Embed Size (px)

Citation preview

Intelligent Database Systems Lab

Advisor : Dr. Hsu

Graduate : Keng-Wei Chang

Author : Javier Contreras

Rosario Espinola

Francisco J. Nogales

Antonio J. Conejo

國立雲林科技大學National Yunlin University of Science and Technology

ARIMA Models to Predict

Next-Day Electricity Prices

IEEE TRANSACTIONS ON POWER SYSTEMS, VOL.18 NO.3, AUGUST 2003

Intelligent Database Systems Lab

Outline

Motivation Objective Introduction ARIMA TIME SERIES ANALYSIS NUMERICAL RESULTS Conclusions Personal Opinion Review

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

Motivation

There are usually incorporate two instruments for trading in the electricity markets : the pool ; bilateral contracts

For both cases, predicting the prices of electricity for tomorrow or for the next 12 months is of the foremost importance.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

Objective

Price forecasts are developed in bidding strategies or negotiation skills in order to maximize benefit.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

Introduction

Therefore, an accurate price forecast for an electricity market has a definitive impact on the bidding strategies by producers or consumers.

Auto Regressive Integrated Moving Average (ARIMA) This paper focuses on the day-ahead price forecast of a daily

electricity market using ARIMA models. Box & Jenkins 於 1976 年提出 ARIMA 模式,認為時間

數列未來的變動會依其過去的資料型態而變動,且運用該模式進行預測時,時間數列的平均數與共變異數必須是固定不變的穩定過程,亦即資料達定態,其型態不隨時間而改變。

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

ARIMA TIME SERIES ANALYSIS

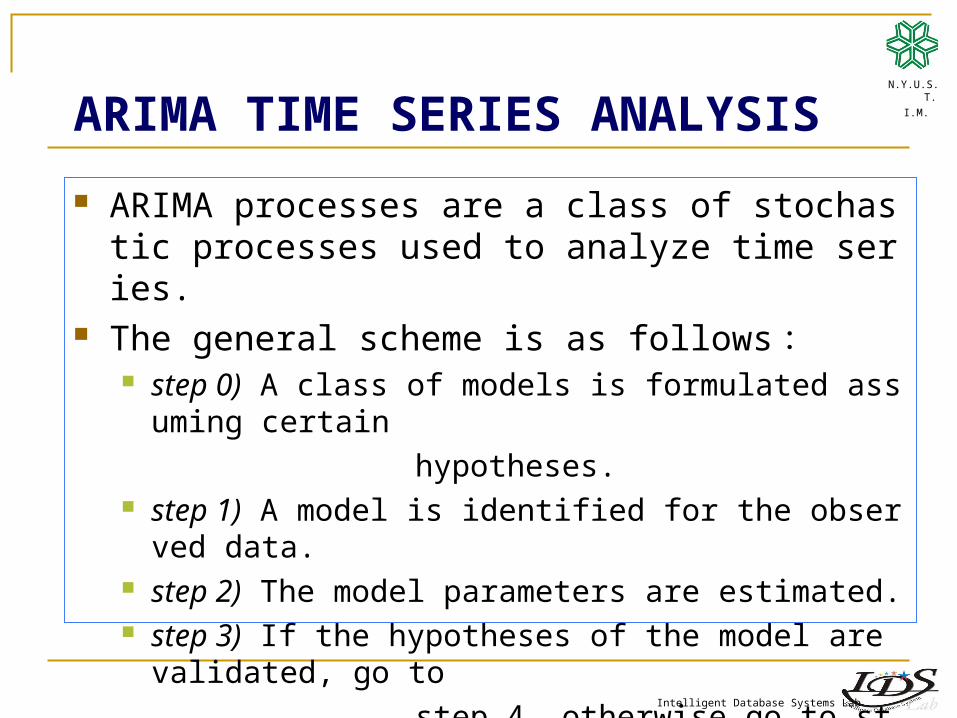

ARIMA processes are a class of stochastic processes used to analyze time series.

The general scheme is as follows : step 0) A class of models is formulated assuming certain

hypotheses. step 1) A model is identified for the observed data. step 2) The model parameters are estimated. step 3) If the hypotheses of the model are validated, go to

step 4, otherwise go to step1 to refine the model. step 4) The model is ready for forecasting.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

step 0) A class of models is formulated assuming certain hypotheses.

