Embed Size (px)

DESCRIPTION

indonesia cement industry

Citation preview

www.dbsvickers.com

ed-SGC / sa- MA

Bulky valuations Unprecedented structural shift will see utilisation

rates reach a new low

Expect pricing power to weaken; do not discount a price war in 2016/17

Multiplier effect of infrastructure projects will only kick in in 2017

Valuations are rich but earnings growths are slowing; initiate coverage of SMGR and INTP with FULLY VALUED ratings

Unprecedented structural shift. Indonesia’s cement industry is experiencing an unprecedented structural shift that will see the derating of the key incumbent listed players. Cement demand growth peaked in 2010-2013, driven by the property sector which generated a multiplier of 2.4-2.7x GDP. But by 2017, cement supply will outstrip demand by a staggering 26m tonnes with incoming capacities from new foreign entrants. For the first time since 2010, we estimate industry utilisation rate will fall below 80%, and to 74% by 2017 (lowest since 2007). The more vulnerable segment will be bulk cement despite an expected acceleration in infrastructure spending, because this will likely be the target market for new entrants. Bulk cement is already generating lower margins than bag cement.

Situation exacerbated by weak pricing power. The supply-demand imbalance will continue to weaken pricing power and erode margins of cement players. This was evident last year, when the price hike was insufficient to offset cost increases. The situation was made worse after Jokowi instructed SOE cement companies (Semen Indonesia and Semen Baturaja) to reduce bag cement price by 4-5%, which offset the benefit of low energy prices. Also, floating electricity tariffs and fuel prices starting this year implies higher volatility for cement players. Do not discount a price war as early as 2016/2017, when most of the new supply comes on stream. Our channel checks reveal that Anhui’s and Siam Cement’s Indonesian presence account for c.3% of their total production, respectively, suggesting they may sacrifice pricing to gain market share.

Rich valuations unwarranted given slower earnings growth

and declining ROE. SMGR and INTP are currently trading at 15x/14x FY15F/16F EPS (slightly above their 10-year mean P/E), but earnings growth will slow to <5% CAGR (FY14-FY17) from 13-16% between FY09 and FY13. ROE will also drop from 31%-27% (in FY12) to 19%-20% (in FY17). Our TPs are based on 12x FY16F EPS (-1SD of mean). Our forecast earnings are 11-14% below consensus estimates. Of the two, Semen Indonesia is less vulnerable because of its geographical reach and the bulk of new supply which is coming onstream is in Western Java, where Indocement is dominant. We initiate coverage of SMGR and INTP with FULLY VALUED calls.

JCI : 5,337.50

Analyst Deidy WIJAYA +6221 3003 4931 [email protected] CHONG Tjen San, CFA +603 26043972 [email protected]

STOCKS

Source: Bloomberg Finance L.P., DBS Vickers, AllianceDBS

Semen Indonesia : Semen Indonesia (SMGR IJ) : SMGR was established in 1957. In 1995 the company completed an acquisition of Semen Padang and Semen Tonasa. It is currently the largest player in the market with 40.7% market share.

Indocement Tunggal Prakarsa : Indocement was established in 1975. The expanded heavily in the 90’s, prior to Heidelberg Cement Group becoming the majority shareholder in 2001. The company now trades under the brand “Tiga Roda”.

Holcim Indonesia: PT Holcim Indonesia Tbk is an Indonesia-based company primarily engaged in cement manufacturing and distribution. Its business is classified into three segments: cement production and distribution; ready-mix concrete production and aggregates mining, and other services, comprising cement distribution services.

DBS Group Research . Equity 17 Feb 2015

Indonesia Industry Focus

Indonesia Cement Sector

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

Semen Indonesia 14,675 6,823 12,200 (8.5) (2.4) FV Indocement 23,800 6,868 20,200 (3.3) 5.5 FV Holcim Indonesia 1,960 1,172 N.A (13.5) (14.5) N.R

Industry Focus

Indonesia Cement Sector

Page 2

Analysts Deidy WIJAYA +6221 3003 4931 [email protected] CHONG Tjen San, CFA +603 26043972 [email protected]

Table of Contents Investment Thesis 3 Supply/Demand Outlook 5 Significant new capacity in the next three years 7 Positive impact from weak energy prices offset by lower ASP 9 Premium valuation to narrow as oligopoly structure breaks down 11

STOCK PROFILE 12

Indocement Tunggal P. 13 Semen Indonesia 28

Industry Focus

Indonesia Cement Sector

Page 3

Investment Thesis Entering a new era – skewed supply-demand balance. We estimate 33m tons of new capacity will come onstream in the next three years. This will be more than double our forecast cement demand growth (16m tons) over the same period. As such, we forecast industry utilisation will drop from 90% in FY14 to 74% in FY17. SMGR and INTP would be able to keep utilisation relatively high at over 80% due to their strong brand equity and solid distribution channels. But this will depend on how rational the new competition in the form of foreign players will be. For sure, competition will be more intense and pricing power will weaken. Demand to recover partially, driven by rollout of infrastructure projects. We expect cement demand to pick up this year after a very slow 2014 (+3.3% y-o-y vs. 7.6% CAGR over FY04-13) as the government accelerates the rollout of infrastructure projects. The channeling of fuel subsidy into infrastructure and the new land bill (which will be effective from 2015) will boost cement demand from this year onwards. But growth will not return to the hey days as bag demand will be impacted by the slowdown in property sales and slow economic growth this year. Our base case assumption is for cement demand to grow by 6%/8%/10% in FY15/16/17, with demand for bulk cement growing by 14%/18%/20%. Our base case estimate is for bulk cement contribution to increase from 22% currently to 27% by 2017. But this is still insufficient to absorb the additional supply coming on stream. Bulk segment most vulnerable. We estimate bulk cement generate c.500 bps lower gross margin than bag cement. Furthermore, bulk segment will continue to face margin pressure as entry barriers are also much lower. The incumbents will continue to enjoy high market shares in the bag segment for the next few years due to their strong brand equity and solid distribution channels. But in the bulk segment, customers are more price-sensitive and the new entrants could be a serious threat to the incumbents’ pricing power as they try to gain market share. Hence, a price war should not be ruled out. Based on our channel checks, Anhui’s and Siam Cement’s capacity in Indonesia will account for a very small share (c.3%) of their total installed capacity. And given the high capex incurred, they may sacrifice pricing to gain market share. Anhui currently has 260m tons capacity in China, but is targeting for only 6.5m tons capacity in Indonesia by 2017 (<3% of group capacity). Likewise, Siam Cement has 56m tons capacity in Thailand, and is planning to commission 1.8m tons in Indonesia by 2017 (c.3%). This

suggests those players can afford to be aggressive in their pricing in order to win market share in Indonesia. We are already seeing some signs, as the pricing of Semen Merah Putih (by Wilmar Group) is c.5-10% cheaper than the Tiga Roda brand (by Indocement) and Semen Gresik brand (by Semen Indonesia group). Semen Merah Putih bag cement (cement imported from Vietnam) was introduced two years ago so Wilmar would get a head start in marketing the product. In January this year, they have managed to capture 2.4% market share. We believe the new players will pose a bigger threat to the incumbents’ market shares a few years down the road, especially in the bulk market, once they have batching plants to deliver Ready Mix Concrete (RMC). Benefits from low energy prices offset by lower ASP. Margins have fallen in the last two years as cement producers had been reluctant to pass on all of the cost increases. EBITDA margins have fallen by almost 400 bps for both of the cement players, to 31%/34%, attributed to soft demand in the last two years and also to discourage foreign players from entering Indonesia. The cost pressure has eased recently as electricity tariff had been reduced by 15% m-o-m in January (after the 65% hike last year) and a further 2% in February and subsidised diesel price have also been reduced twice in January (-14.6% total after 36.4% hike in Nov 2014). However, these benefits were short-lived as Jokowi had recently instructed SOE cement companies (Semen Indonesia (SMGR) and Semen Baturaja (SMBR)) to reduce bag cement price by Rp3,000/bag (cut by 4-5%) because of the lower energy price. This is the first time that a president has played a role in determining cement prices, and we fear Jokowi would continue to control SMGR’s and SMBR’s cement prices, and erase prospects of margins recovery as a result of lower costs. Rich valuations unwarranted given slower growth and declining ROE. We forecast SMGR and INTP will register slower earnings growth in the next three years (c.5% vs. 13-16% over FY09-13), as their margins continue to decline. EBITDA margins are expected to drop by further 400-500 bps between FY14 and FY17. And ROE would drop from 30.5%-27.1% (in FY12) to 19%-20% (in FY17). These could lead to a derating of the two stocks, from 15-16/14-15x FY15/16 P/E (5 year mean). Our TPs are pegged to 12-13x FY16 EPS (-1Sd of mean) to reflect the weak outlook for the sector. Therefore, we initiate coverage of SMGR and INTP with FULLY VALUED calls.

Industry Focus

Indonesia Cement Sector

Page 4

Key risks to our call. 1) Strong property sales. We expect property sales to be relatively flat this year. But if sales unexpectedly surge this year, there would be upside risk to our demand assumptions. 2) Stronger-than-expected economic growth. If GDP growth is significantly higher than our assumption (>7%), there could be upside risk to our sales volume and utilisation rate assumptions. 3) Major delays in new greenfield projects. If the new players’ plants are delayed by more than a year, there would be downside to our supply assumption, and utilisation rate would be higher, and pricing power of the incumbents would be higher than we predicted. 4) Further drop in coal and oil prices and/or a stronger IDR. If coal and oil prices continue to tumble or the IDR strengthens sharply this year, Indonesian cement players will see minimal cost increases and enjoy stronger margins, assuming the government does not further interfere in cement pricing.

Industry Focus

Indonesia Cement Sector

Page 5

Supply/Demand Outlook

Growth forecast Demand to recover after a slow year, but growth will not be spectacular. Historically, near-term cement demand has strong positive correlation with GDP growth, property presales, as well as infrastructure development. Of these determining factors, only infrastructure development is positive in the near term, as we expect slow economic growth and a lackluster property market this year. But infrastructure development will mainly lift demand for bulk cement, which is a much smaller contributor than bag cement and faces the most competition because there is little differentiation between products. We also do not expect the multiplier effect from infrastructure development to kick in soon, given several headwinds in the property sector in the near term. Indonesia: Cement domestic consumption breakdown

Source: Semen Indonesia Presentation Bulk cement sales will continue to grow faster than bag cement. The bulk segment has been growing faster than bag segment every year since 2008, and contribution has grown from 15% to 22% last year. Following the recent cut in fuel subsidy, the government will save c.Rp200tr under the APBN (Central Government Budget), and based on 2015 RAPBN-P (revised budget), c.50% of the savings would be channeled into infrastructure development. As a result, we expect to see large infrastructure projects being rolled out in the coming years. Such projects typically use bulk cement, which supports our thesis that the bulk segment will continue to grow rapidly in the next few years. We estimate bulk sales will grow by 14%/18%/20% in FY15/16/17, to take bulk contribution to 27% by 2017.

