Embed Size (px)

Citation preview

in association with ABRACOM and IBRI

Thursday June 29th 2006

Governance and communication

“Sunlight is the best disinfectant”

Agenda

• Governance

• Trends in disclosure in major markets

• Key communication issues for public companies – Non financial information – XBRL

• Changing communication solutions for professionals

Governance • What is corporate governance?

• Major concerns for stakeholders: – Corporate governance has shifted from a

compliance obligation to a business imperative.

– Corporate governance is a global imperative.– One size doesn’t fit all investors.– Innovative approaches to corporate

governance challenges.

Trends in disclosure in major markets

Trends in disclosure in major markets

Focus on…

The US •The US has 2 different types of mandatory disclosure: structured and unstructured.

• Information is “material” when there is a “substantial likelihood” that a “reasonable investor” would find it important in the “total mix” of information.

• Structured disclosure: registration statements, prospectus, proxy statement, 10K, 10Q and 8K documents, and their equivalents for foreign companies. Issuers are obliged to file these with the SEC; in 1997, electronic filing to the EDGAR database was progressively introduced.

The US – continued • “Unstructured” disclosure covers dissemination of worthwhile information and prohibits companies from selectively providing material information. Required by NYSE, NASDAQ, AMEX

• Reg FD introduced in 2000. The rule aims to do away with selective material disclosure to investors, analysts, brokers and traders. Companies must distribute material information broadly to the market. Webcasts.

• Sarbanes-Oxley – real time disclosure. Mandates that each company “disclose to the public on a rapid and current basis such additional information concerning material changes in the financial condition or operations of the issuer.”

Trends in disclosure in major markets

Focus on…

European Union

Introducing the Transparency Obligations Directive

Context

•The regulations on financial services have differed among member states since the EU was invented in 1957.

•This has resulted in lack of cross border capital and investment flows.

•The EU wanted a “single” market for investment.

Financial Services Action Plan

• The FSAP was designed to introduce a single market.

• It has comprised 39 different Directives, including …..– IFRS, – Market Abuse, – Prospectus etc

• One of these is TOD.

TOD time line

2002 2003 2004 2005 2006 2007

Comm consults on need

Parliament approves

level 1

CESR publishes

its advice

EU States Publ. level 3

20th

Jan

Comm. Publ

level 2

What’s in TOD?

Major elements are:

•Financial reporting timetable

•Major shareholder reporting

•Dissemination

•Storage

Trends in disclosure in major markets

Focus on…

Asia • Japan – Tokyo Stock Exchange has just completed

major review of its disclosure obligations. – Likely outcome is increased disclosures on

directors dealings, material information etc. – Disclosures made through TD Net

Asia – continued • China – Improvements in disclosure – SOE’s – Foreign investors – Working party – Links to the SEC and ‘common agenda’

Trends in major markets – in summary • Key trends among regulators are to ensure that news is disseminated: •o Simultaneously. Empowering the individual investor in addition to the institutional investor •o Fast. The era of advertisements in national newspapers is ending, and real time electronic distribution is standard.•o “Push versus pull”. Simple posting of news on a website (either the issuer’s or a regulator’s) is insufficient. •o Media. Regulators are staying away from defining specific media outlets to be reached; rather they are using phrases like “appropriate media”, and “capable of reaching investors”.

Agenda

• Governance

• Trends in disclosure in major markets

• Key communication issues for public companies – Non financial information – XBRL

• Changing communication solutions for professionals

Non financial information

BUT! Regulatory disclosure is not enough…

It is about credibility• Investors demand transparency

• Governance fiascos have created a risk avoidance mentality

• World-class transparency and governance enhance valuation

• Emerging market issuers are suspect

• Reputational value drivers are key criteria for investors

Good Governance Builds Value

Investors will pay 28% more for emerging market companies that practice good corporate governance

McKinsey Quarterly

Corporate Value Drivers Changing

Quality of Management replaced EPS Growth as the #1 factor for U.S. money managers.

Reputation Matters More Now

64% of all investors say information about a company’s reputation is more important to them than one year ago. Rating Research Investor Confidence Survey

The Focus is Changing to Reputational Value Drivers•Leadership/Governance

•Communication/Transparency

•Brand Equity

•Intellectual Capital

•Innovation

•Human Capital

•Networks/Alliances

Traditional accounting has remained focused on tangible assets. As a result, a significant portion of corporate assets go under-reported in the financial accounts. The relative lack of accounting recognition of intangibles coupled with their growing importance in the value creation process means that the financial statements have lost some of their value for shareholders. If other information does not fill the void, there could be misallocation of resources in capital markets.

