Embed Size (px)

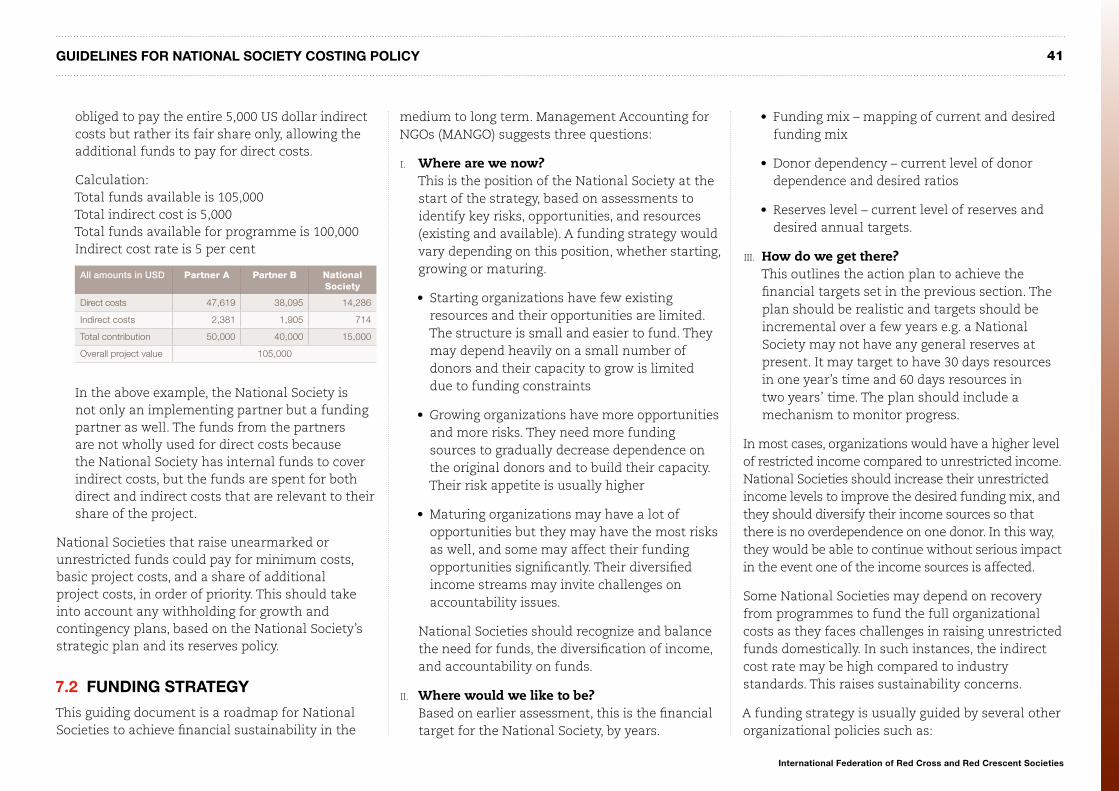

Citation preview

www.ifrc.orgSaving lives, changing minds.

International Federation of Red Cross and Red Crescent Societies

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICYBest practices for project costing and indirect cost recovery procedures

© International Federation of Red Cross and Red Crescent Societies, Geneva, 2016

Any part of this annual report may be cited, copied, translated into other languages or adapted to meet local needs without prior permission from the International Federation of Red Cross and Red Crescent Societies, provided that the source is clearly stated. Requests for commercial reproduction should be directed to the IFRC at [email protected] Guidelines for National Society Costing Policy – August 2016

The International Federation of Red Cross and Red Crescent Societies (IFRC) is the world’s largest volunteer-based humanitarian network. With our 190 member National Red Cross and Red Crescent Societies worldwide, we are in every community reaching 160.7 million people annually through long-term services and development programmes, as well as 110 million people through disaster response and early recovery programmes. We act before, during and after disasters and health emergencies to meet the needs and improve the lives of vulnerable people. We do so with impartiality as to nationality, race, gender, religious beliefs, class and political opinions.

Guided by Strategy 2020 – our collective plan of action to tackle the major humanitarian and development challenges of this decade – we are committed to saving lives and changing minds.

Our strength lies in our volunteer network, our community-based expertise and our independence and neutrality. We work to improve humanitarian standards, as partners in development, and in response to disasters. We persuade decision-makers to act at all times in the interests of vulnerable people. The result: we enable healthy and safe communities, reduce vulnerabilities, strengthen resilience and foster a culture of peace around the world.

Foreword 4

Preface and acknowledgements 5

Executive summary 6

1 Introduction

1.1 Overview, objective and scope 7

1.2 General definitions 7

1.3 Costing policy framework 7

2 Concepts

2.1 Budget architecture 9

2.2 Cost definitions and costing concepts 9

2.3 Costing principle – Full cost recovery 10

2.4 Cost classification 11

3 Methodology

3.1 Cost assignment 14

3.2 Indirect cost recovery 16

3.3 Calculation methods 17

3.4 Cost behaviour 21

3.5 Rates 22

4 Approaches

4.1 Under- and over-recovery 25

4.2 Exceptions 27

4.3 Other considerations 28

5 Influencing factors

5.1 Fair share 30

5.2 Donor cross-subsidization 31

5.3 Value for money 31

5.4 Competitive edge 32

5.5 Multi-layer funding 33

5.6 Cost neutrality 34

6 Risks and responsibility

6.1 Budgeting, policies, and procedures 35

6.2 Management, evaluation, and reporting 36

6.3 Information systems 36

6.4 Accountability 37

6.5 Practicality 38

7 Financial sustainability

7.1 Domestic financial resources 39

7.2 Funding strategy 41

7.3 Reserves 42

Conclusion 45

Bibliography 46

TABLE OF CONTENTS

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

4 > FOREWORD AND ACKNOWLEDGEMENTS

Whenever there is a crisis, we are there. Our ability to respond quickly is part of what makes the Red Cross and Red Crescent so unique and so important. It is rightly a source of pride and is understandably a focus, a preoccupation of National Society leaders and managers.

However, our responsiveness forms only part of our credibility, especially when it comes to our partners and donors. The trust they have in us also comes from our commitment to accountability and transparency. Accountability and transparency are not additional considerations. They are principles that must inform all that we do.

Key to this is how we use funding to cover the costs of providing services to the communities we serve.

This document offers guidance for National Societies to develop and adopt transparent costing policies and cost recovery practices. Effective policies and systems such as these are the foundations of accountability.

These guidelines have been developed in close consultation with National Societies and other experts, and they draw heavily on practices that already exist within our network. They reflect our shared ambition to become the humanitarian partner of choice for all stakeholders.

It is our hope that you will find them useful. We welcome your feedback and hope you can share your successes so that we in turn can capture lessons learnt and share them throughout the network.

Elhadj As Sy Secretary General

FOREWORD

5GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

I am thankful for the contributions of many individuals within the International Red Cross and Red Crescent Movement, particularly the colleagues in National Societies who accompanied me on this journey.

In writing these guidelines over the past four years, I gained invaluable insight into the functioning and running of a National Society. The collaboration with National Societies allowed me to see their perspectives and understand their aspirations. The experience gave me the chance to observe the benefits of full cost recovery, and also recognize the long and often unspoken consequences of under recovering costs.

This document introduces key costing concepts, and describes approaches to develop a costing policy and cost recovery system. It discusses the challenges in fully recovering costs and the implications if the hurdles are not overcome. The chapters could be read independently but those involved in developing costing policies and designing cost recovery systems would benefit reading it right through.

The guidelines could be viewed in three segments:

I. Concepts and methodologies – introduces key terms and principles (technical in nature)

II. Approaches and factors – discusses practices and implications (analytical in nature)

III. Risks, responsibilities, and financial sustainability – explores topics that underpin the subject

On behalf of the International Federation of Red Cross and Red Crescent Societies (IFRC), I would like to thank the National Red Cross and Red Crescent Societies in Africa, Americas, Asia Pacific, Europe, and Middle East North Africa, for participating in the consultation process to develop this guidelines. In addition, I am grateful to the National Societies of Colombia, Ethiopia, Liberia, Myanmar, Nepal, Viet Nam and Philippines for their instrumental role and contribution during the acceptance testing. The guidelines as presented in the next pages, is a result of mutual learning.

I would like to thank colleagues at Norwegian Red Cross for their recommendations. And I extend deepest gratitude to Mr David McConomy from Stephen J.R. Smith School of Business at Queen’s University in Canada, and to Mr Mark Jerome from Asia Pacific’s International Development Assistance Services at KPMG, for their kind editorial inputs.

