Embed Size (px)

Citation preview

Information Asymmetry and the Cost of

Capital: the Role of Market Non-participation

Yaping Wang and Yunhong Yang

Guanghua School of Management

Peking University

Presentation at

Dongbei University of Finance and Economics

December 8, 2014

• Overview– Research questions

– Economic forces and main results

– Related literatures

• Model and equilibrium– Markets, information, ambiguity, informed and uninformed

investors’ demand

– Equilibrium

• Model implications– Information asymmetry and market non-participation

– Cost of capital

– Information asymmetry and the cost of capital

• Conclusion

2014年杨云红 2

Overview: Research questions

• How information asymmetry among investors

affects the cost of capital?

• What policies do we might apply in order to

reduce the cost of capital in an asymmetry-

information market?

2014年杨云红 3

Overview: Motivation

• Fundamental to a variety of corporate decisions is a firm’s cost of capital, a wide range of policy prescriptions have been advanced to help companies lower this cost: accounting standards, market microstructure

• Whether and how information asymmetry among investors affects stock pricing have been long-standing concerns for both accounting/finance academics and practitioners. The consequences of information asymmetry in capital markets, and, in particular, its relation to the cost of capital, are still much debated.– uninformed investors require a risk premium to compensate them for

the adverse selection problem that arises from trading with informed traders, market liquidity will be reduced

– informed trading also makes prices more informative, thereby reducing the risk for the uninformed and lowering the risk premium

2014年杨云红 4

Overview: Motivation

• There exists a gap between the views of the academy

and practitioners in order to reduce the cost of capital

in a asymmetry-information market

– Extant theory research addresses the effect of information

asymmetry among investors on stock pricing in a perfect

competitive market from the perspective of information quantity,

i.e., how information asymmetry affects the information quantity

contained in that market.

– Practitioners, in contrast, treat information asymmetry more

from the perspective of investor confidence in market integrity

and market participation.

2014年杨云红 5

Overview:Economic forces and main results

• Financial market participants absorb a large amount of news, or signals, every day. Processing a signal involves quality judgments: News from a reliable source should lead to more portfolio rebalancing than news from an obscure source.

• Unfortunately, judging quality itself is sometimes difficult. The uncertainty associated with observed public information is essentially different from the uncertainty associated with learned private information for uninformed investors.

2014年杨云红 6

Overview:Economic forces and main results

• For observed public information, such as earnings reports, the uncertainty is based on objective probability. By looking at past data, investors may become quite confident about how well earnings forecast returns.

• For learned private information, the uncertainty associated is based on subjective probability. For example, stock picks from an unknown newsletter without a track record might be very reliable or entirely useless—it is simply hard to tell.

• The former is usually referred to as risk while the latter is usually referred to as ambiguity or Knightian uncertainty. – Ellsberg (1961) showed that people treat them differently and are more

averse to ambiguity than risk.

– Multiple (ambiguous) prior models have been proposed to capture Knightian uncertainty, and the min-max utility function was developed to model this ambiguity aversion (Gilboa and Schmeidler 1989).

2014年杨云红 7

Overview:Economic forces and main results

• When ambiguity aversion exists, information asymmetry among investors makes the private information embedded in price ambiguous, inducing uninformed investors to reluctantly participate in the market, resulting in extra cost of capital (ambiguity premium). Hence, the cost of capital consists of both risk premium and ambiguity premium.

• The risk premium decreases as private-information precision increases if public information is given, but it is independent of the level of information asymmetry if the total information in market is given.

• In contrast, market non-participation and the ambiguity premium increase along with the level of information asymmetry.

• Hence, private-information precision has an uncertain effect on the total cost of capital (risk premium plus ambiguity premium) when public information is given. Under certain circumstances, the cost of capital may have an inverse U-shape relationship with private-information precision.

2014年杨云红 8

Overview:Economic forces and main results

• The risk and ambiguity premiums help to fill the gap between academics (Leland 1992; Lambert et al. 2011) and practitioners. – Leland (1992) argued that insider trading could improve

market efficiency. Lambert et al. (2011) believed that the cost of capital is independent of information asymmetry if the total information in market is given.

