Embed Size (px)

Citation preview

Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

Inserting the Consumer into the Trade Promotion Process

Steve Baumberger & Jim Coleman2004 FMI Conference

2Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

Today’s Discussion• The Situation: The “Daunting Dilemma” of Trade Promotion

– Promotions don’t pay and we can’t figure out what to do

• The High Performance Shopper: Inserting the Consumer into Trade Promotion– Consumers actually create the demand we are trying to

generate

• The Road Ahead: Charting a course for Growth and Profits– Winning retailers and manufacturers will together find a way to

maximize return on investment

3Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

• More Diversity• More Time Challenged• More Stores• More Products

– Sizes, Flavors, Brands, Private Label• More Media & Marketing Noise• More Promotion Dollars• More Regulation and Scrutiny

Consumer packaged goods companies have been facing a number of growth challenges.

Economic Environment and Trends

The Situation: A Daunting Dilemma

4Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

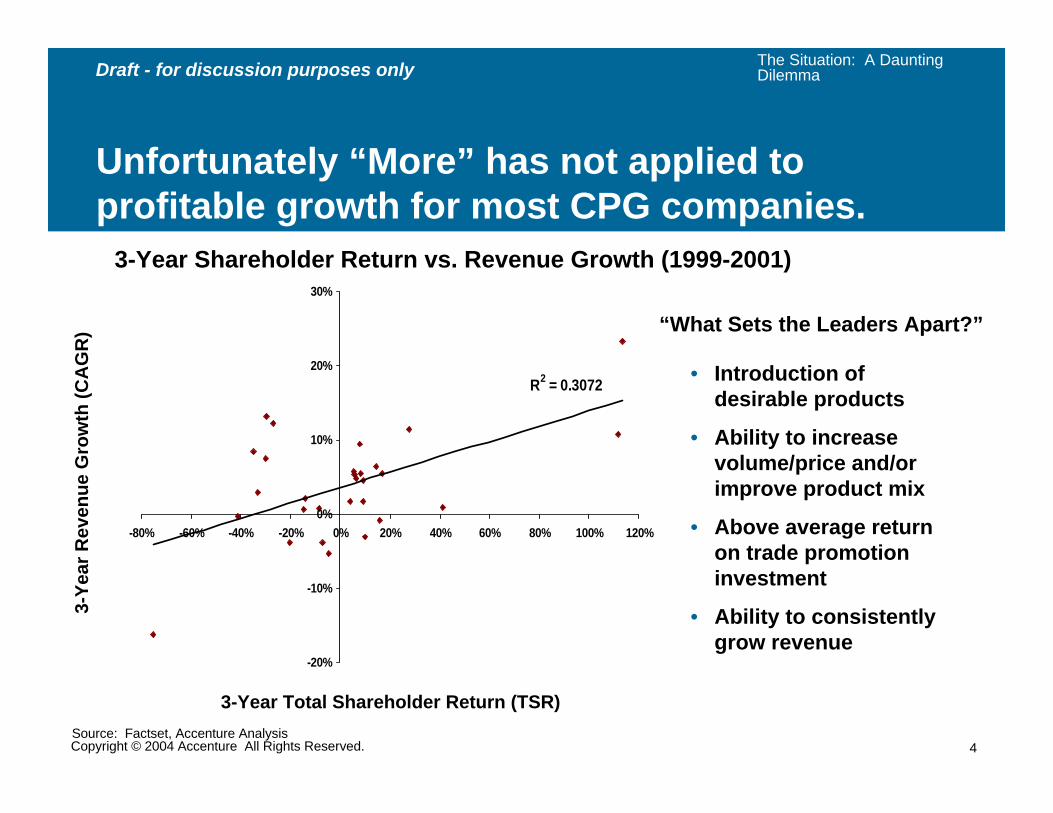

Unfortunately “More” has not applied to profitable growth for most CPG companies.

R2 = 0.3072

-20%

-10%

0%

10%

20%

30%

-80% -60% -40% -20% 0% 20% 40% 60% 80% 100% 120%

3-Year Total Shareholder Return (TSR)

3-Ye

ar R

even

ue G

row

th (C

AG

R)

Source: Factset, Accenture Analysis

• Introduction of desirable products

• Ability to increase volume/price and/or improve product mix

• Above average return on trade promotion investment

• Ability to consistently grow revenue

“What Sets the Leaders Apart?”

3-Year Shareholder Return vs. Revenue Growth (1999-2001)

The Situation: A Daunting Dilemma

5Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

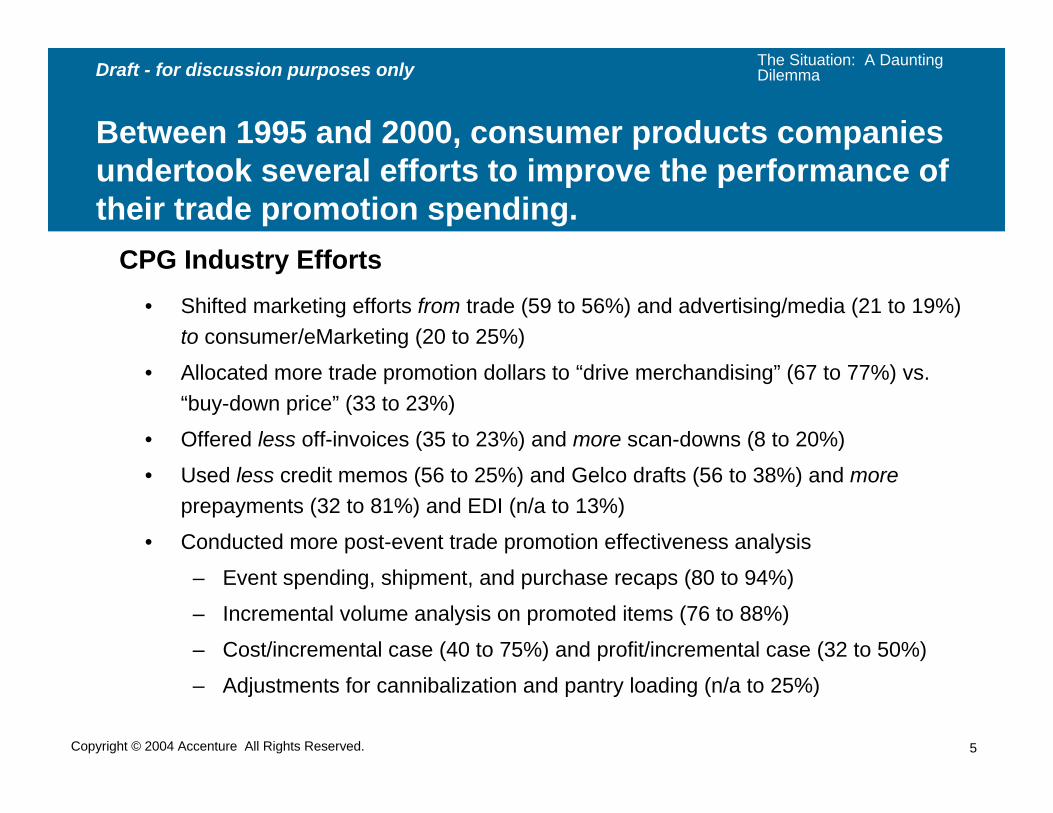

Between 1995 and 2000, consumer products companies undertook several efforts to improve the performance of their trade promotion spending.

