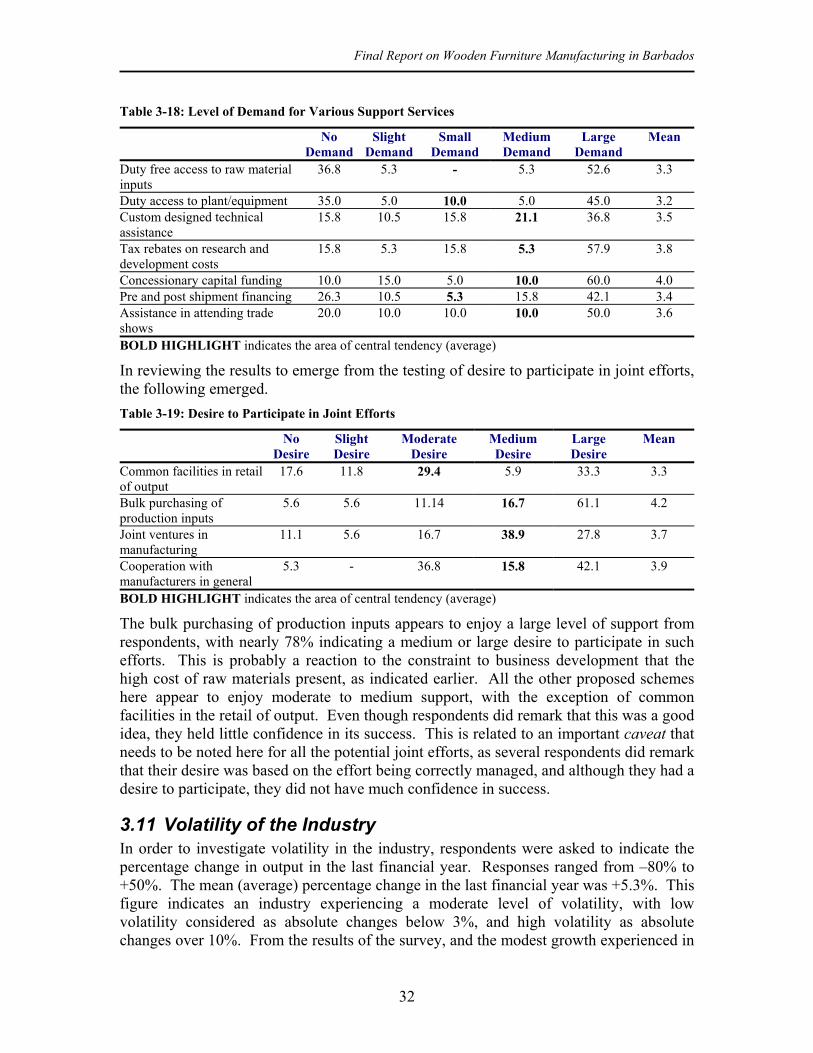

Embed Size (px)

Citation preview

Final Report for the Barbados Investment Development Corporation (BIDC) on the Wooden Furniture/Architectural Millwork

Industry in Barbados

Change in Index of Industrial Production for Total Manufacturing and Wooden Furniture (1982 to 2005)

0

20

40

60

80

100

120

140

160

180

200

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Year

Inde

x of

Indu

stria

l Pro

duct

ion

Total Manufacturing

Wooden Furniture

September 2006

© Jonathan Lashley (2006)

Final Report on Wooden Furniture Manufacturing in Barbados

TABLE OF CONTENTS

EXECUTIVE SUMMARY ………………………………………………...…………... 4 1 Introduction ........................................................................................................................... 13 2 Purpose and Scope .............................................................................................................. 14

2.1 Definition of the Sector.............................................................................................. 15 2.2 Overview of the Wooden Furniture Sector .............................................................. 15 2.3 Methodology ............................................................................................................... 18

3 Survey Results...................................................................................................................... 18 3.1 Company Demographics........................................................................................... 19 3.2 Production Inputs and Equipment ........................................................................... 21 3.3 Human Resources...................................................................................................... 22 3.4 Organisational Style .................................................................................................. 23 3.5 Supply Chain Issues .................................................................................................. 24 3.6 Organisational Strategy/Industry Strategy.............................................................. 25 3.7 Views on Constraints to Business Development ................................................... 26 3.8 Exporting Behaviour.................................................................................................. 29 3.9 Importing Behaviour .................................................................................................. 31 3.10 Needs in Support Services........................................................................................ 31 3.11 Volatility of the Industry ............................................................................................ 32

4 Results of Interviews with Stakeholders ............................................................................... 33 5 Critical Issues and Recommendations ................................................................................. 34

5.1 Demand Estimates ..................................................................................................... 34 5.2 The Economic Importance of the Sector ................................................................. 35 5.3 Major Niches............................................................................................................... 35 5.4 Difficulties Experienced by the Sector .................................................................... 37 5.5 People/Cultural Issues Negatively Affecting the Sector ........................................ 38 5.6 General Recommendations....................................................................................... 38

6 Summary and Conclusions................................................................................................... 40 7 Appendices ........................................................................................................................... 42

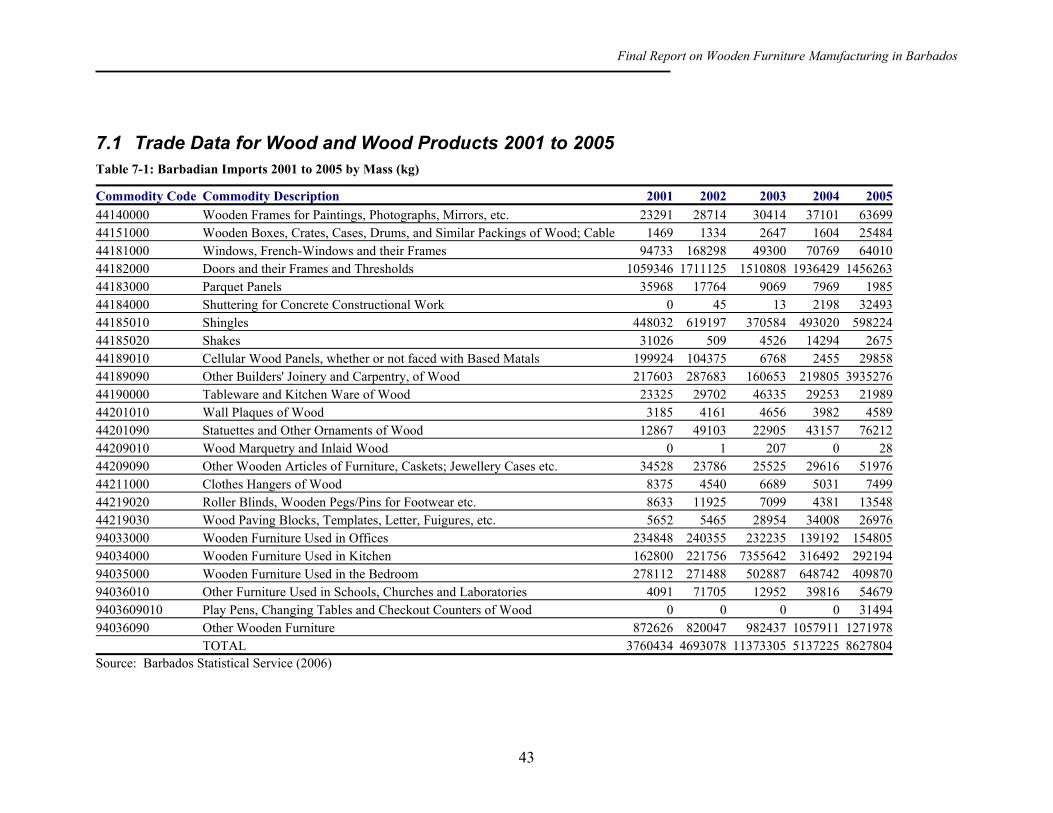

7.1 Trade Data for Wood and Wood Products 2001 to 2005 ........................................ 43 7.2 Survey Instrument...................................................................................................... 45

TABLE OF TABLES

Table 1-1: Profile of the ‘Average’ Wooden Furniture Manufacturer............................................... 5 Table 2-1: Wood Product Imports and Change in Imports 2001-2005.......................................... 16 Table 3-1: Profile of the ‘Average’ Wooden Furniture Manufacturer............................................. 19 Table 3-2: Changes in the Last Two Years in Key Variables........................................................ 20 Table 3-3: Changes Expected in the Next Two Years in Key Variables ....................................... 20 Table 3-4: Sub-sector Involvement................................................................................................ 21 Table 3-5: Wood Type, Number of Companies Using and Usage Levels..................................... 21 Table 3-6: Changes in Employment in the Last Two Years .......................................................... 22 Table 3-7: Changes in Employment in the Next Two Years ......................................................... 23 Table 3-8: Organisational Style- Responses to Statements ......................................................... 23 Table 3-9: Organisational Strategy- Responses to Statements .................................................... 25 Table 3-10: Views on Constraints to Business Development: Supplies........................................ 26 Table 3-11: Views on Constraints to Business Development: Equipment/Infrastructure.............. 26 Table 3-12: Views on Constraints to Business Development: Human Resources ....................... 27 Table 3-13: Views on Constraints to Business Development: Support Environment ................... 27 Table 3-14: Views on Constraints to Business Development: Competition .................................. 27 Table 3-15: Views on Constraints to Business Development: Market .......................................... 28 Table 3-16: Main Problems Experienced in Exporting .................................................................. 31 Table 3-17: Main Problems in Importing ....................................................................................... 31 Table 3-18: Level of Demand for Various Support Services ......................................................... 32

2

Final Report on Wooden Furniture Manufacturing in Barbados

Table 3-19: Desire to Participate in Joint Efforts ........................................................................... 32 Table 7-1: Barbadian Imports 2001 to 2005 by Mass (kg) ............................................................ 43 Table 7-2: Barbadian Imports 2001 to 2005 by Value (BDS$)...................................................... 44

TABLE OF FIGURES Figure 1: The Rise and Fall of Wooden Furniture Manufacturing in Barbados (1982 to 2005) .... 13 Figure 2: Total Exports of Wood Products and Wooden Furniture by Value (BDS$) 2001-2005 . 29 Figure 3: Main Exports of Wood Products and Wooden Furniture by Value (BDS$) 2001 to 2005

.............................................................................................................................................. 30 Figure 4 Main Imports of Wood Products and Wooden Furniture by Value (BDS$) 2001 to 200536

3

Final Report on Wooden Furniture Manufacturing in Barbados

EXECUTIVE SUMMARY The furniture industry is operating on tighter margins and experiencing ever increasing competition. No longer are the days when furniture manufacturers could develop a product and market it for years, if not decades. Furniture manufacturers are often left to their own inherent instincts during the design, production and marketing phases of their product development without any real analytical support to help them assess if their assumptions are correct or not, as demonstrated by the declining fortunes of the industry since the early 1990s, and shown in the figure below, where the current state of industrial production is a mere 8.8% of what it was in 1989. Figure A: The Rise and Fall of Wooden Furniture Manufacturing in Barbados (1982 to 2005)

Change in Index of Industrial Production for Total Manufacturing and Wooden Furniture (1982 to 2005)

0

20

40

60

80

100

120

140

160

180

200

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Year

Inde

x of

Indu

stria

l Pro

duct

ion

Total ManufacturingWooden Furniture

In seeking to address these issues, the current research identifies some of the key challenges faced by wooden furniture manufacturers/architectural mill-workers as well as identifying areas where technical assistance may be offered. It is anticipated that with this support, manufacturers would be able to quickly and accurately model future proposed adaptations to their facilities and marketing strategies without making costly guesses. Furthermore, if modelled correctly, the furniture sector will be able to reap the benefits from a change to plant layout, retooling personnel, and upgrading equipment.

Background

Specifically, the Terms of Reference (TOR) for the project indicated a need to address several specific issues. In addressing these issues the research adopted a mixed methodology which included a survey of manufacturing establishments, interviews with

4

Final Report on Wooden Furniture Manufacturing in Barbados

key stakeholders, and analysis of trade statistics. The issues for examination and the means of measurement are outlined below. 1. Estimate the local demand for wooden furniture. This was addressed by

examining estimates in output growth from the survey instrument as well as from interviews with key stakeholders, accompanied by an examination of trade statistics to identify trends in demand.

