Embed Size (px)

Citation preview

Loyalty Disruption? Prof. Cristina Ziliani , Ph.D - Loyalty Observatory UniPR

IMA Europe Conference

Milan

18 May 2017

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

2

The Loyalty Conference

The Loyalty Observatory at the University of Parma

Founded in 1999 43 academic journal papers 4 books 18 sponsors 16 conferences 2500 attendees 850 companies 110 speakers

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Loyalty Marketing today

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Dunkin' Brands shares jump

as loyalty program hits milestone Monday, 22 Aug 2016 | 4:33 PM ETCNBC.com

Ron Antonelli | Bloomberg | Getty Images

Dunkin' Donuts

Shares of Dunkin' Brands rose nearly 2 percent on Monday

after the company revealed that its loyalty program had reached

a new milestone.

This Is Why Starbucks Might Not Be

the Best Stock to Buy Right Now 21st April 2016

4 Reasons Amazon Stock Will Keep Doubling Every 3 Years

Investing #StockWatch

“We will grow thanks to our loyal customers. Acquisition is too risky

and uncertain” (Brian Moynihan, Bank of America CEO)

“I congratulate Bank of America. Retention is a sound and forward

looking strategy (Warren Buffett)

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Loyalty «disrupted» Marketing

Retention vs Acquisition

customer-based success measures

systematic individual customer information collection

widespread adoption of CRM

loyalty programs

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

1895 - Sperry & Hutchinson Company creates “stamps” to

reward repeat purchase

1980 - American Airlines launches Aadvantage and air miles

1990’s - adoption in European retail

plastic cards

basic segmentation: card holders vs non-holders

rewards take the form of points, gifts, reductions, status

no use of data

overconfidence in program impact on behaviour

first entrant advantage

exits

B2B (trade partner programs)

Milestones in the history of loyalty marketing

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

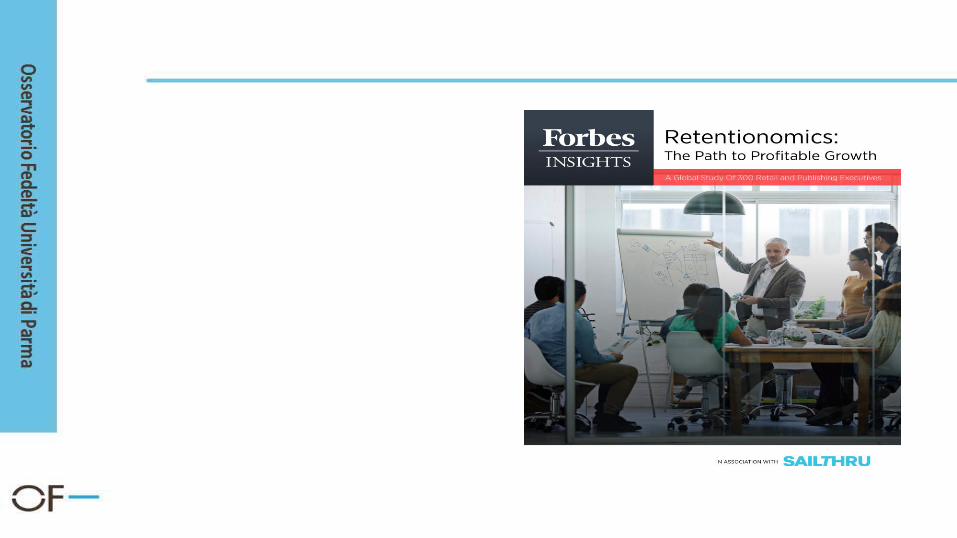

2000’s – diffusion

across industries and countries evolution of loyalty program model rise of loyalty intermediaries consulting firms develop “loyalty” divisions data collection and analysis begin use of loyalty data for marketing decision making begins (Tesco)

