Embed Size (px)

DESCRIPTION

Â

Citation preview

MIGHTY RIVER POWERINTERIM REPORT 31 DECEMBER 2003

03 From the Chairman and Chief Executive07 Interim Financial Statements08 Consolidated Statement of Financial Performance09 Consolidated Statement of Movements in Equity10 Consolidated Statement of Financial Position12 Consolidated Statement of Cash Flows13 Notes to the Consolidated Financial Statements17 Directory

Contents

Highlights

for 6 months to 31 December Operating Surplus before Interest, Non-recurring Items and Taxation ($m)

2003

2002

2001

2000

1999

0 20 40 60 80 100

Operating Surplus before Interest, Non-recurring Itemsand Taxation of $95.3 million, up 20% on 2002.Net Surplus after Taxation of $51.4 million, up 16% on thenormalised 2002 result. Further successful debtrestructuring through a $113.8 million Fixed Rate Bond Issue.Mercury Energy approaching300,000 retail customers.

Long-term contract volumes rise. Waikato River resource consentsgranted for 35-year term, subjectto appeal. Expansion of geothermalgeneration continues. Extensive generation research and development underway.Mercury Energy won the BusinessEthics award at the Deloitte’sManagement Top 200 awards.

Net Debt/Net Debt plus Equity (%)

2003

2002

2001

2000

1999

0 20 40 60 80 100

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 01

at 31 December

Total Generation Volumes (GWh) for 6 months to 31 December Hydro

Net Surplus after Taxation ($m)

2003

2002

2001

2000

1999

2003

2002

2001

2000

1999

0

Total Operating Revenue ($m)

2003

2002

2001

2000

1999

0 50 100 150 200 250 300 350 400

Operating Cashflow ($m)

2003

2002

2001

2000

1999

0

02 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

for 6 months to 31 December

for 6 months to 31 December

for 6 months to 31 December

Cogeneration Geothermal Methane

Normalised Actual

Normalised Actual

0 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 2400 2600 2800

20 40 60 80 100

20 40 60 80 100

From the Chairman and Chief Executive

On behalf of the Board and Management, we are pleased to present Mighty River Power’s performance for the six months to 31 December, 2003.

HighlightsIt is satisfying to look back on a period that has continuedto see the Company perform well. This consistency is afunction of the sound business platform created since theCompany’s formation in 1999 and reflects the hard workand focus of the entire organisation.

In earlier years our focus was on strengthening ourbalance sheet, stabilising our retail operation, andcreating a good balance between generation capacity and retail sales.

The substantial benefits of that focus are reflected in Mighty River Power’s best ever performance in a Julyto December period. Operating Surplus before Interest,Non-recurring Items and Taxation was $95.3 million, aresult enhanced by our decision in December 2002 to exit the onerous Southdown Power Sale Agreement andto acquire the remaining 50% share of the Southdown Co-generation plant.

The full effect of that acquisition was felt in this periodthrough the benefits of completely integrating the Co-generation plant into our generation portfolio to better complement weather-related fluctuations in our hydro production and market conditions.

Getting our balance sheet in order after inheriting heavydebt levels at formation was also rewarded with anupgrade in our Standard & Poor’s credit rating outlookfrom stable to positive, while confidence in our businesswas reflected in a second successful bond issue.

The strength of our current balance sheet gives us theoption of investing in new generation – an area we are pursuing with vigour to meet growing demand. Otherissues impact on our ability to develop new generationopportunities, as discussed later in this report.

Our retail operation continued to perform extremely well, while new products, an emphasis on service and a thriving housing market facilitated new connections and customer acquisition.

Large commercial customers were also attracted to ourfinancial risk management products as they sought to

reduce their exposure to the price risks associated withthe wholesale market. Concerns over security of supplyduring early winter 2003 highlighted future fuel issues andan uncertain climate for investment in new generation,while prompting the Government to act in securing back-up generation for dry-year reserve capacity.

