Embed Size (px)

Citation preview

Improving Forest Management Practices Through the Development

of Markets for Lesser Known Species (LKS) in Bolivia

Bob SmithVictor CossioTom Hammett

Department of Wood Science and Forest Products

College of Natural Resources

Outline

General Overview

Results of the Survey of U.S. Companies

Marketing Recommendations

Conclusions

Questions?

General Overview

271 million acres (1.6 Texas)

131 million acres → tropical forests (48%), 10% of South America’s tropical forest

More than 2 million Ha. are certified FSC

Annual sustainable production capacity 8 billion BF

11 wood species = 75% volume (6 species = 45% in 2004)

72 species exported in 2004

63,000 direct employments

Source: (FAO 2006)

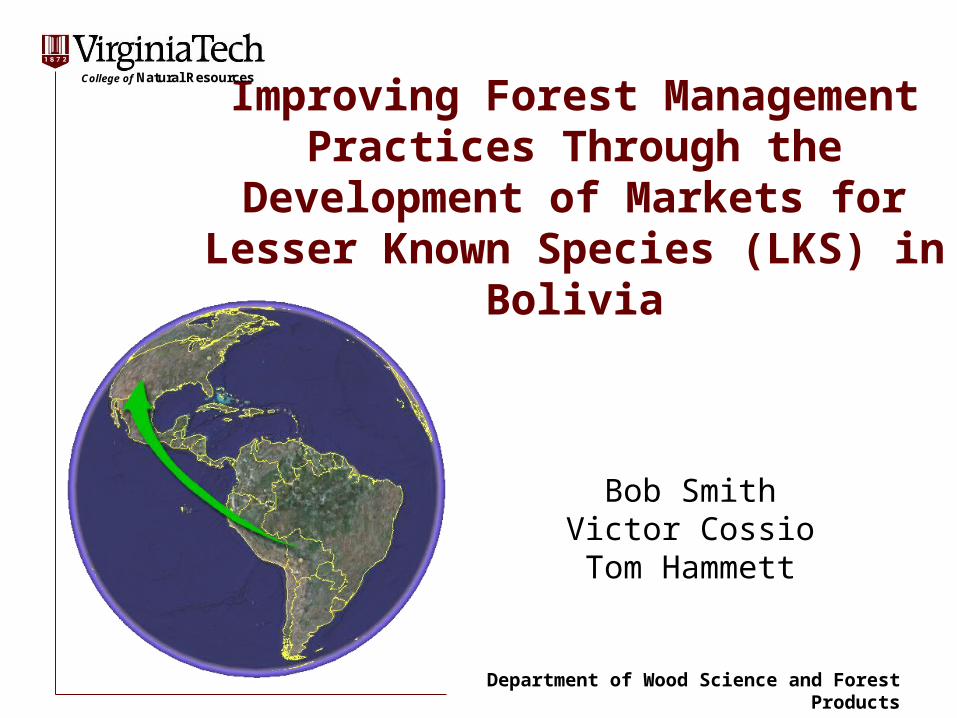

Bolivian Forest Products Sector

General Overview

Bolivian Forest Products Sector

0

20

40

60

80

100

120

140

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04Year

Expo

rts (M

illio

n $)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Perc

enta

ge o

f GD

P (%

)

% of GDP (w ood manufacturing) Certif ied forest productsPrimary processing Secondary processing

Forest products GDP 3%

Wooden products GDP decreased from 0.97% to 0.78% (1994-2004)

The process of forest certification in Bolivia started in 1994

Forestry Law, 1996

Switch between primary to secondary processing

Increase in the exporting of certified forest products

$300 million sales (domestic and exports)

Source: (CFB 2005, INE 2005)

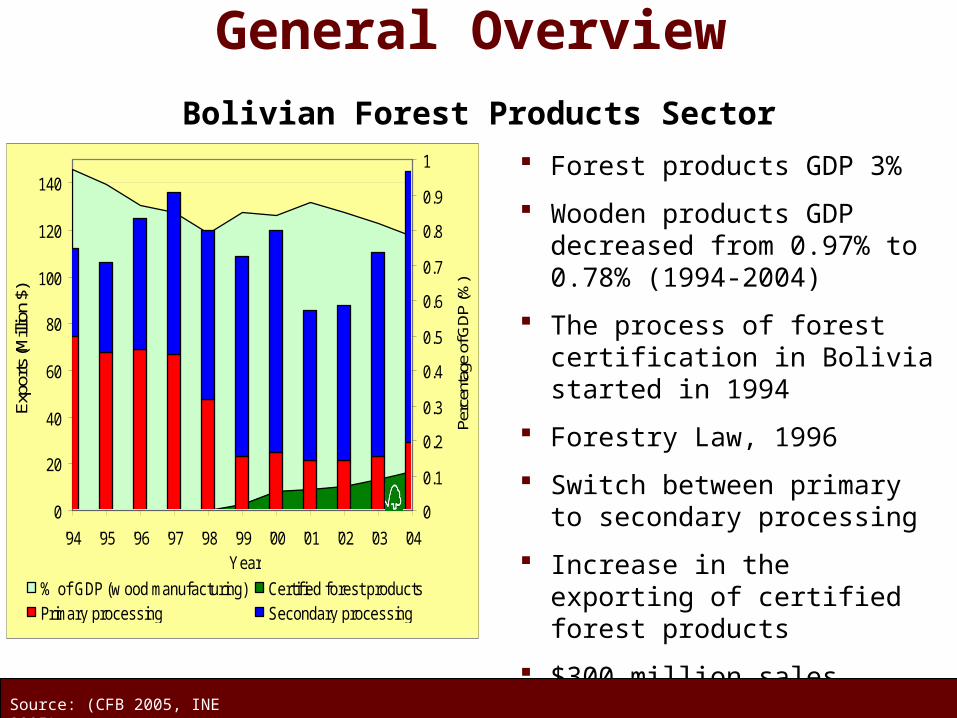

General Overview

Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Bolivian Exports by Wood Specie, 2003-04

0 2 4 6 8

mahogany (0.48)

Spanish cedar (0.5)

Amazonian oak (0.53)

yesquero (0.55)

tornillo (0.57)

morado (0.88)

almendrillo (0.97)

tajibo (0.98)

curupau (1.03)

cuchi (1.22)

Wood s

pecie

(S

pecific

Gra

vity,1

2%

MC

)

Exports (MMBF)

2004

2003

Source: (CFB 2005)