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

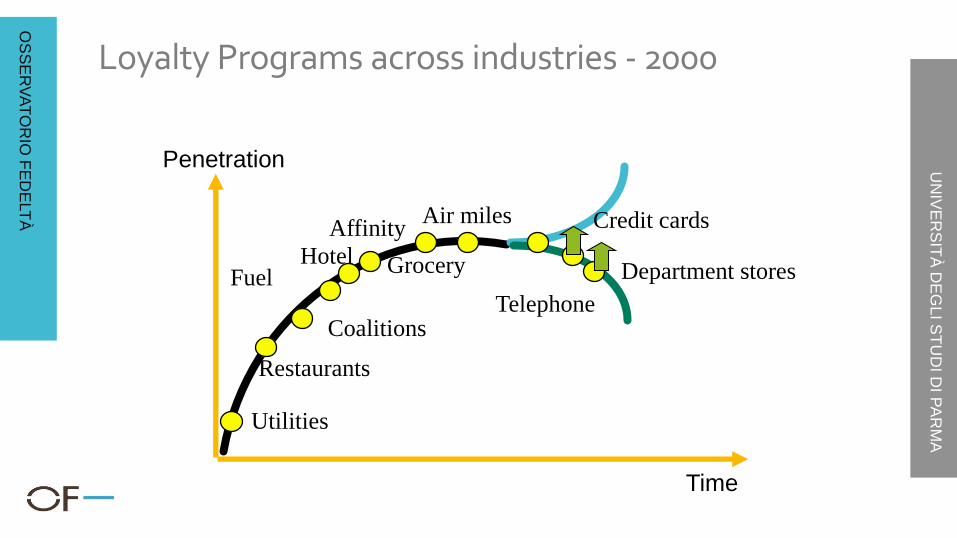

Loyalty Programs across industries - 2000

Penetration

Time

Department stores

Air miles

Grocery Fuel

Restaurants

Credit cards

Hotel

Affinity

Telephone

Utilities

Coalitions

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Supermarket loyalty programs across countries - 2000

time

penetration

Russia, India, China

France

Italy

Benelux

Canada

USA UK

Scandinavia

Spain

East Europe

Malaysia, Thailand

Austria

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

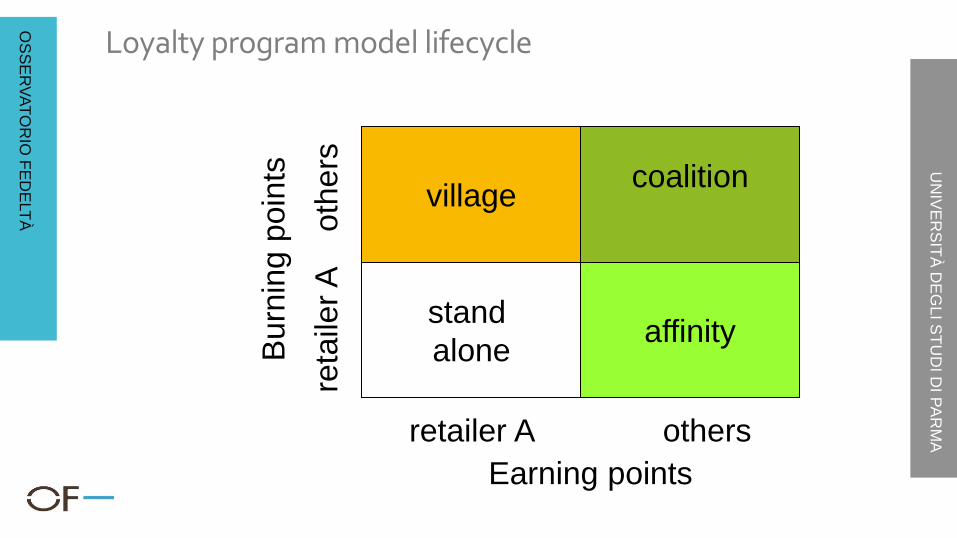

Loyalty program model lifecycle

village

stand

alone affinity

coalition

Earning points

Burn

ing p

oin

ts

retailer A others

reta

iler

A

oth

ers

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Coalitions

Numero annuo di lanci di programmi di tipo coalizione

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Media for loyalty marketing – 2001 to 2012

digital loyalty program

digital coupon

social media

app

telemarketing

kiosks

text messages

customer magazine

e-mailing

coupon at till

direct mailing

website

72%

51%

75%

37%

91%

68%

83%

91%

90%

87%

94%

100%

2012

2009

2001

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

2010’s – maturity AND morphing

Maturity of «traditional» loyalty programs B2B schemes shift from sell in to sell out and database building goals Digital Revolution New promotional scenario New players

