Embed Size (px)

Citation preview

b a c k n e x th o m e

Thomas H. BeechySchulich School of Business,

York University

Joan E. D. ConrodFaculty of Management,

Dalhousie University

PowerPoint slides by:Bruce W. MacLean,Bruce W. MacLean,

Faculty of Management,Faculty of Management,

Dalhousie UniversityDalhousie University

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Intermediate Accounting

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Chapter 16

Accounting for CorporateIncome Taxes

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Introduction

■ The amount of taxable income often differs from the amount of pre-taxnet income reported for accounting purposes.

■ Intraperiod income tax allocation Disaggregate the single netincome tax amount and report it in the appropriate sections ofthe financial statements with related gains and losses.

■ Interperiod tax allocation The accounting carrying values ofassets and liabilities may be different than from their taxbases. Recognize these differences by basing incomeexpense on the accounting values. Future income tax assetsor liabilities may result from temporary timing differences.

■ Accounting for loss carry forward or back.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Provision Or Expense?

■ In the income statement, we always are reporting the expenseexpense forincome taxes. However, it is very common in practice forcompanies to label the income tax expense in the incomestatement as Provision for Income TaxesProvision for Income Taxes. This is a somewhatconfusing label because a provisionprovision usually is used for anestimated liability, such as �Provision for Warranty Costs� �Provision for Warranty Costs� in theliabilities section of a balance sheet.

■ The reason that companies use provisionprovision for the income taxexpense is that when the company has a loss for tax purposes, theincome statement entry for income taxes may be a credit ratherthan a debit. Rather than switch the income statement label from�expense� �expense� to �benefit�, �benefit�, companies use the vague term provisionprovisionto fit all circumstances.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Interperiod Tax Allocation � Introduction

■ A company adopts those accounting policies that managementperceives will best satisfy the objectives of the financial statementusers and preparerspreparers.

■ One general objective is to measure net income, which usually isthe result of many accruals and interperiod allocations.

■ In contrast, the objective of the Income Tax Act and RegulationsIncome Tax Act and Regulationsis to generate revenue for the government.

■ Because it is easier and more objective to assess taxes when cashis flowing, tax policy generally includes revenues and expenses intaxable income on the basis of cash flows rather than accountingallocations, with some important exceptions relating primarily toinventories, capital assets, and multi-period earnings processes(e.g., revenue from long term contracts).

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Differences Between Taxable AndAccounting Income

■ The difference between taxable income and accounting incomearises from two types of sources: permanent permanent differences andtemporarytemporary differences.

■ Permanent differences are items of revenue, expense, gains orlosses that are reported for accounting purposes but never enterinto the computation of taxable income. Permanent differencesalso include those rare items that enter into taxable income but arenever included in accounting income.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Timing Or Temporary Differences?

■ Temporary differences arise when the tax basis of an asset orliability is different from its carrying value on the financialstatements. Alternatively, temporary differences can be viewed asthose components of accounting net income that do enter into thecomputation of taxable income, but do so in a different period thanthey are recognized for financial reporting.

