Embed Size (px)

Citation preview

I d i Pl t ti P l dIndonesia Plantation Pulp and Paper Sector – Current SituationPaper Sector Current Situation

and Future Trends

SIXTEENTH ANNUALAsian Conference

2 June 2015

George KuruAta Marie Group LtdAta Marie Group Ltd

Republic of Indonesiap

Country OverviewCountry Overview

i hi l i i h d f• It is an archipelago comprising thousands of islands

• Indonesia has a land area of 181,115,690 ha –the world’s 15th largestg

• Indonesia is the world's fourth‐most‐populous country with an estimated population of overcountry with an estimated population of over 252 million people R bli ith d ti ll l t d• Republic with a democratically elected legislature and president

Cultural PerspectiveCultural Perspective

• Multi‐cultural, diverse, complex.• Approximately 300 distinct native ethnicApproximately 300 distinct native ethnic groups and 742 different languages and dialectsdialects.

• Worlds largest population of Muslim practitioners but also has significant populations of Christians, Buddhists, andpopulations of Christians, Buddhists, and Hindus.

EconomyEconomy

$• The Indonesian economy nominal GDP of US$928.274 billion in 2012, the world's 16th largest economy.

• Estimated nominal per capita GDP in 2012 was US$3,797.

• GDP growth averaged 6.2% between 2010‐2013.• The country has extensive natural resources including• The country has extensive natural resources, including crude oil, natural gas, tin, copper, and gold. Significant agricultural and forestry sectorsagricultural and forestry sectors.

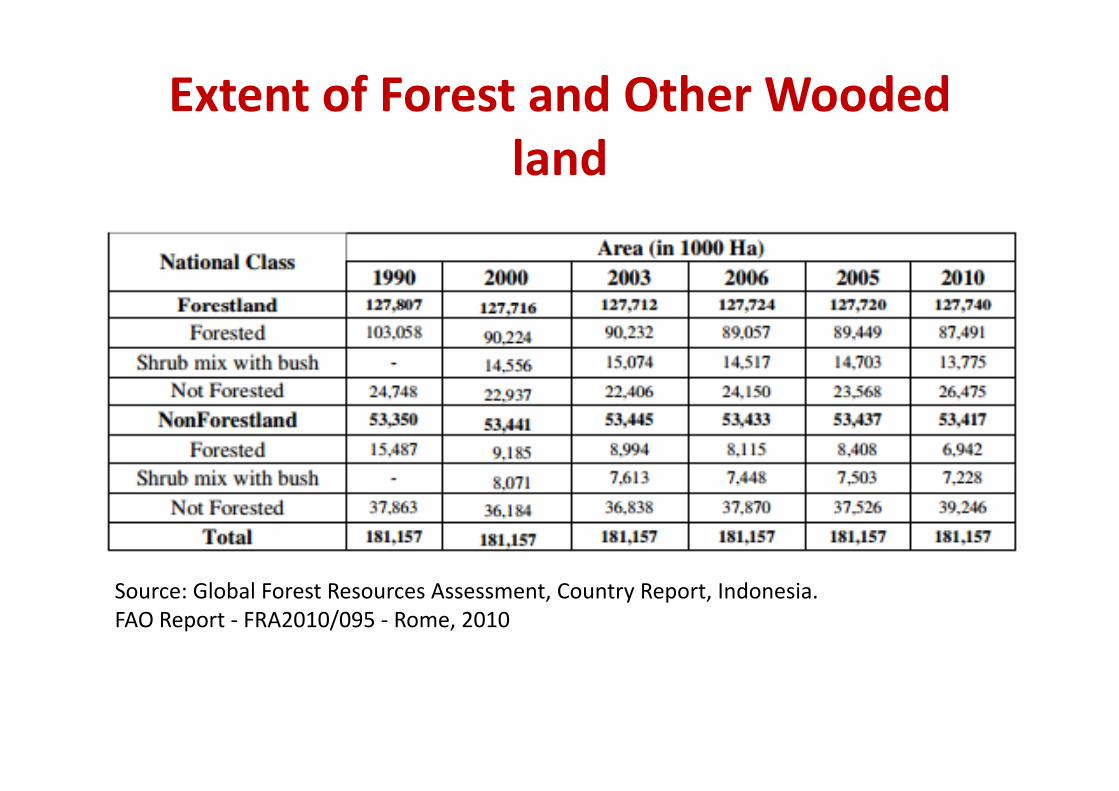

Extent of Forest and Other Wooded land

Source: Global Forest Resources Assessment, Country Report, Indonesia. FAO Report ‐ FRA2010/095 ‐ Rome, 2010

