Embed Size (px)

Citation preview

Information Technology Functional Guide

12 CFR Part 370: Recordkeeping for Timely Deposit Insurance Determination

VERSION 1.0

April 2017

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

[Page intentionally left blank.]

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Contents

How to Read This Document ........................................................................................... 1

1 Introduction ................................................................................................................ 2

2 Overview ..................................................................................................................... 3 2.1 Background ............................................................................................................................................... 3 2.2 Key Concepts ........................................................................................................................................... 3 2.3 CI Failure Scenario .................................................................................................................................. 4 2.4 High-Level Process ................................................................................................................................. 6 2.5 Conceptual Systems Flow ...................................................................................................................... 8

3 Process Requirements .............................................................................................. 9 3.1 Deposit Insurance Determination .......................................................................................................... 9 3.2 Pending File (Input, Process, and Output) ......................................................................................... 13

4 Deposit Insurance Determination Requirements ................................................ 18 4.1 Initial Processing .................................................................................................................................... 18 4.2 Right and Capacity and Deposit Insurance Determination .............................................................. 19 4.3 Apply Funds ............................................................................................................................................ 42

5 Output File Generation Requirements .................................................................. 43 5.1 Output File Population – Customer File .............................................................................................. 43 5.2 Output File Population – Account File ................................................................................................ 44 5.3 Output File Population – Account Participant File............................................................................. 44 5.4 Output File Population – Pending File ................................................................................................ 45

6 Control Report Requirements ................................................................................ 46 6.1 Data Movement ...................................................................................................................................... 46 6.2 Data Quality ............................................................................................................................................ 47 6.3 Control Reports ...................................................................................................................................... 48

7 Summary Report Requirements ............................................................................ 49

8 Certification of Compliance .................................................................................... 50

Appendix A Explanation of Output File Generation Capabilities ............................ 51

Appendix B Explanation of Ownership Account Categories ................................... 61

Appendix C Use Cases .................................................................................................. 68

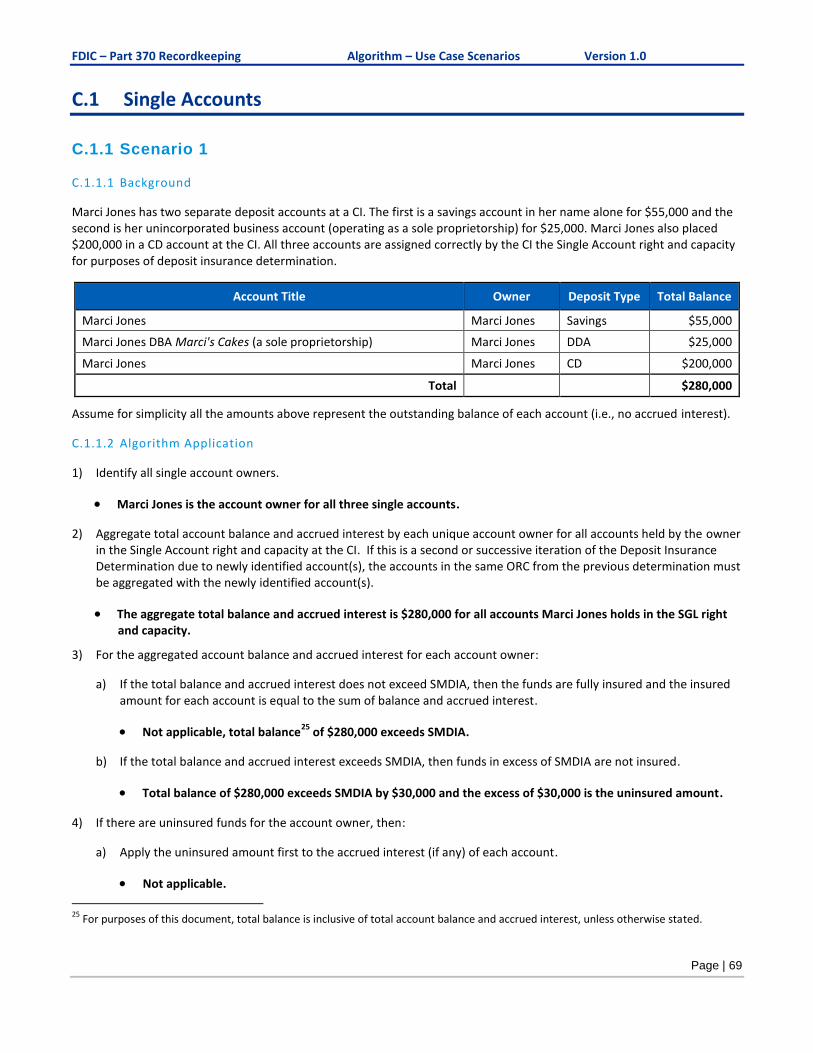

C.1 Single Accounts ................................................................................................... 69

C.1.1 Scenario 1 ............................................................................................................... 69 C.1.1.1 Background ................................................................................................................................... 69 C.1.1.2 Algorithm Application ................................................................................................................ 69 C.1.1.3 Outcome ........................................................................................................................................ 70

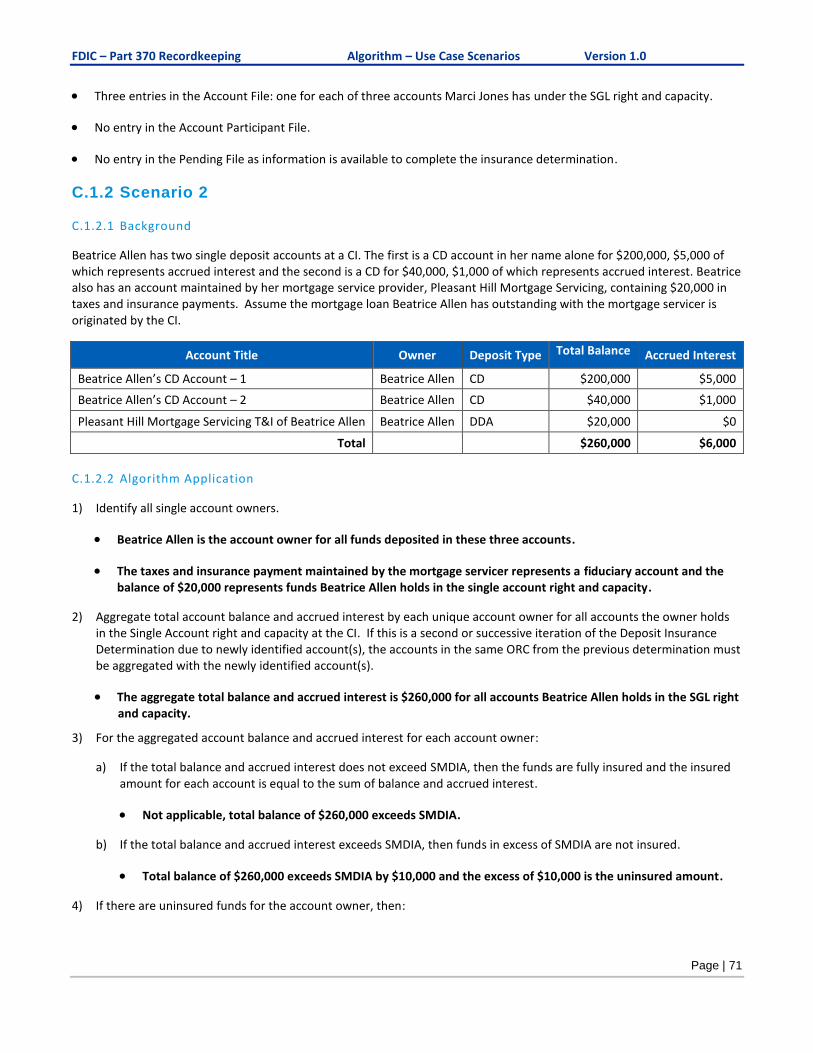

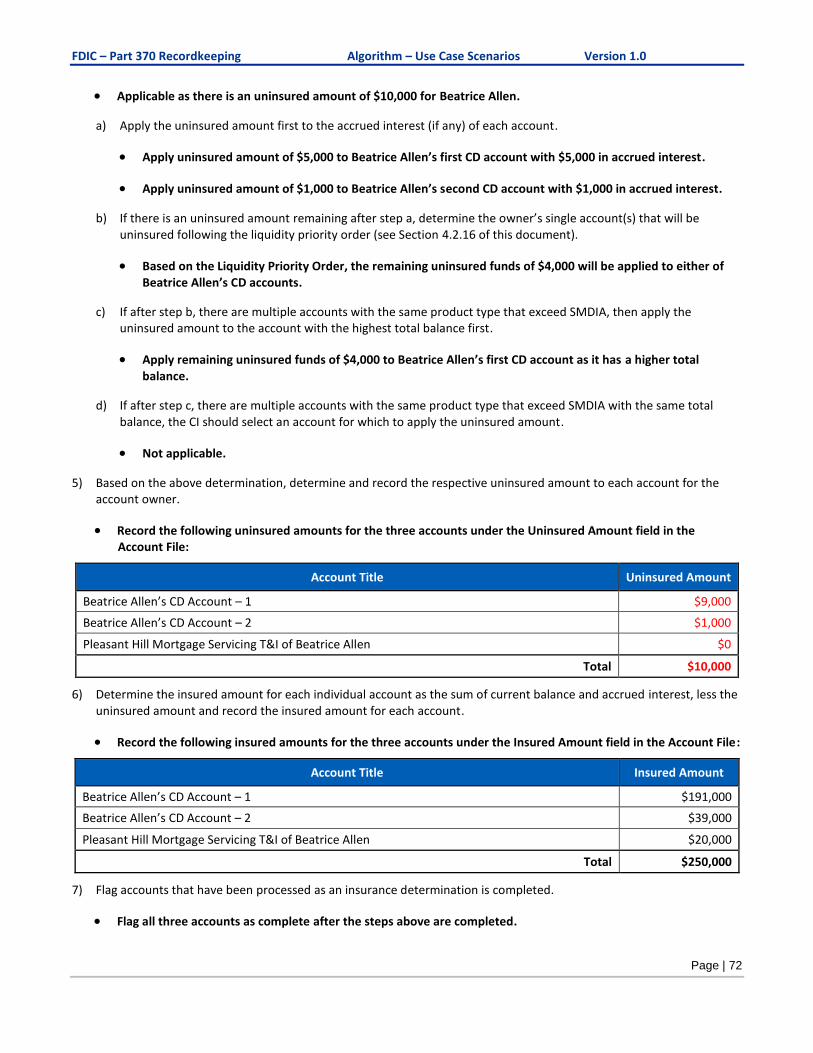

C.1.2 Scenario 2 ............................................................................................................... 71 C.1.2.1 Background ................................................................................................................................... 71 C.1.2.2 Algorithm Application ................................................................................................................ 71 C.1.2.3 Outcome ........................................................................................................................................ 73

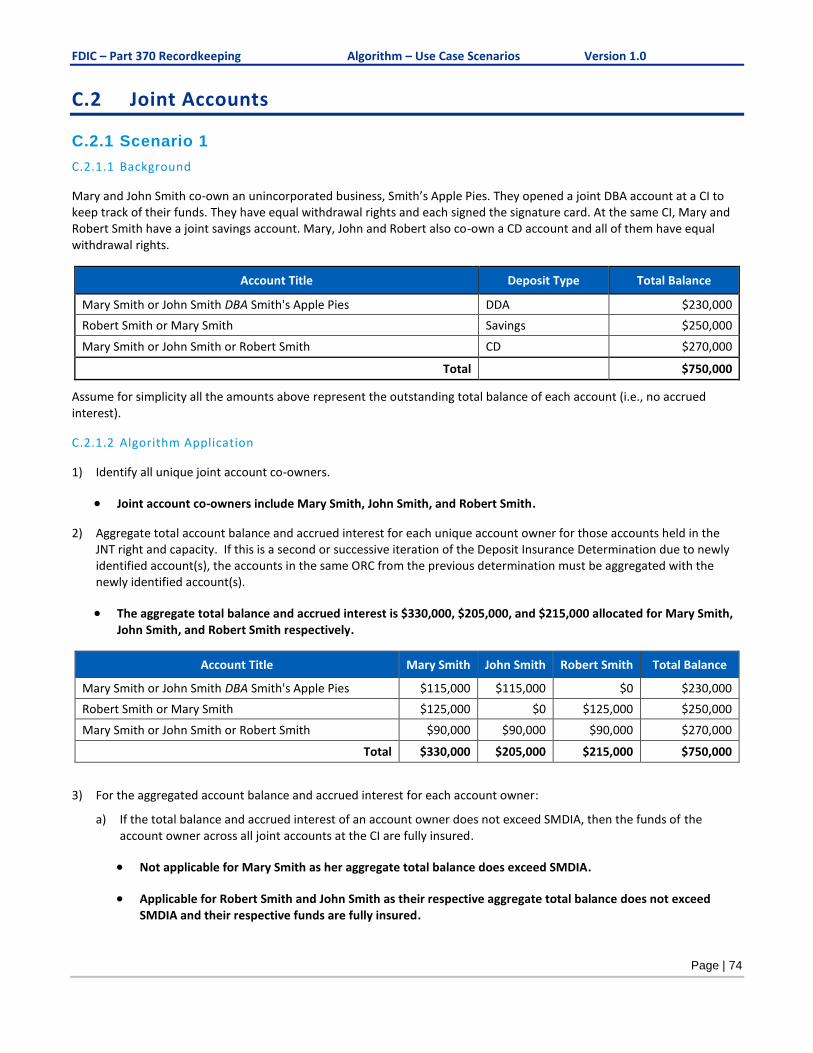

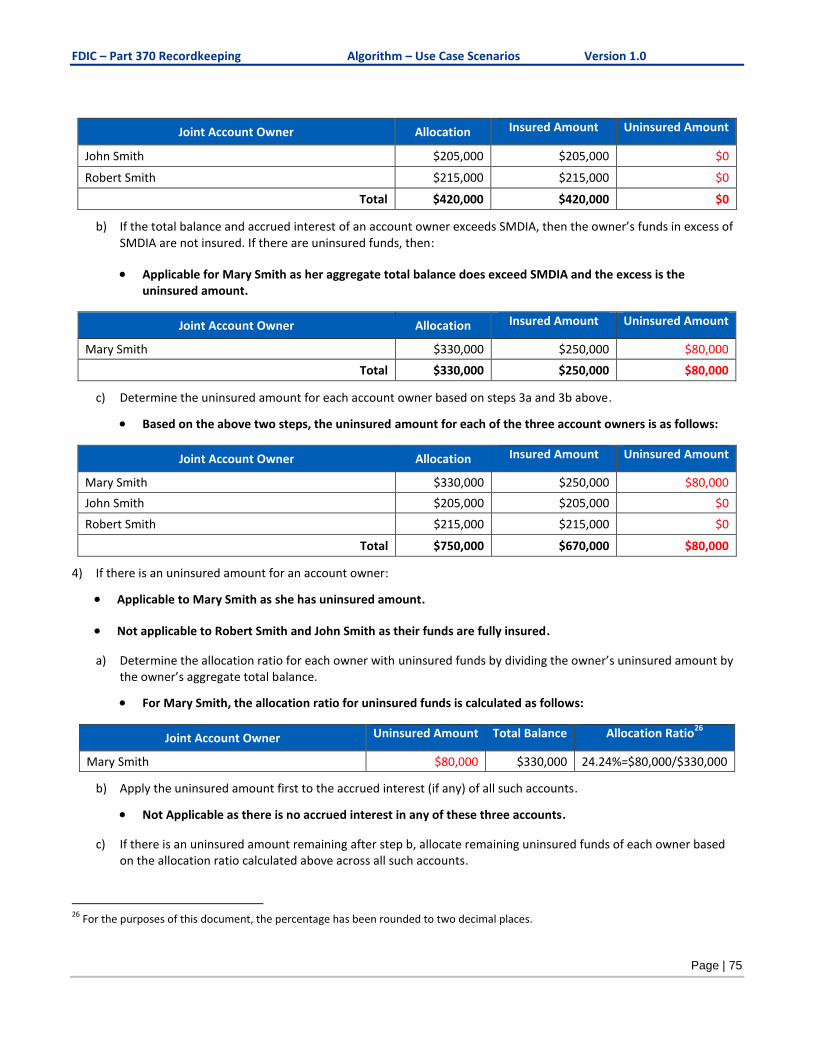

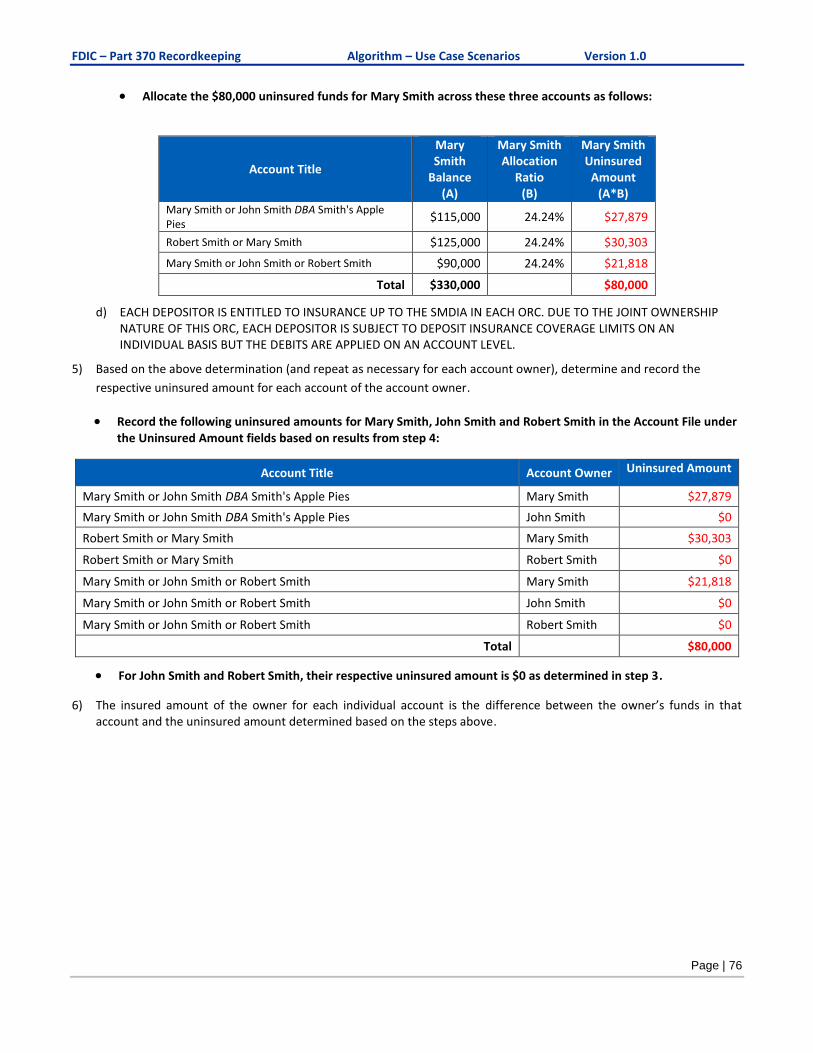

C.2 Joint Accounts ........................................................................................................ 74

