Embed Size (px)

Citation preview

Recommended Accounting Practice 7

Reporting Frameworkfor Unit Trusts(Revised 2012)

www.pwc.com

(Revised 2012)

IMAS Lunchtime Briefing17 July 2012

Agenda

Background

The easy stuff

Key changes

PwC 2

Background

PwC 3

Finally …….!

• A culmination of industry, IMAS and ICPAS efforts over the courseof the last few years

Background

of the last few years

• RAP 7 last revised in 2005

• Significant changes to IFRS/SFRS since then

• ICPAS RAP 7 sub-committee tasked with updating the RAP 7

PwC 4

A chronology of the journey

When What

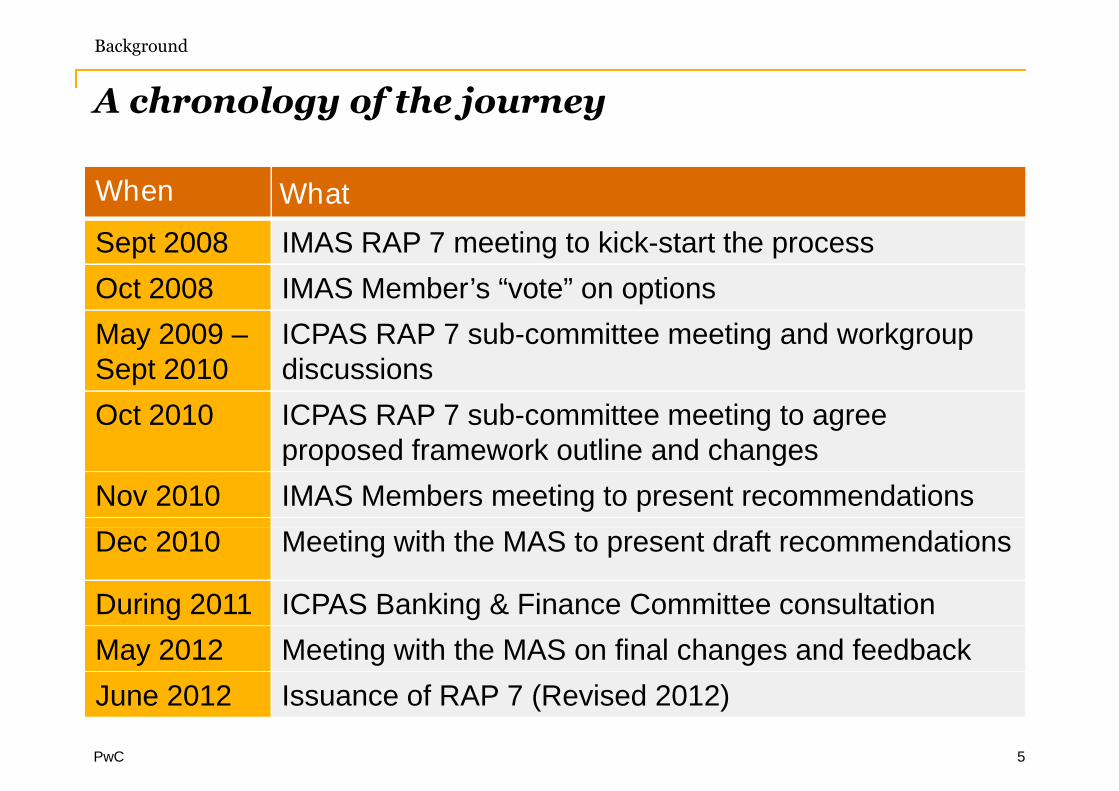

Sept 2008 IMAS RAP 7 meeting to kick-start the process

Background

Oct 2008 IMAS Member’s “vote” on options

May 2009 –Sept 2010

ICPAS RAP 7 sub-committee meeting and workgroupdiscussions

Oct 2010 ICPAS RAP 7 sub-committee meeting to agreeproposed framework outline and changes

Nov 2010 IMAS Members meeting to present recommendations

Dec 2010 Meeting with the MAS to present draft recommendations

PwC 5

Dec 2010 Meeting with the MAS to present draft recommendations

During 2011 ICPAS Banking & Finance Committee consultation

May 2012 Meeting with the MAS on final changes and feedback

June 2012 Issuance of RAP 7 (Revised 2012)

