Embed Size (px)

Citation preview

InnovationsinMSMEFinancing:CreatingCreditHistory,aPathway?AnishaSinghandRupikaSingh,IFMRLEAD

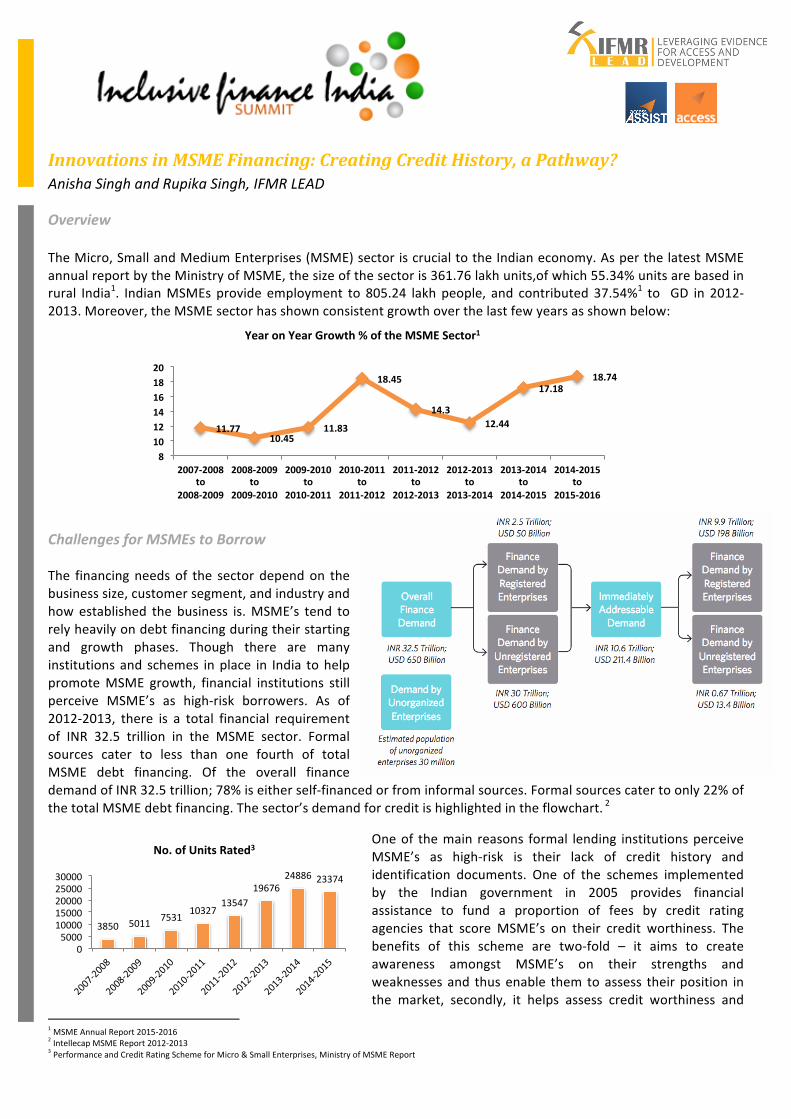

OverviewTheMicro,SmallandMediumEnterprises(MSME)sectoriscrucialtotheIndianeconomy.AsperthelatestMSMEannualreportbytheMinistryofMSME,thesizeofthesectoris361.76lakhunits,ofwhich55.34%unitsarebasedinrural India1. IndianMSMEsprovide employment to 805.24 lakhpeople, and contributed 37.54%1 to GD in 2012-2013.Moreover,theMSMEsectorhasshownconsistentgrowthoverthelastfewyearsasshownbelow:

ChallengesforMSMEstoBorrowThe financingneedsof the sectordependon thebusinesssize,customersegment,andindustryandhowestablished the business is.MSME’s tend torelyheavilyondebtfinancingduringtheirstartingand growth phases. Though there are manyinstitutionsand schemes inplace in India tohelppromoteMSME growth, financial institutions stillperceive MSME’s as high-risk borrowers. As of2012-2013, there is a total financial requirementof INR 32.5 trillion in the MSME sector. Formalsources cater to less than one fourth of totalMSME debt financing. Of the overall financedemandofINR32.5trillion;78%iseitherself-financedorfrominformalsources.Formalsourcescatertoonly22%ofthetotalMSMEdebtfinancing.Thesector’sdemandforcreditishighlightedintheflowchart.2

Oneof themain reasons formal lending institutionsperceiveMSME’s as high-risk is their lack of credit history andidentification documents. One of the schemes implementedby the Indian government in 2005 provides financialassistance to fund a proportion of fees by credit ratingagencies that scoreMSME’s on their credit worthiness. Thebenefits of this scheme are two-fold – it aims to createawareness amongst MSME’s on their strengths andweaknessesand thusenable themtoassess theirposition inthe market, secondly, it helps assess credit worthiness and