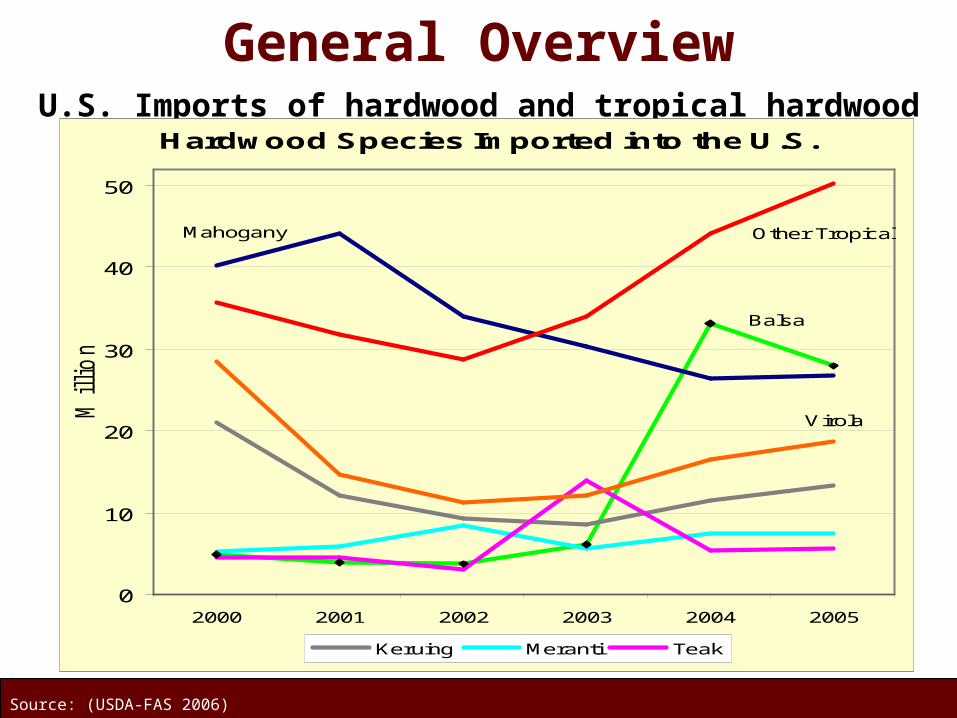

General OverviewU.S. Imports of hardwood and tropical hardwood lumber

Hardwood Species Imported into the U.S.

Balsa

Mahogany Other Tropical

Virola

0

10

20

30

40

50

2000 2001 2002 2003 2004 2005

Million B

F

Keruing Meranti Teak

Source: (USDA-FAS 2006)

General OverviewThe U.S. Hardwood Market

Relevant hardwood market segments for Bolivian wood products

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Consumption of Domestic Lumber in the U.S. by Selected Market Segments, 1995-2006

Furniture Pallet/Crating

Distribution yards

Railroads

0

1

2

3

4

5

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06*

Billi

on b

oard

feet

CabinetsDim./Millw ork/Moulding

Flooring

Miscellaneous

0.4

0.5

0.6

0.7

0.8

0.9

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06*

Source: (WHR 2006)

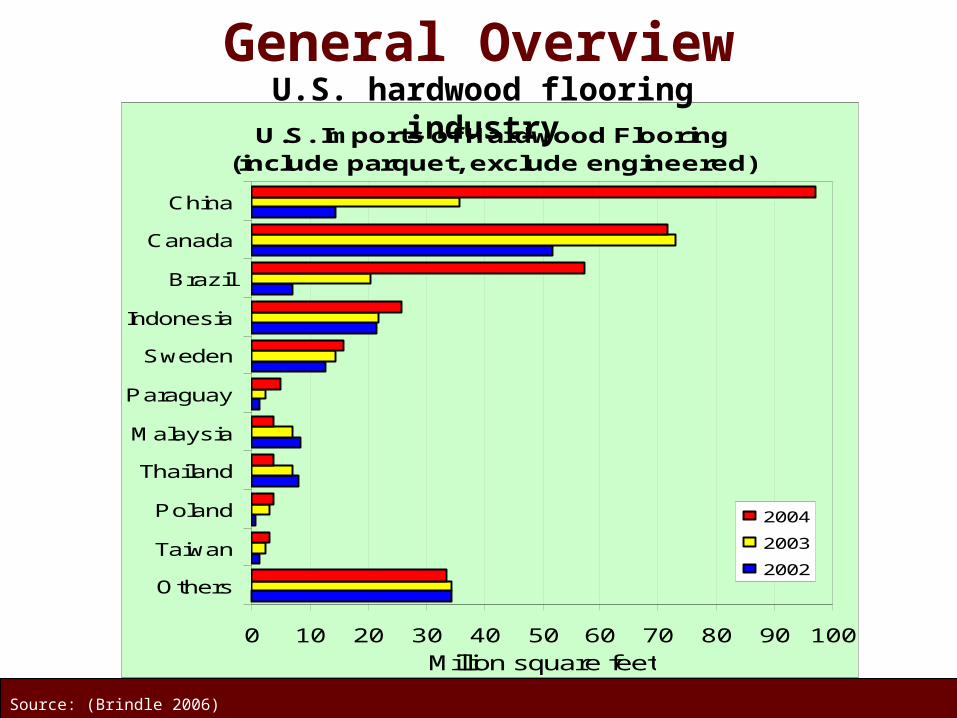

General Overview

U.S. Imports of Hardwood Flooring (include parquet, exclude engineered)

0 10 20 30 40 50 60 70 80 90 100

Others

Taiwan

Poland

Thailand

Malaysia

Paraguay

Sweden

Indonesia

Brazil

Canada

China

Million square feet

2004

2003

2002

U.S. hardwood flooring industry

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKSSource: (Brindle 2006)

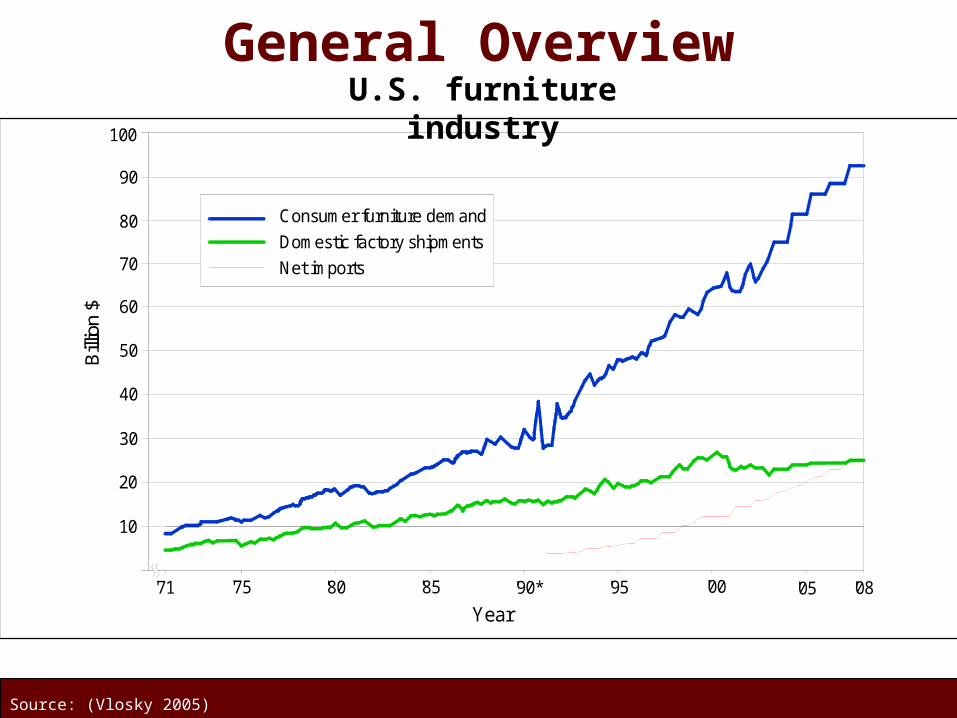

General OverviewU.S. furniture industry

'71 '75 '80 '85 '90* '95 '00 '05 '08

10

20

30

40

50

60

70

80

90

100

Year

Bill

ion

$

Net imports

Domestic factory shipments

Consumer furniture demand

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKSSource: (Vlosky 2005)

