Embed Size (px)

Citation preview

IFRS News

The IASB has published Chapter 6‘Hedge Accounting’ of IFRS 9 ‘FinancialInstruments’ (the new Standard). Thenew requirements look to align hedgeaccounting more closely with entities’risk management activities by: • increasing the eligibility of both

hedged items and hedginginstruments

• introducing a more principles-basedapproach to assessing hedgeeffectiveness.

As a result, the new requirements shouldserve to reduce profit or loss volatility.The increased flexibility of the newrequirements are however partly offsetby entities being prohibited fromvoluntarily discontinuing hedgeaccounting and also by enhanceddisclosure requirements.

This special edition of IFRS Newsinforms you about the new Standard,and the benefits and challenges thatadopting it will bring.

IFRS News: Special Edition December 2013 1

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroduction

IFRS 9 Hedge accounting “IAS 39 ‘Financial Instruments: Recognition andMeasurement’, the previous Standard that dealt with hedgeaccounting, was heavily criticised for containing complex ruleswhich either made it impossible for entities to use hedgeaccounting or, in some cases, simply put them off doing so.

We therefore welcome the publication of IFRS 9’srequirements on hedge accounting. The new requirementsshould make it easier for many entities to reflect their actualrisk management activities in their hedge accounting and thusreduce profit or loss volatility.

At the same time, entities should be aware that while it willbe easier to qualify for hedge accounting, many of the existingcomplexities associated with it (measuring hedge ineffectiveness,etc) will continue to apply once entities are using it.”

Andrew Watchman Executive Director of International Financial Reporting

Special

Edition on

Hedge accounting

Welcome

Introduction

The IASB has published Chapter 6‘Hedge Accounting’ of IFRS 9‘Financial Instruments’. The newrequirements represent a majoraccounting change which merits acorresponding level of planning andconsideration from entities.

We outline in the table below themajor features of the new Standardbefore considering the changes from therequirements of the previous Standard inmore detail in the main body of thenewsletter.

IFRS News: Special Edition December 2013 2

IFRS 9’s hedge accounting requirements at a glance

Features Key points

Objective of the • to better align hedging from an accounting point of view with entities’

Standard underlying risk management activities

Similarities with IAS 39 • hedge accounting remains an optional choice

• the three types of hedge accounting (fair value hedges, cash flow hedges

and hedges of a net investment) remain

• formal designation and documentation of hedge accounting relationships

is required

• ineffectiveness needs to be measured and included in profit or loss

• hedge accounting cannot be applied retrospectively

The major changes • increased eligibility of hedged items

• increased eligibility of hedging instruments and reduced volatility

• revised criteria for hedge accounting qualification and for measuring

hedge ineffectiveness

• a new concept of rebalancing hedging relationships

• new requirements restricting the discontinuance of hedge accounting

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 3

Where do the hedge accounting requirements fit in? The new requirements on hedge accounting represent the latest step in the IASB’sphased plan to replace the existing Standard on financial instruments, IAS 39‘Financial Instruments: Recognition and Measurement’.

Under the IASB’s phased approach, new chapters are added to IFRS 9 as eachstage of the project is completed. The table below shows the status of the main partsof the project following the publication of the hedge accounting chapter, and thetiming of expected future developments.

IFRS 9 Financial Instruments – stage of completion

Chapter Status

Scope • complete

Recognition and derecognition • complete

Classification and measurement • part complete – Exposure Draft on Limited Amendments

published November 2012, final requirements expected

Qtr 1 or Qtr 2 2014

Impairment • discussions ongoing – final requirements expected Qtr 1 or

Qtr 2 2014

General hedge accounting • complete

Macro hedging • discussions ongoing – Discussion Paper expected Qtr 1 2014

Why are IAS 39’s hedge accounting requirements being replaced? IAS 39, the previous Standard dealing with hedge accounting requirements, was heavily criticised forcontaining complex rules which either made it impossible for entities to use hedge accounting or, insome cases, simply put them off doing so. In part, this was a reflection of the fact that the hedgeaccounting requirements were an exception to the normal requirements of that Standard. Nevertheless,there was a perception that hedge accounting did not properly reflect entities’ actual risk managementactivities, thereby reducing the usefulness of their financial statements.

The project to replace IAS 39, which had originally been launched following criticism of the Standardand its alleged role in contributing to the financial crisis, offered an ideal opportunity to address theseconcerns. In setting the requirements of the new Standard, the IASB has introduced an overall objectiveof representing in the financial statements the effect of an entity’s risk management activities that usefinancial instruments to manage exposures arising from particular risks that could affect profit or loss(or, where appropriate, other comprehensive income). Applying hedge accounting is still a voluntarychoice, however, and an exception from IFRS 9’s normal accounting requirements.