Indonesia: Construction spending as % of GDP

Source: CEIC, DBS Vickers, AllianceDBS SOE contractors: new contracts (in Rp bn)

Source: Companies, DBS Vickers, AllianceDBS Cement: bag vs. bulk sales volume (in m tons) and growth

Source: ASI, DBS Vickers, AllianceDBS

Bulk21.0%

Bag79.0%

Housing:c.90%

Cement based industry: c.10%

RMC: c..60%

Fabricator: c.35%

Projects (mortar, render): c.5%

0%

2%

4%

6%

8%

10%

12%

0100200300400500600700800900

1,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Rp bn

Construction spending (LHS) % of GDP (RHS)

3%

14%

26%

19%

0%

5%

10%

15%

20%

25%

30%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2012 2013 2014 2015F 2016F

WIKA PTPP WSKT yoy growth

32.2 32.8 34.2 39.2 44.1 45.7 46.9 48.7 51.2 54.6

5.9 6.2 6.6

8.8 10.8 12.2 13.0

14.8 17.5

21.0

0%

5%

10%

15%

20%

25%

30%

35%

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 2013 2014 2015F 2016F 2017F

Bag Bulk Bag's yoy growth Bulk's yoy growth Bulk's contribution

in m tons

Industry Focus

Indonesia Cement Sector

Page 6

Large housing backlog + growing middle-class = robust long term demand; but there are headwinds in the near-term The property sector will remain bullish over the long term supported by the large housing deficit, a young population, and urbanisation. However, there are several headwinds in the near term. Our Indonesia Property analyst expects transaction volume for listed property developers to drop this year as the affordability ratio is stretched, albeit still lower than in regional cities (see “When the going gets tough” dated 2 Dec 2014 by Edward Tanuwijaya). The other headwinds are: Regulations and liquidity tightening risk Upward trend in BI rate Possible revision to Income Tax article 22 to extend the

scope of residential properties that are subject to 5% additional tax

The slow growth of the Property sector in the near-term will have an impact on cement demand, especially bag cement. Hence, we forecast demand for bag cement to be muted (4-5%) in the next two years. Jakarta property price/income ratio is rising

Source: Numbeo, DBS Vickers Indonesia: maximum Loan-to-Value (LTV) regulation

Category Maximum LTV

1st mortgage 2nd mortgage 3rd mortgage

onwards

House > 70 sqm 70% 60% 50% House 22 - 70 sqm - 70% 60% Apartment > 70 sqm 70% 60% 50% Apartment 22 - 70 sqm 80% 70% 60% Apartment < 21 sqm - 70% 60% Shophouse - 70% 60%

Source: Bank Indonesia (BI), DBS Vickers

Indonesia: Possible revision to income tax article 22 Threshold to be taxed under tax income

article 22

No Taxed Items

Current regulation (PMK no. 253/2008)

Proposed changes

1 Landed residential

1) Transaction value > Rp10bn and/or 2) Building area > 500m2

1) Transaction value > Rp2bn and/or 2) Building area > 400m2

2

Apartment, condominium, etc

1) Transaction value > Rp10bn and/or 2) Building area > 400m2

1) Transaction value > Rp2bn and/or 2) Building area > 150m2

Source: Various sources, DBS Vickers BI rate movement

Source: Bank Indonesia (BI), DBS Vickers Indonesia: Marketing sales of listed property companies

Source: Companies, DBS Vickers Multiplier effects will take years to kick in We are bullish on the multiplier effects of infrastructure projects, especially road construction. Better road access will trigger more housing and commercial developments, which will then be followed by other property developments. These would boost cement consumption further. But this will not kick in so soon as the removal of fuel subsidy will reduce disposable income, and in turn, demand for property.

0

2

4

6

8

10

12

14

16

18

2009 2010 2011 2012 2013 2014

x

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14

BI Rate

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2009 2010 2011 2012 2013 2014F 2015F

+56% CAGR

flattishRpbn

Industry Focus

Indonesia Cement Sector

Page 7

Significant new capacity in the next three years New supply will be twice that of cement demand growth, utilisation will drop below 75% by 2017. Between 2002 and 2017F, we note 3 distinct stages in the demand and supply dynamics of Indonesia cement industry. From 2002 to 2008, supply was more or less constant while demand grew in line with GDP (5.7% CAGR), lifting utilisation gradually from 61% to 80%. Between 2010 and 2013, the unexpected property boom drove cement demand to the roof (12.5% CAGR or about 2x GDP growth). During that period, incremental demand (17.2m

tons) was more than of incremental supply (7.7m tons), pushing domestic utilisation rate to over 95%. We are now entering the third phase, where incremental supply will be significantly more than incremental demand. We forecast new supply in the next three years to reach 34m tons compared to only c.16m tons forecast incremental demand. The biggest incremental supply will come in 2016, which would push utilisation to below 80% for the first time since 2010. By 2017, we estimate utilisation would drop further to 74%, similar to 2007 level.

Indonesia cement industry: supply, demand and utiliaation rate

Source: Companies, DBS Vickers, AllianceDBS Indonesia: Utilisation rate will continue to drop as incremental supply outpaces new demand

Source: Companies, DBS Vickers, AllianceDBS

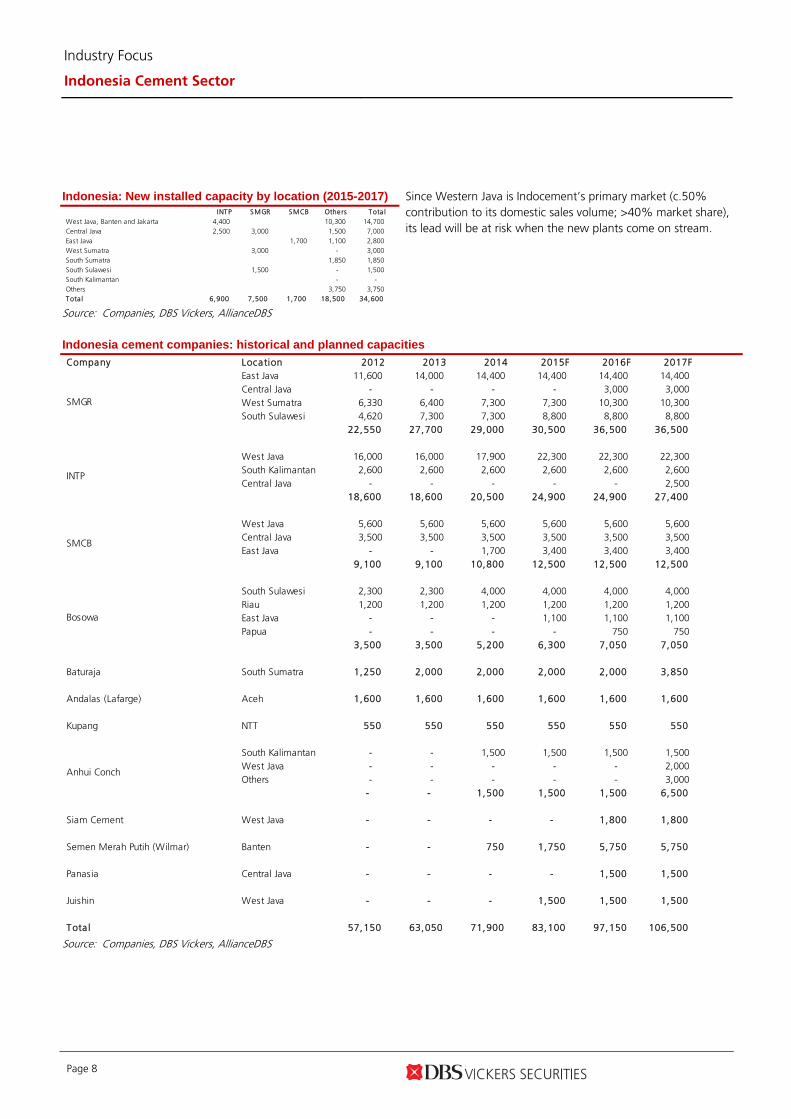

New players eyeing Western Java; Indocement will hurt the most. Since cement is a regional product in Indonesia, not all areas are equally affected. Based on the manufacturers’ expansion plans, Western Java (West Java, Jakarta and Banten) faces the biggest supply risk as 14.7m tons (or 42%) of new supply will be in that region, with 70% of that supply coming from new players (Anhui Conch, Siam Cement and Semen Merah Putih). The incremental new capacities in Java will reach 18.2m tons by end 2017, assuming no major delays in greenfield projects. This is almost twice our forecasted incremental demand of c.10m tons for Java.

61% 61%67% 68% 70%

73%

80%76% 77%

88%

96% 95%

89%85%

77%74%

0%

20%

40%

60%

80%

100%

120%

0

20,000

40,000

60,000

80,000

100,000

120,000

Demand (000 tons) Capacity (000 tons) Utilization rate

Capacity was flat for >6 years, demand growing in line with GDP

Aggressive expansion plans by incumbents and new entrants

Property boom fuelled cement demand

3,054 2,029

3,587

5,105

6,884

3,750

6,300 7,600

14,300

12,550

60%

65%

70%

75%

80%

85%

90%

95%

100%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2013 2014 2015F 2016F 2017F

Incremental demand Incremental effective supply* Utilization rate (RHS)

(in 000 tons)

Industry Focus

Indonesia Cement Sector

Page 8

Indonesia: New installed capacity by location (2015-2017)

Source: Companies, DBS Vickers, AllianceDBS

Since Western Java is Indocement’s primary market (c.50% contribution to its domestic sales volume; >40% market share), its lead will be at risk when the new plants come on stream.

Indonesia cement companies: historical and planned capacities

Source: Companies, DBS Vickers, AllianceDBS

INTP SMGR SMCB Others Tota lWest Java, Banten and Jakarta 4,400 10,300 14,700 Central Java 2,500 3,000 1,500 7,000 East Java 1,700 1,100 2,800 West Sumatra 3,000 - 3,000 South Sumatra 1,850 1,850 South Sulawesi 1,500 - 1,500 South Kalimantan - - Others 3,750 3,750 Tota l 6,900 7,500 1,700 18,500 34,600

Company Location 2012 2013 2014 2015F 2016F 2017FEast Java 11,600 14,000 14,400 14,400 14,400 14,400 Central Java - - - - 3,000 3,000 West Sumatra 6,330 6,400 7,300 7,300 10,300 10,300 South Sulawesi 4,620 7,300 7,300 8,800 8,800 8,800

22,550 27,700 29,000 30,500 36,500 36,500

West Java 16,000 16,000 17,900 22,300 22,300 22,300 South Kalimantan 2,600 2,600 2,600 2,600 2,600 2,600 Central Java - - - - - 2,500

18,600 18,600 20,500 24,900 24,900 27,400

West Java 5,600 5,600 5,600 5,600 5,600 5,600 Central Java 3,500 3,500 3,500 3,500 3,500 3,500 East Java - - 1,700 3,400 3,400 3,400

9,100 9,100 10,800 12,500 12,500 12,500

South Sulawesi 2,300 2,300 4,000 4,000 4,000 4,000 Riau 1,200 1,200 1,200 1,200 1,200 1,200 East Java - - - 1,100 1,100 1,100 Papua - - - - 750 750

3,500 3,500 5,200 6,300 7,050 7,050

Baturaja South Sumatra 1,250 2,000 2,000 2,000 2,000 3,850

Andalas (Lafarge) Aceh 1,600 1,600 1,600 1,600 1,600 1,600

Kupang NTT 550 550 550 550 550 550

South Kalimantan - - 1,500 1,500 1,500 1,500 West Java - - - - - 2,000 Others - - - - - 3,000

- - 1,500 1,500 1,500 6,500

Siam Cement West Java - - - - 1,800 1,800

Semen Merah Putih (Wilmar) Banten - - 750 1,750 5,750 5,750

Panasia Central Java - - - - 1,500 1,500

Juishin West Java - - - 1,500 1,500 1,500

Tota l 57,150 63,050 71,900 83,100 97,150 106,500

SMGR

INTP

SMCB

Bosowa

Anhui Conch

Industry Focus

Indonesia Cement Sector

Page 9

Positive impact from weak energy prices offset by lower ASP Energy accounts for a big chunk of cement players’ cash cost. Coal/fuel accounts for about 20% of SMGR’s and INTP’s cash costs, while electricity accounts for 12-14%. Distribution, transportation and handling costs are also a major cost items, at c.24%/16% of SMGR’s/INTP’s cash costs. We estimate c.30% of the distribution, transportation and handling costs is from diesel, so the price of coal, electricity and diesel collectively account for c.40% of SMGR’s and INTP’s cash costs. SMGR and INTP: cash cost breakdown

Source: Semen Indonesia, Indocement, DBS Vickers, AllianceDBS Benefits of low coal and oil prices offset by recent price control. The benefit of lower energy prices was short-lived for Indonesian cement companies, after Jokowi instructed SMGR and SMBR to cut bag cement price by 4-5%. With c.46% market share between them, this move would have a significant impact on the industry. We expect Indocement (INTP) and Holcim (SMCB) to also lower prices to protect their market shares. In fact, INTP said they have lowered the price of cement in Jakarta (where they are the price leader) by Rp3,000 to maintain the same gap with the rest of the players. We think SMGR’s share price will be affected more by this as: 1) the stock offers lower dividend yield than INTP, and even

that may be cut; and 2) INTP has greater flexibility in determining selling price. If

utilisation remains high, INTP has the option to reduce selling price by a smaller quantum.

