Embed Size (px)

Citation preview

IDLC Finance Limited

Earnings Disclosure

FY 2018

18 February 2019

Forward Looking Statements

This presentation may contain statements that constitute forward-looking statements about the Company, within the

general meaning of the term and within the meaning of applicable securities laws, including financial projections and

estimates and their underlying assumptions, statements regarding plans, objectives and expectations. These statements

may appear in a number of places in this document and may include statements regarding our intent, belief or current

expectations regarding our customer base, estimates regarding future growth in our different business lines, market share,

financial results and other aspects of our activity and situation relating to the Company. The forward looking statements in

this document can be identified, in some instances, by the use of words such as “expects”, “anticipates”, “intends”,

“believes”, and similar language or the negative thereof or by the forward-looking nature of discussions of strategy, plans

or intentions.

Such forward-looking statements, by their nature, are not guarantees of future performance and involve risks and

uncertainties, and actual results may differ materially from those in the forward-looking statements as a result of various

factors.

Neither this presentation nor any of the information contained herein constitutes an offer of purchase, sale or exchange,

nor a request for an offer of purchase, sale or exchange of securities, or any advice or recommendation with respect to

such securities.

Finally, be advised that this document may contain summarized information or information that has not been audited. In

this sense, this information is subject to, and must be read in conjunction with, all other publicly available information.

Slide 2 of 22

Macro factors that shaped 2018

• AD Ratio guidelines affecting liquidity scenario

– As banks scrambled for funds to maintain their AD ratio, and further reduce it to 83.5% following directives from the central bank, interest rates moved

upwards at the beginning of the year

– Situation was stabilized by mid-year

• Current Account deficit and pressure on exchange rate

– Current account deficit of Bangladesh reached its historical highest at USD 9.8 bn in 2018

– As USD got dearer, Central Bank supported the currency throughout the year, soaking up further BDT liquidity from the market

• Capital market scenario

– Transaction volume dried up as stocks fell. Large caps were affected the most and pulled the index down with them

– Corporate profitability was also hit as cost of imported raw materials and cost of financing rose

– As interest rates rose, some investors were incentivized to pull money out of the capital market and invest rather in fixed income instruments

• Political environment

– Political environment was rather calm and there was no significant disruption in the business climate, though activities slowed in the months

