Embed Size (px)

Citation preview

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 1/15

International Finance Assignment

Nike Inc.

Submitted by:

Anmol Dhar (22)

Shefali Dixit (24)

Bhupesh Dua (26)

Ankita Dutta (27)

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 2/15

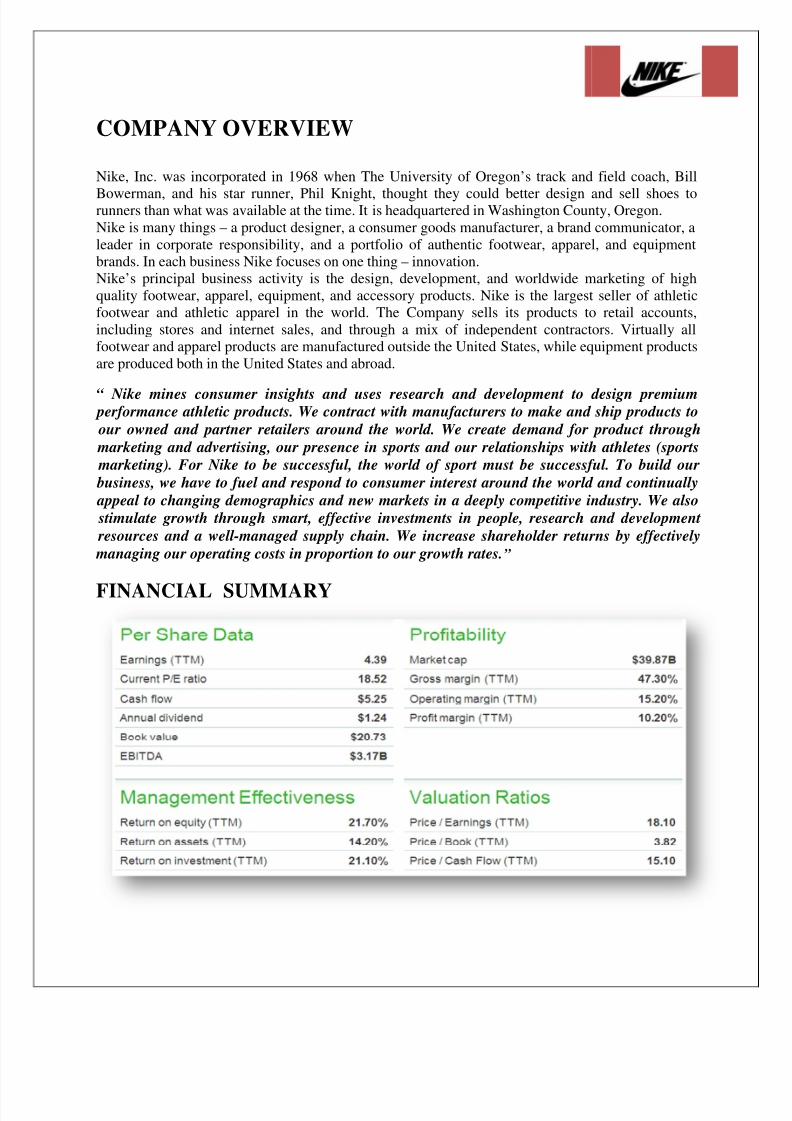

COMPANY OVERVIEW

Nike, Inc. was incorporated in 1968 when The University of Oregon’s track and field coach, Bill

Bowerman, and his star runner, Phil Knight, thought they could better design and sell shoes torunners than what was available at the time. It is headquartered in Washington County, Oregon.Nike is many things – a product designer, a consumer goods manufacturer, a brand communicator, aleader in corporate responsibility, and a portfolio of authentic footwear, apparel, and equipmentbrands. In each business Nike focuses on one thing – innovation.Nike’s principal business activity is the design, development, and worldwide marketing of highquality footwear, apparel, equipment, and accessory products. Nike is the largest seller of athleticfootwear and athletic apparel in the world. The Company sells its products to retail accounts,including stores and internet sales, and through a mix of independent contractors. Virtually allfootwear and apparel products are manufactured outside the United States, while equipment productsare produced both in the United States and abroad.