– However, the SEC (2000) believed that selective disclosure and insider trading could induce a higher cost of capital because uninformed investors reluctantly participate in the market due to loss of confidence in market integrity.

– The arguments of Leland (1992) and Lambert et al. (2011) fit the risk premium precisely, whereas the SEC’s (2000) belief fits the ambiguity premium.

2014年杨云红 9

Overview: three related literatures

• The effect of information asymmetry among investors on stock pricing in a perfect competitive market – Leland (1992) found that allowing insider trading would increase information quantity and stock

prices despite insider presence increasing information asymmetry in the economy.

– Based on the framework of Grossman and Stiglitz (1980), Easley and O’Hara (2004) built an equilibrium model with a fraction of the total information classified as private—that is, known to a fraction of investors—and concluded that the cost of capital is positively correlated with the private-information percentage.

– Based on Wang’s (1993) observation that an increase in private information in the economy affects both information asymmetry and the precision of total information, Lambert et al. (2011) built a multi-asset perfect competition equilibrium model and found that information asymmetry among investors only affects a firm’s cost of capital through investors’ average information precision and not the level of information asymmetry.

– Liquidity risk is another indirect channel through which information asymmetry affects the cost of capital. Greater information asymmetry induces a higher liquidity risk (Amihud and Mendelson 1986), and liquidity risk is closely related with asset pricing (Amihud 2002). Diamond and Verrecchia (1991) examined this liquidity channel.

– Hughes et al. (2007) examined a market with infinite assets. Lambert and Verrecchia (2010) considered imperfect competition among investors and found that interaction between illiquid markets and asymmetric information gives rise to a role for information in the cost of capital that is absent in perfect competition settings.

2014年杨云红 10

Overview: three related literatures

• The impact of Knightian uncertainty and ambiguity aversion on asset prices – Cao et al. (2005) and Easley and O’Hara (2009) used it to explain limited

market participation,

– Anderson et al. (2009) and Epstein and Schneider (2008) examined its impact on cross-sectional stock returns,

– Epstain and Miao (2003) and Kirabaeva (2009) modeled equity investment home bias using asymmetric ambiguity aversion.

– Mele and Sangiorgi (2011) added ambiguity aversion into Grossman and Stiglitz’s (1980) model and examined how the endogeneity of information acquisition affects asset market equilibrium and stock price volatility.

– Anderson(2012), Cao et al. (2005), Caskey (2008), Easley and O’Hara (2009), and Mele and Sangiorgi (2011), Qian and Riedel(2014) introduced information ambiguity without information asymmetry.

– Easley and O’Hara (2010) give the microstructure foundation for ambiguity.

– Epstein and Schneider (2010), Guidolin and Rinaldi (2010) review the literature for ambiguity in asset pricing and portfolio choice.

2014年杨云红 11

Overview: three related literatures

• Empirical findings. – Easley et al. (2002) and Bardong et al. (2009) used the

probability of information-based trading (PIN) developed in the microstructure model of Easley et al. (1996) to measure an individual firm’s information asymmetry and found that it is positively related with the firm’s cost of capital. Botosan et al. (2004) used the Barron, Kim, Lim, and Stevens (BKLS) model (Barron et al. 1998) to estimate public and private information contained in analyst forecasts, and found that the cost of equity capital increases along with private information when public information is controlled.

– Chen et al. (2010) found that firms’ cost of capital decreases after Reg FD, whereas Duarte et al. (2008) found that it increases subsequent to Reg FD.

2014年杨云红 12

Model and equilibrium: the market

• One-period: investment portfolio at time 0, and the investment assets pay off at time 1.

• Two assets in the market: risk-free and risky– The risk-free asset

• perfectly elastic supply

• acts as the numéraire of the economy.

• the net supply is zero.

• the return on the risk-free asset is zero.

– The risky asset• the payoff unknown to investors until time 1.

• the net supply

• Traders trade at price p per share at time 0 and receive payoff of per share at time 1.

2014年杨云红 13

),(~ 1 N

),(~~ 1zNz

Model and equilibrium: the investors

• Two types of investors: informed and

uninformed.