A general ARIMA formulation is selected to model the price data.

Example :

N.Y.U.S.T.

I.M.

)1(.....)()( tt BpB

pt is the price at time t

lttl ppBBB :Boperator backshift theof functions are )( and )(

term. theerror is t

)2().....1)(1)(1()1)(1()( 24168168

4848

2424

22

11 BBBBBBBB

Intelligent Database Systems Lab

step 1) A model is identified for the observed data.

A trial model, as seen in (1), must be identified for the price data.

In a trial, the observation of the autocorrelation and partial autocorrelation plots of the price data can help to make this selection.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

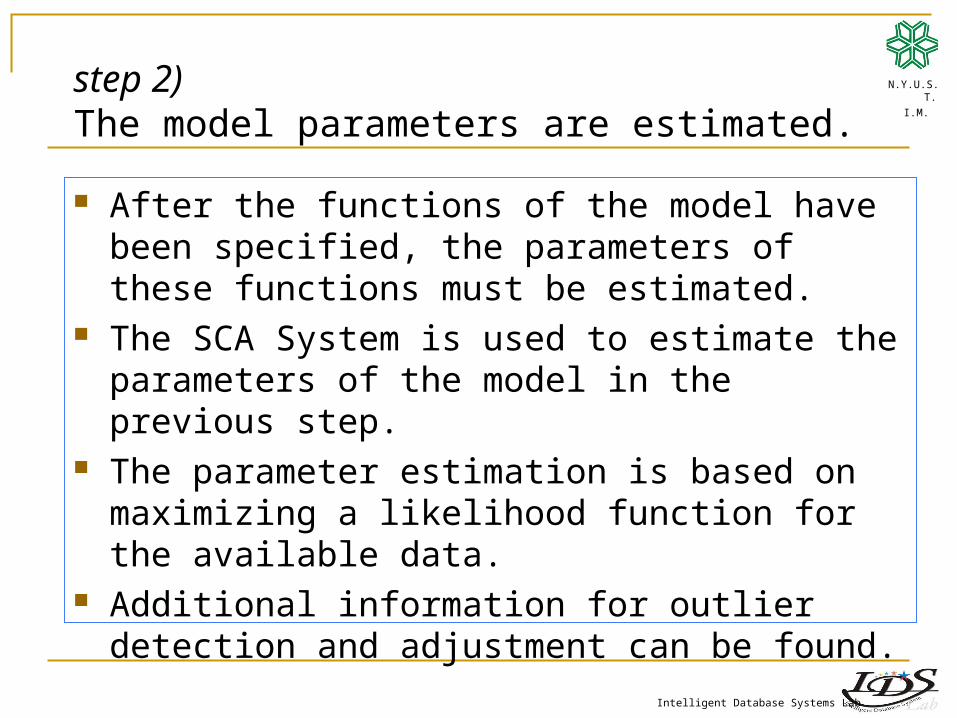

step 2) The model parameters are estimated.

After the functions of the model have been specified, the parameters of these functions must be estimated.

The SCA System is used to estimate the parameters of the model in the previous step.

The parameter estimation is based on maximizing a likelihood function for the available data.

Additional information for outlier detection and adjustment can be found.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

step 3) If the hypotheses of the model are validated, go to step 4, otherwise go to step1 to refine the model.

A diagnosis check is used to validate the model assumptions of step0.

If the hypotheses made on the residuals are true. Residuals must satisfy the requirements of a white noise process :zero mean, constant variance, uncorrelated process and normal distribution.