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

C.2.1 Scenario 1 ............................................................................................................... 74 C.2.1.1 Background ................................................................................................................................... 74 C.2.1.2 Algorithm Application ................................................................................................................ 74 C.2.1.3 Outcome ........................................................................................................................................ 77

C.3 Revocable Trust Accounts ..................................................................................... 78

C.3.1 Scenario 1 ............................................................................................................... 78 C.3.1.1 Background ................................................................................................................................... 78 C.3.1.2 Algorithm Application ................................................................................................................ 78 C.3.1.3 Outcome ........................................................................................................................................ 82

C.3.2 Scenario 2 ............................................................................................................... 82 C.3.2.1 Background ................................................................................................................................... 82 C.3.2.2 Algorithm Application ................................................................................................................ 83 C.3.2.3 Outcome ........................................................................................................................................ 85

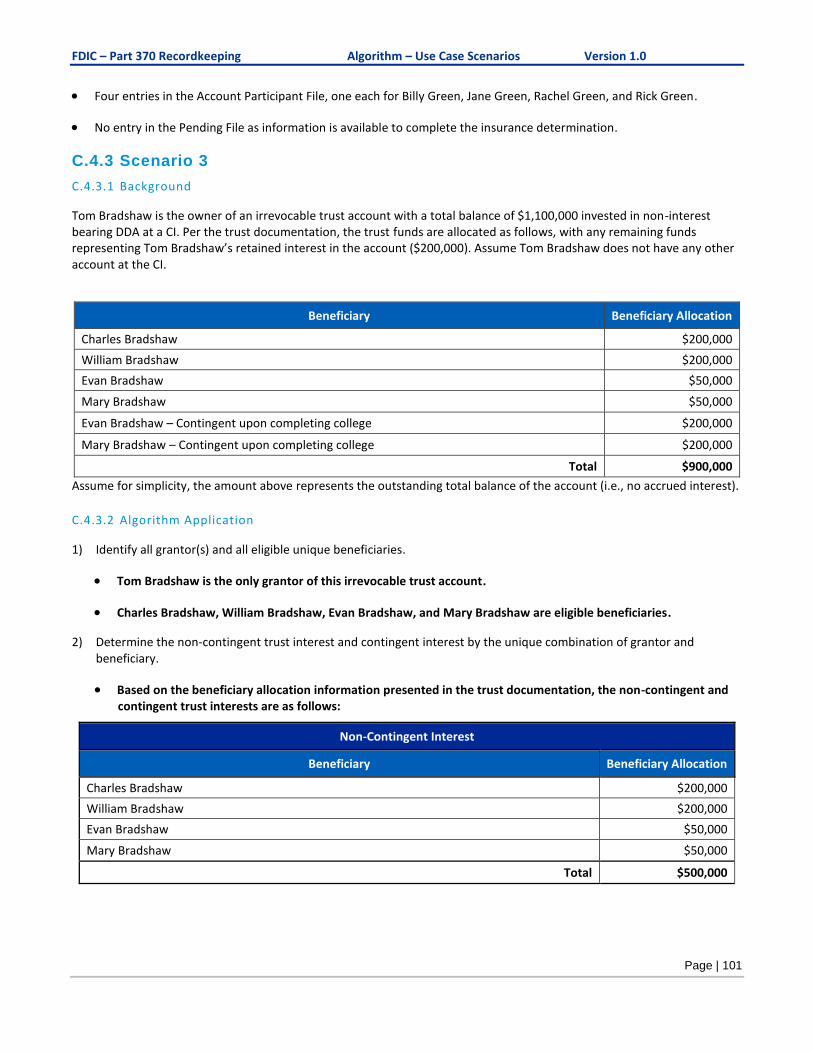

C.3.3 Scenario 3 ............................................................................................................... 86 C.3.3.1 Background ................................................................................................................................... 86 C.3.3.2 Algorithm Application ................................................................................................................ 86 C.3.3.3 Outcome ........................................................................................................................................ 90

C.3.4 Scenario 4 ............................................................................................................... 90 C.3.4.1 Background ................................................................................................................................... 90 C.3.4.2 Algorithm Application ................................................................................................................ 90 C.3.4.3 Outcome ........................................................................................................................................ 93

C.4 Irrevocable Trust Accounts .................................................................................. 94

C.4.1 Scenario 1 ............................................................................................................... 94 C.4.1.1 Background ................................................................................................................................... 94 C.4.1.2 Algorithm Application ................................................................................................................ 94 C.4.1.3 Outcome ........................................................................................................................................ 97

C.4.2 Scenario 2 ............................................................................................................... 97 C.4.2.1 Background ................................................................................................................................... 97 C.4.2.2 Algorithm Application ................................................................................................................ 97 C.4.2.3 Outcome ...................................................................................................................................... 100

C.4.3 Scenario 3 ............................................................................................................. 101 C.4.3.1 Background ................................................................................................................................. 101 C.4.3.2 Algorithm Application .............................................................................................................. 101 C.4.3.3 Outcome ...................................................................................................................................... 104

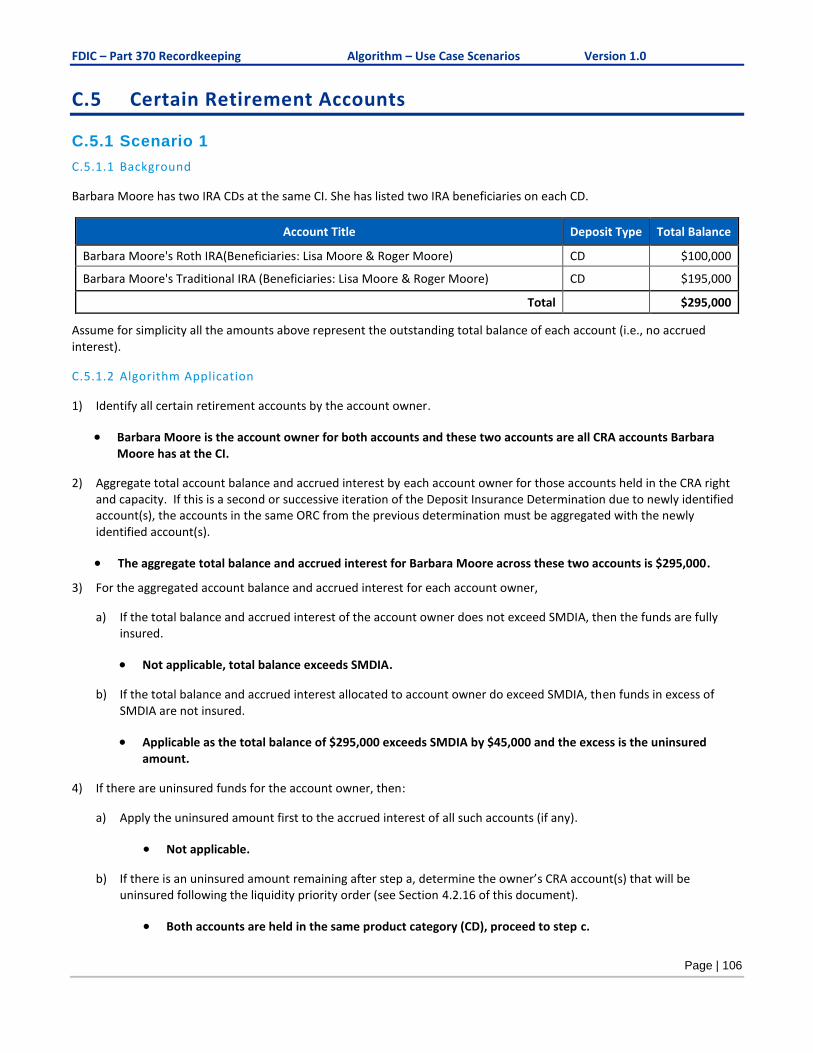

C.5 Certain Retirement Accounts .............................................................................. 106

C.5.1 Scenario 1 ............................................................................................................. 106 C.5.1.1 Background ................................................................................................................................. 106 C.5.1.2 Algorithm Application .............................................................................................................. 106 C.5.1.3 Outcome ...................................................................................................................................... 107

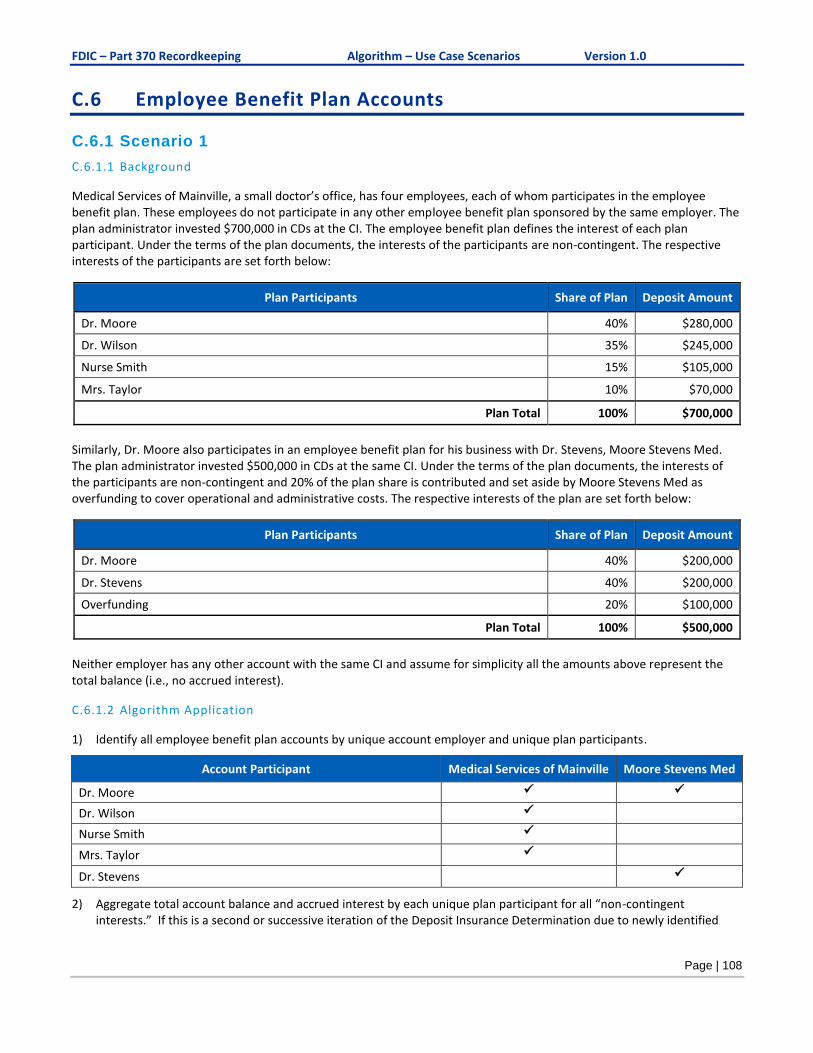

C.6 Employee Benefit Plan Accounts ....................................................................... 108

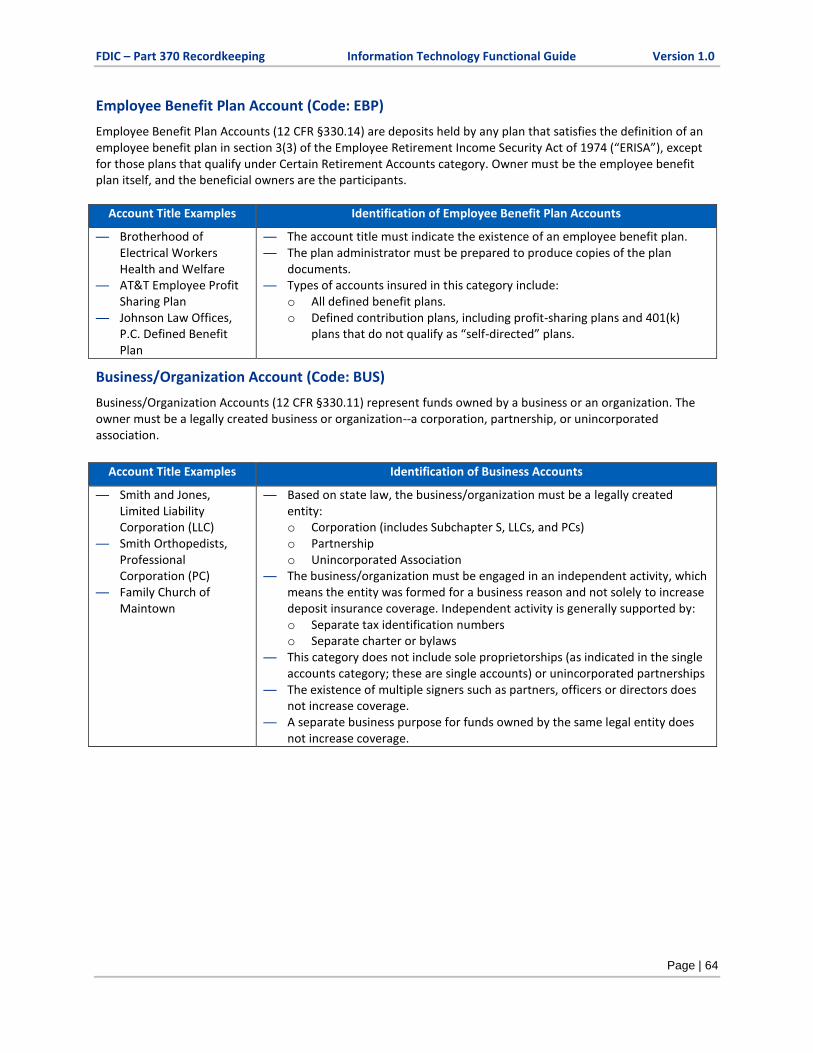

C.6.1 Scenario 1 ............................................................................................................. 108 C.6.1.1 Background ................................................................................................................................. 108 C.6.1.2 Algorithm Application .............................................................................................................. 108 C.6.1.3 Outcome ...................................................................................................................................... 111

