Embed Size (px)

Citation preview

Interchange Academy

The History & Impact of Card Payments

Credit as a Form of Currency

• Before the plastic card used today, customers used metal plates, coins and other objects that could be used to incur credit at a store or other place of business.

• Using these early credit cards allowed consumers to conveniently purchase goods at any time.

• At the turn of the century, large corporations and department stores began issuing proprietary cards.

The First Cards

“Charg-It” cards allowed consumers to make purchases and have the bill forwarded to their bank,.

Diners Club Cards were the first credit cards in widespread use.

Diners Club cards and those issued by American Express for travelers’ expenses added convenience and fostered growth in the American economy.

Revolving Balances, Debit Cards, and the Open Loop System

• 1958- Bank of America Corp. introduces the first bank credit card called BankAmericard• Revolving balance is introduced

• 1966 Visa* issues general purpose credit

card Interbank Card Association establishes

national credit card system. This “Open loop” network allows

consumers to spend money now and pay later.

Program costs are shared amongst members, allowing small financial institutions to join networks.

• 1966- The Bank of Delaware pilots the first debit card, allowing merchants to receive guaranteed, instant payment.

Interchange Fees Allow for Further Expansion

1970- 16 percent of U.S. households own credit cards, greatly expanding the markets for merchants nationwide.

1971- Visa establishes an interchange fee to be paid by the merchant’s bank to the cardholder’s bank. This nominal fee guarantees payment to merchants and fraud protection to customers and merchants alike.

Interchange: The fee for the exchange of money between banks

Payment Card Networks Now

• 2010- 30 years later, 80 percent of consumers own a debit card and 78 percent own a credit card.*

• 2010- The Dodd-Frank Financial Reform act passes with last minute additions from Senator Dick Durbin that endanger payment card networks and the benefits they provide across the American financial system.

• 2011- The Durbin amendment takes effect capping interchange fees, placing the system at risk.

• 2012- The number of credit and debit cards in circulation in the U.S. is projected to reach almost 1.7 billion, with a total purchase volume reaching almost $4.5 trillion.

*Source: "The Survey of Consumer Payment Choice," Federal Reserve Bank of Boston, January 2010)

Benefits of Electronic Payments Systems:Speed, Reliability, Convenience, Security

Network connects…• 25 million merchant locations in more than 150 countries• About 2 million new merchants per year that join the system• Nearly 30,000 small and large banks and credit unions that issue

cards worldwide• Nearly 4,000 banks and card processors that provide card

acceptance services to merchants • More than 2 billion cards in use worldwide

Network manages… • $3.3 trillion in annual payment volume• More than 10,000 transactions per second

Retailers Make More Money and Lower Their Costs When They Accept Credit and Debit

Retailers receive guaranteed payment.• There is no such thing as a bounced debit or credit card payment.• Merchants receive the money in their accounts quickly – typically within

twenty-four hours of the purchase.

Retailers save money on costs associated with accepting checks and cash.• 187 million checks totaling $210 billion bounced in 2006, according to the

Federal Reserve. That’s about 512,000 checks per day.

• Food Marketing Institute reported a median loss of $284,124 in worthless checks per FMI member in 2006.

• FMI reports $21,000 in additional costs per year per member due to employee theft of cash alone

Retailers Increase Sales

• Businesses increase sales by up to 50% when they accept cards. (Entrepreneur Magazine)

• When New York City taxicabs began accepting cards, revenue went up 13 percent – and tips increased by 21 percent, according to The New York Times.

Retailers Increase Sales

• The Salvation Army began accepting card donations at its kettles in 2009 – the average cash donation was $2, while the average card donation was $15.

• Online spending is projected to grow to $250 billion by 2014, or 8 percent of all sales.

• In 2011, 122 million people

bought something online on Cyber Monday alone.