“ Nike mines consumer insights and uses research and development to design premium performance athletic products. We contract with manufacturers to make and ship products to

our owned and partner retailers around the world. We create demand for product through

marketing and advertising, our presence in sports and our relationships with athletes (sports

marketing). For Nike to be successful, the world of sport must be successful. To build our

business, we have to fuel and respond to consumer interest around the world and continually

appeal to changing demographics and new markets in a deeply competitive industry. We also

stimulate growth through smart, effective investments in people, research and development

resources and a well-managed supply chain. We increase shareholder returns by effectively

managing our operating costs in proportion to our growth rates.”

FINANCIAL SUMMARY

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 3/15

BUSINESS DESCRIPTIONS

Products

Nike’s athletic footwear products, the leading revenue segment, are designed primarily for, butnot restricted to, specific athletic use. The main emphasis that the Company places on itsproducts are quality and innovation in products designed for men, women, and children. Nike’stop-selling footwear categories are running, training, basketball, and soccer. Other footwearcategories include aquatic activities, baseball, cheerleading, football, golf, lacrosse, outdooractivities, skateboarding, tennis, volleyball, walking, wrestling, and other athletic andrecreational uses.Nike sells sports apparel and accessories relevant to each sport mentioned above as well as

sports-inspired lifestyle apparel, including bags, socks, sport balls, eyewear, protectiveequipment, basic sport equipment, etc. Apparel and accessories for most sports are designed tocompliment Nike’s footwear products, feature the same trademarks, and are sold through thesame marketing and distribution channels. It is often the case that Nike designs unique footwearstyles for each sport, and apparel and accessories for each sport follow suit on that style. Nikealso markets apparel with licensed college and professional team and league logos.In addition to selling products directly to consumers, Nike enters into license agreements thatpermit unaffiliated parties to manufacture and sell various apparel, equipment, and accessoryitems, such as swimwear, children’s apparel, training equipment, eyewear, electronic devices,and golf accessories. In addition to Nike’s footwear, apparel, and accessories businesses, theCompany sells products under other brand names in particular markets. Nike wholly-owns five

footwear and apparel companies that specialize in different sports: Cole Haan, Converse Inc.,Hurley International LLC, Umbro Ltd., and Nike Golf. Cole Haan, headquartered in Yarmouth,Maine, designs and distributes dress and casual footwear, apparel and accessories for men andwomen under the brand names Cole Haan® and Bragano®. Converse, headquartered in NorthAndover, Massachusetts, designs, distributes, and licenses athletic and casual footwear, appareland accessories under the Converse®, Chuck Taylor®, All Star®, One Star®, and Jack Purcell®trademarks. Hurley, headquartered in Costa Mesa, California, designs and distributes a line of action sports apparel for surfing, skateboarding, and snowboarding, youth lifestyle apparel, andaccessories under the Hurley® trademark. Umbro, headquartered in Manchester, England,designs, distributes and licenses athletic and casual footwear, apparel and equipment, primarilyfor the sport of soccer, under the Umbro® trademark. Nike Golf, headquartered in Beaverton,

Oregon, designs and markets golf equipment, apparel, balls, footwear, bags and accessoriesworldwide.

Manufacturing Footwear

Virtually all of Nike’s footwear is manufactured outside the United States. Factories in China,Vietnam, Indonesia, and Thailand produced 98 percent of total Nike brand footwear in 2010.Nike’s largest footwear factory accounted for five percent of 2010

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 4/15

footwear production

The main materials used in Nike footwear are rubber, plastic compounds, foam cushioningmaterials, nylon, leather, canvas, and polyurethane films used for cushioning components. Nike’s

wholly-owned subsidiary, NIKE IHM (In House Manufacturing), which produces syntheticrubbers and polyurethane films, was the largest supplier of foam and cushioning components.

Manufacturing Apparel

Nike brand apparel is also manufactured almost entirely outside of the United States. Nikeapparel is manufactured by independent contract manufacturers located in 34 countries. Nike’slargest apparel factory accounted for five percent of 2010 apparel production. The main materialsused in Nike apparel are natural and synthetic fabrics and threads, plastic and metal hardware,and water and heat resistant fabrics.