approaching the election at the end of the year

Slide 3 of 22

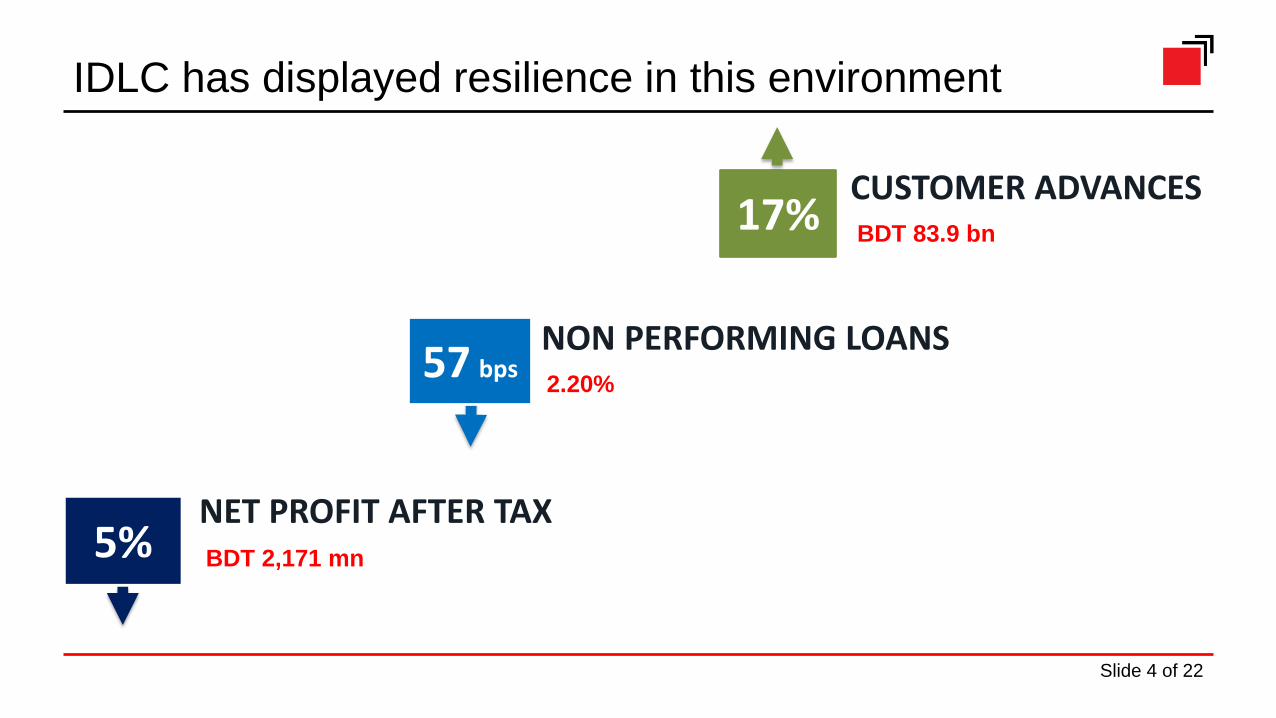

57 bps

IDLC has displayed resilience in this environment

2.20%

NON PERFORMING LOANS

BDT 83.9 bn

CUSTOMER ADVANCES17%

BDT 2,171 mn

NET PROFIT AFTER TAX5%

Slide 4 of 22

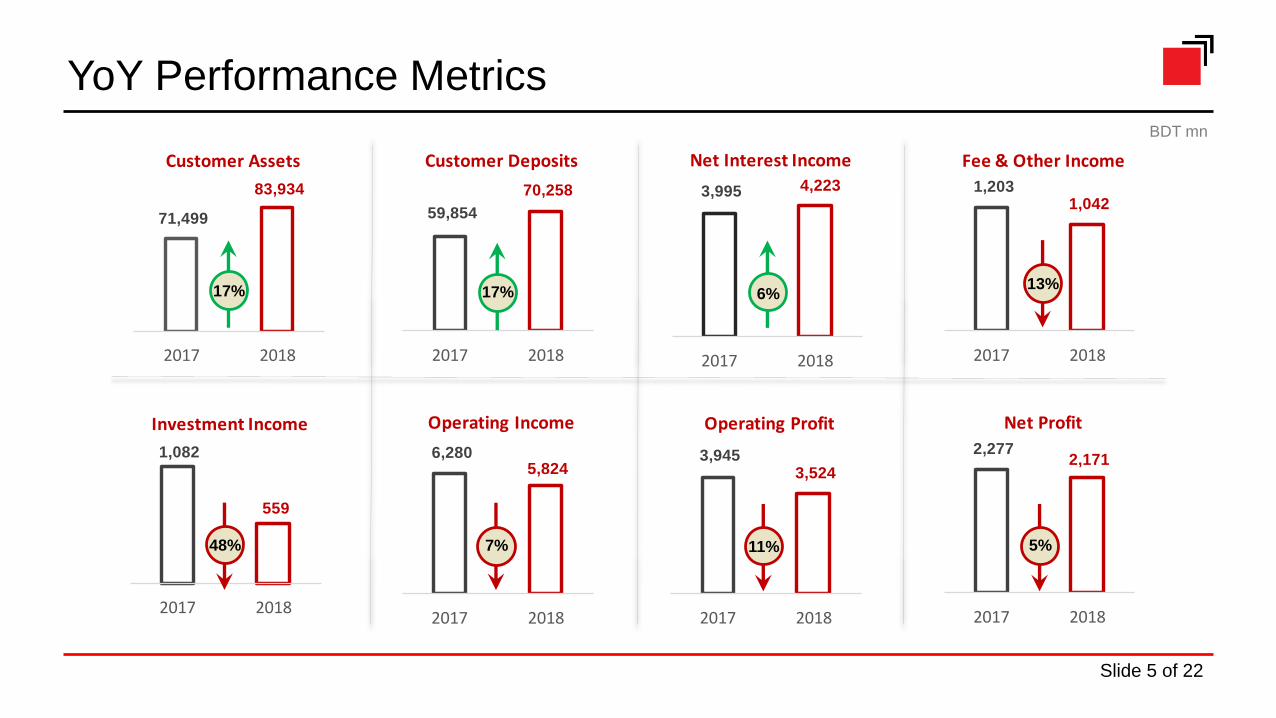

2,277 2,171

2017 2018

Net Profit

3,945 3,524

2017 2018

Operating Profit

6,280 5,824

2017 2018

Operating Income

1,082

559

2017 2018

Investment Income

1,203 1,042

2017 2018

Fee & Other Income

3,995 4,223

2017 2018

Net Interest Income

59,854

70,258

2017 2018

Customer Deposits

71,499

83,934

2017 2018

Customer Assets

13%17% 17% 6%

7% 11% 5%

BDT mn

48%

YoY Performance Metrics

Slide 5 of 22

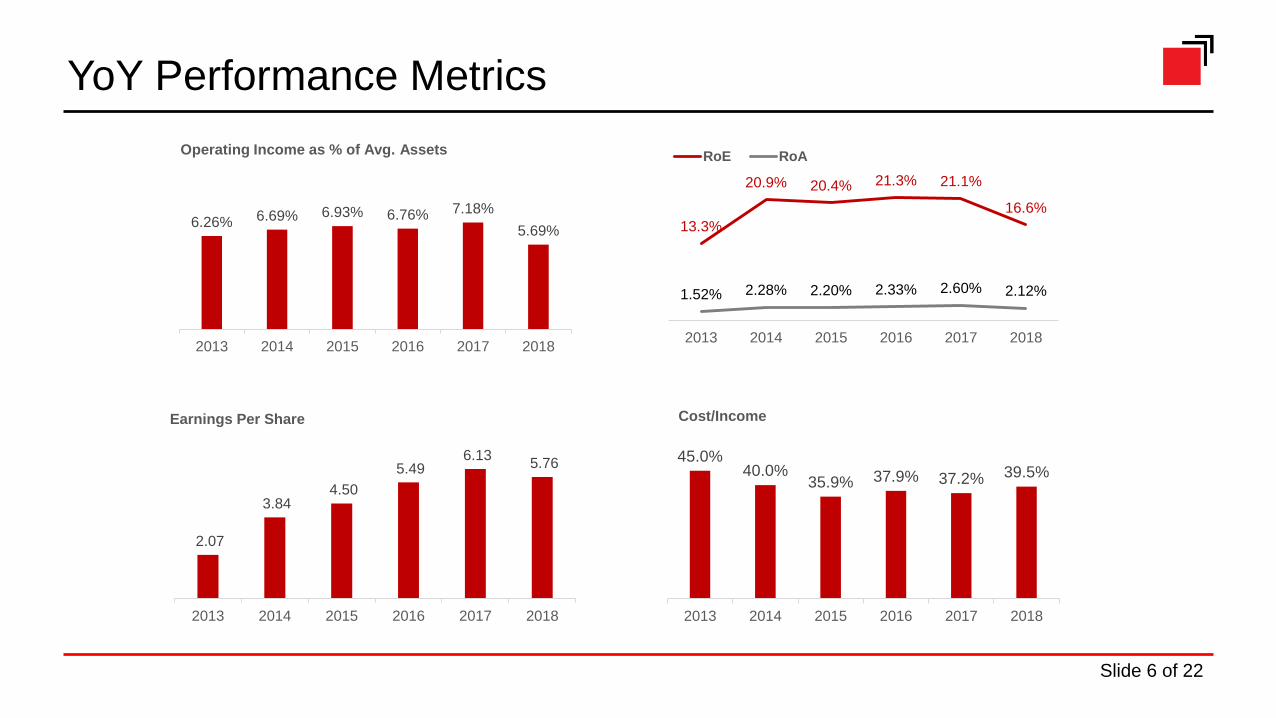

6.26% 6.69% 6.93% 6.76% 7.18%

5.69%

2013 2014 2015 2016 2017 2018

Operating Income as % of Avg. Assets

45.0%40.0%

35.9% 37.9% 37.2% 39.5%

2013 2014 2015 2016 2017 2018

Cost/Income

13.3%

20.9% 20.4% 21.3% 21.1%

16.6%

1.52% 2.28% 2.20% 2.33% 2.60% 2.12%

2013 2014 2015 2016 2017 2018

RoE RoA

2.07

3.84 4.50

5.49 6.13

5.76

2013 2014 2015 2016 2017 2018

Earnings Per Share

YoY Performance Metrics

Slide 6 of 22

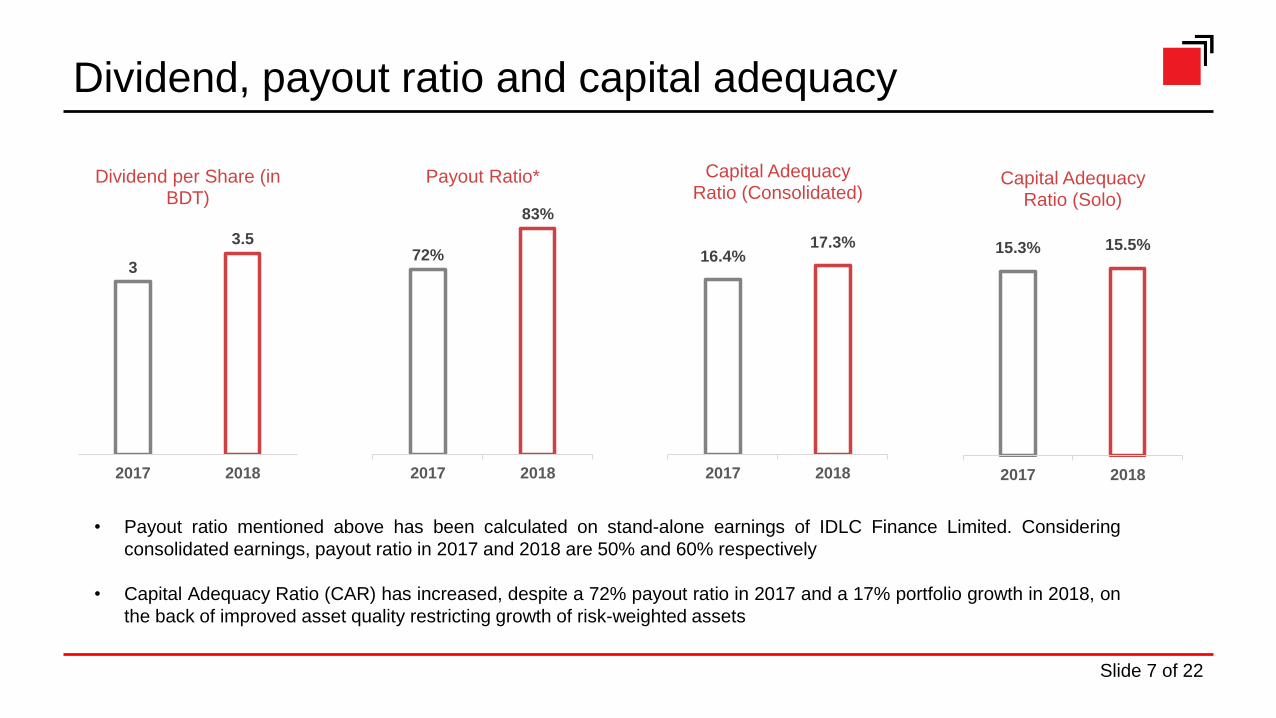

Dividend, payout ratio and capital adequacy

3

3.5

2017 2018

Dividend per Share (in BDT)

