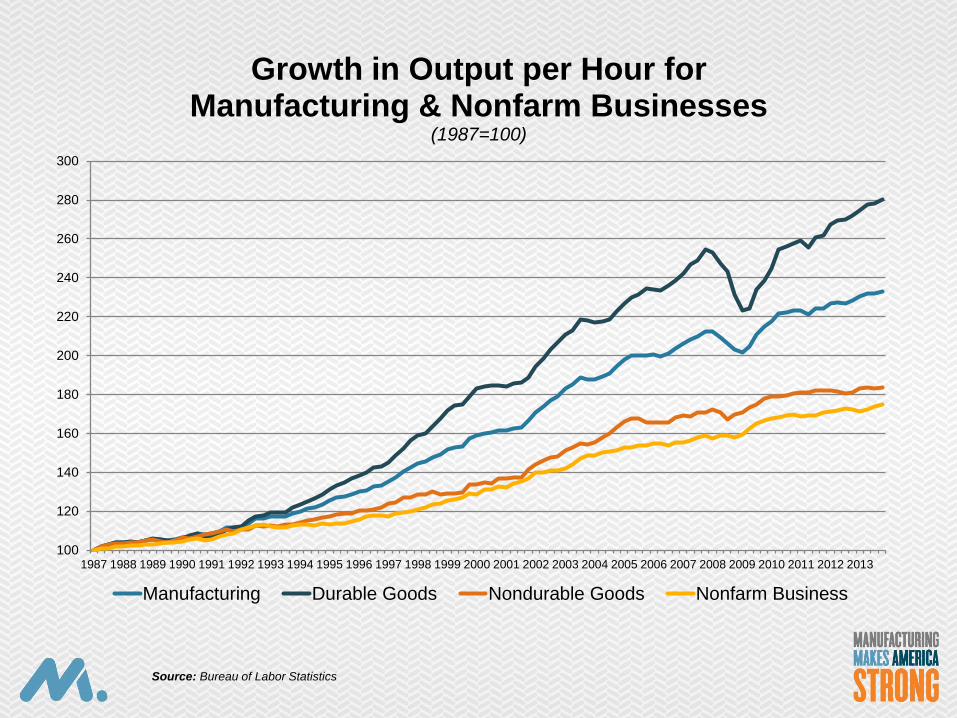

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Growth in Output per Hour for Manufacturing & Nonfarm Businesses

(1987=100)

Manufacturing Durable Goods Nondurable Goods Nonfarm Business

Source: Bureau of Labor Statistics

85

87

89

91

93

95

97

99

101

103

105

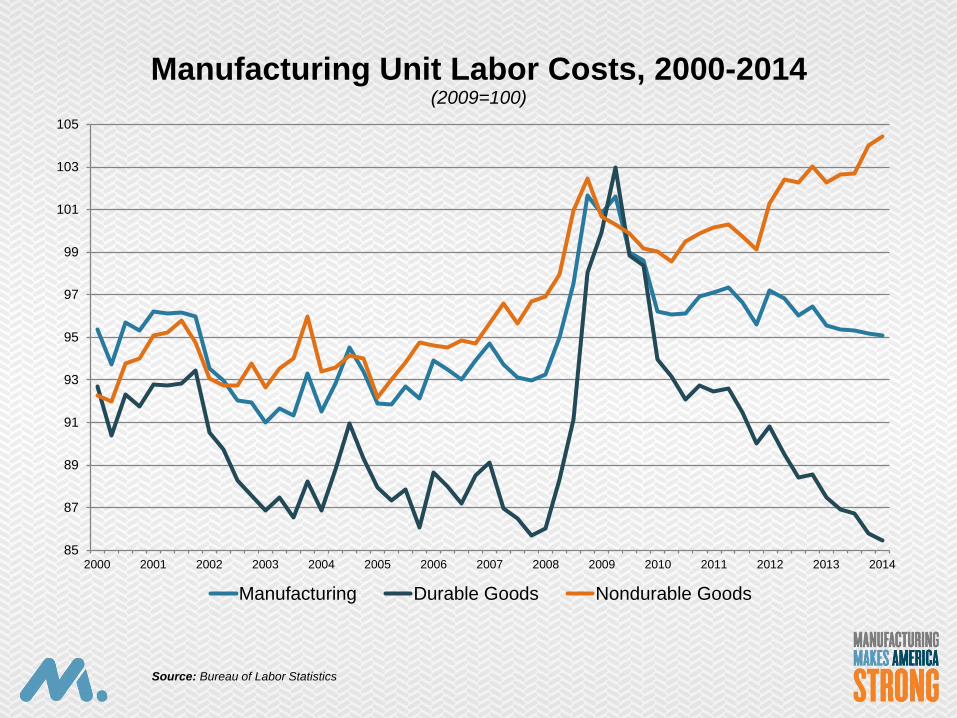

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Manufacturing Unit Labor Costs, 2000-2014 (2009=100)

Manufacturing Durable Goods Nondurable Goods

Source: Bureau of Labor Statistics

Questions?

Dr. Chad Moutray Chief Economist

National Association of Manufacturers

[email protected] (202) 637-3148

@chadmoutray