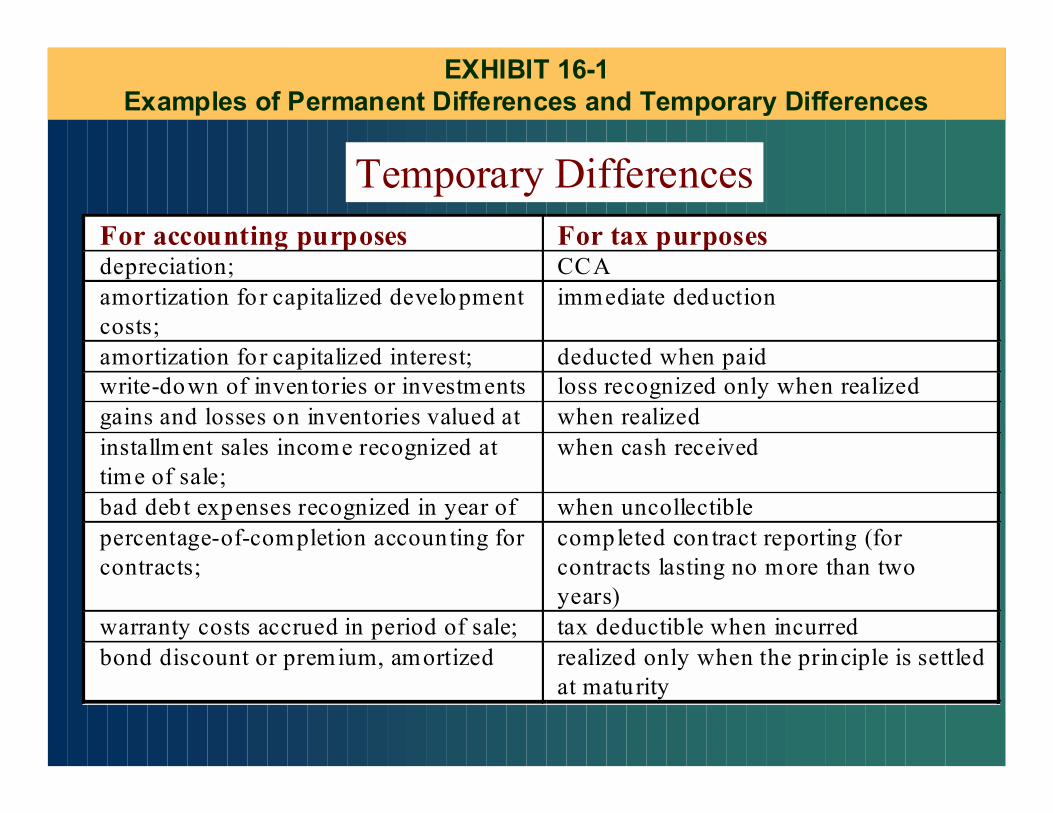

EXHIBIT 16-1Examples of Permanent Differences and Temporary Differences

■ Permanent Differences:

• dividends received by Canadian corporations from othertaxable Canadian corporations

• equity in earnings of significantly-influenced investees

• 25% of capital gains

• golf club dues

• 50% of meals and entertainment expenses

• interest and penalties on taxes

• political contributions

For accounting purposes For tax purposesdepreciation; CCAamortization for capitalized developmentcosts;

immediate deduction

amortization for capitalized interest; deducted when paidwrite-down of inventories or investments loss recognized only when realizedgains and losses on inventories valued at when realizedinstallment sales income recognized attime of sale;

when cash received

bad debt expenses recognized in year of when uncollectiblepercentage-of-completion accounting forcontracts;

completed contract reporting (forcontracts lasting no more than twoyears)

warranty costs accrued in period of sale; tax deductible when incurredbond discount or premium, amortized realized only when the principle is settled

at maturity

Temporary Differences

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Conceptual Issues In Interperiod TaxAllocation

■ The objective of comprehensive interperiod income taxcomprehensive interperiod income taxallocation allocation is to recognize the income tax effect of every item whenthat item is recognized in accounting net income. Alternatives tocomprehensive allocation are the flow-through method flow-through method andpartial allocationpartial allocation.

■ When the item of revenue, expense, gain or loss first enters thecalculation of either either taxable income or accounting income, it is anoriginatingoriginating temporary difference.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Extend Of Allocation

■■ Extent of allocation Extent of allocation refers to the range of temporary differences to whichinterperiod tax allocation is applied. The three basic options are:

✜✜ No allocation: the flow-through methodNo allocation: the flow-through method

✜✜ Full allocation: the comprehensive methodFull allocation: the comprehensive method

✜✜ Partial allocationPartial allocation

■ The flow-through methodflow-through method recognizes the amount of taxes assessed ineach year as the income tax expense for that year: income tax expense =current income tax.

■■ Comprehensive allocation Comprehensive allocation is the opposite extreme: the tax effects of alltemporary differences are allocated, regardless of the timing or likelihoodof their reversal.