72%

83%

2017 2018

Payout Ratio*

16.4%17.3%

2017 2018

Capital Adequacy Ratio (Consolidated)

15.3% 15.5%

2017 2018

Capital Adequacy Ratio (Solo)

• Payout ratio mentioned above has been calculated on stand-alone earnings of IDLC Finance Limited. Considering

consolidated earnings, payout ratio in 2017 and 2018 are 50% and 60% respectively

• Capital Adequacy Ratio (CAR) has increased, despite a 72% payout ratio in 2017 and a 17% portfolio growth in 2018, on

the back of improved asset quality restricting growth of risk-weighted assets

Slide 7 of 22

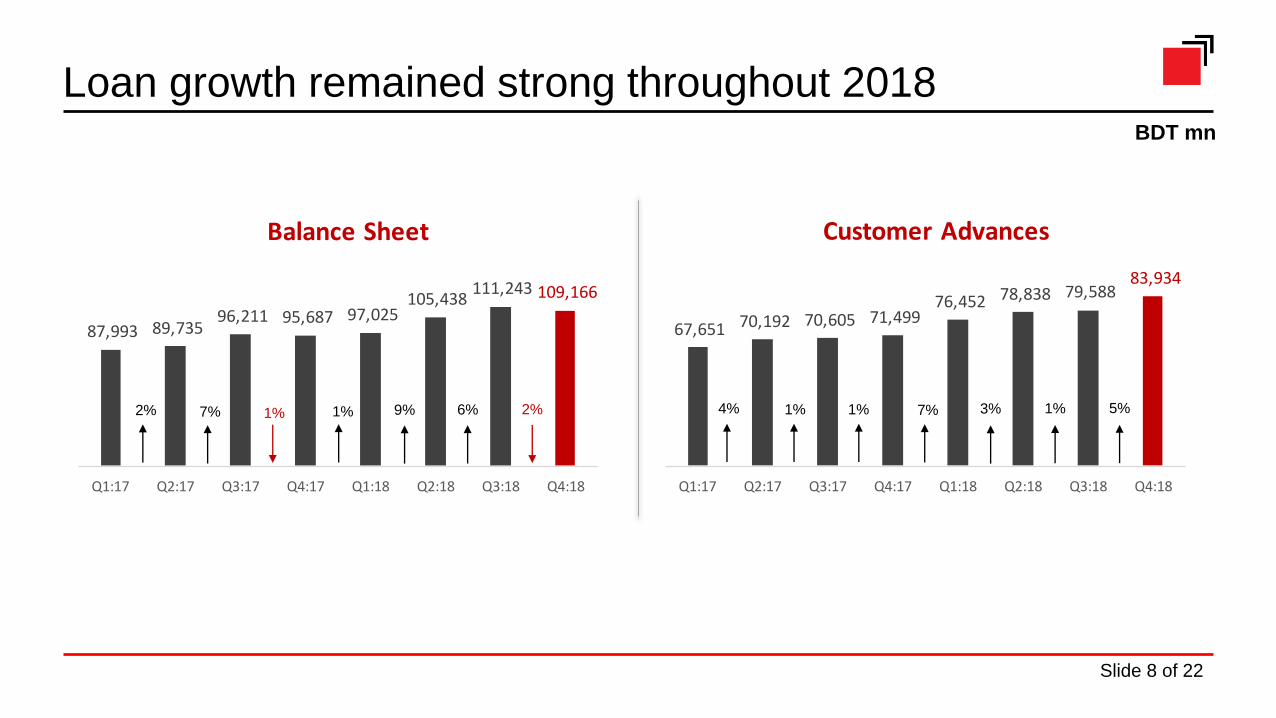

67,651 70,192 70,605 71,499 76,452 78,838 79,588

83,934

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Customer Advances

87,993 89,735 96,211 95,687 97,025

105,438 111,243 109,166

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Balance Sheet

Loan growth remained strong throughout 2018BDT mn

4% 1% 1% 7%2% 7% 1% 1% 9% 3%6% 1%2% 5%

Slide 8 of 22

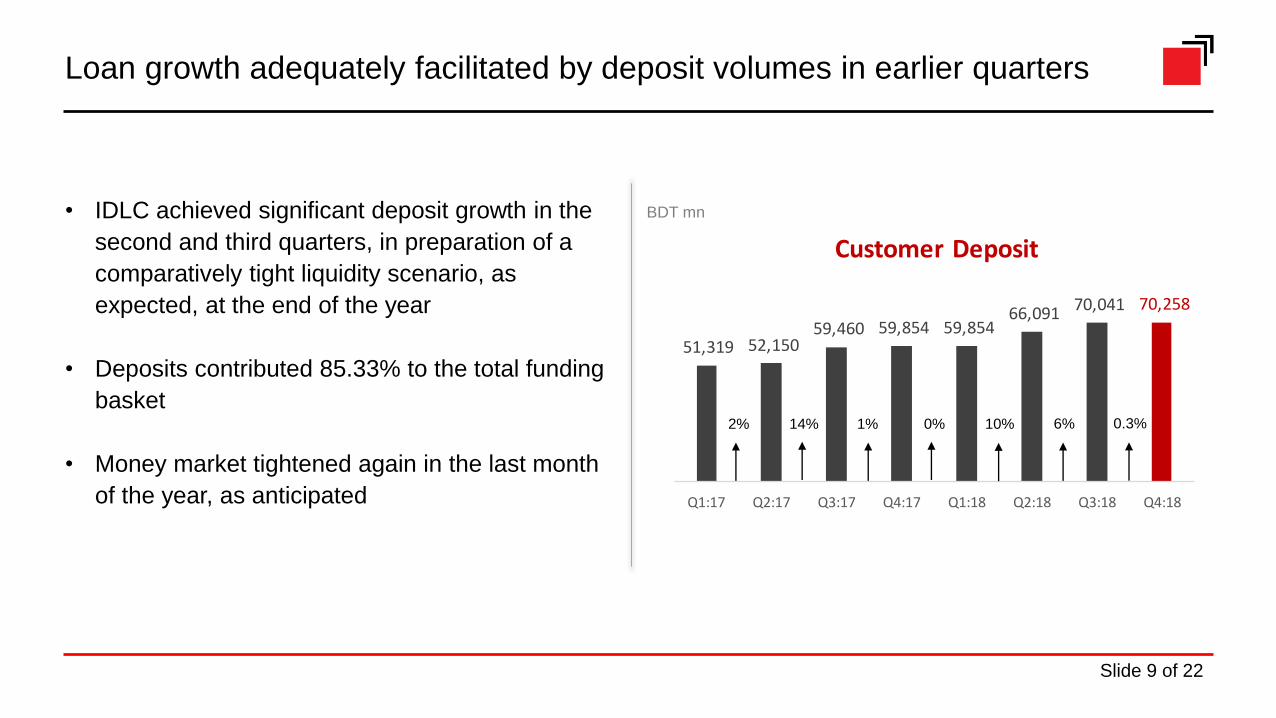

51,319 52,150 59,460 59,854 59,854

66,091 70,041 70,258

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Customer Deposit

Loan growth adequately facilitated by deposit volumes in earlier quarters

BDT mn