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

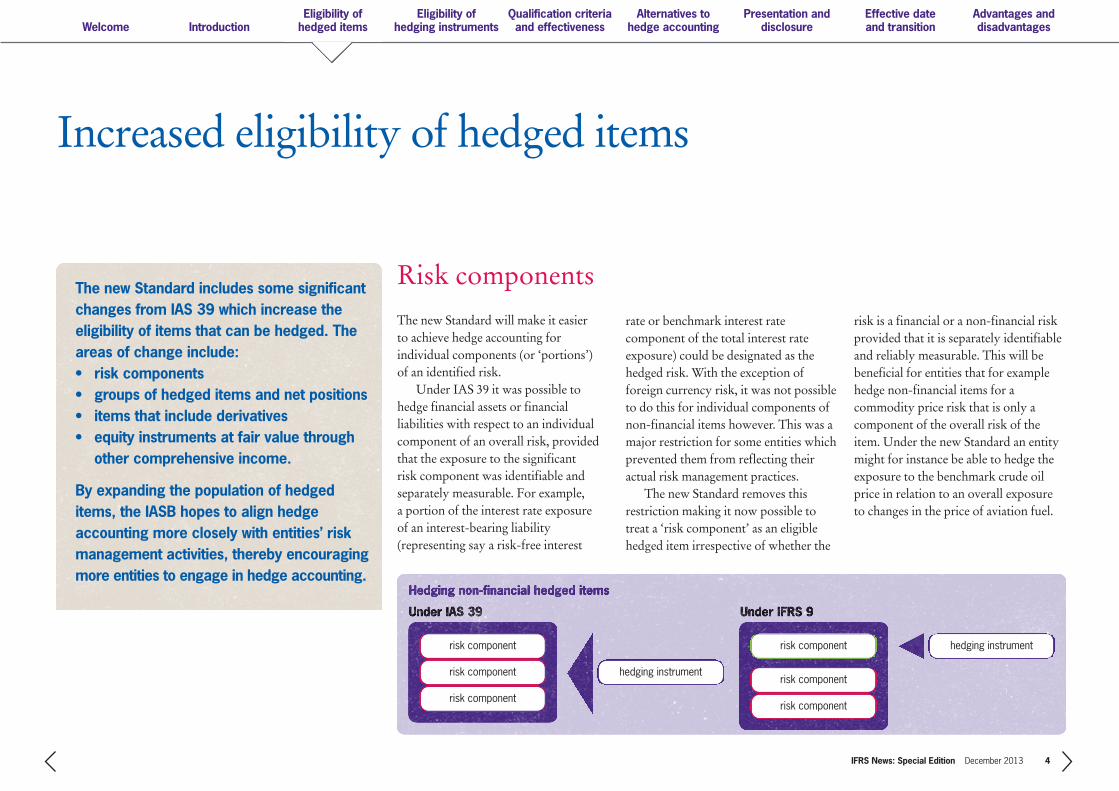

Hedging non-financial hedged items

Under IAS 39 Under IFRS 9

IFRS News: Special Edition December 2013 4

Increased eligibility of hedged items

The new Standard includes some significantchanges from IAS 39 which increase theeligibility of items that can be hedged. Theareas of change include:• risk components• groups of hedged items and net positions• items that include derivatives• equity instruments at fair value through

other comprehensive income.

By expanding the population of hedgeditems, the IASB hopes to align hedgeaccounting more closely with entities’ riskmanagement activities, thereby encouragingmore entities to engage in hedge accounting.

The new Standard will make it easier to achieve hedge accounting forindividual components (or ‘portions’) of an identified risk.

Under IAS 39 it was possible tohedge financial assets or financialliabilities with respect to an individualcomponent of an overall risk, providedthat the exposure to the significant risk component was identifiable andseparately measurable. For example, a portion of the interest rate exposure of an interest-bearing liability(representing say a risk-free interest

rate or benchmark interest ratecomponent of the total interest rateexposure) could be designated as thehedged risk. With the exception offoreign currency risk, it was not possibleto do this for individual components ofnon-financial items however. This was amajor restriction for some entities whichprevented them from reflecting theiractual risk management practices.

The new Standard removes thisrestriction making it now possible totreat a ‘risk component’ as an eligiblehedged item irrespective of whether the

risk is a financial or a non-financial riskprovided that it is separately identifiableand reliably measurable. This will bebeneficial for entities that for examplehedge non-financial items for a commodity price risk that is only acomponent of the overall risk of theitem. Under the new Standard an entitymight for instance be able to hedge theexposure to the benchmark crude oilprice in relation to an overall exposureto changes in the price of aviation fuel.

Risk components

hedging instrument

risk component

risk component

risk component

risk component

risk component

risk component

hedging instrument

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 5

The requirement for the riskcomponent to be separately identifiabledoes not mean that it has to becontractually specified, although it islikely to be significantly harder to fulfilthe requirement where it is not. Theassessment of whether a financial or anon-financial risk component isseparately identifiable and measurableshould instead be performed within thecontext of the particular marketstructure of the item in concern.