• Shifted marketing efforts from trade (59 to 56%) and advertising/media (21 to 19%) to consumer/eMarketing (20 to 25%)

• Allocated more trade promotion dollars to “drive merchandising” (67 to 77%) vs. “buy-down price” (33 to 23%)

• Offered less off-invoices (35 to 23%) and more scan-downs (8 to 20%)

• Used less credit memos (56 to 25%) and Gelco drafts (56 to 38%) and moreprepayments (32 to 81%) and EDI (n/a to 13%)

• Conducted more post-event trade promotion effectiveness analysis

– Event spending, shipment, and purchase recaps (80 to 94%)

– Incremental volume analysis on promoted items (76 to 88%)

– Cost/incremental case (40 to 75%) and profit/incremental case (32 to 50%)

– Adjustments for cannibalization and pantry loading (n/a to 25%)

CPG Industry Efforts

The Situation: A Daunting Dilemma

6Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

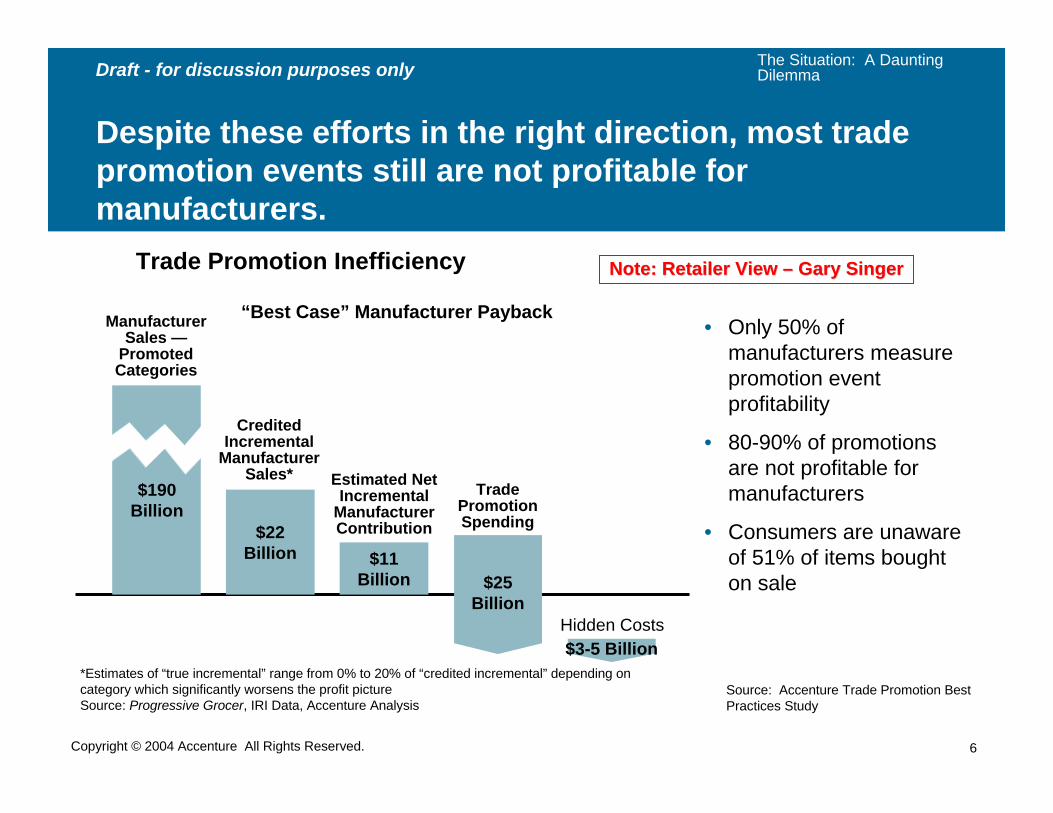

Despite these efforts in the right direction, most trade promotion events still are not profitable for manufacturers.

“Best Case” Manufacturer Payback• Only 50% of

manufacturers measure promotion event profitability

• 80-90% of promotions are not profitable for manufacturers

• Consumers are unaware of 51% of items bought on sale

$22 Billion $11

Billion $25 Billion

$3-5 BillionHidden Costs

Trade Promotion Spending

Estimated Net Incremental

Manufacturer Contribution

Credited Incremental

Manufacturer Sales*

$190Billion

Manufacturer Sales —

Promoted Categories

*Estimates of “true incremental” range from 0% to 20% of “credited incremental” depending on category which significantly worsens the profit pictureSource: Progressive Grocer, IRI Data, Accenture Analysis

Source: Accenture Trade Promotion Best Practices Study

Trade Promotion Inefficiency Note: Retailer View Note: Retailer View –– Gary SingerGary Singer

The Situation: A Daunting Dilemma

7Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

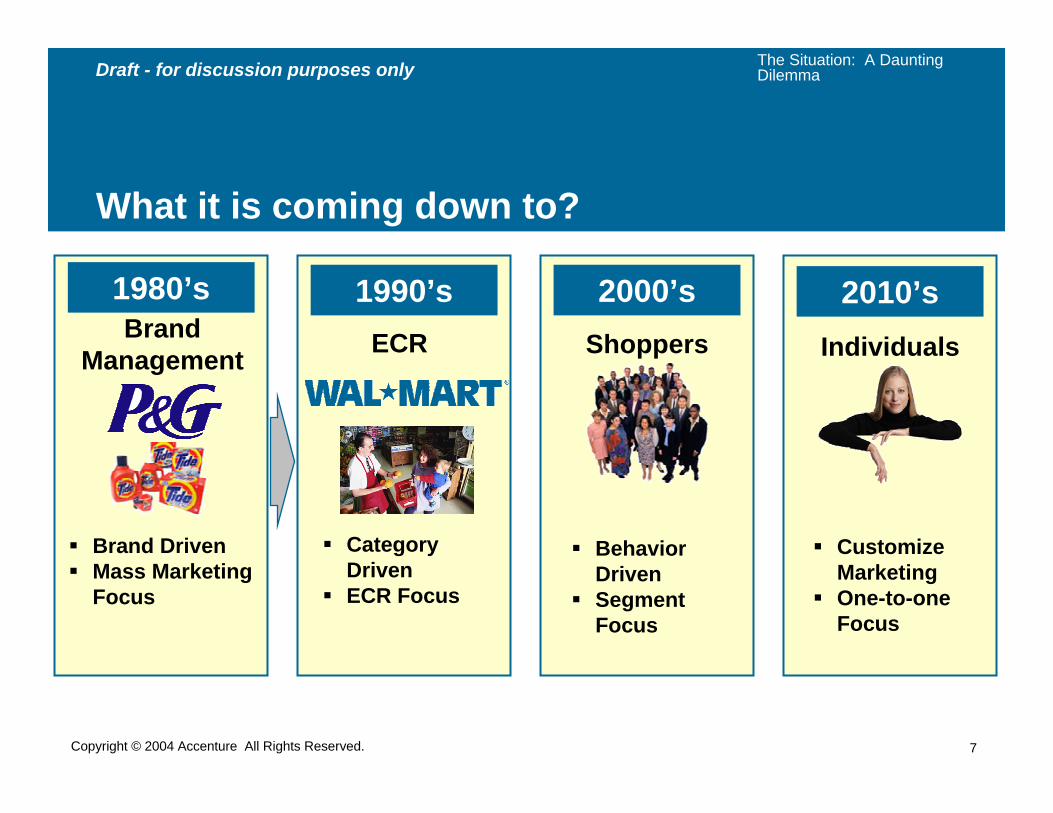

What it is coming down to?

