Embed Size (px)

Citation preview

A little about myself…

1-2

Commerce Degree - 2010 - Memorial University of Newfoundland

MBA - 2012 - MUN / Université Catholique de Lyon

Ernst & Young - 2012/13 - Montreal & St. John’s (Canada)

Phd International Business – 2013 – Trinity College Dublin (Ireland)

Emerging Markets Global analysis of firm level multinationality

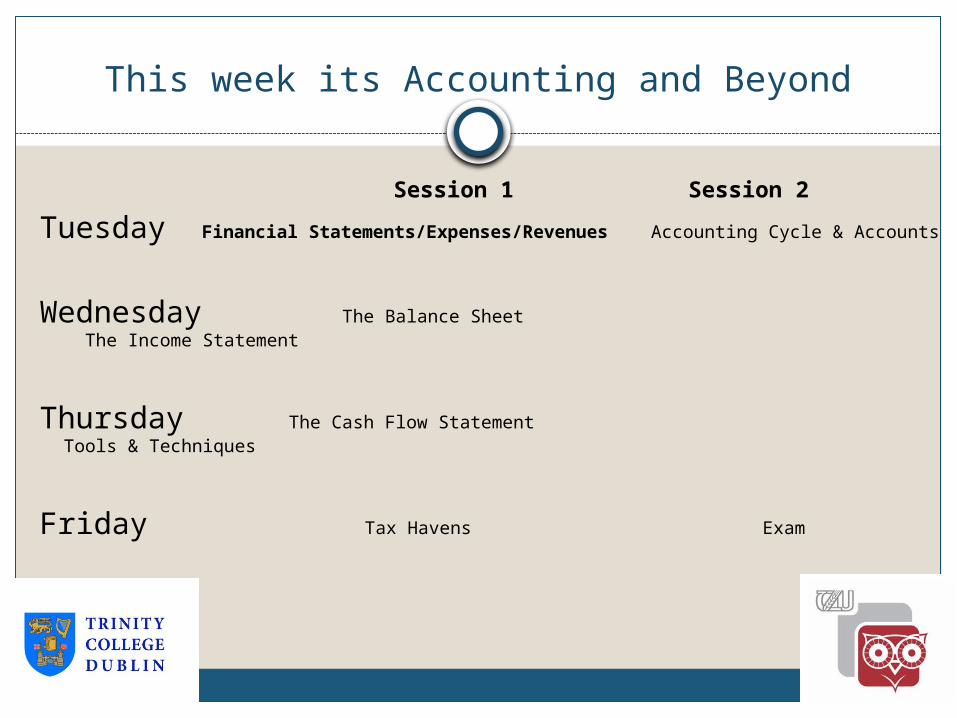

This week its Accounting and Beyond

1-3

Session 1 Session 2

Tuesday Financial Statements/Expenses/Revenues Accounting Cycle & Accounts

Wednesday The Balance Sheet The Income Statement

Thursday The Cash Flow Statement Tools & Techniques

Friday Tax Havens Exam

Grading Scheme

1-4

Exam at the end of the week (70%) Will cover material from Tuesday, Wednesday, Thursday, & Friday Multiple Choice Questions

Participation throughout the four days of lecturing (10%) Open conversation about topics will be encouraged along with

attendance of all sessions

Tax Haven Coverage by each assigned group (20%) Work in groups during the 4 days to present findings on Tax

Haven

5

Grading Scheme

Group Work Friday 1 or 2 members of the group will present with

or without the help of Powerpoint (7-10 minutes) Choose a Tax Haven and explain what makes that

country/region a haven for Multinationals What large Multinationals have subsidiaries here? Is this good or bad for the local economy? What is your view on this country/region being a tax