Inflation as a risk componentThe new Standard contains a rebuttablepresumption that inflation risk is notseparately identifiable and reliablymeasurable, and therefore not an eligiblerisk component that can be hedged,unless it is contractually specified withinthe hedged item.

However, in limited cases, it ispossible to identify a risk component forinflation risk that will be an eligible riskcomponent because of the particularcircumstances of the inflationenvironment and the relevant debtmarket. The Standard mentions as anexample an entity that issues debt in anenvironment in which inflation-linkedbonds have a volume and term structurethat results in a sufficiently liquidmarket that allows constructing a termstructure of zero-coupon real interestrates. Constructing such a calculationwhere inflation has not beencontractually specified as a riskcomponent is however likely to bechallenging in practice for many entities.

Rather than hedging individualpositions, many entities group similarrisk exposures together and hedge onlythe net position. This enables them totake advantage of naturally offsettingrisk positions (for example, the netamount of forecast purchases and sales ina foreign currency), thus reducing thefinancial cost of taking out hedginginstruments.

IAS 39 only permitted items to beaggregated and hedged as a group wherethe individual assets or individualliabilities in the group shared the riskexposure that is designated as beinghedged. Furthermore, the change in fair value attributable to the hedged risk for each individual item in the group had to be expected to be approximatelyproportional to the overall change in fairvalue attributable to the hedged risk ofthe group of items. Many entities felt thatthese restrictions were not consistentwith the way that they managed risk.

The new Standard relaxes theserequirements, making it easier forgroups of items to qualify as hedgeditems. Under the new Standard, a groupof items (including a group of items thatconstitute a net position) is an eligiblehedged item if: • it consists of items (including

components of items) thatindividually are eligible hedged items

• the items in the group are managedtogether on a group basis for riskmanagement purposes.

Additional restrictions apply for a cashflow hedge of a group of items withoffsetting risk positions (ie a netposition). Such hedges are only allowedfor net positions of foreign currency risk.In addition, the hedge documentationneeds to specify the reporting period inwhich the forecast transactions areexpected to affect profit or loss, as wellas their nature and volume.

Groups of hedged items and netpositions

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 6

The new Standard permits an entity todesignate as hedged items aggregatedexposures that are a combination of anexposure and a derivative (sometimesreferred to as ‘synthetic positions’). Thiswas not permitted under IAS 39, whichcreated problems for entities thatmanaged risk in this way.

Items that include derivativesIt is notable that the new Standard

permits cash flows within a net positionto affect profit or loss in different periods(for example in a hedge of the foreigncurrency risk of a net position of foreigncurrency sales and foreign currencyexpenses, the sales may occur in adifferent period than the expenses). As aresult, the change in fair value of cash

flows that affect profit or loss in an earlierperiod has to be carried forward to offsetthe change in fair value of cash flows thatwill occur in a later period. This is doneby deferring the earlier gains (or losses) inother comprehensive income and thenrecycling them to profit or loss when thelater cash flows affect profit or loss.

cash inflows CU100

cash outflows CU90

net cashflows CU10

Under IFRS 9

single hedging instrument

ExampleAn entity has a forecast purchase requirement of coffee purchases in 24 months’time, which must be settled in foreign currency. It may decide to enter a two-yearforward contract to fix the price of the coffee in terms of the foreign currency. In 12 months’ time, the entity may wish to hedge the risk that arises on thecombination of the forecast purchase requirement and the derivative that hasbeen entered into. Unlike under IAS 39, it is possible for such an aggregatedexposure (ie one including a derivative) to qualify as a hedged item under the newStandard. In this example, the hedged item would then be a fixed purchase in aforeign currency amount. A foreign currency derivative could be used as ahedging instrument to hedge this exposure.

cash inflows CU100

cash outflows CU90

Under IAS 39

hedging instrument 2hedging instrument 1

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 7

The new Standard allows hedgeaccounting for equity instruments at fair value through other comprehensiveincome, even though there will be noimpact on profit or loss from theseinvestments. This is a change from IAS 39 and responds to concerns fromentities who told the IASB that it is acommon risk management strategy foran entity to hedge the foreign exchangerisk exposure of equity investments

irrespective of whether they weredesignated for accounting purposes atfair value through profit or loss or at fairvalue through other comprehensiveincome. Entities may also wish to hedgethe equity price risk to protectthemselves against volatility even thoughthey may not be intending to sell theparticular equity investment.

