Embed Size (px)

DESCRIPTION

Â

Citation preview

Mighty River Power

Interim Report 31 December 2004

01 Highlights 2004

04 Board and Chief Executive Report

09 Interim Financial Statements

19 Directory

Mighty River Power Limited Interim Report 31 December 2004

Highlights 2004

$77.3 million Net surplus after taxation

3244 GWh Record total generation volumes

48% savings Gas saved at Southdown

320 MW Consents lodged for a 320MW thermal plant at Marsden Point

Top call centre Mercury Energy the best energy retailer in

2004 Customer Relationship Management Contact Centre Awards

50% increase Gas customer base passes 15,000

$45 million Capital expenditure increases by 250%

Mighty River Power Limited Interim Report 31 December 2004 1

2004

2003

2002

2001

2000

1999

$56.6 million

$65.0 million

$25.8 million

$79.4 million

$95.3 million

$135.7 million

Operating Surplus before Interest, Non-recurring Items and Taxation for 6 months to 31 December

2004

2003

2002

2001

2000

1999

42.9 percent

44.8 percent

48.3 percent

55.9 percent

62.0 percent

61.3 percent

Total Equity/Total Assets at 31 December

2004

2003

2002

2001

2000

1999

$30.4 million

$37.3 million

$14.0 million

$99.8 million

$51.4 million

$77.3 million

Net Surplus after Taxation for 6 months to 31 December

Mighty River Power Limited Interim Report 31 December 20042

2004

2003

2002

2001

2000

1999

$301.2 million

$234.3 million

$352.2 million

$235.1 million

$305.8 million

$306.8 million

Total Operating Revenue for 6 months to 31 December

2004

2003

2002

2001

2000

1999

$57.9 million

$52.3 million

$20.0 million

$47.4 million

$81.6 million

$123.6 million

Operating Cashflow for 6 months to 31 December

2004

2003

2002

2001

2000

1999

45.5 percent

40.5 percent

41.4 percent

36.5 percent

30.1 percent

32.3 percent

Net Debt/Net Debt + Equity at 31 December

Mighty River Power Limited Interim Report 31 December 2004 3

Board and Chief Executive Report

Mok

ai g

eoth

erm

al e

xpan

sion

4 Mighty River Power Limited Interim Report 31 December 2004

On behalf of the Board and Management, we are pleased

to report on Mighty River Power’s performance for the six

months to 31 December, 2004.

Highlights: Mighty River Power has continued its recent run

of sound financial results with another strong performance

in the first half of the 2004/05 financial year.

This period which is traditionally our strongest due to

high customer demand over winter, combined with record

hydro production, to provide a net surplus after taxation of

$77.3 million in the period to December 31, 2004. That is up

50% on the comparable period last year ($51.4 million).

The much wetter than normal winter and spring in the

Waikato/Taupo catchment meant our hydro system generated

very good volumes. High national inflow levels meant that

wholesale electricity prices were very subdued, allowing us

to manage production from the Southdown co-generation

plant to reduce our gas costs.

Retail demand also continued to grow with new

connections continuing at a solid pace on the back of the

strong housing market, particularly in our key Auckland

market. We were also able to attract new customers from

our competitors and our retail gas customer base has

now passed 15,000. We also have 307,000 electricity

customers, 2.3% up on June.

Those successes in the retail market and the continuing

growth in commercial demand for our financial products

offset the revenue loss associated with weak wholesale prices

resulting in only a small gain on 2003 revenues.

Operating cashflows were up approximately 50% at $123.6

million on the comparable period last year ($81.6 million) as

a result of the strong hydro production and lower gas costs.

Dividends of $105 million relating to the year ended 30 June

2004 were paid out during the period under review.

Operating surplus before interest, non-recurring items

and taxation was $135.7 million compared to $95.3 million

in the same period last year. Capital expenditure increased

by 250% to $45 million primarily related to geothermal

exploration and development activities.