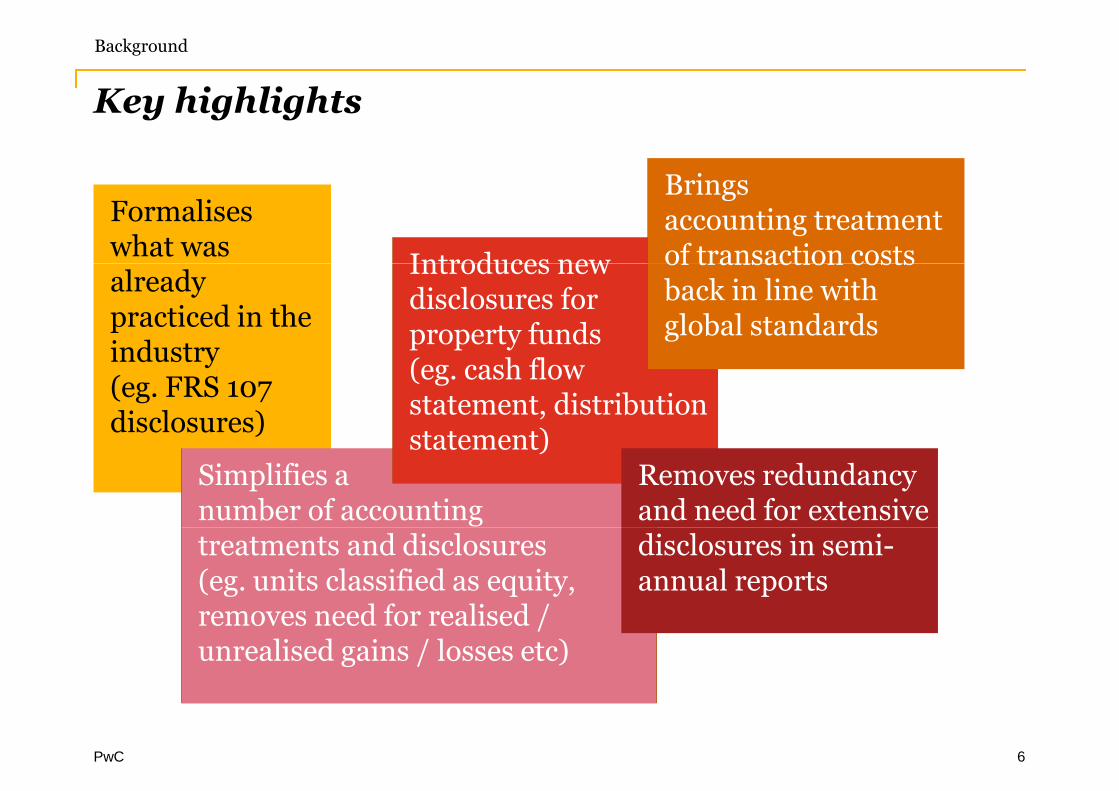

Key highlights

Formaliseswhat was

Introduces new

Bringsaccounting treatmentof transaction costs

Background

alreadypracticed in theindustry(eg. FRS 107disclosures)

Simplifies anumber of accounting

Introduces newdisclosures forproperty funds(eg. cash flowstatement, distributionstatement)

of transaction costsback in line withglobal standards

Removes redundancyand need for extensive

PwC 6

treatments and disclosures(eg. units classified as equity,removes need for realised /unrealised gains / losses etc)

disclosures in semi-annual reports

The easy stuff

PwC 7

RAP 7 (Revised 2012)

1. Ongoing updates

2. Effective date

The easy stuff

2. Effective date

3. Short Form andInterim Financial Statements

4. Trustees’ and Auditors’ Reports

PwC 8

Ongoing updates

• Will be reviewed periodically

• Original “3 year” moratorium has

The easy stuff

• Original “3 year” moratorium hasbeen dropped

• However, will NOT be subject tomandatory changes resulting fromchanges in IFRS/SFRS until next re-issue

• But ICPAS may issue guidance to

PwC

• But ICPAS may issue guidance towhich application may be required

9

Effective date

• Accounting periods commencing on orafter 30 June 2012

The easy stuff

after 30 June 2012

• First application will be in respect ofsemi-annual reports ending 31 December2012