Equity instruments at fair valuethrough other comprehensive income

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 8

Increased eligibility of hedging instruments and reduced volatility

The new Standard includes one changefrom IAS 39 which will increase theeligibility of hedging instruments, therebyencouraging entities to engage in hedgeaccounting. More importantly however, itcontains new rules on the accounting for thetime value of options and the forward pointsin forward contracts which may reduceprofit or loss volatility compared to underIAS 39. We expand on both of these points below:

Under the new Standard, a non-derivative financial instrument can nowbe treated as a hedging instrumentprovided it is measured at fair valuethrough profit or loss. This represents achange from IAS 39 which will in theoryincrease the ability of entities to usehedge accounting. In practice howeverthere are relatively few non-derivativefinancial instruments measured at fairvalue through profit or loss, so this isunlikely to be a big change.

Increased eligibility of hedging instruments

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 9

New rules on options and forward contracts

New rules on the accounting for the time value of options and the forwardpoints in forward contracts mayreduce profit or loss volatilitycompared to under IAS 39.

Under IAS 39, a hedginginstrument usually had to bedesignated as part of a hedgingrelationship in its entirety. The onlyexceptions to this were that an entitycould choose to: • separate the intrinsic value and time

value of an option contract anddesignate as the hedging instrumentonly the change in the intrinsicvalue of the option and not thechange in its time value

• separate the forward element andthe spot element of a forwardcontract and designate as thehedging instrument only thechange in the spot element and notthe forward element.

These exceptions continue to apply inIFRS 9, however the Standard changes the way in which the parts of theseinstruments that are not designated aspart of the hedging instrument are treated.

Accounting for the time value ofoptionsUnder IAS 39, the time value of anoption contract is treated as a derivativenormally would be, meaning thechange in the fair value of the timevalue of the option is recognised inprofit or loss. The natural (and not verypopular) consequence of this treatmentwas volatility in the profit or loss. Thechanges made by IFRS 9 are intendedto address this issue, recognising thatthe time value of the option istantamount to a cost of hedging.

While the time value of an optioncontract continues to be accounted forat fair value under the new Standard,the new Standard requires the changein its fair value to be initially deferredin other comprehensive income (OCI).The Standard then sets outrequirements which determine whenthose deferred amounts are reclassifiedto profit or loss. In doing so, itdistinguishes between:• a ‘transaction related’ hedged item• a ‘time-period related’ hedged item.

Transaction related hedged itemsFor transaction related hedged items,the accumulated change in the fairvalue that has been deferred in OCI isrecognised in profit or loss at the sametime as the hedged item.

If the hedged item subsequentlyresults in the recognition of a non-financial asset or non-financial liability,or a firm commitment for which fairvalue hedge accounting is applied, theamount deferred in OCI is removedand included directly in the initial costor other carrying amount of the assetor liability. For hedging relationshipsother than these, the amount deferredin OCI is reclassified in the sameperiod as the hedged expected futurecash flows affect profit or loss (forexample, when a forecast sale occurs).

‘Costs’ of hedging

Time value of options Forward element of

forward contract

Foreign currency basis

spreads of financial

instruments

Transaction related

hedged items

Time-period related

hedged items

Costs of hedging

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 10

Time-period related hedged itemFor time-period related hedged items,the amounts that have been deferred in equity are reclassified to profit or losson a systematic and rational basis overthe term of the hedging relationship.The logic here is that the option costdoes not match with a specifictransaction.

Accounting for the forward elementof forward contractsThe Standard contains similar guidanceon how to show the change in value ofthe forward points for hedges based onthe spot rate of a forward contract.Unlike the (mandatory) requirementsfor options, however, entities areallowed an accounting policy choiceover following the approach that wasused under IAS 39 of accounting for thechange in value of the forward pointsthrough profit or loss or adopting thenew alternative requirements.

Foreign currency basis spreads offinancial instrumentsA similar choice to that for accountingfor the forward element of forwardcontracts exists when an entityseparates the foreign currency basisspread from a financial instrument andexcludes it from the designation of thatfinancial instrument as the hedginginstrument.

Policy choice for forward contracts*

* a similar choice exists for the foreign currency basis spread of a financial instrument

Account for the change in

value of the forward points

through profit or loss

• defer the change in value of

the forward points through OCI

• reclassify through profit or loss

on a systematic and rational

basis

Choice

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 11

Revised criteria for hedge accounting qualification andfor measuring hedge ineffectiveness

The new Standard makes significantchanges to the criteria for hedgeaccounting qualification, relaxing thecurrent requirements with the objective ofmaking it easier for entities to reflect theirunderlying risk management objectives.

To qualify for hedge accounting under IAS 39, a hedge had tobe highly effective on both a prospective and a retrospectivebasis. ‘Highly effective’ refers to the degree of offset betweenthe changes in fair value or cash flows of the hedginginstrument and the hedged item, and is defined in terms of a‘bright line’ quantitative range of 80-125%. Where the actualresults of a hedge were found to have fallen outside that range,IAS 39 required hedge accounting to be discontinued.

These requirements were widely criticised by preparers forbeing unaligned with their actual risk management practices.The 80-125% accounting threshold was particularly criticisedfor resulting in hedge accounting discontinuance even wherethere had not been a breakdown in the economics of thehedge.