1MSMEAnnualReport2015-20162IntellecapMSMEReport2012-20133PerformanceandCreditRatingSchemeforMicro&SmallEnterprises,MinistryofMSMEReport

11.7710.45

11.83

18.45

14.312.44

17.1818.74

8101214161820

2007-2008to

2008-2009

2008-2009to

2009-2010

2009-2010to

2010-2011

2010-2011to

2011-2012

2011-2012to

2012-2013

2012-2013to

2013-2014

2013-2014to

2014-2015

2014-2015to

2015-2016

YearonYearGrowth%oftheMSMESector1

3850 5011 753110327

1354719676

24886 23374

050001000015000200002500030000

No.ofUnitsRated3

recognize how to improve on this. This facilitates them to access credit at cheaper rates and on easier terms byincreasingtheiracceptabilitywith banks, financial institutions,customers/buyersandvendors. In theperiod from2005-2015, over 1.10 lakh MSME units3 have been rated under this scheme. As for the lack of identificationdocuments,therehasbeenapushbythegovernmentforMSME’storegisterthemselvesundertheUdyogAadhaarscheme.AsofDecember2016,over57lakhunitMSME’shaveregistered4. TechnologyInnovationsinMSMEFinancing

TheuseofmobileInternetandsmartphoneshasseentremendousyearonyeargrowthinthepastcoupleofyears.Yet,thelevelofpenetrationislow,especiallyinruralareas.Itisestimatedthatonlyabout9%oftheruralpopulationhas access tomobile Internet, whereas, 53% of the urban population does5. TheMSME report indicates 45% ofMSMEunitsareinurbanareas.Thisprovidealargenumberofcustomerswhocanbetargetedintheshort-runbydigitalwallets,datacapturedviasmartphones,technologyinnovationsinMSMEfinancingwhichresultfromtie-upsbetweenlendinginstitutionsandtechnologyproviders.

Whileborrowers inurbanareasmaybemore favourablyplaced toaccess these innovations in theshort run, it isprojectedthatby2020,315millionindividualsinruralIndiawillhaveaccesstomobileInternetascomparedtothecurrent 120million6. Thus, as smart-phone andmobile Internet penetration increases, rural Indiawill be able togreatlybenefitfromtheseinnovations.

3PerformanceandCreditRatingSchemeforMicro&SmallEnterprises,MinistryofMSMEReport

4http://udyogaadhaar.gov.in/UA/UdyogAadhar-New.aspx5MobileInternetinIndia,20156InternetusagepicksupinruralIndia,LiveMint,Aug2016

Digitalfootprintbasedlending• Lenddo,acreditassessmentfinancialtechnologycompanythatusessmartphonetrackingisexpandingitsrafngservicestoincludemicrofinanceinsftufons(MFIs)inIndia.ThiswillcoverindividualMFIcustomerswholiveinurbanareasandhaveanandroidphone.AsanMFIofficeruploadsthecustomer’sinformafon,thecustomerreceivesatextwithaloanapplicafonlink.Oncethecustomerdownloadstheapplicafonandagreestosharedata,Lenndoanalysesthecustomerscontacts,SMS’s,callhistory,andbrowsingbehaviourtogivethecustomeracreditrafngwhichisthensharedwiththeMFI.

AlternateDatatoevalulatecreditworthiness• AsinIndiaorganizedlendingisavailableonlytoaluckyfewmainlythosewithhighCIBILscores,IndiaLendspromisestochangethisbyusingvariousrelevantdatapointssuchasbanktransacfons,uflitypayments,etc.tobuildacomprehensivecreditscore,evenforthosewhohavenopreviouslendingorcreditcardhistory.Thishelpsborrowerswithnopreviousaccesstoformallendingtoaccesstheformalsystem.

OvercominglackofKYCdocuments• SwadhaarFinAccesshasfacilitatedthelinkbetweenAxisBankandAirtelMoneywhereincustomerscanperformavarietyoffinancialtransacfons–deposits,withdrawals,andloanrepaymentsthroughtheAirtelMoneywalletontheirsmartphone.TheKYCnormsonthisproductaremorelaxthanthosewithcommercialbanks.ThisisespeciallyusefulforMSME’sintheunorganizedsectorthatdonothaveproperKYCdocumentafon.

Flexiblerepaymentterms• NeoGrowthfocusesonMSME’s,specificallymerchantsandretailers.ItusesaMerchantCashAdvance(MCA)modeltotargetMSME’swhereinitprovidescredittomerchantsinexchangeforanagreeduponpercentageoffuturesalesmadeviacreditcard/debitcard.TherepaymentoftheloandependsontheturnoveroftheMSME’sdailycredit/debitcardsales.Accordingtotheirreport,21.4%clientswereintroducedtotheformalcreditsystemforthefirstfme.