Embed Size (px)

Citation preview

ASC 740 Income Tax

Accounting Challenges in 2013 Tackling Valuations of Deferred Tax Assets, Tax Expense and UTP Reporting, and Other Issues

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, MAY 28, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Douglas Sayuk, Partner, Clifton Douglas, San Jose, Calif.

Cindy Frank, Senior Director, Tax Process Efficiency and Technology, BDO USA, Phoenix

Jeffrey Zawada, Director, FreedMaxick CPAs, Buffalo, N.Y.

For this program, attendees must listen to the audio over the telephone.

Tips for Optimal Quality

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now. (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

ASC 740 Income Tax Accounting Challenges in 2013 Seminar

Douglas Sayuk, Clifton Douglas

May 28, 2013

Cindy Frank, BDO USA

Jeffrey Zawada, FreedMaxick CPAs

Today’s Program

Overview Of ASC 740 And Related Guidance

[Cindy Frank]

Specific Income Tax Accounting Issues, Best

Practices

[Douglas Sayuk, Cindy Frank and Jeffrey

Zawada]

Slide 8 – Slide 26

Slide 27 – Slide 96

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

OVERVIEW OF ASC 740 AND RELATED GUIDANCE

Cindy Frank, BDO USA

FAS 109/ASC 740 Objectives

Recognize:

1. The amount of taxes payable or refundable for the current year

2. Deferred tax liabilities and assets for the future tax consequences

9

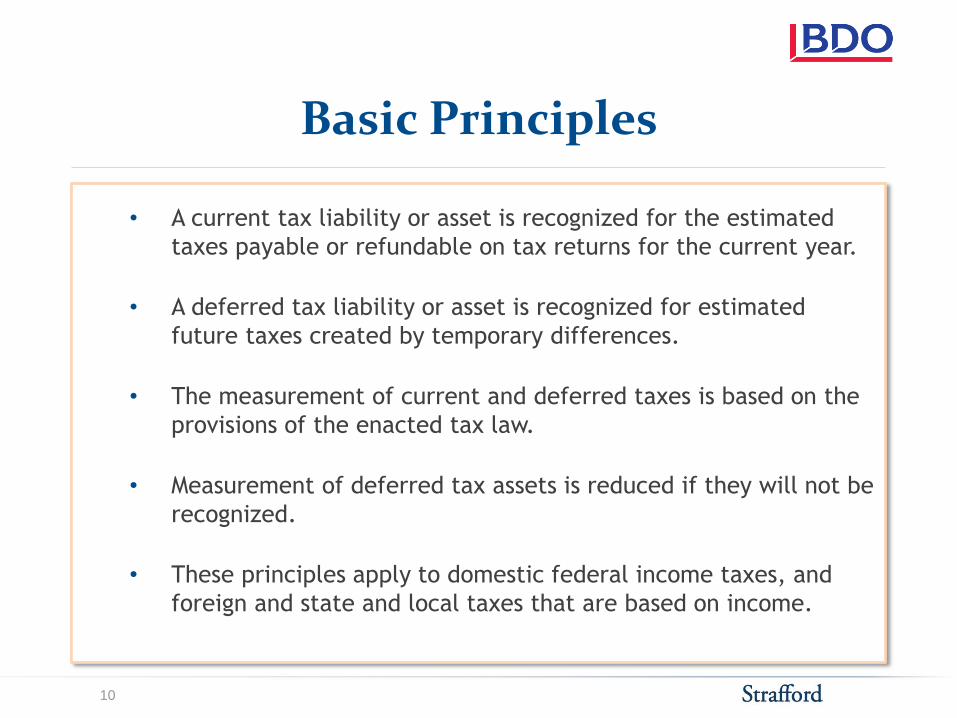

Basic Principles

• A current tax liability or asset is recognized for the estimated

taxes payable or refundable on tax returns for the current year.

• A deferred tax liability or asset is recognized for estimated

future taxes created by temporary differences.

• The measurement of current and deferred taxes is based on the

provisions of the enacted tax law.

• Measurement of deferred tax assets is reduced if they will not be

recognized.

• These principles apply to domestic federal income taxes, and

foreign and state and local taxes that are based on income.

10

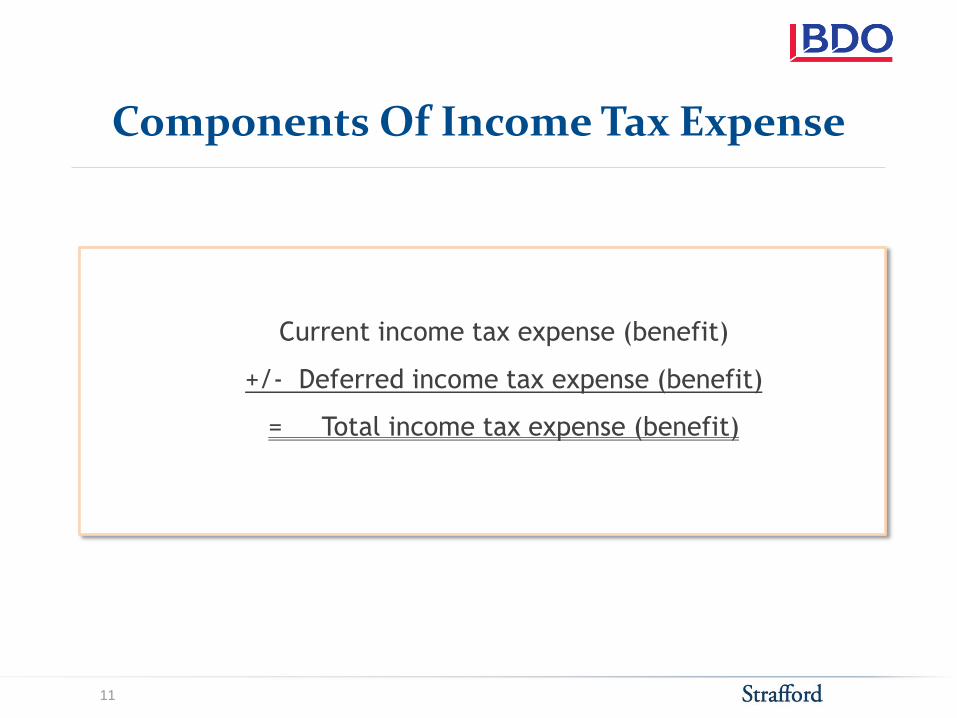

Components Of Income Tax Expense

Current income tax expense (benefit)

+/- Deferred income tax expense (benefit)

= Total income tax expense (benefit)

11

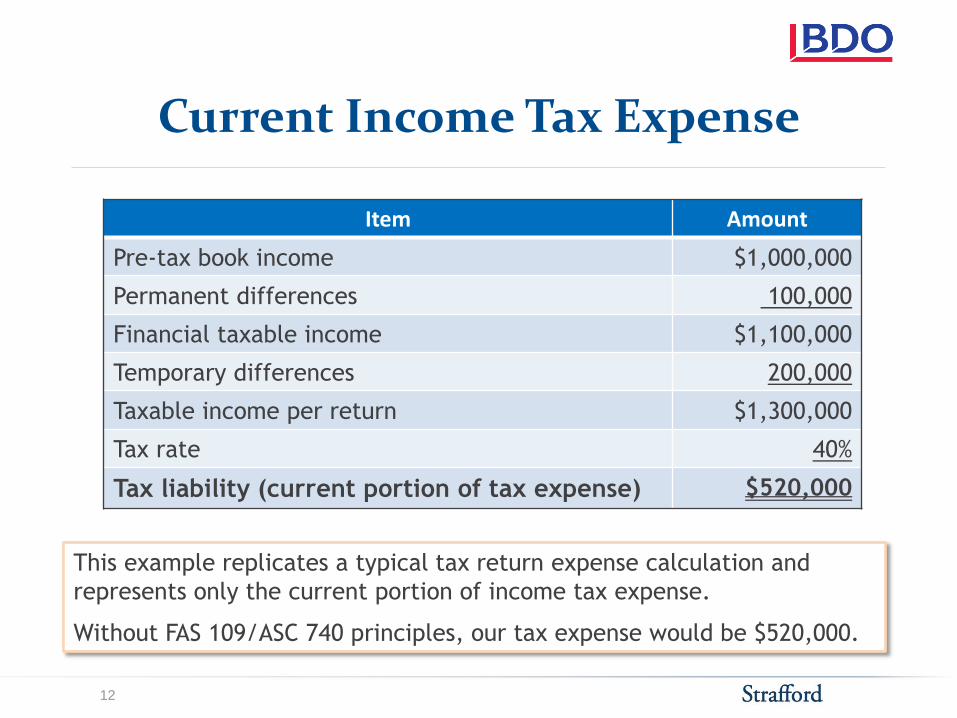

Current Income Tax Expense

This example replicates a typical tax return expense calculation and

represents only the current portion of income tax expense.

Without FAS 109/ASC 740 principles, our tax expense would be $520,000.

Item Amount

Pre-tax book income $1,000,000

Permanent differences 100,000

Financial taxable income $1,100,000

Temporary differences 200,000

Taxable income per return $1,300,000

Tax rate 40%

Tax liability (current portion of tax expense) $520,000

12

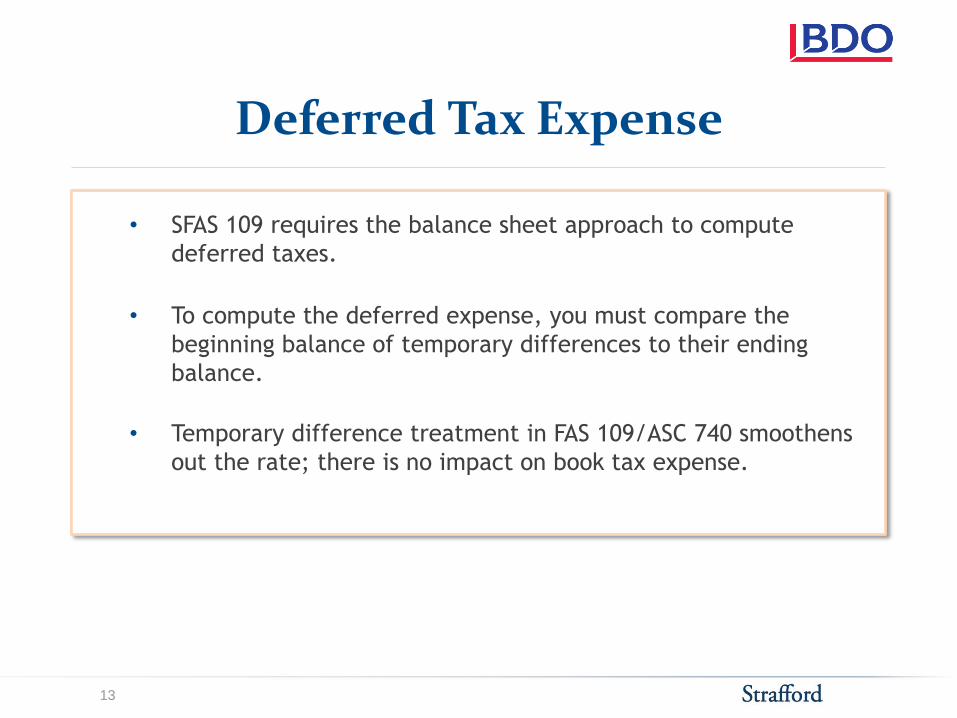

Deferred Tax Expense

• SFAS 109 requires the balance sheet approach to compute

deferred taxes.

• To compute the deferred expense, you must compare the

beginning balance of temporary differences to their ending

balance.

• Temporary difference treatment in FAS 109/ASC 740 smoothens

out the rate; there is no impact on book tax expense.

13

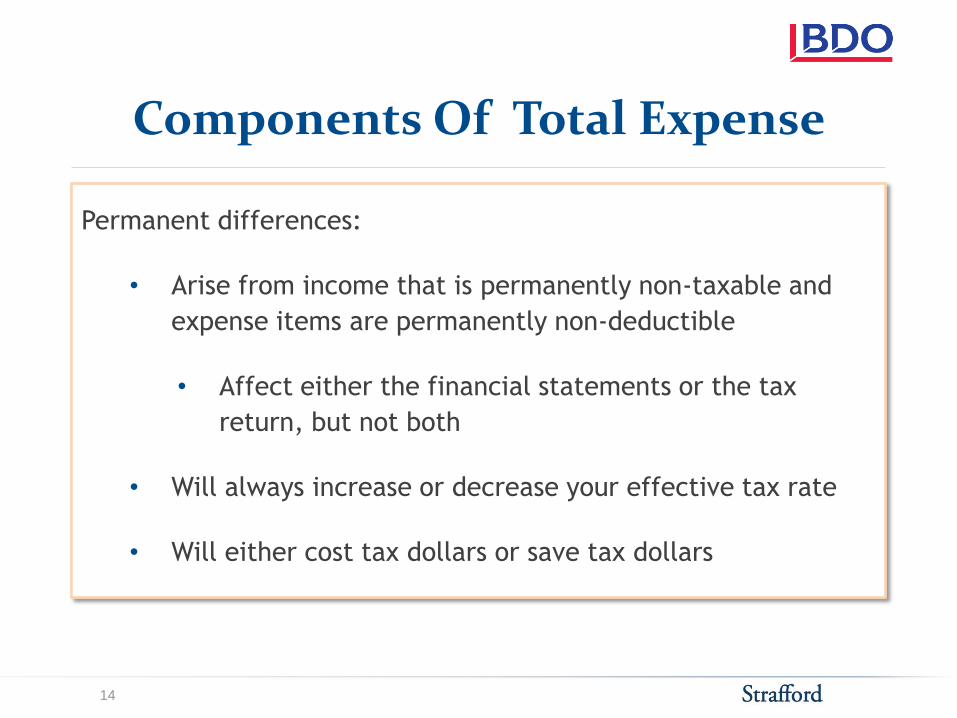

Components Of Total Expense

Permanent differences:

• Arise from income that is permanently non-taxable and

expense items are permanently non-deductible

• Affect either the financial statements or the tax

return, but not both

• Will always increase or decrease your effective tax rate

• Will either cost tax dollars or save tax dollars

14

Current Income Tax Expense

Item Amount

Pre-tax book income $1,000,000

Permanent differences 100,000

Financial taxable income $1,100,000

Temporary differences 200,000

Taxable income per return $1,300,000

Tax rate 40%

Tax liability (current portion of tax expense)

$520,000

15

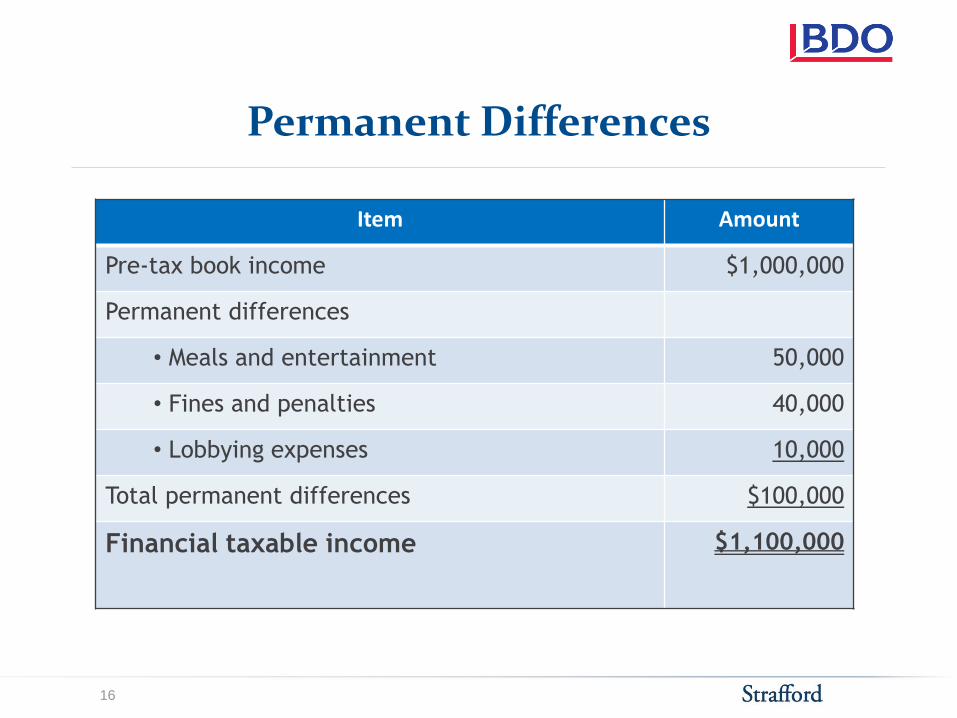

Permanent Differences

Item Amount

Pre-tax book income $1,000,000

Permanent differences

• Meals and entertainment 50,000

• Fines and penalties 40,000

• Lobbying expenses 10,000

Total permanent differences $100,000

Financial taxable income $1,100,000

16

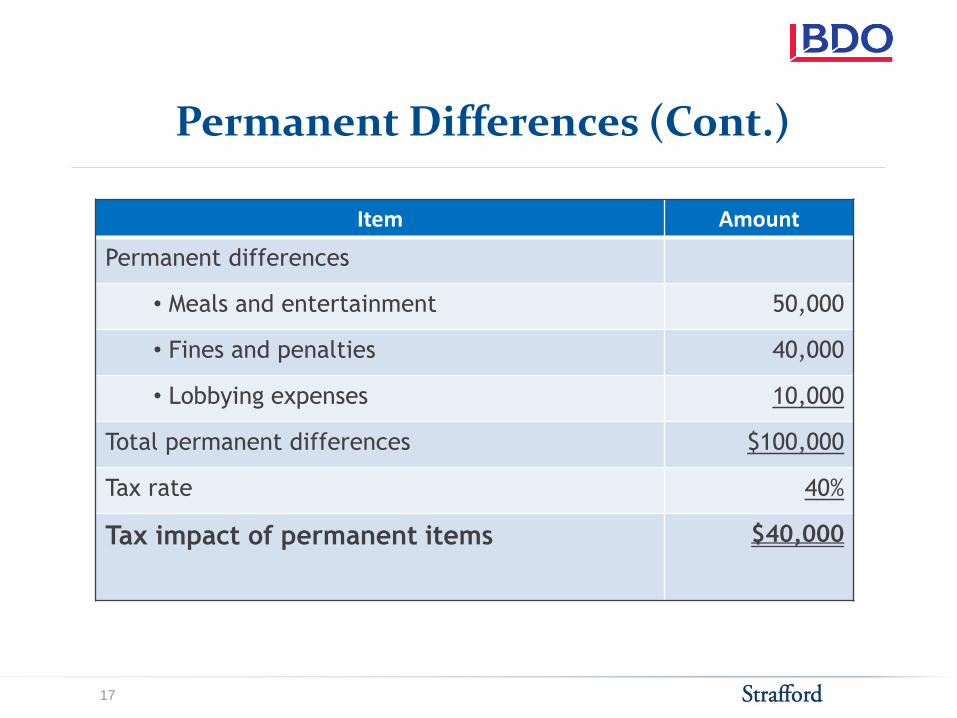

Permanent Differences (Cont.)