Lingering risk of further margin erosion. There will be further margin erosion once the new supply comes on stream from 2016 onwards. Falling oil price could delay the negative impact on cement players’ margins. But this could be short-lived once the new supply comes on stream; we would not discount a price war to gain market share. Our base case assumption is that EBITDA margins will decline by c.500 bps between FY13 and FY17 as cement utilisation rate drops from 95% to 74%. Utilisation rates vs. EBITDA margins

Source: Semen Indonesia, Indocement, DBS Vickers, AllianceDBS Floating electricity and diesel prices imply higher earnings volatility. Starting January 2015, electricity tariff is revised monthly using the following formulas: Tariffnew = Tariffold * (1 + Adjustment)

Tariffold = 1,191 per kWh (based on the tariff regulation set in

Permen ESDM number 09/2014)

Adjustment = %(Kexchange_rate * exchange_rate) + %(Kicp *

ICP) + %(Kinflation * inflation) where, K is the coefficient of

each variable in place, determined by PLN each month

exchange_rate = the difference between the average USD/IDR

exchange rate (2 months prior) and the USD/IDR exchange rate

assumption in 2013 APBN (Rp9,300/USD)

ICP = the difference between Indonesia Crude Price (2 months

prior) and the Indonesia Crude Price assumption in 2013 APBN

(US$100/barrel)

inflation = the difference between monthly inflation rate (2

months prior) and the monthly inflation rate assumption in 2013

APBN (4.9%/12 months)

YTD, the tariff for I4 has been lowered twice (-15%/-2% m-o-m in Jan/Feb) following the sharp drop in the oil price. The adjustment for January/February was based on ICP, USD/IDR exchange rate and inflation rate in November/December 2014 (2

20.1% 19.2%

12.2% 13.7%

23.6%15.9%

8.4%

7.8%

35.7%43.4%

SMGR INTP

Coal/fuel Electricity Distribution, transportation and handling Direct labor Others

20%

25%

30%

35%

40%

45%

50%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014F 2015F 2016F 2017F

Cement's utilization rate INTP's EBITDA margin SMGR's EBITDA margin

Industry Focus

Indonesia Cement Sector

Page 10

months lag). Prices of subsidised gasoline/diesel was also cut by c.13%/12% in January 2015, also due to the sharp drop in ICP. Based on January 2015 prices, the government has completely removed the subsidy for gasoline, but there is still a Rp1,000/liter

subsidy for diesel. This means that subsidised fuel prices will also be floated starting this year. Floating electricity and fuel prices imply higher earnings volatility for cement players going forward.

Electricity tariff for I4 (Industry with >30,000 kVa of power)

Source: PLN, DBS Vickers Historical subsidised fuel prices

Source: Pertamina, DBS Vickers

600

700

800

900

1,000

1,100

1,200

1,300

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Electricity tariff for I4 (per kWh)

in Rp

13% hike every 2 months (65% total increase)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-

05M

ay-0

5Se

p-05

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

a y-0

7Se

p-07

Jan-

08M

a y-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15

Gasoline Diesel

Gasoline price was hiked by 89% in 18 mths

Subsidized fuel price have been lowered twice in January due to low oil price

Industry Focus

Indonesia Cement Sector

Page 11

Premium valuation to narrow as oligopoly structure breaks down More attractive industry structure than China and Thailand, but advantages will gradually be eroded. Indonesian cement players have been enjoying high margins due to the oligopoly structure of the industry, with the top 3 players controlling nearly 90% market share. In Thailand, the top 3 players command c.80% market share, while in China, the top 10 players only control 40-45% market share. In terms of utilisation rate, it was 89% for Indonesia last year vs. 85% for Thailand and 75% for China. However, despite higher forecast

demand growth for Indonesia, we still expect utilisation rates to continue to drop over the next three years to c.74% as new players aggressively ramp up production. As such, we estimate the market share of the top 3 players would fall to c.82% by FY17. Valuation wise, Indonesian cement players are trading on par with Siam Cement and at a premium to the China players, despite slower expected earnings growth. But with the Indonesian cement players experiencing an unprecedented structural shift, we expect their current premium valuation relative to China peers to narrow.

Cement Sector: Indonesia vs Thailand and China

Source: Companies, DBS Vickers Peer comparison of regional cement companies

Company Ticker Code

Current Price (local currency)

Market Cap (USDm)

P/E EV/EBITDA ROE FY15

FY15 FY16 FY15 FY16 Semen Indonesia SMGR IJ 14,525 6,863 14.2 13.5 9.4 8.7 23% Indocement INTP IJ 23,000 6,768 15.1 14.2 9.4 8.7 22% Holcim Indonesia* SMCB IJ 1,970 1,204 15.2 12.8 7.9 7.0 18% Indonesia 14.8 13.5 8.9 8.1 Anhui Conch 914 HK 26.8 18,337 9.0 8.2 5.3 5.2 19% CNBM 3323 HK 7.6 5,288 5.3 5.0 8.3 8.1 14% China Shanshui 691 HK 3.7 1,611 10.8 8.8 7.0 6.4 7% West China Cement 2233 HK 0.9 518 12.4 10.0 4.7 4.5 8% CR Cement 1313 HK 4.7 3,877 6.6 6.4 5.5 5.3 16% China 8.8 7.7 6.2 5.9 Siam Cement SCC TB 472.0 17,688 15.0 13.7 10.3 9.6 20% Thailand 15.0 13.7 10.3 9.6

Source: Bloomberg Finance L.P., DBS Vickers Note*: Based on consensus forecasts

Country CompanyCement Production Capacity (m ton) Uti l iza tion ra te

FY15 demand growth

FY16 demand growth

Semen Indonesia 28.5Indocement 21.5Holchim Indonesia 10.1CNBM 400Anhui Conch 260China Shanshui 107West China Cement 27CR Cement 77

Thailand Siam Cement* 56 85% 5% 5%

China

6.0%Indonesia

75%

8.0%

2.5% 2.5%

98%

Industry Focus

Indonesia Cement Sector

Page 12

STOCK PROFILES

www.dbsvickers.com ed: SGC / sa: MA

FULLY VALUED Rp23,800 JCI : 5,325.50 (Initiating Coverage) Price Target : 12-Month Rp20,200 Reason for Report : Initiating coverage Potential Catalyst: Strong property sales, lower coal and oil price

Analyst Deidy WIJAYA +6221 3003 4931 [email protected]

CHONG Tjen San, CFA +603 2604 3972 [email protected]

Price Relative

Forecasts and Valuation FY Dec (Rp bn) 2013A 2014F 2015F 2016F Revenue 18,691 20,141 22,222 25,089 EBITDA 6,785 6,953 7,370 7,863 Pre-tax Profit 6,595 6,808 7,133 7,510 Net Profit 5,010 5,174 5,421 5,707 Net Pft (Pre Ex.) 5,010 5,174 5,421 5,707 EPS (Rp) 1,361 1,406 1,473 1,550 EPS Pre Ex. (Rp) 1,361 1,406 1,473 1,550 EPS Gth (%) 5 3 5 5 EPS Gth Pre Ex (%) 5 3 5 5 Diluted EPS (Rp) 1,361 1,406 1,473 1,550 Net DPS (Rp) 900 929 974 1,025 BV Per Share (Rp) 6,234 6,739 7,282 7,859 PE (X) 17.5 16.9 16.2 15.4 PE Pre Ex. (X) 17.5 16.9 16.2 15.4 P/Cash Flow (X) 16.2 16.5 14.3 13.7 EV/EBITDA (X) 11.1 10.8 10.2 9.5 Net Div Yield (%) 3.8 3.9 4.1 4.3 P/Book Value (X) 3.8 3.5 3.3 3.0 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 23.7 21.7 21.0 20.5 Earnings Rev (%): - - - Consensus EPS (Rp): 1,411 1,533 1,755 No. of brokers following: B: 20 S: 5 H: 8 ICB Industry : Industrials ICB Sector: Construction & Materials Principal Business: Indocement was established in 1975. The expanded heavily in the 90’s, prior to Heidelberg Cement Group becoming the majority shareholder in 2001. The company now trades under the brand “Tiga Roda”.

Source of all data: Company, DBS Vickers, AllianceDBS, Bloomberg Finance L.P

At A Glance Issued Capital (m shrs) 3,681 Mkt. Cap (Rpbn/US$m) 87,613 / 6,868 Major Shareholders HC Indocement Gmbr (%) 64.1 Mekar Perkasa (%) 13.0 Free Float (%) 22.9 Avg. Daily Vol.(‘000) 3,433

DBS Group Research . Equity 17 Feb 2015

Indonesia Company Focus

Indocement Tunggal Prakarsa Bloomberg: INTP IJ | Reuters: INTP.JK Refer to important disclosures at the end of this report

Most vulnerable to competition Heavily reliant on Java with >70% of sales

volume coming from Java

New players aggressively entering Western Java poses significant threat

Premium margins to face pressure

Initiate with Fully Valued (TP Rp20,200) as valuation is rich at 15x FY16 EPS

Core primary market to face headwinds. INTP derives >70% of its sales volume from Java, while Western Java (West Java, Jakarta and Banten) alone contributes almost 50% of its total sales volume. Based on the companies’ expansion plans, Western Java faces the biggest supply risk as 14.7m tons (or 42%) of the new supply will be from that region and 70% of that supply is coming from new players (Anhui Conch, Siam Cement and Semen Merah Putih).

Premium margins to face pressure. Indocement (INTP) is currently the most profitable cement company with c.35% EBITDA margin primarily due to its pricing power and centralised facilities. It trades under the “Tiga Roda” brand, arguably the most widely known cement brand in the country. It benefits from economics of scale from centralised facilities. However, we think this position will be soon under pressure with the additional competition and we project utilisation rates to fall to 88% in 2017 (94% now) bringing down EBITDA margins to 29.5% (FY17).

Initiate with FULLY VALUED given rich valuation. INTP is currently trading at c.16x 12M forward P/E (above 5-year mean), despite slowing growth (c.5% CAGR FY14-17) and declining ROEs. This appears unjustified in our view with the changing demand and supply dynamics. Moreover, the multiplier effect from infrastructure boom will likely only filters through in 2017 which may coincide with a price war from the heightened competition. Our TP of Rp20,200 is based on 13x FY16 EPS (-1sd below its 5 year mean P/E).

71

91

111

131

151

171

191

211

10,080.0

12,080.0

14,080.0

16,080.0

18,080.0

20,080.0

22,080.0

24,080.0

26,080.0

28,080.0

Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

Relative IndexRp

Indocement Tunggal P. (LHS) Relative JCI INDEX (RHS)

Page 14

Company Focus

Indocement Tunggal Prakarsa

INVESTMENT THESIS

Profile Rationale

Indocement (INTP) is the most profitable cement player with the highest margin. It trades under “Tiga Roda” brand, arguably the most widely known brand in Indonesia. It is the market leader in Western Java where its sales volume is concentrated at (c.50%). It commands a higher margin due to its centralised production facilities and premium pricing. It also has a strong RMC arm.

Cement industry is facing an unprecedented structural shift We estimate new supply to be more than double of new

demand, bringing utilisation down from 89% to 74% by 2017.

Margin projected to keep sliding due to weakening pricing power and increasing contribution from bulk cement 3 major players are entering Indonesia – Semen Merah

Putih (Wilmar Group), Anhui Conch and Siam Cement. Anhui Conch and Siam Cement are market leaders in China and Thailand respectively. With their Indonesia plants contributing only c.3% to their total capacities, there could be price war once their plants come on stream as they try to gain market share.

The fast growing segment in Indonesia is the bulk segment (contribution estimated to rise from 22% to 27% by FY17), which is used for infrastructure projects and high rise buildings. With less barriers to entry (brand equity and distribution channels), this segment (which already commands lower margins) will be the likely target for the new entrants.