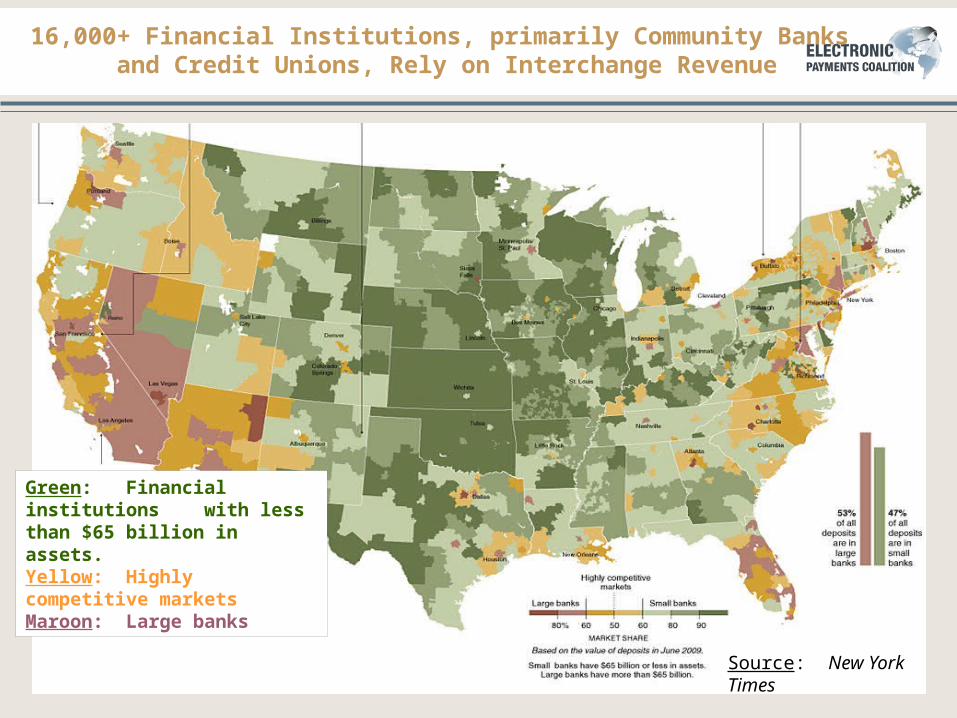

16,000+ Financial Institutions, primarily Community Banks and Credit Unions, Rely on Interchange Revenue

Green: Financial institutions with less than $65 billion in assets.Yellow: Highly competitive marketsMaroon: Large banks

Source: New York Times

How Electronic Payments Work

What is an Interchange Fee?

•Retailers that accept electronic payments access a larger customer base, reduced risk associated with handling cash, and guaranteed payment.

•For this, retailers pay a small fee, known as the “Merchant Discount Fee” (MDF).

•Interchange makes up a portion of the MDF.

• Customer Service

• System Efficiency and Convenience

• Costs of Online Transactions

• Protection of Customer Data (compliance)

• Card Processing Costs

• Fraud Prevention and Losses (cyber-security)

• Maintenance and System Upgrades

Merchants avoid these costs by not managing their own systems.

Interchange is One Part of a Revenue Stream that Supports the Electronic Payments System

Current Controversies and Merchant Myths

What is the Durbin Amendment?

U.S. Senator Dick Durbin (D-IL)

May 10, 2010:

Senator Dick Durbin (D-IL) introduces an amendment to the financial reform bill which would become the Dodd-Frank act.

The amendment was a political favor for giant retailers to help them improve their profits by setting price controls on debit card acceptance fees.

Enacted on October 1, 2011, the Durbin amendment is creating a windfall for giant retailers – and pain for everyone else.

• Capped interchange rates at around 23-24 cents per transactions – a 50% reduction.

• Represents an $8 billion dollar government bonus to retailers, with no benefit to consumers.

• Consumers paying more for banking services as banks and credit unions look to make up for the $8 billion loss.

• Small retailers selling “small-ticket” items now paying more, while big retailers selling expensive items paying significantly less.

• Even community banks and credit unions, despite a theoretical “carve-out,” have already begun to see reductions in interchange rates since Durbin enactment.

What is the Durbin Amendment?

Congress gave giant retailers an $8 billion annual windfall through unprecedented price caps on debit interchange fees, under the guise of helping consumers – yet have steadfastly refused to commit to passing

those savings along.

