Embed Size (px)

Citation preview

IFRS News

Welcome to IFRS News – a quarterly update fromthe Grant ThorntonInternational IFRS team.IFRS News offers asummary of the moresignificant developments in International FinancialReporting Standards(IFRS) along with insightsinto topical issues andcomments and views from the Grant ThorntonInternational IFRS team.

Our third edition of 2012 starts with alook at how work is progressing on themain IFRS and US GAAP convergenceprojects, before focussing in detail onthe new Standards that have beenpublished in the last quarter and thedocuments the IASB has issued forpublic comment.

We then turn to IFRS-related newsat Grant Thornton, including thepublication of our updated exampleinterim IFRS financial statements andour updated US GAAP comparisonguide. We end with a more generalround-up of activities affecting theIASB, and the implementation dates ofnewer Standards that are not yetmandatory.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for comment

IFRS News Quarter 3 2012 1

Round up Effective dates

Update on IFRS and US GAAP convergence

At the end of April, the IASB and FASBissued a ‘Joint Update Note’ on theconvergence of their respectiveStandards.

The update note throws further lighton the plans for completion of the fourremaining convergence projects that wediscussed in the last edition of IFRSNews. We outline some of the mainpoints below.

Financial instrumentsClassification and measurement• the IASB is continuing to deliberate

on making limited-scope changes toIFRS 9

• both the IASB and the FASB arefocussing on discussing whichinstruments are eligible foramortised cost accounting, whetherthere is a need for bifurcation offinancial assets (and, if so, the basisfor bifurcation), the basis for andscope of a possible thirdclassification category (debtinstruments measured at fair value

through other comprehensiveincome); and any knock-on effect ofsuch a decision

• an Exposure Draft is planned for thefourth quarter of 2012.

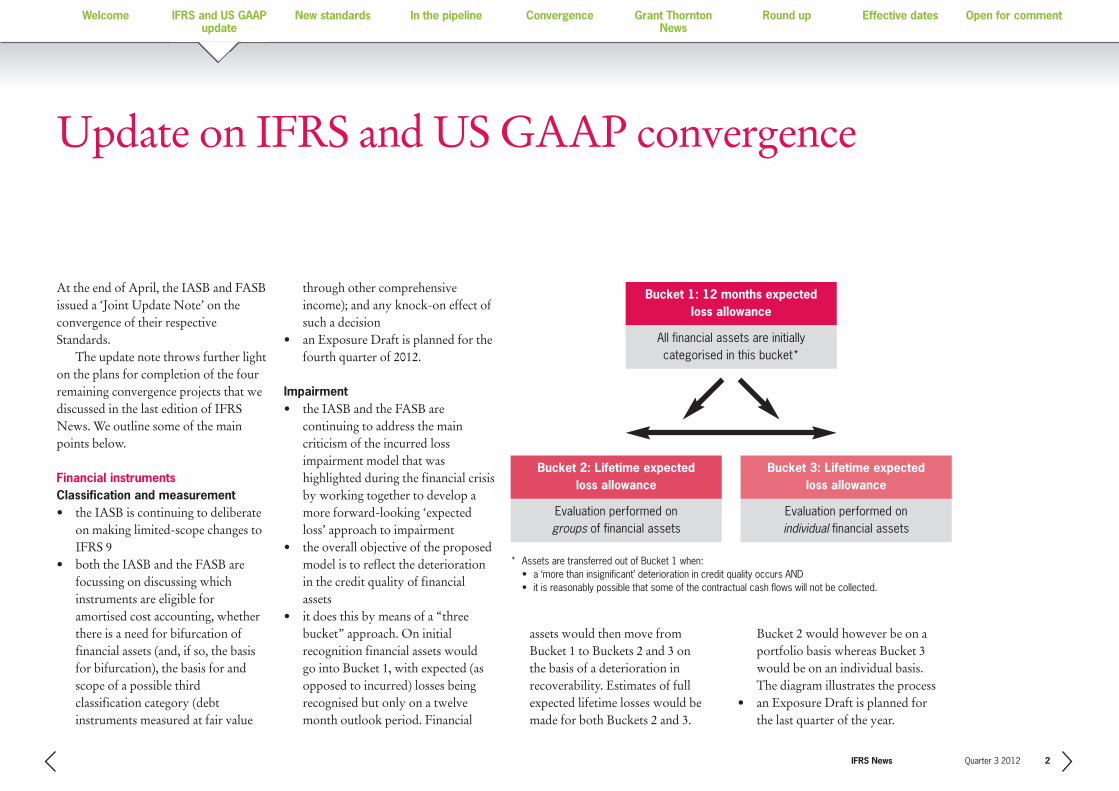

Impairment • the IASB and the FASB are

continuing to address the maincriticism of the incurred lossimpairment model that washighlighted during the financial crisisby working together to develop amore forward-looking ‘expectedloss’ approach to impairment

• the overall objective of the proposedmodel is to reflect the deteriorationin the credit quality of financialassets

• it does this by means of a “threebucket” approach. On initialrecognition financial assets would go into Bucket 1, with expected (asopposed to incurred) losses beingrecognised but only on a twelvemonth outlook period. Financial

IFRS News Quarter 3 2012 2

assets would then move from Bucket 1 to Buckets 2 and 3 on the basis of a deterioration inrecoverability. Estimates of fullexpected lifetime losses would bemade for both Buckets 2 and 3.

Bucket 2 would however be on aportfolio basis whereas Bucket 3would be on an individual basis. The diagram illustrates the process

• an Exposure Draft is planned for the last quarter of the year.

Bucket 1: 12 months expected loss allowance

All financial assets are initially categorised in this bucket*

Bucket 2: Lifetime expected loss allowance

Evaluation performed on groups of financial assets

Bucket 3: Lifetime expected loss allowance

Evaluation performed on individual financial assets

* Assets are transferred out of Bucket 1 when:• a ‘more than insignificant’ deterioration in credit quality occurs AND• it is reasonably possible that some of the contractual cash flows will not be collected.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Hedging The IASB has divided the hedging partof its financial instruments project intotwo parts: General hedge accountingand macro hedge accounting:

General hedge accounting• publication of the part of the final

Standard dealing with general hedgeaccounting is expected in the secondhalf of this year

• it is expected that it will be easier toapply hedge accounting, withremoval of the 80-125% ‘bright line’that currently marks the maximumpermitted range of hedgeineffectiveness, and better alignmentbetween hedge accounting and actualrisk management practices

• it will however not be possible tovoluntarily discontinue hedgeaccounting while the underlying riskmanagement strategy remains thesame. As a result, adequatedocumentation of the hedgeaccounting relationship will be moreimportant than ever.

IFRS News Quarter 3 2012 3

Macro hedge accounting • the second part of the hedge

accounting project considers macrohedging (risk management strategiesreferring to open portfolios heldprimarily by financial institutions)

• at the moment this part of theproject is focussed on interest raterisk management within the bankingindustry, but other risks andindustries will be considered in duecourse

• a discussion paper is planned for thesecond half of 2012, which will elicitviews on a broader range ofaccounting alternatives.

Revenue• the two Boards are currently

considering the feedback receivedfrom the November 2011 ExposureDraft

• at the date of publication of the JointUpdate Note, the two Boardsenvisaged a final Standard beingissued in early 2013. The IASB’slatest work plan however does notshow an anticipated date ofpublication of the Final Standard.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Leases • the two Boards are not planning to

reconsider their overall decision thatall leases should be recorded on thebalance sheet

• the Boards are howeverredeliberating whether the ‘front-loaded’ profit and loss profile forlessees that would result from theapproach proposed in their previousExposure Drafts is appropriate forall leases (see our separate article‘update on lease accounting project’later in the newsletter for moredetail).

Insurance contracts• the Boards are developing a model

that would reflect current estimatesof the amount necessary to fulfil aninsurance obligation

• at present the Boards have notreached consistent conclusions aboutseveral elements of the model. Giventhe strong desire for a globalStandard on insurance however, theBoards are making a conscious effortto understand each other’s decisionsand to resolve differences wherepossible

• a review draft of a final Standard or anew Exposure Draft is expected tobe published before the end of theyear.

