Embed Size (px)

Citation preview

The Florida Office of Early Learning is an equal opportunity employer/program. The Florida Office of Early Learning will provideauxiliary aids and services upon request to individuals with disabilities. All voice telephone numbers on this document may be reached

by persons using TTY/TDD equipment via the Florida Relay Service at 711.

Independent Accountants’ Report onFinancial Compliance Advisory Services

The Early Learning Coalition of Flagler and Volusia Counties, Inc.(ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Independent Accountants’ Report on Financial Compliance Advisory ServicesThe Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Contents

Transmittal Letter .........................................................................................................................1

I. Executive Summary............................................................................................................... 3

1.0 Findings................................................................................................................................ 32.0 Observations ........................................................................................................................ 5

II. Schedule of Findings.............................................................................................................. 61.0 Preventive / corrective action plan (PCAP) implementation ............................................. 62.0 Financial management systems.......................................................................................... 63.0 Internal control environment.............................................................................................. 64.0 Cash management ............................................................................................................ 105.0 OEL statewide information system reporting and reconciliation - N/A .......................... 116.0 Prepaid program items ..................................................................................................... 117.0 Cost allocation and disbursement testing......................................................................... 128.0 Travel ............................................................................................................................... 159.0 Purchasing........................................................................................................................ 1510.0 Contracting....................................................................................................................... 1511.0 Subrecipient monitoring .................................................................................................. 18

III. Schedule of Observations.................................................................................................. 1891.0 Observations from 2014-15 onsite visit........................................................................... 1892.0 Items for OEL follow-up ................................................................................................. 189

December 18, 2014

State of FloridaFlorida Office of Early LearningTallahassee, Florida

We have performed specific financial compliance consulting services asOffice of Early Learning’s 201Coalition of Flagler and Volusia Counties, Inc.contracted by the Office of Early Learningresponsibilities as outlined in

45 Code of Federal Regulations ( Chapter 1002.82(2)(p), Subpart D, Paragraph .400(d) of Office of Management and Budget Circular A

Audits of States, Local Governments and Non

These advisory services were conducted in accordanceby the American Institute of Certified Public Accountants.sufficiency of the procedures performedsufficiency of the proceduresrequested or for any other purpose.

On December 15, 2014 throughFlagler and Volusia Countiesservices as summarized in OELOctober 1, 2013 through September 30findings begin on page 6 of this report.

In addition, during this monitoring engagement, we became aware of certain matters that areopportunities for strengthening internal control and/or operating efficiency. We have includedthese observations in The Schedule of Observationsreview the status of these observations

We were not engaged to and did not conduct an examination, the objective of which would bethe expression of an opinion onfinancial management standards as outlined in applicable Office of Management and BudgetCirculars, Code of Federal Regulations, or other

Page - 1 -

Office of Early Learning

specific financial compliance consulting services as described2014-15 Onsite Financial Monitoring Tool for T

Flagler and Volusia Counties, Inc. (ELC 13 or the Coalition)Office of Early Learning (OEL) to comply with its oversight and monitoring

applicable federal regulations and state statutes.

Code of Federal Regulations (CFR) Part 74.51(a);Chapter 1002.82(2)(p), Florida Statutes; andSubpart D, Paragraph .400(d) of Office of Management and Budget Circular AAudits of States, Local Governments and Non-Profit Organizations

services were conducted in accordance with the attestation standardsby the American Institute of Certified Public Accountants. OEL is solely responsible for t

procedures performed. Consequently, we make no representation regarding thedures performed, either for the purpose for which this report has been

requested or for any other purpose.

through December 18, 2014, we visited The Early Learning Coalition ofFlagler and Volusia Counties, Inc. (ELC 13) and performed financial compliance consulting

OEL’s 2014-15 Onsite Financial MonitoringSeptember 30, 2014. The procedures performed and our related

of this report.

In addition, during this monitoring engagement, we became aware of certain matters that areopportunities for strengthening internal control and/or operating efficiency. We have included

The Schedule of Observations section of this report. We recommendreview the status of these observations.

