Embed Size (px)

Citation preview

www.infoDev.org

+ INNOVATION & ENTREPRENEURSHIP

www.infoDev.org

IMPRO

VING

BUSIN

ESS CO

MPETITIVEN

ESS AN

D IN

CREA

SING

ECO

NO

MIC

GRO

WTH

IN G

HA

NA

IMPROVING BUSINESS COMPETITIVENESS AND INCREASING ECONOMIC GROWTH IN GHANA

The Role of Information and Communication Technologies and ICT-Enabled Services

IMPROVING BUSINESS COMPETITIVENESS AND INCREASING ECONOMIC GROWTH IN GHANA

www.infoDev.org

Information for Development Program

The Role of Information and Communication Technologies & ICT-Enabled Services

Ghana front 2-27-07.indd iGhana front 2-27-07.indd i 2/27/07 10:49:19 AM2/27/07 10:49:19 AM

IMPROVING BUSINESS COMPETITIVENESS AND INCREASING ECONOMIC GROWTH IN GHANA

www.infoDev.org

Information for Development Program

The Role of Information and Communication Technologies & ICT-Enabled Services

Ghana front 2-27-07.indd iGhana front 2-27-07.indd i 2/27/07 10:49:19 AM2/27/07 10:49:19 AM

To cite this publication:Hewitt Associates. 2006. Improving Business Competitiveness and Increasing Economic Growth in Ghana: The Role of Information and Communication Technologies & IT-Enabled Services. Washington, DC: infoDev / World Bank. Available at: http://www.infodev.org/en/Publication.170.html

©2005The International Bank for Reconstruction and Development/The World Bank1818 H Street, N.W.Washington, D.C. 20433U.S.A.

All rights reservedManufactured in the United States of America

The fi ndings, interpretations and conclusions expressed herein are entirely those of the author(s) and do not necessarily refl ect the view of infoDev, the Donors of infoDev, the International Bank for Reconstruction and Development/The World Bank and its affi liated organizations, the Board of Executive Directors of the World Bank or the governments they represent. The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply on the part of the World Bank any judgement of the legal status of any territory or the endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Copying or transmitting portions of this work may be a violation of applicable law. The World Bank encourages dissemination of its work and normally will promptly grant permission for use. For permission to copy or reprint any part of this work, please contact [email protected].

Ghana front 2-27-07.indd iiGhana front 2-27-07.indd ii 2/27/07 10:49:20 AM2/27/07 10:49:20 AM

To cite this publication:Hewitt Associates. 2006. Improving Business Competitiveness and Increasing Economic Growth in Ghana: The Role of Information and Communication Technologies & IT-Enabled Services. Washington, DC: infoDev / World Bank. Available at: http://www.infodev.org/en/Publication.170.html

©2005The International Bank for Reconstruction and Development/The World Bank1818 H Street, N.W.Washington, D.C. 20433U.S.A.

All rights reservedManufactured in the United States of America

The fi ndings, interpretations and conclusions expressed herein are entirely those of the author(s) and do not necessarily refl ect the view of infoDev, the Donors of infoDev, the International Bank for Reconstruction and Development/The World Bank and its affi liated organizations, the Board of Executive Directors of the World Bank or the governments they represent. The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply on the part of the World Bank any judgement of the legal status of any territory or the endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Copying or transmitting portions of this work may be a violation of applicable law. The World Bank encourages dissemination of its work and normally will promptly grant permission for use. For permission to copy or reprint any part of this work, please contact [email protected].

Ghana front 2-27-07.indd iiGhana front 2-27-07.indd ii 2/27/07 10:49:20 AM2/27/07 10:49:20 AM

Table of Contents . iii

TABLE OF CONTENTS

ABOUT THIS REPORT vii

ABBREVIATIONS AND ACRONYMS viii

1 EXECUTIVE SUMMARY 1

1.1 Introduction 1

1.2 ITES as a Source of Enhanced Economic Growth 1

1.3 Key Findings and Recommendations of our Study 3

1.4 Suggested Target Markets and Segments 8

1.5 Monitoring and Evaluation Indicators 9

1.6 Conclusion 11

2 GHANA’S ATTRACTIVENESS IN THE GLOBAL ITES-BPO ARENA 13

2.1 Overall Analysis 13

2.2 Analysis on the People Driver 15

2.3 Analysis on the Infrastructure Driver 18

2.4 Analysis of the Environment Driver 21

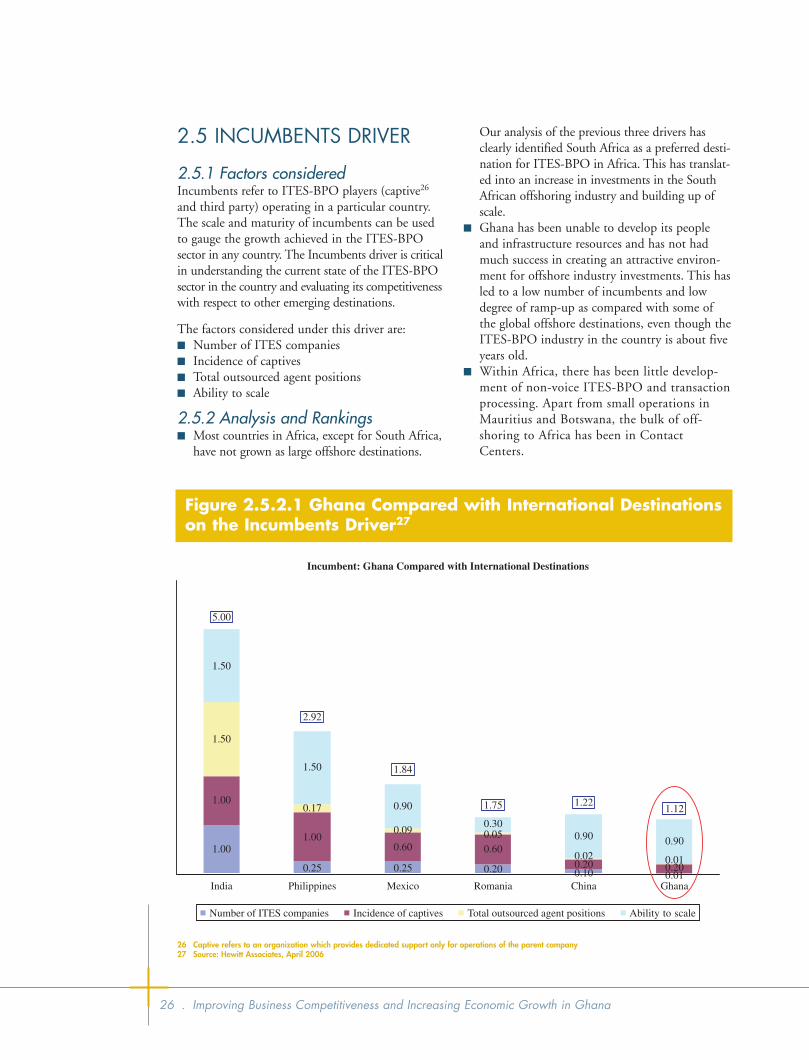

2.5 Incumbents Driver 26

3 GHANA TODAY: KEY FINDINGS 31

3.1 People 31

3.2 Infrastructure 36

3.3 Environment 44

3.4 Clusters 48

3.5 Incumbents 51

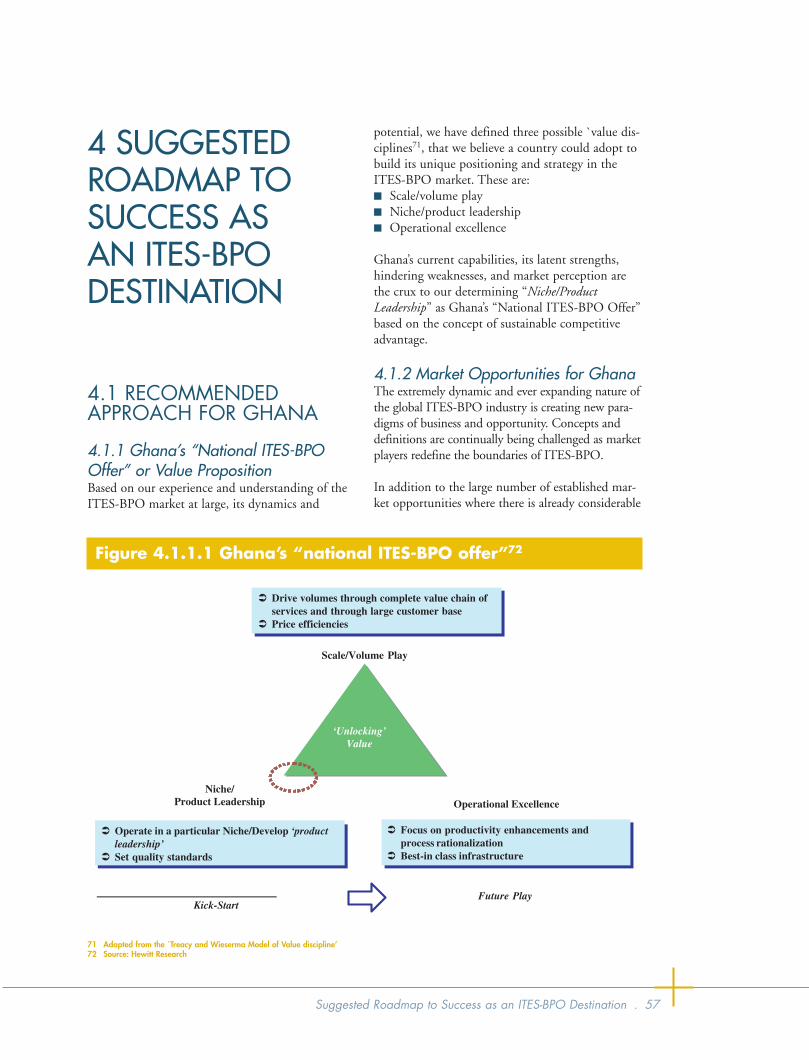

4 SUGGESTED ROADMAP TO SUCCESS AS AN ITES-BPO DESTINATION 57

4.1 Recommended Approach for Ghana 57

4.2 Strategic Recommendations 67

Ghana front 2-27-07.indd iiiGhana front 2-27-07.indd iii 2/27/07 10:49:20 AM2/27/07 10:49:20 AM

Table of Contents . iii

TABLE OF CONTENTS

ABOUT THIS REPORT vii

ABBREVIATIONS AND ACRONYMS viii

1 EXECUTIVE SUMMARY 1

1.1 Introduction 1

1.2 ITES as a Source of Enhanced Economic Growth 1

1.3 Key Findings and Recommendations of our Study 3

1.4 Suggested Target Markets and Segments 8

1.5 Monitoring and Evaluation Indicators 9

1.6 Conclusion 11

2 GHANA’S ATTRACTIVENESS IN THE GLOBAL ITES-BPO ARENA 13

2.1 Overall Analysis 13

2.2 Analysis on the People Driver 15

2.3 Analysis on the Infrastructure Driver 18

2.4 Analysis of the Environment Driver 21

2.5 Incumbents Driver 26

3 GHANA TODAY: KEY FINDINGS 31

3.1 People 31

3.2 Infrastructure 36

3.3 Environment 44

3.4 Clusters 48

3.5 Incumbents 51

4 SUGGESTED ROADMAP TO SUCCESS AS AN ITES-BPO DESTINATION 57

4.1 Recommended Approach for Ghana 57

4.2 Strategic Recommendations 67

Ghana front 2-27-07.indd iiiGhana front 2-27-07.indd iii 2/27/07 10:49:20 AM2/27/07 10:49:20 AM

iv . Improving Business Competitiveness and Increasing Economic Growth in Ghana

4.3 Proposed Industry Bodies 70

4.4 ITES-BPO Policy Framework 74

4.5 Technology Park Framework 75

4.6 Skills Sets for ITES-BPO 77

4.7 The Future 79

5 INVESTMENT PROMOTION STRATEGY 83

5.1 Purpose of Investment Promotion 83

5.2 Recommended Investment Promotion Strategy 83

5.3 Components of Proposed Investment Promotion Strategy 83

5.4 Ownership of ITES Investment Promotion in Ghana—Investment Promotion Cell 84

5.5 Target Market Segments 85

5.6 Marketing Message 86

5.7 Key Strategic Initiatives 87

5.8 Suggested Marketing and Promotion Activities 88

5.9 Marketing and Promotion Tools and Materials 89

5.10 Conclusion 85

6 MONITORING & EVALUATION INDICATORS FOR ITES-BPO INDUSTRY IN GHANA 93

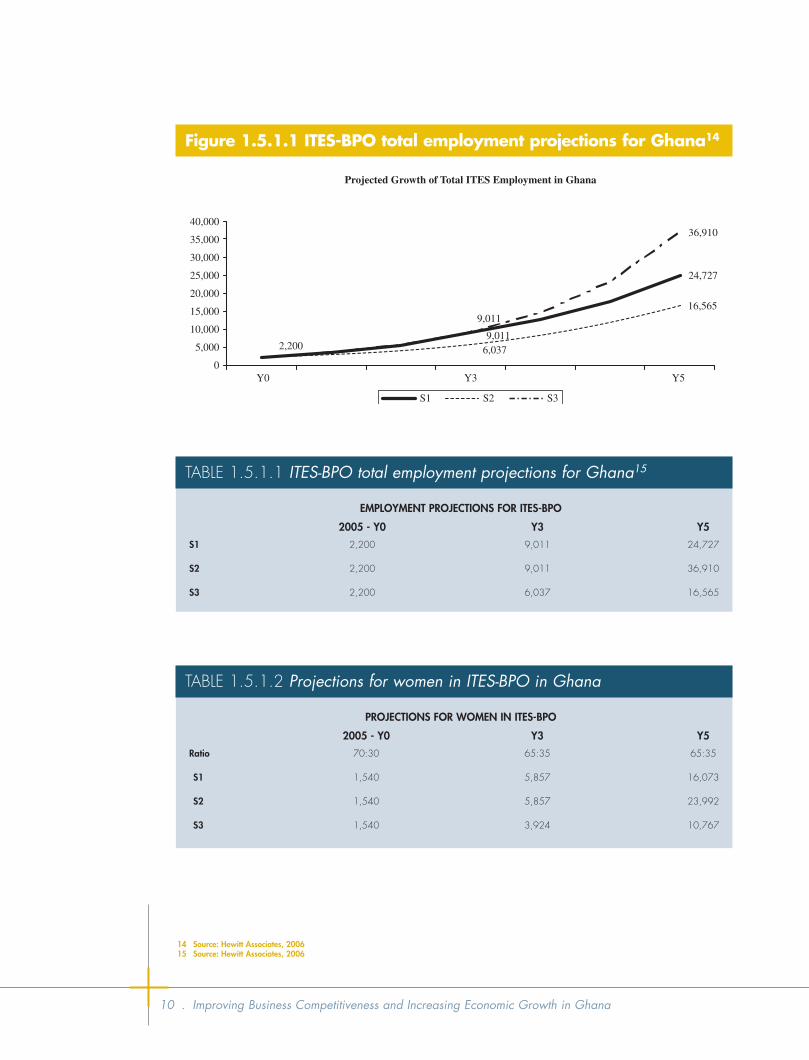

6.1 ITES-BPO Workforce Projections 93

6.2 Other Demographic Projections 95

6.3 Revenue Creation by ITES-BPO 96

Ghana front 2-27-07.indd ivGhana front 2-27-07.indd iv 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

iv . Improving Business Competitiveness and Increasing Economic Growth in Ghana

4.3 Proposed Industry Bodies 70

4.4 ITES-BPO Policy Framework 74

4.5 Technology Park Framework 75

4.6 Skills Sets for ITES-BPO 77

4.7 The Future 79

5 INVESTMENT PROMOTION STRATEGY 83

5.1 Purpose of Investment Promotion 83

5.2 Recommended Investment Promotion Strategy 83

5.3 Components of Proposed Investment Promotion Strategy 83

5.4 Ownership of ITES Investment Promotion in Ghana—Investment Promotion Cell 84

5.5 Target Market Segments 85

5.6 Marketing Message 86

5.7 Key Strategic Initiatives 87

5.8 Suggested Marketing and Promotion Activities 88

5.9 Marketing and Promotion Tools and Materials 89

5.10 Conclusion 85

6 MONITORING & EVALUATION INDICATORS FOR ITES-BPO INDUSTRY IN GHANA 93

6.1 ITES-BPO Workforce Projections 93

6.2 Other Demographic Projections 95

6.3 Revenue Creation by ITES-BPO 96

Ghana front 2-27-07.indd ivGhana front 2-27-07.indd iv 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