IFRS News Quarter 3 2012 4

SEC publishes final staff report on IFRS Work PlanThe Office of the Chief Accountant of the Securities and Exchange Commission(SEC) has published its final staff report on the ‘Work Plan for the Consideration ofIncorporating International Financial Reporting Standards into the FinancialReporting System for US Issuers’.The highly awaited report takes care to emphasise that its publication does not

imply that the SEC has made any policy decision as to whether IFRSs should beincorporated into the financial reporting system for US issuers, or how any suchincorporation, were it to occur, should be implemented.It instead examines IFRS and the arguments for and against various forms of

adoption. The report notes that it became clear to the SEC staff early on in theprocess that an outright switch to IFRS was not supported by the vast majority ofUS participants. The SEC staff also note that IFRS has become morecomprehensive but still has some gaps, and that the IFRS Foundation (the IASB’sparent) needs to shore up and broaden its funding base. The report also observesthat IFRS lacks many industry-specific standards. The IASB reacted to the report by noting that many of the challenges expressed

in the report were challenges which had been faced by other jurisdictions and whichhad been successfully overcome by them. Regret was also expressed that thereport was not accompanied by a recommended action plan for the SEC, withMichel Prada, Chairman of the Trustees of the IFRS Foundation, stating that “giventhe achievements of the convergence programme inspired by repeated calls of theG20 for global accounting standards, a clear action plan would be welcome”.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

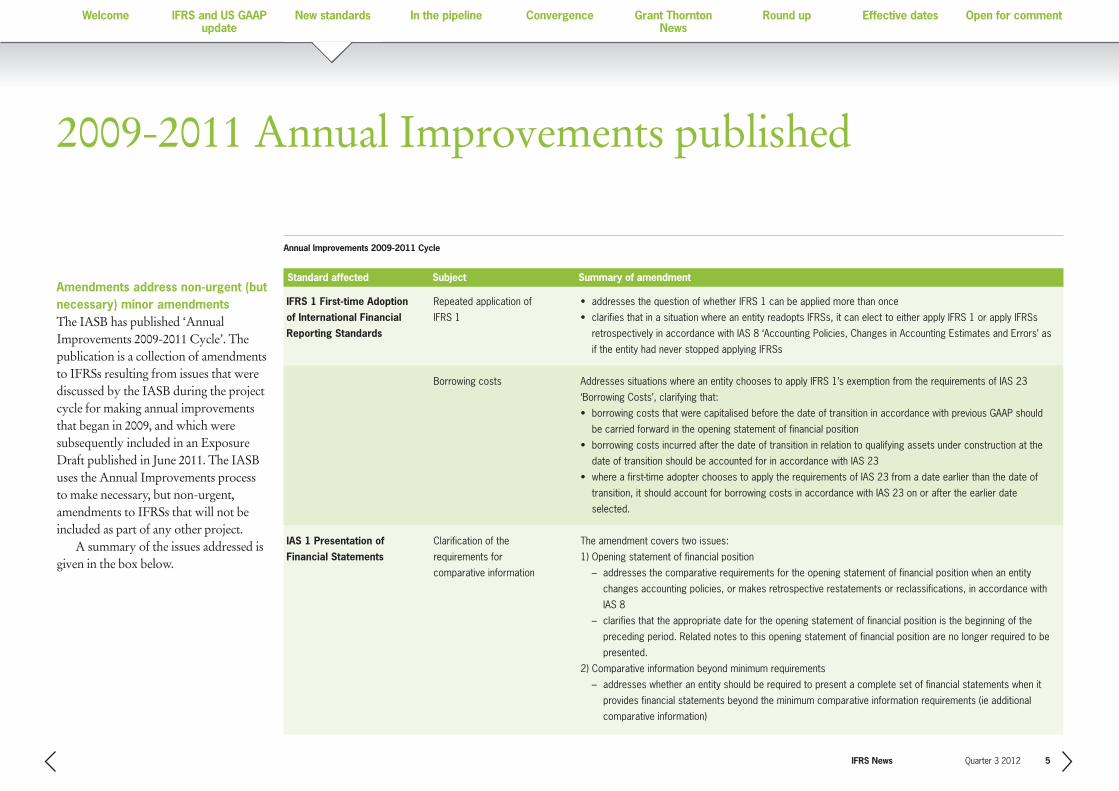

2009-2011 Annual Improvements published

Amendments address non-urgent (butnecessary) minor amendmentsThe IASB has published ‘AnnualImprovements 2009-2011 Cycle’. Thepublication is a collection of amendmentsto IFRSs resulting from issues that werediscussed by the IASB during the projectcycle for making annual improvementsthat began in 2009, and which weresubsequently included in an ExposureDraft published in June 2011. The IASBuses the Annual Improvements processto make necessary, but non-urgent,amendments to IFRSs that will not beincluded as part of any other project.

A summary of the issues addressed isgiven in the box below.

IFRS News Quarter 3 2012 5

Annual Improvements 2009-2011 Cycle

Standard affected Subject Summary of amendment

IFRS 1 First-time Adoption

of International Financial

Reporting Standards

IAS 1 Presentation of

Financial Statements

Repeated application of

IFRS 1

Borrowing costs

Clarification of the

requirements for

comparative information

• addresses the question of whether IFRS 1 can be applied more than once

• clarifies that in a situation where an entity readopts IFRSs, it can elect to either apply IFRS 1 or apply IFRSs

retrospectively in accordance with IAS 8 ‘Accounting Policies, Changes in Accounting Estimates and Errors’ as

if the entity had never stopped applying IFRSs

Addresses situations where an entity chooses to apply IFRS 1’s exemption from the requirements of IAS 23

‘Borrowing Costs’, clarifying that:

• borrowing costs that were capitalised before the date of transition in accordance with previous GAAP should

be carried forward in the opening statement of financial position

• borrowing costs incurred after the date of transition in relation to qualifying assets under construction at the

date of transition should be accounted for in accordance with IAS 23

• where a first-time adopter chooses to apply the requirements of IAS 23 from a date earlier than the date of

transition, it should account for borrowing costs in accordance with IAS 23 on or after the earlier date

selected.

The amendment covers two issues:

1) Opening statement of financial position

– addresses the comparative requirements for the opening statement of financial position when an entity

changes accounting policies, or makes retrospective restatements or reclassifications, in accordance with

IAS 8

– clarifies that the appropriate date for the opening statement of financial position is the beginning of the

preceding period. Related notes to this opening statement of financial position are no longer required to be

presented.

2) Comparative information beyond minimum requirements

– addresses whether an entity should be required to present a complete set of financial statements when it

provides financial statements beyond the minimum comparative information requirements (ie additional

comparative information)

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

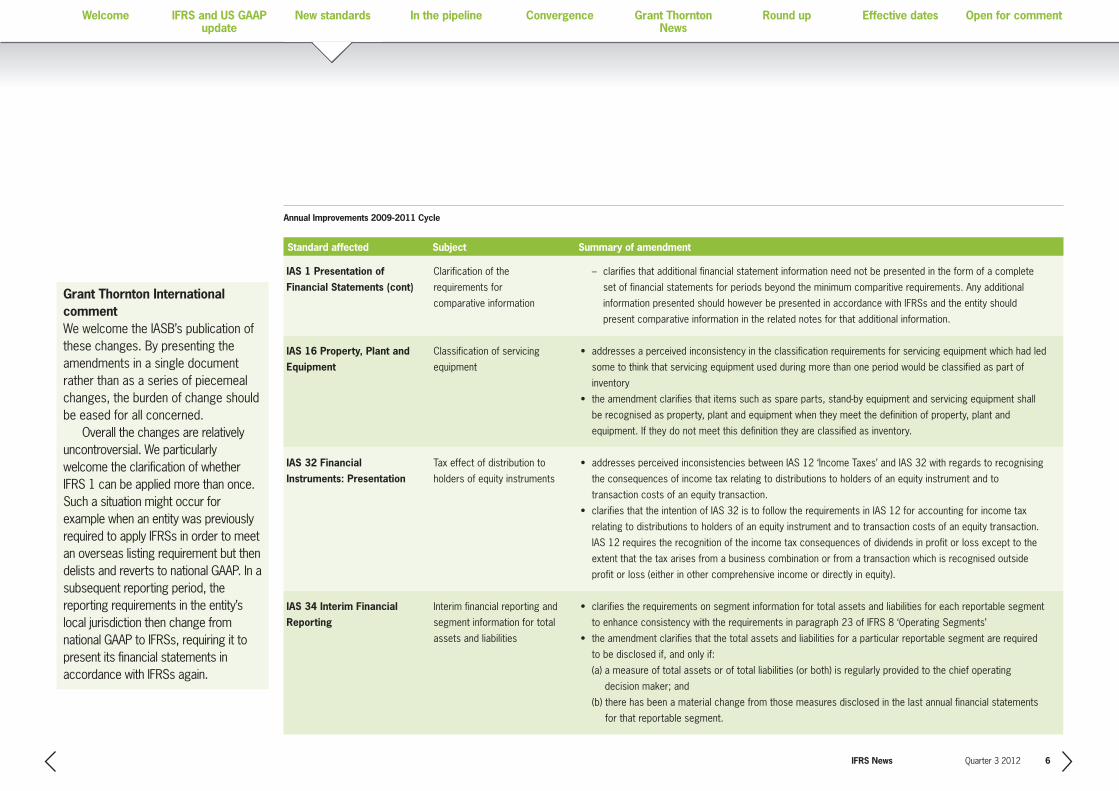

Annual Improvements 2009-2011 Cycle

Standard affected Subject Summary of amendment

IAS 1 Presentation of

Financial Statements (cont)

IAS 16 Property, Plant and

Equipment

IAS 32 Financial

Instruments: Presentation

IAS 34 Interim Financial

Reporting

Clarification of the

requirements for

comparative information

Classification of servicing

equipment

Tax effect of distribution to

holders of equity instruments

Interim financial reporting and

segment information for total

assets and liabilities

– clarifies that additional financial statement information need not be presented in the form of a complete

set of financial statements for periods beyond the minimum comparitive requirements. Any additional

information presented should however be presented in accordance with IFRSs and the entity should

present comparative information in the related notes for that additional information.