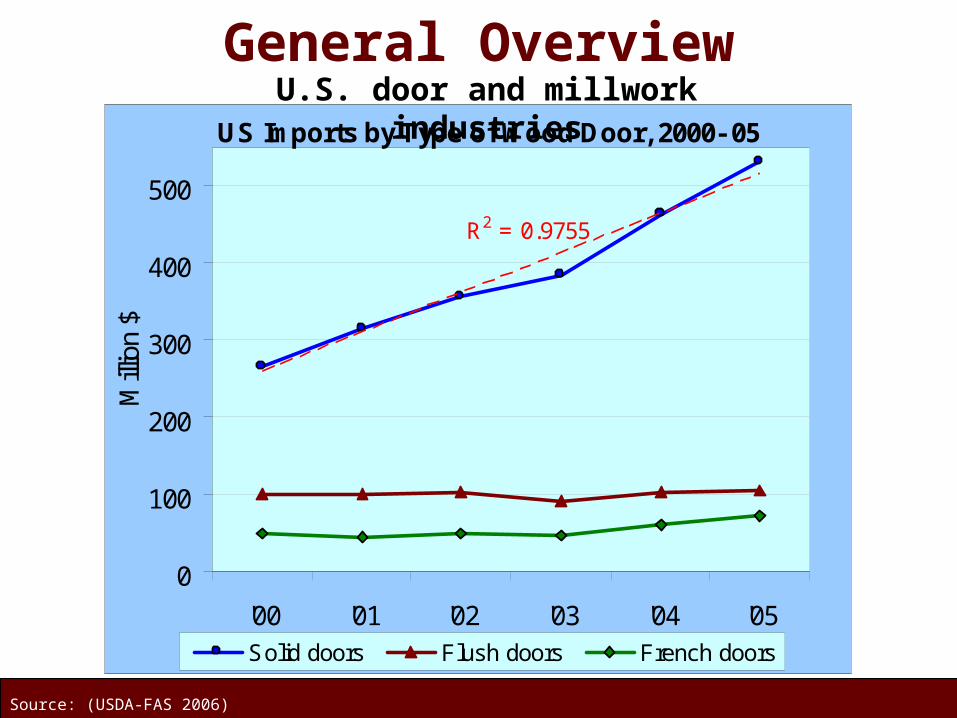

General Overview

US Imports by Type of Wood Door, 2000- 05

R2 = 0.9755

0

100

200

300

400

500

'00 '01 '02 '03 '04 '05

Mill

ion

$

Solid doors Flush doors French doors

U.S. door and millwork industries

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKSSource: (USDA-FAS 2006)

General Overview

Increase the participation of Bolivian wood products in the GDP

Improve the effectiveness of forest products management

Can’t meet the requirements of FSC certification if no market for timber that needs to be harvested to meet management plans.

Ensure the sustainability of Bolivian rainforests

Improve the well-being of Bolivian indigenous communities

U.S. final consumer (LEED, ENGOs)

Justification

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

General Overview

Assess the interest of U.S. companies to import Bolivian wood products made from LKS

Develop marketing recommendations

Objectives

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

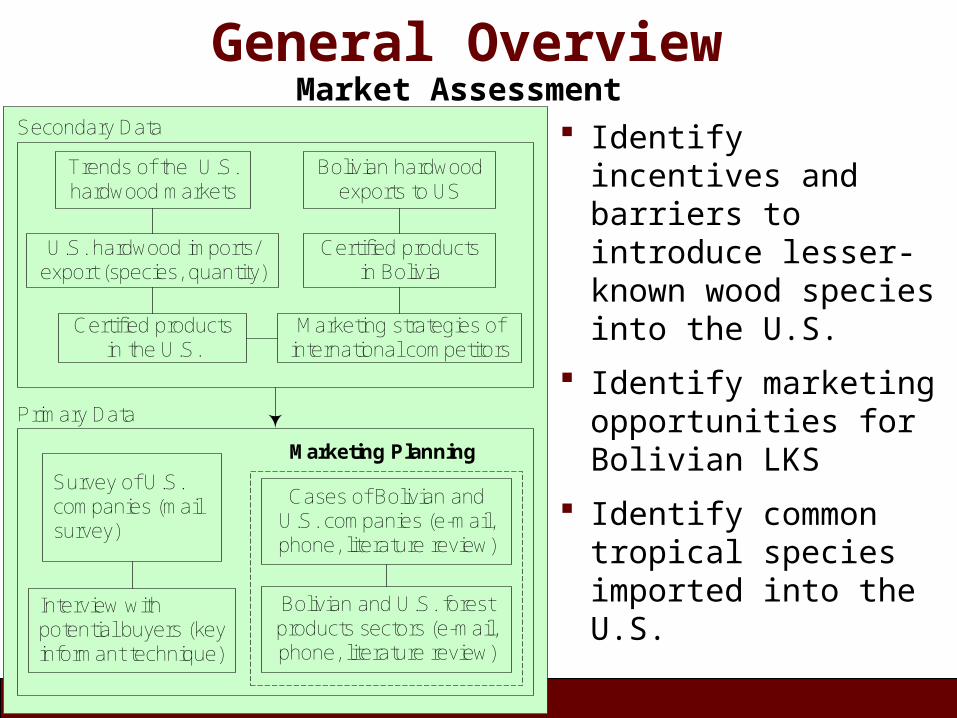

Identify incentives and barriers to introduce lesser-known wood species into the U.S.

General OverviewMarket Assessment

Identify incentives and barriers to introduce lesser-known wood species into the U.S.

Identify marketing opportunities for Bolivian LKS

Identify common tropical species imported into the U.S.

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Marketing Planning

Certified products in the U.S.

Bolivian and U.S. forest products sectors (e-mail, phone, literature review)

Secondary Data

Bolivian hardwood exports to US

U.S. hardwood imports/export (species, quantity)

Trends of the U.S. hardwood markets

Marketing strategies of international competitors

Interview with potential buyers (key informant technique)

Primary Data

Survey of U.S. companies (mail survey)

Cases of Bolivian and U.S. companies (e-mail, phone, literature review)

Certified products in Bolivia

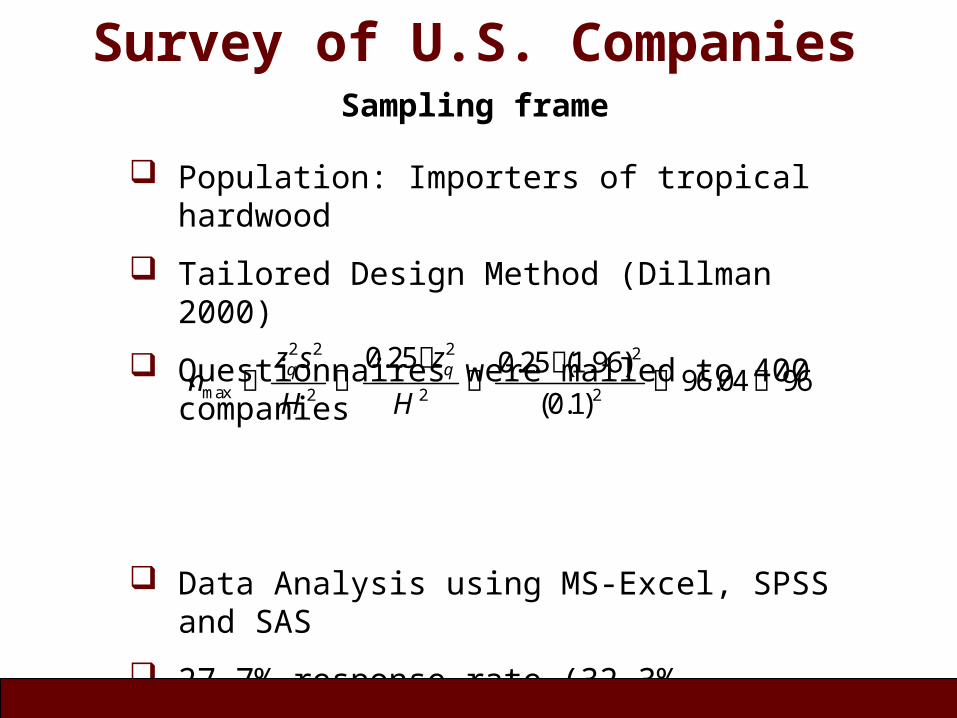

Survey of U.S. CompaniesSampling frame

Population: Importers of tropical hardwood

Tailored Design Method (Dillman 2000)

Questionnaires were mailed to 400 companies

Data Analysis using MS-Excel, SPSS and SAS

27.7% response rate (32.3% adjusted); 111 usable questionnaires.