I am indebted to IFRC colleagues in Geneva, regions, and countries, for their feedback, co-operation, and support during this journey. In particular, I thank Alfred Panico, Jagan Chapagain, John Gwynn, and Umadevi Selvarajah for starting this project. And I thank Andrew Rizk for his advice, and for the vision that led to expanding a regional project to be a global initiative for the benefit of all National Societies.

David Silvaraja, CA (M), CPFA, FCCA Senior Financial Accountant

PREFACE AND ACKNOWLEDGEMENTS

6 > INTRODUCTION GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

National Red Cross and Red Crescent Societies are continuously seeking to remain competitive and relevant in providing humanitarian services with high levels of integrity so that their position as trusted institutions is well recognized and retained, both within the country and internationally. Their capacity to exist, organize, mobilize, perform, and grow is guided by the organization’s strategic vision, is dependent on enabling constitutions and well governed policies, and is further strengthened by systems and procedures.

In order to achieve organizational aims and objectives, National Societies gather, harness, and employ resources. The financial measure, based on industry and national standards, enables National Societies to monitor their performance and maintain strong accountability to their stakeholders. One of the key attributes of a strong financial system is a costing policy that describes an organization’s approach to cost – how cost is defined, funded, and accounted for. This is an essential foundation that would empower National Societies to exist and carry out humanitarian programmes and services for the most vulnerable communities in the foreseeable future.

Any organization must be able to fully cover the costs of its structure, which includes the physical infrastructure and its invaluable human resources. Financial sustainability is a growing concern for

many National Societies who struggle to fully cover their organizational costs and the costs associated with programme and service delivery, risking deficits and discontinuity of programmes, among other consequences. There are two main reasons: Firstly, there are many relevant costs that are not recovered from the correct funding sources, and they slowly deplete the organization’s unrestricted funds and reserves. Secondly, there are costs that could be avoided but are not managed well, and these absorb scarce resources and become unaffordable over time. The process of writing a costing policy allows the National Society to look deeper and understand their organization better, in order to make informed decisions that have a significant impact on its financial resources in the long term.

Following requests from many National Societies, these guidelines for National Society Costing Policy have been developed, using widely accepted standards and practices, to provide a simple and clear guidance to National Societies who wish to prepare or revise their costing policy. It also provides guidance to design and implement an indirect cost recovery system, and makes crucial links to an organization’s funding strategy and accountability. Framed as guidelines, this document harmonizes terminologies, encourages understanding, and prompts National Societies to consider areas that are pertinent in the development of a costing policy and indirect cost recovery system.

This guidance document builds on previous initiatives that the IFRC secretariat has undertaken on the subject of full cost recovery and project costing, complements the 8NS core cost project that focuses on minimum structure and costs, and is based on consultation with a number of National Societies in Africa, Americas, Asia Pacific, Europe, and Middle East and North Africa (MENA) regions. The principles and methods are drawn from a wide catalogue of resources from within and outside the not-for-profit sector - with an intended emphasis on the International Red Cross and Red Crescent Movement to make this document more relevant – and have been tested with National Societies in the various regions.

The development of costing policies and indirect cost recovery systems are not isolated but part of wider efforts that National Societies undertake to ensure financial health, and to contribute towards sustainable programme and service delivery. This aptly refers to the National Society Development Framework 2013, where leaders are encouraged to reflect on approaches that are essential to improve processes deemed critical for their long-term health, image, and collective reputation.

These guidelines offer the tools necessary to embark on a journey to understand costs, to appreciate full cost recovery, and to experience the manifold benefits of effective cost management.

EXECUTIVE SUMMARY

7GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

1.1 OVERVIEW, OBJECTIVE AND SCOPE

Overview

An organization’s costing system should help in achieving its strategic objectives, taking into account its nature, culture, cost structure, operating model, and environment. This tailored approach makes a costing system unique to an organization and makes it less appropriate for one model to be used by all.

Objective

This document is prepared for all National Red Cross and Red Crescent Societies, to provide simple and clear guidance on how to prepare costing policies and indirect cost recovery procedures by using widely accepted standards. National Societies have a need to:

• Fully recover the costs associated with managing donor-funded programmes

• Apply consistent indirect cost recovery rates based on widely accepted standards

• Provide relevant and transparent information to support cost recovery methods and rates.

These costing policy guidelines follow up on previous work such as the Value Chain Study of

2007 and Cost Comparison Study of 2008. The two relevant conclusions of the studies were1:

“The secretariat and National Societies should develop full cost recovery systems, so that total project costs can be determined and fully understood. Such systems would make it possible to evaluate total project costs compared to outputs and outcomes. In addition they would enable financial transparency with stakeholders including donors…”

“A common accounting framework should be developed including common terminology, policies, practices and a chart of accounts to underpin comparison, discussion and learning about costs and financial operation in general.”

Scope

The guidelines provide basic definitions, classification, and assignment methods. They describe concepts and principles that are important for costing and cost recovery processes, and consider factors that influence full cost recovery.

This document aims to bridge the gap in understanding between donors and fund recipients by harmonizing terminologies and approaches within the Movement. It provides guidance on how to calculate indirect cost rates, highlights key considerations for management, and outlines the types of financial information that are integral to cost recovery system management.

1.2 GENERAL DEFINITIONS

The following terms are used in this document and listed here to guide understanding:

I. Partner or partners – represents donors and are used interchangeably

II. Back donor – represents a partner’s donor

III. Recipient or fund recipient – represents a National Society

IV. Organization – used as a general term and as reference to a National Society

V. IFRC – International Federation of Red Cross and Red Crescent Societies

Where a specific example illustrates the relationship between a donor National Society and recipient National Society, the terms partner National Society and operating National Society are used.

1.3 COSTING POLICY FRAMEWORK

Costing policy is important for any organization as it determines how costs are treated and funded. There are many factors that influence a costing policy

7

1. Extracted from studies commissioned by IFRC, Review of overheads along the Federation value chain and review of Secretariat overhead recovery mechanism, 2007; Secretariat and National Societies – A cost comparison study, 2008

1 INTRODUCTION

8 > INTRODUCTION GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

and these are a primary consideration for National Societies who wish to prepare such a policy. The key factors are summarized below:

I. Objective and plan A good costing policy contributes to a National Society’s growth and its sustainability. An organization’s sustainability extends beyond its financial scope and depends on many drivers including – but not limited to – fundraising and resource mobilization. The objective of a costing policy is to foster financial sustainability, where the costs of an organization are fully recovered and will remain recoverable in the foreseeable future.

The financial plan and budget should always follow the operational plan that is informed and led by the organization’s strategic plan. If a multi-year plan is available, this helps to assess the financial sustainability over that period, and to appreciate the inherent ups and downs where a National Society may generate a surplus in one year and a deficit in another.

II. Scope and time horizon The costing policy should not be limited to one particular project or operation, or bound to one particular year. This is based on the assumption that the National Society will remain in business or operation for the foreseeable future. The policy should present a model relevant for a number of years instead of a short-term solution that needs annual revision, which is often impractical and cumbersome. Stakeholders will appreciate the certainty, consistency, and predictability associated with a longer-term financial sustainability plan.

The topic of costing policy or indirect cost recovery often appears when there is a large-scale operation, where there is a concern whether the existing structure can cope with the increase in volume and size of programmes, and whether an expansion, if done, can be effectively and fully funded. The costing policy should be prepared in view, but not in limitation, of such operations based on historical patterns. The idea is to plan and measure financial sustainability by costing for programmes and services holistically.

III. Market The domestic and international markets should be considered when setting costing policies. Donors will likely support policies that are deemed fair and reasonable when they are communicated clearly and transparently. Although a donor’s preference should not dictate a recipient’s costing policy, it is an essential criterion for a costing policy to be effective. How donors treat costs would have an influence on their acceptance of how recipients treat costs.

IV. Capping Due to the nature of programmes and services, and the unpredictability of emergency operations, there is a possibility of significant recoveries when a large-scale project is implemented, exceeding the estimates used in calculation exercises. There is usually a concern on the part of donors, and pressure on the part of operating National Societies, on how over-recoveries will be treated and how capping, if applied, would be managed.

“How donors treat costs would have an influence on their

acceptance of how recipients treat costs.”

9GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

9

2.1 BUDGET ARCHITECTURE

Costing policies and cost recovery procedures should begin with the budget architecture.