Background

The IASB has responded to thesecriticisms by eliminating the 80-125%threshold and introducing moreprinciples-based qualifying criteria.Under IFRS 9, a hedging relationshipmust meet all of the followingrequirements:• there is an economic relationship

between the hedged item and thehedging instrument

• the effect of credit risk does notdominate the value changes thatresult from that economicrelationship

• the hedge ratio of the hedgingrelationship is the same as thatresulting from the quantity of thehedged item that the entity actuallyhedges and the quantity of thehedging instrument that the entityactually uses to hedge that quantityof hedged item.

To prevent abuse of the third criteria, theIASB has included wording thatprevents entities from deliberatelyattempting to achieve a ratio that wouldresult in an outcome that would beinconsistent with the purpose of hedgeaccounting.

Economic relationship The first requirement for an economicrelationship to exist means that thehedging instrument and the hedged itemare expected to move in the oppositedirection because of the same risk (thehedged risk).The Standard gives therelationship between Brent and WTIcrude oil as an example.

The mere existence of a statisticalcorrelation between two variables doesnot, by itself, prove that an economicrelationship exists however. Rather,there must be causality in themovements between the variables. An analysis of the possible behaviour of the hedging relationship during itsterm will therefore be needed toascertain whether it is expected to meet the risk management objective and so demonstrate that an economicrelationship exists.

The new requirements

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 12

Credit risk must not dominateThe second criteria for hedge accountingqualification is that the impact ofchanges in credit risk should not be ofsuch a magnitude that it dominates thevalue changes that result from theeconomic relationship (ie the effect ofthe changes in the underlying variables).

Such a situation might occur wherean entity hedges an exposure tocommodity price risk using anuncollateralised derivative. If thecounterparty to the derivativeexperiences a severe deterioration in itscredit standing, the effect of the changesin the counterparty’s credit standingmight outweigh the effect of changes inthe commodity price on the fair value ofthe hedging instrument, whereas changesin the value of the hedged item dependlargely on the commodity price changes.

Hedge ratioThe third criteria for hedge accountingqualification is that the hedge ratio ofthe hedging relationship must be thesame as that resulting from:• the quantity of the hedge item that

the entity actually hedges and • the quantity of the hedging

instrument that the entity actuallyuses to hedge that quantity ofhedged item.

For example, where an entity hedges lessthan 100% of the exposure on an item,say 85%, it will need to designate thehedging relationship using a hedge ratiothat is the same as that resulting from85% of the exposure and the quantity ofthe hedging instrument that the entityactually uses to hedge that 85%.

The designation of the hedgingrelationship must not however reflect animbalance between the weightings of thehedged item and the hedging instrumentthat would create hedge ineffectivenessthat could result in an accountingoutcome that would be inconsistent withthe purpose of hedge accounting. Thiscaveat is intended, for example, toprevent entities deliberately underhedging so as to minimise the recognitionof ineffectiveness in a cash flow hedge.

Is there an economic relationship between the hedged

item and the hedging instrument?

The qualification process for a new hedging relationship

Does the effect of credit risk dominate the value

changes that result from the economic relationship?

Is the hedge ratio the same as that resulting from the

quantity of the hedged item that the entity actually hedges

and the quantity of the hedging instrument that the entity

actually uses to hedge that quantity of hedged item?

Does the hedge ratio reflect an imbalance that

would create hedge ineffectiveness that could produce

an accounting outcome inconsistent with the purpose

of hedge accounting?

Qualifies for hedge accounting

Does not

qualify for hedge

accounting

Yes

No

Yes

No

Yes

No

Yes

No

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 13

Ongoing hedging relationships – ineffectiveness and rebalancing

Analyse whether sources of

ineffectiveness are

Change in extent of offset between

the hedging instrument and the

hedged item

A new concept of rebalancing hedging relationships

The new Standard requires rebalancingof an existing hedge relationship to beundertaken where the hedgeeffectiveness requirements are no longermet but the entity’s risk managementobjective remains the same.

This involves making adjustmentsto the designated quantities of thehedged item or the hedging instrumentso as to maintain a hedge ratio thatcomplies with the hedge effectivenessrequirements and is a new concept. Byway of contrast, failure to meet thehedge effectiveness requirements underIAS 39 generally resulted indiscontinuance of hedge accounting,meaning that the entity had torecommence hedge accounting with anew hedging relationship.

An example of a situation whererebalancing would be appropriatewould be where an entity hedges anexposure to a foreign currency that ispegged to another foreign currency (ietheir exchange rate is maintainedwithin a band or at an exchange rate setby a central bank or other authority),and the peg changes.

As noted above, rebalancing is alsorequired where an entity deliberatelyundertakes actual risk managementthat results in weightings of the hedgeditem and the hedging instrument thatproduce an accounting result that isinconsistent with the purpose of hedgeaccounting.