Mighty River Power has confirmed that it is technicallypossible to start up its mothballed, oil-fired plant atMarsden Point and, although transmission constraintsmay present challenges, we are continuing discussionswith the recently formed Electricity Commission about thestation’s possible future. Other options for generation atthe Marsden B site are also under investigation as part ofour plan for developing new generation capacity.

Our successful application for more flexibility in our 35-year consents for the Lake Taupo/Waikato River hydrosystem is expected to assist in maximising the efficiency ofour existing hydro generation capacity in meetingconsumer demand. A small number of parties haveappealed some of the consent conditions. We are activelyworking with the appellants and are reasonably confidentthe issues that have been raised will be resolved.

No interim dividend will be paid as agreed with ourshareholders, with the retained earnings used to reducedebt to assist future investment in new generationcapacity.

FinancialOperating Surplus before Interest, Non-recurring Itemsand Taxation was $95.3 million compared to the $79.4million surplus in the same period last year.

Net Surplus after Taxation performance was $51.4 million,compared with $99.8 million in 2002. The 2002 figure wasboosted considerably by the one-off, non-recurring gainassociated with exiting the Southdown Power SaleAgreement. The $51.4 million in the 2003 periodrepresents an improvement of 16% over the normalisedNet Surplus after Taxation in the 2002 period.

Total Operating Revenue of $305.8 million represented amore than $70 million increase period on period reflectingthe impact of full ownership of Southdown, stronger retailand commercial sales and increased retail prices.

Our ongoing focus on an appropriate balance between ourretail sales and generation capacity was assisted by an

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 03

increase in large commercial customers seeking to reducetheir risk exposure to wholesale price fluctuations byelecting to take up our financial contracts.

Restructuring our debt portfolio continued with a secondFixed Rate Bond Issue that raised $113.8 million. TheCompany’s average debt maturity profile has improvedfrom an average 2-3 years to 7-8 years. Net debt wasfurther reduced from $487.8 million to $394.1 million.

Just after the end of the last financial year the outlook forour Standard & Poor’s credit rating improved from BBB(stable outlook) to BBB (positive outlook).

The reduction in debt and the improvement in our debtprofile have given the Company room to prudently invest ingeneration development. Currently, we are committingsignificant amounts of capital to researching anddeveloping generation opportunities.

GenerationTotal production for the six month period was 2,689 gigawatthours, a 6% increase on the corresponding 2002 period.

Mighty River Power has been looking at how we willcontribute to the increased energy needs of the countrywith a focus on expanding its generation capabilities.

Since May 2003 the Company has been a 25% equitypartner in the Tuaropaki Power Company which isundertaking the 39MW Mokai II expansion at the Mokaigeothermal field, due for commissioning in mid-2005.Exploratory drilling is also underway near Kaweraufollowing our agreement with the Putauaki Trust.

Further drilling has been undertaken to restore fullgeneration from the Rotokawa Power station, whilediscussions are continuing on the possibility ofrecommissioning the Marsden B oil-fired plant as dry-yearreserve. Investigations are also being carried out foralternate thermal fuel options for the Marsden B facilitywhile a number of other generation options are beinginvestigated elsewhere.

The granting of consents for the Waikato River hydrosystem for 35 years, and the additional flexibility obtainedin those consents, although subject to appeal, areultimately expected to allow Mighty River Power toincrease the efficiency and flexibility of generation fromthis limited but renewable fuel resource.

CustomersIn the commercial market, Mighty River Power has beenworking closely with end users to provide well-priced,electricity price risk management products. We have seenmore customers keen to eliminate price risk for longerdurations or to cover specific short-term events. Thereciprocal benefit of the increasing number of longer-termcontracts for the Company is an increase in certainty.

Mighty River Power also worked closely with other majorgenerators to introduce a web-based forward price curvewww.energyhedge.co.nz. The aim of the site is to provide a more liquid and transparent mechanism for forwardprice discovery of up to two years.