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

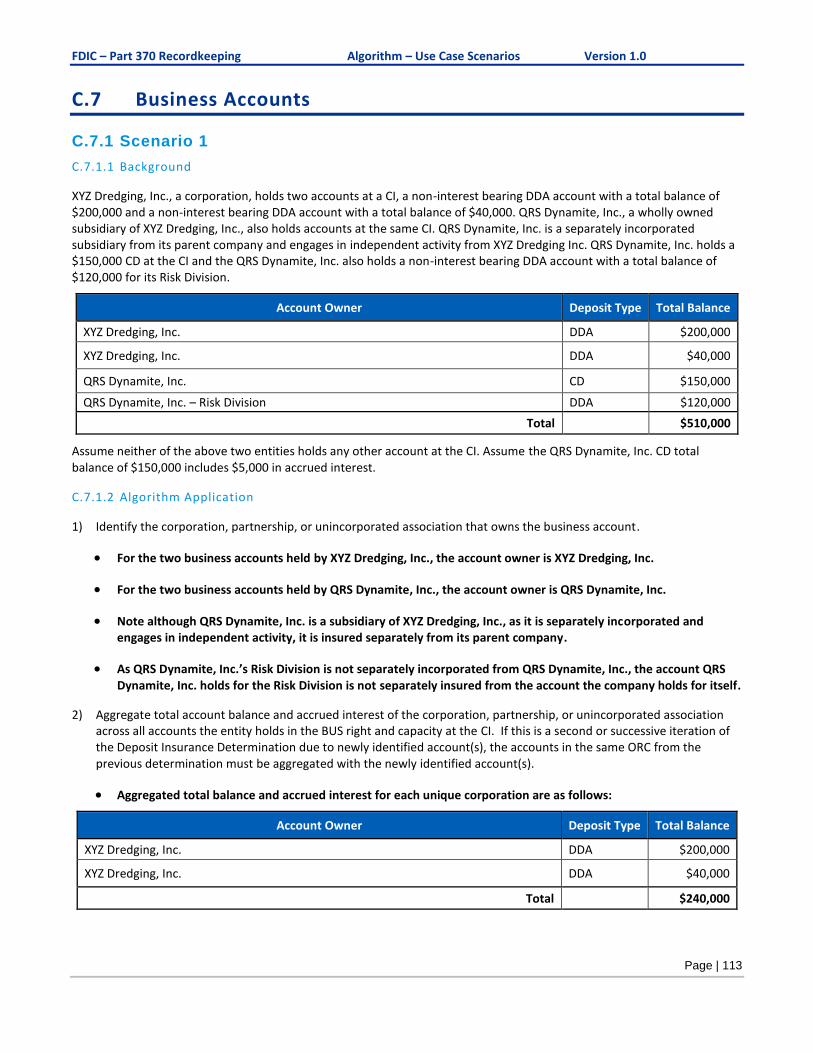

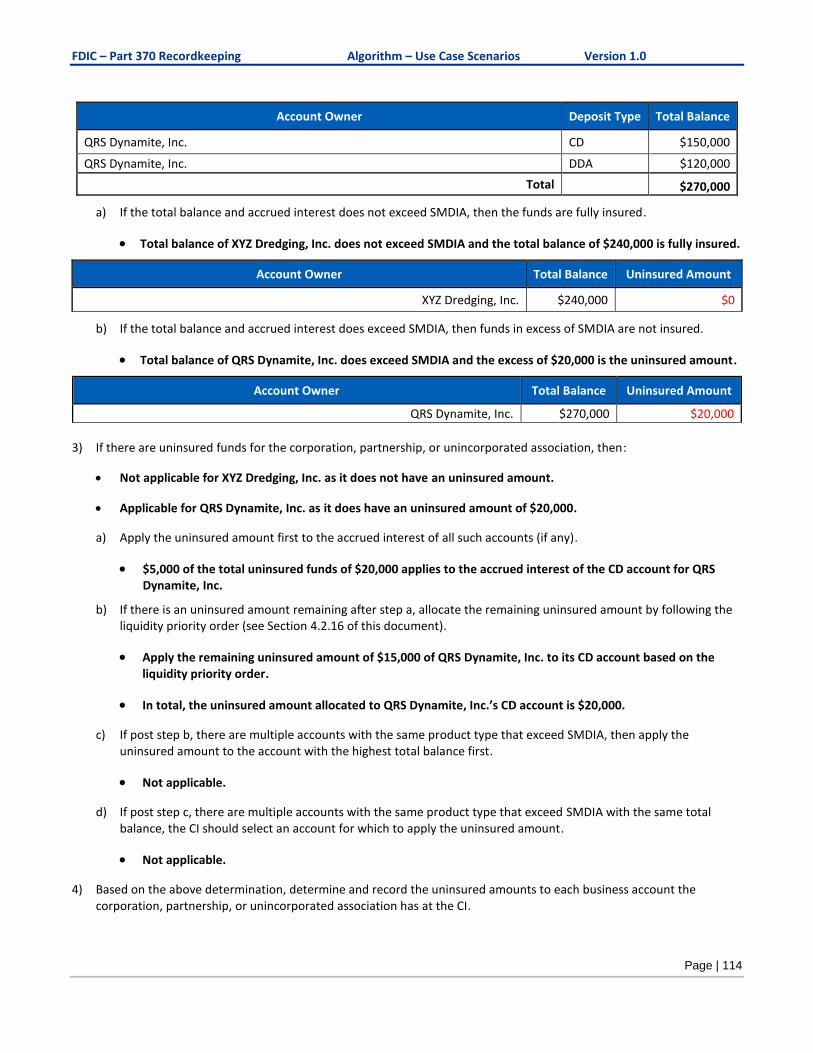

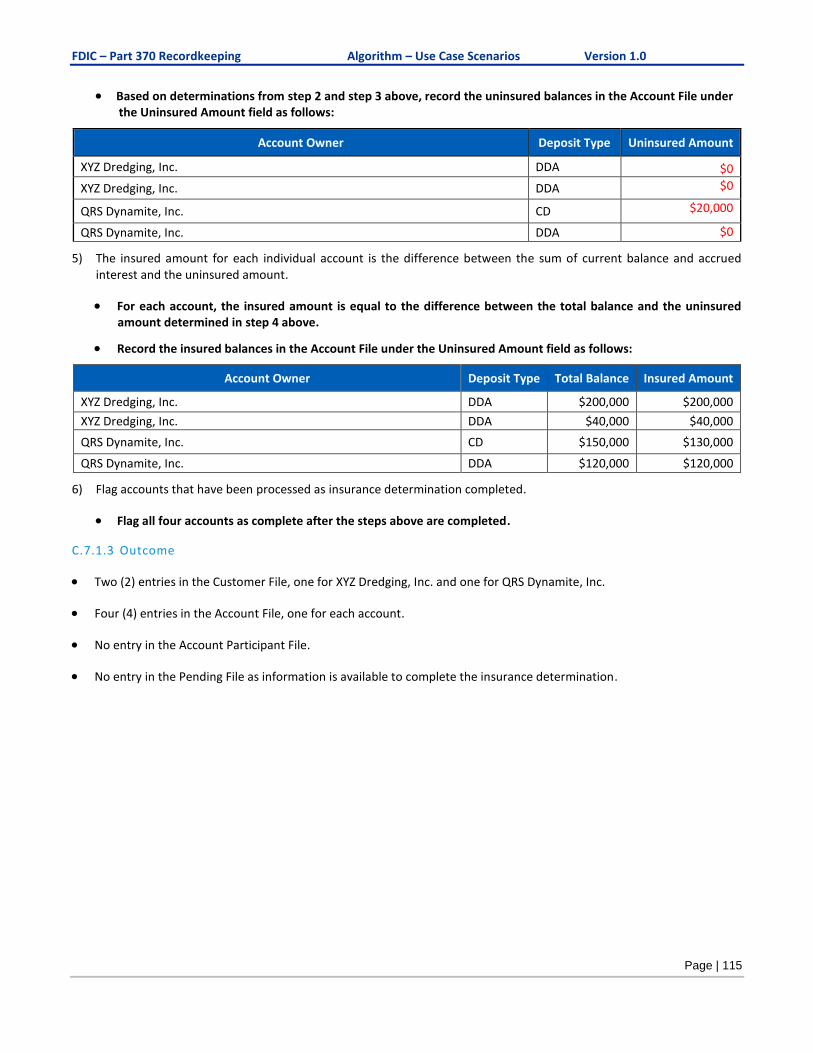

C.7 Business Accounts ............................................................................................... 113

C.7.1 Scenario 1 ............................................................................................................. 113 C.7.1.1 Background ................................................................................................................................. 113 C.7.1.2 Algorithm Application .............................................................................................................. 113 C.7.1.3 Outcome ...................................................................................................................................... 115

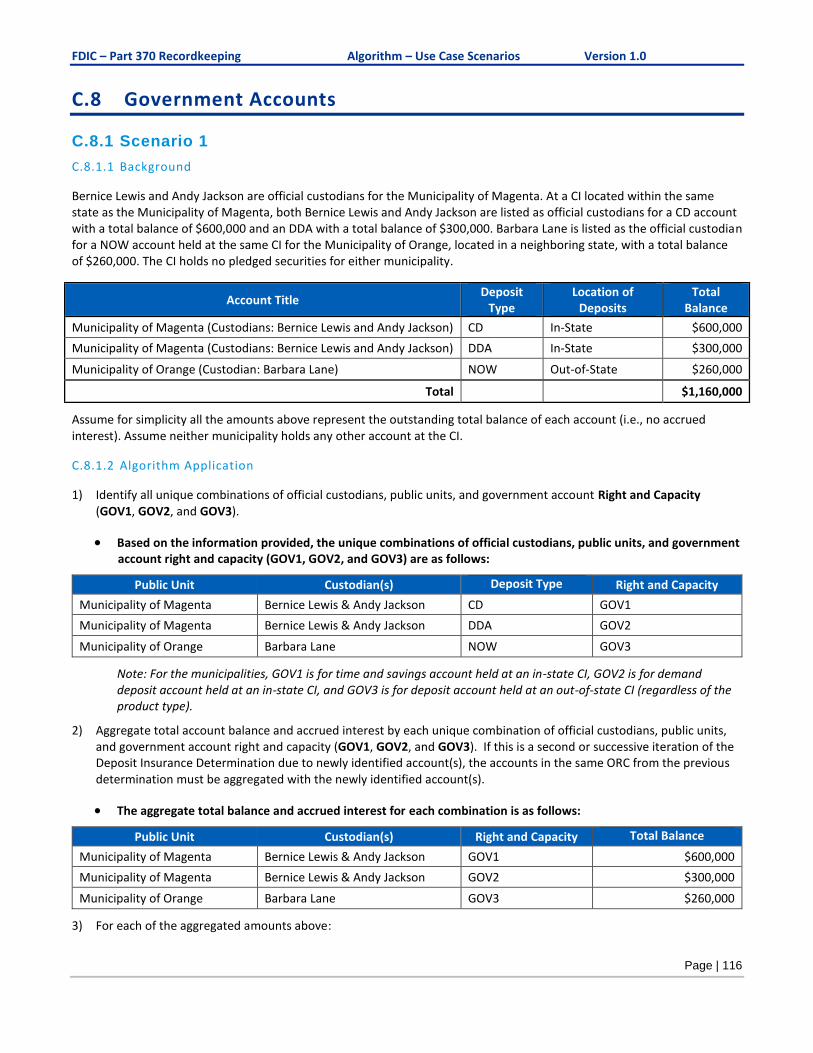

C.8 Government Accounts .......................................................................................... 116

C.8.1 Scenario 1 ............................................................................................................. 116 C.8.1.1 Background ................................................................................................................................. 116 C.8.1.2 Algorithm Application .............................................................................................................. 116 C.8.1.3 Outcome ...................................................................................................................................... 118

C.9 Mortgage Servicing Accounts ............................................................................. 119

C.9.1 Scenario 1 ............................................................................................................. 119 C.9.1.1 Background ................................................................................................................................. 119 C.9.1.2 Algorithm Application .............................................................................................................. 120 C.9.1.3 Outcome ...................................................................................................................................... 124

C.10 Accounts held by a Depository Institution (DI) as the Trustee of an Irrevocable Trust ............................................................................................................ 125

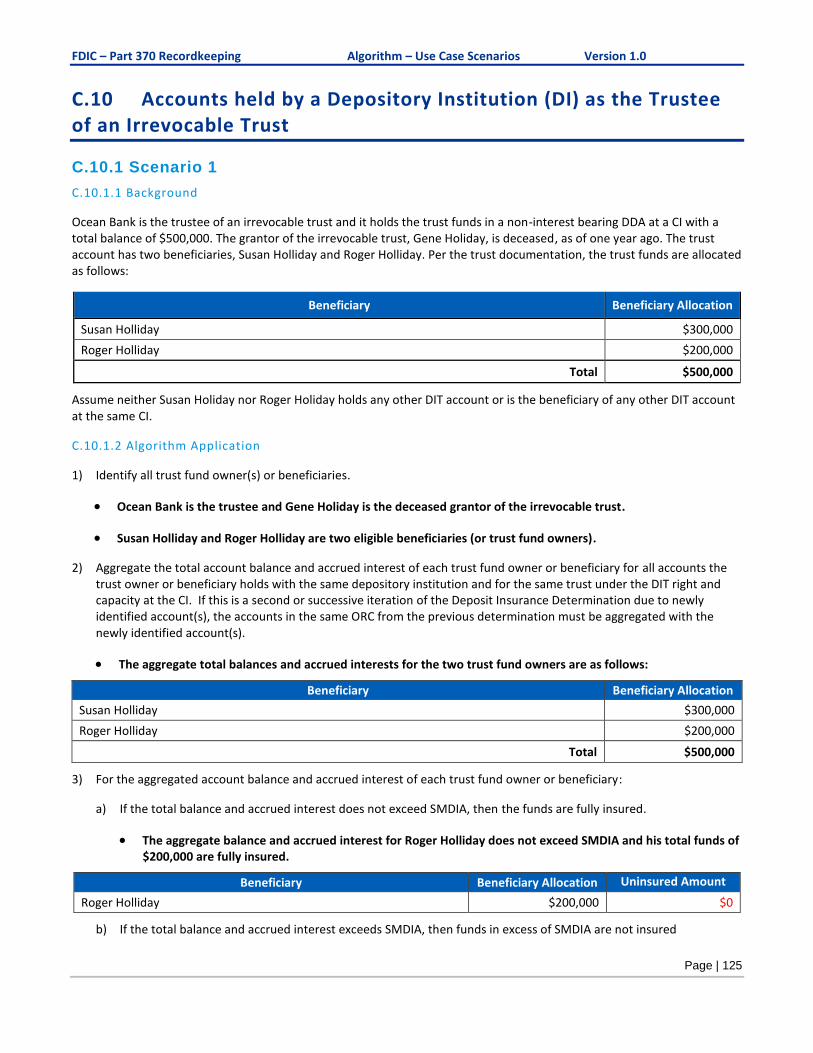

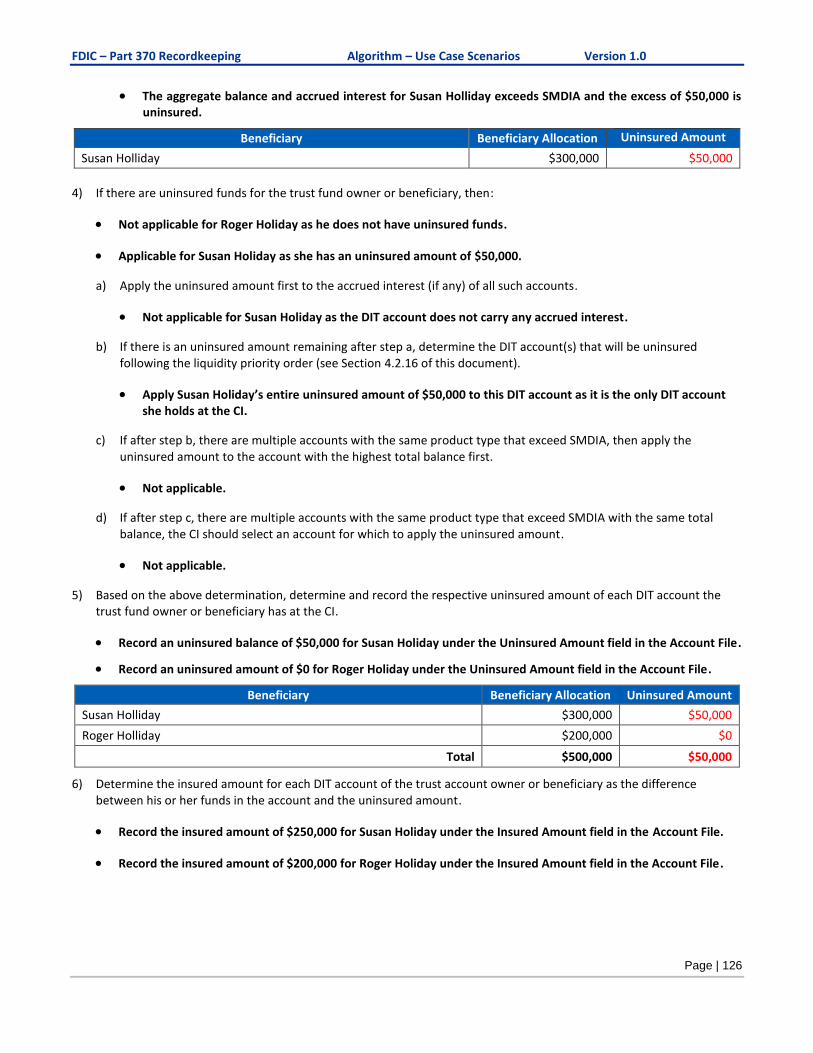

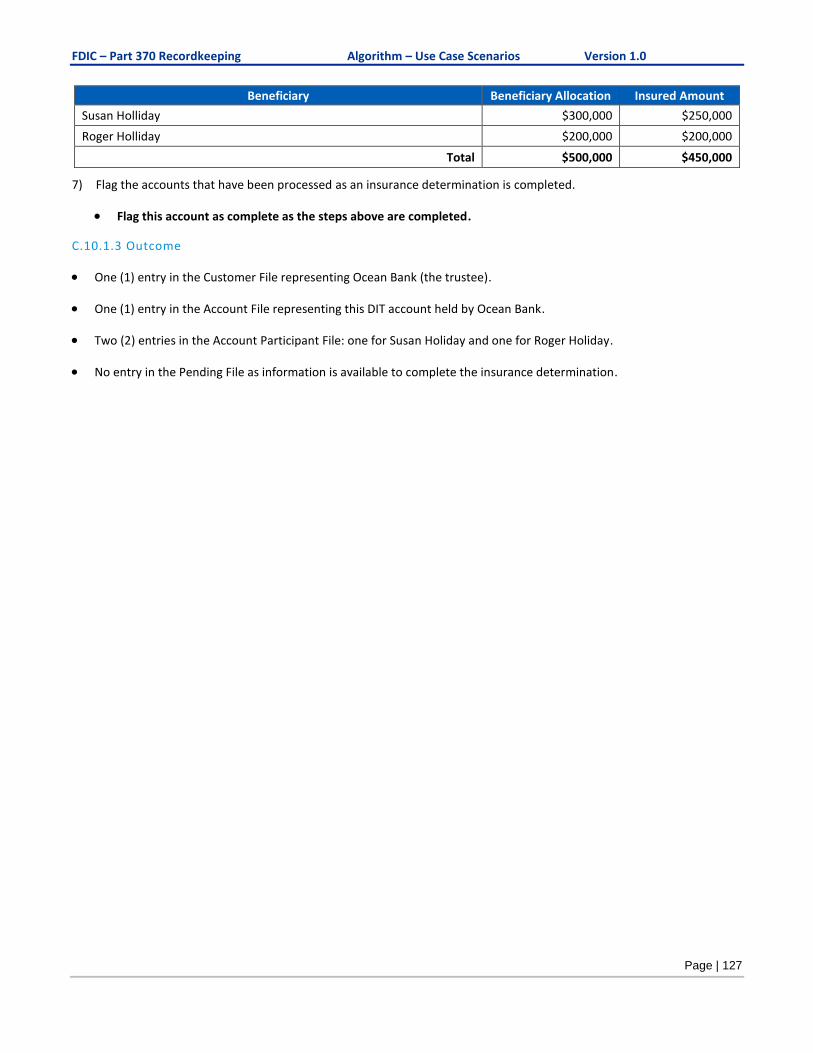

C.10.1 Scenario 1 ................................................................................................................ 125 C.10.1.1 Background .................................................................................................................................... 125 C.10.1.2 Algorithm Application ................................................................................................................. 125 C.10.1.3 Outcome ......................................................................................................................................... 127