We were not engaged to and did not conduct an examination, the objective of which would bethe expression of an opinion on the Coalition’s compliance with the previously describedfinancial management standards as outlined in applicable Office of Management and BudgetCirculars, Code of Federal Regulations, or other state and federal requirements.

described in the Floridafor The Early Learning

the Coalition). These services wereoversight and monitoring

applicable federal regulations and state statutes.

Subpart D, Paragraph .400(d) of Office of Management and Budget Circular A-133,Profit Organizations.

attestation standards establishedOEL is solely responsible for the

Consequently, we make no representation regarding theperformed, either for the purpose for which this report has been

Early Learning Coalition offinancial compliance consulting

onitoring Tool for the periodprocedures performed and our related

In addition, during this monitoring engagement, we became aware of certain matters that areopportunities for strengthening internal control and/or operating efficiency. We have included

port. We recommend OEL

We were not engaged to and did not conduct an examination, the objective of which would becompliance with the previously described

financial management standards as outlined in applicable Office of Management and Budgetstate and federal requirements.

DRAFT

Page - 2 -

Accordingly, we do not express such an opinion. Had we performed additional procedures, othermatters might have come to our attention that would have been reported to OEL.

This report is intended solely for the information and use of OEL and OEL’s management, and isnot intended to be and should not be used by anyone other than these specified parties.

HARVEY COVINGTON & THOMAS OF SOUTH FLORIDA, LLC

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Executive Summary

Page - 3 -

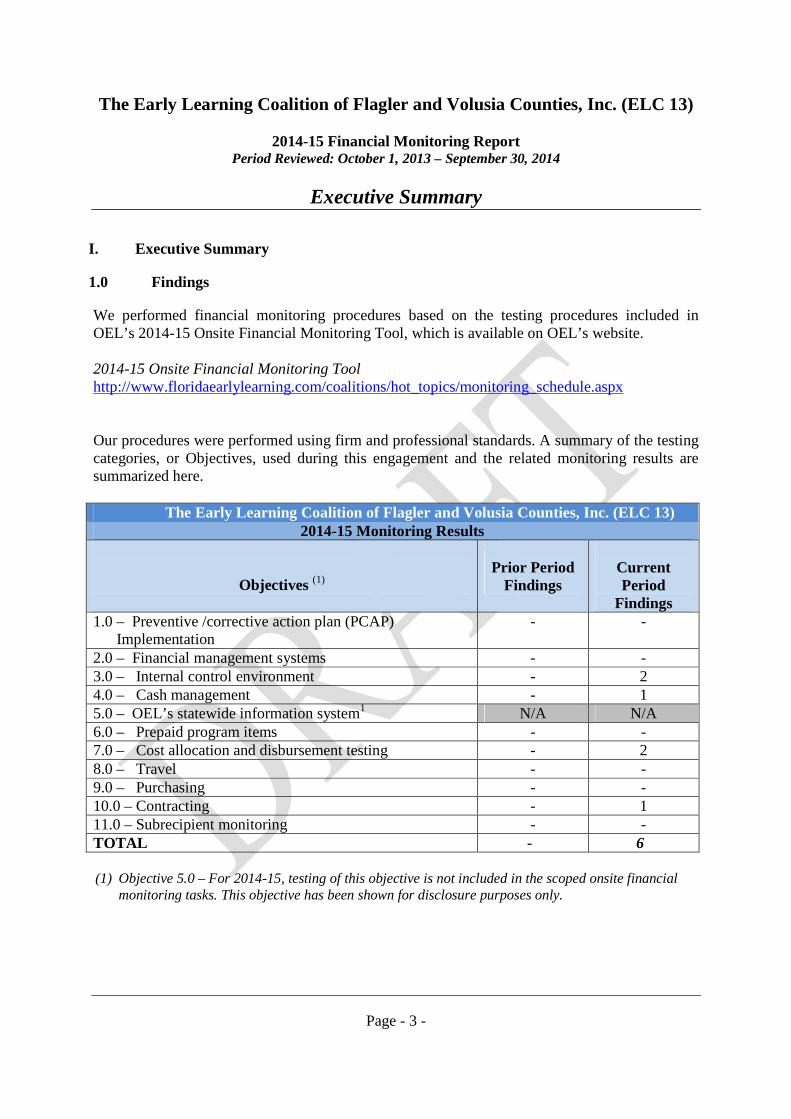

I. Executive Summary

1.0 Findings

We performed financial monitoring procedures based on the testing procedures included inOEL’s 2014-15 Onsite Financial Monitoring Tool, which is available on OEL’s website.