Benefits from low energy prices offset by lower ASP After Semen Indonesia (SMGR) and Semen Baturaja

(SMBR) reduced their prices last month, INTP has also lowered its prices in certain areas to maintain the gap between its product and the competitors’.

Rich valuations unwarranted given slower growth and declining ROE INTP is currently trading at 16x 12M forward P/E (above 5

year mean) despite slowing earnings growth and declining

ROE.

Valuation Risks

Our target price of Rp20,200 is pegged to 13x FY16 EPS (-1 sd of 5 year mean). Initiate with FULLY VALUED call as there is more than 10% downside from the current price

Weak demand growth due to slow rollout of infrastructure projects If the new government does not live up to expectation in speeding up infrastructure development, cement demand growth could disappoint, thus hurting INTP’s utilisation and profitability.

Competition in Western Java INTP’s dominance in Western Java could be under threat once the new players start productions. We think that there would be oversupply in Western Java by 2017 and INTP’s dominance in that region will be under severe threat.

Source: DBS Vickers, AllianceDBS

Page 15

Company Focus

Indocement Tunggal Prakarsa

SWOT Analysis

Strengths Weakness

Centralised facilities. The company adopts a centralised strategy which allows it to obtain economies of scale. Sharing of facilities, largely weighted in West Java enables the company to minimize the cost of production. Strong brand image, especially in Java. INTP trades under the brand “Semen Tiga Roda” which is arguably the most widely known brand in the country. Its brand image is especially strong in Western Java, where it is currently the market leader. It has a strong RMC arm. As RMC is widely used for infrastructure projects, it stands to benefit from potential infrastructure boom.

Lack of presence outside Java. 72% of its cement sales came from Java, so INTP’s cement sales is very heavily dependent on the performance of a single island. Less packing plants compared to SMGR. Currently INTP do not have as many packing plants as SMGR. Therefore, distribution time and readiness of stock can be a problem when demand suddenly spikes up.

Opportunities Threats

Geographically, the company still has a lot of room to expand. As the company is currently very heavily weighted in Java, it has ample opportunities to expand to other islands, backed by its strong balance sheet.

New players (Anhui Conch, Siam Cement and Semen Merah Putih) are all eyeing Western Java, Indocement’s primary market. Based on the companies’ expansion plans, Western Java faces the biggest supply risk as 14.7m tons (or 42%) of the new supply will be from that region and 70% of that supply is coming from new players (Anhui Conch, Siam Cement and Semen Merah Putih).

Source: DBS Vickers, AllianceDBS

Page 16

Company Focus

Indocement Tunggal Prakarsa

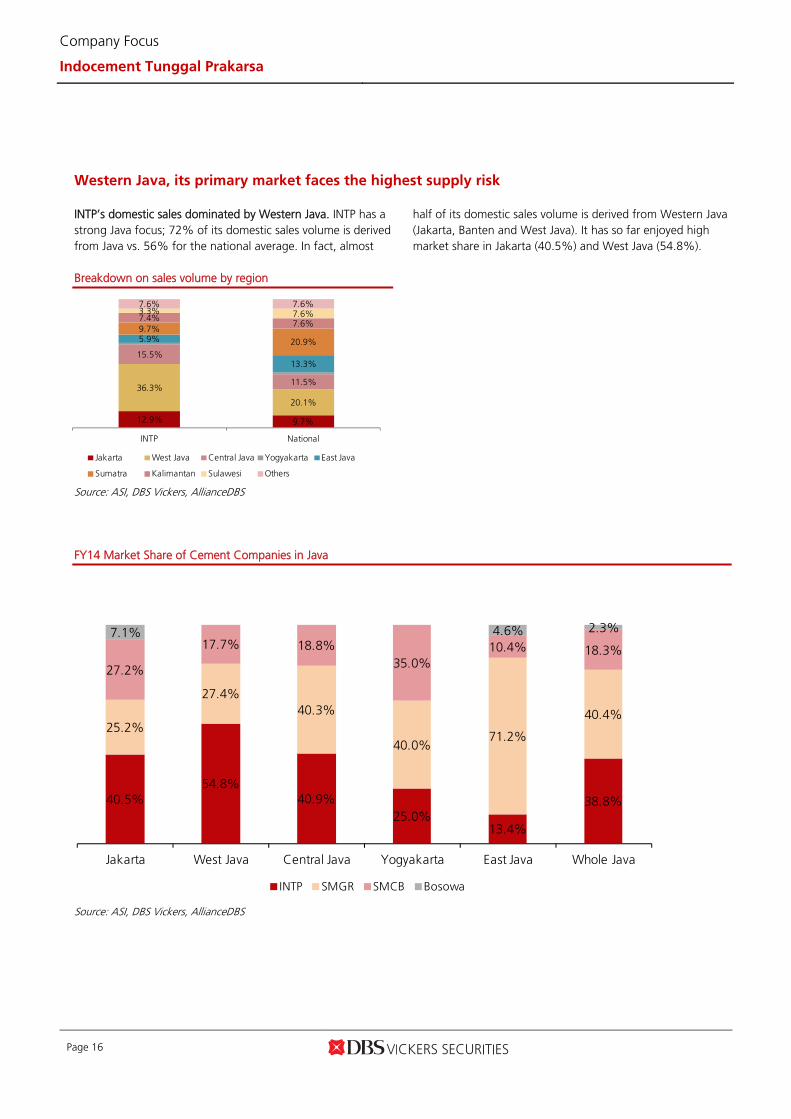

Western Java, its primary market faces the highest supply risk INTP’s domestic sales dominated by Western Java. INTP has a strong Java focus; 72% of its domestic sales volume is derived from Java vs. 56% for the national average. In fact, almost

half of its domestic sales volume is derived from Western Java (Jakarta, Banten and West Java). It has so far enjoyed high market share in Jakarta (40.5%) and West Java (54.8%).

Breakdown on sales volume by region

Source: ASI, DBS Vickers, AllianceDBS

FY14 Market Share of Cement Companies in Java

Source: ASI, DBS Vickers, AllianceDBS

12.9% 9.7%

36.3%

20.1%

15.5%

11.5%

5.9%

13.3%

9.7%

20.9%

7.4%7.6%

3.3% 7.6%7.6% 7.6%

INTP National

Jakarta West Java Central Java Yogyakarta East Java

Sumatra Kalimantan Sulawesi Others

40.5%54.8%

40.9%25.0%

13.4%

38.8%

25.2%

27.4%40.3%

40.0%71.2%

40.4%

27.2%

17.7% 18.8%35.0%

10.4% 18.3%7.1% 4.6% 2.3%

Jakarta West Java Central Java Yogyakarta East Java Whole Java

INTP SMGR SMCB Bosowa

Page 17

Company Focus

Indocement Tunggal Prakarsa

Incoming supply is largely in Western Java. Based on cement companies’ guidance, we estimate that 42% (14.7m tons) of the incoming supply in the next 3 years will be located in Western Java. INTP faces intensifying competition as 70% (14.7m tons) of the new capacities will come from new players. Even if we assume an aggressive growth rate of 10% CAGR between FY14-17 for Western Java, the incremental demand from this region would only be 5.9m tons or merely

40% of the potential increment in capacity. We are concerned that new players would sacrifice margin to gain market share as they try to ramp up their utilisation rate. INTP’s margin, currently being the highest in Indonesia, is therefore at significant risk. Therefore, we built in EBITDA margin erosion from 36.3-34.5% in FY13-FY14 to 33.2-29.7% in FY15-FY17F respectively.

New installed capacity by location (2015-2017)

Source: Companies, DBS Vickers, AllianceDBS

INTP SMGR SMCB Others Tota lWest Java, Banten and Jakarta 4,400 10,300 14,700 Central Java 2,500 3,000 1,500 7,000 East Java 1,700 1,100 2,800 West Sumatra 3,000 - 3,000 South Sumatra 1,850 1,850 South Sulawesi 1,500 - 1,500 South Kalimantan - - Others 3,750 3,750 Tota l 6,900 7,500 1,700 18,500 34,600

Page 18

Company Focus

Indocement Tunggal Prakarsa

Company Background Corporate History. Indocement was established in 1975. In 1989, the Company became PT. Indocement Tunggal Prakarsa following a merger with 6 companies. Two years later, the Company became listed. Following major expansions in the 90’s, Heidelberg Cement Group acquired a majority stake in 2001.

The Company trades cement under the brand “Tiga Road” and currently supplies a number of products ranging from PCC and OPC to less common cements such as oil well cements and white masonry. The Company prides itself as the introducer of Portland Composite Cement (PCC) to Indonesia. Currently, the majority of INTP’s sales volume comes from PCC.

Sales Trend Profitability Trend

Source: Company, DBS Vickers, AllianceDBS

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

5,000

10,000

15,000

20,000

25,000

2012A 2013A 2014F 2015F 2016F

Rp bn

Total Revenue Revenue Growth (%) (YoY)

4,760

5,260

5,760

6,260

6,760

7,260

2012A 2013A 2014F 2015F 2016F

Rp bn

Operating EBIT Pre tax Profit Net Profit

Page 19

Company Focus

Indocement Tunggal Prakarsa

Key Management Team

Christian Kartawijaya President Director

He was appointed as the President Director in May 2014. He has been a member of the Board of Director since 2004. He holds an MBA degree from San Diego State University and Master of Arts in Christian Education from SWBTS, Fort Worth, Texas, USA.

Franciscus Welirang Vice President Director

Has been VP since early 2011. Concurrently also the VP commisioner for Lonsum, diector for Indofood and the chairman for the Indonesian Wheat Flour Producers Association. Was also the President commisioner for the Surabaya Stock Exchange. Graduated from Chemical engeneering from South Bank Polytechnic, England.

Kuky Permana Director

Joined the company in 1978 and became a director in 2006. Previously the Deputy Technical Director of the company. Has a Degree in Civil and Municipal Engineering from University College, London, UK.

Hasan Imer Director

Has been a director since 2008. Previosly was project and investment manager in Turkey . Was also the Asian Regional Coordinator for the Group at the Heidelberg Technology Center. In Germany up until 2004. Holds a degree in Mechanical Engineering from Istanbul State Engineering and Architecture Academy, Turkey.

Tjue Lie Sukanto Director

Appointed director in 2011. Previously served as the Finance Director for a German company subsidiary in Indonesia, beforebecoming the manager for the purchsing division in Indocement. Holds a degree in Industrial Management and Engineering, majoring in Finance and accounting from University of Karlsruhe, Germany.

Ramakanta Bhattacharjee Director

Appointed director in November 2012. Prior to joining Indocement, he served as Deputy Managing Director, HeidelbergCement Bangladesh Ltd. He holds a Bachelor’s of Science in Electrical and Electronic Engineering from Chittagong University of Engineering and Technology in 1988 and a Master’s degree in Business Administration & Management in 1994 from Southeastern University, London, England. Bangladeshi citizen, age 49.

Daniel Kundjono Adam Director

Appointed as director in December 2013. Previously, was the Sales and Marketing Division Manager of the Company since 2002. He holds an MBA degree from Institut Pendidikan dan Pembinaan Manajemen, Jakarta.

Benny S. Santoso Director

Director since 1994. Also serve as President commisioner for PT. Nippon Indosari and commisioner for Indoofood. Also director for First Pacific Co. Ltd. Holds a degree from Ngee Ann College in Singapore.

Daniel R. Fritz Director

Has been director since 2009. Previously worked in Votorantim Cimentos, America as VP and COO. Holds a Bachelor Science dgree in Civil Engineering Technology from University of Massachusetts, USA.

Source: Company

Page 20

Company Focus

Indocement Tunggal Prakarsa

Key Business Risks Weak demand growth due to slow rollout of infrastructure projects. If the new government does not live up to expectation in speeding up infrastructure development, cement demand growth could disappoint, thus hurting INTP’s utilisation and profitability.

Competition in Western Java. INTP’s dominance in Western Java could be under threat once the new players start productions. We think that there would be oversupply in Western Java by 2017 and INTP’s dominance in that region will be under severe threat.