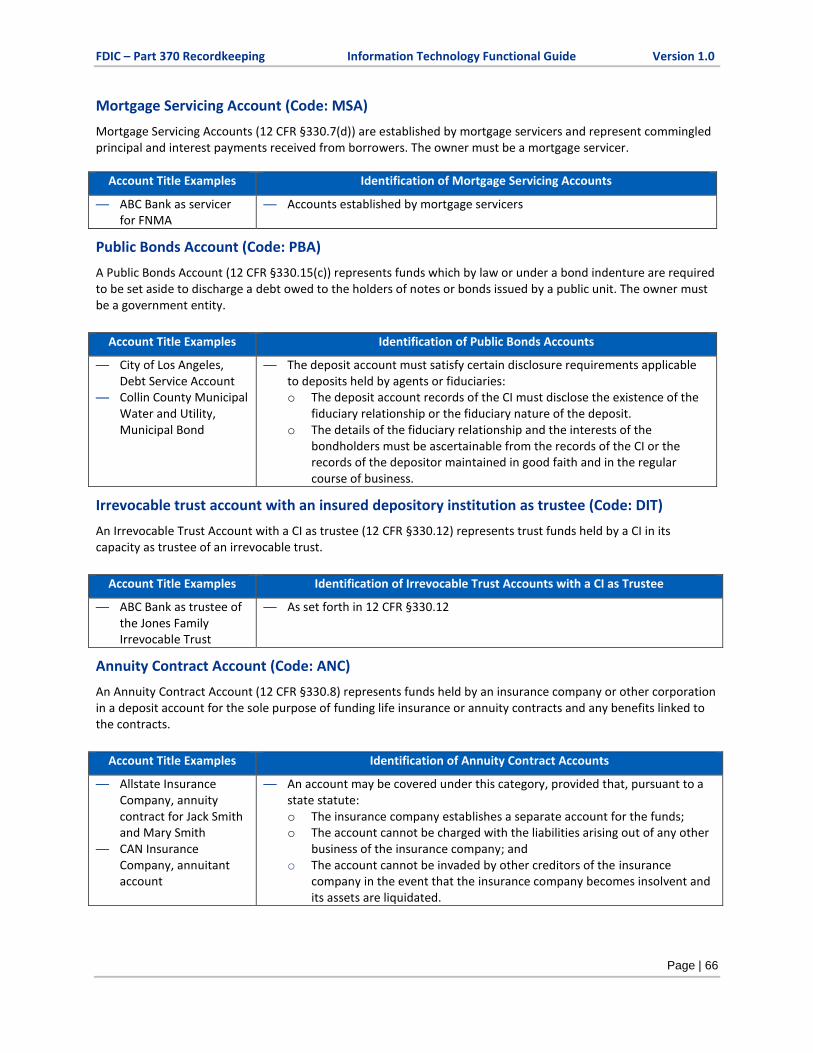

C.11 Annuity Contract Accounts ............................................................................... 128

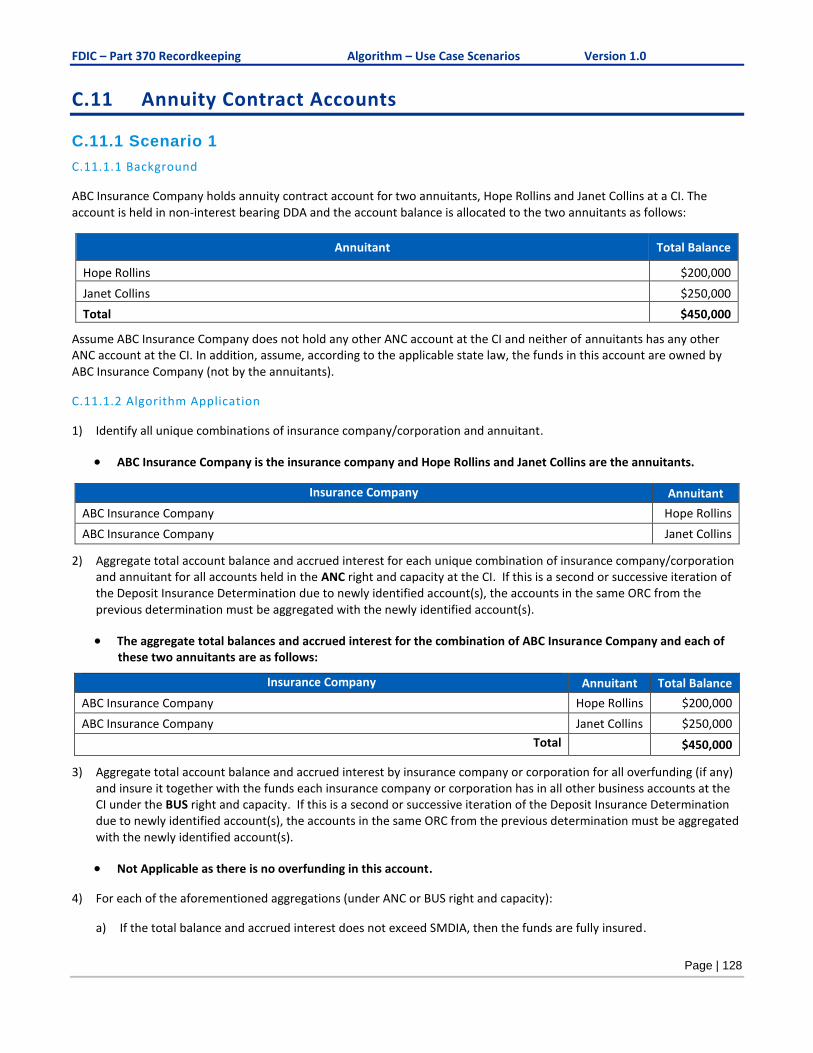

C.11.1 Scenario 1 ................................................................................................................ 128 C.11.1.1 Background .................................................................................................................................... 128 C.11.1.2 Algorithm Application ................................................................................................................. 128 C.11.1.3 Outcome ......................................................................................................................................... 131

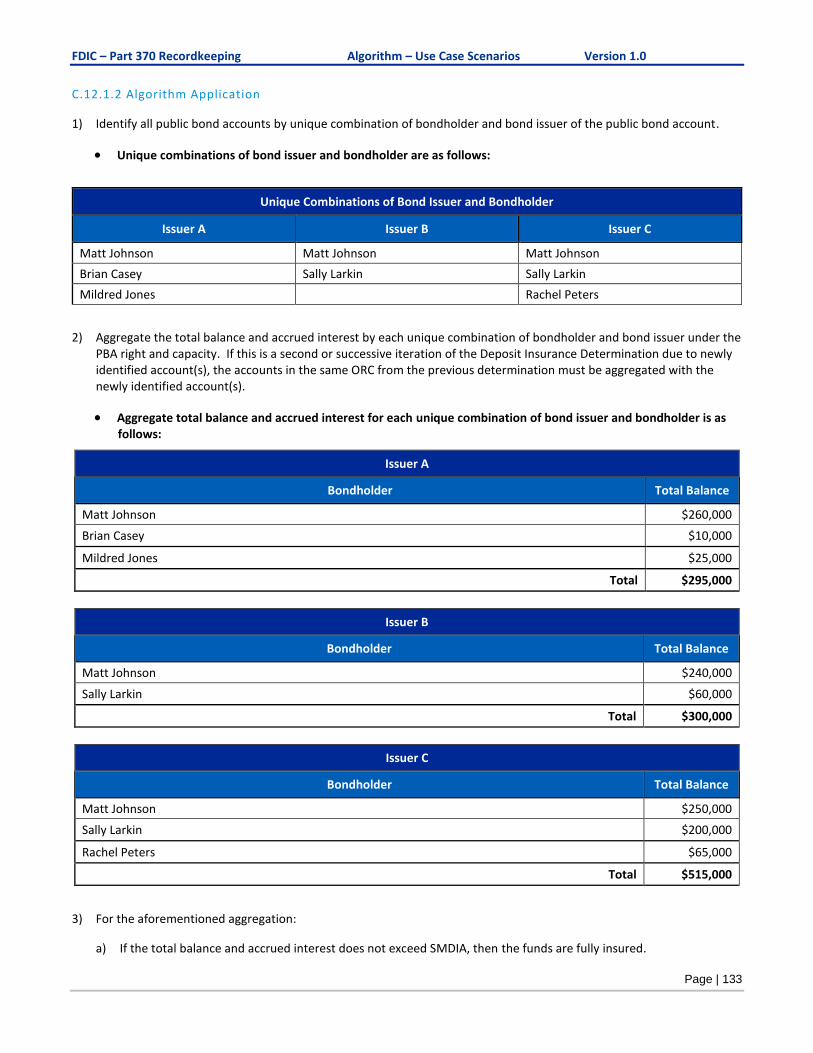

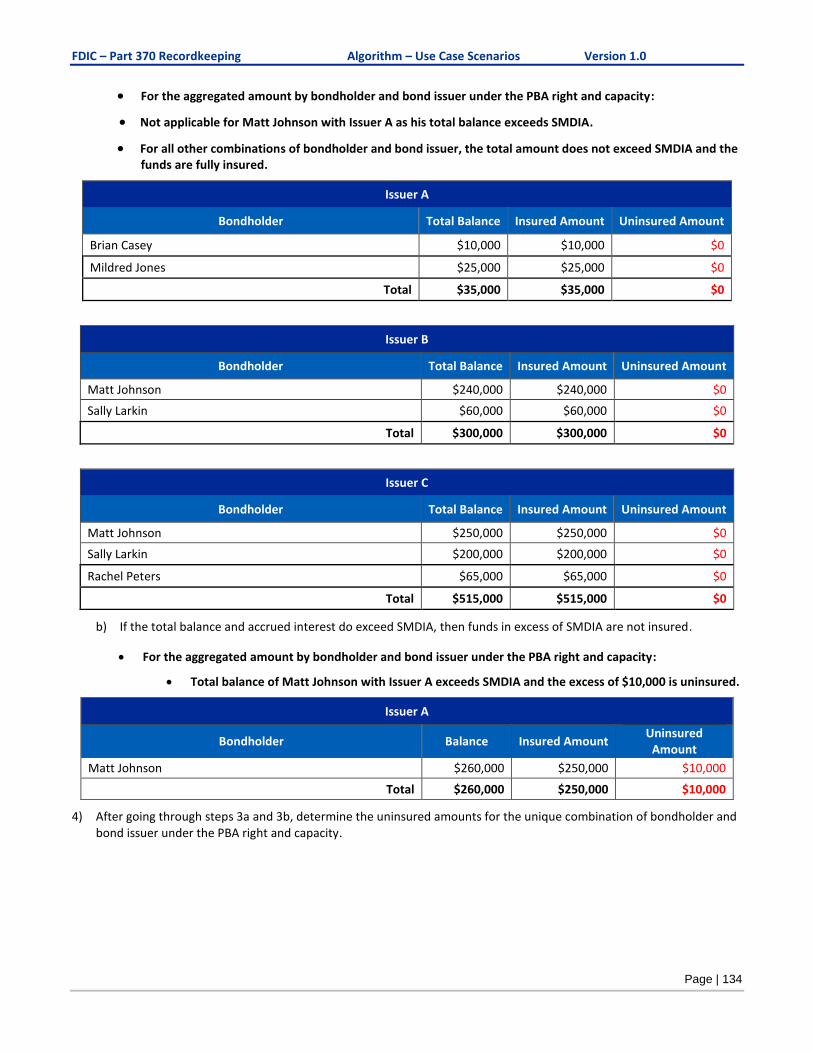

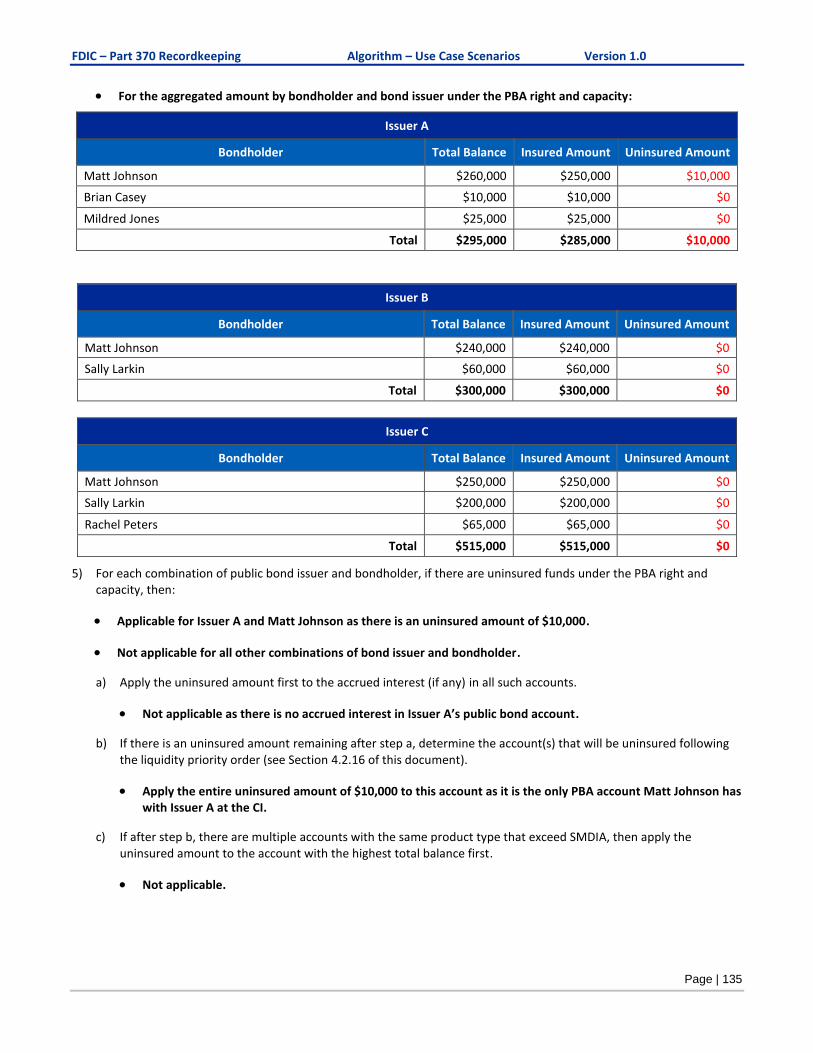

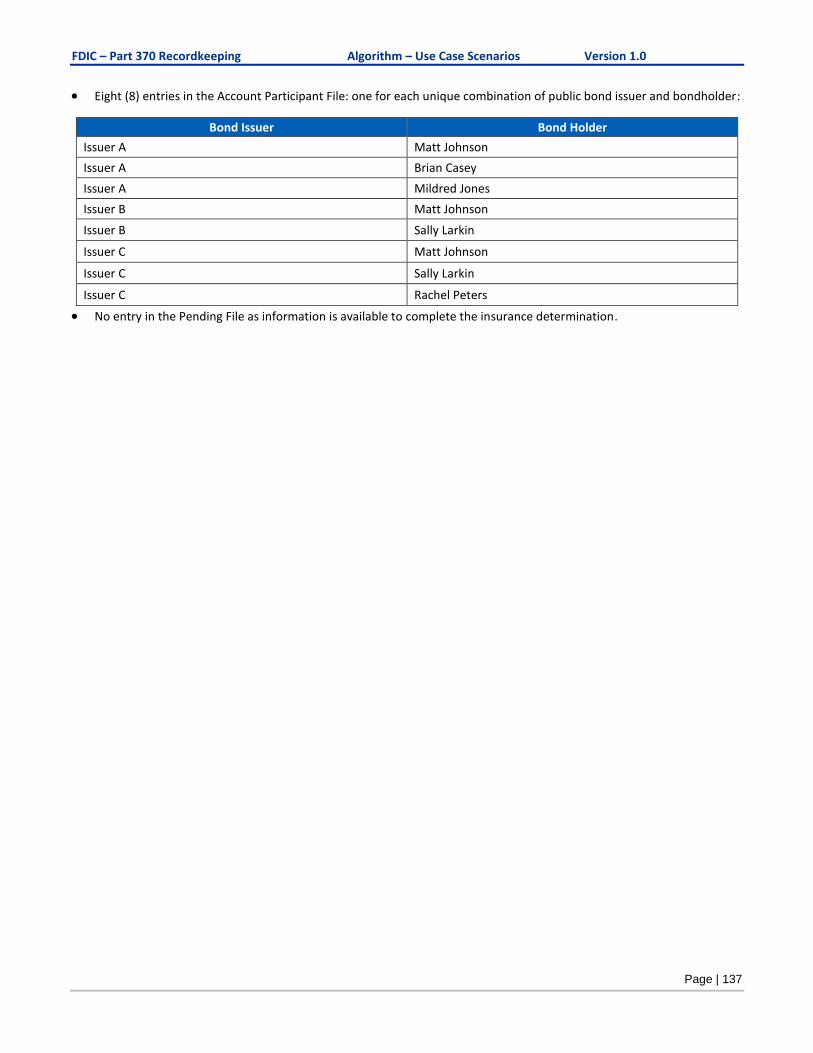

C.12 Public Bond Accounts ........................................................................................ 132