Commercial customers also benefited from another newservice, consisting of email and text message notificationof significant shifts in the wholesale market spot price.This service enables customers to manage their demandaround pricing peaks.

In mass markets, an ongoing focus on service and productdevelopment has contributed to significant growth forMercury Energy’s retail customer base, which is nowapproaching 300,000.

Services such as monthly meter reading, gas and electricityon the same bill (Mercury Duo) and discounts for promptand direct debit payments have been complemented by theaddition of Online Billing and the creation of the OneBillTM

service for customers with more than one property whowant to receive just a single bill. These products are creatinggreater stability in our customer base.

These enhanced services mean competing retailerstargeting Mercury’s customer base are having littlesuccess while the services are attracting new customers.The very strong housing market has also boosted newconnections, particularly across the Auckland region.

A programme targeted on gaining access to difficult-to-read meters, including offering evening and weekendmeter reads, proved very successful.

Mercury Energy’s high profile community initiativescontinued with new, highly specialised, X-ray equipmentprovided to Starship Hospital and our ongoing support forthe Christmas in the Park and Starlight Symphony events.Our association with Christmas family events wassuccessfully expanded to include Hamilton, where wecontinue to grow our retail presence.

04 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

One of the highlights for our retail operation was MercuryEnergy winning the Business Ethics award at the Deloitte’sManagement Magazine Top 200 awards.

The award recognised the environmental work practicesthat lay behind achieving the Platinum Enviromarkstandard, together with Mercury’s unique “Beat your Bill”energy-saving campaign which rewarded individualcustomers for saving power during the national Target10% energy-saving campaign.

Looking ForwardThe country’s most pressing issue is the need to developan energy policy encompassing a strategy for securingfuel supplies in the medium to long term. Such a policy is fundamental to ensuring the security of New Zealand’sfuture electricity supply, so as to sustain the economicwealth of all New Zealanders.

We need clear signals as a company and an industry about the terms on which various fuel options will beavailable to us to reduce the risks associated withinvestment in new generation.

Currently, we face major uncertainties created by NewZealand’s commitments to the Kyoto Protocol and theproposed carbon tax regime, future gas supplies andexploration, and the Resource Management Act for newprojects, especially renewables.

Doubts around Russia’s participation in Kyoto castuncertainty around New Zealand’s commitment to theprotocol as, without such a major player and the absenceof Australia and the United States, there appears to beincreasing uncertainty about the viability of the initiative.

Clear intentions regarding Kyoto and a carbon tax regimefor New Zealand are necessary as carbon taxes impactsignificantly on fuel choices for generation and,consequently, viable development options.

Given the limited hydro and geothermal developmentopportunities and the long lead times associated withgaining consents, coal and gas appear to be the bestmedium-term generation fuel alternatives.

However, coal may be ruled out by a carbon tax regimeand gas may also be adversely affected by carbon taxrequirements. A more pressing concern about gas is itsavailability in New Zealand, especially with the limitedreserves now identified in the Maui field.

The Company is investigating a variety of opportunities to participate in the gas exploration sector.

Finally, the Resource Management Act presents its ownchallenges for those pursuing investment in generation.The Act encourages a local focus on individual projectsrather than taking a view of their national significance.This can result in local interests overriding projects ofnational importance. We see this directly in ourgeothermal developments.

Also at the national level, we have a new body to work with – the Electricity Commission. The Company has madesubmissions on how this body might operate. We lookforward to working with the Commission in developingcoherent strategies to ensure security of electricity supplyto meet New Zealand’s growing energy demands so as tomeet the economic needs of all New Zealanders.

Our PeopleWe again acknowledge the contribution of our staff andthe support of their families in achieving success forMighty River Power.

With a new focus on developing generation, we havestrengthened our environmental and development teams.