Table of Contents . v

FIGURES

Figure 1 Sector-wide employment trends in Ghana 2

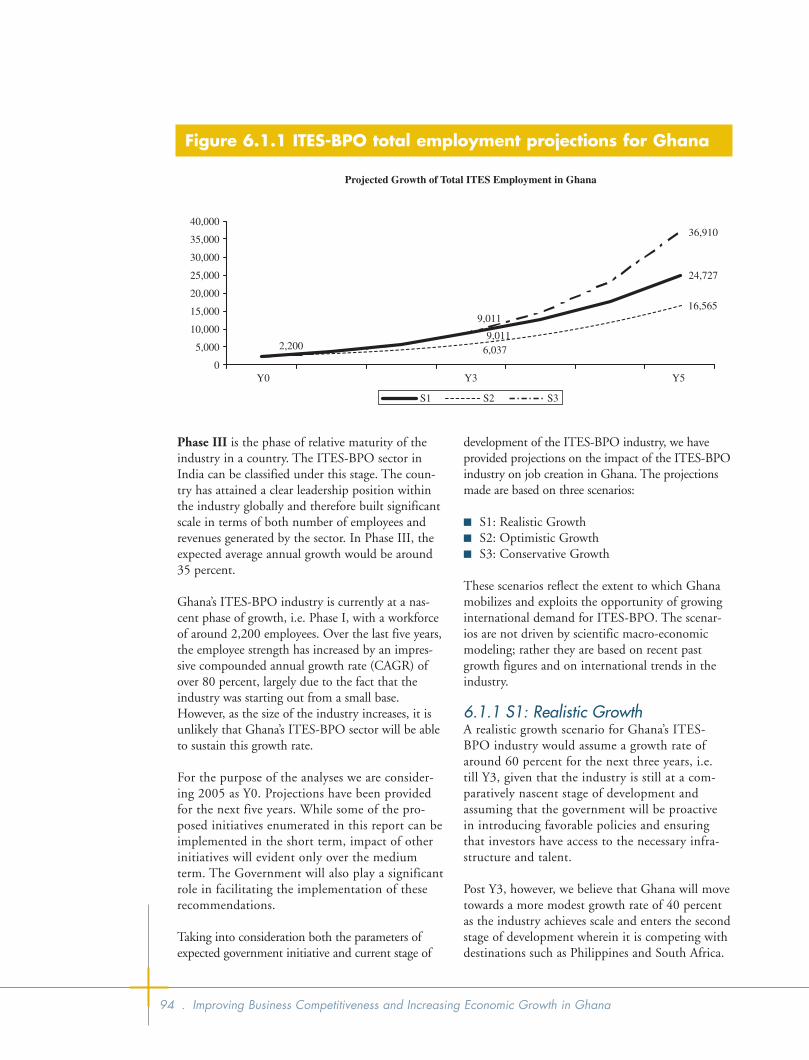

Figure 1.5.1.1 ITES-BPO total employment projections for Ghana 10

Figure 2.1.1 Overall country analysis 14

Figure 2.2.2.1 Ghana compared with international destinations on the people driver 16

Figure 2.2.2.2 Ghana compared with regional destinations on the people driver 16

Figure 2.3.2.1 Ghana compared with international destinations on infrastructure driver 19

Figure 2.3.2.2 Ghana compared with regional destinations on infrastructure driver 20

Figure 2.4.2.1 Ghana compared with international destinations on the environment driver 23

Figure 2.4.2.2 Ghana compared with regional destinations on the environment driver 24

Figure 2.5.2.1 Ghana compared with international destinations on the incumbents driver 26

Figure 2.5.2.2 Ghana compared with regional destinations on the incumbents driver 27