2014-15 Onsite Financial Monitoring Toolhttp://www.floridaearlylearning.com/coalitions/hot_topics/monitoring_schedule.aspx

Our procedures were performed using firm and professional standards. A summary of the testingcategories, or Objectives, used during this engagement and the related monitoring results aresummarized here.

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)2014-15 Monitoring Results

Objectives (1)Prior Period

FindingsCurrentPeriod

Findings1.0 – Preventive /corrective action plan (PCAP)

Implementation- -

2.0 – Financial management systems - -3.0 – Internal control environment - 24.0 – Cash management - 15.0 – OEL’s statewide information system1 N/A N/A6.0 – Prepaid program items - -7.0 – Cost allocation and disbursement testing - 28.0 – Travel - -9.0 – Purchasing - -10.0 – Contracting - 111.0 – Subrecipient monitoring - -TOTAL - 6

(1) Objective 5.0 – For 2014-15, testing of this objective is not included in the scoped onsite financialmonitoring tasks. This objective has been shown for disclosure purposes only.

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Executive Summary

Page - 4 -

Included in the table below is a summary of the results from our review of prior period findings.New findings may occur in the current period if prior period findings which should have beencorrected remain unresolved.

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)Status of Prior Period Findings

Finding ResolvedPartiallyResolved

Unresolved New Finding

No Prior Period Findings - - - -

These financial monitoring procedures apply to both the School Readiness (SR) and VoluntaryPrekindergarten (VPK) programs. Since Chapter 1002, F.S. does not provide specific financialmonitoring steps for the federally-funded School Readiness program or the state-funded VPKprogram, the minimum federal standards have been applied to both programs.

The attached Schedule of Findings contains detailed information about current period and priorperiod findings. If the Coalition has current period findings it must submit apreventive/corrective action plan (PCAP) response to OEL within 30 days of receiving thisreport. Please contact OEL staff with any questions about the PCAP process.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Executive Summary

Page - 5 -

2.0 Observations

Other matters or circumstances may have been noted by us as we completed the indicatedmonitoring tasks. Detailed information about these observations is provided in The Schedule ofObservations and is summarized here.

Observations from 2014-15 onsite visit 3.0 – Internal control environment Review and update operating policies and procedures

Items for OEL follow-upThe monitoring team noted no items for OEL follow-up.

This monitoring report is intended solely for the information and use of the OEL and OEL’smanagement and is not intended to be and should not be used by anyone other than thesespecified parties.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 6 -

II. Schedule of Findings

We performed financial monitoring procedures based on the Testing Procedures included inOEL’s 2014-15 Onsite Financial Monitoring Tool, which is available on OEL’s website.

2014-15 Onsite Financial Monitoring Toolhttp://www.floridaearlylearning.com/coalitions/hot_topics/monitoring_schedule.aspx

The monitoring procedures performed included tests of details of transactions, file inspectionsand interviews with the entity’s personnel (1) to determine the status of recommendations fromthe prior period monitoring visit(s) and (2) to adequately support the current period findings andrecommendations. Detailed information for these items is disclosed in the following sections ofthis report.

1.0 – Preventive/corrective action plan (PCAP) implementation

The current period monitoring procedures were performed to determine if the entity implementedthe required preventive and corrective actions as described in the approved preventive/correctiveaction plan (PCAP) from the most recently closed grant program year.

No findings were noted in the current period.

2.0 – Financial management systems

The current period monitoring procedures were performed to gain an understanding of theentity’s financial and operational environments through review of policies and procedures,observation of processes, document inspection and interviews of entity personnel.

No findings were noted in the current period.

3.0 – Internal control environment

The current period monitoring procedures were performed to gain an understanding of theentity’s internal control environment through testing of key internal controls and observation ofentity operations to ensure compliance with Federal laws, regulations and grant programcompliance requirements.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 7 -

Finding # ELC 13-2014-15-001Internal Control Environment – Incomplete evidence for review of purchases

Finding/Condition: During our detailed testing of internal controls for disbursement reviewswe noted incomplete evidence of the Coalition’s internal control processes. Note: Althoughthe Coalition’s documentation elements were incomplete, no instances of inappropriateactivity were identified.

