Embed Size (px)

Citation preview

1

:KHQ�%DG�7KLQJV�+DSSHQ7R�<RXU�*RRG�1DPH

)HGHUDO�7UDGH�&RPPLVVLRQ

2

LISTEN TO THESE CONSUMERS . . .

Someone used my Social Security number to get credit inmy name. This has caused a lot of problems. I have beenturned down for jobs, credit, and refinancing offers. Thisis stressful and embarrassing. I want to open my ownbusiness, but it may be impossible with this unresolvedproblem hanging over my head.

From a consumer complaint to the FTC, May 18, 1999

Someone is using my name and Social Security number to open creditcard accounts. All the accounts are in collections. I had no idea thiswas happening until I applied for a mortgage. Because these �bad�accounts showed up on my credit report, I didn�t get the mortgage.

From a consumer complaint to the FTC, July 13, 1999

Help! Someone is using my Social Securitynumber to get a job.

From a consumer complaint to the FTC, September 20, 1999

My elderly parents are victims of credit fraud.We don�t know what to do. Someone applied forcredit cards in their name and charged nearly$20,000. Two of the card companies havecleared my parents�s name, but the third hasturned the account over to a collection agency.The agency doesn�t believe Mom and Dad didn�tauthorize the account. What can we do to stopthe debt collector?

From a consumer complaint to the FTC, October 7, 1999

3

Table of Contents

Introduction .................................................................................1

How Identity Theft Occurs ............................................................2

Minimize Your Risk ......................................................................3

Choosing to Share Personal Information � or Not ..........................5Credit Bureaus.........................................................................5Departments of Motor Vehicles .................................................6Direct Marketers ......................................................................6

If You�re a Victim .........................................................................7Your First Three Steps...............................................................7Your Next Steps .......................................................................8

Where There�s Help ................................................................... 11Federal Clearinghouse for Consumer Complaints .................... 11Federal Laws ......................................................................... 11State Laws ............................................................................. 12

Resolving Credit Problems .......................................................... 14Credit Reports ....................................................................... 14Credit Cards ......................................................................... 16Debt Collectors ...................................................................... 17ATM Cards, Debit Cards and Electronic Fund Transfers ............ 17

Resources .................................................................................. 19Federal Government .............................................................. 19State and Local Governments ................................................. 22Credit Bureaus....................................................................... 22

4

$GPLW�2QH

In the course of a busy day,you may write a check at thegrocery store, charge tickets

to a ball game, rent a car, mailyour tax returns, call home onyour cell phone, order newchecks or apply for a credit card.Chances are you don�t give theseeveryday transactions a secondthought. But someone else may.

The 1990�s spawned a newvariety of crooks called identitythieves. Their stock in trade areyour everyday transactions. Eachtransaction requires you to sharepersonal information: your bankand credit card account numbers;your income; your Social Secu-rity number (SSN); and yourname, address and phone num-bers. An identity thief co-optssome piece of your personalinformation and appropriates itwithout your knowledge tocommit fraud or theft. An all-too-common example is when anidentity thief uses your personalinformation to open a credit cardaccount in your name.

Can you completely preventidentity theft from occurring?Probably not, especially ifsomeone is determined tocommit the crime. But you canminimize your risk by managingyour personal informationwisely, cautiously and withheightened sensitivity.

The Congress of the UnitedStates asked the Federal Trade

Commission to provide informa-tion to consumers about identitytheft and to take complaints fromthose whose identities have beenstolen. If you�ve been a victim ofidentity theft, you can call theFTC�s Identity Theft Hotlinetoll-free at 1-877-IDTHEFT(438-4338). The FTC puts yourinformation into a secure con-sumer fraud database and may,in appropriate instances, share itwith other law enforcementagencies and private entities,including any companies aboutwhich you may complain.

Introduction

The FTC, working in con-junction with other governmentagencies, has produced thisbooklet to help you guard againstand recover from identity theft.

5

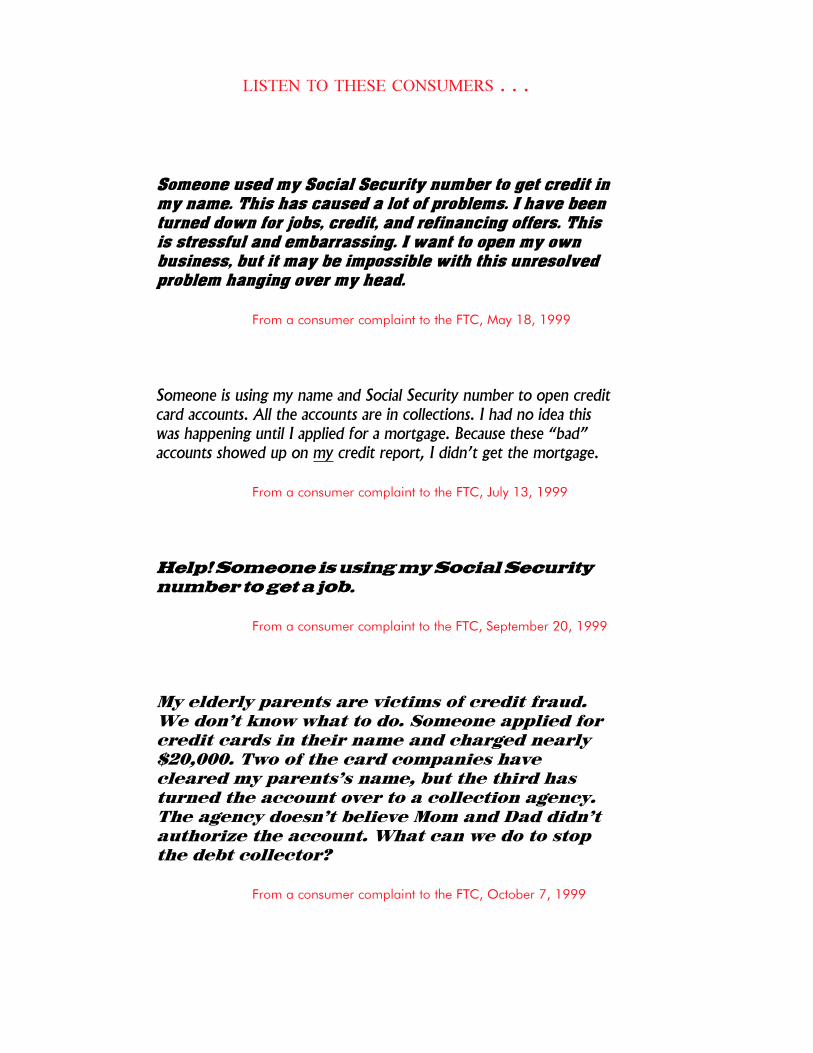

Despite your best effortsto manage the flow ofyour personal informa-

tion or to keep it to yourself,skilled identity thieves may use avariety of methods � low- and hi-tech � to gain access to your data.Here are some of the waysimposters can get your personalinformation and take over youridentity.

How identity thieves get yourpersonal information:

They steal wallets and pursescontaining your identificationand credit and bank cards.

They steal your mail, includingyour bank and credit cardstatements, pre-approvedcredit offers, telephone callingcards and tax information.

They complete a �change ofaddress form� to divert yourmail to another location.

They rummage through yourtrash, or the trash of busi-nesses, for personal data in apractice known as �dumpsterdiving.�

They fraudulently obtain yourcredit report by posing as alandlord, employer or some-one else who may have alegitimate need for � and alegal right to � the information.

They get your business or person-nel records at work.