haven? Submit a one page document summarizing your

findings

6

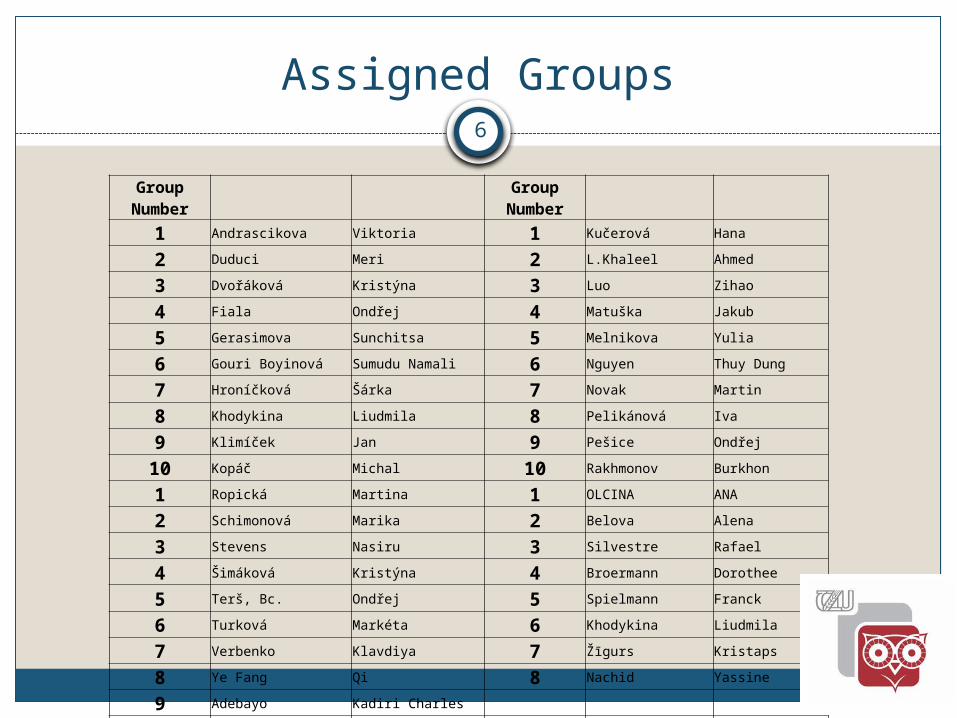

Assigned Groups

Group Number Group Number

1 Andrascikova Viktoria 1 Kučerová Hana

2 Duduci Meri 2 L.Khaleel Ahmed

3 Dvořáková Kristýna 3 Luo Zihao

4 Fiala Ondřej 4 Matuška Jakub

5 Gerasimova Sunchitsa 5 Melnikova Yulia

6 Gouri Boyinová Sumudu Namali 6 Nguyen Thuy Dung

7 Hroníčková Šárka 7 Novak Martin

8 Khodykina Liudmila 8 Pelikánová Iva

9 Klimíček Jan 9 Pešice Ondřej

10 Kopáč Michal 10 Rakhmonov Burkhon

1 Ropická Martina 1 OLCINA ANA

2 Schimonová Marika 2 Belova Alena

3 Stevens Nasiru 3 Silvestre Rafael

4 Šimáková Kristýna 4 Broermann Dorothee

5 Terš, Bc. Ondřej 5 Spielmann Franck

6 Turková Markéta 6 Khodykina Liudmila

7 Verbenko Klavdiya 7 Žīgurs Kristaps

8 Ye Fang Qi 8 Nachid Yassine

9 Adebayo Kadiri Charles

10 Peinado de la Vega Joaquín

7

Lake and Lilypads

8

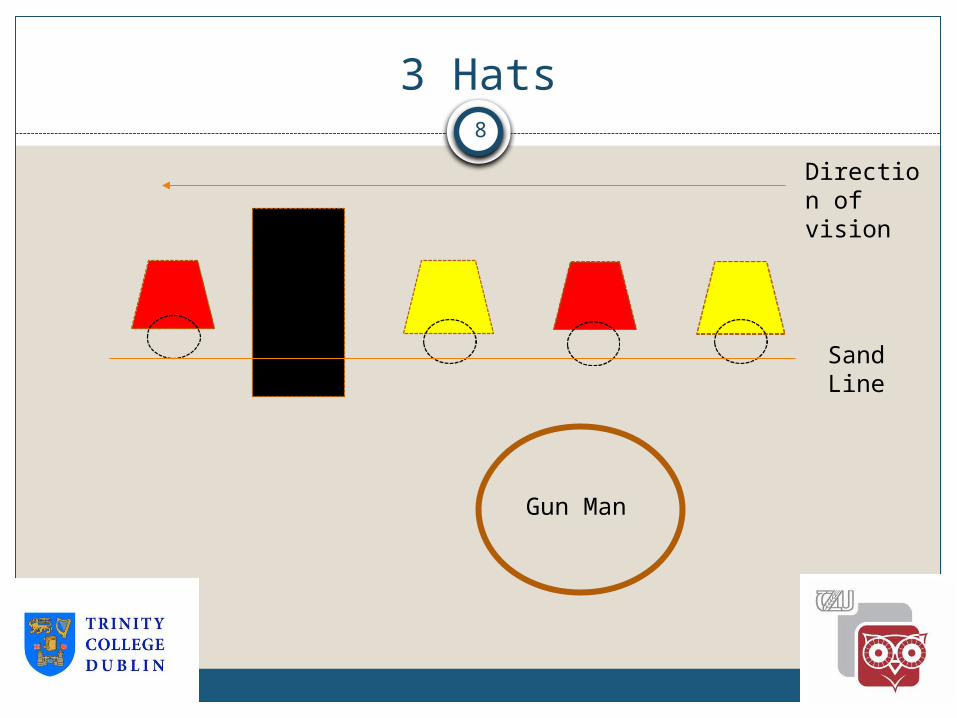

3 Hats

Sand Line

Direction of vision

Gun Man

Map or Maze

1-9

A map helps its user reach a desired destination through clarity of representation.