– rational in terms of maximizing utility based on

available information about the future value of the

risky asset.

– the same negative exponential utility function

defined on wealth W at time 1, with constant

absolute risk aversion

– different in terms of the information received.

2014年杨云红 14

0

Model and equilibrium: information structure

• Two kinds of information: public and private.

– Public information is available to all investors

• Realized at time 0 and is observable to all investors. The realization of the public signal is y.

– Private information is available only to informed investors.

• It is also realized at time 0, but is observable only to informed investors. The realization of the private signal is x.

– The fraction of informed investors in the total rational investors be and that of uninformed investors be

2014年杨云红 15

y~

yy ~),0(~ 1 Ny

xx ~ ),0(~ 1 Nx

1 10

Model and equilibrium: the ambiguity

• The public information– both informed investors and uninformed investors have correct

prior about its distribution

• The private information– the informed investors have a correct prior about its distribution

– the uninformed investors’ prior about the distribution of private information is

• the length of this interval, , measures the degree of ambiguity

2014年杨云红 16

),0(~ 1 Nx

xx ~),(~ 1 xx N ],[ x 0

),0(~ 1 Ny

2

Model and equilibrium: informed investor’s

demand

• An informed investor chooses a portfolio to maximize his or

her conditional expected utility given available information :

• The informed investors’ demand for the risky security

2014年杨云红 17

iI

22 )|(5.0))|(()()|(),( iiiii xIVarxpIE

i

xp

iii eIeEIxv

)|(

)|(

i

ii

IVar

PIEx

)(

1

pxy

pxy

Model and equilibrium: uninformed investor’s

demand

• conjecture the equilibrium price form

• use the price function to derive the demand function

• use the market clear condition to solve the price function and

verify that it fits our initial conjecture.