2. Estimate the economic importance of the sector. From the results of the survey of manufacturers and secondary statistics, estimates are constructed for employment, GDP, and exports.

3. Identify major niches. This area is addressed through reference to the results of the survey of manufacturers, where respondents identified the subsector in which they operated and their percentage of involvement, accompanied by an analysis of trade statistics examining in particular value by mass as a proxy for demand. In addressing this issue, the TOR of ‘Presenting in concise form the unique sales proposition of the sectors where imports dominate’ is also examined.

4. Difficulties experienced by the sector. This is directly addressed through the survey instrument, and interviews with key stakeholders.

5. People/Cultural Issues that will negatively affect the industry. Previous research results are specifically showing that non-cooperative behaviour, rooted in a parochialist nature, and apathy are both negatively affecting the industry. These issues are examined in greater detail in the in-depth analysis of results.

Survey Results

The background research led to the construction of a sample frame of 67 establishments involved in the wooden furniture sector. By the end of August 2006, all establishments were contacted, of which 20 were identified as importers/retailers or not relevant to the survey, and 1 was a subsidiary of another establishment surveyed. This left a sample frame of 46 enterprises. The data analysis is based on 22 valid and completed responses (48% of all wooden furniture manufacturers). The profile of the ‘average’ manufacturer is shown in the table below. Table 1-1: Profile of the ‘Average’ Wooden Furniture Manufacturer

Variable Result Age 19 years old Full-time Employees 11 Part-time Employees 2 Legal Form Incorporated Ownership 100% Barbadian Premises Rented Manufacturing Space 7,200 square feet Company Showroom No Approximate Sales in last financial year BDS$300,000 Expected Sales Growth in next financial year 16% Capital Expenditure in last two years BDS$18,000

The survey sought responses in the following areas. • Profile of the Wooden Furniture Manufacturing Sector (Company Demographics) • Wood types utilised

5

Final Report on Wooden Furniture Manufacturing in Barbados

• Machine types and vintage • Human Resources • Organisational Style • Supply Chain Issues • Organisational and Industry Strategies • Views on Constraints to Business Development • Export and Import Behaviour • Needs in Support Services • Measures of Industry Volatility

Of greatest interest from the survey were the views of respondents of the main constraints to the development of their business. The results of this section of the analysis are shown below.

Views on Constraints to Business Development Overall the results of the survey indicate a level of optimism for output and employment growth. Of interest here, and perhaps a reason for the optimistic outlook for the sector demonstrated, is the issue of domestic demand, where over fifty percent (55%) of respondents indicated that this had either no effect or only a slight effect on the development of their business, suggesting that local demand is currently high. Overall, in looking at constraints to business development, the main issues relate to:

The high price of raw materials • • • • • • •

The high price of productive equipment High overhead and variable costs A lack of skilled staff in the labour market A lack of Government assistance Difficulty in obtaining finance The high level of competition from low quality/cheap imports, mainly from the Far East.

All of these issues rated as having more than a ‘medium’ effect on business development. In the case of architectural millwork, respondents thought that financiers and Government undervalued the contribution of this sub-sector and hence no special attention was offered to plants that specialized in this area. This was despite the fact that the millwork sector was viewed as more technical and provided manufacturers with higher margins based on the fact that it was a ‘high-end’ product. The research, in seeking to enhance the standing of the sector made a number of recommendations to address these problems. It is understood that on an individual level that the Government (or the BIDC) can do little to reduce the cost of raw materials or productive equipment apart from the elimination of duties and levies. However, as a collective entity the sector would be in a stronger position to effect prices. Constraining such as effort is a lack of collaboration in the sector and Government and its related agencies will need to attempt to facilitate such efforts. The same could be said in the area of high overhead and variable costs, however Government can also play a more direct role here, hence also dealing with the issue of a lack of Government assistance.

6

Final Report on Wooden Furniture Manufacturing in Barbados

The other issues that need to be urgently dealt with are a lack of skilled labour and difficulties in obtaining finance. The training aspect here is another area that a cooperative sector can address, through concerted pressure and assistance to the relevant training institutions. The issue of finance is however a more difficult prospect as the culture of the sector is not one that lends itself easily to production, but rather more to trade. This is a characteristic of the banking industry that is affecting all businesses involved in manufacturing and will need to be dealt with as a matter of urgency. The last issue of competition from low quality cheap imports from the Far East is difficult to ameliorate with the current neo-liberal trade regime globally. However, the issue of standards as a trade barrier will need to be investigated as the result of low quality imports is negatively impacting domestic manufacturers and exporters, as consumers do not realise that the goods they are purchasing from retail outlets are imported.

Critical Issues and Recommendations The following issues are based on the requirements of BIDC. These requirements are as outlined in the Terms of Reference (TORs). The TORs of the research were to identify, analyse and critically assess the resources and other industry information for wooden furniture manufacturers/architectural mill-workers with an aim of identifying market demand for the sector between 2006 and 2008. The research gathered information from industry employers and key stakeholders to identify capital information, and data from selected primary sources. The specific elements of the TORs addressed are outlined in turn below.

Demand Estimates The results of this analysis indicate that demand for the next two years will grow moderately as activity in the construction sector levels off. In forming the estimates, two issues were taken into consideration, manufacturers’ predictions of sales growth, and trends in imports for the last five years. On average, respondents indicated growth in the region of 15.8%. If the sample is considered representative, having covered 48% of the sector, this would suggest a total industry output in the last financial year of BDS$13.8million (based on median sales of BDS$300,510), suggesting demand increases in the region of BDS$2.2million, putting demand for the period 2006 to 2007 at approximately BDS$16million. Considering predictions for the levelling off of construction activity in the post-Cricket World Cup period, growth would be expected to remain in the region of 15% to 16% for the period 2007 to 2008. As a lower estimate, this would suggest demand in this period to grow by BDS$2.4million, making total demand for the period 2007 to 2008 BDS$18.4million for the domestic sector. In investigating the trade statistics for the period 2001 to 2005, imports by value were analysed to enable a direct comparison with the results to emerge from the survey of establishments. Although imports by mass have increased by 45% over the period, imports by value have fallen by approximately 5%. If this trend continues, as it is expected to do for the reasons alluded to above, demand in this area can be valued at BDS$25.2million in the 2006 to 2007 period, and BDS$23.9 for 2007 to 2008. This is a

7

Final Report on Wooden Furniture Manufacturing in Barbados

lower estimate for demand as it relates to the cost-insurance-freight value, not the market value to the end consumer. From the analysis it can therefore be estimated that demand for 2006 to 2007 will be approximately BDS$41.2million, and BDS$42.3million for the period 2007 to 2008.

Recommendations It appears from the analysis that demand will increase over the next two years, and domestic producers are optimistic about increases in sales, profits, and personnel over this period. However, this optimism is constrained by a number of variables both internal and external to the enterprise. The Government and the BIDC will need to work in tandem with the manufacturers to ensure that they are able to exploit this moderate increase in demand, especially in the areas of personnel training, marketing, and pricing strategies, particularly at the high-end of the market.

The Economic Importance of the Sector From the results of the survey of manufacturers and secondary statistics, estimates are constructed for employment, GDP, and foreign exchange earnings. In terms of employment, it appears that the sector employs approximately 540 persons, or 0.5% of the workforce. This is however expected to increase over the next two years as manufacturers expand production. There is however a skills shortage, constraining the full effect of any employment generation effects of enhanced demand. In terms of GDP, output in the sector is estimated at BDS$13.8million, or 0.3% of GDP at current prices. In terms of foreign exchange earnings, the sector has earned on average BDS$711,255 per annum over the last five years.

Recommendations Although the results of the analysis indicate that the sector is not a major contributor to the economy, it needs to be appreciated that it is only operating at approximately 9% of the level it was in 1989. Global and regional economic issues played their role in this decline, however as the estimates for demand show, there is potential for growth in the sector. In addition, on average, enterprises were not operating at full capacity. Indeed, it appears that they were only operating at 63% of capacity, providing the potential for output expansion with minimal capital investment. However, if it is considered that this level of capacity utilisation is based on a daily eight-hour shift, it may be considered that the sector has an even greater potential capacity if it were to operate two shifts per day, as is the norm in many other countries. These points would indicate that the sector is currently operating at 31.5% of capacity, and indeed if current output is BDS$13.8million, it suggests that potential output for the sector could be as high as BDS$43.8million, or approximately 1% of GDP. It is recommended here that measures be implemented in the short-run to act as a catalyst for the expansion of capacity utilisation, with one such measure would the facilitation of 24-hour operation to accommodate two eight-hour shifts.