Forest Designation and ManagementForest Designation and Management

Source: Global Forest Resources Assessment, Country Report, Indonesia. FAO Report ‐ FRA2010/095 ‐ Rome, 2010

Indonesia – Pulpwood ConcessionsIndonesia – Pulpwood Concessions

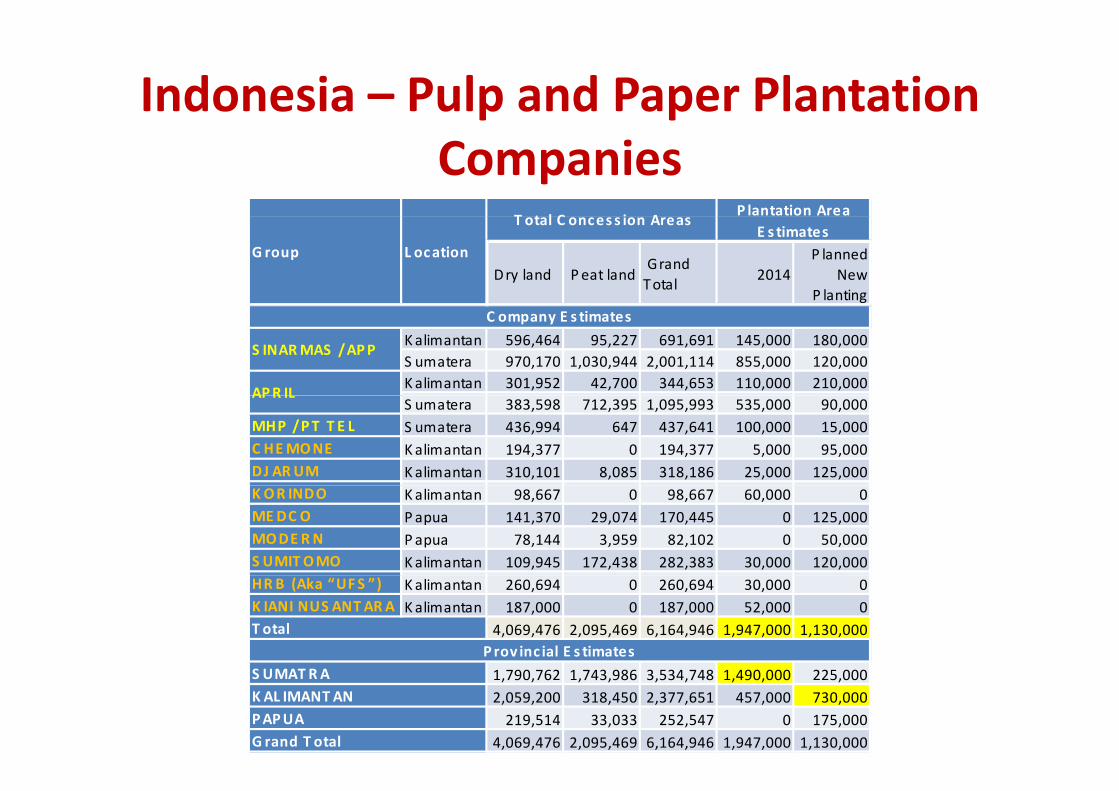

Indonesia – Pulp and Paper Plantation Companies

T t l C i A P lantation Area

Dry land Peat land Grand Total 2014

P lanned New

P lanting

G roup L ocation

T otal C onces s ion Areas E s timates

Kalimantan 596,464 95,227 691,691 145,000 180,000S umatera 970,170 1,030,944 2,001,114 855,000 120,000Kalimantan 301,952 42,700 344,653 110,000 210,000APR IL