Sales and Marketing

Nike is exposed to several demand factors in various geographic and product markets. The mixof product sales may vary considerably as a result of changes in seasonal and geographic demandfor particular types of footwear, apparel and equipment. Because Nike is a consumer productscompany, the relative popularity of various sports and related products, as well as shifting designtrends, affects the overall level of demand.To help market its products, Nike aggressively contracts with highly successful and influentialathletes, coaches, teams, and leagues. In an effort to stay competitive and retain dominant marketshares, Nike actively responds to trends and shifts in consumer preferences by adjusting the mixof existing product offerings, developing new products, styles and categories, and influencingsports and fitness preferences through aggressive marketing. A key imperative for Nike is toimmediately adjust for continuous changes in consumer demands.Nike makes substantial use of its futures ordering program, which allows retailers to order five tosix months in advance of delivery with the commitment that their orders will be delivered withina set time period at a fixed price. In 2010, 89% of Nike’s United States wholesale footwearshipments were made under the futures program.

GEOGRAPHIC ANALYSIS

Nike branch offices are located in over 50 countries. The Company operates 14 internationaldistribution centers and sells to more than 28,000 retail accounts outside the United States. Thefive wholly-owned subsidiaries comprised 13 percent of total revenue; eight percent of whichwas realized in the United States Region.

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 5/15

Major regions are:

• US Region

• EMEA (Europe, Middle East, Asia)

• Asia Pacific Region

• Americas Region

• Other Businesses

Nike recognizes significant growth opportunities in emerging markets, particularly in the AsiaPacific and Americas regions. From 2003 to 2010, total revenue growth for both regions was 144percent. Other Businesses worldwide has also grown tremendously over the past six years, at 18

percent annually on average, reflecting the Company’s success in its diversification strategy.

From 2003 to 2011, the Europe, Middle East, and Asia region average annual growth rate wasmore than ten percent. EMEA is Nike’s second largest regional market, the Company must makeenhanced marketing, product line, and sales initiatives to focus on changing consumer trends anddemands in these markets to ensure that this main region remains profitable in the future.In the Asia Pacific region, changes in currency exchange rates accounted for three percent of revenue growth. Aside from currency impacts in the Asia Pacific region, all countries in thisregion delivered revenue growth, with China being the region leader.

NIKE: SWOT ANALYSIS

Strengths

• Nike is a very competitive organization. Phil Knight (Founder and CEO) is often quotedas saying that 'Business is war without bullets.' Nike has a healthy dislike of iscompetitors. At the Atlanta Olympics, Reebok went to the expense of sponsoring thegames. Nike did not. However Nike sponsored the top athletes and gained valuablecoverage.

• Nike has no factories. It does not tie up cash in buildings and manufacturing workers.

This makes a very lean organization. Nike is strong at research and development, as isevidenced by its evolving and innovative product range. They then manufacture whereverthey can produce high quality product at the lowest possible price. If prices rise, andproducts can be made more cheaply elsewhere (to the same or better specification), Nikewill move production.

• Nike is a global brand. It is the number one sports brand in the World. Its famous'Swoosh' is instantly recognizable, and Phil Knight even has it tattooed on his ankle.

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 6/15

Weaknesses

• The organization does have a diversified range of sports products. However, the incomeof the business is still heavily dependent upon its share of the footwear market. This may

leave it vulnerable if for any reason its market share erodes.• The retail sector is very price sensitive. Nike does have its own retailer in Nike Town.

However, most of its income is derived from selling into retailers. Retailers tend to offera very similar experience to the consumer. Can you tell one sports retailer from another?So margins tend to get squeezed as retailers try to pass some of the low price competitionpressure onto Nike

Opportunities

• Product development offers Nike many opportunities. The brand is fiercely defended byits owners whom truly believe that Nike is not a fashion brand. However, like it or not,consumers that wear Nike product do not always buy it to participate in sport. Somewould argue that in youth culture especially, Nike is a fashion brand. This creates its ownopportunities, since product could become unfashionable before it wears out i.e.consumers need to replace shoes.

