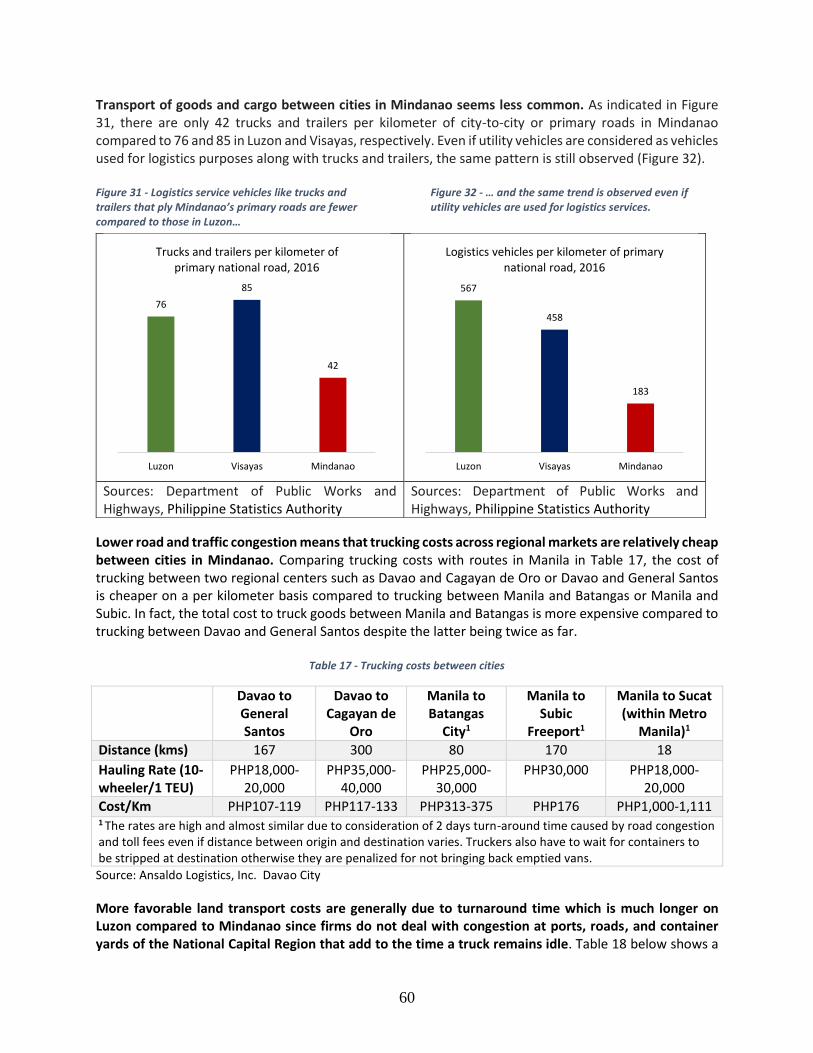

Embed Size (px)

Citation preview

1

Improving Mindanao Agro-Industrial Competitiveness through better Logistics and Connectivity

October 2019

A project of the World Bank Group, with the support of the Australian Government through the

Australia-World Bank Philippines Development Trust Fund.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

2

© 2019 International Bank for Reconstruction and Development / The World Bank

1818 H Street NW

Washington DC 20433

Telephone: 202-473-1000

Internet: www.worldbank.org

This work is a product of the staff of The World Bank Group with external contributions. The findings,

interpretations, and conclusions expressed in this work do not necessarily reflect the view of the Australian

Government, the Canadian Government, the World Bank Group, its Board of Executive Directors, or the

governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors,

denominations, and other information shown on any map in this work do not imply any judgment on the part of

The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this work is subject to copyright. Because The World Bank encourages dissemination of its

knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full

attribution to this work is given.

Any queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications,

The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522- 2625; e-mail:

3

This report was prepared by a World Bank Group team led by Roberto Martin Nolan Galang (Private Sector Specialist). Key inputs were provided by Patrick Verissimo (Lead Agriculture Economist), Mahmoud Momtaz (Private Sector Specialist), Maya Villaluz (Senior Environmental Engineer), Eugeniu Osmochescu (Senior Private Sector Specialist), Andres Garcia (Senior Economist), Charles Kunaka (Lead Private Sector Specialist), Paul Phumpiu (Senior Economist) , Victor Dato (Senior Infrastructure Specialist), Karen Annette Lazaro (Consultant), Maria Beatrice Anne Tanjangco (Consultant), Roberto Arquiza (Consultant), Simon Peter Gregorio (Consultant), and Anton Arguelles (Consultant). Yvette Villostas (Program Assistant), Reinaluz Ona (Program Assistant), and other team members in the Philippine Country Office provided valuable logistics and administrative support. The extended team contributed background papers or provided advice. The following individual consultants prepared background papers for the report: Larry Digal and his team comprised of Marvin Louie Orbeta and Carol Balgos for their Value Chain Analysis of Vegetables and Cacao, Annette O. Pelkmans-Balaoing and Jane Lynn Capacio and their team comprised of Reinier de Guzman and Anthony John Rodriguez for their Network Analysis of Mindanao Value Chains, Celina Agaton, Richard Sigua, Noriel Tiglao, and Joe Cruz for their work on OpenStreetMap, Origin-Destination Commodity Flow Surveys, and Freight Interview Surveys, and Nikki Philline C. de la Rosa and International Alert for statistics on Mindanao security issues. The team would like to thank Natasha Beschorner (Senior Specialist), Rick van der Kamp (Senior Operations Officer – Agribusiness), Brad Roberts (Senior Private Sector Specialist) for their contributions to the IT solutions chapter. The team worked under the overall supervision and guidance of Ndiame Diop (Practice Manager), Mona E. Haddad (Director), Dahlia Khalifa (Practice Manager), Birgit Hansl (Program Leader), Souleymane Coulibaly (Program Leader), and Mara K. Warwick, (Country Director for the Philippines). The team would like to thank those who participated in the Concept Note and Decision review meeting, particularly the reviewers Tanja Goodwin (Senior Economist), Petter Lundkvist (Regulatory Specialist), Carolina Figueroa-Geron (Lead Rural Development Specialist), and Massimiliano Cali (Senior Economist) and other participants who provided helpful comments, Achim Fock (Operations Manager), Ndiame Diop (Practice Manager), Victor Dato (Senior Infrastructure Specialist), Yolanda Azarcon (Senior Operations Officer), David Llorito (Communications Officer), Clarissa David (Senior Communication Officer), Nora Weisskopf (Transport Specialist), and Steven Jaffee (Lead Agriculture Economist). The findings, interpretations, and conclusions expressed in this Report are those of World Bank staff and do not necessarily reflect the views of the Australian Government and the World Bank or its management, Executive Board, or the governments they represent. For questions and comments on the content of this publication, please contact Roberto Martin Nolan Galang ([email protected]). Questions from the media can be addressed to David Llorito ([email protected]). For information on the work of the World Bank Group on Competition Policy, please visit www.worldbank. org/en/topic/competitiveness/brief/competition-policy. For information about the World Bank and its activities in the Philippines, please visit www.worldbank.org/ph

4

Tables of Contents

EXECUTIVE SUMMARY ........................................................................................................................................... 8

INTRODUCTION AND CONTEXT ............................................................................................................................ 14

CHAPTER 1. RURAL LOGISTICS AND AGRICULTURAL DEVELOPMENT ................................................................... 20

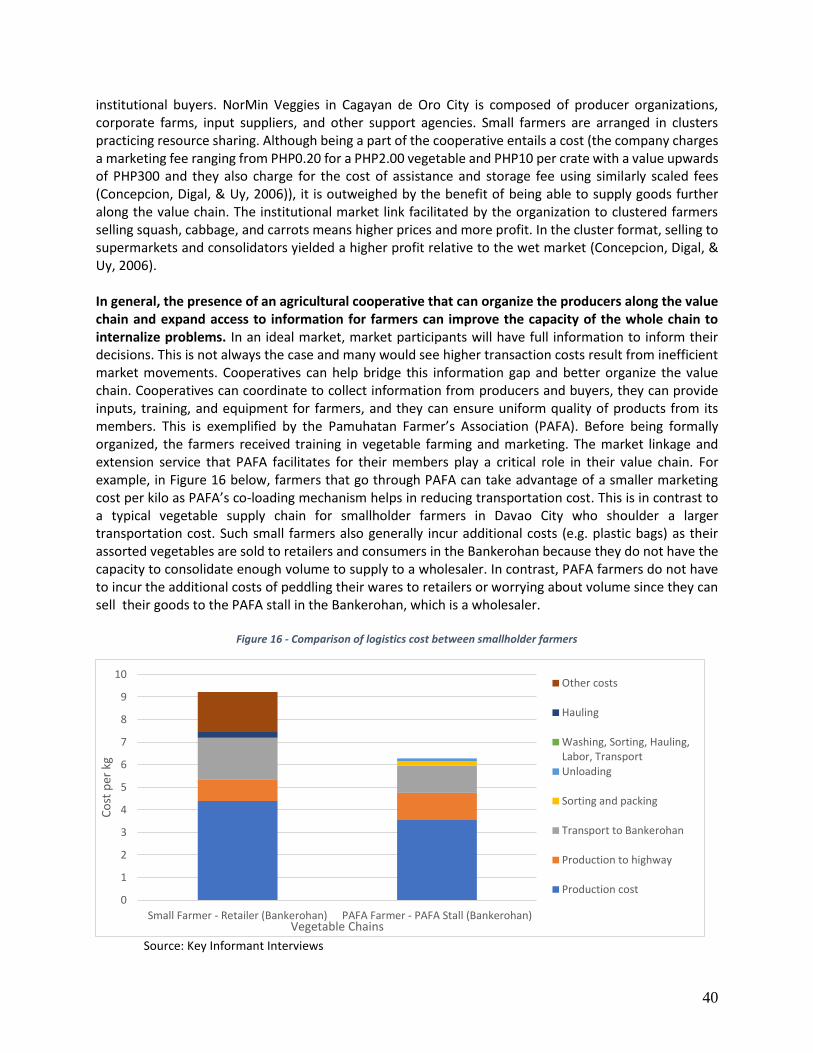

UNDERSTANDING THE VEGETABLE LOGISTICS CHAIN IN MINDANAO .................................................................. 22 PRODUCTION .............................................................................................................................................................. 22 CONSOLIDATION .......................................................................................................................................................... 24 RETAILERS .................................................................................................................................................................. 26

UNDERSTANDING THE CACAO LOGISTICS CHAIN IN MINDANAO ......................................................................... 31 PRODUCTION .............................................................................................................................................................. 31 CONSOLIDATION .......................................................................................................................................................... 32 PROCESSING AND RETAIL ............................................................................................................................................... 33

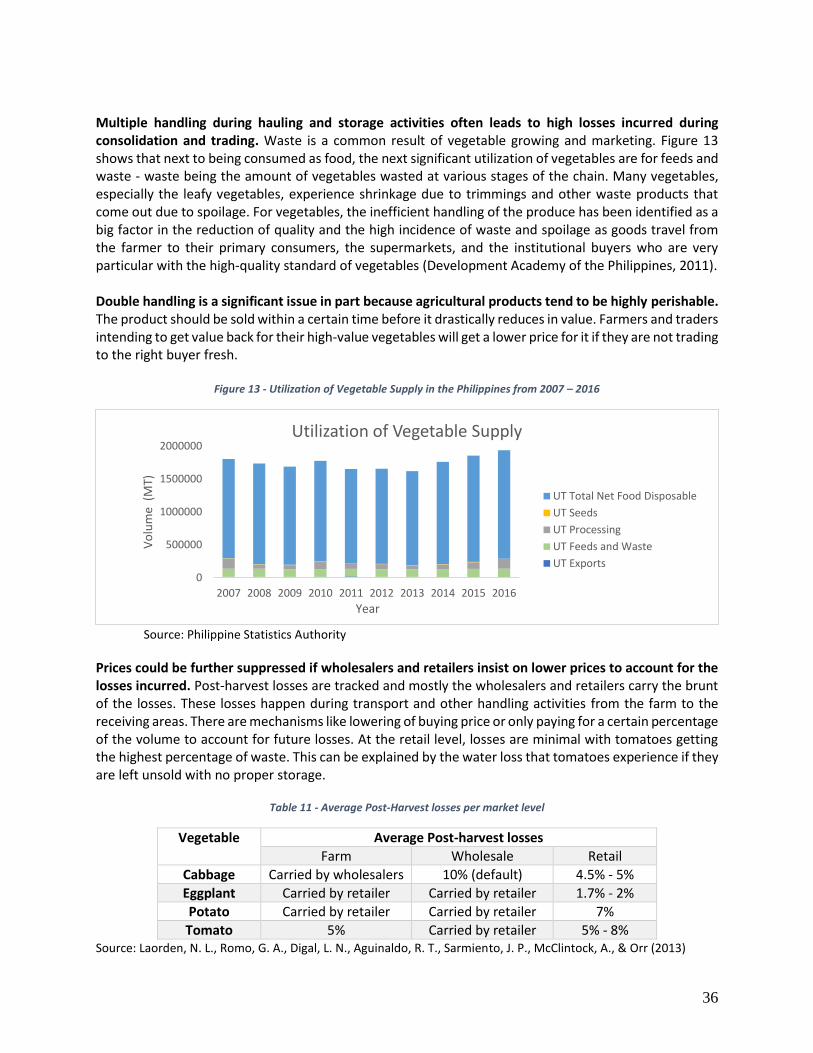

INEFFICIENCIES IN THE AGRICULTURAL LOGISTICS CHAINS .................................................................................. 34 LACK OF INFORMATION ................................................................................................................................................. 34 DOUBLE HANDLING AND SPOILAGE ................................................................................................................................. 35 QUALITY CONTROL ....................................................................................................................................................... 37

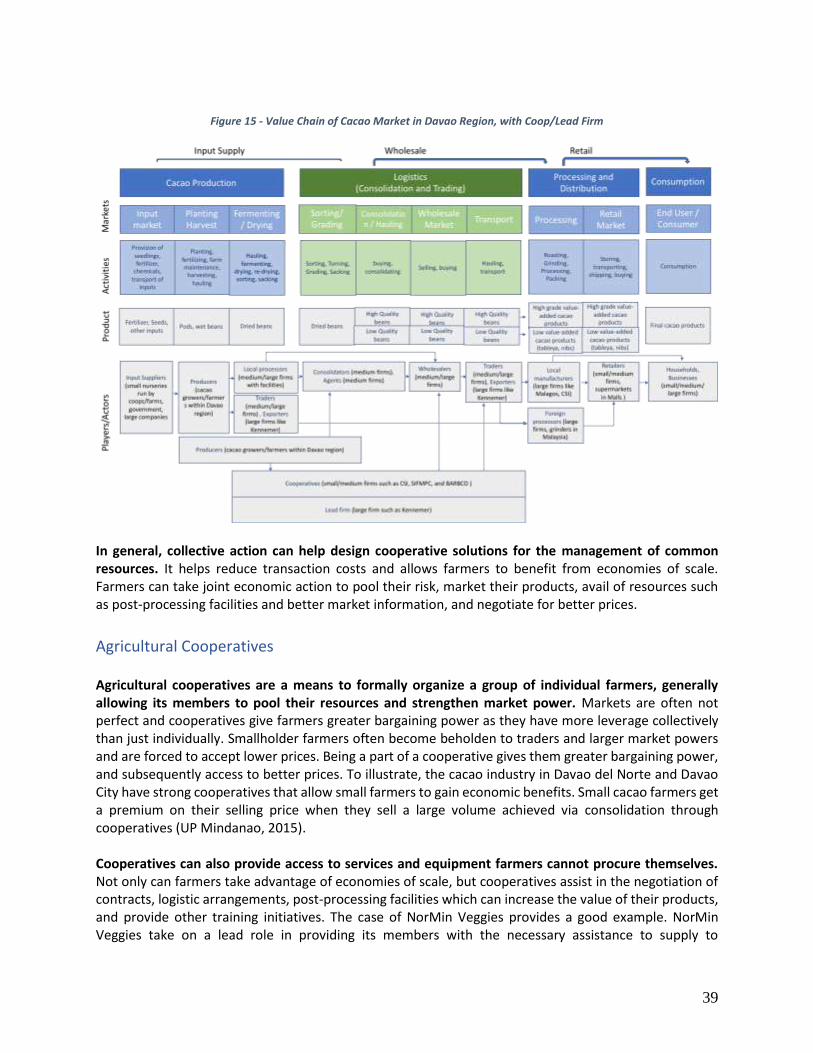

SOLUTIONS TO BETTER ORGANIZING THE AGRO-LOGISTIC VALUE CHAIN ............................................................ 38 AGRICULTURAL COOPERATIVES ....................................................................................................................................... 39 LEAD FIRMS ................................................................................................................................................................ 43 PRODUCTIVE ALLIANCES ................................................................................................................................................ 44 TRADING CENTERS ....................................................................................................................................................... 46 IT SOLUTIONS .............................................................................................................................................................. 49 SUMMARY .................................................................................................................................................................. 52