1980’s

Brand DrivenMass Marketing Focus

1990’s

Category Driven ECR Focus

2000’sShoppers

Behavior DrivenSegment Focus

Individuals

2010’s

Customize Marketing One-to-one Focus

ECRBrand Management

The Situation: A Daunting Dilemma

8Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

CPG Manufacturer and Retailer Challenge

How do we increase the lifetime value and loyalty of our highest potential

consumers?

The Situation: A Daunting Dilemma

9Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

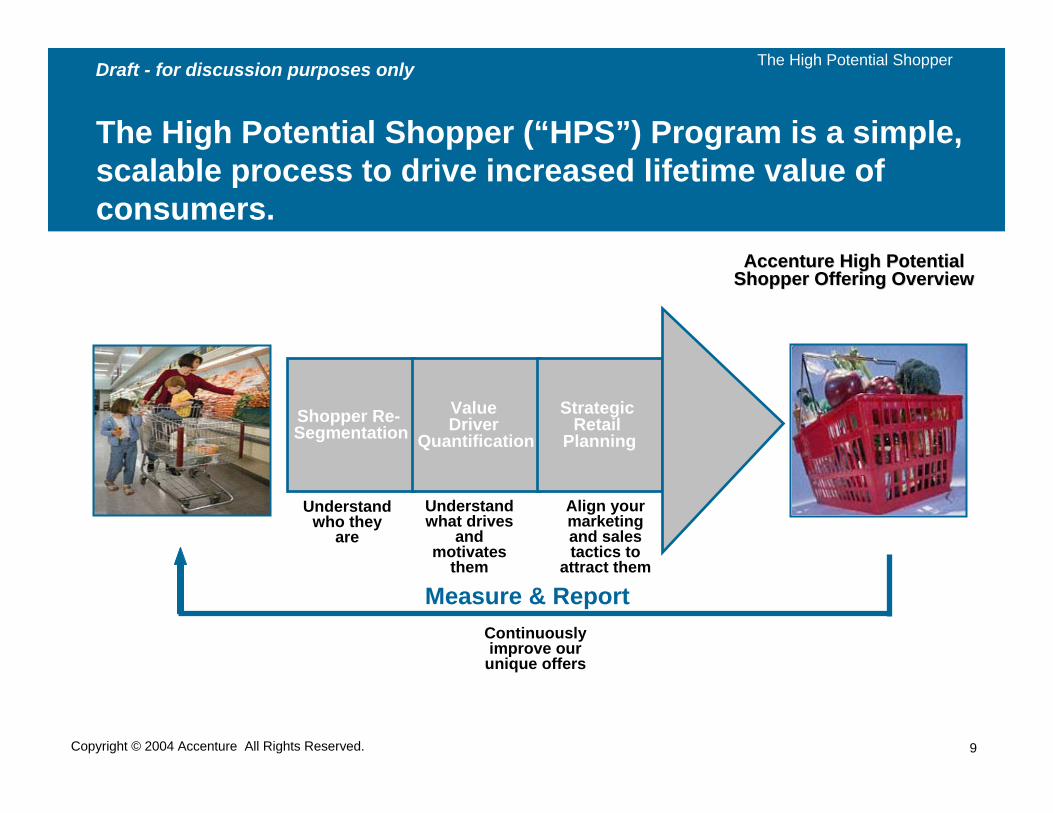

The High Potential Shopper (“HPS”) Program is a simple, scalable process to drive increased lifetime value of consumers.

Shopper Re-Segmentation

Value Driver

Quantification

Strategic Retail

Planning

Measure & Report

Understand who they

are

Understand what drives

and motivates

them

Align your marketing and sales tactics to

attract them

Continuously improve our

unique offers

Accenture High Potential Accenture High Potential Shopper Offering OverviewShopper Offering Overview

The High Potential Shopper

10Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

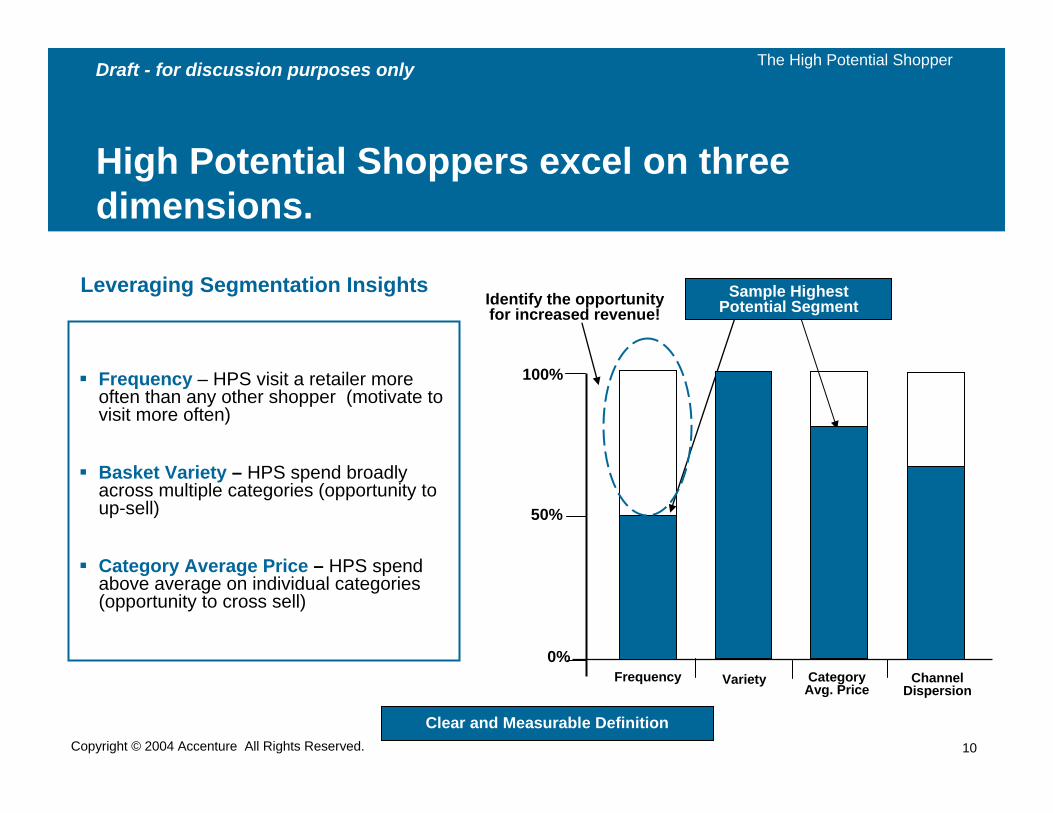

High Potential Shoppers excel on three dimensions.