Upside Risks to Our Call

Strong rebound in property sales. We expect domestic property sales volume to register flattish growth for this year as there are plenty of headwinds in the near term – upward trend in BI rate, regulations and liquidity tightening risk as well as cost pressure from fuel subsidy removal. If property sales actually rebound strongly this year, there would be upside risk to our cement sales volume assumption as property is the biggest contributor to cement consumption. Further drop in oil and coal price. If coal and oil price continues their downtrend, INTP would benefit in the short

term. Almost 40% of its cash cost are linked to coal and oil price. Should coal and oil continue their downtrend, there would be upside to our margin and earnings assumptions for this year. Significant delay in new players’ Greenfield projects. If the new players’ Greenfield projects are delayed or cancelled, our incremental supply assumption would be overstated and cement utilisation rate would be understated. Competition could be less severe than our assumption and thus pricing power would be higher than we predicted.

Page 21

Company Focus

Indocement Tunggal Prakarsa

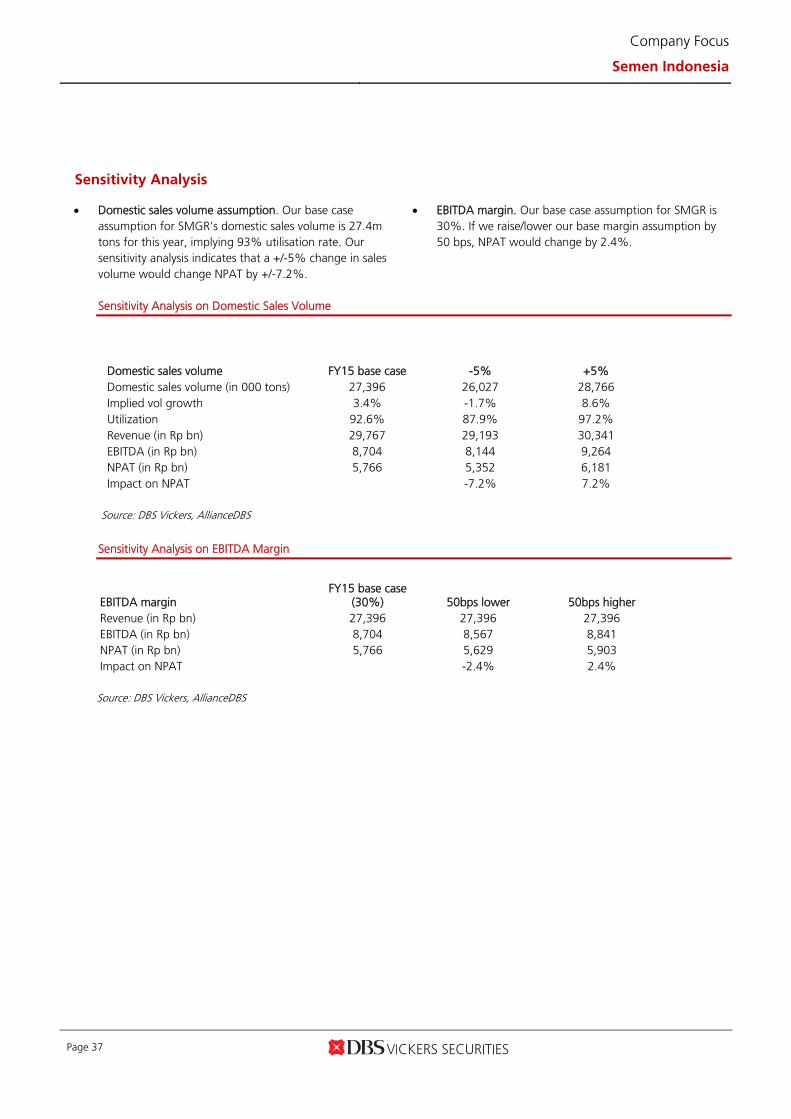

Sensitivity Analysis Domestic sales volume assumption. Our base case

assumption for INTP’s domestic sales volume to be 19.4m tons for this year, implying a utilisation rate of 90.8%. We performed sensitivity analysis and assumed 5% higher and lower sales volume. As a result, NPAT is impacted by +/-3.5%.

EBITDA margin. Our base case assumption for INTP’s EBITDA margin is 33.2%. If we raise/lower our margin assumption by 50 bps, NPAT would be impacted by 2.0%.

Sensitivity Analysis on Domestic Sales Volume

Domestic sales volume FY15 base case -5% +5% Domestic sales volume (in 000 tons) 19,350 18,383 20,318 Implied volume growth 6.4% 1.1% 11.7% Utilisation 90.8% 86.3% 95.3% Revenue (in Rp bn) 22,222 21,224 23,220 EBITDA (in Rp bn) 7,370 7,074 7,666 NPAT (in Rp bn) 5,421 5,230 5,611 Impact on NPAT -3.5% 3.5%

Source: DBS Vickers, AllianceDBS

Sensitivity Analysis on EBITDA Margin

EBITDA margin FY15 base case

(33.2%) 50bps lower 50bps higher Revenue (in Rp bn) 22,222 22,222 22,222 EBITDA (in Rp bn) 7,370 7,259 7,481 NPAT (in Rp bn) 5,421 5,310 5,532 Impact on NPAT -2.0% 2.0%

Source: DBS Vickers, AllianceDBS

Page 22

Company Focus

Indocement Tunggal Prakarsa

Key Assumptions

FY Dec 2011A 2012A 2013A 2014F 2015F 2016F Domestic Sales Vol ('000 tones)

15,122 17,611 17,642 18,189 19,350 20,769

Domestic ASP/tonne (in Rp)

862,953 911,182 958,265 1,001,387 1,031,428 1,075,780

EBITDA margin (%) 36.7 38.3 36.3 34.5 33.2 31.3 Segmental Breakdown

FY Dec 2011A 2012A 2013A 2014F 2015F 2016F Revenues (Rp bn)

Cement 13,260 16,115 17,046 18,316 20,076 22,567

Ready Mix Concrete 1,343 1,934 2,739 2,990 3,486 4,065

Aggregates 71 81 116 139 160 184

Other Businesses (786) (839) (1,209) (1,304) (1,501) (1,727)

Total 13,888 17,290 18,691 20,141 22,222 25,089

Operating profit (Rp bn)

Cement 4,404 5,799 6,139 6,026 6,276 6,503

Ready Mix Concrete (22) 76 (86) 0 70 203

Aggregates 7 2 11 21 24 28

Other Businesses 29 0 0 0 0 0

Total 4,418 5,877 6,064 6,047 6,370 6,734

Operating profit Margins (%)

Cement 33.2 36.0 36.0 32.9 31.3 28.8

Ready Mix Concrete (1.6) 3.9 (3.1) 0.0 2.0 5.0

Aggregates 9.9 2.5 9.2 15.0 15.0 15.0

Other Businesses (3.7) 0.0 0.0 0.0 0.0 0.0

Total 31.8 34.0 32.4 30.0 28.7 26.8

Source: Company, DBS Vickers, AllianceDBS

Sensitivity Analysis 2015

Domestic sales volume +/- 5%

Net Profit +/- 3.5%

EBITDA margin +/- 50bps

Net Profit +/- 2%

Growing RMC business

Page 23

Company Focus

Indocement Tunggal Prakarsa

Income Statement (Rp bn)

FY Dec 2011A 2012A 2013A 2014F 2015F 2016F Revenue 13,888 17,290 18,691 20,141 22,222 25,089

Cost of Goods Sold (7,474) (9,020) (10,037) (11,018) (12,330) (14,219)

Gross Profit 6,414 8,270 8,655 9,123 9,891 10,870

Other Opng (Exp)/Inc (1,987) (2,425) (2,680) (3,076) (3,521) (4,137)

Operating Profit 4,427 5,845 5,975 6,047 6,370 6,734

Other Non Opg (Exp)/Inc (9) 32 89 0 0 0

Associates & JV Inc 8 9 18 19 21 22

Net Interest (Exp)/Inc 282 354 513 742 742 754

Exceptional Gain/(Loss) 0 0 0 0 0 0

Pre-tax Profit 4,708 6,240 6,595 6,808 7,133 7,510

Tax (1,107) (1,476) (1,583) (1,634) (1,712) (1,802)

Minority Interest (5) (3) (2) 0 0 0

Preference Dividend 0 0 0 0 0 0

Net Profit 3,597 4,760 5,010 5,174 5,421 5,707

Net Profit before Except. 3,597 4,760 5,010 5,174 5,421 5,707

EBITDA 5,091 6,619 6,785 6,953 7,370 7,863

Growth

Revenue Gth (%) 24.7 24.5 8.1 7.8 10.3 12.9

EBITDA Gth (%) 9.7 30.0 2.5 2.5 6.0 6.7

Opg Profit Gth (%) 10.1 32.0 2.2 1.2 5.3 5.7

Net Profit Gth (%) 11.5 32.3 5.2 3.3 4.8 5.3

Margins & Ratio

Gross Margins (%) 46.2 47.8 46.3 45.3 44.5 43.3

Opg Profit Margin (%) 31.9 33.8 32.0 30.0 28.7 26.8

Net Profit Margin (%) 25.9 27.5 26.8 25.7 24.4 22.7

ROAE (%) 25.0 27.1 23.7 21.7 21.0 20.5

ROA (%) 21.5 23.3 20.3 18.8 18.4 17.9

ROCE (%) 21.9 24.1 20.5 18.5 18.1 17.8

Div Payout Ratio (%) 30.0 34.8 66.1 66.1 66.1 66.1

Net Interest Cover (x) NM NM NM NM NM NM

Source: Company, DBS Vickers, AllianceDBS

Margins Trend

21.0%

23.0%

25.0%

27.0%

29.0%

31.0%

33.0%

35.0%

2012A 2013A 2014F 2015F 2016F

Operating Margin % Net Income Margin %

We expect margins to keep declining as competition intensifies

Page 24

Company Focus

Indocement Tunggal Prakarsa

Quarterly / Interim Income Statement (Rp bn)

FY Dec 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014 3Q2014 Revenue 4,699 4,430 5,343 4,500 4,999 4,668

Cost of Goods Sold (2,443) (2,385) (2,958) (2,531) (2,764) (2,524)

Gross Profit 2,255 2,045 2,385 1,969 2,235 2,144

Other Oper. (Exp)/Inc (622) (614) (751) (753) (683) (777)

Operating Profit 1,633 1,431 1,635 1,216 1,551 1,367

Other Non Opg (Exp)/Inc 0 0 0 0 0 0

Associates & JV Inc 4 5 5 4 6 7

Net Interest (Exp)/Inc 117 105 172 218 215 180

Exceptional Gain/(Loss) 0 0 0 0 0 0

Pre-tax Profit 1,754 1,541 1,812 1,438 1,773 1,554

Tax (479) (354) (409) (307) (390) (348)

Minority Interest (1) 0 (1) (1) (2) 0

Net Profit 1,275 1,187 1,402 1,129 1,380 1,206

Net profit bef Except. 1,275 1,187 1,402 1,129 1,380 1,206

EBITDA 1,838 1,632 1,843 1,427 1,775 1,580

Growth

Revenue Gth (%) 11.4 (5.7) 20.6 (15.8) 11.1 (6.6)

EBITDA Gth (%) 17.8 (11.2) 12.9 (22.5) 24.4 (11.0)

Opg Profit Gth (%) 19.6 (12.4) 14.2 (25.6) 27.6 (11.9)

Net Profit Gth (%) 11.2 (6.9) 18.1 (19.4) 22.2 (12.6)

Margins

Gross Margins (%) 48.0 46.2 44.6 43.8 44.7 45.9

Opg Margins (%) 34.8 32.3 30.6 27.0 31.0 29.3

Net Profit Margins (%) 27.1 26.8 26.2 25.1 27.6 25.8

Revenue Trend

Source: Company, DBS Vickers, AllianceDBS

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

1,000

2,000

3,000

4,000

5,000

6,000

2Q

20

12

3Q

20

12

4Q

20

12

1Q

20

13

2Q

20

13

3Q

20

13

4Q

20

13

1Q

20

14

2Q

20

14

3Q

20

14

Revenue Revenue Growth % (QoQ)