• addresses a perceived inconsistency in the classification requirements for servicing equipment which had led

some to think that servicing equipment used during more than one period would be classified as part of

inventory

• the amendment clarifies that items such as spare parts, stand-by equipment and servicing equipment shall

be recognised as property, plant and equipment when they meet the definition of property, plant and

equipment. If they do not meet this definition they are classified as inventory.

• addresses perceived inconsistencies between IAS 12 ‘Income Taxes’ and IAS 32 with regards to recognising

the consequences of income tax relating to distributions to holders of an equity instrument and to

transaction costs of an equity transaction.

• clarifies that the intention of IAS 32 is to follow the requirements in IAS 12 for accounting for income tax

relating to distributions to holders of an equity instrument and to transaction costs of an equity transaction.

IAS 12 requires the recognition of the income tax consequences of dividends in profit or loss except to the

extent that the tax arises from a business combination or from a transaction which is recognised outside

profit or loss (either in other comprehensive income or directly in equity).

• clarifies the requirements on segment information for total assets and liabilities for each reportable segment

to enhance consistency with the requirements in paragraph 23 of IFRS 8 ‘Operating Segments’

• the amendment clarifies that the total assets and liabilities for a particular reportable segment are required

to be disclosed if, and only if:

(a) a measure of total assets or of total liabilities (or both) is regularly provided to the chief operating

decision maker; and

(b) there has been a material change from those measures disclosed in the last annual financial statements

for that reportable segment.

IFRS News Quarter 3 2012 6

Grant Thornton Internationalcomment We welcome the IASB’s publication ofthese changes. By presenting theamendments in a single documentrather than as a series of piecemealchanges, the burden of change shouldbe eased for all concerned.Overall the changes are relatively

uncontroversial. We particularlywelcome the clarification of whetherIFRS 1 can be applied more than once.Such a situation might occur forexample when an entity was previouslyrequired to apply IFRSs in order to meetan overseas listing requirement but thendelists and reverts to national GAAP. In asubsequent reporting period, thereporting requirements in the entity’slocal jurisdiction then change fromnational GAAP to IFRSs, requiring it topresent its financial statements inaccordance with IFRSs again.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

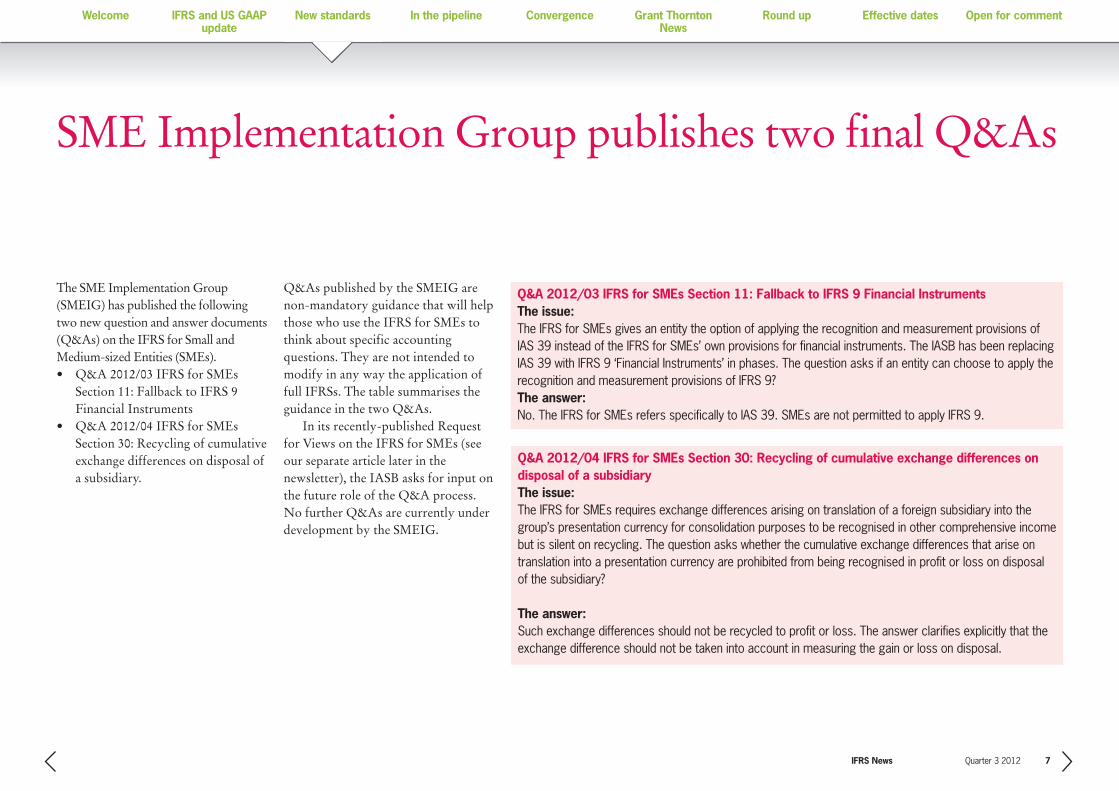

SME Implementation Group publishes two final Q&As

The SME Implementation Group(SMEIG) has published the followingtwo new question and answer documents(Q&As) on the IFRS for Small andMedium-sized Entities (SMEs). • Q&A 2012/03 IFRS for SMEs

Section 11: Fallback to IFRS 9Financial Instruments

• Q&A 2012/04 IFRS for SMEsSection 30: Recycling of cumulativeexchange differences on disposal ofa subsidiary.

Q&As published by the SMEIG arenon-mandatory guidance that will helpthose who use the IFRS for SMEs tothink about specific accountingquestions. They are not intended tomodify in any way the application offull IFRSs. The table summarises theguidance in the two Q&As.

In its recently-published Requestfor Views on the IFRS for SMEs (seeour separate article later in thenewsletter), the IASB asks for input onthe future role of the Q&A process.No further Q&As are currently underdevelopment by the SMEIG.

IFRS News Quarter 3 2012 7

Q&A 2012/03 IFRS for SMEs Section 11: Fallback to IFRS 9 Financial InstrumentsThe issue:The IFRS for SMEs gives an entity the option of applying the recognition and measurement provisions ofIAS 39 instead of the IFRS for SMEs’ own provisions for financial instruments. The IASB has been replacingIAS 39 with IFRS 9 ‘Financial Instruments’ in phases. The question asks if an entity can choose to apply therecognition and measurement provisions of IFRS 9? The answer: No. The IFRS for SMEs refers specifically to IAS 39. SMEs are not permitted to apply IFRS 9.

Q&A 2012/04 IFRS for SMEs Section 30: Recycling of cumulative exchange differences ondisposal of a subsidiaryThe issue:The IFRS for SMEs requires exchange differences arising on translation of a foreign subsidiary into thegroup’s presentation currency for consolidation purposes to be recognised in other comprehensive incomebut is silent on recycling. The question asks whether the cumulative exchange differences that arise ontranslation into a presentation currency are prohibited from being recognised in profit or loss on disposalof the subsidiary?

The answer: Such exchange differences should not be recycled to profit or loss. The answer clarifies explicitly that theexchange difference should not be taken into account in measuring the gain or loss on disposal.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Amendments to IFRS 10, IFRS 11 and IFRS 12 – transition guidance

Amendments to IFRS 10, IFRS 11 andIFRS 12 – transition guidanceThe IASB has published ‘ConsolidatedFinancial Statements, JointArrangements and Disclosure ofInterests in Other Entities: TransitionGuidance – Amendments to IFRS 10,IFRS 11 and IFRS 12’.

The amendments clarify thetransition guidance in IFRS 10‘Consolidated Financial Statements’.