Non-response bias is not considered a limitation

2 2 2 2

max 2 2 2

0.25 0.25 (1.96)96.04 96

(0.1)q qz s z

nH H

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

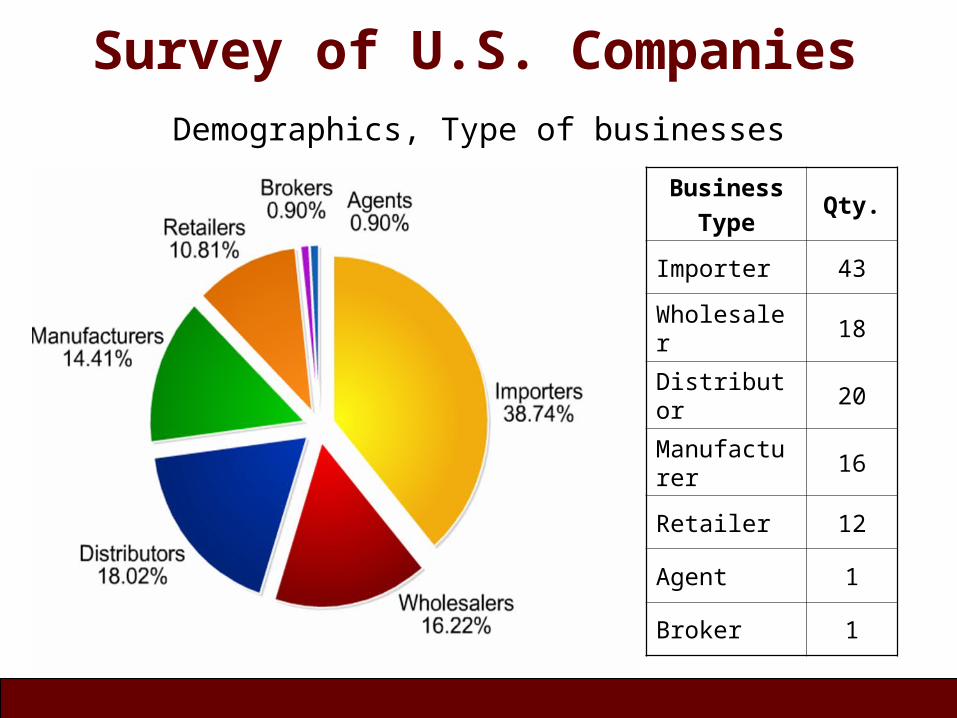

Survey of U.S. CompaniesDemographics, Type of businesses

Business

TypeQty.