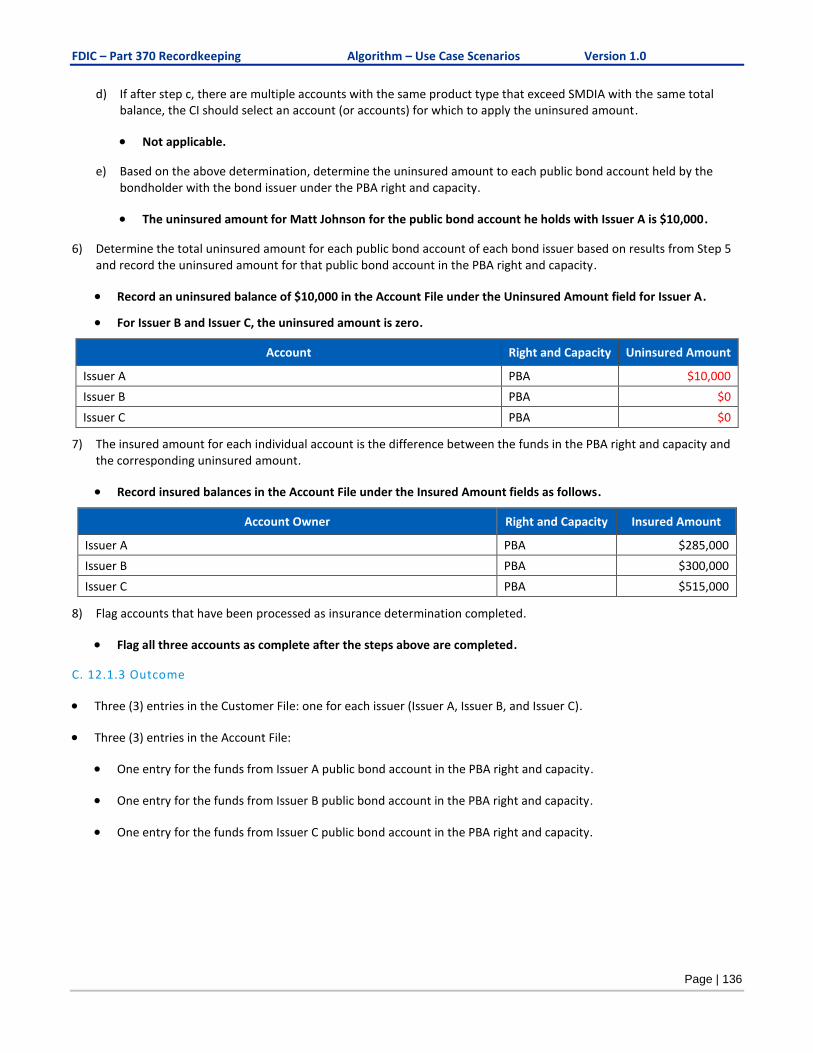

C.12.1 Scenario 1 ................................................................................................................ 132 C.12.1.1 Background .................................................................................................................................... 132 C.12.1.2 Algorithm Application ................................................................................................................. 133 C. 12.1.3 Outcome ....................................................................................................................................... 136

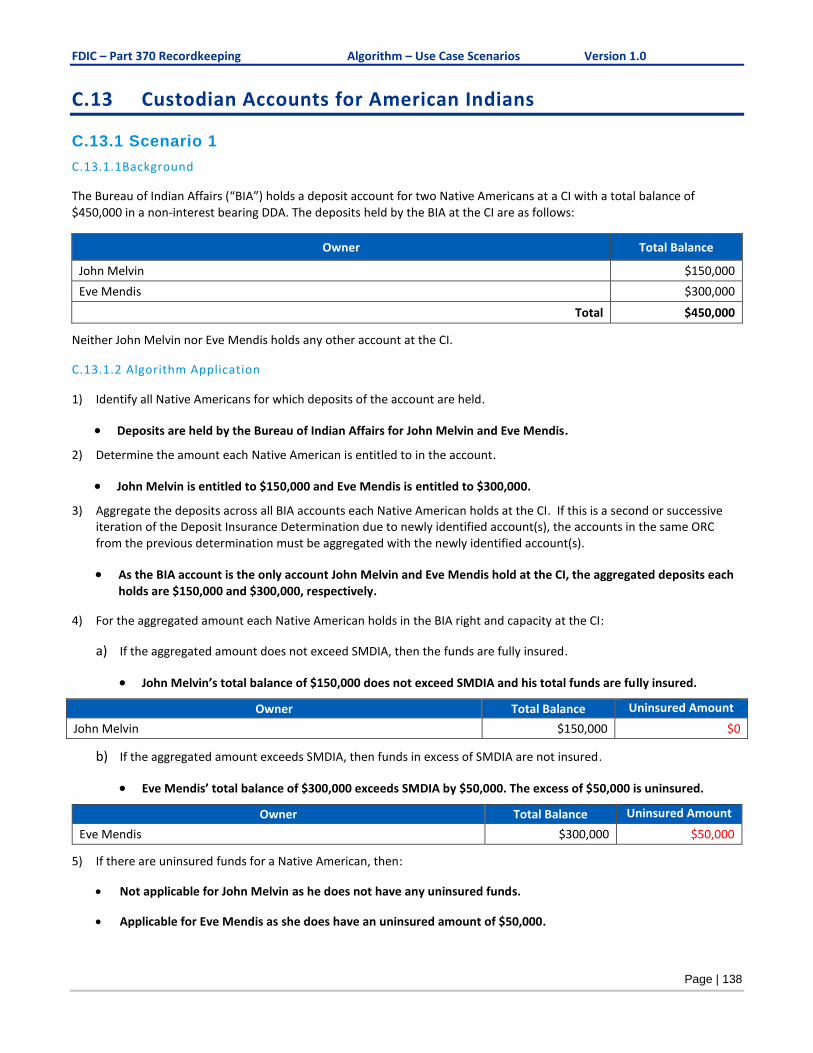

C.13 Custodian Accounts for American Indians ....................................................... 138

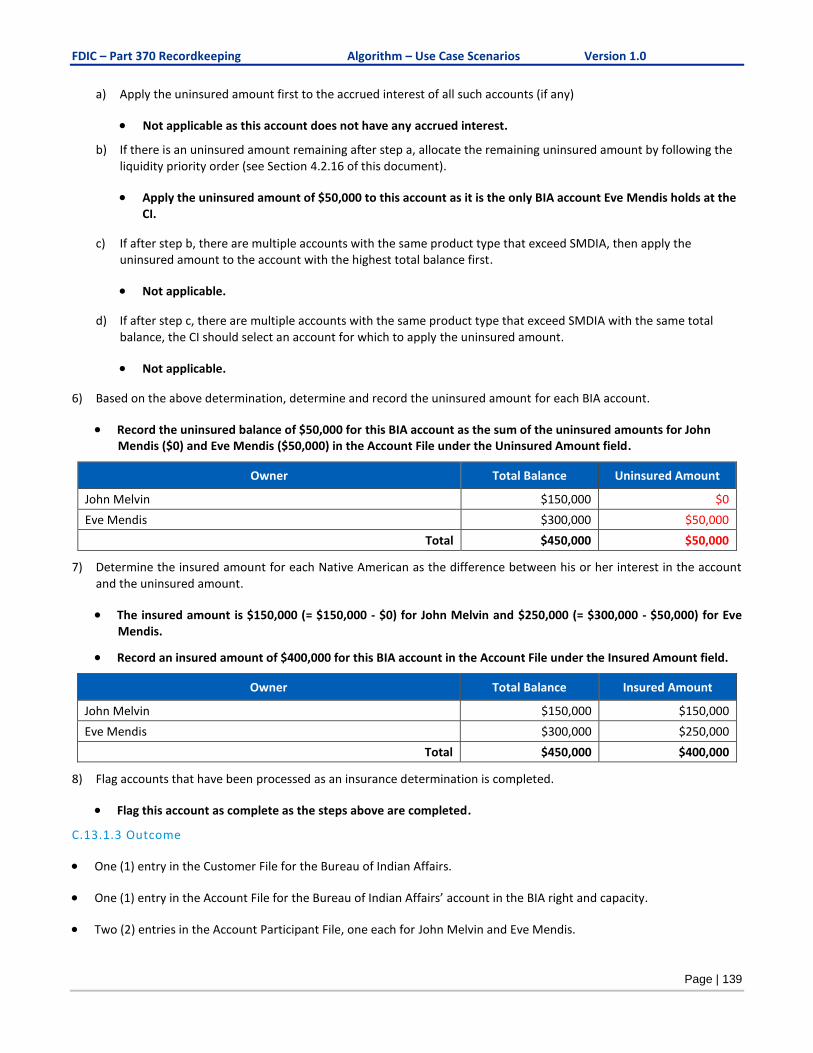

C.13.1 Scenario 1 ................................................................................................................ 138 C.13.1.1Background ..................................................................................................................................... 138 C.13.1.2 Algorithm Application ................................................................................................................. 138 C.13.1.3 Outcome ......................................................................................................................................... 139

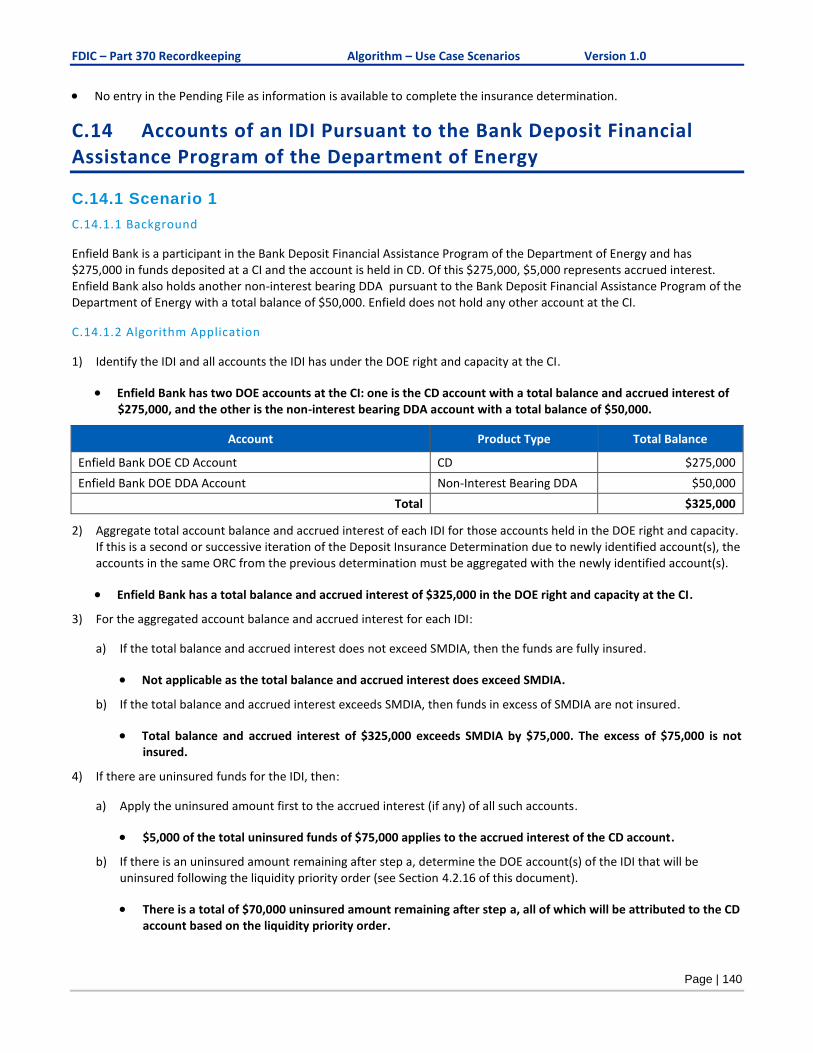

C.14 Accounts of an IDI Pursuant to the Bank Deposit Financial Assistance Program of the Department of Energy ......................................................................... 140

C.14.1 Scenario 1 ................................................................................................................ 140 C.14.1.1 Background .................................................................................................................................... 140 C.14.1.2 Algorithm Application ................................................................................................................. 140 C.14.1.3 Outcome ......................................................................................................................................... 141

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

C.15 Fiduciary Account - Broker/Sweep Accounts ....................................................... 142

C.15.1 Scenario 1 ................................................................................................................ 142 C.15.1.1 Background .................................................................................................................................... 142

C.15.2 Scenario 1 - Day 1 ................................................................................................. 142 C.15.2.1 Algorithm Application ................................................................................................................. 143 C.15.2.1.1 Anytown Broker Account ................................................................................................... 143 15.2.1.2 Deposit Insurance Determination for Marci Jones (SGL) ........................................... 143 C.15.2.1.3 Deposit Insurance Determination for XYZ Dredging, Inc. (BUS) .............................. 145 C.15.2.2 Outcome ......................................................................................................................................... 147

C.15.3 Scenario 1 - Day 15 ............................................................................................... 148 C.15.3.1 Overview ........................................................................................................................................ 148 C.15.3.2 Algorithm Application ................................................................................................................. 148 C.15.3.2.1 Anytown Broker Account ................................................................................................... 148 C.15.3.2.2 Deposit Insurance Determination for Anywhere City (GOV1) ................................... 148 C.15.3.2.3 Deposit Insurance Determination for ABC Trust (REV) ............................................... 150 C.15.3.3 Outcome ......................................................................................................................................... 153

Appendix D Acronyms/Abbreviations/Terms ........................................................ 154

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 1

How to Read This Document

Section Summary

1. Introduction Explanation of the goals and intent of the document.

2. Overview Overview of deposit insurance and the deposit insurance determination process.

3. Process Requirements Explanation of the processes and capabilities that the Federal Deposit Insurance Corporation (“FDIC”) expects all Covered Institutions (“CIs") will be able to demonstrate in order to ensure compliance with 12 CFR Part 370 entitled “Recordkeeping for Timely Deposit Insurance Determination” (“Part 370”).

4. Deposit Insurance Determination Requirements

Detailed explanation of calculations that must be performed by the CI to correctly calculate deposit insurance coverage.

5. Output File Generation Requirements

Explanation of requirements for populating data files where the instructions vary by ownership right and capacity (“ORC”).

6. Control Report Requirements Explanation of data checks that a CI must have in place for accuracy, completeness, and compliance with standards and to meet the objectives of the rule.

7. Summary Report Requirements Explanation of high-level summary reporting requirements that a CI must have in place to support accurate deposit insurance calculation process.

8. Certification of Compliance Explanation of the document that a CI must provide to certify that it has implemented and successfully tested its information technology system for compliance with Part 370 during the preceding calendar year.

9. Appendices Appendix A

— Explanation of data-file-generation capabilities that a CI must have for the calculation of deposit insurance coverage.

Appendix B

— Explanation of the 14 ORCs that are recognized by the FDIC in its deposit insurance determination process.

Appendix C

— Use Cases

Appendix D

Explanation of

— Acronyms/Abbreviations/Terms

— Definitions

— Cross-References

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 2

1 Introduction

About the Part 370 Information Technology Functional Guide

This Part 370 Information Technology Functional Guide (“Guide”) serves as a supplemental resource to assist covered institutions (“CIs”) with the implementation of information technology systems capabilities that will be compliant with 12 C.F.R. Part 370 (“Part 370”). The goals of this Guide are to:

— Provide a single, organized source for CI systems capabilities. — Describe the details of the features, function, and other systems aspects that the FDIC believes

should be present in the CI’s recordkeeping, IT, or data environment. This Guide does not contain:

— Detailed business requirements or technical requirements that would support systems development; rather these should be developed by each CI.

— Descriptions of the methodology used to discover, assess, and specify the underlying guidance.

Important Disclaimers This Guide is technical in nature and does not create any rights, substantive or procedural, enforceable at law by any party in any matter. It does not bind covered institutions or the FDIC to a specific course of action. It is not intended to constitute and should not be considered as legal advice. It is not definitive or comprehensive and should not be relied upon for interpretation of the FDIC’s deposit insurance rules. The Federal Register and the Code of Federal Regulations remain the official sources for regulatory information published by the FDIC. This Guide may be used in conjunction with the FDIC’s deposit insurance reference materials found on the FDIC’s website at www.fdic.gov/deposit. In particular, the Financial Institution Employee’s Guide to Deposit Insurance, accessible on the FDIC’s website at www.fdic.gov/deposit/DIGuideBankers.html may prove helpful and illustrative. Note about possible changes to this Guide This version of the Guide reflects the statutory principles and implementing regulations that are effective as of the date of publication. This Guide will be revised on an on-going basis as laws, policies and procedures change and as feedback regarding system architecture, interfaces, capabilities, and limitations is provided to the FDIC by CIs. It is dated as of the most recent revision date. Contact To the extent questions arise regarding Part 370, including the information contained in this Guide, please contact the FDIC at [email protected].

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 3

2 Overview

The FDIC has issued new requirements for all CIs to ensure that depositors have prompt access to insured deposits in the event of a failure. If a CI fails, the FDIC must provide depositors their insured funds "as soon as possible" after failure while also resolving the failed CI in the least costly manner possible.