They also provide additional transitionrelief in IFRS 10, IFRS 11 ‘JointArrangements’ and IFRS 12 ‘Disclosureof Interests in Other Entities’, limitingthe requirement to provide adjustedcomparative information to only thepreceding comparative period. Inaddition, for disclosures related tounconsolidated structured entities, theamendments remove the requirementto present comparative information forperiods before IFRS 12 is first applied.

IFRS News Quarter 3 2012 8

Grant Thornton International comment We welcome the Amendments. We believe they will help to improve the clarity andthe consistent application of the transition requirements in IFRS 10, 11 and 12. Wealso believe that this pragmatic approach will not adversely affect the interests ofthe users of the financial statements.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IFRS News Quarter 3 2012 9

2010-2012 Annual Improvements exposure draftpublished

The IASB has published ‘AnnualImprovements to IFRSs: 2010-2012Cycle’, an Exposure Draft containingproposals for amendments to elevenInternational Financial ReportingStandards. The proposed amendmentsreflect issues discussed by the IASB in aproject cycle that began in 2010. Byincluding them in a single document, theIASB aims to provide a streamlinedprocess for dealing efficiently with non-urgent but necessary amendmentsto IFRSs.

IFRSs addressed The following table lists the IFRSs andtopics addressed by the proposedamendments.

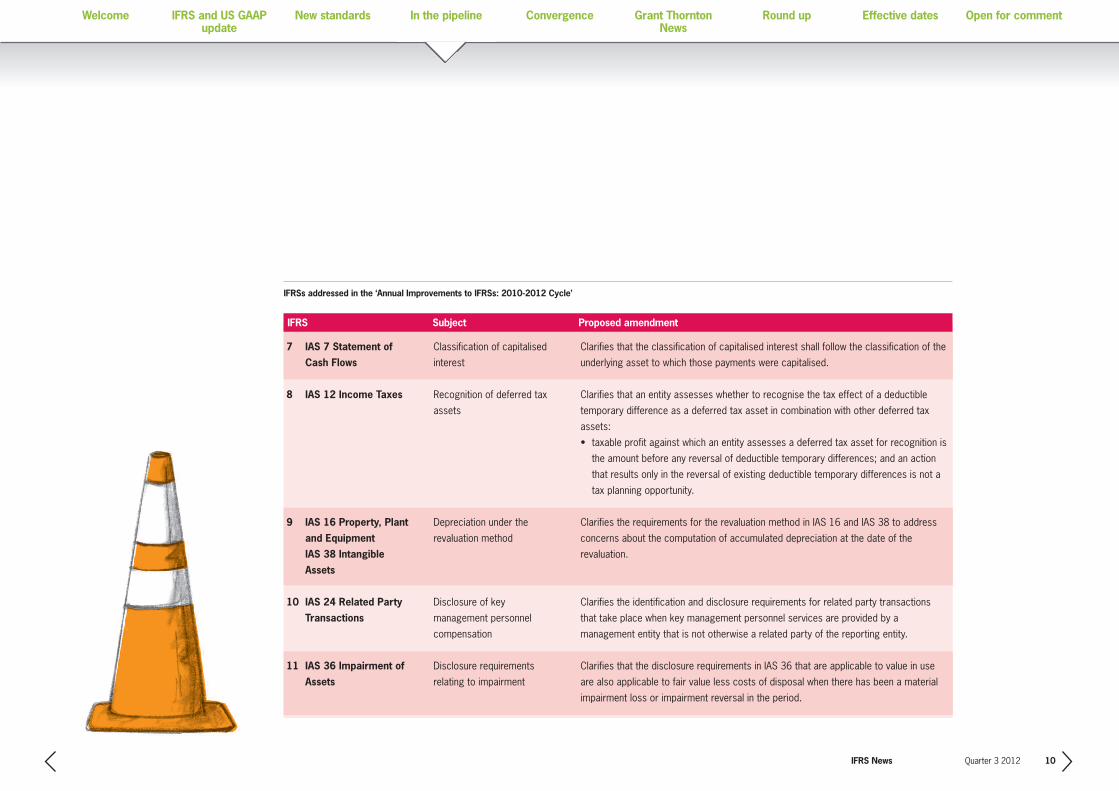

IFRSs addressed in the ‘Annual Improvements to IFRSs: 2010-2012 Cycle’

IFRS Subject Proposed amendment

1 IFRS 2 Share-based

Payment

2 IFRS 3 Business

Combinations

3 IFRS 8 Operating

Segments

4 IFRS 8 Operating

Segments

5 IFRS 13 Fair Value

Measurement

6 IAS 1 Presentation of

Financial Statements

Definition of ‘vesting

conditions’

Classification of contingent

consideration

Aggregation of reportable

segments

Reconciliation of reportable

segments’ assets

Exemption from discounting

for short-term receivables and

payables

Non-current classification

Clarifies the definition of ‘vesting conditions’ by separately defining a ‘performance

condition’ and a ‘service condition’.

Clarifies that contingent consideration is assessed as either a liability or an equity

instrument only on the basis of the requirements of IAS 32 ‘Financial Instruments:

Presentation’; and, that contingent consideration that is not classified as an equity

instrument is subsequently measured at fair value, with the corresponding gain or loss

being recognised either in profit or loss or other comprehensive income in accordance

with IFRS 9.

Requires entities to disclose factors used to identify the entity’s reportable segments

when operating segments have been aggregated.

Clarifies that a reconciliation of the total of the reportable segments’ assets to the

entity’s assets should be disclosed, if that amount is regularly provided to the chief

operating decision maker.

Explains that the deletion of this exemption in IAS 39 and IFRS 9 (on publication of

IFRS 13) was not intended to change practice.

Clarifies that classifying a liability as non-current on the basis of an ability and

expectation to roll over or refinance the obligation is possible only if there is an existing

loan facility with the same lender, on the same or similar terms.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IFRS News Quarter 3 2012 10

IFRSs addressed in the ‘Annual Improvements to IFRSs: 2010-2012 Cycle’

IFRS Subject Proposed amendment

7 IAS 7 Statement of

Cash Flows

8 IAS 12 Income Taxes

9 IAS 16 Property, Plant

and Equipment

IAS 38 Intangible

Assets

10 IAS 24 Related Party

Transactions

11 IAS 36 Impairment of

Assets

Classification of capitalised

interest

Recognition of deferred tax

assets

Depreciation under the

revaluation method

Disclosure of key

management personnel

compensation

Disclosure requirements

relating to impairment

Clarifies that the classification of capitalised interest shall follow the classification of the

underlying asset to which those payments were capitalised.

Clarifies that an entity assesses whether to recognise the tax effect of a deductible

temporary difference as a deferred tax asset in combination with other deferred tax

assets:

• taxable profit against which an entity assesses a deferred tax asset for recognition is

the amount before any reversal of deductible temporary differences; and an action

that results only in the reversal of existing deductible temporary differences is not a

tax planning opportunity.

Clarifies the requirements for the revaluation method in IAS 16 and IAS 38 to address

concerns about the computation of accumulated depreciation at the date of the

revaluation.

Clarifies the identification and disclosure requirements for related party transactions

that take place when key management personnel services are provided by a

management entity that is not otherwise a related party of the reporting entity.

Clarifies that the disclosure requirements in IAS 36 that are applicable to value in use

are also applicable to fair value less costs of disposal when there has been a material

impairment loss or impairment reversal in the period.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IASB invites comments on review of the IFRS for SMEs

The IASB has issued a Request forInformation as the first step in its initialcomprehensive review of the IFRS forSMEs.

When it issued the IFRS for SMEs inJuly 2009, the IASB said it would assessthe Standard after entities had had twoyears’ experience in implementing it.The IASB also said that, after the initialreview, it expected to consideramendments to the IFRS for SMEsapproximately once every three years.

The Request for Information seekspublic views on whether there is a needto make any amendments to the IFRSfor SMEs and, if so, what amendmentsshould be made. It asks specificquestions on particular sections of theIFRS for SMEs, as well as generalquestions about respondents’ experiencewith it. Respondents are alsoencouraged to raise any other issues thatthey want to put forward. Among thespecific questions are whether anychanges to the IFRS for SMEs areneeded as a result of the revisedrequirements in new and amended IFRSsthat have been published after the IFRSfor SMEs was issued in July 2009. Theseinclude IFRS 10 ‘Consolidated FinancialStatements’, IFRS 11 ‘JointArrangements’, IFRS 13 ‘Fair ValueMeasurement’ and IAS 19 ‘EmployeeBenefits (revised)’.

The IASB’s SME ImplementationGroup (SMEIG) worked closely withIASB staff to develop the Request forInformation. Frank Timmins, a seniorpartner in our South African firm,represents Grant Thornton on theSMEIG.

