Embed Size (px)

Citation preview

Inflation and Forest Investment Analysis

What’s real?

What’s Inflation

• An increase in prices that makes a “market basket” of goods and services more expensive over time.

• Basket costs $1,400 in 2003 and $1,550 in 2004, a one year period.– Increase in cost is $150– % increase, the annual rate of inflation, is

• $150/$1,400 = 10.7%, or• $1,550/$1,400 – 1 =1.107 – 1 = 10.7%

Causes of Inflation

• Demand-pull inflation– Too many people chasing too few goods and services

• Cost-push inflation– Costs of factors of production rise, pushing up prices

of goods and services

• Monetary inflation– Government “prints” more money, leading to demand

pull inflation

Terminology

• Price with inflation included– Nominal– Current dollar– Inflated– Actual

• Price with inflation not included– Real– Constant dollar– Deflated– Relative

Nomenclature

• f = annual inflation rate

• r = real interest rate

• i = inflated or nominal interest rate i = (r + f + rf)

• In = inflated or nominal dollar value in year n

• Vn = future value in year n, in constant dollars of year 0

Producer Price Index for Finished Goods

0

20

40

60

80

100

120

140

160

Year

1987

bas

e ye

ar

32.5

143

1957

2003

Average Annual Rate of Inflation

• Rate of inflation between two points in time more than one year apart.

• Calculate as, f = (Vn/V0)1/n -1

= (143/32.5)1/46 – 1

= 4.40.02174 – 1

= 1.0327 – 1

= 3.27% per annum

Converting the value of an asset from its nominal to its real value

• Vn = In/(1+f)n • Example – Timberland is purchased for

$500 per acre in 1957. In 2004 it’s sold for $3,500 per acre. If average annual inflation over this period is 3.27%, what is the sale price of the land in terms of 1957 values?V1957 = $3,500/1.032747 = $796

• What is the real rate of return on the land?r = ($796/$500)1/46 – 1 = 0.01

Table 8. Weighted average actual price, price index, and deflated price for an average and quality stand of timber in Indiana, 1957 to 2003. Average Stand Quality Stand

Year

Producer Price Index

Nominal Price

Index Number

Real

Price 1

Nominal Price

Index Number

Real

Price 1 (1) (2) (3) (4) (5) (6) (7) (8)

($/MBF) ($/MBF) ($/MBF) ($/MBF) 1957 32.5 55.6 100.0 171.1 66.6 100.0 204.9 1958 33.2 53.7 96.6 161.8 64.0 96.1 192.8 1959 33.1 54.8 98.5 165.5 67.5 101.4 204.0 1960 33.4 57.5 103.5 172.3 68.7 103.2 205.7 1961 33.4 58.9 105.9 176.3 70.0 105.1 209.5 1962 33.5 59.6 107.3 178.1 72.3 108.6 215.8 1963 33.4 59.3 106.7 177.6 74.5 111.9 223.1 1964 33.5 60.1 108.1 179.5 74.4 111.8 222.2 1965 34.1 63.6 114.3 186.4 78.5 118.0 230.3 1966 35.2 68.8 123.7 195.4 86.0 129.2 244.3 1967 35.6 70.1 126.0 196.8 87.2 131.0 245.0 1968 36.6 74.7 134.2 204.0 92.7 139.3 253.4 1969 38.0 77.7 139.7 204.5 98.6 148.2 259.6 1970 39.3 83.1 149.4 211.5 103.9 156.0 264.3 1971 40.5 85.9 154.4 212.0 107.4 161.3 265.2 1972 41.8 90.2 162.2 215.8 112.2 168.5 268.4 1973 45.6 112.6 202.5 247.0 139.0 208.8 304.9 1974 52.6 135.3 243.3 257.3 170.2 255.7 323.7 1975 58.2 125.1 225.0 215.0 166.3 249.8 285.8 1976 60.8 133.6 240.2 219.7 172.7 259.4 284.1 1977 64.7 143.6 258.1 221.9 188.0 282.4 290.6 1978 69.8 181.7 326.1 260.3 234.9 352.9 336.6 1979 77.6 201.5 362.3 259.6 260.7 391.6 336.0 1980 88.0 207.8 373.6 236.1 309.3 464.5 351.5