1Q is seasonally weakest

Page 25

Company Focus

Indocement Tunggal Prakarsa

Balance Sheet (Rp bn)

FY Dec 2011A 2012A 2013A 2014F 2015F 2016F Net Fixed Assets 7,638 7,935 9,305 10,399 11,899 13,270

Invts in Associates & JVs 0 0 0 0 0 0

Other LT Assets 199 241 456 456 456 456

Cash & ST Invts 6,865 10,474 12,595 12,600 12,798 13,131

Inventory 1,328 1,470 1,474 1,790 2,004 2,310

Debtors 1,977 2,455 2,519 2,813 3,104 3,505

Other Current Assets 146 180 259 300 338 391

Total Assets 18,151 22,755 26,607 28,359 30,598 33,063

ST Debt

0 0 0 0 0 0

Other Current Liab 1,477 2,419 2,740 2,631 2,871 3,212

LT Debt 131 108 93 93 93 93

Other LT Liabilities 809 809 797 797 797 797

Shareholder’s Equity 15,706 19,388 22,947 24,808 26,808 28,930

Minority Interests 28 31 30 30 30 30

Total Cap. & Liab. 18,151 22,755 26,607 28,359 30,598 33,063

Non-Cash Wkg. Capital 1,973 1,687 1,511 2,273 2,574 2,994

Net Cash/(Debt) 6,733 10,366 12,502 12,507 12,705 13,038

Debtors Turn (avg days) 44.4 46.8 48.6 48.3 48.6 48.1

Creditors Turn (avg days) 37.8 48.0 53.5 49.8 47.4 46.9

Inventory Turn (avg days) 70.4 61.9 58.2 58.9 61.1 60.1

Asset Turnover (x) 0.8 0.8 0.8 0.7 0.8 0.8

Current Ratio (x) 7.0 6.0 6.1 6.7 6.4 6.0

Quick Ratio (x) 6.0 5.3 5.5 5.9 5.5 5.2

Net Debt/Equity (X) CASH CASH CASH CASH CASH CASH

Net Debt/Equity ex MI (X) CASH CASH CASH CASH CASH CASH

Capex to Debt (%) 390.1 886.6 2,161.0 2,155.2 2,694.1 2,694.1

Z-Score (X) 22.7 14.3 16.8 15.8 14.7 NA

Source: Company, DBS Vickers, AllianceDBS

Asset Breakdown (2014)

Net Fixed Assets -37.7%

Assocs'/JVs -0.0%

Bank, Cash and Liquid

Assets -45.6%

Inventory -6.5%

Debtors -10.2%

Strong balance sheet

Page 26

Company Focus

Indocement Tunggal Prakarsa

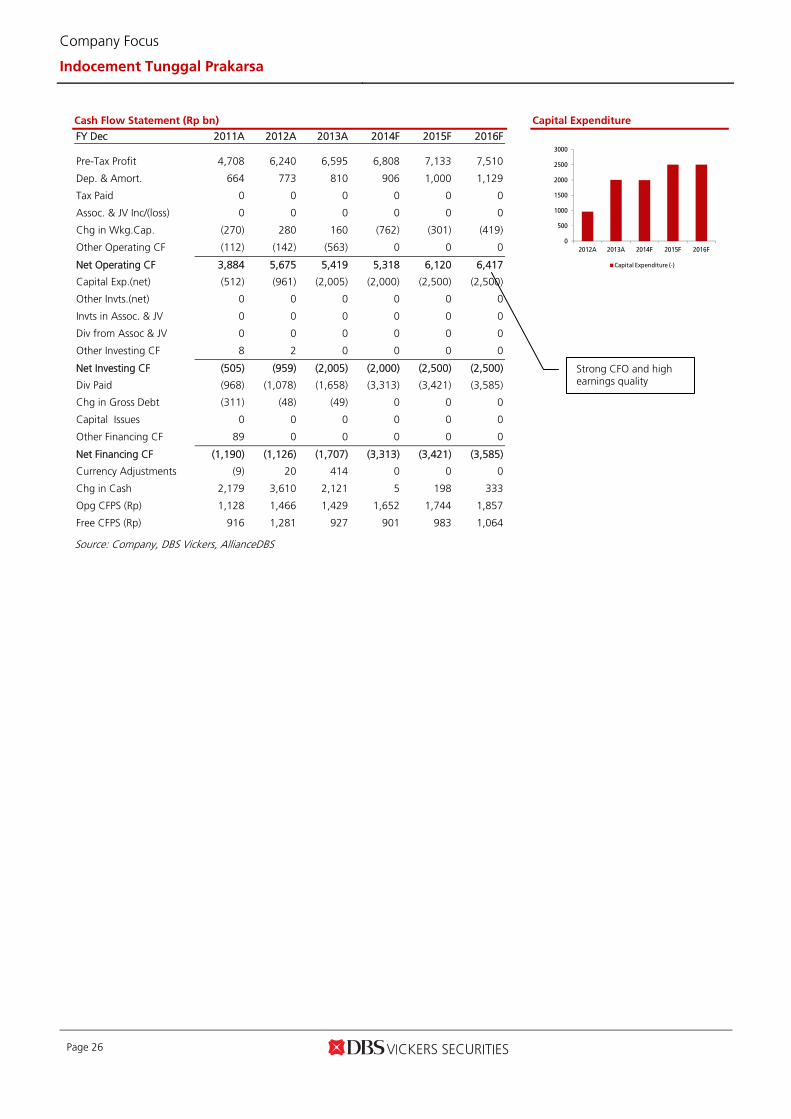

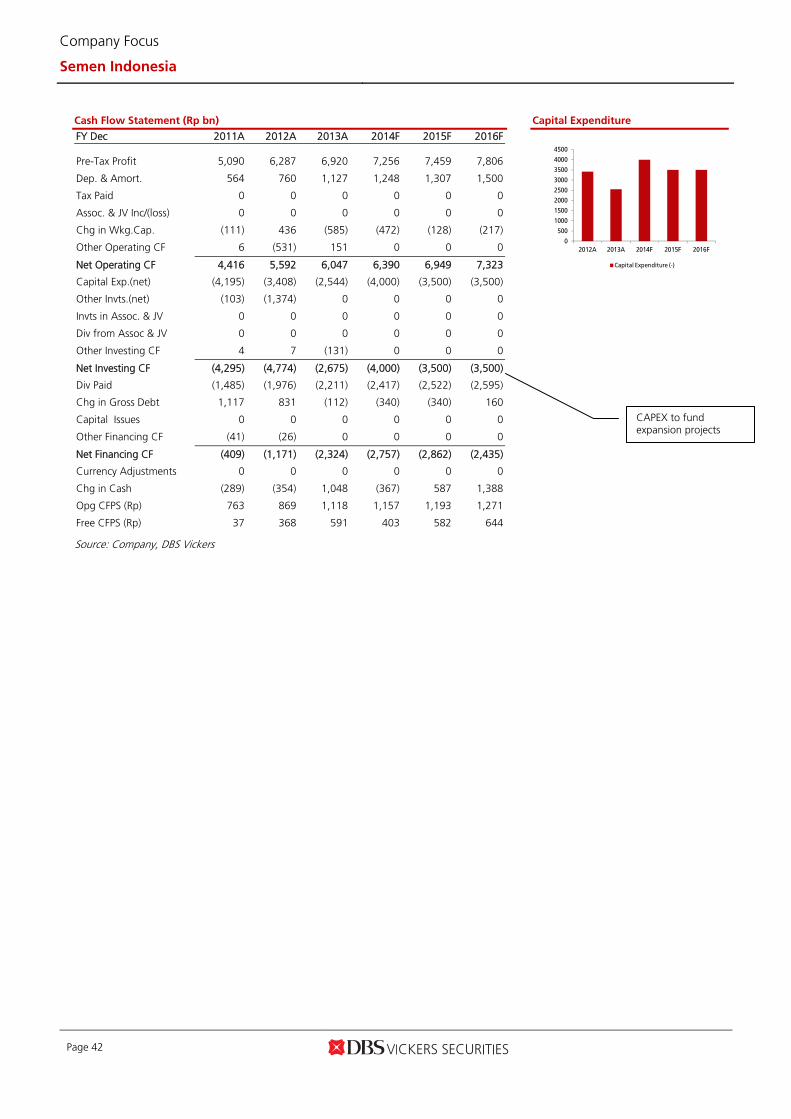

Cash Flow Statement (Rp bn)

FY Dec 2011A 2012A 2013A 2014F 2015F 2016F Pre-Tax Profit 4,708 6,240 6,595 6,808 7,133 7,510

Dep. & Amort. 664 773 810 906 1,000 1,129

Tax Paid 0 0 0 0 0 0

Assoc. & JV Inc/(loss) 0 0 0 0 0 0

Chg in Wkg.Cap. (270) 280 160 (762) (301) (419)

Other Operating CF (112) (142) (563) 0 0 0

Net Operating CF 3,884 5,675 5,419 5,318 6,120 6,417

Capital Exp.(net) (512) (961) (2,005) (2,000) (2,500) (2,500)

Other Invts.(net) 0 0 0 0 0 0

Invts in Assoc. & JV 0 0 0 0 0 0

Div from Assoc & JV 0 0 0 0 0 0

Other Investing CF 8 2 0 0 0 0

Net Investing CF (505) (959) (2,005) (2,000) (2,500) (2,500)

Div Paid (968) (1,078) (1,658) (3,313) (3,421) (3,585)

Chg in Gross Debt (311) (48) (49) 0 0 0

Capital Issues 0 0 0 0 0 0

Other Financing CF 89 0 0 0 0 0

Net Financing CF (1,190) (1,126) (1,707) (3,313) (3,421) (3,585)

Currency Adjustments (9) 20 414 0 0 0

Chg in Cash 2,179 3,610 2,121 5 198 333

Opg CFPS (Rp) 1,128 1,466 1,429 1,652 1,744 1,857

Free CFPS (Rp) 916 1,281 927 901 983 1,064

Source: Company, DBS Vickers, AllianceDBS

Capital Expenditure

0

500

1000

1500

2000

2500

3000

2012A 2013A 2014F 2015F 2016F

Capital Expenditure (-)

Strong CFO and high earnings quality

Page 27

Company Focus

Indocement Tunggal Prakarsa

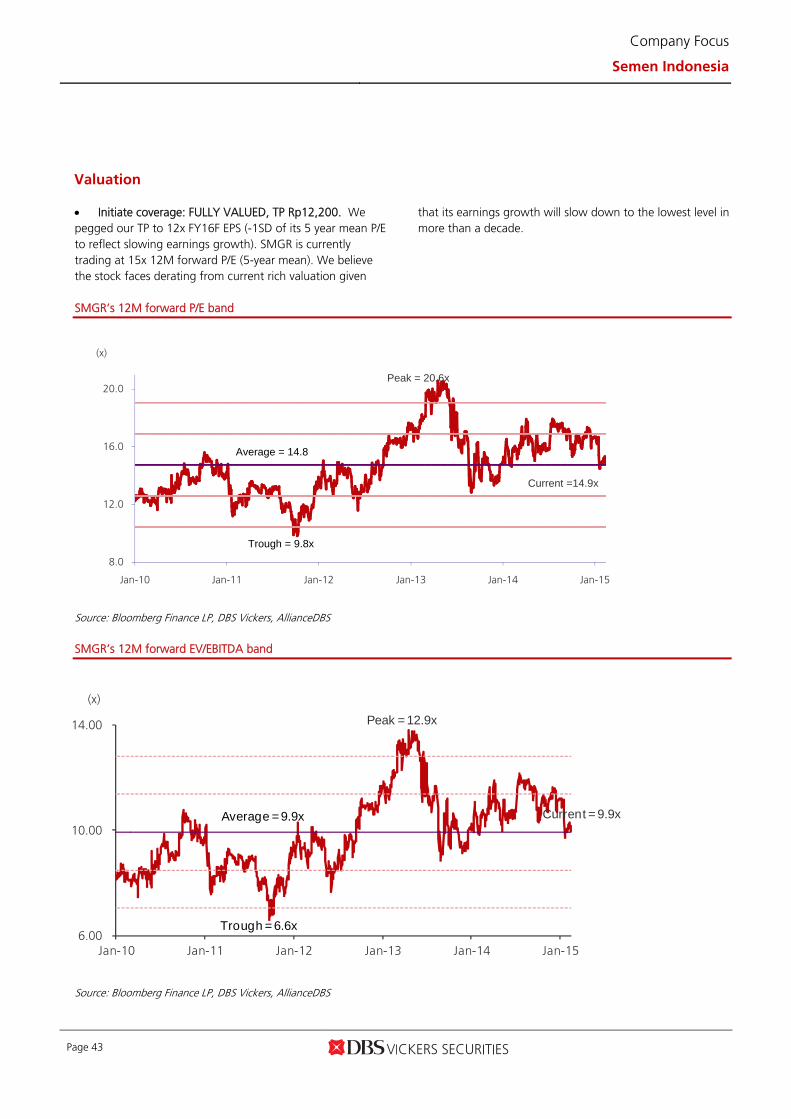

Valuation Initiate coverage: FULLY VALUED, TP Rp20,200. We peg our TP to 13x FY16 EPS (slightly more than 1 sd below its 5 year mean P/E to reflect the slowing earnings growth). INTP is currently trading at c.16x (5 year mean) 12M forward

P/E. We believe the stock faces derating from the current rich valuation as its earnings growth slow to c.5% CAGR (FY14-17) from c.16% (FY09-13).