C ompany E s timates

S INARMAS / APP

S umatera 383,598 712,395 1,095,993 535,000 90,000MHP / PT T E L S umatera 436,994 647 437,641 100,000 15,000C HEMONE Kalimantan 194,377 0 194,377 5,000 95,000DJ ARUM Kalimantan 310,101 8,085 318,186 25,000 125,000

APR IL

K OR INDO Kalimantan 98,667 0 98,667 60,000 0MEDC O Papua 141,370 29,074 170,445 0 125,000MODE RN Papua 78,144 3,959 82,102 0 50,000S UMITOMO Kalimantan 109,945 172,438 282,383 30,000 120,000HRB (Aka “UFS ”) Kalimantan 260,694 0 260,694 30,000 0K IANI NUS ANTARA Kalimantan 187,000 0 187,000 52,000 0

4,069,476 2,095,469 6,164,946 1,947,000 1,130,000T otal Prov inc ial E s timates1,790,762 1,743,986 3,534,748 1,490,000 225,0002,059,200 318,450 2,377,651 457,000 730,000219,514 33,033 252,547 0 175,000

4,069,476 2,095,469 6,164,946 1,947,000 1,130,000G rand T otal

S UMAT RAK AL IMANTANPAPUA

43% of Plantations in Indonesia Located on Peat Lands

• Peat lands are an unique component of pulp plantations in Indonesiap

• Environmentally quite controversialS i bili f l d l i• Sustainability of peat land plantation are questionable

• Peat land plantations are essential to the pulp industry at the moment but will have lessindustry at the moment, but will have less importance in the future as most new l t ti ill b d l dplantations will be on dry lands.

Heavy Reliance on Barge TransportHeavy Reliance on Barge Transport

Indonesia – Pulp and Chip MillsIndonesia – Pulp and Chip Mills

Indonesia – Pulp ProductionIndonesia – Pulp Production

Mill GroupCapacity

Estimated Production

2013

Potential pulp log consumption (capacity)

Tonnes of pulp/year m3/yearCurrent Capacity

PT Indah Kiat Pulp and PaperAPP

2,300,000 2,200,000 10,350,000

PT Lontar Papyrus Pulp and Paper 800,000 750,000 3,600,000

Riau Andalan Pulp and Paper APRIL 2,800,000 2,200,000 12,600,000 APRILPT Toba Pulp Lestari 200,000 200,000 900,000

PT Tanjung Enim Lestari TEL / Marubeni 500,000 350,000 2,250,000

PT Kiani Kertas Nusantara Group 500,000 ‐ 2,250,000

PT Kertas Kraft Aceh 135,000 ‐ 607,500

Total 7,235,000 5,700,000 32,557,500 Future New Capacity

PT OKI Pulp & Paper Mills APP 2,000,000 ‐ 9,000,000

Misc 2‐4,000,000 ‐ 9‐18,000,000

Total 4‐6,000,000 ‐ 18‐27,000,000 Sources:1. Annual Review of Woodchip Statistics 2014. RISI. In preparation.2. Personal communications

Annual Pulp Wood ConsumptionAnnual Pulp Wood Consumption 40.00

35.00

25.00

30.00

mption (m

3)

20.00

ulp Woo

d Co

nsum

10.00

15.00

Annu

al Pu

5.00

‐1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Timber from natural forest Timber from Plantations

MAJOR INDONESIAN PAPER PRODUCT PRODUCERSMAJOR INDONESIAN PAPER PRODUCT PRODUCERS

DJARUMBukit Muria Jaya (BMJ) Karawang ‐ Specialty papers (cigarette) and packaging – ID consumes 195 billion cigarettes/yr

APRIL

Riau Andalan Pulp & Paper (RAPP) Kerinci ‐ Printing and copying paper – 850,000 MT / Year

ASIA PULP & PAPER GROUP

Purinusa Ekapersada Bandung - Corrugated carton box Semarang - Paper packaging and carton packaging