After consideration of the responsesto the Request for Information, theIASB anticipates publishing anExposure Draft of proposedamendments to the Standard in the firsthalf of 2013. The IASB plans to publishthe final revisions in the second half of2013 or the first half of 2014.

IFRS News Quarter 3 2012 11

Breaking newsThe IASB had just published a Requestfor Information ‘Post-implementationReview: IFRS 8 Operating Segments’ at the time of going to press. Post-implementation reviews are

intended to make sure that major newStandards are working as intended. The document asks for information onpeople’s experience of implementingIFRS 8, looking at matters such as themanagement perspective approach tosegment identification taken in theStandard. The Request for Information will

be featured in more detail in the nextedition of IFRS News.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IFRS News Quarter 3 2012 12

Draft IFRIC Interpretations published

The IFRS Interpretations Committee(IFRIC) has published two draftinterpretations for public comment:• ‘Put Options Written on Non-

controlling Interests’• ‘Levies Charged by Public

Authorities on Entities that Operatein a Specific Market’.

Put Options Written on Non-controlling InterestsThe draft IFRIC would apply to a put option written by a parent on the shares of its subsidiary held by a non-controlling interestshareholder that, if exercised, obliges the parent to purchase those shares. IFRS requires a financial liability to be recognised in such asituation for the present value of the redemption amount of the shares.

The issue addressed by the draft IFRICThe draft IFRIC addresses a possible conflict between IAS 32 and IAS 27: IAS 32 requires that the financial liability is subsequentlymeasured in accordance with IAS 39 or IFRS 9. Those Standards require that all changes in the measurement of such financial liabilitiesare recognised in profit or loss. IAS 27 (and IFRS 10 going forward) on the other hand requires that changes in a parent’s ownershipinterest in a subsidiary that do not result in a loss of control are accounted for as equity transactions, meaning that no gain or losswould be recognised.

The proposed approach The draft IFRIC proposes that changes in the measurement of the financial liability would be required to be recognised in profit or lossin accordance with IAS 39 or IFRS 9. IFRIC’s justification for this approach is that changes in the measurement of the financial liabilitydo not change the relative interests in the subsidiary held by the parent and the non-controlling-interest shareholder. Accordingly, writinga put option to a non-controlling-interest shareholder is not an equity transaction.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IFRS News Quarter 3 2012 13

Levies Charged by Public Authorities on Entities that Operate in a Specific MarketThe draft IFRIC addresses the accounting for levies charged by public authorities (national governments, regional governments, localauthorities, and their component entities) on entities that operate in a specific market. A number of such levies were raised followingthe global financial crisis, particularly on banks.

The proposed approachThe draft IFRIC asserts that such levies are not within the scope of IAS 12 ‘Income Taxes’, and therefore proposes to account for themas a provision under IAS 37 ‘Provisions, Contingent Liabilities and Contingent Assets’.The consensus reached by the draft IFRIC is that the obligating event that gives rise to a liability is the activity that triggers the

payment of the levy as identified by the legislation. This means that, for a levy that is triggered by operating in a specific market on aspecific date, the entire expense is recognised on that date (rather than being spread over time). This point in time approach wouldapply even if the amount of the levy is based on financial measures from an earlier date or period. The draft IFRIC specifically rejects the argument that an entity has a constructive obligation to pay a levy that will arise from

operating in a future period as a result of being economically compelled to continue operating in that future period. The IFRIC’sjustification is that such an approach would result in recognising a current period expense for future operating costs.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Update on lease accounting project

The IASB and the US FinancialAccounting Standards Board (FASB)have reached agreement on an approachfor lessee accounting for lease expensesas part of their joint project to reviselease accounting. Many commentatorshave expressed concern about the ‘front-loading’ impact of the Boards’ previousproposal.

The two Boards had previouslyagreed that lessees should record allleases (except short-term leases) on thebalance sheet, but have been continuingto discuss the appropriate classificationand pattern of expenses in the incomestatement. They have now reached ageneral agreement on these issues.

Under their agreed approach:• leases that convey a relatively small

percentage of the life or value of theleased asset, such as many propertyleases, will be recognised as astraight-line lease expense

• other leases, including manyequipment leases, would berecognised in accordance with themethod proposed in the ExposureDraft that was issued jointly by theIASB and FASB in 2010. Under thatapproach, interest would berecognised on the lease liability andas amortisation of the “right of useasset”. This approach results in ahigher level of interest expense beingrecognised in the earlier years of alease, leading to the front-loadingeffect referred to above.

The IASB and FASB plan to issueanother Exposure Draft in the fourthquarter of 2012, that will set out theiragreed approach in more detail forpublic comment.

IFRS News Quarter 3 2012 14

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Findings from Canada’s transition to IFRS

Following Canada’s adoption of IFRSfor publicly accountable enterprises foryears beginning on or after 1 January2011, the majority of those companieshave now completed their transition andcan breathe a little easier. Set out beloware some observations that RaymondChabot Grant Thornton (RCGT), one of our Canadian member firms, madeduring the transition process. Theirfindings will be of use to othercompanies around the world who aremaking the move to IFRS.

Transition-related findings• as expected, there was a significant

increase in the volume of notes tofinancial statements, mainly pertainingto the transition itself, management’ssignificant judgements regarding theapplication of accounting policies,uncertainty surrounding criticalestimates, goodwill and impairmenttesting, impairment losses, andbusiness combinations

• smaller entities experienceddifficulties in adapting their financialstatements to IFRSs, notably when itcame to classifying financialinstruments, recognising deferredtaxes and drafting notes on thesignificant accounting policies, taxes,related party transactions and thetransition itself. However, severalpreparers said that Grant Thornton’sexample financial statements were ofgreat help to them in easing theseproblems

• the most frequent and significanttransition-related adjustments amongRCGT’s clients notably involved therecognition of flow-through shares(mining sector), share-basedpayments (portions considered asseparate awards and forfeitures) anddefined benefit plans (actuarial gainsand losses).

RCGT noted that the work involved inthe preparation of the first annual IFRSfinancial statements seems to have beenmuch easier for entities that investedsufficient time and effort in the yearspreceding the transition and during theinterim periods of the transition yearitself. Additionally, auditing thesefinancial statements was easier whenauditors had previously performed workon the IFRS opening balance sheet, IFRSfinancial statement templates andtransition-year quarterly financialstatements.

What lies ahead?With transition to IFRS complete,Canadian publicly accountableenterprises could be forgiven forexpecting to have some respite. RCGTencourages such entities to continue toimprove the quality of their financialstatements however. They note thatdoing so can only be beneficial andimprove the perception of investors,

lenders, regulatory authorities andanalysts. In addition, thought should begiven to major new IFRSs that haverecently been published (onconsolidations and fair valuemeasurement) and those underdevelopment that will become applicable in the coming years.

IFRS News Quarter 3 2012 15

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

New Grant Thornton International example interimIFRS financial statements released

The Grant Thornton International IFRSteam has published an updated versionof its IFRS ‘Example InterimConsolidated Financial Statements’.

The previous version has beenreviewed and updated to reflect changesin IFRSs that are effective for the yearending 31 December 2012. Thepublication also reflects the early-adoption of ‘Presentation of Items ofOther Comprehensive Income(Amendments to IAS 1 Presentation ofFinancial Statements)’ which is effectivefor annual periods beginning on or after1 July 2012.

To obtain a copy of the publication,please get in touch with the IFRScontact in your local Grant Thorntonoffice.

IFRS News Quarter 3 2012 16

EXAMPLE INTERIM CONSOLIDATED FINANCIAL STATEMENTS 2012

Illustrative Corporation Group30 June 2012

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

IFRS training in Canada

Raymond Chabot Grant Thornton, oneof our two member firms in Canada, iscollaborating with the world-renownedtraining company IASeminars toprovide French training sessions onIFRS in Montréal.

A series of seminars is planned forthe autumn of 2012, covering a varietyof topics including financial instruments,business combinations, share-basedpayment, and accounting for deferredtax as well as the IASB’s new standardson consolidation and fair valuemeasurement.

IFRS News Quarter 3 2012 17

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Comment letter on business combinations undercommon control

The Grant Thornton International IFRSTeam has submitted a comment letter onthe Discussion Paper ‘Accounting forBusiness Combinations under CommonControl’ developed by the EuropeanFinancial Reporting Advisory Group(EFRAG) and the Italian standard-setter, the Organismo Italiano diContabilità (OIC).