Generation: Our decision nearly two years ago to acquire full

control of the Southdown co-generation plant to balance our

hydro and non-hydro based generation assets is paying

dividends. We were able to reduce the use of gas at Southdown

when wholesale electricity prices did not justify using gas.

This lower utilisation of Southdown in wet periods

has provided significant energy and cost efficiency gains,

whilst preserving the ability to provide sustained firm

capacity should national storage levels drop or wholesale

prices increase. Hydro generation volumes of 2631 GWh

compared to 2058 GWh in the same period last year reflect

that good hydrology and comparable Southdown generation

of 459 GWh in 2003 and 224 GWh in 2004 reflect lower gas

use. Geothermal generation also ran at record levels at

Rotokawa. Total generation volumes of 3244 GWh compare

to 2839 GWh in the previous comparable period.

For our business the exciting story around generation is

centred on our drive to expand our current portfolio, through

a range of fuel options, to help meet the predicted growth in

demand in New Zealand.

That has led to the biggest geothermal exploration

programme in New Zealand in the past twenty years with

an initial $20 million programme at Putauaki concluded

and now under test. A $20 million programme at Rotokawa

to prov ide additional production and re-injection

capability to the existing plant, and a potential expansion,

is nearing completion. Plans for generation expansion at the

Rotokawa Field, in conjunction with the Tauhara North No. 2

Trust, are progressing.

Consents were also lodged for exploratory drilling in the

Mangakino area as we look to develop a new geothermal

site in the region. Analysis and plans for a possible geothermal

plant of over 50MW at Kawerau also continue. Once analysis

is complete a decision will be made with our iwi partners about

progressing this project to the consents phase.

The 40MW geothermal expansion at Mokai by the Tuaropaki

Power Company, where we have a 25% equity partnership

with the Tuaropaki Trust, is on schedule to be on-line in late

5Mighty River Power Limited Interim Report 31 December 2004

autumn 2005 providing a timely boost to energy supplies prior

to winter. This project alone will meet around 25% of the

country’s energy demand growth this year.

Consents for a 320 MW coal-fired plant at the existing

Marsden Point plant near Whangarei were lodged just before

Christmas and we continue to work through a thorough

consultation process. We are confident that Marsden B offers

the best new coal fired development option in New Zealand

and provides a prudent way to diversify New Zealand’s medium

term energy supply risks, especially in the scenario where no

significant new domestic gas is commercially developed before

the end of the decade.

We are actively seeking access to several sites to

undertake monitoring of windflows with a view to identifying

sites for economic wind generation. A number of small hydro

development options are under consideration and round out

our portfolio of potential generation developments.

Customers: It has also been a successful first half for the

Mercury Energy retail business with continued strong growth

of electricity and gas customers. Successful acquisition

campaigns have complemented our innovative products which

continue to retain and attract customers.

Following the Government’s introduction of regulations requiring

a low fixed charge tariff we took the opportunity in October to

restructure our pricing plans. Our customers were automatically

moved to the best plan based on their previous usage, providing

we had their usage history for the past twelve months.

Our excellent customer ser vice standards were

recognised through Mercury Energy’s call centre winning a

Gold Award in the 2004 Customer Relationship Management

Contact Centre Awards. We were chosen as the best customer

service provider in the energy retail sector and one of the

top three in all sectors.

Our support of community based initiatives was enhanced

with the establishment of the Star Supporters Club. Our

customers can automatically donate to Starship Children’s

Health through their bills, a facility that has already raised

more than $70,000 which will be used to purchase a Mobile

Image Intensifier for the hospital. We also now support the

Mercury Energy Pohutakawa Festival on the Coromandel

Peninsula while our support for Christmas in the Park

(Auckland), Carols by Candlelight (Auckland) and Christmas

at the Lake (Hamilton) continues along with the lighting of

prominent Auckland landmarks.