If the hypotheses on the residuals are validated by tests and plots, then, the model can be used to forecast prices.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

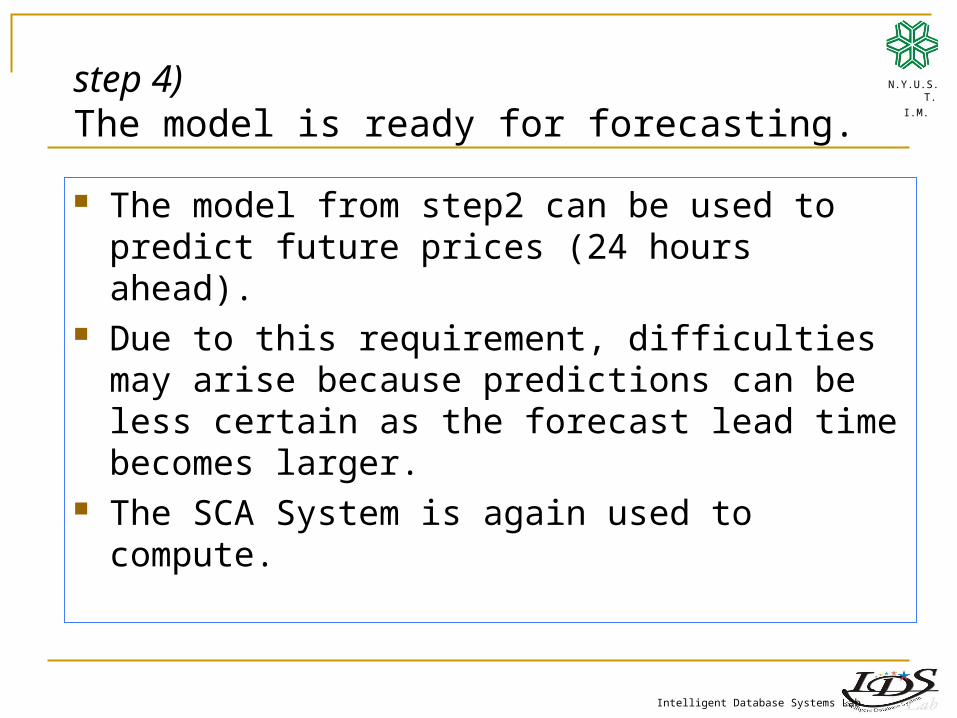

step 4) The model is ready for forecasting.

The model from step2 can be used to predict future prices (24 hours ahead).

Due to this requirement, difficulties may arise because predictions can be less certain as the forecast lead time becomes larger.

The SCA System is again used to compute.