Consumers SufferHigher Costs

No evidence that merchants have lowered their retail pricesPaying more for traditional banking, cuts in rewardsSmall merchants are forced to raise costs

Less Convenience and Security

Durbin Amendment: It’s Not Working

Where’s My Debit Discount?Retailers are pocketing $8 billion in profits from the Durbin amendment

According to an Ipsos Public Affairs survey, only seven percent of respondents believe most retailers are passing their savings on to consumers.Moreover, only six percent believe that retailers ever intended to pass on savings.According to field research, 76 percent of retailers have either raised prices or kept them the same after October 1.

Durbin Amendment: It’s Not Working

Where’s My Debit Discount at the Pump?Debit is the overwhelmingly most popular form of payment at gas stations but consumers aren’t seeing savings.Gas retailers are saving $1 billion annually at the expense of consumers thanks to the Durbin amendment.Several years ago, Visa and MasterCard each voluntarily capped or lowered interchange fees for card transactions on fuel sales.

Durbin Amendment: It’s Not Working

Small Businesses SufferHigher Fees

Prior to government intervention, interchange was about 1% for a debit transaction. Now price-controlled transactions — both the $2 muffin and the $2,000 television — are subject to the same rate of a few dimes For the muffin vendor, that’s nearly a 1000% increase in interchange fees. For the big-box retailer selling the flat-screen TV, they’re paying nearly 100% less. Small merchants selling everyday items are paying the price so that big-box retailers can profit.

Durbin Amendment: It’s Not Working

Small Financial Institutions Suffer

“Carve Out” Fails to ProtectCommunity banks and credit unions will ultimately be harmed along with larger financial institutions.

The routing and exclusivity provisions which contain no such carve out increase the negative impact for small banks as retailers begin to route more transactions over lower-rate networks.

In order to survive and maintain their debit card programs, these institutions will face an impossible decision to either increase fees, or stop issuing debit cards altogether.

Durbin Amendment: It’s Not Working

Merchant Myth #1: Merchants can't negotiate their interchange fees.

Fact:

Merchants can — and do — directly negotiate with the networks to lower their interchange costs through a variety of incentive arrangements with networks, including deals in which the savings are rebated to the merchant.

Merchant Myths

Merchant Myth #2: Merchants can't offer a cash discount.

Fact:

There is nothing prohibiting merchants from offering a cash discount. In fact, federal law allows merchants to offer cash discounts, and the card networks all make very clear in their rules that cash discounts are allowed.

So the question becomes this: why aren’t they offering cash discounts now? Answer — because doing so would make them lose money.

Merchant Myths

Merchant Myth #3: Retailers pay interchange fees

Fact:

A merchant does not pay the interchange fee directly — he or she pays a merchant discount fee, which is the blended rate. The Visa or MasterCard network transfers the interchange fee portion of the merchant discount fee from the retailer’s bank or card processor to the customer’s card issuing bank or credit union.

Merchant Myths

Merchant Myth #4: Interchange fees are confusing

Fact:

Merchants understand the exact breakdown of the fees they will pay based on the agreement they each negotiated with their acquiring bank, including the interchange fee.

Merchant Myths

Merchant Myth #5: Swipe fees are skyrocketing

Fact:

The weighted average of interchange fees has actually decreased since 2005, even with the significant advancements in technology, convenience, and new security and fraud protection measures — all advances that add significant value for merchants and consumers.

Merchant Myths

Merchant Myth #6: Merchants prefer all customers to pay with cash

Fact:

Cash can be time consuming and costly. Consumers spend more when using cards.Airlines and supermarkets are just a few industries moving away from cash/checks to electronic payments .

Merchant Myths

Merchant Myth #7: Swipe fees are higher in U.S. than in any other country.

Fact:

The full amount that retailers pay to accept payments in the U.S. actually compares favorably to rates globally.

When you compare the total cost of acceptance – including interchange, acquirer fees, and other elements – the U.S. is well below some other developed countries.

Merchant Myths

Merchant Myth #8: The Durbin amendment actually helped community banks and credit unions because of an exemption.

Fact:

The theoretical “carve out” won’t work. Community banks and credit unions will ultimately be harmed along with larger financial institutions.

According to the May 2012 Fed report, exempt institutions saw rates drop by 5.4% during the 4th quarter of 2011 – just three months after the Durbin amendment went into effect.

Merchant Myths

For further information please visit:

www.ElectronicPaymentsCoalition.org

Questions? Comments?