Importer 43

Wholesaler 18

Distributor 20

Manufacturer 16

Retailer 12

Agent 1

Broker 1

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

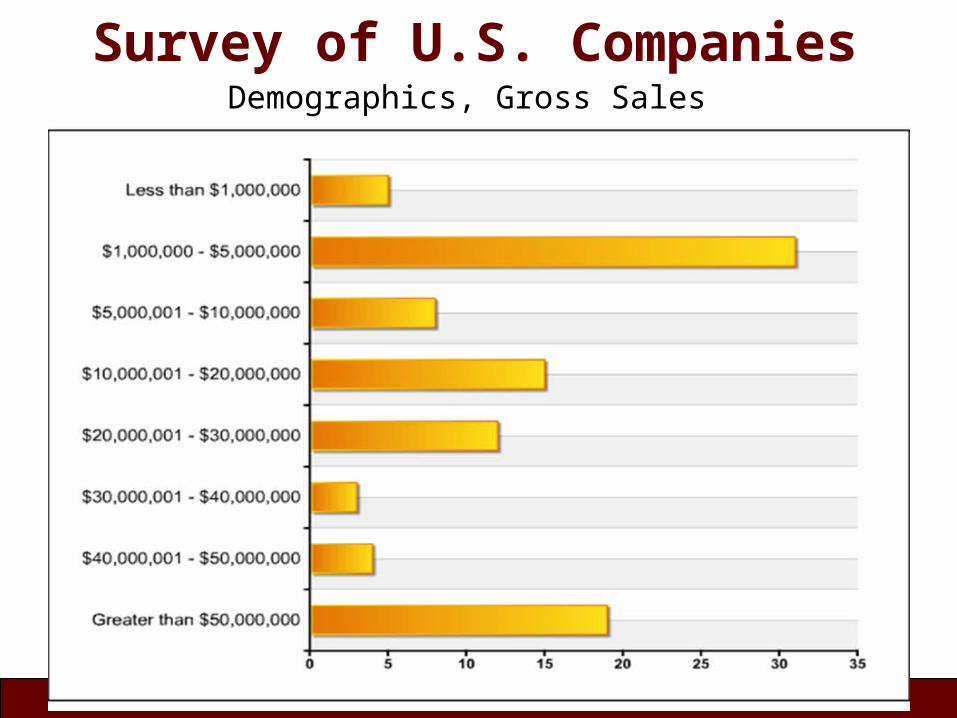

Survey of U.S. CompaniesDemographics, Gross Sales

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

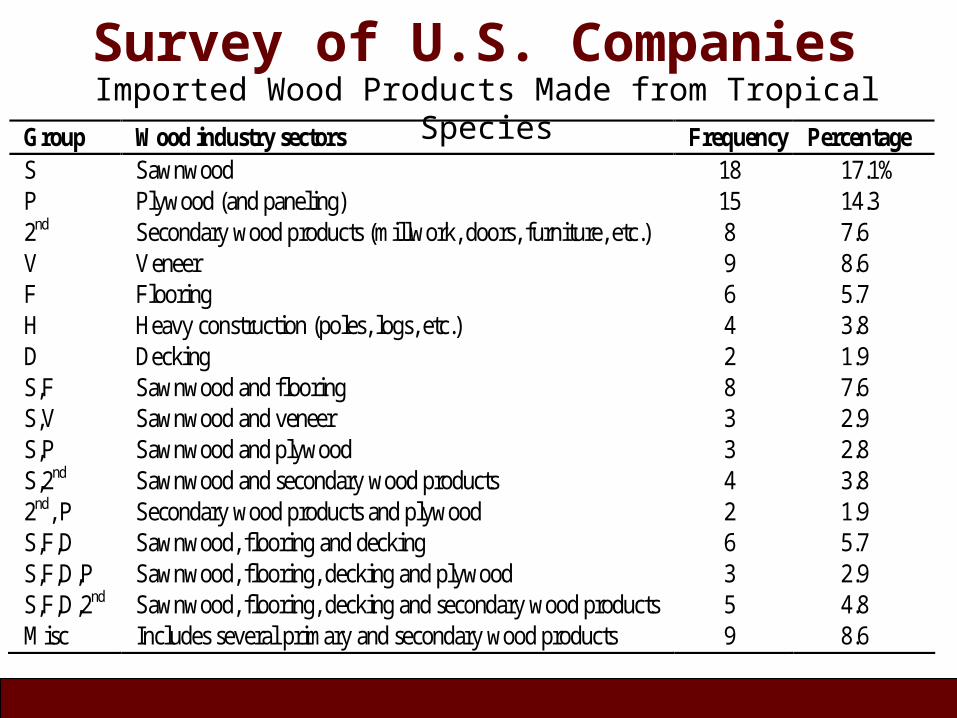

Survey of U.S. CompaniesImported Wood Products Made from Tropical Species

Group Wood industry sectors Frequency Percentage S Sawnwood 18 17.1% P Plywood (and paneling) 15 14.3 2nd Secondary wood products (millwork, doors, furniture, etc.) 8 7.6 V Veneer 9 8.6 F Flooring 6 5.7 H Heavy construction (poles, logs, etc.) 4 3.8 D Decking 2 1.9 S,F Sawnwood and flooring 8 7.6 S,V Sawnwood and veneer 3 2.9 S,P Sawnwood and plywood 3 2.8 S,2nd Sawnwood and secondary wood products 4 3.8 2nd, P Secondary wood products and plywood 2 1.9 S,F,D Sawnwood, flooring and decking 6 5.7 S,F,D,P Sawnwood, flooring, decking and plywood 3 2.9 S,F,D,2nd Sawnwood, flooring, decking and secondary wood products 5 4.8 Misc Includes several primary and secondary wood products 9 8.6

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Survey of U.S. Companies

0

5

10

15

20

25

30

35

1-5% 6-10% 11-15% 16-20% 21-25% >25%

Fre

qu

en

cy

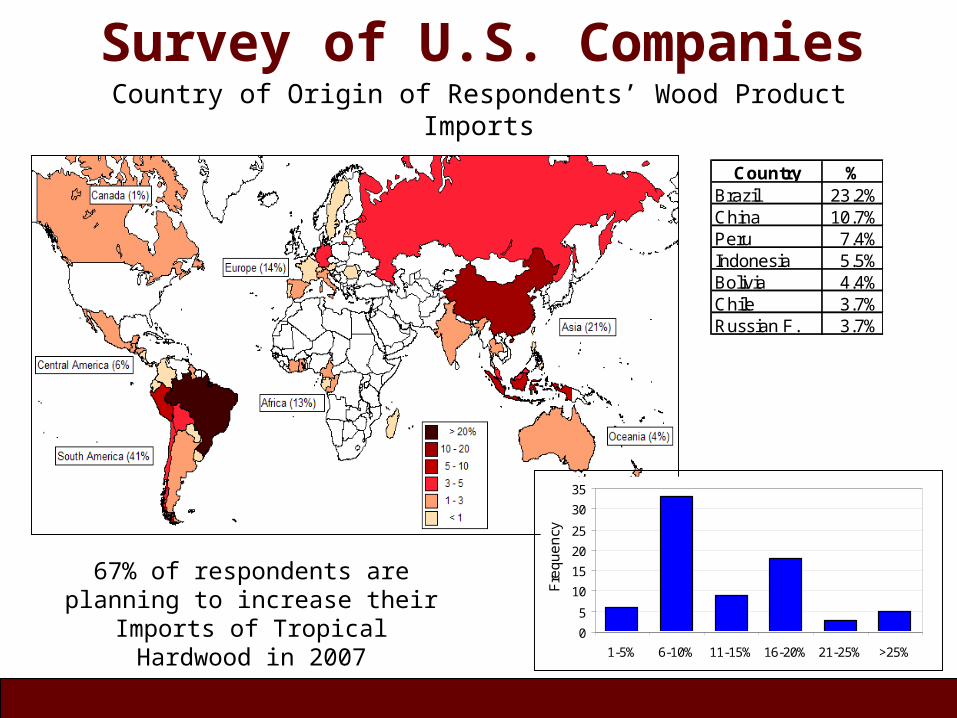

Country %Brazil 23.2%China 10.7%Peru 7.4%Indonesia 5.5%Bolivia 4.4%Chile 3.7%Russian F. 3.7%

Country of Origin of Respondents’ Wood Product Imports

67% of respondents are planning to increase their Imports of Tropical

Hardwood in 2007

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

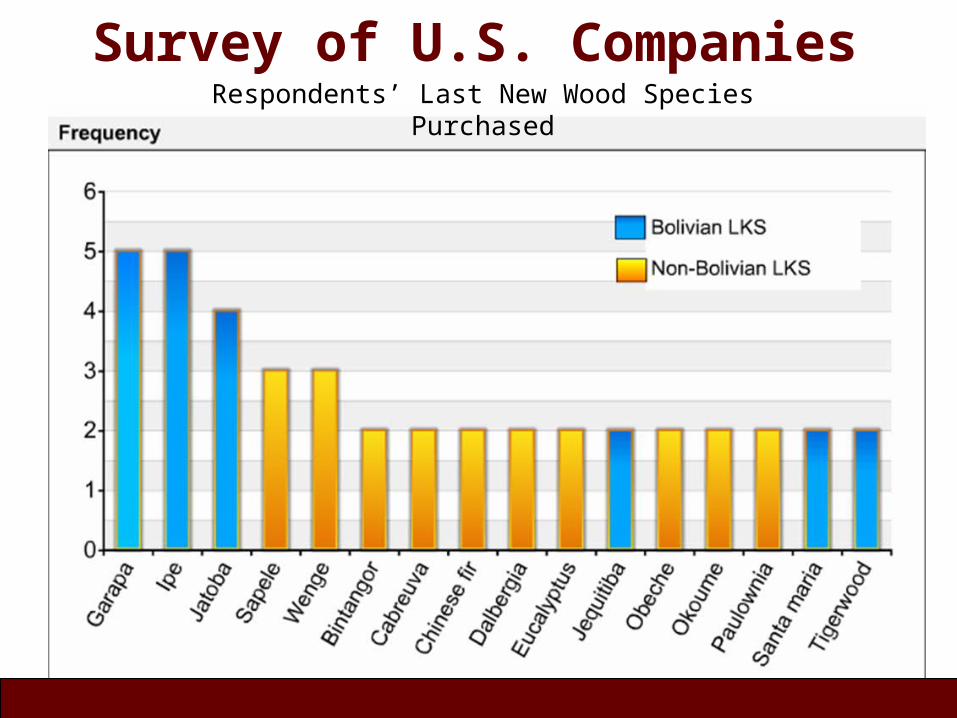

Survey of U.S. CompaniesRespondents’ Last New Wood Species Purchased

Conclusions EndSurvey of U.S Co. Bolivian LKS

Survey of U.S. Companies

%

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

1

1

1

2

2

4

4

5

8

11

13

13

15

16

24

37

38

52

54

58

65

70

0 10 20 30 40 50 60 70 80

Mara Macho (Cedrelinga catenaeformis)

Jichituriqui (Aspidosperma spp.)

Murure (Clarisia racemosa)

Momoqui (Caesalpinia spp.)

Guayabochi (Callycophyllum spruceanum)

Yesquero Blanco (Cariniana ianeirensis)

Ochoo (Hura crepitans)

Bibosi (Ficus glabrata)

Palo María (Calicophyllium braziliensis)

Cuta (Apuleia leicocarpa)

Curupaú (Anadenanthera colubrina)

Sirari (Ormosia coarctata)

Yesquero Negro (Cariniana estrellensis)

Cambará (Erisma uncinatun)

Sangre de Toro (Virola spp.)

Cumarú (Dipteryx odorata)

Meranti (Shorea spp.)