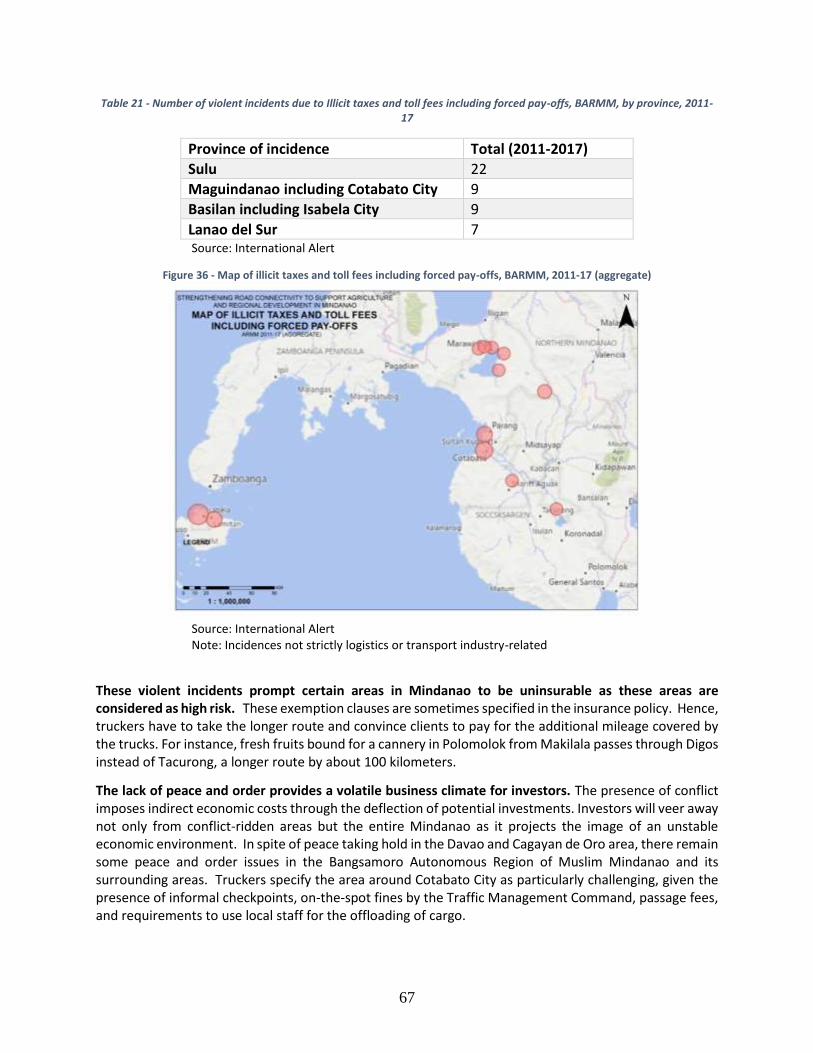

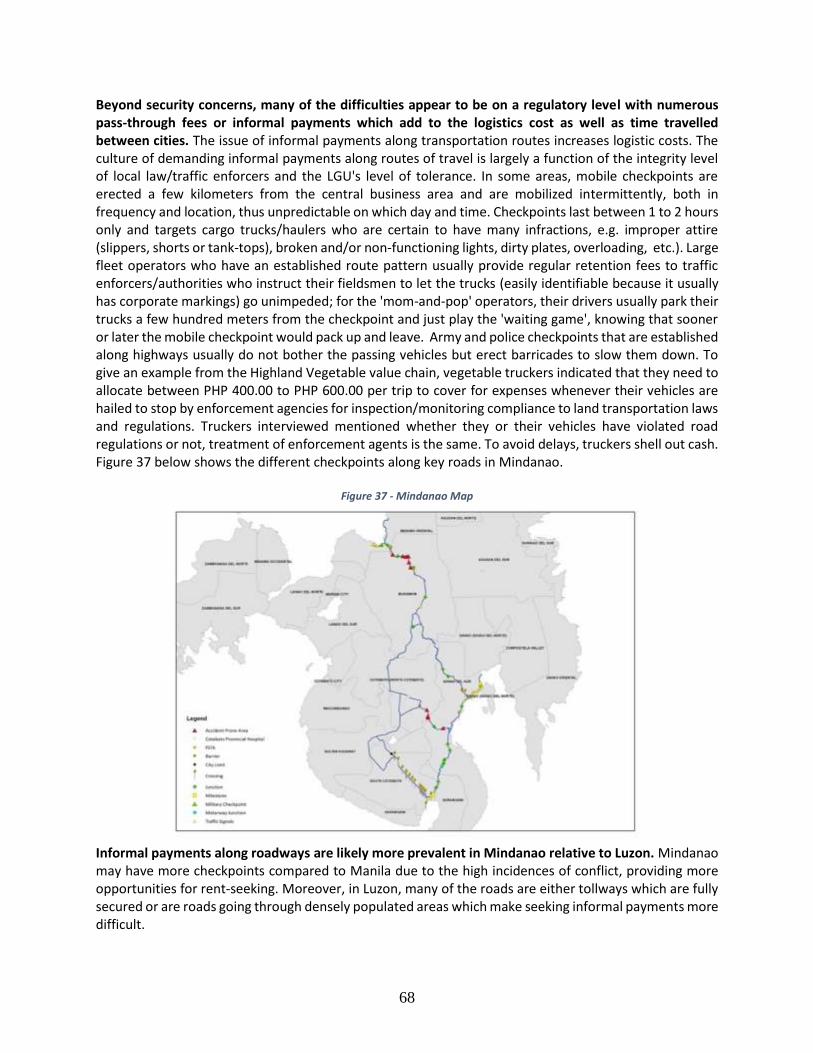

CHAPTER 2. URBAN-TO-URBAN LOGISTICS AND INDUSTRIAL DEVELOPMENT ..................................................... 53 SPATIAL DISPERSION AND FOUR-POLE DEVELOPMENT ......................................................................................................... 56 POTENTIAL FROM BETTER INTER-CITY LOGISTICS ................................................................................................................. 59 SECURITY CONCERNS .................................................................................................................................................... 66 PORT CONSOLIDATION AND REGULATION ......................................................................................................................... 70 SUMMARY .................................................................................................................................................................. 73

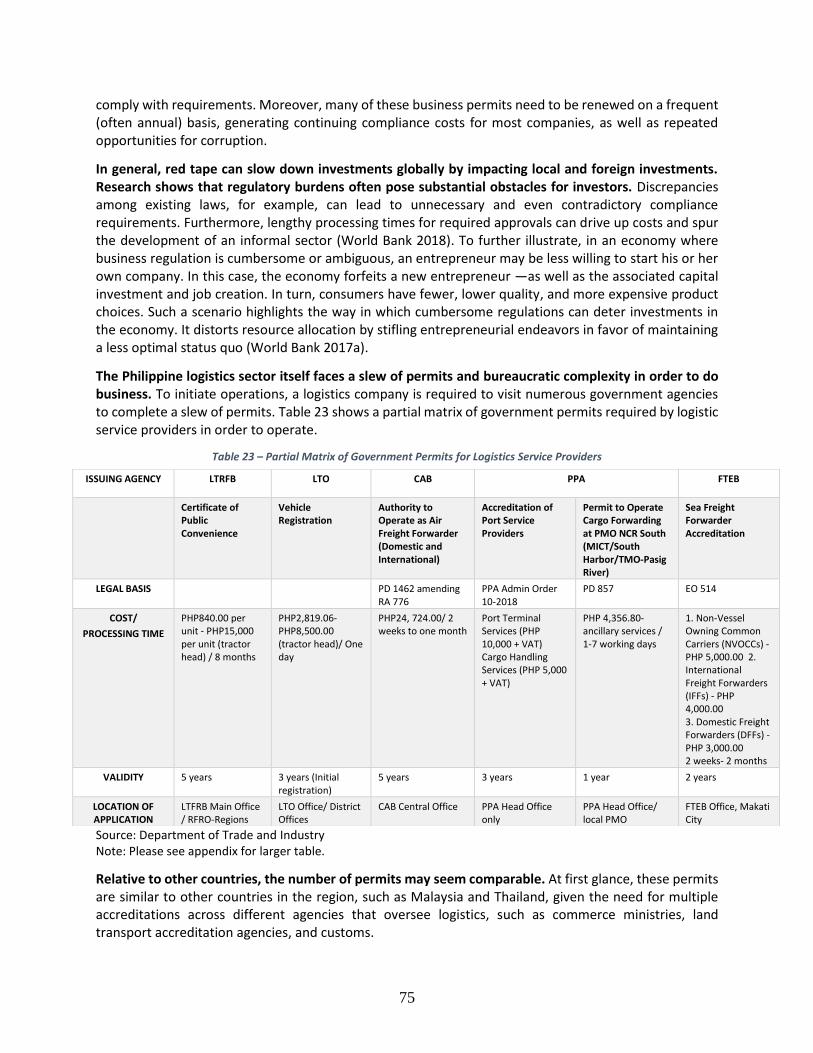

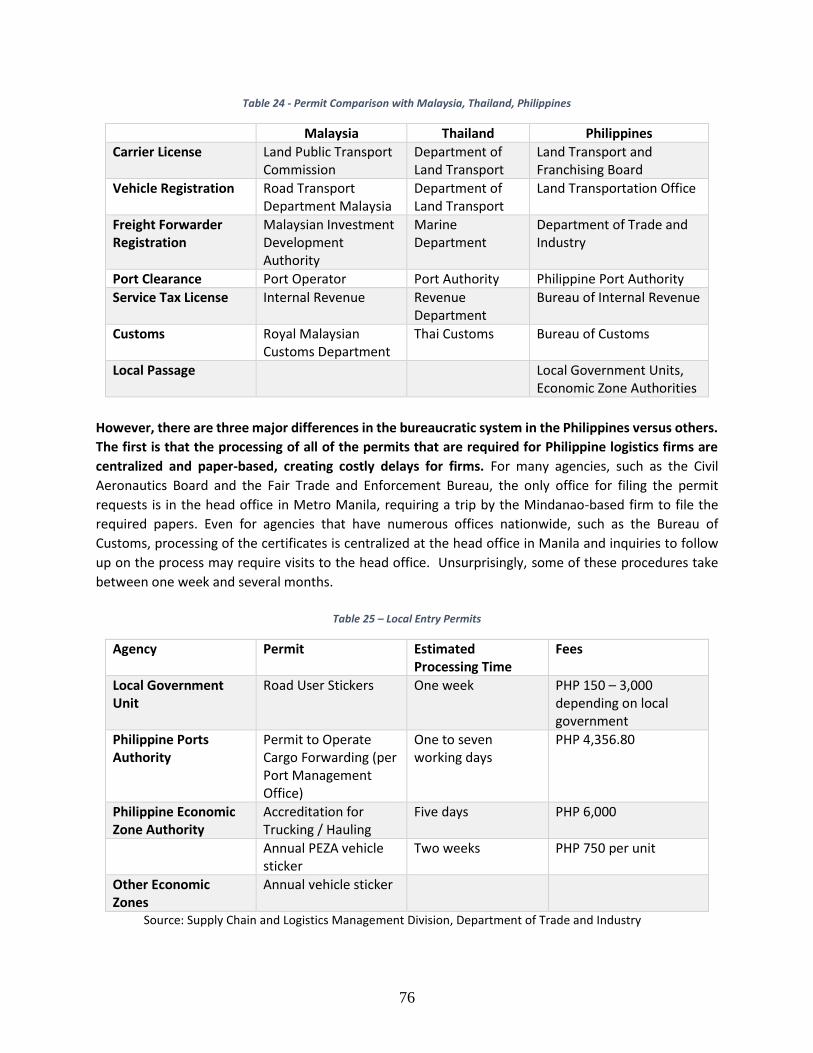

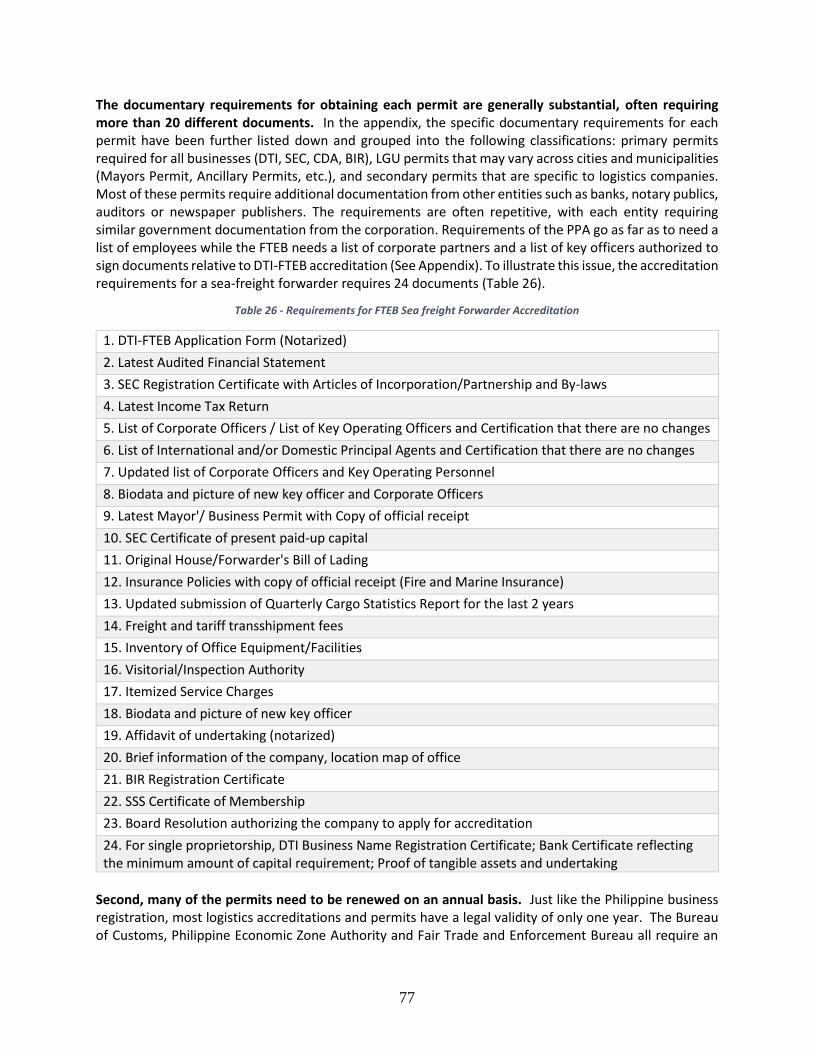

CHAPTER 3. COMPLEX REGULATORY PROCEDURES ............................................................................................. 74 REGIONAL AUTONOMY: THE CASE OF THE BANGSAMORO AUTONOMOUS REGION OF MUSLIM MINDANAO .................................. 81

CHAPTER 4. COMPETITION ASSESSMENT OF KEY LOGISTICS SECTORS ................................................................. 82 ANTI-COMPETITIVE REGULATIONS AND GOVERNMENT INTERVENTION .................................................................................... 85

Trucking .............................................................................................................................................................. 86 Ports ................................................................................................................................................................... 88 Domestic Shipping .............................................................................................................................................. 89 Freight Forwarding ............................................................................................................................................. 90

CONCLUSION ....................................................................................................................................................... 93

RECOMMENDATIONS .......................................................................................................................................... 95

REFERENCES ......................................................................................................................................................... 99