A maze attempts to confuse its user by purposefully introducing conflicting elements and complexities that prevent reaching the desired goal.

Financial statements have the potential for being both map and maze.

Financial Statements as a Map

1-10

Form the basis for understanding the financial position of a firm

Allow users to assess historical and prospective financial performance

Present clear representations of a firm’s financial health

Financial Statements as a Maze

1-11

Overwhelming amount of information

Unreliable auditing

Constantly changing and complex policies and reporting requirements

Considerable discretion given to management

Key information hidden or omitted

Map or Maze

1-12

The main objectives are:ensure that financial statements serve as a

map, not a maze,demonstrate how to read and evaluate

financial statements,provide the tools and techniques needed to

complete a comprehensive financial statement analysis, and

encourage intelligent decision making.

Map or Maze

1-13

Usefulness of Information

Financial positionSuccess of operationsPolicies and strategies of managementInsight into future performance

Map or Maze

1-14

Volume of Information Financial statements Notes to the financial statements Auditor’s report Five-year summary of key financial data High and low stock prices Management’s discussion and analysis of

operations Other material

Map or Maze

1-15

Volume of InformationGenerally accepted accounting principles

(GAAP)Securities and Exchange Commission (SEC)Financial Accounting Standards Board (FASB)International Accounting Standards Board

(IASB)Issues Statements of Financial Accounting

Standards (SFASs)

Map or Maze

1-16

Where to Find a Company’s Financial Statements

Annual report Financial statements Public relations material Sent to shareholders and prospective investors Corporate website

Map or Maze

1-17

The Financial Statements

Balance sheet (or statement of financial position)

Income statement (or earnings statement)

Statement of stockholders’ equity

Statement of cash flows

Map or Maze

1-18

Notes to the Financial Statements

Integral part of the statements

Summary of the firm’s accounting policies

Details about particular accounts

Other supplementary information

Map or Maze

1-19

Auditor’s Report

Attests to the fairness of the presentation of financial statements

Sarbanes-Oxley (SOX) Act of 2002

Map or Maze

1-20

Auditor’s Report Types of reports

Unqualified reports (FS give a true and fair view) Qualified reports (FS are misstated, no affect) Adverse opinion (FS are misstated, not conforming

with GAAP) Disclaimer of opinion (Opinion cannot be formed on

FS) Unqualified opinion with explanatory language

Map or Maze

1-21

Financial Reporting ReformsSOX Title I – Public Company Accounting Oversight

Board (PCAOB)SOX Title II – prohibits non-audit services during

an external auditSOX Titles III and IV – corporate responsibilitySOX Title IX – harsh penalties for violations

Map or Maze

1-22

Proxy Statement

Used to solicit shareholder votes Important in assessing

who manages the firm how management is paid conflict of interest issues

Map or Maze

1-23

Missing and Hard-to-Find Information Employee relations with management Morale and efficiency of employees Reputation of the firm Firm’s prestige in the community Effectiveness of management

Map or Maze

1-24

Continued

Provisions for management successionPotential exposure to regulation changesPublicity in the mediaCompanies operating in several lines of

unrelated business

Quality of Financial Reporting

1-25

Many opportunities for management to affect quality

Timing of revenue and expense recognition

Discretionary items

Revenues26

Assets earned by a company’s operations and business activities

Revenue account is an equity account with credit balance

Typically seen as… Operating Revenues Non-Operating Revenues

Revenues27

Operating Revenue Sales (Manufactures, Wholesalers, Retailers) Rent (Landlord to Tenant) Consulting Services (Professional Services

Provided)

Non-Operating Revenue Interest Revenue

Revenues28

Aaron’s Body Shop repairs cars for local auto dealers. Aaron is currently working on a fender repair for Bill’s Auto Lot. After Aaron finishes the repair, he sends Bill a $1,000 invoice for the labor and records the sale in his accounting system by debiting accounts receivable and crediting revenues.

Aaron records the income because he performed the work and has earned the revenue even though Bill hasn’t actually paid Aaron yet.

Expenses29

Costs incurred to generate revenueExpense accounts decrease the overall

equity balanceThere are many examples of expenses

that can occur for a business, all fit into 2 categories Operating Expenses Non-Operating Expenses

Expenses30

Operating Expenses Rent, Wages, Utilities, Advertising

Non-Operating Expenses Interest Expenses

Loan Interest from banks

Expenses31

Corey’s Food Truck, Inc. is a local food company that delivers sandwiches. Corey places new deli orders for $100 every Monday to a local butcher. When Corey places his order, he debits supplies for $100 and credits cash for $100. This journal entry records the asset, cash, being used up to generate revenues by making sandwiches.

At the end of the year how much does Corey spend on deli meat?

This will be listed as an expense on his income statement.