Embed Size (px)

Citation preview

Innovative Project Financing /

Alternative Project Delivery

Alternative Delivery Methods for

Infrastructure

March 4, 2010Wyndham Garden Hotel

Public-Private Partnerships (PPPs) Innovative Financing, Alternative Project Delivery

Presented by: Yuval Cohen, PB

Transportation Workshop:

Innovative Project Financing/Alternative DeliveryMarch 4 2010, Overland Park, KS

Transportation Workshop Mar 4 2010

Agenda

Definitions

Alternative Delivery Mechanisms in detail

Why now? Why are these back under consideration?

Where/when have they been tried?

Lessons learned

Resource links

Transportation Workshop Mar 4 2010

Public-Private Partnership (PPP), a form ofAlternative Project (Program) Delivery(APD)

What it is:

Alternative procurement and delivery approach to financing and delivery of a project

Contractual arrangement whereby government entity engages the private sector to do more than it usually does in delivering a public use service or facility

Private sector entity assumes obligations to develop, finance, design, construct, operate and maintain

Transportation Workshop Mar 4 2010

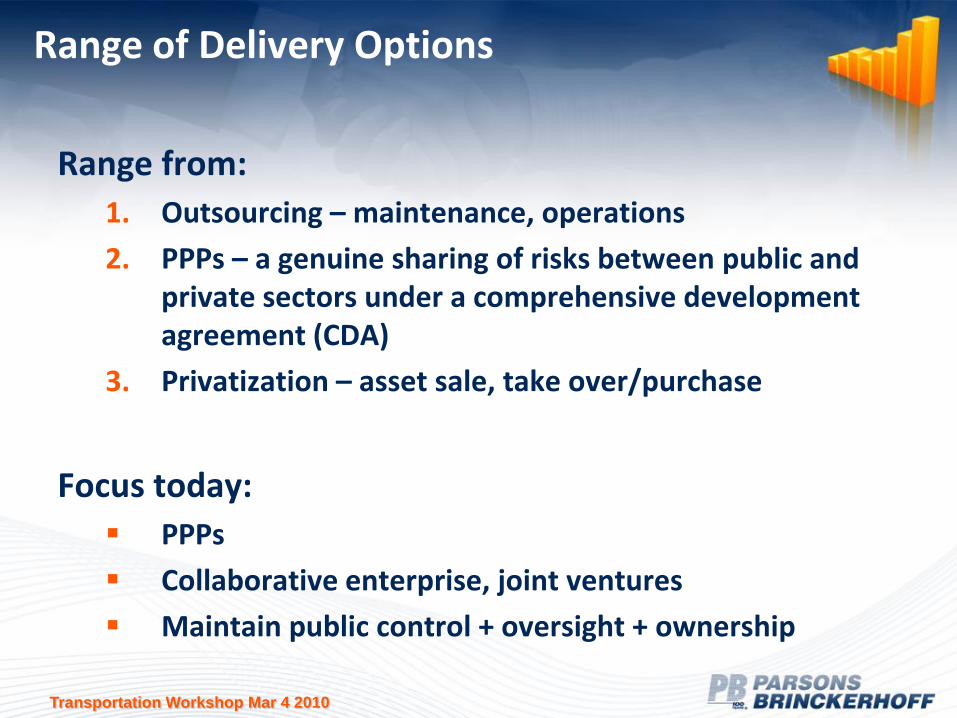

Range of Delivery Options

Range from:

1. Outsourcing – maintenance, operations

2. PPPs – a genuine sharing of risks between public and private sectors under a comprehensive development agreement (CDA)

3. Privatization – asset sale, take over/purchase

Focus today:

PPPs

Collaborative enterprise, joint ventures

Maintain public control + oversight + ownership

Transportation Workshop Mar 4 2010

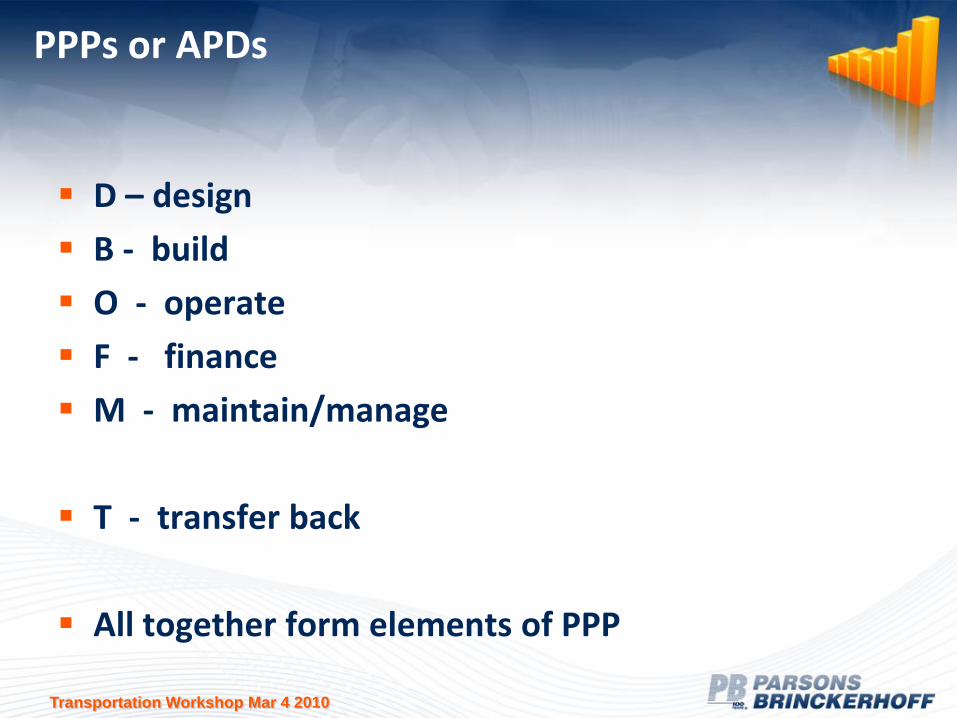

PPPs or APDs

D – design

B - build

O - operate

F - finance

M - maintain/manage

T - transfer back

All together form elements of PPP

Transportation Workshop Mar 4 2010

O & M (+ manage)

Simplest of partnerships

Publicly owned asset

Operated and maintained under contract with private sector

Control is maintained

Payment via fee to contractor, incentives to perform + penalties for non-performance

Examples: transit systems; wastewater treatment; pavement management

Transportation Workshop Mar 4 2010

D + B

Increasing acceptance nationally

Performance specifications, rather than design specs

Private entity incentive to come up with innovation, cost-effective concept

Can delivery of project be accelerated (portions of D + B can be accomplished simultaneously, therefore quicker)?

Better control over delivered price, fewer change orders?

Transportation Workshop Mar 4 2010

D + B + O + M

Combines O + M with design-build in one contract

Public maintains ownership at all times + oversight

D + B + F + O + M: adds finance component

Again, all under one contract: CDA, that spells out responsibilities

Transportation Workshop Mar 4 2010

Design

Construction, usually under fixed price

Operations Contract

Maintenance

Specialized vendors: ITS, toll equipment etc, paving contractors etc.