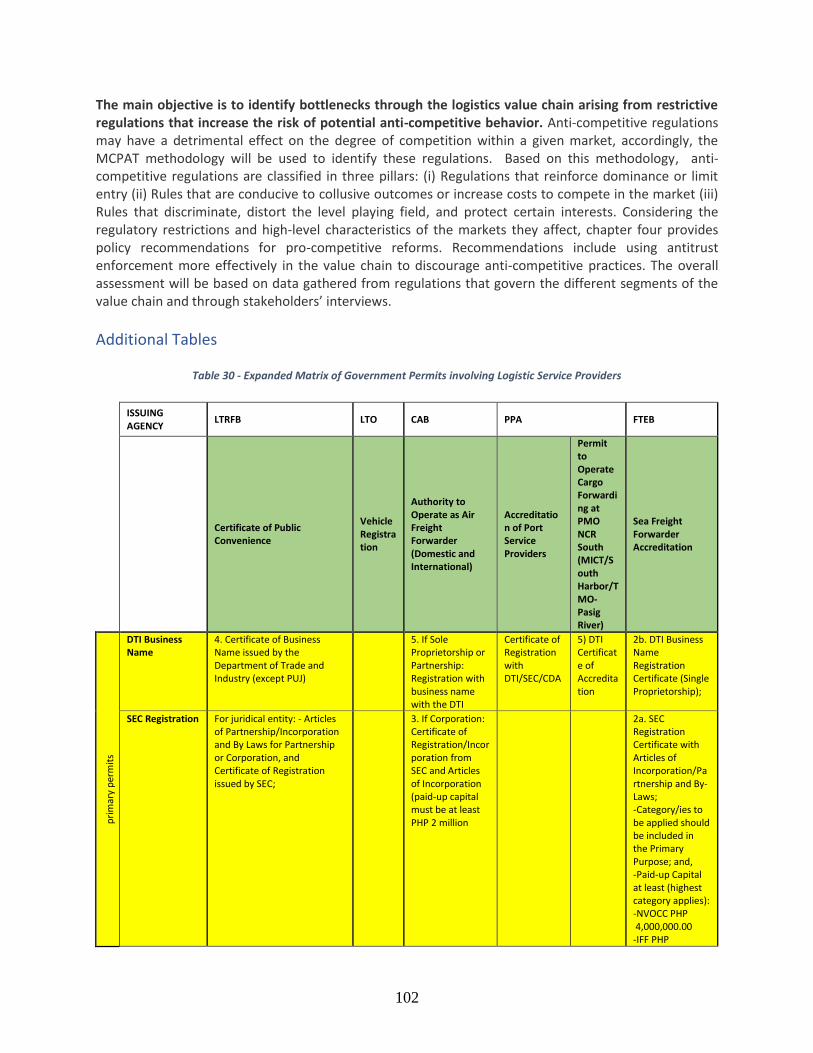

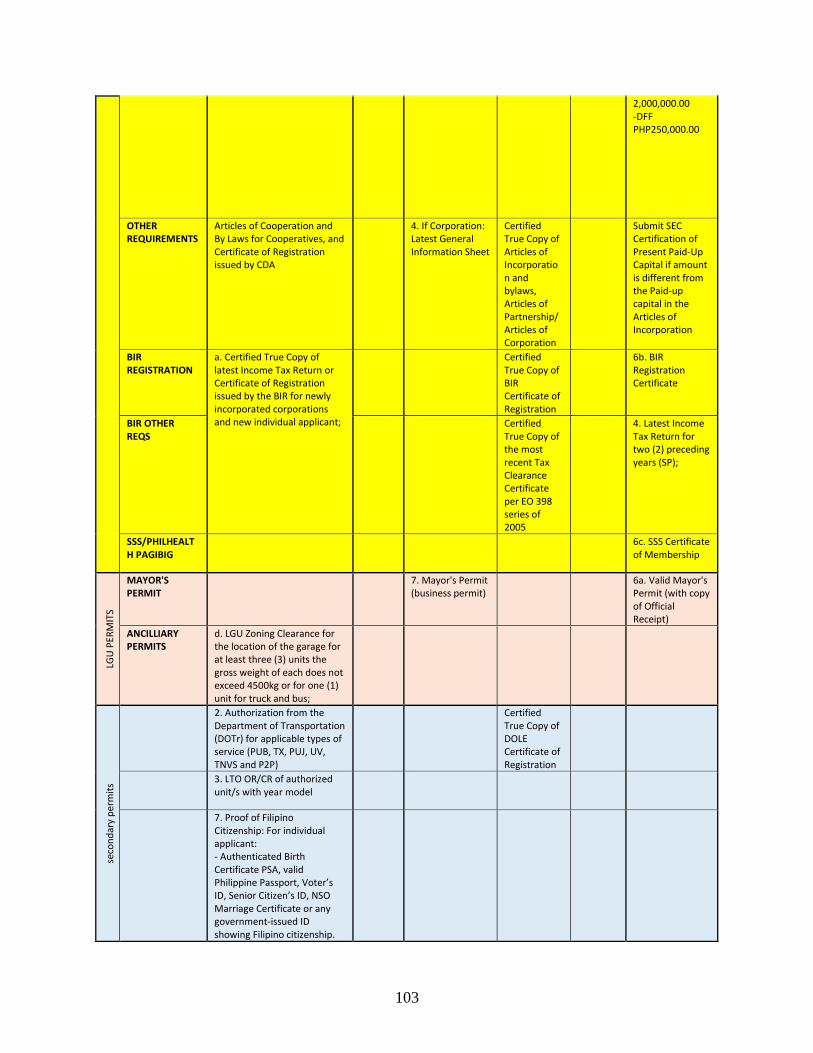

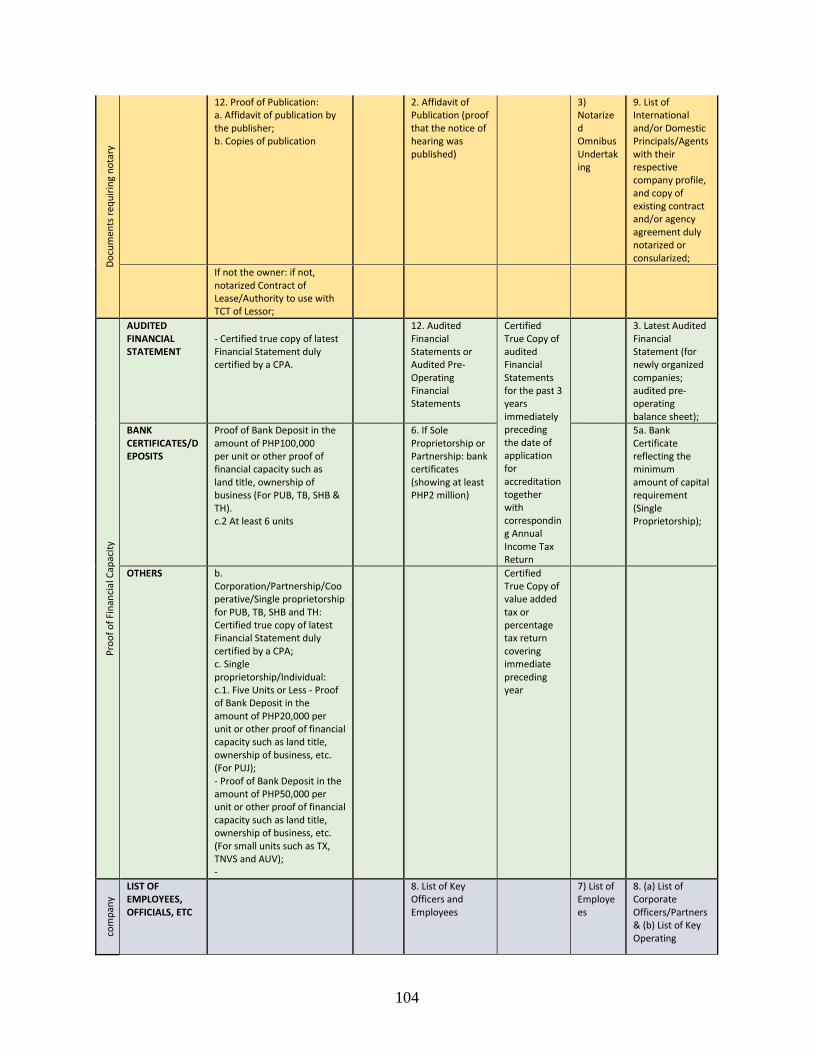

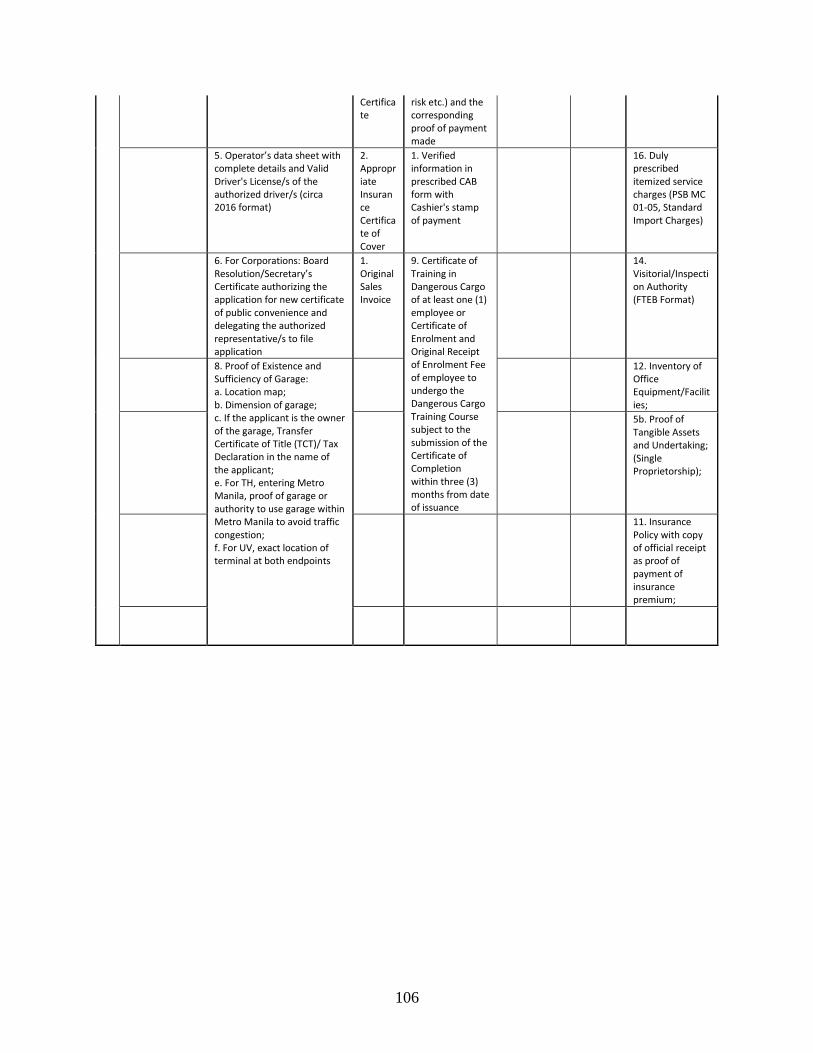

APPENDIX .......................................................................................................................................................... 100 METHODOLOGIES USED ............................................................................................................................................... 100 ADDITIONAL TABLES ................................................................................................................................................... 102

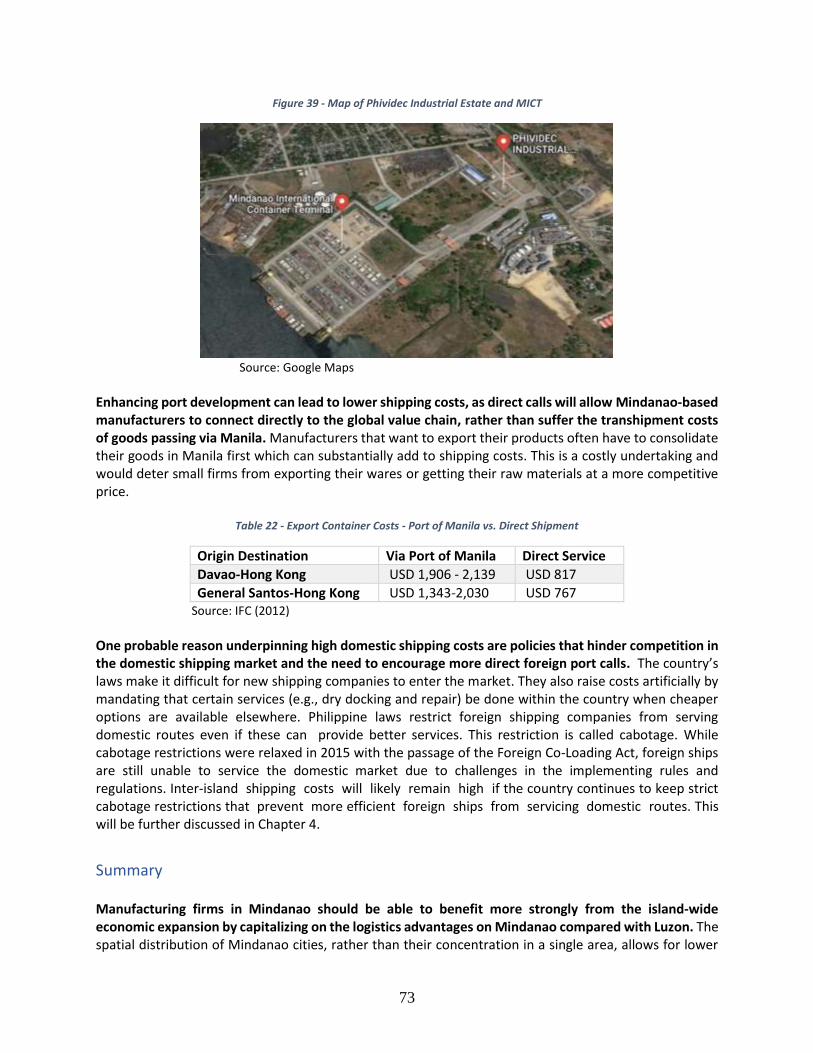

5

List of Tables TABLE 1 - FOOD AND LIVE ANIMALS INTER-ISLAND COMMODITY FLOW PATTERNS (2017) ............................................................. 14 TABLE 2 - GROWTH RATES OF SELECT SECTORS BY REGION (2016 – 2018) ................................................................................ 15 TABLE 3 - SHARE OF EMPLOYMENT IN MANUFACTURING FROM TOTAL, BY MAJOR ISLAND GROUPS, APRIL 2017 ............................. 16 TABLE 4 - COMPARATIVE STATISTICS ................................................................................................................................... 17 TABLE 5 - HOUSEHOLD CONSUMPTION PER CAPITA OF SELECTED VEGETABLES IN THE PHILIPPINES (2000, 2009, 2012) .................... 21 TABLE 6 - SAMPLE QUALITY REQUIREMENTS OF SUPERMARKETS IN DAVAO CITY ......................................................................... 27 TABLE 7 - COST AND RETURNS COMPARISON OF VEGETABLE CLUSTERS BETWEEN THEIR MARKETS ................................................... 27 TABLE 8 - COINTEGRATION OF VEGETABLE PRICES ACROSS MARKETS (RETAIL, WHOLESALE, AND FARMGATE) .................................... 29 TABLE 9 - ESTIMATED VOLUME OF DRIED, FERMENTED BEANS PER ORGANIZATION IN DAVAO REGION ............................................ 33 TABLE 10 - SEASONALITY OF FARM PRICES OF SELECTED VEGETABLES IN MAJOR MARKETS OF MINDANAO (1990-2015) ................... 35 TABLE 11 - AVERAGE POST-HARVEST LOSSES PER MARKET LEVEL ............................................................................................. 36 TABLE 12 - PROFITABILITY COMPARISON: FIRST AND SECOND CHANNELS ................................................................................... 41 TABLE 13 - SAMPLE PRICES OF COMMODITIES PER MARKET OUTLET .......................................................................................... 42 TABLE 14 – AGRI-PINOY TRADING CENTERS PER REGION AND BY STATUS AS OF NOVEMBER 2018 ................................................ 46 TABLE 15 - GROWTH RATES OF SELECT SECTORS BY REGION (2016 – 2018) .............................................................................. 53 TABLE 16 - MODE OF SALE OF PRODUCTS AND BY-PRODUCTS ................................................................................................. 54 TABLE 17 - TRUCKING COSTS BETWEEN CITIES ....................................................................................................................... 60 TABLE 18 - EXAMPLE TURNAROUND SCHEDULE OF TRUCK PLYING MANILA-CALAMBA ROUTE AND PANABO-MADAUM ..................... 61 TABLE 19 - LOAD FACTORS OF FREIGHT VEHICLES EXTRACTED FROM THE FREIGHT INTERVIEW SURVEY ........................................... 62 TABLE 20 - TRUCK BANS IN MINDANAO URBAN CITIES ........................................................................................................... 63 TABLE 21 - NUMBER OF VIOLENT INCIDENTS DUE TO ILLICIT TAXES AND TOLL FEES INCLUDING FORCED PAY-OFFS, BARMM, BY PROVINCE, 2011-17 ... 67 TABLE 22 - EXPORT CONTAINER COSTS - PORT OF MANILA VS. DIRECT SHIPMENT ...................................................................... 73 TABLE 23 – PARTIAL MATRIX OF GOVERNMENT PERMITS FOR LOGISTICS SERVICE PROVIDERS ...................................................... 75 TABLE 24 - PERMIT COMPARISON WITH MALAYSIA, THAILAND, PHILIPPINES ............................................................................. 76 TABLE 25 – LOCAL ENTRY PERMITS ..................................................................................................................................... 76 TABLE 26 - REQUIREMENTS FOR FTEB SEA FREIGHT FORWARDER ACCREDITATION ..................................................................... 77 TABLE 27 - STANDARD COST MODEL - DOCUMENTARY REQUIREMENTS FOR APPLICATION OF ACCREDITATION OF NEW SEA FREIGHT FORWARDERS ... 80 TABLE 28 - KEY PILLARS FOR FOSTERING COMPETITION .......................................................................................................... 83 TABLE 29 - RECOMMENDATIONS FOR ENHANCING PROCOMPETITIVE REGULATIONS AND GOVERNMENT INTERVENTION .................... 91 TABLE 30 - EXPANDED MATRIX OF GOVERNMENT PERMITS INVOLVING LOGISTIC SERVICE PROVIDERS ......................................... 102