In our letter, we: • welcomed the Paper as an important

contribution to the debate on thisissue and a stimulus for futurestandard-setting activity

• questioned whether approaching thechallenge of developing accountingprinciples for business combinationsunder common control by applyingthe logic of the IAS 8 hierarchy (assuggested in the EFRAG and OICDiscussion Paper) will yield a clearconclusion

• strongly endorsed the Paper’scomments that the application of‘predecessor accounting’ has severalvariants in practice and that thisdiversity of application isunsatisfactory

• agreed with the direction of thePaper that a practical solution shouldfocus on acquisition accounting andpredecessor accounting, which arethe approaches most commonly seenin practice

• suggested two main issues forfurther analysis by EFRAG and theIASB: – the basis for selecting between

the two methods, for examplewhether both should bepermitted as a ‘free’ accountingpolicy choice or, alternatively,whether entities should berequired to apply one or theother in particular circumstances

– practical issues on the applicationof each of the two methods.

IFRS News Quarter 3 2012 18

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

US firm focuses on interpreting IFRS in a ‘principled’ way

Our US member firm, Grant ThorntonLLP, has issued a ‘Focus on IFRS’ articleentitled ‘Interpreting IFRS in a“principled” way: IFRS InterpretationsCommittee’.

The article looks at the IFRSInterpretations Committee (IFRIC) andits work in interpreting the applicationof IFRS and providing timely guidanceon financial reporting issues notspecifically addressed in IFRS.

The article can be downloaded from the US firm’s websitehttp://www.grantthornton.com (go to Home>Grant ThorntonThinking>International FinancialReporting Standards) along with anumber of other thought leadershiparticles.

IFRS News Quarter 3 2012 19

Joseph Graziano, Retired Partner, International Matters − Technical

International Financial Reporting Standards (IFRS) are often said to be “principle-based,” meaning that they are based on clear-cut principles that can be applied without the need for detailed interpretive guidance. Even so, principle-based standards need a little interpretation once in a while. Enter the IFRS Interpretations Committee.

Providing updates and analysis of emerging issues in IFRS April 2012

Focus on IFRS

Interpreting IFRS in a “principled” way: IFRS Interpretations Committee

The IFRS Interpretations Committee (IFRIC or the Committee) assists the International Accounting Standards Board (IASB or the Board), which issues IFRS, in improving financial reporting through the timely identification, discussion, and resolution of financial reporting issues. Its mandate is to interpret the application of IFRS and to provide timely guidance on financial reporting issues not specifically addressed in IFRS. The Committee develops this guidance using a principle-based approach founded in the Conceptual Framework for Financial Reporting. The Due Process Handbook for the IFRS Interpretations Committee makes it clear that in providing interpretative guidance, the Committee should not try to create an extensive rules-oriented environment or act as an urgent issues group. The Committee meets approximately six times a year and summarizes the results of each meeting in an IFRIC Update, published electronically on the IASB website.

Three-tiered structure of the IFRS FoundationA little background on the structure of the international standard-setting process may be helpful in understanding the Committee’s role in that process. The IFRS Foundation comprises a three-tiered governance structure: the Monitoring Board, the Trustees of the IFRS Foundation, and the IASB. That structure has been established to ensure the transparency, public accountability, and independence of the international standard-setting process. The Monitoring Board provides a formal link between the Trustees of the IFRS Foundation and public authorities. That link was established to help capital market authorities effectively carry out their mandates relating to investor protection, market integrity, and capital formation. In general, the Monitoring Board, which consists of public capital market authorities, is responsible for approving the appointment of Trustees to the IFRS Foundation and for monitoring the Foundation’s activities.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Grant Thornton’s international expert groups meet

In May, the Grant ThorntonInternational IFRS InterpretationsGroup (IIG) met in the Stockholmoffice of our Swedish member firm.During the meeting they were joined byDan Brännström, Secretary General forthe Swedish Institute of accountants. MrBrännström discussed the status of theIFRS work plan with the members ofthe IIG, as well as the experiences ofSweden with IFRS issues. GrantThornton International’s IFRSInterpretations Group (IIG) consists ofa representative from each of ourmember firms in the United States,Canada, Singapore, Australia, SouthAfrica, India, the United Kingdom,France, Sweden and Germany as well asmembers of the Grant ThorntonInternational IFRS team. It meets inperson twice a year to discuss technicalmatters which are related to IFRS.

Later in May, the Grant ThorntonFinancial Instruments Working Group(FIWG) met in Grant ThorntonInternational’s London office. TheGroup discussed a number of issuesrelating to financial instruments,including the ramifications of theEurozone sovereign debt crisis. TheFIWG consists of a representative fromeach of our member firms in Germany,Greece, France, and the UnitedKingdom, the United States, Canada,New Zealand, the Philippines and Indiaas well as representatives from GrantThornton International.

IFRS News Quarter 3 2012 20

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

US GAAP versus IFRS comparison guide updated

Our US member firm has updated itspublication ‘Comparison between USGAAP and International FinancialReporting Standards’. The publication isintended to help readers identify themajor areas of similarity and differencebetween current US GAAP and IFRS. Itwill also assist those new to either USGAAP or IFRS to gain an appreciationof their major requirements.

Edition 3.0 of the publication hasbeen updated for standards issuedthrough to 31 March 2012. The guidecan be downloaded from GrantThornton LLP’s website(www.grantthornton.com).

IFRS News Quarter 3 2012 21

CompInter

n betwisoarCompal Fination

. GAA.SUen en betwial Ral Fi

P and . GAAting Sta

rdnda

IO

InterN OEDITI 3

al FinationInter.0 2102, 13rchaM

poreial R ecnanal Fi

ndating Stapor

srdnda

ran201© 2 anGrhts reserll rigA

ber firmemU.S.

rn ev

firm

PLLntonrohTtanved s

ernational Ltdornton Int ne hTm of Grant fir

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Spotlight on our IFRS Interpretations Group

Each quarter we throw a spotlight onone of the members of the IIG. Thisquarter we focus on the United States’representative:

Gary Illiano, United StatesGary Illiano is the National Partner-in-Charge, International, in our USmember firm. Gary has been a partner in the National Office of GrantThornton LLP for the past 14 years,with involvement in IFRS matters forthe last seven.

Prior to joining Grant Thornton,Gary worked at the US Securities andExchange Commission. Currently onthe Nasdaq Listing and HearingsReview Council, Gary is a formeradjunct professor at Pace University in New York.

IFRS News Quarter 3 2012 22

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Round-up

Europe moves to adopt the IASB’snew consolidations StandardsOn 1 June 2012 the AccountingRegulatory Committee (ARC) voted on aregulation that requires IFRS 10, IFRS 11,IFRS 12, IAS 27 and IAS 28 to be appliedby companies in the European Union fromthe start of financial years beginning on orafter 1 January 2014 at the latest.The decision means that companies in

the European Union will be able to earlyadopt the new consolidations standardsonce they have been endorsed by theEuropean Commission. The endorsementdecision is expected to be made in thefourth quarter of 2012.

Discussion paper looks towards adisclosure framework The European Financial ReportingAdvisory Group (EFRAG), the Autorité desNormes Comptables (ANC) in France, andthe Financial Reporting Council (FRC) inthe United Kingdom have jointly publisheda discussion paper, ‘Towards a DisclosureFramework for the Notes’.The discussion paper has been

published against a background ofconcern over the ever increasing numberof disclosure requirements that have beenintroduced into IFRS on a piecemeal basisas individual projects have beencompleted by the IASB. Many peoplebelieve that the notes to the financialstatements have as a result become a realburden and do not serve their intendedpurpose of helping users understand thenumbers in the financial statements.Rather than just re-state the problem,

the Discussion Paper sets out some keyprinciples that EFRAG, the ANC and theFRC consider essential to the design of aneffective Disclosure Framework.

ESMA publishes 2011 Activity Reporton IFRS Enforcement In June, the European Securities andMarkets Authority (ESMA) issued itsActivity Report on IFRS Enforcement in2011. The report provides an overview ofthe monitoring of compliance of financialinformation with IFRS and enforcementaction in the European Economic Area(EEA) during the year ended 31 December2011.Particular areas of concern noted in

the report include disclosures related to:fair value hierarchy of financialinstruments; disclosures of assumptionsused as part of impairment tests;presentation of risk factors anduncertainties with an impact on goingconcern assumptions; and variousaspects related to consolidation ofentities.

Emerging Economies Group meetsThe IASB’s Emerging Economies Groupmet in Buenos Aires, Argentina at the endof May. Delegates attending the meetingshared experiences and discussed issuesrelated to agriculture accounting,accounting for telecommunication towers,and the clarification of terms in IFRSs andtranslation issues. The meetings areaimed at providing feedback for the IASBon the types of financial reporting issuesthat are of particular concern todeveloping economies.

IFRS News Quarter 3 2012 23

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

PAFA General Assembly resolution toadopt the IFRS for SMEsThe Pan African Federation ofAccountants (PAFA) General Assembly haspassed a resolution to adopt IFRSs andthe IFRS for SMEs. The resolution represents a broad

policy statement that requires action fromthe 39 constituent members of PAFA,which was established in May 2011 toaccelerate the development of theaccountancy profession in Africa. SomePAFA members have already adoptedIFRSs and the IFRS for SMEs or are takingsteps towards doing so; the resolutionaims to encourage others to follow.