Budget architecture is how the organization views its costs and draws its budgets. Most National Societies have at least two budgets – one for the programmes, and another for organizational costs. The organization budget is also commonly referred to as an infrastructure budget, or core budget. Clearer budgets allow easier matching of income and expenditures.

As the budget architecture is imperative to costing policy and indirect cost recovery systems, it would be useful to categorize budgets into three main categories:

1. Organization budget (unrestricted) – this includes regular costs, including governance

2. Programme budget (restricted) – this includes other costs, programmes and services

3. Capital budget – this includes all non-current assets (some build this into no. 1).

It would be ideal if all budgets were funded at the start of the financial year. However, for an organization to continue in existence, it would be most important to fully fund the organization budget.

There is a financial relationship between the programme (restricted) budget and the organization (unrestricted) budget of an entity. With indirect cost recovery, the portion of unrestricted budget that is not funded by an organization’s own resources is funded by way of recovery from programmes and services.

2.2 COST DEFINITIONS AND COSTING CONCEPTS

Cost – a financial measure of resources consumed for a project implementation or service delivery.

“It should be noted that the costs which should be considered in many types of management decisions are not the recorded costs, but rather the expected future costs which will differ among the possible alternative course of actions2” .

Cost object is an item or group of items whose costs need to be measured. Cost centres (such as projects and departments) are examples of cost objects. Establishing cost objects is important to report cost information to stakeholders. Hence, reporting requirements help to determine cost objects, and this in turn helps to design a cost information system. The quality of the cost information depends on the cost objects, the methods of classifying costs, and the methods of assigning costs.

Management objectives contribute to decide the cost objects of an organization e.g. a National

Society may wish to have information by programmes, projects, activity, geographical regions or a combination of these. Some organizations may require additional cost objects such as departments and functions (e.g. support services). In creating cost objects, the management should also understand how the information would be used for decision-making, how frequently the information is needed, and the cost of collecting and providing the information.

The deeper the cost object in the organization level, the more difficult it will be to attribute costs to it, e.g. it may be easier to measure costs by departments or projects than to measure them by activity or location of activities. The number of cost objects influences the complexity of the cost information system e.g. if the cost information is derived from the financial system, the chart of accounts need to be designed to produce the different cost information that the management requires. The more complex the design, the less practical and useful it would be. Cost objects should be realistic, practical, and based on non-negotiable requirements.

Cost drivers are factors that cause the costs to increase or decrease. They may be determined by

2 CONCEPTS

2. Extracted from Perspectives on Cost Accounting for Governments by IFAC Public Sector Committee

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

10 > CONCEPTS

observation or analysis of the activities. There may be more than one cost driver for a particular cost but the best one should be chosen that fits with the costing objectives of the organization e.g. office rent and utilities are usually distributed by floor space but, where this cannot be easily calculated or does not reflect actual consumption, then the cost could also be distributed by workstation or headcount. Some costs may be common to several cost objects. Cost drivers help to calculate the distribution or sharing formula for the various cost objects. In the example of office rent and utilities, floor space (cost driver) can be used to charge the share of costs to the different departments (cost objects).

Fixed costs are costs that will not vary with the level of activity whereas variable costs are costs that increase or decrease based on activity level.

Programme costs are direct operational costs and are often tangible e.g. procurement and mobilization of relief items, cash disbursements, construction etc. They are always direct in nature but could be either fixed or variable.

Programme support costs are overheads or running costs necessary for the implementation of activities and would not be incurred otherwise. They can be direct or indirect, and fixed or variable.

“Overheads are costs which are increasingly removed in time and space from the beneficiary, which cover more than one project and which are perceived as being prone to increase for reasons not directly connected to the organization’s aims and objectives. Definition is difficult because it requires an arbitrary line to be drawn at some point in the continuum of costs between the beneficiary

and the head office and is significantly dependent on the viewpoint of this drawing and it is consequently open to debate3”.

Overheads, support cost, core costs, and indirect costs mean the same thing to many organizations. It is important to know what overheads encompass, when this term is used. These costs cannot be traced to a single project or service but must be allocated to the project or service using an allocation method that is seen to be fair by all.

Direct costs are costs that can be specifically identified and that can be easily traced to a particular project or service4. They could be fixed or variable in nature e.g. rent of vehicles for the project team (same amount every month) is fixed in nature whereas the cost of running the vehicles (fuel, toll, and parking) is variable in nature.

Indirect costs are costs that cannot be specifically traced to a project or service and are usually common or joint costs. They could be fixed or variable in nature e.g. salary cost of finance or logistics team supporting various projects (same amount every month) is fixed in nature whereas the cost of running those offices (e.g. electricity) is variable in nature. Where variable, they are usually programme-inspired costs.

Full costs describes the process of measuring the total costs of an operating unit or function (both direct and indirect) and assigning them to all of the organization’s project or services. The definition of full costs differs between countries, which imply inclusion or exclusion of certain costs. Full costs of a project or service should include both a component

of direct costs, and its relevant and appropriate share of indirect costs.

2.3 COSTING PRINCIPLE – Full cost recovery

Full cost recovery means recovering or funding the full costs associated with project implementation or service delivery. It includes all project or service costs, either direct or indirect, and an element of more general costs associated with sustaining the organization itself. Full cost recovery systems help to determine and fully understand projects costs.

In addition to costs directly associated with project or service, costs will also be generated in other parts of the organization, e.g. adequate finance, human resources, management and information technology systems are integral components of any project or service5. The first step towards full cost recovery is being able to define what constitutes full costs. This is based on an organization’s ability to understand the cost structures, and to distinguish direct and indirect costs.

Why full cost recovery?

The true cost of delivering a project or service is not fully met if only new or additional resources employed are considered, e.g. if a National Society has one programme funded by three donors and a second programme by a new donor is introduced, the second programme’s full costs are not only

3. Extracted from Review of Overheads along the Federation value chain and Review of Secretariat Overhead recovery mechanism, 2007

4. Definition as per IFRC’s Costing policy

5. Extracted from IFRC’s Costing principles

11GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

the additional costs of the project or service to the organization, but includes a share of the indirect costs which were previously shared by the one programme and its three donors.

Indirect costs must be recovered to ensure the financial stability of an organization, and its continued growth and development. Difficulties in funding indirect costs leads to underinvestment in6:

I. Management and leadership

II. Internal and external infrastructure

III. Strategic development and governance.

When costs are fully recovered, National Societies not only survive and develop, but they are also able to increase the quality and effectiveness of their programmes and services as there are funds available to invest in adequate resources such as staff, equipment, and other infrastructure. The institutes behind “the overhead myth”, in their open letter to donors, concluded based on various studies in the United States, that organizations who build infrastructure and capacities are more likely to succeed and that underinvestment compromises quality and sustainability 7.

Full cost recovery also helps an organization to understand the true, total, and fair costs of its work, which is essential for effective financial management and strategic planning. Further, understanding the full cost enables managers to have more informed dialogues with stakeholders.

Partners also benefit when their fund recipients adopt full cost recovery. They will have:

I. A complete and accurate reflection of the cost of projects and services

II. Reasonable assurance that there is no cross-subsidization

III. Stronger trust in the fund recipient built on increased transparency

IV. Efficient delivery of projects as costs will be better controlled

V. Long term programmes as the fund recipient is able to continue operations.

In the UK National Audit Office’s 2005 report Working with the Third Sector, three types of financial relationships were said to exist between public sector bodies and third sector organizations8. This relationship can also be identified between National Societies and their partners. They are:

I. Shopping relationship: a funder designs a project or a service and contracts a service provider

II. Giving relationship: a funder provides funds for a specific project or the overall objective

III. Investing relationship: a funder provides funds for development or capacity building initiative.

Full cost recovery reflects a move from the traditional shopping relationship towards a more giving and investing relationship, whereby partners are indirectly contributing towards the fund recipient’s sustainability, and are appreciative of the full costs of programming.

The commitment to full cost recovery may pose some challenges for an organization or its funders,

as the principle works on the assumption that costs are reasonable and fundable. If actual indirect costs were substantial, not within the accepted norm in the industry, and not competitive to market conditions, it would be difficult to implement full cost recovery.

Full costs should be the basis for budgeting so that all costs are completely and accurately captured. Measuring full costs is an effective method for cost control and cost reduction, as the overall organizational costs are scrutinized against available income levels.