Frequency – HPS visit a retailer more often than any other shopper (motivate to visit more often)

Basket Variety – HPS spend broadly across multiple categories (opportunity to up-sell)

Category Average Price – HPS spend above average on individual categories (opportunity to cross sell)

Clear and Measurable Definition

Leveraging Segmentation Insights

100%

50%

0%Frequency Variety Category

Avg. PriceChannel

Dispersion

Identify the opportunity for increased revenue!

Sample HighestPotential Segment

The High Potential Shopper

11Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

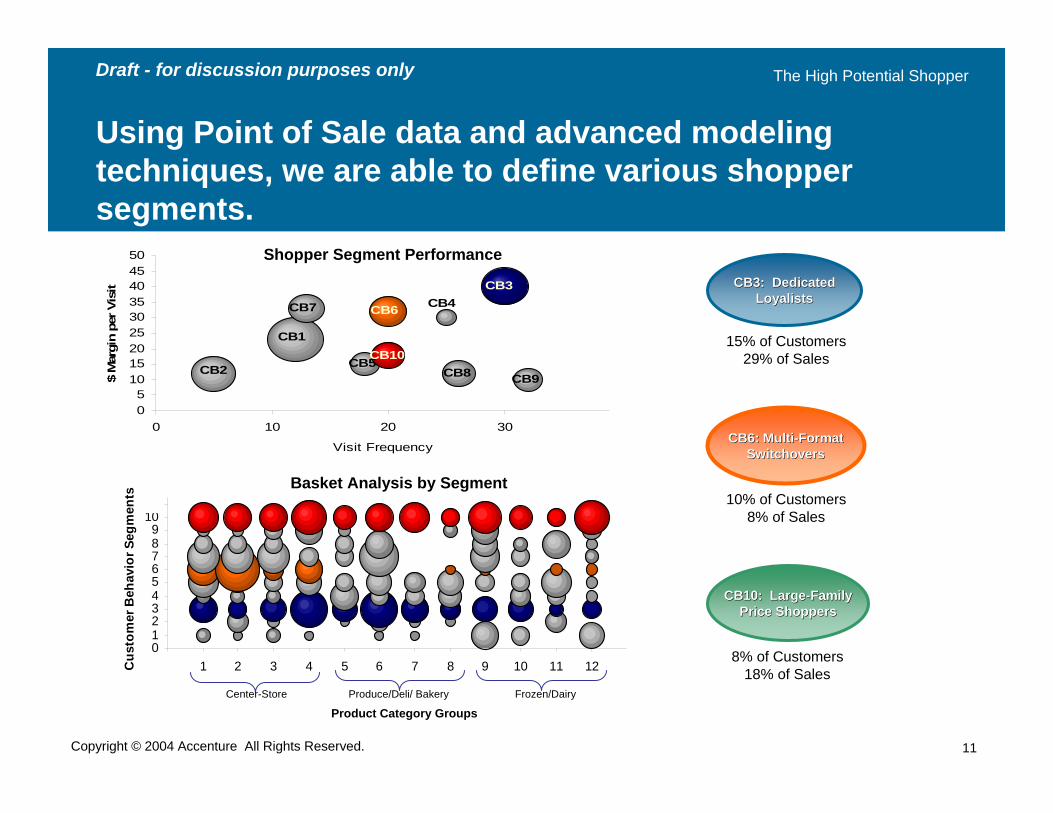

Using Point of Sale data and advanced modeling techniques, we are able to define various shopper segments.

CB3: DedicatedCB3: DedicatedLoyalistsLoyalists

15% of Customers29% of Sales

CB6: MultiCB6: Multi--FormatFormatSwitchoversSwitchovers

CB10: LargeCB10: Large--FamilyFamilyPrice ShoppersPrice Shoppers

10% of Customers8% of Sales

8% of Customers18% of Sales

CB10

CB7 CB6

CB1

CB2

CB3CB4

CB5CB8 CB9

05

101520253035404550

0 10 20 30

Visit Frequency

$ M

argi

n pe

r Vis

it

Shopper Segment Performance

0123456789

1011

0 1 2 3 4 5 6 7 8 9 10 11 12Cus

tom

er B

ehav

ior S

egm

ents

Center-Store Produce/Deli/ Bakery Frozen/Dairy

Basket Analysis by Segment

Product Category Groups

The High Potential Shopper

12Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

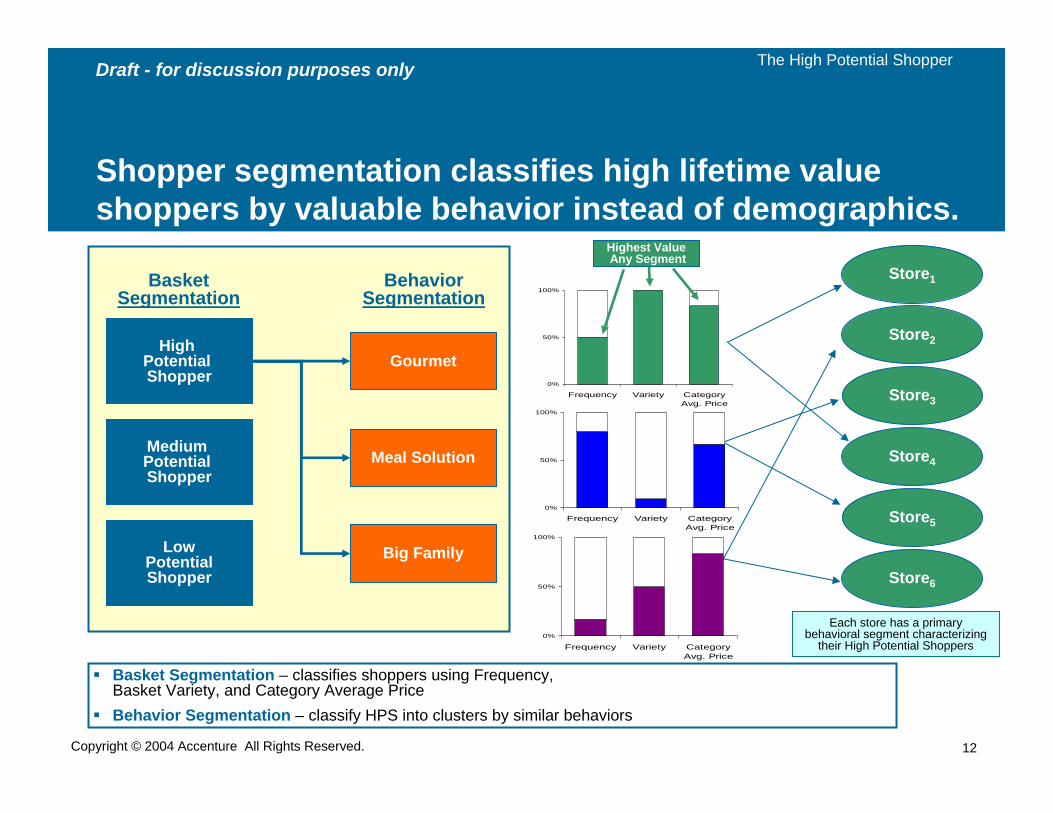

Shopper segmentation classifies high lifetime value shoppers by valuable behavior instead of demographics.