• Comparatives not required forinformation exempted by IFRS/SFRS (eg.FRS 107)

PwC 10

Short Form and Interim financial statements

Short Form financial statements

• Considered redundant

The easy stuff

• Considered redundant

• Has now been removed

Interim financial statements

• Now simplified

• Only primary statements need to be presented, ie. no more notes to

PwC

• Only primary statements need to be presented, ie. no more notes tothe financial statements required

• Information required by the Code on CIS and other MASRegulations and Guidelines will still be necessary (including expenseratios and turnover ratios)

11

Trustees’ and Auditors’ Reports

Trustees’ Report

• Reference to financial statements now removed

The easy stuff

• Reference to financial statements now removed

Auditors’ Report

• Updated to be consistent with clarified SSA 700

• “Manager’s Responsibility” has been amended to reflect that, “theManager is responsible for such internal control as the Manager

PwC

Manager is responsible for such internal control as the Managerdetermines is necessary to enable the preparation of financialstatements that are free from material misstatement”

• Consistent with requirement for companies

12

Key changes

PwC 13

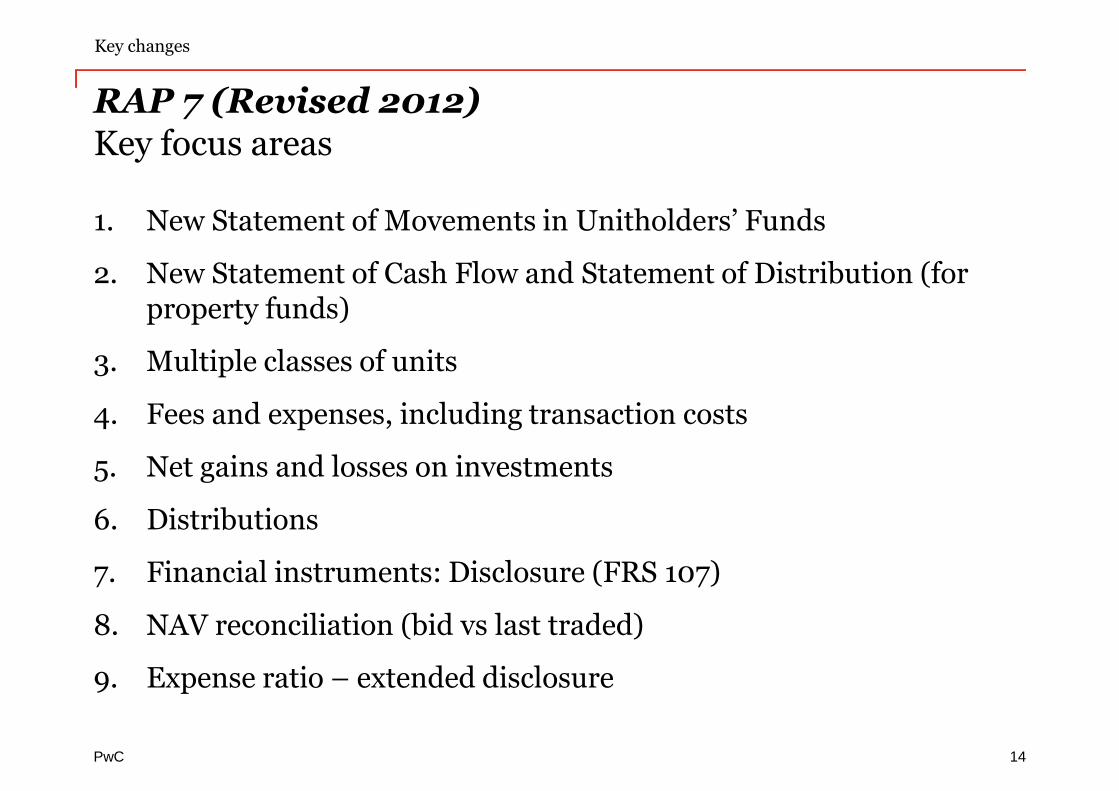

RAP 7 (Revised 2012)Key focus areas

1. New Statement of Movements in Unitholders’ Funds

2. New Statement of Cash Flow and Statement of Distribution (for

Key changes

2. New Statement of Cash Flow and Statement of Distribution (forproperty funds)

3. Multiple classes of units

4. Fees and expenses, including transaction costs

5. Net gains and losses on investments

6. Distributions

PwC

6. Distributions

7. Financial instruments: Disclosure (FRS 107)

8. NAV reconciliation (bid vs last traded)

9. Expense ratio – extended disclosure

14

New Statement of Movements in Unitholders’Funds

• Previously categorized as liabilities

• Now fixed classification to “Equity” to reflect the economic substance

Key changes

• Now fixed classification to “Equity” to reflect the economic substance

• As a result, a new "Statement of Movements in Unitholders' Funds"has been included as one of the primary statements