We continue to build further on the very good workundertaken since our formation and have created a strongand consistently performing business, one that has thecapital and technical capabilities to meet the marketneeds for energy.

Rob ChallinorChairman

Doug HeffernanChief Executive

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 05

06 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

Interim Financial StatementsFor the six months ended 31 December 2003

08 Consolidated Statement of Financial Performance09 Consolidated Statement of Movements in Equity10 Consolidated Statement of Financial Position12 Consolidated Statement of Cash Flows13 Notes to the Consolidated Financial Statements

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 07

798,286 Sales 391,870 316,019

(162,270) Less transmission, line and metering charges (90,777) (86,343)

2,784 Interest income 990 1,512

7,446 Other revenue 3,738 3,863

646,246 Total Operating Revenue 305,821 235,051

119,474 Operating surplus before interest and non-recurring items 95,326 79,417

2,784 Interest income 990 1,512

(29,867) Interest expense (16,222) (14,062)

34,217 Non-recurring items 2 0 35,362

126,608 Surplus Before Taxation 80,094 102,229

(13,077) Taxation expense 3 (28,571) (2,476)

113,531 Surplus After Taxation 51,523 99,753

0 Share of retained deficit of associate company after taxation (80) 0

113,531 Net Surplus After Taxation 51,443 99,753

The notes set out on pages 13 to 16 form part of, and should be read in conjunction with, these Interim Financial Statements.

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 Note $000 $000

Consolidated Statement of Financial PerformanceFor the six months ended 31 December 2003

08 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

The notes set out on pages 13 to 16 form part of, and should be read in conjunction with, these Interim Financial Statements.

759,965 Equity at Beginning of the Period 861,696 759,965

113,531 Net surplus after taxation 51,443 99,753

113,531 Total Recognised Revenues and Expenses for the Period 51,443 99,753

(11,800) Final dividend paid for 2002 0 (11,800)

861,696 Equity at End of the Period 913,139 847,918

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 $000 $000

Consolidated Statement of Movements in EquityFor the six months ended 31 December 2003

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 09

The notes set out on pages 13 to 16 form part of, and should be read in conjunction with, these Interim Financial Statements.