Item Amount

Permanent differences

• Meals and entertainment 50,000

• Fines and penalties 40,000

• Lobbying expenses 10,000

Total permanent differences $100,000

Tax rate 40%

Tax impact of permanent items $40,000

17

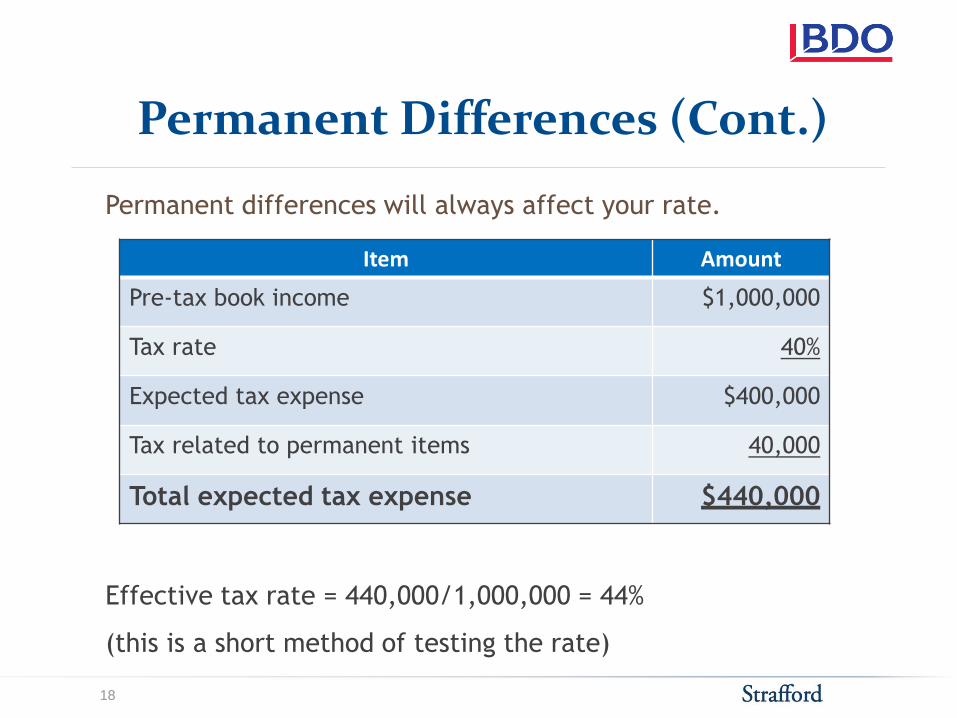

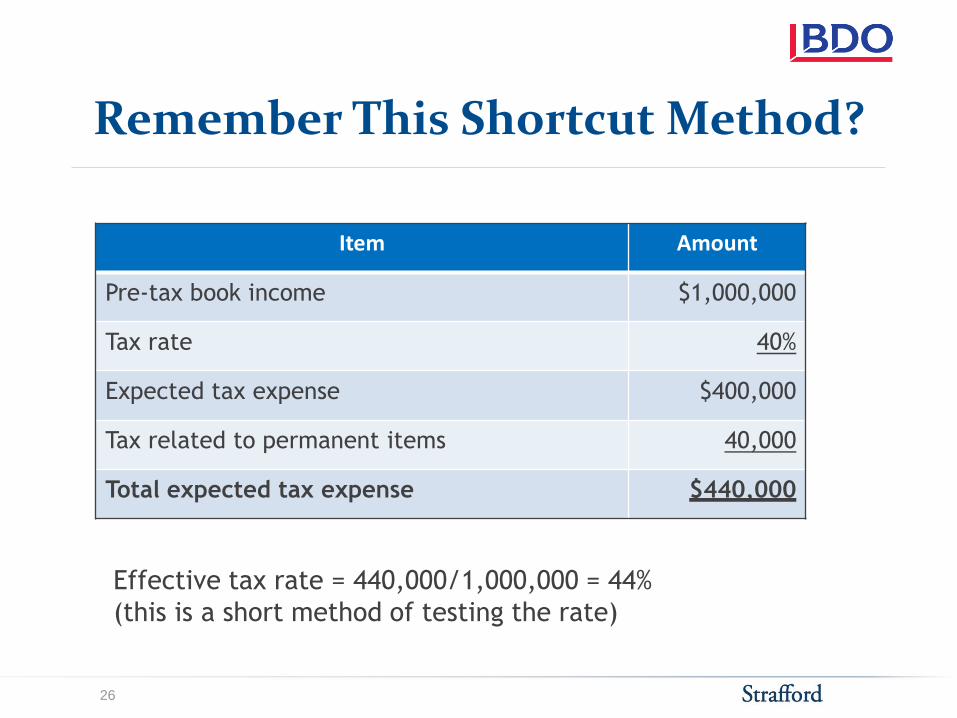

Permanent Differences (Cont.)

Effective tax rate = 440,000/1,000,000 = 44%

(this is a short method of testing the rate)

Permanent differences will always affect your rate.

Item Amount

Pre-tax book income $1,000,000

Tax rate 40%

Expected tax expense $400,000

Tax related to permanent items 40,000

Total expected tax expense $440,000

18

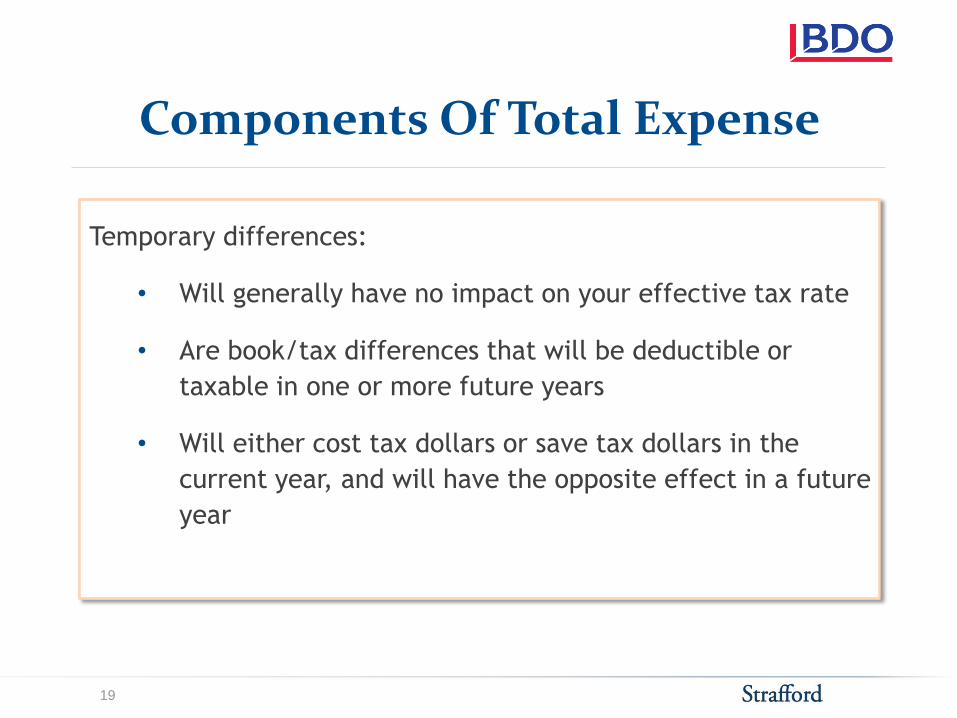

Components Of Total Expense

Temporary differences:

• Will generally have no impact on your effective tax rate

• Are book/tax differences that will be deductible or

taxable in one or more future years

• Will either cost tax dollars or save tax dollars in the

current year, and will have the opposite effect in a future

year

19

Current Income Tax Expense, Revisited

Item Amount

Pre-tax book income $1,000,000

Permanent differences 100,000

Financial taxable income $1,100,000

Temporary differences 200,000

Taxable income per return $1,300,000

Tax rate 40%

Tax liability (current portion of tax expense)

$520,000

20

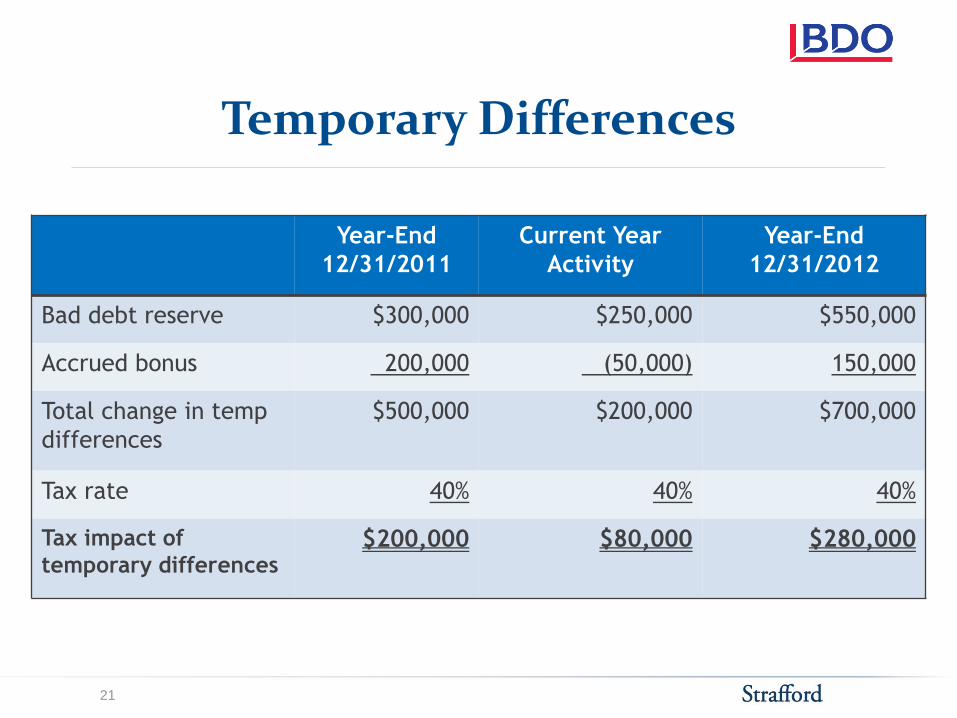

Temporary Differences

Year-End

12/31/2011

Current Year

Activity

Year-End

12/31/2012

Bad debt reserve $300,000 $250,000 $550,000

Accrued bonus 200,000 (50,000) 150,000

Total change in temp

differences

$500,000 $200,000 $700,000

Tax rate 40% 40% 40%

Tax impact of

temporary differences $200,000 $80,000 $280,000

21

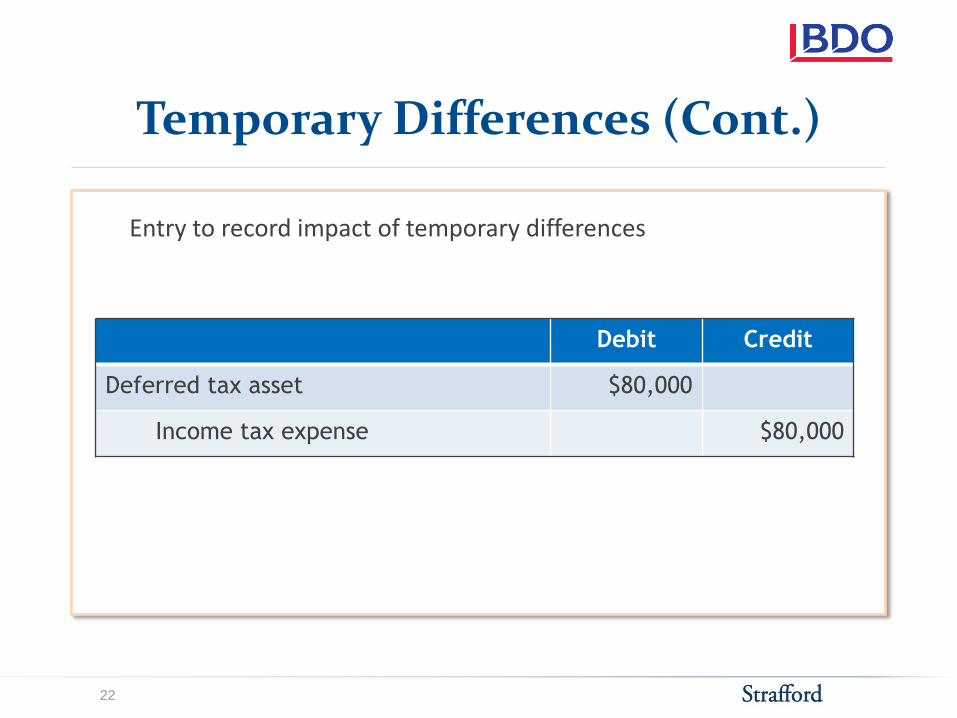

Temporary Differences (Cont.)

Entry to record impact of temporary differences

Debit Credit

Deferred tax asset $80,000

Income tax expense $80,000

22

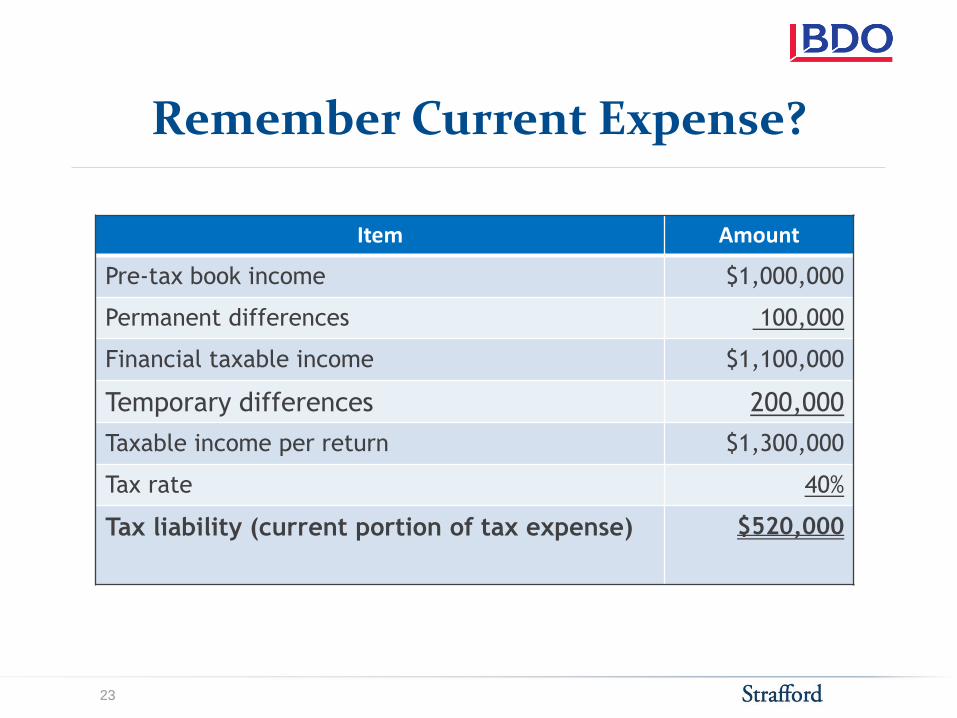

Remember Current Expense?

Item Amount

Pre-tax book income $1,000,000

Permanent differences 100,000

Financial taxable income $1,100,000

Temporary differences 200,000

Taxable income per return $1,300,000

Tax rate 40%

Tax liability (current portion of tax expense)

$520,000

23

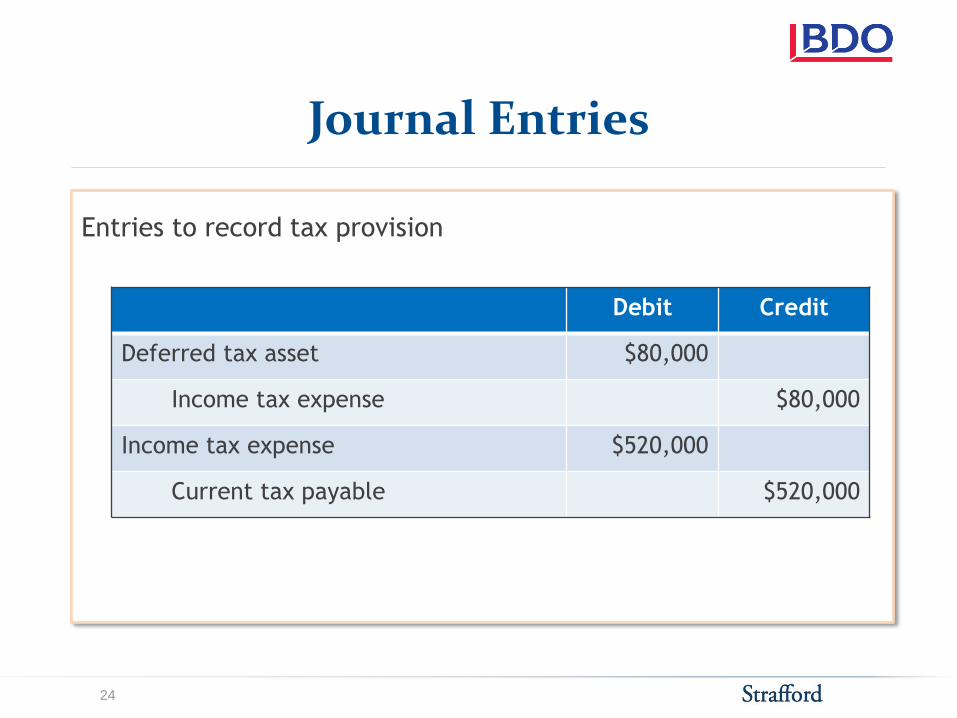

Journal Entries

Entries to record tax provision

Debit Credit

Deferred tax asset $80,000

Income tax expense $80,000

Income tax expense $520,000

Current tax payable $520,000

24

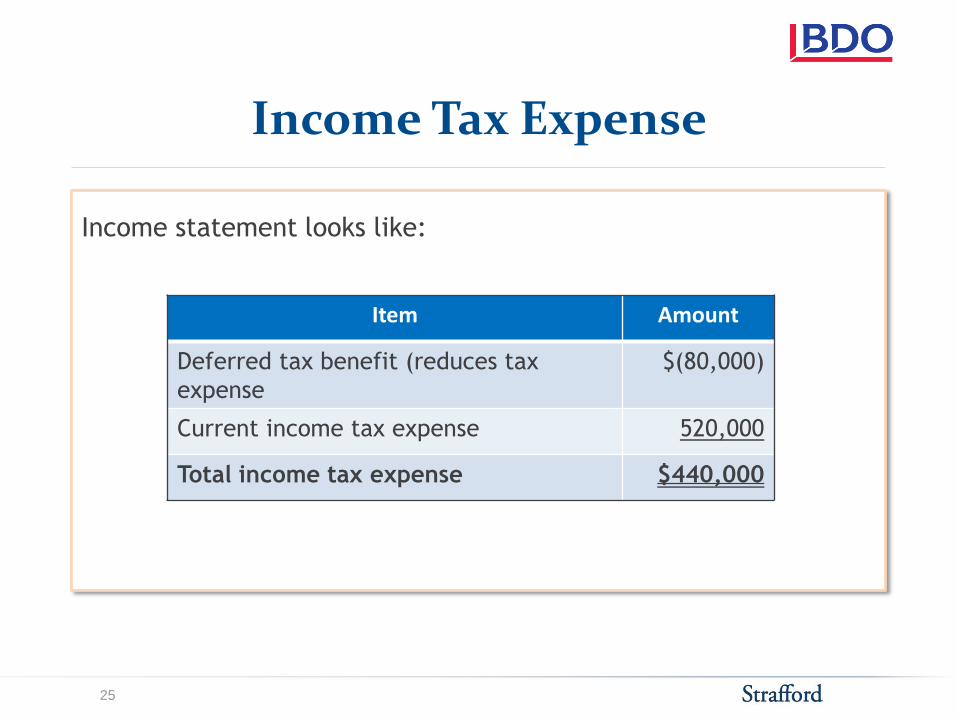

Income Tax Expense

Income statement looks like:

Item Amount

Deferred tax benefit (reduces tax

expense

$(80,000)

Current income tax expense 520,000

Total income tax expense $440,000

25

Remember This Shortcut Method?