• In essence, similar information previously included in the notes tothe financial statements as “net assets attributable to unitholders”

• Auditor's report and statement by the Manager have been updated toinclude the reference to the new primary statement

PwC

include the reference to the new primary statement

15

New Statement of Cash Flow and Statement ofDistribution

• Applicable ONLY to property funds

• Brings the financial reporting of property funds in line with

Key changes

• Brings the financial reporting of property funds in line withinternational standards and REITS practices

• Statement of Cash Flow is similar to that proposed under IFRS/SFRS(indirect or direct)

• Statement of Distribution is new and provides added clarity in thecalculation of distributions per unit

PwC 16

Multiple classes of units

• Where funds issue more than one class of units, additional disclosurerequired:

Key changes

required:

- net asset attributable to unitholders of each unit class (at thebeginning and end of the period)

- distributions attributable to each class

- the different rights and terms attached to each unit class, includingthe rights on winding-up and the policy for allocating taxation anddistributable income

PwC 17

Fees and expenses, including transaction costs

• Clarification on presentation ofexpenses, with mandatory

Key changes

expenses, with mandatorypresentation of the following:

- Management fee (with grossamount less rebate, if any)

- Performance fee

- Trustee fee

- Valuation fee

PwC

- Valuation fee

- Custodian fee

- Audit fee

18

Fees and expenses, including transaction costs(cont’d)

• All expenses relating to the purchase and sale of financialinstruments should be charged against income

Key changes

instruments should be charged against income

• Transaction costs CANNOT be capitalised against investments, andshould be shown separately as a line item under expenses

• NO impact on NAV, as previously would have been charged againstunrealised loss on revaluation of investments

• Does not apply to transaction costs on real property (for REITS)

PwC 19

Net gains and losses on investments

• Previously, net realised and unrealised gains/losses on investmentsand/or derivatives are shown separately

Key changes

and/or derivatives are shown separately

• In line with IFRS/SFRS, there is no need to show realised andunrealised gains/losses separately

• However, net gains/losses on different financial instruments shouldstill be separately disclosed, ie:

- Investments

- Futures

PwC

- Futures

- Options

- Swaps

- Foreign exchange contracts, etc

20

Net gains and losses on investments (cont’d)

• But for financial derivatives, need to consider the nature and purposeof the use of the financial derivative, as it will impact on whether it

Key changes

of the use of the financial derivative, as it will impact on whether itshould be included in

- net gain/loss on investments; OR

- separately under net gain/loss on financial derivatives

Is it for protection of investors’ capital?

Does it resemble a return on deposits (ie interest income)?

PwC

Does it resemble a return on deposits (ie interest income)?

21

Distributions

• Previously, treatment of distributions at year-end was not consistent

• Some accrue for distributions at year-end (ie. ex-date basis), while

Key changes

• Some accrue for distributions at year-end (ie. ex-date basis), whileothers don’t (and only disclose intent to distribute)

• Now, distributions MUST be accrued for at the balance sheet datewhere Manager has the discretion to declare distributions withoutthe need for unit holder or trustee approval, and a constructive orlegal obligation has been created

PwC 22

Financial instruments: Disclosure (FRS 107)

• Most extensive change to RAP 7

• However, majority of funds have already been applying FRS 107

Key changes

• However, majority of funds have already been applying FRS 107disclosures since 2009

• Considered best practice, and useful information for investors

• Brings about disclosures on financial instruments, in particular thefinancial risk management of the portfolio, covering:

- Market risk (including price risk, interest rate risk and currencyrisk)

PwC

risk)

- Liquidity risk (including capital management risk)

- Credit risk (including counterparty risk)

- Fair value estimation and hierarchy (Level 1, 2 and 3)