Indah Kiat Pulp and Paper Perawang - Paper from virgin fiber – 1,200,000 MT / Year

Serang - Recycled paper products (board grade) - 1,570, 000 MT / Year

Tangerang - Colored paper for virgin fiber - 105,000 MT / Year

Lontar Papyrus Pulp and Paper Industries

Jambi - Tissue from virgin fiber approx. 100,000 MT /Year

Pindo Deli Karawang 1 - Jumbo Roll Tissue, Art BoardPindo Deli Karawang 1 Jumbo Roll Tissue, Art Board

Karawang 2 - Photocopy paper, jumbo roll & converted tissue

- Capacity Karawang mills 1,117,000 MT / Year

Perawang - Tissue roll - 400,000 MT / YearTjiwi Kimia Surabaya - Paper and stationary, both from virgin and recycle fiber - 1,677,000 MT / YearTjiwi Kimia Surabaya Paper and stationary, both from virgin and recycle fiber 1,677,000 MT / Year

Ekamas Fortuna Malang - Recycle paper board grade products – 180,000 MT / Year

The Univenus Cikupa - Converted tissue products

Perawang - Tissue jumbo rolls

Surabaya - Converted tissue products

Medan - Converted tissue products

Indonesia – Chip millsIndonesia – Chip millsFactory Name Province Location Ownership Capacity of

chipping (BDT)

Production estimate 2013/14

End Use - Domestic pulp mill or chip chipping (BDT) (BDT/yr) export?

Dumai Riau Province, Sumatra Dumai APRIL 500,000 0

Built to supply Rizhao but has also barged chips to Kerinci

PT Sarana Bina Semesta Alam (SBSA)

East KalimantanTj Karas, Mahakam River, Kbptn Kutai Kertanegara

Sinar Mas Forestry. (legally outside of APP)

900,000 500,000Export, especially to APP Hainan

PT Kutai Chip East KalimantanKariangau, Balikpapan Bay, Balikpapan City.

APRIL 1,000,000 1,000,000 Export to APRIL Rizhaop p y

PT Chipdeco Inti Utama East Kalimantan Tarakan Island

Sinar Mas Forestry (legally outside of APP)

70,000 0 Export

PT Manunggal Anugerah Lestari (MAL)

South Kalimantan Pulau Laut, Kbptn Kotabaru

APP Coal 750,000 0Original plan was for export but also sell d i ( b )(MAL) Kotabaru domestic (on barges)

PT Bintuni Utama Murni Wood Industries

Papua Kbptn Teluk Bintuni Local 100,000 50,000Mangrove high density chip for specialist papers

500 000 chipOriginal plan was for export but may sell500,000 chip

200,000 pellets

PT Korindo Central Kalimantan Kapitan River, Kbptn Kotawaringin Bara Oji / PT Korindo 500,000 250,000

Export chip. Oji's new pulp mill Nantong,

PT Medcopapua Papua Bian River, Kbptn Merauke

MEDCO Group 0export but may sell domestic on barges due to ship loading problems

Kotawaringin Bara China and Japan Summary 4,520,000 1,670,000 37%1,800,000 40%

Indonesia – Wood Chip ExportsIndonesia Wood Chip Exports(Million BDMt)

1.8

2

St d i i d hi

1.4

1.6

1.8 Steady increase in woodchip exports

• 2010 60%

1

1.2

• 2010 – 60%• 2011 – 39%• 2012 – 7%• 2013 27%

0.6

0.8• 2013 – 27%• 2014 – 22%• 2015 – Q1 >100%

0

0.2

0.4

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Indonesia – Future Trends in Chipwood / Pulp / Paper Sectors

• Transition to 100% plantation wood by 2017Transition to 100% plantation wood by 2017.• Tightening of domestic wood chip supply / demand situation in medium

term.– Existing pulp mills are unlikely significantly expand

– Opportunities for existing paper production to expand considerably

– Export woodchip likely to be redirected for domestic use– Export woodchip likely to be redirected for domestic use

• What are the plans of smaller plantation companies?– Some of the of smaller plantation companies are likely to be acquired by the

l ill ipulp mill companies– The smaller plantation companies are unlikely to have sufficient wood to build

a BHKP mill on their own.Groundwood pulp mills "refiner mechanical" pulp (RMP)– Groundwood pulp mills ‐ refiner mechanical pulp (RMP),"thermomechanical" pulp (TMP) and chemi‐thermomechanical pulps (CTMP)– are being considered given the smaller wood requirements of these millsand the low cost of energy in Indonesia (cheap thermal coal).