Criteria: ELC’s 2014-15 Annual Internal Control Questionnaire, Part 2, Administrative Operations,

Question #74 queries: “Does someone from the appropriate level of supervising (notsubordinates) management or governing board member review credit card, debit card oremployee reimbursements for entity management purchases?”

This question was answered “Yes” by the Coalition. However, we noted the following. Written policies and procedures do not require a governing board member to

approve Executive Director (ED) credit card expenses so a gap exists in the currentprocess of credit card approvals for the ED activities.

Travel related expenses for the ED are being reviewed by the Board Chair whichmay cover the majority of credit card expenses, but a gap still exists in thereview/approval process for non-travel related credit card expenses.

Cause: Lack of documentation of the requirement in the policies and procedures manual andlack of management oversight over the process in place.

Effect: The Coalition does not have complete documentation of the supervisory reviewcurrently in place for all credit card transactions. The Coalition has an increased operatingrisk that internal control processes are not operating as intended. Executive Director creditcard expenses currently may be inadvertently paid without a higher level of review/approvalthat could result in potential questioned costs.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm for OEL the results reported here. Testing results indicate writtendocumentation of governing board review/approval for all Executive Director creditcard expenses is incomplete.

2. Review Coalition records for the entire 2014-15 monitoring period to identify creditcard transactions impacted by this process. Prepare a summary or list of theexpenditures identified that includes the amounts spent by date, vendor/payee,purpose and grant program(s)/OCAs charged.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 8 -

3. Examine the Coalition’s current review/ approval process for the specified expensesand compare these results to the governing board’s intended levels of oversight.Summarize these results and any proposed changes identified by management. Note:As part of this process, obtain add review the Coalition’s current documentedinstructions for delegated authority from the governing board to the ExecutiveDirector in case updates/edits are needed.

4. Submit documentation from items #2 and #3 to OEL for analysis. OEL will reviewthis data to provide technical assistance instructions and/or details on related bestpractices for the Coalition’s consideration.

5. Review the Coalition’s related policies, procedures and internal controls to determineif revisions or updates are needed.

6. Update policies, procedures and internal controls, as appropriate.

7. Conduct staff training to help ensure compliance with established or revised policiesand procedures.

Finding # ELC 13-2014-15-002Internal Control Environment – Incomplete test and restore process for Coalition data files

Finding/Condition: During our detailed testing of internal controls we noted incompleteevidence of the Coalition’s internal control processes. Note: Although the Coalition’sdocumentation elements were incomplete, no instances of impaired operations wereidentified.

Criteria: Section 1002.84(13), F.S., which requires a Coalition to establish proper IT securitycontrols including, but not limited, to appropriate backup procedures and disaster recoveryplans.

ELC’s 2014-15 Annual Internal Control Questionnaire, ICQ Part 4, Information Technology,Question #23 queries: “Does the entity, as part of its COOP and disaster recovery plan, testthe backup and restore process to verify that it can access and use key financial tools and data(software copies, general ledger master balance and transaction history files, and fiscal filesnecessary to support grant-funded programs)? If yes, indicate date last test was performed.”

This question was answered “No” by the Coalition, but Coalition policies and proceduresrequire periodic backup testing. In addition, we noted:

Coalition IT policies (see Policy #CMPP00015, Data Back-ups) include arequirement to test backup operating files although the Coalition’s currentContinuity of Operations Plan (COOP) file does not include these instructions.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 9 -

Full testing of backup files on a periodic basis did not occur during the currentmonitoring period.

Cause: Lack of management oversight of policy requirements and related documentation forprocedures performed.

Effect: Noncompliance with state statutes and Coalition policy requirements for adequatedata file backup procedures. The Coalition has an increased operating risk that internalcontrol processes are not operating as intended. If full testing of backup files is notperiodically performed, the Coalition could be unaware of sensitive data and/or key operatingrecords that may be damaged, corrupted or inadvertently deleted.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm for OEL the results reported here. Testing results indicate partial, but notfull, backup recovery tests were performed by the ELC.