8

Final Report on Wooden Furniture Manufacturing in Barbados

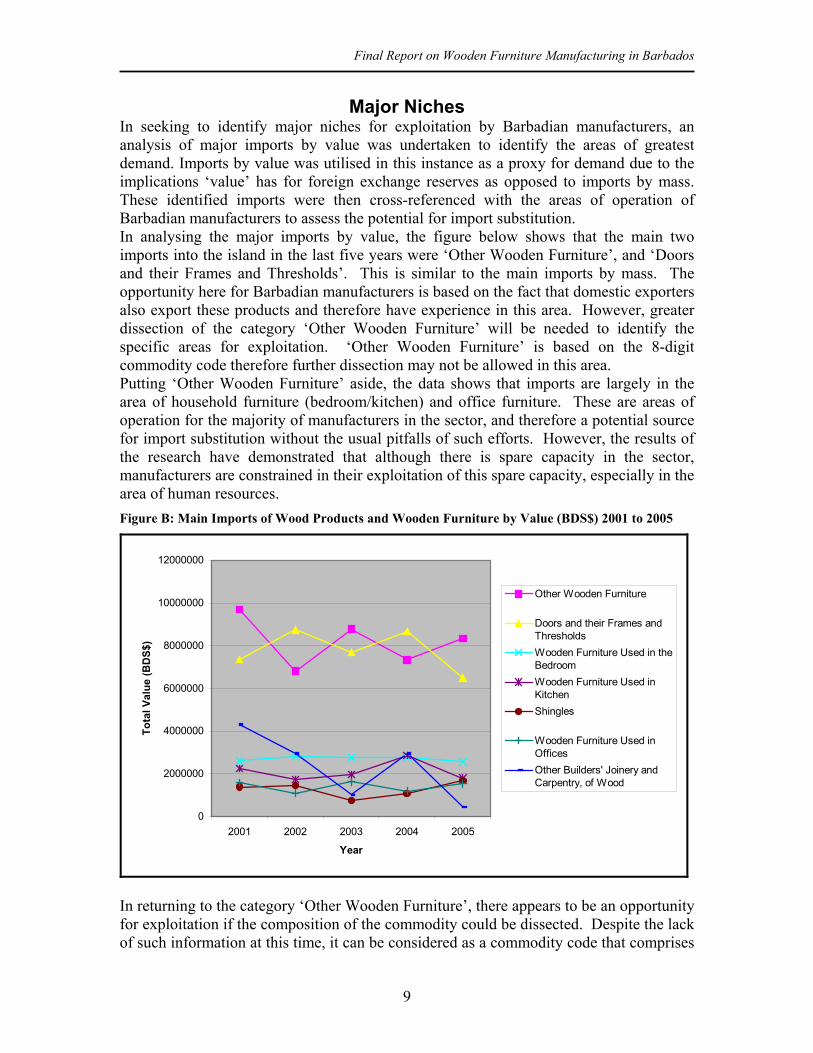

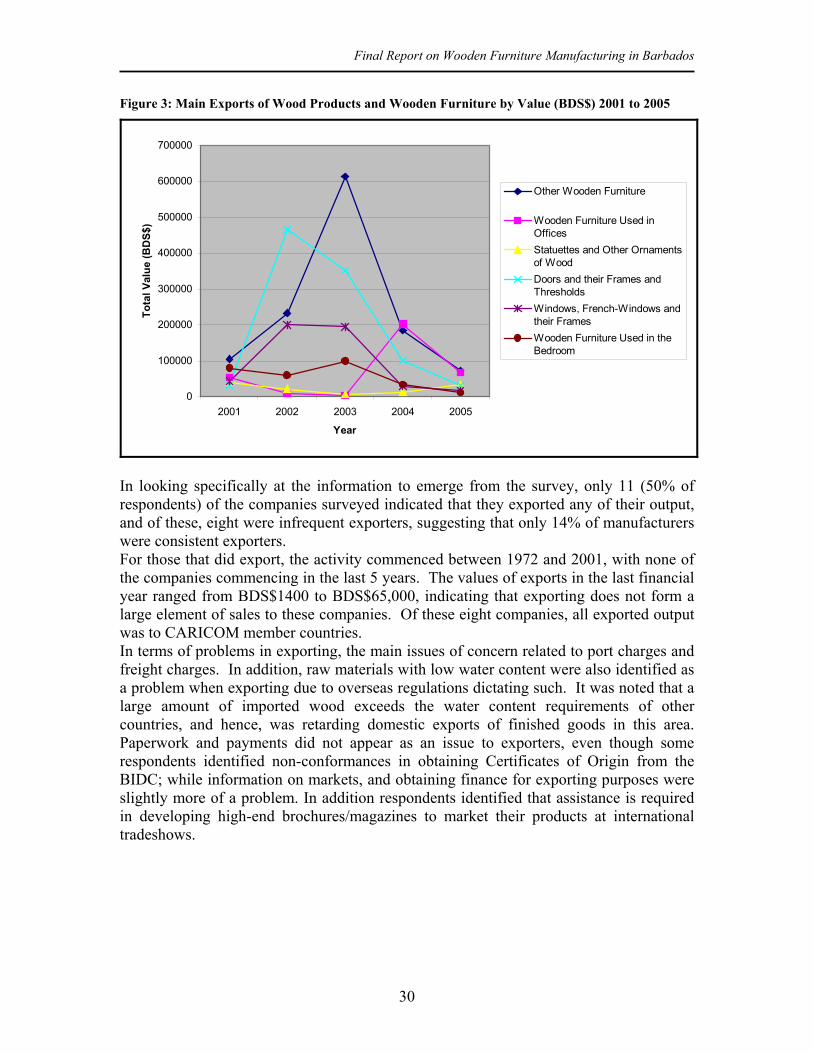

Major Niches In seeking to identify major niches for exploitation by Barbadian manufacturers, an analysis of major imports by value was undertaken to identify the areas of greatest demand. Imports by value was utilised in this instance as a proxy for demand due to the implications ‘value’ has for foreign exchange reserves as opposed to imports by mass. These identified imports were then cross-referenced with the areas of operation of Barbadian manufacturers to assess the potential for import substitution. In analysing the major imports by value, the figure below shows that the main two imports into the island in the last five years were ‘Other Wooden Furniture’, and ‘Doors and their Frames and Thresholds’. This is similar to the main imports by mass. The opportunity here for Barbadian manufacturers is based on the fact that domestic exporters also export these products and therefore have experience in this area. However, greater dissection of the category ‘Other Wooden Furniture’ will be needed to identify the specific areas for exploitation. ‘Other Wooden Furniture’ is based on the 8-digit commodity code therefore further dissection may not be allowed in this area. Putting ‘Other Wooden Furniture’ aside, the data shows that imports are largely in the area of household furniture (bedroom/kitchen) and office furniture. These are areas of operation for the majority of manufacturers in the sector, and therefore a potential source for import substitution without the usual pitfalls of such efforts. However, the results of the research have demonstrated that although there is spare capacity in the sector, manufacturers are constrained in their exploitation of this spare capacity, especially in the area of human resources. Figure B: Main Imports of Wood Products and Wooden Furniture by Value (BDS$) 2001 to 2005

0

2000000

4000000

6000000

8000000

10000000

12000000

2001 2002 2003 2004 2005

Year

Tota

l Val

ue (B

DS$

)

Other Wooden Furniture

Doors and their Frames andThresholdsWooden Furniture Used in theBedroomWooden Furniture Used inKitchenShingles

Wooden Furniture Used inOfficesOther Builders' Joinery andCarpentry, of Wood

In returning to the category ‘Other Wooden Furniture’, there appears to be an opportunity for exploitation if the composition of the commodity could be dissected. Despite the lack of such information at this time, it can be considered as a commodity code that comprises

9

Final Report on Wooden Furniture Manufacturing in Barbados

either customised furniture or ‘specialist’ furniture, which accounts for approximately BDS$8million in imports per annum. In seeking to exploit sectors where imports dominate and present a unique sales proposition, it appears that the smaller companies within the sector may provide a useful avenue to exploit this niche. This is especially related to the accepted benefits of small-scale production (flexibility and dynamism). However, in accepting such an avenue as a reasonable strategy, the smaller manufacturers in the sector will need different forms of support than that supplied to larger scale manufacturers, especially in the areas of plant layout, marketing, multi-skilling, and business skills. One of the benefits of undertaking such an endeavour is that smaller manufacturer can charge a premium on their products. However, technical assistance in the area of pricing will need to be included in any such support service, as the results of the research have demonstrated a lack of skills in the areas of accounting, marketing, and capacity utilisation.

Recommendations The results demonstrate that there is potential for the exploitation of ‘Other Wooden Furniture’ and ‘Doors and their Frames and Thresholds’. Any endeavour undertaken in support of the sector by the BIDC will need to prioritise action areas, and these two sub-sectors appear to have the potential to contribute substantially to any import substitution effort.

People/Cultural Issues Negatively Affecting the Sector Previous studies of the manufacturing sector have shown that cultural issues are indeed playing a role in constraining the development of the sector (Lashley, 2002). The survey results are specifically showing that non-cooperative behaviour, rooted in a parochialist nature, and apathy are both negatively affecting the industry. This was particularly evident in the responses received from potential survey participants, who showed little regard for any efforts that aimed at benefiting the sector as a whole. The lack of networking and use of support organisations is again indicative of this.

Recommendations The individualistic nature of the producers in the sector is representative of wider society in the island. It is not expected that any measures can be directly implemented to ameliorate these problems in the short or medium term, as the issue is one of a mind-set change that will not occur in these time periods.

General Recommendations It has become apparent during the execution of the research that action is needed on several levels, including that of the project sponsor, BIDC. To this end, the following recommendations are made that require execution at the Government and enterprise level. In this situation it is imperative that the BIDC act as both an advocacy and executing agency to ensure such action points are undertaken to facilitate the growth and enhanced position of the sector. These recommendations have emerged from all elements of the current research, including a review of trends in industry globally, a survey of establishments in the island, and interviews with key stakeholders.

10

Final Report on Wooden Furniture Manufacturing in Barbados

Government Level Actions Recommended From the results of the research, it appears that Government needs to improve the business climate/enabling environment for furniture manufacturers if they are to survive and thrive as an industry. It is therefore necessary for a clear message to be sent from Government identifying the realised and potential impact of the sector and its contribution to GDP. It is suggested that there is a need for a Head of Manufacturing in the Ministry in charge of Industry and also a need for officers specifically focused on various subsections of manufacturing. This would allow for suitable research and development to be identified for the improvement of the sector as well as assist in the identification and development of appropriate funds and technical assistance. In addition, the Head could facilitate a ten-year furniture industry strategy and vision. Further, any person in such a position must be prepared to meet the sector regularly, to engage experts as required, and to undertake any additional significant research task. Infrastructure is a key area to the survival of the furniture-manufacturing sector. One of the key areas that need to be addressed is the cost of energy. If furniture manufacturers are to be competitive in their pricing, there needs to be a policy for manufacturers that introduce energy saving units to their factories. Tax incentives should be offered for this type of investment. It appears that there is a need for a coalition body to be formed to assist furniture manufacturers in ordering raw materials as well as in grouping together to satisfy large overseas orders. Allowing for all the stakeholders to contribute in an informed manner to the development of future trade agreements with other countries will also be beneficial. This would reduce the perceived negative impact from the scale of threat from imports, affect on employment, investment (capital and research and development), price wars, export reductions, limited availability of skilled workers and brand recognition. Government also needs to look at the impact of the Rules of Origins provision on the sector, compliance costs, and whether there are greater opportunities to achieve uniformity through other existing agreements.

Enterprise Level Actions Recommended A number of action areas have been identified for furniture manufacturers. This are listed and expanded on below. Apprenticeships. Furniture manufacturers need to provide mechanisms for apprenticeships within their organizations. Strategic Focus. Furniture manufacturers need an enhanced strategic focus. Companies need to identify their product strengths and the core competencies of the company. It is in these areas that the manufacturer would gain its competitive advantage. Consistent Quality. Furniture manufacturers need to standardize their products and product components, as this is key to consistent quality of outputs. Technology. There needs to be an adaptation of technologies to enable more efficient and effective management of limited resources available. Marketing. Furniture manufacturers need to embrace as many means as possible to promote their products.

11

Final Report on Wooden Furniture Manufacturing in Barbados

Research and Development. Companies need to allocate monies for an R&D fund that is commensurate with sales projections for the years to come.

Summary and Conclusions From the results of the research, which included a survey of manufacturing establishments, interviews with key stakeholders and analysis of trade data, it appears that the prospects for the wood products and wooden furniture-manufacturing sector are good. This is based firstly on the responses to the survey, which indicate that producers expect output (and employment) to increase in the next two years despite a couple of years of stasis. In addition, the interviews revealed that the demand for products will continue to be high, even though construction activity is expected to level off in the near future. The analysis of trade statistics as well also suggest good prospects for the sector, although not directly. What the analysis of trade statistics suggest is that there is scope for import substitution in the sector without the usual pitfalls of such efforts as skills and capacity exist to exploit them. This is particularly related to present capacity in the sector. Indeed, it appears that manufacturers are operating at 63% of capacity, providing the potential for output expansion with minimal capital investment. However, if it is considered that this level of capacity utilisation is based on one daily eight-hour shift, it may be considered that the sector has an even greater potential capacity if it were to operate two shifts per day, as is the norm in many other countries. These points would indicate that the sector is currently operating at 31.5% of capacity, and indeed if current output is BDS$13.8million, it suggests that potential output for the sector could be as high as BDS$43.8million, or approximately 1% of GDP. It is recommended here that measures be implemented in the short-run to act as a catalyst for the expansion of capacity utilisation, with one such measure being the facilitation of 24-hour operation. However, they are constraints that will need to be addressed if these prospects for the sector are to be realised. These can be categorised as constraints relating to training, technical assistance, finance, and advocacy. In dealing first with the issue of advocacy, the sector needs a voice. However, there is a severe lack of cooperation within the sector and this is constraining efforts to enhance the prospects of the sector. There will initially need to be a concerted effort to bring the sector together, and perhaps the recommendation that a representative in the Ministry responsible for industry be appointed is a step in the right direction. In looking at the other issues, training and technical assistance will need to be addressed as a matter of urgency if the unused capacity in the sector is to be exploited. However, due to the differing characteristics of firms in the industry, these efforts will need to be tailored to individual needs, especially as regards size. The issue of finance is however a national issue that will need to be addressed. At the moment the commercial banking sector is averse to providing finance for productive purposes, and is predisposed to providing finance for trade or consumption. Apart from these issues, respondents to the survey also noted costs as a major constraint to business development. As mentioned with the issue of advocacy, without cooperation with-in the sector, these issues will not be addressed. Producers need to realise the benefits of such endeavours, where volume of numbers will give them a better bargaining position. It appears that once these difficulties are overcome that the sector can begin to grow and aspire to its heights of the late 1980s.