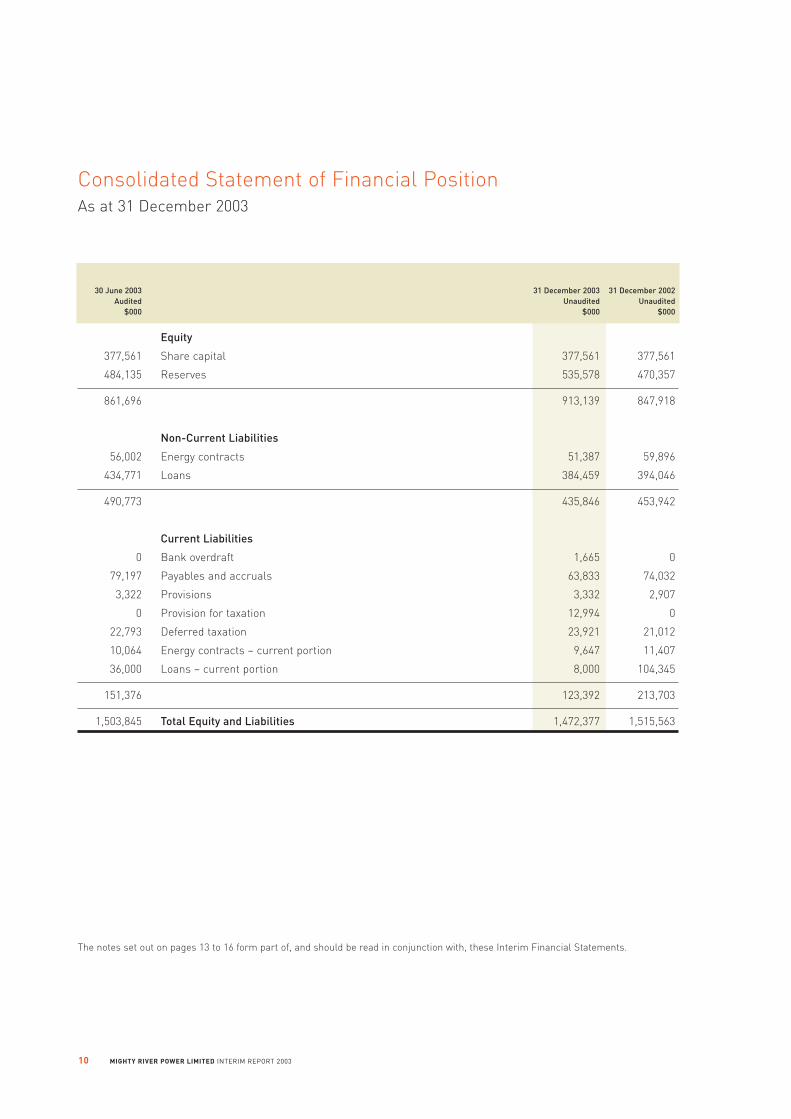

Equity

377,561 Share capital 377,561 377,561

484,135 Reserves 535,578 470,357

861,696 913,139 847,918

Non-Current Liabilities

56,002 Energy contracts 51,387 59,896

434,771 Loans 384,459 394,046

490,773 435,846 453,942

Current Liabilities

0 Bank overdraft 1,665 0

79,197 Payables and accruals 63,833 74,032

3,322 Provisions 3,332 2,907

0 Provision for taxation 12,994 0

22,793 Deferred taxation 23,921 21,012

10,064 Energy contracts – current portion 9,647 11,407

36,000 Loans – current portion 8,000 104,345

151,376 123,392 213,703

1,503,845 Total Equity and Liabilities 1,472,377 1,515,563

30 June 2003 31 December 2003 31 December 2002Audited Unaudited Unaudited

$000 $000 $000

Consolidated Statement of Financial PositionAs at 31 December 2003

10 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

The notes set out on pages 13 to 16 form part of, and should be read in conjunction with, these Interim Financial Statements.

Non-Current Assets

1,375,053 Property, plant and equipment 1,357,846 1,392,038

6,916 Investments 4,255 7,119

14,438 Other non-current assets 15,626 8,976

1,396,407 1,377,727 1,408,133

Current Assets

4,882 Cash 0 10,619

95,091 Receivables and prepayments 91,507 84,204

3,016 Inventories 3,143 2,939

4,449 Taxation receivable 0 9,668

107,438 94,650 107,430

1,503,845 Total Assets 1,472,377 1,515,563

30 June 2003 31 December 2003 31 December 2002Audited Unaudited Unaudited

$000 $000 $000

Consolidated Statement of Financial Position (continued)As at 31 December 2003

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 11

The Board of Directors authorised the issue of the interim financial statements on 25 February 2004.

Cash Flows from Operating Activities

Cash was provided from (applied to):

654,391 Receipts from customers 309,546 254,123

2,416 Interest received 1,025 1,190

(531,193) Payments to suppliers and employees (202,791) (182,767)

(29,983) Interest paid (16,156) (14,888)

(13,904) Taxation paid (10,000) (10,303)

81,727 Net Cash Inflow from Operating Activities 4 81,624 47,355

Cash Flows from Investing Activities

Cash was provided from (applied to):

850 Sale of property, plant and equipment 92 833

453 Proceeds from investments 2,581 0

(25,822) Purchase of property, plant and equipment (10,172) (19,369)

(13,056) Purchase of other non-current assets (2,360) (6,800)

(250) Purchase of associate 0 0

9,293 Purchase of subsidiary and joint venture 0 9,293

(28,532) Net Cash Outflow from Investing Activities (9,859) (16,043)