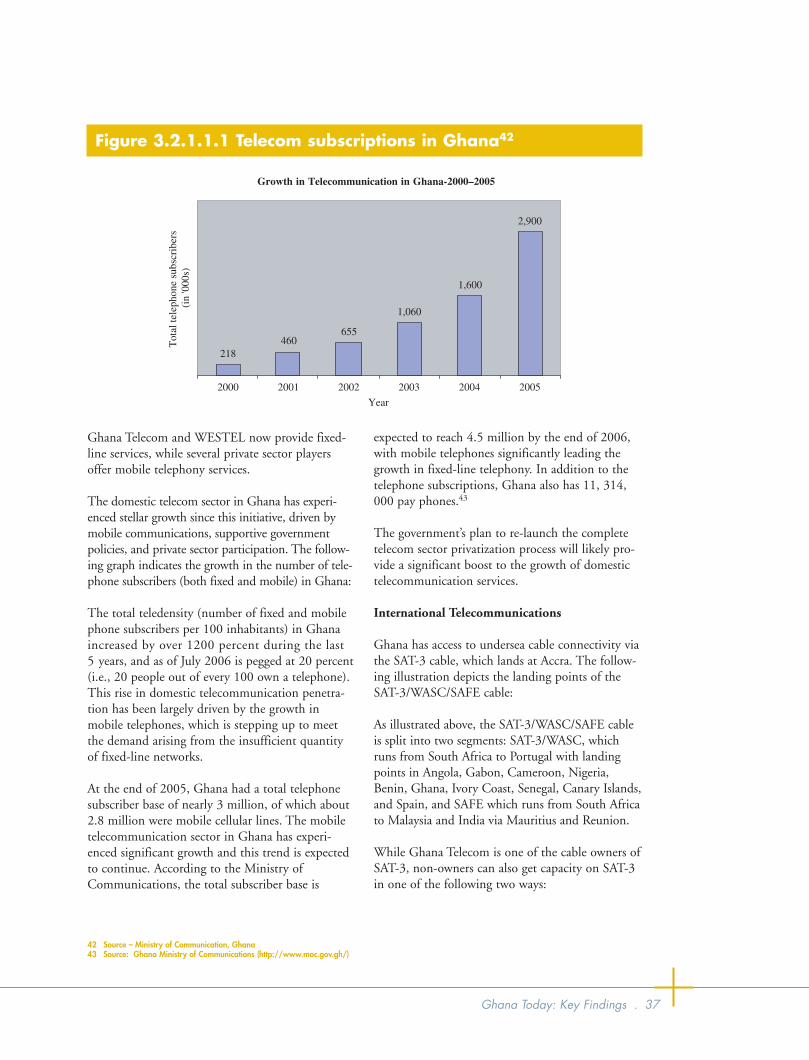

Figure 3.2.1.1.1 Telecom subscriptions in Ghana 37

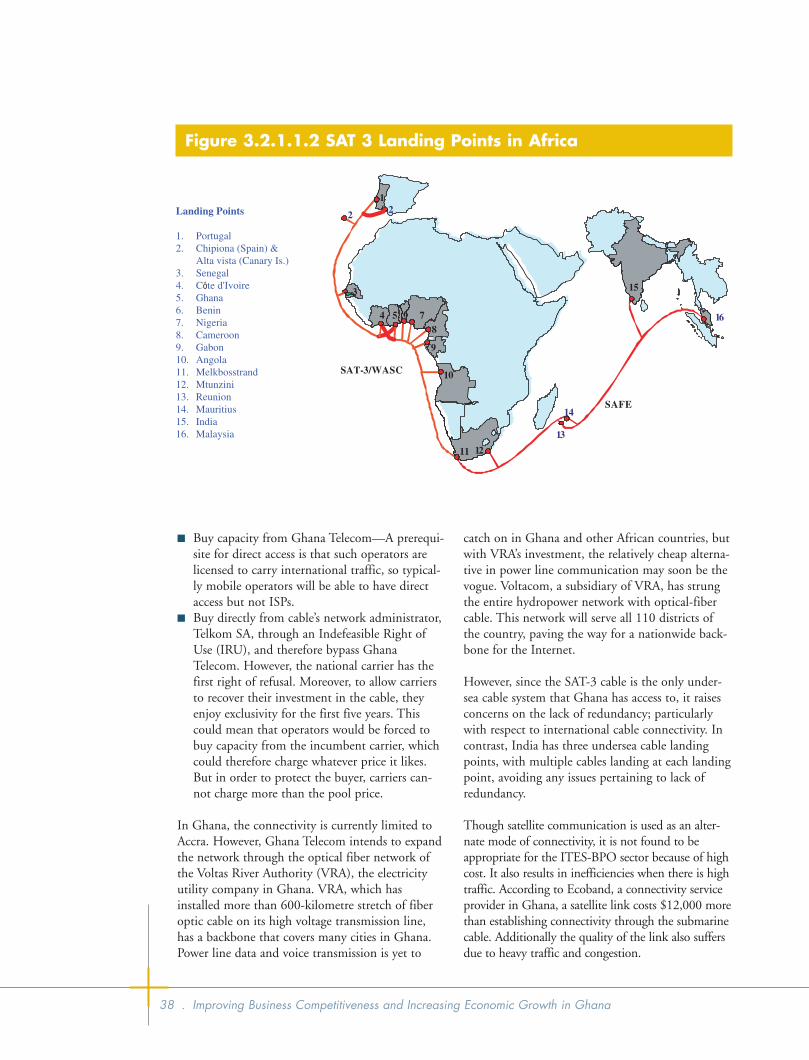

Figure 3.2.1.1.2 SAT 3 Landing points in Africa 38

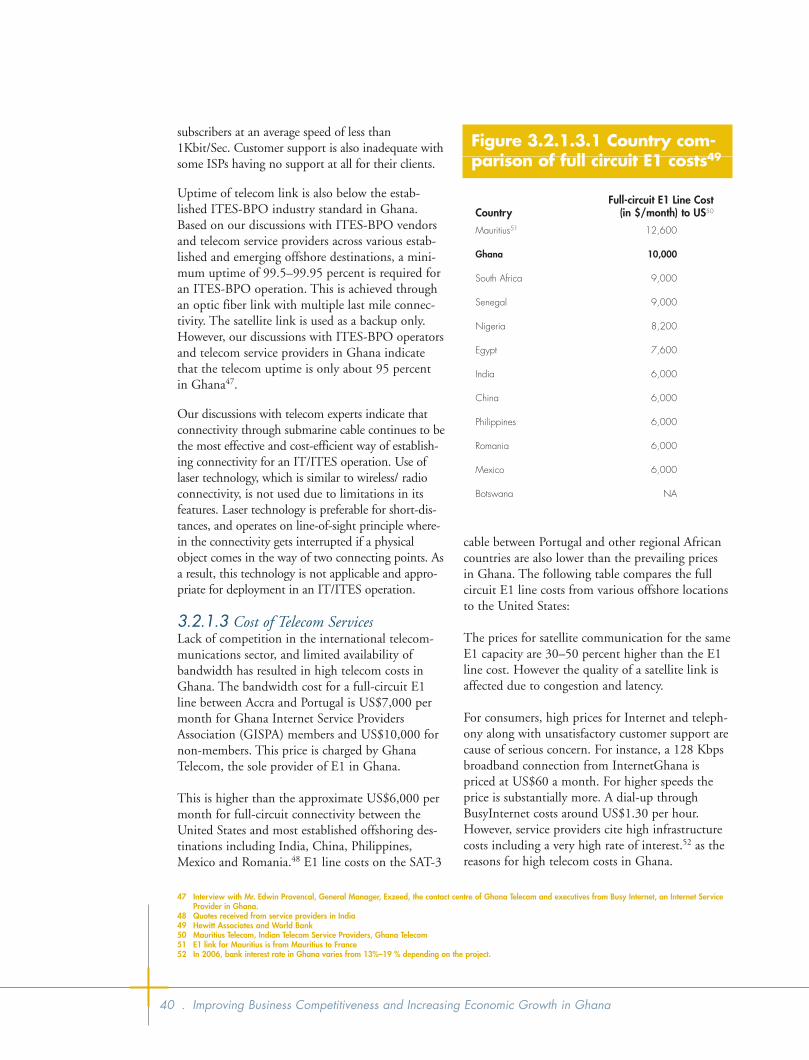

Figure 3.2.1.3.1 Country comparison of full circuit E1 costs 40

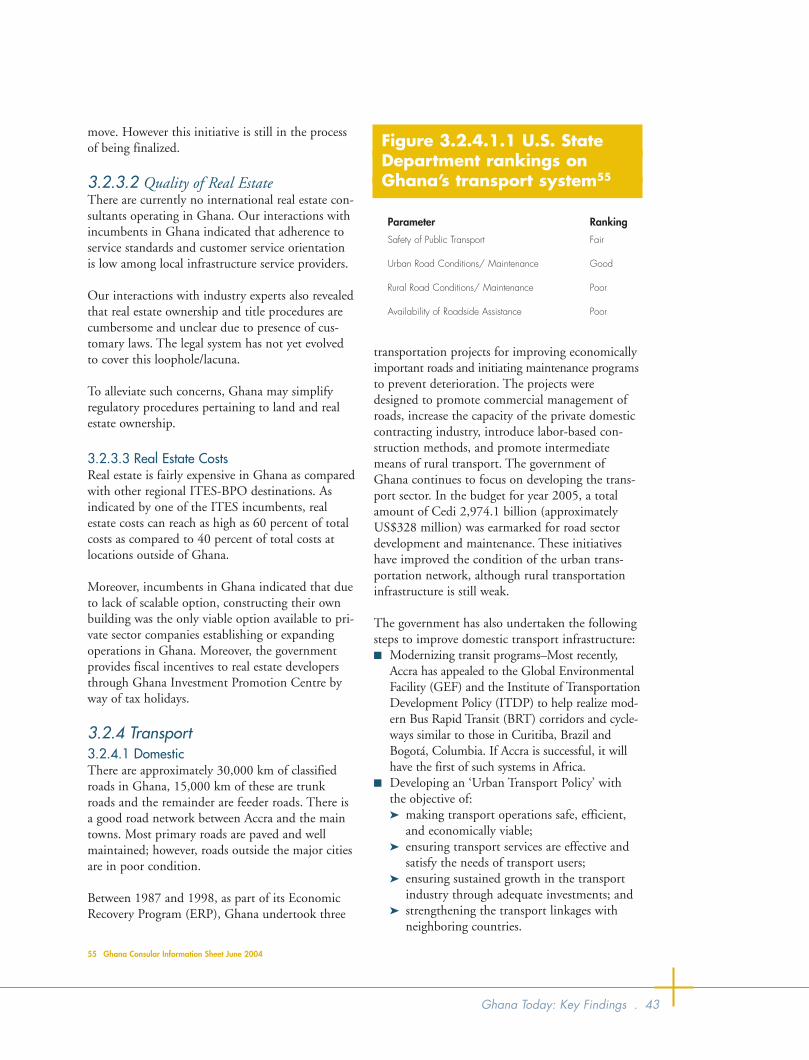

Figure 3.2.4.1.1 U.S. state department rankings on Ghana’s transport system 43

Figure 4.1.1.1 Ghana’s “National ITES-BPO offer” 57

Figure 4.1.3.1.1 ITES-BPO processes 59

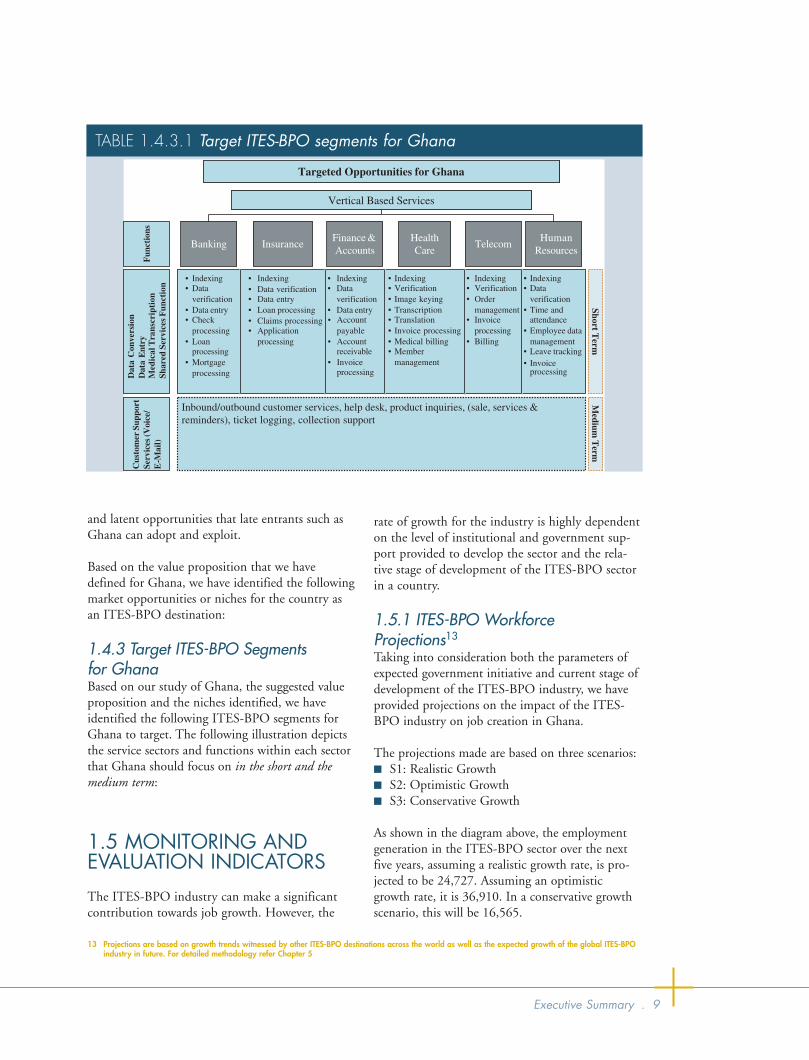

Figure 4.1.3.3.1 Target ITES-BPO segments for Ghana 66

Figure 4.3.1.1 ITES-BPO secretariat structure 71

Figure 4.3.2.1 ITES-BPO association structure 73

Figure 4.4.2.1 Key ITES-BPO policy areas 74

Figure 4.5.2.1 Key components of developing IT/technology parks 76

Figure 4.7.1.1 Issues to be addressed for reaching the destination 80

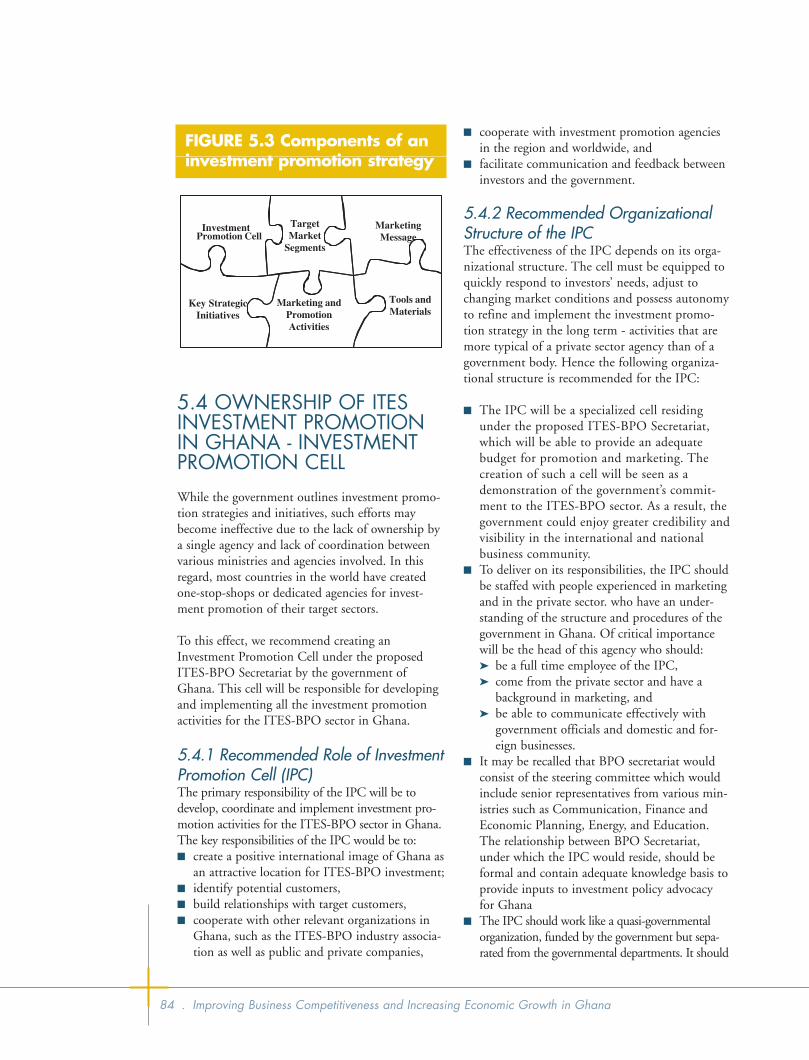

Figure 5.3 Components of an investment promotion strategy 84

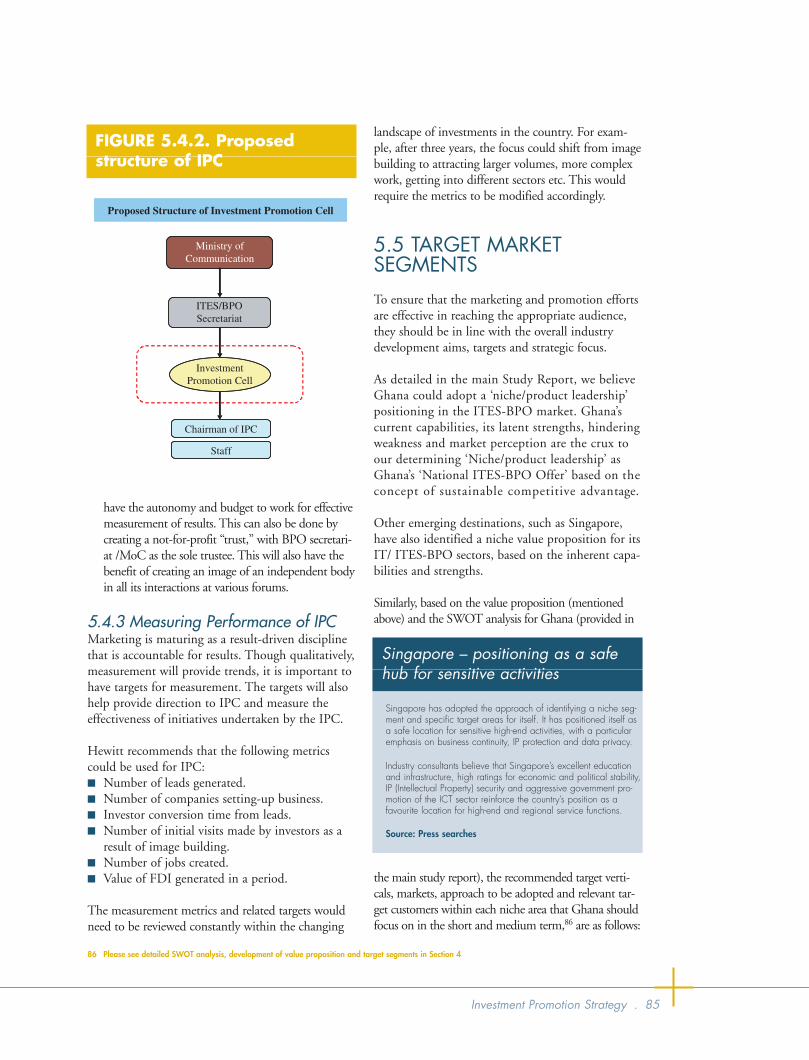

Figure 5.4.2 Proposed structure of IPC 85

Ghana front 2-27-07.indd vGhana front 2-27-07.indd v 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

Table of Contents . v

FIGURES

Figure 1 Sector-wide employment trends in Ghana 2

Figure 1.5.1.1 ITES-BPO total employment projections for Ghana 10

Figure 2.1.1 Overall country analysis 14

Figure 2.2.2.1 Ghana compared with international destinations on the people driver 16

Figure 2.2.2.2 Ghana compared with regional destinations on the people driver 16

Figure 2.3.2.1 Ghana compared with international destinations on infrastructure driver 19

Figure 2.3.2.2 Ghana compared with regional destinations on infrastructure driver 20

Figure 2.4.2.1 Ghana compared with international destinations on the environment driver 23

Figure 2.4.2.2 Ghana compared with regional destinations on the environment driver 24

Figure 2.5.2.1 Ghana compared with international destinations on the incumbents driver 26

Figure 2.5.2.2 Ghana compared with regional destinations on the incumbents driver 27

Figure 3.2.1.1.1 Telecom subscriptions in Ghana 37

Figure 3.2.1.1.2 SAT 3 Landing points in Africa 38

Figure 3.2.1.3.1 Country comparison of full circuit E1 costs 40

Figure 3.2.4.1.1 U.S. state department rankings on Ghana’s transport system 43

Figure 4.1.1.1 Ghana’s “National ITES-BPO offer” 57

Figure 4.1.3.1.1 ITES-BPO processes 59

Figure 4.1.3.3.1 Target ITES-BPO segments for Ghana 66

Figure 4.3.1.1 ITES-BPO secretariat structure 71

Figure 4.3.2.1 ITES-BPO association structure 73

Figure 4.4.2.1 Key ITES-BPO policy areas 74

Figure 4.5.2.1 Key components of developing IT/technology parks 76

Figure 4.7.1.1 Issues to be addressed for reaching the destination 80

Figure 5.3 Components of an investment promotion strategy 84

Figure 5.4.2 Proposed structure of IPC 85

Ghana front 2-27-07.indd vGhana front 2-27-07.indd v 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