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

2016 - maturity

The average US family belongs to 30 loyalty programs (Colloquy, 2016)

Consumers who shop regularly with a loyalty card are between 70% and 90% across Europe (Nielsen 2015)

CPG manufacturers launch brand loyalty programs Overall, coupons, gift cards and loyalty points together account for more than $165 billion in purchasing power in the US, almost as much as total e-commerce sales

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

The Information Revolution (AKA Big Data)

The explosion in the variety and quantity of information available to individuals and organisations, regardless of its location

Disruption

from the Latin verb «dis-rumpere»: “shatter, sever, cause to break apart”

Social

and Mobile

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

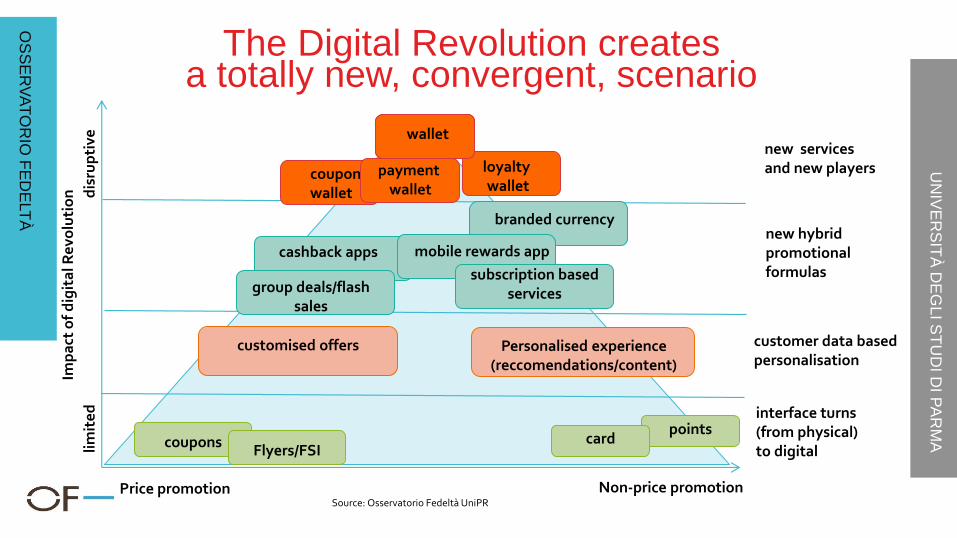

coupon wallet

branded currency

cashback apps

coupons

mobile rewards app

wallet

Non-price promotion

dis

rup

tive

Price promotion

Imp

act

of

dig

ita

l Re

volu

tio

n

lim

ite

d

interface turns (from physical) to digital

customer data based personalisation

new hybrid promotional formulas

new services and new players

points

Flyers/FSI card

customised offers Personalised experience (reccomendations/content)

group deals/flash sales

subscription based services

payment wallet

loyalty wallet

wallet

The Digital Revolution creates a totally new, convergent, scenario

Source: Osservatorio Fedeltà UniPR

Branded currency

• “All forms of currency – points, gift cards, coupons etc. that allow a shopper to exchange with a retailer for its goods and bear the retailer name as an umbrella”

• Retention potential of new means of payment

• Starbuck’s evolution from gift card to «mobile payment tool & loyalty program»