ExampleAn entity hedges an exposure to theHong Kong $ using a currencyderivative that references the US $.The Hong Kong $ and the US $ arepegged. If the exchange ratebetween the Hong Kong $ and theUS $ were changed (ie a new bandor rate was set), rebalancing of thehedge ratio should take place as theentity’s risk management objectivewould remain the same.

Continue

Measure and recognise

hedge ineffectiveness

DiscontinueRebalance and continue

1 determine and recognise

hedge ineffectiveness

2 rebalance the hedging ratio

3 update analysis of the sources

of hedge ineffectiveness that

are expected to affect the

hedging relationship during its

remaining term

4 update hedging documentation

accordingly

An indication that the hedge ratio no longer reflects the

relationship between hedging instrument and the hedge item

Fluctuations around

the hedge ratio which

remains valid

Yes No

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 14

Under the new Standard, entities are required to assesswhether the hedge effectiveness requirements are met both at the inception of the hedging relationship and on an ongoing basis.

The ongoing assessment is required to be performed (atleast) at each reporting date or upon a significant change in thecircumstances affecting the hedge effectiveness requirements,whichever comes first. Unlike under IAS 39, the assessment isnot retrospective but solely forward-looking.

Frequency of assessingwhether the hedgeeffectiveness requirementsare met

Methods for assessing whether the hedge effectivenessrequirements are met

The new Standard does not specify a method forassessing whether a hedging relationship meets thehedge effectiveness requirements or not.

In a simple case where the critical terms of thehedging instrument and the hedged item match orare closely aligned, a qualitative assessment ofhedge effectiveness may be appropriate. Insituations where the critical terms of the hedginginstrument and the hedged item are not closelyaligned however, it may only prove possible toconclude that an economic relationship existswhere a quantitative assessment is performed.Similarly it may be necessary to perform aquantitative assessment in order to assess whetherthe hedge ratio used for designating the hedgingrelationship meets the hedge effectivenessrequirements.

InsightUnder IFRS 9, it is an entity’s risk management that is the main sourceof information to perform the assessment of whether a hedgingrelationship meets the hedge effectiveness requirements.

This means that it is possible for the method used to assesshedge effectiveness to change over time. Where such a situationoccurs, IFRS 9 requires the documentation of the hedging relationshipto be updated for any changes to the methods. This is a change fromIAS 39, which required an entity to specify at inception of the hedgingrelationship the method to be applied to assess hedge effectiveness,and to then apply that method consistently for the duration of thehedging relationship.

It is also possible for an entity to use the same or differentmethods for assessing whether an economic relationship existsbetween the hedged item and the hedging instrument and whether thehedge ratio used for designating the hedging relationship meets thehedge effectiveness requirements.

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 15

The new Standard specifies that where the riskmanagement objective for a hedging relationshiphas changed, rebalancing does not apply and thehedge relationship must instead be discontinued.

Note that under the new Standard, entities canno longer voluntarily choose to discontinue hedgeaccounting where the risk management objectiveremains the same.

In summary, hedge accounting can only bediscontinued when the hedging relationship (or apart of the hedging relationship) ceases to meet the qualifying criteria (after taking account ofrebalancing, if applicable).

For example when:• the hedging relationship no longer meets the

risk management objective • the hedging instrument has expired, been sold,

been terminated or exercised• there is no longer an economic relationship

between the hedged item and the hedginginstrument or the effect of credit risk starts todominate the value changes that result from that economic relationship.

Discontinuing hedge accounting

Risk management strategy versus risk managementobjectiveGuidance in the Standard distinguishes between an entity’s riskmanagement strategy and its risk management objective.

Risk management strategyAn entity’s risk management strategy is established at the highestlevel at which it manages risk. Risk management strategies typicallyidentify the risks to which the entity is exposed and set out how theentity responds to them. Such strategies are typically in place forlengthy periods and may include some flexibility to react to changes incircumstances that occur while the particular strategy is in place (egchanges in interest rate or commodity price levels that would result ina different extent of hedging).

Risk management objective In contrast, the risk management objective for a hedging relationshipapplies at the level of a particular hedging relationship. It relates tohow the particular hedging instrument that has been designated isused to hedge the particular exposure that has been designated asthe hedged item.

From this guidance it is clear that a risk management strategy caninvolve many different hedging relationships whose risk managementobjectives relate to executing that overall risk management strategy.

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 16

Alternatives to hedge accounting

IAS 39 contains an option which allows anentity to designate a financial instrumentthat would otherwise be measured atamortised cost as at fair value throughprofit or loss if doing so eliminates orsignificantly reduces an accountingmismatch. This is known as the ‘fair valueoption’. As well as making the changesrelating to hedge accounting discussedabove, the IASB has extended the use ofthis fair value option in order to provide a(less onerous) alternative to hedgeaccounting in the following two areas: • contracts to buy or sell a non-financial

item for own use• hedging credit risk using creditderivatives.