Item Amount

Pre-tax book income $1,000,000

Tax rate 40%

Expected tax expense $400,000

Tax related to permanent items 40,000

Total expected tax expense $440,000

Effective tax rate = 440,000/1,000,000 = 44%

(this is a short method of testing the rate)

26

SPECIFIC INCOME TAX ACCOUNTING ISSUES, BEST PRACTICES

Douglas Sayuk, Clifton Douglas

Cindy Frank, BDO USA

Jeffrey Zawada, FreedMaxick CPAs

VALUING AND REPORTING DEFERRED TAX ASSETS

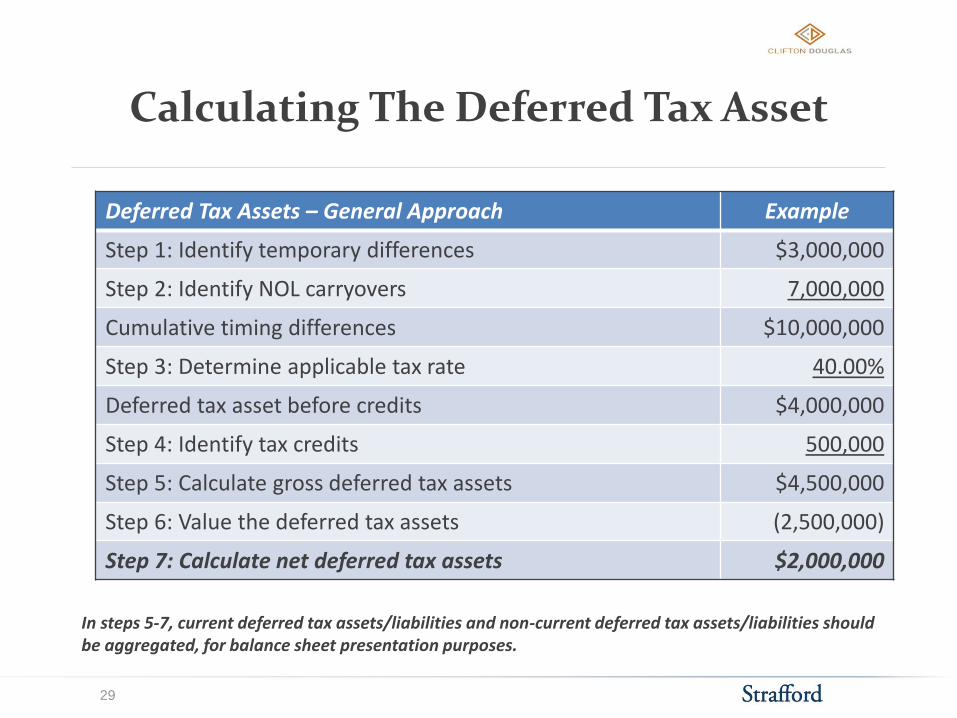

Calculating The Deferred Tax Asset

Deferred Tax Assets – General Approach Example

Step 1: Identify temporary differences $3,000,000

Step 2: Identify NOL carryovers 7,000,000

Cumulative timing differences $10,000,000

Step 3: Determine applicable tax rate 40.00%

Deferred tax asset before credits $4,000,000

Step 4: Identify tax credits 500,000

Step 5: Calculate gross deferred tax assets $4,500,000

Step 6: Value the deferred tax assets (2,500,000)

Step 7: Calculate net deferred tax assets $2,000,000

In steps 5-7, current deferred tax assets/liabilities and non-current deferred tax assets/liabilities should be aggregated, for balance sheet presentation purposes.

29

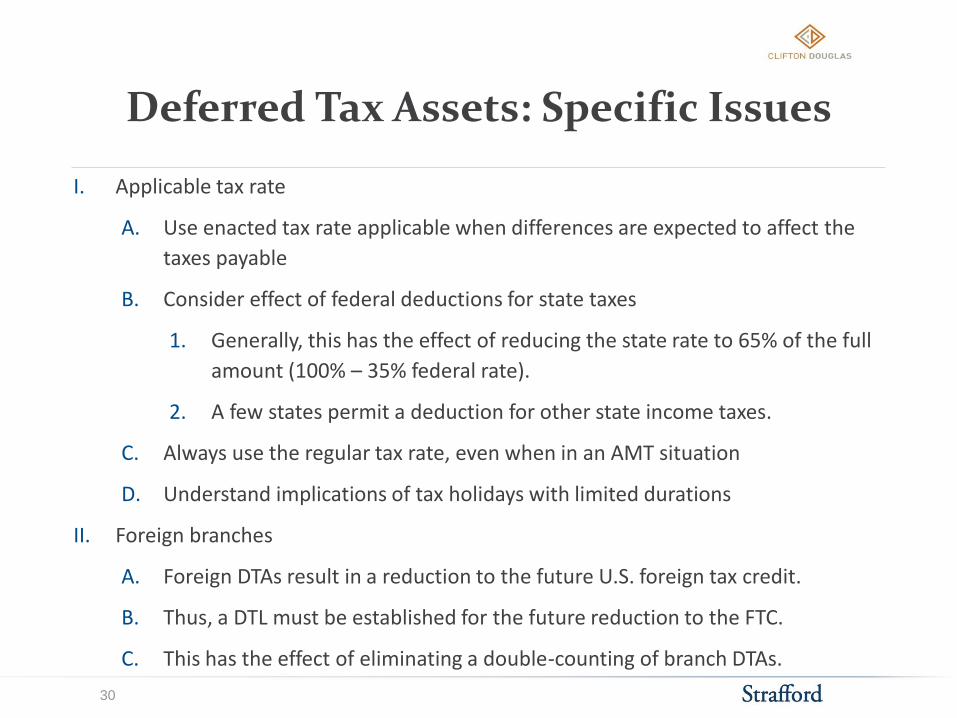

Deferred Tax Assets: Specific Issues

I. Applicable tax rate

A. Use enacted tax rate applicable when differences are expected to affect the

taxes payable

B. Consider effect of federal deductions for state taxes

1. Generally, this has the effect of reducing the state rate to 65% of the full

amount (100% – 35% federal rate).

2. A few states permit a deduction for other state income taxes.

C. Always use the regular tax rate, even when in an AMT situation

D. Understand implications of tax holidays with limited durations

II. Foreign branches

A. Foreign DTAs result in a reduction to the future U.S. foreign tax credit.

B. Thus, a DTL must be established for the future reduction to the FTC.

C. This has the effect of eliminating a double-counting of branch DTAs.

30

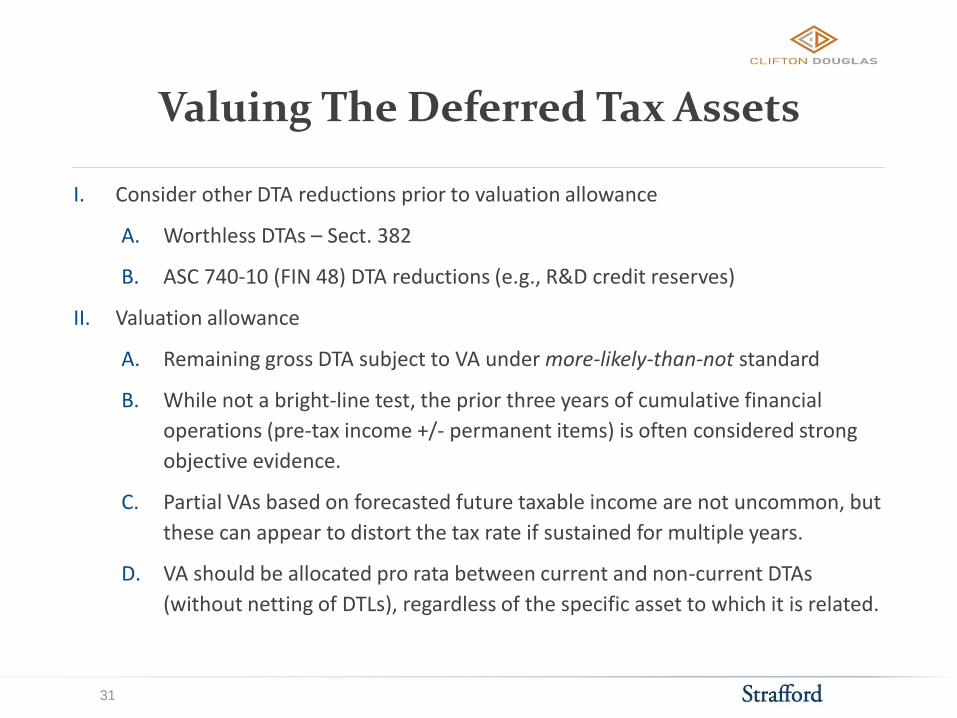

Valuing The Deferred Tax Assets

I. Consider other DTA reductions prior to valuation allowance

A. Worthless DTAs – Sect. 382

B. ASC 740-10 (FIN 48) DTA reductions (e.g., R&D credit reserves)

II. Valuation allowance

A. Remaining gross DTA subject to VA under more-likely-than-not standard

B. While not a bright-line test, the prior three years of cumulative financial

operations (pre-tax income +/- permanent items) is often considered strong

objective evidence.

C. Partial VAs based on forecasted future taxable income are not uncommon, but

these can appear to distort the tax rate if sustained for multiple years.

D. VA should be allocated pro rata between current and non-current DTAs

(without netting of DTLs), regardless of the specific asset to which it is related.

31

Slide Intentionally Left Blank

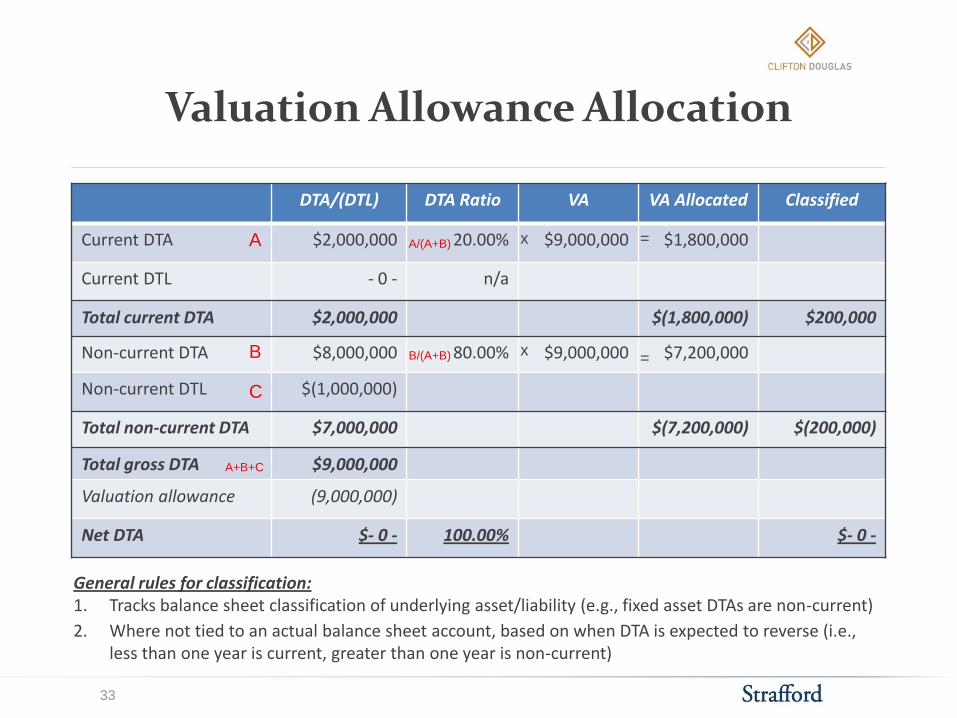

Valuation Allowance Allocation

DTA/(DTL) DTA Ratio VA VA Allocated Classified

Current DTA $2,000,000 20.00% $9,000,000 $1,800,000

Current DTL - 0 - n/a

Total current DTA $2,000,000 $(1,800,000) $200,000

Non-current DTA $8,000,000 80.00% $9,000,000 $7,200,000

Non-current DTL $(1,000,000)

Total non-current DTA $7,000,000 $(7,200,000) $(200,000)

Total gross DTA $9,000,000

Valuation allowance (9,000,000)

Net DTA $- 0 - 100.00% $- 0 -

A

B

A/(A+B)

B/(A+B)

C

A+B+C

x

x

=

=

General rules for classification: 1. Tracks balance sheet classification of underlying asset/liability (e.g., fixed asset DTAs are non-current)

2. Where not tied to an actual balance sheet account, based on when DTA is expected to reverse (i.e., less than one year is current, greater than one year is non-current)

33

DTA Movement Reconciliation: NOL Position

Gross Amount Applicable Rate DTA

Pre-tax book loss $(10,000,000) n/a

Perm differences 2,000,000 n/a

Temp differences 3,000,000 40.00% 1,200,000

Taxable loss $(5,000,000) -40.00% 2,000,000

Tax credits 500,000 100% 500,000

Change to DTA $3,700,000

Gross Amount Applicable Rate DTA

Pre-tax book loss $(10,000,000) -40.00% $4,000,000

Perm differences 2,000,000 -40.00% (800,000)

Tax credits 500,000 100% 500,000

Change to DTA $3,700,000

34

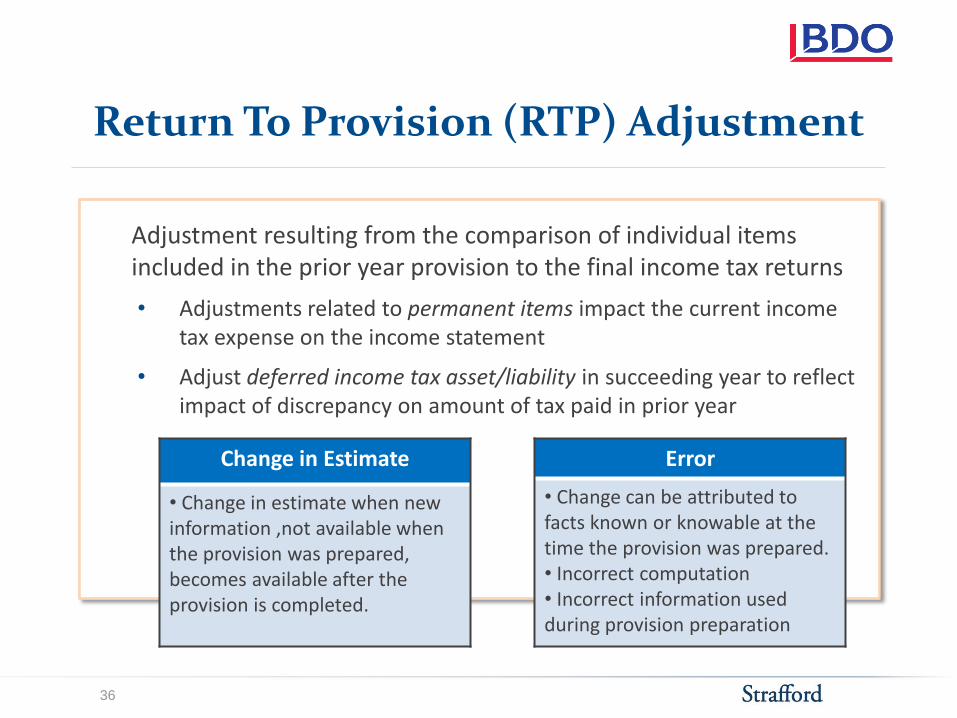

Return To Provision (RTP) Adjustment

• During the provision preparation, a comparison is performed to identify any differences between the numbers used in last year’s tax provision and the amounts used on the tax return.

• Generally computed during Q3

• The differences are “trued up” as part of the tax provision preparation process for the succeeding year.

35

Return To Provision (RTP) Adjustment

Adjustment resulting from the comparison of individual items included in the prior year provision to the final income tax returns

• Adjustments related to permanent items impact the current income tax expense on the income statement

• Adjust deferred income tax asset/liability in succeeding year to reflect impact of discrepancy on amount of tax paid in prior year

36

Change in Estimate

• Change in estimate when new information ,not available when the provision was prepared, becomes available after the provision is completed.