Basket Segmentation – classifies shoppers using Frequency, Basket Variety, and Category Average PriceBehavior Segmentation – classify HPS into clusters by similar behaviors

Each store has a primary behavioral segment characterizing

their High Potential Shoppers

High Potential Shopper

Medium Potential Shopper

LowPotentialShopper

Gourmet

Meal Solution

Big Family

Basket Segmentation

Behavior Segmentation

Store1

Store2

Store3

Store4

Store5

Store6

0%

50%

100%

Frequency Variety CategoryAvg. Price

0%

50%

100%

Frequency Variety CategoryAvg. Price

0%

50%

100%

Frequency Variety CategoryAvg. Price

Highest ValueAny Segment

The High Potential Shopper

13Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

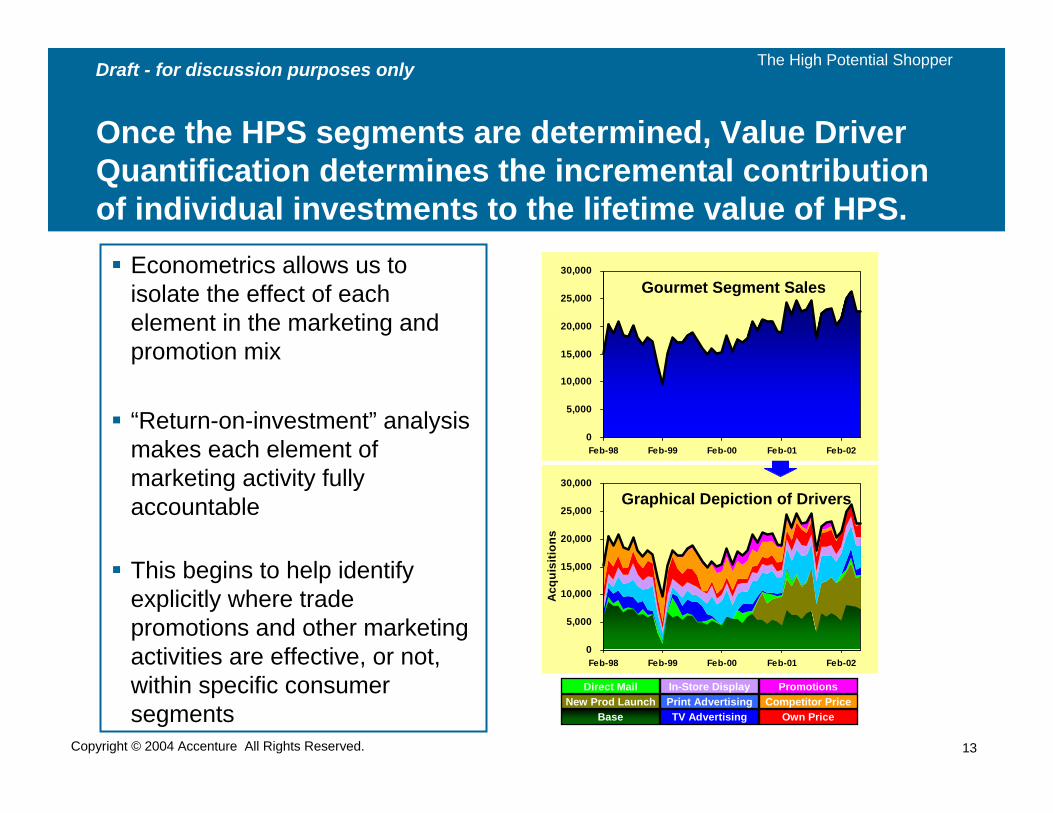

Once the HPS segments are determined, Value Driver Quantification determines the incremental contribution of individual investments to the lifetime value of HPS.

Econometrics allows us to isolate the effect of each element in the marketing and promotion mix

“Return-on-investment” analysis makes each element of marketing activity fully accountable

This begins to help identify explicitly where trade promotions and other marketing activities are effective, or not, within specific consumer segments

0

5,000

10,000

15,000

20,000

25,000

30,000

Feb-98 Feb-99 Feb-00 Feb-01 Feb-02

Acq

uisi

tions

Graphical Depiction of Drivers

BaseNew Prod Launch

Direct Mail

TV AdvertisingPrint AdvertisingIn-Store Display

Own PriceCompetitor Price

Promotions

0

5,000

10,000

15,000

20,000

25,000

30,000

Feb-98 Feb-99 Feb-00 Feb-01 Feb-02

Acq

uisi

tions

Gourmet Segment Sales

The High Potential Shopper

14Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

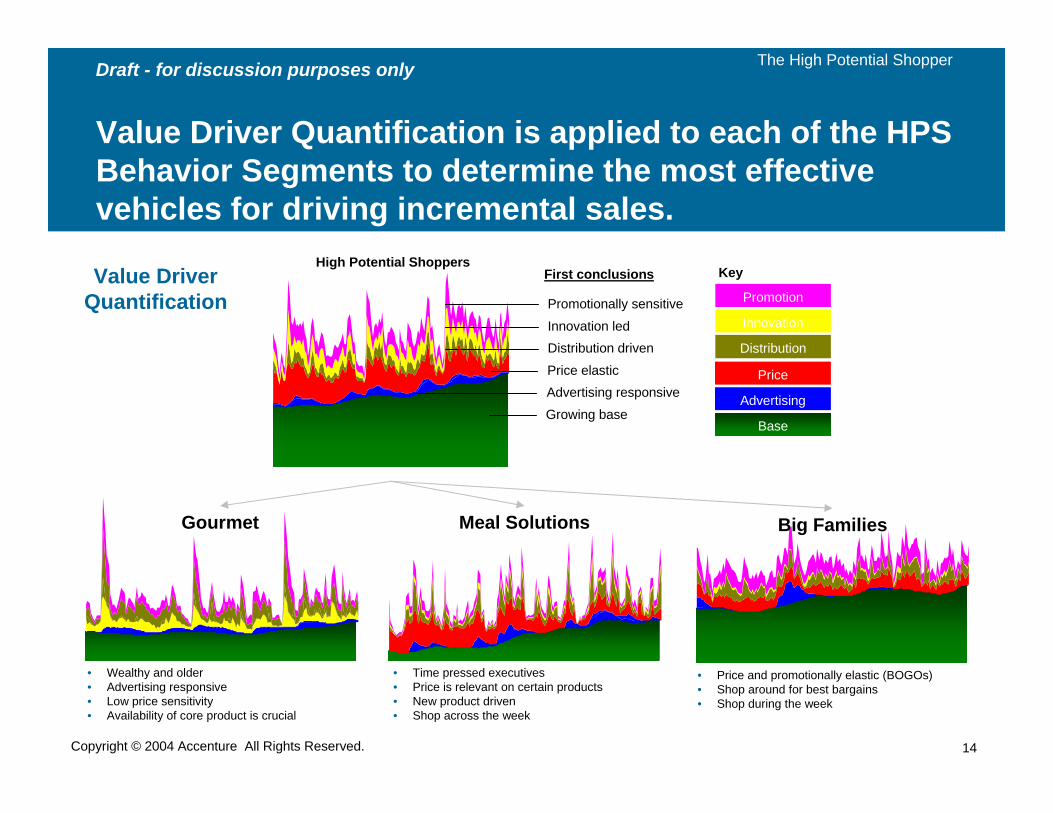

Value Driver Quantification is applied to each of the HPS Behavior Segments to determine the most effective vehicles for driving incremental sales.

