Embed Size (px)

Citation preview

Signs of a structural

improvement in airlines’

financial health?

February 2016

Brian Pearce

Chief Economist

International Air Transport Association

Structural not cyclical gains (or just cheap fuel)?

Source: ICAO, McKinsey, EIU, IATA 2 www.iata.org/economics

-4

-2

0

2

4

6

8

-6

-4

-2

0

2

4

6

8

10

12

14

1995 2000 2005 2010 2015

% g

row

th in

GD

P

% g

row

th in

tra

ffic

an

dR

OIC

as

% in

vest

ed c

apit

alGlobal GDP growth, airline industry ROIC and air traffic growth

Airlines' return on capital

Growth in air travel and cargo volumes

Growth in global GDP(right scale)

Travel business very strong, cargo very weak

Source: ICAO, IATA

30

40

50

60

70

80

90

200

300

400

500

600

700

800

1995 2000 2005 2010 2015

Car

go r

even

ues

, US$

bill

ion

Pass

enge

r re

ven

ue,

US$

bill

ion

Airlines revenues from passengers and cargo

Revenue from tickets and ancillaries

Revenue from cargo

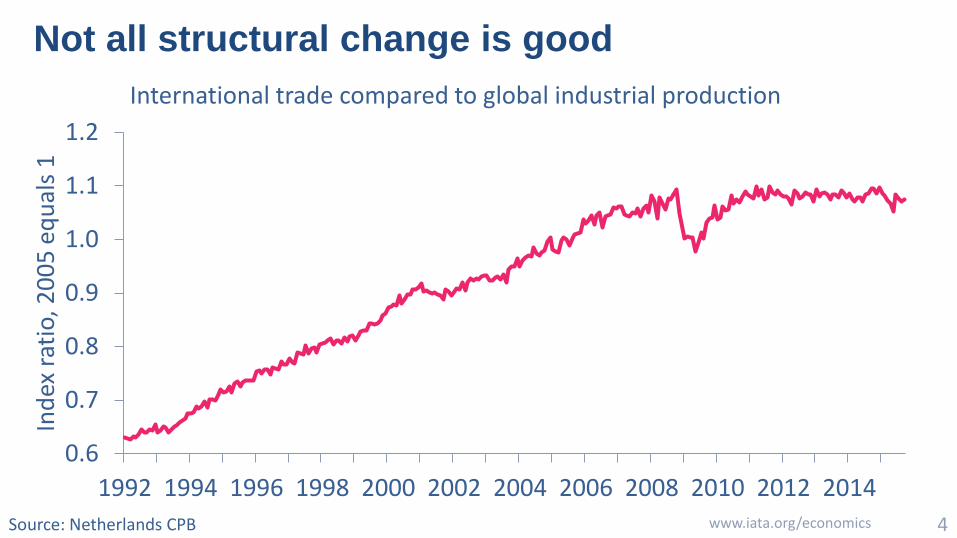

Not all structural change is good

Source: Netherlands CPB 4 www.iata.org/economics

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Ind

ex r

atio

, 20

05

eq

ual

s 1

International trade compared to global industrial production

Airline investors paid a ‘normal’ return for 1st time

Source: McKinsey, IATA 5 www.iata.org/economics

0.0

2.0

4.0

6.0

8.0

10.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

% o

f in

vest

ed c

apit

al

Return on capital invested in airlines

Cost of capital (WACC)

Return on capital (ROIC)

Ending decades of investor capital destruction (?)

Source: McKinsey, IATA 6 www.iata.org/economics

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

US$

bill

ion

Difference between investing in airlines and investing in similar assets elsewhere