1 Actual price deflated by Producer Price Index for Finished Goods, U.S. Dept. Commerce, 1982 base year.

Table 8. Weighted average actual price, price index, and deflated price for an average and quality stand of timber in Indiana, 1957 to 2003. Average Stand Quality Stand

Year

Producer Price Index

Nominal Price

Index Number

Real

Price 1

Nominal Price

Index Number

Real

Price 1 (1) (2) (3) (4) (5) (6) (7) (8)

($/MBF) ($/MBF) ($/MBF) ($/MBF) 1981 96.1 206.7 371.7 215.1 284.9 427.8 296.4 1982 100.0 196.8 353.8 196.8 277.3 416.5 277.3 1983 101.6 207.6 373.3 204.3 294.4 442.2 289.8 1984 103.7 235.8 424.0 227.4 322.7 484.6 311.2 1985 104.7 210.5 378.5 201.0 274.0 411.5 261.7 1986 103.2 223.6 402.0 216.6 312.2 468.9 302.5 1987 105.4 257.3 462.7 244.2 334.6 502.6 317.5 1988 108.0 262.1 471.3 242.7 345.9 519.6 320.3 1989 113.6 285.9 514.0 251.6 404.9 608.1 356.4 1990 119.2 288.3 518.3 241.8 397.9 597.6 333.8 1991 121.7 268.1 482.1 220.3 362.9 545.1 298.2 1992 123.2 293.4 527.6 238.2 417.6 627.1 338.9 1993 124.7 355.2 638.8 284.9 491.2 737.8 393.9 1994 125.5 364.8 655.9 290.6 507.4 762.1 404.3 1995 127.9 354.0 636.4 276.7 451.6 678.3 353.1 1996 131.3 337.7 607.1 257.2 495.4 744.0 377.3 1997 131.8 357.5 642.7 271.2 448.3 673.3 340.2 1998 130.7 391.1 703.3 299.3 501.7 753.5 383.9 1999 133.0 389.2 699.8 292.6 526.3 790.5 395.7 2000 138.0 426.5 766.9 309.1 617.6 927.5 447.5 2001 140.7 389.7 700.8 277.0 538.5 808.8 382.7 2002 138.9 410.7 738.4 295.7 561.2 842.9 404.0 2003 142.5 433.7 779.7 304.3 567.9 852.9 398.5

1 Actual price deflated by Producer Price Index for Finished Goods, U.S. Dept. Commerce, 1982 base year.

Figure 2. Average stand of timber, nominal, deflated, and trend line price series, 1957 to 2003.

0

50

100

150

200

250

300

350

400

450

500

57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03

Year

$ pe

r MBF

Trend line 1.20% per year

Nominal Price

Real price, 1982 $’s

Figure 3. Quality stand of timber, nominal, deflated, and trend line price series 1957 to 2003.

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.057 60 63 66 69 72 75 78 81 84 87 90 93 96 99 02

Year

$ p

er M

BF

Real price, 1982 $’s

Nominal Price

Trend line 1.52% per year

Nominal and Real ROR’s

Loan $100 now to be returned in one year. You want a 5% real rate of return, r, i.e. 5% more than inflation. If inflation will be 4% over the year you need $104 back just to keep same purchasing power of $100.