Error

• Change can be attributed to facts known or knowable at the time the provision was prepared. • Incorrect computation • Incorrect information used during provision preparation

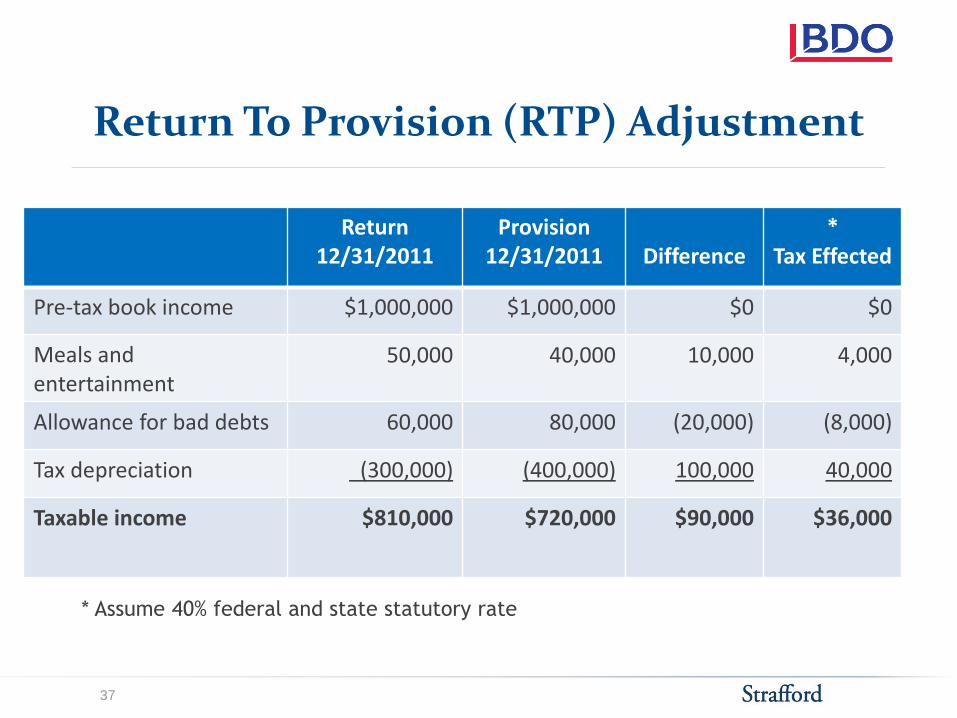

Return To Provision (RTP) Adjustment

37

Return 12/31/2011

Provision 12/31/2011

Difference

* Tax Effected

Pre-tax book income $1,000,000 $1,000,000 $0 $0

Meals and entertainment

50,000 40,000 10,000 4,000

Allowance for bad debts 60,000 80,000 (20,000) (8,000)

Tax depreciation (300,000) (400,000) 100,000 40,000

Taxable income $810,000 $720,000 $90,000 $36,000

* Assume 40% federal and state statutory rate

Return To Provision (RTP) Adjustment

38

Debit Credit

Current income tax expense $ 4,000

Deferred income tax expense 32,000

Income taxes payable $36,000

Entries to record tax provision true-up

ANALYZING AND REPORTING UNCERTAIN TAX POSITIONS

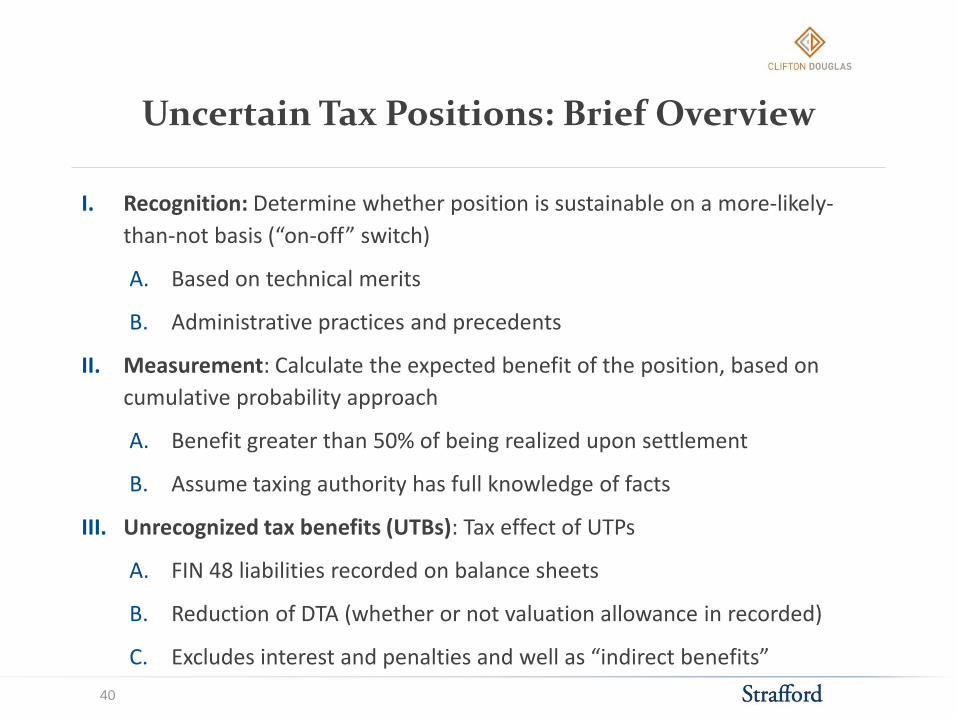

Uncertain Tax Positions: Brief Overview

I. Recognition: Determine whether position is sustainable on a more-likely-

than-not basis (“on-off” switch)

A. Based on technical merits

B. Administrative practices and precedents

II. Measurement: Calculate the expected benefit of the position, based on

cumulative probability approach

A. Benefit greater than 50% of being realized upon settlement

B. Assume taxing authority has full knowledge of facts

III. Unrecognized tax benefits (UTBs): Tax effect of UTPs

A. FIN 48 liabilities recorded on balance sheets

B. Reduction of DTA (whether or not valuation allowance in recorded)

C. Excludes interest and penalties and well as “indirect benefits”

40

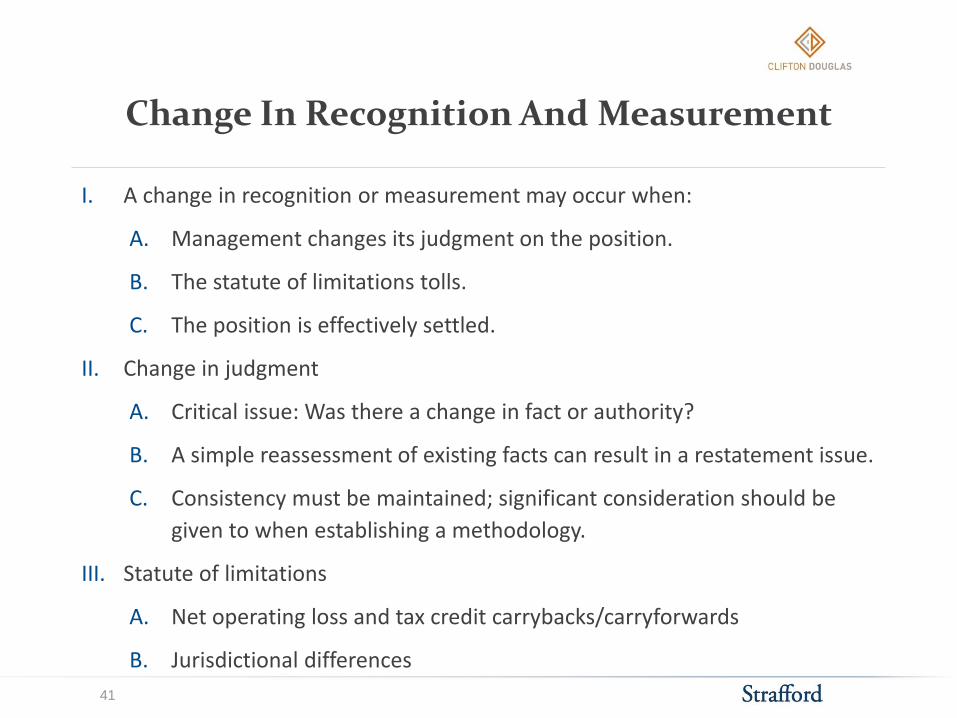

Change In Recognition And Measurement

I. A change in recognition or measurement may occur when:

A. Management changes its judgment on the position.

B. The statute of limitations tolls.

C. The position is effectively settled.

II. Change in judgment

A. Critical issue: Was there a change in fact or authority?

B. A simple reassessment of existing facts can result in a restatement issue.

C. Consistency must be maintained; significant consideration should be

given to when establishing a methodology.

III. Statute of limitations

A. Net operating loss and tax credit carrybacks/carryforwards

B. Jurisdictional differences

41

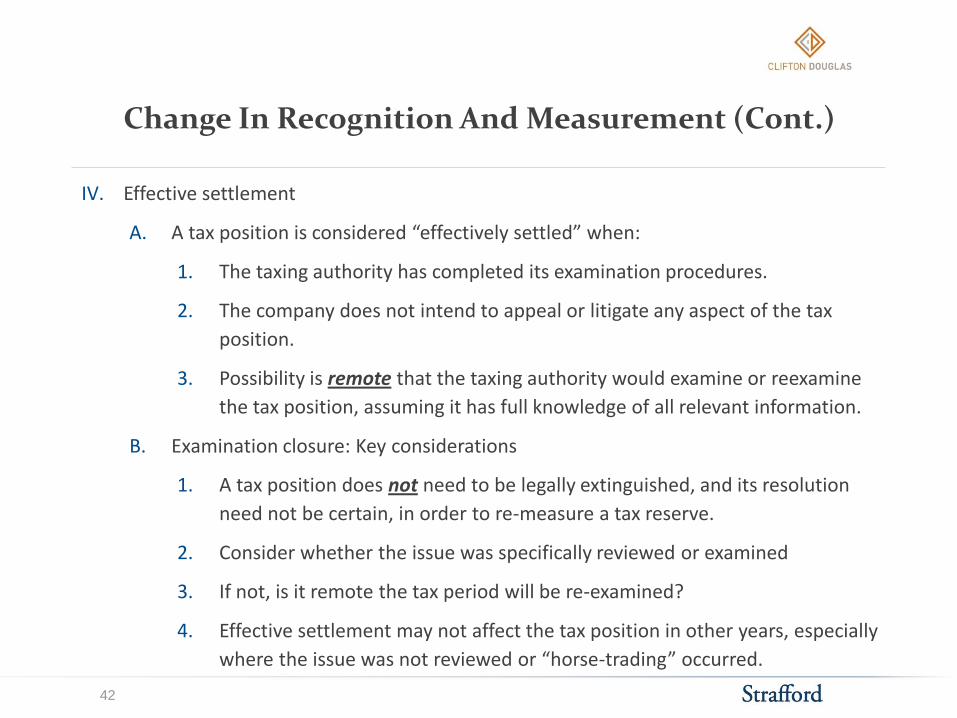

Change In Recognition And Measurement (Cont.)

IV. Effective settlement

A. A tax position is considered “effectively settled” when:

1. The taxing authority has completed its examination procedures.

2. The company does not intend to appeal or litigate any aspect of the tax

position.

3. Possibility is remote that the taxing authority would examine or reexamine

the tax position, assuming it has full knowledge of all relevant information.

B. Examination closure: Key considerations

1. A tax position does not need to be legally extinguished, and its resolution

need not be certain, in order to re-measure a tax reserve.

2. Consider whether the issue was specifically reviewed or examined

3. If not, is it remote the tax period will be re-examined?

4. Effective settlement may not affect the tax position in other years, especially

where the issue was not reviewed or “horse-trading” occurred.

42

Common Unrecognized Tax Benefits

I. Transfer pricing

A. Benefits and limitations of contemporaneous documentation

B. Potential indirect effects – competent authority and withholding taxes

II. State nexus/permanent establishment

A. Consider taxing authorities’ administrative policies and practices on SOL

B. Potential indirect effects – throwback and FTCs

III. Foreign withholding taxes

A. Who is liable? Joint vs. separate liability

B. Potential indirect effects – FTC (or deductions)

IV. R&D credits

V. Anti-deferral provisions (Subpart F, Sect. 956, etc.)

43

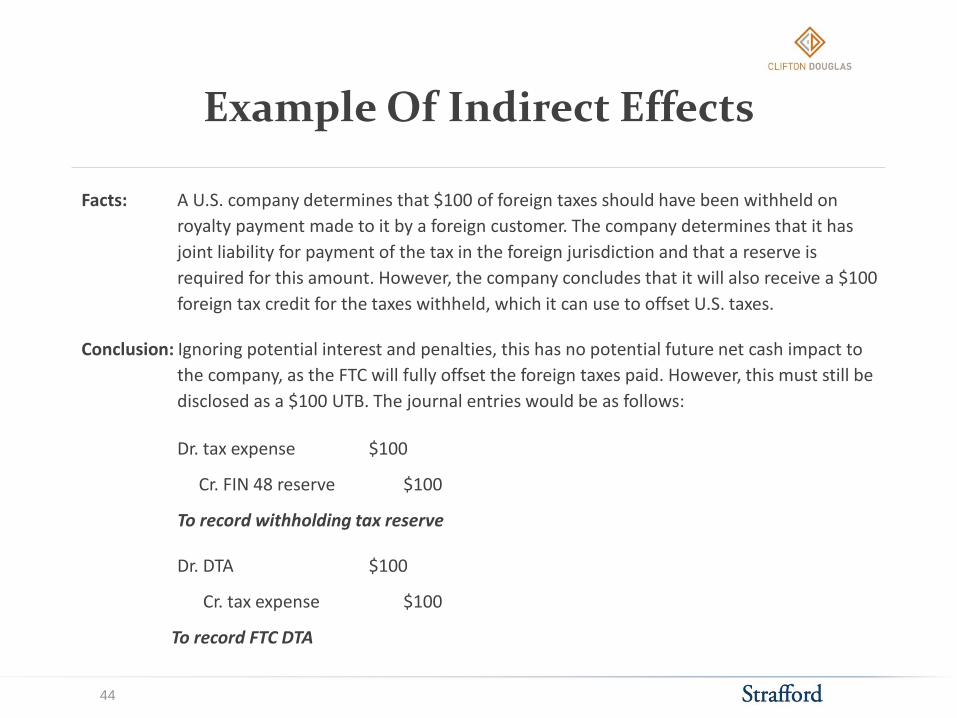

Example Of Indirect Effects

Facts: A U.S. company determines that $100 of foreign taxes should have been withheld on

royalty payment made to it by a foreign customer. The company determines that it has

joint liability for payment of the tax in the foreign jurisdiction and that a reserve is

required for this amount. However, the company concludes that it will also receive a $100

foreign tax credit for the taxes withheld, which it can use to offset U.S. taxes.

Conclusion: Ignoring potential interest and penalties, this has no potential future net cash impact to

the company, as the FTC will fully offset the foreign taxes paid. However, this must still be

disclosed as a $100 UTB. The journal entries would be as follows:

Dr. tax expense $100

Cr. FIN 48 reserve $100

To record withholding tax reserve

Dr. DTA $100

Cr. tax expense $100

To record FTC DTA

44

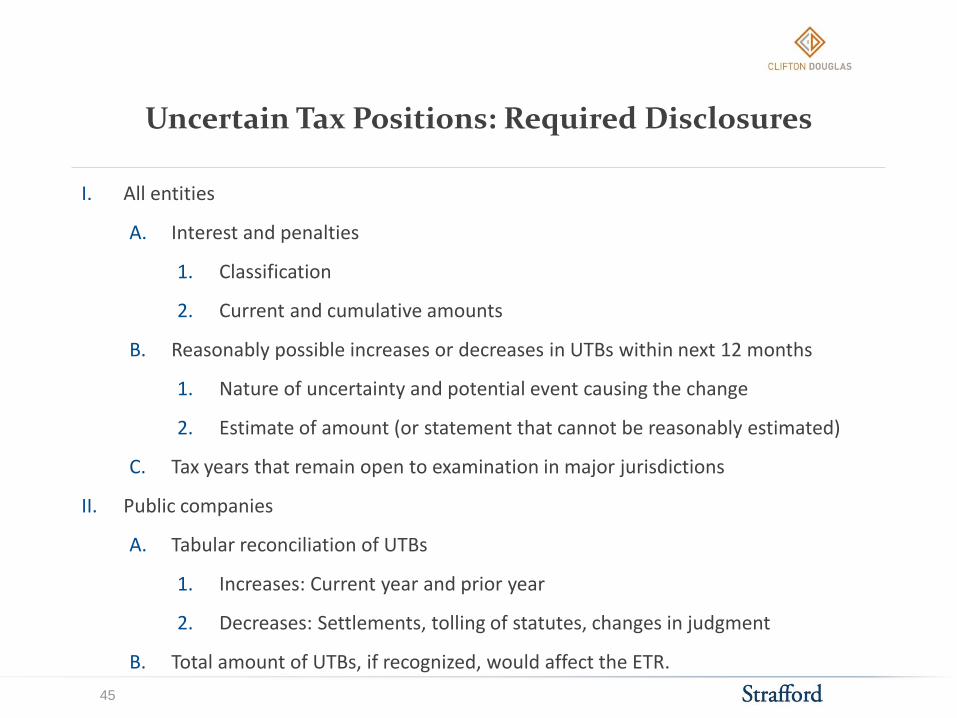

Uncertain Tax Positions: Required Disclosures

I. All entities

A. Interest and penalties

1. Classification

2. Current and cumulative amounts

B. Reasonably possible increases or decreases in UTBs within next 12 months

1. Nature of uncertainty and potential event causing the change

2. Estimate of amount (or statement that cannot be reasonably estimated)

C. Tax years that remain open to examination in major jurisdictions

II. Public companies

A. Tabular reconciliation of UTBs

1. Increases: Current year and prior year

2. Decreases: Settlements, tolling of statutes, changes in judgment

B. Total amount of UTBs, if recognized, would affect the ETR.

45

FINANCIAL STATEMENT DISCLOSURES: OVERVIEW, ISSUES AND SEC COMMENTS

Reported, Discussed And Disclosed

Reported amounts

• Balance sheet presentation

• Income statement presentation

• Statement of cash flows (SFAS No. 95)

• Changes in equity, net of taxes

47

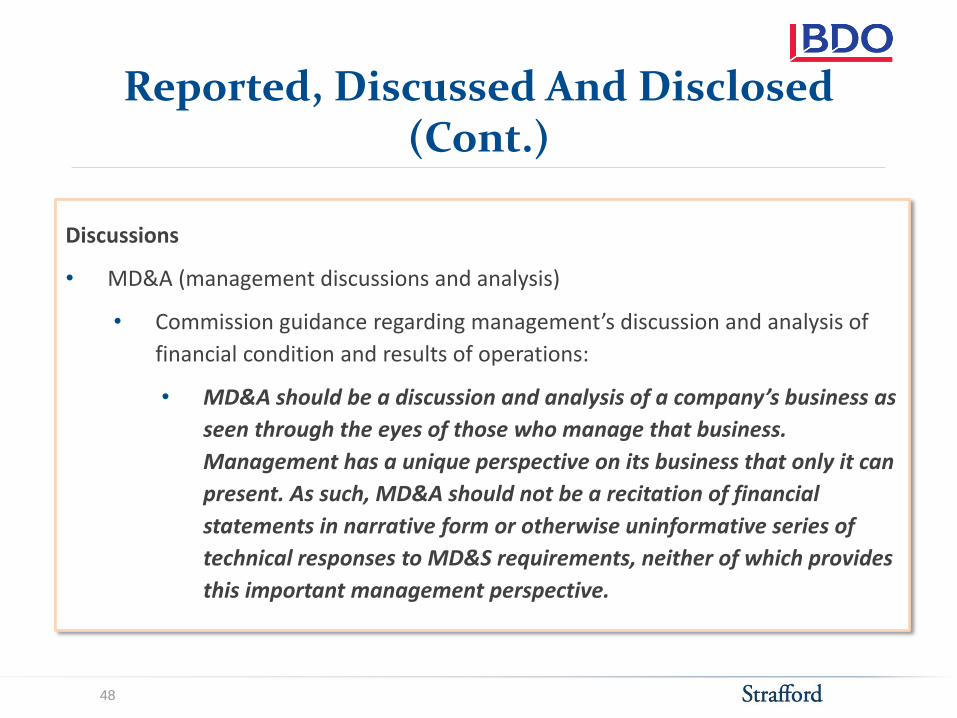

Reported, Discussed And Disclosed (Cont.)