2.4 COST CLASSIFICATION

Apart from identifying cost objects (what are the cost groups), National Societies should decide the methods to classify costs based on objectives (how to group the costs). There are many ways to classify costs, and the classification method is crucial to systematically allocate or assign costs to programmes and services. The not-for-profit industry commonly classifies costs by:

I. Function – programme costs versus programme support costs

II. Variability – fixed cost versus variable cost

III. Traceability – direct cost versus indirect cost.

6. Based on Full cost recovery by ACEVO, KPMG and New Philanthropy Capital

7. Based on The Overhead Myth by BBB Wise giving Alliance, Guidestar, and Charity Navigator.

8. Third sector is used to mean voluntary sector, community sector, not for profit or non-governmental organizations.

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

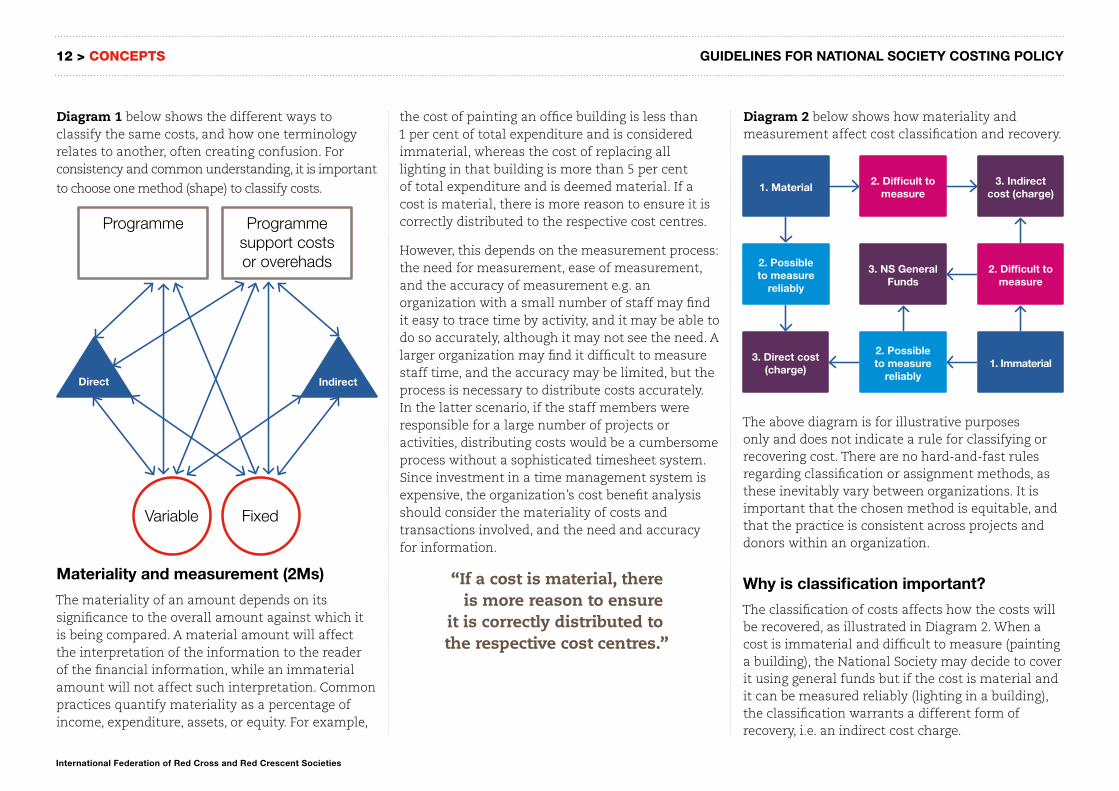

Diagram 1 below shows the different ways to classify the same costs, and how one terminology relates to another, often creating confusion. For consistency and common understanding, it is important

to choose one method (shape) to classify costs.

Materiality and measurement (2Ms)

The materiality of an amount depends on its significance to the overall amount against which it is being compared. A material amount will affect the interpretation of the information to the reader of the financial information, while an immaterial amount will not affect such interpretation. Common practices quantify materiality as a percentage of income, expenditure, assets, or equity. For example,

the cost of painting an office building is less than 1 per cent of total expenditure and is considered immaterial, whereas the cost of replacing all lighting in that building is more than 5 per cent of total expenditure and is deemed material. If a cost is material, there is more reason to ensure it is correctly distributed to the respective cost centres.

However, this depends on the measurement process: the need for measurement, ease of measurement, and the accuracy of measurement e.g. an organization with a small number of staff may find it easy to trace time by activity, and it may be able to do so accurately, although it may not see the need. A larger organization may find it difficult to measure staff time, and the accuracy may be limited, but the process is necessary to distribute costs accurately. In the latter scenario, if the staff members were responsible for a large number of projects or activities, distributing costs would be a cumbersome process without a sophisticated timesheet system. Since investment in a time management system is expensive, the organization’s cost benefit analysis should consider the materiality of costs and transactions involved, and the need and accuracy for information.

“If a cost is material, there is more reason to ensure

it is correctly distributed to the respective cost centres.”

Diagram 2 below shows how materiality and measurement affect cost classification and recovery.

The above diagram is for illustrative purposes only and does not indicate a rule for classifying or recovering cost. There are no hard-and-fast rules regarding classification or assignment methods, as these inevitably vary between organizations. It is important that the chosen method is equitable, and that the practice is consistent across projects and donors within an organization.

Why is classification important?

The classification of costs affects how the costs will be recovered, as illustrated in Diagram 2. When a cost is immaterial and difficult to measure (painting a building), the National Society may decide to cover it using general funds but if the cost is material and it can be measured reliably (lighting in a building), the classification warrants a different form of recovery, i.e. an indirect cost charge.

12 > CONCEPTS

Programme

Variable

IndirectDirect

Fixed

Programme support costs or overehads

1. Material

2. Possible to measure

reliably

3. Direct cost (charge)

3. Indirect cost (charge)

2. Difficult to measure

1. Immaterial

2. Difficult to measure

3. NS General Funds

2. Possible to measure

reliably

13GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

As the type of costs does not automatically determine cost classification, an analysis of each cost group is needed to distinguish between direct and indirect costs.

Example – finance staff costs

a) Direct cost: finance staff is dedicated to one project and the cost is directly charged to the project.

b) Direct cost (shared cost): finance staff is involved in a few projects and the share of cost can be reliably measured, so the cost is directly charged to the respective projects.

c) Indirect cost (shared cost): finance staff service is available for all projects, but the time spent cannot be accurately measured by projects or the cost of such measurement outweighs the benefits (immaterial cost) – the cost is shared to all projects via an indirect cost charge.

If an organization classifies direct costs as indirect costs and does not build this into the programme budget, it loses the opportunity to use restricted income to cover the cost. If indirect costs are incorrectly classified as direct costs, this reduces the credibility of the financial information, and it may raise donor concerns. In both cases, if the amounts were significant, the disproportionate ratios would affect the interpretation of financial information. Indirect cost classified as direct cost usually does not go unnoticed, but direct cost classified as indirect cost is often overlooked although this has equally huge financial implications.

Unrestricted income that is used to pay for direct costs is more expensive if it is generated from indirect cost recovery e.g. it takes 100 US dollars to generate recovery income of 5 US dollars when a 5 per cent recovery rate is used, making the unrestricted income value 20 times more than the restricted income. In addition, unrestricted income is more difficult to obtain and highly flexible to use, further escalating its value and justifying the need to use it more prudently.

Accurate classification of costs allows National Societies to better manage their financial resources so that restricted income is not underused and unrestricted income is not overused, and vice versa.

“Indirect cost classified as direct cost usually does not

go unnoticed, but direct cost classified as indirect cost is

often overlooked although this has equally huge financial

implications.”

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

14 > METHODOLOGY

3.1 COST ASSIGNMENT

Cost assignment is the method used to link costs to appropriate cost objects. Cost assignment is dependent on the choice of the cost object and the choice of cost classification e.g. if an organization monitors costs by departments and classifies them as fixed or variable, its method to assign cost would differ from another organization that monitors costs by projects and classifies them as either direct or indirect. In the latter case, costs would be assigned by way of a direct or indirect cost charge to the projects.

Cost classification and cost assignment often falls under the responsibility of the finance department, although the effectiveness of the costing system is dependent on various functions within the organization. Since the individuals in these functions vary in their understanding on how costs are incurred and should be assigned, they should jointly share the responsibility to choose appropriate cost classifications and cost assignment methods. This will ensure that the costing system developed and used by finance is understood and supported by all relevant parties.

Once chosen, the classification and assignment method should be used consistently for a period of time to allow useful comparison, and to avoid misleading users of financial information. The

market or industry standard may help to select suitable classification and assignment methods. Direct charge and cost allocation are two methods and they are described below.