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

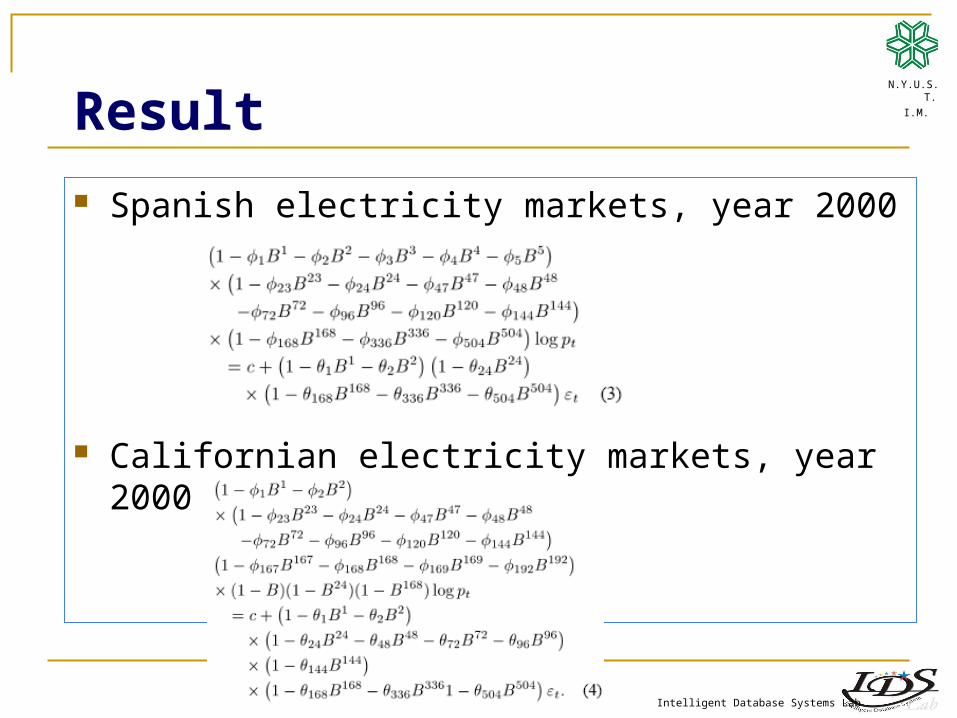

Result

Spanish electricity markets, year 2000

Californian electricity markets, year 2000

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

NUMBERICAL RESULTS

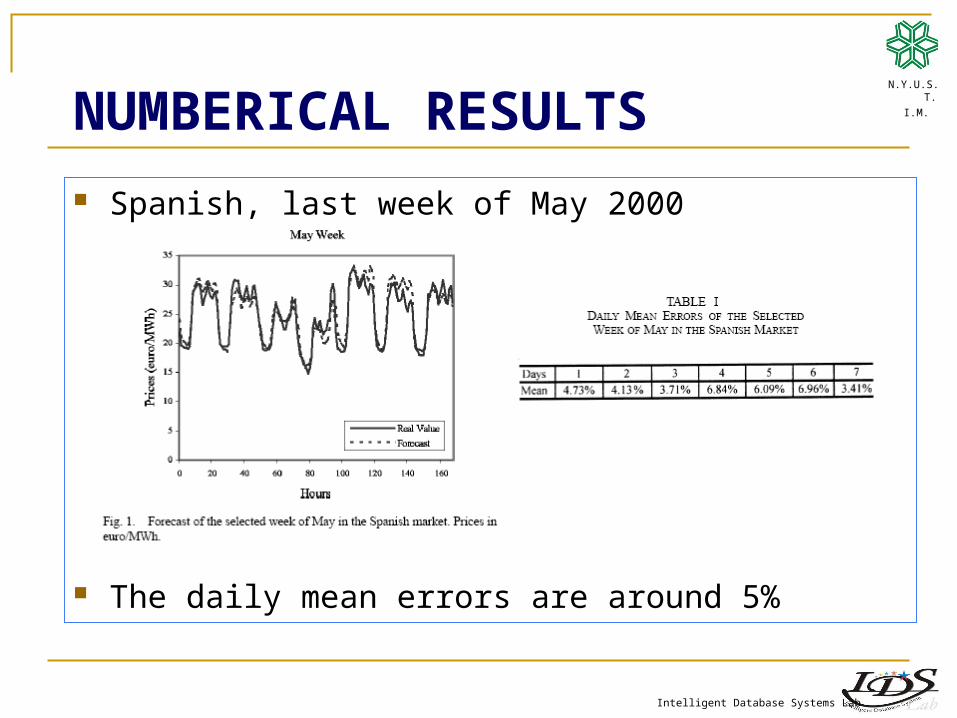

Spanish, last week of May 2000

The daily mean errors are around 5%