2004

2003

2002

2001

2000

1999

Total Generation Volumes for 6 months to 31 December

0

GW

h

500

1000

1500

2000

2500

3000

3500

Hydro Cogeneration Geothermal* Biomass*

* Mighty River Power does not own 100% of these assets

6 Mighty River Power Limited Interim Report 31 December 2004

Metrix: Industry leading levels continue to be the focus of our

Metrix metering business with new housing and switches

between electricity businesses creating steady demand

for our services.

Residential growth in the Auckland region has also provided

a strong growth platform for new meter installations.

Summary: While our current focus at Mighty River Power is

on driving our generation expansion programme, that focus

is not possible without the ongoing support of a strongly

performing company with secure funding.

Our generation business is a well balanced and efficient

unit that has performed very well to take advantage of

good hydro conditions in the past six months. Our different

fuel sources have been used in an efficient manner to meet

market demand and contribute to supply security.

Our retail business is thriving on a mix of innovative

products that attract customers from other competitors,

and ensures we capture a good share of the new business

generated by residential growth. Our commercial sales

have also experienced superior growth from offering

customers the benefits of our integrated energy business

model by removing price volatility.

None of that would have been possible without the

focus and efforts our staff and we thank the teams within

Mighty River Power for their ongoing support.

That we are in such a good position in 2005 is also testimony

to the stewardship of our founding chairman Rob Challinor

who retired from the company at the end of 2004 after six

years at the helm.

Our balance sheet was initially the weakest of the three

new enterprises created in 1999 and much of our focus in the

early years was on strengthening it by ensuring we were a

very efficient operator with excellent capital management.

Under Rob’s leadership we have evolved into a business

that is generating sound cash flow, is growing and is in a

financial position to support an extensive generation

development programme. The company and the current Board

are indebited to Rob for his major contribution to the success

of Mighty River Power. We look to the future with confidence

that this success will be continually enhanced.

Carole Durbin

ChairDoug Heffernan

Chief Executive

7Mighty River Power Limited Interim Report 31 December 2004

MT

surv

ey T

okor

oa

8 Mighty River Power Limited Interim Report 31 December 2004

Interim Financial Statements For the six months ended 31 December 2004

10 Consolidated Statement of Financial Performance

11 Consolidated Statement of Movements In Equity

12 Consolidated Statement of Financial Position

14 Consolidated Statement of Cash Flows

15 Notes ot the Consolidated Interim Financial Statements

Mighty River Power Limited Interim Report 2004 9

Consolidated Statement of Financial Performance for the six months ended 31 December 2004

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 note $000 $000

774,654 Sales 414,775 391,870

(185,844) Less line and metering charges (113,641) (90,777)

2,341 Interest income 1,695 990

8,097 Other revenue 3,980 3,738

599,248 Total Operating Revenue 306,809 305,821

199,551 Operating surplus before interest and non-recurring items 135,686 95,326

2,341 Interest income 1,695 990

(31,742) Interest expense (18,448) (16,222)

(14,705) Non-recurring items 2 0 0

155,445 Surplus Before Taxation 118,933 80,094

(55,748) Taxation expense 3 (41,536) (28,571)

99,697 Surplus After Taxation 77,397 51,523

131 Share of associate net (deficit) surplus (103) (80)

99,828 Net Surplus After Taxation 77,294 51,443

The notes set out on pages 15 to 18 form part of, and should be read in conjunction with, these interim financial statements.

10 Mighty River Power Limited Interim Report 31 December 2004

The notes set out on pages 15 to 18 form part of, and should be read in conjunction with, these interim financial statements.