And awful relative performance

www.iata.org/economics 7 Source: McKinsey

0 20 40 60 80 100

AirlinesUtilitiesTrucking

Automobiles and componentsTransportation & logistics

ShippingRail

Freight forwardingMaterials

Contract logisticsEnergy

Food and staples retailCapital goods

BusConsumer durables and apparel

Consumer servicesRetailing

Postal/CEPTelecom

Semiconductors and equipmentCommunications and professional services

Tech hardware and equipmentFood, beverage, and tobacco

MediaHealthcare equipment and services

Household and personalPharma, biotech, and life sciences

Software and services

Annual return on invested capital, 2004-2013

Debt finance markets still sceptical of change

AA+/-

A+/-

BBB+/- ANZ, Qantas, Lufthansa, Ryanair,

Southwest, Alaska, Westjet

BB+/- Delta, American, United, Allegiant,

Spirit, BA, Turkish, LATAM

B+/- Air Canada, Hawaiian, JetBlue, Avianca,

GOL, SAS, Virgin Australia

Investment

grade

Source: S&P, Airfinance Journal December 2015

As are equity markets

Source: Datastream 9 www.iata.org/economics

0

2

4

6

8

10

12

14

16

18

20

Legacyairlines

LCCs Trucking Rail Integrators Logistics

2016 f

orw

ard

P/E

rati

o

43%

US transportation sector

ROIC improvement in 2014 was narrowly based

Source: The Airline Analyst, IATA Economics

0

1

2

3

4

5

6

7

8

9

10

-20 -16 -12 -8 -4 0 4 8 12 16 20 24 28 32 36 40

% ROIC 2014 Q1-3

Number of airlines in ROIC band

37 airlines: ROIC>WACC

38% of industry capital

Source: The Airlines Analyst, IATA Economics

ROIC>WACC concentrated mostly in US in 2014

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%ROIC as a % invested capital, 2014

Average cost

of capital

N America Europe Asia Pacific LatAm ME Af

But last year ROIC improvement spread

Source: The Airline Analyst, IATA 12 www.iata.org/economics

0

1

2

3

4

5

6

7

8

9

10

-20 -16 -12 -8 -4 0 4 8 12 16 20 24 28 32 36 40

% ROIC 2015 Q1-3

Number of airlines in ROIC band

47 airlines: ROIC>WACC

60% of industry capital

Returns rose in US, Europe and spread to Asia

Source: The Airlines Analyst, IATA Economics

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45% ROIC as % invested capital, 2015 Q1-3 annualized