• There is also the opportunity to develop products such as sport wear, sunglasses and jewelry. Such high value items do tend to have associated with them, high profits.

• The business could also be developed internationally, building upon its strong globalbrand recognition. There are many markets that have the disposable income to spend onhigh value sports goods. For example, emerging markets such as China and India have anew richer generation of consumers. There are also global marketing events that can beutilized to support the brand such as the World Cup (soccer) and The Olympics.

Threats

• Nike is exposed to the international nature of trade. It buys and sells in differentcurrencies and so costs and margins are not stable over long periods of time. Such anexposure could mean that Nike may be manufacturing and/or selling at a loss. This is anissue that faces all global brands.

• The market for sports shoes and garments is very competitive. The model developed byPhil Knight in his Stamford Business School days (high value branded productmanufactured at a low cost) is now commonly used and to an extent is no longer a basis

for sustainable competitive advantage. Competitors are developing alternative brands totake away Nike's market share.• As discussed above in weaknesses, the retail sector is becoming price competitive. This

ultimately means that consumers are shopping around for a better deal. So if one storecharges a price for a pair of sports shoes, the consumer could go to the store along thestreet to compare prices for the exactly the same item, and buy the cheaper of the two.Such consumer price sensitivity is a potential external threat to Nike.

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 7/15

RISKS FACED BY NIKE

Foreign Exchange Risk

As a global leader in consumer products, Nike is exposed to exchange rate risk of severalcurrencies. Its primary foreign currency exposures are related to United States dollar transactionsat wholly-owned foreign subsidiaries, as well as transactions and translation of resultsdenominated in the Euro, British pound, Chinese Yuan, and Japanese Yen. Nike’s foreignexchange risk management program seeks to minimize volatility of currency fluctuations indollar terms. Nike manages these exposures by taking advantage of natural offsets and currencycorrelations that exist within its currency portfolio. Nike also regularly uses derivativeinstruments such as forward contracts and options to hedge foreign exchange risk.

As part of Nike’s foreign exchange risk management program, standard foreign currency ratesare assigned to each NIKE Brand entity in our geographic operating segments and are used torecord any non-functional currency revenues or product purchases into the entity's functionalcurrency. Geographic operating segment revenues and cost of sales reflect use of these standardrates. For all NIKE Brand operating segments, differences between assigned standard foreigncurrency rates and actual market rates are included in Corporate together with foreign currencyhedge gains and losses generated from our centrally managed foreign exchange risk managementprogram.

Political RiskSovereign governments have the right to regulate the movement of goods, capital, and peopleacross their borders. These laws sometimes change in unexpected ways. Political risk cangenerally be understood as execution of political power that threatens a company’s value.

The simplest solution is to conduct a little research on the riskiness of a country, either bypaying for reports from consultants that specialize in making these assessments or doing a littlebit of research yourself, using the many free sources available on the internet. Then you willhave the informed option to not set up operations in countries that are considered to be politicalrisk hot spots. It can sometimes negotiate terms of compensation with the host country, so that

there would be a legal basis for recourse in the event that something happens to disrupt thecompany's operations. However, the problem with this solution is that the legal system in thehost country may not be as developed and foreigners rarely win cases against a host country.Even worse, a revolution could spawn a new government that does not honor the actions of theprevious government.

If Nike enters a country that is considered at risk, one of the better solutions is to purchasepolitical risk insurance. It can go to one of the many organizations that specialize in selling

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 8/15

political risk insurance and purchase a policy that would compensate them if an adverseevent occurred. Because premium rates depend on the country, the industry, the number of risksinsured and other factors, the cost of doing business in one country may vary considerablycompared to another. However, buying political risk insurance does not guarantee that a

company will receive compensation immediately after an adverse event. Certain conditions, suchas trying other channels for recourse and the degree to which the business was affected, must bemet. Ultimately, it may have to wait months before any compensation is received.