List of Figures FIGURE 1 - OUTPUT PER WORKER BY SIZE FIGURE 2 - SHARE OF FIRMS BY FIRM SIZE .............................................................. 16 FIGURE 3 - RURAL BARANGAYS NOT CONNECTED TO A NATIONAL HIGHWAY, BY REGION, 2010, PERCENT ....................................... 18 FIGURE 4 - OPEN SIGNAL MAP FIGURE 5 - BASS MAP ..................................................................................................... 18 FIGURE 6 - ANNUAL PERCENTAGE GROWTH RATE OF VEGETABLE PER CAPITA CONSUMPTION IN SOUTHEAST ASIA (2000 – 2013) ...... 21 FIGURE 7 - LOGISTICS VALUE CHAIN OF VEGETABLE MARKET IN DAVAO REGION ........................................................................ 22 FIGURE 8 - PRODUCTION OF VEGETABLES BY REGION (2019) .................................................................................................. 23 FIGURE 9 - MINDANAO AGRICULTURE INFRASTRUCTURE......................................................................................................... 24 FIGURE 10 - ORIGIN-DESTINATION MAP FOR DAVAO, CAGAYAN DE ORO, AND GENERAL SANTOS WITH RESPECTIVE CATCHMENT AREA ................... 30 FIGURE 11-DISTRIBUTION OF VOLUME OF CARROTS FROM BULUA MARKET (OUTBOUND) IN CAGAYAN DE ORO.............................. 30 FIGURE 12 - VALUE CHAIN OF CACAO MARKET IN DAVAO REGION ........................................................................................... 31 FIGURE 13 - UTILIZATION OF VEGETABLE SUPPLY IN THE PHILIPPINES FROM 2007 – 2016 ........................................................... 36 FIGURE 14 - CACAO PRODUCT PRICE LADDER, AS OF 2018 ..................................................................................................... 37 FIGURE 15 - VALUE CHAIN OF CACAO MARKET IN DAVAO REGION, WITH COOP/LEAD FIRM ........................................................ 39 FIGURE 16 - COMPARISON OF LOGISTICS COST BETWEEN SMALLHOLDER FARMERS ....................................................................... 40 FIGURE 17 - PAFA - DIRECTED GRAPH ................................................................................................................................. 42 FIGURE 18 - CORE ELEMENTS OF A PRODUCTIVE ALLIANCE ...................................................................................................... 45 FIGURE 19 - PROPOSED PROJECTS FROM STAKEHOLDERS ......................................................................................................... 48 FIGURE 20 - LOOP BOOKING STEPS .................................................................................................................................... 51

6

FIGURE 21 - MINDANAO'S INDUSTRY SECTOR HAS RECENTLY GAINED MOMENTUM... .................................................................. 54 FIGURE 22 - ALTHOUGH ITS OUTPUT SHARE HAS CONSISTENTLY REMAINED RELATIVELY SMALL COMPARED TO LUZON ........................ 54 FIGURE 23 - SHARE OF TOTAL REVENUE FROM MANUFACTURING GOODS SOLD DOMESTICALLY ACROSS ISLAND GROUPS ..................... 55 FIGURE 24 - SHARE OF TOTAL REVENUE FROM MANUFACTURING GOODS SOLD ABROAD ACROSS ISLAND GROUPS ............................. 55 FIGURE 25 - OUTPUT PER WORKER BY SIZE ........................................................................................................................... 56 FIGURE 26 - SHARE OF FIRMS BY FIRM SIZE ........................................................................................................................... 56 FIGURE 27 - LOCATIONS OF INDUSTRIAL CLUSTERS IN MINDANAO ............................................................................................ 57 FIGURE 28 - LOCATIONS OF INDUSTRIAL CLUSTERS ALONG THE ROUTE FROM MANILA TO LA UNION (LUZON) ................................. 58 FIGURE 29 - MINDANAO HAS LOW INTER-URBAN TRAFFIC FIGURE 30 - MINDANAO HAS RELATIVELY WIDER PROVINCIAL ROADS DUE

TO FEWER VEHICLES PLYING THE ROADS………………………………………………………………………………………………………………….59 FIGURE 31 - LOGISTICS SERVICE VEHICLES LIKE TRUCKS AND TRAILERS THAT PLY MINDANAO’S PRIMARY ROADS ARE FEWER COMPARED TO THOSE IN LUZON… ....... 60 FIGURE 32 - … AND THE SAME TREND IS OBSERVED EVEN IF UTILITY VEHICLES ARE USED FOR LOGISTICS SERVICES. ............................. 60 FIGURE 33 - CONTAINER TRUCKS ALONG MAIN ROUTE MANILA – LA UNION ............................................................................ 63 FIGURE 34 - CONTAINER TRUCKS ALONG MAIN ROUTE CAGAYAN DE ORO, DAVAO AND GEN SAN PORT ROUTES ............................ 65 FIGURE 35 -CONFLICT IN MINDANAO BY TYPE ...................................................................................................................... 66 FIGURE 36 - MAP OF ILLICIT TAXES AND TOLL FEES INCLUDING FORCED PAY-OFFS, BARMM, 2011-17 (AGGREGATE) ...................... 67 FIGURE 37 - MINDANAO MAP ........................................................................................................................................... 68 FIGURE 38 - VESSEL TRAFFIC, DAVAO SASA VS. DICT ............................................................................................................ 72 FIGURE 39 - MAP OF PHIVIDEC INDUSTRIAL ESTATE AND MICT ............................................................................................... 73 FIGURE 40 - LOGISTICS VALUE CHAIN AND POTENTIAL BOTTLENECKS ........................................................................................ 86 FIGURE 41 - DISTRIBUTION OF TRUCKING COMPANIES BY FLEET SIZE FOR REGION XI .................................................................... 87 FIGURE 42 - THE STANDARD COST MODEL FORMULA .......................................................................................................... 101

List of Boxes BOX 1 - DAVAO FOOD TERMINAL COMPLEX ......................................................................................................................... 49 BOX 2 - INFORMAL PAYMENTS IN THE WOOD INDUSTRY DRIVING LOGISTIC COSTS ..................................................................... 69 BOX 3 - ECONOMY-WIDE MARKET STRUCTURE .................................................................................................................... 84

List of Acronyms

ACIAR Australian Center for International Agricultural Research

APTC Agri-Pinoy Trading Center

ARTA Anti-Red Tape Authority

BASS Bandwidth and Signal Statistics

BARMM Bangsamoro Autonomous Region in Muslim Mindanao

BAPTC Benguet Agri-Pinoy Trading Center

BSU Benguet State University

BIR Bureau of Internal Revenue

BPS Bureau of Philippine Standards

CSI Chokolate de San Isidro

CDA Cooperative Development Authority

CCN Customs Client Number

DICT Davao International Container Terminal

DAR Department of Agriculture

DTI Department of Trade and Industry

DOTR Department of Transportation

7

DFF Domestic Freight Forwarders

EDSA Epifanio delos Santos Avenue

FTEB Fair Trade and Enforcement Bureau

FMR Farm-to-market roads

FEB Farmer Entrepreneurship Program

FIS Freight Interview Survey

GIS Geographic Information System

GVA Gross Value Added

HHI Herfindahl-Hirschman Indices

ICC Import Commodity Clearance

IT Information Technology

IFC International Finance Corporation

IFF International Freight Forwarders

JFC Jollibee Foods Corporation

KFI Kennemer Foods International

LTFRB Land Transport and Franchising Regulatory Board

LPI Logistics Performance Index

MICT Manila International Container Terminal

MARINA Maritime Industry Authority

MCPAT Markets Competition Policy Assessment Tool

NGO Non-governmental organization

NPDL Non-Professional Driver’s License

NVOCC Non-Vessel Operating Cargo Carrier

NVOCC Non-Vessel Owning Common Carriers

PAFA Pamuhatan Farmer’s Association

PCM Price Cost Margins

PTO Permit to Operate

PEZA Philippine Economic Zone Authority

POS Point-Of-Sale

PPA Philippine Ports Authority

PRDP Philippine Rural Development Project

PMO Port Management Office

PMR Product Market Regulation

PA Productive Alliance

PDL Professional Driver’s License

SPS sanitary and phytosanitary

SEC Securities and Exchange Commission

SME Small and Medium Enterprises

TEFASCO Terminal Facilities and Services Corp

TEU Twenty-foot Equivalent Unit

8

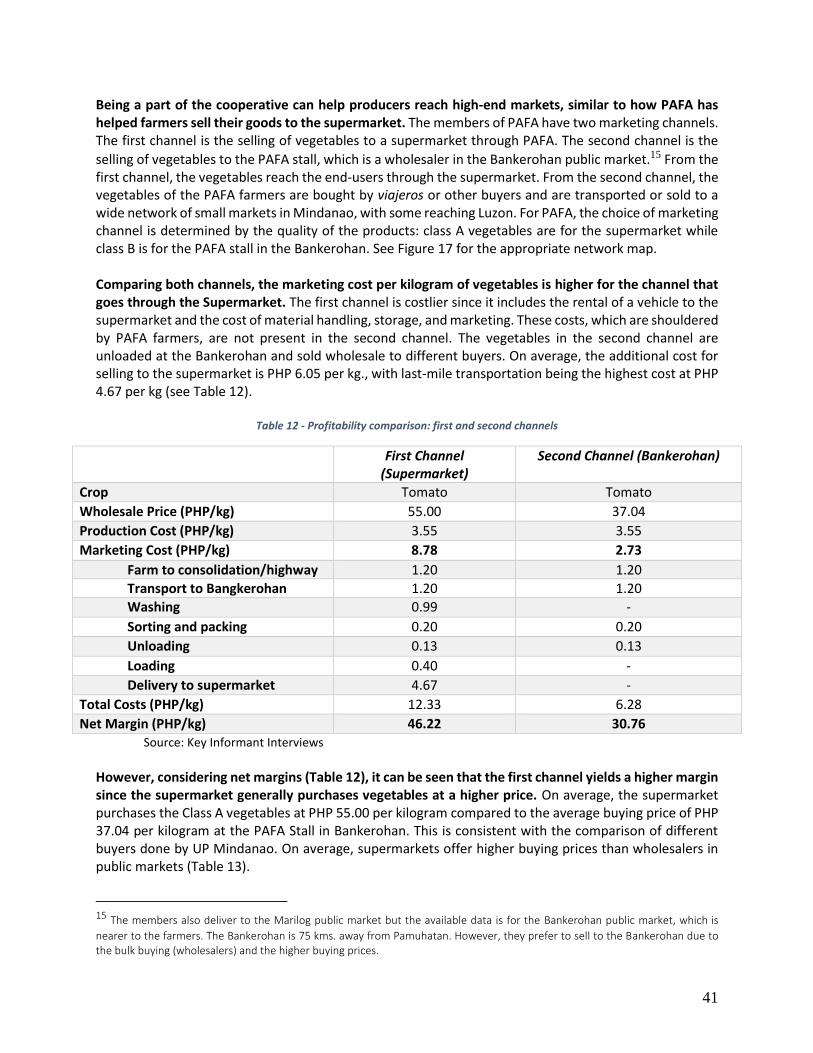

Executive Summary Despite being the largest food producer of the country, Mindanao remains Philippines’ poorest region. Mindanao is blessed with abundant natural resources, and the region supplies over 40 percent of the country’s food requirements and contributes more than 30 percent to national food trade. Yet, eight of the ten poorest provinces in the country are in Mindanao, with the Bangsamoro Autonomous Region in Muslim Mindanao (BARMM) being the poorest region in the country. At the heart of Mindanao’s high poverty rate is the region’s weak ability to transform its natural advantage into a competitive one in domestic and foreign markets. Products from the region are indeed not efficiently marketed and the quality remains sub-optimal due to logistical constraints. Alleviating these constraints will allow farmers to raise their margins and increase their profits. Buyers of vegetables, for instance, range from the wet markets to supermarkets and high-end industrial consumers. Greater farmers’ reach to supermarkets and industries would raise quality standards and, at the same time, raise potential margins for those able to supply to them. Similarly, for exportable products such as cocoa, meeting higher standards of quality is a key challenge for local producers. This report examines the key constraints faced by Mindanao agricultural and manufacturing producers along the supply chains. For agricultural products, vegetables and cacao were chosen as illustration of the typical constraints faced along different value chains. Vegetables is a smallholder crop consumed domestically with a relatively short supply chain composed of producers, consolidators, and primary consumers. This short supply chain reflects the domestic market focus and limited extent of processing Cacao, on the other hand, has a longer supply chain extending to export markets. Compared to vegetables, cacao requires an additional layer of processing (from wet beans to dry fermented beans to processing for chocolate) before it can reach its final markets. The report finds a host of constraints that undermine agricultural competitiveness in Mindanao. The long-standing issues of farm-to-market roads and inadequate infrastructure are still considerable concerns for Mindanao (and these are analyzed more extensively in the companion Mindanao Roads Connectivity report), but we also find that lack of market information, double handling, and quality control are equally pressing issues for the average farmer. The lack of information can reduce a farmers’ bargaining power, lead to poorly chosen investments, and inadequate production planning. Information gaps often lead to inefficient double handling practices resulting from a lack of trust among players in the value chain, which subsequently affects the amount of spoilage and waste. The infrastructure necessary to limit double handling and ensure consistent quality is either lacking or poorly designed. Several policy options are recommended to better organize the value chain of agricultural products and improve coordination. These include allowing agricultural cooperatives or lead firms to better manage the value chain, forging productive alliances among stakeholders, leveraging information technology, and organizing well-planned trading posts. A cooperative or a lead firm can improve the management of the value chain by introducing training programs to better organize production, act as a stable end-market, and reduce the number of middlemen along the value chain. Productive alliances can help address the issues of trust along the value chain as well as provide support (investments, technical assistance, and business development). Using information technology can improve efficiency and provide cutting edge solutions to logistic problems such as a transport booking app. Trading posts that are well located, community-driven, and providing updated market information facilitate coordination and exchange.

9

The report finds a striking contrast between agricultural and manufacturing supply chains, as logistics for the manufacturing sector is quite developed, compared to Luzon. Mindanao’s advantage over Luzon in terms of inter-city road freight and logistics stems from the dispersion of the population of Mindanao across different cities which reduces the level of transport congestion of Mindanao-based firms compared with their Luzon counterparts. Mindanao enjoys low-interurban traffic, relatively wider national roads, cheaper trucking costs on a per kilometer basis, an absence of number coding schemes, and more opportunities for backhaul. These provide significant potential benefits for growth and upgrading for manufacturing firms seeking to expand their activities. In fact, a large number of firms are leveraging this advantage already: Mindanao has been experiencing the highest rates of growth in the country over the past decade. Despite its rapid growth in recent years, further growth opportunities exist. First, firms on the island are still small, less productive, still focused on primary product processing, and generally geared for the domestic market, and thus display significant room for further development. Second, Mindanao itself is not yet considered a single market given its four urban centers are widely dispersed. Instead of treating the island as a potential 22-million wide consumer market, firms treat the cities of Davao, Cagayan de Oro, General Santos, and Zamboanga as separate markets. Industrial clusters have formed around these poles, while in contrast, in Luzon, industrial clusters developed in regions near highways. This helps explain why logistic development on the island has generally been port-city driven. Mindanao can also avoid the mistakes Metro Manila has made in addressing some of its logistic concerns. Many of the congestion problems in Metro Manila have started to appear in Mindanao such as traffic, lack of truck parking space, and container yard congestion issues. Mindanao has the opportunity to learn from Luzon’s experience by ensuring storage facilities remain sufficient and roads and parking areas for trucks are developed while land remains abundant. To address within-city congestion, Mindanao has opted to follow Metro Manila by implementing its own truck bans. While decongesting the roads, this may have implications for competition. For a durable expansion of an efficient logistics industry to support agriculture and manufacturing in Mindanao, however, further issues must be addressed:

• Security. Existing security concerns in urban areas pose additional impediments to moving cargo

around. Idle trucks can be victim to gas theft and informal checkpoints may impose additional

costs for travelling trucks. Conflict in certain areas also limits the routes a truck may travel through

and act as a deterrent for investments in affected areas.