They find personal information inyour home.

They use personal informationyou share on the Internet.

They buy your personal infor-mation from �inside� sources.For example, an identity thiefmay pay a store employeefor information about youthat appears on an applica-tion for goods, services orcredit.

How identity thieves useyour personal information:

They call your credit cardissuer and, pretending to beyou, ask to change themailing address on yourcredit card account. Theimposter then runs upcharges on your account.Because your bills are beingsent to the new address, itmay take some time beforeyou realize there�s a prob-lem.

They open a new credit cardaccount, using your name,date of birth and SSN.When they use the creditcard and don�t pay the bills,the delinquent account isreported on your creditreport.

They establish phone orwireless service in yourname.

They open a bank account inyour name and write badchecks on that account.

They file for bankruptcy underyour name to avoid payingdebts they�ve incurred underyour name, or to avoideviction.

They counterfeit checks ordebit cards, and drain yourbank account.

They buy cars by taking outauto loans in your name.

How Identity Theft Occurs

6

While you probablycan�t prevent identitytheft entirely, you can

minimize your risk. By manag-ing your personal informationwisely, cautiously and with anawareness of the issue, you canhelp guard against identity theft:

� Before you reveal any person-ally identifying information,find out how it will be usedand whether it will be sharedwith others. Ask if you have achoice about the use of yourinformation: can you chooseto have it kept confidential?

� Pay attention to your billingcycles. Follow up with credi-tors if your bills don�t arriveon time. A missing credit cardbill could mean an identitythief has taken over yourcredit card account andchanged your billing addressto cover his tracks.

� Guard your mail from theft.Deposit outgoing mail in postoffice collection boxes or atyour local post office.Promptly remove mail fromyour mailbox after it has beendelivered. If you�re planning tobe away from home and can�tpick up your mail, call the U.S.Postal Service at1-800-275-8777 to request avacation hold. The PostalService will hold your mail atyour local post office until youcan pick it up.

� Put passwords on your creditcard, bank and phone ac-counts. Avoid using easily

Minimize Your Risk

available information like yourmother�s maiden name, yourbirth date, the last four digits ofyour SSN or your phonenumber, or a series of consecu-tive numbers.

� Minimize the identificationinformation and the number ofcards you carry to what you�llactually need.

� Do not give out personalinformation on the phone,through the mail or over theInternet unless you haveinitiated the contact or knowwho you�re dealing with.Identity thieves may pose asrepresentatives of banks,Internet service providers andeven government agencies toget you to reveal your SSN,mother�s maiden name, finan-

cial account numbers and otheridentifying information. Legiti-mate organizations with whomyou do business have theinformation they need and willnot ask you for it.

� Keep items with personalinformation in a safe place. Tothwart an identity thief whomay pick through your trash orrecycling bins to capture yourpersonal information, tear orshred your charge receipts,copies of credit applications,insurance forms, physicianstatements, bank checks andstatements that you are dis-carding, expired charge cardsand credit offers you get in themail.

� Be cautious about where youleave personal information in

7

your home, especially if youhave roommates, employoutside help or are havingservice work done in yourhome.

� Find out who has access toyour personal information atwork and verify that therecords are kept in a securelocation.

� Give your SSN only whenabsolutely necessary. Ask touse other types of identifierswhen possible.

� Don�t carry your SSN card;leave it in a secure place.

� Order a copy of your creditreport from each of the threemajor credit reporting agen-cies every year. Make sure it isaccurate and includes onlythose activities you�ve autho-rized. The law allows creditbureaus to charge you up to$8.50 for a copy of your creditreport.

Your credit report containsinformation on where you workand live, the credit accounts thathave been opened in your name,how you pay your bills andwhether you�ve been sued,arrested or filed for bankruptcy.Checking your report on aregular basis can help you catchmistakes and fraud before theywreak havoc on your personalfinances. See �Credit Reports� onpage 14 for details about remov-ing fraudulent and inaccurateinformation from your creditreport.

CREDIT BUREAUS

Equifax � www.equifax.comTo order your report, call: 800-685-1111 or write:P.O. Box 740241, Atlanta, GA 30374-0241To report fraud, call: 800-525-6285 and write:P.O. Box 740241, Atlanta, GA 30374-0241

Experian � www.experian.comTo order your report, call: 888-EXPERIAN (397-3742) orwrite: P.O. Box 949, Allen TX 75013-0949To report fraud, call: 888-EXPERIAN (397-3742) and write:P.O. Box 949, Allen TX 75013-0949

Trans Union � www.tuc.comTo order your report, call: 800-916-8800 or write:P.O. Box 1000, Chester, PA 19022To report fraud, call: 800-680-7289 and write:Fraud Victim Assistance Division, P.O. Box 6790, Fullerton,CA 92834

Your employer and financialinstitution will likely need yourSSN for wage and tax report-ing purposes. Other privatebusinesses may ask you foryour SSN to do a credit check,such as when you apply for acar loan. Sometimes, however,they simply want your SSN forgeneral record keeping. Youdon�t have to give a businessyour SSN just because theyask for it. If someone asks foryour SSN, ask the followingquestions:

� Why do you need my SSN?

� How will my SSN beused?

� What law requires me togive you my SSN?

� What will happen if I don�tgive you my SSN?

Sometimes a business maynot provide you with theservice or benefit you�reseeking if you don�t provideyour SSN. Getting answers tothese questions will help youdecide whether you want toshare your SSN with thebusiness. Remember, though,that the decision is yours.

A SPECIAL WORD ABOUT SOCIAL SECURITY NUMBERS

8

237�287

237�287

237�287What happens to the

personal informationyou provide to com-

panies, marketers and govern-ment agencies? They may useyour information just to processyour order. They may use it tocreate a profile about you andthen let you know about prod-ucts, services or promotions. Orthey may share your informationwith others. More organizationsare offering consumers choicesabout how their personal infor-mation is used. For example,many let you �opt out� of havingyour information shared withothers or used for promotionalpurposes.

You can learn more about thechoices you have to protect yourpersonal information from creditbureaus, state Departments ofMotor Vehicles and directmarketers.

Credit Bureaus

Pre-Screened Credit OffersIf you receive pre-screenedcredit card offers in the mail(namely, those based upon yourcredit data), but don�t tear themup after you decide you don�twant to accept the offer, identitythieves may retrieve the offersfor their own use without yourknowledge.

Choosing to Share YourPersonal Information � or Not

9

To opt out of receiving pre-screened credit card offers, call:1-888-5-OPTOUT (1-888-567-8688). The three major creditbureaus use the same toll-freenumber to let consumers choosenot to receive pre-screenedcredit offers.

Marketing ListsOf the three major credit bu-reaus, only Experian offersconsumers the opportunity tohave their names removed fromlists that are used for marketingand promotional purposes. Tohave your name removed fromExperian�s marketing lists, call1-800-407-1088.

Departments ofMotor VehiclesTake a look at your driver�slicense. All the personal infor-mation on it � and more � is onfile with your state Departmentof Motor Vehicles (DMV). Astate DMV may distribute yourpersonal information for lawenforcement, driver safety orinsurance underwriting purposes,but you may have the right tochoose not to have the DMVdistribute your personal informa-tion for other purposes, includingfor direct marketing.

Not every DMV distributespersonal information for directmarketing or other purposes. Youmay be able to opt out if yourstate DMV distributes personalinformation for these purposes.Contact your state DMV formore information.