■■ Partial allocationPartial allocation actually is a �family� of alternatives that falls betweenthe two extremes of no allocation and full allocation. Under partialallocation, interperiod income tax allocation is applied to some types oftemporary differences but not to all.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

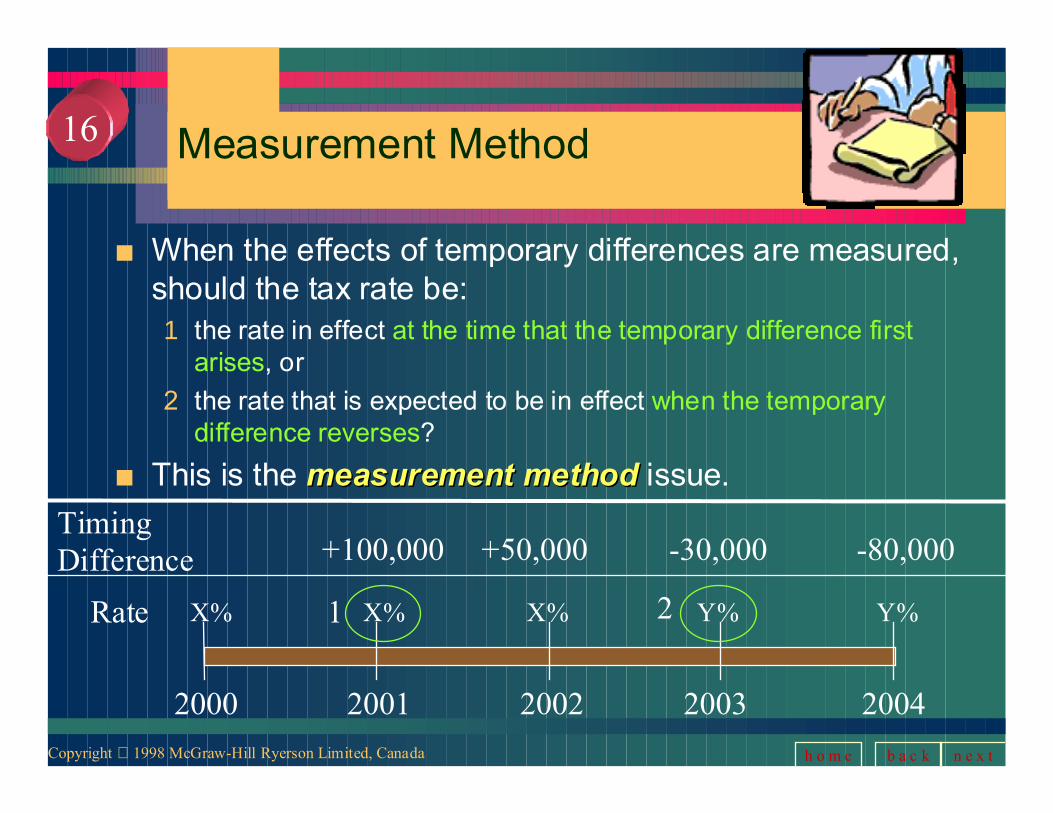

Measurement Method

■ When the effects of temporary differences are measured,should the tax rate be:1 the rate in effect at the time that the temporary difference first

arises, or

2 the rate that is expected to be in effect when the temporarydifference reverses?

■ This is the measurement method measurement method issue.

2000 2001 2002 2003 2004

Rate X% X% X% Y% Y%

TimingDifference +100,000 +50,000 -30,000 -80,000

1 2

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Discounting

■ If the deferred tax balances are discounted, interest is imputed onthe balance each year, using the same rate as was used fordiscounting. The income tax expense on the income statementwould therefore include:

� the discounted present value discounted present value of the future tax impact oftemporary differences that originated in the current period,

� plus interest interest on the balance at the beginning of the year,

� plus or minus adjustmentsadjustments to the ending balance for tax rateincreases or decreases,

� less drawdownsdrawdowns that occurred during the current period due toreversal of the temporary difference.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Effective Tax Rate

■ One objective of interperiod income tax allocation is to reflect in netincome the effective tax rate that the corporation is paying.

■ The effective tax rate effective tax rate as the ratio of the income tax expenseexpense(including the tax expense relating to temporary differences) dividedby the pretax net income.

■ Financial analysts often calculate the effective tax rate as the ratio ofcurrentcurrent income taxes (that is, without including the tax expense orbenefit related to temporary differences) to pretax net income.

■ However, the CICA Handbook CICA Handbook speaks of the �income tax rate�[CICA 3465.92(c)] [CICA 3465.92(c)] in a context that includes the effects of temporarydifferences,

■ The CICA HandbookCICA Handbook requires that public companiespublic companies provide areconciliation between the effective and statutory rate.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Future Income Tax Assets

■ Future income taxes are not discounted.