References to actions to be taken by a CI after the FDIC has been appointed as receiver are intended to be taken at

the direction of or on behalf of the FDIC, as applicable.

2.1 Background

In November 2016, the FDIC approved for publication in the Federal Register a final rule requiring large Insured Depository Institutions (“IDIs”) with two million or more deposit accounts to maintain complete and accurate data on each depositor’s ownership interest in deposit accounts by right and capacity. The IDIs covered by this rule, now CIs, must also develop and maintain IT systems capability to calculate the insured and uninsured amounts for each deposit owner by right and capacity for all deposit accounts. Should a CI fail, this capability will be used by the FDIC to facilitate timely payment of deposit insurance.

Please refer to the Final Rulemaking at 81 FR 87734 (December 5, 2016) and the supplementary information contained therein for more information.

2.2 Key Concepts

2.2.1 Deposit insurance coverage has increased over time

Deposit insurance was established through the Banking Act of 1933 with a standard maximum deposit insurance amount (“SMDIA”) of $2,500. As the economy and banking industry evolved, Congress and the FDIC recognized the need for additional coverage. Consequently, the Federal Deposit Insurance Act and relevant regulations have been amended to both increase the SMDIA and provide for additional coverage through the creation of different ownership “rights and capacities” (“ORCs”). Congress most recently raised the SMDIA to $250,000 in 2010. 2.2.2 Prompt access to insured deposits is essential

Confidence in the FDIC is critical to the public’s confidence in the banking system. No depositor has lost a single penny of insured deposits since the FDIC was established in 1933. Of equal importance, the FDIC strives to make funds available to depositors as soon as possible, often by the next business day after an IDI fails.

2.2.3 Depositors are insured separately at each insured CI

While each depositor’s insurance coverage is limited to the SMDIA for each insurance category, each depositor is insured separately at each CI. A depositor’s coverage in a category at one CI does not affect the depositor’s coverage in that same insurance category for an account at a different CI. 2.2.4 FDIC will rely on the CI’s deposit account records

In the event of the failure of a CI, the FDIC relies upon the deposit account records of the CI to determine the ownership of an account and thereby the amount of the deposit insurance coverage available to each depositor. If the records are complete, clear, and unambiguous, then those records shall be considered binding on the depositor, and the FDIC shall consider no other records on the manner in which the deposits are owned. 2.2.5 Depositors are insured in different ownership “rights and capacities”

Deposit insurance coverage is provided for deposits held in 14 different ORCs. All deposits, whether in one account or multiple accounts, held in an IDI are aggregated and insured for up to the SMDIA for the particular ORC.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 4

2.2.6 Fiduciary and agency accounts may receive pass-through coverage

Fiduciary or agency accounts may be entitled to receive pass-through deposit insurance coverage. These accounts are established and maintained by third parties on behalf of the beneficial owner of a deposit. These pass-through deposits would be aggregated with all other deposits within the same ORC that the owner may have at the failed CI. 2.2.7 Deposits eligible for FDIC deposit insurance

Deposit insurance coverage only applies to domestic deposits. Non-deposit accounts, such as securities accounts, and deposits at foreign branches are excluded for purposes of deposit insurance calculation.

2.3 CI Failure Scenario

The processes for Part 370 may be conducted in three phases: 1) implementation and initial validation, 2) ongoing auditing and compliance testing, and 3) CI failure. 2.3.1 Implementation period and initial validation

Part 370 sets a three-year time frame for implementation. The FDIC will provide technical guidance and input upon request by a CI during this period. A CI must implement key system functionalities and ensure that all required data is complete and accurate so as to enable performance of an automatic deposit insurance calculation. The data requirements include, but are not limited to, assigning unique identifiers to account owners and assigning each deposit account into one of the 14 ORCs.

Throughout this document, work functions and processes are described in great detail in order to fully portray the functionalities, capacities, and operations that CI systems must be able to perform. Before expiration of the three-year time frame, a CI must submit a certification of compliance signed by the Chief Executive Officer (“CEO”) or Chief Operating Officer (“COO”) of the CI and a summary deposit insurance coverage report, unless an extension is granted. 2.3.2 Ongoing compliance testing

Compliance testing will begin after the expiration of the Part 370 three-year implementation period. The FDIC will test 1) the completeness and accuracy of the CI’s customer and deposit data; and 2) the accuracy of the CI’s insurance calculation and reporting. The CI will 1) address any deficiencies identified during compliance testing; and 2) test processes to integrate data concerning alternate recordkeeping and exception accounts.

A CI’s systems must be compliant with Part 370 and, at a minimum, be capable of generating the output files for the Customer File, Account File, Account Participant File, and Pending File (collectively, the “Output Files”) and performing initial and multiple subsequent iterations of deposit insurance calculations.

The compliance testing framework will be made available once the FDIC has developed sufficient understanding of CI system capabilities and limitations. Compliance testing procedures will include but not be limited to:

Verification of depositor data against the books and records of the CI, Reconciliation of the deposit account balances to the general ledger, Calculation check of insured and uninsured amounts, Reconciliation of insured, uninsured and pending balances to the deposit systems, Validating accuracy of subsequent iterations of the deposit insurance calculation, and For accounts eligible for pass-through deposit insurance where ultimate account ownership data is not

held on CI systems, processing of test data to simulate integration and processing of information received from third-parties containing underlying account information.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 5

2.3.3 Bank Failure

A bank failure is a closing of a bank by a federal or state banking agency. The bank is typically closed when it becomes critically undercapitalized or is unable to meet its obligations to depositors or others.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 6

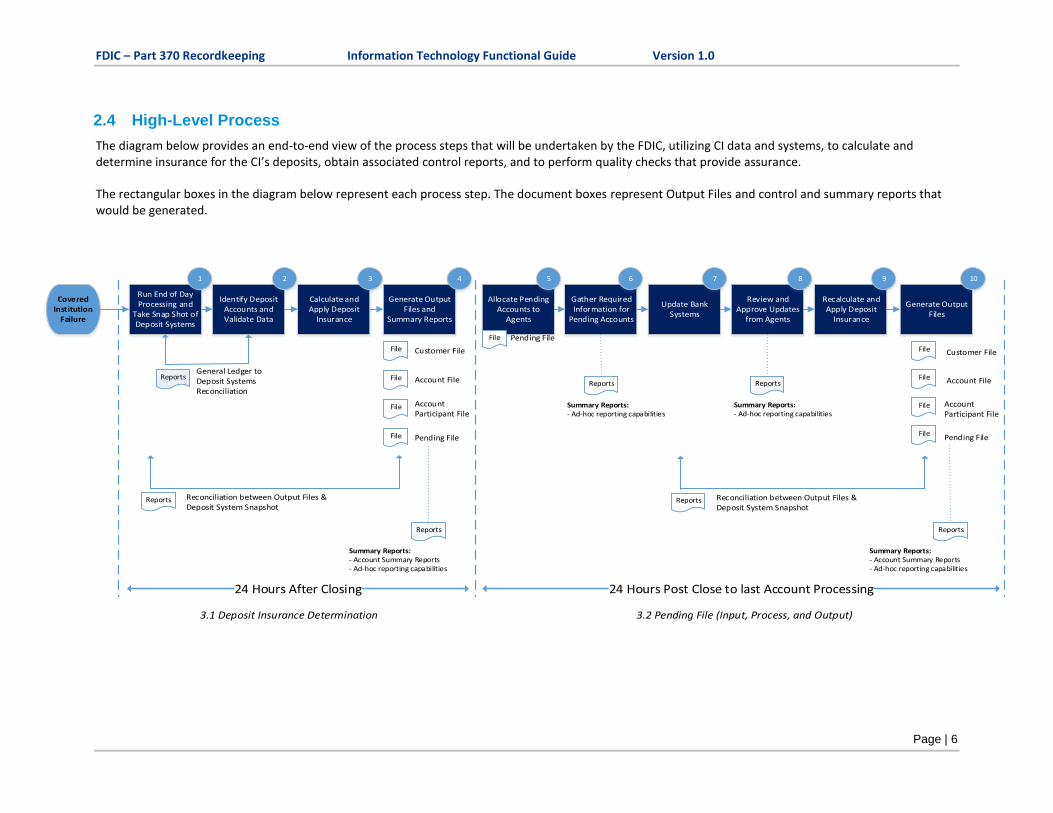

2.4 High-Level Process

The diagram below provides an end-to-end view of the process steps that will be undertaken by the FDIC, utilizing CI data and systems, to calculate and determine insurance for the CI’s deposits, obtain associated control reports, and to perform quality checks that provide assurance.

The rectangular boxes in the diagram below represent each process step. The document boxes represent Output Files and control and summary reports that would be generated.

Covered Institution

Failure

Run End of Day Processing and

Take Snap Shot of Deposit Systems

Identify Deposit Accounts and Validate Data

Calculate and Apply Deposit

Insurance

Generate Output Files and

Summary Reports

General Ledger to Deposit Systems Reconciliation

Reconciliation between Output Files & Deposit System Snapshot

24 Hours After Closing

Allocate Pending Accounts to

Agents

Gather Required Information for

Pending Accounts

Update Bank Systems

Review and Approve Updates

from Agents

Recalculate and Apply Deposit

Insurance

Generate Output Files

24 Hours Post Close to last Account Processing

Reports

File

File

File

File

Customer File

Account File

Account Participant File

Pending File

Reports

File Pending File

Reports

File

File

File

File

Customer File

Account File

Account Participant File

Pending File

Reconciliation between Output Files & Deposit System Snapshot

Reports

1 2 3 4 5 6 7 8 9 10

Summary Reports:- Ad-hoc reporting capabilities

Reports

Summary Reports:- Account Summary Reports- Ad-hoc reporting capabilities

Reports

Summary Reports:- Ad-hoc reporting capabilities

Reports

Summary Reports:- Account Summary Reports- Ad-hoc reporting capabilities

3.1 Deposit Insurance Determination 3.2 Pending File (Input, Process, and Output)

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 7

Process steps 1-4 represent the first 24 hours after closing: Within the first 24 hours after the failed CI’s closing, the FDIC, using CI systems and data, undertakes a number of steps to ensure a baseline deposit insurance calculation can be established and liquidity can be quickly provided to depositors. Specifically, the following capabilities are required of the CI systems:

1. Generate deposit account balances as of the end-of-day on the day of failure. Generate snapshot of end-

of-day deposits for deposit insurance calculation purposes.

2. Identify insured deposits within each ORC at the CI.

3. Aggregate depositor account and balance data and use that data to perform the deposit insurance

calculation.

4. Generate the Output Files.

Process steps 5-10 represent the second 24 hours after closing: After the initial 24 hour period following closing, the CI’s systems will be leveraged by the FDIC to process outstanding accounts subject to the alternative recordkeeping provision and other pending accounts. As such, the following capabilities are required:

5. Assign accounts on the Pending File to FDIC agents by product type, pending reason, ORC, etc.

6. Track progress against workload and volume of pending accounts.

7. Update data attributes in the Pending File without entering adjustments into core banking systems.

8. Review and approve updates to pending accounts with information provided by third-party intermediaries

holding depositor data for pass-through insurance eligible accounts.

9. Recalculate depositor account and balance data from the Pending File and use that data to perform the

deposit insurance determination.

10. Generate the Output Files.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 8

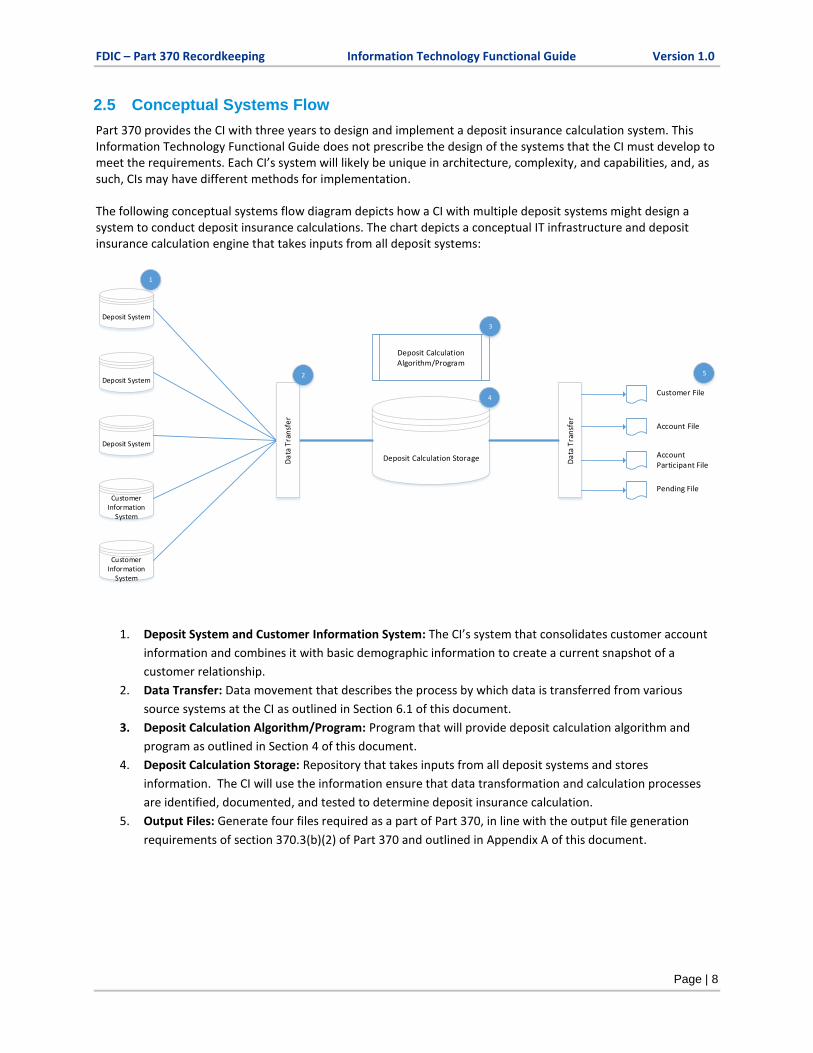

2.5 Conceptual Systems Flow

Part 370 provides the CI with three years to design and implement a deposit insurance calculation system. This Information Technology Functional Guide does not prescribe the design of the systems that the CI must develop to meet the requirements. Each CI’s system will likely be unique in architecture, complexity, and capabilities, and, as such, CIs may have different methods for implementation.

The following conceptual systems flow diagram depicts how a CI with multiple deposit systems might design a system to conduct deposit insurance calculations. The chart depicts a conceptual IT infrastructure and deposit insurance calculation engine that takes inputs from all deposit systems:

1. Deposit System and Customer Information System: The CI’s system that consolidates customer account

information and combines it with basic demographic information to create a current snapshot of a

customer relationship.

2. Data Transfer: Data movement that describes the process by which data is transferred from various

source systems at the CI as outlined in Section 6.1 of this document.

3. Deposit Calculation Algorithm/Program: Program that will provide deposit calculation algorithm and

program as outlined in Section 4 of this document.

4. Deposit Calculation Storage: Repository that takes inputs from all deposit systems and stores

information. The CI will use the information ensure that data transformation and calculation processes

are identified, documented, and tested to determine deposit insurance calculation.

5. Output Files: Generate four files required as a part of Part 370, in line with the output file generation

requirements of section 370.3(b)(2) of Part 370 and outlined in Appendix A of this document.

Deposit System

Deposit Calculation Storage

Deposit System

Deposit System

Customer Information

System

Customer Information

SystemD

ata

Tra

nsf

er

Customer File

Account File

Account Participant File

Pending File

Deposit Calculation Algorithm/Program

Da

ta T

ran

sfe

r1

2

3

5

4

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 9

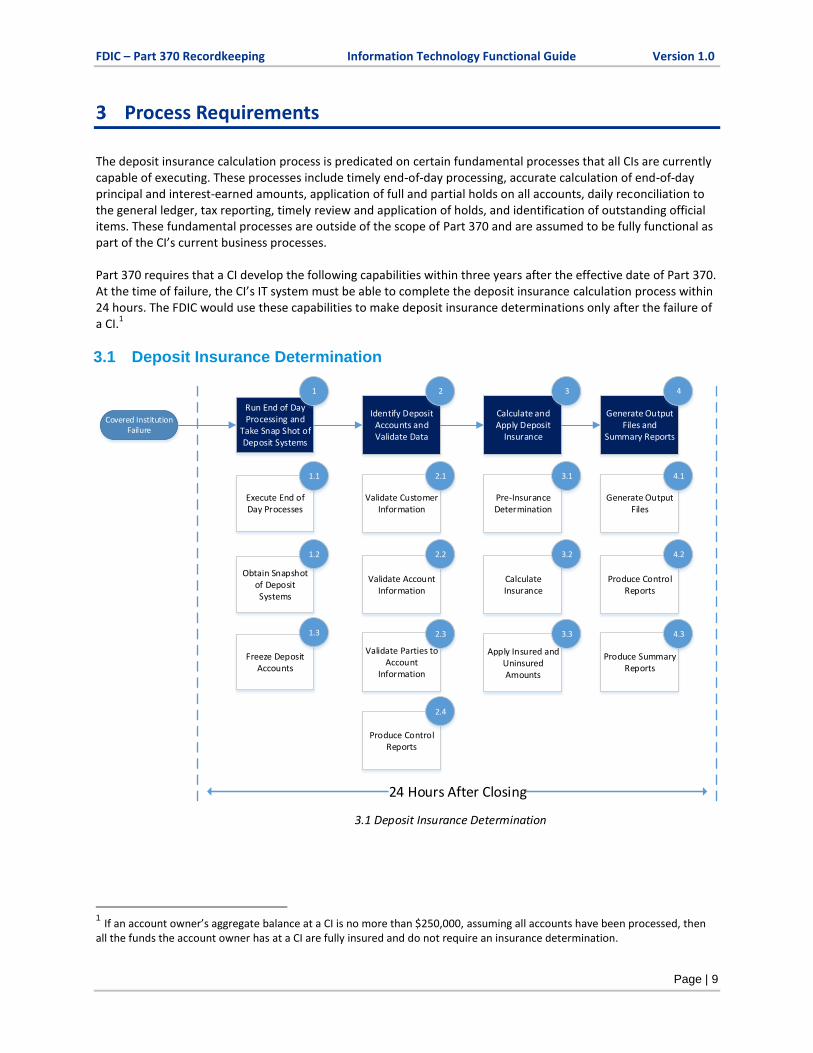

3 Process Requirements

The deposit insurance calculation process is predicated on certain fundamental processes that all CIs are currently capable of executing. These processes include timely end-of-day processing, accurate calculation of end-of-day principal and interest-earned amounts, application of full and partial holds on all accounts, daily reconciliation to the general ledger, tax reporting, timely review and application of holds, and identification of outstanding official items. These fundamental processes are outside of the scope of Part 370 and are assumed to be fully functional as part of the CI’s current business processes. Part 370 requires that a CI develop the following capabilities within three years after the effective date of Part 370. At the time of failure, the CI’s IT system must be able to complete the deposit insurance calculation process within 24 hours. The FDIC would use these capabilities to make deposit insurance determinations only after the failure of a CI.