Discussions

• MD&A (management discussions and analysis)

• Commission guidance regarding management’s discussion and analysis of

financial condition and results of operations:

• MD&A should be a discussion and analysis of a company’s business as

seen through the eyes of those who manage that business.

Management has a unique perspective on its business that only it can

present. As such, MD&A should not be a recitation of financial

statements in narrative form or otherwise uninformative series of

technical responses to MD&S requirements, neither of which provides

this important management perspective.

48

Reported, Discussed And Disclosed (Cont.)

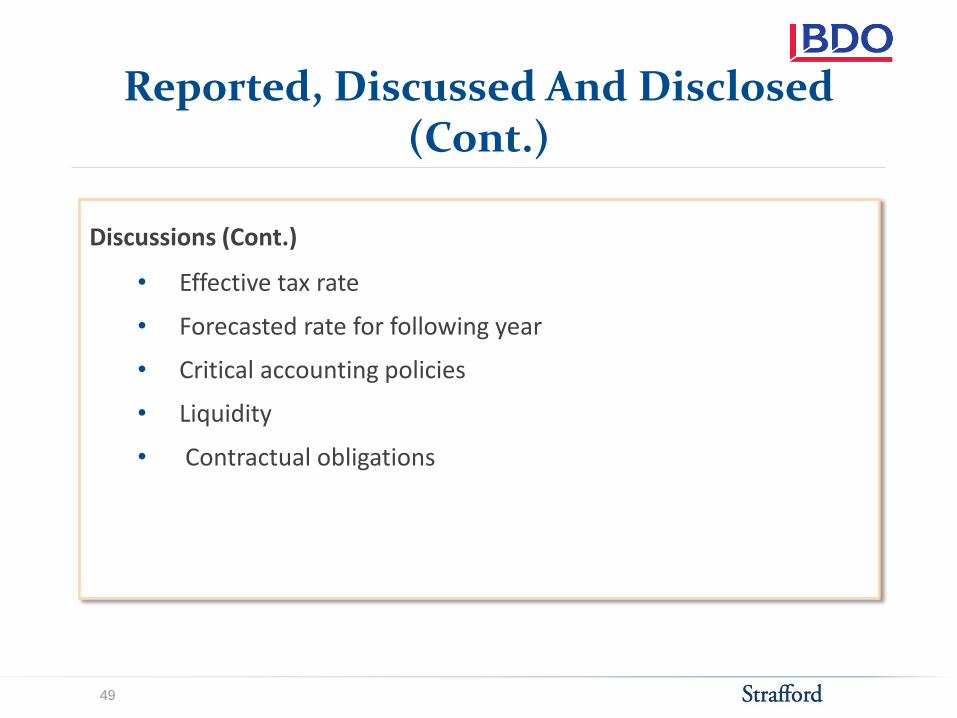

Discussions (Cont.)

• Effective tax rate

• Forecasted rate for following year

• Critical accounting policies

• Liquidity

• Contractual obligations

49

Reported, Discussed And Disclosed (Cont.)

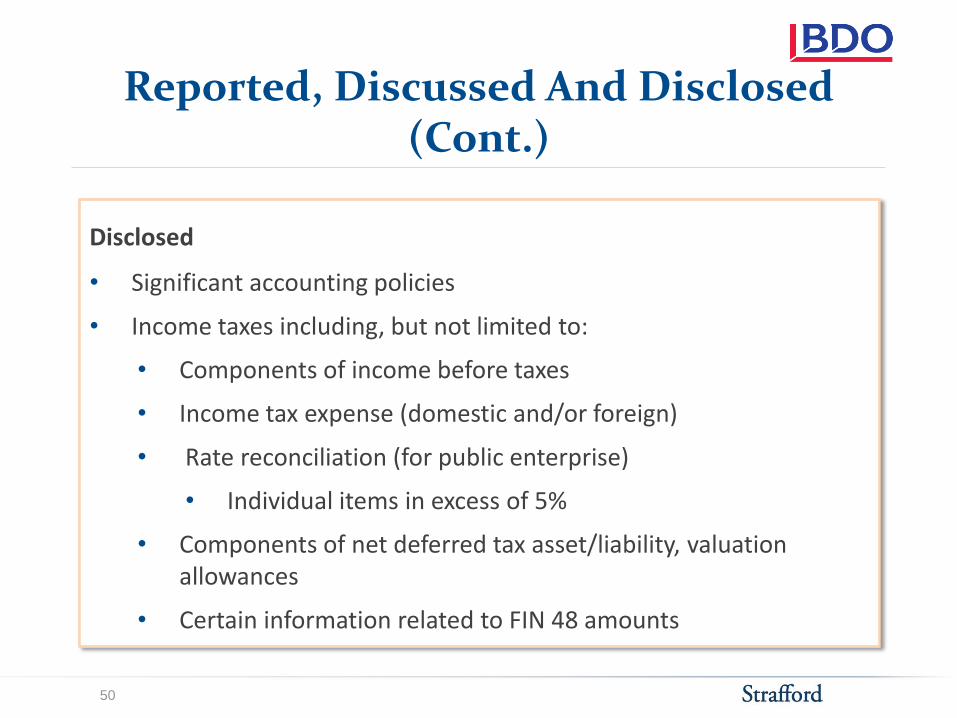

Disclosed

• Significant accounting policies

• Income taxes including, but not limited to:

• Components of income before taxes

• Income tax expense (domestic and/or foreign)

• Rate reconciliation (for public enterprise)

• Individual items in excess of 5%

• Components of net deferred tax asset/liability, valuation allowances

• Certain information related to FIN 48 amounts

50

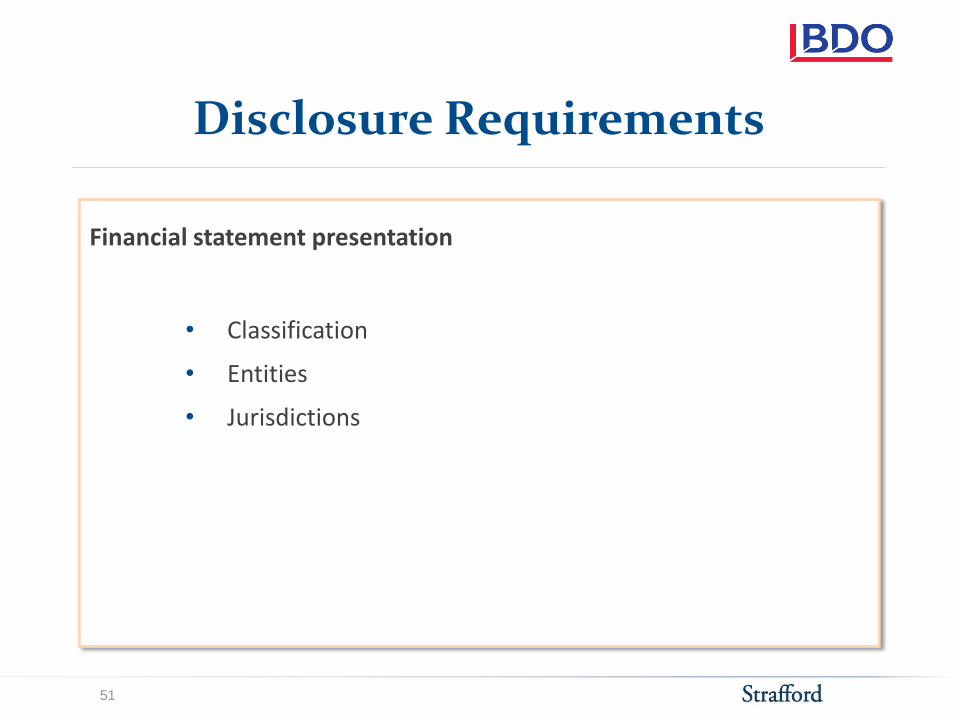

Disclosure Requirements

Financial statement presentation

• Classification

• Entities

• Jurisdictions

51

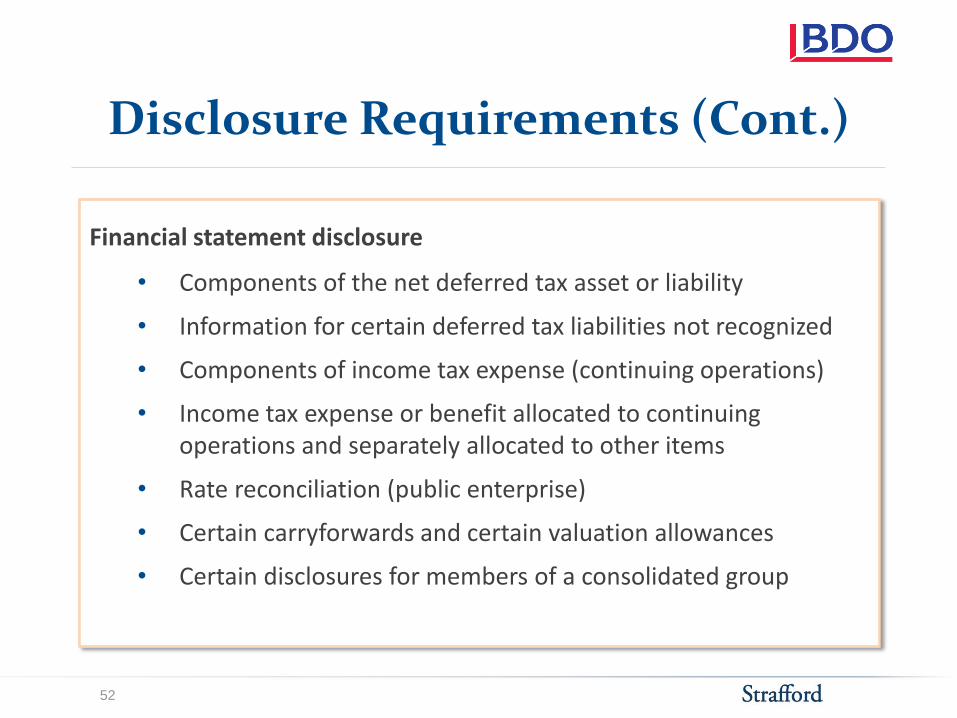

Disclosure Requirements (Cont.)

Financial statement disclosure

• Components of the net deferred tax asset or liability

• Information for certain deferred tax liabilities not recognized

• Components of income tax expense (continuing operations)

• Income tax expense or benefit allocated to continuing operations and separately allocated to other items

• Rate reconciliation (public enterprise)

• Certain carryforwards and certain valuation allowances

• Certain disclosures for members of a consolidated group

52

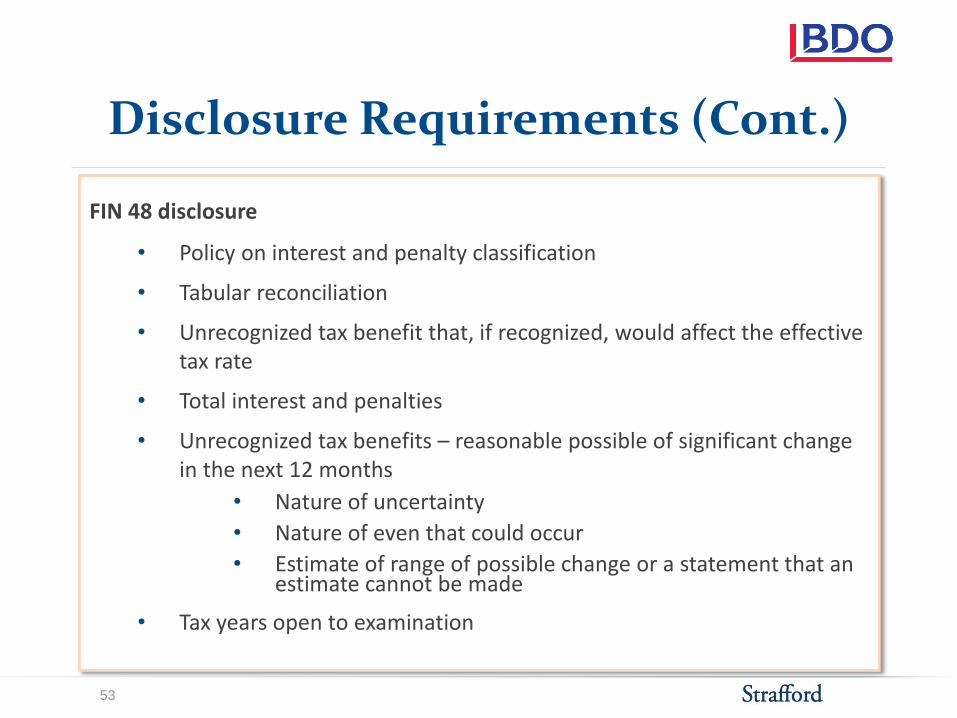

Disclosure Requirements (Cont.)

FIN 48 disclosure

• Policy on interest and penalty classification

• Tabular reconciliation

• Unrecognized tax benefit that, if recognized, would affect the effective tax rate

• Total interest and penalties

• Unrecognized tax benefits – reasonable possible of significant change in the next 12 months

• Nature of uncertainty

• Nature of even that could occur

• Estimate of range of possible change or a statement that an estimate cannot be made

• Tax years open to examination

53

Disclosure Requirements (Cont.)

What to remember:

• Understand the netting rules when it comes to current and non-current deferred tax assets and liabilities

• Understand how amounts are compiled and reported from different jurisdictions

• Significant accounting policies related to tax should be disclosed (SFAS 109, FIN 48, policies on interest and penalties).

• Components of income (from different jurisdictions)

• Components of expense (by jurisdiction, by classification)

• Rate reconciliation (dollars or percentages)

• Details for amounts > 5% of total for public companies

• Robust disclosures for estimates and changes in estimates (valuation allowances, uncertain tax positions)

54

SEC Comments: Areas Of Focus

Management estimates and judgments

• Valuation allowances

• Basis for having or not having a VA

• Timing of recording changes

• Consistency with other forward-looking information

• FIN 48-related items

• Paragraph 21 disclosures

• Interest and penalty policy disclosures

• Disclosures and adjustments on adoption

• Timing of recording changes

55

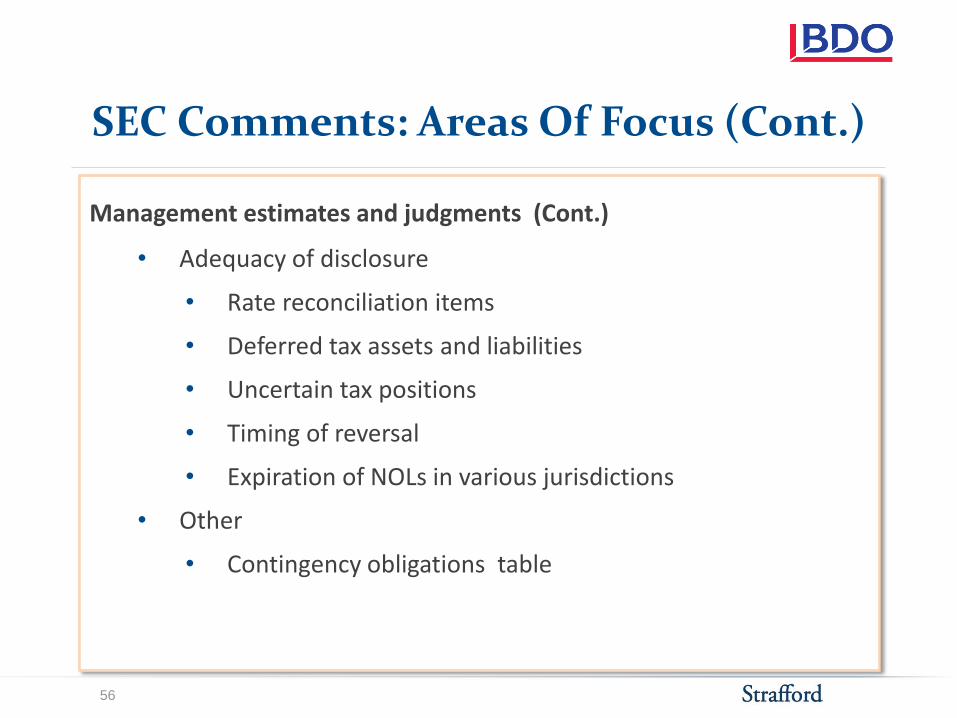

SEC Comments: Areas Of Focus (Cont.)

Management estimates and judgments (Cont.)

• Adequacy of disclosure

• Rate reconciliation items

• Deferred tax assets and liabilities

• Uncertain tax positions

• Timing of reversal

• Expiration of NOLs in various jurisdictions

• Other

• Contingency obligations table

56

SEC Comments: Areas Of Focus (Cont.)

What to remember – SEC Comments

• SEC may ask for clarification related to management’s material estimates and/or judgments.

• Changes in estimates should be well-documented.

• Responses to SEC comment letters are easier if the company has documentation related to:

• Alternative views considered • Company policies that provide guidance on estimates • Criteria used in evaluation

• Consider information that could be important to the user of the financial statements

57

Slide Intentionally Left Blank

DECIDING ON APPROPRIATE INTRA-PERIOD ALLOCATIONS

Intraperiod Tax Allocations

I. Income tax expense or benefit should be allocated among:

A. Continuing operations

B. Other components

1. Discontinued operations

2. Extraordinary items

3. Other comprehensive income

4. Items charged or credited directly to shareholders’ equity

II. Steps in allocation process

A. Step 1 - Calculate total tax expense

B. Step 2 - Determine tax related to continuing operations

C. Step 3 - Allocate remainder to other components (disc. ops, OCI, etc.)

60

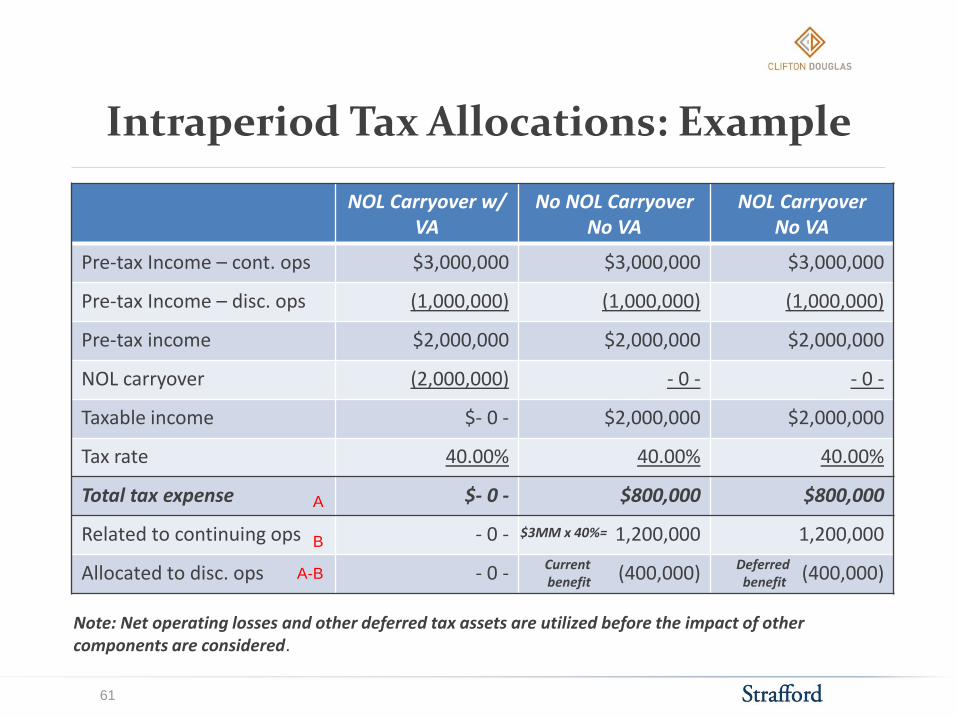

Intraperiod Tax Allocations: Example

NOL Carryover w/ VA

No NOL Carryover No VA

NOL Carryover No VA

Pre-tax Income – cont. ops $3,000,000 $3,000,000 $3,000,000

Pre-tax Income – disc. ops (1,000,000) (1,000,000) (1,000,000)

Pre-tax income $2,000,000 $2,000,000 $2,000,000

NOL carryover (2,000,000) - 0 - - 0 -

Taxable income $- 0 - $2,000,000 $2,000,000

Tax rate 40.00% 40.00% 40.00%

Total tax expense $- 0 - $800,000 $800,000

Related to continuing ops - 0 - 1,200,000 1,200,000

Allocated to disc. ops - 0 - (400,000) (400,000)

A

B

A-B

$3MM x 40%=

Note: Net operating losses and other deferred tax assets are utilized before the impact of other components are considered.