12

Final Report on Wooden Furniture Manufacturing in Barbados

Final Report for the Barbados Investment Development Corporation (BIDC) on the Wooden Furniture/Architectural Millwork Industry in Barbados

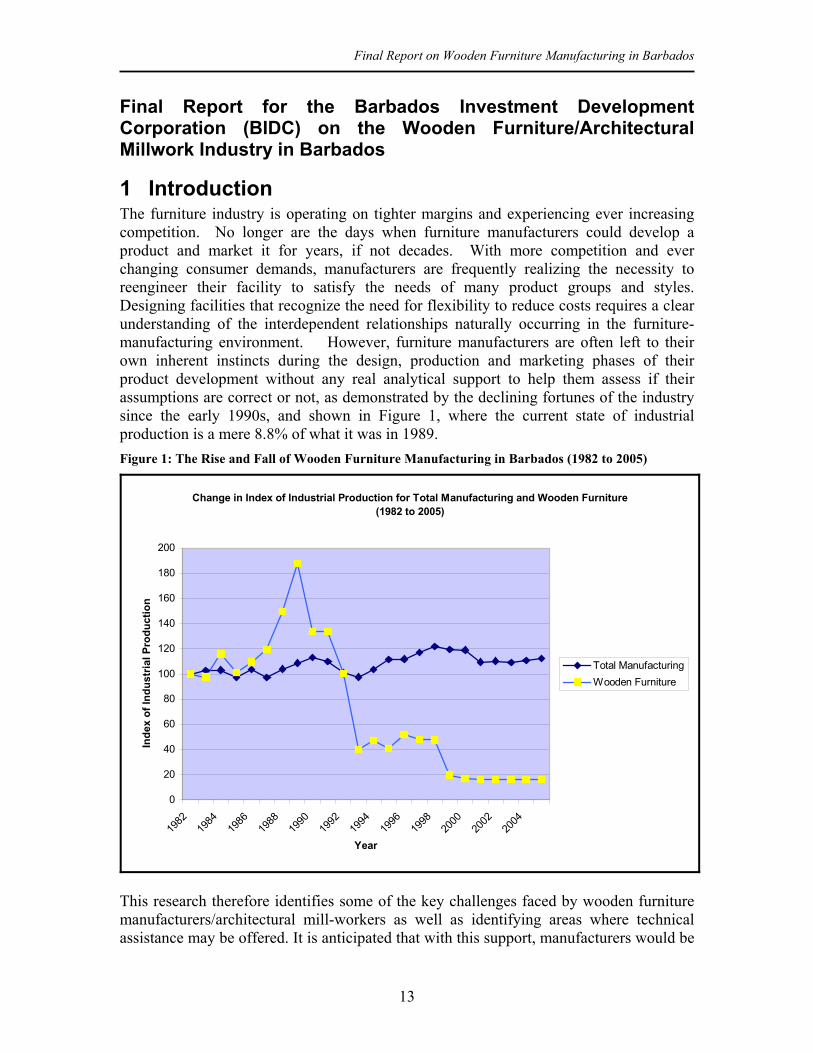

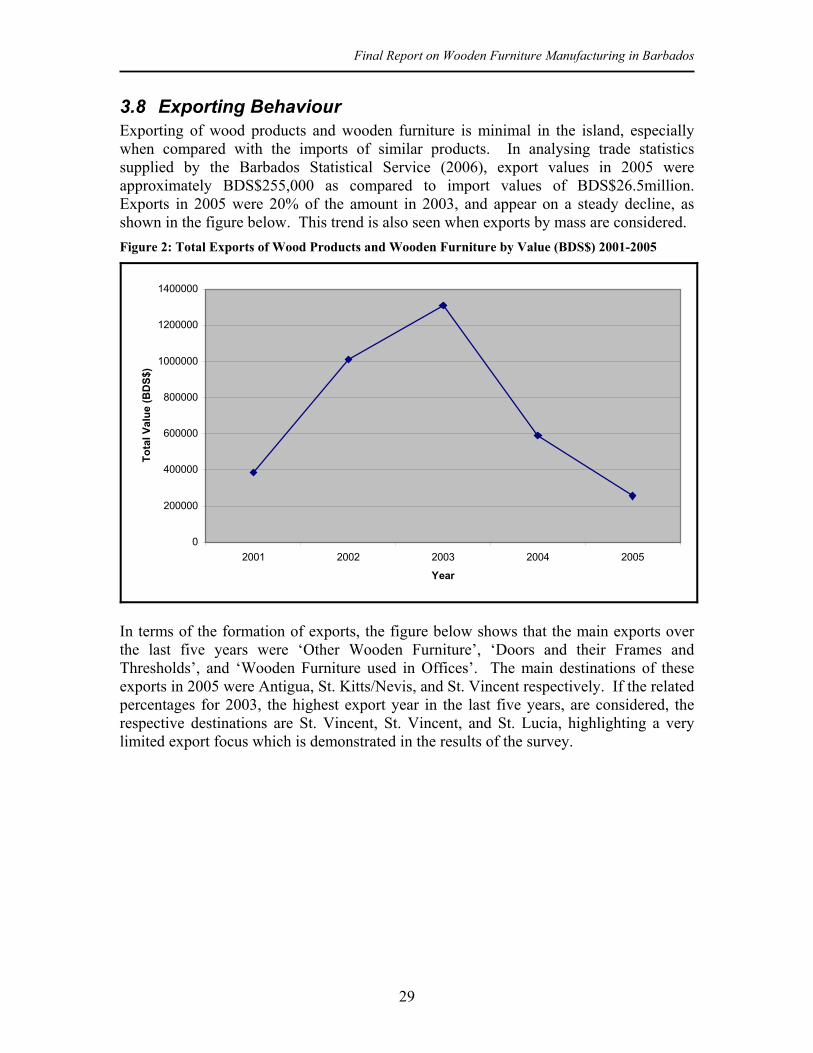

1 Introduction The furniture industry is operating on tighter margins and experiencing ever increasing competition. No longer are the days when furniture manufacturers could develop a product and market it for years, if not decades. With more competition and ever changing consumer demands, manufacturers are frequently realizing the necessity to reengineer their facility to satisfy the needs of many product groups and styles. Designing facilities that recognize the need for flexibility to reduce costs requires a clear understanding of the interdependent relationships naturally occurring in the furniture-manufacturing environment. However, furniture manufacturers are often left to their own inherent instincts during the design, production and marketing phases of their product development without any real analytical support to help them assess if their assumptions are correct or not, as demonstrated by the declining fortunes of the industry since the early 1990s, and shown in Figure 1, where the current state of industrial production is a mere 8.8% of what it was in 1989. Figure 1: The Rise and Fall of Wooden Furniture Manufacturing in Barbados (1982 to 2005)

Change in Index of Industrial Production for Total Manufacturing and Wooden Furniture (1982 to 2005)

0

20

40

60

80

100

120

140

160

180

200

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Year

Inde

x of

Indu

stria

l Pro

duct

ion

Total ManufacturingWooden Furniture

This research therefore identifies some of the key challenges faced by wooden furniture manufacturers/architectural mill-workers as well as identifying areas where technical assistance may be offered. It is anticipated that with this support, manufacturers would be

13

Final Report on Wooden Furniture Manufacturing in Barbados

able to quickly and accurately model future proposed adaptations to their facilities and marketing strategies without making costly guesses. Furthermore, if modelled correctly, the furniture sector will be able to reap the benefits from a change to plant layout, retooling personnel, and upgrading equipment. In addition, the research can be a stepping-stone to creating an operational planning tool that can be utilized on a continued basis to evaluate issues such as scheduling sequences or batch sizes within the industry. In addition it can also be used by support service organizations to base their decision-making on the various types of technical assistance to be offered. In the industry it is not surprising that many of the common areas examined for improvement and cost reductions begin on the plant floor itself. However, the ease of determining where to begin is often a function of the overall complexity of the manufacturing system, and in the furniture manufacturing industry, the challenge presented can at times be substantial. The complexity of interdependent relationships created by the sheer quantity of unique parts, machine operation sequences in furniture manufacturing, human resource, and budgeting limitations, cause the process to be very challenging. The current research aims to contribute to the amelioration of these constraints.

2 Purpose and Scope The Terms of Reference (TOR) of the research was to identify, analyse and critically assess the resources and other industry information for wooden furniture manufacturers/architectural mill-workers with an aim of identifying market demand for the sector between 2006 and 2008. The research gathered information from industry employers and key stakeholders to identify capital and supply chain information, as well data from selected primary sources. Specifically, the TOR indicated a need to address several specific issues. These issues and the means of measurement are outlined below.

• Estimate the local demand for wooden furniture. This was addressed by examining estimates in output growth from the survey instrument as well as from interviews with key stakeholders, accompanied by an examination of trade statistics to identify trends in demand.

• Estimate the economic importance of the sector. From the results of the survey of manufacturers and secondary statistics, estimates are constructed for employment, GDP, and exports.

• Identify major niches. This area is addressed through reference to the results of the survey of manufacturers where respondents identified the subsector in which they operated and the percentage of involvement, accompanied by an analysis of trade statistics examining in particular value by mass as a proxy for demand. In addressing this issue, the TOR of ‘Presenting in concise form the unique sales proposition of the sectors where imports dominate’ will also be examined.

• Difficulties experienced by the sector. This is directly addressed through the survey instrument, and interviews with key stakeholders.

• People/Cultural Issues that will negatively affect the industry. Previous studies of the manufacturing sector have shown that cultural issues are indeed playing a role in constraining the development of the sector (Lashley, 2002). The

14

Final Report on Wooden Furniture Manufacturing in Barbados

survey results are specifically showing that non-cooperative behaviour, rooted in a parochialist nature, and apathy are both negatively affecting the industry. These issues are examined in greater detail in the indepth analysis of results.

Overall the report outlines the following categories:

• Definition of the Wooden Furniture Manufacturing Sector • Overview of the Industrial Organisation of the Wooden Furniture Sector • Profile of the Wooden Furniture Manufacturing Sector (Company Demographics) • Wood types utilised • Machine types and vintage • Human Resources • Organisational Style • Supply Chain Issues • Organisational and Industry Strategies • Views on Constraints to Business Development • Export and Import Behaviour • Needs in Support Services • Measures of Industry Volatility

The report also includes the findings from the statistical reviews undertaken for the project; the findings of the employer and stakeholder surveys and site visits.

2.1 Definition of the Sector The Barbadian wooden furniture/architectural millwork sector is highly fragmented and as such there is no uniformly accepted definition of the sector. However, the sector was defined, for the purposes of this report, primarily by the types of furniture manufactured.

• Wooden kitchen cabinets • Wooden bathroom cabinets • Wooden doors and windows • Other millwork • Prefabricated wood Buildings • Wooden household furniture • Upholstered Wooden Furniture • Wooden Office furniture • Hotel/Restaurant/Institutional Furniture and Fixtures

2.2 Overview of the Wooden Furniture Sector In reviewing the overall results of the survey of wooden furniture manufacturers, interviews with key stakeholders, and a review of trade data, a profile of the industrial organisation of the sector was constructed. The basic Structure-Conduct-Performance of the sector is outlined below.