Cash Flows from Financing Activities

Cash was provided from (applied to):

8,712 Loans advanced 0 0

0 Loans repaid (78,312) (12,168)

(48,500) Loans of purchased subsidiary 0 0

(11,800) Dividends paid 0 (11,800)

(51,588) Net Cash Outflow from Financing Activities (78,312) (23,968)

1,607 Net Increase (Decrease) in Cash Held (6,547) 7,344

3,275 Cash Balance at Beginning of the Period 4,882 3,275

4,882 Cash Balance at End of the Period (1,665) 10,619

Consolidated Statement of Cash FlowsFor the six months ended 31 December 2003

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 Note $000 $000

The notes set out on pages 13 to 16 form part of, and should be read in conjunction with, these Interim Financial Statements.

12 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

Notes to the Consolidated Financial StatementsFor the six months ended 31 December 2003

2. Non-Recurring Items

1. Statement of Accounting Policies

The interim financial statements presented here are the unaudited consolidated financial statements of Mighty RiverPower Limited for the six months ended 31 December 2003.

These interim financial statements have been prepared in accordance with FRS-24 Interim Financial Statements, andshould be read in conjunction with the Annual Report for the period ended 30 June 2003. The accounting policies usedin the preparation of these interim financial statements are consistent with those used in the annual financialstatements and the previously published interim financial statements.

Certain prior year comparatives have been restated to conform with current period presentation.

43,153 Exit from Southdown Power Sale Agreement 0 43,153

(8,243) Write-off of Southdown goodwill 0 (8,243)

(693) Other 0 452

34,217 0 35,362

Exit from Southdown Power Sale Agreement

On 28 November 2002 the Group exited from the Southdown Power Sale Agreement. The amount of $43,153,000 relates

to the net gain from exiting this arrangement, including a termination payment and reversal of an onerous energy

contract provision.

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 $000 $000

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 13

14 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

Notes to the Consolidated Financial Statements (continued)For the six months ended 31 December 2003

126,608 Surplus before taxation 80,094 102,229

41,781 Taxation at 33 cents 26,431 33,736

Taxation effect of permanent differences:

(24,470) Release from Southdown energy contract 0 (24,470)

(1,486) Amortisation of energy contracts 0 (1,590)

(2,324) Other permanent differences 2,140 (5,200)

(424) Prior year adjustments 0 0

13,077 Taxation expense 28,571 2,476

Analysis of taxation expense:

9,623 Current taxation 27,443 804

3,454 Deferred taxation 1,128 1,672

13,077 28,571 2,476

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 $000 $000

3. Taxation Expense

Notes to the Consolidated Financial Statements (continued)For the six months ended 31 December 2003

113,531 Net Surplus After Taxation 51,443 99,753

Add (less) non-cash items:

53,696 Depreciation 27,389 25,967

0 Share of retained deficit of associate company 80 0

(15,610) Amortisation of energy contracts (5,032) (10,373)

469 Amortisation of goodwill 0 469

1,347 Amortisation of other non-current assets 907 542

0 Movement in obligations assumed on acquisition of businesses (76) (842)

(74,153) Release from Southdown energy contract 0 (74,153)

8,243 Write-off of Southdown goodwill 0 8,243

326 Other non-cash items 174 4,400

(25,682) 23,442 (45,747)

Add (less) movements in working capital

4,319 Decrease in receivables and prepayments 3,584 15,206

(201) Increase in inventories (127) (124)

(6,688) Decrease in payables and accruals (15,278) (11,427)

(3,679) (Decrease) increase in provision for taxation 17,443 (8,898)

9,207 Increase in deferred taxation 1,128 7,426

2,958 6,750 2,183

Add (less) items classified as investing activities

(9,603) Working capital acquired on purchase of subsidiary and joint venture 0 (9,603)

523 Movement in other non-current assets (11) 769

(9,080) (11) (8,834)