■ Future income tax assets and liabilities are classified ascurrent assets/liabilities if the temporary differences relate tocurrent assets or liabilities. Future income tax balances thatrelate to long-term assets and liabilities are reportedseparately from other long-term assets and liabilities.

■ Future income tax assets arise from:� Write-downs of inventory or other assets for accounting purposes,

tax deduction at the time of sale

� Deferred executive compensation treated as an expense foraccounting purposes, tax deduction when paid

� Warranty costs estimated and charged to income at the time of sale

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Balance Sheet Presentation

■ Within each classification of current and non-current, futureincome tax balances relating to different items are nettedand reported as a single amount. Current and non-currentfuture tax liability balances may not be netted against eachother. Future income tax assets and liabilities that arise dueto differing tax and accounting treatments for the followingassets and liabilities will be classified as current.current.� Installment notes receivable allowance for doubtful accounts

� inventories accrued receivables

� warranty liabilities notes payable

� accrued liabilities temporary investments

�� This classification does not depend upon the period of reversalThis classification does not depend upon the period of reversal..

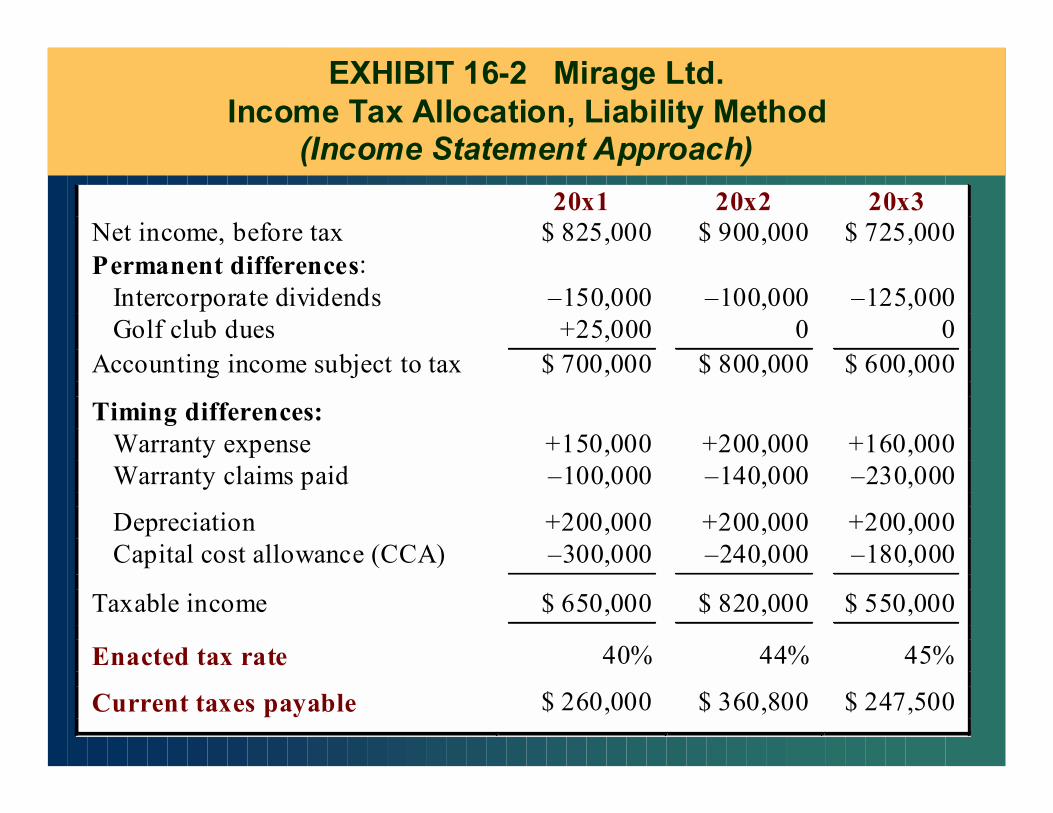

EXHIBIT 16-2 Mirage Ltd.Income Tax Allocation, Liability Method

(Income Statement Approach)

20x1 20x2 20x3Net income, before tax $ 825,000 $ 900,000 $ 725,000Permanent differences: Intercorporate dividends �150,000 �100,000 �125,000 Golf club dues +25,000 0 0Accounting income subject to tax $ 700,000 $ 800,000 $ 600,000

Timing differences: Warranty expense +150,000 +200,000 +160,000 Warranty claims paid �100,000 �140,000 �230,000