2% 14% 1% 0% 10% 6%

• IDLC achieved significant deposit growth in the

second and third quarters, in preparation of a

comparatively tight liquidity scenario, as

expected, at the end of the year

• Deposits contributed 85.33% to the total funding

basket

• Money market tightened again in the last month

of the year, as anticipated

0.3%

Slide 9 of 22

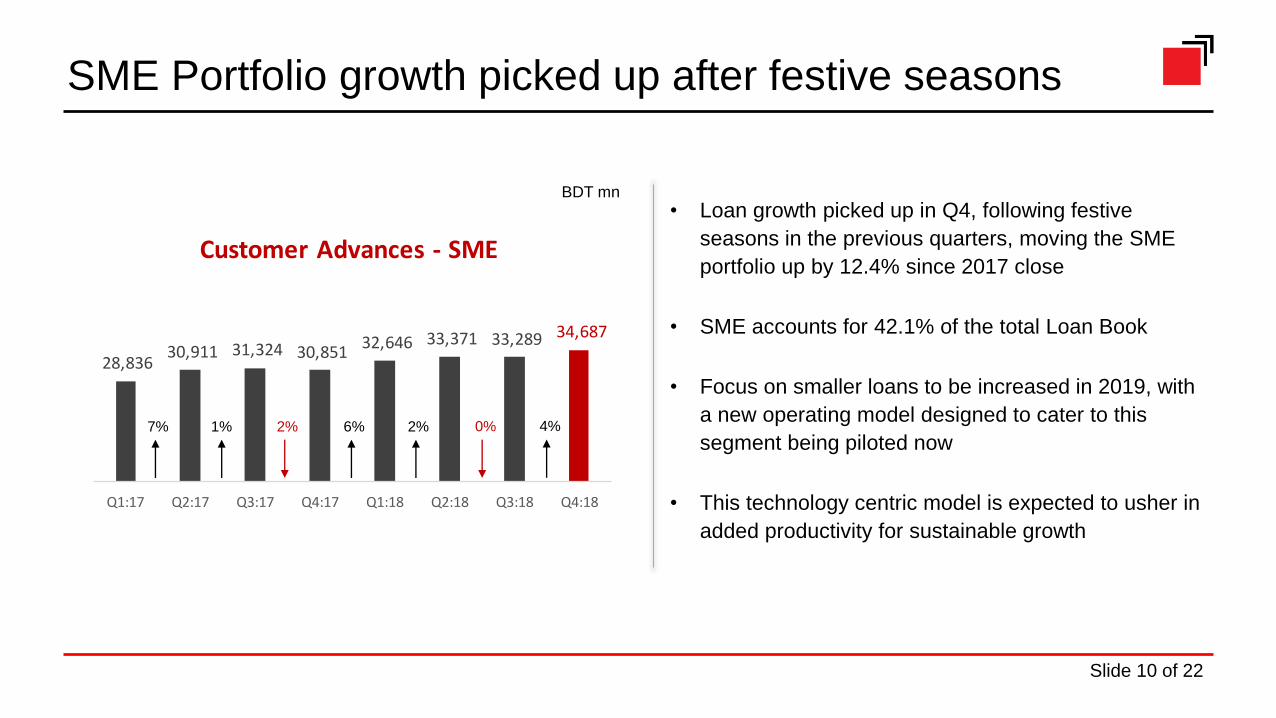

28,836 30,911 31,324 30,851

32,646 33,371 33,289 34,687

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Customer Advances - SME

SME Portfolio growth picked up after festive seasons

BDT mn

7% 1% 2% 6% 2% 0%

• Loan growth picked up in Q4, following festive

seasons in the previous quarters, moving the SME

portfolio up by 12.4% since 2017 close

• SME accounts for 42.1% of the total Loan Book

• Focus on smaller loans to be increased in 2019, with

a new operating model designed to cater to this

segment being piloted now

• This technology centric model is expected to usher in

added productivity for sustainable growth

4%

Slide 10 of 22

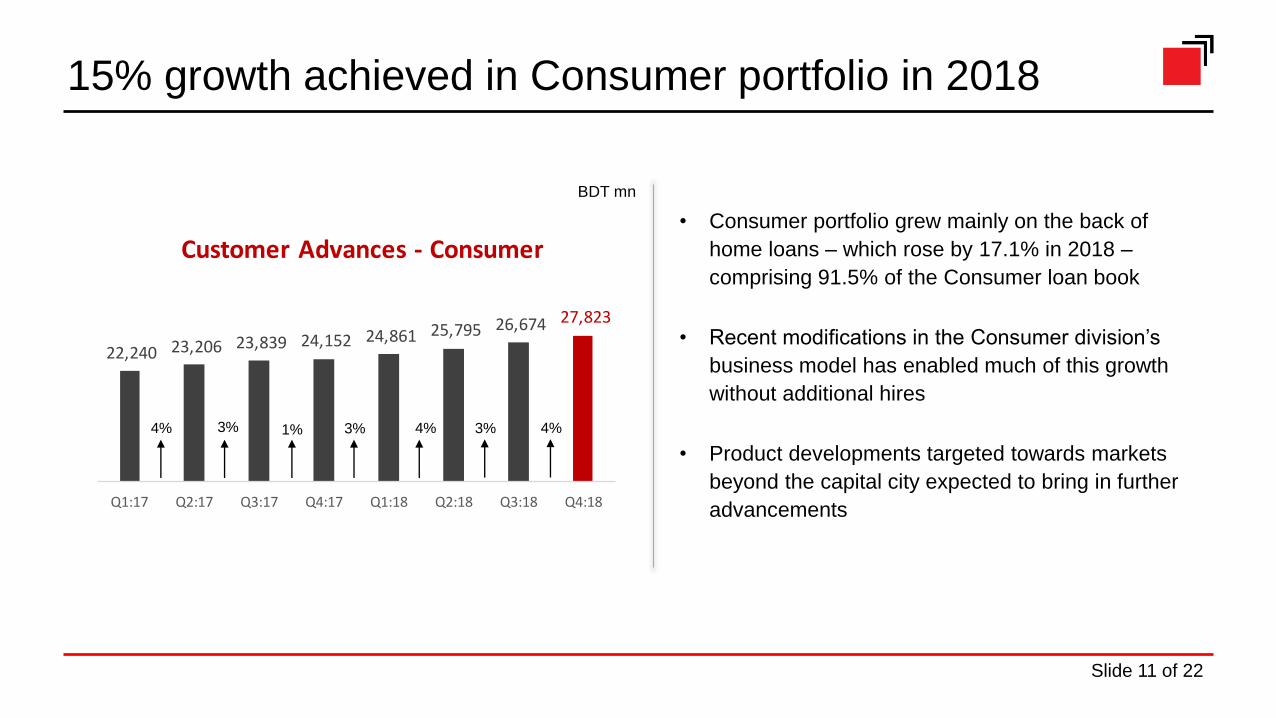

22,240 23,206 23,839 24,152 24,861 25,795 26,674 27,823

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Customer Advances - Consumer