Sapele (Entandrophragma cylindricum)

Teak (Tectona grandis)

Tajibo (Tabebuia spp)

Paquio (Hymenaea courbaril)

Mahogany (Swietenia spp, khaya spp)

Non Bolivian LKSBolivian LKS

Bolivian LKS imported by respondents

Survey of U.S. CompaniesNumber of New Wood Species Tried in 2006

0

5

10

15

20

25

30

35

40

45

50

Distributor Importer Wholesaler Retailer Manufacturer

Type of business

Num

ber

of w

ood

spec

ies

impo

rted

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Survey of U.S. Companies

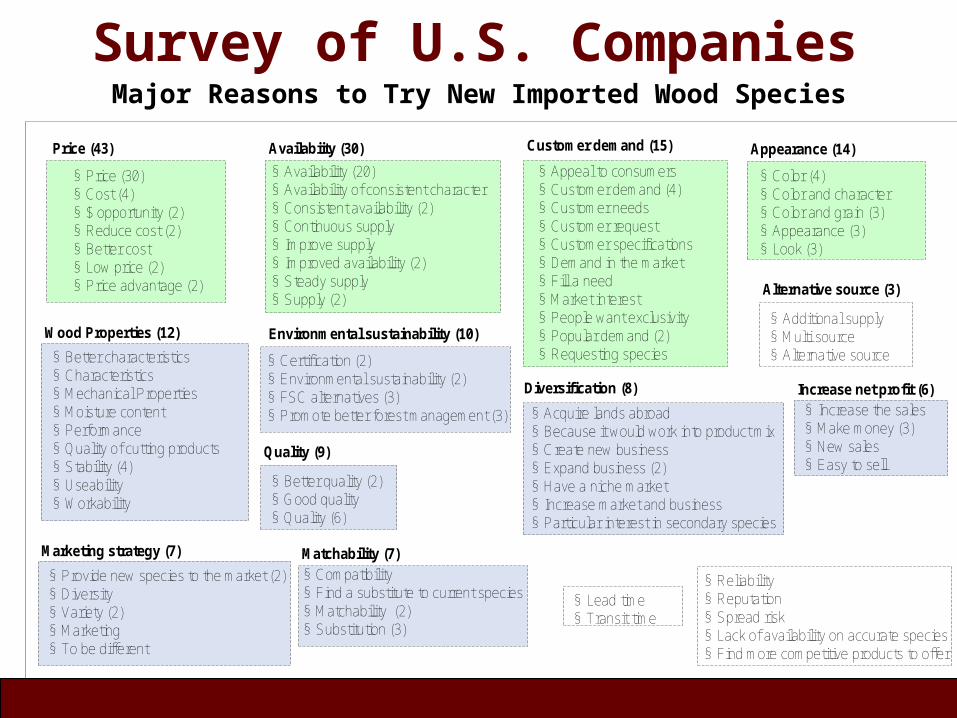

Price (43)

§ Price (30)§ Cost (4)§ $ opportunity (2)§ Reduce cost (2)§ Better cost § Low price (2) § Price advantage (2)

Availabiity (30)

§ Availability (20)§ Availability of consistent character § Consistent availability (2)§ Continuous supply § Improve supply § Improved availability (2)§ Steady supply § Supply (2)

Customer demand (15)

§ Appeal to consumers § Customer demand (4)§ Customer needs § Customer request § Customer specifications § Demand in the market § Fill a need § Market interest § People want exclusivity § Popular demand (2)§ Requesting species

Appearance (14)

§ Color (4)§ Color and character § Color and grain (3)§ Appearance (3)§ Look (3)

Wood Properties (12)

§ Better characteristics § Characteristics § Mechanical Properties § Moisture content § Performance § Quality of cutting products § Stability (4)§ Useability § Workability

Quality (9)

§ Better quality (2)§ Good quality § Quality (6)

Alternative source (3)

§ Additional supply § Multi source § Alternative source

Diversification (8)

§ Acquire lands abroad § Because it would work into product mix § Create new business § Expand business (2)§ Have a niche market § Increase market and business § Particular interest in secondary species

Environmental sustainability (10)

§ Certification (2)§ Environmental sustainability (2)§ FSC alternatives (3)§ Promote better forest management (3)

Matchability (7)§ Compatibility § Find a substitute to current species § Matchability (2)§ Substitution (3)

Increase net profit (6)§ Increase the sales § Make money (3)§ New sales § Easy to sell

§ Lead time § Transit time

Marketing strategy (7)

§ Provide new species to the market (2)§ Diversity § Variety (2)§ Marketing § To be different

§ Reliability§ Reputation§ Spread risk§ Lack of availability on accurate species§ Find more competitive products to offer

Major Reasons to Try New Imported Wood Species

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Survey of U.S. CompaniesImportant Factors to Try New Imported Wood Species (5-point Likert scale)

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

4.7

4.6

4.1

4.3

4.2

3.1

3.4

4.0

3.7

3.5

3.6

3.7

3.4

3.3

3.8

4.2

3.6

3.3

3.1

3.0 3.5 4.0 4.5 5.0

Somewhat important Very important

Easy to machine

Easy to f inish

Mechanical properties

Natural durability

Color

Strength

Texture

Density(Specif ic gravity)

Surface hardness

Stability (shrinkage/sw ell)

Straightness

Environmentally certif ied

Price

Long-run availability

Trustw orthy (supplier)

Kiln-dried

Graded under US standards

Quality

Know n supplier

Survey of U.S. CompaniesImportant Factors to Try New Wood Species

Significance

Secondary Flooring Plywood Sawnwood Veneer p-value

(n=8) (n=6) (n=15) (n=18) (n=9)Easy to machine 3.4 2.8 3.7 3.5 2.9 0.44Easy to finish 4.7 3.2 3.7 3.4 4.1 0.03*Mechanical properties 3.3 3.3 3.2 3.5 3.2 0.9Natural durability 3.7 3.8 3.4 3.4 2.4 0.36Color 4.6 3.0 4.0 3.9 4.9 < 0.01***Strength 3.3 3.7 3.3 2.9 2.7 0.2Texture 3.3 2.0 3.6 3.4 4.1 < 0.01**Density(Specific gravity) 2.7 3.0 3.3 3.0 2.6 0.23Surface hardness 3.3 4.2 3.3 2.9 2.8 < 0.01**Stability (shrinkage/swell) 4.1 4.3 4.3 4.1 4.0 0.8Straightness 4.3 3.5 4.5 4.3 4.1 0.06Environmentally certified 4.0 3.3 2.5 2.8 3.8 0.04*Price 3.6 4.2 4.7 3.9 4.3 0.07Long-run availability 4.1 3.5 4.7 3.9 4.8 0.01*Trustworthy (supplier) 4.6 4.2 4.8 4.5 4.9 0.13Kiln-dried 4.4 3.7 4.1 4.1 2.4 0.08Graded under US standards 3.5 3.0 3.7 3.7 3.2 0.55Quality 4.9 4.5 4.7 4.7 4.9 0.55Known supplier 3.0 3.3 3.5 3.6 3.9 0.58