15

Final Report on Wooden Furniture Manufacturing in Barbados

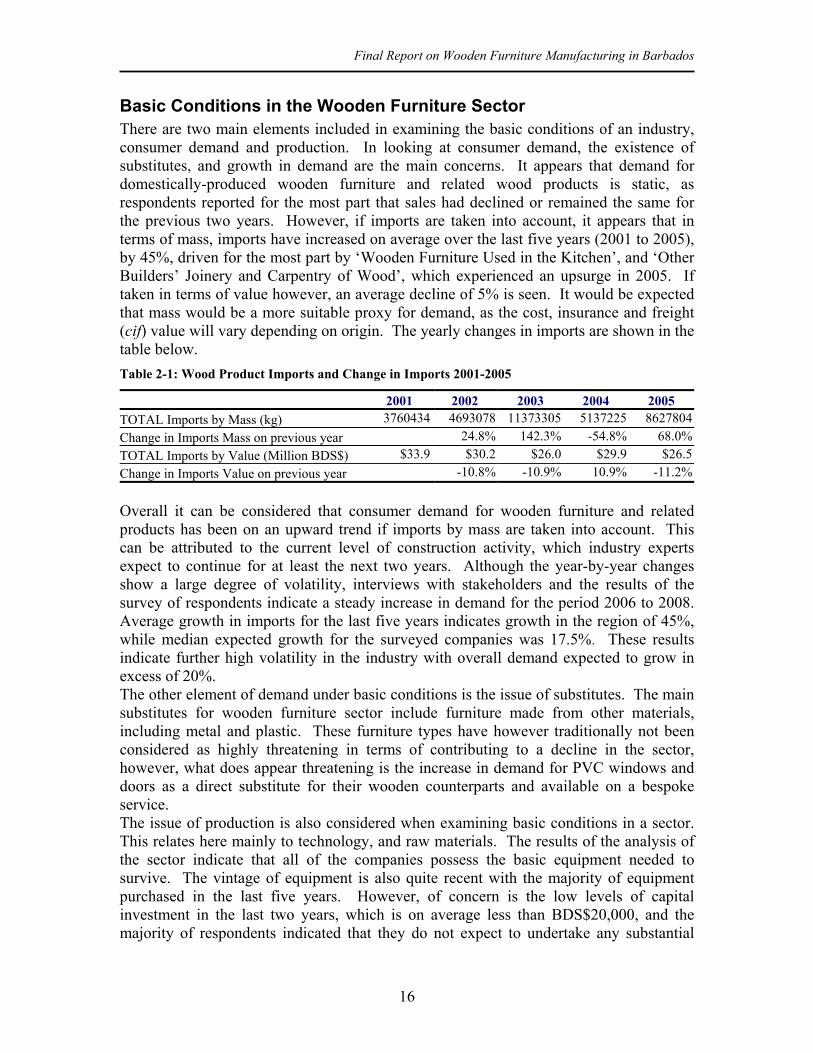

Basic Conditions in the Wooden Furniture Sector There are two main elements included in examining the basic conditions of an industry, consumer demand and production. In looking at consumer demand, the existence of substitutes, and growth in demand are the main concerns. It appears that demand for domestically-produced wooden furniture and related wood products is static, as respondents reported for the most part that sales had declined or remained the same for the previous two years. However, if imports are taken into account, it appears that in terms of mass, imports have increased on average over the last five years (2001 to 2005), by 45%, driven for the most part by ‘Wooden Furniture Used in the Kitchen’, and ‘Other Builders’ Joinery and Carpentry of Wood’, which experienced an upsurge in 2005. If taken in terms of value however, an average decline of 5% is seen. It would be expected that mass would be a more suitable proxy for demand, as the cost, insurance and freight (cif) value will vary depending on origin. The yearly changes in imports are shown in the table below. Table 2-1: Wood Product Imports and Change in Imports 2001-2005

2001 2002 2003 2004 2005 TOTAL Imports by Mass (kg) 3760434 4693078 11373305 5137225 8627804Change in Imports Mass on previous year 24.8% 142.3% -54.8% 68.0%TOTAL Imports by Value (Million BDS$) $33.9 $30.2 $26.0 $29.9 $26.5Change in Imports Value on previous year -10.8% -10.9% 10.9% -11.2% Overall it can be considered that consumer demand for wooden furniture and related products has been on an upward trend if imports by mass are taken into account. This can be attributed to the current level of construction activity, which industry experts expect to continue for at least the next two years. Although the year-by-year changes show a large degree of volatility, interviews with stakeholders and the results of the survey of respondents indicate a steady increase in demand for the period 2006 to 2008. Average growth in imports for the last five years indicates growth in the region of 45%, while median expected growth for the surveyed companies was 17.5%. These results indicate further high volatility in the industry with overall demand expected to grow in excess of 20%. The other element of demand under basic conditions is the issue of substitutes. The main substitutes for wooden furniture sector include furniture made from other materials, including metal and plastic. These furniture types have however traditionally not been considered as highly threatening in terms of contributing to a decline in the sector, however, what does appear threatening is the increase in demand for PVC windows and doors as a direct substitute for their wooden counterparts and available on a bespoke service. The issue of production is also considered when examining basic conditions in a sector. This relates here mainly to technology, and raw materials. The results of the analysis of the sector indicate that all of the companies possess the basic equipment needed to survive. The vintage of equipment is also quite recent with the majority of equipment purchased in the last five years. However, of concern is the low levels of capital investment in the last two years, which is on average less than BDS$20,000, and the majority of respondents indicated that they do not expect to undertake any substantial

16

Final Report on Wooden Furniture Manufacturing in Barbados

capital investment in the next two years. In addition, respondents also stated that local financiers do not understand the furniture-manufacturing sector and hence they use this as an excuse to classify it as risky, therefore justify refraining from offering capital at crucial points in the business cycle. In terms of raw materials, the majority is sourced locally, although practically all of the wood in the island is imported, indicating that only a small percentage of producers are importing raw materials directly. Other elements of the production process such as human resources are examined in greater detail in the analysis of the survey of manufacturers.

Structure of the Wooden Furniture Sector Investigating the structure of the wooden furniture sector entails a detailed examination of the supply chain. In terms of number of producers, the survey of establishments identified 46 manufacturers operating in the sector, of varying sizes. Overall, the wooden furniture-manufacturing sector appears to be dominated by five or six manufactures. In terms of sellers of wooden furniture, although some manufacturers sell directly to the consumer, in conducting the research, approximately 20 retailers were identified as dealing largely in wooden furniture retail. These retailers purchase approximately 14% of the output of manufacturers in Barbados, the rest being imported, as indicated by the large volumes of imports outlined above. Of these 20 retailers, three dominate in purchasing from domestic manufacturers. These are DaCosta Mannings, Courts, and Standard. In this sense the sector as a whole can be characterised as oligopsonic, with a few large buyers dominating the market. In terms of vertical integration in the sector, this is minimal. Less than one-half (43%) of the manufacturing companies surveyed operated a showroom, and even less imported any of their raw materials directly. In terms of integration in general, there is very little cooperation, or networking in the sector that is contributing to the continued dominance of a few buyers in the market.

Conduct in the Wooden Furniture Sector In looking at the conduct of the companies in the sector, research and development was static in the last two years, however, it is expected to increase somewhat in the next two. In terms of pricing behaviour, the majority of companies indicated they did not compete on price, which is not surprising considering the inability to achieve economies of scale within the Barbadian economy.

Performance of the Wooden Furniture Sector The performance of the sector has not been on the whole encouraging. This is especially seen where profits have either declined or remained the same for the last two years, although there has been some increase in turnover. Some respondents have identified the ‘zero rating’ of hotels as one of the main reasons for reduction in sales as hotels are able foreign purchases without any limitations. In addition, respondents also stated that the quality of wood imported had a high level of water content and hence this restricted manufacturers from using it in products for export to North American markets. In terms of human resources, there appears to also have been very little employment generation, with very few manufacturers indicating any increase in any of the

17

Final Report on Wooden Furniture Manufacturing in Barbados

occupational categories. In addition, manufacturers have only been operating at approximately 63% of capacity, suggesting a potential for turnover expansion with minimal capital investment at this time.

2.3 Methodology The market demand survey incorporated several methodologies to collect and interpret sector information. Detailed below are the specific steps and the methodologies utilised in the execution of the project.

Survey Methodology Two surveys were developed in consultation with the BIDC to collect information from employers and key stakeholders. In terms of sample design, the consultants created a furniture manufacturers sample list based on the BIDC database of existing companies, complimented by additions from various other sources. Statistical data on imports and exports were obtained from the Barbados Statistical Service. The background research led to the construction of a sample frame of 67 establishments involved in the wooden furniture sector. By the end of August 2006, all establishments were contacted, of which 20 were identified as importers/retailers or not relevant to the survey, and 1 was a subsidiary of another establishment surveyed. This left a sample frame of 46 enterprises. The data analysis is based on 22 valid and completed responses (48% of all wooden furniture manufacturers). The remaining undelivered responses were either in the process of being completed, the enterprise was closed/uncontactable, or the respondent declined the request to participate. An outline of the main results of the establishment survey is outlined in the section below. The survey instrument for manufacturers was pre-tested and slight modifications to the instrument were suggested from the pre-test and these modifications were made. Research assistants were then trained and used to administer the surveys. Cover letters and the questionnaire survey were then delivered to the entire sample of employers and key stakeholders. The cover letters contained the consultants’ email addresses, fax and telephone numbers. The research assistants followed up the initial distribution by telephone and site visits.

Secondary Data Analysis Trade data for wood and wood products were obtained from the Barbados Statistical Service for the last five years. The data was analysed by mass and value to assist in the identification of any trends in demand, and assist in the identification of any market niches that could be exploited through the development of indigenous manufacturing.

3 Survey Results The following presentation of results is based on raw frequencies and related statistics. No higher-level statistical analysis could be undertaken due to the low number of responses that preclude the execution of such. More robust statistical analysis can only be undertaken on sample sizes that exceed 30 in number.

18

Final Report on Wooden Furniture Manufacturing in Barbados

3.1 Company Demographics Of the twenty-two companies that responded, ages ranged from 5 years to 34 years, with an average age of nineteen years, suggesting a level of maturity of companies in the sector. On average the companies provided employment for 11 persons full time, ranging from a low of 2 persons, to a maximum of 43. If the sample were considered representative of the sector, this would suggest a total employment in the sector of 500, or 0.5% of the workforce in Barbados. In terms of part-time employment, on average each company had 2 part-time employees, ranging from 0 to 20. In actuality however, only 9 companies (41%) utilised this approach to cope with fluctuations in demand. In terms of legal form of company, the majority of companies were incorporated (45.5%), while 31.8% were limited liability, with the remaining companies being partnerships or sole proprietorships. As it relates to ownership, nearly all companies had Barbadian owners, with the majority (86.4%) being 100% Barbadian, and 9.0% being jointly owned, and 4.6% being owned by North American interests. The majority of manufacturing premises were rented by the company (61.9%), while 38.1% were owned. Manufacturing space ranged from 200 square feet to 26,240 square feet (average of 7,200 square feet), while only 40.9% of the respondents operated a showroom for the company’s products. In terms of sales, approximate sales for the last financial year ranged from BDS$30,000 to BDS$3.8M, with a median sales level of over BDS$300,000. However, the outlook for sales growth varies significantly across companies, with predictions ranging from a decline of 15% to growth of 50%. On average, respondents expect growth to be in the region of 16%. As relates to capital investment, twelve respondents (55%) indicated that they had undertaken any capital investment in the last two years. Investments ranged from BDS$5000 to BDS$0.75M, with a median of BDS$18000. From this initial analysis, the ‘average’ company can be profiled, as shown in the table below. Table 3-1: Profile of the ‘Average’ Wooden Furniture Manufacturer

Another issue investigated via the questionnaire survey was the issue of changes experienced by the company in the last two years as it related to financials and other key variables. In terms of profits, the majority of respondents indicated that they had either declined (45.5%) or remained the same (27.3%). Only 27.3% indicated an increase in profits over the

previous two years. However, if this is compared to sales, 45.5% indicated an increased in the last two years, while 36.4% indicated that they had declined. For Research and Development, Exporting, and Capital Investment, the majority of respondents indicated

Variable Result Age 19 years old Full-time Employees 11 Part-time Employees 2 Legal Form Incorporated Ownership 100% Barbadian Premises Rented Manufacturing Space 7,200 square feet Company Showroom No Approximate Sales in last financial year BDS$300,000 Expected Sales Growth in next financial year 16% Capital Expenditure in last two years BDS$18,000