vi . Improving Business Competitiveness and Increasing Economic Growth in Ghana

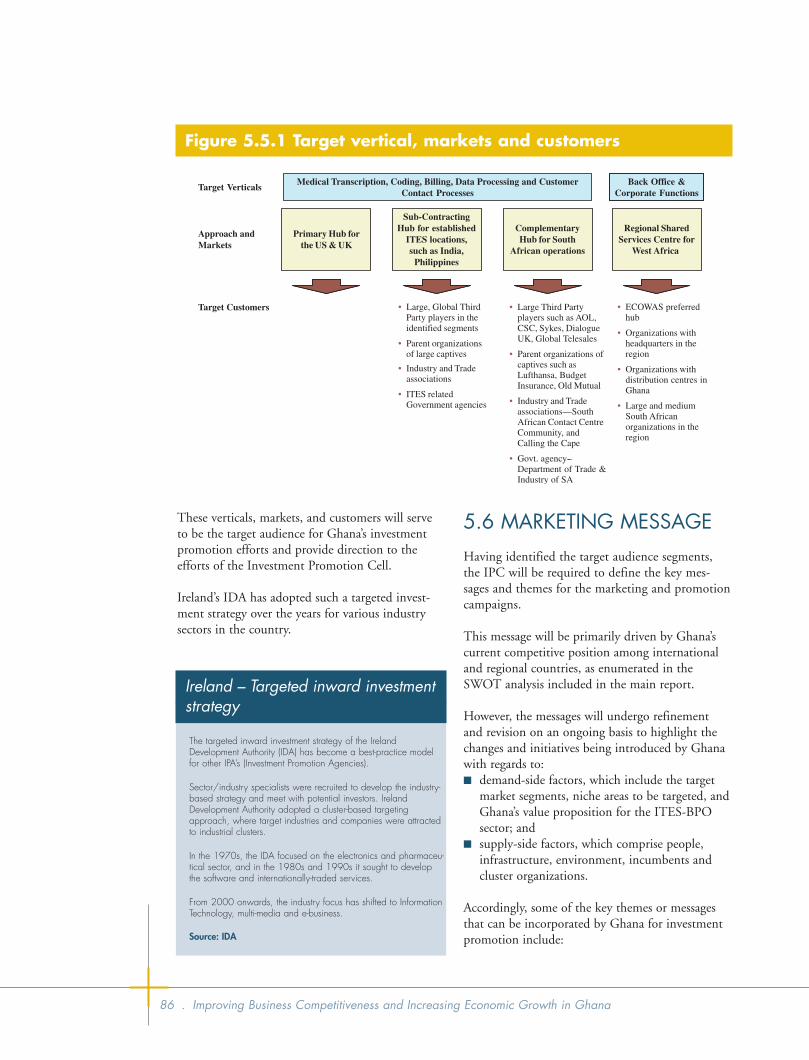

Figure 5.5.1 Target vertical, markets and customers 86

Figure 5.6.1 Defining the message 87

Figure 6.1.1 ITES-BPO total employment projections for Ghana 94

TABLES

Table 1.2.1 Worldwide ITES-BPO market forecast1 (USD millions) 1

Table 1.4.3.1 Target ITES-BPO segments for Ghana 9

Table 1.5.1.1 ITES-BPO total employment projections for Ghana 10

Table 1.5.1.2 Projections for women in ITES-BPO in Ghana 10

Table 1.5.1.3 Projections for ITES-BPO revenue generation in Ghana 11

Table 3.1.1.1.1 Country comparison for number of tertiary enrolments 31

Table 3.1.2.1.1 Country comparison on quality of education 33

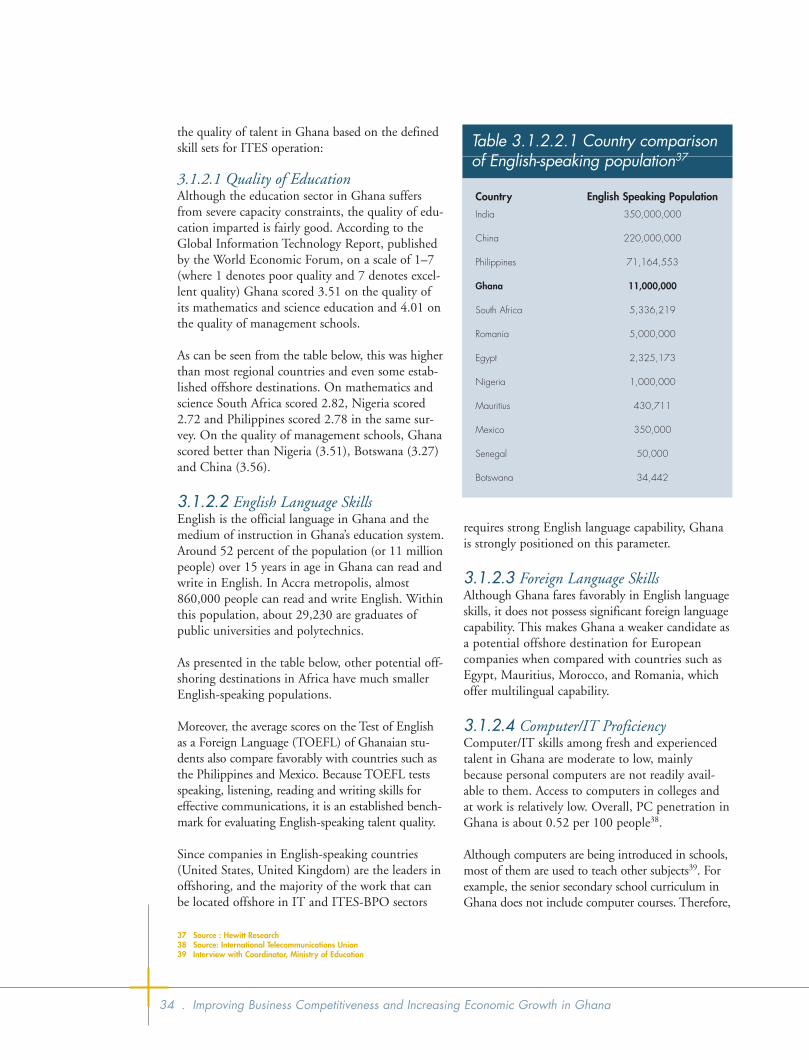

Table 3.1.2.2.1 Country comparison of English-speaking population 34

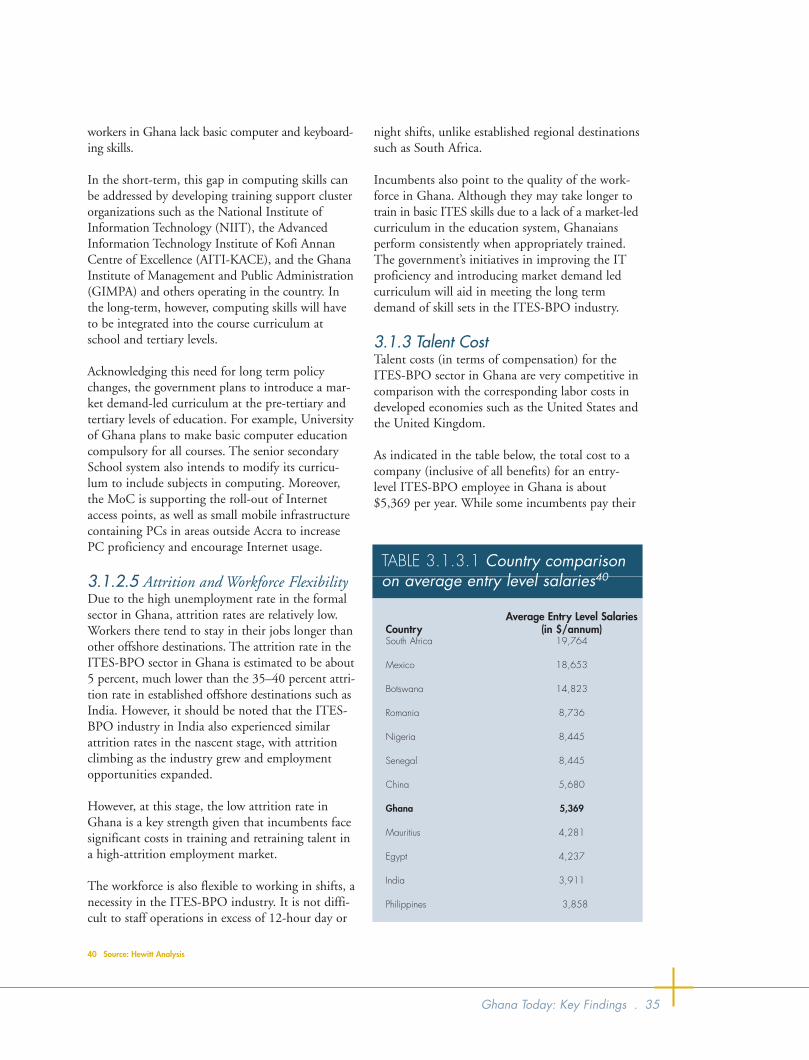

Table 3.1.3.1 Country comparison on average entry level salaries 35

Table 3.5.1.1.1 Existing ITES-BPO incumbents in Ghana 53

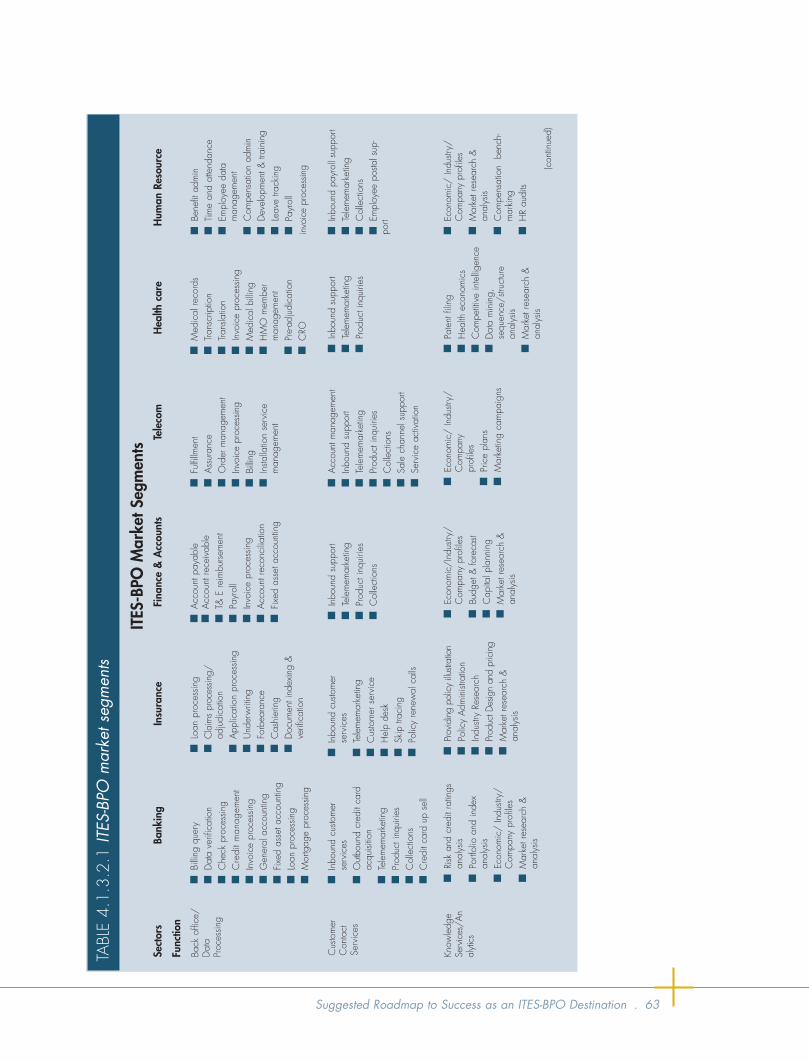

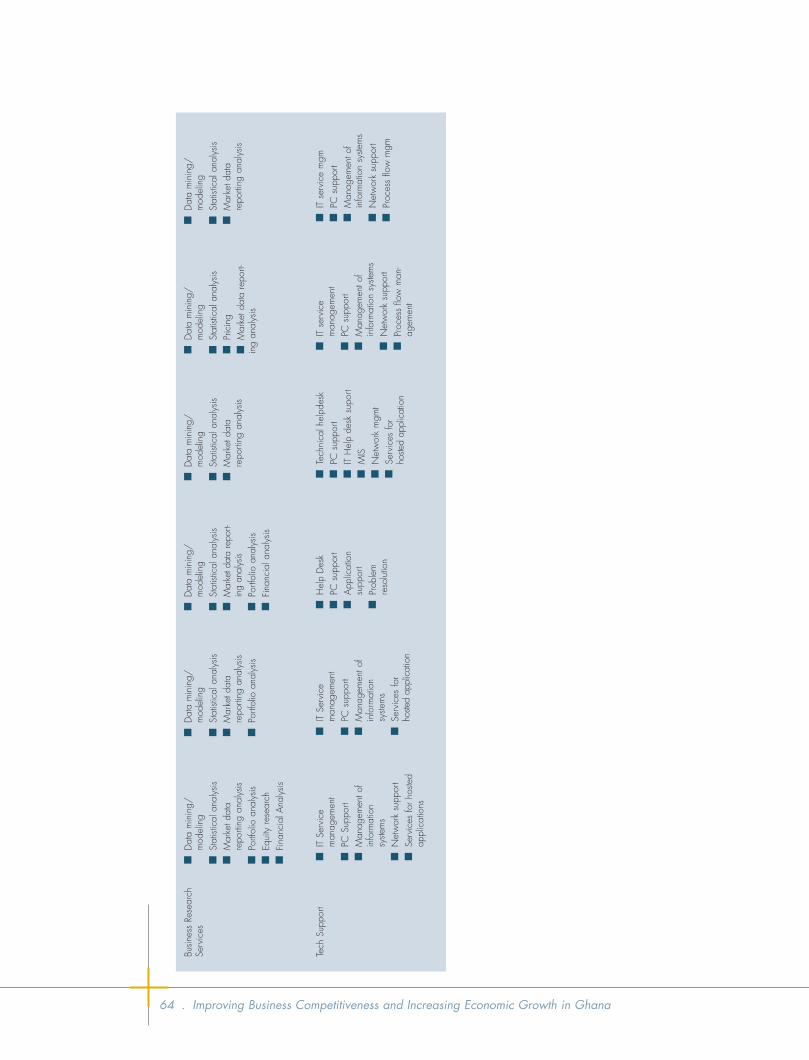

Table 4.1.3.2.1 ITES-BPO market segments 63

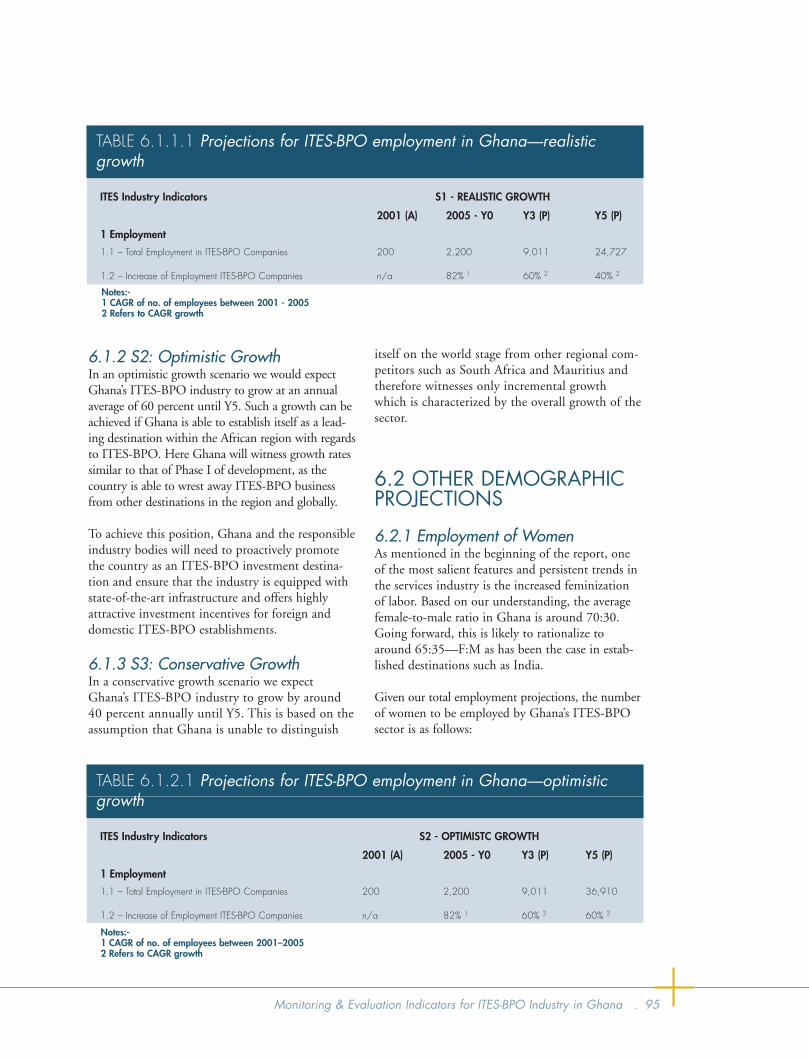

Table 6.1.1.1 Projections for ITES-BPO employment in Ghana—realistic growth 95

Table 6.1.2.1 Projections for ITES-BPO employment in Ghana—optimistic growth 95

Table 6.1.3.1 Projections for ITES-BPO employment in Ghana—conservative growth 96

Table 6.2.1.1 Projections for women in ITES-BPO in Ghana 96

Table 6.2.2.1 Projections for employment by skill—level 96

Table 6.3.1 Projections for ITES-BPO revenue generation in Ghana 96

Ghana front 2-27-07.indd viGhana front 2-27-07.indd vi 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

vi . Improving Business Competitiveness and Increasing Economic Growth in Ghana

Figure 5.5.1 Target vertical, markets and customers 86

Figure 5.6.1 Defining the message 87

Figure 6.1.1 ITES-BPO total employment projections for Ghana 94

TABLES

Table 1.2.1 Worldwide ITES-BPO market forecast1 (USD millions) 1

Table 1.4.3.1 Target ITES-BPO segments for Ghana 9

Table 1.5.1.1 ITES-BPO total employment projections for Ghana 10

Table 1.5.1.2 Projections for women in ITES-BPO in Ghana 10

Table 1.5.1.3 Projections for ITES-BPO revenue generation in Ghana 11

Table 3.1.1.1.1 Country comparison for number of tertiary enrolments 31

Table 3.1.2.1.1 Country comparison on quality of education 33

Table 3.1.2.2.1 Country comparison of English-speaking population 34

Table 3.1.3.1 Country comparison on average entry level salaries 35

Table 3.5.1.1.1 Existing ITES-BPO incumbents in Ghana 53

Table 4.1.3.2.1 ITES-BPO market segments 63

Table 6.1.1.1 Projections for ITES-BPO employment in Ghana—realistic growth 95

Table 6.1.2.1 Projections for ITES-BPO employment in Ghana—optimistic growth 95

Table 6.1.3.1 Projections for ITES-BPO employment in Ghana—conservative growth 96

Table 6.2.1.1 Projections for women in ITES-BPO in Ghana 96

Table 6.2.2.1 Projections for employment by skill—level 96

Table 6.3.1 Projections for ITES-BPO revenue generation in Ghana 96

Ghana front 2-27-07.indd viGhana front 2-27-07.indd vi 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

About This Report . vii

ABOUT THIS REPORTThis document discusses the role of information and communication technology (ICT) and informa-tion technology-enabled services (ITES) in improving business competitiveness and increasing economic growth in Ghana. In this context, the document includes:■ An analysis of Ghana’s ability to compete globally as well as regionally in the information technology-

enabled services (ITES)-business process outsourcing/offshoring (BPO) sector and the primary con-straints to improving Ghana’s competitiveness in the sector.

■ Recommendations for concrete actions for Ghana to increase its competitiveness and capability as an ITES-BPO destination, and target ITES-BPO activities and market segments in which it can be com-petitive in the short and medium term.

■ A roadmap for developing the ITES-BPO industry in Ghana, including a skills development compo-nent, policy framework, and measurement matrix.

■ Recommended investment promotion strategy for developing and attracting investments in Ghana’s ITES-BPO sector.

■ A monitoring and evaluation framework for the ITES-BPO sector in Ghana, providing baselines and targets.

The analysis presented in this report is based on information and findings as of April 2006, and may not reflect the impact of subsequent changes and developments.

This report was commissioned by the Information for Development Program (infoDev) in partnership with the Government of Ghana through the Ministry of Communications and the World Bank Group, and prepared by Hewitt Associates (India).

Ghana front 2-27-07.indd viiGhana front 2-27-07.indd vii 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

About This Report . vii

ABOUT THIS REPORTThis document discusses the role of information and communication technology (ICT) and informa-tion technology-enabled services (ITES) in improving business competitiveness and increasing economic growth in Ghana. In this context, the document includes:■ An analysis of Ghana’s ability to compete globally as well as regionally in the information technology-

enabled services (ITES)-business process outsourcing/offshoring (BPO) sector and the primary con-straints to improving Ghana’s competitiveness in the sector.

■ Recommendations for concrete actions for Ghana to increase its competitiveness and capability as an ITES-BPO destination, and target ITES-BPO activities and market segments in which it can be com-petitive in the short and medium term.

■ A roadmap for developing the ITES-BPO industry in Ghana, including a skills development compo-nent, policy framework, and measurement matrix.

■ Recommended investment promotion strategy for developing and attracting investments in Ghana’s ITES-BPO sector.

■ A monitoring and evaluation framework for the ITES-BPO sector in Ghana, providing baselines and targets.

The analysis presented in this report is based on information and findings as of April 2006, and may not reflect the impact of subsequent changes and developments.

This report was commissioned by the Information for Development Program (infoDev) in partnership with the Government of Ghana through the Ministry of Communications and the World Bank Group, and prepared by Hewitt Associates (India).