• Ports. An upgrading of Mindanao’s ports should complement the improvements in inter-city

travel and lead to greater port consolidation and more direct shipments. The government should

more strongly leverage the private sector to design and implement large scale projects, utilizing

the privately-owned Davao International Container Terminal as an example for expanding the

capacity of Cagayan de Oro, General Santos and Davao-Sasa ports.

• Complex regulations and red tape. Complex regulatory procedures continue to hamper

investments in the logistics sector, especially the centralized processing of paper-based

requirements in Manila, the annual renewal of permits, and the prevalence of local pass-through

permits. Doing business in the Philippines is notably difficult with the country ranking 95th out of

190 countries in the latest 2020 World Bank Doing Business Indicators. To compound this, many

of the requirements are paper-based and processed centrally in Metro Manila.

10

• Limited clarity of responsibilities between public entities. The complexity of the regulations is

made worse by the lack of clarity in the devolution of powers to the Bangsamoro Autonomous

Region of Muslim Mindanao (BARMM). Instead of regional offices, BARMM has parallel

government agencies that may or may not be coordinated with the national government. There

does not seem to be any clear guidelines detailing which particular functions have been devolved

to the BARMM regional government and which functions are retained by the national

government.

• Competition issues. Several regulations reduce the degree of competition in logistics services,

namely trucking, port operations, domestic shipping, and freight forwarding. To illustrate, there

are foreign ownership restrictions in transportation and freight forwarding. Other competition

restrictions include the truck bans that limit the number of vehicles on the road, and inadequate

port facilities and other physical infrastructural limitations that restrict the kind of vessels serving

Mindanao.

In sum, Mindanao is rich with untapped potential that can be unleashed if we can better organize the agro-logistic value chain, further enhance inter-city logistics so Mindanao can function as an entire market and producer, streamline regulations and remove complex regulatory barriers, and improve market competition to ensure a more efficient and lower cost of doing business on the island. The table below summarizes the recommendations in the paper.

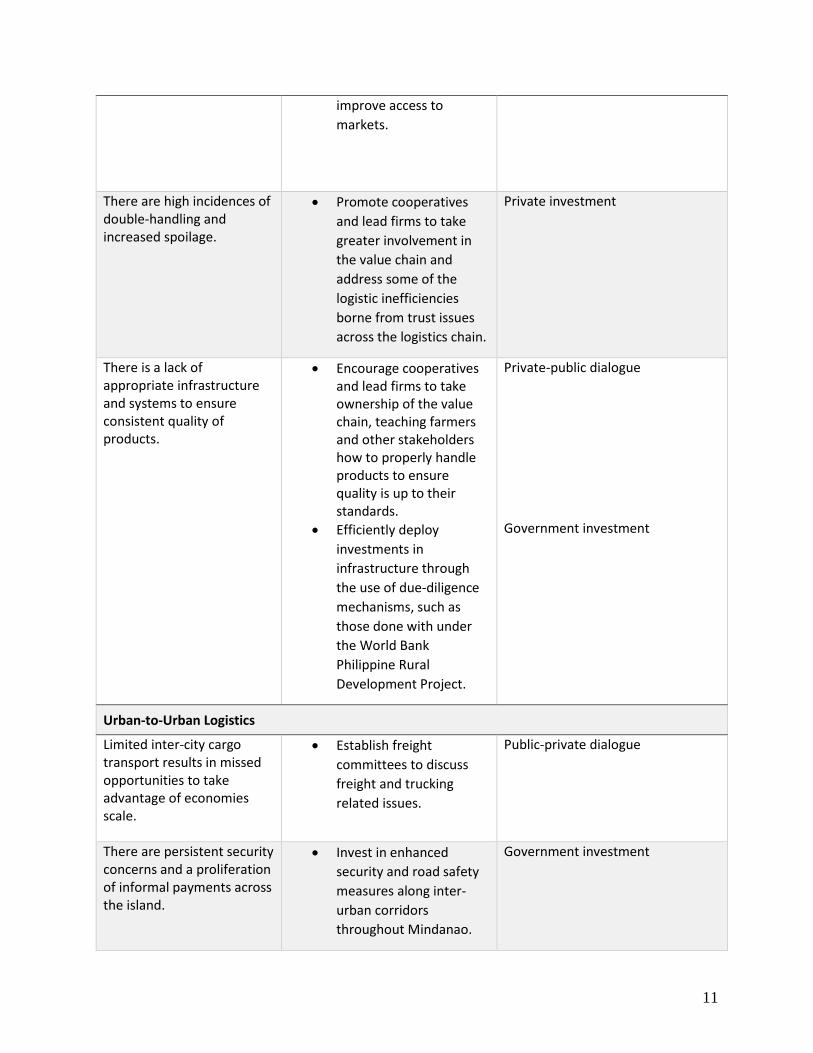

Issue Recommendation Instrument

Rural-to-Urban Logistics

There is a general lack of information or access to up-to-date information in terms of market prices and consumer demand.

• Set up additional trading centers that provide better information. These centers should be based on intensive consultations with users and built with specifications required by stakeholders.

• Employ suggested IT solutions to improve access to information and finance.

• Encourage the formation

of productive alliances

between producers,

buyers, and the public

sector to better

coordinate production,

sell collectively, increase

competitiveness, and

Private – public partnership Private investment Public-private dialogue

11

improve access to

markets.

There are high incidences of double-handling and increased spoilage.

• Promote cooperatives

and lead firms to take

greater involvement in

the value chain and

address some of the

logistic inefficiencies

borne from trust issues

across the logistics chain.

Private investment

There is a lack of appropriate infrastructure and systems to ensure consistent quality of products.

• Encourage cooperatives and lead firms to take ownership of the value chain, teaching farmers and other stakeholders how to properly handle products to ensure quality is up to their standards.

• Efficiently deploy

investments in

infrastructure through

the use of due-diligence

mechanisms, such as

those done with under

the World Bank

Philippine Rural

Development Project.

Private-public dialogue Government investment

Urban-to-Urban Logistics

Limited inter-city cargo transport results in missed opportunities to take advantage of economies scale.

• Establish freight

committees to discuss

freight and trucking

related issues.

Public-private dialogue

There are persistent security concerns and a proliferation of informal payments across the island.

• Invest in enhanced

security and road safety

measures along inter-

urban corridors

throughout Mindanao.

Government investment

12

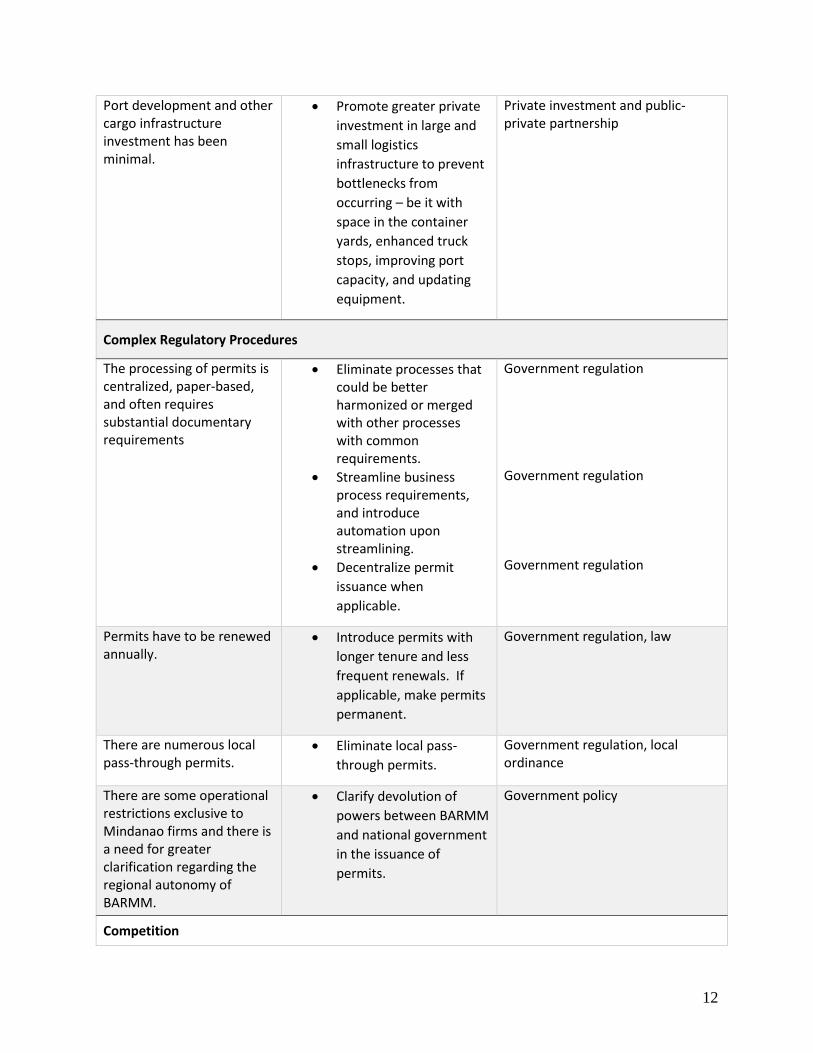

Port development and other cargo infrastructure investment has been minimal.

• Promote greater private

investment in large and

small logistics

infrastructure to prevent

bottlenecks from

occurring – be it with

space in the container

yards, enhanced truck

stops, improving port

capacity, and updating

equipment.

Private investment and public-private partnership

Complex Regulatory Procedures

The processing of permits is centralized, paper-based, and often requires substantial documentary requirements

• Eliminate processes that could be better harmonized or merged with other processes with common requirements.

• Streamline business process requirements, and introduce automation upon streamlining.

• Decentralize permit

issuance when

applicable.

Government regulation Government regulation Government regulation

Permits have to be renewed annually.

• Introduce permits with

longer tenure and less

frequent renewals. If

applicable, make permits

permanent.

Government regulation, law

There are numerous local pass-through permits.

• Eliminate local pass-

through permits.

Government regulation, local ordinance

There are some operational restrictions exclusive to Mindanao firms and there is a need for greater clarification regarding the regional autonomy of BARMM.

• Clarify devolution of

powers between BARMM

and national government

in the issuance of

permits.

Government policy

Competition

13

The ban on private trucking from carrying freight not belonging to the registered owner reduces efficiency and may represent a barrier to entry for new digital platforms.

• Reduce the restrictions

on private trucks to carry

freight not belonging to

the registered owner

while ensuring safety

standards are still met.

Government regulation

There are restrictions on foreign entry into public utility services.

• Clarify the legal definition

of Public Utilities to allow

greater foreign

investments in trucking

and other transport

services.

National law

The discretionary power granted to MARINA to intervene in prices for domestic shipping may negatively affect competition.

• Elimination of price

interference in Freight

Forwarding and Domestic

Shipping.

Government policy

There is a conflict of interest regarding the PPA's role as both regulator and operator of ports.

• Ensure competitive neutrality between public and private ports.

• Separate the PPA

regulatory function from

its ports development

and operations functions

to level the playing field

through greater private

management of ports.

Government policy National law

14

Introduction and Context A well-functioning logistics sector and greater connectivity is imperative for more inclusive growth, particularly for an archipelago like the Philippines where the transport sector feeds into many sectors, Developing infrastructure to connect distant areas to economic centers, increasing the mobility of people and goods, can diffuse economic concentration and facilitate quicker convergence of living standards for people living in the periphery. As an archipelago with no direct neighbors, the role of transportation and logistics is significant in the cost of doing business, as goods are trucked, ferried, and delivered to different parts of the country. This is particularly important for a region like Mindanao, which is geographically separated by several islands and bodies of water from the country’s capital. Mindanao is the southernmost island group of the Philippines, one of the three major subdivisions of the country (the others being Luzon and Visayas). Mindanao consists of the main-island Mindanao, several small islands off the northern and southern coast, and the Sulu Archipelago in the west which stretches to Borneo. Mindanao covers two-fifths of the country’s total land area, a third of territorial waters, and a fifth of the total population. Metro Manila to the northern most urban center of Cagayan de Oro is roughly 1,400 kilometers through the Pan-Philippine Highway. Being the second largest island and having the best agro-climatic conditions compared to the rest of the country, Mindanao has been named as the Philippines’ ‘food basket’. Mindanao supplies over 40 percent of the country’s food requirements and contributes more than 30 percent to national food trade. Table

11 shows that in 2017, a substantial amount of Mindanao’s total food and live animal production went to Luzon and Visayas. The island produces the majority of the country’s high-value export crops, such as 89

percent of pineapples and 72 percent of bananas,2 as well as numerous vegetables, fish, meats, grains and other goods for domestic consumption. Many of these exports are produced by multinational corporations and large local conglomerates that are supported by efficient and predictable supply chains.

Table 1 - Food and live animals inter-island commodity flow patterns (2017)

Destination (in metric tons)

Origin Luzon Visayas Mindanao Total

Luzon 664,185 1,057,269 318,880 2,040,334

Visayas 1,120,060 638,598 292,908 2,051,566

Mindanao 607,176 1,772,143 95,239 2,474,558

Total 2,391,421 3,468,010 707,027 6,566,458 Source: Philippine Statistics Authority

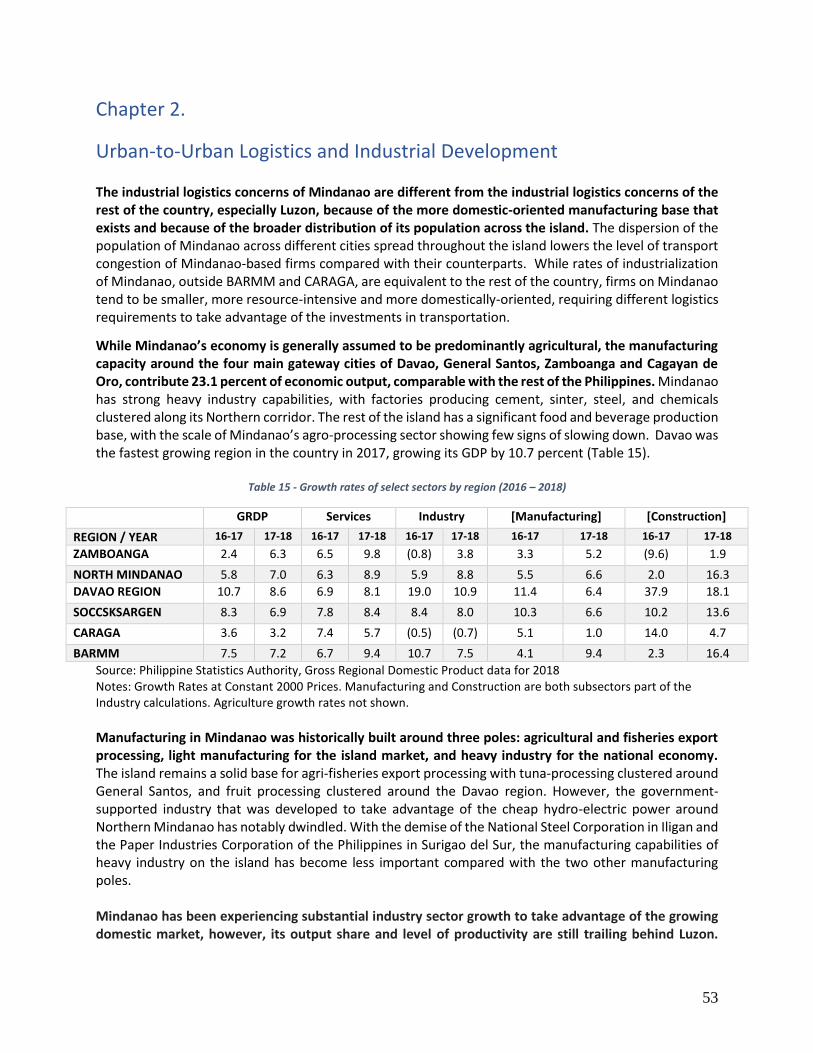

While Mindanao’s economy is generally assumed to be predominantly agricultural, the manufacturing capacity around the four main gateway cities of Davao, General Santos, Zamboanga and Cagayan de Oro, contribute 23.1 percent of economic output, comparable with the rest of the Philippines. Mindanao has a strong heavy industry capability, with factories producing cement, sinter, steel and chemicals clustered along its Northern corridor. The rest of the island has a significant food and beverage production