• 1 bn $ in app

• 20% transactions through app

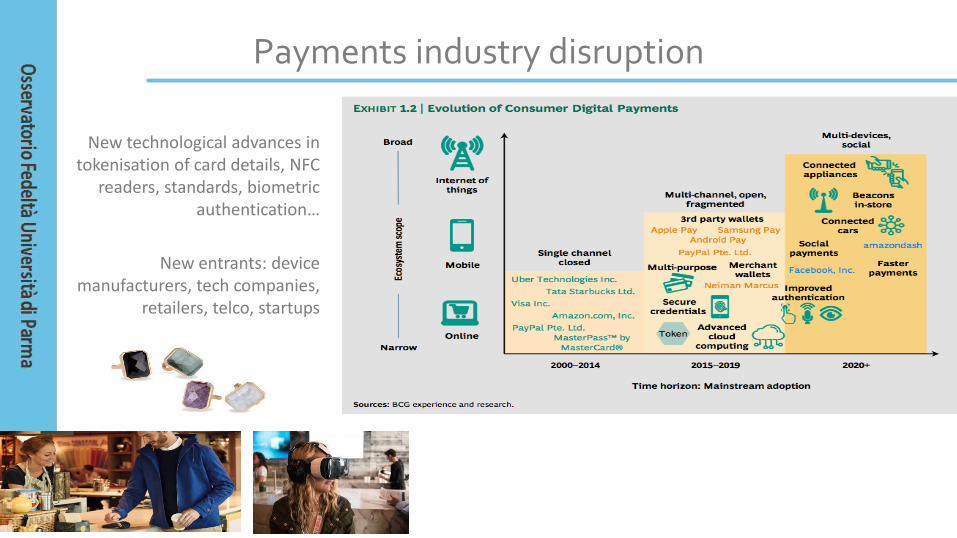

Payments industry disruption

New technological advances in tokenisation of card details, NFC

readers, standards, biometric authentication…

New entrants: device manufacturers, tech companies,

retailers, telco, startups

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

1995 2015

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

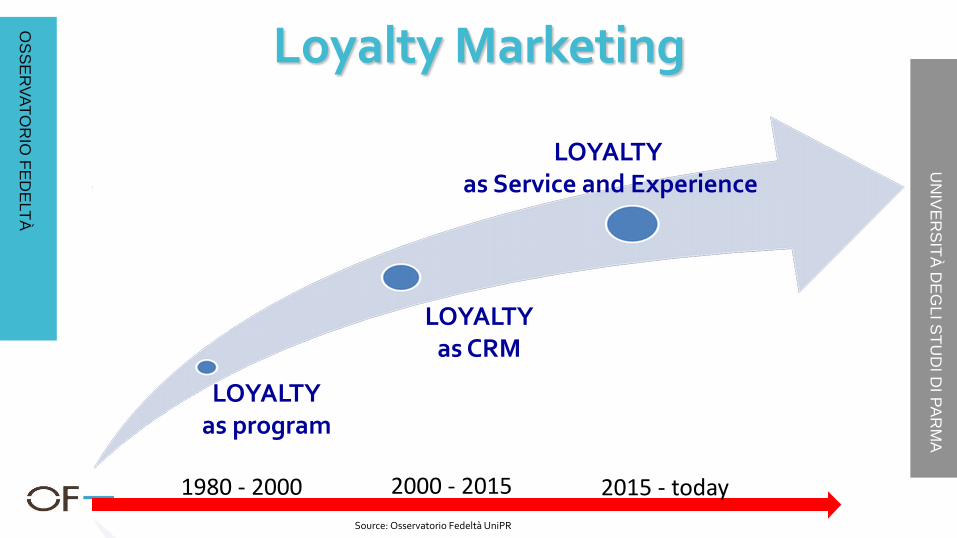

Loyalty Marketing

LOYALTY as program

LOYALTY as CRM

LOYALTY as Service and Experience

1980 - 2000 2000 - 2015 2015 - today

Source: Osservatorio Fedeltà UniPR

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

23

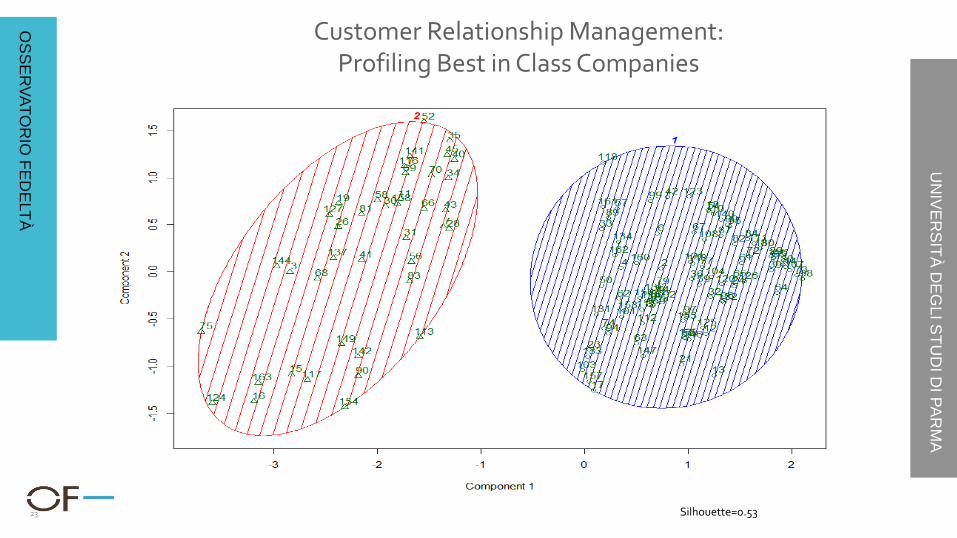

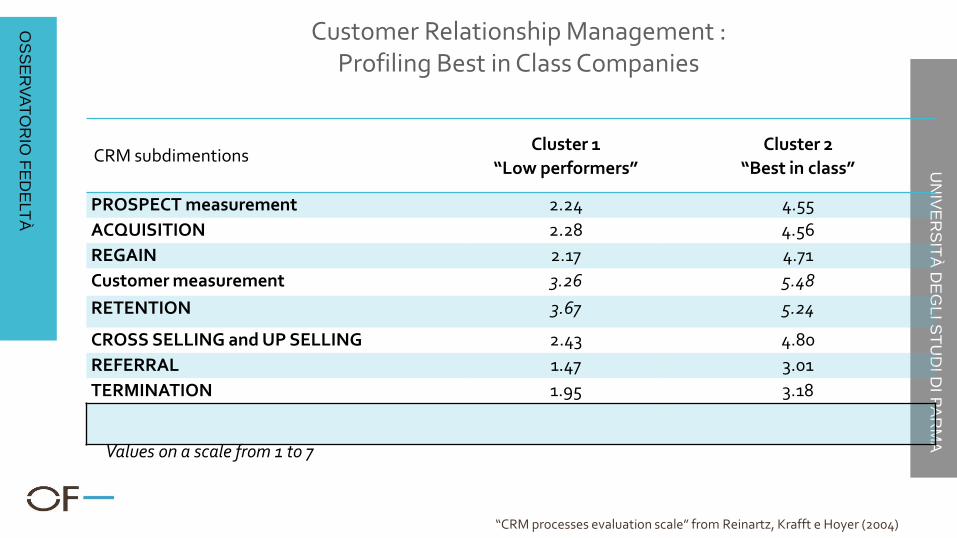

Customer Relationship Management: Profiling Best in Class Companies

Silhouette=0.53

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

CRM subdimentions Cluster 1

“Low performers”

Cluster 2

“Best in class”

PROSPECT measurement 2.24 4.55

ACQUISITION 2.28 4.56

REGAIN 2.17 4.71

Customer measurement 3.26 5.48

RETENTION 3.67 5.24

CROSS SELLING and UP SELLING 2.43 4.80

REFERRAL 1.47 3.01

TERMINATION 1.95 3.18

Values on a scale from 1 to 7

Customer Relationship Management : Profiling Best in Class Companies

“CRM processes evaluation scale” from Reinartz, Krafft e Hoyer (2004)

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

CRM best in class

Use loyalty KPIs at all organisation levels and in all departments

Are multichannel, specifically use offline to drive online

Spend more of the marketing budget on loyalty

Train employees to manage customer segments differently based on value

Reward employees for customer retention

Consider the website pivotal for retention

Began CRM 2,5 years in advance compared to others Believe that personalisation is the most effective retention