Depreciation +200,000 +200,000 +200,000 Capital cost allowance (CCA) �300,000 �240,000 �180,000

Taxable income $ 650,000 $ 820,000 $ 550,000

Enacted tax rate 40% 44% 45%

Current taxes payable $ 260,000 $ 360,800 $ 247,500

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

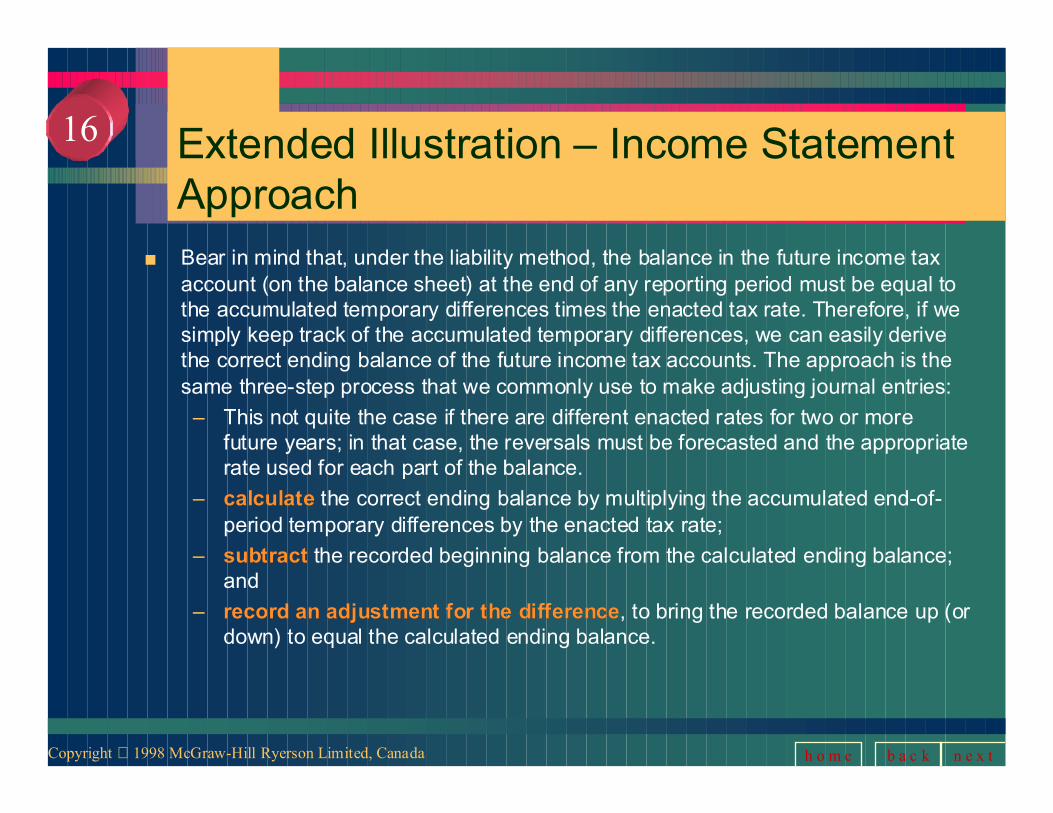

Extended Illustration � Income StatementApproach

■ Bear in mind that, under the liability method, the balance in the future income taxaccount (on the balance sheet) at the end of any reporting period must be equal tothe accumulated temporary differences times the enacted tax rate. Therefore, if wesimply keep track of the accumulated temporary differences, we can easily derivethe correct ending balance of the future income tax accounts. The approach is thesame three-step process that we commonly use to make adjusting journal entries:

� This not quite the case if there are different enacted rates for two or morefuture years; in that case, the reversals must be forecasted and the appropriaterate used for each part of the balance.

�� calculatecalculate the correct ending balance by multiplying the accumulated end-of-period temporary differences by the enacted tax rate;

�� subtractsubtract the recorded beginning balance from the calculated ending balance;and

�� record an adjustment for the differencerecord an adjustment for the difference, to bring the recorded balance up (ordown) to equal the calculated ending balance.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Extended Illustration � Balance SheetApproach

■ The advocates of the liability approach often argue that we shouldbe looking at the balance sheet instead of the income statement.