1 Gilberto M. Llanto, Mercedita A. Sombilla, and Francis Mark A. Quimba, “ Interregional Trade of High-value Fruits and Vegetables: Issues on Transport and Shipping”, PIDS Discussion Paper No. 2012-08, March 2012 2 Philippine Statistical Authority, “Major Fruit Crops Quarterly Bulletin”. Vol 10 No. 3. https://psa.gov.ph/sites/default/files/Q3%202016%20FRUITS_0_0.pdf

15

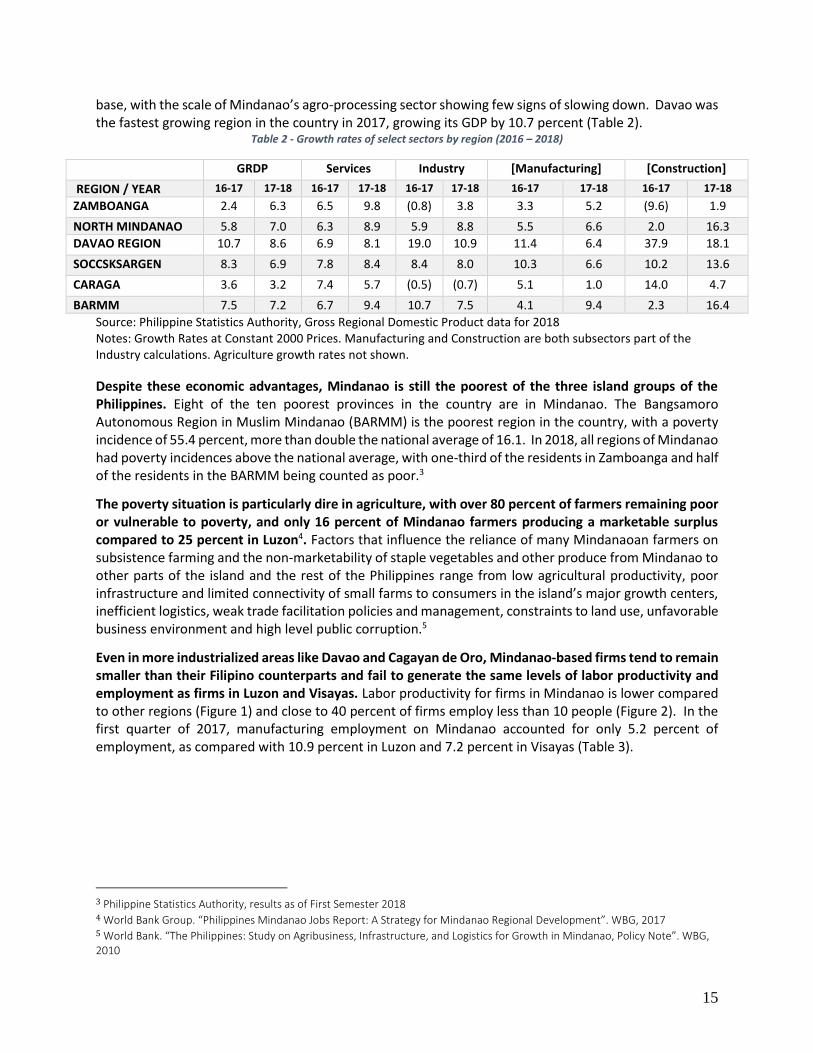

base, with the scale of Mindanao’s agro-processing sector showing few signs of slowing down. Davao was the fastest growing region in the country in 2017, growing its GDP by 10.7 percent (Table 2).

Table 2 - Growth rates of select sectors by region (2016 – 2018)

GRDP Services Industry [Manufacturing] [Construction]

REGION / YEAR 16-17 17-18 16-17 17-18 16-17 17-18 16-17 17-18 16-17 17-18

ZAMBOANGA 2.4 6.3 6.5 9.8 (0.8) 3.8 3.3 5.2 (9.6) 1.9

NORTH MINDANAO 5.8 7.0 6.3 8.9 5.9 8.8 5.5 6.6 2.0 16.3

DAVAO REGION 10.7 8.6 6.9 8.1 19.0 10.9 11.4 6.4 37.9 18.1

SOCCSKSARGEN 8.3 6.9 7.8 8.4 8.4 8.0 10.3 6.6 10.2 13.6

CARAGA 3.6 3.2 7.4 5.7 (0.5) (0.7) 5.1 1.0 14.0 4.7

BARMM 7.5 7.2 6.7 9.4 10.7 7.5 4.1 9.4 2.3 16.4

Source: Philippine Statistics Authority, Gross Regional Domestic Product data for 2018 Notes: Growth Rates at Constant 2000 Prices. Manufacturing and Construction are both subsectors part of the Industry calculations. Agriculture growth rates not shown.

Despite these economic advantages, Mindanao is still the poorest of the three island groups of the Philippines. Eight of the ten poorest provinces in the country are in Mindanao. The Bangsamoro Autonomous Region in Muslim Mindanao (BARMM) is the poorest region in the country, with a poverty incidence of 55.4 percent, more than double the national average of 16.1. In 2018, all regions of Mindanao had poverty incidences above the national average, with one-third of the residents in Zamboanga and half of the residents in the BARMM being counted as poor.3

The poverty situation is particularly dire in agriculture, with over 80 percent of farmers remaining poor or vulnerable to poverty, and only 16 percent of Mindanao farmers producing a marketable surplus compared to 25 percent in Luzon4. Factors that influence the reliance of many Mindanaoan farmers on subsistence farming and the non-marketability of staple vegetables and other produce from Mindanao to other parts of the island and the rest of the Philippines range from low agricultural productivity, poor infrastructure and limited connectivity of small farms to consumers in the island’s major growth centers, inefficient logistics, weak trade facilitation policies and management, constraints to land use, unfavorable business environment and high level public corruption.5

Even in more industrialized areas like Davao and Cagayan de Oro, Mindanao-based firms tend to remain smaller than their Filipino counterparts and fail to generate the same levels of labor productivity and employment as firms in Luzon and Visayas. Labor productivity for firms in Mindanao is lower compared to other regions (Figure 1) and close to 40 percent of firms employ less than 10 people (Figure 2). In the first quarter of 2017, manufacturing employment on Mindanao accounted for only 5.2 percent of employment, as compared with 10.9 percent in Luzon and 7.2 percent in Visayas (Table 3).

3 Philippine Statistics Authority, results as of First Semester 2018 4 World Bank Group. “Philippines Mindanao Jobs Report: A Strategy for Mindanao Regional Development”. WBG, 2017 5 World Bank. “The Philippines: Study on Agribusiness, Infrastructure, and Logistics for Growth in Mindanao, Policy Note”. WBG, 2010

16

Figure 1 - Output per worker by size Figure 2 - Share of firms by firm size

Source: Census of Philippine Businesses and Industries, 2012,

Manufacturing Source: Census of Philippine Businesses and Industries, 2012,

Manufacturing

Table 3 - Share of Employment in Manufacturing from Total, by major island groups, April 2017

Region/Year April 2017 Share of Manufacturing from Total Employment

Total Manufacturing Employment

Luzon 2,434 10.9%

Visayas 597 7.2%

Mindanao 502 5.2%

Total Employment

Luzon 22,390

Visayas 8,291

Mindanao 9,591 Source: Philippine Statistics Authority Note: units in (‘000 persons)

While Mindanao can ideally be seen as a single island market, it is still logistically divided around its main urban centers, leading to the loss of economies of scale. Firms consider the four major cities as four separate markets. Unlike Luzon where a bulk of the population is concentrated around a highly congested capital region, Mindanao’s population is spread across the urban centers on its Northern, Eastern, Southern and Western sides. The four major cities are Cagayan de Oro, Davao, General Santos and Zamboanga, respectively, each of which has a population that ranges from 600,000 to 1.5 million people6. With a total population comprising of almost 22 million people, Mindanao’s market can benefit from being treated as a single market, which can lead to economies of scale and dramatically lower logistics costs.

6 According to the 2010 Census, Davao city had a population of 1,449,296, Cagayan de Oro City had a population of 602,088, General Santos City had a population of 538,086, and Zamboanga of 807,129.

17

Improving logistics efficiency becomes essential to achieving the economic transformation of Mindanao; but unfortunately, the Philippines ranks poorly in the logistics space compared with its regional peers7. At a global scale, several studies identify agro-logistics as one of the key constraints to agri-business development and growth in agricultural trade8. Table 4 provides an overview of some of the commonly used indicators to compare the logistics, trade and shipping performance across several World Bank indices. The Philippines performs below regional peers in the Logistics Performance Index, Trading Across Borders in the Doing Business Ranking (with the exception of Indonesia), and the Logistics Shipping Connectivity Index computed by UNCTAD. The country ranks 60th in the LPI, even lower than that of Indonesia, Thailand, Malaysia, and Vietnam. This is much further than its more developed peers Japan (#5) and Korea (#25).

Table 4 - Comparative Statistics

Statistic Year Malaysia Thailand Indonesia Philippines Vietnam

Logistics Performance Index (Ranking) 2018 41/160 32/160 46/160 60/160 39/160

Logistics Performance Index (Rating) 2018 3.22/5.00 3.41/5.00 3.15/5.00 2.90/5.00 3.27/5.00

Liner Shipping Connectivity Index 2017 98.1/100 41.0/100 40.9/100 25.0/100 65.61/100

Trading Across Borders (Ranking) 2020 49/190 62/190 116/190 113/190 104/190

Trading Across Borders (Rating) 2020 88.5/100 84.6/100 67.5/100 68.4/100 70.8/100

Services Trade Restrictiveness Index 2012 42.7 46.8 54.4 50.7

Container Port Throughput (000 TEUs) 2017 24,719 10,732 13,860 8,197

Merchant Fleet (000 DWT) 2018 19,524 7,559 20,299 1,927 Source: World Bank and UNCTAD

Many manufacturers and farmers have raised concerns about the inefficiencies of logistics on Mindanao

that limit their competitiveness. Among the specific issues raised are the lack or absent market or storage

areas, high freight and shipping cost, lack of consolidation, and complex permitting procedures issued

from Manila. While large growers such as Dole and Del Monte can internalize many of these costs, such

logistics concerns are insurmountable to many smallholder farmers. This high cost of logistics has been

partially quantified by recent survey data on SMEs from a World Bank Group supported study by the

Department of Trade and Industry. They indicate that in Mindanao, logistics can cost a manufacturing firm

a third of its sales, much higher than compared to Luzon (17.5 percent) or Visayas (25 percent), indicating

that logistics costs faced by Mindanao farmers will be much more prohibitive.9

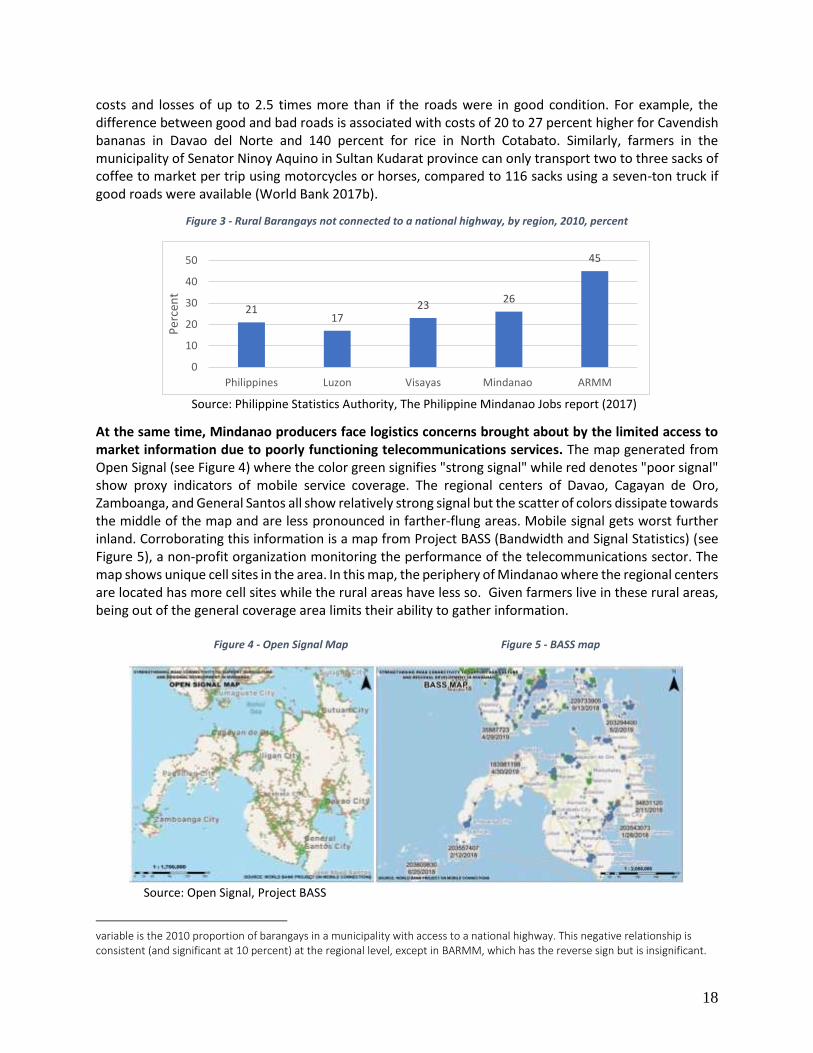

Many of the logistical issues are rightly attributed to transport infrastructure concerns on Mindanao, chief among which is the lack of well-lit, paved, and secure roads to connect farms to their markets. The Mindanao Jobs Report (2017) highlights that 26 percent of rural barangays in Mindanao—45 percent in the BARMM—were not connected to a national road (Figure 3), a much higher proportion than in Luzon or the Visayas. The report also writes that there is a high correlation between a barangay’s lack of access to a national highway and municipal poverty; a 1 percentage point increase in the percentage of barangays with no access to a national highway is associated with a 0.2 percentage point increase in the incidence of municipal poverty10. It also states that poor village roads in Mindanao lead to higher transportation

7 World Bank Group, 2018. https://lpi.worldbank.org/international/global 8 World Bank Group. “Agro-Logistics in Central America: A Supply Chain Approach”. EU SSD, LAC, WBG, 2012 9 Banomyong, Ruth. “Understanding Logistics Performance in the Philippines”. WBG-DTI. (See Manufacturing Logistics Performance Philippines 2017v1 (full).pptx) 10 According to the Philippine Mindanao Jobs report (2017), this finding is based on a double log regression with regional dummies and a control for altitude. The dependent variable is the 2012 incidence of municipal poverty and the independent

18

costs and losses of up to 2.5 times more than if the roads were in good condition. For example, the difference between good and bad roads is associated with costs of 20 to 27 percent higher for Cavendish bananas in Davao del Norte and 140 percent for rice in North Cotabato. Similarly, farmers in the municipality of Senator Ninoy Aquino in Sultan Kudarat province can only transport two to three sacks of coffee to market per trip using motorcycles or horses, compared to 116 sacks using a seven-ton truck if good roads were available (World Bank 2017b).

Figure 3 - Rural Barangays not connected to a national highway, by region, 2010, percent

Source: Philippine Statistics Authority, The Philippine Mindanao Jobs report (2017)

At the same time, Mindanao producers face logistics concerns brought about by the limited access to market information due to poorly functioning telecommunications services. The map generated from Open Signal (see Figure 4) where the color green signifies "strong signal" while red denotes "poor signal" show proxy indicators of mobile service coverage. The regional centers of Davao, Cagayan de Oro, Zamboanga, and General Santos all show relatively strong signal but the scatter of colors dissipate towards the middle of the map and are less pronounced in farther-flung areas. Mobile signal gets worst further inland. Corroborating this information is a map from Project BASS (Bandwidth and Signal Statistics) (see Figure 5), a non-profit organization monitoring the performance of the telecommunications sector. The map shows unique cell sites in the area. In this map, the periphery of Mindanao where the regional centers are located has more cell sites while the rural areas have less so. Given farmers live in these rural areas, being out of the general coverage area limits their ability to gather information.

Figure 4 - Open Signal Map Figure 5 - BASS map

Source: Open Signal, Project BASS

variable is the 2010 proportion of barangays in a municipality with access to a national highway. This negative relationship is consistent (and significant at 10 percent) at the regional level, except in BARMM, which has the reverse sign but is insignificant.