Public Body: state, granting authority

Special Purpose Company:

Concessionaire

Loans $• Private lenders

• TIFIA

• BAB’s

Equity/Shareholders $

EPC Contractor

Construction JVOperating Company

Grants $

Availability

Payments $

CDA:

F+D+B+O/M

contract

Transportation Workshop Mar 4 2010

PPP:

Structure that shares delivery and risk responsibilities of both public and private sectors:

Existing assets (“brownfield”): Private partner assumes responsibility/risk for existing asset: long term

lease, outright purchase

Focus on O&M, meeting/exceeding performance

In exchange for lease, up front payment to the public agency/owner

Managed lanes, corridors in existing R-O-W, demand management I-595, FL, I-635 Managed Lanes, Dallas-FW

New assets (“greenfield”): Private sector develops, delivers, maintains/operates new facility

SR-125 South Bay Expressway, CA

Transportation Workshop Mar 4 2010

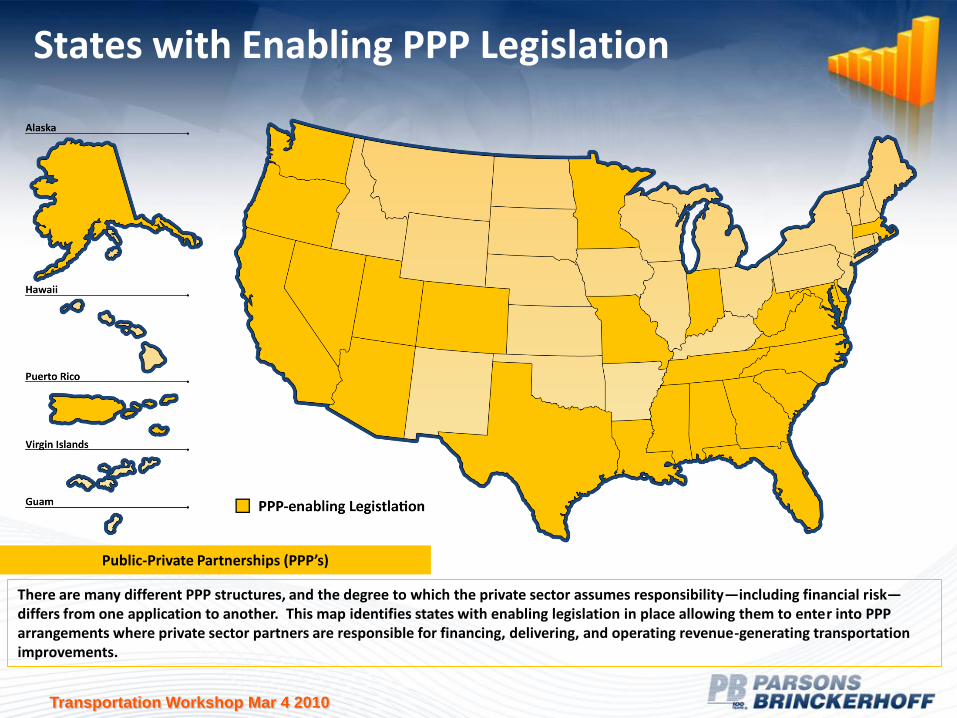

States with Enabling PPP Legislation

There are many different PPP structures, and the degree to which the private sector assumes responsibility—including financial risk—differs from one application to another. This map identifies states with enabling legislation in place allowing them to enter into PPP arrangements where private sector partners are responsible for financing, delivering, and operating revenue-generating transportation improvements.

Public-Private Partnerships (PPP’s)

Transportation Workshop Mar 4 2010

Innovative Financing

Financing methods are not really “innovative”

Instead, this refers to:

Alternative delivery methods where some form of private capital is involved

Combination of private financing and public funding

Financial mechanisms bundled to deliver projects more timely, efficiently, value for money basis

Expanded choice set of available tools

Transportation Workshop Mar 4 2010

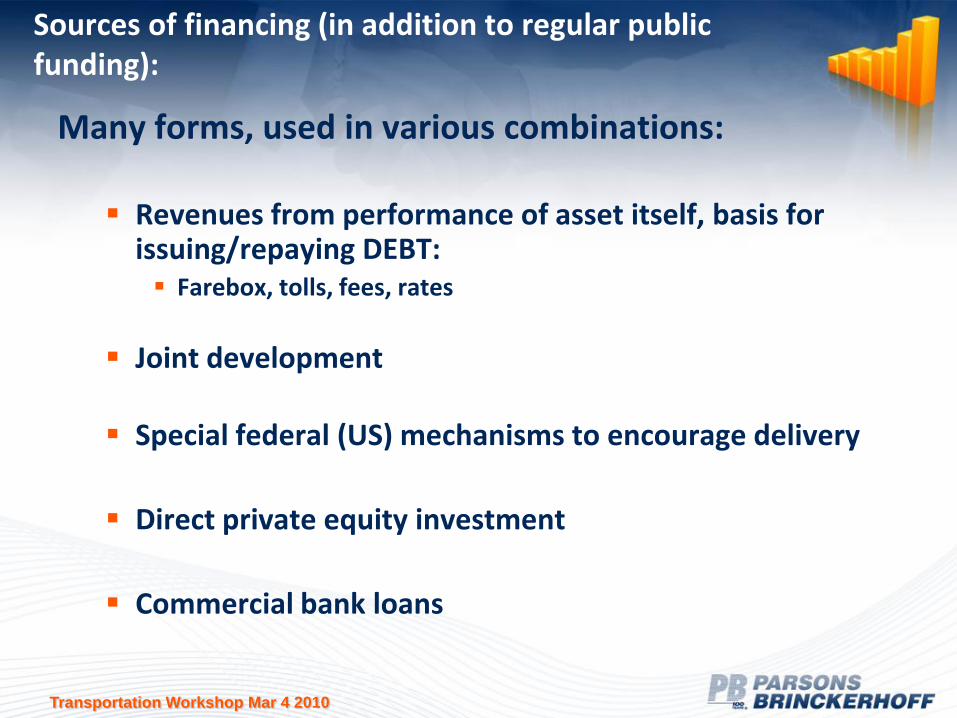

Sources of financing (in addition to regular public funding):

Many forms, used in various combinations:

Revenues from performance of asset itself, basis for issuing/repaying DEBT: Farebox, tolls, fees, rates

Joint development

Special federal (US) mechanisms to encourage delivery

Direct private equity investment

Commercial bank loans

Transportation Workshop Mar 4 2010

Mechanisms to Encourage Project Delivery:

Availability payments Public sponsor, state DOT or authority

Supplemented from state highway funds Appropriations based

Annual payment to concessionaire for performance of road

1. Based upon specific project milestones (acceptance payment) Completion of facility by certain deadline or other construction milestones

2. Facility performance standards: Lane availability, incident management metrics Penalties for not meeting metrics:

Lane closures for maintenance, lane availability Snow removal; mowing grass; clearing debris LOS performance can also be used as metric for managed lanes concessions

3. Suitable when inadequate toll revenues to finance lifecycle of construction + O&M costs

4. Less risk to private sector than under full road concessions: little T&R risk Concessionaire receives predictable, fixed set of payments over life of concession Reliance on public agency credit/appropriations

5. Used extensively in Canada, Europe, Australia

Transportation Workshop Mar 4 2010

Mechanisms to Encourage Project Delivery:

Private activity bonds (PAB) Tax exempt bonds issued by public entity for benefit of

private developers who are responsible for repayment

Repayment risk: relying on toll revenues

$2 billion North Tarrant Express managed lanes project, Fort Worth TX (2009): $400m in (senior lien) revenue bond financing

Issued on project’s behalf by Texas PAB Surface Transportation Corporation

Even with risk of managed lanes (toll free alternative is a few feet away)!

Transportation Workshop Mar 4 2010

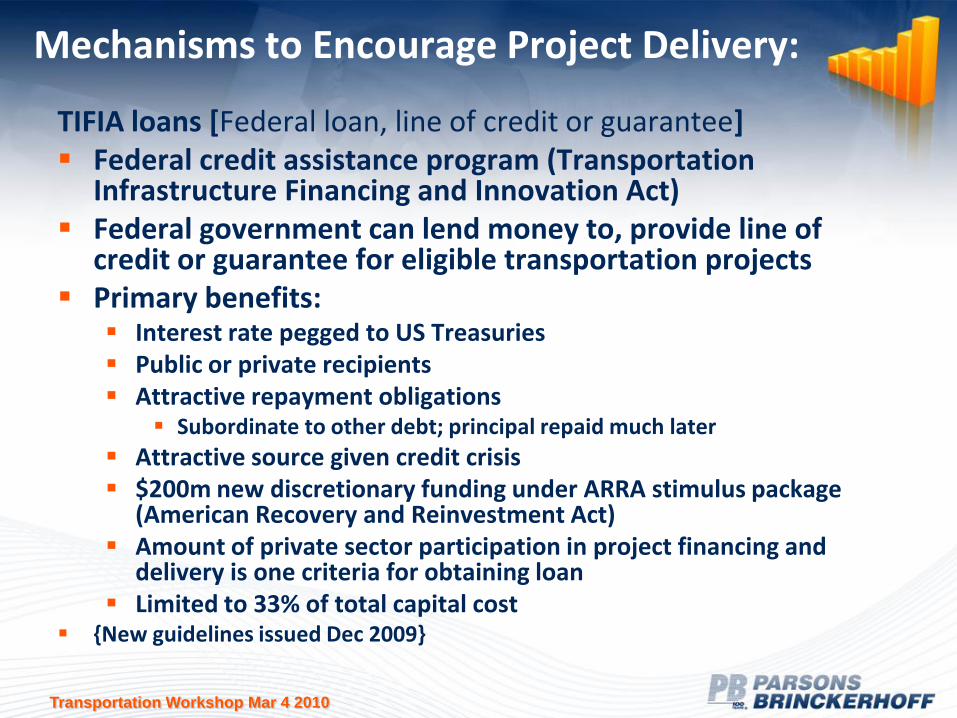

Mechanisms to Encourage Project Delivery:

TIFIA loans [Federal loan, line of credit or guarantee] Federal credit assistance program (Transportation

Infrastructure Financing and Innovation Act) Federal government can lend money to, provide line of

credit or guarantee for eligible transportation projects Primary benefits:

Interest rate pegged to US Treasuries Public or private recipients Attractive repayment obligations

Subordinate to other debt; principal repaid much later

Attractive source given credit crisis $200m new discretionary funding under ARRA stimulus package

(American Recovery and Reinvestment Act) Amount of private sector participation in project financing and

delivery is one criteria for obtaining loan Limited to 33% of total capital cost

{New guidelines issued Dec 2009}

Transportation Workshop Mar 4 2010

TIFIA

The TIFIA of 1998 is a Federal program through which USDOT provides credit assistance in the form of direct loans, loan guarantees, and credit assistance to major surface transportation projects with dedicated revenue streams. TIFIA has provided credit assistance to state departments of transportation, transit operators, special authorities, local governments, and private entities undertaking highway, transit, rail and intermodal improvements. The program is designed to fill market gaps and leverage limited Federal resources and substantial co-investment by providing projects with supplemental or subordinate debt rather than grants. This map identifies states and individual projects that have received TIFIA credit enhancements. TIFIA program has provided $5.8 billion in credit assistance leveraging projects with a construction value of $21.8 billion.

Transportation Infrastructure Finance and Innovation Act (TIFIA)

Transportation Workshop Mar 4 2010

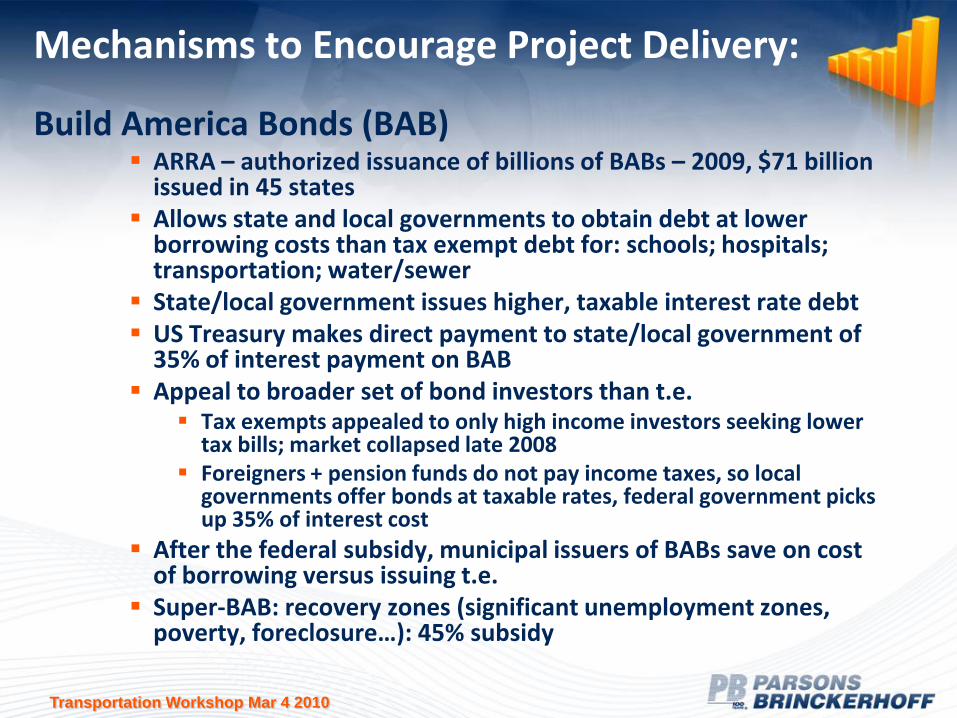

Mechanisms to Encourage Project Delivery:

Build America Bonds (BAB) ARRA – authorized issuance of billions of BABs – 2009, $71 billion

issued in 45 states Allows state and local governments to obtain debt at lower

borrowing costs than tax exempt debt for: schools; hospitals; transportation; water/sewer

State/local government issues higher, taxable interest rate debt US Treasury makes direct payment to state/local government of

35% of interest payment on BAB Appeal to broader set of bond investors than t.e.

Tax exempts appealed to only high income investors seeking lower tax bills; market collapsed late 2008

Foreigners + pension funds do not pay income taxes, so local governments offer bonds at taxable rates, federal government picks up 35% of interest cost

After the federal subsidy, municipal issuers of BABs save on cost of borrowing versus issuing t.e.

Super-BAB: recovery zones (significant unemployment zones, poverty, foreclosure…): 45% subsidy

Transportation Workshop Mar 4 2010

Mechanisms to Encourage Project Delivery:

GARVEE

Grant Anticipation Revenue Vehicles

Bonds permit states (and sometimes localities) to repay debt service with future Federal-aid highway apportionments

Used in advance construction to enable using Federal-aid funds to spread payments over useful life of asset (rather than over construction period)

Transportation Workshop Mar 4 2010

GARVEE

GARVEE bonds are financing instruments backed by a pledge of future Federal-aid from USDOT. States must enact enabling legislation providing the authority to issue GARVEE debt, and a great variety in GARVEE procedures exist from state to state. GARVEEs generate upfront capital for major capital projects that a state would likely be unable to construct in the near-term using traditional pay-as-you-go funding approaches. Bond-related costs eligible for Federal-aid reimbursement include interest payments, retirement of principal, and any other cost incidental to the sale of an eligible bond issue. States, political subdivisions, and public authorities have issued GARVEE debt. This map indicates states that have done so.

Grant Anticipation Revenue Vehicle (GARVEE) Bonds

Transportation Workshop Mar 4 2010

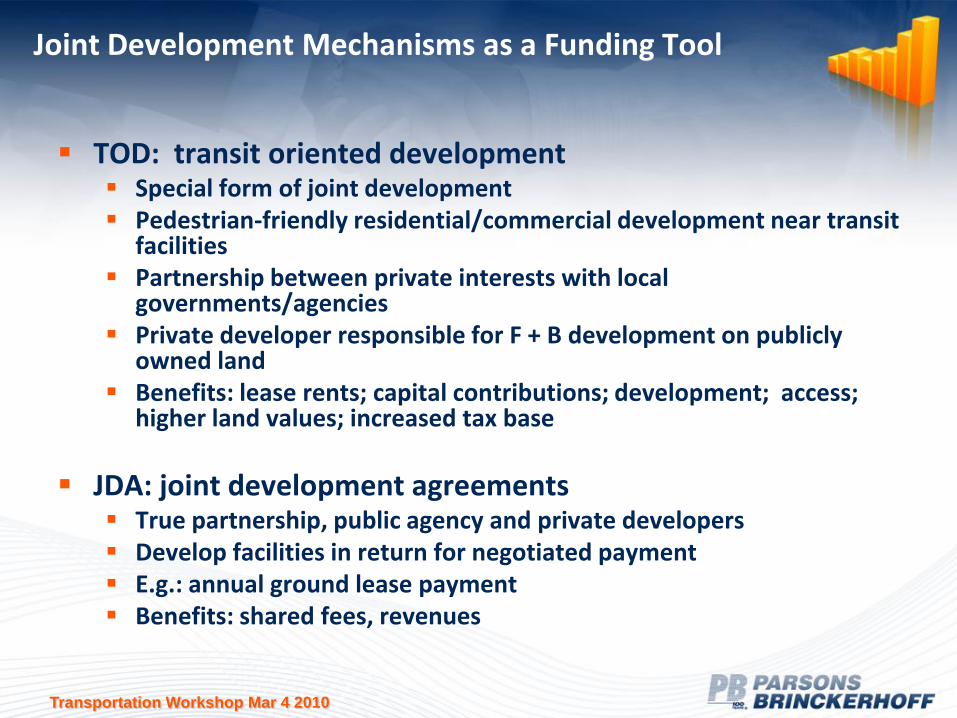

Joint Development Mechanisms as a Funding Tool

TOD: transit oriented development Special form of joint development Pedestrian-friendly residential/commercial development near transit

facilities Partnership between private interests with local

governments/agencies Private developer responsible for F + B development on publicly

owned land Benefits: lease rents; capital contributions; development; access;

higher land values; increased tax base

JDA: joint development agreements True partnership, public agency and private developers Develop facilities in return for negotiated payment E.g.: annual ground lease payment Benefits: shared fees, revenues