2014年杨云红 18

Model and equilibrium: uninformed investor’s

demand

• Define the compound signal of private information and

random supply

• the priors for private information are ambiguous the

compound signal s is also ambiguous information

2014年杨云红 19

x~z~

sx zzxzxs

~~~)~,~(~

),(~ 1

z

s N

1)(

1 21

),(~ 1 Ns],[

z

z

Model and equilibrium: uninformed investor’s

demand

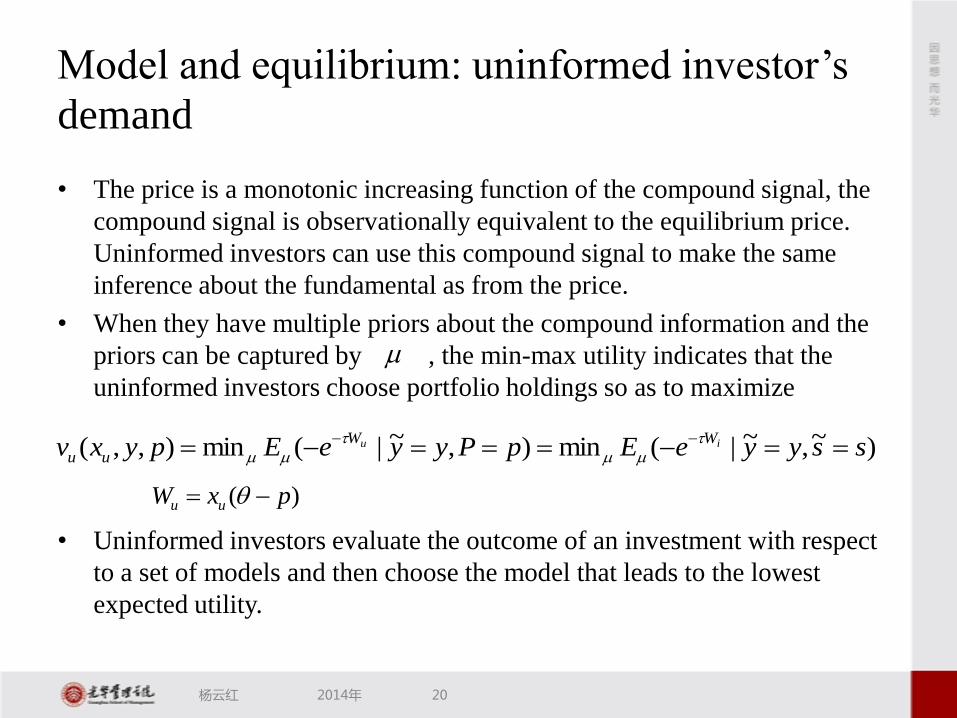

• The price is a monotonic increasing function of the compound signal, the

compound signal is observationally equivalent to the equilibrium price.

Uninformed investors can use this compound signal to make the same

inference about the fundamental as from the price.

• When they have multiple priors about the compound information and the

priors can be captured by , the min-max utility indicates that the

uninformed investors choose portfolio holdings so as to maximize

• Uninformed investors evaluate the outcome of an investment with respect

to a set of models and then choose the model that leads to the lowest

expected utility.

2014年杨云红 20

)~,~|(min),~|(min),,( ssyyeEpPyyeEpyxv iu WW

uu

)( pxW uu

Model and equilibrium: uninformed investor’s

demand

2014年杨云红 21

)~,~|(min),~|(min),,( ssyyeEpPyyeEpyxv iu WW

uu

)),|(5.0}]),|({[minexp(22

uu xsyVarxpsyE

• Simplify the formula

• Define

• So

),,()(

),|(

syMsy

syE

0

0

)),,(

)),,(}]),|({[min

u

u

u

u

ux

x

if

if

xpsyM

xpsyMxpsyE

Model and equilibrium: uninformed investor’s

demand

• The demand function for uninformed investors

2014年杨云红 22

),,(

)],,(),,,([

),,(

),|(

)),,(0

),|(

)),,(

)),(,,(

syMp

syMsyMp

syMp

for

syVar

psyM

syVar

psyM

syPypxu

1),|( syVar ),,(),,( syMsyM

Model and equilibrium: uninformed investor’s

demand

2014年杨云红 23

),,( syM),,( syM

Demand

p

0

Model and equilibrium: uninformed investor’s

demand

• Uninformed investors will participate in the market only when the observed

equilibrium price is sufficiently favorable to them. This favorable price has

to be able to bring the investors positive expected profit, even in the worst-

case scenario.

– The worst-case expected profit is precisely per share when

investors long the risky asset, and per share when they

short the asset.

• Uninformed investors do not participate in the asset market if equilibrium

price realization p is not favorable enough

• Naturally, the price function P(y, x, z) and cutoff prices and

are all endogenous, to be determined in equilibrium.

2014年杨云红 24

psyM ),,(

),,( syMp

)],,(),,,([ syMsyMp

),,( syM ),,( syM

Model and equilibrium: equilibrium

• In equilibrium, risky asset demand is equal to supply

2014年杨云红 25

zsyPypxxypx ui )),(,,()1(),,(

Model and equilibrium: equilibrium

• Proposition 1: The equilibrium price is a piecewise linear in

the compound signal and public information

2014年杨云红 26

BAq

BAqBA

BAq

for

sy

sy

sy

syP

)1(

))1(()1(

)1(

))1(()1(

),(

q

z

q VV

ysq

)()(

2)( qV

q

z

VA

)(

)(

qVB

)(

)(

)1,0(~ Nq

Model and equilibrium: the special case

• A special case where there is no ambiguity

• Equilibrium price reduces to a simple linear function

• This is equivalent to the price function (15) of Easley and

O’Hara (2004).

2014年杨云红 27

0

0B

z

),()1(

))1(()1(

),( syP

sy

syP b

z

Model and equilibrium: the special case

• Rewrite the general equilibrium price function as

• The difference between the general price function and the benchmark price function caused by ambiguity is piecewise linear in compound variable q,

• When there is no ambiguity ( ), there is no price difference

2014年杨云红 28

)(),(),( qPsyPsyP b

0

BAq

BAqBA

BAq

for

qV

qP

zq

)-(1

)-(1

))-(1)((

)()-)(-(1

)-(1

)-(1

)(

0B 0)( qP

Model Implication: Information asymmetry and

market non-participation

• When the equilibrium market price is sufficiently low ( ), or the

compound variable q , uninformed investors long the risky asset, but

ambiguity aversion causes them to hold fewer risky assets than the benchmark case;

hence, the equilibrium price is lower than the benchmark case by amount

2014年杨云红 29

),,( syMP

BA

)-(1

)-(1