■ Indeed, temporary differences are defined in the CICA HandbookCICA Handbookby the differences between tax bases and balance sheet carryingvalues.

■ Because the balance sheet approach may be a little more difficultto conceptualize than the income statement approach, weconsidered the income statement approach first.

■ However, we also must understand the balance sheet approach,especially since this is the approach cited in the CICA HandbookCICA Handbook.

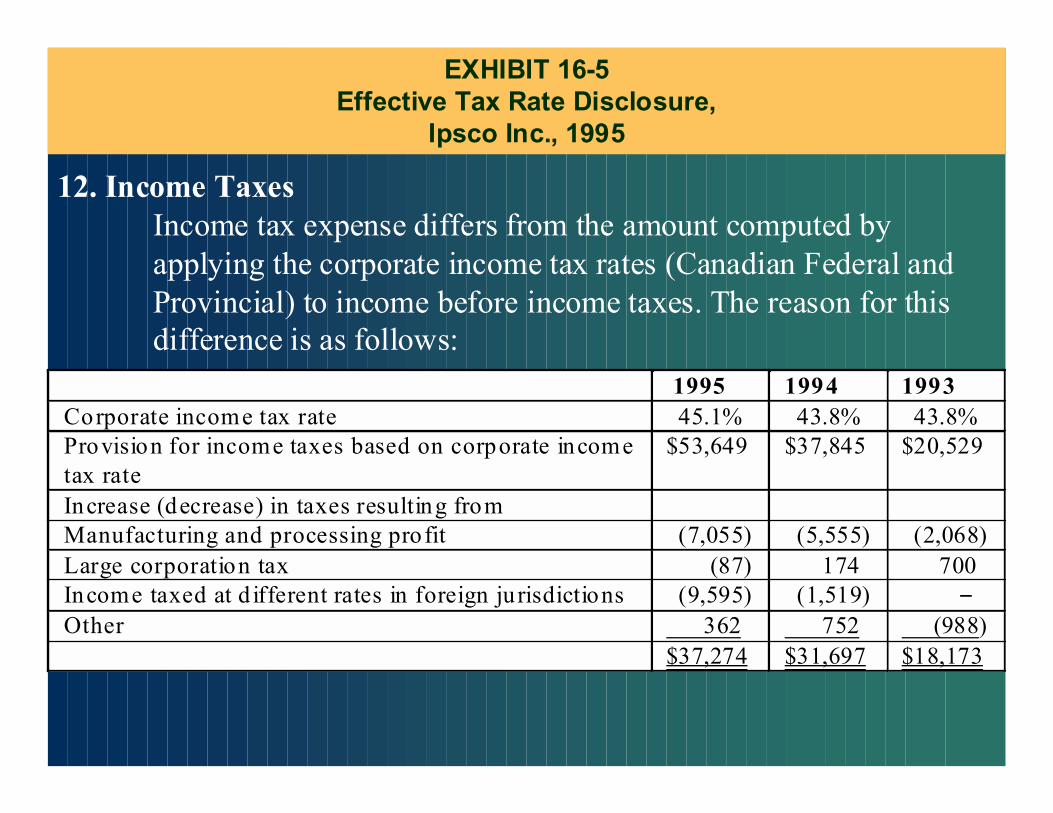

EXHIBIT 16-5Effective Tax Rate Disclosure,

Ipsco Inc., 1995

12. Income TaxesIncome tax expense differs from the amount computed byapplying the corporate income tax rates (Canadian Federal andProvincial) to income before income taxes. The reason for thisdifference is as follows:

1995 1994 1993Corporate income tax rate 45.1% 43.8% 43.8%Provision for income taxes based on corporate incometax rate

$53,649 $37,845 $20,529

Increase (decrease) in taxes resulting fromManufacturing and processing profit (7,055) (5,555) (2,068)Large corporation tax (87) 174 700Income taxed at d ifferent rates in foreign jurisdictions (9,595) (1,519) −Other 362 752 (988)