IFAC calls for G20 to adopt globalstandards The International Federation ofAccountants (the IFAC) has written to theG20 (the Group of Twenty FinanceMinisters and Central Bank Governors)encouraging all G20 countries who havenot yet adopted IFRS and InternationalStandards on Auditing to do so. In theletter, the IFAC also recommendsincreasing resources for regulators andstandard setters, and supporting theInternational Integrated Reporting Council’sproposed integrated reporting framework.

IVSC release draft valuation guideThe International Valuations StandardsCouncil (IVSC) has released draftguidance aimed at helping professionalvaluers who may be engaged to provideexpert advice to either an auditor or acompany preparing its financialstatements. Although focussed onprofessional valuers, the IVSC hopes thatthe guidance will be a useful document forall parties involved in the preparation ofthe financial statements.

Managing Complexity in FinancialReportingThe Australian Financial Reporting Council(FRC) has released a report ‘ManagingComplexity in Financial Reporting’. Thereport explores the issue of complexity infinancial reporting from an Australianperspective and suggests strategies tobetter manage complexity. Their suggestions include making

better use of developments in informationtechnology and delivery, addressing legalimpediments to preparers determiningrelevant material disclosures, developingguidelines that encourage more use offinancial reporting terms and definitions,as well as influencing the direction of theIASB’s work.

IFRS News Quarter 3 2012 24

PAIB report on processes foreffective business reportingThe Professional Accountants in BusinessCommittee of the International Federationof Accountants (IFAC) has issuedproposed ‘International Good PracticeGuidance – Eleven Principles for EffectiveBusiness Reporting Processes’, for publiccomment. The guidance aims to establish a

benchmark for good practice inimplementing effective business reportingprocesses in an organisation. It isintended to help professional accountantsin business and their organisations createa cycle of continuous improvement fortheir business reporting processes toassist stakeholders in making informeddecisions.

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Canadian measurement paper onfinancial reporting measurementThe Canadian institute of CharteredAccountants has posted to its website aresearch paper “Toward a MeasurementFramework for Financial Reporting byProfit-oriented Entities” to stimulate studyand debate on the concept of currentmarket value, and to provide input for theInternational Accounting Standards Board(IASB) and Financial Accounting StandardsBoard (FASB).

ISDA paper on offsetting forderivativesThe International Swaps and DerivativesAssociation has published a paper‘Netting and Offsetting: ReportingDerivatives Under US GAAP and UnderIFRS’.The paper is intended to give the

reader an insight into the differentrequirements that apply to balance sheetoffsetting under IFRS and US GAAP andtheir impact on the new Basel III LeverageRatio for the banking industry.

UK report on going concern andliquidity risksThe Sharman Panel of Inquiry haspublished its final report andrecommendations on ‘Going Concern andLiquidity Risks: Lessons for companiesand auditors’. The inquiry was launchedby the UK’s Financial Reporting Council inMarch 2011 to draw on the experience ofcompanies and auditors who have had toaddress going concern and liquidityissues in times of difficulty, includingduring the credit crisis. Although targetedat a UK audience, the report’s findings willbe of general interest to a wideraudience.

The Panel’s key recommendations are that:• the primary purpose of the goingconcern assessment and reportingshould be to reinforce responsiblebehaviour in the management of goingconcern risks; and

• the going concern considerationsmade by directors and reviewed byauditors should cover both solvencyand liquidity and that these should beconsidered over the cycle, taking anappropriately prudent view of futureprospects.

Update on reporting in an uncertaineconomic environment The UK’s Financial Reporting Council haspublished an ‘Update for Directors ofListed Companies in the UK’ to assistthem in responding to continuedeconomic uncertainties facing a numberof countries around the world.The Update aims to draw together a

number of the more significant issuesdirectors may consider in preparinginterim reports, given the heightenedcountry and currency risk that many UKcompanies face. Although the reportspecifically relates to UK companies, itssuggestions may also be of interest tocompanies overseas.

IFRS News Quarter 3 2012 25

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

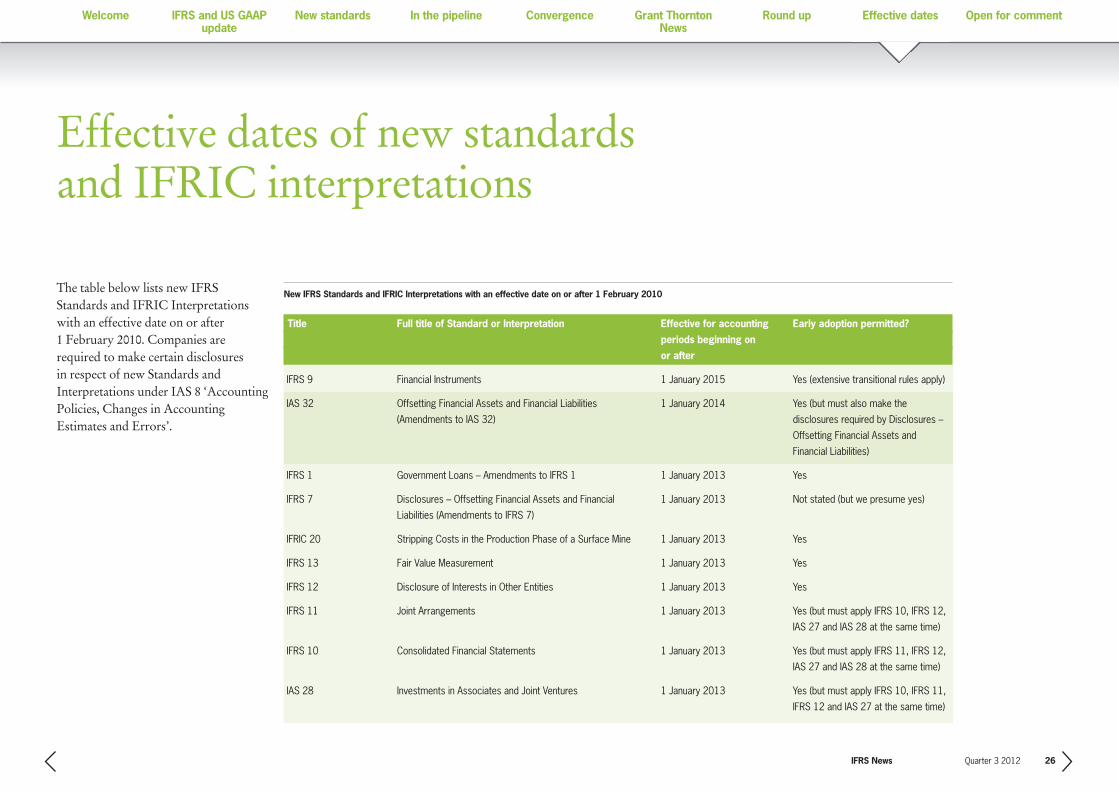

Effective dates of new standards and IFRIC interpretations

The table below lists new IFRSStandards and IFRIC Interpretationswith an effective date on or after 1 February 2010. Companies arerequired to make certain disclosures in respect of new Standards andInterpretations under IAS 8 ‘AccountingPolicies, Changes in AccountingEstimates and Errors’.

IFRS News Quarter 3 2012 26

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 February 2010

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IFRS 9 Financial Instruments 1 January 2015 Yes (extensive transitional rules apply)

IAS 32 Offsetting Financial Assets and Financial Liabilities 1 January 2014 Yes (but must also make the

(Amendments to IAS 32) disclosures required by Disclosures –

Offsetting Financial Assets and

Financial Liabilities)

IFRS 1 Government Loans – Amendments to IFRS 1 1 January 2013 Yes

IFRS 7 Disclosures – Offsetting Financial Assets and Financial 1 January 2013 Not stated (but we presume yes)

Liabilities (Amendments to IFRS 7)

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine 1 January 2013 Yes

IFRS 13 Fair Value Measurement 1 January 2013 Yes

IFRS 12 Disclosure of Interests in Other Entities 1 January 2013 Yes

IFRS 11 Joint Arrangements 1 January 2013 Yes (but must apply IFRS 10, IFRS 12,

IAS 27 and IAS 28 at the same time)

IFRS 10 Consolidated Financial Statements 1 January 2013 Yes (but must apply IFRS 11, IFRS 12,

IAS 27 and IAS 28 at the same time)

IAS 28 Investments in Associates and Joint Ventures 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 27 at the same time)