4% 3% 1%

BDT mn

3% 4% 3%

15% growth achieved in Consumer portfolio in 2018

• Consumer portfolio grew mainly on the back of

home loans – which rose by 17.1% in 2018 –

comprising 91.5% of the Consumer loan book

• Recent modifications in the Consumer division’s

business model has enabled much of this growth

without additional hires

• Product developments targeted towards markets

beyond the capital city expected to bring in further

advancements

4%

Slide 11 of 22

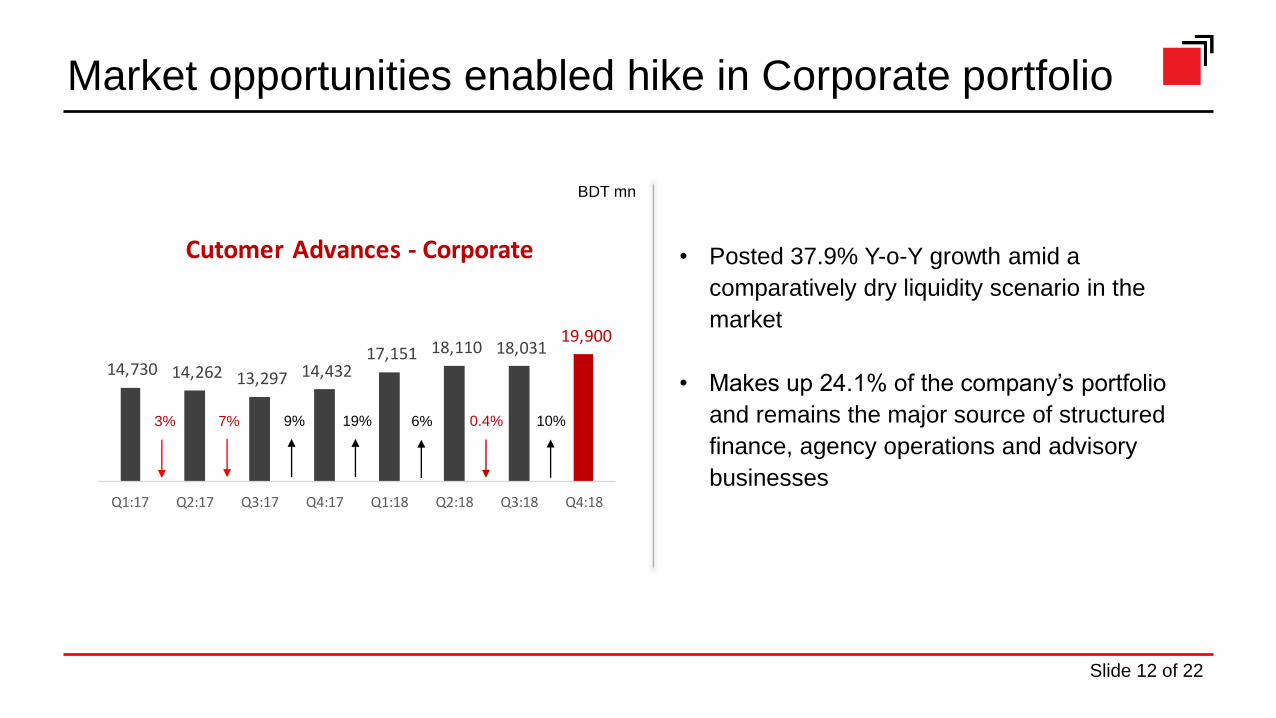

14,730 14,262 13,297 14,432 17,151 18,110 18,031

19,900

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

Cutomer Advances - Corporate

3% 7% 9%

• Posted 37.9% Y-o-Y growth amid a

comparatively dry liquidity scenario in the

market

• Makes up 24.1% of the company’s portfolio

and remains the major source of structured

finance, agency operations and advisory

businesses

BDT mn

19% 6% 0.4%

Market opportunities enabled hike in Corporate portfolio

10%

Slide 12 of 22

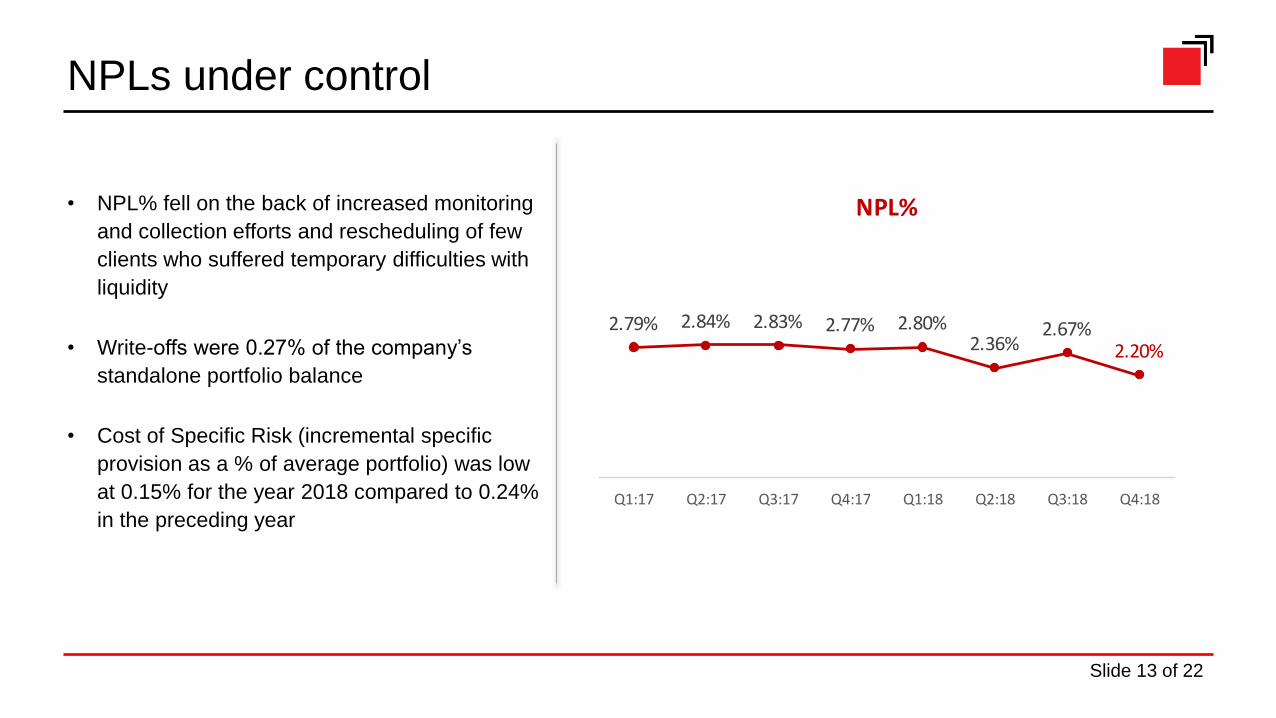

• NPL% fell on the back of increased monitoring

and collection efforts and rescheduling of few

clients who suffered temporary difficulties with

liquidity

• Write-offs were 0.27% of the company’s

standalone portfolio balance

• Cost of Specific Risk (incremental specific

provision as a % of average portfolio) was low

at 0.15% for the year 2018 compared to 0.24%

in the preceding year

NPLs under control

2.79% 2.84% 2.83% 2.77% 2.80%2.36%

2.67%2.20%

Q1:17 Q2:17 Q3:17 Q4:17 Q1:18 Q2:18 Q3:18 Q4:18

NPL%

Slide 13 of 22

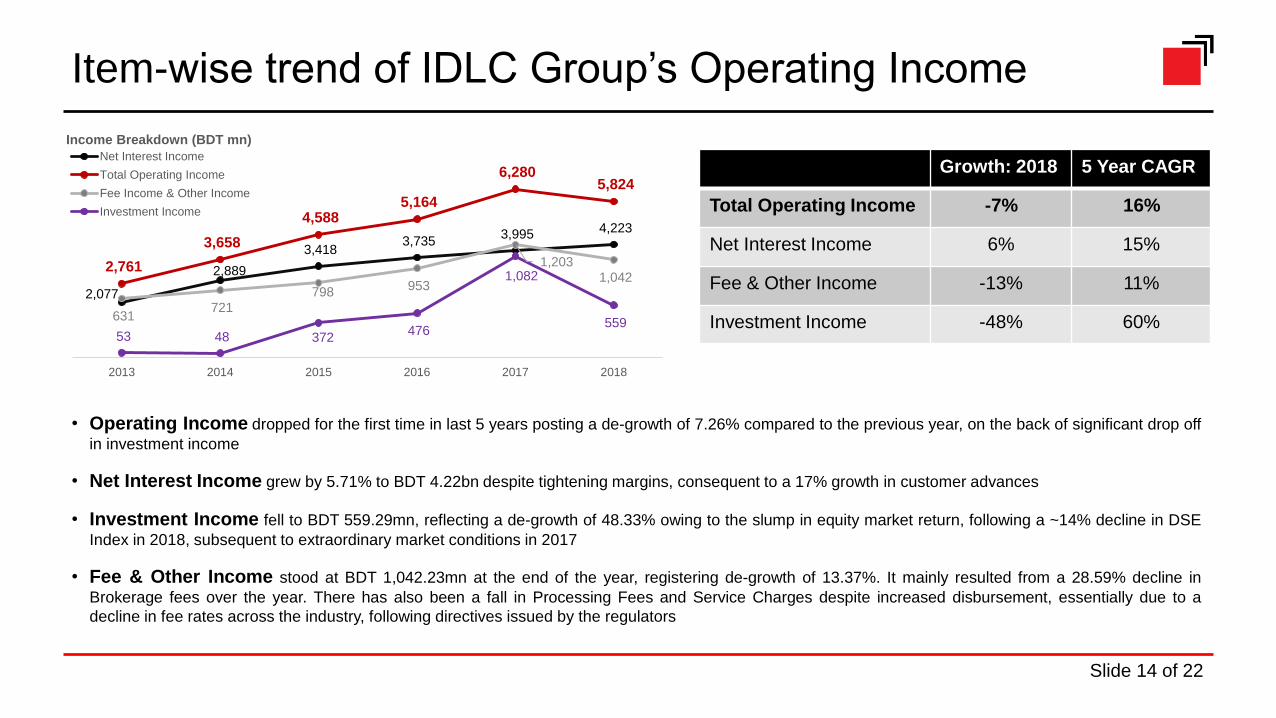

Item-wise trend of IDLC Group’s Operating Income

Growth: 2018 5 Year CAGR

Total Operating Income -7% 16%

Net Interest Income 6% 15%

Fee & Other Income -13% 11%

Investment Income -48% 60%

2,077

2,889

3,418 3,735

3,995 4,223

2,761

3,658

4,588 5,164

6,280 5,824

631 721

798 953

1,203 1,042

53 48 372 476

1,082

559

2013 2014 2015 2016 2017 2018

Income Breakdown (BDT mn)

Net Interest Income

Total Operating Income

Fee Income & Other Income