I. Direct charge

Direct charge is the most equitable method as costs are identified, traced to output, and charged directly to the relevant cost object(s). Direct charge works when cost can be measured reliably and attributed to a particular project.

Examples: First scenario: Procurement and transportation of water and sanitation equipment. The cost can be easily traced by activities and directly charged to projects.

Second scenario: Staff members are dedicated to a particular project and a vehicle is assigned to a particular department. The full cost of each resource is directly charged to the relevant cost object.

Where cost is not unique to one particular cost object, it needs to be spread among the relevant cost objects in the most accurate manner possible. The important principle is cause and effect – the cost should be traced to the cost object (e.g. project) that caused it to occur.

Examples: First scenario: Water and sanitation equipment and non-food items are shipped together. The cost of the shipment can be split between two projects based on volume such as cubic metre.

Second scenario: A programme officer supports five projects, and the salary cost is split across the five projects based on time as a suitable cost driver, derived from timesheet records.

Third scenario: A vehicle is shared by three projects and the cost, which includes rent, fuel, and per diem, is charged to the projects based on actual usage, derived from vehicle log books.

The following criteria should be met for costs to be included under a direct charge method:

I. Costs are necessary for the implementation of the projects (non-avoidable cost)

II. The benefits are limited to the concerned projects only

III. Costs meet the cause and effect principle (project that necessitated the expenditure)

IV. Costs can be traced to the projects and reliably measured.

3 METHODOLOGY

15GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

Direct charge is the most transparent mechanism, as it fosters accountability and supports a value for money framework. The method is simple: easy to understand, explain, and apply.

Some organizations set rules to determine the materiality of costs before a cost assignment method is selected. This guides them to assess materiality objectively, and discourages them from spending too many resources on measuring immaterial costs, where the cost of measurement exceeds the benefit e.g. an organization may use a 10 per cent rule for staff costs, as this is the level of salary and benefit that it considers material, and which can be reliably tracked and allocated through its payroll system. If the staff spends more than 10 per cent of total time (per annum) on a project other than that originally assigned, the relevant cost should be charged out to the concerned project.

II. Cost allocation

Cost allocation method is the second preferred method of charging costs to projects. Costs that are remote and independent from projects (indirect in nature) are charged to the cost objects in a systematic manner. These costs are necessary for the running of the project but they may also be incurred in the absence of projects. Different methods are available to calculate the share for each project, taking into account incoming and outgoing projects.

Examples: First scenario: office building costs are common to all the functions and departments on the premises. The costs could be allocated based on

the physical floor space occupied by each unit, or allocated by the headcount or number of workstations. The choice depends on the division of space and considers which method is more reflective of actual consumption.

Second scenario: warehouse rental and truck hire in a relief operation may be shared by a number of donors in a project, or a number of projects in an organization. The costs may be aptly allocated by the value or volume of goods stored and transported. During an emergency operation, the mobilization costs associated with relief items and equipment (including airfreight, shipping, taxes, loading, unloading, storage, and transportation) can be significant and incurred at various locations and by different partners. Driven by urgency, it is often easier and more economical to contract and pay collectively. The challenge would be to accurately split and recover such costs.

Third scenario: the organization’s administration department provides services to all the projects. It is not possible to measure and trace the cost of the department’s services to each project, so the costs are allocated to all projects by a fixed amount each month, shared based on headcount as the cost driver.

The following criteria should be met for the costs to be included under a cost allocation method:

I. Costs are necessary for the implementation of the projects

II. Costs are remote and independent from the projects

III. The resource is available to all projects irrespective of whether they are consumed

IV. Costs cannot be accurately measured and traced to the projects.

The cost allocation method could be criticized mainly for its lack of equitability, e.g. a particular project manager or donor may feel that they are charged for a service that was not used, or they may feel that the charge is too high for that particular service. If viewed purely from the point of actual consumption, it is difficult to justify whether the charge is too little, enough, or too much.

In regards to staff costs, in the absence of a time recording system, the line manager may be responsible for verifying how much time staff spent on the projects in order to arrive at a cost-sharing formula, which would then be applied for the duration of the project. However, if the staff does not spend the same amount of time on the projects each month, then the amount charged to the projects should also be different. However, this depends on whether the fluctuations are material and can be measured reliably. Unless the cost difference between the methods is significant, and the cost of managing a more complex system is justified, a one-formula method should be used for the period of the project or for the duration of the financial year.

The group of costs recovered using a cost-sharing formula should be easily distinguishable from a group of costs that is charged directly to the projects, so that the costs are not perceived as double-charged. This information could be made available

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

16 > METHODOLOGY

and shared with projects to increase clarity and promote transparency.

The purpose of cost allocation is not to trace every dollar to actual consumption but to assign costs as fairly as possible, using systematic calculation in a consistent manner. One of the methods of indirect cost allocation is an indirect cost recovery system.

3.2 INDIRECT COST RECOVERY

Indirect costs are those incurred for common or joint objectives, which cannot be specifically identified with a project or service (IFRC). Indirect costs can be further distinguished between those that are fixed in nature and those that are variable. Indirect cost recovery is a method by which indirect costs are recovered from programmes or services.

Indirect cost charge is an amount or percentage that is applied on programme (restricted) expenditure in order to recover the indirect costs. Indirect cost charge should be calculated in a systematic way so that it represents a fair share for each project. Fair share is relative and highly depends on the National Society’s ability to assure fair share, and the partners’ acceptance of that fair share9. Below are suggested steps to implement an indirect cost recovery system:

I. Review – the National Society should gather and review the below information, in order to analyse the cost structure, and to make a financial projection (the list below is a guide):

• Financial statements (detailed income and expenditure statement) for the previous two or three years

• Management accounts – for additional details to be used along with financial statements

• Programme and organization budgets (restricted/unrestricted) for the most present year

• Organizational chart depicting minimum structure and the associated costs per year

• Income sources, levels and trends, and the extent it funds the organizational costs

The purpose of the review is to establish a trend that will help to make a financial projection for the following year(s). If primary data is not available, the required information may need to be extracted from a number of secondary sources. The amount of historical data required is dependent on the quality of the information. Sometimes, it might be necessary to go back four or five years in order to establish a trend that is not influenced by an exceptionally large ad hoc project. This would help to visualize the minimum structure and to avoid overestimating costs in the projection. All assumptions and limitations used in the projection should be documented and referenced, as this will guide future review and revision processes.

II. Calculate – the financial projection should be prepared for the following financial period based on the above analysis, adjusted for exceptional increase or decrease, in order to reflect the level of programme and structure in a normal given year, e.g. emergency projects that drive up costs in certain periods should be removed from the projection, unless the costs are expected

to incur for a number of following years. The financial projection should also include costs that are essential for an organization to run its business in a normal condition even if such costs are not presently incurred, provided they would likely incur in the following year e.g. an organization may not have adequate office space or staff at present, but it intends to expand its infrastructure and human resources in the following year, and the foreseen additional costs should be factored into the projection.

Based on a simple method (described in the next section), calculate the indirect cost ratio using available data, and test the rate for accuracy and reasonableness. A significantly lower or higher than market rate may suggest a calculation error. Although it is tempting to compare the rate to other National Societies, comparison with like-natured organizations in the country is essential, to reflect the operating environment and local market conditions. Sometimes, the rate imposes additional questions or informs a management decision to manage and control costs, and to right-size the organizational structure.

III. Prepare – the National Society should assess its financial systems, policies, and procedures, and make necessary modifications to ensure they support the new recovery system. This includes development of a costing policy and an indirect cost recovery procedure that is approved by its governing board or senior management. As needed, the financial software and processes

9. ‘Fair share’ concept is elaborated in Chapter 5

17GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

should also include new accounting entries, codes, and templates to enable the National Society to effectively monitor and manage the recovery system. This may require additional customisation or minor tweaks to the financial software.

IV. Communicate – the National Society should communicate the costing policy and relevant information to the existing partners, both in-country and externally. This can be effectively done via partnership meeting platforms where there is room for dialogue. In lieu of a formal meeting, electronic circulation with room for feedback is a practical method. The effective date for the implementation should be mutually agreed to facilitate transition.

V. Amend – Upon mutual agreement, partners and the National Society should revise project agreements and budgets, to include the indirect costs share and to remove corresponding direct budget line items e.g. finance department cost will no longer be budgeted under project directly if the cost is recoverable through an indirect cost allocation rate. It might be challenging to incorporate the new system in an on-going project due to funding constraints and back donor restrictions. In such circumstances, the National Society may continue the project under the existing conditions and apply the new rate only to future projects with the same donor.