Direct MarketersThe Direct MarketingAssociation�s (DMA) Mail,E-mail and Telephone PreferenceServices allow consumers to optout of direct mail marketing,e-mail marketing and/ortelemarketing solicitations frommany national companies.Because your name will not beon their lists, it also means thatthese companies can�t rent orsell your name to other compa-nies.

To remove your name frommany national direct mail lists,write:

DMA Mail Preference ServiceP.O. Box 9008Farmingdale, NY 11735-9008

To remove your e-mail addressfrom many national direct e-maillists, visit www.e-mps.org

To avoid unwanted phone callsfrom many national marketers,send your name, address, andtelephone number to:

DMA Telephone Preference ServiceP.O. Box 9014Farmingdale, NY 11735-9014

For more information, visitwww.the-dma.org

10

Sometimes an identity thiefcan strike even if you�vebeen very careful about

keeping your personal informa-tion to yourself. If you suspectthat your personal informationhas been hijacked and misappro-priated to commit fraud or theft,take action immediately, andkeep a record of your conversa-tions and correspondence. Youmay want to use the form on page10. Exactly which steps youshould take to protect yourselfdepends on your circumstancesand how your identity has beenmisused. However, three basicactions are appropriate in almostevery case.

Your First Three StepsFirst, contact the fraud depart-ments of each of the threemajor credit bureaus.

Tell them that you�re anidentity theft victim. Requestthat a �fraud alert� be placed inyour file, as well as a victim�sstatement asking that creditorscall you before opening any newaccounts or changing yourexisting accounts. This can helpprevent an identity thief fromopening additional accounts inyour name.

At the same time, ordercopies of your credit reports fromthe credit bureaus. Credit bureausmust give you a free copy of yourreport if your report is inaccuratebecause of fraud, and you requestit in writing. Review your reportscarefully to make sure no addi-tional fraudulent accounts havebeen opened in your name orunauthorized changes made toyour existing accounts. Also,check the section of your report

If You�re a Victim

11

that lists �inquiries.� Where�inquiries� appear from thecompany(ies) that opened thefraudulent account(s), requestthat these �inquiries� be removedfrom your report. (See �CreditReports� on page 14 for moreinformation.) In a few months,order new copies of your reportsto verify your corrections andchanges, and to make sure nonew fraudulent activity hasoccurred.

Second, contact the credi-tors for any accounts that havebeen tampered with or openedfraudulently.

Creditors can include creditcard companies, phone compa-nies and other utilities, andbanks and other lenders. Ask tospeak with someone in thesecurity or fraud department ofeach creditor, and follow up witha letter. It�s particularly impor-tant to notify credit card compa-nies in writing because that�s theconsumer protection procedurethe law spells out for resolvingerrors on credit card billingstatements. Immediately closeaccounts that have been tamperedwith and open new ones with newPersonal Identification Numbers(PINs) and passwords. Hereagain, avoid using easily avail-able information like yourmother�s maiden name, yourbirth date, the last four digits ofyour SSN or your phone number,or a series of consecutive num-bers.

Third, file a report withyour local police or the policein the community where theidentity theft took place.

Get a copy of the policereport in case the bank, credit

card company or others needproof of the crime. Even if thepolice can�t catch the identitythief in your case, having a copyof the police report can help youwhen dealing with creditors.

Your Next StepsAlthough there�s no questionthat identity thieves can wreakhavoc on your personal finances,there are some things you can doto take control of the situation.For example:

� Stolen mail. If an identitythief has stolen your mail toget new credit cards, bank andcredit card statements, pre-screened credit offers or taxinformation, or if an identitythief has falsified change-of-address forms, that�s a crime.Report it to your local postalinspector. Contact your localpost office for the phonenumber for the nearest postalinspection service office orcheck the Postal Service website at www.usps.gov/websites/depart/inspect

� Change of address on creditcard accounts. If you dis-cover that an identity thief haschanged the billing address onan existing credit card ac-count, close the account.When you open a new ac-count, ask that a password beused before any inquiries orchanges can be made on theaccount. Avoid using easilyavailable information likeyour mother�s maiden name,your birth date, the last fourdigits of your SSN or yourphone number, or a series of

consecutive numbers. Avoidusing the same information andnumbers when you create aPIN.

� Bank accounts. If you havereason to believe that anidentity thief has tamperedwith your bank accounts,checks or ATM card, close theaccounts immediately. Whenyou open new accounts, insiston password-only access tominimize the chance that anidentity thief can violate theaccounts.

In addition, if your checkshave been stolen or misused,stop payment. Also contactthe major check verificationcompanies to request that theynotify retailers using theirdatabases not to accept thesechecks, or ask your bank tonotify the check verificationservice with which it doesbusiness.

National Check Fraud Service:1-843-571-2143SCAN: 1-800-262-7771TeleCheck: 1-800-710-9898 or927-0188CrossCheck: 1-707-586-0551Equifax Check Systems:1-800-437-5120International Check Services:1-800-526-5380

If your ATM card has beenlost, stolen or otherwisecompromised, cancel the cardas soon as you can and getanother with a new PIN.

� Investments. If you believethat an identity thief has

12

SHOULD I APPLY FOR ANEW SOCIAL SECURITY

NUMBER?

Under certain circum-stances, SSA may assignyou a new SSN � at yourrequest � if, after trying toresolve the problemsbrought on by identitytheft, you continue toexperience problems.Consider this optioncarefully. A new SSN maynot resolve your identitytheft problems, and mayactually create new prob-lems. For example, a newSSN does not necessarilyensure a new creditrecord because creditbureaus may combine thecredit records from yourold SSN with those fromyour new SSN. Even whenthe old credit informationis not associated with yournew SSN, the absence ofany credit history underyour new SSN may makeit more difficult for you toget credit. And finally,there�s no guarantee thata new SSN wouldn�t alsobe misused by an identitythief.

tampered with your securitiesinvestments or a brokerageaccount, immediately report itto your broker or accountmanager and to the Securitiesand Exchange Commission.

� Phone service. If an identitythief has established newphone service in your name; ismaking unauthorized calls thatseem to come from � and arebilled to � your cellular phone;or is using your calling cardand PIN, contact your serviceprovider immediately tocancel the account and/orcalling card. Open newaccounts and choose newPINs.

If you are having troublegetting fraudulent phonecharges removed from youraccount, contact your statePublic Utility Commission forlocal service providers or theFederal CommunicationsCommission for long-distanceservice providers and cellularproviders at www.fcc.gov/ccb/enforce/complaints.html or1-888-CALL-FCC.

� Employment. If you believesomeone is using your SSN toapply for a job or to work,that�s a crime. Report it to theSSA�s Fraud Hotline at 1-800-269-0271. Also call SSA at 1-800-772-1213 to verify theaccuracy of the earningsreported on your SSN, and torequest a copy of your SocialSecurity Statement. Follow upyour calls in writing.

� Driver�s license. If yoususpect that your name or SSNis being used by an identitythief to get a driver�s license ora non-driver�s ID card, contactyour Department of MotorVehicles. If your state usesyour SSN as your driver�slicense number, ask to substi-tute another number.

� Bankruptcy. If you believesomeone has filed for bank-ruptcy using your name, writeto the U.S. Trustee in theRegion where the bankruptcywas filed. A listing of the U.S.Trustee Program�s Regionscan be found atwww.usdoj.gov/ust, or look inthe Blue Pages of your phonebook under U.S. Government� Bankruptcy Administration.

Your letter should describe thesituation and provide proof ofyour identity. The U.S.Trustee, if appropriate, willmake a referral to criminal lawenforcement authorities if youprovide appropriate documen-tation to substantiate yourclaim. You also may want tofile a complaint with the U.S.Attorney and/or the FBI in thecity where the bankruptcy wasfiled.