Investment Income

• Operating Income dropped for the first time in last 5 years posting a de-growth of 7.26% compared to the previous year, on the back of significant drop off

in investment income

• Net Interest Income grew by 5.71% to BDT 4.22bn despite tightening margins, consequent to a 17% growth in customer advances

• Investment Income fell to BDT 559.29mn, reflecting a de-growth of 48.33% owing to the slump in equity market return, following a ~14% decline in DSE

Index in 2018, subsequent to extraordinary market conditions in 2017

• Fee & Other Income stood at BDT 1,042.23mn at the end of the year, registering de-growth of 13.37%. It mainly resulted from a 28.59% decline in

Brokerage fees over the year. There has also been a fall in Processing Fees and Service Charges despite increased disbursement, essentially due to a

decline in fee rates across the industry, following directives issued by the regulators

Slide 14 of 22

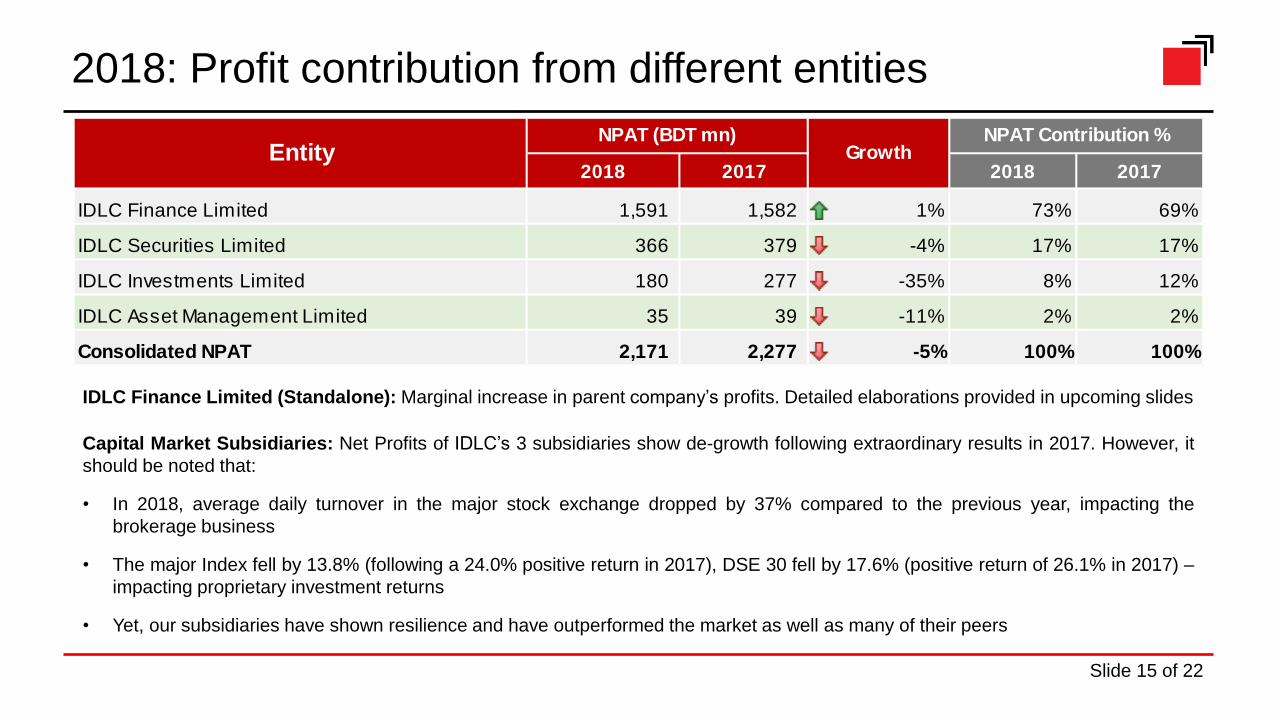

2018: Profit contribution from different entities

2018 2017 2018 2017

IDLC Finance Limited 1,591 1,582 1% 73% 69%

IDLC Securities Limited 366 379 -4% 17% 17%

IDLC Investments Limited 180 277 -35% 8% 12%

IDLC Asset Management Limited 35 39 -11% 2% 2%

Consolidated NPAT 2,171 2,277 -5% 100% 100%

EntityNPAT Contribution %

GrowthNPAT (BDT mn)

IDLC Finance Limited (Standalone): Marginal increase in parent company’s profits. Detailed elaborations provided in upcoming slides

Capital Market Subsidiaries: Net Profits of IDLC’s 3 subsidiaries show de-growth following extraordinary results in 2017. However, it

should be noted that:

• In 2018, average daily turnover in the major stock exchange dropped by 37% compared to the previous year, impacting the

brokerage business

• The major Index fell by 13.8% (following a 24.0% positive return in 2017), DSE 30 fell by 17.6% (positive return of 26.1% in 2017) –

impacting proprietary investment returns

• Yet, our subsidiaries have shown resilience and have outperformed the market as well as many of their peers