Ghana front 2-27-07.indd viiGhana front 2-27-07.indd vii 2/27/07 10:49:21 AM2/27/07 10:49:21 AM

viii . Improving Business Competitiveness and Increasing Economic Growth in Ghana

ABBREVIATIONS AND ACRONYMS

BPO: Business Process Outsourcing/Offshoring

CAGR: Compounded Annual Growth Rate

ECOWAS: Economic Community of West African States

GDP: Gross Domestic Product

GIMPA: Ghana Institute of Management and Public Administration

GISPA: Ghana Internet Service Providers Association

GoG: Government of Ghana

GZFB: Ghana Free Zone Board

KPO: Knowledge Process Outsourcing

ICT4AD Policy: ICT for Accelerated Development Policy

ITES: Information Technology Enabled Services

MNC: Multinational Corporation

MoC: Ministry of Communications

NCA: National Communications Authority

OEM: Original Equipment Manufacturer

PC: Personal Computer

SLA: Service Level Agreement

SSS: Senior Secondary School

UK: United Kingdom

US: United States of America

USD: US Dollars

VoC: Voice of Customer

VoIP: Voice over Internet Protocol

WAMU: West African Monetary Union

Ghana front 2-27-07.indd viiiGhana front 2-27-07.indd viii 2/27/07 10:49:22 AM2/27/07 10:49:22 AM

viii . Improving Business Competitiveness and Increasing Economic Growth in Ghana

ABBREVIATIONS AND ACRONYMS

BPO: Business Process Outsourcing/Offshoring

CAGR: Compounded Annual Growth Rate

ECOWAS: Economic Community of West African States

GDP: Gross Domestic Product

GIMPA: Ghana Institute of Management and Public Administration

GISPA: Ghana Internet Service Providers Association

GoG: Government of Ghana

GZFB: Ghana Free Zone Board

KPO: Knowledge Process Outsourcing

ICT4AD Policy: ICT for Accelerated Development Policy

ITES: Information Technology Enabled Services

MNC: Multinational Corporation

MoC: Ministry of Communications

NCA: National Communications Authority

OEM: Original Equipment Manufacturer

PC: Personal Computer

SLA: Service Level Agreement

SSS: Senior Secondary School

UK: United Kingdom

US: United States of America

USD: US Dollars

VoC: Voice of Customer

VoIP: Voice over Internet Protocol

WAMU: West African Monetary Union

Ghana front 2-27-07.indd viiiGhana front 2-27-07.indd viii 2/27/07 10:49:22 AM2/27/07 10:49:22 AM

Executive Summary . 1

1 EXECUTIVESUMMARY

1.1 INTRODUCTIONThe Government of Ghana has identified IT-enabled services (ITES) as one of the key sectorsfor enhancing economic growth, along with agro-processing and tourism. It is implementing severalprograms under the e-Ghana initiative to improveits skills and infrastructure.

In an effort to understand Ghana’s capability and real-ize its potential in ITES, Hewitt Associates (India)Private Ltd., on behalf of the Government of Ghana,the Information for Development Program (infoDev),and the World Bank Group, conducted a study onthe role of ICTs and ITES in improving businesscompetitiveness and increasing economic growth inGhana.

1.2 ITES AS A SOURCE OFENHANCED ECONOMICGROWTHAfter studying economic progress in relation to theeconomic structure of different countries over time,it is clear that a higher average level of real incomeis always associated with a high proportion of theworking population engaged in the service or publicutility sectors. In many large economies, the servicesector is the largest in terms of employment, due

mostly to a massive increase in productivity growthand the progressively higher income elasticity in theprimary and secondary sectors. More economicallyadvanced countries, such as the United States,Germany, and the United Kingdom, have followedthe movement from agriculture as the largest sourceof employment, to industry, and finally to services.The structural transformation of employment hasoccurred even more markedly from agriculture toservices in the later developed and some of the cur-rently developing countries. The service sector isbecoming a dominant feature of the economic land-scape in these countries as its contributions towardsGDP steadily increase and the contributions of theagricultural sector to GDP decrease.

Within services, the IT-enabled service segment isbeginning to be perceived as the new growth fron-tier. The rise of this segment is driven by rapidgrowth in global outsourcing and offshoring.Outsourcing is defined as the delegation of one ormore IT-intensive business processes to an externalprovider who in turn, owns, administers, and man-ages selected processes, based on defined and meas-urable performance metrics. Offshoring refers tothe administration of these processes in a locationother than the company’s home country.

Countries such as India, Philippines, the CzechRepublic, and Ireland have completely transformedtheir economies by adopting IT and ITES-BPOsegments as the engine that propels their economies inan accelerated mode in relatively short periods of time.

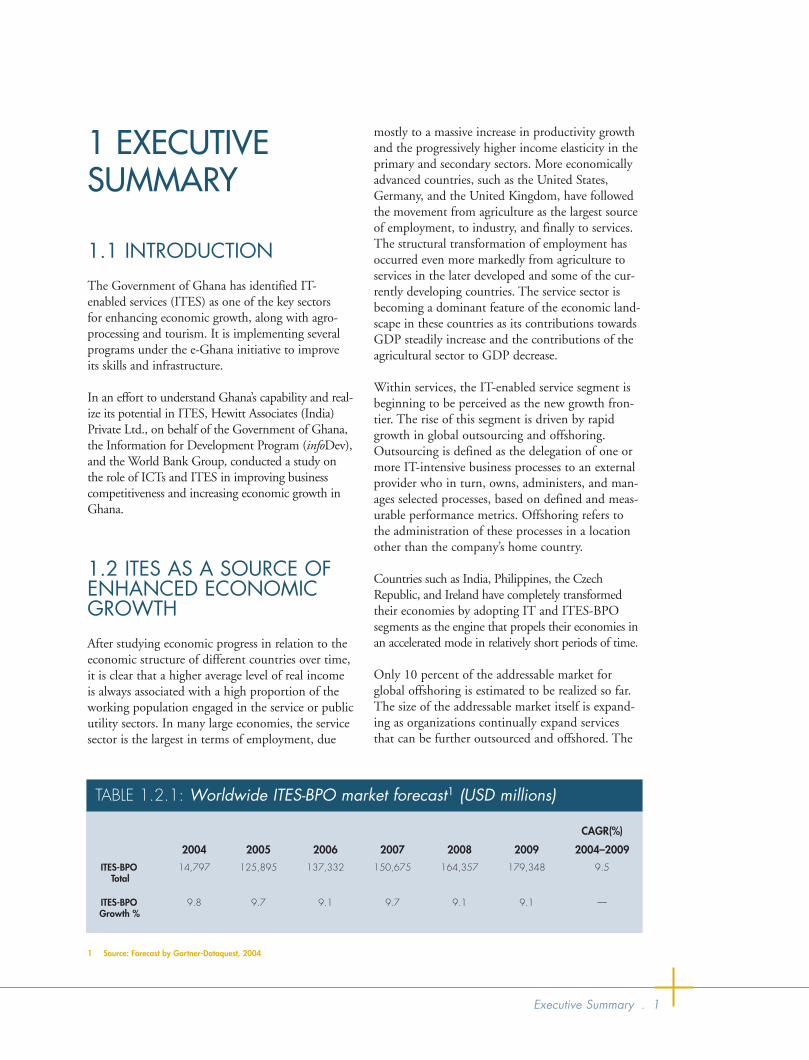

Only 10 percent of the addressable market forglobal offshoring is estimated to be realized so far.The size of the addressable market itself is expand-ing as organizations continually expand servicesthat can be further outsourced and offshored. The

TABLE 1.2.1: Worldwide ITES-BPO market forecast1 (USD millions)

CAGR(%)

2004 2005 2006 2007 2008 2009 2004–2009

ITES-BPO 14,797 125,895 137,332 150,675 164,357 179,348 9.5Total

ITES-BPO 9.8 9.7 9.1 9.7 9.1 9.1 —Growth %

1 Source: Forecast by Gartner-Dataquest, 2004

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 1

Executive Summary . 1

1 EXECUTIVESUMMARY

1.1 INTRODUCTIONThe Government of Ghana has identified IT-enabled services (ITES) as one of the key sectorsfor enhancing economic growth, along with agro-processing and tourism. It is implementing severalprograms under the e-Ghana initiative to improveits skills and infrastructure.

In an effort to understand Ghana’s capability and real-ize its potential in ITES, Hewitt Associates (India)Private Ltd., on behalf of the Government of Ghana,the Information for Development Program (infoDev),and the World Bank Group, conducted a study onthe role of ICTs and ITES in improving businesscompetitiveness and increasing economic growth inGhana.

1.2 ITES AS A SOURCE OFENHANCED ECONOMICGROWTHAfter studying economic progress in relation to theeconomic structure of different countries over time,it is clear that a higher average level of real incomeis always associated with a high proportion of theworking population engaged in the service or publicutility sectors. In many large economies, the servicesector is the largest in terms of employment, due

mostly to a massive increase in productivity growthand the progressively higher income elasticity in theprimary and secondary sectors. More economicallyadvanced countries, such as the United States,Germany, and the United Kingdom, have followedthe movement from agriculture as the largest sourceof employment, to industry, and finally to services.The structural transformation of employment hasoccurred even more markedly from agriculture toservices in the later developed and some of the cur-rently developing countries. The service sector isbecoming a dominant feature of the economic land-scape in these countries as its contributions towardsGDP steadily increase and the contributions of theagricultural sector to GDP decrease.

Within services, the IT-enabled service segment isbeginning to be perceived as the new growth fron-tier. The rise of this segment is driven by rapidgrowth in global outsourcing and offshoring.Outsourcing is defined as the delegation of one ormore IT-intensive business processes to an externalprovider who in turn, owns, administers, and man-ages selected processes, based on defined and meas-urable performance metrics. Offshoring refers tothe administration of these processes in a locationother than the company’s home country.

Countries such as India, Philippines, the CzechRepublic, and Ireland have completely transformedtheir economies by adopting IT and ITES-BPOsegments as the engine that propels their economies inan accelerated mode in relatively short periods of time.

Only 10 percent of the addressable market forglobal offshoring is estimated to be realized so far.The size of the addressable market itself is expand-ing as organizations continually expand servicesthat can be further outsourced and offshored. The

TABLE 1.2.1: Worldwide ITES-BPO market forecast1 (USD millions)

CAGR(%)

2004 2005 2006 2007 2008 2009 2004–2009

ITES-BPO 14,797 125,895 137,332 150,675 164,357 179,348 9.5Total

ITES-BPO 9.8 9.7 9.1 9.7 9.1 9.1 —Growth %

1 Source: Forecast by Gartner-Dataquest, 2004

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 1

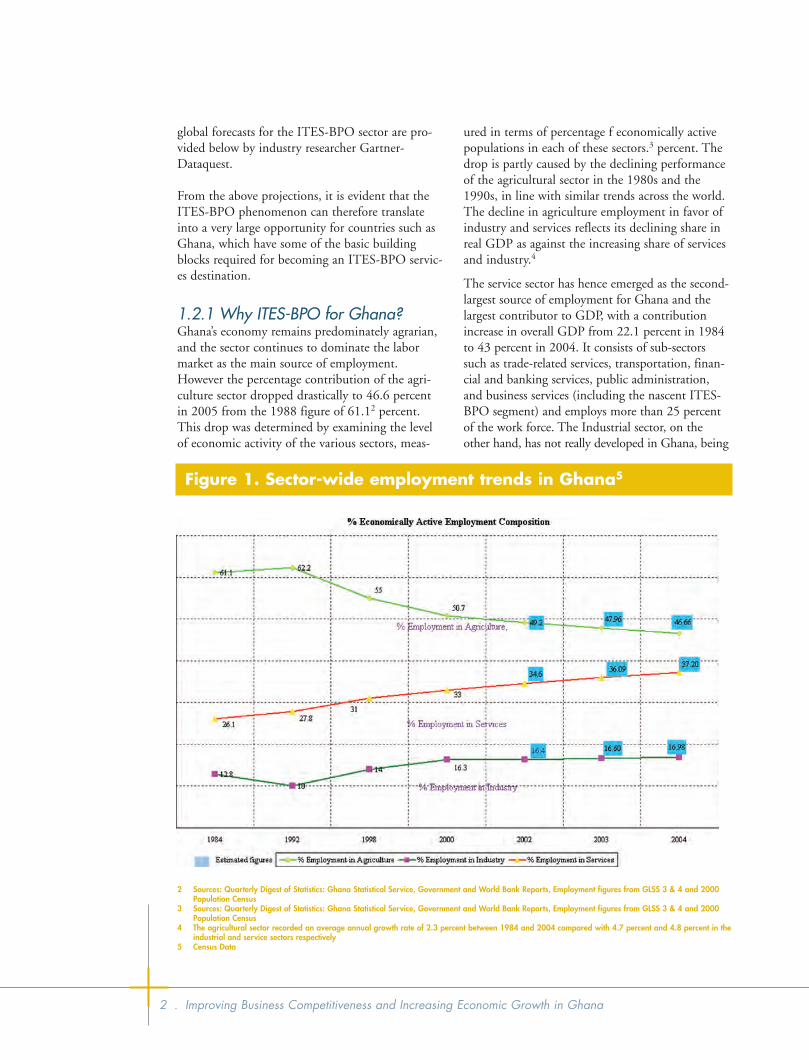

2 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

2 Sources: Quarterly Digest of Statistics: Ghana Statistical Service, Government and World Bank Reports, Employment figures from GLSS 3 & 4 and 2000Population Census

3 Sources: Quarterly Digest of Statistics: Ghana Statistical Service, Government and World Bank Reports, Employment figures from GLSS 3 & 4 and 2000Population Census

4 The agricultural sector recorded an average annual growth rate of 2.3 percent between 1984 and 2004 compared with 4.7 percent and 4.8 percent in theindustrial and service sectors respectively

5 Census Data

Figure 1. Sector-wide employment trends in Ghana5

global forecasts for the ITES-BPO sector are pro-vided below by industry researcher Gartner-Dataquest.

From the above projections, it is evident that theITES-BPO phenomenon can therefore translateinto a very large opportunity for countries such asGhana, which have some of the basic buildingblocks required for becoming an ITES-BPO servic-es destination.

1.2.1 Why ITES-BPO for Ghana?Ghana’s economy remains predominately agrarian,and the sector continues to dominate the labormarket as the main source of employment.However the percentage contribution of the agri-culture sector dropped drastically to 46.6 percentin 2005 from the 1988 figure of 61.12 percent.This drop was determined by examining the levelof economic activity of the various sectors, meas-

ured in terms of percentage f economically activepopulations in each of these sectors.3 percent. Thedrop is partly caused by the declining performanceof the agricultural sector in the 1980s and the1990s, in line with similar trends across the world.The decline in agriculture employment in favor ofindustry and services reflects its declining share inreal GDP as against the increasing share of servicesand industry.4

The service sector has hence emerged as the second-largest source of employment for Ghana and thelargest contributor to GDP, with a contributionincrease in overall GDP from 22.1 percent in 1984to 43 percent in 2004. It consists of sub-sectorssuch as trade-related services, transportation, finan-cial and banking services, public administration,and business services (including the nascent ITES-BPO segment) and employs more than 25 percentof the work force. The Industrial sector, on theother hand, has not really developed in Ghana, being

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 2

2 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

2 Sources: Quarterly Digest of Statistics: Ghana Statistical Service, Government and World Bank Reports, Employment figures from GLSS 3 & 4 and 2000Population Census

3 Sources: Quarterly Digest of Statistics: Ghana Statistical Service, Government and World Bank Reports, Employment figures from GLSS 3 & 4 and 2000Population Census

4 The agricultural sector recorded an average annual growth rate of 2.3 percent between 1984 and 2004 compared with 4.7 percent and 4.8 percent in theindustrial and service sectors respectively

5 Census Data

Figure 1. Sector-wide employment trends in Ghana5

global forecasts for the ITES-BPO sector are pro-vided below by industry researcher Gartner-Dataquest.

From the above projections, it is evident that theITES-BPO phenomenon can therefore translateinto a very large opportunity for countries such asGhana, which have some of the basic buildingblocks required for becoming an ITES-BPO servic-es destination.

1.2.1 Why ITES-BPO for Ghana?Ghana’s economy remains predominately agrarian,and the sector continues to dominate the labormarket as the main source of employment.However the percentage contribution of the agri-culture sector dropped drastically to 46.6 percentin 2005 from the 1988 figure of 61.12 percent.This drop was determined by examining the levelof economic activity of the various sectors, meas-

ured in terms of percentage f economically activepopulations in each of these sectors.3 percent. Thedrop is partly caused by the declining performanceof the agricultural sector in the 1980s and the1990s, in line with similar trends across the world.The decline in agriculture employment in favor ofindustry and services reflects its declining share inreal GDP as against the increasing share of servicesand industry.4

The service sector has hence emerged as the second-largest source of employment for Ghana and thelargest contributor to GDP, with a contributionincrease in overall GDP from 22.1 percent in 1984to 43 percent in 2004. It consists of sub-sectorssuch as trade-related services, transportation, finan-cial and banking services, public administration,and business services (including the nascent ITES-BPO segment) and employs more than 25 percentof the work force. The Industrial sector, on theother hand, has not really developed in Ghana, being

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 2

Executive Summary . 3

the lowest employer, with 16.98 percent economi-cally active population employed by this sector.