2. Make arrangements to perform a full test of the Coalition’s backup recovery data filesas soon as possible. Retain in Coalition files documentation of results and any follow-up tasks required. Provide a summary of these results to OEL.

3. Modify COOP disclosures to clarify testing requirements for data backup files.

4. Review current Coalition staff instructions related to periodic test/restore tasks forbackup files. Verify staff instructions are complete.

5. Review the Coalition’s other related policies, procedures and internal controls todetermine if additional updates or revisions are needed.

6. Update policies, procedures and internal controls, as appropriate.

7. Conduct staff training to help ensure adherence with established or revised policiesand procedures.

See The Schedule of Observations for observations related to this objective.

4.0 – Cash management

The current period monitoring procedures were performed to determine if sampleddocumentation demonstrated appropriate and sufficient cash management procedures are in place

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 10 -

and being followed. The processes examined include cash management procedures related tosources of other non-grant revenues.

Finding # ELC 13-2014-15-003Cash Management – Incomplete documentation for match income

Finding/Condition: The Coalition had incomplete documentation to indicate whether fundstotaling $58,200 from Flagler County were derived from sources that can be utilized formatch purposes. In addition, we noted:

The match funds will be utilized during the 2014-15 grant period. The Coalition verbally discussed the match sources with the County prior to receipt

of funds from the grant, but the source of funds received was not documented inwriting for 2014-15 files.

Note: While the monitoring team was onsite the Coalition contacted the donor to obtainsupport in writing that related funds were from sources that are allowable for matchpurposes.

Criteria: 45 CFR Part 74.23(a)(5) and (1) states: “To be accepted, all cost sharing ormatching contributions, including cash and third party-in-kind, shall meet all of the followingcriteria…(1) Are verifiable from the recipient's records.; and, (5) Are not paid by the FederalGovernment under another award, except where authorized by Federal statute to be used forcost sharing or matching.”

OEL Fiscal Guidance 10.02, Match Reporting Guidance states: ”The Coalition must set upprocedures to verify, record, and ensure that sufficient detail is kept at the coalition for auditpurposes.”

Cause: Lack of management oversight of the documentation requirements.

Effect: Noncompliance with federal and state match reporting requirements. Match moniesfrom local governments are typically derived from general revenue resources but this was notdocumented in the 2014-15 agreement with Flagler County. Incomplete documentationincreases the Coalition’s risk of receiving match funds from an unallowable source that couldresult in potential questioned or disallowed costs.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm for OEL the results reported here. Testing results indicate the ELC receiveda $58,200 2014-15 match grant from Flagler County and there was no writtendocumentation of staff tasks completed to identify the source of match funds.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 11 -

2. Identify and analyze all match revenue transactions during the period to determine ifthe source of other match funds is properly documented.

3. Prepare a summary list of other match fund agreements (if any) with incompletedocumentation for the source of match income. The summary list should include theamounts received, date and entity name.

4. Submit results from items #2 and #3 (if any) to OEL for review. Upon review, OELwill provide technical assistance suggestions and instructions for obtaining adequate“after-the-fact” documentation for missing documentation.

5. Review the Coalition’s policies, procedures and internal controls to determine ifupdates or revisions are needed.

6. Update policies, procedures and internal controls, as appropriate.

7. Conduct staff training to help ensure adhere to established or revised policies andprocedures.

5.0 – OEL’s statewide information system reconciliation and reporting – N/A for 2014-15

6.0 – Prepaid program items

The current period monitoring procedures were performed to identify any prepaid programactivity for this entity. If such activity was found, monitoring procedures were applied todetermine if all prepaid program items were appropriately safeguarded, managed, trackedand reported.

Based on results obtained from inquiries made to and an inspection of data itemsprovided by entity personnel the monitors noted no current year prepaid program itemactivity.

7.0 – Cost allocation and disbursement testing

The current period monitoring procedures were performed to determine if sampleddisbursements were appropriately incurred and posted within the entity’s financial records.Sampled items were tested to ensure the activity: is allowable, has appropriate approval(including pre-approval from OEL if needed), and meets the period of availability requirementsfor the grant monies used to fund disbursements. Sampled items are also tested to verify

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 12 -

appropriate allocation in accordance with applicable cost principles, grant program compliancerequirements and guidance issued by OEL.