Model Implication: Information asymmetry and

market non-participation

• When the equilibrium market price is sufficiently high ( ), or the

compound variable q , uninformed investors short the risky asset, but

ambiguity aversion causes them to short fewer risky assets than the benchmark

case; hence, the equilibrium price is higher than the benchmark case by amount

•

2014年杨云红 30

),,( syMP

BA

)-(1

)-(1

Model Implication: Information asymmetry and

market non-participation

• When the equilibrium market price is not favorable enough, or the compound

variable q is between level and level , uninformed investors do not

participate in the market at all; hence, the investor base is smaller than that of the

benchmark case, which causes a linear price difference between the two cases.

2014年杨云红 31

BA BA

Model Implication: Two information symmetry

cases

• All investors are informed– no price difference

– As nobody is at an information disadvantage, there is no information ambiguity and hence no market non-participation problem.

• All investors are uninformed– uninformed investors’ learned information has zero precision

– there is no non-participation problem

•

– When there are no informed investors, uninformed investors have nothing to learn; hence, there is no information ambiguity.

• These two cases clearly show that information asymmetry can induce information ambiguity.

2014年杨云红 32

1

0)( qP

0

0

BABAqP ,0)(

Model Implication: Information asymmetry and

market non-participation

• Proposition 2: When information asymmetry exists, the level

of uninformed investors’ market non-participation increases as

private information precision increases or public information

precision decreases. When private information precision is big

enough, uninformed investors do not participate in the market

at all. Or mathematically, when , we have

and

2014年杨云红 33

10

0

B0

B

Blim

Model Implication: Information asymmetry and

market non-participation

• This proposition demonstrates that the higher the information asymmetry level (the larger the ratio of private information to the total information caused by more private information or less public information), the more severe the market non-participation problem. Because higher information asymmetry means that uninformed investors face a severer information disadvantage, they participate in the market less. Furthermore, when the information asymmetry is severe enough, uninformed investors will completely lose confidence in the market’s integrity and keep out of it altogether. This is the aftermath of insider trading.

• Cao et al. (2005) and Easley and O’Hara (2009) used ambiguity aversion directly to explain the market non-participation problem. In their models, all information is ambiguous, and heterogeneous ambiguity-aversion levels among investors cause some investors not to participate in the market. In our model, information asymmetry induces information ambiguity, which further discourages uninformed investor participation in markets.

2014年杨云红 34

Model Implication: The cost of capital

• Define the cost of capital as

– The average return of the risky asset for investors

– The average difference of what the firm holders are selling ( ) and

what they can get (the selling price, P).

– The expectation is computed with respect to all prior information.

2014年杨云红 35

)())|(( PEPIEE

Model Implication: The cost of capital

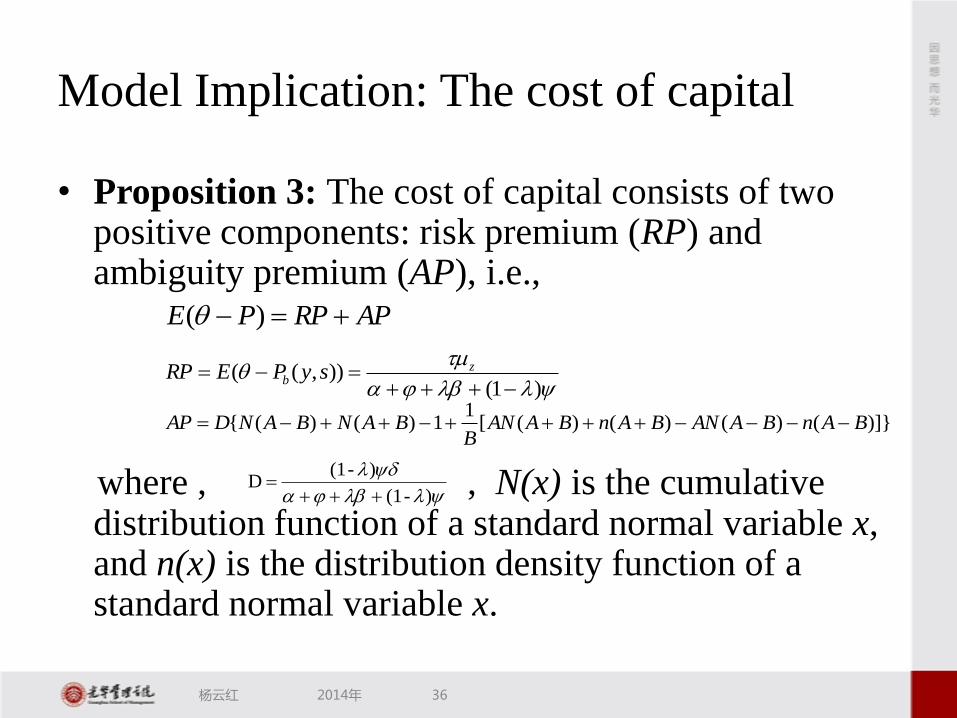

• Proposition 3: The cost of capital consists of two positive components: risk premium (RP) and ambiguity premium (AP), i.e.,

where , , N(x) is the cumulative distribution function of a standard normal variable x, and n(x) is the distribution density function of a standard normal variable x.

2014年杨云红 36

APRPPE )(

)1()),((

z

b syPERP

)]}()()()([1

1)()({ BAnBAANBAnBAANB

BANBANDAP

)-(1

)-(1D

Model Implication: The cost of capital

• The first item – corresponds with the benchmark case

– this part is the usual risk premium

– when the investors are all risk neutral, i.e., , it is zero. • If agents are risk neutral, then the asset’s underlying risk does not