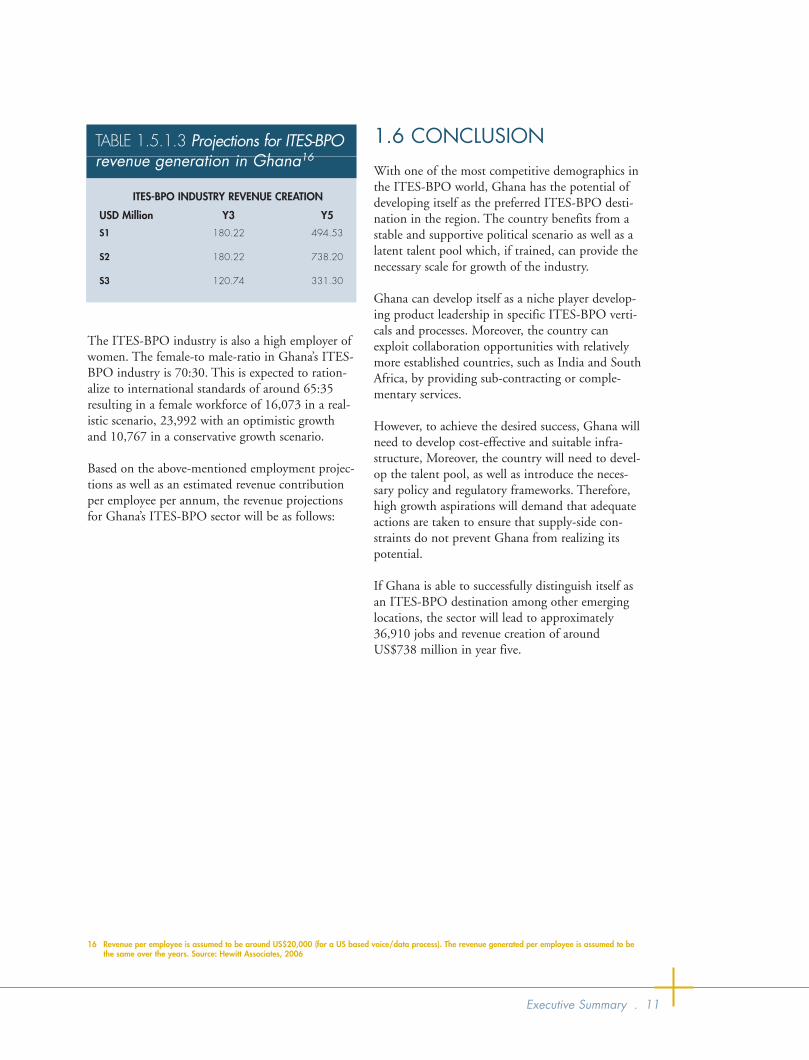

Conclusion: Ghana has entered a phase of acceler-ated economic expansion over the last three years,with real GDP growth averaging 5.2 percent, com-pared to a 20-year average of 4.4 percent. To main-tain and enhance these growth rates, it becomesimperative that service sectors such as ITES-BPObecome the new focus for Ghana because of theirunique potential as harbingers of enhanced job cre-ation and accelerated economic growth. This senti-ment has also been expressed in the Ghana PovertyReduction Strategy which has identified ITES-BPOas one of the non-traditional sectors with thepotential to accelerate economic growth in Ghana.

Some key benefits that this industry can be expectedto bring to Ghana are summarized below:■ Enhanced job creation. As Ghana attains

greater development and maturity in the ITES-BPO sector, it will lead to more jobs, as it is alabor-intensive industry. Here, scale is achievedby the high deployment of people, unlike tradi-tional sectors where growth and development donot imply an increase in jobs.

■ Quick source of revenue. Unlike traditionalsectors of the economy, the ITES-BPO sectorrequires relatively smaller investments in bothtime and funds to set up and start generatingrevenues. Other sectors are structurally slow toestablish, requiring large capital and physicalinfrastructure with high gestation periods. Thismakes it a quick-win for a developing, economi-cally weaker economy such as Ghana.

■ Enhanced foreign direct investment. TheITES-BPO sector is primarily export-oriented.Focusing on this sector can enhance foreigndirect investment into Ghana, which can boostexport earnings, jobs, wages, and skills of theworkforce.

■ Positive spillover effects of the ITES-BPO sector.These include improvements in the informationand communication technology (ICT) infra-structure and business services, which furtherlead to an increase in business opportunities fordomestic companies.

■ Increased female participation in the work-force. One of the most salient features and per-sistent trends in the services industry is theincreased feminization of the labor force andthis is also evidenced in the ITES-BPO sector.

Female participation in the workforce is around44 percent (excluding sales-related sectors) andcan be expected to increase with development ofITES-BPO in Ghana.

■ Improved Performance. A constant focus onperformance metrics such as quality, timeliness,and accountability is a primary characteristic ofthe ITES-BPO industry. Such attributes can, inturn, help Ghanaian firms improve organiza-tional systems and adopt more globally competi-tive and strategic management approaches.Moreover, as such generic skills are portable,they can potentially benefit other sectors of theeconomy.

■ Indirect Employment Impact. The growth ofthe ITES-BPO industry in Ghana will also cre-ate demand for ancillary and support servicesand industries, such as housekeeping, security,catering, transport, language and domain train-ing, telecom and computer equipment provi-sion, maintenance, and real estate. It is estimat-ed that for every direct employment created inthe ITES-BPO sector, four indirect jobs arecreated in other aspects of the economy. Hence,the industry will be able to create large scaleindirect employment opportunities for the lessskilled and less educated

1.3 KEY FINDINGS ANDRECOMMENDATIONS OF OUR STUDY

1.3.1 Strengths, Weaknesses,Opportunities, and Threats (SWOT)Analysis for Ghana as an ITES-BPODestinationWe have studied Ghana’s current positioningunder each of the classifications of the HewittFive Driver Model, namely People, Infrastructure,Environment, Incumbents and Clusters. Ouranalytical framework for conducting the bench-marking aspects of this project is built upon thesefive drivers. Each of these drivers is further bro-ken down into factors, parameters, and elementsto comprehensively analyze each aspect.

Weights were assigned to each driver and parameterlevel to get the overall scores for comparator coun-tries both at regional and international levels. These

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 3

Executive Summary . 3

the lowest employer, with 16.98 percent economi-cally active population employed by this sector.

Conclusion: Ghana has entered a phase of acceler-ated economic expansion over the last three years,with real GDP growth averaging 5.2 percent, com-pared to a 20-year average of 4.4 percent. To main-tain and enhance these growth rates, it becomesimperative that service sectors such as ITES-BPObecome the new focus for Ghana because of theirunique potential as harbingers of enhanced job cre-ation and accelerated economic growth. This senti-ment has also been expressed in the Ghana PovertyReduction Strategy which has identified ITES-BPOas one of the non-traditional sectors with thepotential to accelerate economic growth in Ghana.

Some key benefits that this industry can be expectedto bring to Ghana are summarized below:■ Enhanced job creation. As Ghana attains

greater development and maturity in the ITES-BPO sector, it will lead to more jobs, as it is alabor-intensive industry. Here, scale is achievedby the high deployment of people, unlike tradi-tional sectors where growth and development donot imply an increase in jobs.

■ Quick source of revenue. Unlike traditionalsectors of the economy, the ITES-BPO sectorrequires relatively smaller investments in bothtime and funds to set up and start generatingrevenues. Other sectors are structurally slow toestablish, requiring large capital and physicalinfrastructure with high gestation periods. Thismakes it a quick-win for a developing, economi-cally weaker economy such as Ghana.

■ Enhanced foreign direct investment. TheITES-BPO sector is primarily export-oriented.Focusing on this sector can enhance foreigndirect investment into Ghana, which can boostexport earnings, jobs, wages, and skills of theworkforce.

■ Positive spillover effects of the ITES-BPO sector.These include improvements in the informationand communication technology (ICT) infra-structure and business services, which furtherlead to an increase in business opportunities fordomestic companies.

■ Increased female participation in the work-force. One of the most salient features and per-sistent trends in the services industry is theincreased feminization of the labor force andthis is also evidenced in the ITES-BPO sector.

Female participation in the workforce is around44 percent (excluding sales-related sectors) andcan be expected to increase with development ofITES-BPO in Ghana.

■ Improved Performance. A constant focus onperformance metrics such as quality, timeliness,and accountability is a primary characteristic ofthe ITES-BPO industry. Such attributes can, inturn, help Ghanaian firms improve organiza-tional systems and adopt more globally competi-tive and strategic management approaches.Moreover, as such generic skills are portable,they can potentially benefit other sectors of theeconomy.

■ Indirect Employment Impact. The growth ofthe ITES-BPO industry in Ghana will also cre-ate demand for ancillary and support servicesand industries, such as housekeeping, security,catering, transport, language and domain train-ing, telecom and computer equipment provi-sion, maintenance, and real estate. It is estimat-ed that for every direct employment created inthe ITES-BPO sector, four indirect jobs arecreated in other aspects of the economy. Hence,the industry will be able to create large scaleindirect employment opportunities for the lessskilled and less educated

1.3 KEY FINDINGS ANDRECOMMENDATIONS OF OUR STUDY

1.3.1 Strengths, Weaknesses,Opportunities, and Threats (SWOT)Analysis for Ghana as an ITES-BPODestinationWe have studied Ghana’s current positioningunder each of the classifications of the HewittFive Driver Model, namely People, Infrastructure,Environment, Incumbents and Clusters. Ouranalytical framework for conducting the bench-marking aspects of this project is built upon thesefive drivers. Each of these drivers is further bro-ken down into factors, parameters, and elementsto comprehensively analyze each aspect.

Weights were assigned to each driver and parameterlevel to get the overall scores for comparator coun-tries both at regional and international levels. These

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 3

4 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

were—People Driver—40 percent; Infrastructure—30 percent; Environment—20 percent andIncumbents—10 percent. Overall, Ghana wasplaced in the 10th position with respect to thesecountries.

Ghana’s positioning across these Drivers was bench-marked with respect to that of five leading andupcoming International ITES-BPO destinations(India, China, Philippines, Romania and Mexico)as well as six regional emerging or potential ITES-BPO destinations (South Africa, Egypt, Mauritius,Botswana, Nigeria and Senegal). In addition to theabove, we had several interactions with stakeholders,including incumbent organizations during thecourse of the study.

Based on our findings from the international bench-marking and an analysis of the development ofGhana’s ITES-BPO sector, we have identified theoverall SWOT for Ghana and made recommenda-tions that will help facilitate the growth of the sector.

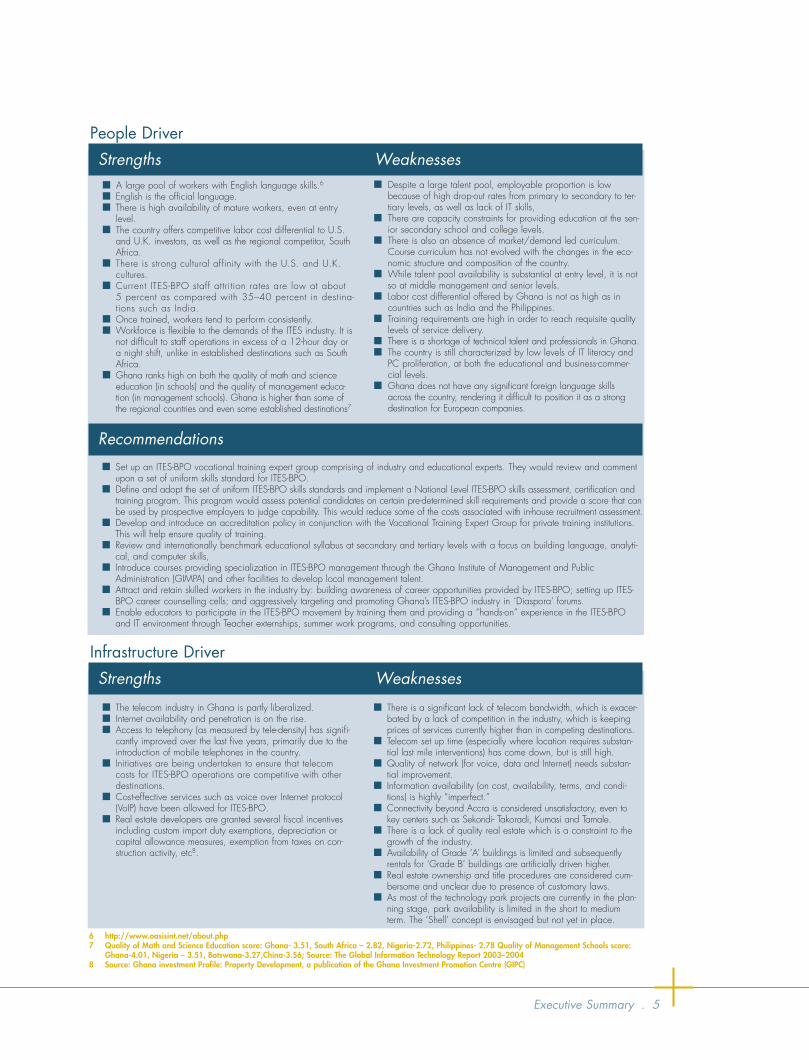

1.3.2 People DriverHuman resources are a key differentiator of thecapability of a location to attract and sustain a par-ticular industry. The ITES-BPO sector is especiallylabor intensive and dependent on talent. To succeedin this sector, Ghana would require availability of

an abundant, low-cost, efficient, and suitable tal-ent pool. The following table addresses thestrengths and weaknesses of Ghana under thePeople Driver and provides recommendations fordeveloping the same with regards to the ITES-BPOindustry.

1.3.3 Infrastructure DriverAvailability of reliable infrastructure is anothercritical aspect for ITES-BPO establishments. Theindustry is heavily dependent on real time connec-tivity, with high demand for a robust telecom andpower infrastructure. Civic amenities such as goodroads, transportation systems, etc., make it easierfor companies to do business out of a particularlocation. The following table includes strengthsand weaknesses of Ghana under the InfrastructureDriver and provides recommendations for develop-ing it with regards to the ITES-BPO industry.

1.3.4 Environment DriverExternal environment refers to the legal and regula-tory setup. The attitude and support of governmentand other related administrative bodies in terms ofpolicies, procedures, ease of getting approvals,incentives, exemptions, special benefits, ease of han-dling, etc, are relevant in reducing the ‘pain-points’of doing business in a particular location. The fol-lowing table addresses the strengths and weaknesses

■ Large pool of potentially good English speaking population.■ Competitive labor costs differential to U.S. and U.K. companies.■ Stable geo-political environment in comparison with neighbor-

ing as well as other countries worldwide.■ ITES-BPO sector identified as a focus areas for economic

development by the government. ■ Availability and penetration of telecom and Internet services

are rising.■ Several investor-friendly policies including tax holidays, 100

percent foreign ownership are in place.■ Cyber laws to protect ITES-BPO investors are in the process

of being promulgated.

■ Employability in the context of the ITES-BPO industry of large tal-ent pool is proportionately low.

■ Inadequate education infrastructure and training facilities.■ Low levels of IT literacy and PC proliferation at educational and

business-commercial levels.■ Although infrastructure costs may be lower in comparison with

some countries, there is a lack of suitable telecommunications andquality real estate infrastructure, which is a bottleneck for investors.

■ High inflation and interest rates, despite recent decreases.■ No policies or incentives specifically for the ITES-BPO sector.■ Low level of incumbent presence in spite of early offshoring

activity (ACS.)

Strengths Weaknesses

■ Leverage the image of its democratic and relatively stablepolitical environment towards establishing itself as a regionalhub for offshoring services.

■ Establish itself as a subcontracting hub for more establisheddestinations.