� Criminal records/arrests. Inrare instances, an identity thiefmay create a criminal recordunder your name. For ex-ample, your imposter may giveyour name when being ar-

rested. If this happens to you,you may need to hire anattorney to help resolve theproblem. The procedures forclearing your name vary byjurisdiction.

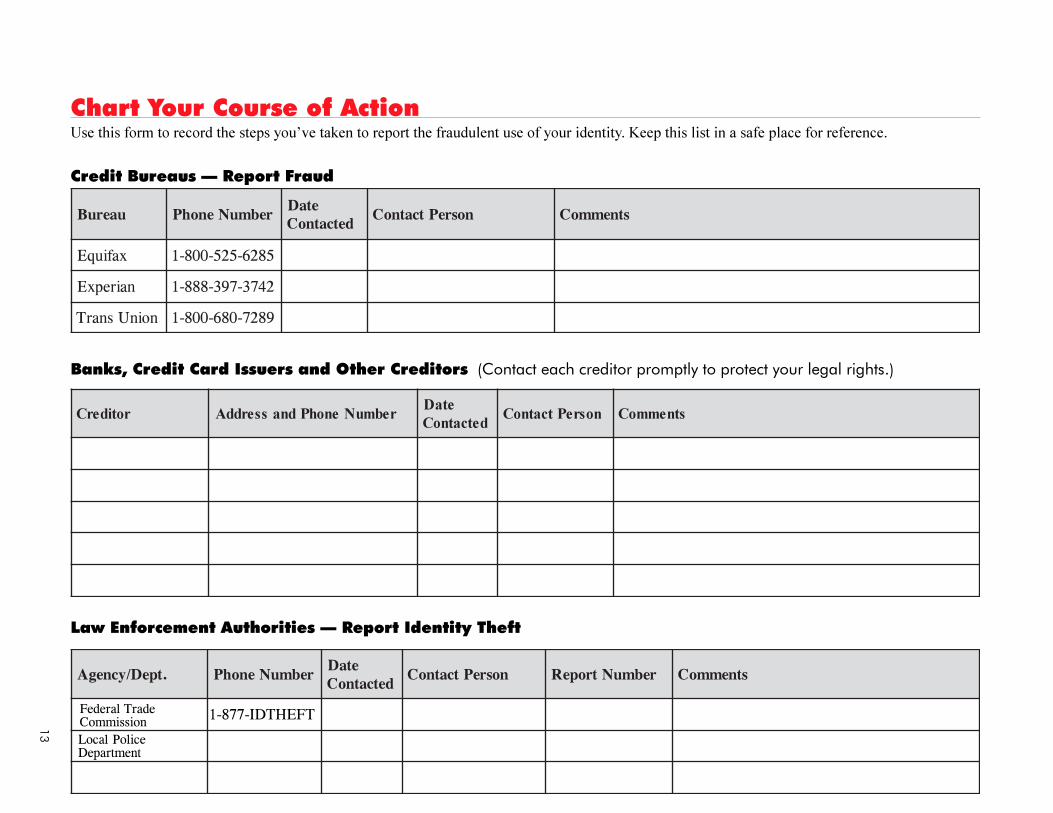

13

Chart Your Course of ActionUse this form to record the steps you�ve taken to report the fraudulent use of your identity. Keep this list in a safe place for reference.

Credit Bureaus � Report Fraud

Banks, Credit Card Issuers and Other Creditors (Contact each creditor promptly to protect your legal rights.)

Law Enforcement Authorities � Report Identity Theft

.tpeD/ycnegA rebmuNenohP etaDdetcatnoC nosrePtcatnoC rebmuNtropeR stnemmoC

uaeruB rebmuNenohP etaDdetcatnoC nosrePtcatnoC stnemmoC

xafiuqE 5826-525-008-1

nairepxE 2473-793-888-1

noinUsnarT 9827-086-008-1

rotiderC rebmuNenohPdnasserddAetaD

detcatnoCnosrePtcatnoC stnemmoC

Federal TradeCommission 1-877-IDTHEFT

Local PoliceDepartment

14

Where There�s Help...

The FTC collects com-plaints about identity theftfrom consumers who have

been victimized. Although theFTC does not have the authorityto bring criminal cases, theCommission can help victimsof identity theft byproviding informa-tion to assistthem inresolving thefinancial andother problemsthat can resultfrom this crime. The FTC alsorefers victim complaints to otherappropriate government agenciesand private organizations forfurther action.

If you�ve been a victim ofidentity theft, file a complaintwith the FTC by contacting theFTC�s Identity Theft Hotline bytelephone: toll-free 1-877-IDTHEFT (438-4338); TDD:202-326-2502; by mail: IdentityTheft Clearinghouse, FederalTrade Commission, 600 Pennsyl-vania Avenue, NW, Washington,DC 20580; or online:www.consumer.gov/idtheft

Other agencies and organiza-tions also are working to combatidentity theft. If specific institu-tions and companies are notbeing responsive to your ques-tions and complaints, you alsomay want to contact the govern-ment agencies with jurisdictionover those companies. They arelisted in the Resources section ofthis booklet on page 19.

Federal LawsThe Federal government andnumerous states have passed

Identity Theft and Assumption DeterrenceAct of 1998

The Identity Theft and Assumption Deterrence Actmakes it a federal crime when someone:

�knowingly transfers or uses, without lawfulauthority, a means of identification of anotherperson with the intent to commit, or to aid orabet, any unlawful activity that constitutes aviolation of federal law, or that constitutes afelony under any applicable state or local law.�

Note that under the Act, a name or SSN is consid-ered a �means of identification.� So is a credit cardnumber, cellular telephone electronic serial numberor any other piece of information that may be usedalone or in conjunction with other information toidentify a specific individual.

15

laws that address the problem ofidentity theft.

The Identity Theft andAssumption Deterrence Act,enacted by Congress in October1998 (and codified, in part, at 18U.S.C. §1028) is the federal lawdirected at identity theft. (Seebox on page 11.)

Violations of the Act areinvestigated by federal lawenforcement agencies, includingthe U.S. Secret Service, the FBI,the U.S. Postal InspectionService and SSA�s Office of theInspector General. Federalidentity theft cases are pros-ecuted by the U.S. Departmentof Justice.

In most instances, a convic-tion for identity theft carries amaximum penalty of 15 yearsimprisonment, a fine and forfei-ture of any personal propertyused or intended to be used tocommit the crime. The Act alsodirects the U.S. SentencingCommission to review andamend the federal sentencingguidelines to provide appropriatepenalties for those personsconvicted of identity theft.

Schemes to commit identitytheft or fraud also may involveviolations of other statutes, suchas credit card fraud; computerfraud; mail fraud; wire fraud;financial institution fraud; orSocial Security fraud. Each ofthese federal offenses is a felonyand carries substantial penalties� in some cases, as high as 30years in prison, fines and crimi-nal forfeiture.

State LawsMany states have passed lawsrelated to identity theft; othersmay be considering such legisla-tion. Where specific identity theftlaws do not exist, the practicesmay be prohibited under otherlaws. Contact your State Attor-ney General�s office or localconsumer protection agency tofind out whether your state haslaws related to identity theft, orvisit www.consumer.gov/idtheft

State laws that had beenenacted at the time of thisbooklet�s publication are listedbelow.