Finding # ELC 13-2014-15-004Cost Allocation and Disbursement Testing – Improper allocation of general operating costs

Finding/Condition: During testing, we identified 2 of 26 sampled disbursements thatincluded cost pool allocations to incorrect or unallowable OCA codes.

Check#: 25272, Payee: Copytronics, Amount: $903.68, Date: 10/3/2014,

Description: Printing and reproduction, OCA Code/Year: CP allocation of $15.42 to

97QCS/2014-2015

Check#: 25036, Payee: Florida Capital Bank/A&G Marketing Group, Amount:$1,529.15, Date: 5/23/2014, Description: Website costs, OCA Code/Year: CPallocation of $30.77 to 97QCS/2013-2014

Criteria: 2 CFR 230 Appendix A Section A(4)(a) states: "A cost is allocable to a particularcost objective, such as a grant, contract, project, service, or other activity, in accordance withthe relative benefits received." There is also State-level guidance from OEL for the relativebenefits received for quality-related costs.

OEL Fiscal Guidance 250.01 instructs Coalitions to record shared/ pooled costs for generalbusiness activities to only four quality OCAs – 97QOO, 97INT, 97QI4 and 97QIN. All otherQuality OCA codes (such as 97QCS as utilized above in the sample items) are reserved fordirectly-charged costs specifically identifiable to the grant program(s) receiving benefit.

Cause: The allocation errors were due to a misunderstanding of the new OCAs and OELfiscal guidance.

Effect: Noncompliance with OEL guidance. This error in coding shared quality-related costsappears to be a systemic issue for all cost pool allocations. Over-allocations of cost poolexpenses to numerous unallowable Quality OCA codes have occurred, which increases theCoalition’s risk for potential questioned or unallowable costs.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm total costs for the allocation errors for OEL. Tested records indicateallocation errors total $46.19.

2. Review Coalition records and prepare a summary analysis of other monthly

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 13 -

allocations for shared/pooled quality costs from July 1, 2014 through the current date.Summary analysis should include dates, amounts and OCAs originally charged.

3. Prepare adjusting journal entries with documented explanations to correct anyidentified monthly allocation errors of shared/pooled quality costs.

4. Submit results from items #2 and #3 above along with any supporting monthlyallocation files to OEL for analysis. Upon review, OEL will provide technicalassistance suggestions and instructions on remitting any funds determined to beincurred for unallowable costs (if applicable).

5. Coordinate with OEL staff (as needed) to review and revise the template allocationspreadsheet files used to allocated monthly shared/pooled costs.

6. Review, and revise as necessary, the Coalition’s internal controls, policies andprocedures related to invoice processing activities to ensure adequate guidance tostaff.

7. Compare the Coalition’s current and/or revised policies and processes to the costallocation plan (CAP) disclosures to determine if CAP updates are necessary.Coordinate with OEL to make these plan modifications, if appropriate.

8. Conduct staff training as necessary to help ensure adherence to established or revisedpolicies and procedures.

Finding # ELC 13-2014-15-005Cost Allocation and Disbursement Testing – Improper allocation of legal expenses

Finding/Condition: During testing, we identified 1 of 26 sampled disbursements thatincluded cost pool allocations to incorrect or unallowable OCA codes.

Check#: 25275, Payee: Foley & Lardner LLP, Amount: $18,923.41, Date:10/3/2014, Description: Legal Services, OCA Code/Year: CP (“Cost Pool”)/2014-2015

Criteria: 2 CFR 230 Appendix A Section A(4)(a) states: "A cost is allocable to a particularcost objective, such as a grant, contract, project, service, or other activity, in accordance withthe relative benefits received." There is also State-level guidance from OEL for the relativebenefits received for quality-related costs.

OEL Fiscal Guidance 250.01 instructs Coalitions to record legal costs only to administrativeOCA codes 97BBA and VPADM.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 14 -

Cause: The allocation error to the cost pool account was due to a misunderstanding of thenew OCAs and OEL fiscal guidance.