$100 (1+f)n = 100 (1.04)1 = $104

To get 5% return need to multiply $104 by (1+r)n,

$104 (1.05)1 = $109.20

Nominal and Real ROR’s

Combining the steps,

In = V0 (1+r)n (1+f)n

= V0 (1+ r + f + rf)n = V0 (1+i)n,therefore,

i = r + f + rf = 0.05 + 0.04 + 0.05*0.04 = 0.09 + 0.002 = 0.092,

or, i = (1 + r) (1 + f) -1

Nominal and Real ROR’s

If you know the nominal rate of return and inflation rate, solve for the real rate of return,

(1 + r) (1 + f) = 1 + i

1 + r = (1 + i) / (1 + f)

r = [(1 + i) / (1 + f)] - 1

Calculating Inflation Adjusted PV’s

PV = In/(1+i)n

= [Vn (1+f)n] / (1+r+f+rf)n

= [Vn(1+f)n]/[(1+r)n(1+f)n]

= [Vn(1+f)n]/[(1+r)n(1+f)(1+f)nn]

= Vn/(1+r)n

Calculating Inflation Adjusted PV’s

• Guidelines for computing net present value (NPV)– If future cash flows are in constant dollars

compute NPV with a real interest rate, r– If future cash flows are in current dollars

compute NPV with a nominal interest rate. Use same inflation rate in the cash flows and nominal interest rate

Warning

• Never mix real dollars and nominal dollars in the same equation

Recommendation

• It’s usually easier to work in real terms, that is adjust all cash flows to real values, and discount with real interest rate, r

• However, have to use nominal values for after-tax calculations,– Tax laws generally don’t adjust rates for

inflation, and never adjust basis of assets for inflation

Income tax on gain from disposal of assets

C = basis of asset

In = nominal value in year n

Ti = tax rate (5% or 15%)

Tax due = Ti (In – C)

Example

George buys timberland in 1975 for $120,000 of which $80,000 is attributable to merchantable timber. In 1980 he sells 20% of the merchant-able timber for $50,000. What is the tax on the sale?C = 0.2 * $80,000 = $16,000

I80 = $50,000

Ti = 15%Tax due = 0.15 ($50,000 - $16,000)

= 0.15 * $34,000 = $5,100

After-tax gain = $50,000 - $5,100 = $44,900

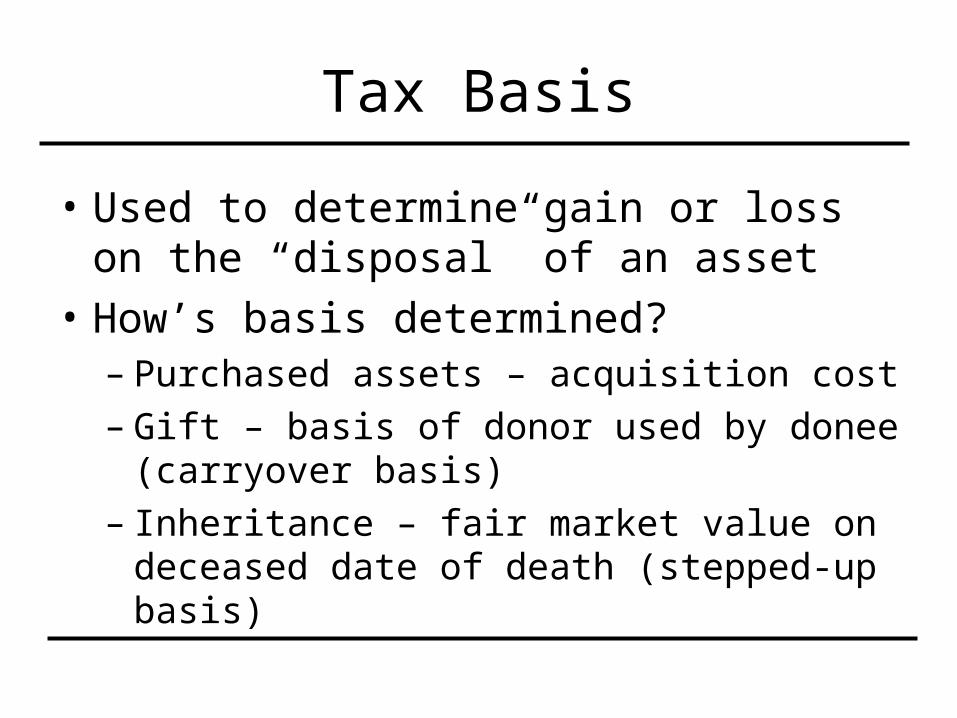

Tax Basis

• Used to determine gain or loss on the “disposal” of an asset

• How’s basis determined?– Purchased assets – acquisition cost– Gift – basis of donor used by donee