• Smaller plantation companies ‐Move to non‐chipwood forest plantations – rubber, biomass, charcoal

Demise of Acacia mangiumDemise of Acacia mangium• Acacia mangium is the dominant species for g pwood fiber production in Indonesia

• A. mangium has proven to be a reliable g pspecies but with limited production potential.

• Increases in pests and diseases over time areIncreases in pests and diseases over time are markedly impacting on the long‐term viability of A. mangium as a plantation speciesg p p

• Many companies are replacing their A. mangium plantations with Eucalyptusg p yp

Acacia mangiumAcacia mangium

• Typical Acacia mangium – moderate growth rates (25MAI), multi‐leaders, variable growth, high mortality, poor form.

Three headed hydra (1) Ganoderma philippii

Three headed hydra (2) Stem wilt: Ceratocystis

Three headed hydra (3) Monkey damage

hSumatran macaque Oranghutans

Rise of EucalyptusRise of Eucalyptus• Early plantings of E. grandis, E. uropylla, E. y p g g , py ,camaldulensis etc in Indonesia largely failed.

• Exceptions – APRIL have established world classExceptions APRIL have established world class E. grandis, E. uropylla plantations at high altitude on volcanic soils.

• After a long period of R&D, Indonesian industry has established E. pellita as a viable andhas established E. pellita as a viable and competitive plantation species

• Rapidly increasing growth rates improving• Rapidly increasing growth rates, improving density and pulping characteristics, and improved resilience against pests and diseasesg p