$37,274 $31,697 $18,173

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

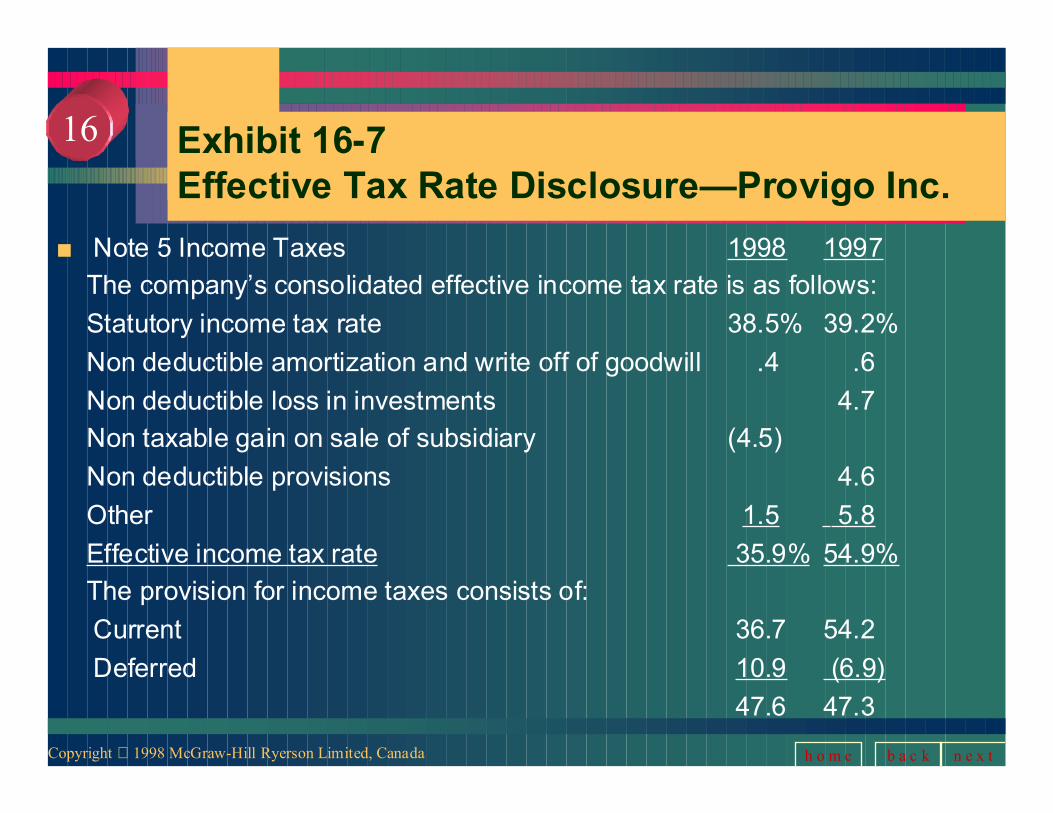

Exhibit 16-7Effective Tax Rate Disclosure�Provigo Inc.

■ Note 5 Income Taxes 1998 1997

The company�s consolidated effective income tax rate is as follows:

Statutory income tax rate 38.5% 39.2%

Non deductible amortization and write off of goodwill .4 .6

Non deductible loss in investments 4.7

Non taxable gain on sale of subsidiary (4.5)

Non deductible provisions 4.6

Other 1.5 5.8

Effective income tax rate 35.9% 54.9%

The provision for income taxes consists of:

Current 36.7 54.2

Deferred 10.9 (6.9)