1

3.1 Deposit Insurance Determination

1 If an account owner’s aggregate balance at a CI is no more than $250,000, assuming all accounts have been processed, then

all the funds the account owner has at a CI are fully insured and do not require an insurance determination.

Covered Institution Failure

Run End of Day Processing and

Take Snap Shot of Deposit Systems

Identify Deposit Accounts and Validate Data

Calculate and Apply Deposit

Insurance

Generate Output Files and

Summary Reports

24 Hours After Closing

1 2 3 4

Execute End of Day Processes

Obtain Snapshot of Deposit Systems

1.1

1.2

Validate Customer Information

Validate Account Information

Validate Parties to Account

Information

2.1

2.2

2.3

Pre-Insurance Determination

Calculate Insurance

3.1

3.2

Produce Control Reports

Generate Output Files

Produce Summary Reports

4.1

4.2

4.3

Apply Insured and Uninsured Amounts

3.3

Freeze Deposit Accounts

1.3

Produce Control Reports

2.4

3.1 Deposit Insurance Determination

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 10

Step 1: Run End-of-Day Processing and Take Snapshot of Deposit Systems

Major Activity: To execute the end-of-day processing on the CI’s systems post-failure to ensure baseline depositor data records and balances exist to undertake a deposit insurance calculation and, ultimately, a deposit insurance determination by the FDIC.

Key Inputs Key Outputs

— N/A — Baseline for Deposit Insurance — Snapshot of Bank’s Deposit Systems and Records

Key Steps: The following activities are conducted by the FDIC to ensure that a baseline and snapshot can be taken of the CI’s deposit systems.

Execute End-of-Day Processes: Execute the end-of-day processes to ensure that all pending transactions are

applied to the deposit systems and all balances reconcile with the general ledger. The complete minimum

requirements are detailed in 12 CFR § 360.8 Method for determining deposit and other liability account

balances at a failed insured depository institution. [https://www.fdic.gov/regulations/laws/rules/2000-

7800.html#fdic2000part360.8]

Obtain Snapshot of Deposit Systems: Obtain a snapshot of all deposit systems and customer file

systems that contain information pertinent to the deposit insurance calculations and/or remitting

insurance payments to the depositor.

Restrict Access to Deposit Accounts: Restrict access to all deposit accounts in the core banking

systems to ensure no changes can be applied to ownership or access to the account and any balance

or accrued interest.

Step 2: Identify Deposit Accounts and Validate Data

Major Activity: Segregate deposit accounts that are eligible for deposit insurance and accounts that are not eligible for deposit insurance and validate that the required information is present on deposit accounts to perform an insurance determination.

Key Inputs Key Outputs

— Baseline for Deposit Insurance — Snapshot of Bank’s Deposit Systems and Records — Third Party Data Sets (as required)

— Accounts for Deposit Insurance Identified and Information Validated

— General Ledger Reconciled with Deposit Systems

Key Steps: The FDIC will conduct the following activities on the CI system to ensure deposit accounts are eligible for insurance determination.

Validate Customer Information: Validate all customer information needed for insurance

determination is present and execute the following key steps:

— Identify that customer account is eligible for Deposit Insurance under 12 CFR § 330 Deposit

Insurance Coverage [https://www.fdic.gov/regulations/laws/rules/2000-5400.html]

— Identify a unique set of customers, including removing and/or merging any duplicative

customers into a single customer record as required

— Identify that all customer information has been captured to determine insurance

— Identify customers requiring additional information

— Identify customers who have outstanding debts with the CI

— Identify government customers who have security pledged to them as a part of their deposit

agreement with the CI

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 11

— Execute data quality controls on the customer data as outlined in Section 6.2 of this document

to determine any data quality gaps/known issues

Validate Account Information: Validate the information required to populate the Account File and

any special flags. These include but are not limited to:

— Identify any accounts that are covered under the alternative recordkeeping requirements as

outlined in Section 370.4 (b) of Part 370

[https://www.federalregister.gov/documents/2016/12/05/2016-28396/recordkeeping-for-

timely-deposit-insurance-determination]

— Identify whether any of the alternative recordkeeping accounts have transactional features

— Identify whether the accounts are associated with prepaid cards

— Identify whether accounts are pass-through accounts (i.e., those accounts held by fiduciaries,

agents, and brokers on behalf of the customer)

— Validate that each account has at least one customer associated with it (i.e., there are no

orphan accounts)

— Execute data quality controls on the account data as outlined in Section 6.2 of this document to

determine any data quality gaps/known issues

Validate Account Participant Information: Validate that the CI has captured all information for all

parties to accounts. These include but are not limited to:

— Identify unique sets of account participant records, including removing and/or merging any

duplicative participants into a single record as required

— Validate that each participant record is associated to at least one account (i.e., there are no

orphan account parties)

Produce Control Reports: Generate control reports and validate that the total account population

considered for insurance determination matches the total number of accounts in the general ledger.

The CI systems should be capable of generating the control reports outlined in Section 6.3 of this

document.

Step 3: Calculate and Apply Deposit Insurance Rules

Major Activity: Aggregate depositor accounts for all ORCs by owner and apply deposit insurance rules to all eligible deposit accounts held at the CI.

Key Inputs Key Outputs

— Accounts for Deposit Insurance Identified and Information Validated

— General Ledger Reconciled with Deposit Systems

— Deposit Insurance Determination — Allocation of Insured and Uninsured

Balance Among Owners

Key Steps: The following activities are conducted by the CI system to calculate deposit insurance and used by the FDIC to determine deposit insurance.

Pre-Insurance Determination: Identify pre-insurance determination under the Deposit Insurance

Determination as outlined in Section 4.1 of this document.

Calculate Insurance: Calculate insurance under the Deposit Insurance Determination as outlined in

Section 4.2 of this document.

Apply insured and uninsured amounts: Allocate insured and uninsured balance among account

owners as outlined in Section 4.3 of this document.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 12

Step 4: Generate Output Files and Summary Reports

Major Activity: Generate Output Files that will act as the permanent record of the insurance determination for the customers at time of closing, including accounts in a pending status. In addition to the permanent record, additional control and summary reports will be produced to verify accuracy and completeness of the determination.

Key Inputs Key Outputs

— Deposit Insurance Determination — Allocation of insured and uninsured balance among

owners

— Customer File — Account File — Account Participant File — Pending File — Summary Reports — Control Reports

Key Steps: The following activities are conducted by the CI system and utilized by the FDIC.

Generate Output File: Generate four files required as a part of Part 370, in line with the Output File

generation requirements in Section 4 of this document and outlined in Appendix A. The four key files

are:

— Customer File: The Customer File is used by the FDIC to capture information regarding the

account owners

— Account File: The Account File specifies the insured and uninsured balances available to each

account

— Account Participant File: The Account Participant File identifies account participants, captures

indicative information, and captures account participant allocations

— Pending File: The Pending File captures accounts that require additional information before a

deposit insurance determination can be completed

Produce Control Reports: Generate control reports and validate that the total account population

considered for the insurance determination matches the total number of accounts in the account

and Pending Files. The CI system should generate the control reports outlined in Section 6.3 of this

document.

Produce Summary Reports: Generate the summary reports required by the FDIC and the CI that

highlight the total account allocations by various dimensions. The details of the specific account

summary reports required are outlined in Section 7 of this document.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 13

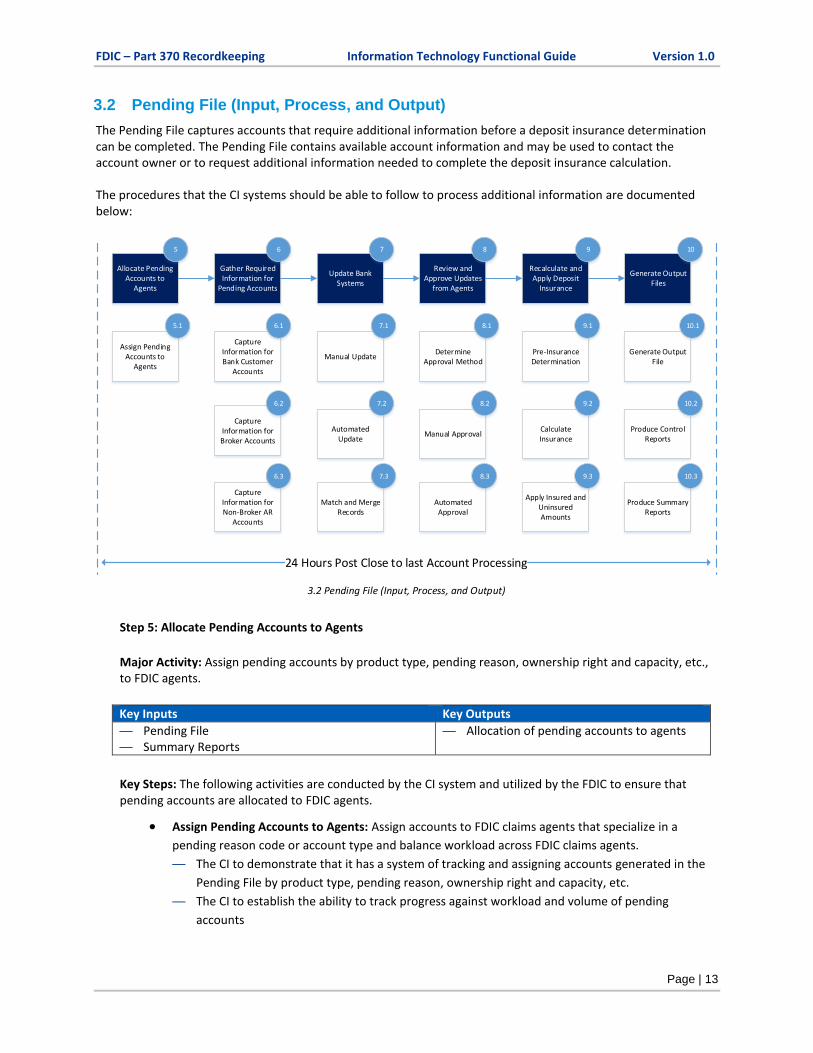

3.2 Pending File (Input, Process, and Output)

The Pending File captures accounts that require additional information before a deposit insurance determination can be completed. The Pending File contains available account information and may be used to contact the account owner or to request additional information needed to complete the deposit insurance calculation.

The procedures that the CI systems should be able to follow to process additional information are documented below:

Step 5: Allocate Pending Accounts to Agents

Major Activity: Assign pending accounts by product type, pending reason, ownership right and capacity, etc., to FDIC agents.

Key Inputs Key Outputs

— Pending File — Summary Reports

— Allocation of pending accounts to agents

Key Steps: The following activities are conducted by the CI system and utilized by the FDIC to ensure that pending accounts are allocated to FDIC agents.

Assign Pending Accounts to Agents: Assign accounts to FDIC claims agents that specialize in a

pending reason code or account type and balance workload across FDIC claims agents.

— The CI to demonstrate that it has a system of tracking and assigning accounts generated in the

Pending File by product type, pending reason, ownership right and capacity, etc.

— The CI to establish the ability to track progress against workload and volume of pending

accounts

Allocate Pending Accounts to

Agents

Gather Required Information for

Pending Accounts

Update Bank Systems

Review and Approve Updates

from Agents

Recalculate and Apply Deposit

Insurance

Generate Output Files

24 Hours Post Close to last Account Processing

5 6 7 8 9 10

Produce Control Reports

Generate Output File

Produce Summary Reports

10.1

10.2

10.3

Determine Approval Method

8.1

Assign Pending Accounts to

Agents

Capture Information for Broker Accounts

Capture Information for Non-Broker AR

Accounts

Manual Update

Automated Update

Manual Approval

Automated Approval

5.1

6.2

6.3

7.1

7.2 8.2

8.3

Capture Information for Bank Customer

Accounts

6.1

Match and Merge Records

7.3

Pre-Insurance Determination

Calculate Insurance

9.1

9.2

Apply Insured and Uninsured Amounts

9.3

3.2 Pending File (Input, Process, and Output)

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 14

Step 6: Gather Required Information for Pending Accounts

Major Activity: Conduct outreach to gather and capture information needed to complete the deposit insurance determination.

Key Inputs Key Outputs

— Allocation of pending accounts to agents — Captured Information to be updated

Key Steps: The following activities are conducted by CI systems and utilized by the FDIC in order to capture data needed to complete the deposit insurance determination.

Capture Information for Bank Customer Accounts: Update all aspects of the account that will be

used to determine insurance.

— The CI system to capture all outbound information provided by the customer

Capture Information for Broker Accounts: Update all aspects of the broker account that will be used

to determine insurance.

— The FDIC to contact the broker for information on pending accounts

— The FDIC to anticipate the broker communicating via a flat file which can be loaded into the CI’s

system

Capture Information for Non-Broker Alternative Record Keeping Accounts: Update all aspects of

these accounts, which will be used by:

— The FDIC to contact the third party for information on accounts

— The FDIC to anticipate the third party communicating via a flat file which can be loaded into the

CI’s system

Step 7: Update Bank Systems

Major Activity: Update the information provided by customers, brokers, and third parties into the CI’s systems for the purposes of calculating deposit insurance.

Key Inputs Key Outputs

— Captured Information to-be Updated — Updated Customer and Account Information — Supporting Documentation — Audit Log of Changes

Key Steps: The following activities are conducted by the CI systems and utilized by the FDIC to update bank systems.

Manual Update: Manual upload/type of information provided by customers directly into a data

capture system. Importantly, the CI system is required to:

— Provide the capability for an FDIC claims agent to manually update all data elements required to

support the recalculation of deposit insurance

— Provide the capability to attach additional documentation, such as electronic trust documents,

declarations to support any updates

— Assess the quality and completeness of the data provided by the customer in line with its

internal data quality requirements

— Track the updates made to each element by a user, including the old and new values and the

date and time of the update

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 15

Automated Update: Upload of information provided by brokers or third parties directly into a data

capture system. Importantly, the CI system is required to:

— Provide the capability for an automated file load to update all data elements required to

support the recalculation of deposit insurance, in line with the agreed broker and third-party

data exchange formats

— Assess the quality and completeness of the data provided by the third parties in line with their

internal data quality requirements

— Provide the capability for any erroneous load of data to be either rolled back in full or manually

adjusted and reprocessed

— Track the updates made to each element and record by the automated file import, including the

old and new values and the date and time of the update

— Maintain a static read only copy of the file that was updated successfully for audit purposes

Match and Merge Customers/Account Participant Records: Once the data has been loaded into the

system, the CI system should have capability to:

— Match and merge any new customer records provided within the existing customer records held

by the CI

— Match and merge any new account participant records provided within the existing account

participant records held by the CI

The CI is responsible for the development of any matching rules, and the CI will apply matching rules in line with Anti-Money Laundering and Know Your Customer rules.

Step 8: Review and Approve Updates

Major Activity: The deemed approver at the FDIC reviews and approves updates from FDIC claims agents that are providing information for pending accounts.

Key Inputs Key Outputs

— Updated Customer and Account Information — Supporting Documentation — Audit Log of Changes

— Approval or Rejection of Account Updates — Updated Information ready for Insurance

Determination

Key Steps: The following activities are conducted by the CI systems and utilized by the FDIC to ensure that information input into CI systems is validated and approved.

Determine Approval Method: Route the approval of the update to either the manual or automated

approval methods. To enable this capability the CI is required to:

— Provide the capability to segment approval channel by ORC, product type, total account value,

total insured amount, and other factors

— Provide the capability for multi-level approvals, allowing for at least two tiers of approvals. The

determination of the tiers should be driven based on the same attributes above

— Provide approver access to all accounts owned by unique depositor

Manual Approval: If a manual approval is required based on a set of metrics (e.g., account balance,

insured amount, etc.), the CI system must be able to:

— Allocate the record to the correct approver, based on the approval matrix noted above

— The manual approver must be able to review attachments from the FDIC resolution agent. The

needed information on what modification was done and the supporting information for the

modification

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 16

— The manual approver must be able to approve and reject records. It is expected that a standard

list will be created by the CI in its systems, but, at a minimum, two categories, “More

Information Required” and “Disagree with Assessment,” are expected

Automated Approval: If no manual approval is required, execute automated approval if permissible

based on a set of metrics (e.g., account balance, insured amount, etc.).