Interest rate risk

Interest rate risk is simply the risk to which a portfolio or institution is exposed because futureinterest rates are uncertain. Bond prices are obviously interest rate sensitive. If rates rise, then thepresent value of a bond will fall sharply. This can also be thought of in terms of market rates: if interest rates rise, then the price of a bond will have to fall for the yield to match the new marketrates. The longer the duration of a bond the more sensitive it will be to movements in interestrates. Shares are also sensitive to interest rates; again it is obvious that if interest rates change(and other things remain equal, which the Fisher effect suggests may not be the case) then DCFvaluations will fall. In addition, the profits of highly geared companies will be significantlyaffected by the level of their interest payments. Banks can also have significant interest rate risk:for example they may have depositors locked into fixed rates and borrowers on floating rates orvice versa. Interest rate risk can be hedged using swaps and interest rate based derivatives.

Ways in which interest rate risk can be controlled include:

• investment in floating rate rather than fixed rate securities

• investing only in securities due to mature in the short term• buying interest rate derivatives.

As a consumer products company Nike is exposed to consumers’ discretionary income which iscorrelated to market cyclicality and interest rates. Decreased consumer disposable income andsentiment has adversely affected Nike’s performance during the global economic crisis. Negativemacroeconomic events pose a significant threat to Nike. The capital structure remains the samefor Nike under different scenarios because Nike historically has low levels of debt, and does notchange its borrowing patterns under different market interest rates.

Accounting risk

In finance, for an outsourcing company, many of its problems have no domestic counterpart—the payment of dividends in another currency, for example, or the need to shelter working capitalfrom the risk of devaluation, risk of currency fluctuations, or the choices between owning andlicensing.. The preparation of these financial statements requires making estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, andrelated disclosure of contingent assets and liabilities. Economic and legal questions must be dealtwith in drastically different ways. All this sums up to accounting risk for which Nike is no

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 9/15

differentNIKE, Inc. is currently rated as having Average Accounting & Governance Risk (AGR). Thisplaces them in the 43rd percentile among all companies, indicating higher Accounting &Governance Risk (AGR) than 57% of companies. AGR scores are based on statistical analysis of

accounting and governance risk factors. Lower scores indicate heightened corporate integrity risk,indicating an increased likelihood of future class action litigation, material financial restatements orimpaired equity performance.

Economic RiskEconomic risks can endanger the ability of a seller to get payment for goods or services in manyways. This type of risk can sometimes be forecast but is often completely out of the control of either the buyer or seller. Purchasing transaction insurance is essential for a buyer to minimizeeconomic risk.

Elements of economic risk include but are not limited to:

1. Convertibility risk 2. Foreign exchange risk 3. Translation risk 4. Central bank activities (interest rate fluctuation, availability of funds)5. Economic indicator movement (GDP, unemployment, purchasing power, inflation, etc.).

1. Convertibility RiskConvertibility risk is an issue when a buyer has received the goods promised and is now ready tomake payment but can’t because, for any number of possible reasons, the buyer’s governmentbars the conversion of its local currency to that of any other country. The reasons for this action

could be a possible war, a major building infrastructure program, or a massive negative tradebalance. The buyer naturally has the currency of his own country in his bank account. When thebuyer goes to the bank to exchange the local currency to the currency specified in the purchasecontract or to the currency of the seller’s country – or for that matter the currency of any “hardcurrency” country, the conversion cannot be made without proper authorization. Convertibilityrisks usually occur when the buyer’s currency does not have a ready world market. Although thetransfer of the local currency out of the buyer’s country may not have been specifically barred, itprovides little value since the seller may not be able to find a buyer for the funds.

2. Foreign Exchange Risk

Foreign exchange risk is not the same as either transfer risk or convertibility risk. Foreignexchange risk occurs when the rate of exchange between the seller’s currency and the buyer’scurrency changes dramatically between the time the order is quoted and the time the finalpayment is received. When payment is not made in a cross‐border transaction, the difficulty of collection can be compounded significantly, especially if the transaction is hedged. Therefore, itis much better to assess the level of risk and know ways to mitigate, manage, transfer or acceptthe risks.