Factor

Mean

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

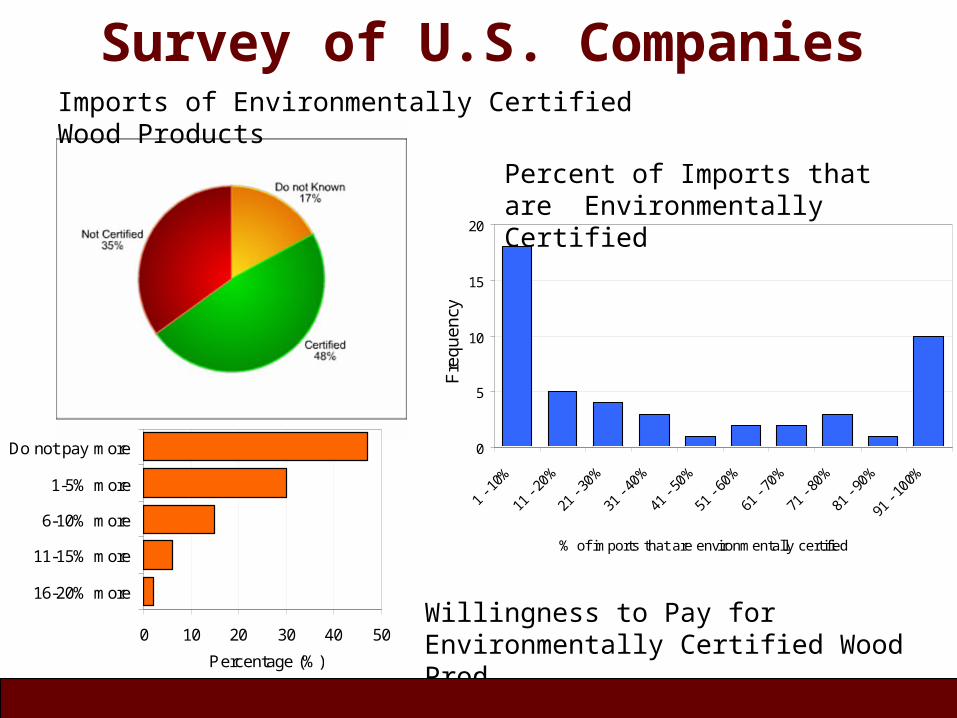

Survey of U.S. CompaniesImports of Environmentally Certified Wood Products

0

5

10

15

20

1 - 1

0%

11 -

20%

21 -

30%

31 -

40%

41 -

50%

51 -

60%

61 -

70%

71 -

80%

81 -

90%

91 -

100%

% of imports that are environmentally certified

Fre

qu

en

cy

0 10 20 30 40 50

16-20% more

11-15% more

6-10% more

1-5% more

Do not pay more

Percentage (%)

Percent of Imports that are Environmentally Certified

Willingness to Pay for Environmentally Certified Wood Prod.

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

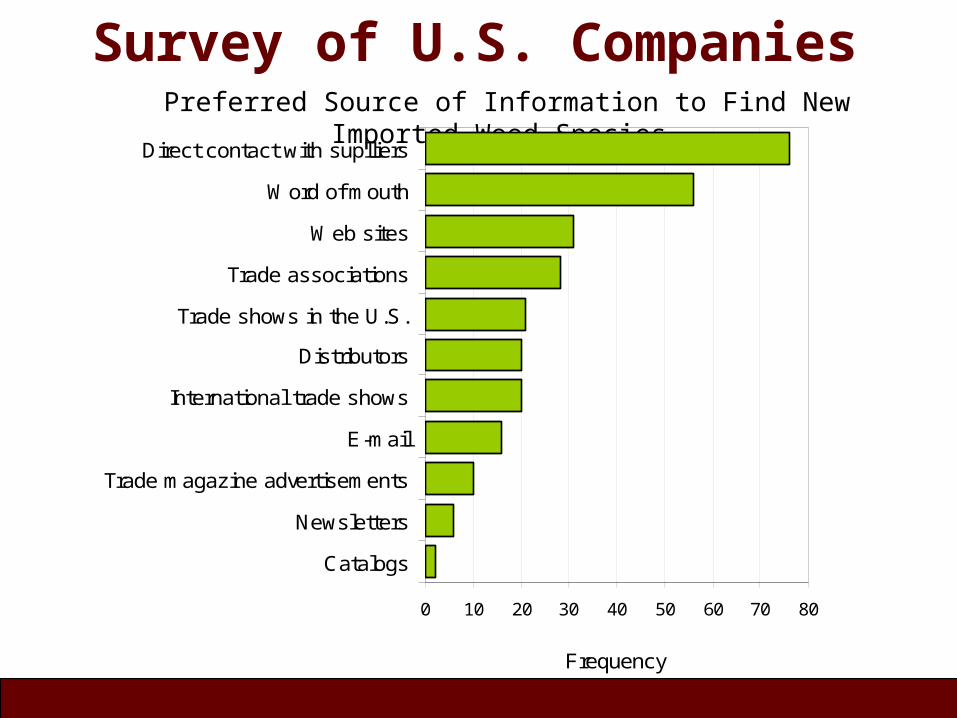

Survey of U.S. CompaniesPreferred Source of Information to Find New Imported Wood Species

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

0 10 20 30 40 50 60 70 80

Catalogs

Newsletters

Trade magazine advertisements

International trade shows

Distributors

Trade shows in the U.S.