VI. Apply – With effect from the date of the policy and amended project agreement, the National Society should apply the indirect cost recovery rate consistently for all projects and partners

– whether Movement or external, domestic or international, emergency or development projects. This is an extremely important step to ensure the system is fair.

VII. Measure – A periodic review (annual or biannual) should be undertaken to measure the effectiveness of the system, and to manage significant under- or over-recoveries. This may not dictate an immediate adjustment but provides internal assurance that the full costs of programmes and services are being recovered. This process also provides assurance to stakeholders who might be concerned about recoverability (risk of deficit) and accountability (risk of excessive surplus).

Some partners may need to consult their headquarters and back donors before accepting a newly introduced indirect cost rate. In principle, the National Society is not seeking an approval, but merely informing the partners of its decision to introduce the indirect cost recovery system. It is done in a consultative manner because it changes existing agreements and practices.

3.3 CALCULATION METHOD

The foremost step in calculating indirect cost rate is to distinguish between direct costs and indirect costs. This may not be a straightforward exercise as organizations differ in their definition and classification of costs, and in the terminologies they use to communicate cost information – what is indirect to one organization may be direct to another; and within an organization, a cost may be indirect in one period and direct in another.

The financial statements and management accounts offer primary insight into the budget and cost structure of an organization. The type of financial information available and the ease of retrieval can make the calculation process either simple or tedious. Some information may need to be analysed and adjusted for accuracy before use.

The simple calculation method below is only one way of calculating the indirect cost recovery rate. It describes the underlying principles but does not indicate a fixed rule for calculation. The method can also be used to review a rate. The objective is to have a ratio of indirect costs over direct costs, based on the organization’s estimated budget or forecast for the following two to three years.

3.3.1 Calculation steps

I. Obtain the financial information listed in section 3.2. Financial statements, preferably audited, should be analysed alongside management accounts, to have a clear reflection of organization costs and programme expenditure. Some organizations may have this information in a consolidated format in the financial statements, whereas some may have bifurcated statements. Multi-year information would help to analyse trend, and to project realistic forecasts. The current period’s year-to-date financial statements would strengthen the analysis and forecasts.

Programme and organization budgets (restricted and unrestricted) for the subsequent years are useful, as the indirect cost rate would be applied prospectively. In the absence of such information

– e.g. due to budgeting cycle – the current year budget and performance, along with results

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

from prior years’ trend analysis, may be used to estimate the following year’s budgets. It might be that the organization budget or unrestricted expenditure is wholly indirect but this is not always the case.

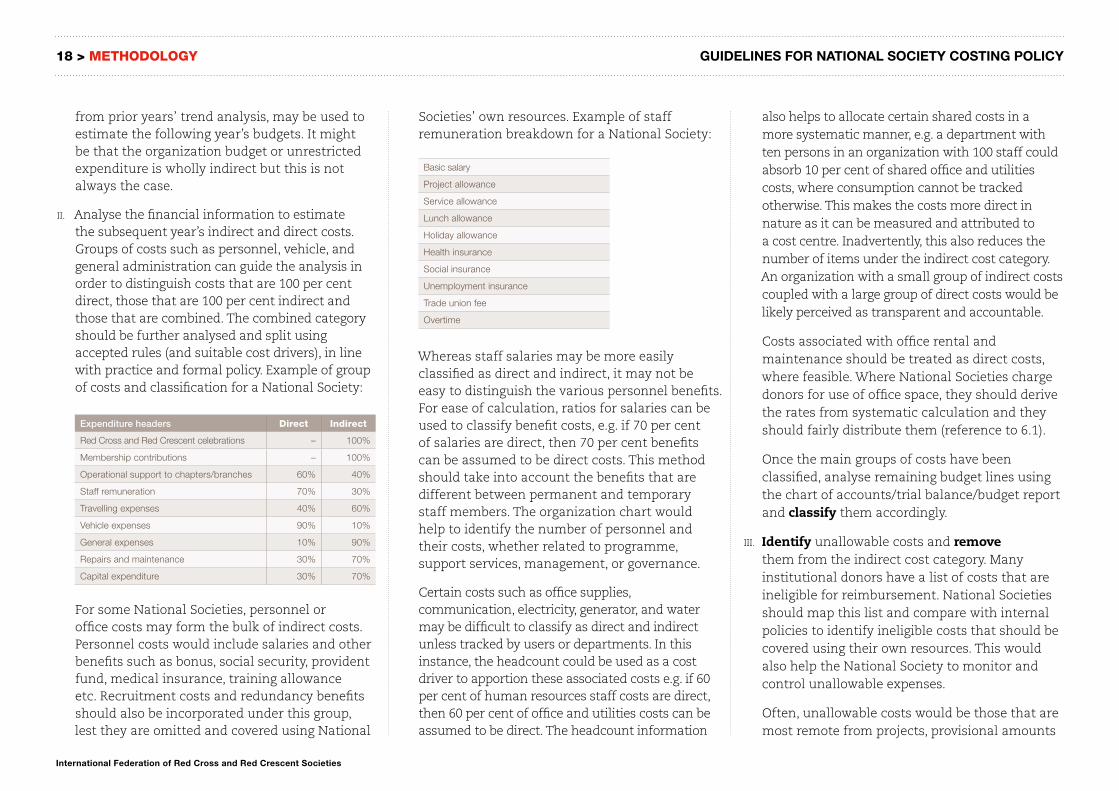

II. Analyse the financial information to estimate the subsequent year’s indirect and direct costs. Groups of costs such as personnel, vehicle, and general administration can guide the analysis in order to distinguish costs that are 100 per cent direct, those that are 100 per cent indirect and those that are combined. The combined category should be further analysed and split using accepted rules (and suitable cost drivers), in line with practice and formal policy. Example of group of costs and classification for a National Society:

Expenditure headers Direct Indirect

Red Cross and Red Crescent celebrations – 100%

Membership contributions – 100%

Operational support to chapters/branches 60% 40%

Staff remuneration 70% 30%

Travelling expenses 40% 60%

Vehicle expenses 90% 10%

General expenses 10% 90%

Repairs and maintenance 30% 70%

Capital expenditure 30% 70%

For some National Societies, personnel or office costs may form the bulk of indirect costs. Personnel costs would include salaries and other benefits such as bonus, social security, provident fund, medical insurance, training allowance etc. Recruitment costs and redundancy benefits should also be incorporated under this group, lest they are omitted and covered using National

Societies’ own resources. Example of staff remuneration breakdown for a National Society:

Basic salary

Project allowance

Service allowance

Lunch allowance

Holiday allowance

Health insurance

Social insurance

Unemployment insurance

Trade union fee

Overtime

Whereas staff salaries may be more easily classified as direct and indirect, it may not be easy to distinguish the various personnel benefits. For ease of calculation, ratios for salaries can be used to classify benefit costs, e.g. if 70 per cent of salaries are direct, then 70 per cent benefits can be assumed to be direct costs. This method should take into account the benefits that are different between permanent and temporary staff members. The organization chart would help to identify the number of personnel and their costs, whether related to programme, support services, management, or governance.

Certain costs such as office supplies, communication, electricity, generator, and water may be difficult to classify as direct and indirect unless tracked by users or departments. In this instance, the headcount could be used as a cost driver to apportion these associated costs e.g. if 60 per cent of human resources staff costs are direct, then 60 per cent of office and utilities costs can be assumed to be direct. The headcount information

also helps to allocate certain shared costs in a more systematic manner, e.g. a department with ten persons in an organization with 100 staff could absorb 10 per cent of shared office and utilities costs, where consumption cannot be tracked otherwise. This makes the costs more direct in nature as it can be measured and attributed to a cost centre. Inadvertently, this also reduces the number of items under the indirect cost category. An organization with a small group of indirect costs coupled with a large group of direct costs would be likely perceived as transparent and accountable.

Costs associated with office rental and maintenance should be treated as direct costs, where feasible. Where National Societies charge donors for use of office space, they should derive the rates from systematic calculation and they should fairly distribute them (reference to 6.1).

Once the main groups of costs have been classified, analyse remaining budget lines using the chart of accounts/trial balance/budget report and classify them accordingly.

III. Identify unallowable costs and remove them from the indirect cost category. Many institutional donors have a list of costs that are ineligible for reimbursement. National Societies should map this list and compare with internal policies to identify ineligible costs that should be covered using their own resources. This would also help the National Society to monitor and control unallowable expenses.

