Embed Size (px)

Citation preview

IFTEKHA HASANFordham University and Bank of Finland

LIULING LIUBowling Green State University

HAIZHI WNAGIllinois Institute of Technology

Trust and Contracting with Foreign Banks: Evidence from China

1

04/18/23Conference on China's Financial Intermediation

Motivation

Cross-border financial exchanges face significant informational costs. For example, Home bias in equity investment (Cooper and Kaplanis,

1994; Kang and Stulz, 1997) Syndicated loan pricing puzzle (Carey and Nini, 2007)

Mechanisms to deal with information problems Local sources of information Importance of Institutions, including legal systems

04/18/23Conference on China's Financial Intermediation

2

Motivation (cont’d)

Social trust and information processing

Social trust changes the incentives of economic agents and creates a cooperative environment (Algan and Cahuc, 2010)

Trusting or trustworthiness is a crucial determining factor when individuals choose to act or react toward others (Hardin, 2002)

Social trust tend to greatly influence the way people release and process information (Cook, 2001; Hardin, 2002)

04/18/23Conference on China's Financial Intermediation

3

Research questions

In this study, we intend to relate social trust to cross-border syndicated loan contractual terms

Social trust and foreign loan contracts Cost of bank loans Fees in loan contracts Non-price terms in loan contracts (i.e., maturity and collateral)

04/18/23Conference on China's Financial Intermediation

4

Literature review

Lending at distance (cross-border syndicated loans) Interest rate spreads vary across different regions

(Carey and Nini, 2007; Houston et al., 2007)

Informational costs (Mian, 2006)

Negotiation costs (Degryse and Ongena, 2007)

Enforcement costs in the events of default (Haas and VHoren, 2013)

04/18/23Conference on China's Financial Intermediation

5

Literature review (cont’d)

Social trust, as a form of social capital, plays an important role in economic transactions Social trust facilitates economic growth (Algan and

Cahuc, 2010) Social capital and financial development (Guiso, 2004) Social trust and international trade (Guiso et al.,

2009) Social trust and equity investment (Guiso et al., 2008) Social trust and selection of money managers

(Gennaioli et al., 2015) Trust and crediquality of financial reporting (Jha,

2013)

04/18/23Conference on China's Financial Intermediation

6

Literature review (cont’d)

Social trust: Chinese evidence Trust and regional economic development (Zhang and

Ke, 2002) Social trust and foreign high-tech companies’

investment (Ang et al;, 2014) Provinces with high social trust scores attract more foreign

investments in high-tech industry Foreign firms located in high-social-trust regions conduct more

R&D, higher more R&D personnel and are more likely to establish JVs with local partners

Social trust and trade credit (Wu et al., 2014) Firms located in high-social-trust regions use more trade credit

from suppliers, extend more trade credit to customers and collect receivables and pay payables more quickly

04/18/23Conference on China's Financial Intermediation

7

Literature Review (Cont’d)

Institutions Formal institutions (China evidence)

Enforcement of property rights significantly affect firm reinvestment decision (Cull and Xu, 2005)

Enforcement of intellectual property rights impacts firm financing and investment decision (Ang et al., 2015)

04/18/23Conference on China's Financial Intermediation

8

Literature Review (Cont’d)

04/18/23Conference on China's Financial Intermediation

9

Institutions Informal institutions (China evidence)

Financing channels and governance mechanisms based on reputation and relationships support the growth of the private sector (Allen, et al., 2005)

In contrast, firms with formal bank financing are associated with faster growth, compared to firms with informal financing (Ayyagari, et al., 2010)

Additional research question

Social trust, as an important component of social capital, can function as informal institution

We ask one additional research question Does social trust complement or substitute the role of

formal institutional development in terms of borrowing cost?