Deferred benefit

Current benefit

61

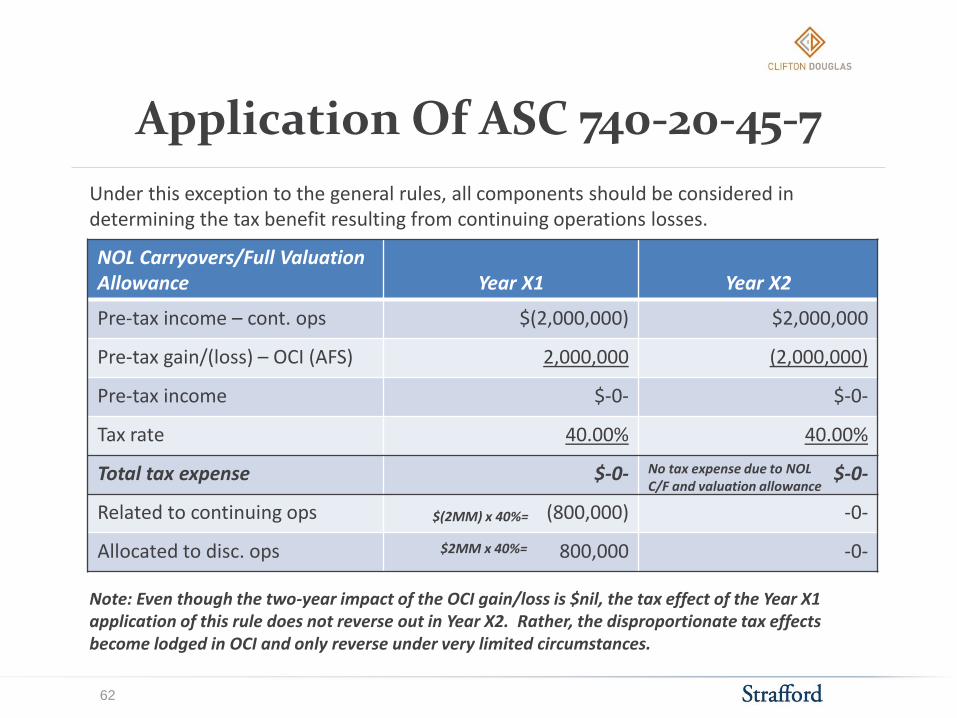

Application Of ASC 740-20-45-7

NOL Carryovers/Full Valuation Allowance

Year X1

Year X2

Pre-tax income – cont. ops $(2,000,000) $2,000,000

Pre-tax gain/(loss) – OCI (AFS) 2,000,000 (2,000,000)

Pre-tax income $-0- $-0-

Tax rate 40.00% 40.00%

Total tax expense $-0- $-0-

Related to continuing ops (800,000) -0-

Allocated to disc. ops 800,000 -0-

$(2MM) x 40%=

Note: Even though the two-year impact of the OCI gain/loss is $nil, the tax effect of the Year X1 application of this rule does not reverse out in Year X2. Rather, the disproportionate tax effects become lodged in OCI and only reverse under very limited circumstances.

Under this exception to the general rules, all components should be considered in determining the tax benefit resulting from continuing operations losses.

$2MM x 40%=

No tax expense due to NOL C/F and valuation allowance

62

INTERIM PERIOD TAX COMPUTATION CALCULATIONS

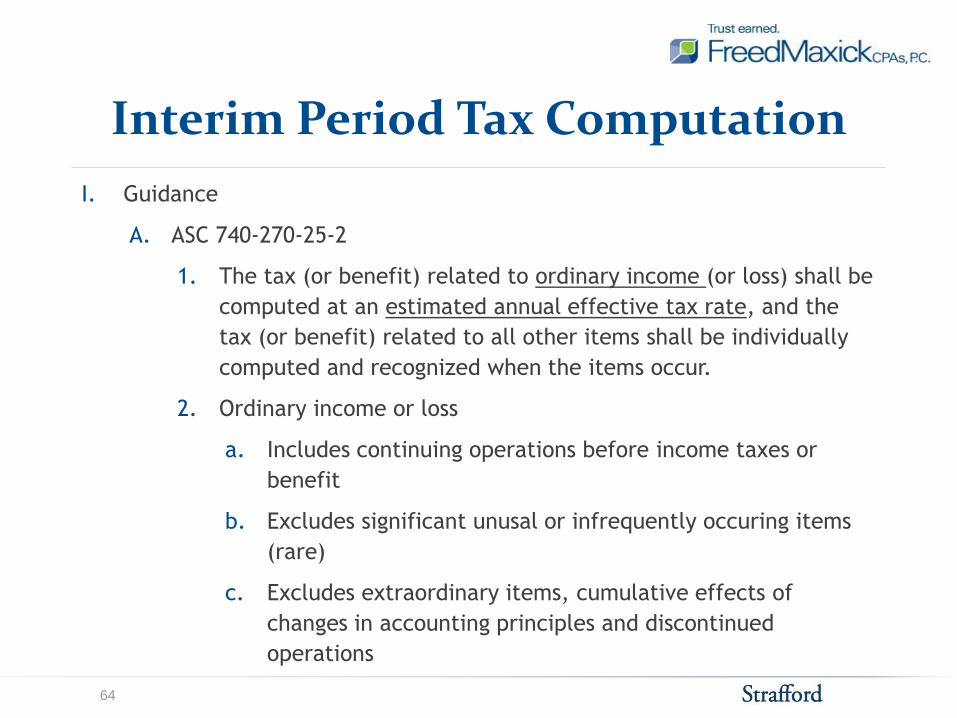

Interim Period Tax Computation

I. Guidance

A. ASC 740-270-25-2

1. The tax (or benefit) related to ordinary income (or loss) shall be

computed at an estimated annual effective tax rate, and the

tax (or benefit) related to all other items shall be individually

computed and recognized when the items occur.

2. Ordinary income or loss

a. Includes continuing operations before income taxes or

benefit

b. Excludes significant unusal or infrequently occuring items

(rare)

c. Excludes extraordinary items, cumulative effects of

changes in accounting principles and discontinued

operations

64

Interim Period Tax Computation (Cont.)

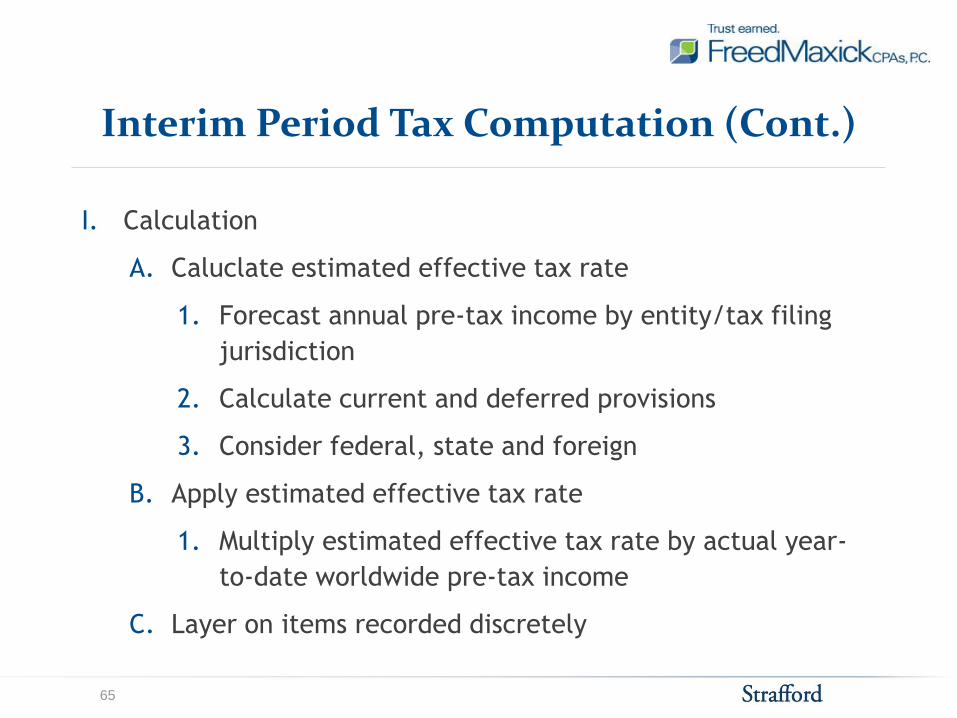

I. Calculation

A. Caluclate estimated effective tax rate

1. Forecast annual pre-tax income by entity/tax filing

jurisdiction

2. Calculate current and deferred provisions

3. Consider federal, state and foreign

B. Apply estimated effective tax rate

1. Multiply estimated effective tax rate by actual year-

to-date worldwide pre-tax income

C. Layer on items recorded discretely

65

Interim Period Tax Computation (Cont.)

I. Items recorded discretely in the interim period

A. Prior-year uncertain tax positions

B. Current-year uncertain tax positions related to income excluded

from the effective tax rate calculation

C. Interest and penalties related to uncertain tax positions

D. Change in tax law

E. Change in tax status

F. Changes in realizability of deferred tax assets

G. Changes in judgment regarding APB 23 items (unremitted earnings of

foreign subsidiaries and other outside basis items)

H. Changes in estimates from prior-year provisions (provision to return

adjustments)

66

Interim Period Tax Computation (Cont.)

I. Modification to estimated effective tax rate approach (ASC 740-270-

30-30 through ASC 740-270-30-34)

A. Loss limitation (year-to-date loss exceeds the full-year expected

loss, and full realization of tax benefit is assured, i.e. no need

for a valuation allowance)

A. Recalculate tax based on year-to-date results

B. Good example: ASC 740-270-55-16

B. Loss limitation (year-to-date loss exceeds the full year expected

loss, and partial realization of tax benefit is assured)

A. Calculate estimated effective tax rate based on amount of

tax benefit assured

B. Recalculate tax based on year-to-date results

C. Good example: ASC 740-270-55-20

67

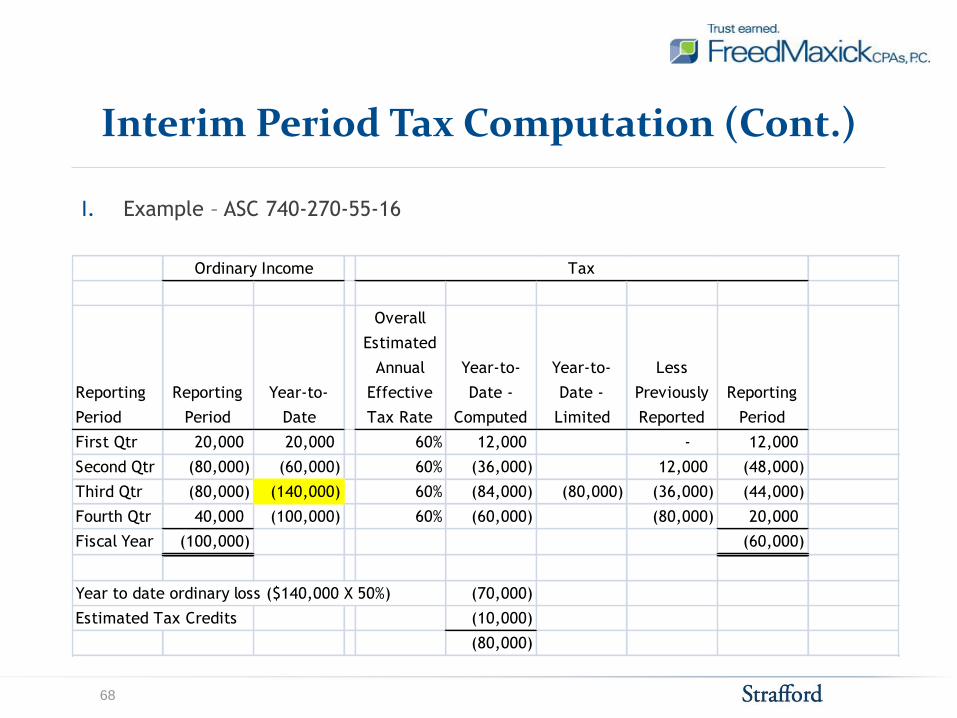

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-16

Reporting

Period

Reporting

Period

Year-to-

Date

Overall

Estimated

Annual

Effective

Tax Rate

Year-to-

Date -

Computed

Year-to-

Date -

Limited

Less

Previously

Reported

Reporting

Period

First Qtr 20,000 20,000 60% 12,000 - 12,000

Second Qtr (80,000) (60,000) 60% (36,000) 12,000 (48,000)

Third Qtr (80,000) (140,000) 60% (84,000) (80,000) (36,000) (44,000)

Fourth Qtr 40,000 (100,000) 60% (60,000) (80,000) 20,000

Fiscal Year (100,000) (60,000)

Year to date ordinary loss ($140,000 X 50%) (70,000)

Estimated Tax Credits (10,000)

(80,000)

Ordinary Income Tax

68

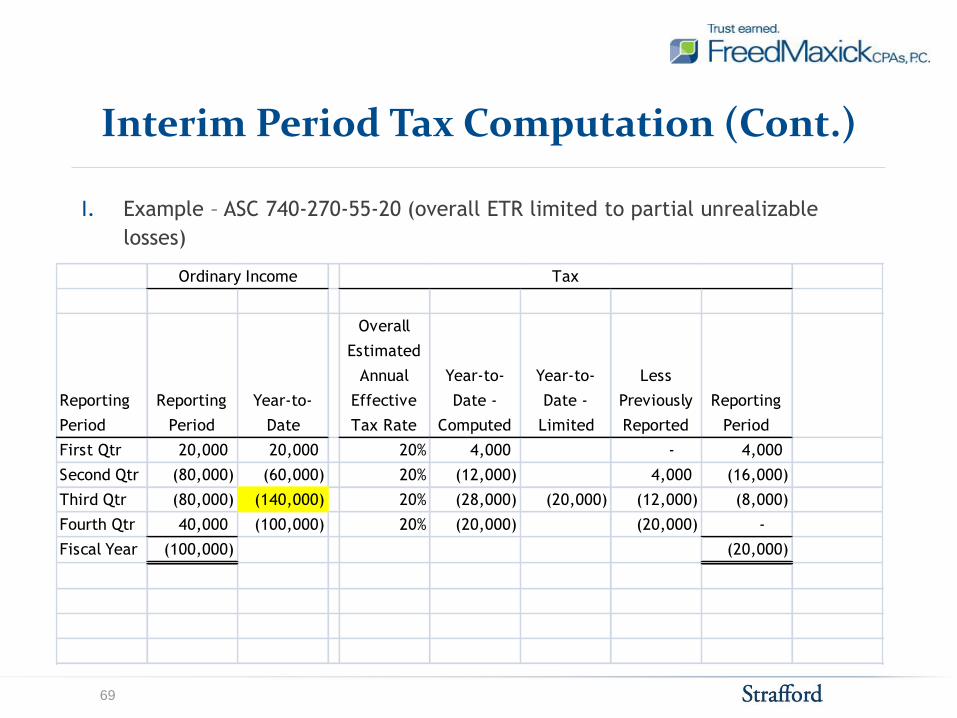

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-20 (overall ETR limited to partial unrealizable

losses)

Reporting

Period

Reporting

Period

Year-to-

Date

Overall

Estimated

Annual

Effective

Tax Rate

Year-to-

Date -

Computed

Year-to-

Date -

Limited

Less

Previously

Reported

Reporting

Period

First Qtr 20,000 20,000 20% 4,000 - 4,000

Second Qtr (80,000) (60,000) 20% (12,000) 4,000 (16,000)

Third Qtr (80,000) (140,000) 20% (28,000) (20,000) (12,000) (8,000)

Fourth Qtr 40,000 (100,000) 20% (20,000) (20,000) -

Fiscal Year (100,000) (20,000)

Ordinary Income Tax

69

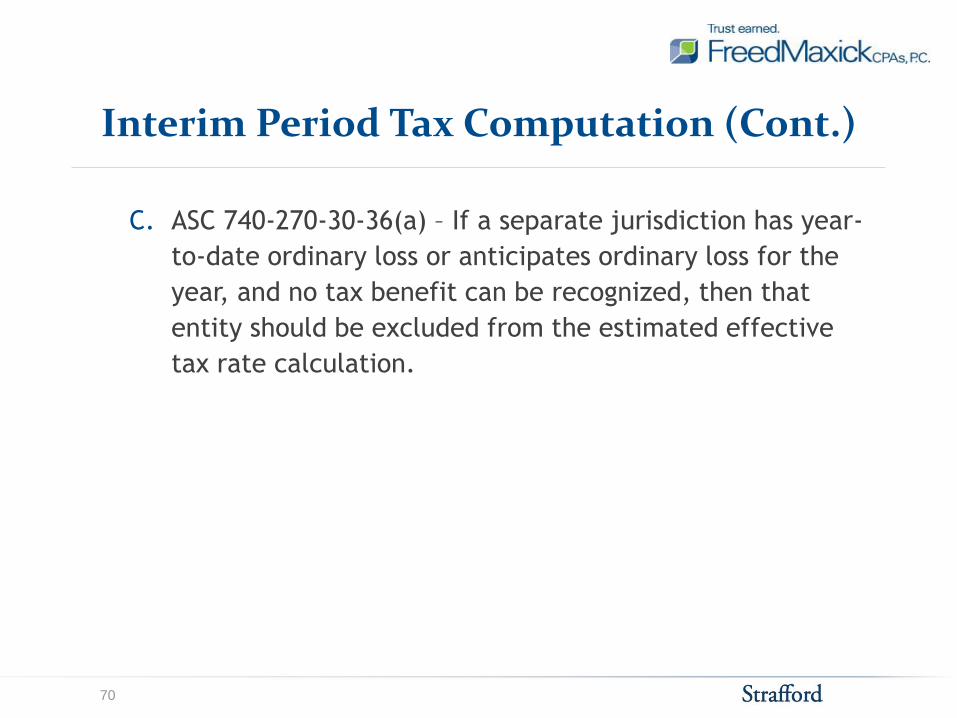

Interim Period Tax Computation (Cont.)