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

NUMBERICAL RESULTS

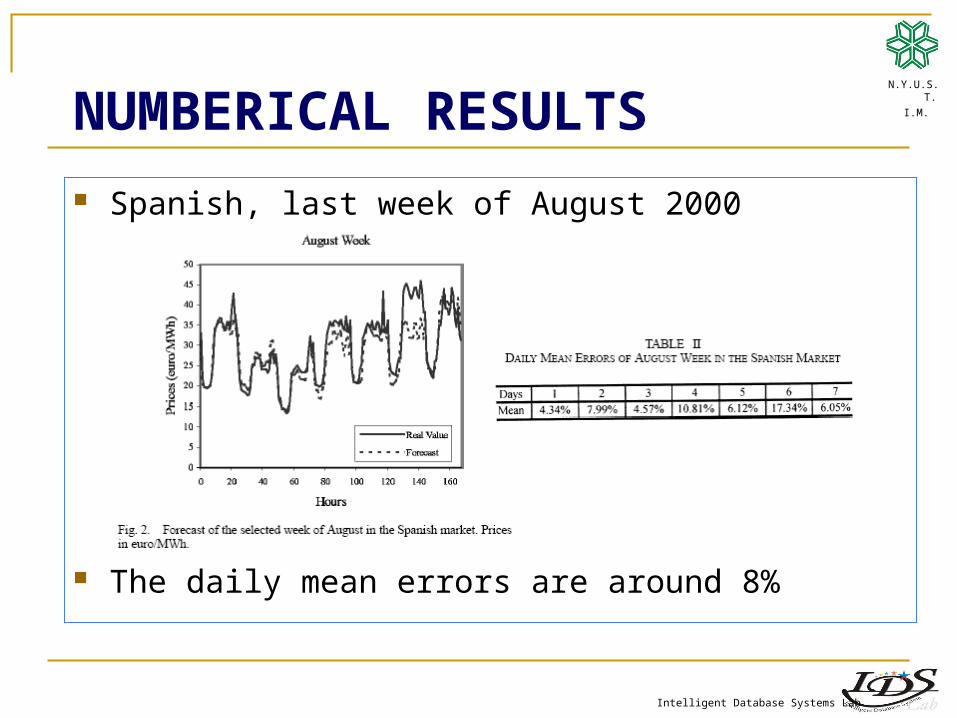

Spanish, last week of August 2000

The daily mean errors are around 8%

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

NUMBERICAL RESULTS

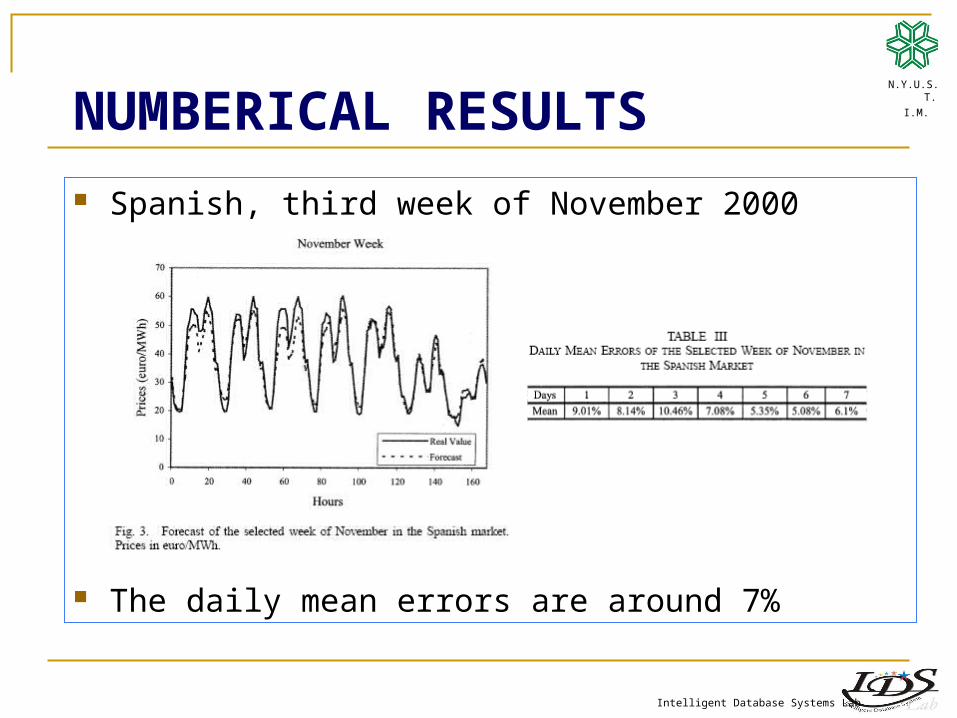

Spanish, third week of November 2000

The daily mean errors are around 7%

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