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 10/15

• AT NIKE : Strategy -

Nike diversifies its profit sources to hedge against currency risks. Nike has establishedmultinational operations, so that one nation and currency cannot dominate earnings. Smallerinvestors can purchase shares within Nike to achieve diversification and hedge currency risks.Multinational also facilitates payments in the local currency to the local manufacturer and hencealso guard against Covertibility Risks.

Some Information about NIKE’s Risk Management Team from

LINKEDIN.COM

John Goodson's Summary

Financial Manager with a background in international finance and economics. Recent experience has focused on

foreign exchange risk management at American and European Multi-nationals and performance management.Specialties

Corporate Financial Risk Management

Financial Risk Management CoE Lead

NikePublic Company; NKE; Sporting Goods industry

September 2009 – Present (2 years 1 month)• Lead community of 18 financial risk management professionals managing foreign exchangerisk, interest rate risk, insurance, and process control risk

• Led collaborative development of vision for new Financial Risk Center of Excellenceorganization

• Proposed and leading project to develop a new FX exposure forecasting method to forecastsourcing exposures based off of Nike supply chain purchase order and planning information; thefirst time this information has been leveraged by the Nike Finance organization

• Formulate seasonal FX strategy for EUR and JPY exposures with FRM team

• Leading implementation of Value-at-Risk at Nike for FX portfolio management

Treasury Lead - Nike Trading Company ProgramNike

Public Company; NKE; Sporting Goods industry

August 2007 – August 2009 (2 years 1 month)• Developed foreign exchange business case for Trading Company to sustainably cut Nike’sannual foreign exchange volatility in half and save up to $33 M p.A. in hedge costs byemploying natural hedges and portfolio risk management techniques

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 11/15

• Introduced Trading Company to key corporate stakeholders in large presentations and toexternal business partners in international roadshows.

• Negotiated agreement between Nike’s regional CFO’s and the global product engines(Footwear, Apparel, Equipment) to change timelines for internal rate setting and allow for thetransfer of FX risk from sourcing within a season to Nike’s Treasury.

• Led three-week cross-functional process workshop to allow treasury functional experts tocollaboratively interface with treasury business partners to develop new treasury processes forNike under the Trading Company Program culminating in a 77 page document describingTreasury’s future state; Collaborative and productive atmosphere of workshop was held out asexemplary by Nike’s lean process organization for future workshop design.

• Developed concept (jointly with cross-functional trading company team) to compensate Nike’s

factories for changes in FX rates after pricing by paying in a single currency (usually USD) off an FX index

European FX Manager

Nike EMEA

Public Company; NIKE; Sporting Goods industry

February 2005 – July 2007 (2 years 6 months)• Managed exposures and proposed operational and tactical FX Risk Management strategies forapproximately USD 2.8 Billion of exchange rate exposure from Nike Sales in Europe

• Improved accuracy of P&L forecasting of FX impacts through design and implementation of a

new method of forecasting and accounting after convincing international accounting departmentto adopt new method; FY06, for instance, came in $1.5 M above budget vs. $24 M variance inprior year

• Proposed tactical hedge strategies for EUR and GPB together with Financial Risk Managementteam that improved European results by $60 M for FY06 and FY07 compared to averageexecution

• Proposed strategy to extend hedge horizon of Turkish Lira for first time ever to cover Nikeagainst TRY collapse in summer of 2006, saving Nike $2.5 M in FX losses over three monthperiod

• Developed effective presentation of FX issues (Net Hedging, Long-term risk to financial plan)to shape how EMEA stakeholders (CFO, Business Units, Strategic Planning, Business Planning)think about FX issues

• Built support for Turkish-Lira sourcing through road-show type presentation of business case toApparel sourcing team, Apparel Finance, CEMEA strategic planning and finance functions,EMEA CFO, Nike Turkey, and Turkey NLO

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 12/15

• Coordinated Apparel sourcing, pricing, and IT functions, along with benchmarking againstfootwear experience, to work-through potential difficulties of changing vendor currency fromEUR to TRY

• Worked with Demand Planning and BU finance functions to improve Purchasing Forecasts