04/18/23Conference on China's Financial Intermediation

10

Data and Sample

Dealscan and CSMAR 177 loan facilities from 1998 to 2013

Dependent measures All-in-spread-drawn (AISD) Total fees

Upfront fee All-in-spread-undrawn (AISU) including commitment fee

and facility fee Non-price terms

Collateral Maturity

04/18/23Conference on China's Financial Intermediation

11

Measures

Main explanatory variables Trust1

Survey conducted by the “Chinese Enterprise Survey System in 2001

Mutually trustworthiness among corporate managers for a particular province

Trust2 China General Social Survey (2003) General trustworthiness of strangers by residents in a

particular province Blood

Blood donation per capita in a province

04/18/23Conference on China's Financial Intermediation

12

Measures (cont’d)

Other control variables Firm size Book leverage Profitability (ROA) Sales growth rate Loan size

04/18/23Conference on China's Financial Intermediation

13

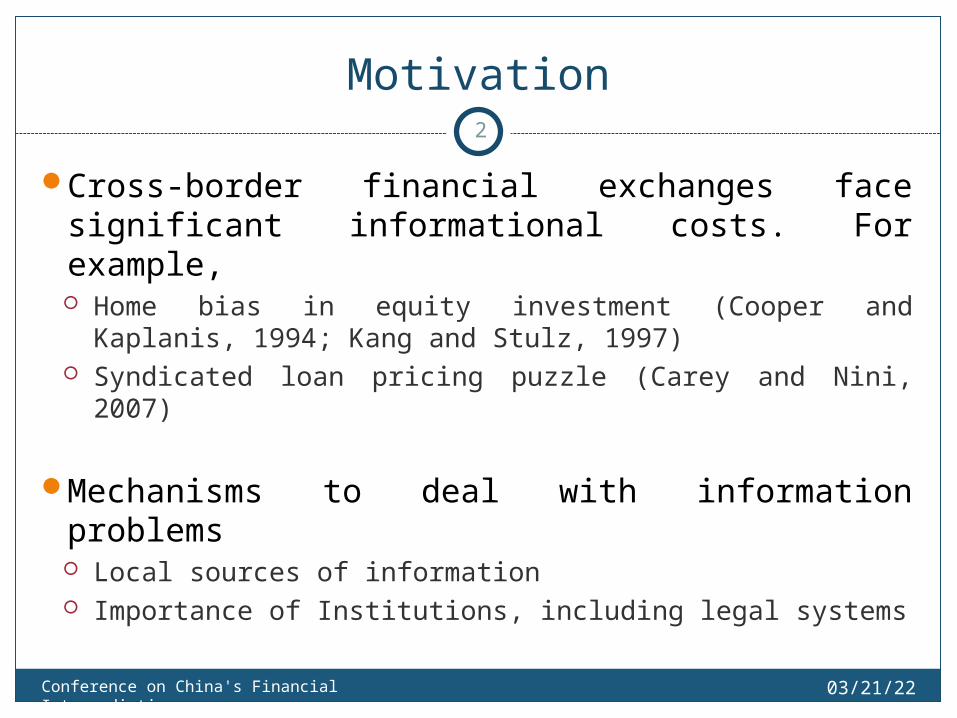

Baseline regression: trust and AISD

04/18/23Conference on China's Financial Intermediation

14

Independent variablesModel 1 Model 2 Model 3 Model 4 Model 5

Trust1 -18.505** -21.042*** 23.094Trust2 (-)164.090**Blood -13.491**Firm size -8.182*** -30.368*** -26.883*** -6.548*** -8.08***Book leverage 89.365** 129.047*** 687.598*** 73.781** 92.914**ROA -182.414*** -199.167*** -191.557** -139.738*** -176.212***Profitability volatility 27.415** 123.891* 87.036 62.434** 31.607**Sales growth 1.044 -0.137 -108.330** 1.562 0.798Loan size -2.254* -5.018** -8.348* -2.330* -2.040*Costant -142.268 -462.783** 115.846** -452.856* -190.869

Loan purpose fixe effects Yes Yes Yes Yes YesIndustry fixed effects Yes Yes Yes Yes Yesclustered standard errors Firm Firm Firm Firm FirmLocal partners in loan syndicate NA Yes No NA NA

Observations 177 128 49 177 177F-statistic 2.71** 2.82*** 4.58*** 3.74*** 2.49**Adjusted R-squared 0.1112 0.2185 0.083 0.0936 0.1047