Consolidated Statement of Movements in Equity for the six months ended 31 December 2004

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

861,696 Equity at Beginning of the Period 886,524 861,696

99,828 Net surplus after taxation 77,294 51,443

99,828 Total Recognised Revenues and Expenses for the Period 77,294 51,443

Distributions to owners:

(75,000) Special dividend 0 0

0 Final dividend paid for 2004 (30,000) 0

886,524 Equity at End of the Period 933,818 913,139

11Mighty River Power Limited Interim Report 31 December 2004

30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

Equity

377,561 Share capital 377,561 377,561

508,963 Reserves 556,257 535,578

886,524 933,818 913,139

Non-current Liabilities

1,204 Energy contracts 1,204 51,387

329,821 Loans 365,821 384,459

331,025 367,025 435,846

Current Liabilities

0 Bank overdraft 0 1,665

91,863 Payables and accruals 84,417 63,833

75,000 Provision for dividend 0 0

4,254 Provisions 3,411 3,332

2,032 Provision for taxation 22,653 12,994

24,114 Deferred taxation 24,029 23,921

0 Energy contracts – current portion 0 9,647

98,494 Loans – current portion 89,225 8,000

295,757 223,735 123,392

1,513,306 Total Equity and Liabilities 1,524,578 1,472,377

Consolidated Statement of Financial Position As at 31 December 2004

The notes set out on pages 15 to 18 form part of, and should be read in conjunction with, these interim financial statements.

12 Mighty River Power Limited Interim Report 31 December 2004

30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

Non-current Assets

1,369,319 Property, plant and equipment 1,380,689 1,357,846

2,352 Investment in associate 13,278 4,255

15,494 Other non-current assets 13,981 15,626

1,387,165 1,407,948 1,377,727

Current Assets

3,457 Cash 3,707 0

0 Short term deposits 5,000 0

1,985 Investment in associate 0 0

116,649 Receivables and prepayments 104,639 91,507

4,050 Inventories 3,284 3,143

126,141 116,630 94,650

1,513,306 Total Assets 1,524,578 1,472,377

The Board of Directors authorised the issue of the interim financial statements on 23 February 2005

Consolidated Statement of Financial Position (continued) As at 31 December 2004

The notes set out on pages 15 to 18 form part of, and should be read in conjunction with, these interim financial statements.

13Mighty River Power Limited Interim Report 31 December 2004

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 note $000 $000

Cash Flows from Operating Activities

Cash was provided from (applied to):

574,572 Receipts from customers 318,117 309,546

1,426 Interest received 1,707 1,025

(408,544) Payments to suppliers and employees (157,051) (202,791)

(30,966) Interest paid (18,151) (16,156)

(47,500) Taxation paid (21,000) (10,000)

88,988 Net Cash Inflow from Operating Activities 4 123,622 81,624

Cash Flows from Investing Activities

Cash was provided from (applied to):

436 Sale of property, plant and equipment 41 92

2,710 Proceeds from investments 4,725 2,581

(47,120) Purchase of property, plant and equipment (31,869) (10,172)

(3,983) Purchase of other non-current assets 0 (2,360)

0 Purchase of associate (13,000) 0

(47,957) Net Cash Outflow from Investing Activities (40,103) (9,859)

Cash Flows from Financing Activities

Cash was provided from (applied to):

0 Loan advances 26,731 0

(42,456) Loans repaid 0 (78,312)

0 Dividends paid (105,000) 0

(42,456) Net Cash Outflow from Financing Activities (78,269) (78,312)

(1,425) Net Increase (Decrease) in Cash Held 5,250 (6,547)

4,882 Cash Balance at Beginning of the Period 3,457 4,882

3,457 Cash Balance at End of the Period 8,707 (1,665)

Cash balance comprises:

3,457 Cash (bank overdraft) 3,707 (1,665)

0 Short term deposits 5,000 0

3,457 8,707 (1,665)

Consolidated Statement of Cash Flows for the six months ended 31 December 2004

The notes set out on pages 15 to 18 form part of, and should be read in conjunction with, these interim financial statements.

14 Mighty River Power Limited Interim Report 31 December 2004

Notes to the Consolidated Financial Statements for the six months ended 31 December 2004

1. Statement of Accounting Policies

The interim financial statements presented here are the unaudited consolidated financial statements of Mighty River Power Limited

for the six months ended 31 December 2004.

These interim financial statements have been prepared in accordance with FRS-24 Interim Financial Statements, and should be

read in conjunction with the Annual Report for the period ended 30 June 2004. The accounting policies used in the preparation of

these interim financial statements are consistent with those used in the annual financial statements and the previously published

interim financial statements.