FX Risk Manager

Nike

Public Company; NKE; Sporting Goods industry

December 2001 – January 2005 (3 years 2 months)• Managed exposures and proposed operational and tactical FX Risk Management strategies forapproximately USD 3 Billion of exchange rate exposure from Nike Sales in Asia and theAmericas

• Led technical conversion of Nike’s FX settlements to CLS, working with technical and ITexperts from FXpress, Nike’s FX Management software, and HSBC, Nike’s CLS Gateway Bank,to ensure a technically flawless conversion

• Proposed that Nike’s new sales entity in Russia operate on ‘currency units’ (USD), eventuallysaving Nike $26 M in foregone currency losses during the rapid ruble depreciation in Nike’s2009 fiscal year

• Created first consolidated summary of Nike’s FX Sales exposures enabling more holistic risk

management

• Pioneered P&L Impact forecasting for primary Nike sales companies in Asia and the Americas• Proposed and implemented market-based method of assessing performance of Nike’s tacticalhedge program

3. Translation RiskTranslation risk involves the revaluation of foreign assets that are held in a foreign currency.There may be a difference in the current foreign exchange rate from the time of the original

transaction to time of the fulfillment of the sales contract. Assets held on the balance sheet inforeign currency must periodically be revalued to the current market price of that currency. Thiskind of revaluation to the current market will create an exchange loss or gain. This exchangegain or loss is unrealized but still impacts the value of the assets held overseas. An example follows:

Plant and equipment of an international company are marked to market at year‐end for financialreporting purposes. Conditions throughout the year have caused a decline in the value of the

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 13/15

currency of their foreign holdings of 20%. This decline has the immediate affect of reducing thevalue of these assets by 20%, which then has the direct impact of reducing the company’sprofitability for the year by the same value even though no direct transaction has occurred otherthan the revaluation to create this loss.

At NIKE: Specific to Nike, Nike has its manufacturing units in India, China, Bietnam and forfew products in U.S. and the GDP growth and the market conditions of these markets are quitevaried.

4. Economic indicator movement (GDP, unemployment, purchasing

power, inflation, etc.)

4.1 Inflation: The main negative effects of inflation are:

Inflation erodes international competitiveness. Exports cost more abroad. This can cause adecrease in demand for exports. That in turn can lead to a decrease in demand for the currencyand to a devaluation of the currency. The devaluation may restore exports, but at the cost of making imports more expensive, thus increasing inflation again! It is because inflation erodesinternational competitiveness that most governments make controlling inflation the central pillarof their economic policy.

At NIKE: Nike's labor costs comprise just 5% of Nike's total product costs. In fact, the biggestchunk of operating costs, such as R&D, logistics, marketing and product design, are still kept inthe U.S. Outsourcing production to developing countries helps Nike alleviate pressure to increaseprices. After all, not too many consumers want to see a pair of Nike running shoes at Foot

Locker with a price tag of $300 dangling from the sole.Nike has begun to show progress by implementing Lean and Human resource management infactories. Lean and Human Resource Management deals with quality over quantity. Nike’sstrategy is to build a more lean, green, empowered and equitable supply chain. This managementhas helped to reduce waste and toxics, and increased their use of environmentally preferredmaterials.

4.2 Difficult Economic Times (GDP) The economic slowdown began with a decline in business capital spending and investment.

As a consumer products company Nike is exposed to consumers’ discretionary income which is

correlated to market cyclicality and interest rates. Decreased consumer disposable income andsentiment has adversely affected Nike’s performance during the global economic crisis. Negativemacroeconomic events pose a significant threat to Nike.

A simple way to differentiate commercial and country‐risk is provided below:

country risk = political risk + economic risk

commercial risk = business transaction risk

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 14/15

RISK REDUCTION TECHNIQUE

At Nike :

Risk Management

Since Nike markets its products in over 140 countries with foreign sales revenue accountingfor 46 percent of its total revenue, the Company is exposed to global market risks, including theeffect of changes in foreign currency exchange rates and interest rates. The Company does nothold or issue derivatives for trading purposes. The Company uses derivatives to manage financialexposures that occur in the normal course of business. it is the company’s policy to utilizederivative financial instruments to reduce foreign exchange risks where internal netting strategiescannot be effectively employed. Fluctuation in the value of the hedging instruments are offset byfluctuations in the value of the underlying exposures being hedged.