Use both digital and traditional media in a targeted way to contact customer

Are very open to partnerships with new intermediaries and e-commerce pure players

16% 24% 21% 18% 21%

39%

26% 18%

7% 9%

0%

10%

20%

30%

40%

50%

0-5% 6-10% 11-15% 16-20% oltre il20%

Best in class Altri

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

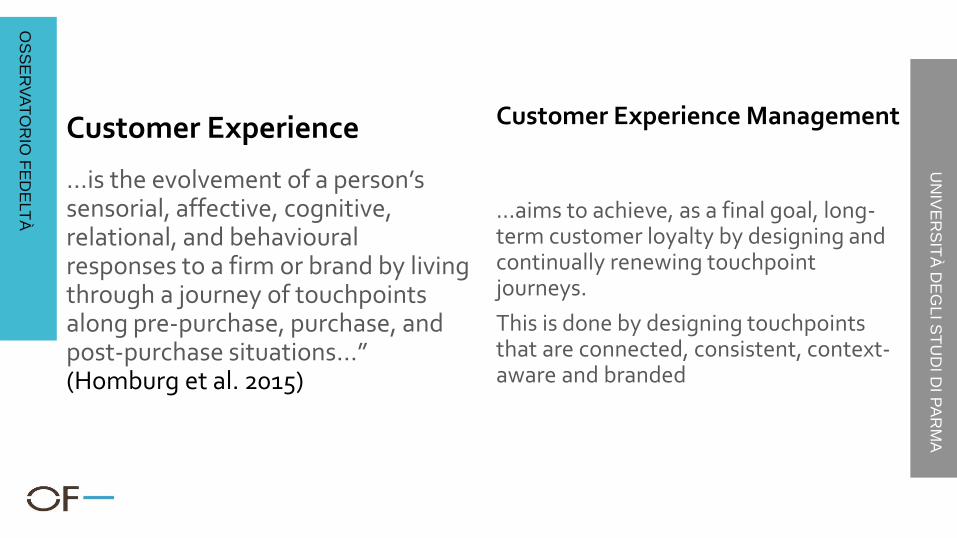

…is the evolvement of a person’s sensorial, affective, cognitive, relational, and behavioural responses to a firm or brand by living through a journey of touchpoints along pre-purchase, purchase, and post-purchase situations…” (Homburg et al. 2015)

Customer Experience Management

…aims to achieve, as a final goal, long-term customer loyalty by designing and continually renewing touchpoint journeys.

This is done by designing touchpoints that are connected, consistent, context-aware and branded

Customer Experience

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Is the Customer Experience Management concept clear for companies?