Transportation Workshop Mar 4 2010

Other Funding Tools

Business improvement districts (BID) BIDs assess properties within defined areas to finance variety of

services (security, maintenance, parking, transportation)

Benefits: property tax assessment revenues

Tax increment financing (TIF) Municipality finances development through increased property taxes

derived from enhanced property values resulting from activities

TIFs can use revenue stream to finance infrastructure (streets etc)

TIF can be debt issued by municipality, repaid from enhanced property value proceeds, provided the development materializes

Benefit: dedicated funding stream to repay debt without increasing tax rates

Transportation Workshop Mar 4 2010

Funding Mechanisms …..

Long-term leases Public agency leases to private concessionaire

Under lease, concessionaire agrees to pay upfront fee to agency in return for right to collect fees (tolls) for 25-99 years

Agrees to operate/maintain facility for lease term

No change in ownership

Benefits: large up-front revenues, transferring risks of operation/financial to private concessionaire

Chicago Skyway (05): $1.8 billion up front in exchange for 99-yr lease

Indiana Toll Road (05): $3.8 b for 75-years, fully funding state’s 10-yr plan + each county in state for local projects

Parking lease: Chicago received $563m for 99-yr lease of 4 garages + $1.2b for 75-yr lease on 36,000 metered spaces

Problem: most of proceeds will be spent before the leases end, temptation to renegotiate/cancel lease as higher tolls/charges kick in

Transportation Workshop Mar 4 2010

“Concessionaire” is key actor

Contracts with government body/agency for a particular project Investment vehicle: either wholly owned, or portion of a joint venture

arrangement Funded by equity investment from parent, lead or other j.v. partners Benefits from proceeds from borrowings raised from debt capital

markets, or commercial bank loan Responsible for developing, building, operating and maintaining asset

under PPP structure Receives income (returns on investment) from ongoing operations:

Hospitals: number of beds available Roads:

Volume of traffic, tolls, toll revenues Availability payment for making facility “available” Shadow tolls/”pass through tolls”: payment for each vehicle counted

Military housing: fees paid directly to concessionaire Prisons: number of inmates (payment for each one served)

Transportation Workshop Mar 4 2010

State Infrastructure Bank (SIB)

State Departments of Transportation use Federal Highway funding to create State Infrastructure Banks (SIBs)

SIBs are revolving loan funds for transportation projects Any private or public entity may apply for SIB credit assistance, for

eligible project Amount of assistance depends on the size of the state’s SIB SIBs vary widely in size: from under $1 million to more than $100 million SIBs can also provide loan guarantees for private loans, or a line of credit Interest rate is set by the state (maximum at market rate, but typically

below or even 0%) Maximum loan term is 35 years (though DOT will usually negotiate for

less) State may be willing to take more risk than a commercial bank Significant public benefits

Transportation Workshop Mar 4 2010

Why now, again?

Funding constraints: Diminishing traditional sources of funding Timing of appropriations cycle, segmented delivery vs integrated Debt capacity of even the best capitalized authorities

Capital needs to renew, replace, maintain, operate Congestion management Highway/transit/port capacity Delivered + clean water needs

Unfunded mandates priorities: Security at ports, environmental

Global credit crisis, effects on municipal tax-exempt borrowing

Desire by private consortia to play more active role in delivering infrastructure Private capital/credit made available up front

Transportation Workshop Mar 4 2010

Benefits of PPPs/APD?

Addresses highway capacity/congestion mitigation earlier Government can leverage its resources better,

accomplishing more projects for the same $’s Raises new investment capital from investors (Dallas Police

& Fire Pension Fund, IH-635 LBJ Freeway, TX) Risk sharing with investors More business like approaches More innovations, packaging, ideas (inc. D/B):

Capital Beltway (VA), proposed 2 HOT lanes instead of state’s concept of 2 HOV lanes, $2 billion cost savings for same capacity

POMT + I-595, Florida

Up front payments from concessionaires ($1/2 billion paid by BRISA/CCR for Northwest Parkway, CO, 99-yr lease)

Faster…..?

Transportation Workshop Mar 4 2010

Value for Money?

Does alternative delivery method ostensibly: Deliver project earlier than design-bid-build, PAYGO approach?

Minimize outlays while sharing risk with private sector?

Accomplish goals more cost effectively, on a present value (future costs and benefits) basis?

How do you analyze this? Estimate costs, schedule, possible revenues etc under

traditional delivery vs. alternative delivery methods

Will potentially higher financing costs and risk premiums be more than offset by: Advancing completion of works; delivering project earlier; other

efficiency gains; lifecycle cost savings, performance gains during operations?

NPV analysis of cost and benefit streams

Transportation Workshop Mar 4 2010

Public Sector Interests Need to be Preserved:

Are delivery, procurement, financing options effective?

Do these methods have potential for value added? Will programs be delivered faster, more cost effectively over life

cycle (value for money analysis)?

Will this approach be attractive to private interests?

Assess risks: technical, market (revenue, patronage), environmental (programmatic), financial

Is there sufficient protection of the public interest? Quality? Safety?

Stability of private sector developers over time?

Transportation Workshop Mar 4 2010

Other Questions…..

Will these mechanisms feature local job creation/preservation?

Roads designed/built to state/local specifications/standards, approvals, monitoring?

Robust environmental process

Basic premise: these are partnerships, not a cessation of public control/oversight/ownership functions……

Transportation Workshop Mar 4 2010

History of PPP/APD in US: Over 200 Years

Private sector has always been involved in delivering U.S. infrastructure Post-Revolutionary War, local authorities faced financial burden of debts

accumulated State governments chartered private companies to construct + deliver

roads “turn the pike”:

US: 3,200 companies successfully financed, built, and operated toll roads, 1792-1902: Private, stock-financed corporations, designed to pay dividends to its

shareholders Higher class of service, stone/packed gravel surface, then wooden planks

(“getting farmers out of the mud”) Faster speeds, shorter travel times to market, for a fee 1st turnpike: Alexandria-Berryville, VA, 1792 1st private turnpike: Philadelphia-Lancaster, PA, 1792 Typical profile:

Relatively high construction costs (<$2,000/mile), 15-40 miles in length Few earned profit, paid out dividends to investors: initial stock offerings paid for

construction; toll receipts then paid for operating expenses Value: not in profits to shareholders, but in providing access to landowners, access to

markets, improved land values

Most successful: private toll bridge companies (Boston’s Charles River Bridge): average annual return of 10.5% for investors (1790s): no toll exemptions, little toll evasion, no conflict over location of toll gates

Transportation Workshop Mar 4 2010

Interesting Historical Facts: We’ve Done These Before

Mid-Atlantic/New England: private turnpike companies amounted to 1/3 of all business corporations during 1790s-1850s

1850s: rise of private toll roads in West: CO (414), NV, CA, following passage of general laws of incorporation. Private entrepreneurs built/operated toll roads even before there was a state of Nevada

1789-1933: majority of infrastructure projects delivered using methods similar to PPPs for: canals, roads, railroads, telegraph, telephone, power generation & distribution

In transportation: combination of Congress’ own funds + concession/private charter and leases

Congress used Design-Build-Finance-Operate-Maintain (D-B-F-O-M) method more than any other method

Transportation Workshop Mar 4 2010

End of an Era: Economic/Social Drivers Created Change

Private toll roads turned increasingly unprofitable, reduced demand Economic, regulatory reasons:

“Shunpikers” Concerns over “monopolistic” practices led legislatures to write numerous

restrictions into private turnpike charters: Toll gates could no longer be spaced closer than 5-10 miles apart This enabled evading tolls more often Exemptions to tolling implemented: family trips; those attending/returning from

churches, funerals, town meetings… Tolls were increased + penalties against shunpikers

Advent of expansion of canals for moving goods and people + railroads (mid-1800s)

Increasing numbers of chartered companies bankrupt: maintenance + admin costs grew faster than revenues

Policy movement against private toll roads (ownership and operation by private companies) contrary to “public sentiment”

Result: local public authorities assumed operation, local public delivery became the norm (1920s onwards)

Transportation Workshop Mar 4 2010

PPPs/APD in the Modern era

First generation: VA: passed Highway Corporation Act 1988, enabling private entities

to build and operate toll roads on public lands Result: Dulles Greenway Toll Road: 15-mile, limited access highway

extending from an existing toll road west to Loudoun County

CA: (1989): passed Assembly Bill AB680, enabling Caltrans to enter into franchise agreements with private parties seeking to design, build, finance, operate and maintain transportation facilities Result: four toll road projects submitted for consideration The only ones financed & built:

CPTC 91 Express Lanes (sold 2003), Orange-Riverside, CA SR 125 (now the South Bay Expressway), Orange, CA

Others: AZ (1991), WA, SC, all PPP statutes AZ Article I: state owns/leases out the facility; exercises its eminent

domain powers if necessary, franchises with private party (7 proposals submitted)

Article II: state would allow transfer of ownership to private entity; state would not be able to exercise right of eminent domain (1 proposal submitted)

Transportation Workshop Mar 4 2010

PPPs/APD in the Modern era

Second generation: 1991 ISTEA (Intermodal Surface Transportation Efficiency Act), major

changes to core delivery option: federal highway funds could now be used to pay for cost of building a public/private toll road, as long as facility was new, substantially improved & not part of interstate system

International developers/operators started taking notice of US PPP market

2004 USDOT Report to Congress on PPPs spurred new generation of PPP activity + numerous developments at state and federal level removing impediments to PPPs Jan 05: Chicago Skyway long term (99 yr) lease (Macquarie/Cintra) 2005: Indiana Toll Road (75-yr) lease, again Cintra/Macquarie 2006: 99-yr concession to operate + maintain Pocahontas Parkway

(Transurban) + construct Richmond Airport Connector

Hits: Northwest Parkway (CO); I-595 Corridor D-B-F-O-M (FL), 35-yr concession (ACS); Chicago $1.2 billion lease of city’s parking meter system; Port of Miami Tunnel (POMT, 2009)

Misses: Pennsylvania Turnpike concession; Alligator Alley (FL), Midway Airport (Il)

Transportation Workshop Mar 4 2010

Some Recent Transactions: How to get this done

Florida: I-595 Managed Lanes Upgrade 10.5-mile segment I-595 (AADTs 184,000) Florida DOT signed agreement with I-595 Express LLC, ACS-led consortium: D-B-

O-M project for 35 years $1.8 billion, upgrading current 6-lane highway to include 3 reversible managed

lanes in median, 2/4 auxiliary lanes outside general purpose lanes + others, congestion reliever

In exchange, concessionaire receives annual availability payment of $64m, as long as certain performance metrics are met

DOT collects toll revenues and sets toll rates Private Equity: $207m $607m debt from FHWA TIFIA loan:

Principal repayments scheduled to begin 2031 Subordinate to bank debt. Low rate at 3.64%, 1st interest payment 2014 First disbursement made in March 2009

$780m debt loaned by 12 commercial banks: 10-yr maturity: $255m tranche repaid with proceeds from FDOT availability payments $525m tranche repaid by acceptance payments from FDOT for completion of works

Construction commenced; projected completion 2014

Transportation Workshop Mar 4 2010

Second Example: POMT (Port of Miami Tunnel)

$1.06 billion capital costs, 1.2-km tunnel + access roads NO TOLLS, 35-yr concession Mostly availability payments + TIFIA loans $80 million in private equity (Bouygues/Meridiam) Acceptance payments:

$100m for design + construction milestones $350m construction completion milestone payment

$33 million in annual availability payment starts at substantial completion to fund O&M

$341 million TIFIA loan repaid from availability payments (grace period on interest until 2016 + on principal till 2033)

City of Miami + Miami-Dade contributed rights-of-way valued at $55m

County contributed $100 million in cash

Transportation Workshop Mar 4 2010

3rd Example: North Tarrant Express, Texas

$2.05 billion, 21.4-km managed lanes project

Awarded by TXDoT

Government (state) contributed $573 million

Private equity contributed: $427 m (Cintra,

Meridiam, Dallas Police & Fire Pension System)

Debt: $650m TIFIA loan + $400m PAB loan underwritten by JPMorgan + Bank of America

Closed end of Dec 09

Transportation Workshop Mar 4 2010

Up and Coming…….

LBJ Freeway IH-635 TX ($2.7 billion): managed lanes (equity commitments from Dallas Police & Fire Pension System)

Presidio Parkway/Doyle Drive, CA ($.96 b): tunnel + roadway (availability payments)

Miami Dade Expressway I-395 FL ($1 b?): managed lanes

Goethals Bridge, Port Authority of New York & New Jersey ($1.6b): availability payment

I-35 East, Texas: managed lanes

Michigan, Bi-National Bridge, US-Canada

Parking assets: Los Angeles, Pittsburgh + Philadelphia –others as well – all leases to private developers

Transportation Workshop Mar 4 2010

Public-Private Partnerships (PPP), a form ofAlternative Project (Program) Delivery(APD)

What these are not: Universal panacea, solution for all funding shortfalls A substitute for state/local programs Free financing from the private sector Always preferred alternatives Always demonstrate value for money (always cost

effective) Standardized + straightforward Devoid of politics Devoid of requiring public champions, stakeholder

outreach Involve loss of control/oversight functions for

government

Transportation Workshop Mar 4 2010

Issues/Risks

Public acceptance: private profit/tolls/new partners

Control

Political stability (AZ TX others)

Protectionism (foreign)

Complexities

Not a long track record + not wanting to be a pioneer

Usual project life cycle cost coverage

State/local staffing + champions

Default Project company on Southern Connector (Greenville SC) defaulted

on bond debt

Las Vegas Monorail filed for Chapter 11 (DBFOM)

Transportation Workshop Mar 4 2010

Lessons Learned?

It can be done Needs enabling legislation + local process adapted Is it worthwhile from a value for money viewpoint? Flexible, adaptable in financing structure, procurement

process, contract documents Ability to finance in stressed market Variety of funding sources Not a substitute for federal/state/local financing Often needs federal/state/local funding support Willingness to find solutions, even some at 11th hour DOT willingness + capabilities Support at state + local levels Federal support has to mirror state/local Strong support from local stakeholders, cities/counties Strong DOT outreach, public hearings eliciting public support It’s an ART, not a science

Transportation Workshop Mar 4 2010

Some Resources on PPPsAlternative Financing + Delivery

AASHTO Innovative Finance Web Site:http://www.transportation-finance.org/

FHWA Office of Innovative Program Delivery:http://www.fhwa.dot.gov/ipd/

FHWA PPP Homepage: http://www.fhwa.dot.gov/PPP/ Public Works Financing Newsletter:

http://pwfinance.net US DOT Report to Congress on Costs, Benefits and Efficiencies of PPPs

for Fixed Guideway Capital Projects, available from FTA:

http://www.fta.dot.gov/documents/Costs_Benefits_Efficiencies_of_Public-Private_Partnerships.pdf

Contact: Yuval Cohen at [email protected]

Alternative Delivery Methods for Infrastructure

www.5CountyStudy.org

Five-County Study Innovative Financing / Delivery Workshop

March 4, 2010

Joseph J. Erskine, Deputy Secretary- Finance & Administration

Kansas Department of TransportationT WORKS TRANSPORTATION WORKS FOR KANSAS

Jobs Safety Economic Development

Agenda

• Discussion of Long Range Transportation

Plan and TLINK Process

• Needs Identified and Delivery Techniques

• Funding and Financing Scenarios

Public Input

• Long Range Transportation Plan

• T-LINK

• More than 60 meetings held

• More than 1,000 Kansans participating

• Strong online presence: www.ktoc.net

Highways

• Enhanced Project Selection

– Link project selection to economic

development

– More frequent project selection to address

emerging opportunities

– This approach has been vetted with Kansans

Highways:

Fully Fund Preservation

1985

49%

Today

85%

As early as 2020

50%

Highways

• Increase funding for

capacity needs

• Implement Practical

Improvement

Approach

Local Roads

• Continued funding under the Special City County Highway Fund & Sustainable Priority Network Concept

• Fund Exchange Program– Moving forward

Transit

• Regional approach to improve rural

services & efficiency

• Revised rural & urban funding formulas

• Create a commuter corridor transit

funding program

Rail

• Expand program to

allow local govts.,

shippers & industrial

parks to be eligible

• Increase funding

Before After

Aviation

• Strategic approach to

improve air

ambulance

coverage & enhance

economic

development

• Increase funding

Multimodal Economic

Development Program

• Fund at $20 million

• Project decisions made on continuous

cycle

• Opens program to other modes

Funding & Finance

• T-LINK Recommended Program Size

• Preservation Gap for first 3 years (assuming delayed

program)

• Cash Flow/Debt Management Strategy to fill 3

year Preservation Gap

• T-EDL (Transportation - Economic Development

Loans)

• Tolling Considerations

• Funding Scenarios

Program Size Over 10 years

• Preservation- $4.6 Billion

• Modernization- $430 Million

• Expansion/Capacity- $3.6 Billion

• Additional Modal Support- $240 Million

• Additional Local Support- $645 Million

When All Added to Existing Programs

(approx.) $10 Billion over 10 Years

Funding Gap

$5.7 Billion over 10 Years

Preservation Gap

$250 Million Gap(Aggregate for FY 2011-2013)

• Amount required to maintain current system condition

• Does not include any future transfers from SHF to SGF

• Based on assumption of steady federal funding and current

state revenue projections

• Addresses preservation-only spending- i.e., no new

construction (modernization, expansion, modes,

local support, etc.)

Cash Flow/Debt Management

Strategies

• 18% Debt Service Cap

• Build America Bond Program

– To maximize benefit, requires authority to issue 25 year bonds

– Part of ARRA Program (program expires end CY 2010)

– 35% federal interest payment subsidy

– Use of a $300MM BAB creates approx. $20 Million debt

service savings to Kansas with 25 year bond issue

– Over $60 Billion BAB’s have been issued nationwide

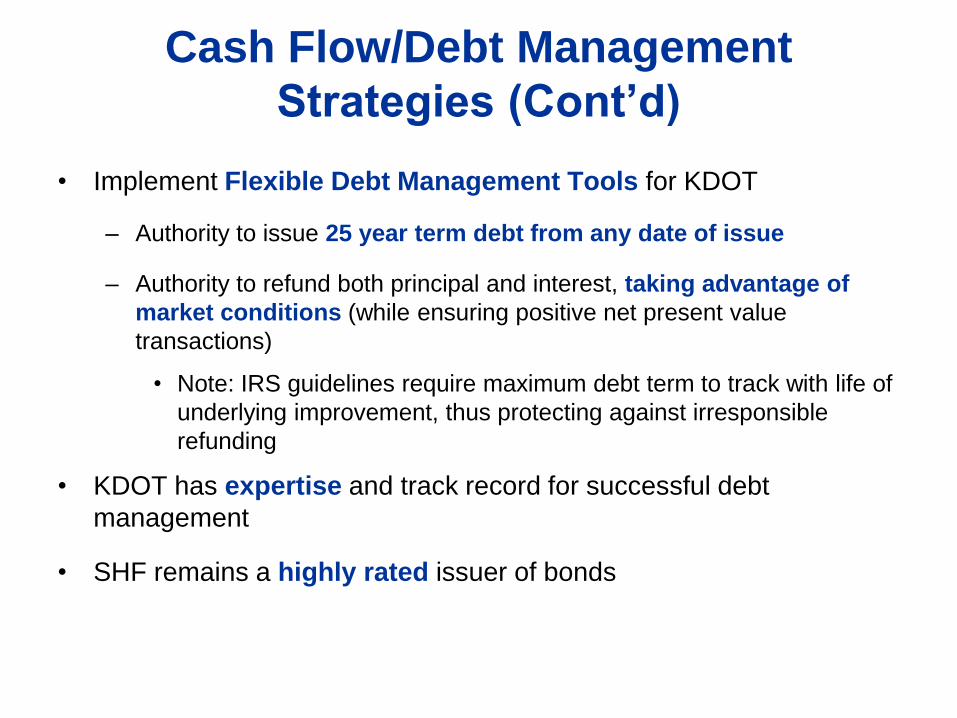

Cash Flow/Debt Management

Strategies (Cont’d)

• Implement Flexible Debt Management Tools for KDOT

– Authority to issue 25 year term debt from any date of issue

– Authority to refund both principal and interest, taking advantage of

market conditions (while ensuring positive net present value

transactions)

• Note: IRS guidelines require maximum debt term to track with life of

underlying improvement, thus protecting against irresponsible

refunding

• KDOT has expertise and track record for successful debt

management

• SHF remains a highly rated issuer of bonds

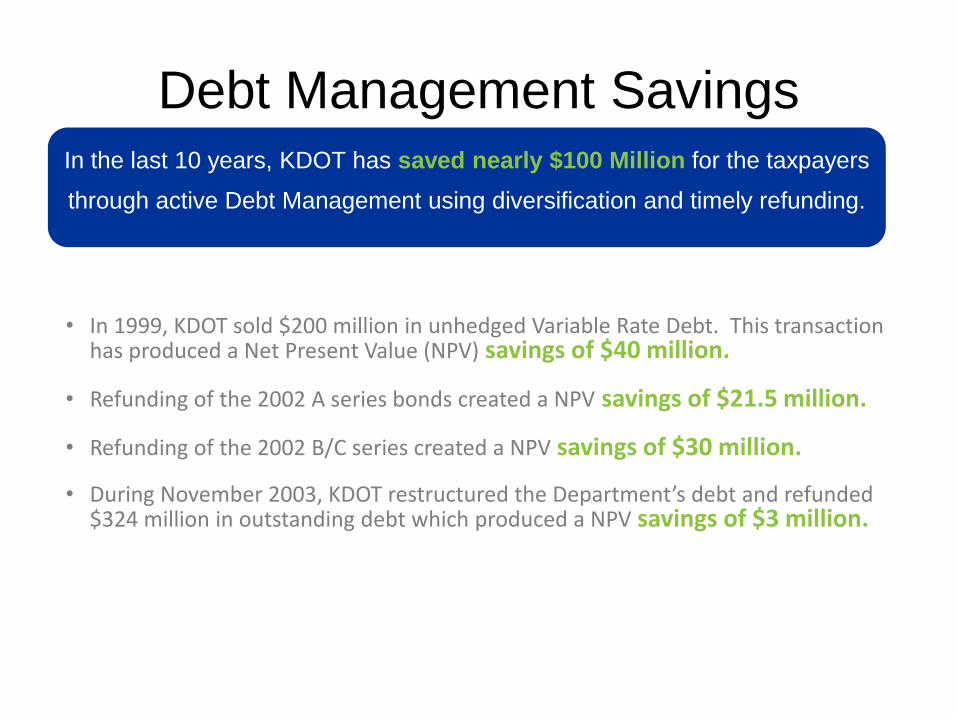

Debt Management SavingsIn the last 10 years, KDOT has saved nearly $100 Million for the taxpayers

through active Debt Management using diversification and timely refunding.

• In 1999, KDOT sold $200 million in unhedged Variable Rate Debt. This transaction has produced a Net Present Value (NPV) savings of $40 million.

• Refunding of the 2002 A series bonds created a NPV savings of $21.5 million.

• Refunding of the 2002 B/C series created a NPV savings of $30 million.

• During November 2003, KDOT restructured the Department’s debt and refunded $324 million in outstanding debt which produced a NPV savings of $3 million.