NUMBERICAL RESULTS

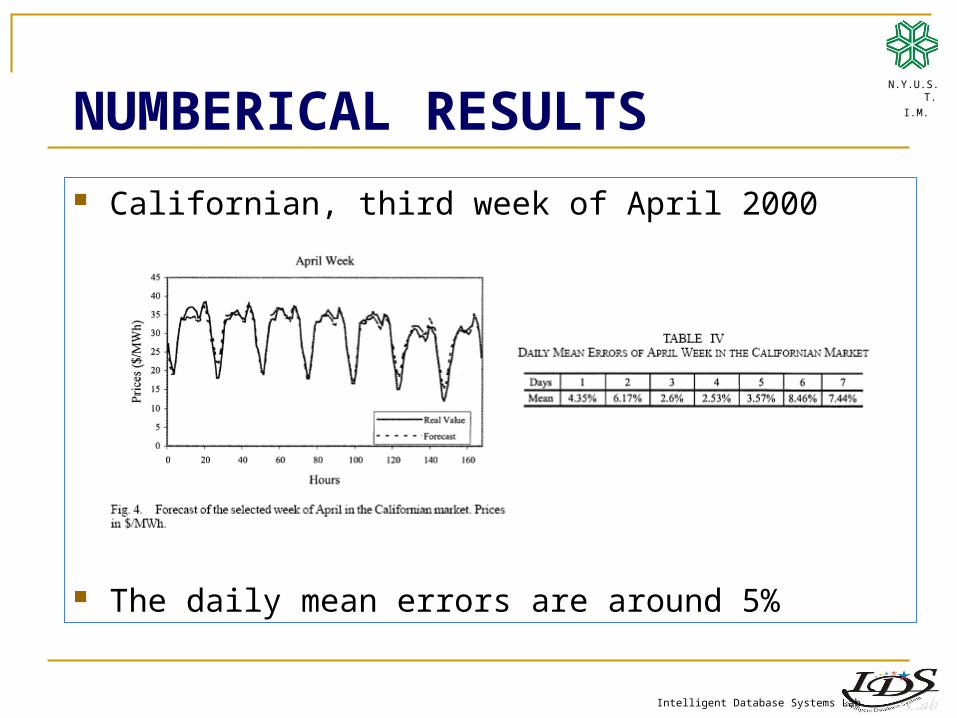

Californian, third week of April 2000

The daily mean errors are around 5%

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

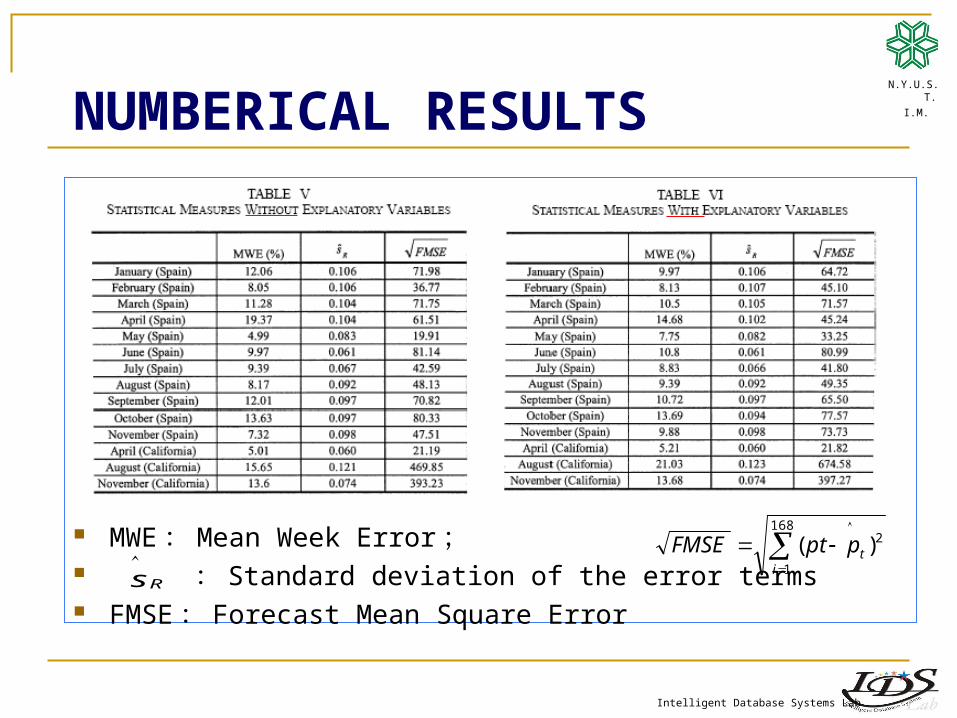

NUMBERICAL RESULTS

MWE : Mean Week Error ; : Standard deviation of the error terms FMSE : Forecast Mean Square Error

N.Y.U.S.T.