Often, unallowable costs would be those that are most remote from projects, provisional amounts

18 > METHODOLOGY

19GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

(costs that do not have certainty of occurring), and items that are extraordinary in nature (those that would not occur in the normal course of activities). Unallowable costs also include those that are incurred due to an organization’s negligence e.g. penalties. The National Society should analyse if the unallowable cost is material and if they are related to all projects. This helps to decide if the cost should be included in the indirect cost calculation, charged directly to the concerned project or cost centre, or covered by the organization’s own resources. Some common unallowable costs include (the list is not exhaustive or conclusive):

P Bad debts or doubtful debts provision

P Donations or contributions to other organizations (including subcontracts)

P Financial support to branches

P Entertainment or representation costs

P Borrowing costs (loan interests)

P Financial charges (late payment and penalties)

P General fundraising costs (should be covered by funds raised)

P Lobbying cost (with Government or other regulators)

P Professional fees (accounting, legal and others)

P Valuation fees (for land and building)

P Statutory obligations (membership fees and statutory requirements)

P Non-cash costs and other provisions (audit fees, depreciation – note below)

Some of the above costs that initially appear unallowable can be treated as direct costs if they are linked to projects, such as representation, borrowing costs, financial charges or audit fees, e.g. forensic audit for suspicion of fraud is deemed extraordinary in nature and unallowable, but may be categorised as direct if it is commissioned by a donor.

Notes on assets and depreciation The value of assets and depreciation can have a big impact on project funds when they are material. Depreciation charged for assets should be included in project costing, if they had been purchased using the National Society’s internal funds and used for the project. If the assets are donated and the costs are fully charged to a project and not capitalised, then additional depreciation charge amounts to double funding. This should be considered before including depreciation (a non-cash item) in the indirect costs category for calculation.

Some National Societies consider depreciation as replacement funds. This is acceptable if the asset was capitalised or the National Society intends to replace the asset using its own funds. If assets are usually replaced using project funds, building a reserve for the same purpose may not appear appropriate. Replacement funds in the form of depreciation, if charged to projects, should be supported by an asset replacement plan and policy.

Depreciation policies between donors and fund recipients also differ. This is mainly due to accepted accounting standards. It is difficult for a National Society to depreciate each of its assets based on donors’ accounting standards. Where depreciation is used, it should follow the organization’s accounting standards. National Societies should have a policy on capital expenditure to determine when assets should be capitalised (recognized in balance sheet) and when they should be expensed (recognized in income and expenditure statement). This should be in line with the accepted accounting standards.

IV. Adjust the subsequent year’s forecast or estimate for known trends and other factors, such as growth in programme or organization structure, likelihood of emergency operations, changes in market forecasts and inflation. Currency fluctuations could be considered if they are significant based on past trends (only potential losses should be considered) but due to the inherent limitation to forecast this reliably, this factor is usually omitted.

The organization’s strategy and decisions may influence its estimates e.g. organization’s domestic income from a business activity may be steadily increasing but it may intend to sell that business and focus on intensifying community health work. Where forecasts of economic and market conditions are used, the period of validity should be stated.

V. Extend forecasts for at least three years. As a best practice, the indirect cost recovery rate should be applicable for a few years before revision

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

(covered later in the document). This requires the rate to be practical for the few subsequent years. Some organizations have long-term plans and top-line budget information that can be used for estimating several prospective years. Otherwise, the one-year estimate prepared using historical data, trends, and strategy, can be extended for another two years with minor adjustments. Such adjustments should be as consistent as possible (e.g. 5 per cent increase per annum).

The budget information should be used for the analysis as it reflects which costs should have been direct and indirect under normal circumstances, irrespective of the source of funding at present. This enables a more realistic prediction of the coming years by adjusting for exceptional nature that affects cost classification.

Example: A vehicle was budgeted for 12 months under the health project. The activity requiring the vehicle was delayed, and the vehicle was only used for the last seven months and charged accordingly. The cost for the initial five months was charged to the general pool as per the organization’s policy (some organizations might require a different treatment where the health project must absorb the 12 months as budgeted despite actual consumption, because the organization is not prepared for the sudden change). At face value, actual income and expenditure would show seven months’ worth of direct costs and five months’ worth of indirect costs. The situation might change if another project needed the vehicle for that corresponding five months and the cost is then recognized as direct (assuming budget revisions are done).

The changes during the year are caused by many factors but since the (indirect cost) rate is meant to cover prospective years, changes are irrelevant unless they are permanent and affect subsequent years’ budgets. In short, costs should be classified as direct and indirect based on the financial information available, for a normal given year.

VI. Calculate a simple ratio – the result of total indirect costs divided by the total direct costs.

Example 1: A National Society expects to incur indirect costs of 28,000 US dollars per annum. It also expects to manage an average of five projects with the following estimated values:

Project Value (USD)

A 55,000

B 78,000

C 72,000

D 130,000

E 65,000

Total 400,000

Calculation: 28,000 US dollars ÷ 400,000 US dollars = 7 per cent. If the organization applies 7 per cent on programme expenditure, and the project budget is fully spent, 28,000 US dollars is recovered.

Project Value (USD) 7% charge

A 55,000 3,850

B 78,000 5,460

C 72,000 5,040

D 130,000 9,100

E 65,000 4,550

Total 400,000 28,000

There may be layers of indirect costs within the organization, e.g. If the fundraising department benefits the disaster response, health and youth programmes, and the fundraising department costs are meant to be covered by the other three programmes, each of the programme is not only paying the first level of indirect costs charged, but a share of indirect costs absorbed by the fundraising department.

Example 2: Disaster response project is 55,000 US dollars, fundraising department is 10,000 US dollars, and the indirect cost recovery rate is 7 per cent.

Project Value (USD)

Disaster response – direct costs 55,000

Add: Indirect costs (7%) 3,850

Add: Fundraising department costs * 3,567

Full costs 62,417

*10,000 + 7 per cent = 10,700, share for disaster response project is 10,700 ÷ 3 = 3,567

The disaster response project pays for 3,850 US dollar indirect costs, but also pays for 3,567 US dollars (its share of fundraising department costs, which carries an indirect cost of 700 US dollars, making the total indirect costs paid by the disaster response project 4,550 US dollars. To exempt the fundraising department from the first indirect cost charge altogether would be to understate the actual costs. This concept is similar to the indirect cost accumulation when funding flows through different layers of the organization when each applies an indirect cost charge.

20 > METHODOLOGY

21GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

VII. Adjust ratio based on known trends and factors e.g. 80 per cent of direct costs should be used for the ratio if actual expenditure is usually 80 per cent of budget based on past trend. Indirect cost ratio can be calculated for various level of programme implementation (60 per cent, 70 per cent, 80 per cent, 90 per cent and 100 per cent) and an average rate, or one closest to reality, can be adopted.

Where the organization uses domestic income to cover a portion of its costs, the gap or unfunded indirect costs should be used to calculate ratio. This would mean that an organization that has a healthy unrestricted income is able to manipulate its rate to make it lower or more competitive. This highly depends on the National Society’s strategy and policy, on using unrestricted income, building reserves, and recovering costs. Full cost recovery principle requires actual (and not subsidised) share to be assigned to the cost centres.

National Societies that receive Government grants may be required to spend the funds on very specific budget lines. Such Government funding would usually not allow a fixed rate of indirect costs from the fund recipient. In this instance, it would be necessary to calculate the ratio on adjusted indirect costs so that the recovery rate is not overstated. Example:

Description Value (USD)

Total indirect costs 200,000

Less: Government’s contribution to indirect costs 20,000

Adjusted indirect costs A 180,000

Direct costs B 3,000,000

Indirect cost recovery rate (A/B) 6%

If the National Society has a financial information system that easily generates the above information, the calculation would be easier. However, it is not possible to fully automate the steps as many of them rely on the professional judgement of the team involved in calculation. Although the calculation is often done by finance personnel, inputs from senior management and programme managers are crucial.

The 8NS core cost model suggests a method of grouping costs to facilitate calculation. Costs are grouped as activity costs, personnel costs, current costs (branch structure and financial management), and governance costs. The groups are then mapped against broader classification such as project and non-project costs10.

3.4 COST BEHAVIOUR

Cost behaviour is the relationship between input and output and their relevant costs. If the level of activity increases, there will be an increase in indirect costs, although not proportionately. E.g. a National Society may maintain support services that costs 2,000 US dollars to support five projects worth 100,000 US dollars. The same support services structure may support up to eight projects worth 150,000 US dollars. When the number of projects reaches a certain threshold, – perhaps ten projects – the National Society may need more staff to cope with the workload. It may not translate into doubling the support services structure costing 4,000 US dollars but it may fall somewhere between 2,000 and 4,000 US dollars.