2117

2326

45

0

10

20

30

40

50

Philippines Luzon Visayas Mindanao ARMM

Per

cen

t

19

As transportation and communications infrastructure issues are tackled in different World Bank Reports, this study will focus solely on other logistical concerns that lead to inefficient outcomes. Logistics refers to the services, technology, infrastructure and information systems that allow commodities to move from the original point of production to the final point of consumption. Logistics concerns all activities in the supply chain to match product supply from the producer to the market demand for those products. It aims at getting the right commodity in the right place, at the right time, with the right specifications (including quality requirements), and at the lowest cost. Logistics inefficiencies can manifest in the form of poor coordination, limited information, limited consolidation centers, security issues, trucking bans, absence of laboratory testing facilities, and complex permitting procedures for compliance with business registration, biosecurity and food safety requirements.11 Large agri-business firms can internalize many of these costs and can operate with a higher degree of vertical integration, giving them a comparative advantage over unorganized, SME-based supply chain suppliers. For smaller firms, difficulties in compliance with regulations to formalize prevent even simple transactions, such as producers wanting to sell directly to hotels or supermarkets as they require formal contracts and official receipts.

More specific logistic concerns pertaining to physical infrastructure will be tackled separately in the

Mindanao Roads Connectivity report produced by the Transport Global Practice of the World Bank, as

such, this paper will limit its discussion towards soft logistic issues. Logistics issues often concern

infrastructure which can be subdivided into “Hard Infrastructure” and “Soft Infrastructure.” Hard

Infrastructure refers to the physical networks necessary (i.e. roads and bridges) to ensure movements of

goods from their origin to their destination. This report looks at the softer logistics infrastructure affecting

private sector development. For the purposes of this report, soft infrastructure refers to the non-physical

requirements for distribution such as technology, regulations, competition, and so on. This paper shows

that while farm-to-market roads are important, the information that farmers receive, the trust among

stakeholders, the regulations and market competition that govern the supply chain, are all equally

important to ensure the most efficient delivery of products.

This study reflects on the logistics performance of Mindanao across four interrelated lenses: rural-to-

urban logistics, urban-to-urban logistics, government regulation and private-sector competition. These

four topics allow us to subdivide the analysis of logistics by focusing on the logistics requirements of

archetypal agricultural and industrial products produced on the island, the regulations imposed by the

government on the firm that produces these products, and the government interventions that affect the

behavior of third-party firms that supply the logistics inputs. Such a holistic approach allows us a better

snapshot of the main logistics issues faced by firms and helps highlight the priority reform areas that

would allow for the flourishing of the logistics sector on Mindanao. More details on some of the

methodology used in this report can be found in the Appendix.

11 Issues raised during consultation workshops held in Davao, November 2017

20

Chapter 1.

Rural Logistics and Agricultural Development

In rural Mindanao, inefficient rural-to-urban logistics contribute to the low performance of most agricultural supply chains and the persistence of high rates of poverty.12 For producers of fruits, meats and other agricultural commodities, logistics efficiency is critical to guarantee freshness, quality and safety when the product reaches the final market. Particularly for export agri-business products, costs remain the main driver for competition for these widely-traded commodities, and therefore, the value chain needs to be cost-efficient at all stages.13 Efficient logistics is the first factor of competitiveness in agriculture and a primary constraint particularly for smallholders.

Especially given the growing urban population on the island, food security and economic livelihoods are becoming increasingly dependent on agricultural supply chains that can overcome many logistic inefficiencies, particularly those found at the farm level. With greater urbanization and increasing consumption on the island, the ability of the rural hinterlands to produce and deliver fresh fruits, meats and vegetables for households, restaurants, or food processors to the main towns and cities is integral to Mindanao’s economic development. This chapter seeks to understand these issues in greater detail by (1) identifying rural-urban logistics inefficiencies, from farm gate to the retail point in Mindanao; (2) performing a network analysis of a key value chain; and (3) providing examples of mechanisms to facilitate more efficient rural-urban logistics. For the sake of expediency, the logistics chain analyses in this paper focuses on only two archetypal value chains: vegetables for the domestic market and cacao for the export market, in order to demonstrate the logistics issues that are prevalent, albeit in different degrees, to other agricultural production chains, such as fruit, livestock and grains. The former serves as a good example of a value chain with a large end domestic market, while the latter serves as a good example of a value chain that has strong linkages with the international supply chain. Vegetables were chosen primarily because this smallholder crop has a relatively short logistics chain of producers, consolidators, and primary consumers since vegetables are consumed locally as a food source in Mindanao, with only a small percentage used for food processing. Yet, the product has many logistics concerns given its significant handling needs to maintain freshness and limit wastage. The largest trading center in the country, the Benguet Trading complex, estimates that 330 MT per day volume of waste is generated in its facilities alone during peak operation (Development Academy of the Philippines 2011). Over the last fifteen years, vegetable supply registered an average annual growth rate of 3 percent resulting to a total of volume of 5.26 million metric tons, even though the land area planted for vegetables experienced only an average growth rate of 0.2 percent, which is not sufficient to feed the growing local population. As such, vegetable consumption is trending down in the country (Philippine Statistics Authority 2018), especially with the consumption of root crops and leguminous vegetables taking a significant fall from 2000 to 2012 (See Table 5). Consumption of vegetables is even less apparent when compared to neighboring countries where the Philippines falls last among its neighbors in Southeast Asia

12 World Bank. “Rural Connectivity and Smallholder Agricultural Supply Chains in Remote Areas of Southeast Asia: Case Studies from Vietnam and the Philippines”. WBG: 2014 13 World Bank. “The Philippines: Study on Agribusiness, Infrastructure, and Logistics for Growth in Mindanao, Policy Note”. WBG, 2010

21

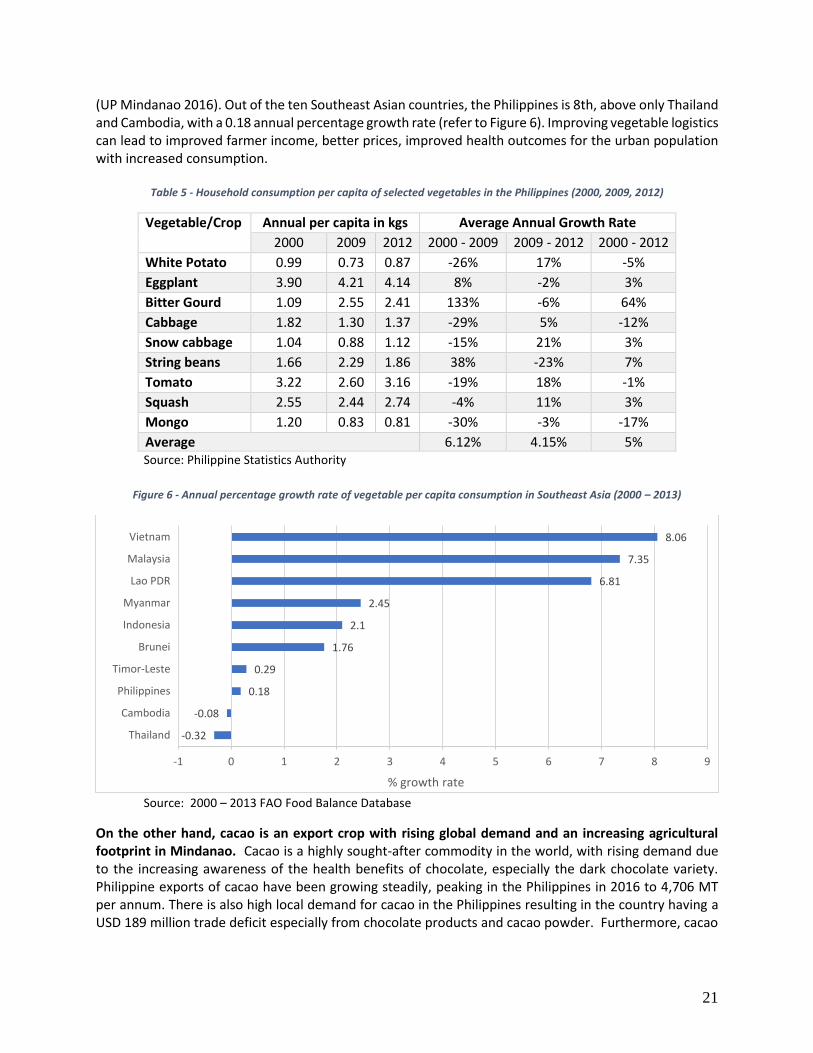

(UP Mindanao 2016). Out of the ten Southeast Asian countries, the Philippines is 8th, above only Thailand and Cambodia, with a 0.18 annual percentage growth rate (refer to Figure 6). Improving vegetable logistics can lead to improved farmer income, better prices, improved health outcomes for the urban population with increased consumption.

Table 5 - Household consumption per capita of selected vegetables in the Philippines (2000, 2009, 2012)

Vegetable/Crop Annual per capita in kgs Average Annual Growth Rate

2000 2009 2012 2000 - 2009 2009 - 2012 2000 - 2012

White Potato 0.99 0.73 0.87 -26% 17% -5%

Eggplant 3.90 4.21 4.14 8% -2% 3%

Bitter Gourd 1.09 2.55 2.41 133% -6% 64%

Cabbage 1.82 1.30 1.37 -29% 5% -12%

Snow cabbage 1.04 0.88 1.12 -15% 21% 3%

String beans 1.66 2.29 1.86 38% -23% 7%

Tomato 3.22 2.60 3.16 -19% 18% -1%

Squash 2.55 2.44 2.74 -4% 11% 3%

Mongo 1.20 0.83 0.81 -30% -3% -17%

Average 6.12% 4.15% 5% Source: Philippine Statistics Authority

Figure 6 - Annual percentage growth rate of vegetable per capita consumption in Southeast Asia (2000 – 2013)

Source: 2000 – 2013 FAO Food Balance Database

On the other hand, cacao is an export crop with rising global demand and an increasing agricultural footprint in Mindanao. Cacao is a highly sought-after commodity in the world, with rising demand due to the increasing awareness of the health benefits of chocolate, especially the dark chocolate variety. Philippine exports of cacao have been growing steadily, peaking in the Philippines in 2016 to 4,706 MT per annum. There is also high local demand for cacao in the Philippines resulting in the country having a USD 189 million trade deficit especially from chocolate products and cacao powder. Furthermore, cacao

-0.32

-0.08

0.18

0.29

1.76

2.1

2.45

6.81

7.35

8.06

-1 0 1 2 3 4 5 6 7 8 9

Thailand

Cambodia

Philippines

Timor-Leste

Brunei

Indonesia

Myanmar

Lao PDR

Malaysia

Vietnam

% growth rate

22

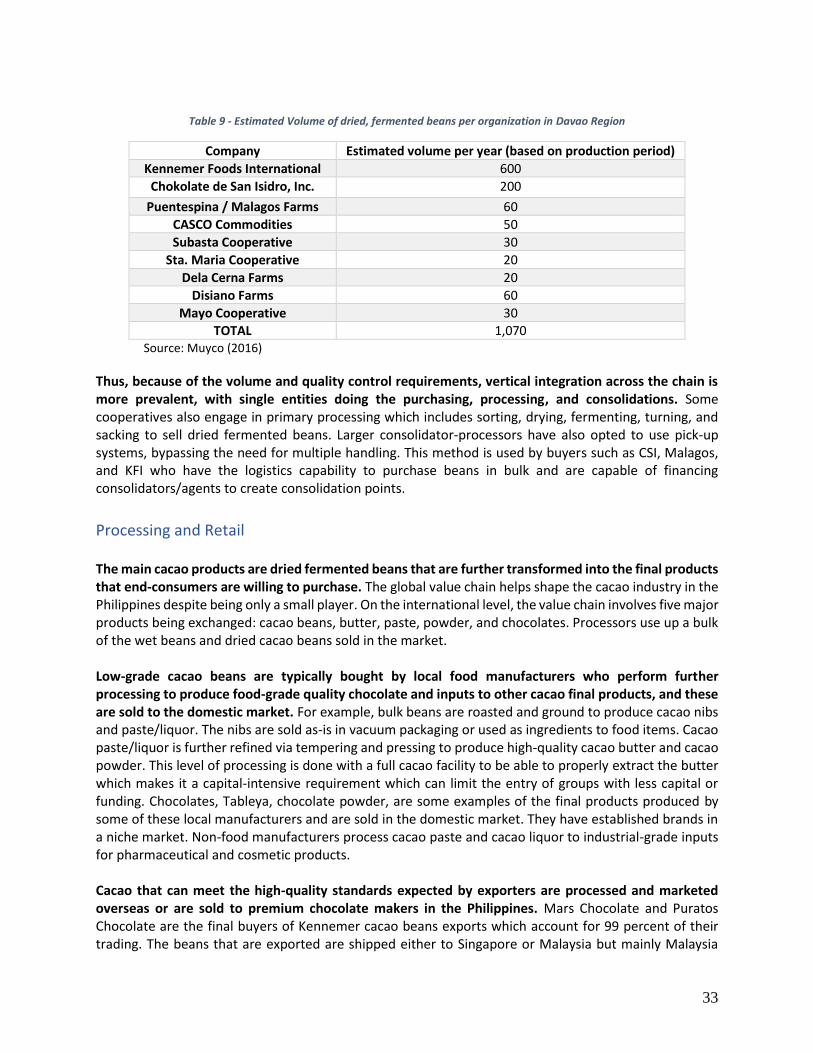

requires a more complex supply chain, which includes processors, grinders, and chocolate manufacturers, allowing us to also assess product quality and transformation issues.

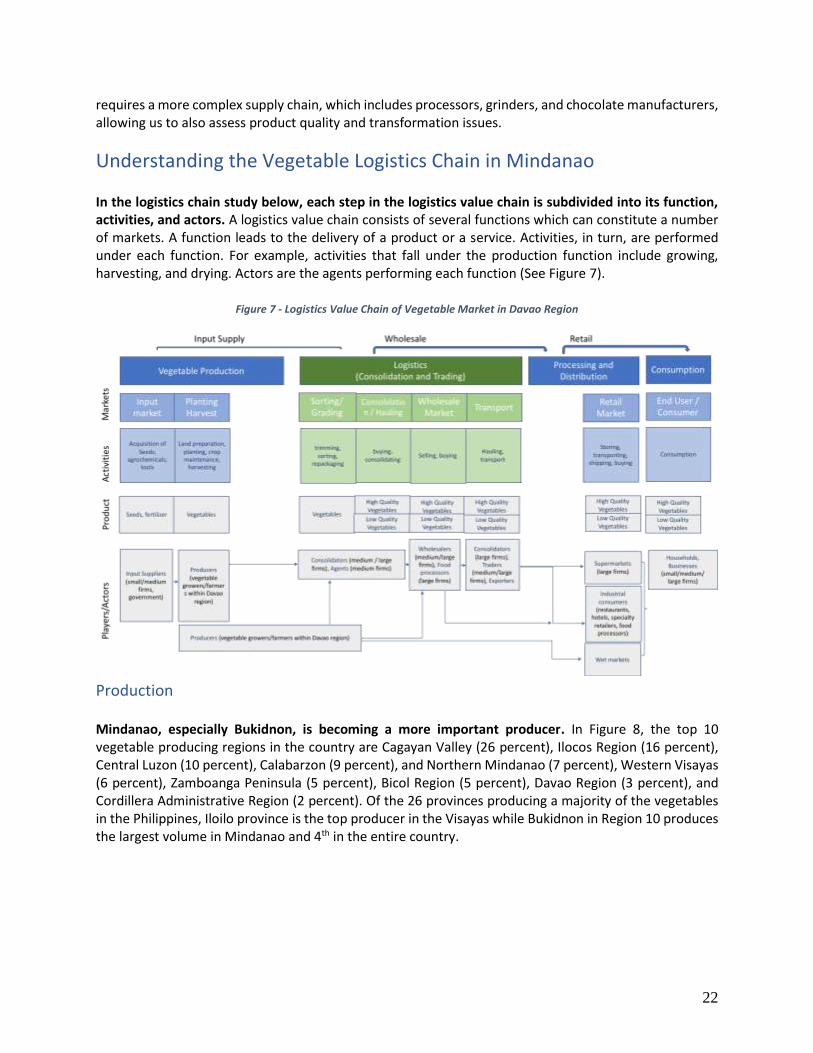

Understanding the Vegetable Logistics Chain in Mindanao In the logistics chain study below, each step in the logistics value chain is subdivided into its function, activities, and actors. A logistics value chain consists of several functions which can constitute a number of markets. A function leads to the delivery of a product or a service. Activities, in turn, are performed under each function. For example, activities that fall under the production function include growing, harvesting, and drying. Actors are the agents performing each function (See Figure 7).