■ Collaborate with countries such as South Africa and offercomplementary services.

■ Develop offerings such as medical transcription and dataprocessing in the short and medium term.

■ Proactive investment promotion of the ITES-BPO industry by com-peting regional destinations, such as Nigeria, Mauritius,Botswana.

■ Lack of development of necessary educational and traininginfrastructure resulting in limited scalability for the industry.

Opportunities Threats

SWOT Analysis for Ghana as an ITES-BPO Destination

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 4

4 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

were—People Driver—40 percent; Infrastructure—30 percent; Environment—20 percent andIncumbents—10 percent. Overall, Ghana wasplaced in the 10th position with respect to thesecountries.

Ghana’s positioning across these Drivers was bench-marked with respect to that of five leading andupcoming International ITES-BPO destinations(India, China, Philippines, Romania and Mexico)as well as six regional emerging or potential ITES-BPO destinations (South Africa, Egypt, Mauritius,Botswana, Nigeria and Senegal). In addition to theabove, we had several interactions with stakeholders,including incumbent organizations during thecourse of the study.

Based on our findings from the international bench-marking and an analysis of the development ofGhana’s ITES-BPO sector, we have identified theoverall SWOT for Ghana and made recommenda-tions that will help facilitate the growth of the sector.

1.3.2 People DriverHuman resources are a key differentiator of thecapability of a location to attract and sustain a par-ticular industry. The ITES-BPO sector is especiallylabor intensive and dependent on talent. To succeedin this sector, Ghana would require availability of

an abundant, low-cost, efficient, and suitable tal-ent pool. The following table addresses thestrengths and weaknesses of Ghana under thePeople Driver and provides recommendations fordeveloping the same with regards to the ITES-BPOindustry.

1.3.3 Infrastructure DriverAvailability of reliable infrastructure is anothercritical aspect for ITES-BPO establishments. Theindustry is heavily dependent on real time connec-tivity, with high demand for a robust telecom andpower infrastructure. Civic amenities such as goodroads, transportation systems, etc., make it easierfor companies to do business out of a particularlocation. The following table includes strengthsand weaknesses of Ghana under the InfrastructureDriver and provides recommendations for develop-ing it with regards to the ITES-BPO industry.

1.3.4 Environment DriverExternal environment refers to the legal and regula-tory setup. The attitude and support of governmentand other related administrative bodies in terms ofpolicies, procedures, ease of getting approvals,incentives, exemptions, special benefits, ease of han-dling, etc, are relevant in reducing the ‘pain-points’of doing business in a particular location. The fol-lowing table addresses the strengths and weaknesses

■ Large pool of potentially good English speaking population.■ Competitive labor costs differential to U.S. and U.K. companies.■ Stable geo-political environment in comparison with neighbor-

ing as well as other countries worldwide.■ ITES-BPO sector identified as a focus areas for economic

development by the government. ■ Availability and penetration of telecom and Internet services

are rising.■ Several investor-friendly policies including tax holidays, 100

percent foreign ownership are in place.■ Cyber laws to protect ITES-BPO investors are in the process

of being promulgated.

■ Employability in the context of the ITES-BPO industry of large tal-ent pool is proportionately low.

■ Inadequate education infrastructure and training facilities.■ Low levels of IT literacy and PC proliferation at educational and

business-commercial levels.■ Although infrastructure costs may be lower in comparison with

some countries, there is a lack of suitable telecommunications andquality real estate infrastructure, which is a bottleneck for investors.

■ High inflation and interest rates, despite recent decreases.■ No policies or incentives specifically for the ITES-BPO sector.■ Low level of incumbent presence in spite of early offshoring

activity (ACS.)

Strengths Weaknesses

■ Leverage the image of its democratic and relatively stablepolitical environment towards establishing itself as a regionalhub for offshoring services.

■ Establish itself as a subcontracting hub for more establisheddestinations.

■ Collaborate with countries such as South Africa and offercomplementary services.

■ Develop offerings such as medical transcription and dataprocessing in the short and medium term.

■ Proactive investment promotion of the ITES-BPO industry by com-peting regional destinations, such as Nigeria, Mauritius,Botswana.

■ Lack of development of necessary educational and traininginfrastructure resulting in limited scalability for the industry.

Opportunities Threats

SWOT Analysis for Ghana as an ITES-BPO Destination

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 4

Executive Summary . 5

■ A large pool of workers with English language skills.6■ English is the official language. ■ There is high availability of mature workers, even at entry

level.■ The country offers competitive labor cost differential to U.S.

and U.K. investors, as well as the regional competitor, SouthAfrica.

■ There is strong cultural affinity with the U.S. and U.K.cultures.

■ Current ITES-BPO staff attrition rates are low at about5 percent as compared with 35–40 percent in destina-tions such as India.

■ Once trained, workers tend to perform consistently.■ Workforce is flexible to the demands of the ITES industry. It is

not difficult to staff operations in excess of a 12-hour day ora night shift, unlike in established destinations such as SouthAfrica.

■ Ghana ranks high on both the quality of math and scienceeducation (in schools) and the quality of management educa-tion (in management schools). Ghana is higher than some ofthe regional countries and even some established destinations7

■ Despite a large talent pool, employable proportion is lowbecause of high drop-out rates from primary to secondary to ter-tiary levels, as well as lack of IT skills,

■ There are capacity constraints for providing education at the sen-ior secondary school and college levels.

■ There is also an absence of market/demand led curriculum.Course curriculum has not evolved with the changes in the eco-nomic structure and composition of the country.

■ While talent pool availability is substantial at entry level, it is notso at middle management and senior levels.

■ Labor cost differential offered by Ghana is not as high as incountries such as India and the Philippines.

■ Training requirements are high in order to reach requisite qualitylevels of service delivery.

■ There is a shortage of technical talent and professionals in Ghana.■ The country is still characterized by low levels of IT literacy and

PC proliferation, at both the educational and business-commer-cial levels.

■ Ghana does not have any significant foreign language skillsacross the country, rendering it difficult to position it as a strongdestination for European companies.

Strengths Weaknesses

■ The telecom industry in Ghana is partly liberalized.■ Internet availability and penetration is on the rise.■ Access to telephony (as measured by tele-density) has signifi-

cantly improved over the last five years, primarily due to theintroduction of mobile telephones in the country.

■ Initiatives are being undertaken to ensure that telecomcosts for ITES-BPO operations are competitive with otherdestinations.

■ Cost-effective services such as voice over Internet protocol(VoIP) have been allowed for ITES-BPO.

■ Real estate developers are granted several fiscal incentivesincluding custom import duty exemptions, depreciation orcapital allowance measures, exemption from taxes on con-struction activity, etc8.

■ There is a significant lack of telecom bandwidth, which is exacer-bated by a lack of competition in the industry, which is keepingprices of services currently higher than in competing destinations.

■ Telecom set up time (especially where location requires substan-tial last mile interventions) has come down, but is still high.

■ Quality of network (for voice, data and Internet) needs substan-tial improvement.

■ Information availability (on cost, availability, terms, and condi-tions) is highly “imperfect.”

■ Connectivity beyond Accra is considered unsatisfactory, even tokey centers such as Sekondi- Takoradi, Kumasi and Tamale.

■ There is a lack of quality real estate which is a constraint to thegrowth of the industry.

■ Availability of Grade ‘A’ buildings is limited and subsequentlyrentals for ‘Grade B’ buildings are artificially driven higher.

■ Real estate ownership and title procedures are considered cum-bersome and unclear due to presence of customary laws.

■ As most of the technology park projects are currently in the plan-ning stage, park availability is limited in the short to mediumterm. The ‘Shell’ concept is envisaged but not yet in place.

Strengths Weaknesses

6 http://www.oasisint.net/about.php7 Quality of Math and Science Education score: Ghana- 3.51, South Africa – 2.82, Nigeria-2.72, Philippines- 2.78 Quality of Management Schools score:

Ghana-4.01, Nigeria – 3.51, Botswana-3.27,China-3.56; Source: The Global Information Technology Report 2003–20048 Source: Ghana investment Profile: Property Development, a publication of the Ghana Investment Promotion Centre (GIPC)

People Driver

Recommendations■ Set up an ITES-BPO vocational training expert group comprising of industry and educational experts. They would review and comment

upon a set of uniform skills standard for ITES-BPO.■ Define and adopt the set of uniform ITES-BPO skills standards and implement a National Level ITES-BPO skills assessment, certification and

training program. This program would assess potential candidates on certain pre-determined skill requirements and provide a score that canbe used by prospective employers to judge capability. This would reduce some of the costs associated with in-house recruitment assessment.

■ Develop and introduce an accreditation policy in conjunction with the Vocational Training Expert Group for private training institutions.This will help ensure quality of training.

■ Review and internationally benchmark educational syllabus at secondary and tertiary levels with a focus on building language, analyti-cal, and computer skills,

■ Introduce courses providing specialization in ITES-BPO management through the Ghana Institute of Management and PublicAdministration (GIMPA) and other facilities to develop local management talent.

■ Attract and retain skilled workers in the industry by: building awareness of career opportunities provided by ITES-BPO; setting up ITES-BPO career counselling cells; and aggressively targeting and promoting Ghana’s ITES-BPO industry in `Diaspora’ forums.

■ Enable educators to participate in the ITES-BPO movement by training them and providing a “hands-on” experience in the ITES-BPOand IT environment through Teacher externships, summer work programs, and consulting opportunities.

Infrastructure Driver

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 5

Executive Summary . 5

■ A large pool of workers with English language skills.6■ English is the official language. ■ There is high availability of mature workers, even at entry

level.■ The country offers competitive labor cost differential to U.S.

and U.K. investors, as well as the regional competitor, SouthAfrica.

■ There is strong cultural affinity with the U.S. and U.K.cultures.

■ Current ITES-BPO staff attrition rates are low at about5 percent as compared with 35–40 percent in destina-tions such as India.

■ Once trained, workers tend to perform consistently.■ Workforce is flexible to the demands of the ITES industry. It is

not difficult to staff operations in excess of a 12-hour day ora night shift, unlike in established destinations such as SouthAfrica.

■ Ghana ranks high on both the quality of math and scienceeducation (in schools) and the quality of management educa-tion (in management schools). Ghana is higher than some ofthe regional countries and even some established destinations7

■ Despite a large talent pool, employable proportion is lowbecause of high drop-out rates from primary to secondary to ter-tiary levels, as well as lack of IT skills,

■ There are capacity constraints for providing education at the sen-ior secondary school and college levels.

■ There is also an absence of market/demand led curriculum.Course curriculum has not evolved with the changes in the eco-nomic structure and composition of the country.

■ While talent pool availability is substantial at entry level, it is notso at middle management and senior levels.

■ Labor cost differential offered by Ghana is not as high as incountries such as India and the Philippines.

■ Training requirements are high in order to reach requisite qualitylevels of service delivery.

■ There is a shortage of technical talent and professionals in Ghana.■ The country is still characterized by low levels of IT literacy and

PC proliferation, at both the educational and business-commer-cial levels.

■ Ghana does not have any significant foreign language skillsacross the country, rendering it difficult to position it as a strongdestination for European companies.

Strengths Weaknesses

■ The telecom industry in Ghana is partly liberalized.■ Internet availability and penetration is on the rise.■ Access to telephony (as measured by tele-density) has signifi-

cantly improved over the last five years, primarily due to theintroduction of mobile telephones in the country.

■ Initiatives are being undertaken to ensure that telecomcosts for ITES-BPO operations are competitive with otherdestinations.

■ Cost-effective services such as voice over Internet protocol(VoIP) have been allowed for ITES-BPO.

■ Real estate developers are granted several fiscal incentivesincluding custom import duty exemptions, depreciation orcapital allowance measures, exemption from taxes on con-struction activity, etc8.

■ There is a significant lack of telecom bandwidth, which is exacer-bated by a lack of competition in the industry, which is keepingprices of services currently higher than in competing destinations.

■ Telecom set up time (especially where location requires substan-tial last mile interventions) has come down, but is still high.

■ Quality of network (for voice, data and Internet) needs substan-tial improvement.

■ Information availability (on cost, availability, terms, and condi-tions) is highly “imperfect.”

■ Connectivity beyond Accra is considered unsatisfactory, even tokey centers such as Sekondi- Takoradi, Kumasi and Tamale.

■ There is a lack of quality real estate which is a constraint to thegrowth of the industry.

■ Availability of Grade ‘A’ buildings is limited and subsequentlyrentals for ‘Grade B’ buildings are artificially driven higher.

■ Real estate ownership and title procedures are considered cum-bersome and unclear due to presence of customary laws.

■ As most of the technology park projects are currently in the plan-ning stage, park availability is limited in the short to mediumterm. The ‘Shell’ concept is envisaged but not yet in place.

Strengths Weaknesses

6 http://www.oasisint.net/about.php7 Quality of Math and Science Education score: Ghana- 3.51, South Africa – 2.82, Nigeria-2.72, Philippines- 2.78 Quality of Management Schools score:

Ghana-4.01, Nigeria – 3.51, Botswana-3.27,China-3.56; Source: The Global Information Technology Report 2003–20048 Source: Ghana investment Profile: Property Development, a publication of the Ghana Investment Promotion Centre (GIPC)

People Driver

Recommendations■ Set up an ITES-BPO vocational training expert group comprising of industry and educational experts. They would review and comment

upon a set of uniform skills standard for ITES-BPO.■ Define and adopt the set of uniform ITES-BPO skills standards and implement a National Level ITES-BPO skills assessment, certification and

training program. This program would assess potential candidates on certain pre-determined skill requirements and provide a score that canbe used by prospective employers to judge capability. This would reduce some of the costs associated with in-house recruitment assessment.

■ Develop and introduce an accreditation policy in conjunction with the Vocational Training Expert Group for private training institutions.This will help ensure quality of training.

■ Review and internationally benchmark educational syllabus at secondary and tertiary levels with a focus on building language, analyti-cal, and computer skills,

■ Introduce courses providing specialization in ITES-BPO management through the Ghana Institute of Management and PublicAdministration (GIMPA) and other facilities to develop local management talent.

■ Attract and retain skilled workers in the industry by: building awareness of career opportunities provided by ITES-BPO; setting up ITES-BPO career counselling cells; and aggressively targeting and promoting Ghana’s ITES-BPO industry in `Diaspora’ forums.

■ Enable educators to participate in the ITES-BPO movement by training them and providing a “hands-on” experience in the ITES-BPOand IT environment through Teacher externships, summer work programs, and consulting opportunities.

Infrastructure Driver

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 5

6 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

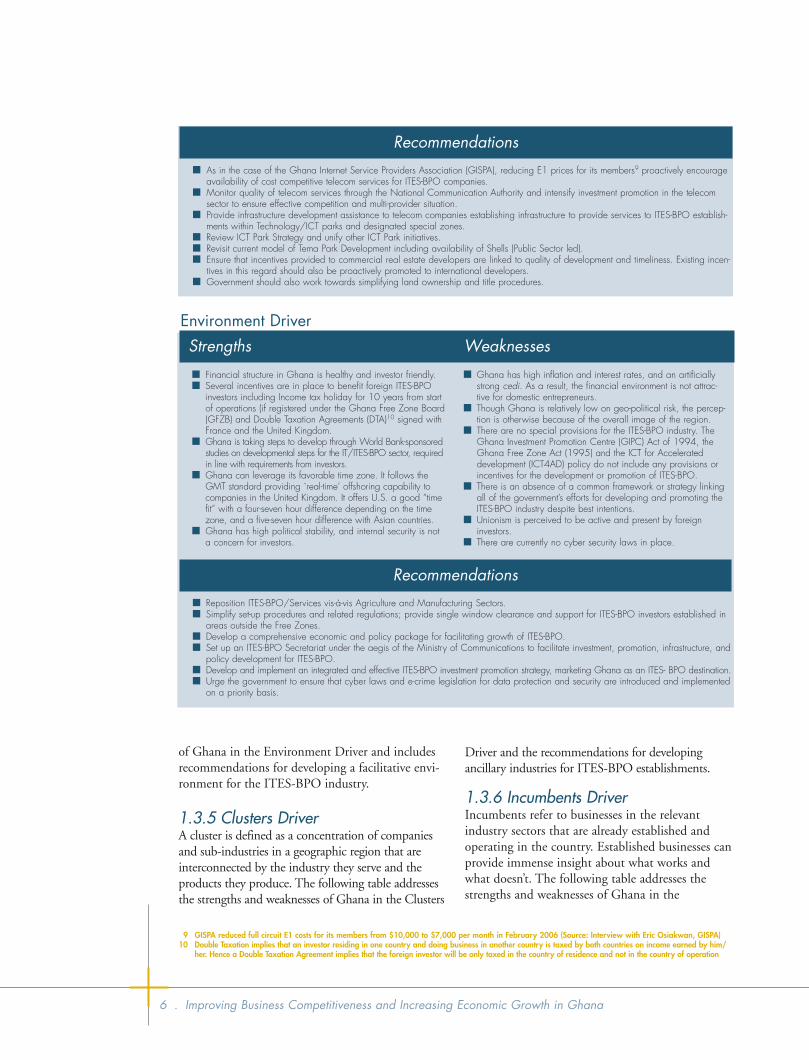

of Ghana in the Environment Driver and includesrecommendations for developing a facilitative envi-ronment for the ITES-BPO industry.