Gourmet

• Wealthy and older• Advertising responsive• Low price sensitivity• Availability of core product is crucial

Meal Solutions

• Time pressed executives• Price is relevant on certain products• New product driven• Shop across the week

Big Families

• Price and promotionally elastic (BOGOs)• Shop around for best bargains• Shop during the week

High Potential Shoppers

Growing base

Price elastic

Innovation led

Promotionally sensitive

Distribution driven

First conclusions

Advertising responsive

Promotion

Innovation

Distribution

Price

Advertising

Base

KeyValue Driver Quantification

The High Potential Shopper

15Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

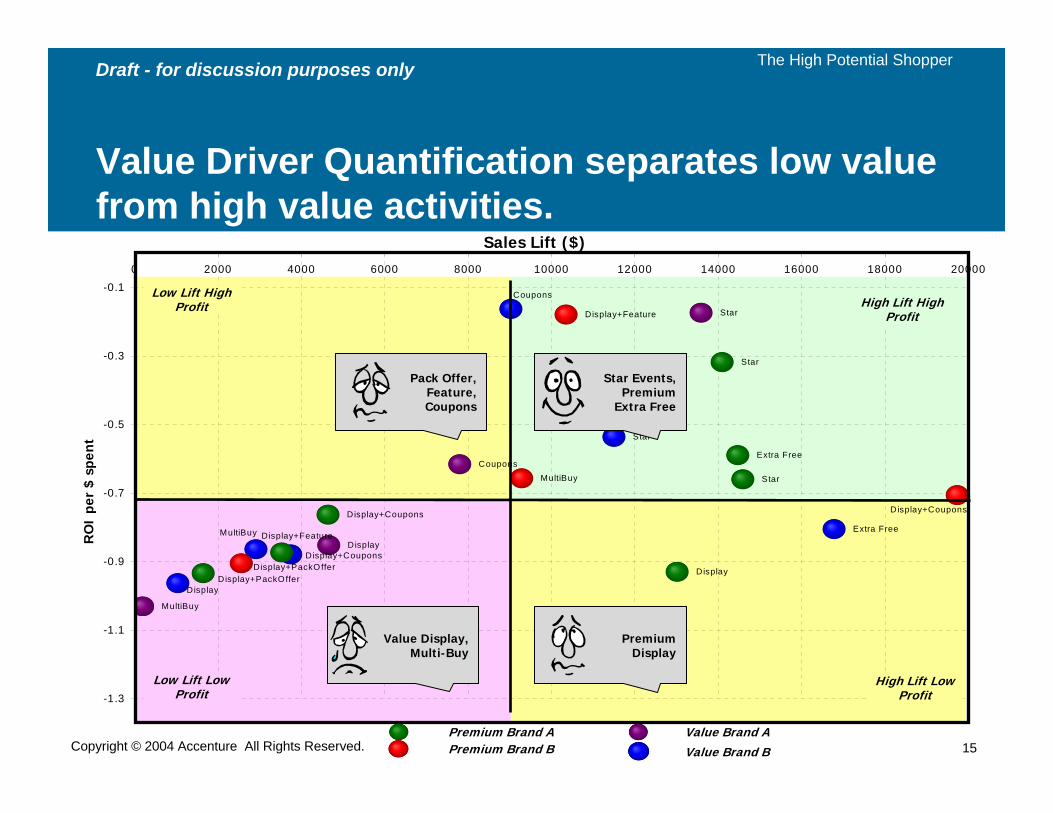

Value Driver Quantification separates low value from high value activities.

Star

Star

Extra Free

Display+PackOffer

Display+Feature

Display+Coupons

Display

MultiBuy

Display+PackOffer

Display+Feature

Display+Coupons

Star

MultiBuy

Display

Coupons

Star

MultiBuy Extra Free

Display+Coupons

Display

Coupons

-1.3

-1.1

-0.9

-0.7

-0.5

-0.3

-0.10 2000 4000 6000 8000 10000 12000 14000 16000 18000 20000

RO

I pe

r $

spe

nt

Sales Lift ($)