Certain prior year comparatives have been restated to conform with current period presentation.

2. Non-recurring Items

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

(14,098) Exit from Contracts for Differences 0 0

600 Revaluation of office land and buildings 0 0

(1,207) Other 0 0

(14,705) 0 0

Exit from Contracts for Differences

On 28 June 2004 the Group exited from two Contracts for Differences. The amount of $14,098,000 relates to the net loss from

exiting these arrangements, including a termination payment and reversal of a provision for an onerous energy contract.

15Mighty River Power Limited Interim Report 31 December 2004

Notes to the Consolidated Financial Statements (continued) for the six months ended 31 December 2004

3. Taxation Expense

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

155,445 Surplus before taxation 118,933 80,094

51,297 Taxation at 33 cents 39,248 26,431

Taxation effect of permanent differences:

4,395 Other permanent differences 2,288 2,140

56 Prior year adjustments 0 0

55,748 Taxation expense 41,536 28,571

Analysis of taxation expense:

54,427 Current taxation 41,621 27,443

1,321 Deferred taxation (85) 1,128

55,748 41,536 28,571

16 Mighty River Power Limited Interim Report 31 December 2004

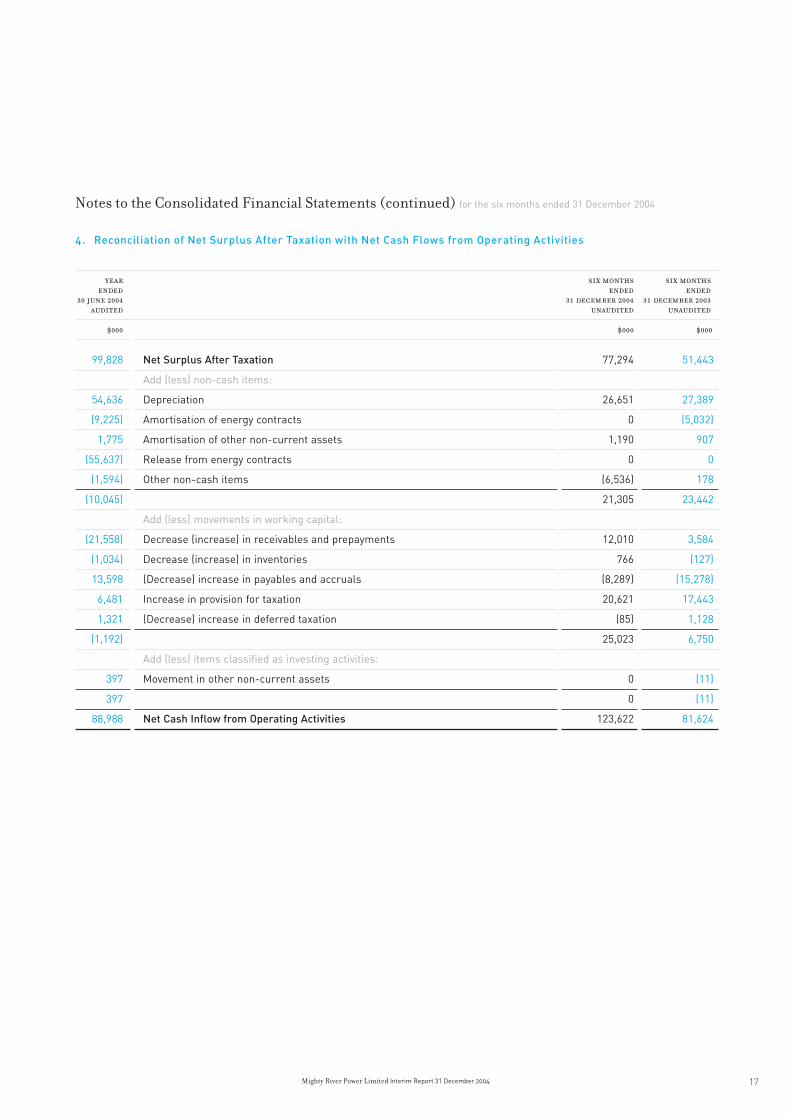

4. Reconciliation of Net Surplus After Taxation with Net Cash Flows from Operating Activities

year six months six months ended ended ended 30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