INTP’s 12M forward P/E band

Source: Bloomberg Finance LP, DBS Vickers, AllianceDBS INTP’s 12M forward EV/EBITDA band

Source: Bloomberg Finance LP, DBS Vickers, AllianceDBS

8.0

12.0

16.0

20.0

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

(x)Peak = 20.3x

Trough = 9.2x

Current = 15.9x

Mean = 15.4x

5.0

8.0

11.0

14.0

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

(x)

Peak = 13.2x

Mean = 10x

Trough = 5.7x

Current = 10.4x

www.dbsvickers.com ed: SGC / sa: MA

FULLY VALUED Rp14,675 JCI : 5,325.50 (Initiating Coverage) Price Target : 12-Month Rp 12,200 Reason for Report : Initiating coverage Potential Catalyst: Strong property sales, lower coal and oil price Analyst Deidy WIJAYA +6221 3003 4931 [email protected]

CHONG Tjen San, CFA +603 2604 3972 [email protected]

Price Relative

Forecasts and Valuation FY Dec (Rp bn) 2013A 2014F 2015F 2016F Revenue 24,501 27,132 29,035 31,910 EBITDA 8,099 8,451 8,704 9,197 Pre-tax Profit 6,920 7,256 7,459 7,806 Net Profit 5,370 5,604 5,766 6,040 Net Pft (Pre Ex.) 5,370 5,604 5,766 6,040 EPS (Rp) 905 945 972 1,018 EPS Pre Ex. (Rp) 905 945 972 1,018 EPS Gth (%) 11 4 3 5 EPS Gth Pre Ex (%) 11 4 3 5 Diluted EPS (Rp) 905 945 972 1,018 Net DPS (Rp) 407 425 437 458 BV Per Share (Rp) 3,521 4,058 4,605 5,186 PE (X) 16.2 15.5 15.1 14.4 PE Pre Ex. (X) 16.2 15.5 15.1 14.4 P/Cash Flow (X) 14.4 13.6 12.5 11.9 EV/EBITDA (X) 10.8 10.3 9.9 9.3 Net Div Yield (%) 2.8 2.9 3.0 3.1 P/Book Value (X) 4.2 3.6 3.2 2.8 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 28.1 24.9 22.4 20.8 Earnings Rev (%): - - - Consensus EPS (Rp): 956 1,032 1,183 No. of brokers following: B: 20 S: 8 H: 6 ICB Industry : Industrials ICB Sector: Construction & Materials Principal Business: Semen Gresik (SMGR IJ) : SMGR was established in 1957. In 1995 the company completed an acquisition of Semen Padang and Semen Tonasa. It is currently the largest player in the market with 40.7% market share.

Source of all data: Company, DBS Vickers, Bloomberg Finance L.P

At A Glance Issued Capital (m shrs) 5,932 Mkt. Cap (Rpbn/US$m) 87,045 / 6,823 Major Shareholders Govt. of Indonesia (%) 60.0 Free Float (%) 40.0 Avg. Daily Vol.(‘000) 8,405

DBS Group Research . Equity 17 Feb 2015

Indonesia Company Focus

Semen Indonesia Bloomberg: SMGR IJ | Reuters: SMGR.JK Refer to important disclosures at the end of this report

Market lead under pressure Pole position under pressure

Further margin degradation as pricing power erodes

Expensive at 15x/14x FY15/16F EPS given pedestrian growth

Initiate coverage: FULLY VALUED, TP Rp12,200 (pegged to 12x FY16F EPS)

Market lead will be eroded. Semen Indonesia (SMGR) currently leads with 44% share of cement sales in Indonesia. But this will be eroded gradually after the anticipated new capacities come on stream in 2016. We estimate its market share would shrink to 41% by 2017, partly mitigated by its strong and established brand equity. SMGR sells cement under three brands, “Semen Gresik”, “Semen Padang” and “Semen Tonasa” which have strong brand equities in Java, Sumatra and Sulawesi, respectively. Also, the different price points for each brand allow the company to tap different market segments to maximise its market share. Hurt least by rising competition, but not spared. SMGR sells 52% of its output to Java vs 72% for Indocement and 71% for Holcim. It also has >30% market share on the major islands in Indonesia. Hence, it should be less affected by incoming competition which will be mainly in Java. However, its margins will not be spared; we anticipate they will drop to 30% by this year from 33.1% and 31.1% in FY13-14F. This also takes into account the 4-5% mandated price cuts by Jokowi for bag cement, which effectively offset potential savings arising from lower electricity and diesel costs.

High valuation unwarranted given slowing growth.

SMGR is currently trading 15x 12M forward P/E (5 year mean), despite much slower earnings growth of c.5% CAGR over FY14-17 vs. 13.9% over FY09-13. The stock is likely to be derated as earnings growth will be at its slowest since 2004.

81

101

121

141

161

181

201

221

6,930.0

8,930.0

10,930.0

12,930.0

14,930.0

16,930.0

18,930.0

Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

Relative IndexRp

Semen Gresik (LHS) Relative JCI INDEX (RHS)

Page 29

Company Focus

Semen Indonesia

INVESTMENT THESIS

Profile Rationale

Semen Indonesia (SMGR) is the largest cement player in Indonesia with >40% market share. It has production facilities on three key islands (Java, Sumatra and Sulawesi) and solid distribution channels, which enables it to command high market shares throughout Indonesia. SMGR sells cement under three brands, “Semen Gresik”, “Semen Padang” and “Semen Tonasa” which have strong brand equities in Java, Sumatra and Sulawesi, respectively.

Cement industry is facing an unprecedented structural shift We estimate new supply to be more than double of new

demand, bringing utilisation down from 89% to 74% by 2017.

Margin projected to keep sliding due to weakening pricing power and increasing contribution from bulk cement 3 major players are entering Indonesia – Semen Merah

Putih (Wilmar Group), Anhui Conch and Siam Cement. Anhui Conch and Siam Cement are market leaders in China and Thailand respectively. With their Indonesia plants contributing only c.3% to their total capacities, there could be price war once their plants come on stream as they try to gain market share.

The fast growing segment in Indonesia is the bulk segment (contribution estimated to rise from 22% to 27% by FY17), which is used for infrastructure projects and high rise buildings. With less barriers to entry (brand equity and distribution channels), this segment (which already commands lower margins) will be the likely target for the new entrants.

Benefits from low energy prices offset by lower ASP After Jokowi recently instructed SOE cement companies

to reduce bag cement price by Rp3,000/bag (cut by 4-5%), the positive impact from lower energy prices are wiped out. We also fear Jokowi would continue to control SMGR’s and SMBR’s cement prices, and erase prospects of higher margins as a result of lower costs.

Rich valuations unwarranted given slower growth and declining ROE SMGR is currently trading at 15x 12M forward P/E (5 year

mean) despite the slowest earnings growth expected in a decade.

Valuation Risks

Our target price of Rp12,200 is pegged to 12x FY16 EPS (-1 sd of 5 year mean). Initiate with FULLY VALUED call as there is more than 10% downside from the current price

Weak demand due to slow rollout of infrastructure projects If the new government fails in speeding up infrastructure

developments, cement demand growth could disappoint and hurt SMGR’s utilisation rates and profitability.

Timely completion of facilities SMGR plans to increase capacity by c.25% over the next

three years. Delays could cause SMGR to lose market share.

Expansion outside Indonesia facing some risks We believe that SMGR faces some country and political

risks as it expands into Vietnam and Myanmar. Also, the expansion will reduce SMGR’s profitability as ASPs are much lower in these countries.

Source: DBS Vickers, AllianceDBS

Page 30

Company Focus

Semen Indonesia

SWOT Analysis

Strengths Weakness

Largest market share in the industry. SMGR had 44% market share in FY14. It has production facilities on three key islands (Java, Sumatra and Sulawesi) and solid distribution channels, which enables it to command high market shares throughout Indonesia.

Expansion beyond Indonesia may pressure margins as ASPs in other countries are much lower than in Indonesia. Higher transportation costs than INTP and SMCB as its distribution covers a wider area.

Opportunities Threats

Large growth opportunities outside Java. Eastern Indonesia is growing rapidly due to the low base. SMGR will be the main beneficiary when that market starts to generate meaningful contribution as it is already building brand equity and distribution networks in those regions.

Entry of new players such as Anhui Conch, Siam Cement, Semen Merah Putih could disrupt the oligopoly structure of Indonesia’s cement sector. Potential price war if the competitors decide to fight for market share. Government intervention to lower prices, as demonstrated recently for bag cement.

Source: DBS Vickers, AllianceDBS

Page 31

Company Focus

Semen Indonesia

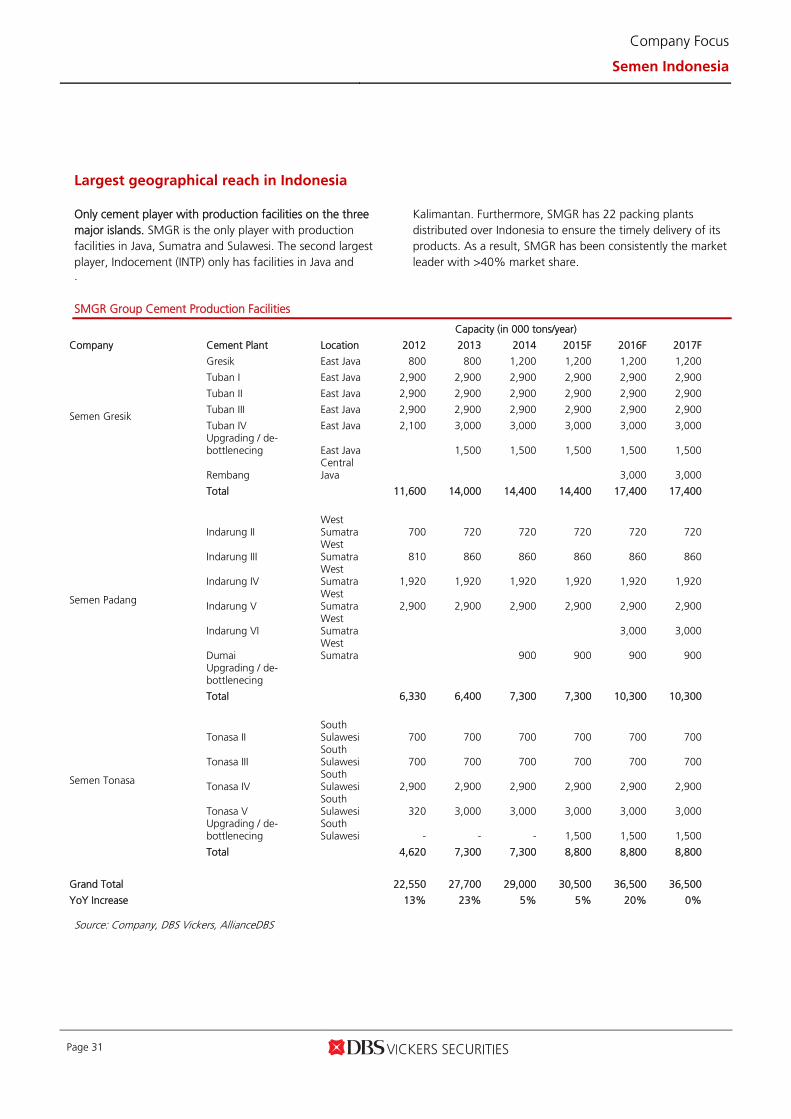

Largest geographical reach in Indonesia Only cement player with production facilities on the three major islands. SMGR is the only player with production facilities in Java, Sumatra and Sulawesi. The second largest player, Indocement (INTP) only has facilities in Java and

Kalimantan. Furthermore, SMGR has 22 packing plants distributed over Indonesia to ensure the timely delivery of its products. As a result, SMGR has been consistently the market leader with >40% market share.