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

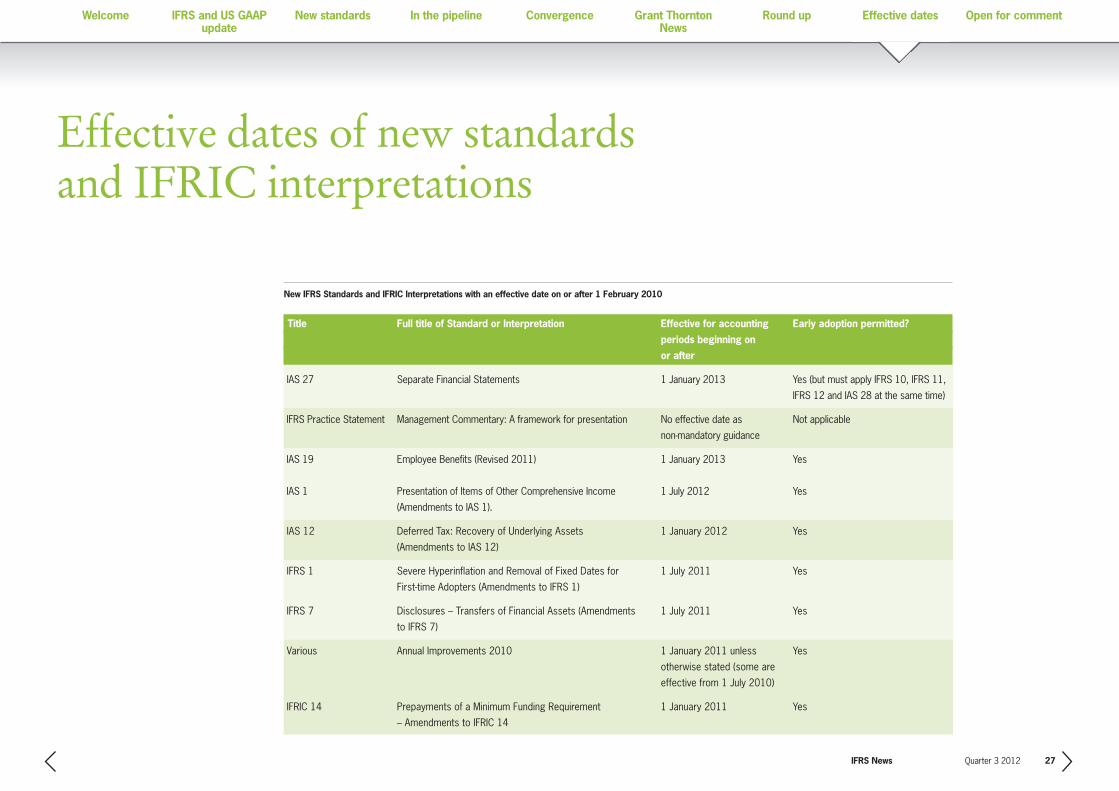

Effective dates of new standards and IFRIC interpretations

IFRS News Quarter 3 2012 27

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 February 2010

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IAS 27 Separate Financial Statements 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 28 at the same time)

IFRS Practice Statement Management Commentary: A framework for presentation No effective date as Not applicable

non-mandatory guidance

IAS 19 Employee Benefits (Revised 2011) 1 January 2013 Yes

IAS 1 Presentation of Items of Other Comprehensive Income 1 July 2012 Yes

(Amendments to IAS 1).

IAS 12 Deferred Tax: Recovery of Underlying Assets 1 January 2012 Yes

(Amendments to IAS 12)

IFRS 1 Severe Hyperinflation and Removal of Fixed Dates for 1 July 2011 Yes

First-time Adopters (Amendments to IFRS 1)

IFRS 7 Disclosures – Transfers of Financial Assets (Amendments 1 July 2011 Yes

to IFRS 7)

Various Annual Improvements 2010 1 January 2011 unless Yes

otherwise stated (some are

effective from 1 July 2010)

IFRIC 14 Prepayments of a Minimum Funding Requirement 1 January 2011 Yes

– Amendments to IFRIC 14

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

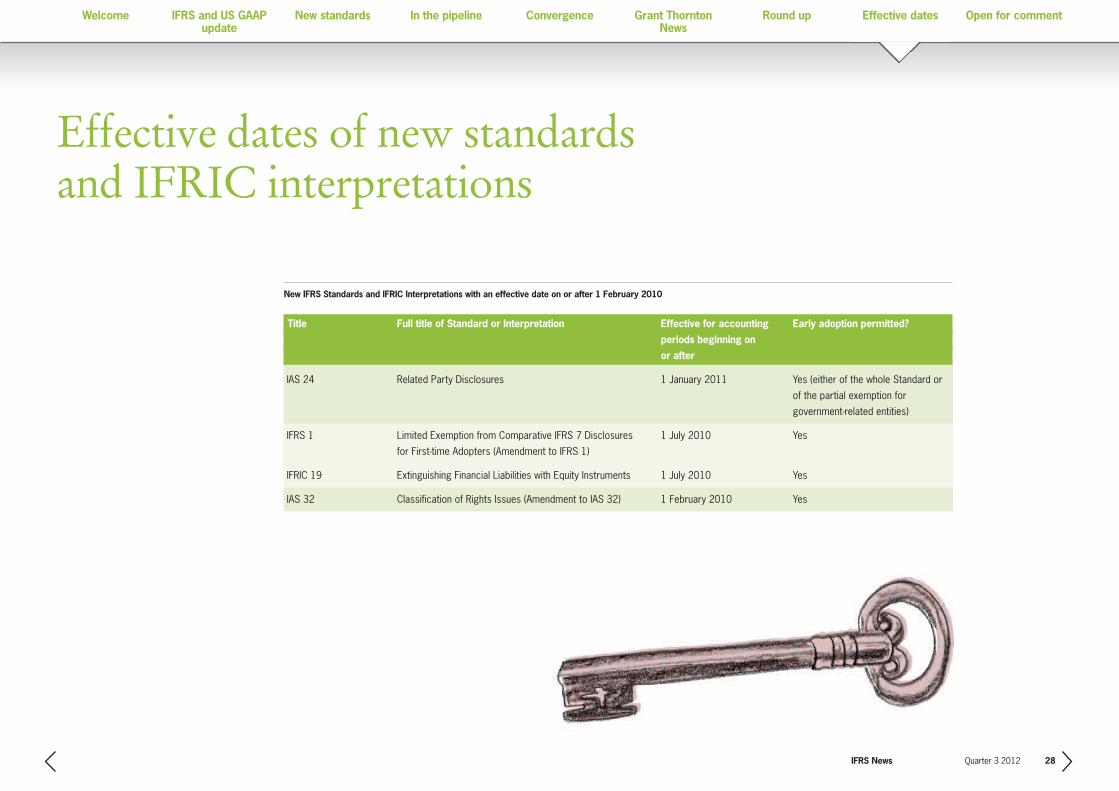

Effective dates of new standards and IFRIC interpretations

IFRS News Quarter 3 2012 28

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 February 2010

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IAS 24 Related Party Disclosures 1 January 2011 Yes (either of the whole Standard or

of the partial exemption for

government-related entities)

IFRS 1 Limited Exemption from Comparative IFRS 7 Disclosures 1 July 2010 Yes

for First-time Adopters (Amendment to IFRS 1)

IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments 1 July 2010 Yes

IAS 32 Classification of Rights Issues (Amendment to IAS 32) 1 February 2010 Yes

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates

Open for comment

This table lists the documents that theIASB currently has out to comment andthe comment deadline. Grant ThorntonInternational aims to respond to each ofthese publications.

IFRS News Quarter 3 2012 29

© 2012 Grant ThorntonInternational Ltd. All rightsreserved.References to “GrantThornton” are to the brandunder which the GrantThornton member firmsoperate and refer to one ormore member firms, as the context requires.Grant Thornton Internationaland the member firms arenot a worldwidepartnership. Services aredelivered independently bymember firms, which arenot responsible for theservices or activities of oneanother. Grant ThorntonInternational does notprovide services to clients.

Current IASB documents

Document type Title Comment deadline

Exposure Draft Annual Improvements to IFRSs 2010—2012 Cycle 5 September 2012

Draft IFRIC Levies Charged by Public Authorities on Entities that 5 September 2012

Operate in a Specific Market

Due process document IFRS Foundation Due Process Handbook 5 September 2012

Draft IFRIC Put Options Written on Non-controlling Interests 1 October 2012

Request for Information Post-implementation Review: IFRS 8 Operating Segments 16 November 2012

Request for Information Comprehensive Review of the IFRS for SMEs 30 November 2012

Welcome IFRS and US GAAPupdate

New standards In the pipeline Convergence Grant ThorntonNews

Open for commentRound up Effective dates