matter to them; hence, the information structure does not matter.

• The second item – corresponds with the price difference

– this part is caused by ambiguity aversion, and is ambiguity premium

– when there is no ambiguity ( ), the ambiguity premium is zero

– the ambiguity premium is positively associated with the magnitude of ambiguity

2014年杨云红 37

RP

0

0

BP

Model Implication: Information asymmetry and

the cost of capital

• Proposition 4: The risk premium decreases in private information when public information is given ( ), but is independent of the information asymmetry level when the total price information is constant ( ). When the fraction of informed investors is small, the ambiguity premium increases in private information and decreases in public information (when is small, , ).

– the risk premium is precisely the whole cost of capital in Easley and O’Hara (2004) and Lambert et al. (2011) and proposition 4 shows that the main properties in their model hold here.

– the risk premium is a decreasing function of private information precision if public information is given because more information is included in the market, as the formula shows. Leland (1992) similarly argued that insider trading can improve market efficiency, and Wang (1993) noted that private information in the economy affects both information asymmetry and the precision of total information

2014年杨云红 38

0

RP

0| )1(

RP

0

AP0

AP

Model Implication: Information asymmetry and

the cost of capital

• Proposition 4: The risk premium decreases in private information when public information is given ( ), but is independent of the information asymmetry level when the total price information is constant ( ). When the fraction of informed investors is small, the ambiguity premium increases in private information and decreases in public information (when is small, , ).

– the risk premium is completely determined by the information quantity in price function

– To avoid the joint effect of information asymmetry and information quantity caused by private information, Easley and O’Hara (2004) shifted information from public to private while the total market information was constant, i.e., increasing while keeping constant. Under this restriction, they found that the cost of capital increased in private information.

– Lambert et al. (2011) further argued that if we shift information from public to private while keeping the total information in price function constant, then the cost of capital is independent of the variation of private information precision. This is also true in our model.

2014年杨云红 39

0

RP

0| )1(

RP

0

AP0

AP

)1(

)1(

Model Implication: Information asymmetry and

the cost of capital

• Proposition 4: The risk premium decreases in private information when public information is given ( ), but is independent of the information asymmetry level when the total price information is constant ( ). When the fraction of informed investors is small, the ambiguity premium increases in private information and decreases in public information (when is small, , ).

– the higher the information asymmetry level (the larger the ratio of private information to the total information caused by more private information or less public information), the larger the ambiguity premium.

– Because the risk premium decreases in private information and the ambiguity premium increases, private information has an uncertain effect on the total cost of capital. In certain circumstances, the cost of capital may have an inverse U-shape relationship with the information asymmetry level measured by private information precision.

– it is difficult to use the risk premium alone to explain practitioner beliefs and empirical findings. Private information generated by insider trading reduces the risk premium, but the SEC believed that insider trading increases the cost of capital because it hurts the market by reducing market participation.