(carryover basis)– Inheritance – fair market value on deceased

date of death (stepped-up basis)

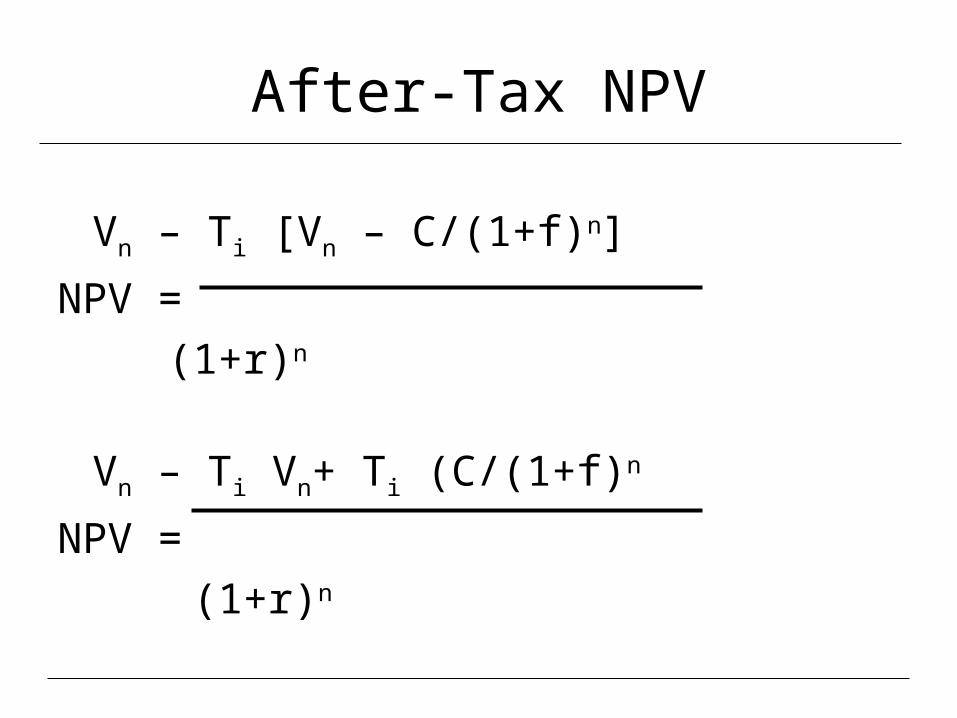

After-Tax NPV

Vn – Ti [Vn – C/(1+f)n]

NPV =

(1+r)n

Vn – Ti Vn+ Ti (C/(1+f)n

NPV =

(1+r)n

After-Tax NPV, Example

Buy an asset for $2,000 and sell it 8 years for $8,000. Annual inflation rate is 9.05%.

f = 0.0905, r = 0.05

Ti = 0.15

I8 = $4,000/1.09058 = $8,000

$4,000 – 0.15[4,000 – 2,000/(1.09058)]

NPV =

(1.05)8

= $2,402.78

$2,000

$4,000

$6,000

$8,000

Basis = $2,000 nominal

Vn = $4,000

In = $8,000

Years 8

Capital gain = $6,000

Real gain = $2,000

Nominal and real gain

4

After-Tax NPV With No Inflation

$4,000 – 0.15 ($4,000 – $2,000)

NPV =

(1.05)8

= $2,504.31

Decrease in after-tax NPV due to inflation is,

$2,504.31 - $2,402.78 = $101.52

Affect of Inflation on Series Payment Formulas – annual and periodic

• Basic formulas assume fixed payments

• If payments are fixed in nominal terms must use nominal interest rate, i, in series payment formulas.

• If nominal payments rise at exactly the inflation rate, they are fixed in real terms and must use real interest rate in formulas.