We discuss these two areas of changebelow:

Under IAS 39, the accounting forexecutory contracts to buy or sell a non-financial item that can be settled net incash could give rise to accountingmismatches in some situations. This wasparticularly the case for commoditycontracts.

Many commodity contracts areaccounted for as derivatives because thecommodities can be readily converted tocash and the contracts allow for them tobe net settled in cash. Where this is thecase, the derivative is measured at fairvalue through profit or loss. If an entityenters into a derivative to hedge theexposure to changes in the value of thecommodity contract, then both thecontract and the derivative which isbeing used to (economically) hedge thecontract are measured at fair value andthere is no need to apply actual hedgeaccounting, there being a natural offset.

Non-financial items that can be netsettled in cash are however outside thescope of IAS 39 where they are held forthe entity’s ‘own use’. As a result, manycommodity contracts are accounted foras normal sale or purchase contracts.Where this is the case and an entityenters into a derivative contract to hedgethe changes in the fair value of thecontract, an accounting mismatch iscreated. This is because the change in thefair value of the derivative is recognisedin profit or loss while the change in thefair value of the commodity supplycontract is not recognised.

To eliminate this accountingmismatch, an entity could apply hedgeaccounting. However, hedge accountingin these circumstances can beadministratively burdensome as thesetypes of contract are typically enteredinto in large volumes and managed on anet basis, often resulting in the netposition being adjusted on a daily basis.

The new Standard provides relieffrom this accounting mismatch bymaking consequential amendmentswhich allow an entity to elect at the dateof initial recognition of the contract toirrevocably designate a contract to buyor sell a non-financial item that can besettled net in cash as measured at fairvalue through profit or loss.

This amendment effectively allowscommodity contracts for own use to beaccounted for as derivatives andtherefore measured at fair value. Wherean actual derivative has been taken outto hedge against the change in value ofthe commodity contract, there willtherefore be a natural offset in terms ofthe effect on profit or loss and hedgeaccounting will therefore not benecessary. The new Standard specifieshowever that this option can only beused where it eliminates or significantlyreduces an accounting mismatch thatwould otherwise result.

Contracts to buy or sell a non-financial item for own use

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 17

The second area where the ‘fair valueoption’ has been extended relates tohedging credit risk using creditderivatives.

Many financial institutions entersuch hedges to manage the credit riskexposures which arise from their lendingactivities. In order to hedge suchexposures under both the new Standardand IAS 39, the credit risk componentneeds to be separately identifiable andreliably measurable which can inpractice prove to be challenging.

As a result, financial institutions thatuse credit default swaps to hedge creditrisk of their loan portfolios measuretheir loan portfolios at amortised costand do not recognise most loancommitments. This creates anaccounting mismatch due to the creditdefault swaps being measured at fairvalue through profit or loss.

To allow for the management ofcredit risk, the IASB has thereforeextended the fair value option toaccommodate certain credit exposures asan alternative to hedge accounting.

The new Standard permits an entityto designate a credit exposure asmeasured at fair value through profit orloss provided the following criteria arefulfilled:• it is hedged with a credit derivative • the name of the credit exposure

matches the reference entity of thecredit derivative

• the seniority of the financialinstrument or part of the financialinstrument that constitutes the creditexposure matches that of theinstruments that can be delivered inaccordance with the credit derivative.

Designation can be made at initialrecognition or subsequently or evenwhile the credit exposure isunrecognised (which might be the casefor a loan commitment for example).

Hedging credit risk using credit derivatives

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 18

Presentation and disclosure

While the accounting mechanics andpresentation requirements set out inIAS 39 remain largely unchanged, thenew Standard amends IFRS 7‘Financial Instruments: Disclosures’ tointroduce extensive new disclosurerequirements to compensate in part forthe increased flexibility of the newrequirements.

The new Standard requires all itsdisclosure requirements on the effectsof hedge accounting to be disclosed inone comprehensive note in thefinancial statements, reflectingconcerns expressed by users that IAS 39’s hedge accounting disclosureswere not helpful. This note covers:

• the entity’s risk managementstrategy and how it applies thatstrategy to manage risk

• how the entity’s hedging activitiesaffect the amount, timing anduncertainty of future cash flows

• the effects of hedge accounting onthe primary financial statements

In addition, there are specificdisclosures for dynamic strategies andcredit risk hedging.

In making the disclosures requiredby the new Standard, entities shoulduse their judgement to determine:• how much detail to disclose• how much emphasis to place

on different aspects of thedisclosure requirements

• the appropriate level of aggregation or disaggregation

• whether users of financialstatements need additionalexplanations to evaluate thequantitative information disclosed.