23

Financial instruments: Disclosure (FRS 107)(cont’d)

• Disclosure of sensitivity analysis and the impact on NAV

• For first time application, NO comparatives needed (but disclosure in

Key changes

• For first time application, NO comparatives needed (but disclosure inthe first year of application required)

PwC 24

NAV reconciliation (bid vs last traded)

• Difference in accounting and pricing NAV arises due to the differencein valuation methods used

Key changes

in valuation methods used

- Bid and offer under RAP 7

- Last traded per prospectus

• Where the accounting NAV is materially different from pricing NAV,RAP 7 now requires a reconciliation of net assets attributable tounitholders per unit to be shown in the notes

PwC 25

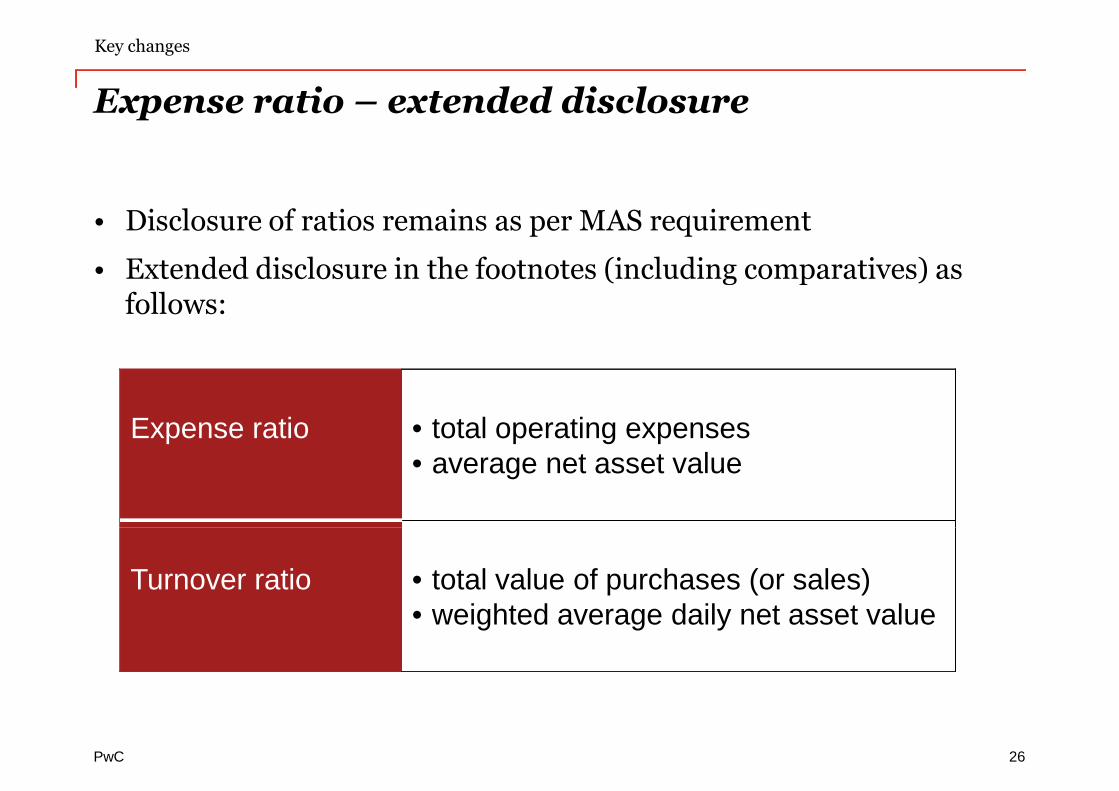

Expense ratio – extended disclosure

• Disclosure of ratios remains as per MAS requirement

• Extended disclosure in the footnotes (including comparatives) as

Key changes

• Extended disclosure in the footnotes (including comparatives) asfollows:

Expense ratio • total operating expenses• average net asset value

PwC 26

Turnover ratio • total value of purchases (or sales)• weighted average daily net asset value

Questions?

PwC 27PwC

www.pwc.com/assetmanagement

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, itsmembers, employees and agents do not accept or assume any liability, responsibility or duty ofcare for any consequences of you or anyone else acting, or refraining to act, in reliance on theinformation contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers toPricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopersInternational Limited, each member firm of which is a separate legal entity.