Alaska2000 Alaska Sess. Laws 65

ArizonaAriz. Rev. Stat. § 13-2008

ArkansasArk. Code Ann. § 5-37-227

CaliforniaCal. Penal Code § 530.5

Colorado2000 Colo. Legis. Serv. ch. 159(May 19, 2000)

Connecticut1999 Conn. Acts 99

Delaware72 Del. Laws 297 (2000)

FloridaFla. Stat. Ann. § 817.568

GeorgiaGa. Code Ann. §§ 16-9-121

IdahoIdaho Code § 18-3126

Illinois720 ILCS 5/16G

IndianaInd. Code § 35-43-5-4 (2000)

IowaIowa Code § 715A.8

KansasKan. Stat. Ann. § 21-4108

KentuckyRev. Stat. Ann. § 160, ch. 514

LouisianaLa. Rev. Stat. Ann. § 67.16

MaineMe. Rev. Stat. Ann. tit. 17-A,§ 354-2A

MarylandMd. Ann. Code art. 27 § 231

MassachusettsMass. Gen. Laws ch. 266 § 37E

MinnesotaMinn. Stat. Ann. § 609.527

MississippiMiss. Code Ann. § 97-19-85

MissouriMo. Rev. Stat. § 570.223

NevadaNev. Rev. Stat. § 205.465

New HampshireN.H. Rev. Stat. Ann. § 638:26

New JerseyN.J. Stat. Ann. § 2C:21-17

North CarolinaN.C. Gen. Stat. § 14-113.20

North DakotaN.D.C.C. § 12.1-23-11

OhioOhio Rev. Code Ann. 2913.49

OklahomaOkla. Stat. tit. 21, § 1533.1

OregonOr. Rev. Stat. § 165.800

PennsylvaniaPa. Cons. Stat. Ann. § 4120

Rhode IslandR.I. Gen. Laws § 11-49.1-1

16

South CarolinaS.C. Code Ann. § 16-13-500, 501

South DakotaS.D. Codified Laws§ 22-30A-3.1.

TennesseeTenn. Code Ann. § 39-14-150

TexasTex. Penal Code § 32.51

UtahUtah Code Ann.§ 76-6-1101-1104

VirginiaVa. Code Ann. § 18.2-186.3

WashingtonWash. Rev. Code § 9.35.020

West VirginiaW. Va. Code § 61-3-54

WisconsinWis. Stat. § 943.201

WyomingWyo. Stat. Ann. § 6-3-901

17

Resolving credit problemsresulting from identitytheft can be time-con-

suming and frustrating. The goodnews is that there are federallaws that establish proceduresfor correcting credit report errorsand billing errors, and forstopping debt collectors fromcontacting you about debts youdon�t owe.

Here is a brief summary ofyour rights, and what to do toclear up credit problems thatresult from identity theft.

Credit ReportsThe Fair Credit Reporting Act(FCRA) establishes proceduresfor correcting mistakes on yourcredit record and requires thatyour record be made availableonly for certain legitimatebusiness needs.

Under the FCRA, both thecredit bureau and the organiza-tion that provided the informa-tion to the credit bureau (the�information provider�), such asa bank or credit card company,are responsible for correctinginaccurate or incomplete infor-mation in your report. To protectyour rights under the law, con-tact both the credit bureau andthe information provider.

First, call the credit bureauand follow up in writing. Tellthem what information youbelieve is inaccurate. Includecopies (NOT originals) ofdocuments that support yourposition. In addition to providingyour complete name and ad-dress, your letter should clearlyidentify each item in your reportthat you dispute, give the factsand explain why you dispute the

Resolving Credit Problems

18

When the investigation iscomplete, the credit bureau mustgive you the written results and afree copy of your report if thedispute results in a change. If anitem is changed or removed, thecredit bureau cannot put the

information, and request deletionor correction. You may want toenclose a copy of your reportwith circles around the items inquestion. Your letter may looksomething like the sample atright. Send your letter by certifiedmail, and request a return receiptso you can document what thecredit bureau received and when.Keep copies of your dispute letterand enclosures.

Credit bureaus must investi-gate the items in question �usually within 30 days � unlessthey consider your disputefrivolous. They also must forwardall relevant data you provideabout the dispute to the informa-tion provider. After the informa-tion provider receives notice of adispute from the credit bureau, itmust investigate, review allrelevant information provided bythe credit bureau and report theresults to the credit bureau. If theinformation provider finds thedisputed information to beinaccurate, it must notify anynationwide credit bureau that itreports to so that the creditbureaus can correct this informa-tion in your file. Note that:

� Disputed information thatcannot be verified must bedeleted from your file.

� If your report contains errone-ous information, the creditbureau must correct it.

� If an item is incomplete, thecredit bureau must complete it.For example, if your file showsthat you have been late makingpayments, but fails to showthat you are no longer delin-

quent, the credit bureau mustshow that you�re current.

� If your file shows an accountthat belongs to someone else,the credit bureau mustdelete it.

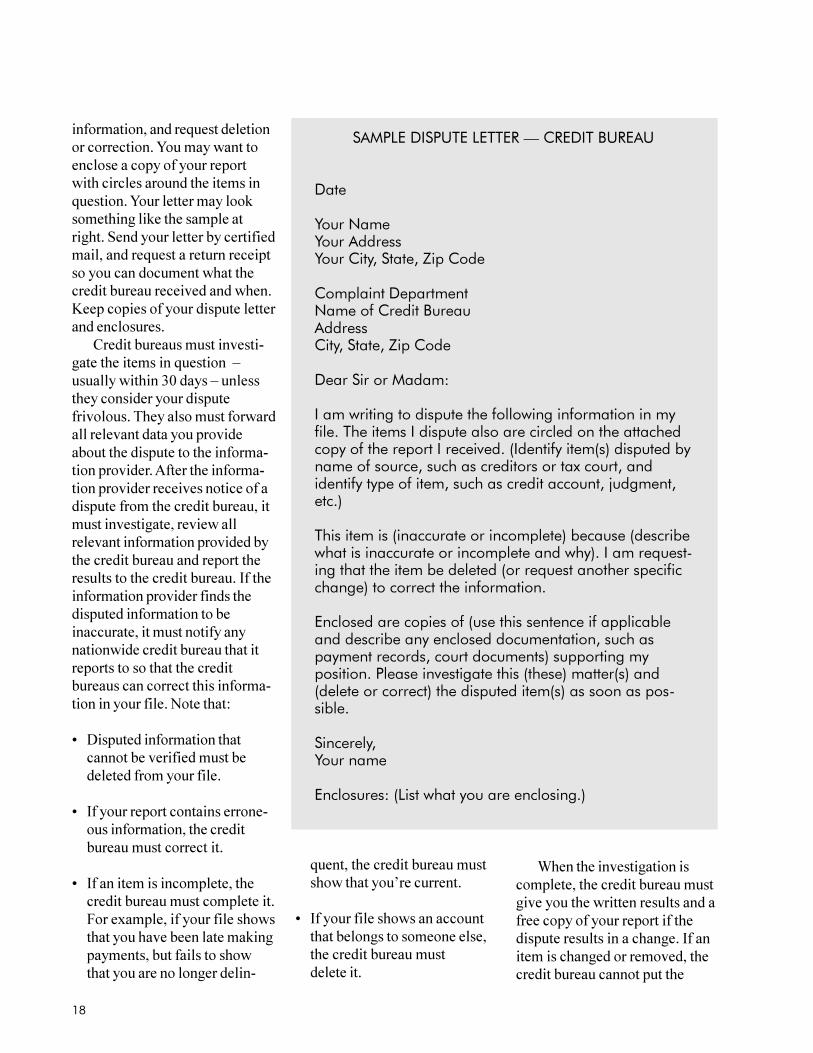

SAMPLE DISPUTE LETTER � CREDIT BUREAU

Date

Your NameYour AddressYour City, State, Zip Code

Complaint DepartmentName of Credit BureauAddressCity, State, Zip Code

Dear Sir or Madam:

I am writing to dispute the following information in myfile. The items I dispute also are circled on the attachedcopy of the report I received. (Identify item(s) disputed byname of source, such as creditors or tax court, andidentify type of item, such as credit account, judgment,etc.)