N America Europe Asia Pacific LatAm ME

Average cost of

capital

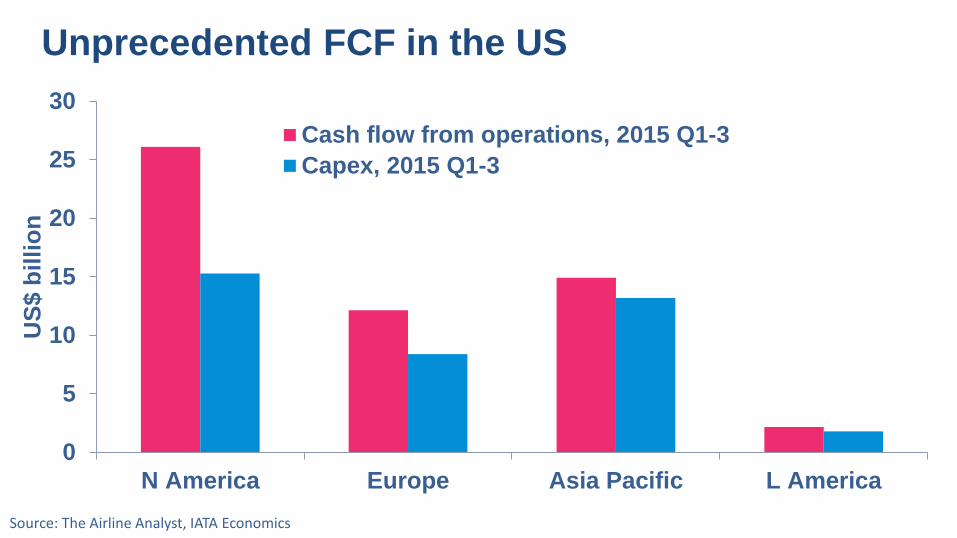

Unprecedented FCF in the US

Source: The Airline Analyst, IATA Economics

0

5

10

15

20

25

30

N America Europe Asia Pacific L America

US

$ b

illi

on

Cash flow from operations, 2015 Q1-3

Capex, 2015 Q1-3

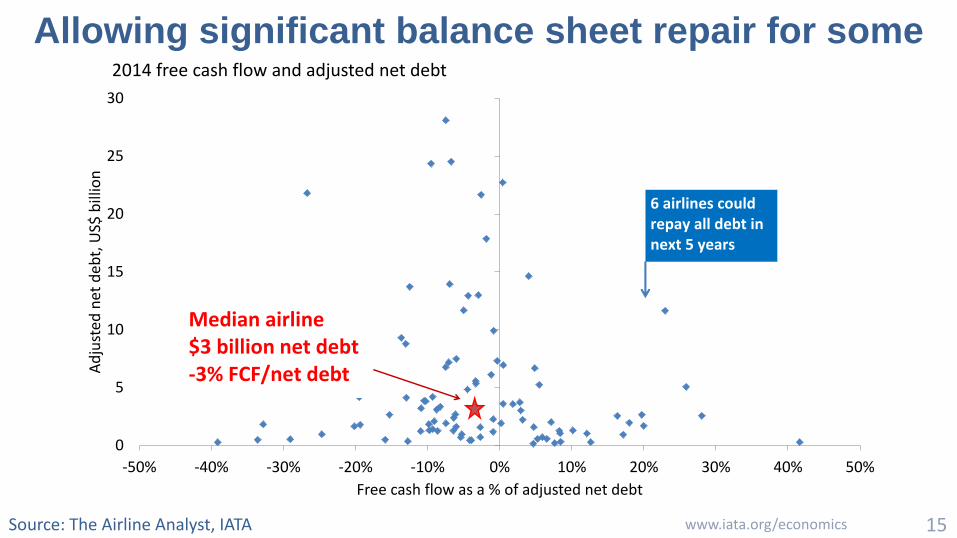

Allowing significant balance sheet repair for some

Source: The Airline Analyst, IATA 15 www.iata.org/economics

0

5

10

15

20

25

30

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

Ad

just

ed n

et d

ebt,

US$

bill

ion

Free cash flow as a % of adjusted net debt

2014 free cash flow and adjusted net debt

6 airlines could repay all debt in next 5 years

Median airline$3 billion net debt-3% FCF/net debt

It’s not just cheap fuel

Source: ICAO, McKinsey, IATA 16 www.iata.org/economics

0

2

4

6

8

10

5

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012 2014 2016

% r

etu

rn o

n in

vest

ed c

apit

al

US

cen

ts p

er A

TKFuel unit costs and airline return on capital

Airlines return on capital

Fuel unit cost

Suppliers mostly generate much better returns

Source: McKinsey for IATA 17 www.iata.org/economics

0%

5%

10%

15%

20%

25%

30%

% R

OIC

Return on capital across the air transport supply chain

1996-2014 2007-2014

But this is not the main issue for airline earnings

www.iata.org/economics 18 Source: McKinsey for IATA

0.8

(2.5) 0.3 0.7 0.4 2.0

TOTAL

(16.7) –

(18.0)

Freight

Forwarders

1.2

Travel

Agents

0-2.0

CRS

GDS

0.5

Airlines

(19.4)

ANSPAirportsCateringGroundMROLessors

(0.7) - (2.0)

Manufac-

turers

Estimate

Average yearly economic profit, USD billion, 2007-2014

Most of the value created ends up with consumers

Source: ICAO, Boeing, OAG, IATA 19 www.iata.org/economics

0.5

1

1.5

2

2.5

3

3.5

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US$

/RTK

in 2

01

4U

S$

Nu

mb

er o

f u

niq

ue

city

-pai

rs

Unique city-pairs and real transport costs

Unique city pairs

Real cost of air transport

Step change in airlines’ asset use since the GFC

Source: ICAO, IATA 20 www.iata.org/economics

58

59

60

61

62

63

64

65

66

67

68

2000 2002 2004 2006 2008 2010 2012 2014

% A

TK

s

Breakeven and achieved load factor (LF)