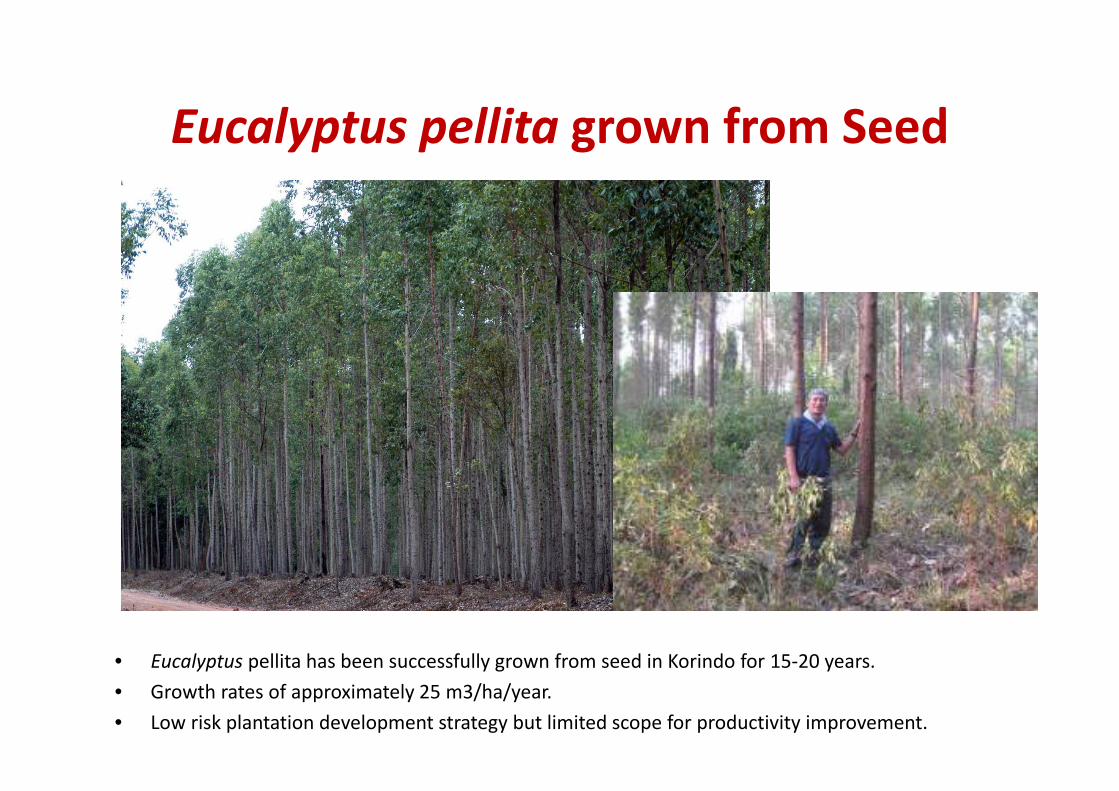

Eucalyptus pellita grown from SeedEucalyptus pellita grown from Seed

• Eucalyptus pellita has been successfully grown from seed in Korindo for 15‐20 yearsEucalyptus pellita has been successfully grown from seed in Korindo for 15 20 years.• Growth rates of approximately 25 m3/ha/year.• Low risk plantation development strategy but limited scope for productivity improvement.

A New Paradigm – Intensively Managed Eucalyptus pellita clones

• Rapid genetic improvement through clonal propagation of E. pellita. • Hybridizing with E. grandis, E. urophylla, E. tereticornis• Intensive site preparation, weed control and fertilizer regimes to improve

l i fplantation performance.• Improved operational efficiencies through mechanization.

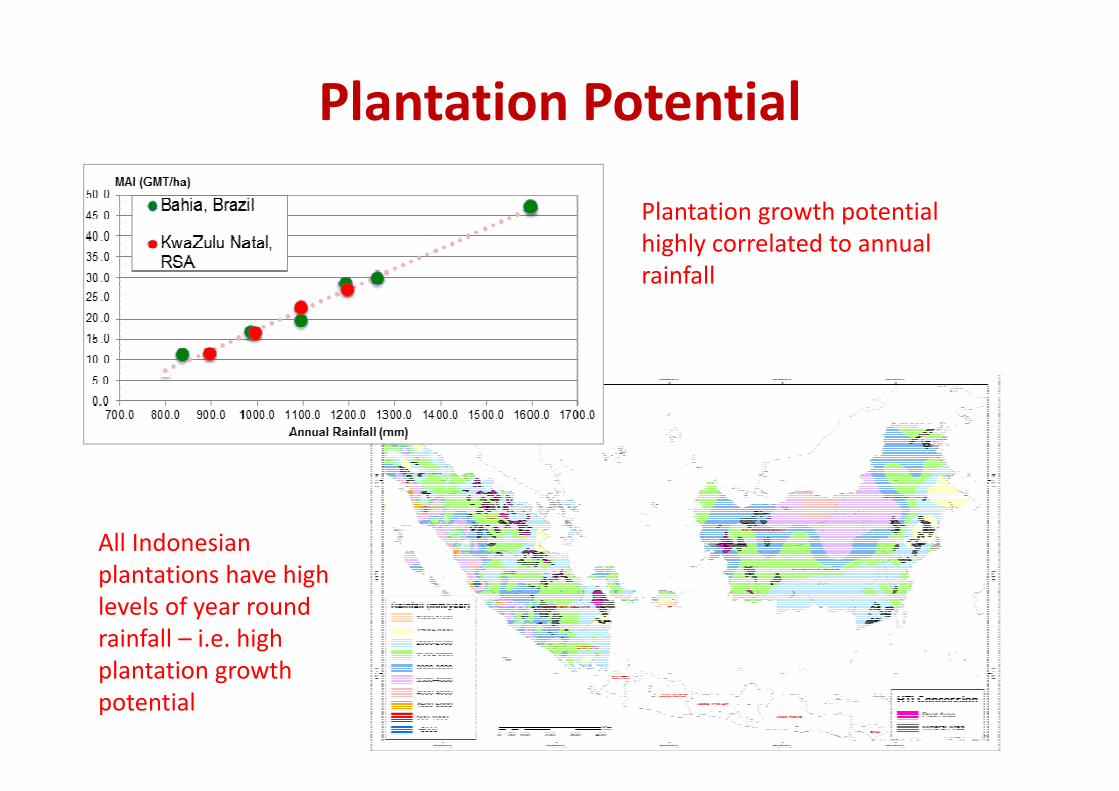

Plantation Potential

Plantation growth potentialPlantation growth potential highly correlated to annual rainfall