Nike uses forward contracts

for firm commitments to hedge receivables and payables as well as intercompany foreigncurrency transactions, while using currency options to hedge certain anticipated but not yetfirmly committed export sales and purchase transactions expected in futures denominated inforeign currency. Cross-currency swaps are employed to hedge foreign currency-denominatedpayments related to intercompany loan agreements

Substantially all derivatives outstanding are designated as either cash flow, fair valuehedges or net investment hedges. All derivatives are recognized on the balance sheet at their fairvalue. Unrealized gain positions are recorded as other current assets or other non-current assets,depending on the instrument’s maturity date. Unrealized loss positions are recorded as accruedliabilities or other non-current liabilities. All changes in fair values of outstanding cash flowhedge derivatives, except the ineffective portion, are recorded in other comprehensive income,

until net income is affected by the variability of cash flows of the hedged transaction. Changes inthe fair value of hedges designated as fair value hedges are recorded in net income and are offsetby the change in fair value of the underlying asset or liability being hedged. Changes in the fairvalues of outstanding net investment hedges, except any ineffective portion, are recorded withinthe cumulative translation adjustment component of other comprehensive income.

Foreign currency exposures and hedging practices

As a global leader in consumer products, Nike is exposed to exchange rate risk of severalcurrencies. Its primary foreign currency exposures are related to United States dollar transactions

at wholly-owned foreign subsidiaries, as well as transactions and translation of resultsdenominated in the Euro, British pound, Chinese Yuan, and Japanese Yen. Nike’s foreignexchange risk management program seeks to minimize volatility of currency fluctuations indollar terms. Nike manages these exposures by taking advantage of natural offsets and currencycorrelations that exist within its currency portfolio.

8/4/2019 If Assignment_Group No. 5

http://slidepdf.com/reader/full/if-assignmentgroup-no-5 15/15

Hedging policies:

1) Nike uses Value-at-Risk (“VaR”) to monitor the foreign exchange risk of our foreigncurrency forward and foreign currency option derivative instruments. The VaR

determines the maximum potential one-day loss in the fair value of these foreignexchange rate-sensitive financial instruments. While the total notional value of ourforeign currency derivative instruments has declined since May 31, 2008, foreigncurrency volatilities have increased significantly and have resulted in an increasedestimated maximum one-day loss in fair value of $61.8 million as of February 28, 2009as compared to $34.9 million as of May 31, 2008. This hypothetical loss in fair value of our derivatives would be offset by increases in the value of the underlying transactionsbeing hedged.

2) Nike maintains disclosure controls and procedures that are designed to ensure thatinformation required to be disclosed in their Exchange Act reports is recorded, processed,summarized and reported within the time periods specified in the Securities andExchange Commission’s rules and forms and that such information is accumulated andcommunicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow for timely decisions regarding requireddisclosure. In designing and evaluating the disclosure controls and procedures,management recognizes that any controls and procedures, no matter how well designedand operated, can provide only reasonable assurance of achieving the desired controlobjectives, and management is required to apply its judgment in evaluating the cost-benefit relationship of possible controls and procedures .it carries out a variety of on-going procedures under the supervision and with the participation of our management,including our Chief Executive Officer and Chief Financial Officer, to evaluate theeffectiveness of the design and operation of our disclosure controls and procedures.

CONCLUSION

While most of these risks mentioned above have been eliminated in the derivative markets inwhich the trade takes place in organized exchanges, the risks of over-the-counter transactionsremain fairly substantial worldwide. Furthermore, the greater interdependencies among variouseconomic units and the increase in the use and abuse of derivatives as well as greatercoordination of fiscal and monetary policies in the context of various treaties (i.e., EuropeanUnion, North American Free Trade Agreement, Asian Free Trade Agreement, and EconomicCooperation of West African Economies) have created an environment in which a shock to alocal economy can easily spread to other trading partners.