Trade associations

Web sites

Word of mouth

Direct contact with suplliers

Frequency

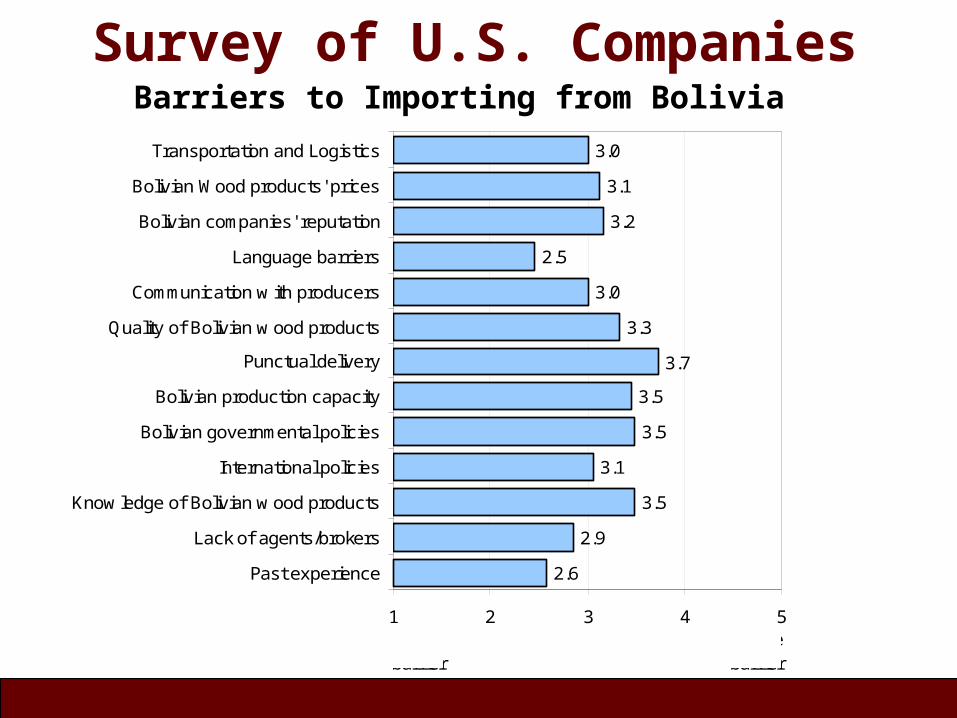

Survey of U.S. CompaniesBarriers to Importing from Bolivia

2.6

2.9

3.5

3.1

3.5

3.5

3.7

3.3

3.0

2.5

3.2

3.1

3.0

1 2 3 4 5

Past experience

Lack of agents/brokers

Know ledge of Bolivian w ood products

International policies

Bolivian governmental policies

Bolivian production capacity

Punctual delivery

Quality of Bolivian w ood products

Communication w ith producers

Language barriers

Bolivian companies' reputation

Bolivian Wood products' prices

Transportation and Logistics

Not a barrier

Large barrier

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

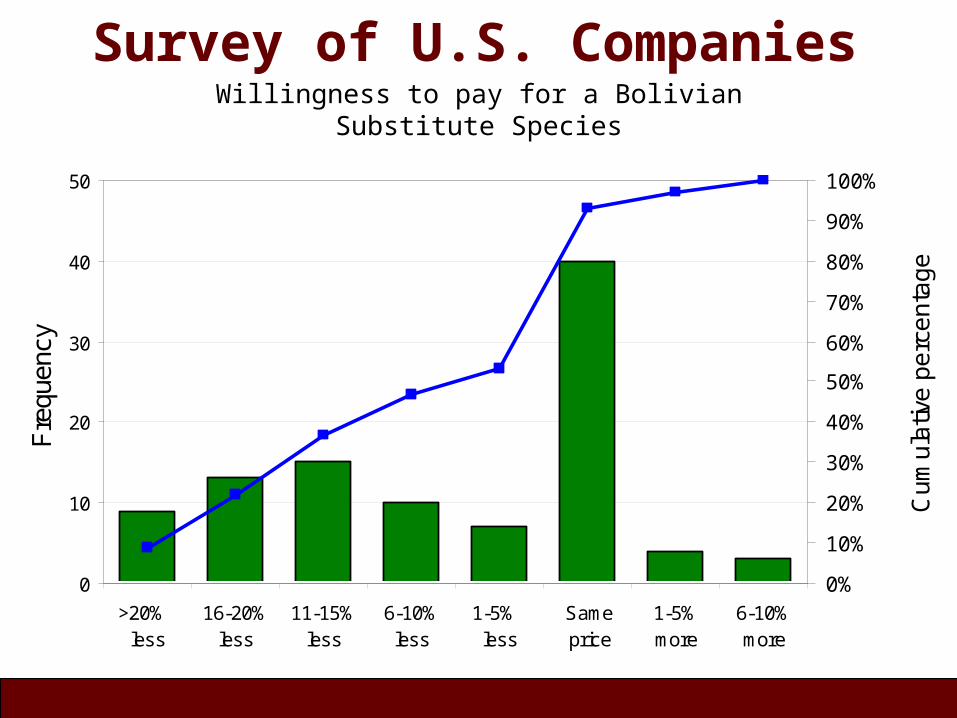

Survey of U.S. CompaniesWillingness to pay for a Bolivian Substitute Species

0

10

20

30

40

50

>20% less

16-20%less

11-15%less

6-10%less

1-5% less

Sameprice

1-5%more

6-10%more

Fre

quen

cy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cu

mu

lativ

e p

erc

en

tag

e

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

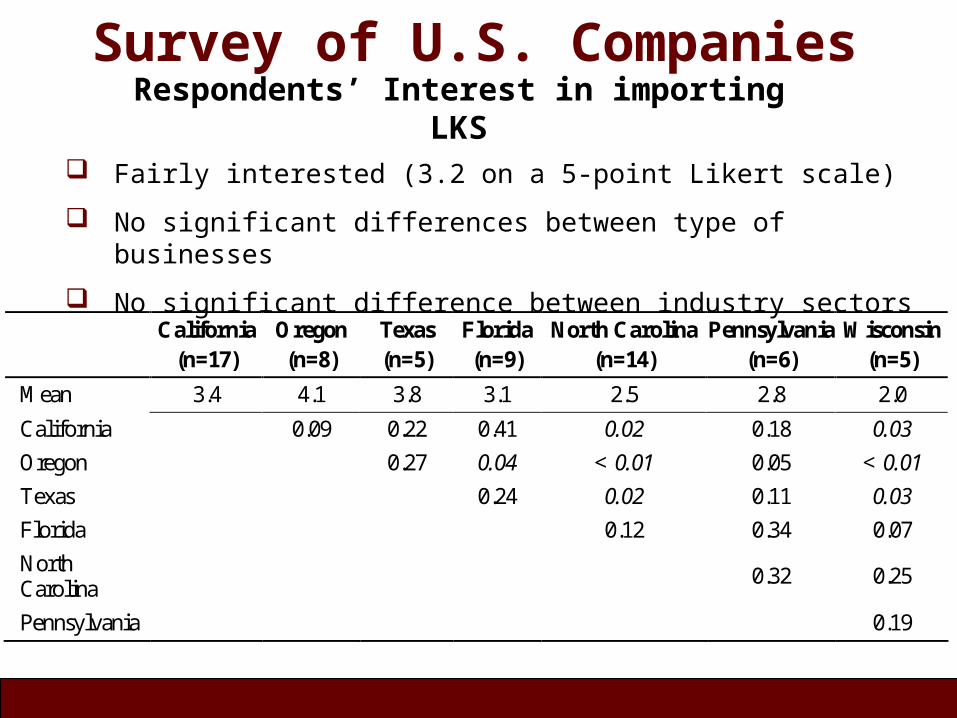

Survey of U.S. CompaniesRespondents’ Interest in importing LKS

California

(n=17) Oregon (n=8)

Texas (n=5)

Florida (n=9)

North Carolina (n=14)

Pennsylvania (n=6)

Wisconsin (n=5)

Mean 3.4 4.1 3.8 3.1 2.5 2.8 2.0

California 0.09 0.22 0.41 0.02 0.18 0.03

Oregon 0.27 0.04 < 0.01 0.05 < 0.01

Texas 0.24 0.02 0.11 0.03

Florida 0.12 0.34 0.07

North Carolina

0.32 0.25

Pennsylvania 0.19

Fairly interested (3.2 on a 5-point Likert scale)

No significant differences between type of businesses

No significant difference between industry sectors

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Survey of U.S. CompaniesOther Results

Past experience importing Bolivian LKS (neither good nor bad)

Preferred brand names for Bolivian LKS would be associated to U.S. species names

Sawnwood is the sector that more likely will try new species

Personal interviews

Image of Bolivian forest products sector

Competitive advantage of environmental certification

Impact of CITES

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Marketing RecommendationsSWOT

Strengths

Commitment with environmental certification

Variety of species

Weaknesses

Landlocked country

Political instability

Limited capacity

Production technology

Opportunities

Wood species in CITES

Demand for certified products

Accessible information systems

Threats

Emergence of new composite materials

Marketing initiatives of competitors

Duty and tax exemption

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Marketing RecommendationsPromotion

Use well-established brand names instead of common Bolivian names for certain species

Associate U.S. domestic species to similar Bolivian LKS

Marketing penetration strategies for some Bolivian LKS

Marketing development strategies for other Bolivian LKS

Promote environmental certification through architects and retailers

Take advantage of Internet technologies

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Marketing Recommendations

Price and Distribution

It is required a “price structure” for Bolivian LKS

Some Bolivian LKS should be marketed at low prices (5% to 20% less)

Western of the U.S. constitutes a better target market for Bolivian LKS

U.S. importers are reluctant to use intermediaries

Take advantage of the Internet and e-business

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

General Conclusions

Several Bolivian LKS wood species are well-known in the U.S. marketplace

Environmental certification can provide competitive advantage

U.S. importers, in general, are planning to increase their imports of tropical hardwoods

Significant differences were found between geographic regions respect the interest on LKS

Important factors to try new wood species were identified

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

General ConclusionsLimitations and Avenues for

Future Research

Other segment like architects or constructors were not included in this research

Characterization of Bolivian LKS was based on literature review

More research on technical information is required for certain Bolivian LKS (ASTM)

Outline Overview Conclusions EndSurvey of U.S Co. Bolivian LKS

Thank you!

Research project sponsored by:

The Center for Forest Products

Marketing and Management