Achieved LF

Breakeven LF

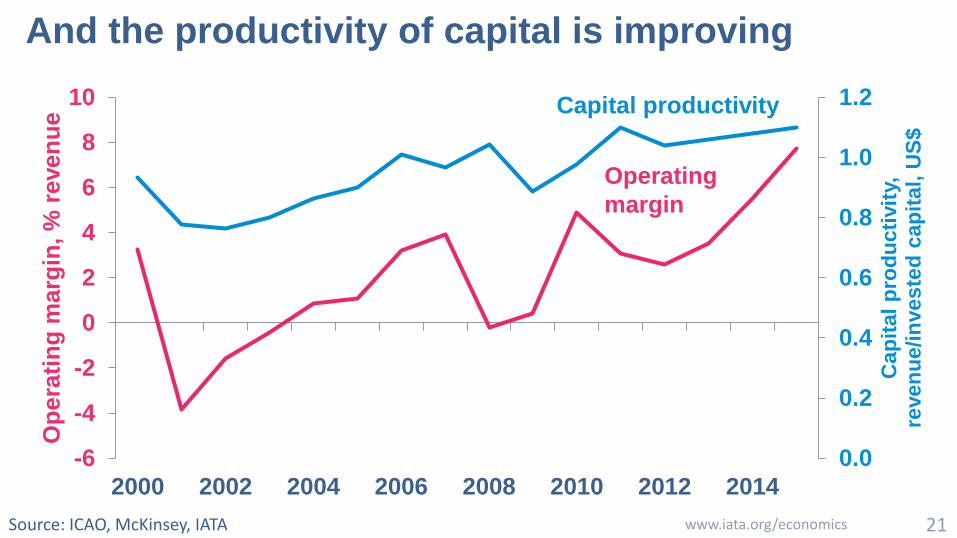

And the productivity of capital is improving

Source: ICAO, McKinsey, IATA 21 www.iata.org/economics

0.0

0.2

0.4

0.6

0.8

1.0

1.2

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014

Ca

pit

al

pro

du

cti

vit

y,

reve

nu

e/i

nve

ste

d c

ap

ita

l, U

S$

Op

era

tin

g m

arg

in, %

reven

ue

Capital productivity

Operating

margin

Still driven primarily by the US

Source: ICAO, IATA 22 www.iata.org/economics

-5%

0%

5%

10%

15%

N America Europe Asia Pacific Middle East LatinAmerica

Africa

% r

even

ues

Operating profit margins by region, 2016 vs 2010

2010 2016

Only a few generated economic profits consistently

www.iata.org/economics 23 Source: McKinsey for IATA

0 500 1000 1500 2000 2500

AegeanVuelling

AlaskaWizz

AllegiantSpirit

WestjetAeroflot

COPAEmirates

EasyjetRyanair

Economic profit ((ROIC-WACC)*IC), US$ million

Economic profit, cumulated 2005-2014 Average ROIC12.5%11.8%10.0%12.5%10.5%9.6%12.1%24.1%12.4%7.6%7.3%8.7%

What differentiates the few?

• Route network with time advantages/high QSI

• A brand that consumers value in some way

• Cost advantage versus key competitors

• Less capital?

• Shorter-haul?

www.iata.org/economics 24

Are we measuring the right thing?

• Economic losses persisted for 70 years

• No apparent shortage of capital

• Operating cash flow covers leasing cost/depreciation

• Are aircraft really capital?

• Is WACC overstated?

• Are airlines doing better than we think?

www.iata.org/economics 25

BACK UP SLIDES

www.iata.org/economics 26

Wide variation in travel growth by country

-5

0

5

10

15

20

25

India China US Eurozone Brazil Russia

% c

han

ge o

ver

pre

vio

us

year

Economic and passenger growth in 2015 to date

GDP Pax

Source: Datastream, IATA Statistics 27 www.iata.org/economics

Equity markets not always a good signal

www.iata.org/economics 28

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Index (January 2005 = 100)

Bird flu outbreak

Shanghai composite share

Domestic China air passenger trips (seasonally adjusted)

Int'l air passenger trips to/from China (seasonally adjusted)

Source: Datastream, IATA

Partly driven by major exchange rate shifts

29 www.iata.org/economics Source: Datastream

30

40

50

60

70

80

90

100

110

120

130

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Jet fuel price index (Jan 2014 = 100)

US dollar: -63%

Indian rupee: -60%Chinese yuan: -61%

Euro: -54%

Brazil: -40%

Russian ruble: -23%

% changes in jet fuel prices since Jan 2014

Premium slowing yield decline in some markets

www.iata.org/economics 30 Source: PaxIS+, IATA

2.9%

4.2%

3.3%

8.4%

5.8%

4.4%

24.6%

3.2%

14.7%

12.4%

-7% -6% -5% -4% -3% -2% -1% 0% 1% 2%

North-South America

Within Europe

Asia-Southwest Pacific

Within Asia

Europe-Middle East

Europe-Southern Africa

North Atlantic

South Atlantic

Europe-Asia

North And Mid Pacific

Change in premium's share of revenues (Nov'15 vs. Nov'14, %-point)

Each route's share of industry-wide premium revenues

Still vast potential in air travel marketes

www.iata.org/economics 31

0.0

0.1

1.0

10.0

$0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000

Air passenger journeys per capita (2014, log scale)

GDP per capita (2014, US dollars)

Iran

UAE

Saudi Arabia

Qatar Oman

Kuwait

Jordan

Iraq

Zoomed portion of chart

US

UK

Germany

Norway

0.0

0.1

1.0

10.0

$0 $2,500 $5,000 $7,500 $10,000

Air passenger journeys per capita (2014, log scale)

GDP per capita (2014, US dollars)

Iran

A) The expected increase in living standards in Iran now that sanctions have been lifted will underpin a rise in the average number of air journeys taken each year...

B) ...but a much bigger increase in trip frequencies is possible if the Iranian air

market 'normalizes' over the coming years.

'Normal' line

A

B