Slide 15 of 22

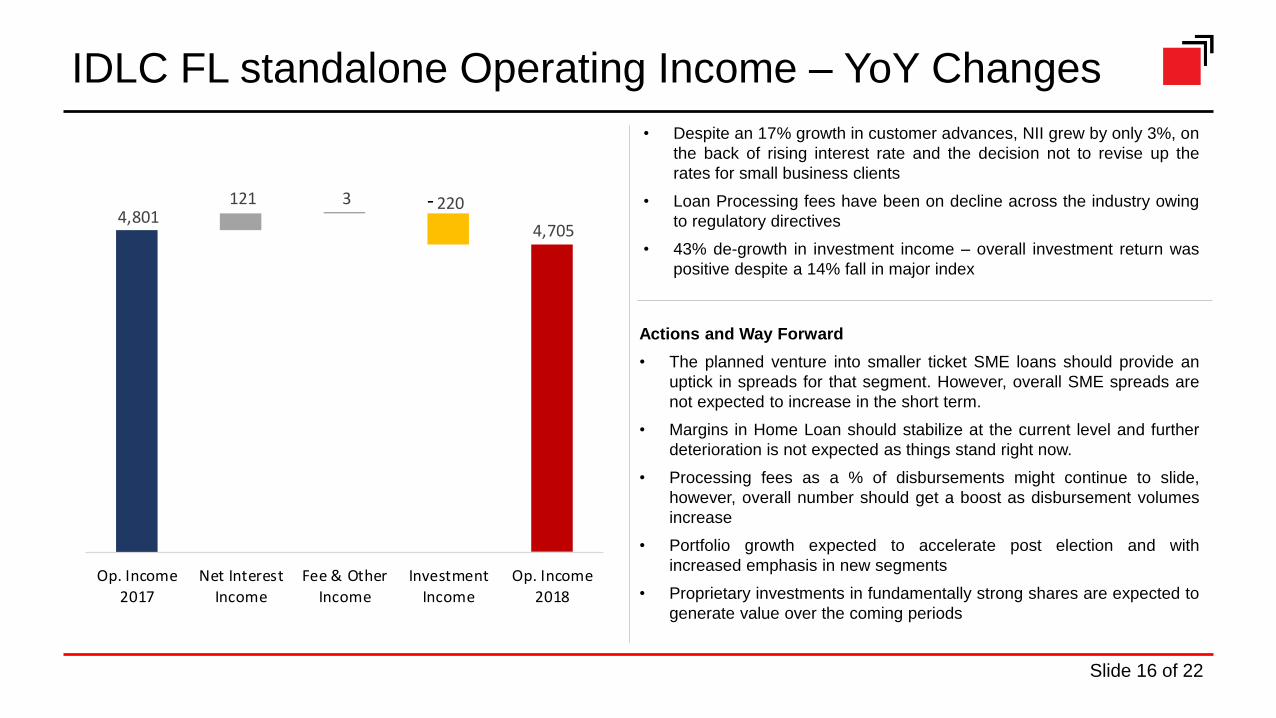

• Despite an 17% growth in customer advances, NII grew by only 3%, on

the back of rising interest rate and the decision not to revise up the

rates for small business clients

• Loan Processing fees have been on decline across the industry owing

to regulatory directives

• 43% de-growth in investment income – overall investment return was

positive despite a 14% fall in major index

Actions and Way Forward

• The planned venture into smaller ticket SME loans should provide an

uptick in spreads for that segment. However, overall SME spreads are

not expected to increase in the short term.

• Margins in Home Loan should stabilize at the current level and further

deterioration is not expected as things stand right now.

• Processing fees as a % of disbursements might continue to slide,

however, overall number should get a boost as disbursement volumes

increase

• Portfolio growth expected to accelerate post election and with

increased emphasis in new segments

• Proprietary investments in fundamentally strong shares are expected to

generate value over the coming periods

IDLC FL standalone Operating Income – YoY Changes

4,705

220 4,801

121 3

Op. Income

2017

Net Interest

Income

Fee & Other

Income

Investment

Income

Op. Income

2018

-

Slide 16 of 22

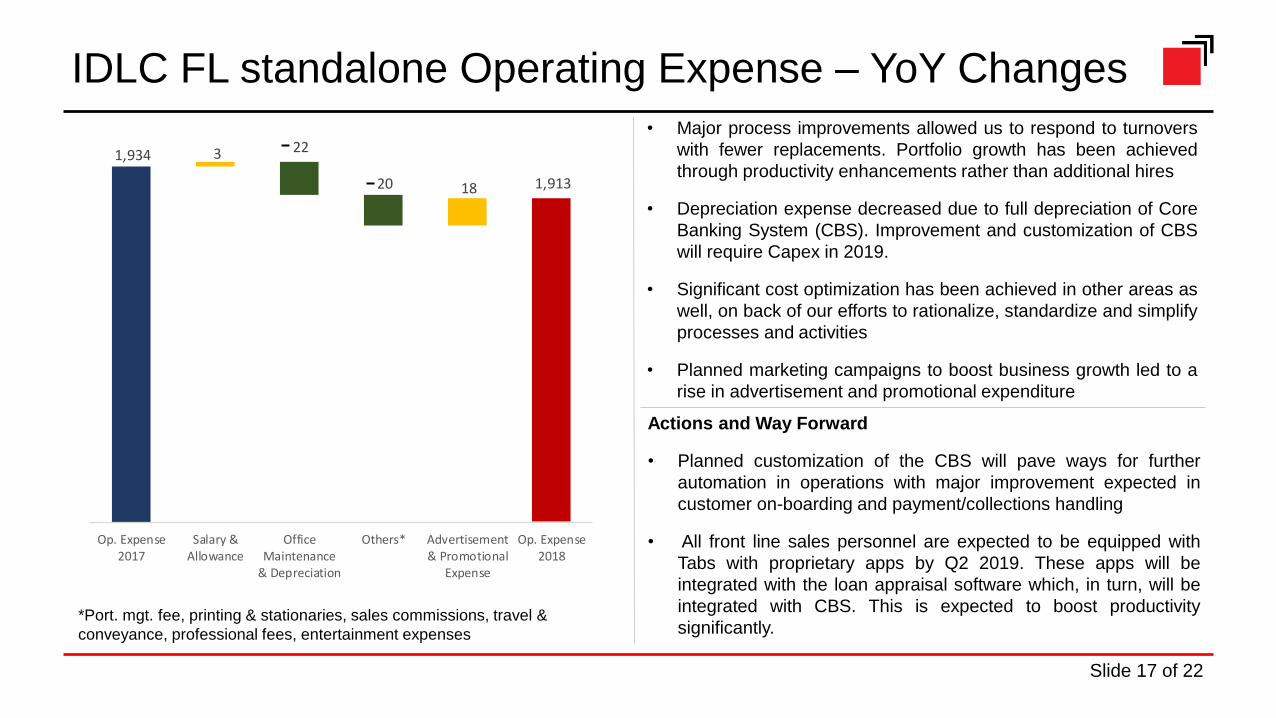

1,913

22

20

1,934 3

18

Op. Expense2017

Salary &Allowance

OfficeMaintenance

& Depreciation

Others* Advertisement& Promotional

Expense

Op. Expense2018

• Major process improvements allowed us to respond to turnovers

with fewer replacements. Portfolio growth has been achieved

through productivity enhancements rather than additional hires

• Depreciation expense decreased due to full depreciation of Core

Banking System (CBS). Improvement and customization of CBS

will require Capex in 2019.