1.3.5 Clusters DriverA cluster is defined as a concentration of companiesand sub-industries in a geographic region that areinterconnected by the industry they serve and theproducts they produce. The following table addressesthe strengths and weaknesses of Ghana in the Clusters

Driver and the recommendations for developingancillary industries for ITES-BPO establishments.

1.3.6 Incumbents DriverIncumbents refer to businesses in the relevantindustry sectors that are already established andoperating in the country. Established businesses canprovide immense insight about what works andwhat doesn’t. The following table addresses thestrengths and weaknesses of Ghana in the

Recommendations■ As in the case of the Ghana Internet Service Providers Association (GISPA), reducing E1 prices for its members9 proactively encourage

availability of cost competitive telecom services for ITES-BPO companies. ■ Monitor quality of telecom services through the National Communication Authority and intensify investment promotion in the telecom

sector to ensure effective competition and multi-provider situation.■ Provide infrastructure development assistance to telecom companies establishing infrastructure to provide services to ITES-BPO establish-

ments within Technology/ICT parks and designated special zones.■ Review ICT Park Strategy and unify other ICT Park initiatives.■ Revisit current model of Tema Park Development including availability of Shells (Public Sector led).■ Ensure that incentives provided to commercial real estate developers are linked to quality of development and timeliness. Existing incen-

tives in this regard should also be proactively promoted to international developers. ■ Government should also work towards simplifying land ownership and title procedures.

■ Financial structure in Ghana is healthy and investor friendly.■ Several incentives are in place to benefit foreign ITES-BPO

investors including Income tax holiday for 10 years from startof operations (if registered under the Ghana Free Zone Board(GFZB) and Double Taxation Agreements (DTA)10 signed withFrance and the United Kingdom.

■ Ghana is taking steps to develop through World Bank-sponsoredstudies on developmental steps for the IT/ITES-BPO sector, requiredin line with requirements from investors.

■ Ghana can leverage its favorable time zone. It follows theGMT standard providing `real-time’ offshoring capability tocompanies in the United Kingdom. It offers U.S. a good “timefit” with a four-seven hour difference depending on the timezone, and a five-seven hour difference with Asian countries.

■ Ghana has high political stability, and internal security is nota concern for investors.

■ Ghana has high inflation and interest rates, and an artificiallystrong cedi. As a result, the financial environment is not attrac-tive for domestic entrepreneurs.

■ Though Ghana is relatively low on geo-political risk, the percep-tion is otherwise because of the overall image of the region.

■ There are no special provisions for the ITES-BPO industry. TheGhana Investment Promotion Centre (GIPC) Act of 1994, theGhana Free Zone Act (1995) and the ICT for Accelerateddevelopment (ICT4AD) policy do not include any provisions orincentives for the development or promotion of ITES-BPO.

■ There is an absence of a common framework or strategy linkingall of the government’s efforts for developing and promoting theITES-BPO industry despite best intentions.

■ Unionism is perceived to be active and present by foreigninvestors.

■ There are currently no cyber security laws in place.

Recommendations■ Reposition ITES-BPO/Services vis-à-vis Agriculture and Manufacturing Sectors.■ Simplify set-up procedures and related regulations; provide single window clearance and support for ITES-BPO investors established in

areas outside the Free Zones. ■ Develop a comprehensive economic and policy package for facilitating growth of ITES-BPO.■ Set up an ITES-BPO Secretariat under the aegis of the Ministry of Communications to facilitate investment, promotion, infrastructure, and

policy development for ITES-BPO.■ Develop and implement an integrated and effective ITES-BPO investment promotion strategy, marketing Ghana as an ITES- BPO destination.■ Urge the government to ensure that cyber laws and e-crime legislation for data protection and security are introduced and implemented

on a priority basis.

Strengths Weaknesses

9 GISPA reduced full circuit E1 costs for its members from $10,000 to $7,000 per month in February 2006 (Source: Interview with Eric Osiakwan, GISPA)10 Double Taxation implies that an investor residing in one country and doing business in another country is taxed by both countries on income earned by him/

her. Hence a Double Taxation Agreement implies that the foreign investor will be only taxed in the country of residence and not in the country of operation

Environment Driver

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 6

6 . Improving Business Competitiveness and Increasing Economic Growth in Ghana

of Ghana in the Environment Driver and includesrecommendations for developing a facilitative envi-ronment for the ITES-BPO industry.

1.3.5 Clusters DriverA cluster is defined as a concentration of companiesand sub-industries in a geographic region that areinterconnected by the industry they serve and theproducts they produce. The following table addressesthe strengths and weaknesses of Ghana in the Clusters

Driver and the recommendations for developingancillary industries for ITES-BPO establishments.

1.3.6 Incumbents DriverIncumbents refer to businesses in the relevantindustry sectors that are already established andoperating in the country. Established businesses canprovide immense insight about what works andwhat doesn’t. The following table addresses thestrengths and weaknesses of Ghana in the

Recommendations■ As in the case of the Ghana Internet Service Providers Association (GISPA), reducing E1 prices for its members9 proactively encourage

availability of cost competitive telecom services for ITES-BPO companies. ■ Monitor quality of telecom services through the National Communication Authority and intensify investment promotion in the telecom

sector to ensure effective competition and multi-provider situation.■ Provide infrastructure development assistance to telecom companies establishing infrastructure to provide services to ITES-BPO establish-

ments within Technology/ICT parks and designated special zones.■ Review ICT Park Strategy and unify other ICT Park initiatives.■ Revisit current model of Tema Park Development including availability of Shells (Public Sector led).■ Ensure that incentives provided to commercial real estate developers are linked to quality of development and timeliness. Existing incen-

tives in this regard should also be proactively promoted to international developers. ■ Government should also work towards simplifying land ownership and title procedures.

■ Financial structure in Ghana is healthy and investor friendly.■ Several incentives are in place to benefit foreign ITES-BPO

investors including Income tax holiday for 10 years from startof operations (if registered under the Ghana Free Zone Board(GFZB) and Double Taxation Agreements (DTA)10 signed withFrance and the United Kingdom.

■ Ghana is taking steps to develop through World Bank-sponsoredstudies on developmental steps for the IT/ITES-BPO sector, requiredin line with requirements from investors.

■ Ghana can leverage its favorable time zone. It follows theGMT standard providing `real-time’ offshoring capability tocompanies in the United Kingdom. It offers U.S. a good “timefit” with a four-seven hour difference depending on the timezone, and a five-seven hour difference with Asian countries.

■ Ghana has high political stability, and internal security is nota concern for investors.

■ Ghana has high inflation and interest rates, and an artificiallystrong cedi. As a result, the financial environment is not attrac-tive for domestic entrepreneurs.

■ Though Ghana is relatively low on geo-political risk, the percep-tion is otherwise because of the overall image of the region.

■ There are no special provisions for the ITES-BPO industry. TheGhana Investment Promotion Centre (GIPC) Act of 1994, theGhana Free Zone Act (1995) and the ICT for Accelerateddevelopment (ICT4AD) policy do not include any provisions orincentives for the development or promotion of ITES-BPO.

■ There is an absence of a common framework or strategy linkingall of the government’s efforts for developing and promoting theITES-BPO industry despite best intentions.

■ Unionism is perceived to be active and present by foreigninvestors.

■ There are currently no cyber security laws in place.

Recommendations■ Reposition ITES-BPO/Services vis-à-vis Agriculture and Manufacturing Sectors.■ Simplify set-up procedures and related regulations; provide single window clearance and support for ITES-BPO investors established in

areas outside the Free Zones. ■ Develop a comprehensive economic and policy package for facilitating growth of ITES-BPO.■ Set up an ITES-BPO Secretariat under the aegis of the Ministry of Communications to facilitate investment, promotion, infrastructure, and

policy development for ITES-BPO.■ Develop and implement an integrated and effective ITES-BPO investment promotion strategy, marketing Ghana as an ITES- BPO destination.■ Urge the government to ensure that cyber laws and e-crime legislation for data protection and security are introduced and implemented

on a priority basis.

Strengths Weaknesses

9 GISPA reduced full circuit E1 costs for its members from $10,000 to $7,000 per month in February 2006 (Source: Interview with Eric Osiakwan, GISPA)10 Double Taxation implies that an investor residing in one country and doing business in another country is taxed by both countries on income earned by him/

her. Hence a Double Taxation Agreement implies that the foreign investor will be only taxed in the country of residence and not in the country of operation

Environment Driver

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 6

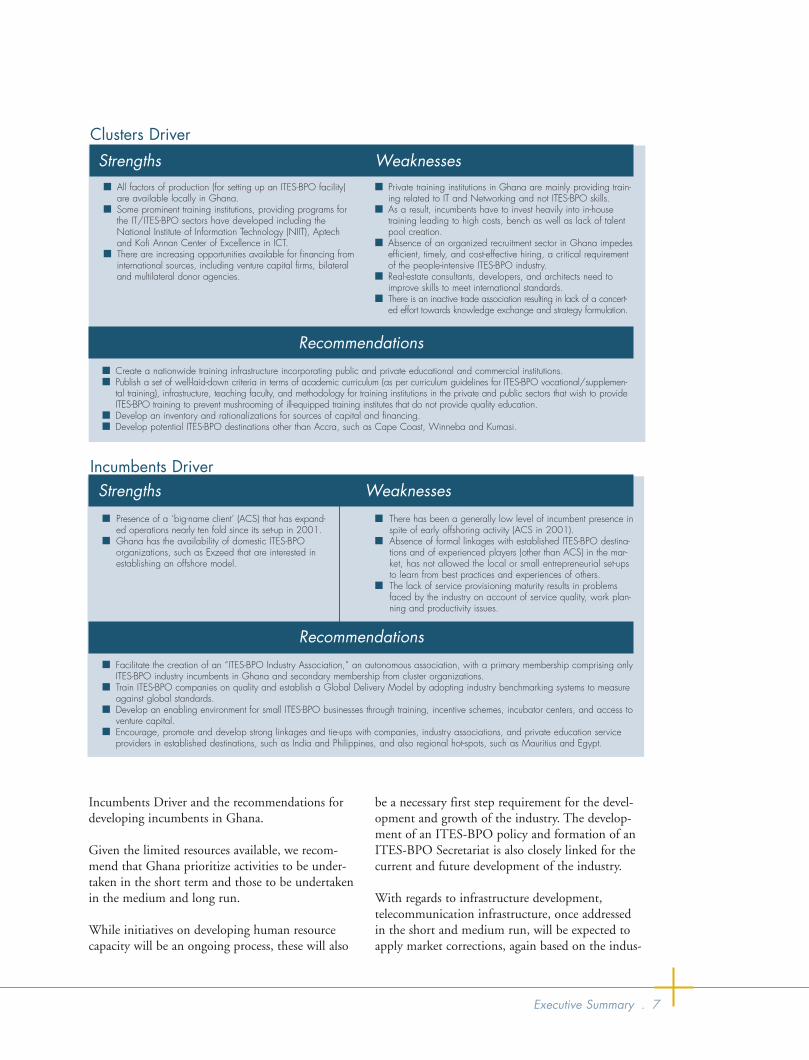

Incumbents Driver and the recommendations fordeveloping incumbents in Ghana.

Given the limited resources available, we recom-mend that Ghana prioritize activities to be under-taken in the short term and those to be undertakenin the medium and long run.

While initiatives on developing human resourcecapacity will be an ongoing process, these will also

be a necessary first step requirement for the devel-opment and growth of the industry. The develop-ment of an ITES-BPO policy and formation of anITES-BPO Secretariat is also closely linked for thecurrent and future development of the industry.

With regards to infrastructure development,telecommunication infrastructure, once addressedin the short and medium run, will be expected toapply market corrections, again based on the indus-

■ All factors of production (for setting up an ITES-BPO facility)are available locally in Ghana.

■ Some prominent training institutions, providing programs forthe IT/ITES-BPO sectors have developed including theNational Institute of Information Technology (NIIT), Aptechand Kofi Annan Center of Excellence in ICT.

■ There are increasing opportunities available for financing frominternational sources, including venture capital firms, bilateraland multilateral donor agencies.

■ Private training institutions in Ghana are mainly providing train-ing related to IT and Networking and not ITES-BPO skills.

■ As a result, incumbents have to invest heavily into in-housetraining leading to high costs, bench as well as lack of talentpool creation.

■ Absence of an organized recruitment sector in Ghana impedesefficient, timely, and cost-effective hiring, a critical requirementof the people-intensive ITES-BPO industry.

■ Real-estate consultants, developers, and architects need toimprove skills to meet international standards.

■ There is an inactive trade association resulting in lack of a concert-ed effort towards knowledge exchange and strategy formulation.

Recommendations■ Create a nationwide training infrastructure incorporating public and private educational and commercial institutions.■ Publish a set of well-laid-down criteria in terms of academic curriculum (as per curriculum guidelines for ITES-BPO vocational/supplemen-

tal training), infrastructure, teaching faculty, and methodology for training institutions in the private and public sectors that wish to provideITES-BPO training to prevent mushrooming of ill-equipped training institutes that do not provide quality education.

■ Develop an inventory and rationalizations for sources of capital and financing.■ Develop potential ITES-BPO destinations other than Accra, such as Cape Coast, Winneba and Kumasi.

Strengths Weaknesses

■ Presence of a `big-name client’ (ACS) that has expand-ed operations nearly ten fold since its set-up in 2001.

■ Ghana has the availability of domestic ITES-BPOorganizations, such as Exzeed that are interested inestablishing an offshore model.

■ There has been a generally low level of incumbent presence inspite of early offshoring activity (ACS in 2001).

■ Absence of formal linkages with established ITES-BPO destina-tions and of experienced players (other than ACS) in the mar-ket, has not allowed the local or small entrepreneurial set-upsto learn from best practices and experiences of others.

■ The lack of service provisioning maturity results in problemsfaced by the industry on account of service quality, work plan-ning and productivity issues.

Recommendations■ Facilitate the creation of an “ITES-BPO Industry Association,” an autonomous association, with a primary membership comprising only

ITES-BPO industry incumbents in Ghana and secondary membership from cluster organizations. ■ Train ITES-BPO companies on quality and establish a Global Delivery Model by adopting industry benchmarking systems to measure

against global standards.■ Develop an enabling environment for small ITES-BPO businesses through training, incentive schemes, incubator centers, and access to

venture capital.■ Encourage, promote and develop strong linkages and tie-ups with companies, industry associations, and private education service

providers in established destinations, such as India and Philippines, and also regional hot-spots, such as Mauritius and Egypt.

Strengths Weaknesses

Executive Summary . 7

Clusters Driver

Incumbents Driver

WB Ghana text 2-27-07.qxd 2/27/07 11:11 AM Page 7

Incumbents Driver and the recommendations fordeveloping incumbents in Ghana.

Given the limited resources available, we recom-mend that Ghana prioritize activities to be under-taken in the short term and those to be undertakenin the medium and long run.

While initiatives on developing human resourcecapacity will be an ongoing process, these will also

be a necessary first step requirement for the devel-opment and growth of the industry. The develop-ment of an ITES-BPO policy and formation of anITES-BPO Secretariat is also closely linked for thecurrent and future development of the industry.