This item is (inaccurate or incomplete) because (describewhat is inaccurate or incomplete and why). I am request-ing that the item be deleted (or request another specificchange) to correct the information.

Enclosed are copies of (use this sentence if applicableand describe any enclosed documentation, such aspayment records, court documents) supporting myposition. Please investigate this (these) matter(s) and(delete or correct) the disputed item(s) as soon as pos-sible.

Sincerely,Your name

Enclosures: (List what you are enclosing.)

19

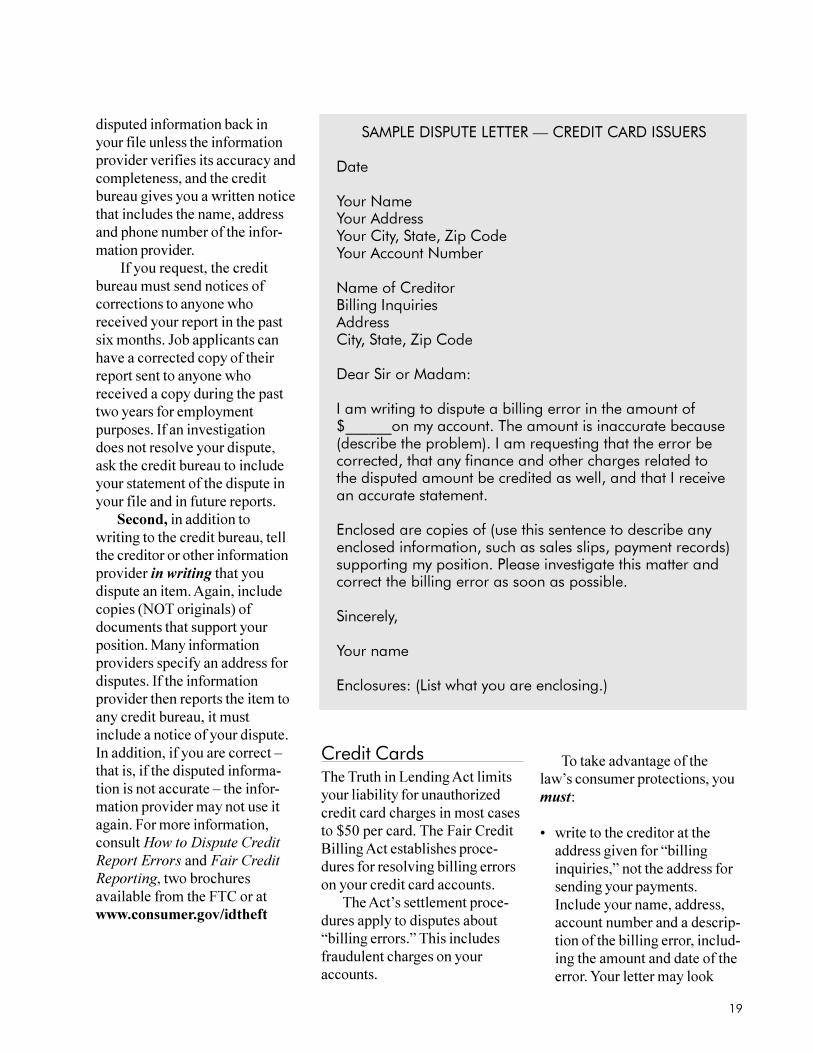

To take advantage of thelaw�s consumer protections, youmust:

� write to the creditor at theaddress given for �billinginquiries,� not the address forsending your payments.Include your name, address,account number and a descrip-tion of the billing error, includ-ing the amount and date of theerror. Your letter may look

SAMPLE DISPUTE LETTER � CREDIT CARD ISSUERS

Date

Your NameYour AddressYour City, State, Zip CodeYour Account Number

Name of CreditorBilling InquiriesAddressCity, State, Zip Code

Dear Sir or Madam:

I am writing to dispute a billing error in the amount of$______on my account. The amount is inaccurate because(describe the problem). I am requesting that the error becorrected, that any finance and other charges related tothe disputed amount be credited as well, and that I receivean accurate statement.

Enclosed are copies of (use this sentence to describe anyenclosed information, such as sales slips, payment records)supporting my position. Please investigate this matter andcorrect the billing error as soon as possible.

Sincerely,

Your name

Enclosures: (List what you are enclosing.)

disputed information back inyour file unless the informationprovider verifies its accuracy andcompleteness, and the creditbureau gives you a written noticethat includes the name, addressand phone number of the infor-mation provider.

If you request, the creditbureau must send notices ofcorrections to anyone whoreceived your report in the pastsix months. Job applicants canhave a corrected copy of theirreport sent to anyone whoreceived a copy during the pasttwo years for employmentpurposes. If an investigationdoes not resolve your dispute,ask the credit bureau to includeyour statement of the dispute inyour file and in future reports.

Second, in addition towriting to the credit bureau, tellthe creditor or other informationprovider in writing that youdispute an item. Again, includecopies (NOT originals) ofdocuments that support yourposition. Many informationproviders specify an address fordisputes. If the informationprovider then reports the item toany credit bureau, it mustinclude a notice of your dispute.In addition, if you are correct �that is, if the disputed informa-tion is not accurate � the infor-mation provider may not use itagain. For more information,consult How to Dispute CreditReport Errors and Fair CreditReporting, two brochuresavailable from the FTC or atwww.consumer.gov/idtheft

Credit CardsThe Truth in Lending Act limitsyour liability for unauthorizedcredit card charges in most casesto $50 per card. The Fair CreditBilling Act establishes proce-dures for resolving billing errorson your credit card accounts.

The Act�s settlement proce-dures apply to disputes about�billing errors.� This includesfraudulent charges on youraccounts.

20

If you�re a victim of identitytheft, including a copy (NOToriginal) of the police report youfiled may be particularly useful.

For more information,consult Fair Debt Collection, abrochure available from the FTCor at www.consumer.gov/idtheft

ATM Cards, Debit Cardsand Electronic FundTransfersThe Electronic Fund TransferAct provides consumer protec-tions for transactions involvingan ATM or debit card or otherelectronic way to debit or creditan account. It also limits yourliability for unauthorized elec-tronic fund transfers.

It�s important to report lost orstolen ATM and debit cardsimmediately because the amountyou can be held responsible fordepends on how quickly youreport the loss.

� If you report your ATM cardlost or stolen within twobusiness days of discoveringthe loss or theft, your lossesare limited to $50.

something like the sample onpage 16.

� send your letter so that itreaches the creditor within 60days after the first bill contain-ing the error was mailed toyou. If the address on youraccount was changed by anidentity thief and you neverreceived the bill, your disputeletter still must reach thecreditor within 60 days ofwhen the creditor would havemailed the bill. This is why it�sso important to keep track ofyour billing statements andimmediately follow up whenyour bills don�t arrive on time.