The behaviour is partly caused by fixed costs that do not vary with the level of activity. The anomaly is also caused by economies of scale where a National Society is able to meet the requirements of certain new

projects without incurring additional overheads, as consumption of support services between projects and activities vary. Although indirect costs are generally lower as a percentage to direct costs, this is usually the case for National Societies with sustained growth. For smaller National Societies or those in early stages of development, the indirect costs may be significant as they could be investing in capital assets or they may not have achieved economies of scale.

When the number of projects and their value decrease or increase significantly, the National Society may need to downsize or upsize the organization’s structure to match the demands. Often, the challenge is with downsizing, resulting in a bulk of costs that is not commensurate with projects and activity level. This makes it difficult to fund and there is a risk of recovering more than the fair share from projects. The below scenarios show how changes to one set of values influences the other. The examples are not comprehensive and for illustrative purposes only.

Scenario 1: Actual expenditure is lower than initial values

Project Value (USD) Actual expenditure

7% charge

A 55,000 50,000 3,500

B 78,000 65,000 4,550

C 72,000 70,000 4,900

D 130,000 124,000 8,680

E 65,000 55,000 3,850

Total 400,000 364,000 25,480

10. The model refers to non-project costs as ‘core costs’.

GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

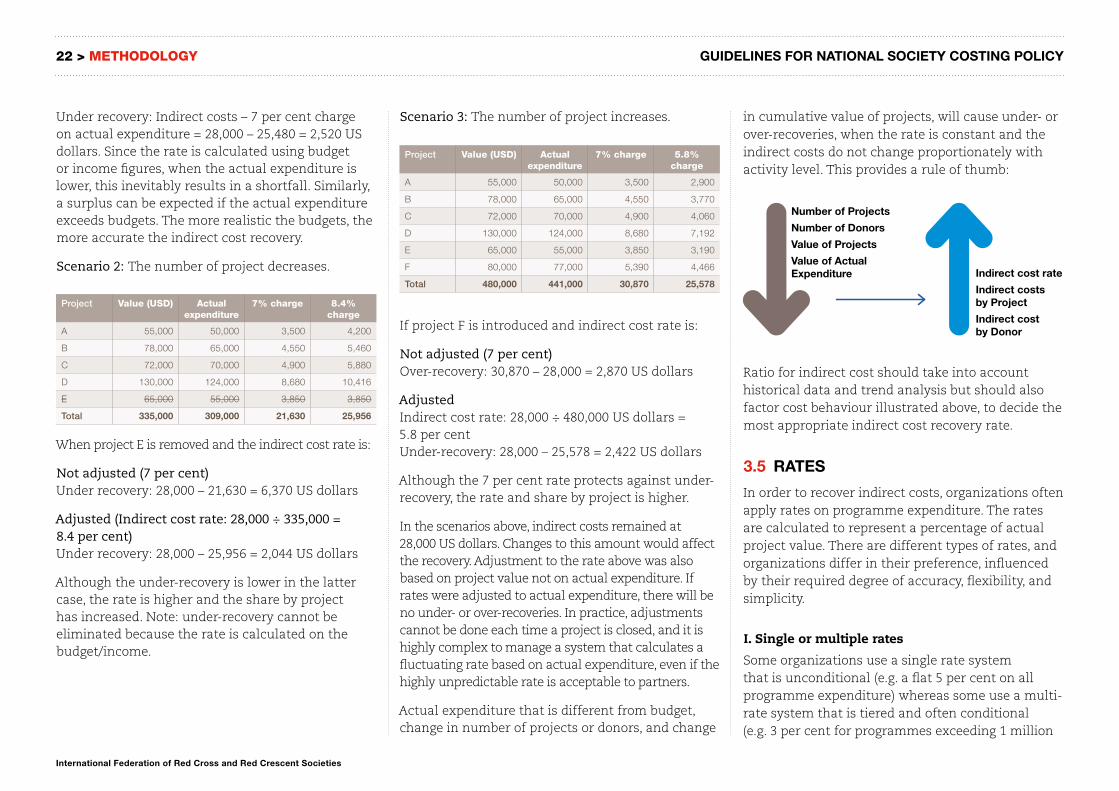

Under recovery: Indirect costs – 7 per cent charge on actual expenditure = 28,000 – 25,480 = 2,520 US dollars. Since the rate is calculated using budget or income figures, when the actual expenditure is lower, this inevitably results in a shortfall. Similarly, a surplus can be expected if the actual expenditure exceeds budgets. The more realistic the budgets, the more accurate the indirect cost recovery.

Scenario 2: The number of project decreases.

Project Value (USD) Actual expenditure

7% charge 8.4% charge

A 55,000 50,000 3,500 4,200

B 78,000 65,000 4,550 5,460

C 72,000 70,000 4,900 5,880

D 130,000 124,000 8,680 10,416

E 65,000 55,000 3,850 3,850

Total 335,000 309,000 21,630 25,956

When project E is removed and the indirect cost rate is:

Not adjusted (7 per cent) Under recovery: 28,000 – 21,630 = 6,370 US dollars

Adjusted (Indirect cost rate: 28,000 ÷ 335,000 = 8.4 per cent) Under recovery: 28,000 – 25,956 = 2,044 US dollars

Although the under-recovery is lower in the latter case, the rate is higher and the share by project has increased. Note: under-recovery cannot be eliminated because the rate is calculated on the budget/income.

Scenario 3: The number of project increases.

Project Value (USD) Actual expenditure

7% charge 5.8% charge

A 55,000 50,000 3,500 2,900

B 78,000 65,000 4,550 3,770

C 72,000 70,000 4,900 4,060

D 130,000 124,000 8,680 7,192

E 65,000 55,000 3,850 3,190

F 80,000 77,000 5,390 4,466

Total 480,000 441,000 30,870 25,578

If project F is introduced and indirect cost rate is:

Not adjusted (7 per cent) Over-recovery: 30,870 – 28,000 = 2,870 US dollars

Adjusted Indirect cost rate: 28,000 ÷ 480,000 US dollars = 5.8 per cent Under-recovery: 28,000 – 25,578 = 2,422 US dollars

Although the 7 per cent rate protects against under-recovery, the rate and share by project is higher.

In the scenarios above, indirect costs remained at 28,000 US dollars. Changes to this amount would affect the recovery. Adjustment to the rate above was also based on project value not on actual expenditure. If rates were adjusted to actual expenditure, there will be no under- or over-recoveries. In practice, adjustments cannot be done each time a project is closed, and it is highly complex to manage a system that calculates a fluctuating rate based on actual expenditure, even if the highly unpredictable rate is acceptable to partners.

Actual expenditure that is different from budget, change in number of projects or donors, and change

in cumulative value of projects, will cause under- or over-recoveries, when the rate is constant and the indirect costs do not change proportionately with activity level. This provides a rule of thumb:

Indirect cost rate

Indirect costs by Project

Indirect cost by Donor

Number of Projects

Number of Donors

Value of Projects

Value of Actual Expenditure

Ratio for indirect cost should take into account historical data and trend analysis but should also factor cost behaviour illustrated above, to decide the most appropriate indirect cost recovery rate.

3.5 RATES

In order to recover indirect costs, organizations often apply rates on programme expenditure. The rates are calculated to represent a percentage of actual project value. There are different types of rates, and organizations differ in their preference, influenced by their required degree of accuracy, flexibility, and simplicity.

I. Single or multiple rates

Some organizations use a single rate system that is unconditional (e.g. a flat 5 per cent on all programme expenditure) whereas some use a multi-rate system that is tiered and often conditional (e.g. 3 per cent for programmes exceeding 1 million

22 > METHODOLOGY

23GUIDELINES FOR NATIONAL SOCIETY COSTING POLICY

International Federation of Red Cross and Red Crescent Societies

US dollars, 5 per cent for emergencies, and 10 per cent for long-term development programmes). The single rate is more rigid but easier to manage and, while the latter appeals to most stakeholders for the flexibility, the system itself may be difficult to manage.

A. Single rate system Fixed or flat rate is preferred by some organizations because it is simpler to use. The rate is consistent and predictable, and this helps in budgeting and planning. Managing a single rate is undoubtedly easier, but determining a single rate is a challenge as it relies on the National Society to accurately forecast its indirect costs for one to three years. Even an organization with sophisticated systems may only achieve this with reasonable accuracy.