All Indonesian plantations have highplantations have high levels of year round rainfall – i.e. high l t ti thplantation growth

potential

1st Generation Eucalyptus pellita clones

• 1st generation Eucalyptus pellita clones. • Tall but reduced DBH growth. Very light crowns. Significant variability and some mortality.

2nd Generation Eucalyptus pellita Clones

• Sinar Mas has been a leader in the development of clonal Eucalyptus pellita Now developing 2ndSinar Mas has been a leader in the development of clonal Eucalyptus pellita. Now developing 2generation of Eucalyptus pellita clones.

• Rapid improvement in MAI, tree form, and wood density and wood properties.

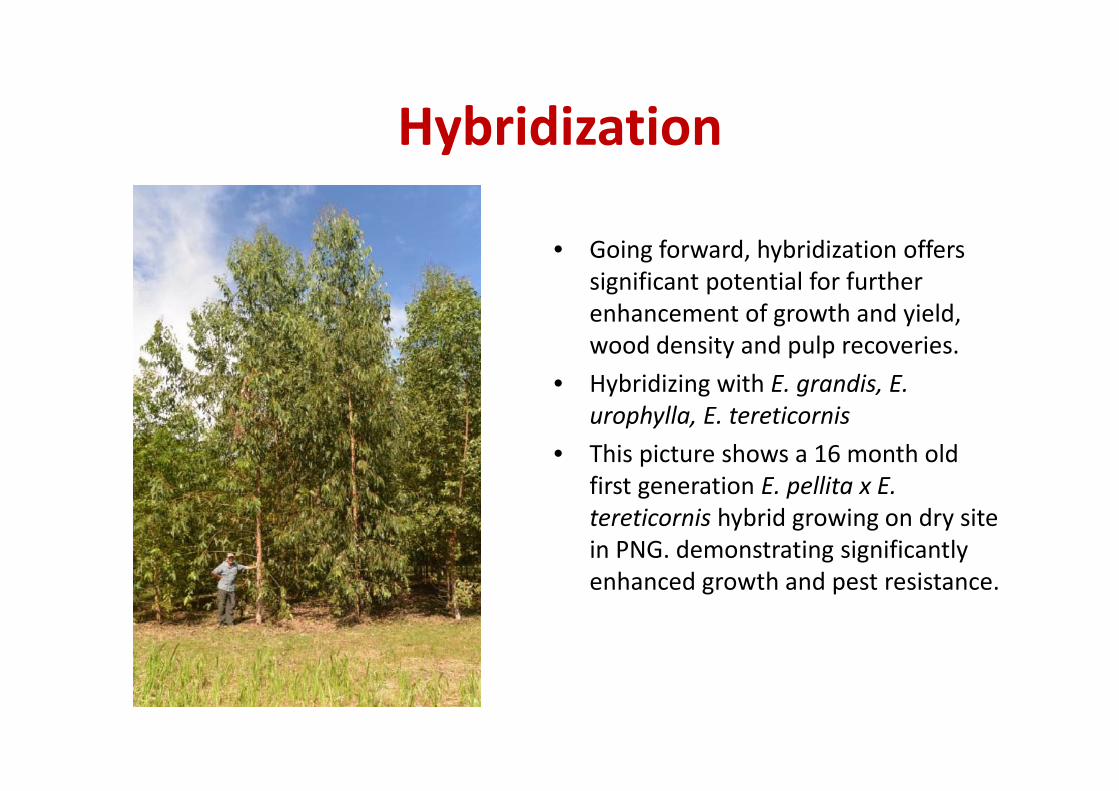

HybridizationHybridization

• Going forward, hybridization offers significant potential for further

h f h d i ldenhancement of growth and yield, wood density and pulp recoveries.