19

Final Report on Wooden Furniture Manufacturing in Barbados

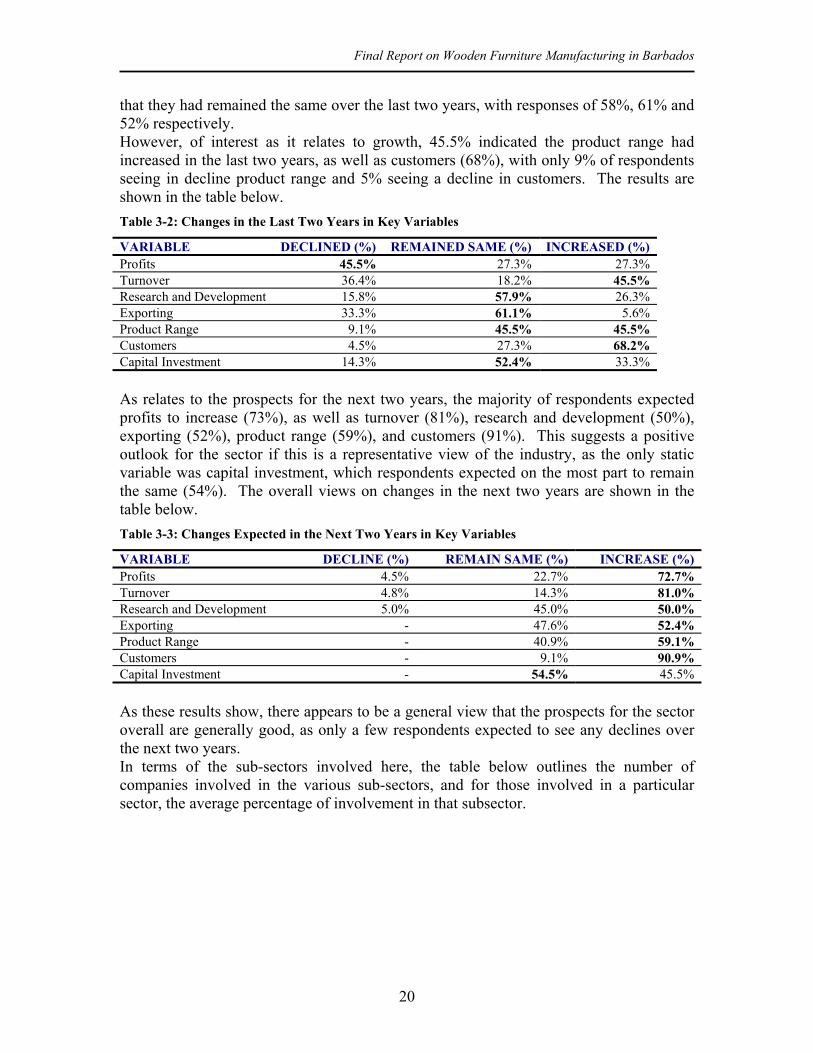

that they had remained the same over the last two years, with responses of 58%, 61% and 52% respectively. However, of interest as it relates to growth, 45.5% indicated the product range had increased in the last two years, as well as customers (68%), with only 9% of respondents seeing in decline product range and 5% seeing a decline in customers. The results are shown in the table below. Table 3-2: Changes in the Last Two Years in Key Variables

VARIABLE DECLINED (%) REMAINED SAME (%) INCREASED (%) Profits 45.5% 27.3% 27.3% Turnover 36.4% 18.2% 45.5% Research and Development 15.8% 57.9% 26.3% Exporting 33.3% 61.1% 5.6% Product Range 9.1% 45.5% 45.5% Customers 4.5% 27.3% 68.2% Capital Investment 14.3% 52.4% 33.3% As relates to the prospects for the next two years, the majority of respondents expected profits to increase (73%), as well as turnover (81%), research and development (50%), exporting (52%), product range (59%), and customers (91%). This suggests a positive outlook for the sector if this is a representative view of the industry, as the only static variable was capital investment, which respondents expected on the most part to remain the same (54%). The overall views on changes in the next two years are shown in the table below. Table 3-3: Changes Expected in the Next Two Years in Key Variables

VARIABLE DECLINE (%) REMAIN SAME (%) INCREASE (%) Profits 4.5% 22.7% 72.7% Turnover 4.8% 14.3% 81.0% Research and Development 5.0% 45.0% 50.0% Exporting - 47.6% 52.4% Product Range - 40.9% 59.1% Customers - 9.1% 90.9% Capital Investment - 54.5% 45.5% As these results show, there appears to be a general view that the prospects for the sector overall are generally good, as only a few respondents expected to see any declines over the next two years. In terms of the sub-sectors involved here, the table below outlines the number of companies involved in the various sub-sectors, and for those involved in a particular sector, the average percentage of involvement in that subsector.

20

Final Report on Wooden Furniture Manufacturing in Barbados

Table 3-4: Sub-sector Involvement

SUBSECTOR COMPANIES (%)

AVERAGE INVOLVEMENT (%)

Wooden kitchen cabinets 45.5 14.2 Wooden bathroom cabinets 31.8 7.0 Wooden bedroom cabinets 36.4 11.0 Wooden doors and windows 40.9 44.8 Other millwork 36.4 28.5 Prefabricated wood Buildings 0.0 0.0 Wooden household furniture 50.0 31.0 Upholstered Furniture 18.2 28.5 Other office furniture 36.4 20.0 Hotel/Restaurant/Institutional Furniture and Fixtures

31.8 29.3

Other 22.7 28.2 As the table above demonstrates, with the exception of the grouping Other, the bulk of resources are directed towards wooden doors and windows, hotel/restaurant/institutional fixtures and fittings, and wooden household furniture, which is also the sector in which the majority of companies also participate. The participation in wooden doors is especially interesting here as this is also one of the largest import categories in the last five years (Barbados Statistical Service, 2006).

3.2 Production Inputs and Equipment In looking at production inputs and equipment, the survey sought to elicit responses related to the types of wood used in production, their source, and types of equipment used and their vintage. As regards wood type utilised, the table below outlines the main types used and the average percentage used in production. Table 3-5: Wood Type, Number of Companies Using and Usage Levels

As the table shows, the majority of companies utilise Pine, and Plywood in their production process, while only two companies used White Mahogany and only three each used Oak, and Teak. In terms of importance in the production process, the table shows that Cedar,

Brown Mahogany, and Particle Board/MDF comprise the bulk of inputs to those companies that utilise them.

WOOD TYPE NUMBER OF COMPANIES

AVERAGE USAGE (%)

Ash 4 18.8 Cedar 9 49.7 Green Heart 4 17.9 Brown Mahogany 10 42.2 White Mahogany 2 3.0 Oak 3 5.3 Particle Board/MDF 9 29.4 Pine 14 27.8 Plywood 15 18.7 Purple Heart 8 8.0 Teak 3 5.7

21

Final Report on Wooden Furniture Manufacturing in Barbados

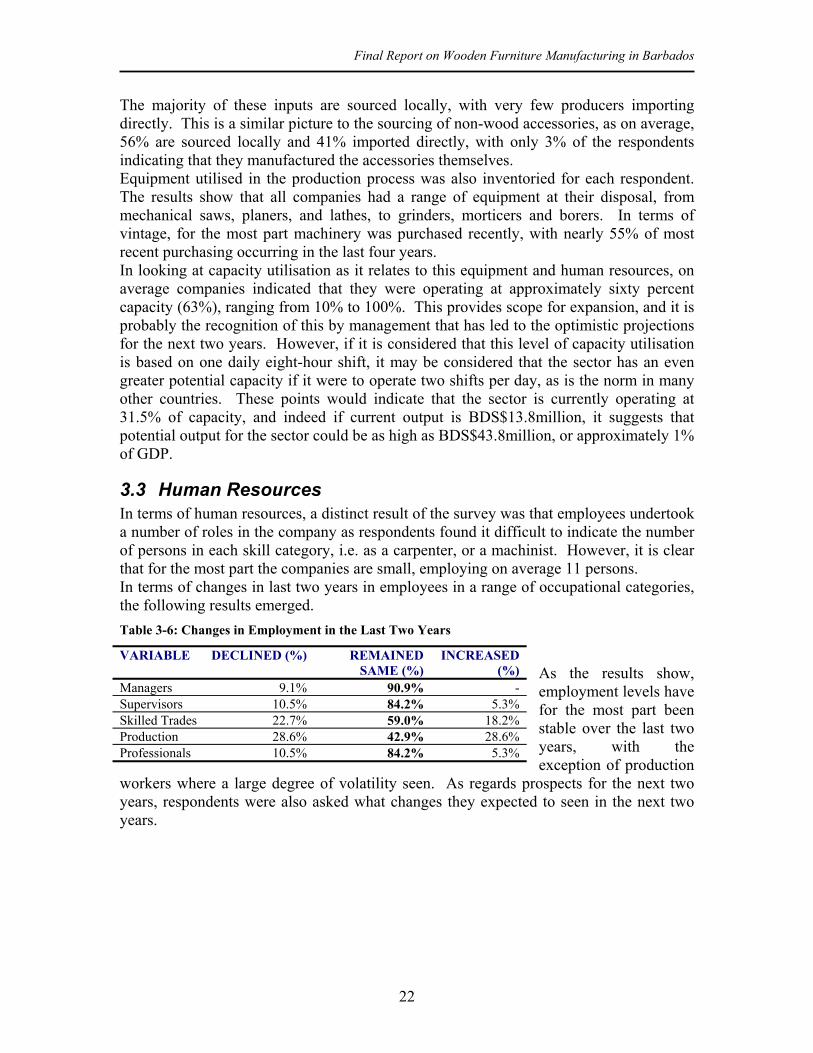

The majority of these inputs are sourced locally, with very few producers importing directly. This is a similar picture to the sourcing of non-wood accessories, as on average, 56% are sourced locally and 41% imported directly, with only 3% of the respondents indicating that they manufactured the accessories themselves. Equipment utilised in the production process was also inventoried for each respondent. The results show that all companies had a range of equipment at their disposal, from mechanical saws, planers, and lathes, to grinders, morticers and borers. In terms of vintage, for the most part machinery was purchased recently, with nearly 55% of most recent purchasing occurring in the last four years. In looking at capacity utilisation as it relates to this equipment and human resources, on average companies indicated that they were operating at approximately sixty percent capacity (63%), ranging from 10% to 100%. This provides scope for expansion, and it is probably the recognition of this by management that has led to the optimistic projections for the next two years. However, if it is considered that this level of capacity utilisation is based on one daily eight-hour shift, it may be considered that the sector has an even greater potential capacity if it were to operate two shifts per day, as is the norm in many other countries. These points would indicate that the sector is currently operating at 31.5% of capacity, and indeed if current output is BDS$13.8million, it suggests that potential output for the sector could be as high as BDS$43.8million, or approximately 1% of GDP.

3.3 Human Resources In terms of human resources, a distinct result of the survey was that employees undertook a number of roles in the company as respondents found it difficult to indicate the number of persons in each skill category, i.e. as a carpenter, or a machinist. However, it is clear that for the most part the companies are small, employing on average 11 persons. In terms of changes in last two years in employees in a range of occupational categories, the following results emerged. Table 3-6: Changes in Employment in the Last Two Years

As the results show, employment levels have for the most part been stable over the last two years, with the exception of production

workers where a large degree of volatility seen. As regards prospects for the next two years, respondents were also asked what changes they expected to seen in the next two years.