Pack Offer,Feature,Coupons

Star Events,Premium

Extra Free

Premium Display

Value Display,Multi-Buy

Premium Brand APremium Brand B

Value Brand AValue Brand B

Low Lift High Profit

Low Lift Low Profit

High Lift High Profit

High Lift Low Profit

The High Potential Shopper

16Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

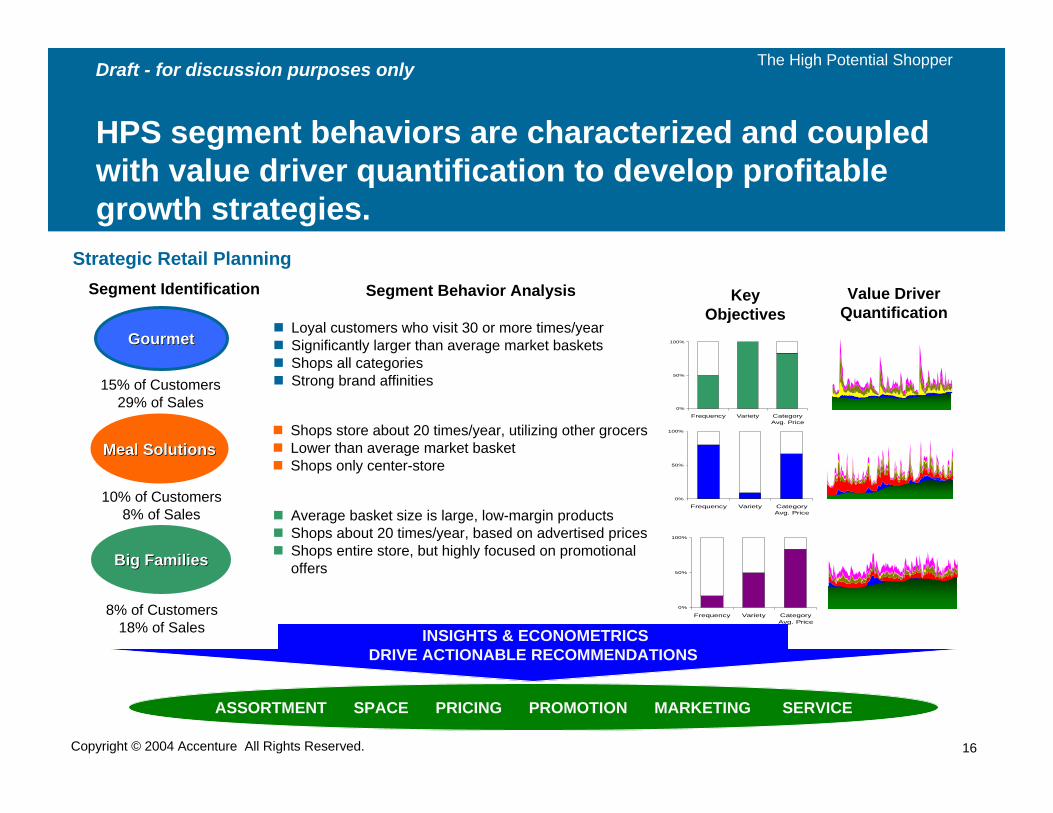

HPS segment behaviors are characterized and coupled with value driver quantification to develop profitable growth strategies.

GourmetGourmet

15% of Customers29% of Sales

Meal SolutionsMeal Solutions

Big FamiliesBig Families

10% of Customers8% of Sales

8% of Customers18% of Sales

Loyal customers who visit 30 or more times/yearSignificantly larger than average market basketsShops all categoriesStrong brand affinities

Shops store about 20 times/year, utilizing other grocersLower than average market basketShops only center-store

Average basket size is large, low-margin productsShops about 20 times/year, based on advertised pricesShops entire store, but highly focused on promotional offers

INSIGHTS & ECONOMETRICSDRIVE ACTIONABLE RECOMMENDATIONS

ASSORTMENT SPACE PRICING PROMOTION MARKETING SERVICE

Value Driver Quantification

Segment Behavior AnalysisSegment Identification Key Objectives

0%

50%

100%

Frequency Variety CategoryAvg. Price

0%

50%

100%

Frequency Variety CategoryAvg. Price

0%

50%

100%

Frequency Variety CategoryAvg. Price

Strategic Retail Planning

The High Potential Shopper

17Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

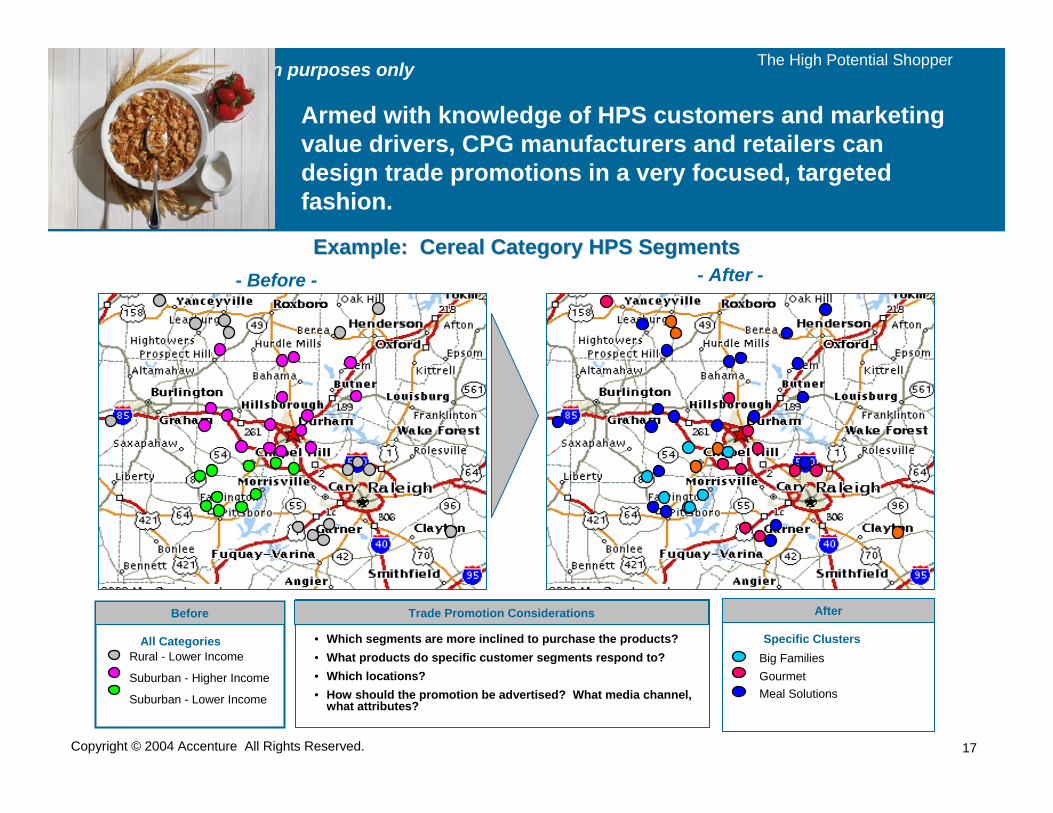

Armed with knowledge of HPS customers and marketing value drivers, CPG manufacturers and retailers can design trade promotions in a very focused, targeted fashion.

Before

Rural - Lower Income

Suburban - Higher Income

Suburban - Lower Income

All Categories

- Before - - After -

Specific Clusters

After

Meal Solutions

Big FamiliesGourmet

The High Potential Shopper

Example: Cereal Category HPS SegmentsExample: Cereal Category HPS Segments

• Which segments are more inclined to purchase the products?• What products do specific customer segments respond to?• Which locations?• How should the promotion be advertised? What media channel,

what attributes?