Transportation – Economic

Development Loans (T-EDL)(TLINK Executive Summary Report-January 2009)

To open financing options for local communities, allow the

Secretary of transportation to review transportation-related

economic development opportunities and authorize the use of

debt financing with repayment streams flowing from the

development revenue.

T-LINK recognized that communities –even growing communities –struggle to

fund improvements to serve new development. Current financing options

are difficult and cumbersome for communities to use. Therefore, T-LINK

recommends combining into a single piece of legislation approaches similar

to the economic development and transportation specific elements found in

STAR Bonds, Transportation Development Districts (TDD’s) and Tax

Increment Financing (TIF).

Transportation – Economic

Development Loans (T-EDL)• Administered through the Transportation Revolving Fund (TRF)

• Loans for local governments to fund transportation improvements to serve economic development

• Authorizes the SHF to bridge the debt service gap between construction and when new, incremental revenues begin to flow

• Authorize revenues from CIDs, TDDs, TIFs, in addition to other pledged sources, to service the T-EDL loan payments

• Feasibility Study Required

• Projects Approved on Project by Project Basis by Secretary of Transportation, with consultation from Secretaries of Commerce and Revenue

TollingT-LINK Positions:

• Kansas should consider toll financing

where practical;

• Any new toll revenues should be used forroads and highways;

• Tolling practices should not require 100% of costs to be covered by tolling revenue.

Scenarios Sales Tax on Motor Fuel

Delayed Program beginning

1/1/2013

Motor Fuel Tax -5¢

Indexing Motor Fuel Tax NO

Car Registration $20

Truck Registration $100

Sales Tax on Fuel YES

Policy Revenue Enhancements YES

Bonds Issued $2.0B

KDOT New Revenue $4.0B

% of T-LINK Gap Filled 70%

SCCHF Net Difference -$235M

City and County Sales Tax on Fuel Revenue $619M

City and County New Revenue Total $384M

Total New Revenue $4.4B

Scenarios Sales Tax on Motor Fuel

Delayed Program beginning

1/1/2013

Increase & Indexing of Motor

Fuel Tax Delayed Program

beginning 1/1/2013

Motor Fuel Tax -5¢ 7¢

Indexing Motor Fuel Tax NO YES (+8.2¢)

Car Registration $20 $20

Truck Registration $100 $100

Sales Tax on Fuel YES NO

Policy Revenue Enhancements YES YES

Bonds Issued $2.0B $2.0B

KDOT New Revenue $4.0B $3.6B

% of T-LINK Gap Filled 70% 63%

SCCHF Net Difference -$235M $139M

City and County Sales Tax on Fuel Revenue $619M N/A

City and County New Revenue Total $384M $139M

Total New Revenue $4.4B $3.73B

Questions?

Senate Transportation Committee

Scheduled to open hearings next week,

(approx.) Wednesday, March 10th.

Alternative Delivery Methods for Infrastructure

www.5CountyStudy.org

Transportation Workshop on Innovative Project DeliveryMarch 4, 2010

Missouri Department

of Transportation

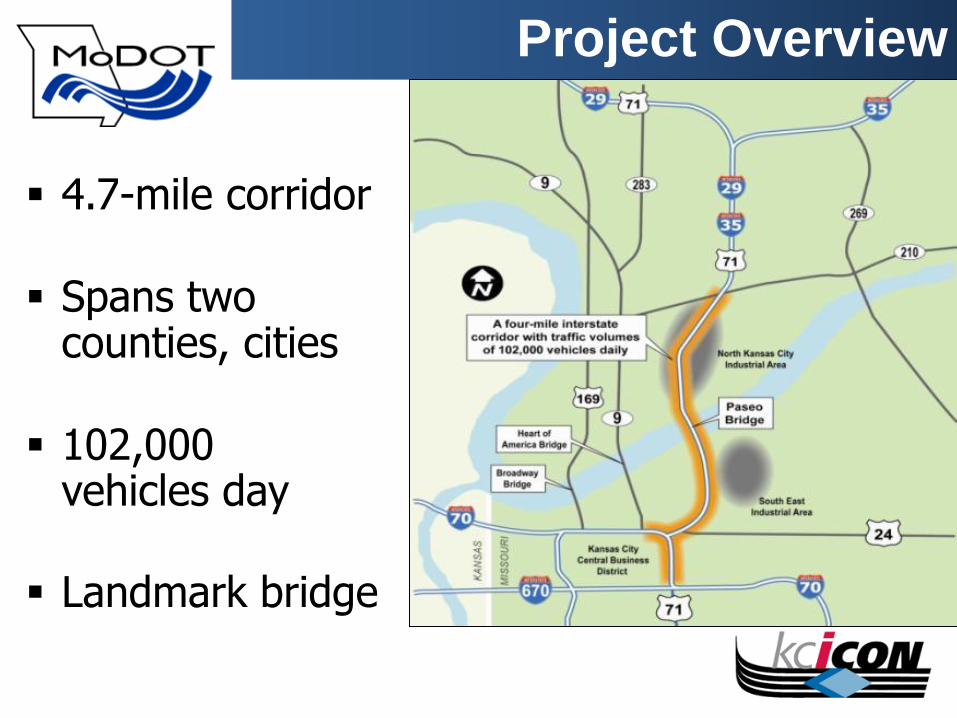

Project Overview

KC

4.7-mile corridor

Spans two counties, cities

102,000vehicles day

Landmark bridge

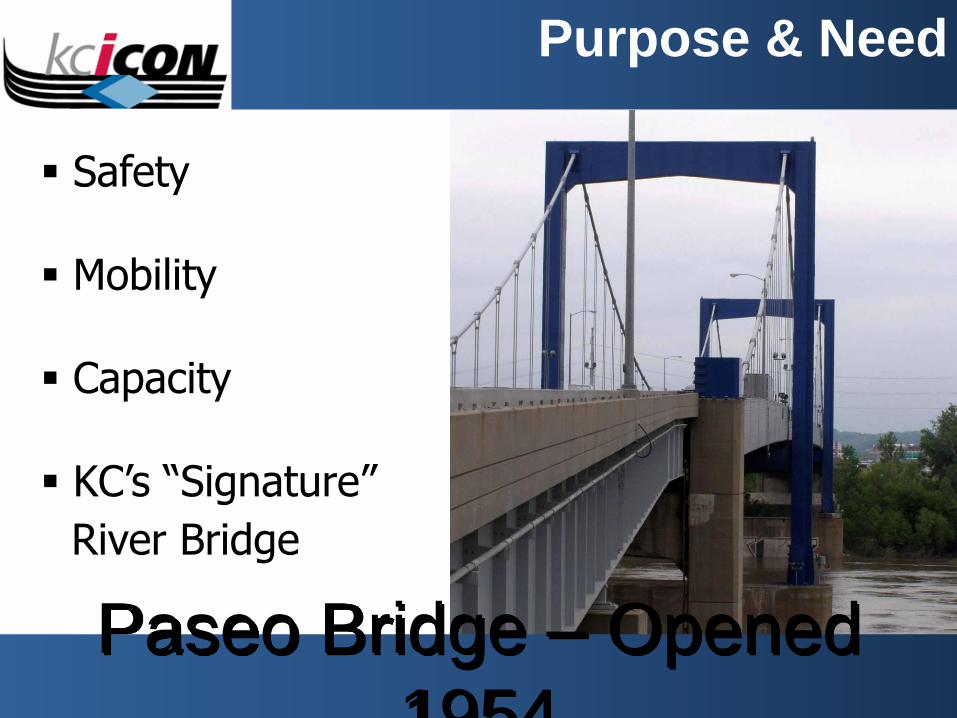

Purpose & Need

Safety

Mobility

Capacity

KC’s “Signature”

River Bridge

Paseo Bridge – Opened

1954

NE corner Downtown KC

Dozens of railroad tracks

Mobility vs. Aesthetics

Approach / New Model

Design-Build

Fixed Price/

Best Value

“Be Bold”

“WOW”

Approach / New Model

Go “unreasonably” fast

Maximum Flexibility

Small, empowered core team

….and, complete NEPA (EIS)