Figure 7 - Logistics Value Chain of Vegetable Market in Davao Region

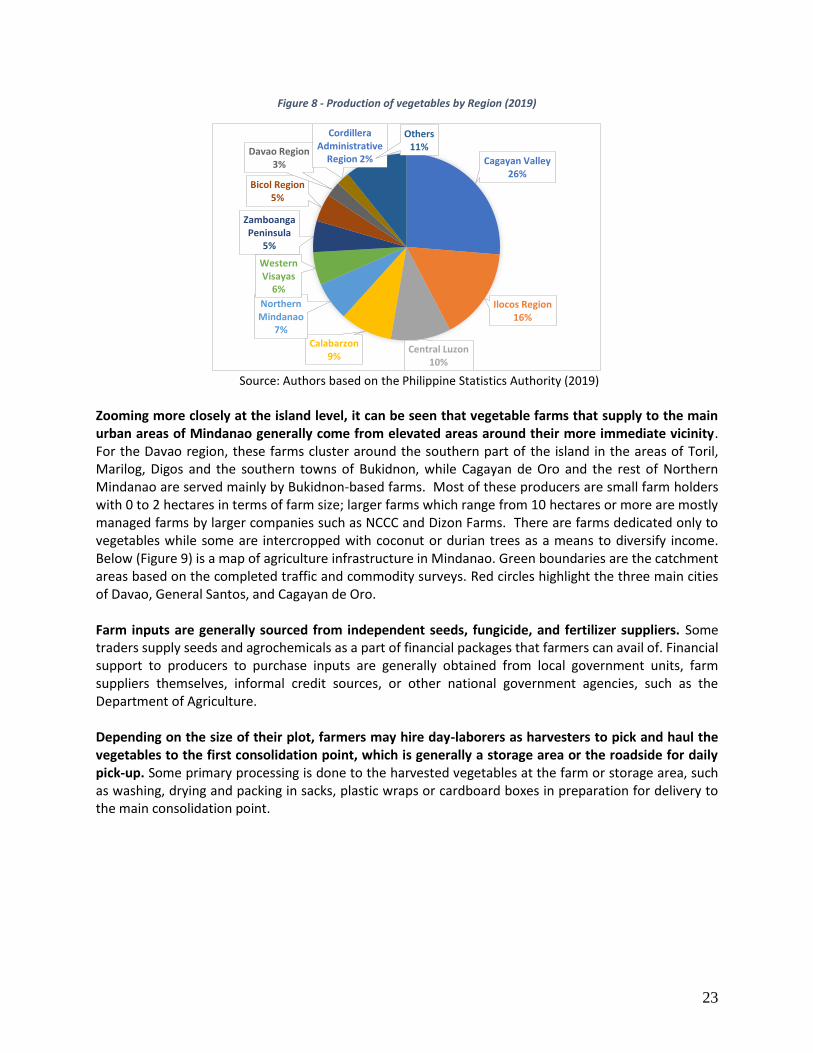

Production Mindanao, especially Bukidnon, is becoming a more important producer. In Figure 8, the top 10 vegetable producing regions in the country are Cagayan Valley (26 percent), Ilocos Region (16 percent), Central Luzon (10 percent), Calabarzon (9 percent), and Northern Mindanao (7 percent), Western Visayas (6 percent), Zamboanga Peninsula (5 percent), Bicol Region (5 percent), Davao Region (3 percent), and Cordillera Administrative Region (2 percent). Of the 26 provinces producing a majority of the vegetables in the Philippines, Iloilo province is the top producer in the Visayas while Bukidnon in Region 10 produces the largest volume in Mindanao and 4th in the entire country.

23

Figure 8 - Production of vegetables by Region (2019)

Source: Authors based on the Philippine Statistics Authority (2019)

Zooming more closely at the island level, it can be seen that vegetable farms that supply to the main urban areas of Mindanao generally come from elevated areas around their more immediate vicinity. For the Davao region, these farms cluster around the southern part of the island in the areas of Toril, Marilog, Digos and the southern towns of Bukidnon, while Cagayan de Oro and the rest of Northern Mindanao are served mainly by Bukidnon-based farms. Most of these producers are small farm holders with 0 to 2 hectares in terms of farm size; larger farms which range from 10 hectares or more are mostly managed farms by larger companies such as NCCC and Dizon Farms. There are farms dedicated only to vegetables while some are intercropped with coconut or durian trees as a means to diversify income. Below (Figure 9) is a map of agriculture infrastructure in Mindanao. Green boundaries are the catchment areas based on the completed traffic and commodity surveys. Red circles highlight the three main cities of Davao, General Santos, and Cagayan de Oro. Farm inputs are generally sourced from independent seeds, fungicide, and fertilizer suppliers. Some traders supply seeds and agrochemicals as a part of financial packages that farmers can avail of. Financial support to producers to purchase inputs are generally obtained from local government units, farm suppliers themselves, informal credit sources, or other national government agencies, such as the Department of Agriculture. Depending on the size of their plot, farmers may hire day-laborers as harvesters to pick and haul the vegetables to the first consolidation point, which is generally a storage area or the roadside for daily pick-up. Some primary processing is done to the harvested vegetables at the farm or storage area, such as washing, drying and packing in sacks, plastic wraps or cardboard boxes in preparation for delivery to the main consolidation point.

Cagayan Valley26%

Ilocos Region16%

Central Luzon10%

Calabarzon9%

Northern Mindanao

7%

Western Visayas

6%

Zamboanga Peninsula

5%

Bicol Region5%

Davao Region3%

Cordillera Administrative

Region 2%

Others11%

24

Figure 9 - Mindanao Agriculture Infrastructure

As the sorting and grading of vegetables are relatively simple, given relatively simple size, texture and shape requirements by high-end customers like modern supermarkets, food processors and restaurant chains, the initial sorting is done at the farm level. Farmers can sort the vegetables by quality at the premises and achieve higher compensation for the product that is targeted for more sophisticated buyers.

Consolidation While there are different consolidation practices done by value chain actors participating in the vegetable industry, as the practices differ based on their market, location, farm terrain, labor presence, and the available infrastructure and facilities in their area, the processes described in this section provides a general description of the main consolidation mechanism through the main vegetable trading hubs. Before shipment to the main trading hub, the vegetables are sorted and packaged by the individual or a small group of farmers for delivery, and the farmers hire a jeepney or truck to transport the vegetables to the nearest rural trading point, usually the most central village in the rural hinterlands. Farmers pay for the transport fare of the vegetables they want to be delivered. These are then further consolidated and brought to one of the two main trading hubs in Mindanao.

25

Bankerohan in Davao City and Bulua in Cagayan de Oro are the primary vegetable trading hubs of Mindanao that operate in a similar fashion as many trading hubs in the country. The vegetables produced in the Davao Region are shipped usually to the Bankerohan Public Market within the city itself which acts as the main vegetable trading hub in Southern Mindanao; while vegetables produced in Bukidnon and other vegetable producing areas end up in the Bulua Public Market in Cagayan de Oro City for distribution. Some individual farmers selling to Bankerohan or Bulua can directly deliver to their preferred traders after each harvest. The trading hub consists of a concrete floor and a roof, with trading operations consisting mainly of the rental of stalls to different traders or farmers groups. The hub is usually owned by the government, sometimes by the local government or by the Department of Agriculture. For example, part of the Bankerohan vegetable wholesale market is being managed by the Davao City government and part-owned

and managed by the Marfori Family14. Traders generally rent infrastructure and maintain basic stalls at the trading hubs to solicit produce from their farmer-suppliers and sell goods to their customers. These buyers are usually larger consolidators or direct-to-customer firms with large volumes, such as restaurants, supermarkets, hotels or food processors. The Bankerohan and Bulua trading hubs currently do not offer cold storage facilities. The entire operation is managed mainly by the traders and the hubs do not provide additional published information to farmers such as price monitoring, quality requirements, scheduling, or transportation. Trading is done in an unorganized manner where buyers transact directly with their particular seller and agreeing on the price and quality is done on a relatively opaque basis. In essence, the only service of the consolidation center is to provide a site for different farmers, traders, and buyers to meet and transact at the hub on an individual basis. Even if the vegetables have been pre-sorted, weighed, and graded at the farm, a secondary quality control process that involves the re-sorting, packing, grading, and weighing on site is completed to ensure the fairness of the transaction among parties. Frequent disputes among the farmer, trader, and even the transport provider, require that this process is duly witnessed by all transaction parties to ensure the validity of the transaction. Traders complain of being sold produce with only the top layer being of top quality while farmers complain of being short-changed by the trader. Apart from the wasted time, the peeling and discarding of misshapen or damaged portions of the vegetables due to the re-sorting process adds to the logistics inefficiencies at this stage. Trading hubs that provide cold storage facilities find these areas hardly being used by the vegetable industry. In most cases, vegetables are sold within the day, with minimal need for storage at the trading hub. As the costs of using refrigerated trucks are generally 40 percent higher than unrefrigerated trucks, vegetable traders generally prefer to maintain the vegetables at the ambient temperature and only put them in cold storage once they reach the final buyers’ destination such as the main commissary or the main supermarket. Very limited storage is done at the trading hub and produce that is unsold will need to be disposed of or transported back by the farmer.

14 It is important to note that while they manage the trading hub, the city government cannot provide proof that the area they are managing was donated. It is not under a usufruct contract according to the City Economic Enterprise Officer. Although it has been known that the property has been donated by the Marforis long prior and they are waiting for the documents. The issue of ownership in fact brought up in June 2019 as the city government cannot push through with its plan of rehabilitation, given the Commission on Audit (COA) may ask for proof of ownership which the city cannot provide yet.

26

For farming communities that are further from the city, smaller rural trading posts serve as the first collection posts. There is a main trading post operating as the central collection point for agricultural products, including vegetables, from the highland farms in the area, usually managed privately by a local trading association or a large trader. Similar to the main city trading posts, these smaller, privately owned trading posts conduct another initial sorting and quality check at this node. Generally, these private trading posts mostly cater to small individual farmers in the hinterlands who are too small to afford a transport vehicle to get their products from their farms down to the main trading post (Key Informant Interviews, 2018). Buyers at the trading posts consist mainly of consolidators who play a role in the supply of vegetables to major buyers in the city, such as restaurants, malls or supermarkets. From the trading hub, the volume is consolidated inside their cold storage warehouse before it is delivered to the final consumer. The role of the consolidator is to buy from numerous trading hubs to ensure that the vegetable supply of their end-customer is fulfilled with the right amount, time, and quality. These consolidators are also in charge of transporting the goods from Mindanao to anywhere in the Philippines, including Manila and Cebu, if prices and quantities so dictate. Competition among consolidators is high as their services are substitutable. In Bankerohan alone, more than 50 small-scale wholesalers are operating and there are constant negotiations for supply agreements and business relationships with traders to ease the threat of their customers from going to other consolidators for the supply they need.

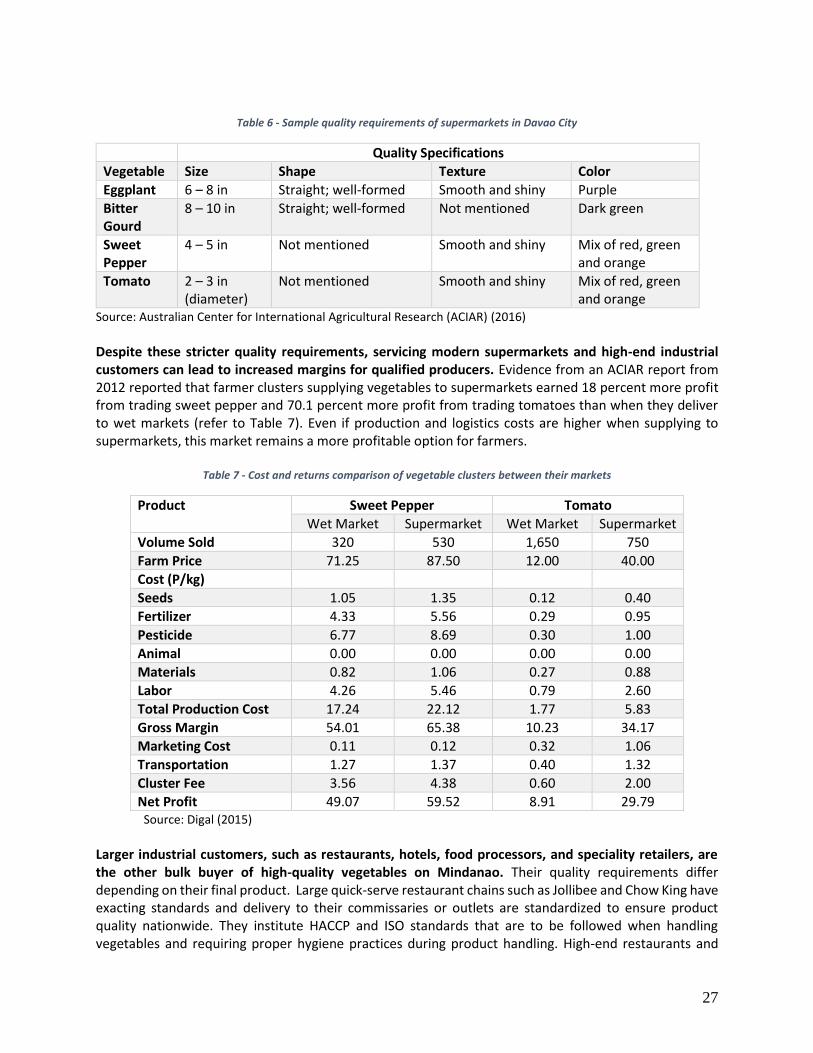

Retailers The consolidators generally sell vegetables in bulk to three types of outlets: wet markets, supermarkets, and industrial customers, with lower quality vegetables destined for wet markets. The wet market continues to be the main market for farmers and producer organizations, which are generally small stalls attached close to trading hubs. Quality requirements for this type of retail outlet are low as they serve a more price-sensitive consumer that shops on a daily basis. Stalls near the Bangkerohan market would only require that the vegetables provided are delivered in sacks or cardboard boxes to be packed in large volumes. Most of their customers have no requirements in terms of size, shape, or color. Supermarkets require higher quality vegetables and their proliferation has risen with the expansion of modern retailing in Mindanao, where more and more people buy directly from groceries and supermarkets such as national chains like SM, Gaisano, or local chains like NCCC. These buyers tend to have stricter requirements for quality control and freshness, and impose penalties for providers that run out of stock. They generally have some cold storage space to allow them to maintain vegetable quality for longer than the wet market. Consolidators serving these customers need to consider numerous physical characteristics, degree of ripeness, and that the vegetable must have no damage. These retailers have merchandisers waiting at the malls’ receiving area to check the vegetables for quality based on the identified physical characteristics of specific vegetables, visible damage, ripeness, among others. For example, for vegetables such as eggplants, supermarkets accept only a specific variety because the grown plant produces vegetables that follow their preferred dimensions. Table 6 shows a sample set of specifications certain supermarkets have in Davao City.

27

Table 6 - Sample quality requirements of supermarkets in Davao City

Quality Specifications

Vegetable Size Shape Texture Color

Eggplant 6 – 8 in Straight; well-formed Smooth and shiny Purple

Bitter Gourd

8 – 10 in Straight; well-formed Not mentioned Dark green

Sweet Pepper

4 – 5 in Not mentioned Smooth and shiny Mix of red, green and orange

Tomato 2 – 3 in (diameter)

Not mentioned Smooth and shiny Mix of red, green and orange

Source: Australian Center for International Agricultural Research (ACIAR) (2016) Despite these stricter quality requirements, servicing modern supermarkets and high-end industrial customers can lead to increased margins for qualified producers. Evidence from an ACIAR report from 2012 reported that farmer clusters supplying vegetables to supermarkets earned 18 percent more profit from trading sweet pepper and 70.1 percent more profit from trading tomatoes than when they deliver to wet markets (refer to Table 7). Even if production and logistics costs are higher when supplying to supermarkets, this market remains a more profitable option for farmers.

Table 7 - Cost and returns comparison of vegetable clusters between their markets

Product Sweet Pepper Tomato

Wet Market Supermarket Wet Market Supermarket

Volume Sold 320 530 1,650 750

Farm Price 71.25 87.50 12.00 40.00

Cost (P/kg)

Seeds 1.05 1.35 0.12 0.40

Fertilizer 4.33 5.56 0.29 0.95

Pesticide 6.77 8.69 0.30 1.00

Animal 0.00 0.00 0.00 0.00

Materials 0.82 1.06 0.27 0.88

Labor 4.26 5.46 0.79 2.60

Total Production Cost 17.24 22.12 1.77 5.83

Gross Margin 54.01 65.38 10.23 34.17

Marketing Cost 0.11 0.12 0.32 1.06

Transportation 1.27 1.37 0.40 1.32

Cluster Fee 3.56 4.38 0.60 2.00

Net Profit 49.07 59.52 8.91 29.79 Source: Digal (2015)