47.6 47.3

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

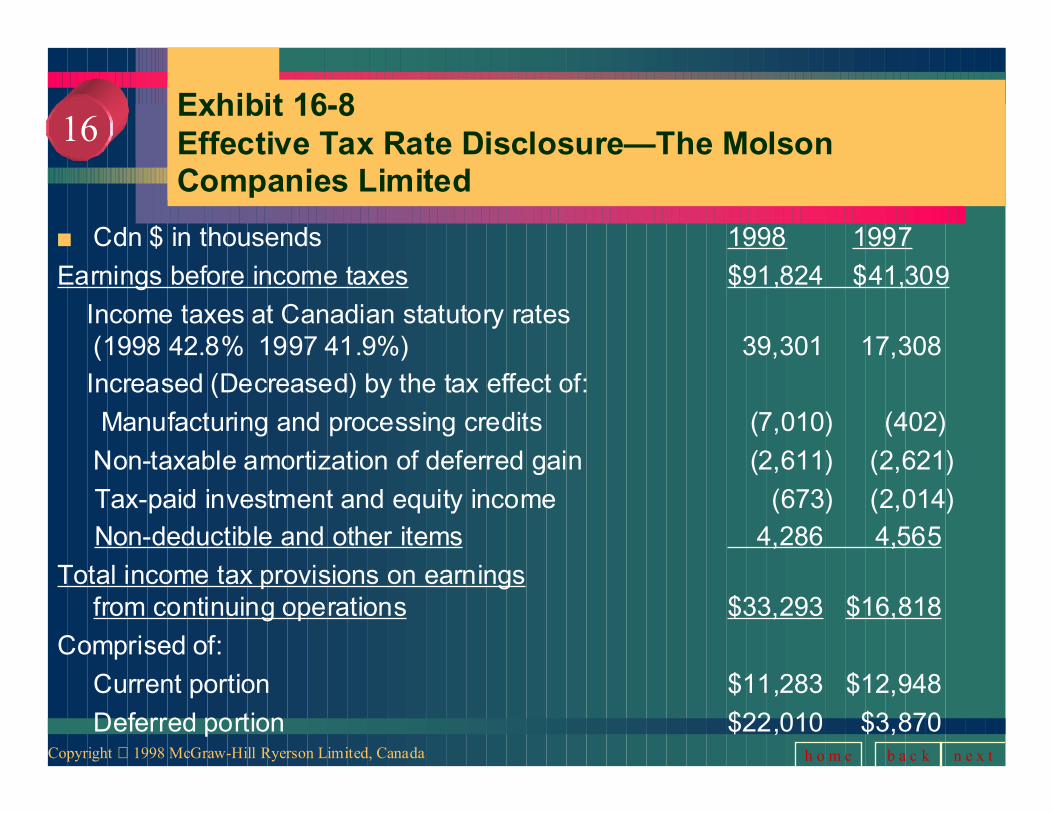

Exhibit 16-8Effective Tax Rate Disclosure�The MolsonCompanies Limited

■ Cdn $ in thousends 1998 1997

Earnings before income taxes $91,824 $41,309

Income taxes at Canadian statutory rates(1998 42.8% 1997 41.9%) 39,301 17,308

Increased (Decreased) by the tax effect of:

Manufacturing and processing credits (7,010) (402)

Non-taxable amortization of deferred gain (2,611) (2,621)

Tax-paid investment and equity income (673) (2,014)

Non-deductible and other items 4,286 4,565

Total income tax provisions on earningsfrom continuing operations $33,293 $16,818

Comprised of:

Current portion $11,283 $12,948

Deferred portion $22,010 $3,870

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Cash Flow Statement

■ The cash flow statement will include only the amounts of taxes actuallythe amounts of taxes actuallypaid or received for the yearpaid or received for the year. All allocations, whether for temporarydifferences or for tax loss carry forwards, must be reversed out.

■ The impact of income tax accounting on the cash flow statement is clear: alltax allocation amounts must be reversed out of transactions reported on thecash flow statement. The cash flow statement must include only the actualmust include only the actualtaxes paid.taxes paid.

■ When the indirect method of presentation is used for operating cash flow,future tax assets and liabilities that have been credited (or charged) toincome must be subtracted from (or added back to) net income. Thereversals include both (1) allocations relating to temporary differences(1) allocations relating to temporary differencesand (2) benefits recognized for the future benefits of tax loss carry(2) benefits recognized for the future benefits of tax loss carryforwardsforwards. When the direct method of presentation is used, the cash used for(or provided by) income taxes must include only the taxes actually paid (orpayable) to the government and tax refunds actually received (or receivable)from the government.

b a c k n e x th o m e

16

Copyright 1998 McGraw-Hill Ryerson Limited, Canada

Appendix : The Investment Tax Credit

■ The investment tax credit (ITC) is a direct reduction of income taxes that isgranted to enterprises that invest in certain types of assets or in researchand development costs.

■ There are two possible approaches to accounting for ITCs: (1) the flow-through approach, and (2) the cost-reduction approach.

■ The CICA Handbook recommends using the cost-reduction approach,wherein the ITC is deducted from the expenditures that gave rise to theITC..

■ ITC on expenditures that are reported as current expenses are usuallydeducted from income tax expense rather than from the functionalexpense itself.

■ When qualifying expenditures are made to acquire an asset (includingdeferred development costs), the ITC can either be (1) deducted from theasset�s carrying value, with depreciation based on the net amount, or (2)deferred separately and amortized on the same basis as the asset itself.