. SMGR Group Cement Production Facilities

Capacity (in 000 tons/year)

Company Cement Plant Location 2012 2013 2014 2015F 2016F 2017F

Semen Gresik

Gresik East Java 800 800 1,200 1,200 1,200 1,200

Tuban I East Java 2,900 2,900 2,900 2,900 2,900 2,900

Tuban II East Java 2,900 2,900 2,900 2,900 2,900 2,900

Tuban III East Java 2,900 2,900 2,900 2,900 2,900 2,900

Tuban IV East Java 2,100 3,000 3,000 3,000 3,000 3,000 Upgrading / de-bottlenecing East Java 1,500 1,500 1,500 1,500 1,500

Rembang Central Java 3,000 3,000

Total 11,600 14,000 14,400 14,400 17,400 17,400

Semen Padang

Indarung II West Sumatra 700 720 720 720 720 720

Indarung III West Sumatra 810 860 860 860 860 860

Indarung IV West Sumatra 1,920 1,920 1,920 1,920 1,920 1,920

Indarung V West Sumatra 2,900 2,900 2,900 2,900 2,900 2,900

Indarung VI West Sumatra 3,000 3,000

Dumai West Sumatra 900 900 900 900

Upgrading / de-bottlenecing

Total 6,330 6,400 7,300 7,300 10,300 10,300

Semen Tonasa

Tonasa II South Sulawesi 700 700 700 700 700 700

Tonasa III South Sulawesi 700 700 700 700 700 700

Tonasa IV South Sulawesi 2,900 2,900 2,900 2,900 2,900 2,900

Tonasa V South Sulawesi 320 3,000 3,000 3,000 3,000 3,000

Upgrading / de-bottlenecing

South Sulawesi - - - 1,500 1,500 1,500

Total 4,620 7,300 7,300 8,800 8,800 8,800

Grand Total 22,550 27,700 29,000 30,500 36,500 36,500

YoY Increase 13% 23% 5% 5% 20% 0% Source: Company, DBS Vickers, AllianceDBS

Page 32

Company Focus

Semen Indonesia

SMGR Group Sales Volume and Market Share

Source: Company, DBS Vickers, AllianceDBS Multi-brand strategy to maximise market share. Unlike INTP and SMCB which sell under one brand name, SMGR sells its products under three different brands. The main reason for this is that all three brands have strong brand equities in their respective regions before SMGR acquired Semen Padang and Semen Tonasa. Each brand has a different geographical focus: Semen Gresik on Java and Kalimantan, Semen Padang

on Sumatra, Jakarta and West Java, and Semen Tonasa on Sulawesi, Kalimantan and East Indonesia. Furthermore, because of their different price points, SMGR is able to maximise market share by capturing customers from different market segments. Semen Gresik is the group’s premium brand, while Semen Padang and Semen Tonasa are priced c.5% cheaper.

Primary Markets for SG, SP and ST Company Plant Location Primary Markets

Semen Gresik East Java Java, Kalimantan Semen Padang West Sumatra Sumatra, Jakarta, West Java Semen Tonasa South Sulawesi Sulawesi, Kalimantan, Eastern

Indonesia Source: Company, DBS Vickers, AllianceDBS

38%

39%

40%

41%

42%

43%

44%

45%

46%

47%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Semen Gresik Semen Padang Semen Tonasa SMGR's market share (RHS)

Page 33

Company Focus

Semen Indonesia

Less dependent on Java than Indocement and Holcim

Java only contributes c.50% of SMGR’s sales volume. This is much smaller than for Indocement (72%) and Holcim (71%). Therefore, SMGR should be affected less by the incoming new supply and competition from new players, which will be

concentrated in Java. By island, SMGR is also the market leader (by sales volume) on all the major islands (Java, Sumatra, Sulawesi, Kalimantan).

Sales volume by region

Source: ASI, DBS Vickers, AllianceDBS

FY14 Market Share of Cement Companies By Region

Region SMGR INTP SMCB Bosowa Andalas Baturaja Kupang

Java 40.4% 38.8% 18.3% 2.3% 0.0% 0.0% 0.0%

Sumatra 42.9% 14.1% 14.7% 3.2% 15.0% 10.1% 0.0%

Kalimantan 50.2% 29.6% 11.1% 9.1% 0.0% 0.0% 0.0%

Sulawesi 63.1% 13.3% 0.9% 22.7% 0.0% 0.0% 0.0%

Others 43.8% 29.9% 4.1% 18.5% 0.0% 0.0% 3.7%

Total Indonesia 43.7% 30.4% 14.6% 5.8% 3.1% 2.1% 0.3% Source: ASI, DBS Vickers, AllianceDBS

52.1%

72.0% 70.7%56.3%

20.5%

9.7%20.9%

20.9%

8.7%

7.4%

5.8%

7.6%10.9%

3.3%0.4%

7.6%

7.7% 7.6% 2.2% 7.6%

SMGR INTP SMCB National

Java Sumatra Kalimantan Sulawesi Others

Page 34

Company Focus

Semen Indonesia

Company Background Corporate History. Semen Indonesia (formerly known as Semen Gresik) started in 1957 as a state-owned company with an installed capacity of 250,000 tons. The government completed the IPO over 20 years ago by releasing 27% of its

shares to the public. In 1995, Semen Indonesia increased its capacity significantly by acquiring PT Semen Padang and PT Semen Tonasa. In 1998, the public float increased as the government pared down its stake to 51%.

Sales Trend Profitability Trend

Source: Company, DBS Vickers, AllianceDBS Capacity. Semen Indonesia (SMGR) is currently the largest cement producer in Indonesia with 29m tons/year installed capacity (40% of national installed capacity). It has integrated facilities in East Java, West Sumatra and South Sulawesi, and is building a new facility in Central Java.

East Java is the largest contributor. The company’s largest single largest contributor is East Java. More than 20% of the group’s output is sold to East Java, where it has >70% market share.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

2012A 2013A 2014F 2015F 2016F

Rp bn

Total Revenue Revenue Growth (%) (YoY)

4,847

5,347

5,847

6,347

6,847

7,347

2012A 2013A 2014F 2015F 2016F

Rp bn

Operating EBIT Pre tax Profit Net Profit

Page 35

Company Focus

Semen Indonesia

Key Management Team

Suparni President Director Suparni was born on December 13, 1958. He was appointed as a Director of the Company at the 2015 EGM. He was previously the Director of Production and R & D. Current tenure as Director will expire in 2017. He joined the Company in 1986. He was previously the Head Compartment Tuban (2007), Head of Corporate Development Department (2006-2007), and Head of Production II Tuban (2002-2006). He has a Bachelor’s degree in Electrical Engineering from ITS Surabaya.

Ahyanizzaman Director Ahyanizzaman was born on July 6, 1966. He was appointed as Director of

Finance at the EGM on 11 March 2011; the term will end in 2016. He previously served as Head of the Finance Division (2006-2010), Head of Finance and Accounting (2010-2011), Head of Financial Accounting (2006-2007), Head of Accounting (2004-2006), and Acting Head of Accounting (2002). He joined the Company in 1991. He has a Bachelor degree in accounting from Airlangga University, Surabaya.

Amat Pria Darma Director Amat Men Darma was born on August 13, 1961. He was appointed as a

member of the Board of Directors in 2012 and his current term will expire in 2017. Previously, he served as Head of Distribution and Transportation Department. He started his career in PT Semen Gresik (Persero) Tbk in 1986. He graduated with Bachelor of Chemical Engineering degree from Institut Teknologi Sepuluh Nopember in 1985.

Gatot Kustyadji Director Gatot Kustyadji was born on July 25, 1963. He was appointed as a member

of the Board of Directors at the 2014 AGM; the current term expires in 2019. Previously, he served as Director of Research and Development at PT Semen Tonasa (2005-2010), Director of Research and Development and Operations at PT Semen Tonasa (2011-2012), Production Director at PT Semen Tonasa (2012-2014), and Director at PT. Semen Gresik. He has a Chemical Engineering degree from Institut Teknologi Sepuluh Nopember and a Bachelor’s degree in Management from University of Indonesia. He has a Master degree in Economic Planning and Development from University of Andalas. He received his Doctorate degree in the field of human resources from Universitas Brawijaya.

Johan Samudra Director Johan Samudra was born on June 22, 1956. He was appointed as a

member of the Board of Directors at the 2014 AGM; the current term expires in 2019. Previously, he served as CEO of Thang Long Cement Vietnam, Director of Research and Development at PT Semen Padang (2003-2005), and as GM Capex Management Group at PT Semen Gresik. He has a Master’s degree in Financial Management from Andalas University.

Rizkan Chandra Director Rizkan Chandra was born in Jakarta on January 27, 1969. He was

appointed as a member of the Board of Directors at the EGM in 2015. Previously, he served as Director of Network, IT & Solution PT Telekomunikasi Indonesia (Persero) Tbk, Commissioner of PT Telkomsel and Director of PT Sigma Cipta Caraka. He has a Bachelor’s degree in Computer Science from Institut Teknologi Bandung (ITB) and a MSc in Management of Technology from National University of Singapore.

Source: Company, DBS Vickers, AllianceDBS

Page 36

Company Focus

Semen Indonesia

Key Business Risks Weak demand growth due to slow rollout of infrastructure projects. If the new government does not live up to expectation in speeding up infrastructure developments, cement demand growth could disappoint and hurt SMGR’s utilisation rates and profitability. Timely completion of facilities. SMGR plans to increase capacity by c.25% over the next three years. Delays could cause SMGR to lose market share.

Expansion outside Indonesia facing some risks. SMGR has decided to expand beyond Indonesia by acquiring Thang Long (a Vietnam-based cement producer) at the end of 2012 The management also indicated that they are looking at countries such as Myanmar and Bangladesh for future acquisitions. However, we believe that SMGR faces some political risks in these countries. Also, the expansion will reduce SMGR’s profitability as ASPs are much lower in these countries.

Upside Risks to Our Call

Strong rebound in property sales. We expect domestic property sales volume to register flattish growth for this year as there are plenty of headwinds in the near term – upward trend in BI rate, regulations and liquidity tightening risk as well as cost pressure from fuel subsidy removal. If property sales actually rebound strongly this year, there would be upside risk to our cement sales volume assumption as property is the biggest contributor to cement consumption. Further drop in oil and coal price. If coal and oil price continues their downtrend, SMGR would benefit in the short term. Roughly 40% of its cash cost are linked to coal and oil

price. Should coal and oil continue their downtrend, there would be upside to our margin and earnings assumptions for this year. Significant delay in new players’ Greenfield projects. If the new players’ Greenfield projects are delayed or cancelled, our incremental supply assumption would be overstated and cement utilization rate would be understated. Competition could be less severe than our assumption and thus pricing power would be higher than we predicted.

Page 37

Company Focus