99,828 Net Surplus After Taxation 77,294 51,443

Add (less) non-cash items:

54,636 Depreciation 26,651 27,389

(9,225) Amortisation of energy contracts 0 (5,032)

1,775 Amortisation of other non-current assets 1,190 907

(55,637) Release from energy contracts 0 0

(1,594) Other non-cash items (6,536) 178

(10,045) 21,305 23,442

Add (less) movements in working capital:

(21,558) Decrease (increase) in receivables and prepayments 12,010 3,584

(1,034) Decrease (increase) in inventories 766 (127)

13,598 (Decrease) increase in payables and accruals (8,289) (15,278)

6,481 Increase in provision for taxation 20,621 17,443

1,321 (Decrease) increase in deferred taxation (85) 1,128

(1,192) 25,023 6,750

Add (less) items classified as investing activities:

397 Movement in other non-current assets 0 (11)

397 0 (11)

88,988 Net Cash Inflow from Operating Activities 123,622 81,624

Notes to the Consolidated Financial Statements (continued) for the six months ended 31 December 2004

17Mighty River Power Limited Interim Report 31 December 2004

5. Commitments

30 june 2004 31 december 2004 31 december 2003 audited unaudited unaudited

$000 $000 $000

Capital Commitments

33,725 Commitments for future capital expenditure 25,504 39,438

Operating Commitments

6,948 Commitments for future operating expenditure 8,094 8,194

40,673 33,598 47,632

6. Contingencies

Mighty River Power Limited has a number of potential obligations under on-going support projects with community based groups.

Mighty River Power Limited has a contingent liability in respect of the Accident Compensation Corporation’s residual claims levy.

The levy is payable annually from May 1999 for up to fifteen years. The Group’s future liability is a function of the Accident

Compensation Corporation’s unfunded liability for past claims and future payments to employees.

Mighty River Power Limited has guaranteed payment obligations of $16.8 million pursuant to a letter of credit provided by

a bank in favour of TPC Holdings Limited.

Mighty River Power Limited holds land and interests that may be affected by certain claims that have been brought or

are pending against the Crown under the Treaty of Waitangi Act 1975. In the event that a recommendation is made by the

Waitangi Tribunal for the return of some or all of the affected land, and that recommendation is confirmed by the Crown,

resumption would be effected by the Crown under the Public Works Act 1981 and compensation would be payable to

Mighty River Power Limited.

7. Subsequent Events

There have been no events subsequent to balance date that would affect the fair presentation of these interim financial statements.

Notes to the Consolidated Financial Statements (continued) for the six months ended 31 December 2004

18 Mighty River Power Limited Interim Report 31 December 2004

Directors

Carole Durbin, Chair

John Baird

Caroline Ball

Ian Fraser

David McConnell

Sandy Maier

Tania Simpson

Rob Challinor, Chairman to 31.12.04

Executive Management

Doug Heffernan Chief Executive

Tim Densem General Manager Hydro/Thermal

John Foote Group Operations Manager

Tony Gray Group Finance Manager

Stuart Lush General Manager Generation Development

William Meek Enterprise Risk Strategist

James Moulder General Manager Trading

Greg Raasch General Manager Geothermal

David Reeve General Manager Metrix

Neil Williams General Manager External Affairs

Company Secretary

Tony Nagel

Registered Office

Level 19, 1 Queen Street, Auckland

Telephone: 09 308 8200

Facsimile: 09 308 8209

Email: [email protected]

Website: www.mightryriverpower.co.nz

Directory

19Mighty River Power Limited Interim Report 31 December 2004