– In our model, the ambiguity premium is precisely the cost of capital caused by insider trading. Empirically, Botosan et al. (2004) found that the cost of equity capital increases along with the precision of private information. This finding, although not consistent with the risk premium, is consistent with the ambiguity premium.

2014年杨云红 40

0

RP

0| )1(

RP

0

AP0

AP

Model Implication: Information asymmetry and

the cost of capital

• Proposition 4: The risk premium decreases in private information when public information is given ( ), but is independent of the information asymmetry level when the total price information is constant ( ). When the fraction of informed investors is small, the ambiguity premium increases in private information and decreases in public information (when is small, , ).

– Much empirical research has been performed on the effectiveness of Reg FD. • Duarte et al. (2008) found that NASDAQ firms’ cost of capital increases subsequent to Reg FD while presenting no

significant changes for NYSE/Amex firms.

• Chen et al. (2010) found that firms’ cost of capital decreases after Reg FD, but that the decrease is mainly for medium and large firms and insignificant for small firms.

– These findings demonstrate that there is a large cross-sectional variation in the effect of information asymmetry on the cost of capital. One proposed argument is that while Reg FD can shift some private information to public, it also induces financial analyzers to produce less information for small firms/NASDAQ firms; hence, the effect of the cost of capital is different between larger firms and small firms.

– Our model provides an alternative explanation for this cross-sectional variation: the cost of capital may have an inverse U-shape relationship with the information asymmetry level. When the level is relatively lower, reducing information asymmetry can reduce the cost of capital. In contrast, when the level is higher, reducing information asymmetry may increase the cost of capital. Small firms may belong to the latter case because they usually have a higher information asymmetry level; hence, although Reg FD reduces their information asymmetry, their cost of capital may increase.

2014年杨云红 41

0

RP

0| )1(

RP

0

AP0

AP

Conclusion

• Academics and practitioners have different perspectives on how information asymmetry among investors affects stock pricing. – Extant research addresses it from the perspective of how information

asymmetry affects the information quantity contained in the market. Leland (1992) argued that insider trading could improve market efficiency through the addition of private information. Easley and O’Hara (2004) showed that shifting information from public to private would increase firms’ cost of capital, whereas Lambert et al. (2011) believed that the cost of capital is independent of information asymmetry if the total price information is given.

– However, the SEC (2000) believed that selective disclosure and insider trading could induce a higher cost of capital because of uninformed investors’ reluctant market participation due to their loss of confidence in the market’s integrity.

• In this paper, we fill this gap by directly modeling the effect of information asymmetry onto market participation.

2014年杨云红 42

Conclusion

• Under our model framework, the arguments of Leland (1992) and Lambert et al. (2011) fit the risk premium precisely, whereas the SEC’s (2000) beliefs fit the ambiguity premium. The theoretical prediction is also consistent with extant empirical findings. For example, it explains the finding of Botosan et al. (2004) that the cost of equity capital increases along with the precision of private information. It also explains the finding of Duarte et al. (2008) and Chen et al. (2010) that there is a large cross-sectional variation in the effect of information asymmetry on the cost of capital.

• Of course, information asymmetry is not the sole cause of market non-participation and information ambiguity. Transaction costs or other market inefficiencies may also cause market non-participation. This paper argues only that information asymmetry can affect market participation through ambiguity aversion and have a major effect on asset pricing.

• Multi-assets model

2014年杨云红 43

Thanks!