Trade Promotion Considerations

18Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

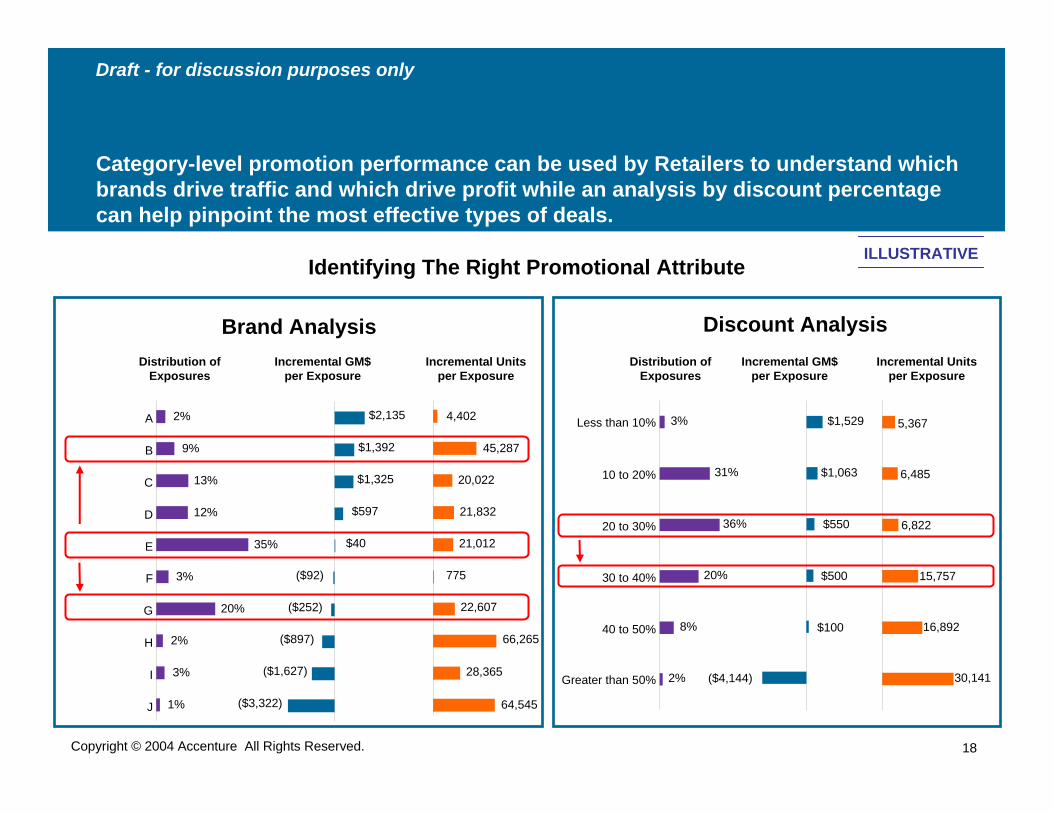

Incremental Units per Exposure

4,402

45,287

20,022

21,832

21,012

775

22,607

66,265

28,365

64,545

2%

9%

13%

12%

35%

3%

20%

2%

3%

1%

Distribution ofExposures

A

B

C

D

E

F

G

H

I

J

Incremental GM$ per Exposure

($92)

($252)

($897)

($1,627)

($3,322)

$2,135

$1,392

$1,325

$597

$40

3%

31%

36%

20%

8%

2%

Less than 10%

10 to 20%

20 to 30%

30 to 40%

40 to 50%

Greater than 50%

Distribution ofExposures

$1,529

$1,063

$550

$500

$100

($4,144)

Incremental GM$ per Exposure

5,367

6,485

6,822

15,757

16,892

30,141

Incremental Units per Exposure

Discount AnalysisBrand Analysis

Category-level promotion performance can be used by Retailers to understand which brands drive traffic and which drive profit while an analysis by discount percentage can help pinpoint the most effective types of deals.

Identifying The Right Promotional AttributeILLUSTRATIVE

19Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

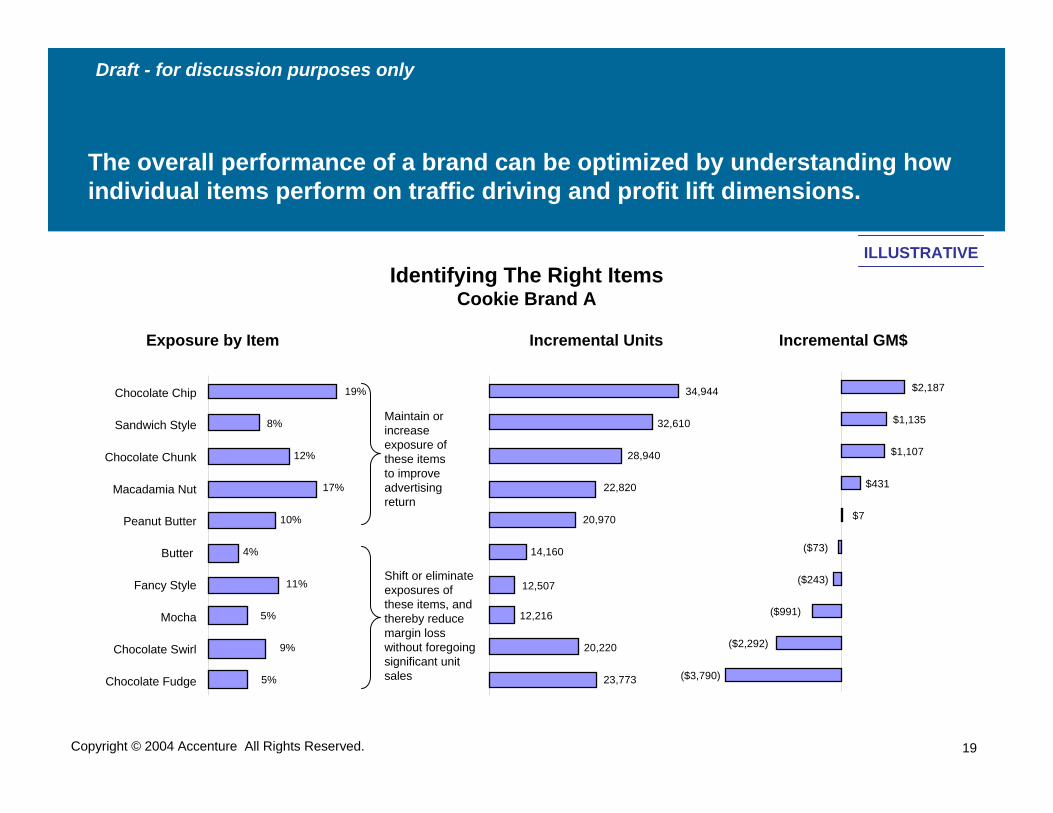

The overall performance of a brand can be optimized by understanding how individual items perform on traffic driving and profit lift dimensions.

Identifying The Right Items Cookie Brand A

Incremental Units Incremental GM$

$2,187

$1,135

$1,107

$431

$7

($73)

($243)

($991)

($2,292)

($3,790)

34,944

32,610

28,940

22,820

20,970

14,160

12,507

12,216

20,220

23,773

19%

8%

12%

17%

10%

4%

11%

5%

9%

5%

Chocolate Chip

Sandwich Style

Chocolate Chunk

Macadamia Nut

Peanut Butter

Butter

Fancy Style

Mocha

Chocolate Swirl

Chocolate Fudge

Exposure by Item

Shift or eliminate exposures of these items, and thereby reduce margin loss without foregoing significant unit sales

Maintain or increase exposure of these items to improve advertising return

ILLUSTRATIVE

20Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

Conclusions• The Daunting Dilemma continues, and it’s only getting more

complicated and more competitive • Successful ROI on Trade Promotions and other investments lies in

achieving a true understanding of customer segments and their behaviors.

• Value Driver Quantification must be used to understand the responsiveness of marketing activities, including promotions.

• Merchandising and Marketing strategies must be realigned to build off of the customer insight.

• Collaboration, including the sharing of data, insight and results will become ever more important in achieving positive ROI on trade promotions profitable growth overall.

21Copyright © 2004 Accenture All Rights Reserved.

Draft - for discussion purposes only

Call to Action• Understand who the High Potential Shoppers are• Understand what drives and motivates them• Align marketing and sales tactics to attract them• Collaborate between CPG Manufacturer/Retailer –

share data, insight, learnings openly• Create joint accountability for success• Measure, assess, learn and continuously improve