Effect: Noncompliance with OEL guidance. This error in coding appears to be a systemicissue for all legal expenses that should be coded directly to 97BBA and/or VPADM Over-allocation of cost pool expenses to numerous unallowable OCA codes have occurred, whichincreases the Coalition’s risk for potential questioned or unallowable costs.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm total costs for the allocation errors for OEL. Tested records indicate allocationerrors of $18,923.41.

2. Review Coalition records and prepare a summary analysis of all legal transactionsallocated to the cost pool OCA code from July 1, 2014 through the current date.Summary analysis should include dates, amounts and OCAs originally charged.

3. Prepare adjusting journal entries with documented explanations to correct any identifiedmonthly allocation errors of shared/pooled costs.

4. Submit results items #2 and #3 above along with any supporting monthly allocation filesto OEL for analysis. Upon review, OEL will provide technical assistance suggestions andinstructions on remitting any funds determined to be incurred for unallowable costs (ifapplicable).

5. Coordinate with OEL staff (as needed) to review and revise the template allocationspreadsheet files used to allocated monthly shared/pooled costs.

6. Review, and revise as necessary, the Coalition’s internal controls, policies and proceduresrelated to invoice processing activities to ensure adequate guidance to staff.

7. Compare the Coalition’s current and/or revised policies and processes to the costallocation plan (CAP) disclosures to determine if CAP updates are necessary. Coordinatewith OEL to make these plan modifications, if appropriate.

8. Conduct staff training as necessary to help ensure adherence to established or revisedpolicies and procedures.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 15 -

8.0 – Travel

The current period monitoring procedures were performed to determine if the entity’s sampledtravel-related expenditures are paid in accordance with applicable federal/state laws and rules,and entity-established policies.

No findings were noted in the current period.

9.0 – Purchasing

The current period monitoring procedures were performed to determine if the sampledprocurement transactions comply with the appropriate federal or state procurement laws, as wellas the entity’s procurement policies.

No findings were noted in the current period.

10.0 – Contracting

The current period monitoring procedures were performed to determine if the sampled contracttransactions demonstrate the entity’s contracting processes comply with federal and staterequirements, as well as the entity’s own contracting policies.

Finding # ELC 13-2014-15-006Contracting - Noncompliance with contract and procurement standards and requirements

Finding/Condition: During our detailed testing of 3 contracts, we noted deficiencies for thefollowing contract and procurement transaction.

Check#: 25250, Payee: Bright House Networks, Amount: $2,273.45, Date:9/14/14, Description: Internet/Network Services – Deland Office $573.45, OCACode/Year: VPENR $86.02 /2014-2015

The Coalition executed a vendor contract with Bright House Networks for a 3 year periodand total value of $79,200 ($2,200 for 36 months) for internet and network services. Missingitems from the contract and procurement files include, but may not be limited to, (1)vendor/contract checklist, (2) Sole source documentation or bid requirements (if applicable),(3) cost price analysis documentation, (4) OEL and Board approval, (5) formal Coalitioncontract with required state and federal provisions.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 16 -

Criteria: Section 1002.84, F.S., Early learning coalitions; school readiness powers andduties, instructs that each early learning coalition shall “…(12) Comply with federalprocurement requirements and the procurement requirements of ss. 215.971, 287.057, and287.058.”

Written agreements or purchase orders for goods/services are “contracts”. Such writtenagreements must be (1) executed by following specific processes and (2) must includespecific language for terms and conditions to assist the ELC in ensuring goods and servicespaid for are received.

In addition, federal and state procurement rules (45 CFR Parts 74.45 and 74.48; and sections287.058 and 216.3475, F.S.) provide that cost analysis (i.e., verifying the scope of work datafor proposed goods/services and the evaluation of related costs) is required. State statutesspecifically mandate a cost analysis whenever services are non-competitively procured.

Cause: Inadequate management oversight and understanding of the procurement process andcontract requirements for non-routine procurements. The Coalition moved Daytona Beachoffice locations in 2013 and believed fiber optic services were already present in the newbuilding. After the move management determined the network connections were notsufficient. The Coalition contacted local internet provider Bright House Networks, and thisprovider required a 3 year contract to “offset or protect” their costs of connecting thebuilding to a fiber optic network. The Coalition did not follow procurement and contractprocedures prior to entering into the 3 year contract for internet services since typicallyinternet service providers do not require a contract agreement.