Send your letter by certifiedmail, and request a return re-ceipt. This will be your proof ofthe date the creditor received theletter. Include copies (NOToriginals) of sales slips or otherdocuments that support yourposition. Keep a copy of yourdispute letter.

The creditor must acknowl-edge your complaint in writingwithin 30 days after receiving it,unless the problem has beenresolved. The creditor mustresolve the dispute within twobilling cycles (but not more than90 days) after receiving yourletter.

For more information, seeFair Credit Billing and AvoidingCredit and Charge Card Fraud,two brochures available from theFTC or at www.consumer.gov/idtheft

Debt CollectorsThe Fair Debt Collection Prac-tices Act prohibits debt collectors

from using unfair or deceptivepractices to collect overdue billsthat a creditor has forwarded forcollection.

You can stop a debt collectorfrom contacting you by writing aletter to the collection agencytelling them to stop. Once the debtcollector receives your letter, thecompany may not contact youagain � with two exceptions: theycan tell you there will be nofurther contact and they can tellyou that the debt collector or thecreditor intends to take somespecific action.

A collector also may notcontact you if, within 30 daysafter you receive the writtennotice, you send the collectionagency a letter stating you do notowe the money. Although such aletter should stop the debtcollector�s calls, it will not neces-sarily get rid of the debt itself,which may still turn up on yourcredit report. In addition, acollector can renew collectionactivities if you are sent proof ofthe debt. So, along with yourletter stating you don�t owe themoney, include copies of docu-ments that support your position.

A SPECIAL WORD ABOUT LOST OR STOLEN CHECKS

While no federal law limits your losses if someone stealsyour checks and forges your signature, state laws protectyou. Most states hold the bank responsible for losses froma forged check. At the same time, however, most statesrequire you to take reasonable care of your account. Forexample, you may be held responsible for the forgery ifyou fail to notify the bank in a timely manner that a checkwas lost or stolen. Contact your state banking or con-sumer protection agency for more information.

21

� If you report your ATM cardlost or stolen after the twobusiness days, but within 60days after a statement showingan unauthorized electronic fundtransfer, you can be liable forup to $500 of what a thiefwithdraws.

� If you wait more than 60 days,you could lose all the moneythat was taken from youraccount after the end of the 60days and before you report yourcard missing.

The best way to protectyourself in the event of an error orfraudulent transaction is to call thefinancial institution and follow upin writing � by certified letter,return receipt requested � so youcan prove when the institutionreceived your letter. Keep a copyof the letter you send for yourrecords.

After notification about anerror on your statement, theinstitution generally has 10business days to investigate. Thefinancial institution must tell youthe results of its investigationwithin three business days aftercompleting it and must correct anerror within one business dayafter determining that the errorhas occurred. If the institutionneeds more time, it may take upto 45 days to complete the investi-gation � but only if the money in

dispute is returned to youraccount and you are notifiedpromptly of the credit. At the endof the investigation, if no errorhas been found, the institutionmay take the money back if itsends you a written explanation.

Note: VISA and MasterCardvoluntarily have agreed to limitconsumers� liability for unautho-rized use of their debit cards inmost instances to $50 per card,no matter how much time haselapsed since the discovery of theloss or theft of the card.

For more information, consultElectronic Banking and Creditand ATM Cards: What to Do IfThey�re Lost or Stolen, twobrochures available from theFTC or at www.consumer.gov/idtheft

22

)257+(

&21680(5

Federal GovernmentFederal Trade Commission (FTC) � www.ftc.govThe FTC is the federal clearinghouse for complaints by victims of identity theft. Although the FTC doesnot have the authority to bring criminal cases, the Commission helps victims of identity theft by provid-ing them with information to help resolve the financial and other problems that can result from identitytheft. The FTC also may refer victim complaints to other appropriate government agencies and privateorganizations for action.

If you�ve been a victim of identity theft, file a complaint with the FTC by contacting the FTC�sIdentity Theft Hotline by telephone: toll-free 1-877-IDTHEFT (438-4338); TDD: 202-326-2502; bymail: Identity Theft Clearinghouse, Federal Trade Commission, 600 Pennsylvania Avenue, NW, Wash-ington, DC 20580; or online: www.consumer.gov/idtheft

FTC publications:� Avoiding Credit and Charge Card Fraud� Credit and ATM Cards: What to Do If They�re Lost or Stolen� Credit Card Loss Protection Offers: They�re The Real Steal� Electronic Banking� Fair Credit Billing� Fair Credit Reporting� Fair Debt Collection� Getting Purse-onal: What To Do If Your Wallet or Purse Is Stolen� How to Dispute Credit Report Errors� Identity Crisis... What to Do If Your Identity Is Stolen� Identity Thieves Can Ruin Your Good Name: Tips for Avoiding Identity Theft

Resources

23

Banking AgenciesIf you�re having trouble getting your financial institution to help you resolve your banking-relatedidentity theft problems � including problems with bank-issued credit cards � contact the agencywith the appropriate jurisdiction. If you�re not sure which agency has jurisdiction over yourinstitution, call your bank or visit www.ffiec.gov/nic/default.htm

Federal Deposit Insurance Corporation (FDIC) � www.fdic.govThe FDIC supervises state-chartered banks that are not members of the Federal Reserve Systemand insures deposits at banks and savings and loans.

Call the FDIC Consumer Call Center at 1-800-934-3342; or write: Federal Deposit InsuranceCorporation, Division of Compliance and Consumer Affairs, 550 17th Street, NW, Washington,DC 20429.

FDIC publications:� Classic Cons... And How to Counter Them � www.fdic.gov/consumers/consumer/news/

cnsprg98/cons.html� Pretext Calling and Identity Theft � www.fdic.gov/regulations/resources/fraud/Pretext.html� Your Wallet: A Loser�s Manual � www.fdic.gov/consumers/consumer/news/cnfall97/

wallet.html� A Crook Has Drained Your Account. Who Pays? � www.fdic.gov/consumers/consumer/news/

cnsprg98/crook.html

Federal Reserve System (Fed) � www.federalreserve.govThe Fed supervises state-chartered banks that are members of the Federal Reserve System.

Call: 202-452-3693; or write: Division of Consumer and Community Affairs, Mail Stop 801,Federal Reserve Board, Washington, DC 20551; or contact the Federal Reserve Bank in your area.The 12 Reserve Banks are located in Boston, New York City, Philadelphia, Cleveland, Richmond,Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas and San Francisco.

National Credit Union Administration (NCUA) � www.ncua.govThe NCUA charters and supervises federal credit unions and insures deposits at federal creditunions and many state credit unions.

Call: 703-518-6360; or write: Compliance Officer, National Credit Union Administration,1775 Duke Street, Alexandria, VA 22314.

Office of the Comptroller of the Currency (OCC) � www.occ.treas.govThe OCC charters and supervises national banks. If the word �national� appears in the name of abank, or the initials �N.A.� follow its name, the OCC oversees its operations.

Call: 1-800-613-6743 (business days 9:00 a.m. to 4:00 p.m. CST); fax: 713-336-4301; or write:Customer Assistance Group, 1301 McKinney Street, Suite 3710, Houston, TX 77010.

OCC publications:� Check Fraud: A Guide to Avoiding Losses � www.occ.treas.gov/chckfrd/idassume.htm

Office of Thrift Supervision (OTS) � www.ots.treas.govThe OTS is the primary regulator of all federal and many state-chartered thrift institutions, whichinclude savings banks and savings and loan institutions.

Call: 202-906-6000; or write: Office of Thrift Supervision, 1700 G Street, NW, Washington,DC 20552.