…YES for 19% of respondents

for 27,5% of those who sell online

for 6,8% of those who don’t

…and WE ARE GOOD AT IT 13% of respondents agree

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

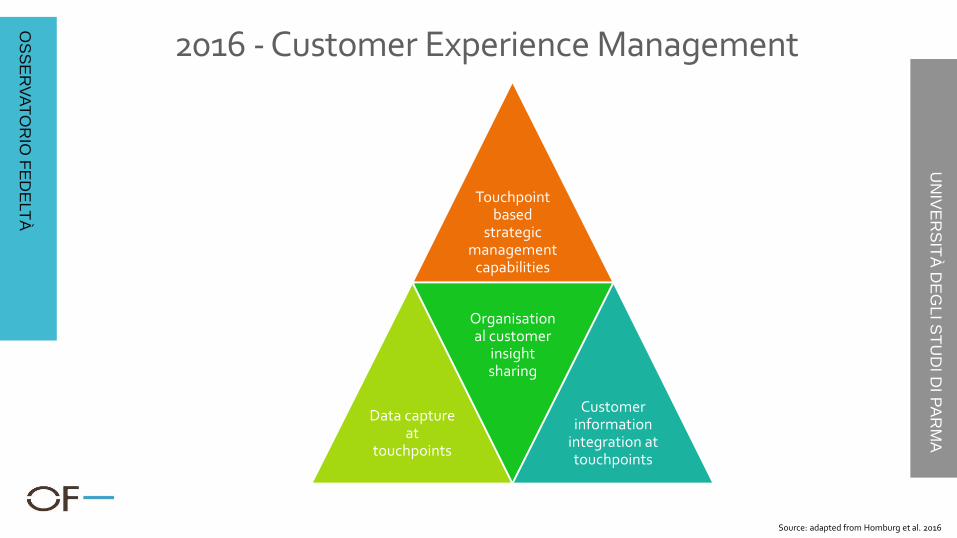

Touchpoint based

strategic management

capabilities

Data capture at

touchpoints

Organisational customer

insight sharing

Customer information

integration at touchpoints

2016 - Customer Experience Management

Source: adapted from Homburg et al. 2016

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

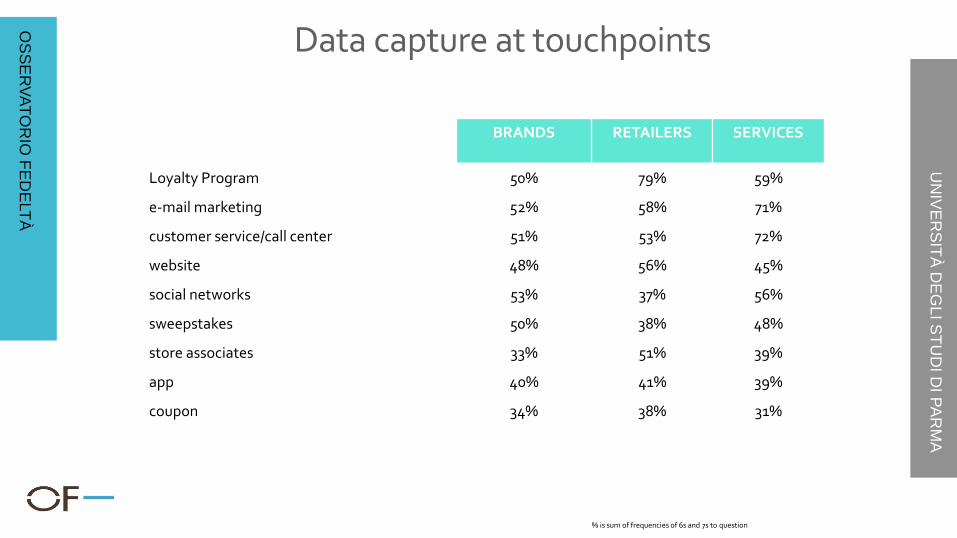

BRANDS RETAILERS SERVICES

Loyalty Program 50% 79% 59%

e-mail marketing 52% 58% 71%

customer service/call center 51% 53% 72%

website 48% 56% 45%

social networks 53% 37% 56%

sweepstakes 50% 38% 48%

store associates 33% 51% 39%

app 40% 41% 39%

coupon 34% 38% 31%

Data capture at touchpoints

% is sum of frequencies of 6s and 7s to question

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

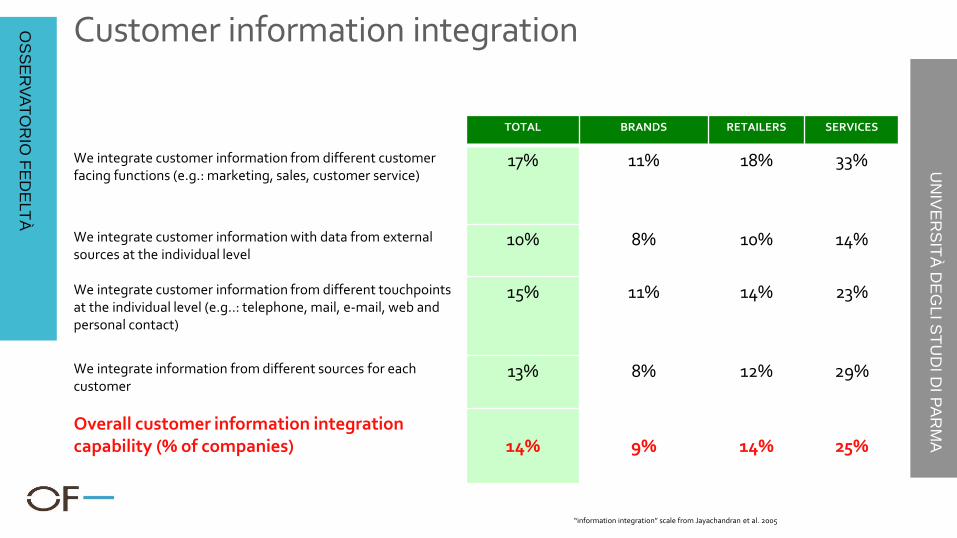

Customer information integration

TOTAL BRANDS RETAILERS SERVICES

We integrate customer information from different customer facing functions (e.g.: marketing, sales, customer service)

17%

11%

18%

33%

We integrate customer information with data from external sources at the individual level

10%

8%

10%

14%

We integrate customer information from different touchpoints at the individual level (e.g..: telephone, mail, e-mail, web and personal contact)

15%

11%

14%

23%

We integrate information from different sources for each customer

13% 8% 12% 29%

Overall customer information integration capability (% of companies)