VARIABLE DECLINED (%) REMAINED SAME (%)

INCREASED (%)

Managers 9.1% 90.9% - Supervisors 10.5% 84.2% 5.3% Skilled Trades 22.7% 59.0% 18.2% Production 28.6% 42.9% 28.6% Professionals 10.5% 84.2% 5.3%

22

Final Report on Wooden Furniture Manufacturing in Barbados

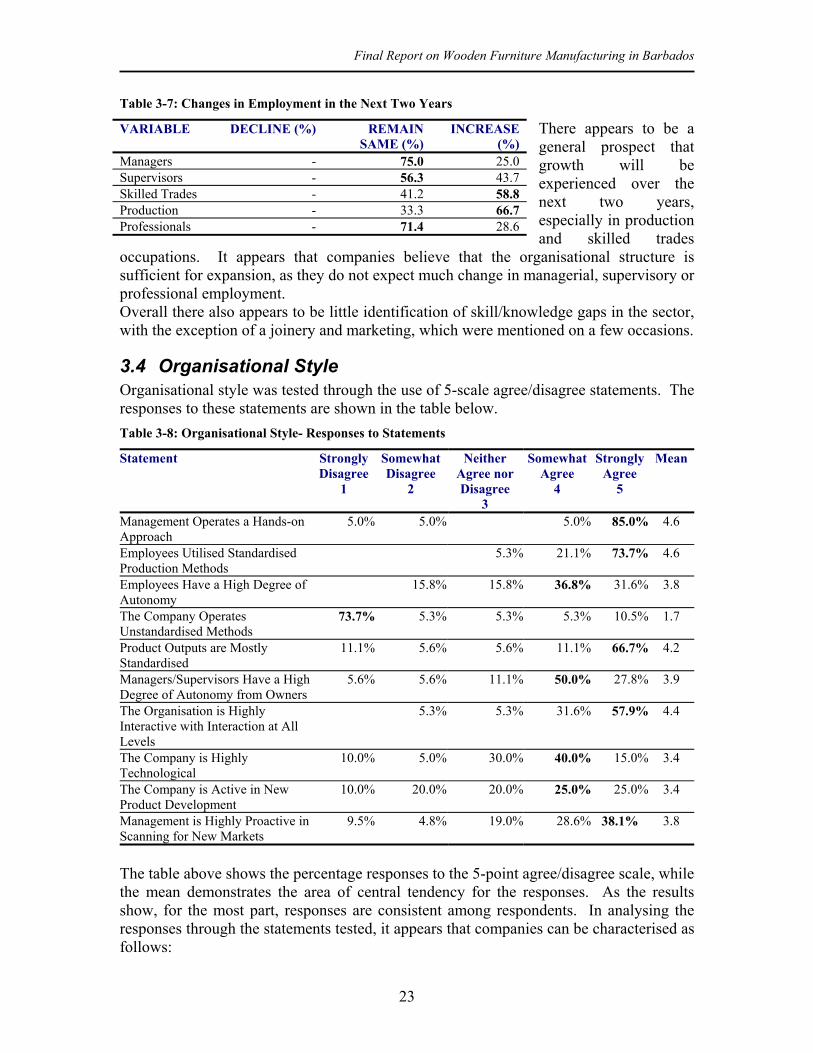

Table 3-7: Changes in Employment in the Next Two Years

There appears to be a general prospect that growth will be experienced over the next two years, especially in production and skilled trades

occupations. It appears that companies believe that the organisational structure is sufficient for expansion, as they do not expect much change in managerial, supervisory or professional employment.

VARIABLE DECLINE (%) REMAIN SAME (%)

INCREASE (%)

Managers - 75.0 25.0 Supervisors - 56.3 43.7 Skilled Trades - 41.2 58.8 Production - 33.3 66.7 Professionals - 71.4 28.6

Overall there also appears to be little identification of skill/knowledge gaps in the sector, with the exception of a joinery and marketing, which were mentioned on a few occasions.

3.4 Organisational Style Organisational style was tested through the use of 5-scale agree/disagree statements. The responses to these statements are shown in the table below. Table 3-8: Organisational Style- Responses to Statements

Statement Strongly Disagree

1

Somewhat Disagree

2

Neither Agree nor Disagree

3

Somewhat Agree

4

Strongly Agree

5

Mean

Management Operates a Hands-on Approach

5.0% 5.0% 5.0% 85.0% 4.6

Employees Utilised Standardised Production Methods

5.3% 21.1% 73.7% 4.6

Employees Have a High Degree of Autonomy

15.8% 15.8% 36.8% 31.6% 3.8

The Company Operates Unstandardised Methods

73.7% 5.3% 5.3% 5.3% 10.5% 1.7

Product Outputs are Mostly Standardised

11.1% 5.6% 5.6% 11.1% 66.7% 4.2

Managers/Supervisors Have a High Degree of Autonomy from Owners

5.6% 5.6% 11.1% 50.0% 27.8% 3.9

The Organisation is Highly Interactive with Interaction at All Levels

5.3% 5.3% 31.6% 57.9% 4.4

The Company is Highly Technological

10.0% 5.0% 30.0% 40.0% 15.0% 3.4

The Company is Active in New Product Development

10.0% 20.0% 20.0% 25.0% 25.0% 3.4

Management is Highly Proactive in Scanning for New Markets

9.5% 4.8% 19.0% 28.6% 38.1% 3.8

The table above shows the percentage responses to the 5-point agree/disagree scale, while the mean demonstrates the area of central tendency for the responses. As the results show, for the most part, responses are consistent among respondents. In analysing the responses through the statements tested, it appears that companies can be characterised as follows:

23

Final Report on Wooden Furniture Manufacturing in Barbados

1. Hands-on management style 2. Standardised production methods and products 3. Employees with some degree of autonomy 4. Management with some degree of autonomy from owners 5. Interactive among all levels 6. Mediumly technological 7. Intermediately active in new product development 8. Some proactivity in new market development

In this manner, the companies appear constrained in growth due to organisational style operated, and a lack of use of technology (especially where over seventy percent (72.7%) indicated that their technological intensiveness was either ‘Low’ or ‘Medium’). This constraint is especially where managers are hampered in their use of proactive, new undertakings due to a hands-on/involved approach to production. In this sense, it appears managers are not managing in the sense of dynamism in new product development and market scanning, but managing the production process itself. In addition to these areas tested, respondents were also asked to identify organisational membership and support services used. These issues demonstrate the use of networking and proactive financial management. The results demonstrate findings seen in previous studies on manufacturing in Barbados (Lashley 2002), where for the most part companies are not members of support organisations or utilise any support services. For the seventeen (22) respondents analysed, only four (4) were members of the Barbados Manufacturers’ Association, and three (3) were members of the Small Business Association. In terms of support services, nine (9) companies indicated that they had utilised the services of BIDC. Outside of these formal organisations, respondents were also asked to indicate whether they participated in any cooperative arrangement with other companies in the sector. As with the other variables tested for networking activity, only six companies (27% of respondents) indicated any formal or informal arrangement. Related again to the issue of networking is attendance at trade shows for goods and equipment as both an exhibitor and a customer. Again the results indicate little involvement in this area, as only six respondents (27%) attended trade shows annually as an exhibitor for finished goods, and merely seven (32%) as a consumer. The results are less promising for attendance at trade shows for equipment, where the relevant numbers are one (4%) as a exhibitor, and three (12%) as a consumer.

3.5 Supply Chain Issues The competitive environment in which these companies operate can be considered moderately high, as over eighty percent (85%) indicate that it is either Medium (60%), High (10%), or Very High (15). However, in looking at the location of this competition, respondents indicated that it was local on the most part (60% of respondents indicated this as one of their main competitors location). However, the Caribbean, USA and the Far East were also considered main sources of competition. In looking at more concrete supply chain issues, the main destination of output is the private consumer, where on average 39% of output is sold. The other customers are the

24

Final Report on Wooden Furniture Manufacturing in Barbados

construction industry (25% of output), retailers (13%), and the hotel/restaurant industry (14%). The remaining output was sold to ‘other’ customers.

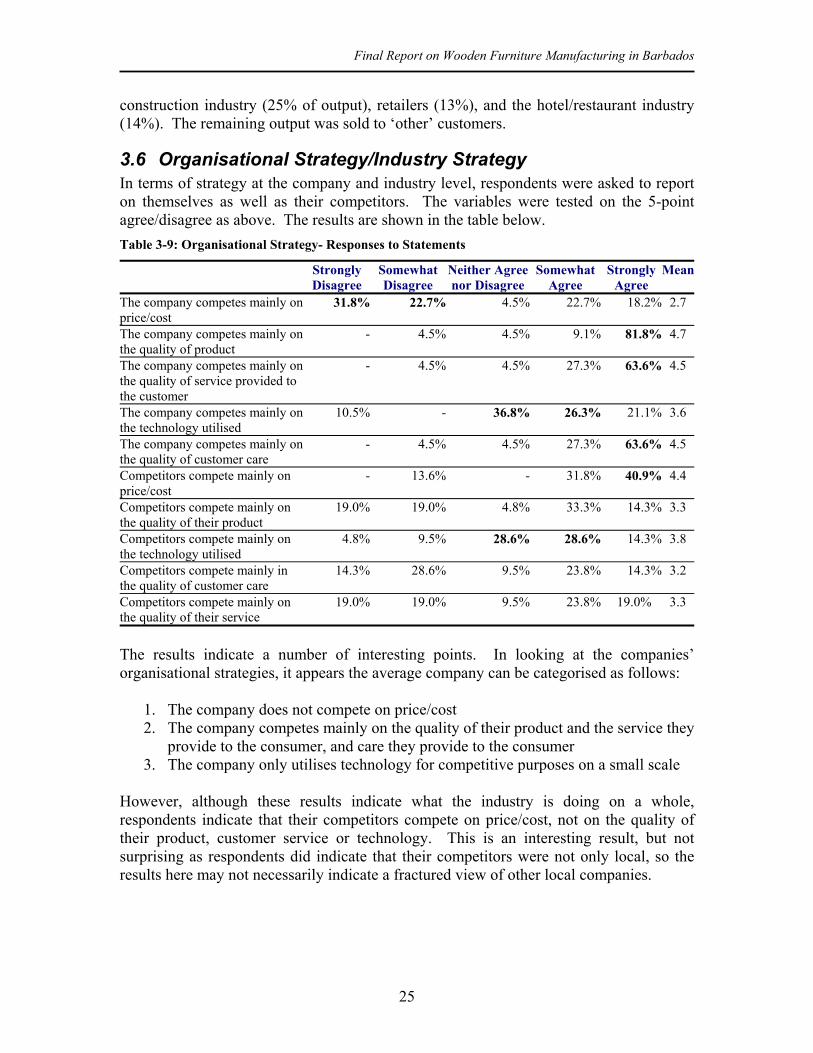

3.6 Organisational Strategy/Industry Strategy In terms of strategy at the company and industry level, respondents were asked to report on themselves as well as their competitors. The variables were tested on the 5-point agree/disagree as above. The results are shown in the table below. Table 3-9: Organisational Strategy- Responses to Statements

Strongly Disagree

Somewhat Disagree

Neither Agree nor Disagree

Somewhat Agree

Strongly Agree

Mean

The company competes mainly on price/cost

31.8% 22.7% 4.5% 22.7% 18.2% 2.7

The company competes mainly on the quality of product

- 4.5% 4.5% 9.1% 81.8% 4.7

The company competes mainly on the quality of service provided to the customer

- 4.5% 4.5% 27.3% 63.6% 4.5

The company competes mainly on the technology utilised

10.5% - 36.8% 26.3% 21.1% 3.6

The company competes mainly on the quality of customer care

- 4.5% 4.5% 27.3% 63.6% 4.5

Competitors compete mainly on price/cost

- 13.6% - 31.8% 40.9% 4.4

Competitors compete mainly on the quality of their product

19.0% 19.0% 4.8% 33.3% 14.3% 3.3

Competitors compete mainly on the technology utilised

4.8% 9.5% 28.6% 28.6% 14.3% 3.8

Competitors compete mainly in the quality of customer care

14.3% 28.6% 9.5% 23.8% 14.3% 3.2

Competitors compete mainly on the quality of their service

19.0% 19.0% 9.5% 23.8% 19.0% 3.3

The results indicate a number of interesting points. In looking at the companies’ organisational strategies, it appears the average company can be categorised as follows:

1. The company does not compete on price/cost 2. The company competes mainly on the quality of their product and the service they

provide to the consumer, and care they provide to the consumer 3. The company only utilises technology for competitive purposes on a small scale

However, although these results indicate what the industry is doing on a whole, respondents indicate that their competitors compete on price/cost, not on the quality of their product, customer service or technology. This is an interesting result, but not surprising as respondents did indicate that their competitors were not only local, so the results here may not necessarily indicate a fractured view of other local companies.