I.M.

Rs

2168

1

)(

i

tpptFMSE

Intelligent Database Systems Lab

NUMBERICAL RESULTSN.Y.U.S.T.

I.M.

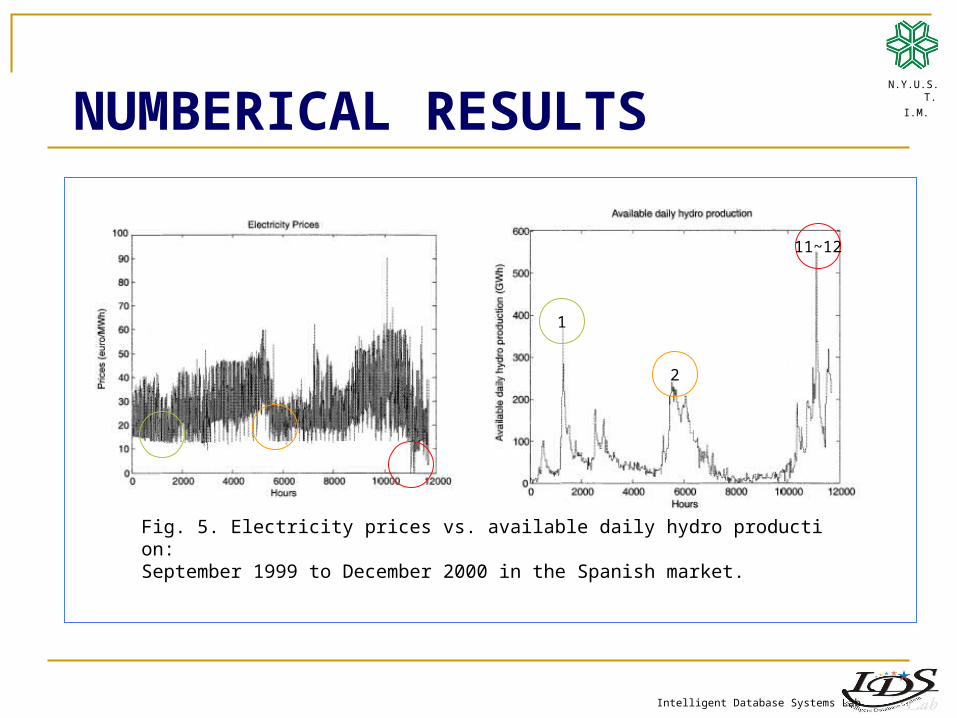

Fig. 5. Electricity prices vs. available daily hydro production: September 1999 to December 2000 in the Spanish market.

11~12

2

1

Intelligent Database Systems Lab

Conclusions

The Spanish model needs 5 hours to predict future prices, as opposed to the 2 hours needed by the Californian model.

These differences may reflect different bidding structures and ownership.

Average errors in the Spanish market are around 10%, and 5% in the stable period of the Californian (around 11% considering the three weeks, and without explanatory variables).

N.Y.U.S.T.

I.M.

Intelligent Database Systems Lab

Personal OpinionN.Y.U.S.T.

I.M.

![Nogales International (Nogales, Ariz.) 1937-05-08 [p PAGE TWO] · 2019. 12. 18. · NOGALES INTERNATIONAL The majority of the rural schools J in Santa Cruz County will close on Friday,](https://img.pdfslide.us/doc/110x75/60e91dd48d596f57d6514af5/nogales-international-nogales-ariz-1937-05-08-p-page-two-2019-12-18-nogales.jpg)

![Nogales International (Nogales, Ariz.) 1943-04-09 [p PAGE FOUR] · 2019. 12. 18. · nogales international- nogales’ home newspaper-* aero quiz by aeronca what prominent american](https://img.pdfslide.us/doc/110x75/60d999297f8dc7237311efe3/nogales-international-nogales-ariz-1943-04-09-p-page-four-2019-12-18.jpg)

![[Hua Loo Keng] Introduction to Number Theory](https://img.pdfslide.us/doc/110x75/563dbbac550346aa9aaf3cea/hua-loo-keng-introduction-to-number-theory.jpg)