(OECD)

The Coloplast test

• One group of analysts received the full (excellent) non financial disclosures.

• A second group of analysts received a minimum compliant document.

• The result?

• The first group issued more BUY recommendations, even though they issued lower valuations.

(Source PWC)

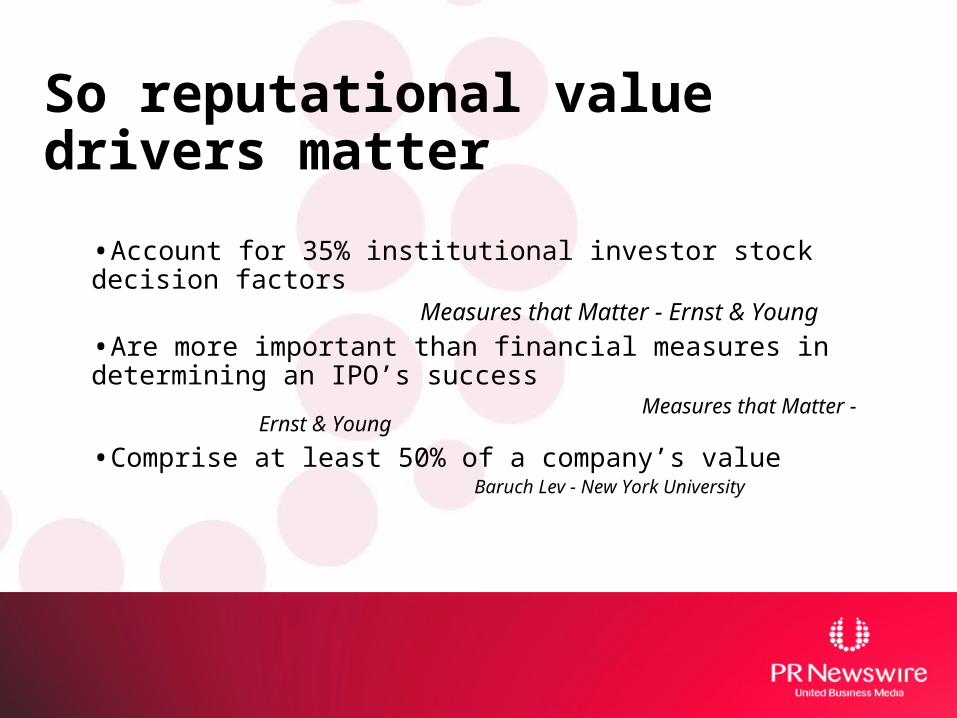

So reputational value drivers matter

•Account for 35% institutional investor stock decision factors

Measures that Matter - Ernst & Young

•Are more important than financial measures in determining an IPO’s success

Measures that Matter - Ernst & Young

•Comprise at least 50% of a company’s valueBaruch Lev - New York University

XBRL

• XBRL is a language for the electronic communication of business and financial data which is revolutionising business reporting around the world. It provides major benefits in the preparation, analysis and communication of business information. It offers cost savings, greater efficiency and improved accuracy and reliability to all those involved in supplying or using financial data.

XBRL in Action

Agenda

• Governance

• Trends in disclosure in major markets

• Key communication issues for public companies – Non financial information – XBRL

• Changing communication solutions for professionals

Changing role for the news release • Knowledge workers move away from press articles as key information source, to press releases

• Today’s news release reaches: – The media PLUS – Web users– Bloggers, – Social media networks, online communities,

• Using multi media – image, audio, video – RSS, podcasts…..

The wire: complete and simultaneous delivery to media, investors and end users

Press releases

Information distribution

Validation Formatting

Translations

Information network

• Companies in the private or public sector , • Communication agencies

“wire” Internet, satellites, Dedicated lines, fax

Email, print

Journalists

Investors

The public

Targets

Press agencies

Internet sites

Financial news wires

Aggregators (Intranets)

PRNJPR Newswire

for Journalists

MEDIAtlas

Clients

In conclusion • Stakeholders are demanding excellence in corporate governance.

• Disclosure is a practical means of compliance….

•….but is not enough. Non financial information adds to the story.

• XBRL is one the most exciting opportunities for issuers

• And technology presented by PR Newswire is available to help communicate with with audiences.

Thank you.

Any questions?