• Hybridizing with E. grandis, E. y g gurophylla, E. tereticornis

• This picture shows a 16 month old first generation E pellita x Efirst generation E. pellita x E. tereticornis hybrid growing on dry site in PNG. demonstrating significantly

h d th d t i tenhanced growth and pest resistance.

Historically Poor Performance of Plantation Management

• Relatively low tech approach to plantation operationsoperations

• High level of manual labor / low g /productivity rates / high costs

• Social / community issues with encroachment and fire riskencroachment and fire risk.

• Neglect of environmental values

Low Tech Approach to HarvestingLow Tech Approach to Harvesting

Historical Low Tech Approach to TransportHistorical Low Tech Approach to Transport

Eucalyptus Requires More Intensive High Tech Management Approach

Improved Operational Efficiency and Effectiveness

f d• Increasing focus in Indonesia in improving operation efficiency and productivity:– Investment in R&D to improved effectiveness and efficiency of silviculturaland efficiency of silvicultural

– Increased mechanization of silviculture and harvestingharvesting

– Research into improving logistics through t t ti t h l i d I fi ldnew transportation technologies and In field

chipping

Improving Social PerformanceImproving Social Performance

• Minimizing social conflict and associated resource losses andimproving worker productivity and welfare

Application of FPIC program according to best practices

Implementation of participatory planning and community Implementation of participatory planning and communitydevelopment programs

Programs and training to protect worker welfare and increase Programs and training to protect worker welfare and increaseworker skills and productivity

Transparent and evidenced based reporting of social performance Transparent and evidenced based reporting of social performance

Improving Environmental PerformanceImproving Environmental Performance

• Implementing credible and substantive sustainableenvironmental managementenvironmental management

High conservation value forest assessments – HCV

Improved mapping of natural resources ‐ HCS

Integrated Forest Management Planning ‐ IFMP

Land use planning based on sound environmental principles

Transparent and evidence based reporting of environmentalperformance

Plantation Performance

Cost of ProductionCost of ProductionBHKP Cash Costs ‐ Delivered to Western Europe (CIF) ‐ FEB 2012)

500

600BHKP Cash Costs Delivered to Western Europe (CIF) FEB 2012)

Chemicals EnergyLabour MaintenanceOther Mill Costs FreightMarketing and Sales Wood

300

400

(USD

/ADT)

100

200

Cost (

0

100

Indonesia Brazil Chile ChinaSource PWC / Hawkin WrightSource: PWC / Hawkin Wright

• The Indonesian mill costs are very competitive however the delivered cost of wood fiber is i ifi tl hi h th it i titsignificantly higher than its main competitors.

• The transition to Eucalyptus should result in reduced average plantation costs per tonne and significantly improve cost competiveness of the industry.

Delivered Cost of WoodDelivered Cost of Wood

75

DELIVERED WOOD COSTS AS PERCENTAGE OF TOTAL PULP PRODUCTION COST

65

70

CTION COST

60

65

ULP PRODUC

55

% OF PU

Brazil Chile Indonesia

502012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2

Source: WQI ex Fisher Institute

Future of Indonesian IndustryFuture of Indonesian Industry

• High productivity sustainable plantation management Significantly improving growth rates (50%+ gain on dry lands)g y p g g ( g y ) Full utilization of land resources (12% gain) Improving workforce productivity (25% gain)

• Commercial pay off Long-term security of fibre supply based on 100% plantation wood Lower cost of wood (10-30% reduction) Lower cost of wood (10-30% reduction)

• Market pay off Market recognition of sustainability programs Securing existing markets in Asia and Pacific Better access to high value markets in Nth America / Europe (10-15%)

THANK YOUTHANK YOU

C t t G KContact: George Kuru

Ata Marie Group Ltd

Web: www.ata‐marie.com

Email: george.kuru@ata‐marie.co.id