24

Department of Justice (DOJ) � www.usdoj.govThe DOJ and its U.S. Attorneys prosecute federal identity theft cases. Information on identity theft isavailable at www.usdoj.gov/criminal/fraud/idtheft.html

Federal Bureau of Investigation (FBI) � www.fbi.govThe FBI is one of the federal criminal law enforcement agencies that investigates cases of identity theft.Local field offices are listed in the Blue Pages of your telephone directory.

FBI publications:� Protecting Yourself Against Identity Fraud � www.fbi.gov/contact/fo/norfolk/ident.htm

Federal Communications Commission (FCC) � www.fcc.govThe FCC regulates interstate and international communications by radio, television, wire, satellite andcable. The FCC�s Consumer Information Bureau is the consumer�s one-stop source for information,forms, applications and current issues before the FCC. Call: 1-888-CALL-FCC; TTY: 1-888-TELL-FCC;or write: Federal Communications Commission, Consumer Information Bureau, 445 12th Street, SW,Room 5A863, Washington, DC 20554. You can file complaints via the online complaint form atwww.fcc.gov, or e-mail questions to [email protected].

Internal Revenue Service (IRS) � www.treas.gov/irs/ciThe IRS is responsible for administering and enforcing the internal revenue laws. If you believe someonehas assumed your identity to file federal Income Tax Returns, or to commit other tax fraud, call toll-free:1-800-829-0433. For assistance to victims of identity theft schemes who are having trouble filing theircorrect returns, call the IRS Taxpayer Advocates Office, toll-free: 1-877-777-4778.

U.S. Secret Service (USSS) � www.treas.gov/usssThe U.S. Secret Service is one of the federal law enforcement agencies that investigates financial crimes,which may include identity theft. Although the Secret Service generally investigates cases where the dollarloss is substantial, your information may provide evidence of a larger pattern of fraud requiring theirinvolvement. Local field offices are listed in the Blue Pages of your telephone directory.� Financial Crimes Division �

www.treas.gov/usss/financial_crimes.htm� Frequently Asked Questions: Protecting Yourself

www.treas.gov/usss/faq.htm

Social Security Administration (SSA) � www.ssa.govSSA may assign you a new SSN � at your request � if you continue to experience problems even aftertrying to resolve the problems resulting from identity theft. SSA field office employees work closely withvictims of identity theft and third parties to collect the evidence needed to assign a new SSN in these cases.

SSA Office of the Inspector General (SSA/OIG) � The SSA/OIG is one of the federal law enforcementagencies that investigates cases of identity theft.

Direct allegations that an SSN has been stolen or misused to the SSA Fraud Hotline. Call: 1-800-269-0271; fax: 410-597-0118; write: SSA Fraud Hotline, P.O. Box 17768, Baltimore, MD 21235; or e-mail:[email protected]

SSA publications:� SSA Fraud Hotline for Reporting Fraud � www.ssa.gov/oig/guidelin.htm� Social Security � When Someone Misuses Your Number (SSA Pub. No. 05-10064)

www.ssa.gov/pubs/10064.html

25

� Social Security � Your Number and Card (SSA Pub. No. 05-10002)www.ssa.gov/pubs/10002.html

U.S. Postal Inspection Service (USPIS) � www.usps.gov/websites/depart/inspectThe USPIS is one of the federal law enforcement agencies that investigates cases of identity theft.USPIS is the law enforcement arm of the U.S. Postal Service. USPIS has primary jurisdiction in allmatters infringing on the integrity of the U.S. mail. You can locate the USPIS district office nearest youby calling your local post office or checking the list at the web site above.

U.S. Securities and Exchange Commission (SEC) � www.sec.govThe SEC�s Office of Investor Education and Assistance serves investors who complain to the SEC aboutinvestment fraud or the mishandling of their investments by securities professionals. If you�ve experi-enced identity theft in connection with a securities transaction, write: SEC, 450 Fifth Street, NW,Washington, DC, 20549-0213. You also may call 202-942-7040 or send an e-mail to [email protected].

U. S. Trustee (UST) � www.usdoj.gov/ustIf you believe someone has filed for bankruptcy using your name, write to the U.S. Trustee in the regionwhere the bankruptcy was filed. A list of the U.S. Trustee�s Regional Offices is available on the USTweb site, or check the Blue Pages of your phone book under U.S. Government � Bankruptcy Adminis-tration. Your letter should describe the situation and provide proof of your identity. The U.S. Trustee, ifappropriate, will make a criminal referral to criminal law enforcement authorities if you provide appro-priate documentation to substantiate your claim. You also may want to file a complaint with the U.S.Attorney and/or the FBI in the city where the bankruptcy was filed.

The U.S. Trustee does not provide legal representation, legal advice or referrals to lawyers. Thatmeans you may need to hire an attorney to help convince the bankruptcy court that the filing is fraudu-lent. The U.S. Trustee does not provide consumers with copies of court documents. Those documents areavailable from the bankruptcy clerk�s office for a fee.

State and Local GovernmentsMany states and local governments have passed laws related to identity theft; others may be consideringsuch legislation. Where specific identity theft laws do not exist, the practices may be prohibited underother laws. Contact your State Attorney General�s office (for a list of state offices, visit www.naag.org)or local consumer protection agency to find out whether your state has laws related to identity theft, orvisit www.consumer.gov/idtheft/

Credit BureausEquifax � www.equifax.comTo order your report, call: 1-800-685-1111 or write: P.O. Box 740241, Atlanta, GA 30374-0241To report fraud, call: 1-800-525-6285 and write: P.O. Box 740241, Atlanta, GA 30374-0241

Experian � www.experian.comTo order your report, call: 1-888-EXPERIAN (397-3742) or write: P.O. Box 949, Allen TX 75013-0949To report fraud, call: 1-888-EXPERIAN (397-3742) and write: P.O. Box 949, Allen TX 75013-0949

Trans Union � www.tuc.comTo order your report, call: 800-916-8800 or write: P.O. Box 1000, Chester, PA 19022. To report fraud,call: 1-800-680-7289 and write: Fraud Victim Assistance Division, P.O. Box 6790, Fullerton, CA 92834

26

When you contact us with complaints or requests forinformation, you can contact us by telephone, toll-free at 1-877-ID-THEFT (438-4338); by postal mail: Federal Trade Commission,Identity Theft Clearinghouse, 600 Pennsylvania Avenue, NW,Washington, DC 20580; or electronically via our online complaintform, located at www.consumer.gov Before you do, there are afew things you should know.

The material you submit may be seen by various people. Weenter the information you send into our electronic database. Thisinformation is shared with our attorneys and investigators. It mayalso be shared with employees of various other federal, state, orlocal authorities who may use this data for regulatory or law en-forcement purposes. We may also share some information withcertain private entities, such as credit bureaus and any companiesyou may have complained about, where we believe that doing somight assist in resolving identity theft-related problems. You maybe contacted by the FTC or any of the agencies or private entities towhom your complaint has been referred. In other limited circum-stances, including requests from Congress, we may be required bylaw to disclose information you submit.

You have the option to submit your information anonymously.However, if you do not provide your name and contact information,law enforcement and other entities will not be able to contact you toobtain additional information to assist in identity theft investigationsand prosecutions.

Privacy Policy

27

www.consumer.gov/idtheft

Toll-free 1.877.IDTHEFT

![ID Theft Phishing Research[1]](https://img.pdfslide.us/doc/110x75/577d234b1a28ab4e1e9971ee/id-theft-phishing-research1.jpg)