Step 9: Recalculate and Apply Deposit Insurance

Major Activity: Aggregate depositor accounts for all ORCs, and perform and apply deposit insurance rules to all eligible deposit accounts held at the CI.

Key Inputs Key Outputs

— Approval or Rejection of Account Updates — Updated Information Ready for Insurance

Determination

— Updated Deposit Insurance Determination — Allocation of Insured / Uninsured Amounts by

Accounts

Key Steps: The following activities are conducted by the CI systems utilized by the FDIC to calculate and determine deposit insurance.

Pre-Insurance Determination: Identify pre-insurance determination under the Deposit Insurance

Determination as outlined in Section 4.1 of this document.

Calculate Insurance: Recalculate insurance under the Deposit Insurance Determination as outlined

in Section 4.2 of this document.

Apply Insured and Uninsured Amounts: Allocate insured and uninsured balance among account

owners under the Deposit Insurance Determination as outlined in Section 4.3 of this document.

Step 10: Generate Output Files

Major Activity: Following the recalculation of deposit insurance, the CI system will regenerate all the Output Files that will act as the permanent record of the deposit insurance determination. Importantly, the requirement is to regenerate the files in full, and not only to produce the variances that have been updated. In addition to the permanent record, the CI’s system is required to generate the control and summary reports that will verify accuracy and completeness of the determination.

Key Inputs Key Outputs

— Updated Deposit Insurance Determination — Allocation of Insured / Uninsured Amounts by

Accounts

— Customer File — Account File — Account Participant File — Pending File — Summary Reports — Control Reports

Key Steps: The following activities are conducted by the CI system and utilized by the FDIC to ensure that Output Files are generated.

Generate Output File: Regenerate four files required as a part of Part 370, in line with the Output

File creation details in Section 4 of this document and outlined in Appendix A. The four key files are:

— Customer File: The Customer File is used by the FDIC to capture indicative information regarding

the Account owners

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 17

— Account File: The Account File specifies the insured and uninsured balances available to each

account

— Account Participant File: The Account Participant File identifies account participants, captures

indicative information, and captures account participant allocations.

— Pending File: The Pending File captures accounts that require additional information before a

deposit insurance determination can be completed.

Produce Control Reports: Generate control reports and validate that the total account population

considered for insurance determination matches the total value of accounts in the account and

Pending Files. The CI system should generate the control reports outlined in Section 6.3 of this

document that will confirm that baseline data reconciles with final output of all accounts.

Produce Summary Reports: Generate the summary reports required by the FDIC and the CI that

highlight the total account allocations by various dimensions. The details of the specific account

summary reports required are outlined in Section 7 of this document.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 18

4 Deposit Insurance Determination Requirements

In the event that a CI fails, the following process must be followed to accurately identify each account’s right and capacity for its owner(s) and determine the deposit insurance coverage for each account/account owner. References to actions to be taken by a CI and/or its systems after the FDIC has been appointed receiver are intended to be taken at the direction of or on the behalf of the FDIC in its receivership capacity, as applicable. The CI’s systems must be able to:

1) Identify each account and its owner(s) and determine if the CI has enough information for making a deposit insurance determination for each account/account owner within 24 hours of bank failure.

2) Make the right and capacity determination for each account/account owner and determine the deposit insurance coverage for the account/account owner based on the right and capacity and the deposit insurance calculation rules described in the following sections for accounts in that right and capacity.

3) Apply insured and uninsured funds determined in capability number 2 above.

The following sections describe the process necessary for completing meeting capabilities 1-3 above. Accounts should be processed in the manner described in Sections 4.1 through 4.3 below (these processes are intended to be performed in sequential order, beginning with Section 4.1).

Note, for purposes of this document, the right and capacity determination and the deposit insurance calculation processes have been documented by right and capacity. Please refer to the corresponding segment of Section 4.2 below for details of these two processes.

4.1 Initial Processing

4.1.1 Overview

This section outlines the initial processing steps that must be performed on an account before making an insurance determination. Before making an insurance determination, the CI must identify if the necessary account information is known, if an account belongs to recently merged IDIs, and if an account is a fiduciary account.

4.1.2 Identification of Account Information

1) If the CI lacks sufficient information for identifying account owner(s), beneficiary, or fiduciary (e.g., trustee, agent, custodian), then place the account in the Pending File (see Section 5.4 of this document).

2) For an account for which an account owner is identified:

a) If the account lacks sufficient information for purposes of calculating the deposit insurance coverage, then place the account and the account owner in the Pending File (see Section 5.4 of this document)

4.1.3 Merger of IDIs

If there is a recent merger of two IDIs, then the CI may be required to separately calculate deposit insurance and generate a separate set of Output Files (one from the acquired IDI and the other from the acquiring IDI. If the account does not belong to a recently merged IDI (more than six months prior to the CI failure) or if the depositor only holds funds at one of the two IDIs that merged, then proceed to Section 4.2 of this document. 1) If there is a merger which occurred less than six months prior to CI failure, the CI calculates deposit insurance

on the accounts at each of the merged entities separately and produces a set of files for each.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 19

2) If the merger occurred more than six months prior to failure, the CI must:

a) Separately insure time deposits that mature after the six-month grace period until they mature and separate these accounts and produce a set of files for these accounts.

b) Separately insure time deposits that are renewed on identical terms within the first six months after the effective date of the merger until the first maturity date after the expiration of the six-month period and produce a set of files for these accounts.

c) If the above account scenarios do not exist, the CI should process all accounts in a single insurance determination and produce a single set of files.

4.1.4 Alternative Recordkeeping and Fiduciary Accounts

If an account meets FDIC’s definition of fiduciary account2:

1) If sufficient information of a principal and his ownership interest in the fiduciary account is available so that the deposit insurance coverage can be determined within 24 hours of bank failure, then place the account and the principal in the Account File.

2) If sufficient information of a principal and/or his ownership interest in the fiduciary account is not available so that the insurance determination cannot be completed within 24 hours of bank failure, then place the account and the principal in the Pending File.

3) If the account and principal are placed in the Pending File, then determine the deposit insurance coverage upon obtainment of sufficient information based on the actual right and capacity of the funds held by the principal.

4.1.5 Pre-Insurance Determination

If an account owner’s aggregate balance at a CI is no more than $250,000, then all the funds the account owner has at a CI are fully insured and do not require an insurance determination.

4.2 Right and Capacity and Deposit Insurance Determination

4.2.1 Overview

This section outlines the steps for completing the ORC, SMDIA, and deposit insurance determinations on accounts. For purposes of this document, the ORC, SMDIA, and deposit insurance determinations have been grouped by right and capacity. The ORC determination for each account/account owner must be made first. After the ORC determination has been made, follow the procedures outlined below for accounts in each ORC to make deposit insurance determination for each account/account owner.

4.2.2 Single Accounts

4.2.2.1 Right and Capacity and SMDIA Determination

Determine if account meets FDIC requirements for a single account:

1) Identify account owner(s).3

2) If there are multiple account owners, refer to section 4.2.3 of this document for Joint Accounts.

2 Fiduciary accounts are deposit accounts established by a person or entity (the fiduciary) for the benefit of one or more parties,

also known as principals. Fiduciary accounts are not insured as a separate ORC and the deposit insurance coverage for such accounts depends on the actual ORC in which the principal or owner holds the funds. As a result, fiduciary accounts are added to the principal’s other accounts in the same ORC at the same CI for purpose of a deposit insurance determination. 3 Account owner shall be deemed as a depositor entitled to up to the SMDIA as provided for under the applicable ownership

category.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 20

3) If the account owner has designated eligible beneficiaries, then refer to Section 4.2.4 or Section 4.2.5 of this document for either revocable or irrevocable trust accounts.

4) If the account is a self-directed retirement plan account, then refer to Section 4.2.6 of this document for Certain Retirement Accounts.

5) If an account owner is deceased, then:

a) If within six months of the death of the account owner, then the decedent should be treated as though he or she were still alive, assuming no change to the titling of the account and this treatment benefits the depositor.

b) If the account owner has been deceased for more than six months, then calculate deposit insurance based on the actual ownership.

c) If the deceased is the sole owner of the single account, funds in all single accounts held by the deceased owner at the CI is insured up to SMDIA.

6) If an account meets the definition of a single account (see Appendix B), then set DP_Right_Capacity equal to SGL.

7) The account owner of a single account for the combined amount of his or her interests in all single accounts at the same CI is entitled to SMDIA.

4.2.2.2 Single Account Deposit Insurance Calculation

If all single accounts have been processed through Section 4.2.2.1 Right and Capacity and SMDIA Determination or placed in the Pending File (see Section 5.4 of this document), then:

1) Identify all single account owners.

2) Aggregate total account balance and accrued interest by each unique account owner for all accounts held by the owner in the single account right and capacity at the CI. If this is a second or successive iteration of the Deposit Insurance Determination due to newly identified account(s), the accounts in the same ORC from the previous determination must be aggregated with the newly identified account(s).

3) For the aggregated account balance and accrued interest for each account owner:

a) If the total balance and accrued interest does not exceed SMDIA, then the funds are fully insured and the insured amount for each account is equal to the sum of balance and accrued interest.

b) If the total balance and accrued interest exceeds SMDIA, then funds in excess of SMDIA are not insured.

4) If there are uninsured funds for the account owner, then:

a) Apply the uninsured amount first to the accrued interest (if any) of each account.

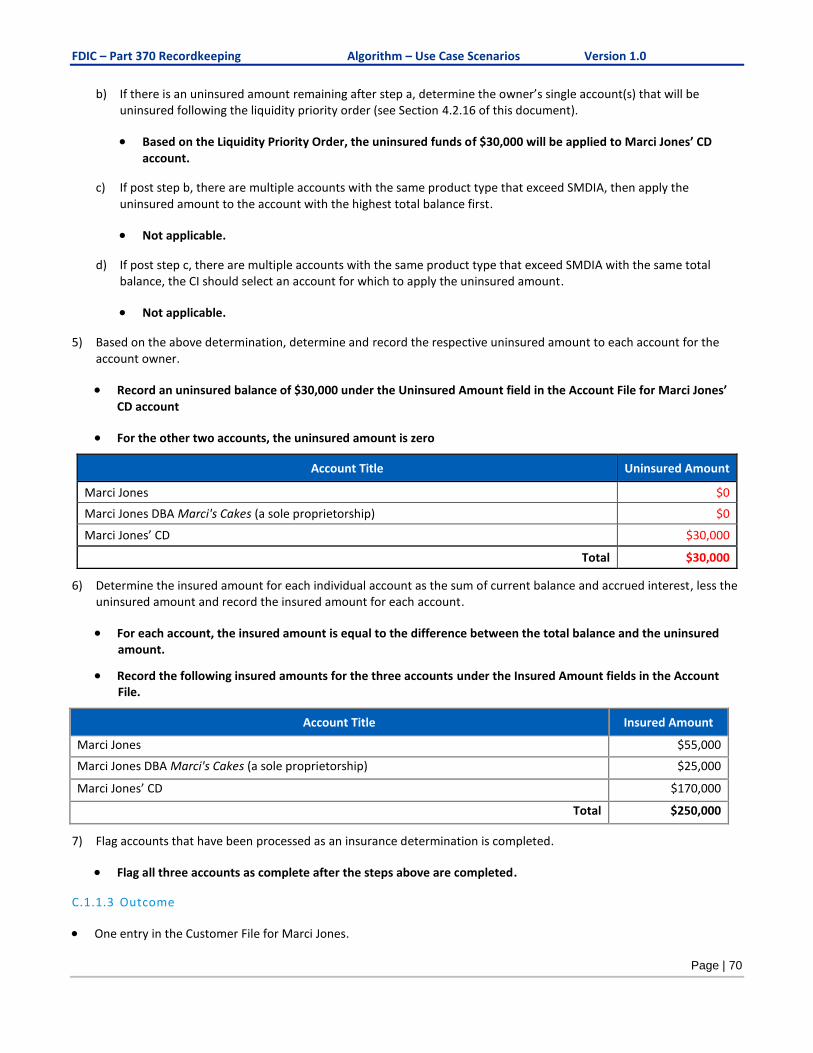

b) If there is an uninsured amount remaining after step 4 (a), determine the owner’s single account(s) that will be uninsured following the liquidity priority order (see Section 4.2.16 of this document).

c) If after step 4 (b), there are multiple accounts with the same product type that exceed SMDIA, then apply the uninsured amount to the account with the highest total balance first.

d) If after step 4 (c), there are multiple accounts with the same product type that exceed SMDIA with the same total balance, the CI should select an account for which to apply the uninsured amount.

5) Based on the above determination, determine and record the respective uninsured amount to each account for the account owner.

6) Determine the insured amount for each individual account as the sum of current balance and accrued interest, less the uninsured amount and record the insured amount for each account.

7) Flag accounts that have been processed as an insurance determination is completed.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 21

4.2.3 Joint Accounts

4.2.3.1 Right and Capacity and SMDIA Determination

Determine if account meets FDIC requirements for a joint account:

1) Identify all co-owners of the account and their withdrawal rights.

2) If withdrawal rights are unequal across all co-owners, then refer to Section 4.2.2 of this document for Single Accounts.

3) If an account co-owner is deceased, then:

a) If within six months of the death of the account co-owner, the decedent should be treated as though he or she were still alive, assuming no change to the titling of the account.

b) If the account co-owner has been deceased for more than six months, the decedent is not considered an account co-owner. As a result, calculating deposit insurance based on the actual ownership may cause funds to revert from the joint account category to the single account category if there are no longer multiple account owners. Please refer to Section 4.2.2 of this document for SMDIA Determination for details on the determination for the single account category.

4) If account meets the definition of a joint account (see Appendix B), then set DP_Right_Capacity equal to JNT.

5) Split the total account balance and accrued interest equally across the total number of account co-owners.

6) Each co-owner of a joint account for their combined amount of his or her interests in all joint accounts at the same CI is entitled to SMDIA.

7) EACH DEPOSITOR IS ENTITLED TO INSURANCE UP TO THE SMDIA IN EACH ORC. DUE TO THE JOINT OWNERSHIP NATURE OF THIS ORC, EACH DEPOSITOR IS SUBJECT TO DEPOSIT INSURANCE COVERAGE LIMITS ON AN INDIVIDUAL BASIS BUT THE DEBITS ARE APPLIED ON AN ACCOUNT LEVEL.

4.2.3.2 Joint Account Deposit Insurance Calculation

If all joint accounts have been processed through Section 4.2.3.1 Right and Capacity and SMDIA Determination or placed in the Pending File (see Section 5.4 of this document), then:

1) Identify all unique joint account co-owners.

2) Aggregate total account balance and accrued interest for each unique account owner for those accounts held in the JNT right and capacity. If this is a second or successive iteration of the Deposit Insurance Determination due to newly identified account(s), the accounts in the same ORC from the previous determination must be aggregated with the newly identified account(s).

3) For the aggregated account balance and accrued interest for each account owner:

a) If the total balance and accrued interest of an account owner does not exceed SMDIA, then the funds of the account owner across all joint accounts at the CI are fully insured.

b) If the total balance and accrued interest of an account owner exceeds SMDIA, then the owner’s funds in excess of SMDIA are not insured. If there are uninsured funds, then:

c) Determine the uninsured amount for each account owner based on steps 3(a) and 3(b) above.

4) If there is an uninsured amount for an account owner:

a) Determine the allocation ratio for each owner with uninsured funds by dividing the owner’s uninsured amount by the owner’s aggregate total balance.

b) Apply the uninsured amount first to the accrued interest (if any) of all such accounts.

c) If there is an uninsured amount remaining after step 4(b), allocate remaining uninsured funds of each owner based on the allocation ratio calculated above across all such accounts.

FDIC – Part 370 Recordkeeping Information Technology Functional Guide Version 1.0

Page | 22

5) Based on the above determination (and repeat as necessary for each account owner), determine and record the respective uninsured amount for each account of the account owner.

6) The insured amount of the owner for each individual account is the difference between the owner’s funds in that account and the uninsured amount determined based on the steps above.

7) Flag the owner’s accounts that have been processed as an insurance determination is completed.

4.2.4 Revocable Trust Accounts

4.2.4.1 Right and Capacity and SMDIA Determination

Determine if account meets FDIC requirements for a revocable trust account:

1) Identify all account owner(s) and all unique primary beneficiaries.

a) A beneficiary is a primary beneficiary if his or her interest in the trust does not depend on the death of another trust beneficiary.

2) If an account owner is deceased, then:

a) If within six months of the death of the account owner, the decedent should be treated as though he or she were still alive, assuming no change to the titling of the account.

b) If the account owner has been deceased for more than six months, the decedent is not considered an account owner. Instead, the estate of the decedent is considered the actual owner of the account. As a result, calculate the deposit insurance by treating the estate of the decedent as the account owner.

3) Identify eligible unique primary beneficiaries.

a) If a primary beneficiary is deceased, then:

i) If there is no substitute or contingent beneficiary named in the revocable trust document for that primary beneficiary, then the beneficiary should be ignored for purposes of deposit insurance calculation.

(1) Funds associated with that primary beneficiary should be treated as funds in a single or joint account ORC belonging to the trust account owner(s) and aggregated and insured with other accounts of the trust account owner(s) in the corresponding ORC.

ii) If the trust document indicates the interest associated with the deceased primary beneficiary is passed to other beneficiaries (e.g., per stirpes

4 or per capita), determine the eligibility of the

successor beneficiaries and the total number of unique eligible beneficiaries (including eligible successor beneficiaries) for purposes of deposit insurance determination.

b) For Payable-on death (POD) revocable trust account.

i) If a beneficiary is ineligible,5 then the beneficiary should be ignored for purposes of deposit insurance