• Significant cost optimization has been achieved in other areas as

well, on back of our efforts to rationalize, standardize and simplify

processes and activities

• Planned marketing campaigns to boost business growth led to a

rise in advertisement and promotional expenditure

IDLC FL standalone Operating Expense – YoY Changes

Actions and Way Forward

• Planned customization of the CBS will pave ways for further

automation in operations with major improvement expected in

customer on-boarding and payment/collections handling

• All front line sales personnel are expected to be equipped with

Tabs with proprietary apps by Q2 2019. These apps will be

integrated with the loan appraisal software which, in turn, will be

integrated with CBS. This is expected to boost productivity

significantly.*Port. mgt. fee, printing & stationaries, sales commissions, travel &

conveyance, professional fees, entertainment expenses

Slide 17 of 22

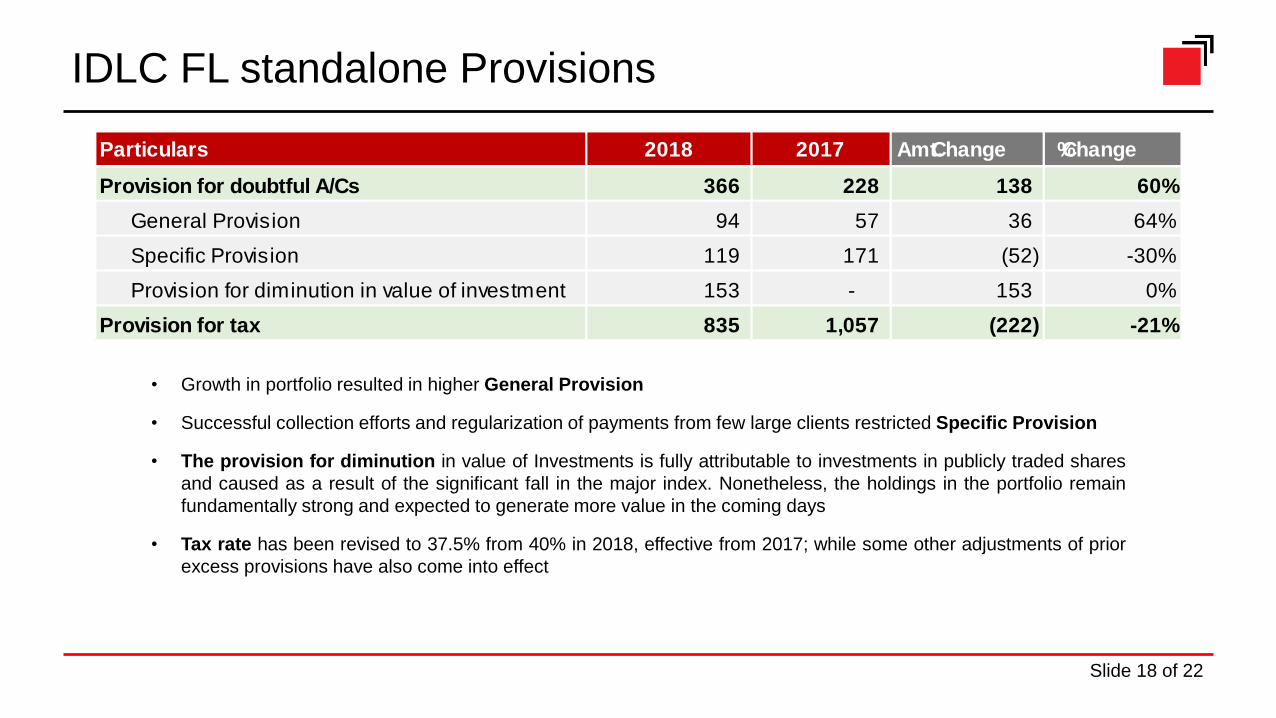

• Growth in portfolio resulted in higher General Provision

• Successful collection efforts and regularization of payments from few large clients restricted Specific Provision

• The provision for diminution in value of Investments is fully attributable to investments in publicly traded shares

and caused as a result of the significant fall in the major index. Nonetheless, the holdings in the portfolio remain

fundamentally strong and expected to generate more value in the coming days

• Tax rate has been revised to 37.5% from 40% in 2018, effective from 2017; while some other adjustments of prior

excess provisions have also come into effect

IDLC FL standalone Provisions

Particulars 2018 2017 Amt. Change % Change

Provision for doubtful A/Cs 366 228 138 60%

General Provision 94 57 36 64%

Specific Provision 119 171 (52) -30%

Provision for diminution in value of investment 153 - 153 0%

Provision for tax 835 1,057 (222) -21%

Slide 18 of 22

Ongoing challenges and mitigation avenues

• Maturity mismatch – lack of a mature bond market and limited availability of other long-term funding means creates a maturity

mismatch for most Banks and NBFIs that book long-term loan assets

Focus on maintaining renewal rates

o On an average, 75%-80% deposits in IDLC are renewed upon maturity

Continue to seek long-term funding opportunities through the bond market and other avenue for borrowing

Any reform of the National Savings Certificate will potentially boost mobilization of long term deposits

• Tightening margins – growing competition in home loans as well as SMEs have gradually reduced margins over the years

Roll-out product development initiatives targeted towards markets beyond the capital city

o Mainly through developing the right offerings for lower ticket sizes, both for SME and Home Loans

Continue efforts at improving operational efficiency and scalability to reduce loan acquisition and management costs

Continue improvements in loan underwriting and collections policies and procedures to decrease cost of risk further

Slide 19 of 22

Ongoing challenges and mitigation avenues

• Shrinking Fee Incomes – reduction in fee rates on loan disbursements following regulatory directives

Growth in disbursement volumes is expected to restrict further deterioration in fee incomes

Focus to be on Brokerage Fees, Structured Finance, Advisory Services, Investment Banking and Fund Management

businesses for a sustainable source of Fee Income. However, these will only start contributing significantly in the medium-

long term

• Rise in Operating Expenses – while numerous process improvements have shown a glimpse of cost minimization for the year in

review, rate of OPEX growth is expected to catch up in 2019.

Unlocking tectonic shifts in organizational productivity and resource utilization will require investments as well as regulatory

support in some cases

While some scalability measures require policy level advancements in the regulatory landscape, our business model change

initiatives and various tech adoption strategies are expected to bring in significant productivity improvements over the

coming years under the existing regulatory guidelines

Slide 20 of 22

Accomplishments of 2018 and focus areas going forward

• Upgradation of customer acquisition, loan processing and management model

Business model of Consumer Division upgraded to improve scalability of operations expected to achieve business growth with

less than proportionate increase in resources

Business model of SME Division also undergoing change for added efficiency, while general process improvement efforts are

being conducted for all verticals

The aim of all the adopted changes are to enable the organization to handle significantly increased number of small ticket cases,

in line with the overall strategy of being a more retail centric organization

• Diagnostics for customization of core banking software and preparations for tech adoptions

These customizations are expected to –

o Boost productivity

o Enable a more data-driven culture of strategy formulation and decision-making

Most of these are expected to be executed in 2019, while some undertakings are estimated to take place over the next 2-3

years, in alignment with organizational and customer readiness

Slide 21 of 22

Accomplishments of 2018 and focus areas going forward

• New product developments and initiatives that have aided in building the bedrocks for new business opportunities

Affordable housing segment,

Micro business segments

Flexible savings schemes for recurring depositors deposit and other wealth management products

New avenues opened up with the alternative investments license obtained in July 2018

• Customization and development of product offerings based on customer feedback are to continue

• HR initiatives, particularly in talent recognition and development have had significantly positive impact

Performance management process has been revitalized with renewed emphasis on rewarding top talents and nurturing potential

achievers

Voluntary attritions have come down to 11% in 2018, from 15% in the previous year – expected to improve further as more talent

recognition and employee engagement initiatives come into effect

Slide 22 of 22

Thank you

Q & A

![20140408 digital newspapers collections [idlc kuala lumpur]](https://img.pdfslide.us/doc/110x75/53fea18e8d7f72835c8b4595/20140408-digital-newspapers-collections-idlc-kuala-lumpur.jpg)