Effect: Noncompliance with federal and state procurement rules. Incomplete documentationof procurement processes or the terms/conditions for contracted goods/services increase theCoalition’s operating risk for or inadvertent staff errors or activities that are not incompliance with federal and state grant program requirements. Unauthorized or improper useof federal and state award monies may result in potential questioned or unallowable costs.

Recommendation(s): The Coalition should complete tasks that include, but are not limitedto, the following.

1. Confirm for OEL the results reported here. Testing results indicate procurement andcontract standards were not followed in full for the Coalition’s 3 year contractagreement (total value $79,200) with Bright House Networks for internet services.

2. Review the Coalition’s records for the entire monitoring period to identify otherprocurement transactions (if any) for active contracts generated under similarcircumstances. Prepare a summary or list of the expenditures identified that includes

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Findings

Page - 17 -

the amounts spent by date, vendor/payee, purpose and grant program(s)/OCAscharged.

3. Submit results from items #2 and #3 (if any) to OEL for review. Upon review, OELwill provide technical assistance suggestions and instructions for obtaining adequate“after-the-fact” documentation for missing documentation. Note: technical assistancemay include more details on required federal/state contract elements, provisions,terms and conditions.

4. Review and revise the Coalition’s policies, procedures and internal controls asnecessary to ensure adequate guidance to staff is available for sole sourceprocurements and bidding requirements.

5. Conduct staff training as necessary to help ensure adherence to established or revisedpolicies and procedures.

11.0 – Subrecipient monitoring

The current period monitoring procedures were performed to identify any subrecipient activityfor this entity. If such activity was found, monitoring procedures were applied to determine if theentity’s disclosure requirements and subrecipient monitoring activities comply with federal grantprogram requirements, state laws and the entity’s own policies and procedures.

Based on results obtained from inquiries made to and an inspection of data itemsprovided by entity personnel the monitors noted no current year subrecipient activity.

DRAFT

The Early Learning Coalition of Flagler and Volusia Counties, Inc. (ELC 13)

2014-15 Financial Monitoring ReportPeriod Reviewed: October 1, 2013 – September 30, 2014

Schedule of Observations

Page - 18 -

III. Schedule of Observations

1.0 Observations from 2014-15 onsite visit

Observation #13.0 – Internal Control Environment – Review and update operating policies and procedures

We identified topics in the Coalition’s policies and procedures that need additionaldisclosures. No compliance issues were noted during our 2014-15 monitoring proceduresrelated to the items listed below; however, without complete and current policies andprocedures for staff the Coalition has an increased risk of errors and/or potential questionedcosts related to these areas of operations. We recommend the Coalition review and update itswritten policies and procedures to address these items before the close of program year 2014-15. Note: Coalition management confirmed an existing plan to update policies in 2015.

The Accounts Payable Policy and Procedure FSPP00002 is fairly comprehensivebut does not specifically require someone reconcile invoice quantities, prices, andpurchasing terms with the original purchase order. The Coalition is currentlyperforming this level of reconciliation but the documented procedures should bemodified to document this requirement since it is an important process of internalcontrol prior to payment for goods or services.

Policy CMPP00020 addresses Data Security and policy CMPP000001 addressesManagement Information Systems but neither of these policies specifically notesin writing for staff that uninstalling or disabling anti-virus software is prohibited.Policies currently indicate that personnel are not allowed to modify theconfiguration of computers, but additional specific requirements for computerupdates and anti-virus software may be warranted as people tend to turn off thesecritical updates and programs to remove the requirement for additional rebootmessages or speed up computer processing.

Procurement and Purchasing Policy was updated in the prior year to address theprocurement threshold from $25,000 to $35,000 but gaps remain in the policy forsteps necessary for procurements in excess of $25,000 but less than $34,999. Theinstructions for quote requirements should be updated to reflect currentrequirements for amounts ranging from $25,000 to $34,999.99.

2.0 Items for OEL follow-upThe monitoring team noted no items for OEL follow-up.