14%

9%

14%

25%

“information integration” scale from Jayachandran et al. 2005

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Insight sharing across the organisation

TOTAL BRANDS RETAILERS SERVICES

Customer insight is shared across departments/functions

8%

3%

8%

24%

Customer insight is shared across organisational levels

13%

8%

10%

23%

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

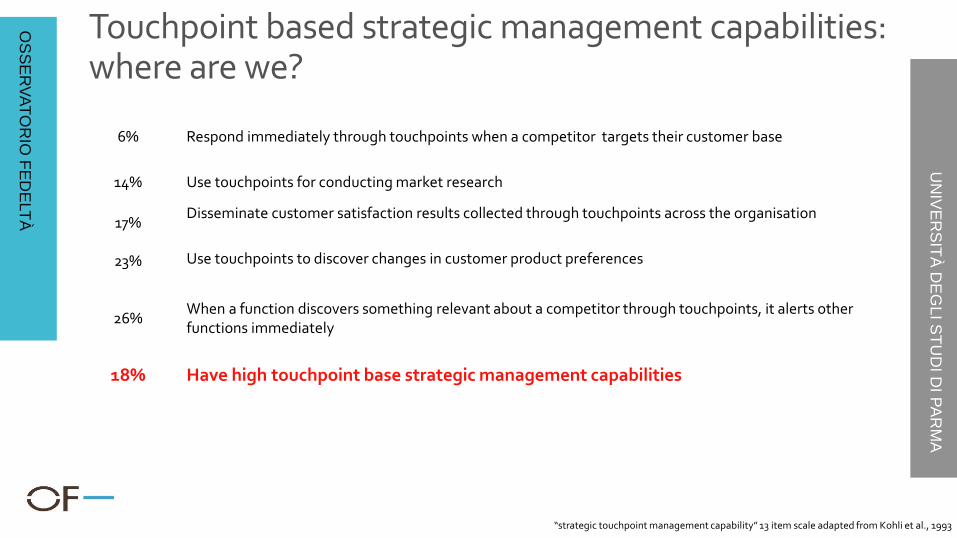

Touchpoint based strategic management capabilities: where are we?

18% CAPACITA’ COMPLESSIVA

6% Respond immediately through touchpoints when a competitor targets their customer base

14% Use touchpoints for conducting market research

17% Disseminate customer satisfaction results collected through touchpoints across the organisation

23% Use touchpoints to discover changes in customer product preferences

26%

When a function discovers something relevant about a competitor through touchpoints, it alerts other functions immediately

18% Have high touchpoint base strategic management capabilities

“strategic touchpoint management capability” 13 item scale adapted from Kohli et al., 1993

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Touchpoint based strategic management capabilities are strongly positively correlated with company performance:

Sales Margins Overall economic performance

Why should companies embrace Customer Experience Management?

Controlling for company size, industry and loyalty orientation

OS

SE

RV

AT

OR

IO F

ED

ELT

À

UN

IVE

RS

ITÀ

DE

GL

I ST

UD

I DI P

AR

MA

Thank you for your attention!

@Oss_Fedelta