25

Final Report on Wooden Furniture Manufacturing in Barbados

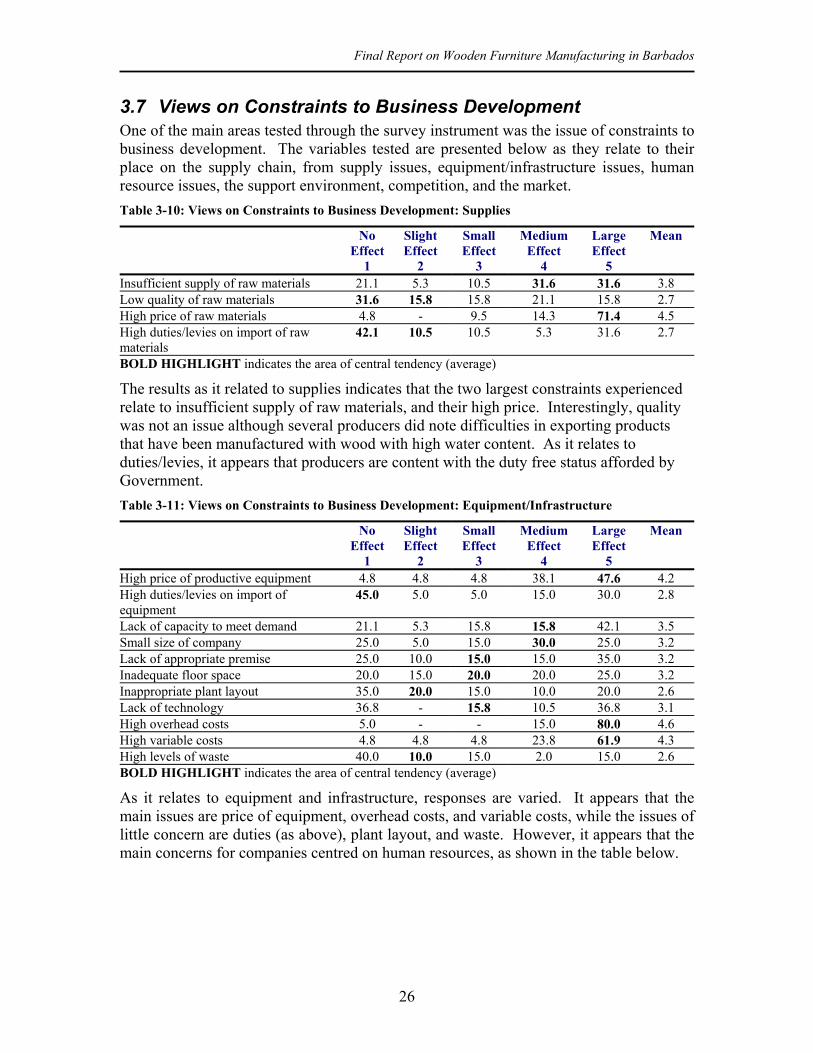

3.7 Views on Constraints to Business Development One of the main areas tested through the survey instrument was the issue of constraints to business development. The variables tested are presented below as they relate to their place on the supply chain, from supply issues, equipment/infrastructure issues, human resource issues, the support environment, competition, and the market. Table 3-10: Views on Constraints to Business Development: Supplies

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

Insufficient supply of raw materials 21.1 5.3 10.5 31.6 31.6 3.8 Low quality of raw materials 31.6 15.8 15.8 21.1 15.8 2.7 High price of raw materials 4.8 - 9.5 14.3 71.4 4.5 High duties/levies on import of raw materials

42.1 10.5 10.5 5.3 31.6 2.7

BOLD HIGHLIGHT indicates the area of central tendency (average)

The results as it related to supplies indicates that the two largest constraints experienced relate to insufficient supply of raw materials, and their high price. Interestingly, quality was not an issue although several producers did note difficulties in exporting products that have been manufactured with wood with high water content. As it relates to duties/levies, it appears that producers are content with the duty free status afforded by Government. Table 3-11: Views on Constraints to Business Development: Equipment/Infrastructure

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

High price of productive equipment 4.8 4.8 4.8 38.1 47.6 4.2 High duties/levies on import of equipment

45.0 5.0 5.0 15.0 30.0 2.8

Lack of capacity to meet demand 21.1 5.3 15.8 15.8 42.1 3.5 Small size of company 25.0 5.0 15.0 30.0 25.0 3.2 Lack of appropriate premise 25.0 10.0 15.0 15.0 35.0 3.2 Inadequate floor space 20.0 15.0 20.0 20.0 25.0 3.2 Inappropriate plant layout 35.0 20.0 15.0 10.0 20.0 2.6 Lack of technology 36.8 - 15.8 10.5 36.8 3.1 High overhead costs 5.0 - - 15.0 80.0 4.6 High variable costs 4.8 4.8 4.8 23.8 61.9 4.3 High levels of waste 40.0 10.0 15.0 2.0 15.0 2.6 BOLD HIGHLIGHT indicates the area of central tendency (average)

As it relates to equipment and infrastructure, responses are varied. It appears that the main issues are price of equipment, overhead costs, and variable costs, while the issues of little concern are duties (as above), plant layout, and waste. However, it appears that the main concerns for companies centred on human resources, as shown in the table below.

26

Final Report on Wooden Furniture Manufacturing in Barbados

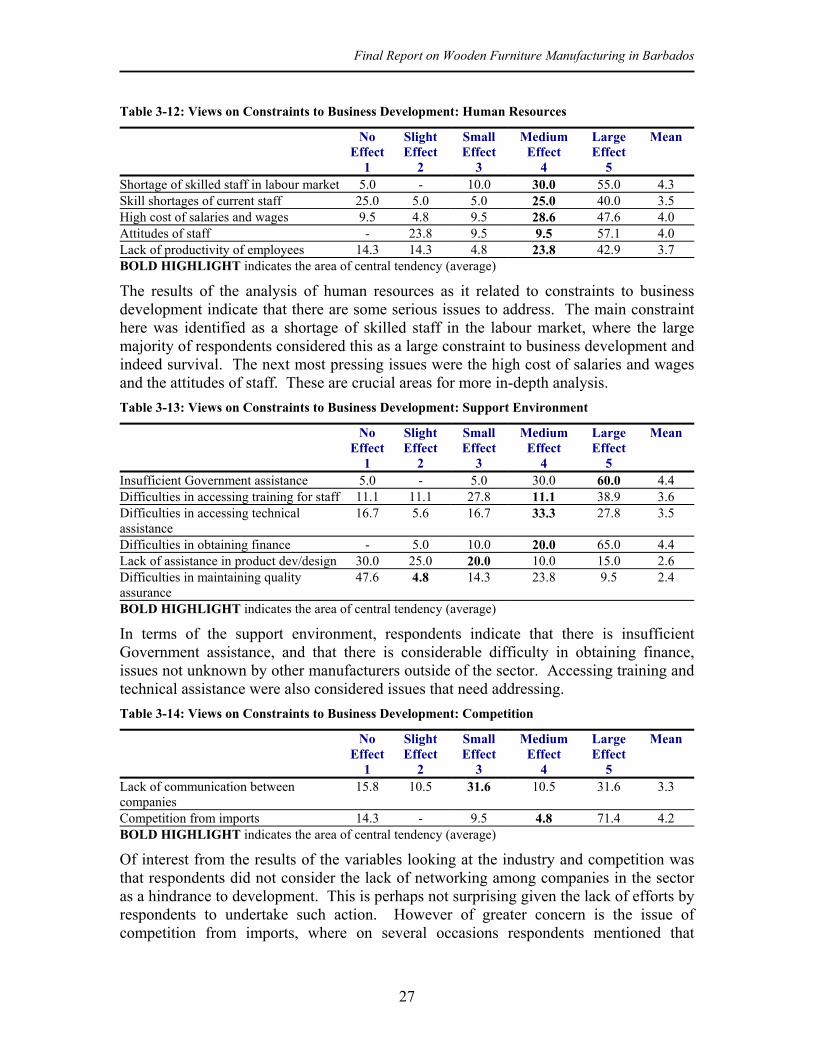

Table 3-12: Views on Constraints to Business Development: Human Resources

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

Shortage of skilled staff in labour market 5.0 - 10.0 30.0 55.0 4.3 Skill shortages of current staff 25.0 5.0 5.0 25.0 40.0 3.5 High cost of salaries and wages 9.5 4.8 9.5 28.6 47.6 4.0 Attitudes of staff - 23.8 9.5 9.5 57.1 4.0 Lack of productivity of employees 14.3 14.3 4.8 23.8 42.9 3.7 BOLD HIGHLIGHT indicates the area of central tendency (average)

The results of the analysis of human resources as it related to constraints to business development indicate that there are some serious issues to address. The main constraint here was identified as a shortage of skilled staff in the labour market, where the large majority of respondents considered this as a large constraint to business development and indeed survival. The next most pressing issues were the high cost of salaries and wages and the attitudes of staff. These are crucial areas for more in-depth analysis. Table 3-13: Views on Constraints to Business Development: Support Environment

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

Insufficient Government assistance 5.0 - 5.0 30.0 60.0 4.4 Difficulties in accessing training for staff 11.1 11.1 27.8 11.1 38.9 3.6 Difficulties in accessing technical assistance

16.7 5.6 16.7 33.3 27.8 3.5

Difficulties in obtaining finance - 5.0 10.0 20.0 65.0 4.4 Lack of assistance in product dev/design 30.0 25.0 20.0 10.0 15.0 2.6 Difficulties in maintaining quality assurance

47.6 4.8 14.3 23.8 9.5 2.4

BOLD HIGHLIGHT indicates the area of central tendency (average)

In terms of the support environment, respondents indicate that there is insufficient Government assistance, and that there is considerable difficulty in obtaining finance, issues not unknown by other manufacturers outside of the sector. Accessing training and technical assistance were also considered issues that need addressing. Table 3-14: Views on Constraints to Business Development: Competition

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

Lack of communication between companies

15.8 10.5 31.6 10.5 31.6 3.3

Competition from imports 14.3 - 9.5 4.8 71.4 4.2 BOLD HIGHLIGHT indicates the area of central tendency (average)

Of interest from the results of the variables looking at the industry and competition was that respondents did not consider the lack of networking among companies in the sector as a hindrance to development. This is perhaps not surprising given the lack of efforts by respondents to undertake such action. However of greater concern is the issue of competition from imports, where on several occasions respondents mentioned that

27

Final Report on Wooden Furniture Manufacturing in Barbados

uneducated consumers are causing damage to the prospects of the industry by purchasing low quality, cheap goods from the Far East especially. This has led to deterioration in the customer base for manufacturers, and incorrect assumptions that ‘local’ quality is poor, as consumers do not realise that the goods that they are purchasing are imported and not actually produced locally. Table 3-15: Views on Constraints to Business Development: Market

No Effect

1

Slight Effect

2

Small Effect

3

Medium Effect

4

Large Effect

5

Mean

Difficulties in exporting 35.3 11.8 11.8 11.8 29.4 2.9 Difficulties in finding markets abroad 27.8 22.2 5.6 22.2 22.2 2.9 Lack of demand domestically 50.0 5.0 15.0 10.0 20.0 2.4 Difficulties in marketing 14.3 4.8 23.8 14.3 42.9 3.7 Late payment by customers 14.3 19.0 23.8 9.5 33.3 3.3 BOLD HIGHLIGHT indicates the area of central tendency (average)

The last issue investigated in terms of constraints to business development related to markets in general. It appears that exporting and finding markets abroad are not necessarily a problem, nor is late payment by customers. However difficulties in marketing do appear as an important issue. Although finding foreign markets was not viewed as a problem in this instance, the large quantity of products expected to be ordered was seen as a challenge, one that cannot be overcome without joint venture and sectoral cooperation. In addition, it was recognised that factories would need to be retooled to realize higher levels of efficiency. Of interest here, and perhaps a reason for the optimistic outlook for the sector as examined earlier, is the issue of domestic demand, where over fifty percent (55%) of respondents indicated that this had either no effect or only a slight effect on the development of their business, suggesting that local demand is currently high. Overall, in looking at constraints to business development, the main issues relate to:

The high price of raw materials • • • • • • •

The high price of productive equipment High overhead and variable costs A lack of skilled staff in the labour market A lack of Government assistance Difficulty in obtaining finance The high level of competition from low quality/cheap imports, mainly from the Far East.

All of these issues rated as having more than a ‘medium’ effect on business development. In the case of architectural millwork, respondents thought that financiers and Government undervalued the contribution of this sub-sector and hence no special attention was offered to plants that specialized in this area. This was despite the fact that the millwork sector was viewed as more technical and provided manufacturers with higher margins based on the fact that it was a ‘high-end’ product.

28

Final Report on Wooden Furniture Manufacturing in Barbados