81,727 Net Cash Inflow from Operating Activities 81,624 47,355

Year Ended Six months ended Six months ended30 June 2003 31 December 2003 31 December 2002

Audited Unaudited Unaudited$000 $000 $000

4. Reconciliation of Net Surplus After Taxation with Net Cash Flows from Operating Activities

MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003 15

16 MIGHTY RIVER POWER LIMITED INTERIM REPORT 2003

Capital Commitments

31,964 Commitments for future capital expenditure 39,438 8,633

Operating Commitments

7,844 Commitments for future operating expenditure 8,194 9,148

39,808 47,632 17,781

6. Contingencies

Mighty River Power Limited has guaranteed payment obligations of $20.0 million pursuant to a letter of credit

provided by a bank in favour of the market clearing company (M-Co Clearing House Limited).

Mighty River Power Limited has a number of potential obligations under on-going support projects with

community-based groups.

Mighty River Power Limited has a contingent liability in respect of the Accident Compensation Corporation’s residual

claims levy. The levy is payable annually from May 1999 for up to fifteen years. The Group’s future liability is a function

of the Accident Compensation Corporation’s unfunded liability for past claims and future payments to employees.

Mighty River Power Limited has guaranteed payment obligations of $29.8 million pursuant to a letter of credit provided

by a bank in favour of TPC Holdings Limited.

Mighty River Power Limited holds land and interests that may be affected by certain claims that have been brought or

are pending against the Crown under the Treaty of Waitangi Act 1975. In the event that a recommendation is made by

the Waitangi Tribunal for the return of some or all of the affected land, and that recommendation is confirmed by the

Crown, resumption would be effected by the Crown under the Public Works Act 1981 and compensation would be

payable to Mighty River Power Limited.

7. Subsequent Events

There have been no events subsequent to balance date that would affect the fair presentation of these interim financial

statements.

30 June 2003 31 December 2003 31 December 2002Audited Unaudited Unaudited

$000 $000 $000

5. Commitments

Notes to the Consolidated Financial Statements (continued)For the six months ended 31 December 2003

Directory

DirectorsRob Challinor ChairmanCarole Durbin Deputy ChairCaroline BallIan FraserSandy MaierDavid McConnellTania SimpsonWayne Walden

Executive ManagementDoug Heffernan Chief ExecutiveTim Densem General Manager Hydro/ThermalJohn Foote Group Operations ManagerTony Gray Group Finance ManagerOlwen Hyslop Group HR ManagerStuart Lush General Manager Generation DevelopmentWilliam Meek Enterprise Risk StrategistJames Moulder General Manager TradingGreg Raasch General Manager GeothermalDavid Reeve General Manager MetrixNeil Williams General Manager External Affairs

Company Secretary Richard Taylor

Registered OfficeLevel 19 1 Queen StreetAuckland

PO Box 90-399, AucklandTelephone: 09 308 8200Facsimile: 09 308 8209Email: [email protected]: www.mightyriverpower.co.nz

Mighty River Power generates the bulk ofits power from eight dams on the WaikatoRiver and geothermal resources nearTaupo. That generation is complementedby the Southdown Co-generation plant inAuckland and methane gas recovery sitesin Auckland and Wellington.Current generation assets are:

HydroAratiatia 78 MWOhakuri 106 MWAtiamuri 74 MWWhakamaru 98 MWMaraetai 352 MWWaipapa 54 MWArapuni 182 MWKarapiro 96 MWGeothermalRotokawa 32 MWMokai* 55 MWCo-generationSouthdown 118 MWMethane Gas RecoveryRosedale (Auckland)** 5 MWGreenmount (Auckland)** 5 MWSilverstream (Wellington)** 3 MW

(*25% owned by Mighty River Power)(** majority owned by Mighty River Power)

MIGHTY RIVER POWER INTERIM REPORT 31 DECEMBER 2003