12 members

Named by

local leaders

Regular meetings

Local priorities

Community Advisory Group

Project Goals

Meet $245 million budget

Build landmark bridge

Improve safety, mobility,

aesthetics, capacity

Engage stakeholders

Beat October 2011 deadline

Scoring System

Criterion Points

Project Definition 30

Landmark Missouri River Bridge(s) – Aesthetics 20

Landmark Missouri River Bridge(s) – Durability 10

Method of Handling Traffic (MOT) 15

Completion Schedule 10

Disadvantaged Businesses/Workforce Development 10

Public Information 5

TOTAL 100

8 new bridges 5 bridges widened20 MSE walls 5 Noise walls5 Interchanges 4+ mi of Interstate

Design & FAA Challenge

316 ft.

above

river’s

surfac

e

Co-location & Partnering

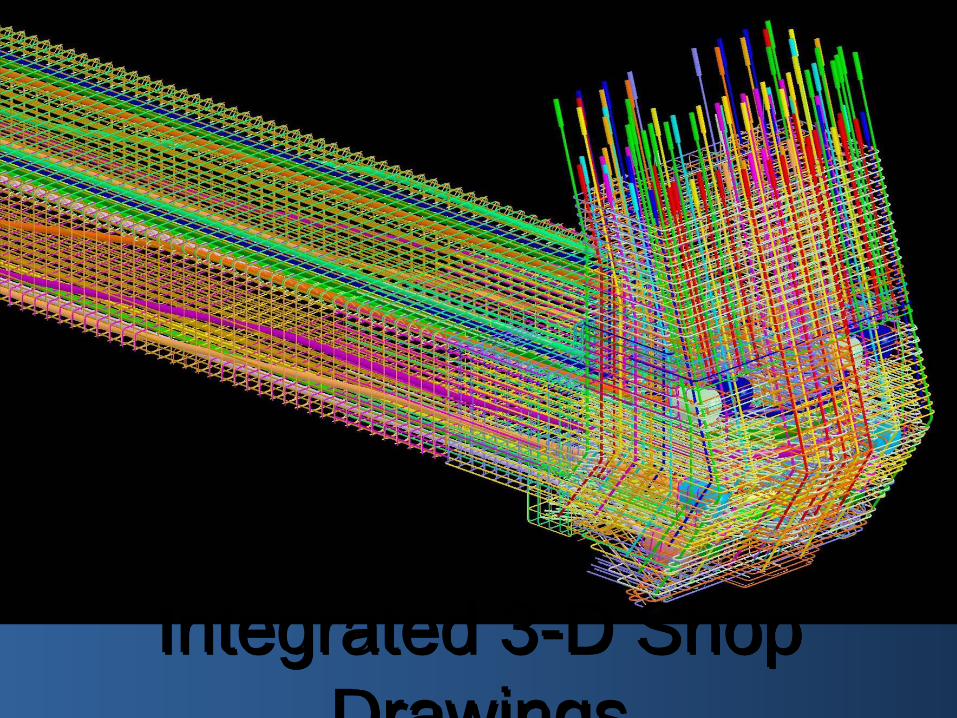

Integrated 3-D Shop

Drawings

#@&*%

Rebar in the “knuckle”

Three Web cams &

“Winter work”

July 2011 - open

66% complete

So far, so good…

www.kcicon.com

Alternative Delivery Methods for Infrastructure

www.5CountyStudy.org

Public-Private Partnerships (P3)in

Transportation Development

5-County Innovative Financing Study

March 3, 2010

Agenda

• Transporation Development Districts (TDD)

• Community Improvement Districts (CID)

• Tax Increment Financing (TIF)

• Questions

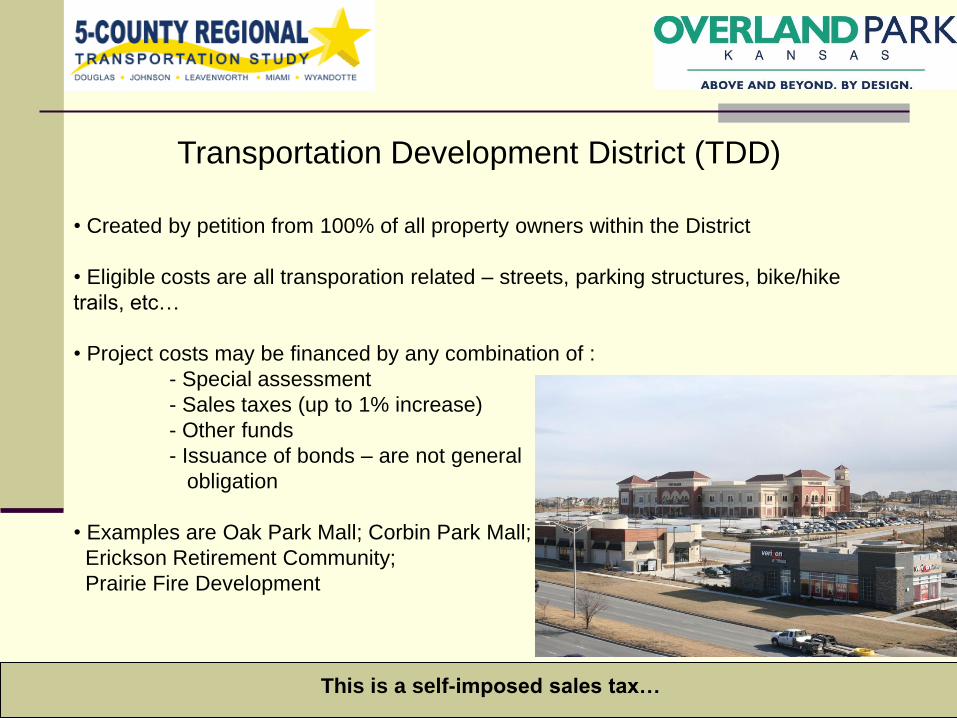

Transportation Development District (TDD)

• Created by petition from 100% of all property owners within the District

• Eligible costs are all transporation related – streets, parking structures, bike/hike

trails, etc…

• Project costs may be financed by any combination of :

- Special assessment

- Sales taxes (up to 1% increase)

- Other funds

- Issuance of bonds – are not general

obligation

• Examples are Oak Park Mall; Corbin Park Mall;

Erickson Retirement Community;

Prairie Fire Development

This is a self-imposed sales tax…

Community Improvement District (CDD)

• Created by petition:

- 100% of all property owners within the District if special assessments are

used

- 55% of all property owners or 55% of assessed value

• Eligible costs are broad – transporation, utilities, facilities, operations, etc.

• Project costs may be financed by any combination of :

Special assessment

Sales taxes (up to 2% increase) – self imposed

Other funds

Issuance of bonds – special obligation or general obligation

• Examples ….none yet

The way of the public-private partnership in the future …

Tax Increment Financing (TIF)

• “Eligible” Areas – must comply with State statues

- Blighted Area

- Conservation Area

- Enterprise Zone

- Historic Theater

- Major Commercial Entertainment

and Tourism Area

- Bioscience Development Area

- Major Tourism Area – NASCAR Race

Track Project Only

Eligibility is determined in coordination with the City’s Bond Counsel

• Requires creation of a redevelopment district following a public hearing

- Can be vetoed by County or School District

• Requires approval of a redevelopment project area plan

- Financial Feasibility Study

- Relocation Assistance Plan

• Eligible costs are usually site plan costs – no buildings

- Utilities, streets, stormwater, etc…

• Paid as either pay-as-you-go proceeds or issuance of bonds

- Bonds can be special obligation or full faith and credit tax

increment bonds

• Paid for by incremental property tax and/or sales tax

• City may use eminent domain in all areas except “conservation areas”

Tax Increment Financing (TIF)

Tax Increment Financing (TIF)

• Example:

- Market Lofts …$1.4M out of total project cost of $12M

* underground parking

* utilities

* sidewalks

* alleyway

Tax Increment Financing (TIF)

Example:

Cherokee South …$3M our of total project cost of $21M

* stormwater

* street improvements

* sidewalks

* parking lot improvements

Some Considerations for Council

• Cost of the project – funding; amount of equity invested; “but-for” analysis

• Experience and financial stability of the developer

• Viability and quality of the project – tenant activity; quality of tenants;

economic competition in the area

• Performance guarantees

• Liability to the City – how is the development agreement structured?

Questions?

Alternative Delivery Methods

for Infrastructure

Team Brainstorming Session

Lawrence / Douglas County MPO