C. ASC 740-270-30-36(a) – If a separate jurisdiction has year-

to-date ordinary loss or anticipates ordinary loss for the

year, and no tax benefit can be recognized, then that

entity should be excluded from the estimated effective

tax rate calculation.

70

Interim Period Tax Computation (Cont.)

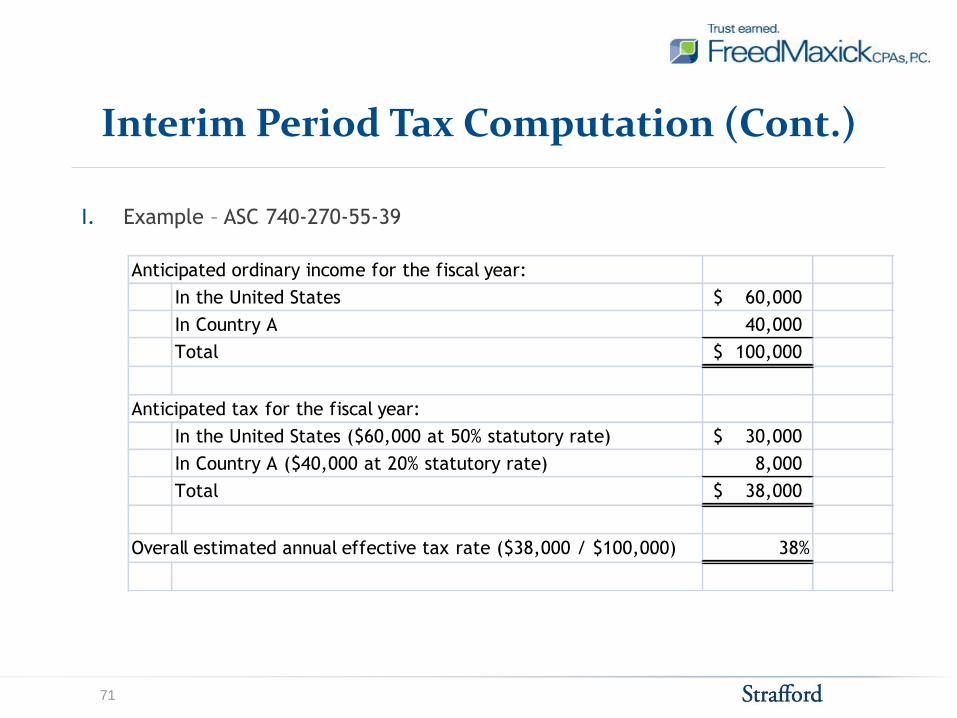

I. Example – ASC 740-270-55-39

Anticipated ordinary income for the fiscal year:

In the United States 60,000$

In Country A 40,000

Total 100,000$

Anticipated tax for the fiscal year:

In the United States ($60,000 at 50% statutory rate) 30,000$

In Country A ($40,000 at 20% statutory rate) 8,000

Total 38,000$

Overall estimated annual effective tax rate ($38,000 / $100,000) 38%

71

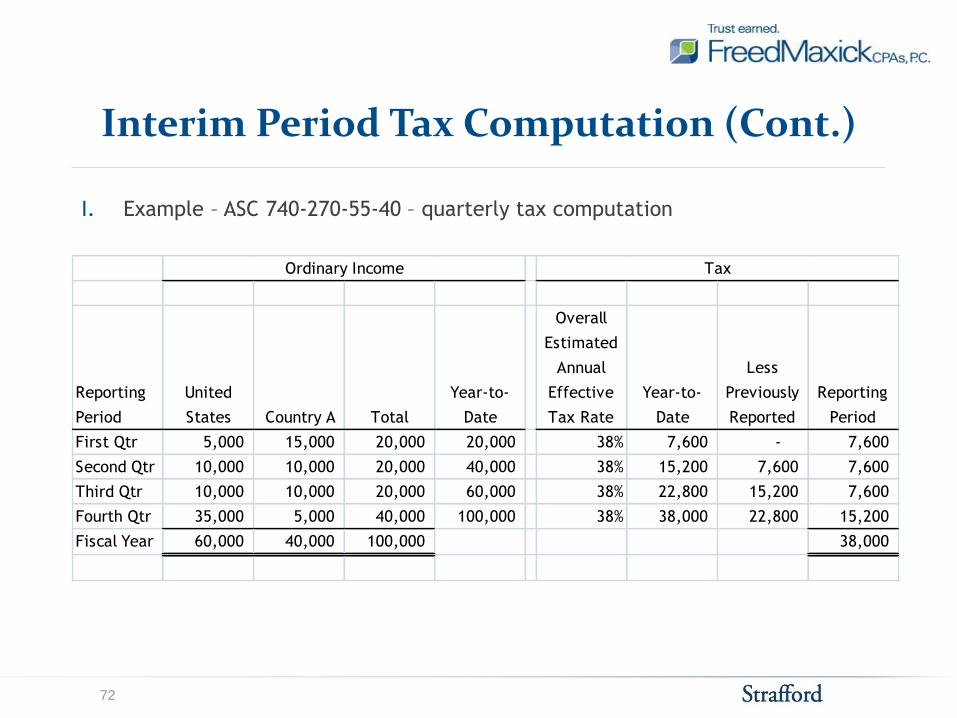

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-40 – quarterly tax computation

Reporting

Period

United

States Country A Total

Year-to-

Date

Overall

Estimated

Annual

Effective

Tax Rate

Year-to-

Date

Less

Previously

Reported

Reporting

Period

First Qtr 5,000 15,000 20,000 20,000 38% 7,600 - 7,600

Second Qtr 10,000 10,000 20,000 40,000 38% 15,200 7,600 7,600

Third Qtr 10,000 10,000 20,000 60,000 38% 22,800 15,200 7,600

Fourth Qtr 35,000 5,000 40,000 100,000 38% 38,000 22,800 15,200

Fiscal Year 60,000 40,000 100,000 38,000

Ordinary Income Tax

72

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-41 – ordinary loss; realization not MLTN

I. Country B history of losses, 40% rate, expected tax benefit will not be

realized on these losses

Reporting

Period

United

States Country A Country B Total

Year-to-

Date

Overall

Estimated

Annual

Effective

Tax Rate

Year-to-

Date -

Excluding

Country B

Less

Previously

Reported

Reporting

Period

First Qtr 5,000 15,000 (5,000) 15,000 15,000 38% 7,600 - 7,600

Second Qtr 10,000 10,000 (25,000) (5,000) 10,000 38% 15,200 7,600 7,600

Third Qtr 10,000 10,000 (5,000) 15,000 25,000 38% 22,800 15,200 7,600

Fourth Qtr 35,000 5,000 (5,000) 35,000 60,000 38% 38,000 22,800 15,200

Fiscal Year 60,000 40,000 (40,000) 60,000 38,000

Note: Format above different than actual ASC 740-270-55-41 example

Ordinary Income Tax

73

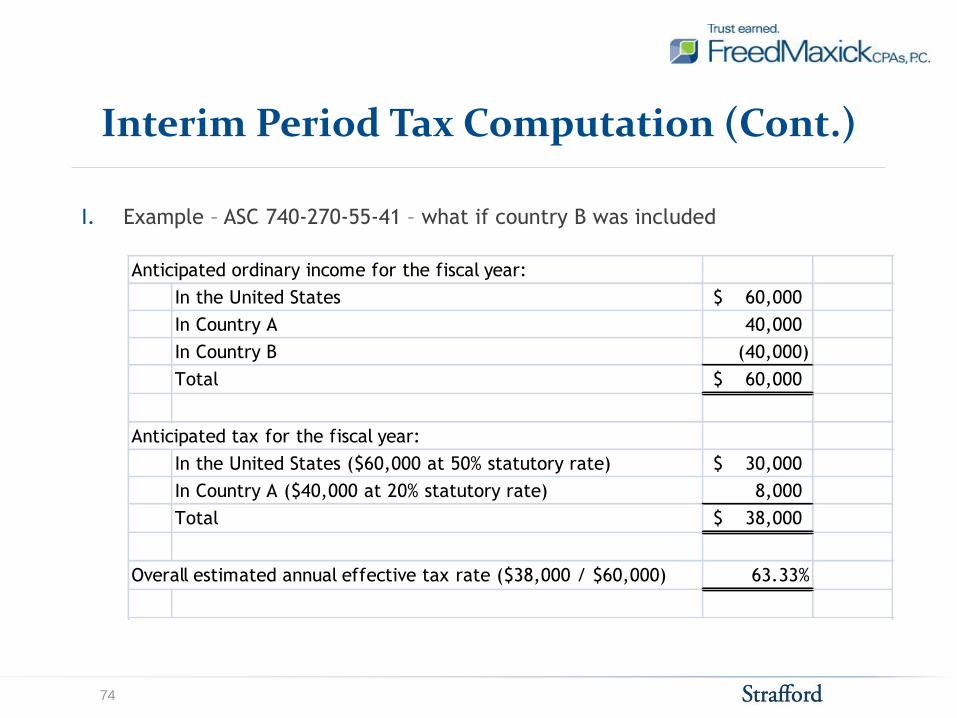

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-41 – what if country B was included

Anticipated ordinary income for the fiscal year:

In the United States 60,000$

In Country A 40,000

In Country B (40,000)

Total 60,000$

Anticipated tax for the fiscal year:

In the United States ($60,000 at 50% statutory rate) 30,000$

In Country A ($40,000 at 20% statutory rate) 8,000

Total 38,000$

Overall estimated annual effective tax rate ($38,000 / $60,000) 63.33%

74

Interim Period Tax Computation (Cont.)

I. Example – ASC 740-270-55-41 – what if country B was included (Cont.)

I. Country B history of losses, 40% rate, expected tax benefit will not be

realized on these losses

Reporting

Period

United

States Country A Country B Total

Year-to-

Date

Overall

Estimated

Annual

Effective

Tax Rate

Year-to-

Date -

Including

Country B

Less

Previously

Reported

Reporting

Period

First Qtr 5,000 15,000 (5,000) 15,000 15,000 63.33% 9,500 - 9,500

Second Qtr 10,000 10,000 (25,000) (5,000) 10,000 63.33% 6,333 9,500 (3,167)

Third Qtr 10,000 10,000 (5,000) 15,000 25,000 63.33% 15,833 6,333 9,500

Fourth Qtr 35,000 5,000 (5,000) 35,000 60,000 63.33% 37,998 15,833 22,166

Fiscal Year 60,000 40,000 (40,000) 60,000 37,998

Note: Format above different than actual ASC 740-270-55-41 example

Ordinary Income Tax

75

Slide Intentionally Left Blank

MERGER AND ACQUISITION TOPICS

Business Combinations: Key Steps

Step 1: Determine transaction structure (stock vs. asset acquisition)

• Stock – historical tax basis carryover; can lead to significant DTA/DTLs

• Asset – tax basis stepped up to FMV; DTA/DTL may be minimal

Step 2: Identify existing deferred tax assets and liabilities

• Typically, a short period cut-off provision is calculated.

• Consider the impact of stock awards and other non-recurring charges.

• When combined returns will be filed with the acquirer, the applicable tax rate in valuing DTA/DTLs should be reassessed.

Step 3: Calculate DTA/DTL from purchase accounting fair value adjustments

• In a stock transaction, every FV adjustment will result in a DTA/DTL. Non-goodwill intangibles often result in a significant DTL.

• Consider the impact of an acquired DTL on the acquirer’s VA, as the benefit of any release will be recorded to P&L.

78

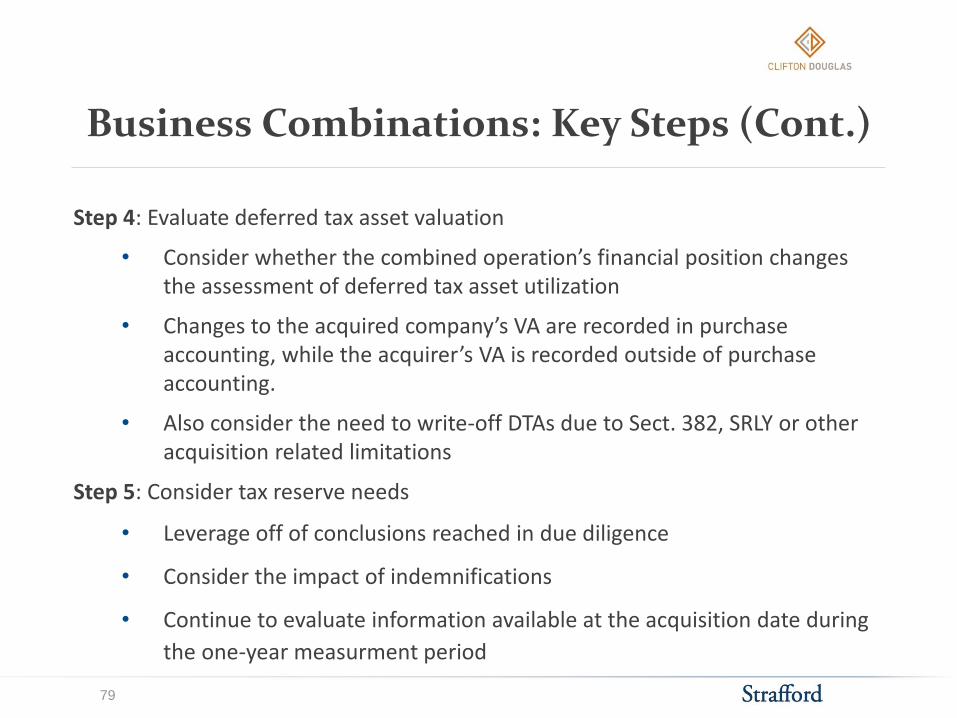

Business Combinations: Key Steps (Cont.)

Step 4: Evaluate deferred tax asset valuation

• Consider whether the combined operation’s financial position changes the assessment of deferred tax asset utilization

• Changes to the acquired company’s VA are recorded in purchase accounting, while the acquirer’s VA is recorded outside of purchase accounting.

• Also consider the need to write-off DTAs due to Sect. 382, SRLY or other acquisition related limitations

Step 5: Consider tax reserve needs

• Leverage off of conclusions reached in due diligence

• Consider the impact of indemnifications

• Continue to evaluate information available at the acquisition date during

the one-year measurment period

79

STOCK AWARD ISSUES

Stock Awards

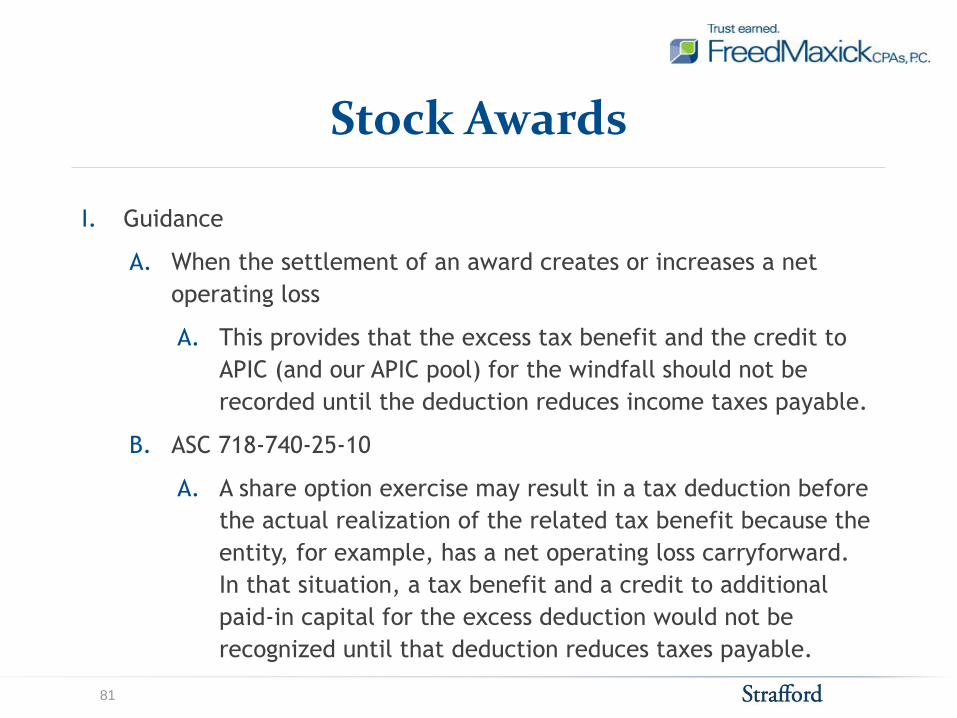

I. Guidance

A. When the settlement of an award creates or increases a net

operating loss

A. This provides that the excess tax benefit and the credit to

APIC (and our APIC pool) for the windfall should not be

recorded until the deduction reduces income taxes payable.

B. ASC 718-740-25-10

A. A share option exercise may result in a tax deduction before

the actual realization of the related tax benefit because the

entity, for example, has a net operating loss carryforward.

In that situation, a tax benefit and a credit to additional

paid-in capital for the excess deduction would not be

recognized until that deduction reduces taxes payable.

81

Stock Awards (Cont.)