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 19

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

Macro hedging The IASB currently has a separate, active project onaccounting for macro hedging activities (covering ways toaccount for dynamic risk management of open portfolios).

Currently entities applying hedge accounting to suchrisk management activities, use a combination of IAS 39’sgeneral hedge accounting requirements and the specificmodel in IAS 39 for accounting for macro hedging.

IFRS 9 has been designed so that entities would not be adversely affected while the macro hedging projectcontinues to be developed. Therefore an entity undertakingmacro hedging activities can apply the new accountingmodel in IFRS 9 while continuing to apply the specific IAS 39 accounting for macro hedges if they wish to do so.As noted above, the IASB is also allowing entities a choiceof continuing to apply IAS 39 for all their hedge accountinguntil the macro hedging project is completed.

Effective date

Prior to the publication of the newhedge accounting requirements, themandatory effective date of IFRS 9was 1 January 2015. On publicationof the new requirements however,the IASB decided that this datewould not allow sufficient time forentities to prepare to apply IFRS 9.Therefore at the same as publishingthe amendments that introduced thedisclosure requirements into IFRS 9, the IASB removed theStandard’s mandatory effective date.

Early application is permittedprovided that all of the other(existing) requirements of IFRS 9have been applied or are applied atthe same time. When an entity firstapplies IFRS 9 (as amended inNovember 2013), it may howeverchose to continue to apply IAS 39’shedge accounting requirementsinstead of IFRS 9’s.

IFRS News: Special Edition December 2013 20

The new requirements are to be appliedprospectively subject to certainexceptions. The principal exceptions are:• retrospective application for the

time value of options is requiredwhere previously only the changein an option’s intrinsic value hasbeen designated under IAS 39 as ahedging instrument in a hedgerelationship

• entities may elect to retrospectivelyapply the accounting for theforward element of forwardcontracts where previously onlythe change in the spot element of aforward contract has beendesignated as a hedging instrumentunder IAS 39, provided that theelection is applied consistently

• the accounting for foreign currencybasis spreads may be appliedretrospectively for those hedgingrelationships that existed at thebeginning of the earliestcomparative period or weredesignated thereafter.

The Standard requires that in order to apply hedge accounting from thedate of initial application for existinghedging relationships, the hedgeaccounting requirements of the newStandard must be met at that date.

Existing hedge relationships thatqualify under the requirements of the new Standard (after taking intoaccount any rebalancing on transition)are regarded as continuing.

Similarities with IAS 39Amid all the change created by the publication of the new Standard, it is easy to forget that some significant areas are unchanged from the previousrequirements of IAS 39. These include the following:• hedge accounting remains a voluntary choice• entities will still need to identify a hedged item and a hedging instrument

and document the relationship between them at inception• the three types of hedge relationship used in IAS 39 (fair value hedges,

cash flow hedges and hedges of a net investment) and the mechanics ofaccounting for them remain the same

• the method for determining hedge ineffectiveness is unchanged • it is not possible to use a written option as a hedging instrument.

Entities should be particularly aware that while it may be easier to qualify forhedge accounting under the new Standard, many of the existing complexitiesthat result from the mechanics of applying it (such as calculating hedgeineffectiveness) will remain once they are using it.

Transition

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome

IFRS News: Special Edition December 2013 21

© 2013 Grant ThorntonInternational Ltd. All rightsreserved.“Grant Thornton” refers tothe brand under which theGrant Thornton memberfirms provide assurance,tax and advisory services totheir clients and/or refersto one or more memberfirms, as the contextrequires. Grant ThorntonInternational Ltd (GTIL) andthe member firms are not a worldwide partnership.GTIL and each member firmis a separate legal entity.Services are delivered bythe member firms. GTILdoes not provide servicesto clients. GTIL and itsmember firms are notagents of, and do notobligate, one another and are not liable for one another’s acts oromissions.

Advantages and disadvantages of the new requirements

Increased opportunities to use hedge accounting:• ability to designate non-financial risk components• more flexibility to hedge groups of items• increased ability to hedge net items

Not possible to voluntarily discontinue hedge accounting

New treatment of time value of options will reduce profitand loss volatility

Need to rebalance

Increased eligibility of hedging instruments (aggregatedexposures)

Reduced ability to use rollover strategies

Introduces fair value option for credit risk (removesaccounting mismatch)

Cost and effort of measuring hedge ineffectivenessremain (albeit reduced)

Reduces cost and effort associated with measuringhedge ineffectiveness (80-125% retrospective testeliminated)

Costs associated with dedesignation (resulting fromhaving to close out derivative positions in order todedesignate)

Lack of convergence with US GAAP

Advantages Disadvantages

Alternatives tohedge accounting

Presentation anddisclosure

Effective date and transition

Advantages anddisadvantages

Eligibility ofhedged items

Eligibility of hedging instruments

Qualification criteriaand effectivenessIntroductionWelcome