Dependent variable: All-in-spread drawn

Other price terms: fees

04/18/23Conference on China's Financial Intermediation

15

Independent variables

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Trust1 -1.396** -1.485*** 1.089Trust2 -2.694** -6.354** 1.049Firm size -1.349* -1.279* -1.240** -1.477*** -0.109 0.198Book leverage -5.894* -1.735* -3.483** -1.816* 9.376 2.552ROA 17.012 -1.094 13.786 16.057 3.226 -17.151Profitability volatility -67.758 -69.531 -23.910 -27.473 -43.848 -42.058Sales growth -0.726 -0.577 -0.493 -0.586 -0.233 0.009Loan size -0.101* -0.069* -0.038* -0.078* -0.063 0.009Costant 39.415** 17.156* 29.314*** 53.103* 0.001 0.259

Loan purpose fixe effects Yes Yes Yes Yes Yes YesIndustry fixed effects Yes Yes Yes Yes Yes Yesclustered standard errors Firm Firm Firm Firm Firm Firm

Observations 177 177 177 177 177 177F-statistic 3.43*** 2.81*** 2.49** 2.53** 2.74** 2.32**Adjusted R-squared 0.0748 0.0636 0.0547 0.0612 0.0699 0.1027

Dependent variableTotal fees Upfront fee Commitment fee

Nonprice terms

04/18/23Conference on China's Financial Intermediation

16

Independent variables

AISD Maturity Collateral AISD Maturity CollateralModel 1 Model 2 Model 3 Model 4 Model 5 Model 6

Trust1 -19.901** 0.051 -0.039** (-)10.596** 0.178 -0.091**Maturity -9.991** 0.143*** -244.194*** 0.243**Collateral 20.256*** 0.621*** 103.702*** 0.829***Firm size -7.029*** 0.075** -0.070*** 90.665*** 0.362*** -0.060*Book leverage 28.327** 1.276*** -0.793*** 7.539 0.021 -0.070***ROA -134.653*** 3.915*** -0.975* -224.835** 1.509 -0.411**Profitability volatility 42.250* 5.105** -1.204 1,130.098*** 3.634** -0.206Sales growth 0.616 0.013 -0.010 546.753 1.952 -1.170Loan size -6.005** 0.263*** -0.007 -4.195 0.014* -0.016Costant -133.792 -3.591*** 1.504*** -1,020.195* -4.458 1.064

Loan purpose fixed effects Yes Yes Yes Yes Yes YesIndustry fixed effects Yes Yes Yes Yes Yes Yesclustered standard errors Firm Firm Firm Firm Firm FirmObservations 164 164 164 164 164 164F-statistic 2.768** 11.72*** 5.08***Chi-square 31.13*** 63.87*** 25.03***Adjusted R-squared 0.1100 0.3447 0.1699 0.1254 0.1611 0.0764

OLS 3SLSDependent variable

Interaction effect of trust and instituions

04/18/23Conference on China's Financial Intermediation

17

Independent variablesModel 1 Model 2 Model 3

Trust1 -54.65** -60.845*** -13.491**Rule of law -324.284***Trust1 * Rule of law 60.124**Financial development -12.208*Trust1 * Financial development 3.897**Business protection -157.847***Trust1 * Business protection 30.173*Firm size 9.564 3.005 4.298Book leverage 39.526 7.054 75.113ROA 95.556 12.853 169.944Profitability volatility 12.170 -212.184 140.904Sales growth 2.319 1.985 0.900Loan size 4.737 3.262 0.837Costant 30.056 137.987 83.325Loan purpose fixe effects Yes Yes YesIndustry fixed effects Yes Yes Yesclustered standard errors Firm Firm Firm

Observations 177 177 177F-statistic 3.19** 2.23** 2.93***Adjusted R-squared 0.1287 0.0945 0.1639

Dependent variable: All-in-spread drawn (AISD)

Take away…

Social trust is negatively correlated with cost of bank loans The negative effect is more pronounced for syndicated

loans with local partner

Social trust is negatively correlated with fees The negative effect is more pronounced for upfront fees

Social trust is negatively correlated with the likelihood of collateral usage but insignificantly related to loan maturity

The effect of social trust is weaker whether there exists better formal institutional development

04/18/23Conference on China's Financial Intermediation

18

![FORDHAM #3 of 3; Fordham v Hobson (Dewsash) (Home.B) [2013] NSWCTTT 590](https://img.pdfslide.us/doc/110x75/55cf29a9bb61ebb2668b4659/fordham-3-of-3-fordham-v-hobson-dewsash-homeb-2013-nswcttt-590.jpg)