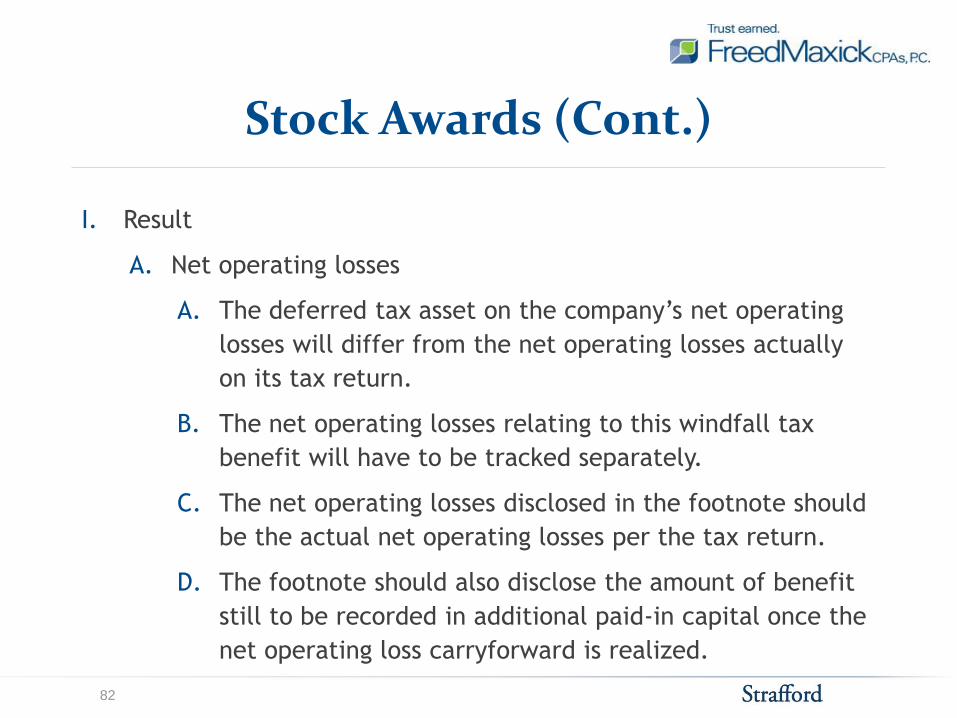

I. Result

A. Net operating losses

A. The deferred tax asset on the company’s net operating

losses will differ from the net operating losses actually

on its tax return.

B. The net operating losses relating to this windfall tax

benefit will have to be tracked separately.

C. The net operating losses disclosed in the footnote should

be the actual net operating losses per the tax return.

D. The footnote should also disclose the amount of benefit

still to be recorded in additional paid-in capital once the

net operating loss carryforward is realized.

82

Stock Awards (Cont.)

I. Accounting policy

A. Generally two approaches allowed:

A. With and without – results in windfall tax benefits

being realized last

B. Tax law ordering – results in windfall tax benefit being

realized first (should be less complex)

B. Election of method is an accounting policy that must be

applied consistently.

83

Stock Awards (Cont.)

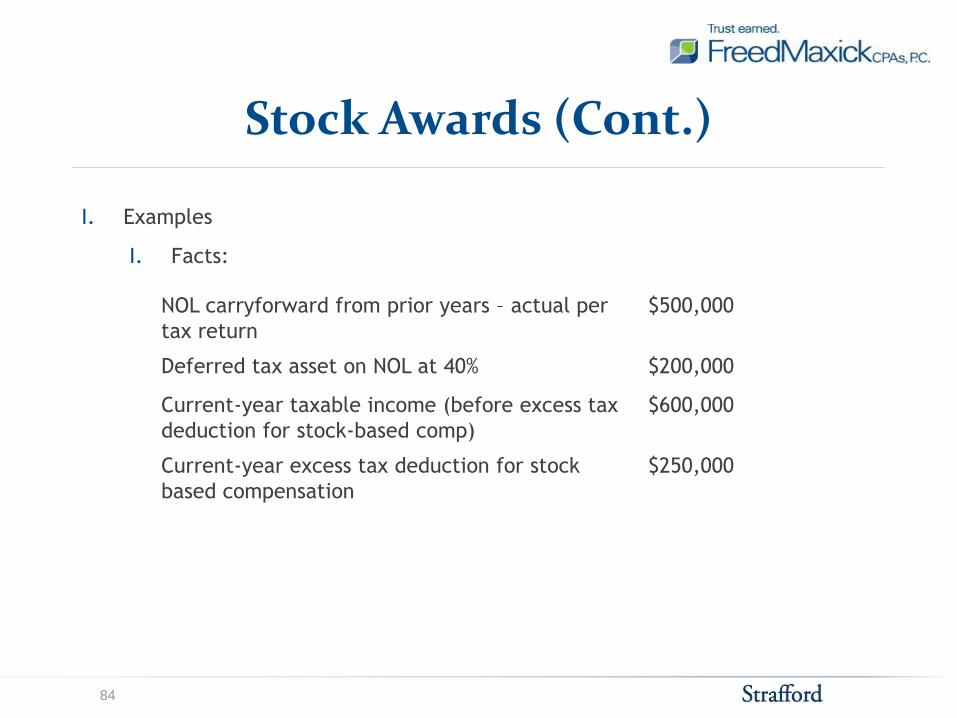

I. Examples

I. Facts:

NOL carryforward from prior years – actual per

tax return

$500,000

Deferred tax asset on NOL at 40% $200,000

Current-year taxable income (before excess tax

deduction for stock-based comp)

$600,000

Current-year excess tax deduction for stock

based compensation

$250,000

84

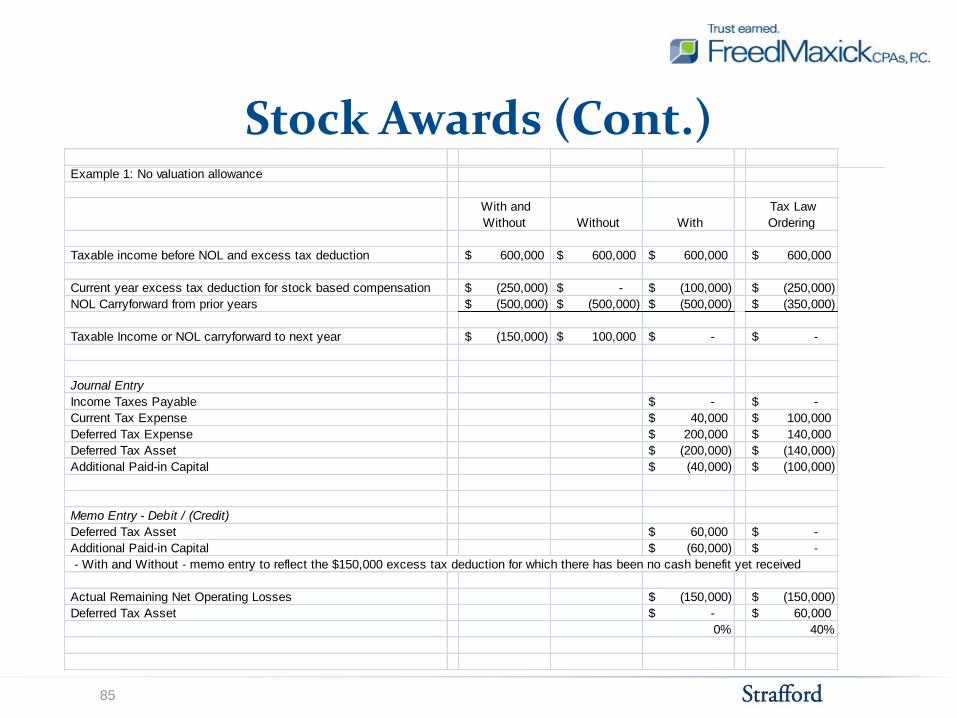

Stock Awards (Cont.) Example 1: No valuation allowance

With and

Without Without With

Tax Law

Ordering

Taxable income before NOL and excess tax deduction 600,000$ 600,000$ 600,000$ 600,000$

Current year excess tax deduction for stock based compensation (250,000)$ -$ (100,000)$ (250,000)$

NOL Carryforward from prior years (500,000)$ (500,000)$ (500,000)$ (350,000)$

Taxable Income or NOL carryforward to next year (150,000)$ 100,000$ -$ -$

Journal Entry

Income Taxes Payable -$ -$

Current Tax Expense 40,000$ 100,000$

Deferred Tax Expense 200,000$ 140,000$

Deferred Tax Asset (200,000)$ (140,000)$

Additional Paid-in Capital (40,000)$ (100,000)$

Memo Entry - Debit / (Credit)

Deferred Tax Asset 60,000$ -$

Additional Paid-in Capital (60,000)$ -$

- With and Without - memo entry to reflect the $150,000 excess tax deduction for which there has been no cash benefit yet received

Actual Remaining Net Operating Losses (150,000)$ (150,000)$

Deferred Tax Asset -$ 60,000$

0% 40%

85

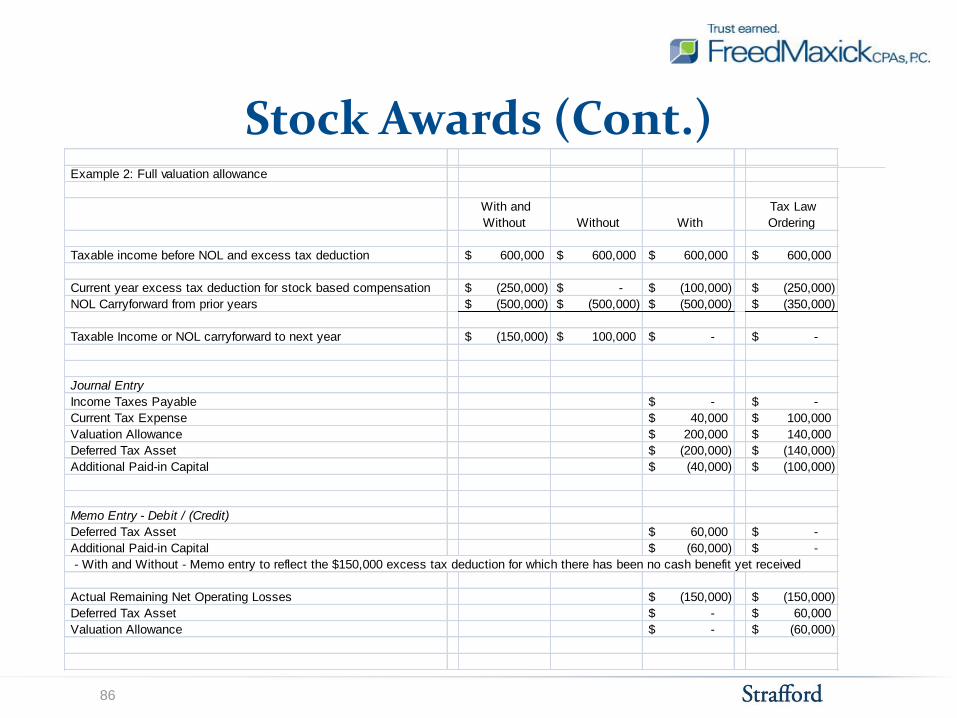

Stock Awards (Cont.) Example 2: Full valuation allowance

With and

Without Without With

Tax Law

Ordering

Taxable income before NOL and excess tax deduction 600,000$ 600,000$ 600,000$ 600,000$

Current year excess tax deduction for stock based compensation (250,000)$ -$ (100,000)$ (250,000)$

NOL Carryforward from prior years (500,000)$ (500,000)$ (500,000)$ (350,000)$

Taxable Income or NOL carryforward to next year (150,000)$ 100,000$ -$ -$

Journal Entry

Income Taxes Payable -$ -$

Current Tax Expense 40,000$ 100,000$

Valuation Allowance 200,000$ 140,000$

Deferred Tax Asset (200,000)$ (140,000)$

Additional Paid-in Capital (40,000)$ (100,000)$

Memo Entry - Debit / (Credit)

Deferred Tax Asset 60,000$ -$

Additional Paid-in Capital (60,000)$ -$

- With and Without - Memo entry to reflect the $150,000 excess tax deduction for which there has been no cash benefit yet received

Actual Remaining Net Operating Losses (150,000)$ (150,000)$

Deferred Tax Asset -$ 60,000$

Valuation Allowance -$ (60,000)$

86

CURRENT AUDITOR RED FLAGS

Current Auditor Hot Topics

I. PCAOB materiality guidelines

II. Deferred tax asset disclosure

A. Classification – current vs. non-current

B. Stock-based compensation

1. Terminations and cancellations

2. Sect. 83(b) elections

C. Cost basis – fixed/intangible assets

D. “True-up” impact – estimate vs. error

III. Permanent reinvestment of foreign earnings rep under APB 23

A. Ability – sufficient cash to fund domestic operations

B. Intent – established company policy; earnings need to fund operations

C. Reasonable estimate of deferred taxes

88

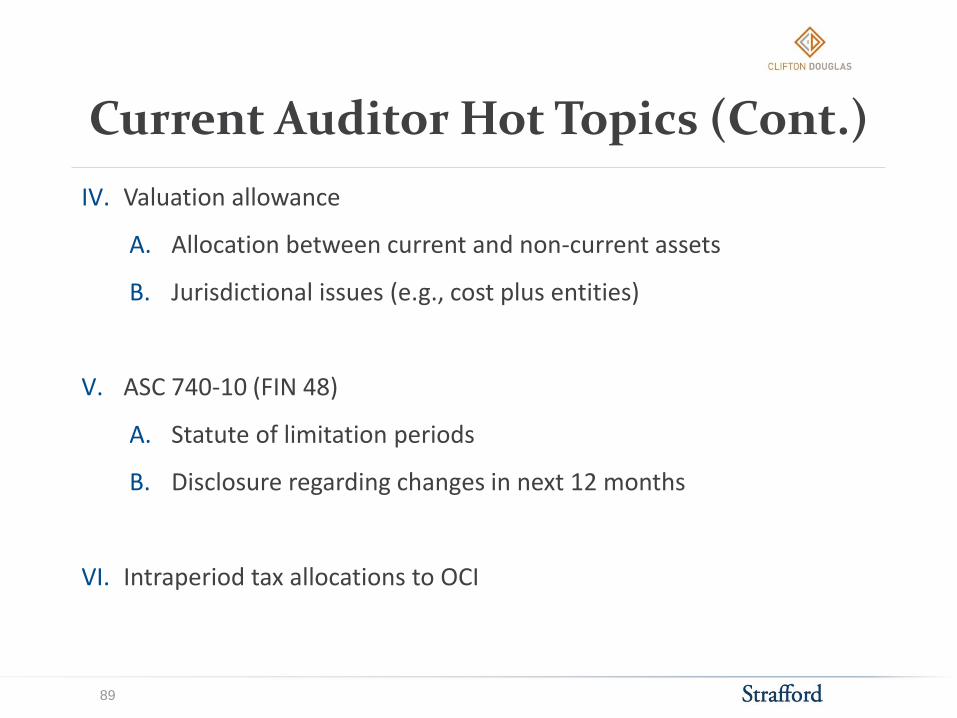

Current Auditor Hot Topics (Cont.)

IV. Valuation allowance

A. Allocation between current and non-current assets

B. Jurisdictional issues (e.g., cost plus entities)

V. ASC 740-10 (FIN 48)

A. Statute of limitation periods

B. Disclosure regarding changes in next 12 months

VI. Intraperiod tax allocations to OCI

89

Current Auditor Red Flags

I. Effective tax rate reconciliation

A. Foreign effective tax rate varies significantly from

statutory rate.

II. Business combinations

A. Contingent liabilities and consideration

III. Deferred tax roll

IV. Uncertain tax positions

A. Inter-company transactions/transfer pricing

B. Foreign audits

90

Slide Intentionally Left Blank

RISK MITIGATION

Risk Mitigation

I. Valuation allowance documentation

II. ASC 740-30-25-17 (APB 23) documentation

III. Tax provision software

IV. Department capability and internal controls

93

Risk Mitigation (Cont.)

I. Valuation allowance documentation

I. Four sources of taxable income

A. Taxable income in carryback years

1. Consider character of income

B. Future reversal of existing temporary differences

1. Consider timing of future reversals

C. Tax planning strategies

1. Must be prudent and feasible

2. Must be something management wouldn’t ordinarily

take

3. Must prevent deferred tax asset from expiring unused

4. Must result in the realization of a deferred tax asset

94

Risk Mitigation (Cont.)

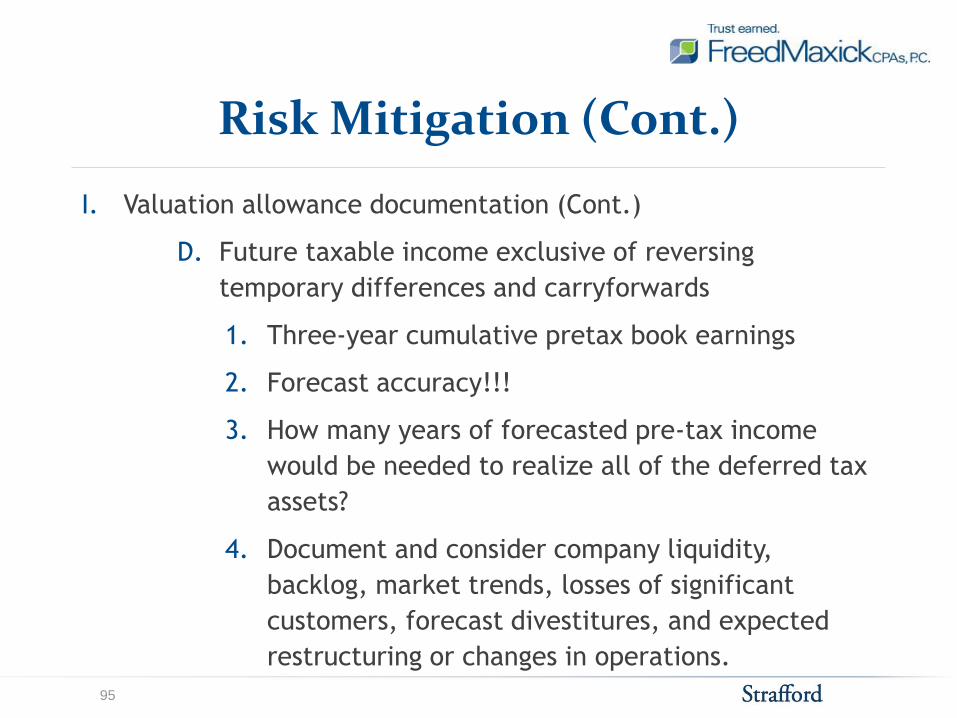

I. Valuation allowance documentation (Cont.)

D. Future taxable income exclusive of reversing

temporary differences and carryforwards

1. Three-year cumulative pretax book earnings

2. Forecast accuracy!!!

3. How many years of forecasted pre-tax income

would be needed to realize all of the deferred tax

assets?

4. Document and consider company liquidity,

backlog, market trends, losses of significant

customers, forecast divestitures, and expected

restructuring or changes in operations.

95

Risk Mitigation (Cont.)

I. ASC 740-30-25-17 (APB 23) documentation

A. Document policy of permanent reinvestment

B. Consider all aspects of outside basis differences (unremitted earnings,

cumulative translation adjustments, transactions with non-controlling

shareholders and other comprehensive income)

C. Document uses of excess cash at foreign subsidiary (working capital needs,

capital expenditures, acquisitions, repay inter-company obligations, loan to

other foreign entities, etc.

D. Document or forecast need or lack thereof of cash at the parent company

1. Operations, debt service, acquisitions, capital expenditures, inter-

company obligations

E. Consider history of earnings remittances

1. Consider policy of not remitting past earnings

F. Consider dispositions/available for sale entities

96